The 6 Threat Vectors Killing Traditional B2B Software in 2026 (And How to Fight Back)

Introduction: The Perfect Storm Facing Enterprise Software

Traditional B2B software and SaaS companies face an unprecedented challenge in 2026. While the software market continues to expand—with global IT spending projected to exceed

The surface-level story looks bullish. The pie is getting bigger. Enterprise budgets are increasing. CIOs are committing to digital transformation. Yet beneath these encouraging headlines lies a more troubling reality: established software vendors are experiencing stock price declines that would have been unthinkable just years ago.

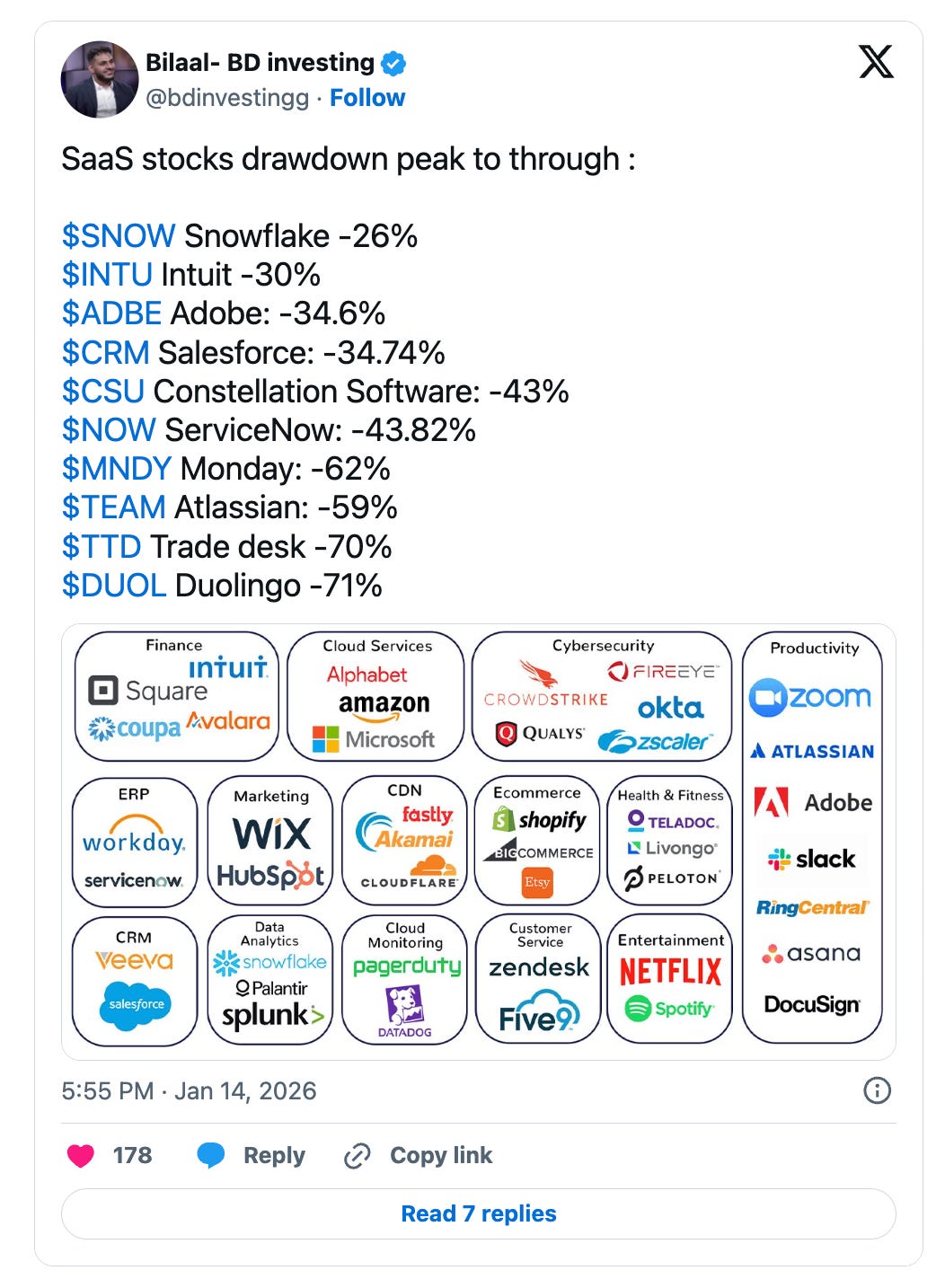

The 2026 Valuation Collapse:

- Snowflake ($SNOW): -26% from peak

- Intuit ($INTU): -30% decline

- Adobe ($ADBE): -34.6% drawdown

- Salesforce ($CRM): -34.74% decline

- Constellation Software ($CSU): -43% drop

- Service Now ($NOW): -43.82% decline

- Monday.com ($MNDY): -62% slide

- Atlassian ($TEAM): -59% correction

- Trade Desk ($TTD): -70% plunge

- Duolingo ($DUOL): -71% collapse

This isn't cyclical volatility. This is structural disruption. The traditional software playbook—the one built on predictable seat-based growth, annual price increases, sticky enterprise contracts, and inertia-driven retention—is breaking down simultaneously across multiple dimensions.

What makes this moment uniquely dangerous is that traditional B2B software isn't being disrupted by a single competitor or threat. It's being attacked from six different vectors at once. Each vector is powerful enough to challenge business models on its own. Combined, they create a perfect storm that many established vendors are unprepared to weather.

This comprehensive analysis examines each threat vector in detail, explores the underlying dynamics driving disruption, and provides actionable strategies for companies seeking to remain competitive in this transformed landscape.

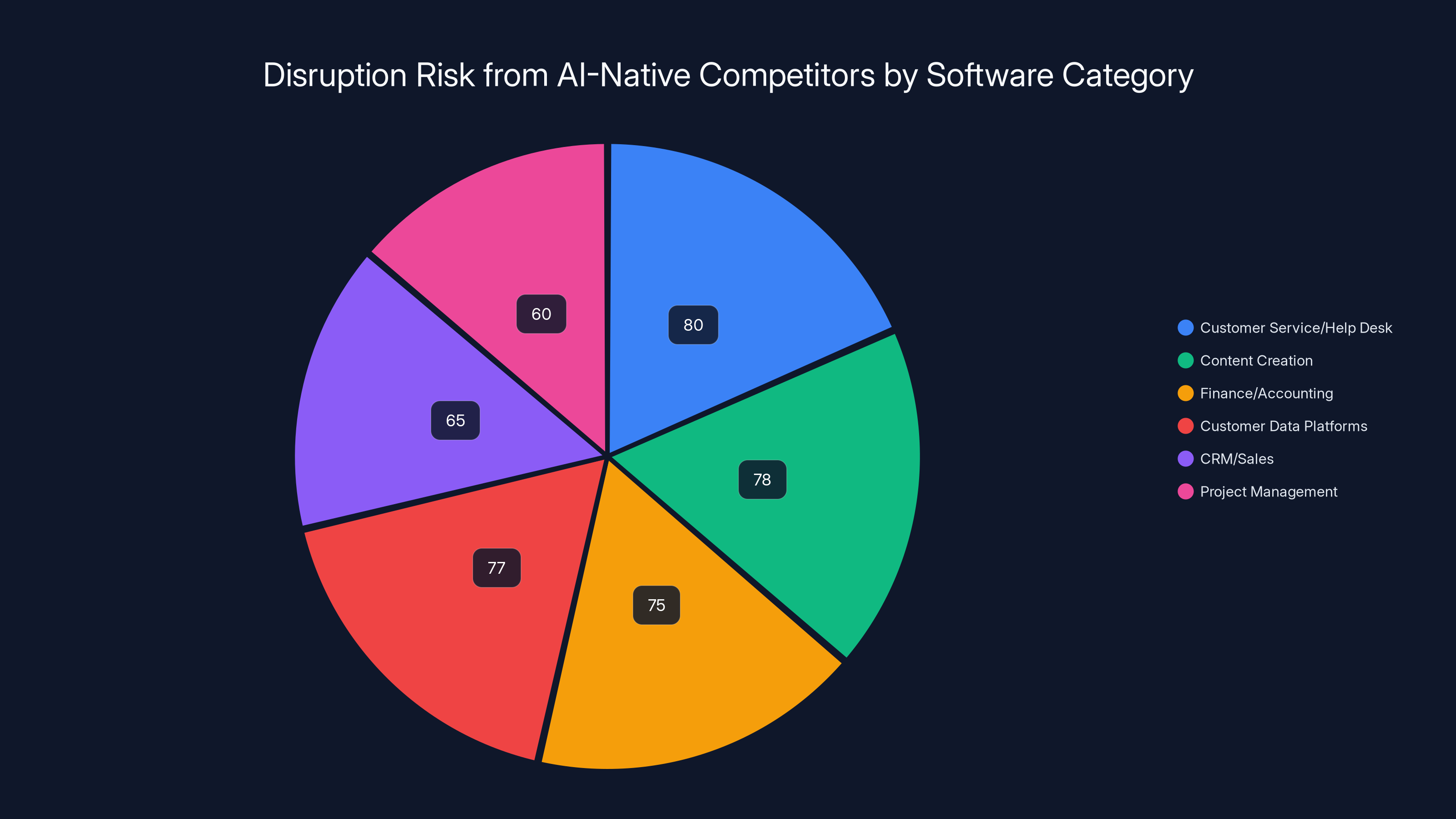

Customer service/help desk, content creation, finance/accounting, and customer data platforms face the highest disruption risk from AI-native competitors, with probabilities exceeding 75%. Estimated data.

