![Another Raises $2.5M Seed to Transform Excess Retail Inventory Management [2025]](https://tryrunable.com/blog/another-raises-2-5m-seed-to-transform-excess-retail-inventor/image-1-1768934261279.jpg)

The Retail Inventory Crisis: Why Another Exists

Retail is drowning in excess inventory. Every year, retailers accumulate millions of units of unsold products sitting in warehouses, consuming storage space, accumulating carrying costs, and generating zero revenue. The problem isn't new—retailers have dealt with inventory management for decades—but the technological solutions haven't kept pace with modern retail complexity. When inventory doesn't move through traditional retail channels, it ends up in a liquidation spiral: discounts deepen, margins shrink, and ultimately, products get destroyed.

Corina Marshall spent over a decade observing this problem from the inside. Working in retail digital marketing across major brands, she witnessed firsthand how outdated systems created bottlenecks at every stage of the off-channel inventory lifecycle. A product returns from a customer. Days pass before the return is processed and assessed. More days pass before someone decides where it should go—perhaps to a discount retailer like Nordstrom Rack, or to a liquidation marketplace. The timing is critical because retail secondary markets operate on razor-thin windows. A seasonal item that misses its selling window might never recover its value. An item listed on the wrong marketplace at the wrong price point can destroy thousands of dollars in potential margin.

The core insight driving Another's creation addresses a fundamental operational challenge: retail brands need real-time visibility and coordination across their entire off-channel inventory ecosystem. Currently, most retailers manage this process manually or through fragmented systems that don't communicate with each other. Warehouses operate independently. Sales teams guess at pricing. Marketplace coordination happens via spreadsheets and emails. The result is inefficiency, lost revenue, and massive waste.

This inefficiency represents a multi-billion dollar problem. According to industry estimates, retailers collectively hold over

Another emerged from this need with a software solution designed to modernize how retailers approach excess inventory. Rather than replacing existing systems, Another acts as an intelligent orchestration layer that connects to retailers' existing software infrastructure—their returns management systems, warehouse management systems, and marketplace integrations. This architectural approach addresses the primary pain point: fragmentation.

Another's $2.5M Seed Round: Validation and Momentum

The Funding Announcement and Lead Investors

In January 2025, Another announced the completion of its $2.5 million seed funding round, led by two specialized investment firms with deep expertise in fintech and operational innovation: Anthemis FIL and Westbound. This funding validates both the market need and the team's ability to execute on the vision.

Anthemis FIL brings particular credibility to the round. As part of the Anthemis Group, a London-based venture capital firm focused on financial services and supply chain innovation, Anthemis FIL understands supply chain financing and operational efficiency at sophisticated levels. Their involvement signals confidence in Another's ability to address a complex, regulated market. Westbound, as a seed-stage focused investor, brings operational experience in helping early-stage companies scale and navigate the challenging middle stages of growth where many promising startups stumble.

Marshall has previously indicated that investor discovery happened through organic channels—specifically, meeting the Anthemis and Westbound teams at industry conferences. This represents the highest-quality investor relationship, built on genuine market understanding and trust rather than traditional venture capital networking. The fact that these investors found Another compelling enough to lead a seed round, rather than treating it as follow-on participation, suggests exceptional product-market fit signals.

How the Funding Will Be Deployed

Marshall explicitly stated that the $2.5 million seed capital would be allocated toward two primary initiatives: accelerating product development and expanding the team. While this represents relatively focused capital deployment, it reflects smart prioritization for a pre-Series A company.

The product development focus likely addresses several critical capabilities that retail software companies need to scale: enhanced integrations with major retailers' existing systems, more sophisticated pricing optimization algorithms, improved reporting dashboards, and potentially expansion into adjacent features like demand forecasting or inventory lifecycle management. The Anthemis and Westbound investors likely pushed for roadmap items that directly impact revenue retention and expansion—the metrics that matter for Series A fundraising.

Team expansion at this stage typically means three categories of hires: sales specialists who can manage enterprise relationships with major retailers, product/engineering resources to build out the platform, and operations/customer success team members to ensure customer implementations succeed. For a B2B SaaS company targeting retailers, customer success often makes or breaks enterprise adoption. A sophisticated retail software implementation can take 3-6 months; if customers don't see ROI during that window, churn accelerates. Strong implementation and success teams directly drive expansion revenue.

