5 Interesting Learnings from Zoom at ~27B Market Cap, and a 25x Anthropic Windfall | Saa Str AI

Overview

AI VC AI Mentor: Digital Jason + Amelia AI Startup Benchmarking

AI Agent Playbook Free e Books

e Book: Hiring a Great VP of Sales

e Book: Raising Capital

e Book: The First $1m ARR

Details

University All Posts Podcasts The Top CROs VC Fundraising Top Videos Q&A Best of Saa Str #1 Bestselling Book Search Everything Join the Community

Free e Books

e Book: Hiring a Great VP of Sales

e Book: Raising Capital

e Book: The First $1m ARR

AI Annual 2026 Events Overview Sponsors

Event Sponsorship

Media Sponsorship

Digital AI Day 2026 (Free) Speaker Submissions Speaker Requirements Overview

5 Interesting Learnings from Zoom at ~27B Market Cap, and a 25x Anthropic Windfall

by Jason Lemkin | 5 Interesting Things, Blog Posts, Scale

Almost everyone wrote Zoom off a few years back. The story was tidy: the app everyone loved before 2022, but then almost a COVID one-hit-wonder that peaked in 2021 after going from

But … Zoom is back to growth. Modest growth, mature growth, enterprise-driven growth. But growth. Zoom’s Q1 FY2027 (ended April 30, 2026) came in with revenue re-accelerating, AI that customers are actually paying for, and free cash flow margins north of 40%. It’s a mature B2B leader clawing growth back while becoming a cash machine, which is rarer and more repeatable than another hypergrowth story.

Zoom has had its share of post-2020 challenges. It almost had to. It was the Lock Down Poster Child. But in just 15 years, it built a dominant leader with a

Zoom has had its share of post-2020 challenges. It almost had to. It was the Lock Down Poster Child.

But in just 15 years, it built a dominant leader with a $27B market cap, up +21% the last 12 months, and wildly profitable

— Jason ✨👾Saa Str. Ai✨ Lemkin (@jasonlk) July 14, 2026

Revenue: $1.239B in the quarter (Q1 FY2027, ended April 30, 2026), up 5.5% Yo Y and above guidance

Revenue run-rate (≈ARR): ~

Revenue multiple: ~5.4x run-rate, and closer to ~4x after netting out $7.7B in cash and investments

Free cash flow: $500M in the quarter, a 40.4% FCF margin

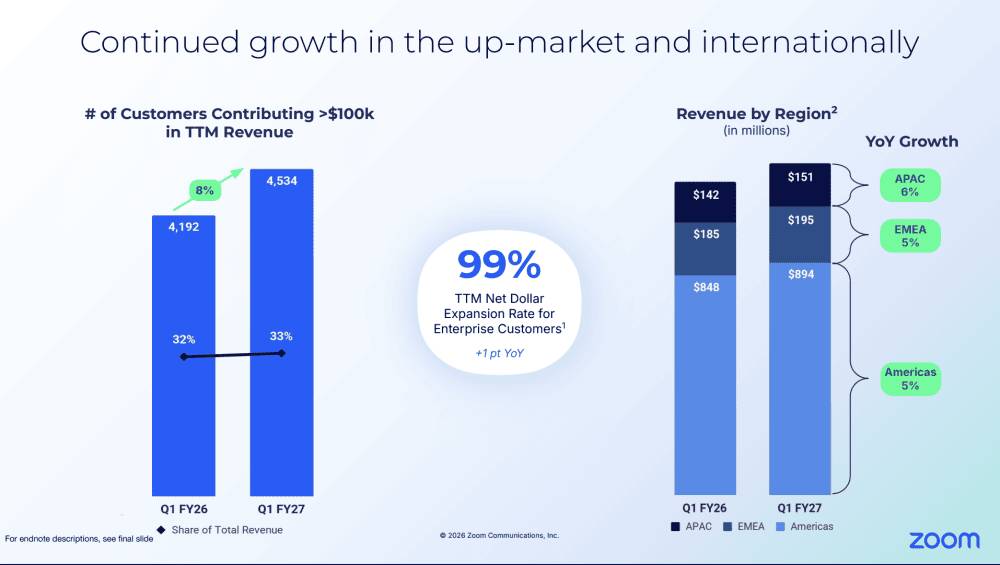

Enterprise net revenue retention: 99%, with Enterprise now 61% of revenue and growing 7.2%

Anthropic stake: carried at

1. Growth Is Re-Accelerating, Albeit Very Modestly, At ~$5 Billion in Revenue.

Revenue hit $1.239B in the quarter, up 5.5% year-over-year, above the high end of guidance. That doesn’t sound dramatic until you remember the trajectory. Zoom fell to roughly 3% growth. Now growth has climbed for multiple quarters, and full-year FY26 growth accelerated 130 basis points to 4.4%.

At scale, growth doesn’t die, it plateaus. And a plateau can be climbed back out of if you attach genuinely new products to a big installed base. The install base is the asset. The second and third products are the growth.

2. They’re Actually Monetizing AI. And It’s Working (To An Extent)

AI Companion paid users grew 184% year-over-year. “My Notes” reached 1.5 million licensed users within four months of launch. Customer Experience is growing at high double digits, and paid AI showed up in every one of Zoom’s top 10 CX deals last quarter. Zoom built AI into paid SKUs, and customers are buying them. Charging for it instead of giving it away is a completely different financial outcome.