#1: The Seat Slowdown—When Growth Engines Stall

Understanding the Seat Slowdown Phenomenon

The seat-based software model seemed bulletproof for decades. Add more employees to a company. Those employees need software. Software vendors add seats. Revenue grows predictably. It was a virtuous cycle that generated reliable, compounding growth for thousands of SaaS companies.

That cycle has broken.

Major vendors across the industry are acknowledging a brutal reality: customers are committing to lower headcount levels on renewals compared to previous years. Workday CEO Carl Eschenbach stated on their Q1 FY25 earnings call that the company observes "customers committing to lower headcount levels on renewals compared to what we had expected," with management explicitly noting they "expect these dynamics to persist in the near term."

The data confirms this shift is structural, not temporary:

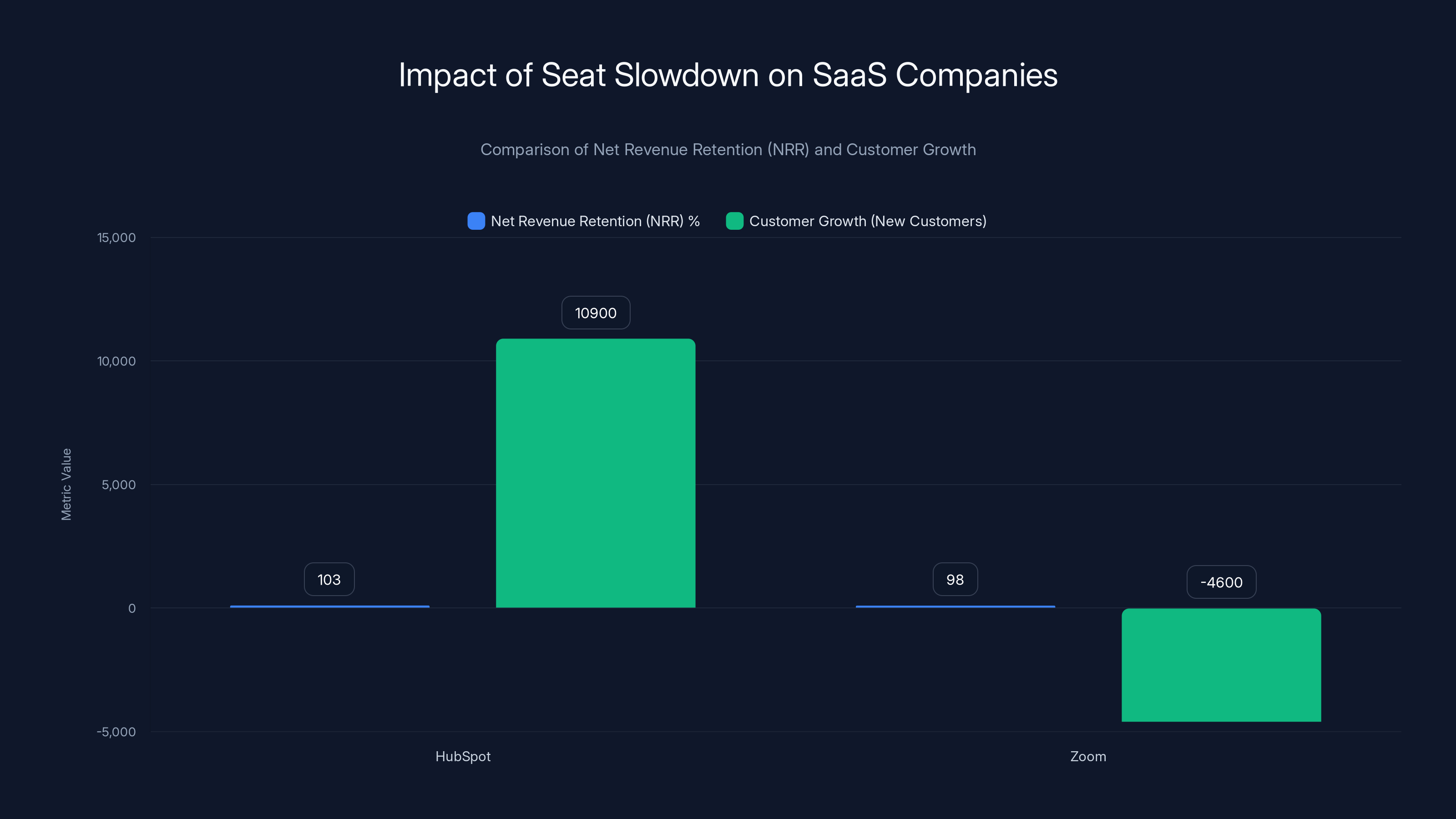

HubSpot's Expansion Engine Stalls:

- Net Revenue Retention (NRR) flat at 103% in Q3 2025

- Customer dollar retention declined to high 80s

- Added 10,900 new customers to reach 279,000 total

- Expansion from existing customers essentially frozen

Zoom's Enterprise Customer Contraction:

- Enterprise NRR fell to 98%—indicating existing enterprise customers are actually shrinking spending

- Enterprise customer count declined to approximately 192,400

- Revenue grew just 4% YoY

- Yet still generated $614 million in free cash flow

When a market-leading company like Zoom—with incredible brand recognition, essential products, and dominant market position—sees enterprise customers literally declining in number while the company generates $614 million in annual free cash flow, you're watching something fundamental shift. The company is in harvest mode, extracting value from an increasingly stagnant customer base.

The Root Causes: Tech Hiring Flatlines and Automation

The seat slowdown stems from two distinct but interconnected dynamics.

First, tech hiring has fundamentally reset. After years of aggressive hiring across the technology sector, companies have reached equilibrium. The frenzy of hiring that characterized 2020-2021 gave way to mass layoffs in 2022-2023, followed by cautious, measured hiring practices in 2024-2025. The result: headcount growth has essentially flatlined. When headcount stops growing, the primary driver of seat-based SaaS expansion disappears.

But there's something deeper happening beyond mere hiring cycles. Automation is reducing the marginal value of additional seats. As companies deploy AI tools, intelligent automation, and process optimization, they accomplish more work with fewer people. A customer might have needed five team members to manage a business process in 2022. In 2025, the same process might require three team members augmented by AI tools. The customer has the same revenue and serves the same markets, but with materially fewer software seats.

This dynamic proves particularly powerful in back-office functions like finance, HR, and customer service—precisely the use cases driving HubSpot's expansion in recent years.

The Vendor Response: Shifting from Seat Expansion to Value Extraction

Since seat growth is stalling, vendors are pursuing multiple strategies to maintain revenue growth—none of which are winning them friends:

Strategy 1: Price Increases

- Annual increases (sometimes biannual) that average 8-15% per year

- Justified by AI features and security improvements

- Consuming 50%+ of incremental IT budget

Strategy 2: Feature Consolidation Taxes

- Bundling previously separate products

- Forcing upgrades to higher tiers

- Eliminating flexibility in pricing structures

Strategy 3: Usage-Based Billing

- Shifting from predictable per-seat models to consumption models

- Creating budget uncertainty and surprise charges

- Difficult to forecast and control

Strategy 4: AI Tax Premiums

- Adding "AI copilot" features as premium add-ons

- Charging $15-30+ per user monthly for AI capabilities

- Capitalizing on AI hype to extract additional value

These strategies create a vicious cycle: price increases make software increasingly expensive for customers, which constrains their ability to purchase new solutions or expand existing ones.

Companies Bucking the Trend

Not all software vendors are experiencing seat slowdown. The outliers share a common characteristic: they've successfully repositioned themselves as AI-native or have credibly migrated significant user value to AI functionality.

OpenAI, Anthropic, and Cursor all operate seat-based or consumption-based models but achieve expansion because their products fundamentally change how customers work. Users get demonstrably more productive, more creative, or more capable with these tools. Expansion feels natural, not extractive.