Valuation Implications

While Another has not disclosed its post-money valuation, seed rounds of

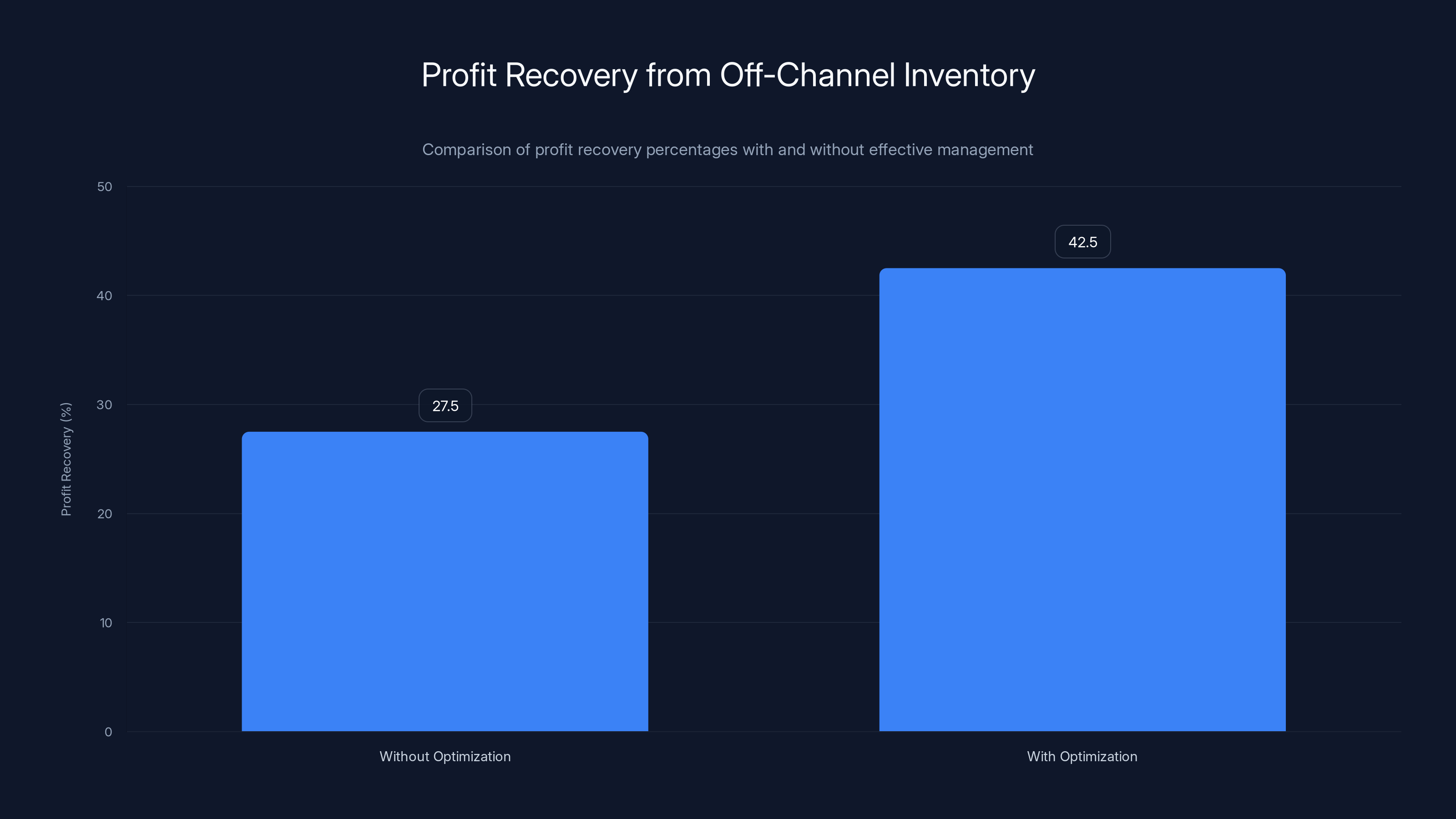

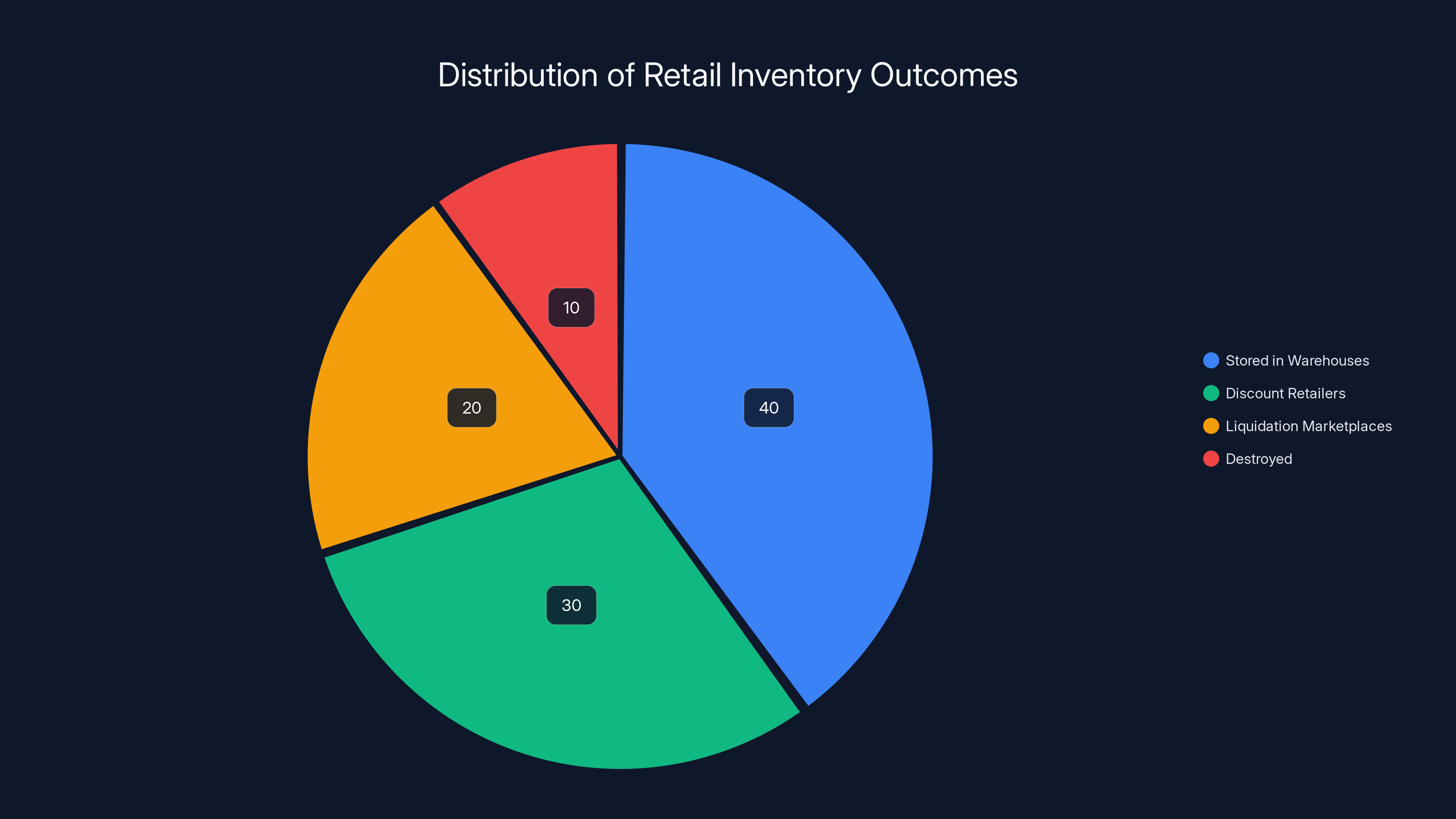

Effective off-channel inventory management can increase profit recovery from an average of 27.5% to 42.5% of the original retail value. Estimated data.

Understanding Off-Channel Inventory: The Problem Another Solves

What Is Off-Channel Inventory and Why It Matters

Off-channel inventory refers to products that don't sell through a retailer's primary sales channels—their own websites, physical stores, and authorized distribution partners. This inventory comes from several sources: overstock from seasonal miscalculations, returned items that can't be resold as new, damaged merchandise that's still saleable at a discount, clearance items, and inventory written off due to discontinued styles or colors.

