![AMD GPU Price Hikes & 16GB Memory Shift: What's Really Happening [2025]](https://tryrunable.com/blog/amd-gpu-price-hikes-16gb-memory-shift-what-s-really-happenin/image-1-1770221498723.jpg)

The GPU Market Is Shifting, And Not In Your Favor

Something's brewing in the graphics card market. If you've been paying attention to the whispers in hardware forums and tech rumors, you've probably heard the story: AMD and its partners are considering price increases. Again. And they're quietly phasing out 16GB models in favor of cheaper 8GB variants, as reported by 36Kr.

Now, this isn't just idle gossip. This is the market doing what markets do—manufacturers testing boundaries, squeezing margins, and hoping consumers won't notice the sleight of hand. But here's the thing: understanding what's actually happening beneath these rumors matters if you're planning to buy a graphics card anytime soon.

The GPU landscape has been absolutely wild the past couple of years. We went from shortage-induced insanity to oversupply. We've seen cryptocurrency miners pivot away from graphics cards. We've watched AI accelerators steal the spotlight from gaming GPUs. And through it all, pricing has been a chaotic mess.

What makes the current situation different is the strategy shift. It's not just about raising prices on existing models. It's about fundamentally reshaping what GPU buyers expect to get for their money. Less VRAM, same (or higher) price tags.

Let's break down what's actually happening, why manufacturers are making these moves, and what it means for you—whether you're a gamer, a content creator, or someone running machine learning workloads.

TL; DR

- Price pressures mounting: AMD and AIB partners are considering new price increases as market competition tightens and demand normalizes

- Memory tier shift: Manufacturers are prioritizing 8GB models over 16GB as a cost-cutting strategy while maintaining margins

- Nvidia's influence: Nvidia's approach to VRAM allocation is setting a precedent that AMD may follow, fragmenting the market

- Consumer impact: Buyers face trade-offs between performance, memory, and budget as the value proposition changes

- Timing matters: Current market conditions create urgency for purchases before potential price hikes take effect