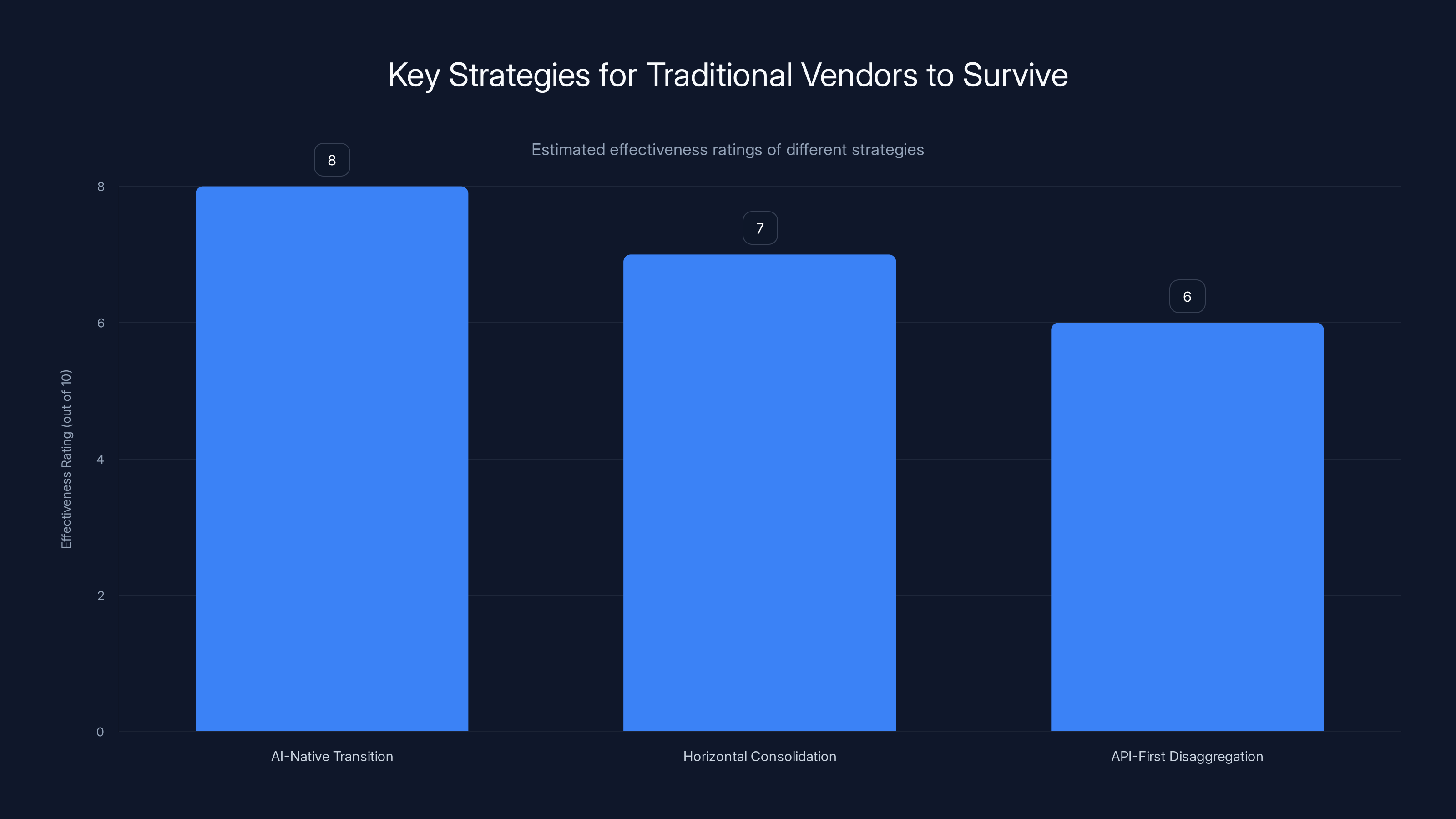

AI-Native Transition is estimated to be the most effective strategy for traditional vendors to survive, with a rating of 8 out of 10. Estimated data.

#2: Price Increases Crowding Out Budget for Innovation

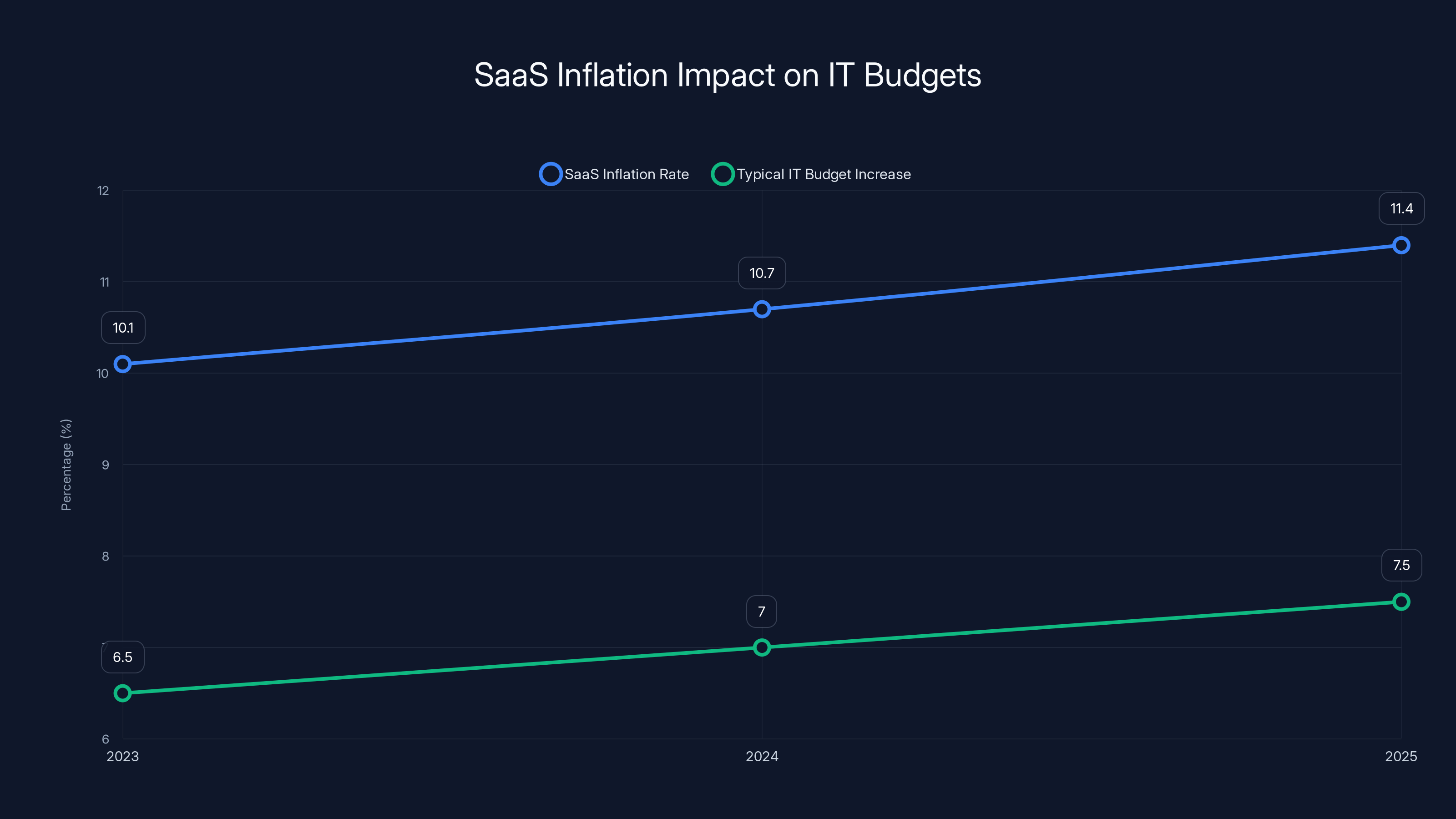

The SaaS Inflation Crisis

Enterprise software has entered an inflationary death spiral. The inflation isn't driven by manufacturing costs, supply chain constraints, or commodity pricing. It's driven by vendors attempting to maintain growth targets in a market where organic seat expansion has stalled.

The scale of SaaS inflation is staggering:

Key Inflation Metrics:

- SaaS inflation hit 11.4% YoY as of January 2025—nearly 5x higher than the 2.7% average market inflation rate of G7 countries

- **SaaS cost per employee: 8,700 in 2024 and $7,900 in 2023 (a 15% increase over just two years)

- 8 of typical organizational spend now flows to SaaS

- Average company spends $49 million annually on SaaS (9.3% YoY increase)

- 72% of Salesforce's 2025 growth came from price increases, not new customer acquisition or expansion revenue

- 60% of vendors deliberately mask their rising prices through complex pricing structures, feature bundling, and obfuscated cost models

The Mechanics of the Pricing Squeeze

What makes the current pricing environment particularly dangerous is that price increases are being justified, at least partially, by legitimate cost drivers. Gartner's John-David Lovelock confirmed it clearly: "The cost of software is going up and both the cost of features and functionality is going up as well thanks to Gen AI."

This creates a dilemma for CIOs:

The CIO's Budget Trap:

- CIO receives IT budget increase (typically 5-8% annually)

- Existing vendor contracts increase 8-15% annually due to SaaS inflation

- Result: Budget increase is consumed by existing vendor price hikes

- Outcome: Zero budget remaining for new solutions, new vendors, or innovation

This dynamic mathematically eliminates budget for competitive alternatives. When Salesforce, Microsoft, Adobe, and your other enterprise vendors are each raising prices 10-15% annually, that's consuming 100%+ of new budget allocation.

Why Price Increases Feel Different This Time

Vendor price increases have always existed in enterprise software. What's different in 2026:

The Breadth of Price Increases Is Unprecedented

Historically, isolated vendors might raise prices aggressively. In 2024-2025, price increases became synchronized across the entire industry. Nearly every major SaaS vendor raised prices simultaneously, making it impossible for customers to switch to alternatives. Every vendor is more expensive.

The Justification Is Becoming Thin

Early AI price increases (2023-2024) were somewhat justifiable—vendors were implementing genuinely new capabilities. By 2025, many "AI features" are wrapper experiences around commodity models or features that offer marginal value to most users. Customers increasingly resent paying $20+ monthly per user for AI copilots that don't materially change how they work.

The Masking Is Getting More Sophisticated

Vendors have become expert at obscuring true cost increases:

- Feature bundling: Moving previously included features into higher-tier products

- Complex SKU structures: Creating pricing tiers with overlapping functionality

- Consumption pricing opacity: Usage-based pricing with unclear forecasting

- Hidden fees: Support tiers, implementation costs, and compliance add-ons

According to Vertice research, 66.5% of IT leaders report experiencing unexpected charges from consumption-based or AI pricing models—charges that weren't anticipated during initial contract negotiations.