For the retail industry, off-channel inventory represents both a massive cost and a massive opportunity. The cost side is straightforward: warehousing, insurance, handling, and the capital tied up in merchandise that generates zero revenue. A $100 item sitting in a warehouse costs money every day it sits there—direct storage costs, but also opportunity cost and the risk of further deterioration or obsolescence.

The opportunity exists because secondary markets for this inventory are robust and valuable. Nordstrom Rack, TJ Maxx, Ross, Marshall's, Costco, and various online liquidation platforms collectively purchase tens of billions of dollars in off-channel inventory annually. These retailers pay something for the merchandise—perhaps 20-40% of original retail value depending on condition and type. To a manufacturer or primary retailer who otherwise might have to destroy the product or store it indefinitely, this represents recovered revenue.

The challenge is that success in secondary markets requires speed, precision, and coordination. Nordstrom Rack operates with tight seasonal windows. If winter coats miss the December-January selling window, they're worth 70% less in February. Online liquidation platforms like Liquidation.com feature highly dynamic pricing based on available supply and current demand. An item listed today might be worth

Current Pain Points in Off-Channel Inventory Management

Most retailers manage off-channel inventory using processes that would look familiar to companies 15-20 years ago. A product is returned or identified as excess. It enters a returns processing center where it's assessed for salability. This assessment might involve physical inspection, condition rating, and SKU verification. All of this happens manually or through legacy systems that don't integrate with modern retail infrastructure.

Once assessed, the product faces a decision point: which secondary market should it go to? Who makes this decision? Typically, someone in a back-office role reviews available options and makes a judgment call. The problem is they're making this decision with incomplete information. They might not know what similar items are currently selling for on different platforms. They might not know which marketplace is currently experiencing demand for that category. They might not know whether the item will still be in-demand in 30 days when it might reach that marketplace.

The coordination challenge multiplies when dealing with bulk shipments. A retailer might have 5,000 units of a specific jacket that needs to be distributed across multiple secondary markets. Should all 5,000 go to Nordstrom Rack? Should some go to TJ Maxx? Some to liquidation.com? Should some be held for future seasons? The decision matrix is complex, and most retailers don't have sophisticated tools to model it.

Pricing compounds the challenge. Secondary market pricing is dynamic. An item's value depends on current supply, current demand, seasonality, condition, and timing. A retailer might negotiate with Nordstrom Rack for $25 per unit, but that price only holds if the retailer can deliver the inventory within a specific window. If the retailer takes 45 days to collect inventory from dispersed warehouses, assemble it, and prepare it for shipment, they might miss the pricing window.

Visibility across the entire process is fragmented. A retailer might have one system managing returns processing, another managing warehouse operations, and a third managing marketplace relationships. These systems don't talk to each other. Data about what's been assessed, where it currently is, when it will be ready to ship, and what price it was sold at for different items remains trapped in silos.

Another's Technology Architecture and Core Features

How Another's Platform Works

Another's fundamental approach is architectural innovation rather than attempting to replace entire retail technology stacks. Instead of requiring retailers to rip-and-replace their existing systems, Another positions itself as an intelligent middleware layer that sits between a retailer's existing software and the off-channel inventory process.

The platform connects to retailers' returns management systems (RMS), warehouse management systems (WMS), and direct marketplace integrations. Through these connections, Another aggregates data about what inventory is available, where it's located, when it will be ready for shipment, and what its market value currently is. This aggregation alone represents significant value because it creates centralized visibility where previously there was none.

On top of this data layer, Another builds intelligent workflow automation and decision support. The system can automatically route products to the optimal secondary market based on current pricing, demand signals, and inventory characteristics. It can flag opportunities—"You have 300 winter coats that are in Nordstrom Rack's buying window; if you can deliver them within 10 days, the price is

The platform also provides real-time dashboards that give retailers visibility into the performance of their off-channel inventory by marketplace, by category, by quarter, and by supplier. A retail manager can see that jackets sold through Nordstrom Rack at an average of

Key Platform Capabilities

Centralized Inventory Data Hub: Another aggregates inventory data from multiple sources—returns processing systems, warehouse management systems, buyer adjustment reports—into a single source of truth. Instead of different teams using different spreadsheets with different numbers, everyone operates from the same data.