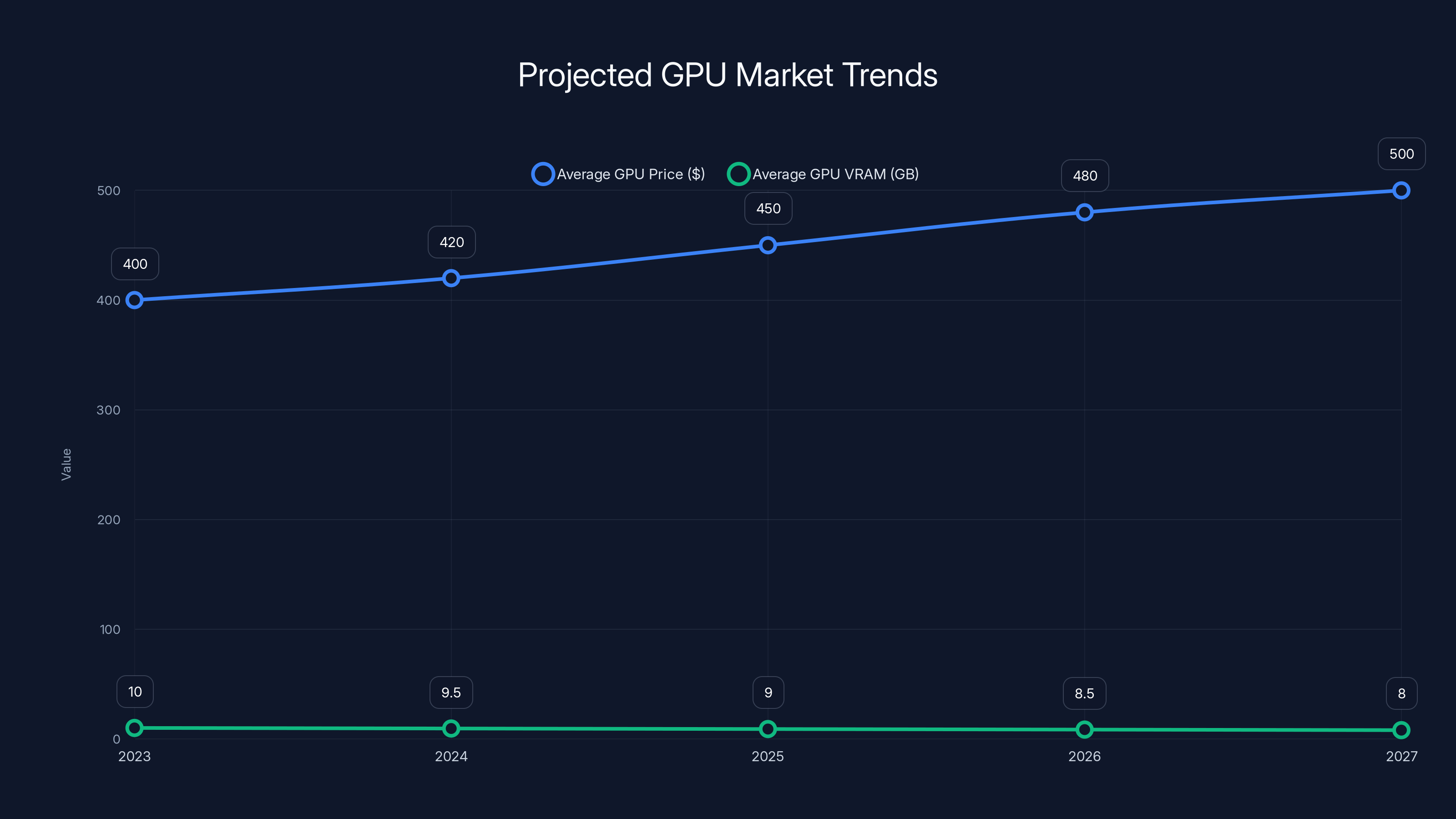

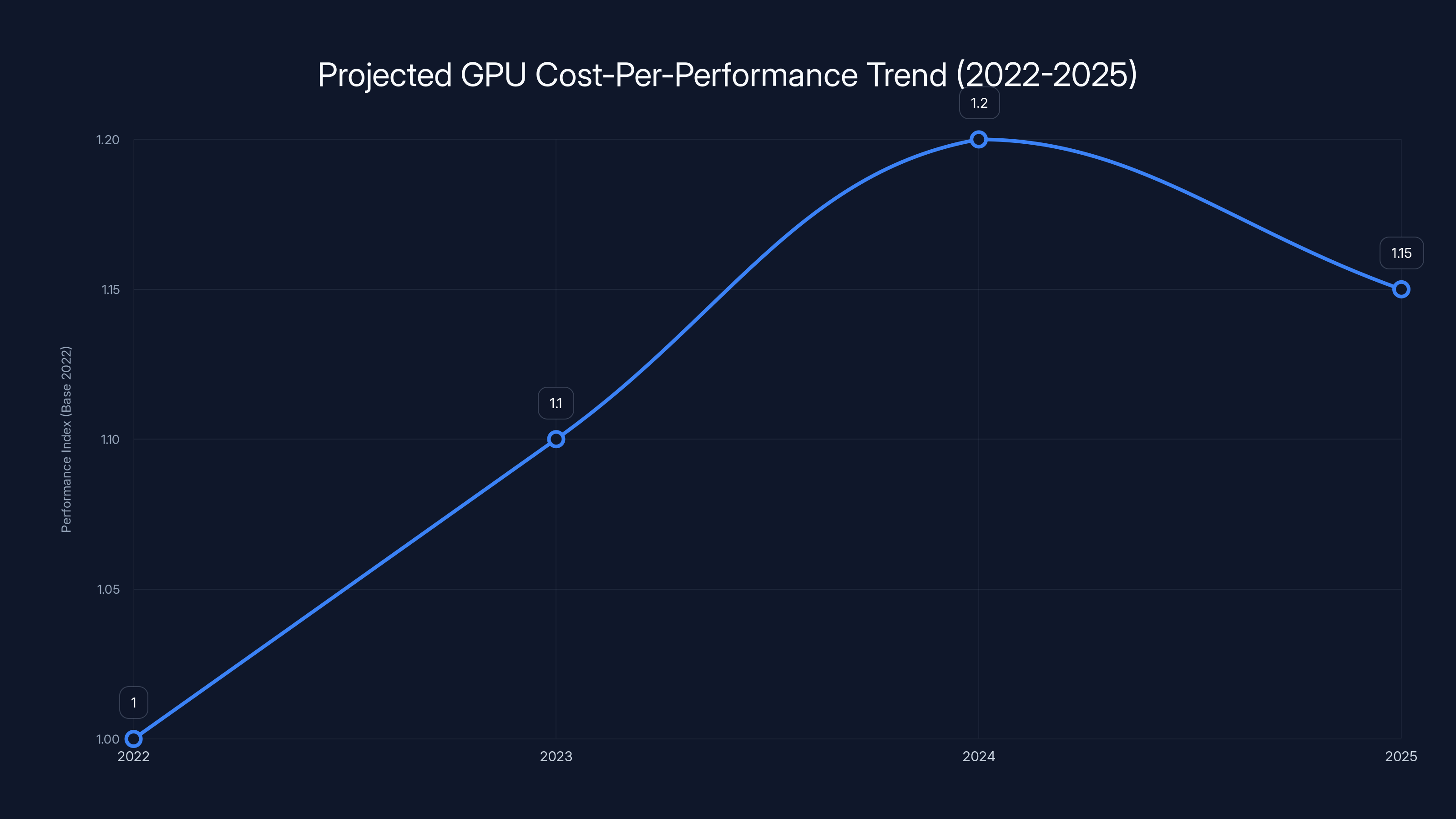

Estimated data suggests a gradual increase in GPU prices and a reduction in average VRAM over the next few years, reflecting manufacturers' focus on margins and strategic product configurations.

Why AMD And Its Partners Are Considering Price Hikes

Let's start with the financial reality. Graphics card manufacturers don't raise prices because they're feeling generous. They raise prices because they need to. The GPU market dynamics have shifted in ways that make margin pressure a real concern.

First, there's the normalization of demand. After the post-pandemic, crypto-fueled GPU shortage that artificially inflated prices, the market cooled significantly. Mining profitability tanked. Ethereum moved to proof-of-stake, eliminating the GPU mining incentive entirely. Gaming demand normalized. Suddenly, manufacturers were left holding inventory and competing on price.

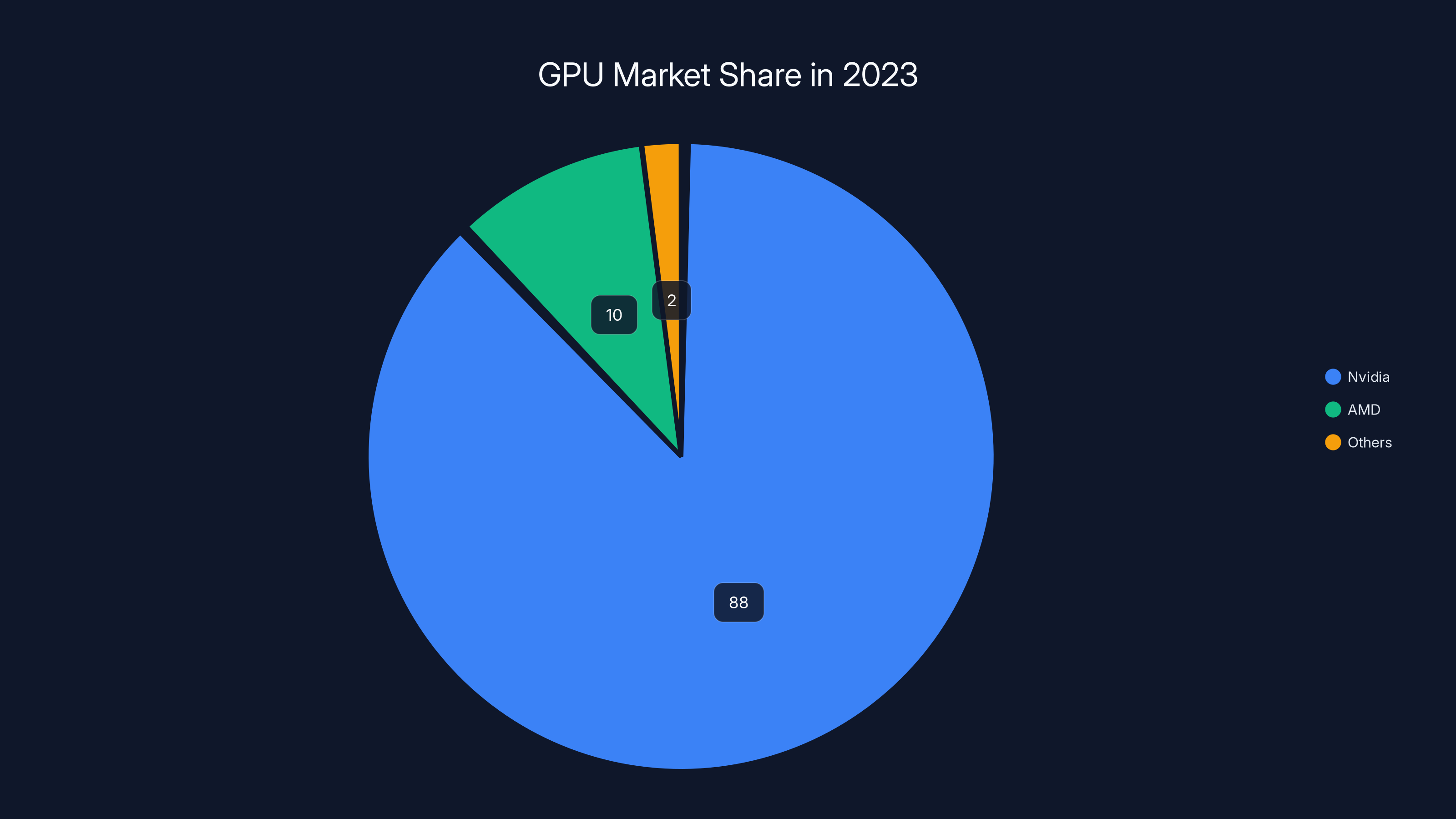

Second, there's the competitive landscape. Nvidia still dominates the discrete GPU market with roughly 88% market share in gaming, but AMD has been chipping away. RDNA 3 and RDNA 4 architectures have actually delivered competitive performance at lower prices. This forces AMD to walk a tightrope: compete on price without destroying margins, or find ways to maintain profitability despite lower unit prices.