The Competitive Opportunity

The price-increase squeeze creates a significant competitive opening for vendors willing to pursue different strategies:

Strategy 1: Transparent, Predictable Pricing

- Simple per-user pricing with no hidden costs

- Commitment to no price increases for 2-3 years

- Clear feature roadmap so customers understand value

Strategy 2: Radical Affordability For teams seeking cost-effective automation solutions, platforms like Runable ($9/month per user) demonstrate that powerful software need not carry enterprise price tags. By focusing on AI-powered automation for developers and teams rather than premium positioning, alternative vendors can capture price-sensitive segments.

Strategy 3: Disaggregated Tools Over Monolithic Suites

- Point solutions that integrate via APIs

- Customers pay only for what they use

- Easy to swap out underperforming tools

Strategy 4: Open-Source or Self-Hosted Options

- Lower pricing for on-premise deployments

- Appeal to budget-conscious or control-focused buyers

- Build community loyalty

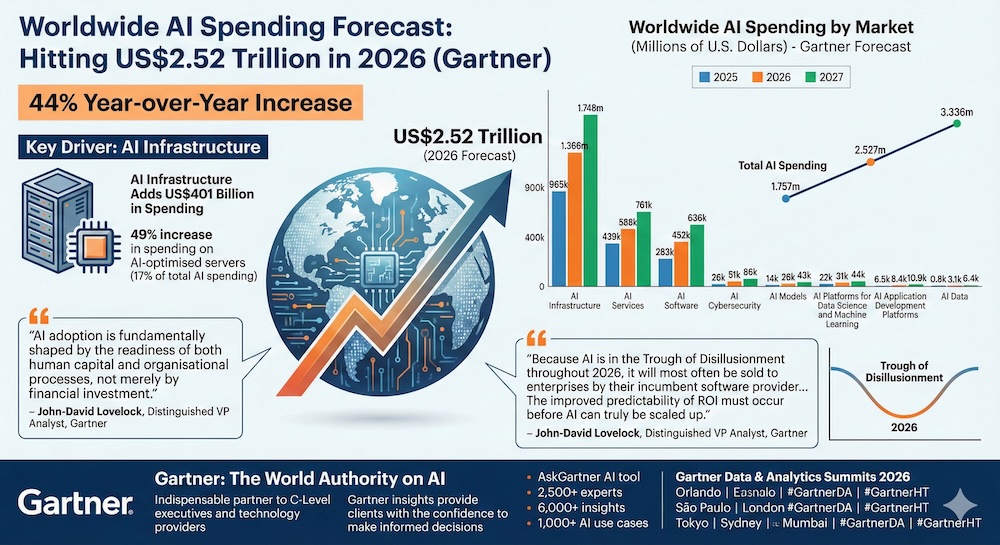

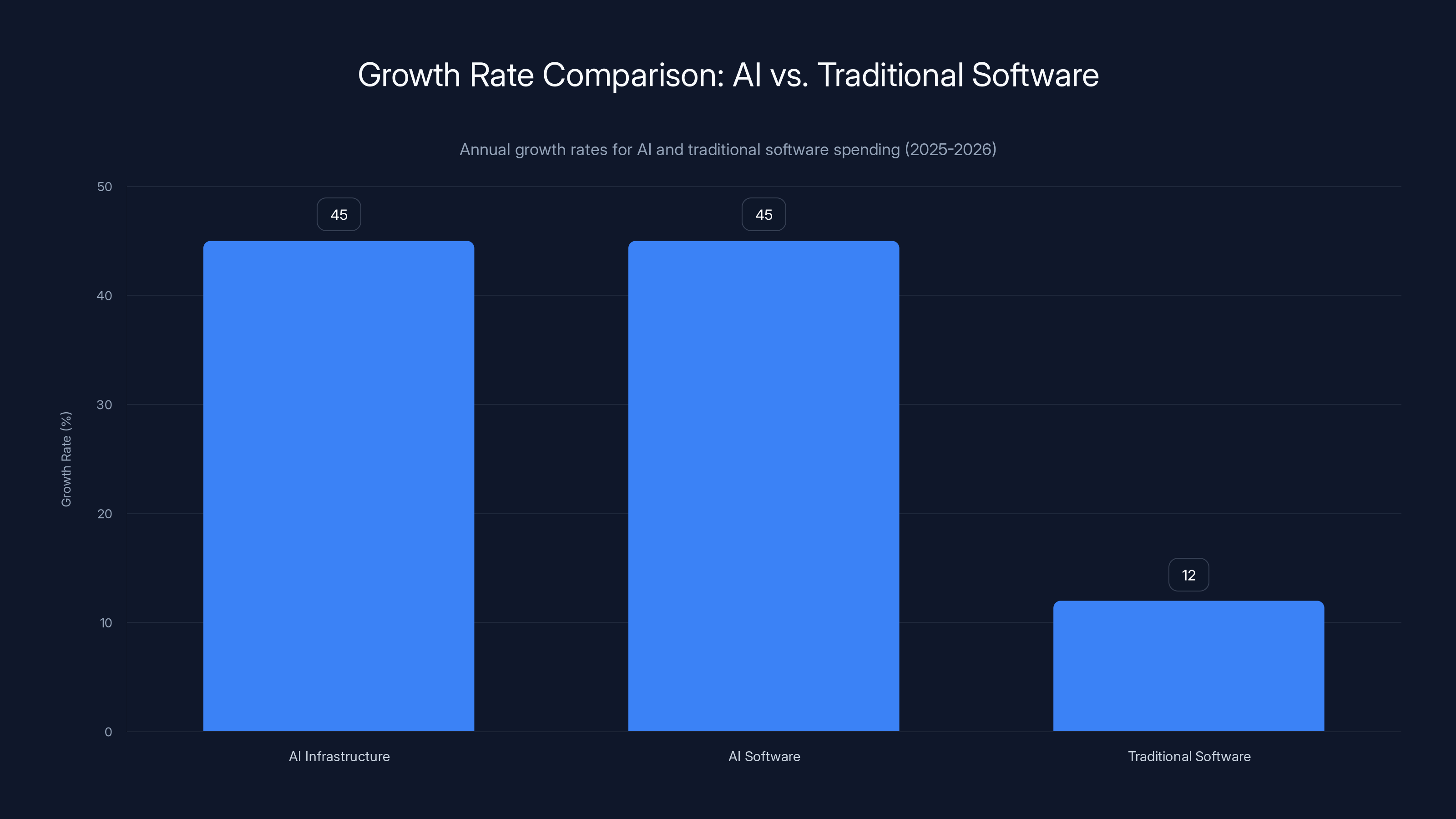

#3: All New Budget Is Flowing to AI

The AI Budget Reallocation Thesis

Here's the inconvenient truth traditional software vendors face: every new dollar of enterprise IT budget in 2025-2026 is flowing to AI. Not most. Not many. Virtually all incremental budget is being allocated to AI capabilities, AI infrastructure, and AI implementation.

This creates a challenging dynamic: traditional vendors can either (1) successfully reposition themselves as AI-native vendors or (2) watch their market share decline as budget flows to pure-play AI companies.

Measuring AI's Budget Capture

The evidence for AI's budget dominance is overwhelming:

AI Spending Growth vs. Traditional SaaS:

- AI infrastructure and software spending is growing at 40-50% annually

- Traditional enterprise software is growing at 8-15% annually

- AI is capturing 3-5x the growth rate of traditional software

- 70%+ of CIOs report prioritizing AI investments over traditional software expansion

Budget Allocation Shifts:

- Enterprises are reallocating 15-25% of existing IT budgets from traditional software to AI

- New project approvals heavily favor AI-related initiatives

- Traditional software enhancement budgets are being frozen

Why Traditional Vendors Struggle with AI

Buying a successful traditional software company doesn't automatically make it successful at AI. The challenges are multifaceted:

Cultural Misalignment

- Traditional software companies optimize for predictability, backward compatibility, and incremental improvement

- AI requires experimentation, tolerance for failure, and continuous model updates

- These cultures fundamentally conflict

Technical Debt Constraints

- Legacy codebases built on relational databases, synchronous APIs, and monolithic architectures

- AI requires asynchronous processing, unstructured data handling, and modular model pipelines

- Retrofitting AI into legacy systems often produces mediocre results

Talent Acquisition Challenges

- Best AI engineers prefer greenfield projects and pure-play AI companies

- Top AI talent often leaves large enterprises for startups

- Salary arbitrage (AI engineers earn 2-3x traditional software engineers) strains budgets

User Acceptance Issues

- Traditional software users often distrust AI features from incumbents

- Perception of "AI features" being tacked on rather than core to product

- Users prefer specialized AI tools from pure-play vendors

The AI-Native Vendors Winning

Meanwhile, AI-native companies are capturing disproportionate budget share:

OpenAI (ChatGPT, GPT-4 API) has become the de facto standard for enterprise AI infrastructure. Organizations of all sizes are building applications on OpenAI's APIs, giving OpenAI disproportionate influence over enterprise technology stacks.

Anthropic (Claude, Claude API) is gaining traction in enterprise contexts, particularly in industries with high compliance requirements. Claude's emphasis on safety and accuracy appeals to regulated industries.

Specialized AI Solutions in document processing, code generation, data analysis, and customer service are proliferating. Each vertical is seeing 3-5 pure-play AI startups addressing that use case.

Traditional Vendor Responses: Hit or Miss

Successful AI Repositioning:

- Microsoft successfully positioned Copilot across Office, GitHub, Dynamics, and Azure

- Databricks evolved from pure data warehouse company to AI-platform provider

- Stripe launched significant AI-powered products and services

Struggling AI Initiatives:

- Salesforce despite major AI investments (Einstein), sees customers viewing AI as separate from core Salesforce value proposition

- SAP AI initiatives seen as incremental rather than transformative

- Oracle struggling to position Oracle Cloud as compelling alternative to cloud-native AI platforms

SaaS inflation consistently outpaces typical IT budget increases, squeezing resources for innovation. Estimated data highlights the growing budgetary pressure.