Real-Time Pricing Optimization: The platform connects to marketplace pricing feeds, competitor data, and demand signals to recommend optimal pricing and marketplace routing for each SKU. Instead of static contracts with Nordstrom Rack at

Automated Workflow Management: The system can automate the routing of inventory between different facilities, marketplace platforms, and logistics providers based on optimized parameters. Inventory that meets specific criteria automatically gets flagged for shipment to the highest-value marketplace, reducing manual touchpoints.

Marketplace Integration and Coordination: Another manages relationships with major secondary retailers and platforms, handling bulk upload of inventory, pricing updates, and sales reporting. This integration layer removes friction from what's typically a manual, error-prone process.

Predictive Analytics: By analyzing historical data about which products sell well in which marketplaces and at what seasons, Another can predict future demand and recommend inventory allocation strategies that maximize value recovery.

Jackets sold through Nordstrom Rack averaged

The Off-Channel Inventory Market: Scale and Opportunity

Market Size and Growth Trajectory

The off-channel inventory management market operates within a much larger ecosystem of retail supply chain and inventory management technology. While specific market sizing for off-channel inventory management software is limited, the underlying market dynamics are substantial.

Retailers collectively hold between

The market is growing for several structural reasons. E-commerce has increased inventory complexity; online retailers overstock more frequently because demand is harder to predict than in physical retail. Product proliferation has accelerated; retailers now carry more SKUs than ever, increasing the likelihood of inventory imbalance. Sustainability concerns are growing; brands increasingly face pressure to minimize waste rather than destruction, driving demand for secondary market solutions. Supply chain volatility has increased inventory carrying; brands build buffer stock against disruption, sometimes resulting in excess.

Competitive Dynamics and Market Participants

The off-channel inventory management space is less crowded than general retail software, but it's not empty. Ghost, mentioned in the original funding announcement as a competitor to Another, is perhaps the most direct competitor. Ghost specifically targets off-channel inventory management for fashion and apparel brands and operates as a marketplace-meets-platform hybrid. Ghost helps brands sell excess inventory through its own platform while also facilitating relationships with secondary retailers.

Other companies operate in adjacent spaces. Inventory management platforms like Trace Link focus on supply chain visibility but weren't specifically designed for off-channel optimization. Liquidation marketplaces like Liquidation.com and B-Stock primarily operate as marketplaces for liquidated goods rather than as operational software platforms for managing the liquidation process. Specialized consulting firms work with retailers on off-channel strategy but aren't technology-enabled.

The fragmented competitive landscape suggests the market is still early. No dominant software standard has emerged. This creates both opportunity and risk for Another: opportunity because there's room to establish market leadership, risk because the market might not be as deep or valuable as it appears.

Another's Competitive Positioning Against Ghost and Alternatives

Another vs. Ghost: Different Approaches to the Same Problem

While Ghost and Another both address off-channel inventory, they approach the problem from fundamentally different angles. Ghost operates primarily as a marketplace platform. Brands list their excess inventory on Ghost's platform, where it can be purchased by retailers, resellers, and other buyers. Ghost takes a commission on transactions and serves as both platform operator and transaction facilitator.

Another, by contrast, operates as operational software for off-channel inventory management. Rather than creating a new marketplace, Another helps retailers optimize their distribution across existing marketplaces—Nordstrom Rack, TJ Maxx, liquidation platforms, and direct buyer relationships. Another isn't trying to become the marketplace itself; it's trying to help retailers make better decisions about which existing marketplace to use for each piece of inventory.

This strategic difference has profound implications for different customer segments. A brand that wants to maintain existing relationships with Nordstrom Rack, TJ Maxx, and traditional liquidators should find Another's approach compelling. It improves their existing processes without requiring them to build new marketplace relationships. A brand that wants to explore direct-to-reseller channels or build its own community of buyers might find Ghost's marketplace approach more compelling.

The positioning also affects unit economics and pricing strategy. Ghost must attract critical mass as a marketplace—both inventory supply and buyer demand—to create liquidity. Another needs to penetrate a relatively small number of large retail organizations; ten major retailers would represent a meaningful customer base. This difference affects go-to-market strategy, customer acquisition cost, and revenue scaling.