Shipping the most AI doesn’t always win in B2B + AI. Figuring out the paid SKU and the attach motion does. Shipping AI is table stakes now. Charging for it, and getting customers to say yes, is the actual skill.

3. Enterprise Passed Online. And Carries the Whole Company Now.

Enterprise revenue was

What drove Zoom’s original explosion: self-serve SMB, millions of people swiping a credit card during COVID. That base is now the slow-growth anchor, growing at a third of the enterprise rate. The direct, sales-led enterprise motion is the engine keeping the whole thing moving.

Self-serve got Zoom to massive scale but couldn’t sustain the growth on its own. The durable growth came from moving upmarket. If your self-serve base is decelerating, the fix is usually enterprise and multi-product, not simply pouring more into the top of the self-serve funnel.

4. Net Revenue Retention Is Still Below 100%. And They’re Growing Anyway. But It Does “Hurt”

Enterprise net dollar expansion ticked up to 99%, from 98% a year ago. Still under 100%. And Online average monthly churn actually got worse, rising to 3.0% from 2.8%. Meanwhile $100k+ customers grew 8.2% to 4,534.

The growth is being driven by new logos and new product attach, not by the existing base expanding on its own.

You don’t strictly need 120% NDR to grow. You can grow with sub-100% retention if you add enough new customers and attach enough new products on top. But it’s much harder, and it’s lower-quality growth. Most great B2B companies would kill for Zoom’s cash flow. Zoom, in turn, would love to get its NDR back well over 100%.

5. It Became a Cash Machine. And Capital Return Is the Story Now.

The profitability here is almost hard to believe for a company still growing. Non-GAAP operating margin was 41.1%. Free cash flow was

And they’re returning it. The board added another

The takeaway: at maturity, the game shifts from growth to durable profit and capital return. Zoom is a Rule-of-46 company where the “40” carries it. That’s not a failure state. For a company its size, it’s a valuable end state, and one a lot of today’s high-burn AI companies will need to grow into eventually.

Bonus Learning: The Anthropic Stake May Be Worth More Than the Market Gives Zoom Credit For

This is the part of the quarter that has nothing to do with meetings, phone, or CX, and it might matter as much as any of it.

Zoom booked a

An initial ~

Now put that against the operating company. Zoom’s market cap is around

There’s a strategic layer on top of the financial one. The stake buys Zoom deep access to Claude inside its federated AI approach, where it routes tasks to different models based on cost and performance. Without an ownership position, Zoom would be renting frontier AI at retail from a partner of a direct competitor, and the 40% free cash flow margins in Learning #5 would be a lot harder to defend. The investment protects the growth story and the margin story at the same time.

Three cautions worth stating plainly, because they’re the difference between paper and value:

It’s a mark, not money. The $1.27B is a carrying value, not cash. Zoom can’t spend it without a sale or secondary, and the gain reverses in a down round.

It’s concentrated and illiquid. One private company is two-thirds of the strategic book. That’s real single-name risk sitting on the balance sheet.

It distorts GAAP earnings. The

The founder takeaway: a single early, high-conviction strategic investment can create more shareholder value than years of operating execution, and can reprice how the market sees an entire company. Zoom’s operating business grew 5.5% last quarter. Its Anthropic stake is up roughly 25x. One of those shows up in cash flow. The other is a paper mark the market is still learning how to price.

Dilution is actually shrinking. Stock-based comp fell to

GAAP margins are catching up to non-GAAP. GAAP operating margin jumped 450 basis points to 25.1%. As SBC comes down, the gap between “real” and “adjusted” profit keeps closing.

They raised guidance on the beat. FY27 revenue guidance moved up to

AI compute isn’t crushing gross margin. Cost of revenue actually fell year-over-year even as revenue grew, pushing gross margin to ~77.9% from ~76.3%. The bear case that AI features would eat margins hasn’t shown up in the numbers yet.

Zoom will never headline a 5IL for hypergrowth. But the lesson here is more durable than another 60%-grower story. A company can get written off, re-accelerate through multi-product attach, actually charge for AI while everyone else gives it away, and compound cash the entire time. Growth plus durable profitability is not something you win once. The best B2B companies keep re-earning it, quarter after quarter.

Everyone's Adding AI. But That Doesn't Mean It's Accelerating Growth.

How to Scale Go-to-Market Through IPO with ICONIQ Growth's General Partners

Everyone's Adding AI. But That Doesn't Mean It's Accelerating Growth.

How to Scale Go-to-Market Through IPO with ICONIQ Growth's General Partners

Get from

Key Takeaways

-

AI VC AI Mentor: Digital Jason + Amelia AI Startup Benchmarking

-

AI Agent Playbook Free e Books

e Book: Hiring a Great VP of Sales e Book: Raising Capital e Book: The First $1m ARR -

University All Posts Podcasts The Top CROs VC Fundraising Top Videos Q&A Best of Saa Str #1 Bestselling Book Search Everything Join the Community

-

Free e Books

e Book: Hiring a Great VP of Sales e Book: Raising Capital e Book: The First $1m ARR -

AI Annual 2026 Events Overview Sponsors

Event Sponsorship Media Sponsorship