#4: Consolidation Reducing Addressable Market

The Consolidation Paradox

When customers consolidate vendors and reduce their tech stack, the total addressable market for enterprise software shrinks. This paradoxically happens while customer IT budgets are increasing.

CIOs are increasingly asking themselves a fundamental question: "Why are we paying for 200+ SaaS subscriptions when we could consolidate to 20-30 core platforms?"

The pressure toward consolidation is intense:

Drivers of Consolidation

Driver 1: Cost Control

- IT leaders want visibility into SaaS spending

- Shadow IT creates audit and compliance risks

- Consolidating reduces cost surface area

Driver 2: Integration Complexity

- Each new tool requires API integrations, data mappings, and custom workflows

- Reducing tools reduces integration debt

- Monolithic suites (like Microsoft 365, Salesforce ecosystem) reduce integration complexity

Driver 3: Data Governance

- GDPR, CCPA, and other regulations require clear data lineage

- More vendors = more data copies = greater compliance complexity

- Consolidation reduces data governance challenges

Driver 4: User Experience

- Employees switching between 30+ applications creates productivity friction

- Integrated suites reduce switching costs

- Single sign-on, unified interfaces, and shared workflows improve UX

Driver 5: Vendor Consolidation Capability

- Large vendors increasingly can address 70-80% of enterprise needs

- Point solutions becoming less defensible against integrated suites

- Smaller vendors losing ability to compete

Evidence of Consolidation in Action

Microsoft's Consolidation Win: Microsoft 365 (Office, Teams, OneDrive, SharePoint) has become the de facto collaboration and productivity suite for most enterprises. Integration of Copilot across these products is driving further stickiness.

Salesforce's Ecosystem Play: Salesforce acquired Slack, Tableau, and Einstein to build an integrated CRM ecosystem. While execution has been mixed, the strategic intent is clear: consolidate customer relationships through platform integration.

HubSpot's Horizontal Integration: HubSpot (CRM) is aggressively positioning to replace fragmented Marketing, Sales, and Service tools. Success here would consolidate 3-5 vendor categories into one platform.

The Inevitable Market Share Concentration

Consolidation mathematically reduces the total addressable market for non-core tools. If an enterprise reduces from 200 SaaS subscriptions to 50, it's eliminating 150 vendors from its tech stack.

This creates a brutal dynamic:

Market concentration increases even as total market size grows. By 2026, we expect:

- Top 50 global software companies control 60%+ of enterprise SaaS spend (up from ~45% today)

- Top 10 companies control 30%+ of spend (up from ~18% today)

- Mid-market software vendors face existential pressure

- Point solution vendors without clear consolidation path face acquisition or decline

#5: AI-Native Competitors Entering Traditional Markets

The AI-Native Displacement Thesis

For the first time, established software categories are facing disruption from AI-native competitors who didn't exist three years ago. These companies:

- Have no legacy code to maintain

- Are built from the ground up to leverage AI capabilities

- Price 70-90% lower than incumbents

- Achieve feature parity in 6-12 months

- Attract early adopter customers at scale

Category-by-Category Disruption

Customer Service / Help Desk

- Incumbent: Zendesk, Freshdesk, Intercom

- AI-Native Challenger: Specialized chatbot builders, AI-first support platforms

- Disruption Pattern: AI handles 60-80% of support tickets automatically, eliminating need for large help desk teams

- Winner: Companies moving to AI-first models seeing 40-50% cost reduction

Content Creation / Marketing

- Incumbent: Adobe, HubSpot, Marketo

- AI-Native Challenger: Specialized content generation platforms

- Disruption Pattern: AI-native tools generate blog posts, social content, email copy at 1/10 the cost

- Winner: Generalist AI tools from OpenAI, Anthropic creating pressure on specialized vendors

Code Development / DevOps

- Incumbent: GitHub, GitLab, JetBrains

- AI-Native Challenger: Cursor, Codeium, Amazon CodeWhisperer

- Disruption Pattern: AI-powered code completion and generation reduce development time by 20-40%

- Winner: Pure-play AI coding assistants gaining significant market share from IDE vendors

Data Analysis / Business Intelligence

- Incumbent: Tableau, Looker, Power BI

- AI-Native Challenger: Natural language query builders, AI-powered analytics

- Disruption Pattern: LLMs enable non-technical users to query data without SQL or DAX knowledge

- Winner: AI-first analytics platforms reducing need for dedicated BI teams

Document Processing / Contract Review

- Incumbent: Adobe, Docusign, specialized contract platforms

- AI-Native Challenger: LLM-based document parsing and analysis

- Disruption Pattern: AI rapidly processes and extracts information from unstructured documents

- Winner: Generalist models making specialized document tools less differentiated

Why AI-Native Competitors Win Fast

Speed of Innovation AI-native companies can iterate at 4-5x the speed of traditional vendors. New model capabilities every month. Incumbent vendors need 12-18 months to add comparable features.

User Experience Building products around AI capabilities creates fundamentally better UX. AI-native tools feel natural and intuitive because the entire product is designed around AI. Incumbent vendors retrofitting AI often create clunky experiences.

Cost Structure AI-native companies are built on commodity LLM infrastructure (OpenAI, Anthropic APIs). This scales to millions of users without adding marginal cost. Incumbent vendors carry cost of maintaining legacy infrastructure.

Cultural Velocity Small teams moving fast beat large organizations with process overhead. AI-native companies have zero legacy customers to defend, enabling aggressive feature development.

Strategic Implications

For traditional software vendors, competition from AI-native companies presents a no-win scenario:

- Ignore the threat: Market share erodes as customers adopt AI-native alternatives

- Compete head-to-head: Difficult given cost structure disadvantage and speed disadvantage

- Acquire AI-native competitor: Expensive and often disrupts their cultural velocity (integration kills what made them successful)

- Partner with AI-native companies: Gives competitors access to customer relationships

HubSpot maintains a stable NRR at 103% with customer growth, while Zoom experiences a decline in enterprise NRR to 98% and a reduction in customer count. Estimated data for Zoom's customer count change.

#6: Customer Empowerment Through Generative AI

The Customer Agency Revolution

Perhaps the most profound threat to traditional software vendors is the simplest: customers no longer need vendors' permission to solve their own problems. Generative AI has fundamentally shifted the balance of power between software vendors and their customers.

Historically, if a customer needed specialized software capability, they had limited options:

- Buy an existing product that partially addressed the need

- Custom develop a solution (expensive, time-consuming, risky)

- Hire a consulting firm (expensive, creates vendor lock-in)

There was substantial friction in each path, which benefited software vendors. These frictions are evaporating.

Generative AI as Democratization Engine

Scenario 1: Content Generation Historically: Hire writers, designers, or buy specialized software Today: Prompt ChatGPT 4 to generate content variants Result: In-house team generates 10x more content at 1/10 the cost

Scenario 2: Data Analysis Historically: Hire data analyst or buy analytics software Today: Upload data to Claude, ask questions in plain English Result: Non-technical users self-serve analytics they previously needed specialists for

Scenario 3: Software Development Historically: Hire developers or outsource to agencies Today: Use Cursor + Claude to generate 80% of boilerplate code Result: Non-technical founders can build software that previously required engineering teams

Scenario 4: Customer Support Historically: Hire customer service team or buy help desk software Today: Deploy AI chatbot that handles 70-80% of queries Result: One person managing thousands of customer interactions

The Long-Tail SaaS Disruption

For decades, software vendors benefited from a supply-demand mismatch: far more businesses needed specialized software than existed commercial solutions. Generalist software companies (SAP, Oracle, Salesforce) became dominant because they addressed broad use cases profitably.

Generative AI is eliminating this supply-demand mismatch. Customers can now generate specialized tools tailored to their exact use cases, at 1/100 the cost of commercial software.

This doesn't mean long-tail software solutions disappear. It means they'll be built by internal teams using AI tools, not purchased from external vendors.

Implications for Vendor Lock-In

One of software vendors' greatest assets was lock-in through switching costs. Migrating off Salesforce meant months of work, massive implementation costs, data migration risk, and retraining. The high switching cost kept customers trapped even as they became dissatisfied.

Generative AI is reducing switching costs by:

Faster Implementation With AI assistance, migrating from one platform to another takes weeks instead of months. AI tools can help with data migration, configuration, and custom development.

Reduced Switching Risk Proof-of-concept environments can be spun up in hours rather than weeks. Testing before commitment is easier and cheaper.

In-House Capability Customers with AI tools can customize new platforms to match their specific workflows, reducing the need for vendor professional services.

The Empowered Customer as Existential Threat

When customers have the capability and tools to solve their own problems, they fundamentally rewrite the customer-vendor relationship.

Instead of asking "Should we renew with Vendor X?", customers start asking "Is Vendor X's rate of innovation faster than our in-house AI-assisted development?"

For many traditional vendors, the answer is no.

The Compounding Effect: When Six Threats Converge

Why Individual Threats Are Survivable, Combined Threats Are Not

Each of the six threats described above would challenge traditional software vendors. Combined, they create a perfect storm that tests the viability of legacy business models.

Threat 1 (Seat Slowdown) kills predictable revenue expansion.

Threat 2 (Price Increases) tries to compensate for lost expansion revenue by raising prices on existing customers.

Threat 3 (AI Budget Reallocation) diverts new budget to AI instead of software expansion.