Where Retailers Might Consider Alternative Solutions

For teams seeking broader supply chain visibility beyond just off-channel inventory, platforms like AI-powered automation capabilities that extend into inventory documentation, workflow automation, and analytics might be valuable. While Runable's core strength lies in AI-generated reports and workflow automation rather than specialized inventory management, teams already using Runable for other operational processes might find value in its automation layer.

Larger enterprises with sophisticated in-house development capabilities sometimes build custom solutions. A company like Shopify or Woo Commerce integrator might develop bespoke off-channel inventory management features tailored to a specific retailer's needs. This represents high implementation cost but maximum customization.

Generalist supply chain platforms like Blue Yonder (formerly JDA) or Kinaxis offer off-channel inventory management as one feature within broader supply chain planning solutions. These platforms make sense for massive enterprises already running their entire supply chain on these systems but represent overkill for mid-market retailers.

The Business Model: How Another Generates Revenue

SaaS Subscription Model

Another almost certainly operates on a SaaS subscription model, charging retailers monthly or annual fees based on some consumption metric. The exact pricing structure hasn't been publicly disclosed, but typical off-channel inventory software companies charge either:

Per-Unit Fees: A fixed fee per SKU or per unit of inventory managed through the platform. This aligns costs directly with retailer scale—a retailer managing 100,000 excess units annually would pay proportionally more than one managing 10,000 units. Per-unit pricing typically ranges from

Tiered Subscription Model: Fixed monthly fees based on feature tier or inventory volume band. Small retailers might pay

Transaction-Based Fees: A commission on transaction value or a percentage of marketplace sales volume facilitated through the platform. This creates strong alignment with customer success but introduces volatility into revenue.

Another likely combines elements of these approaches. A base monthly subscription for access to the platform, plus per-unit fees scaled to inventory volume, might make sense. Alternatively, a tiered model where pricing increases with complexity of integrations and customization would align with enterprise software norms.

Revenue Expansion and Unit Economics

For a B2B SaaS company focused on enterprise retail customers, expansion revenue matters as much as new customer revenue. A retailer that starts by using Another to manage 20% of its off-channel inventory might expand to managing 50% or 80% as the platform demonstrates value. A retailer that initially uses Another only for returns inventory might expand to include markdown inventory or seasonal overstock.

Unit economics for this business model are potentially very attractive. The marginal cost of serving an additional customer is relatively low—primarily developer time for integrations and customer success costs. If Another can land customers at $15,000 annual revenue per customer and keep churn below 10% annually while growing existing customers at 30-40% annually through expansion, the company builds sustainable, high-margin growth.

The challenge lies in customer acquisition. Enterprise software sales to retailers involve long sales cycles (3-6 months typical), high deal complexity (integrations, pilot programs, contract negotiations), and meaningful upfront implementation costs. Another likely needs to invest significantly in sales and implementation resources to drive customer acquisition, meaning unit economics might be challenged in the near term.

Estimated data shows that small retailers pay between

Implementation and Integration Complexity

The Implementation Challenge

Another's value proposition depends entirely on its ability to integrate with retailers' existing systems. A retailer with a modern, well-documented returns management system and warehouse management system can likely integrate with Another in 4-8 weeks. A retailer with legacy systems, custom integrations, and inconsistent data practices might require 3-6 months of integration work.

This integration complexity represents both a moat and a risk. The moat: once Another is integrated into a retailer's processes, switching costs become substantial. The company has created operational dependencies. The risk: implementation challenges or integration failures create customer friction, hurt the product's reputation, and can drive churn.

Another likely addresses this through dedicated implementation services. A customer success team works with each customer to map their systems, design data flows, handle custom integrations, and manage the cutover process. This requires significant operational overhead but is standard for enterprise software companies in retail.

Data Quality and Governance

A critical challenge that Another must address is data quality and governance. Off-channel inventory processes often involve messy, inconsistent data. A returns management system might classify a product as "customer return" while another system classifies the same process as "damage/markdown." One warehouse might track condition as "like-new" while another uses "first quality." Pricing data across systems might use different currencies, tax treatments, or formats.