Third, there's component cost inflation. Manufacturing costs don't decrease in a straight line. Yields on cutting-edge silicon vary. Memory costs fluctuate. Power delivery components, PCB materials, cooling solutions—all of these have their own supply chain dynamics. If component costs are rising, manufacturers need higher prices to maintain the same profit per unit.

Fourth, there's the AI accelerator pressure. Data centers have become the real money-maker for GPU manufacturers. Consumer graphics cards—gaming GPUs—are increasingly treated as a secondary market. This means less competitive pressure to lower prices in the consumer space. The real competition is in data centers where specialized chips like Nvidia's H100 and H200 command eye-watering prices.

What makes the rumored price hikes interesting is the timing. We're not seeing this in response to massive demand or shortage conditions. We're seeing it in a market with relatively normal supply and moderate demand. That suggests manufacturers believe they can raise prices without significant volume loss—or they're willing to accept volume loss if it maintains profitability.

For AMD specifically, price hikes are risky. Their entire value proposition has been "same performance, lower price than Nvidia." If they raise prices without a corresponding performance improvement, they lose that positioning. But if they don't raise prices, margins get squeezed. Hence the strategy of shifting memory configurations—it's a way to raise effective prices without raising list prices.

Nvidia holds a dominant 88% market share, significantly influencing pricing strategies in the GPU market. Estimated data.

The Memory Tier Strategy: Why 8GB Is Becoming The New Standard

This is where the actual clever bit happens. Instead of blatantly raising prices, manufacturers are reshuffling memory configurations. The rumor is that AMD and its partners are prioritizing 8GB models and de-emphasizing 16GB variants, as noted by The Tacoma Ledger.

On the surface, this seems backwards. More memory is better, right? Why would manufacturers move away from 16GB? The answer is pure economics combined with a misunderstanding of actual workload requirements.

Here's the thing about GPU memory: it's expensive. GDDR6 or GDDR6X memory makes up a significant portion of GPU manufacturing costs. A 16GB variant costs considerably more to produce than an 8GB variant. The die itself might be identical, but you're doubling the memory subsystem—twice as many memory modules, twice the memory interface complexity, potentially different PCB layouts.

Let's do some rough math. If VRAM accounts for roughly 15-25% of GPU manufacturing cost, and doubling memory nearly doubles that component cost, you're looking at an additional

That's the margin compression. By shifting customers toward 8GB, manufacturers maintain better margins on each unit. They might sell fewer high-margin products, but the overall margin percentage improves.

But there's another layer to this strategy. It's also about market segmentation and steering buyers toward higher-priced SKUs. If an 8GB model costs

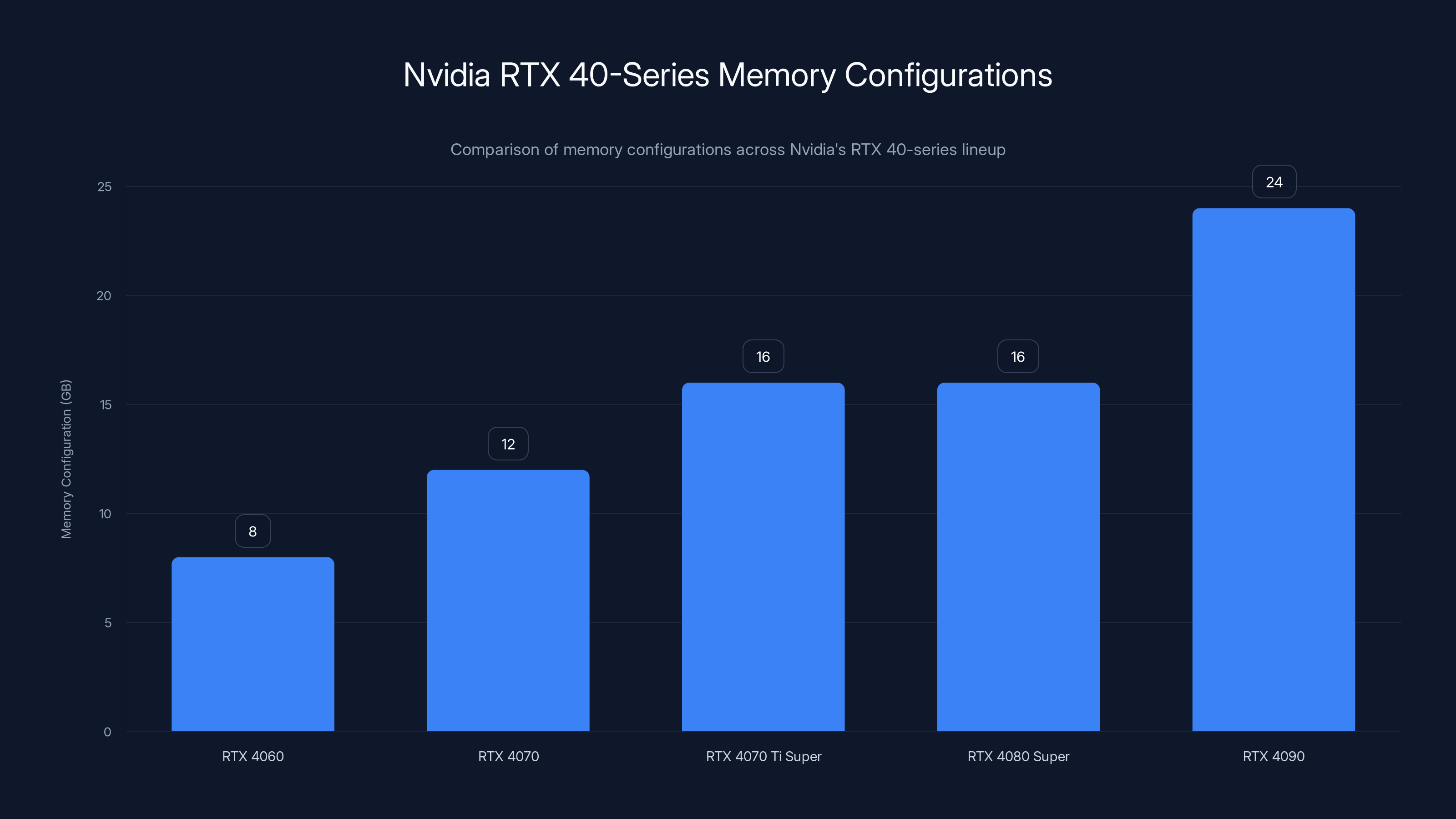

There's also the perception element. Nvidia has been shipping 12GB on the RTX 4060 and RTX 4070, 16GB on the RTX 4070 Ti Super, and 24GB on the RTX 4080. The fact that Nvidia ships varying amounts of VRAM means the market is already fragmented. There's no clear expectation that a specific price point gets a specific amount of memory. Manufacturers can push memory configurations around without customers feeling like they're getting a worse deal.