Threat 4 (Consolidation) reduces total addressable market by eliminating point solution vendors.

Threat 5 (AI-Native Competition) captures new customers at lower price points.

Threat 6 (Customer Empowerment) gives customers capability to build their own solutions.

What makes these six threats compounding rather than additive:

They reinforce each other:

- Price increases (Threat 2) make customers more amenable to consolidation (Threat 4)

- Consolidation (Threat 4) reduces addressable market for smaller vendors, making them vulnerable to AI-native competitors (Threat 5)

- AI budget reallocation (Threat 3) funds development of AI-native competitors (Threat 5)

- Customer empowerment (Threat 6) gives customers exit ramps from consolidation vendors if they become too expensive

Market Share Reallocation Model

Using simplified modeling, here's how we expect market share to shift through 2026-2027:

2025 Enterprise Software Market Share (Baseline):

- Top 10 vendors: 28%

- Vendors 11-50: 22%

- Vendors 51-500: 35%

- Long-tail vendors (<500): 15%

2027 Enterprise Software Market Share (Projected):

- Top 10 vendors: 38-42% (consolidation benefit)

- Vendors 11-50: 18-20% (acquisition pressure)

- Vendors 51-500: 25-28% (AI-native displacement)

- Long-tail vendors: 8-12% (customers build in-house)

This represents substantial market share reallocation within a growing market—complexity, since absolute revenue might grow while relative market share declines significantly.

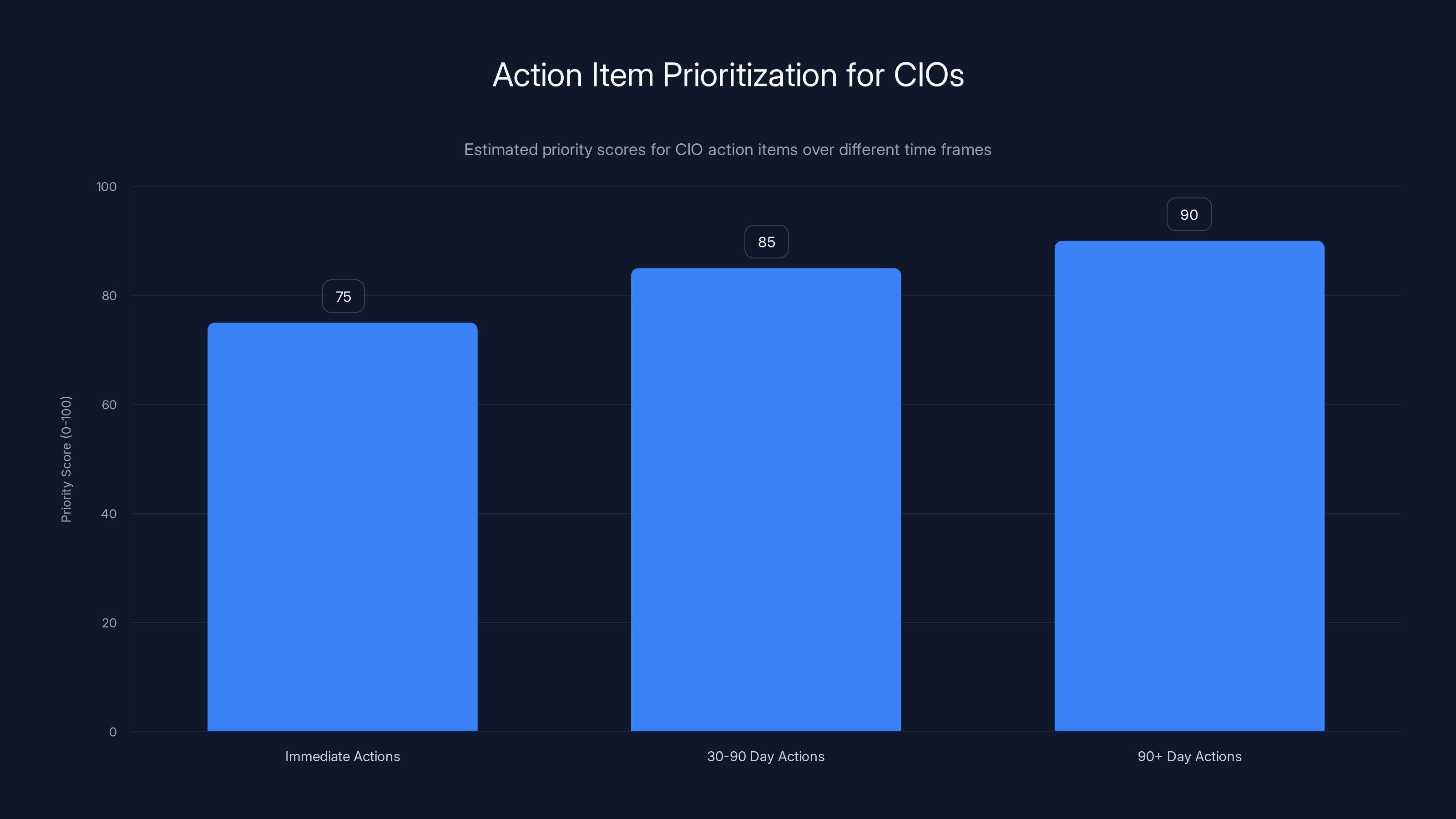

Estimated data suggests that CIOs should prioritize actions in the 90+ day timeframe, focusing on consolidation and AI-native exploration.

Defensive Strategies: How Traditional Vendors Can Survive

Strategy 1: Become Genuinely AI-Native

Half-measures don't work. Vendors that bolt AI onto existing products suffer from:

- User perception of AI as tacked-on

- Lack of cultural commitment to AI-first

- Technical debt preventing rapid AI iteration

Successful repositioning requires:

Structural Changes:

- Reorganize engineering around AI-first product development

- Reallocate technical debt paydown budget to AI research

- Hire top AI researchers (not just software engineers)

- Partner with foundation model companies (OpenAI, Anthropic)

Product Changes:

- Rebuild core workflows around AI assistance, not just automating existing workflows

- Design UX for natural language interaction

- Implement continuous model evaluation and improvement

- Create AI-powered analytics and insights unavailable in non-AI products

Market Changes:

- Reposition messaging around AI-native capabilities

- Emphasize AI ROI in sales conversations

- Benchmark against AI-native competitors, not incumbent competitors

Strategy 2: Pivot to Horizontal Consolidation

If seat expansion is dead, the next frontier is consolidating multiple vertical functions into a single platform. Microsoft's success with 365 demonstrates this clearly.

The Consolidation Play:

- Start with core product (CRM, HR, Finance, etc.)

- Expand adjacent functionality organically or through acquisition

- Integrate seamlessly so switching costs increase

- Price bundled solution at discount to point solutions

- Capitalize on simplification benefits

Successful execution requires:

- Customer success focus on adoption of adjacent products

- Integration as core product differentiator, not afterthought

- Single, unified data model across products

- Cross-product analytics and insights

Strategy 3: Disaggregate and Become API-First

Consolidation favors large vendors. Conversely, disaggregation and modular architecture favor smaller, focused vendors.

The Disaggregation Thesis:

- Build best-of-breed solution for specific problem

- Expose capabilities via clean APIs and webhooks

- Integrate deeply with other point solutions (Slack, Zapier, Make, etc.)

- Price cheaply since customers aren't forced to buy bundle

- Focus on best possible user experience for narrow use case

Execution examples:

- Calendly (scheduling) dominates by being best-in-class for single function

- Stripe (payments) owns market through API-first approach

- Figma (design) wins through superior UX for narrow use case

Strategy 4: Embrace a Freemium-to-Enterprise Model

Traditional SaaS enterprise sales are under attack. Freemium models invert the sales funnel:

How Freemium Disrupts Traditional Sales:

- Eliminate sales gatekeeping (users self-discover)

- Build habits and workflow integration at no cost

- Convert high-engagement users to paid tiers

- Capture long-tail customers at low acquisition cost

Comparison of traditional vs. freemium motion:

| Metric | Traditional | Freemium |

|---|---|---|

| Sales Cycle | 3-12 months | 2-8 weeks |

| CAC | $15k-100k | $1k-10k |

| Time to ROI | 6-18 months | 1-3 months |

| User Self-Discovery | 5-10% | 60-80% |

| Product-Market Fit Timeline | 18-36 months | 6-12 months |

Successful freemium execution requires:

- Clear upgrade path from free to paid

- Free tier valuable enough to drive adoption

- Freemium unit economics that support enterprise payoff

- Self-serve onboarding and product-led growth

Strategy 5: Focus Ruthlessly on Customer Success

In a market with stalled seat expansion and customer empowerment via AI, retention becomes more valuable than acquisition. Every churned customer is both lost revenue and competitive victory for alternative vendors.

CS Excellence Framework:

- Expand NRR through value expansion (not seat/price expansion)

- Reduce churn through proactive engagement (before customers leave)

- Build communities and user networks (increase switching costs)

- Create customer advisory boards (improve product-market fit)

- Measure and optimize logo retention (leading indicator of health)

For vendors like Runable and other scrappy alternatives, customer success is competitive advantage—spending 2x+ on CS per customer as percentage of revenue, creating fanatical loyalty that enterprise vendors can't match.

Strategy 6: Attack Pricing and Cost Structure

Price increases are crowding out budget for alternatives. What if vendors went the opposite direction?