Another factor is actual workload requirements. For gaming at 1440p with high settings, 8GB is genuinely sufficient in 2025. At 4K, it gets tighter. For machine learning and AI applications, you actually want more than 16GB—you want 24GB or more. The sweet spot for "general purpose" GPU work, it turns out, isn't 16GB. It's fragmented. Some use cases max out at 8GB. Others need 24GB or more. 16GB is the awkward middle child that doesn't quite fit anywhere perfectly.

By moving to 8GB as the volume leader, manufacturers align with the actual needs of the largest customer segment (gamers, where 8GB is reasonable), and push power users toward higher-tier products where memory is less of a compromise.

How Nvidia's Strategy Shaped The Market

Nvidia didn't invent this strategy, but they've perfected it. And their approach is basically a template that AMD is now considering following.

Look at Nvidia's current generation RTX 40-series lineup. The memory configurations are all over the map. The RTX 4060 ships with 8GB. The RTX 4070 comes with 12GB. The RTX 4070 Ti Super has 16GB. The RTX 4080 Super has 16GB. The RTX 4090 has 24GB. There's no consistent pattern. You can't look at price and predict memory.

This is intentional. Nvidia learned a long time ago that customers are willing to pay for perceived performance differences, but memory amounts have become a commodity. If everyone knows that higher price should mean more memory, you create a value expectation. By decoupling memory from price, you create confusion. And confusion is actually advantageous for pricing power.

When there's confusion about whether an extra $50 should get you 2GB more memory, consumers stop using memory as the primary comparison metric. They fall back to looking at raw performance numbers, which are actually more favorable to the manufacturer because performance improvements can be smaller than the price increases.

Nvidia also used this strategy to manage product tiers. The RTX 4070 at 12GB is deliberately positioned between the 4060 at 8GB and the 4070 Ti at 16GB. It's not just a memory difference—it's a performance difference too. But the unconventional memory amount makes direct comparison harder. You can't just look at specs and say "if I need more memory, the 4070 Ti is the obvious choice." Maybe 16GB is overkill. Maybe you can work around 12GB. The ambiguity is actually good for Nvidia's margins.

AMD is now recognizing this. By shifting toward 8GB as a volume product, they can follow Nvidia's playbook: fragment the market, make comparisons harder, reduce the value pressure on higher-end products, and maintain better margins overall.

The broader implication is that memory, which used to be a simple way to segment the market (4GB, 8GB, 16GB), has become a tool for psychological pricing. Manufacturers can use non-standard memory amounts to make price-to-performance comparisons harder, which gives them more pricing power.

Nvidia's strategy of varying memory configurations across its RTX 40-series lineup creates consumer confusion, which can lead to higher pricing power and better margins. Estimated data.

The Financial Reality: Margin Pressure In a Normalized Market

Here's what's actually happening beneath the surface: GPU manufacturers are struggling with margin compression.

During the crypto boom and pandemic shortage, GPU margins were spectacular. Cards that cost

When the market normalized, manufacturers were suddenly facing margin reality. A

The goal now is to restore some of those margins without raising prices so much that volume collapses completely. It's a balancing act. Price too high and sales plummet. Price too low and profitability becomes unacceptable. The sweet spot requires some optimization.

Shifting memory configurations is one optimization. Reducing SKU variety is another. Focusing on specific market segments—premium gaming, AI, data centers—is another. Some of these moves are about efficiency. Some are about steering customers toward more profitable products.

For AMD specifically, there's additional pressure because they're not the market leader. Nvidia can afford to play games with memory and SKUs because they have pricing power from brand dominance. AMD needs to maintain some price advantage or risk losing market share. But they also can't sustain volume-based profitability if margins are too thin. Hence the rumored price increases—they're an attempt to improve the margin equation without completely abandoning the value positioning.

What 8GB GPUs Can Actually Do In 2025

Now let's talk about whether 8GB is actually sufficient. This is important because the shift toward 8GB only makes sense if it doesn't completely hamstring the user experience.

For gaming, 8GB is genuinely adequate in 2025. I'd say it's becoming the baseline. At 1440p with high or ultra settings, most new games run comfortably on 8GB. At 4K with high settings, you're starting to push it—some games will hit VRAM limits and start doing frame rate dips when texture detail exceeds available VRAM. At 4K with ultra settings, 8GB becomes noticeably tight. But acceptable for most scenarios.

The real question is game developers. As new engines mature and texture density increases, will games require more than 8GB? Probably, eventually. But that's a 2-3 year timeframe. Right now, 8GB is fine for current games.

For content creation—3D rendering, video editing, image processing—8GB becomes tighter. If you're working with large datasets or complex scenes in Blender or similar tools, you probably want more. But again, it depends on your specific workflow. Simple to moderate projects? 8GB works. Large-scale professional work? You need more.

For machine learning and AI, 8GB is almost universally insufficient. Most serious ML work requires 12GB, 16GB, or 24GB. If you're training models or running large inference jobs, 8GB is a non-starter. This is where the market really fragments. Gaming-focused users accept 8GB. AI-focused users need 24GB or more. Business AI applications sometimes work with 16GB. There's no single ideal amount.

Consumer demand actually supports this fragmentation. Gamers don't need more than 8GB most of the time. AI researchers actively avoid 8GB because it's not useful for their workloads. There's a weird gap in the 12-16GB range where needs don't align cleanly with available products.

So when manufacturers shift toward 8GB, they're actually aligning with the real needs of their largest market segment. The trade-off is that anyone with more demanding needs is pushed toward higher tiers or alternatives. But for the mass market of casual and moderate gamers, 8GB makes sense.

The challenge is the messaging. If manufacturers make this sound like a feature cut rather than a strategic realignment, customers feel cheated. "You're giving me less for the same price" is a message that drives customers to competitors. But "we're optimizing for the needs of gaming users" is a message that feels more acceptable. Same move, different framing.

The trend shows a slight decline in performance per dollar for GPUs in 2025 compared to previous years, indicating a potential increase in cost-per-performance. Estimated data.

Nvidia's Dominance Makes AMD's Position Tricky

Here's the uncomfortable reality for AMD: they're competing against a company with 88% market share in discrete gaming GPUs. That's not a competitive market—that's market dominance.

When Nvidia can maintain prices despite AMD offering similar performance at lower cost, it's because of brand loyalty, driver maturity, CUDA software ecosystem, and market momentum. AMD's RDNA 3 and RDNA 4 are legitimately competitive. The performance-per-dollar is better. But customers still choose Nvidia, often for reasons that have nothing to do with the hardware specs.

This creates a specific constraint for AMD. They can't just copy Nvidia's strategy wholesale. If Nvidia raises prices and reduces memory, AMD can follow because Nvidia has brand loyalty to fall back on. If AMD raises prices and reduces memory, they're giving up the one advantage they have—being the cheaper alternative.

But if AMD doesn't raise prices and doesn't adjust memory configurations, their margins get crushed. Component costs don't stay flat. Manufacturing complexity increases. Competition from Nvidia's newer products forces them to keep older products at lower price points to clear inventory.

So AMD is in a position where they need to improve margins without sacrificing their value positioning. The rumored approach—raise prices modestly while shifting to 8GB as the volume product—is a compromise. It's not as aggressive as Nvidia can afford to be, but it's more than enough to upset customers who expect AMD to maintain price leadership.

The real risk for AMD is losing customers to Nvidia during this transition. If customers feel like AMD is now more expensive and less feature-complete (less memory), they might just pay the extra money for Nvidia brand recognition and driver stability. AMD has to execute this carefully—raising prices enough to improve margins but not so much that they lose their value positioning entirely.

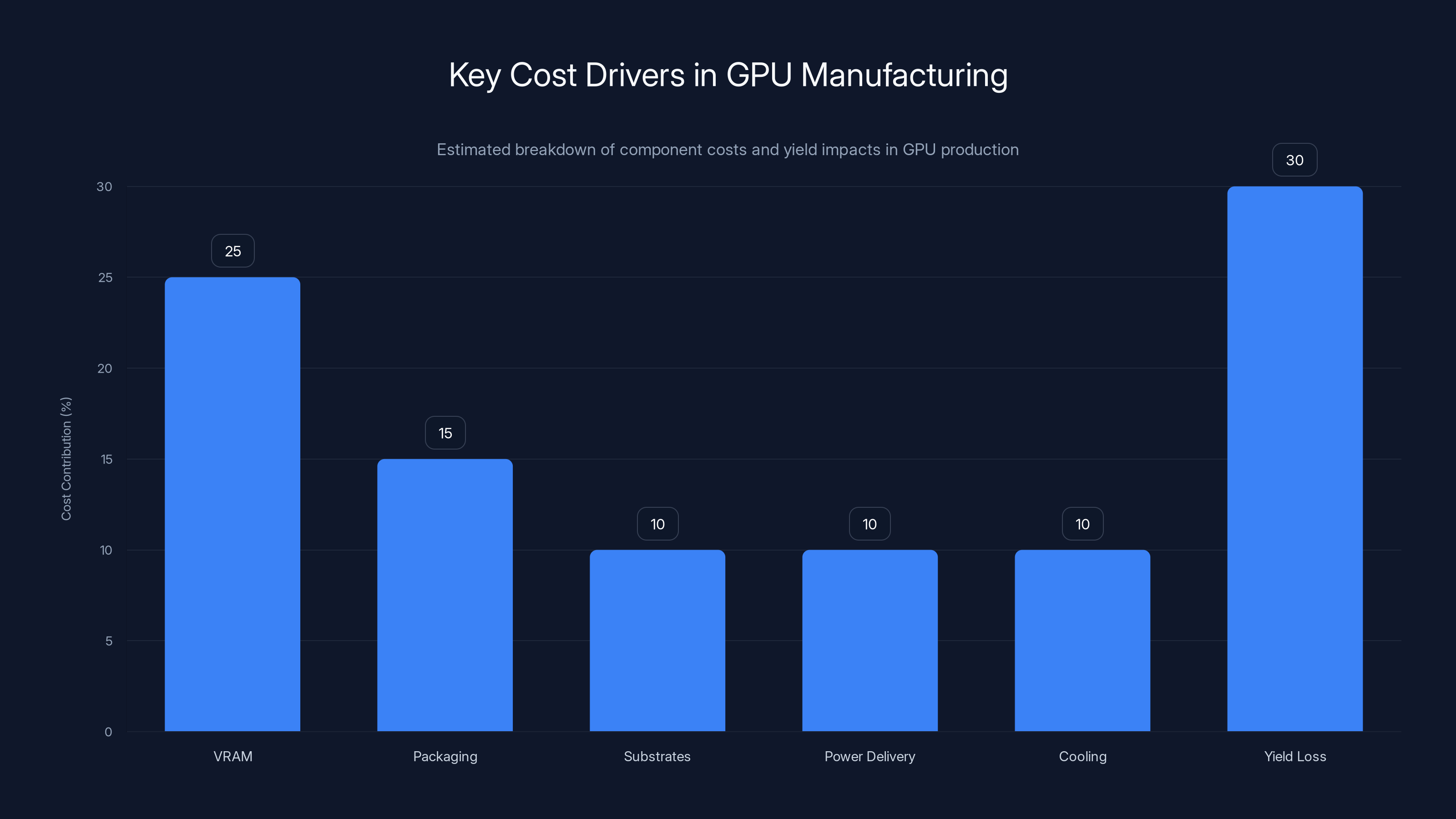

The Supply Chain Layer: Component Costs And Manufacturing Reality

Why are manufacturers considering price increases in a normalized market? Let's look at the actual supply chain.

GDDR6 and GDDR6X memory pricing has been relatively stable the past year, but it's not free. VRAM is one of the highest-cost components on a GPU. Add packaging, substrates, power delivery components, cooling solutions, and you're at a significant materials cost before even accounting for manufacturing, logistics, and retail markup.

But the real constraint isn't memory pricing—it's yields. Not every GPU manufactured works perfectly. Yields on leading-edge semiconductor manufacturing are typically 40-60%. You might produce 100 dies and only get 50 good ones. The good ones subsidize the bad ones. If yields drop, your effective manufacturing cost per working unit increases.

AMD and Nvidia both manufacture at leading-edge process nodes (5nm, 3nm) where yield management is critical. A 5% drop in yields across a production run effectively raises manufacturing costs by 5-10% per unit. That drives price increases.

There's also the packaging and substrate layer. GPU packages are complex—high pin count, specialized materials, specific heat dissipation requirements. Advanced packaging (like chiplet designs) adds cost. If manufacturers are moving toward more advanced designs to improve performance, that's another cost driver.

When you layer all of these factors—stable VRAM costs, variable yields, advancing manufacturing process costs, advanced packaging complexity—you end up with subtle but consistent cost pressure. Not massive inflation, but enough to justify price increases if you can get away with it.

AMD and partners are essentially testing whether the market will bear price increases in this normalized environment. They're betting that the value improvement from new architectures justifies the higher prices. But because yields and component costs are relatively stable rather than declining, the value proposition is tighter than in previous generations.