Radical Affordability as Competitive Weapon:

- Simplify pricing to single SKU (per user/month)

- Commit to no price increases for 3+ years

- Undercut incumbents by 50%+ (e.g., 35-50/month)

- Build scale to overcome lower margins

Who's Winning with Affordability:

- Runable ($9/month for AI automation) captures price-sensitive developers

- Loom ($80/month for unlimited users) captures SMB video communication

- Figma ($180/month for design) disrupted Adobe through accessibility

Offensive Strategies: How New Entrants Can Win

The AI-Native Playbook

AI-native competitors don't need to compete with legacy vendors on their terms. Instead, they can follow a proven playbook:

Step 1: Identify Legacy Vendor Weak Point

Find an area where incumbent vendors are:

- Slow to innovate (feature takes 12+ months)

- Carrying technical debt (legacy system prevents rapid iteration)

- Misaligned with customer needs (feature rarely used)

- Overpriced (customers resentful of pricing)

Step 2: Build AI-First Solution

- Leverage LLM APIs (OpenAI, Anthropic) rather than building models

- Design product specifically for AI capabilities

- Iterate rapidly (weekly/biweekly releases)

- Focus on top 20% of use cases, solve them perfectly

Step 3: Launch with Product-Led Growth

- Free trial or freemium tier

- Zero sales gatekeeping

- Self-serve onboarding

- Focused on early adopters

Step 4: Expand Horizontally

Once product achieves PMF:

- Expand to adjacent use cases

- Build integrations with complementary tools

- Create community and network effects

- Explore vertical expansion or horizontal consolidation

Case Study: Cursor vs. GitHub Copilot

GitHub Copilot (incumbent play):

- Built by Microsoft (GitHub acquisition)

- Integrated into VS Code

- $10-20/month

- Feature parity with legacy development environments

- Slower iteration

Cursor (AI-native play):

- Built on Claude and GPT-4

- Intentionally designed for AI-first development

- $20/month (competitive)

- Dramatically better UX for AI-powered coding

- Weekly feature releases

- Captured significant developer mindshare in first 18 months

Cursor's competitive advantage isn't price or features—it's cultural fit. Developers prefer tools built by developers who understand AI-first workflows.

AI spending is growing at an estimated 40-50% annually, significantly outpacing traditional software's 8-15% growth. Estimated data.

Vertical and Horizontal Implications

Which Verticals Face Greatest Disruption Risk?

Highest Risk (75%+ probability of major disruption):

- Customer Service/Help Desk: AI handles 70-80% of queries, eliminating need for large teams

- Content Creation: AI generates content at 1/100 cost of human creation

- Finance/Accounting: AI automates transaction processing, reconciliation, expense management

- Customer Data Platforms: AI natural language querying eliminates complex SQL/ETL needs

Medium Risk (50-75% probability):

- CRM/Sales: AI prospecting and email automation reduce manual work, but strategic selling remains

- Project Management: AI task tracking and scheduling helpful, but people coordination remains core

- HR/Talent: AI recruiting and onboarding accelerates process, but culture/retention remain human-centric

- Business Intelligence: AI-powered analytics democratizes BI, but strategic insights remain valuable

Lower Risk (25-50% probability):

- ERP Systems: Core financial backbone requires stability and compliance, less susceptible to disruption

- Supply Chain: Domain-specific complexity creates high switching costs

- Engineering Collaboration: Network effects and integration prevent easy displacement

- Cybersecurity: Regulatory requirements create switching costs

Horizontal Implications: The Platform Winners and Losers

Winners:

- Cloud Infrastructure (AWS, Azure, GCP): Benefiting from AI workload growth

- Foundation Models (OpenAI, Anthropic): Becoming strategic layer for all software

- Integration Platforms (Zapier, Make, Segment): Becoming critical in disaggregated software ecosystem

- Developer Platforms (GitHub, GitLab): Central to software development workflows

Losers:

- Traditional ERP (SAP, Oracle): Slower innovation, higher pricing, legacy tech stack

- Marketing Automation (HubSpot, Marketo): Pressure from AI-native content and analytics tools

- Business Intelligence (Tableau, Looker): Disrupted by natural language querying

- Point Solutions (Help Desk, Project Management): Being consolidated into broader platforms

The Role of Economics in Software Disruption

Unit Economics Transformation

One reason AI-native companies win so decisively is radical unit economics improvement.

Traditional SaaS Unit Economics:

- CAC (Customer Acquisition Cost): $8,000-15,000

- ACV (Annual Contract Value): $5,000-25,000

- CAC Payback Period: 8-16 months

- Gross Margin: 70-75%

AI-Native SaaS Unit Economics:

- CAC: $1,000-3,000 (product-led growth)

- ACV: $1,500-8,000 (lower price point, higher volume)

- CAC Payback Period: 2-4 months

- Gross Margin: 80-85% (leveraging API-based infrastructure)

The 4-10x improvement in CAC payback period fundamentally changes business dynamics. An AI-native company can achieve profitability in 24-36 months versus 48-72 months for traditional SaaS.

This creates a compounding advantage: profitable AI-native companies can reinvest margins into product development and marketing, accelerating competitive displacement.

Pricing Power Analysis

Why AI-Native Companies Price Lower:

- Lower cost structure: API-based costs scale linearly; no infrastructure overhead

- PLG advantages: No sales team overhead; lower CAC enables lower prices

- Rapid iteration: Faster innovation justifies premium pricing less necessary

- Market dynamics: New entrants need market share; lower prices accelerate adoption

Why Traditional Vendors Price Higher:

- Enterprise sales costs: Sales teams, implementation, professional services

- Legacy costs: Supporting older infrastructure, maintaining backward compatibility

- Market position: Established vendors have some pricing power

- Margin requirements: Shareholders expect 70%+ gross margins and 30%+ operating margins

This creates an unstoppable dynamic:

- AI-Native: Low price → High volume → Profitable → Reinvest → Better product

- Traditional: High price → Lower volume → Margin pressure → Less reinvestment → Worse product

Future State Prediction: Enterprise Software in 2027-2028

The Likely Outcome

Based on historical software disruption patterns (Netscape → Chrome, client-server → SaaS, on-premise → cloud), we expect:

By 2027:

- Top 10 vendors increase market share to 38-42% (consolidation benefit)

- Vendors 11-50 experience 10-15% revenue decline (displacement + consolidation)

- AI-Native cohort (founded 2021-2024) captures 15-20% of software spending

- Long-tail/in-house development grows to 8-12% (customer empowerment)

- 40-50% of mid-market software vendors pursue acquisition or decline

By 2028:

- AI-Native/AI-Augmented becomes table stakes (all vendors must offer credible AI)

- Pricing equilibrates around AI value delivered (not seat count)

- Consolidation continues: 30-40% fewer independent vendors

- Switching costs decline as AI tools reduce implementation friction

- Customer retention becomes competitive battleground (NRR optimization critical)

The Winners' Circle

Survivors will likely share these characteristics:

- Genuine AI integration (not bolt-on features)

- Clear strategic positioning (not trying to be everything to everyone)

- Exceptional customer success (retention focus)

- Reasonable pricing (transparent, not exploitative)

- Rapid product iteration (quarterly major releases minimum)

- Strong platform/API strategy (interoperability)

- Community and network effects (user loyalty beyond product)

Specific Action Items for Different Stakeholder Groups

For Enterprise Software CIOs: Preparing for 2026

Immediate Actions (Next 30 Days):

- Audit SaaS portfolio for consolidation opportunities (potential 15-20% cost reduction)

- Evaluate AI readiness of existing vendors (request detailed AI roadmaps)

- Benchmark pricing against market to identify overpayment (hire SaaS management firm if needed)

- Assess vendor health (stock price, NRR, employee count trends) to identify acquisition risk

- Identify switching costs for major vendors (implementation effort, data migration)

30-90 Day Actions:

- Develop AI strategy independent of vendors (what problems will you solve with AI internally?)

- Evaluate AI-native alternatives to existing point solutions

- Renegotiate major contracts leveraging multivendor evaluation pressure

- Plan vendor consolidation roadmap (prioritize by switching cost and ROI)

- Build internal AI capability (hire data scientists, establish AI COE)

90+ Day Actions:

- Execute consolidation plan (migrate off point solutions to consolidated platforms)

- Implement SaaS governance (prevent shadow IT, optimize spend)

- Build vendor scorecard (evaluate NRR, innovation, pricing, customer success)

- Establish AI-native exploration program (allocate 10-15% of budget to experimental AI tools)

- Develop customer empowerment model (enable teams to build custom solutions with AI)

For Mid-Market Software Vendors: Strategic Choices

Path 1: Consolidation (Acquire or Be Acquired)

- Identify complementary vendors in adjacent verticals

- Pursue acquisition strategy to build platform

- Rebrand around consolidated offering

- Reallocate sales focus to existing customer expansion

- Example: HubSpot acquiring adjacent MarTech tools

Path 2: Specialization (Go Niche)

- Focus ruthlessly on best-of-breed solution for specific vertical

- Develop vertical-specific features competitors won't match

- Build community and network effects

- Price at premium for specialized capability

- Example: Figma in design, Calendly in scheduling

Path 3: AI-Native Pivot

- Rebuild product around AI-first capabilities

- Expand TAM through AI-powered features competitors can't match

- Reposition pricing and packaging around AI value

- Recruit top AI talent to engineering team

- Example: Databricks evolving from Spark company to AI platform

Path 4: Acquisition Target

- Position as acquisition target for larger consolidators

- Optimize for acquisition multiples (profitable, growth, customer quality)

- Build optionality (could operate independently or as bolt-on)

- Explore strategic acquirers proactively

For Founders Building AI-Native Companies: Maximizing Opportunity

Phase 1: Product-Market Fit (Months 0-12)

- Identify pain point where incumbent vendors are weak

- Build 80/20 solution that solves it 90% as well at 10% the cost

- Launch to early adopters (not general market)

- Obsess over customer feedback and product iteration

- Avoid distractions: Fundraising, enterprise sales, market expansion

Phase 2: Scaling (Months 12-24)

- Double down on product-led growth (free trial, freemium, community)

- Expand TAM horizontally to adjacent use cases

- Build integrations with complementary tools (Slack, Zapier, etc.)