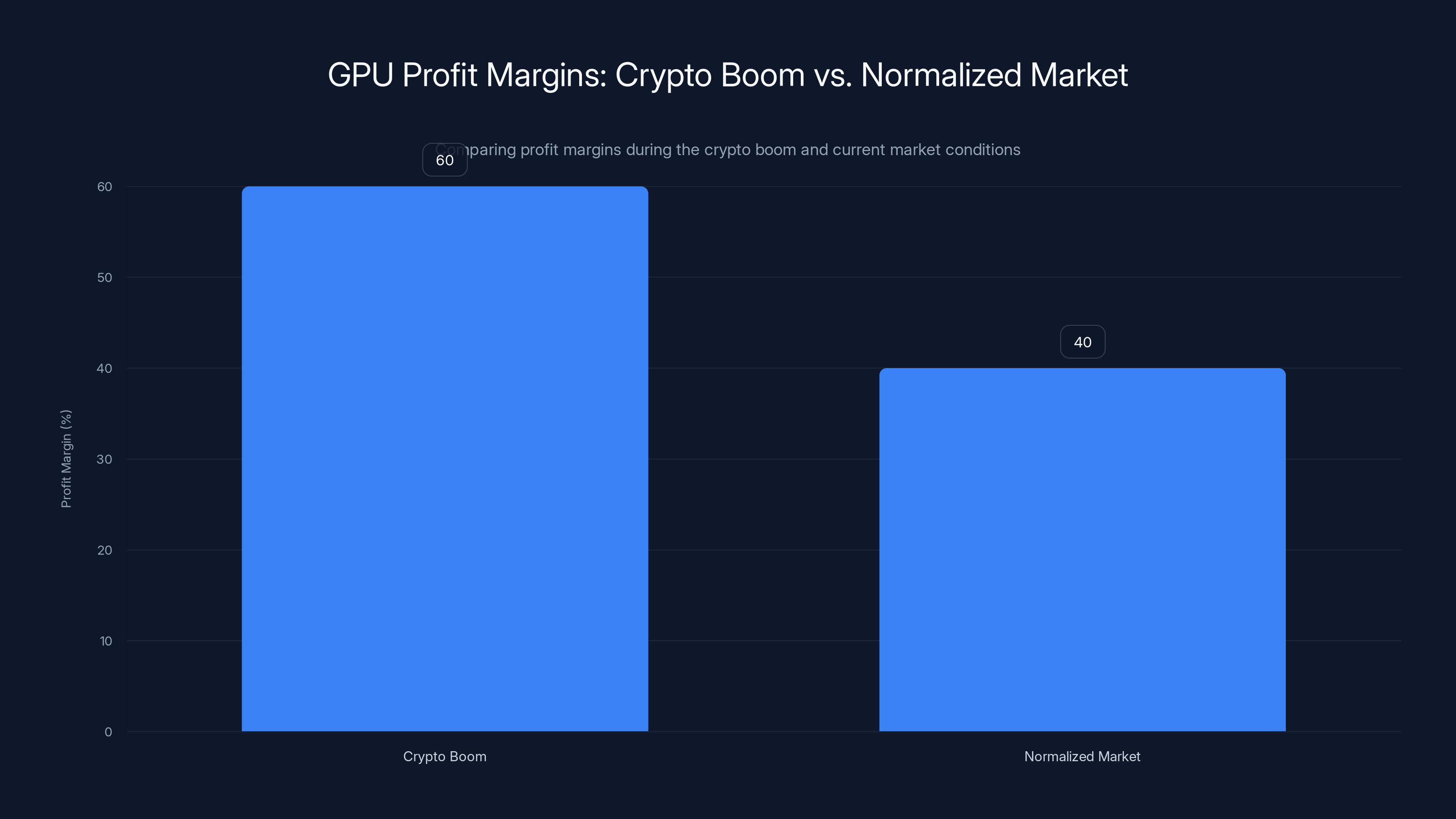

During the crypto boom, GPU profit margins soared to 60%, but have now normalized to around 40%. Estimated data.

Market Segmentation: Steering Customers Toward Higher-Tier Products

The memory configuration shift is also a subtle form of market segmentation. By controlling what memory is available at specific price points, manufacturers influence which customers buy which products.

Consider this scenario: In the previous generation, a

Manufacturers are betting that many customers will stretch. That drives revenue up without requiring a huge increase in the base product price—just a narrowing of the mid-tier options.

This is similar to what Apple does with iPhones—offering different storage tiers at different prices, where the price differences far exceed the actual cost differences in storage. It's effective pricing psychology.

AMD can't be quite as aggressive as Apple (because they lack the brand loyalty), but they can play the same game at a smaller scale. By controlling memory configurations, they control the value perception and steer customers toward higher-priced products when possible.

The challenge is that informed buyers will recognize the pattern. Tech enthusiasts follow hardware forums. They know what different configurations cost. When they see memory amounts dropping without price decreases, they notice. Whether that drives them away or just makes them unhappy depends on available alternatives.

What This Means For Gamers: Your Cost-Per-Performance Is Going Up

If you're a gamer considering a graphics card purchase in 2025, this situation is worth understanding because it affects your buying decision.

Historically, GPU value has improved year-over-year. A

But that trend is being compressed. If AMD raises prices while maintaining the same performance, or raises prices while actually reducing memory, then value isn't improving—it's degrading. Your $500 doesn't buy you as much in 2025 as it would have bought in 2024.

This isn't catastrophic. The GPUs are still reasonably priced and capable. But it's a shift. For a while, GPU buyers got used to improving value every generation. Now you're starting to see the opposite.

What should you do about it? If you need a GPU now, buy now before these price increases take effect. If you can wait, hold off—see what the actual price landscape looks like in Q2-Q3 2025 once these moves play out. If you're planning a build in 6 months, budget higher than you might have expected. Factor in 10-15% price increases across the board as a possibility.

Also, be skeptical of memory as a decision factor. If a $400 GPU ships with 8GB and you'd ideally want 16GB, think about whether that memory difference actually matters for your use case. Many gaming workloads don't hit the 8GB wall. If you're comfortable with frame rate reductions when VRAM is exceeded, 8GB might be acceptable. If you need consistent performance, 16GB or more is worth the premium.

Don't get drawn into the memory wars. Manufacturers want you thinking about VRAM as a primary decision factor because it's easier to add memory (and charge for it) than to improve actual performance. Focus on real-world performance benchmarks in games you play. That's the actually useful metric.

Estimated data shows that yield loss and VRAM are significant cost contributors in GPU manufacturing, driving potential price increases.

The AI And Data Center Effect: Where The Real Money Is

You might be wondering why manufacturers care about margins on consumer GPUs at all. The answer is that consumer GPUs are actually a lower-priority market now.

Data centers are where the money is. Nvidia's data center revenue is roughly triple their gaming revenue. AMD is growing their data center business aggressively. Intel is trying to break into the market. The real competition is for data center AI accelerator contracts, where a single chip costs thousands of dollars and customers buy them by the thousands.

In that context, consumer gaming GPUs are almost a distraction. Manufacturers make them because they're relatively easy to produce (they're basically downbinned or alternative configurations of data center chips), they help maintain manufacturing volume and yield learning, and they provide a pipeline of engaged customers who might eventually buy into data center products.

But they don't represent the highest-value use of manufacturing capacity. If AMD has a choice between allocating advanced nodes to data center GPUs or consumer gaming GPUs, they're allocating to data center every time. Data center customers pay more, commit to longer contracts, and are less price-sensitive.

This actually explains the price increases and memory shifts. Manufacturers can afford to let consumer GPU margins compress or even decline, because they're not the priority. The price increases aren't about maximizing consumer GPU profitability—they're about maintaining minimum acceptable margins on a secondary product category.

Consumers feel the squeeze, but it's not the primary focus for manufacturers. The real innovation, the real engineering resources, and the real margin pressure is all in data center AI accelerators. Consumer GPUs are getting the leftover attention.

That said, data center demand influences consumer pricing. If data center customers are buying more GPUs, that creates supply constraints. Those constraints can push prices higher across the board. Conversely, if data center demand softens, manufacturers might need to move more consumer volume to maintain capacity utilization, which could actually push prices down.

Driver Support And The Software Ecosystem As Pricing Factors

Here's a factor that doesn't get discussed as much as it should: driver quality and software ecosystem influence GPU pricing power.