- Establish pricing that scales with usage but remains affordable

- Focus on retention over acquisition (NRR > CAC)

Phase 3: Competitive Moat (Months 24-36)

- Build platform or API enabling ecosystem development

- Create network effects through community, marketplace, or data network

- Expand to adjacent verticals or adjacent products

- Evaluate consolidation opportunities (acquire complementary products)

- Establish market position as category leader

Conclusion: Navigating the Transformed Software Market

The Fundamental Shift

We are witnessing the most significant transformation in software markets since the transition from on-premise to cloud (2005-2015). The drivers are different but equally powerful:

- Seat-based growth models are mathematically unsustainable

- Price increases are crowding out alternatives

- AI is capturing all new budget flowing to enterprise software

- Consolidation pressures are reducing vendor count and addressable market

- AI-native competitors are entering categories at lower cost

- Customer empowerment is reducing dependence on software vendors

These aren't cyclical trends that will reverse. They represent structural changes in how enterprises buy, deploy, and benefit from software.

The Winners' Playbook

Companies thriving in this environment will share common characteristics:

- Honest assessment of competitive position (not wishful thinking)

- Strategic clarity on consolidation vs. specialization vs. pivot

- Ruthless prioritization (do fewer things better)

- Customer obsession (especially retention and success)

- Courage to change (old playbooks won't work)

- Reasonable pricing (transparency builds trust)

- Rapid iteration (move fast, fail fast, learn)

Those clinging to legacy business models—hoping price increases and AI feature bolt-ons will sustain growth—are increasingly likely to face displacement.

Opportunities Hidden in Threat

For the right competitors, the threats described in this analysis are opportunities:

- Seat slowdown creates opportunity for value-based (not seat-based) pricing

- Price increases create opportunity for affordable alternatives

- AI budget flows create opportunity for pure-play AI tools

- Consolidation creates opportunity for best-of-breed point solutions serving niche verticals

- AI-native competition creates opportunity for founders unburdened by legacy

- Customer empowerment creates opportunity for enabling platforms and building tools

The Investment Thesis

If you're evaluating software companies or building software strategies:

- Avoid: Traditional vendors with poor AI strategy, high prices, and negative NRR

- Monitor: Consolidators with credible vertical expansion strategies and customer success focus

- Invest in: AI-native companies with PMF, efficient unit economics, and clear moats

- Build: Specialized solutions for vertical use cases where customer ROI is undeniable

- Enable: Platforms that let customers build custom solutions without vendor dependence

Final Thoughts

The 2026 software market is unforgiving. Companies that thrived in 2015-2025 cannot assume success in 2026-2030 based on past momentum. The old playbooks are broken.

But for those willing to adapt—truly adapt, not cosmetically rebrand—the opportunity is enormous. Enterprise software spending continues growing. Customers want tools that solve their problems efficiently. The market will flow to vendors that deliver genuine value, not extraction.

The question isn't whether disruption will happen. It's happening now. The question is whether your company will lead the disruption or be disrupted by it.

FAQ

What are the main threat vectors attacking traditional B2B software in 2026?

The six primary threats are: (1) seat slowdown from flattened tech hiring and automation, (2) price increases crowding out innovation budgets, (3) AI budget reallocation away from traditional software, (4) vendor consolidation reducing addressable market, (5) AI-native competitors entering established categories, and (6) customer empowerment through generative AI. These threats are compounding rather than additive—each reinforces the others, creating a difficult environment for legacy software vendors.

Why is the seat-based software model failing?

The seat-based model assumes headcount growth drives software expansion. This assumption broke when tech hiring plateaued in 2024-2025. Additionally, automation and AI tools let companies accomplish more work with fewer people. When headcount stops growing and productivity per employee increases, the expansion engine for seat-based software stalls. Companies like Zoom ($ZOOM) and HubSpot show enterprise customers actually declining in count despite overall market growth.

How much are enterprises actually spending on SaaS inflation?

SaaS inflation is running at 11.4% annually (nearly 5x higher than general inflation), with cost per employee rising from

Which software categories face the highest disruption risk from AI-native competitors?

Customer service/help desk, content creation, finance/accounting, and customer data platforms face 75%+ disruption probability. These categories are being displaced by AI-native solutions because AI can handle 70-80% of tasks at 1/10 the cost. CRM/sales, project management, HR/talent, and business intelligence face 50-75% disruption risk. ERP systems, supply chain, engineering collaboration, and cybersecurity face lower risk (25-50%) due to domain complexity and regulatory requirements creating switching costs.

What strategies should traditional vendors pursue to survive?

Traditional vendors have six primary strategic options: (1) become genuinely AI-native by rebuilding products around AI-first capabilities, (2) pursue horizontal consolidation acquiring adjacent products to increase switching costs, (3) disaggregate into best-of-breed point solutions with clean APIs, (4) embrace freemium-to-enterprise models to reduce sales friction, (5) focus ruthlessly on customer success and retention, or (6) attack pricing with radical affordability. Success requires choosing one strategy and executing with commitment, not pursuing multiple conflicting strategies.

How much market share will AI-native vendors capture by 2027?

Based on historical disruption patterns (on-premise to cloud, client-server to SaaS), AI-native vendors are projected to capture 15-20% of enterprise software spending by 2027. Meanwhile, top 10 vendors are consolidating to 38-42% market share, vendors 11-50 are declining, and long-tail/in-house development is growing. This represents substantial market reallocation within a growing market—absolute revenue might grow while relative market positions shift dramatically.

What advantages do AI-native competitors have over traditional vendors?

AI-native companies benefit from: (1) no legacy code burden enabling 4-5x faster iteration, (2) lower cost structures (APIs vs. legacy infrastructure) supporting lower pricing, (3) better user experience (products designed around AI, not AI bolted on), (4) cultural velocity (small teams move faster than large organizations), and (5) superior unit economics (CAC payback 2-4 months vs. 8-16 months). These advantages compound—profitable AI-native companies reinvest margins into product development, further widening competitive gaps.

How is generative AI changing the customer-vendor relationship?

Generative AI fundamentally shifts power to customers by eliminating switching costs and enabling in-house solution building. Historically, customers needed vendor permission to solve problems (buy software, hire consultants, custom develop). Today, customers can prompt Claude or ChatGPT to generate custom solutions. This eliminates lock-in through switching costs—vendors must now compete on continuous innovation and value delivery rather than inertia and implementation friction.

What should CIOs do to prepare for the 2026 software market?

Immediate actions: (1) audit SaaS portfolio for consolidation opportunities (potential 15-20% cost savings), (2) evaluate existing vendors' AI strategy, (3) benchmark pricing against market, (4) assess vendor health (stock price, NRR trends), (5) identify switching costs. 30-90 day actions: develop independent AI strategy, evaluate AI-native alternatives, renegotiate major contracts, plan vendor consolidation roadmap. 90+ day actions: execute consolidation, implement SaaS governance, develop vendor scorecard, allocate budget to experimental AI tools, enable customer empowerment model.

Which software verticals are most likely to consolidate?

Marketing technology, HR/talent acquisition, financial planning and analysis, and project management are consolidating rapidly around horizontal platforms (Salesforce, Workday, SAP) and specialized consolidators (HubSpot). These verticals have overlapping customer needs and complementary functions creating natural consolidation opportunities. Conversely, security, infrastructure, and engineering tools are remaining specialized because domain-specific expertise and compliance requirements create permanent differentiation.

How can mid-market software vendors position for acquisition?

Mid-market vendors can increase acquisition attractiveness by: (1) optimizing for acquisition multiples (profitability, growth rate, customer quality matter more than absolute scale), (2) building vertical specialization that larger acquirers can't easily replicate, (3) establishing customer loyalty through exceptional success (high NRR, low churn), (4) maintaining clean architecture enabling integration with acquirer's platform, and (5) developing platform or API strategy enabling ecosystem contribution. Conversely, vendors with declining NRR, poor customer success, and deteriorating unit economics face acquisition as distressed asset rather than strategic bolt-on.

Key Takeaways

- Seat-based software growth has stalled as tech hiring flatlines and automation increases productivity per employee

- SaaS inflation at 11.4% YoY (5x general inflation) is crowding out innovation budgets and creating customer resentment

- All incremental enterprise IT budget is flowing to AI, starving traditional software of growth capital

- Vendor consolidation is reducing addressable market and concentration is increasing among top 10 vendors

- AI-native competitors entering established categories with 4-5x faster iteration and 50-90% lower pricing

- Generative AI is empowering customers to build custom solutions, eliminating vendor lock-in through switching costs

- Traditional vendors must choose: consolidate, specialize, pivot to AI-native, or position for acquisition

- AI-native companies achieve superior unit economics (CAC payback 2-4 months vs. 8-16 months traditional) enabling market share capture

- Market share will consolidate: top 10 vendors to 38-42%, AI-native cohort to 15-20%, long-tail in-house development to 8-12%

- Winners in 2026 market will share: genuine AI integration, customer success focus, reasonable pricing, rapid iteration, and strong platforms