Nvidia has a substantial advantage here. CUDA is ubiquitous in AI and machine learning. Most ML frameworks are optimized for CUDA first, everything else second. Even when other platforms are technically equivalent, CUDA's maturity and optimization library mean developers choose CUDA GPUs.

Nvidia also has decades of driver optimization. Their drivers are stable, well-tested, and comprehensive. AMD's drivers are actually quite good now, but they're still playing catch-up. For gaming, AMD's drivers have improved dramatically. For machine learning and professional applications, CUDA's ecosystem advantage is still massive.

This ecosystem advantage translates to pricing power. Nvidia can charge more because customers feel like they're getting more—not just raw performance, but software support, optimization, and compatibility. AMD has to compete on price because their ecosystem advantage is smaller.

But this also creates a trap for AMD. If they raise prices while not simultaneously improving driver quality or ecosystem support, they're giving up the one advantage that might justify premium pricing. They need to match Nvidia on software, or they need to undercut on hardware. Doing both is hard.

The rumored price increases might actually make this problem worse for AMD. If customers feel like they're paying more for less (both in terms of memory and software support), they'll just buy Nvidia. The value proposition inverts from "AMD is the better deal" to "Nvidia is worth the premium."

This is AMD's real challenge. They need to improve margins, but not in ways that undercut their fundamental value proposition. That's a tightrope. Memory reductions and price increases are walking that tightrope precariously.

What The Rumor Actually Tells Us About Market Direction

Let's zoom out and think about what the mere existence of these rumors indicates.

Manufacturers don't leak price increase rumors because they want publicity. They leak them because they want to test market reaction. It's a form of price signaling. By leaking rumors, they can gauge customer response before committing to price changes. If there's massive backlash, they can recalibrate. If the market absorbs it calmly, they proceed.

The fact that these specific rumors are circulating—price increases and memory reductions—tells us that manufacturers are testing the market for a particular strategy. They want to see if they can improve margins through a combination of price increases and product repositioning.

The broader implication is that the era of aggressive year-over-year value improvements in consumer GPUs is probably ending. We're moving into a period where prices are more sticky and improvements are smaller. That's not catastrophic, but it's a shift from what we've seen for the past decade.

It's also worth noting that this is cyclical. Markets have periods of value improvement and periods of margin focus. We've been in a value improvement period since about 2017. Moving into a margin focus period is normal. Eventually the cycle will shift again—competition or oversupply will force prices down and value will improve again. But that might be 2-3 years out.

Timeline Expectations: When Will These Changes Actually Happen?

Rumors are rumors, but based on product release cycles, here's what might actually happen:

AMD's next major GPU generation is probably RDNA 5, expected sometime in 2026. That would be the natural time to introduce new memory configurations and new pricing. But AIB partners might jump ahead with their own SKUs before that.

What's more likely in 2025 is subtle adjustments. New SKUs with different memory configurations. Older models at lower prices to clear inventory. New products with aggressive specifications but aggressive pricing as well.

Don't expect a sudden, obvious shift. It'll be more like product lineup evolution—some models disappear, new models appear with different specs. Prices drift up gradually rather than jumping all at once.

For consumers, this means the next 6 months are probably fine—current generation products are still available with current specs at current prices. By mid-2025, you might start seeing the new lineup emerge with different memory configurations and higher prices. The chaos will probably peak around fall 2025 as manufacturers launch new products and clear old inventory.

If you're planning a purchase, timing matters. Early 2025 probably offers the best value before these changes take effect. Late 2025 might offer better performance specs but higher prices. There's no perfect time, but understanding the timeline helps you make informed decisions.

The Competitive Response: Intel And The GPU Market

One factor that could disrupt this entire strategy is Intel's discrete GPU business.

Intel Arc has been a bit of a mess—competitive performance marred by driver issues and limited software ecosystem. But Intel is also doubling down on Arc, and their Battlemage generation (B580) is showing genuine promise.

If Intel Arc becomes competitive and stable, it becomes a wildcard in the price sensitivity equation. AMD and Nvidia can't raise prices too aggressively without risking customers switching to Intel. Intel doesn't have the ecosystem maturity, but they have the pricing power to undercut if necessary.

Right now, Intel is small enough that AMD and Nvidia don't see them as an immediate threat. But if Intel executes well on drivers and software support, that calculation changes fast. Intel could become the value leader that AMD currently is—good performance, competitive pricing, but with the backing of a massive chip conglomerate.

That would actually be a check on AMD's price increases. If AMD gets too aggressive with pricing, Intel Arc becomes the more attractive option. That's probably why AMD is testing market reaction with rumors rather than just implementing changes unilaterally. They're trying to gauge how much pricing power they actually have given Intel's presence in the market.

What Buyers Should Actually Care About

Beyond the pricing and memory discussion, here's what actually matters for GPU purchasing decisions:

Performance in the games or applications you care about. That's it. That's the metric that matters. Does the GPU run your games at your desired settings and frame rates? Does it handle your workload? That's what you're paying for.

Memory is a spec. Bandwidth is a spec. Power consumption is a spec. These matter for determining performance, but they're not the actual thing you care about. You care about frame rates, rendering time, or inference speed.

When evaluating GPUs, benchmark them in applications you actually use. Don't rely on aggregate benchmarks or marketing claims. Find reviews that test the specific games or workloads you care about. Then price-per-performance becomes clear.

Memory becomes relevant only if you're hitting VRAM limits. For most gaming workloads, 8GB is fine. For AI workloads, 16GB or more is necessary. For creative professional work, it depends on project complexity. Don't make memory decisions in a vacuum—make them based on actual workload requirements.

Brand preference is real and has real consequences (driver support, ecosystem, resale value), but don't let brand loyalty make you overpay by too much. There's a maximum premium you should pay for brand, and beyond that, value is value.

Final note: Buy GPUs when you need them, not when rumors suggest you should. Predicting the GPU market is hard. Trying to time your purchase based on rumored future price changes is often a losing game. If you need a GPU now and your budget allows, buy now. If you can wait, wait for more concrete information. But don't delay a purchase you need just to avoid a potential future price increase.

Looking Forward: What 2025 And Beyond Holds For GPU Pricing

Let's make some predictions, understanding that they're predictions and not guarantees.

In the next 12 months, you'll probably see AMD and partners implement modest price increases—maybe 5-10% across the board. You'll see memory configurations shift, with 8GB becoming the volume product. You'll see higher-tier products maintain or increase their memory amounts to justify premium pricing. You'll see new product launches that make this transition less obvious by introducing new architectures with new configurations.

In 2026, you'll see RDNA 5 (or whatever AMD's next generation is called) with new pricing and new memory tiers. That's when the real shift happens. New generation, new baseline for value expectations.

Beyond that, the market depends on competition. If Intel Arc improves significantly, prices stay competitive. If data center demand remains strong, consumer GPU margins might actually improve (less need to push volume). If new architectures offer genuine performance improvements, higher prices are more justified.

The wild card is always cryptocurrency and mining. If mining becomes profitable again, GPU prices will spike. It's happened multiple times. It will happen again eventually. When it does, the current price concerns will seem quaint.

But in the near term, for the next 1-2 years, expect slowly increasing prices, shifting memory configurations, and value erosion for consumers. It's not catastrophic. GPUs will still be capable and reasonably priced. But the days of aggressive year-over-year value improvement are probably ending.

FAQ

Why are AMD and GPU manufacturers considering price increases in a normalized market?

Manufacturers face margin compression as GPU markets normalize after the shortage and crypto boom. Component costs, manufacturing complexity, and yields influence pricing decisions. AMD specifically needs to improve margins without abandoning their value positioning against Nvidia. Price increases allow manufacturers to maintain profitability while investing in new architectures.

How does shifting away from 16GB to 8GB as the volume product help manufacturers?

Reducing memory lowers manufacturing costs since VRAM is an expensive component. By prioritizing 8GB (which satisfies gaming workloads), manufacturers improve margins on volume products while steering customers toward higher-priced products for workloads requiring more memory. This is a psychological pricing strategy that fragments the market and reduces price comparison clarity.

Will 8GB be enough for gaming in 2025 and beyond?

Yes, 8GB is currently sufficient for gaming at 1440p with high settings. At 4K, it becomes tighter but still acceptable. Game developers will eventually require more memory as texture density and complexity increase, but that's a 2-3 year progression. For current and near-term games, 8GB is adequate for most scenarios, though 12GB or 16GB provides more headroom for future games and complex textures.

How does Nvidia's market dominance influence AMD's pricing strategy?

Nvidia's 88% market share gives them pricing power that AMD lacks. Nvidia can raise prices and adjust memory configurations because brand loyalty supports it. AMD must balance margin improvement with maintaining their value positioning as the more affordable alternative. This limits how aggressively AMD can raise prices without losing market share to Nvidia.

What impact does AI and data center focus have on consumer GPU pricing?

Data center AI accelerators are now the primary profit driver for GPU manufacturers, effectively making consumer gaming GPUs a secondary market. This allows manufacturers to be less aggressive with consumer GPU innovation and support, and enables them to focus resources on higher-margin data center products. Consumer GPU buyers feel the squeeze because manufacturers prioritize data center contracts over consumer satisfaction.

When should I buy a GPU if price increases are rumored?

Buy when you actually need the GPU, not based on rumors about future prices. Timing GPU purchases based on speculation is risky. If you need immediate performance, buy now while current-generation products are available at current prices. If you can wait 6 months, you'll see what actual changes manufacturers implement rather than guessing based on rumors.

How does driver quality and software ecosystem support factor into GPU pricing?

Nvidia's CUDA ecosystem and mature drivers provide tangible value that justifies premium pricing. AMD's drivers have improved significantly but still trail in professional and machine learning applications. If AMD raises prices without improving driver quality or ecosystem support, they lose the value justification and customers will choose Nvidia. This creates a pricing ceiling for AMD without corresponding software improvements.

Could Intel Arc's emergence disrupt AMD and Nvidia's pricing strategy?

Yes, if Intel Arc achieves driver stability and wider software support, it becomes a competitive wildcard. Intel could position Arc as a value alternative, essentially replacing AMD's role in the market. This would force AMD and Nvidia to moderate pricing or risk losing customers to Intel. Currently, Arc is too immature to threaten incumbents, but within 2 years that could change significantly.

What's the difference between GDDR6 and GDDR6X memory, and does it affect GPU pricing?

GDDR6X is faster than GDDR6, offering higher bandwidth but also higher costs. High-end GPUs use GDDR6X because the bandwidth improvement justifies the cost. Mid-range products use GDDR6 for cost efficiency. The choice influences manufacturing costs and effective performance, so manufacturers use memory type as another tool for product differentiation and pricing strategy.

How do yields affect GPU pricing and why manufacturers don't discuss them publicly?

Yields (percentage of manufactured chips that work without defects) vary based on process node maturity, design complexity, and manufacturing conditions. Lower yields effectively raise per-unit manufacturing costs because defective chips subsidize working ones. Manufacturers don't discuss yields publicly because they're competitive intelligence, but yield problems can drive hidden price increases as manufacturers compensate for lower usable production volumes.

Conclusion: Navigating The Shifting GPU Market

The GPU market is at an inflection point. The period of cheap, plentiful graphics cards with improving value year-over-year is ending. We're transitioning to a market where manufacturers prioritize margins, where product configuration becomes a strategic pricing tool, and where consumers need to be more thoughtful about their purchases.

The rumors about AMD price increases and 16GB GPU reduction aren't shocking—they're logical extensions of normal market dynamics. Manufacturers have learned from Nvidia's playbook that pricing power comes from brand dominance and ecosystem lock-in, not just from raw performance. If you can't win on price, you optimize for margin. If you can't command premium prices, you use product fragmentation to reduce price comparison clarity.

What should you do about it? First, understand that these changes are coming gradually, not overnight. There won't be a sudden moment where all GPUs get 10% more expensive and 8GB becomes the only option. Instead, you'll see product lineup evolution, with new models having different configurations while old models clear inventory.

Second, don't make purchasing decisions based on rumors. Wait for actual products and actual prices before changing your buying timeline. But do understand the direction the market is moving so you're not surprised when it happens.

Third, focus on value for your actual use case. Don't get caught up in specs that don't matter for your workload. If you're gaming, 8GB is probably fine. If you're doing machine learning, 8GB is definitely not fine. If you're a content creator, it depends on project scope. Benchmark in your actual workloads and make decisions based on real-world performance, not marketing claims or specification lists.

Fourth, remember that the GPU market is cyclical. We're probably moving into a period of margin focus and slower value improvement. But eventually, competition will pick up again, oversupply will return, or new architectures will offer genuine improvements. When any of those things happen, value will improve again and prices will come down. This period of tight margins and careful product positioning won't last forever.

Finally, don't panic. GPUs are still capable, still reasonably priced, and still improving performance. You're not facing a crisis—just a transition from explosive year-over-year value growth to more modest, careful improvements. It's less fun for consumers, but it's normal market behavior.

The GPU market will keep evolving, manufacturers will keep optimizing pricing, and consumers will keep making purchasing decisions. Understand the dynamics, make informed choices based on your actual needs, and buy when the timing aligns with your requirements. That's the best strategy in any market condition.

Key Takeaways

- AMD and GPU manufacturers are testing price increases in a normalized market to recover post-shortage margins that compressed significantly

- 8GB is shifting from niche to volume product because VRAM costs represent 15-25% of manufacturing expense, directly improving margins per unit

- Nvidia's 88% market dominance gives them pricing power AMD cannot match, forcing AMD to carefully balance price increases without abandoning value positioning

- Data center AI accelerators now generate 3x more revenue than consumer gaming GPUs, effectively making consumer products secondary priority for manufacturers

- Memory fragmentation (8GB, 12GB, 16GB at different tiers) intentionally makes price-to-performance comparisons harder, giving manufacturers pricing flexibility

Related Articles

- Apeiron Labs Autonomous Underwater Robots: Ocean Intelligence Revolution [2025]

- Super Bowl 2026 TV Deals: Complete Guide to Savings & Best Options

- Paylocity Review 2025: Features, Pricing & Alternatives

- Russian Spy Satellites Targeting EU Communications: A Space Security Crisis [2025]

- Shark Stratos IZ400 Cordless Vacuum Review: Does This Older Model Still Win? [2025]

- Curling at Winter Olympics 2026: Free Streams & TV Channels [2025]