Another needs to build sophisticated data cleaning and normalization capabilities to handle this. The platform must provide configuration interfaces that let retailers map their data to standardized schemas without requiring developer expertise. The platform must flag data quality issues—"This SKU has conflicting condition ratings; which is correct?"—and help remediate them.

Data governance also includes access controls. Different users within a retailer should have different visibility and action capabilities. A warehouse manager might see inventory locations and readiness status but not pricing or profit margins. A pricing manager might see pricing and marketplace data but not warehouse locations.

Use Cases and Customer Segments

Apparel and Fashion Retailers

Apparel and fashion represents the primary use case for off-channel inventory software because the value of fashion inventory deteriorates rapidly over time. A summer dress has value in June; it has dramatically less value in August. A winter coat has value in November; it's essentially worthless by May. This time-value dynamic creates urgency around off-channel inventory management and makes the ROI case for Another compelling.

For a fashion retailer like Gap or Banana Republic, Another could enable meaningful improvements. Rather than warehouse teams waiting for buying/merchandising teams to tell them where to route excess inventory, the system could automatically optimize routing based on current market conditions. A retailer currently recovering 35% of original retail value on excess inventory might improve to 45% through better timing and marketplace matching.

The typical fashion retailer customer for Another would likely be mid-sized ($100-500M in annual revenue range) with complex omnichannel operations, multiple brands or divisions, and meaningful excess inventory volume (millions of units annually). Smaller fashion retailers might not have sufficient inventory volume to justify the cost; larger retailers might have already built custom solutions.

Multi-Channel Retailers

Retailers managing inventory across multiple brands, stores, websites, and distribution channels generate complexity that creates opportunities for Another. When a Walmart or Target has to coordinate off-channel inventory across thousands of categories, hundreds of distribution centers, and multiple marketplace relationships, the coordination challenge becomes severe enough that a dedicated solution makes economic sense.

A multi-channel retailer might use Another primarily to prevent forced liquidation. Rather than routing excess inventory to bulk liquidators at 15% of original value, the retailer can use Another to optimally distribute it across discount retailers at 30-40% of original value. This 15-25 percentage point improvement in recovery rate, applied across billions of units of inventory, generates hundreds of millions in value.

Direct-to-Consumer Brands

D2C brands that have scaled to meaningful size often face off-channel inventory challenges. As direct-to-consumer brands mature, they accumulate inventory through overstock, returned items, and seasonal imbalance. Some D2C brands operate their own warehouse and logistics; managing off-channel sales for these brands involves similar coordination challenges.

However, D2C brands might find Another's value lower than wholesale retailers because D2C brands often have more flexibility in managing inventory. They can run their own sales, offer deeper discounts to their customers, and adjust product mix in real-time based on demand. The urgency and complexity of off-channel management is lower.

The Sustainability Angle: Business and Environmental Impact

The Waste Problem in Retail

One of the most compelling aspects of Another's positioning is the sustainability dimension. Excess inventory that can't be sold ends up destroyed—burned for energy, sent to landfills, or sometimes buried. Industry estimates suggest that tens of billions of articles of clothing are destroyed annually, representing not just environmental waste but also significant resource waste (water, energy, chemicals used in production).

From a business perspective, this represents pure loss. A manufacturer and retailer invested resources to produce an item; if it ends up destroyed, that represents complete value destruction. From an environmental perspective, it represents waste.

Another positions its solution as addressing both the business problem and the environmental problem. By helping retailers sell excess inventory rather than destroying it, Another theoretically reduces waste while improving profitability. This dual-benefit positioning resonates with sustainability-conscious investors (like Anthemis, which emphasizes sustainable investing) and with modern consumers and brands increasingly focused on environmental impact.

Regulatory and Stakeholder Pressure

Regulatory pressure around textile waste is increasing in some markets. The European Union has proposed regulations that might eventually require brands to be responsible for end-of-life disposition of their products, creating potential liability for destroyed inventory. Some jurisdictions are exploring textile waste taxes or disposal restrictions. These emerging regulations create additional incentive for brands to prioritize secondary markets over destruction.

Brand reputation considerations also matter. Major retailers and brands increasingly face public pressure to minimize waste. Patagonia, for example, has made sustainability a core brand positioning. Consumers increasingly prefer brands with strong environmental commitments. Anything that helps brands reduce waste while maintaining profitability improves brand reputation.

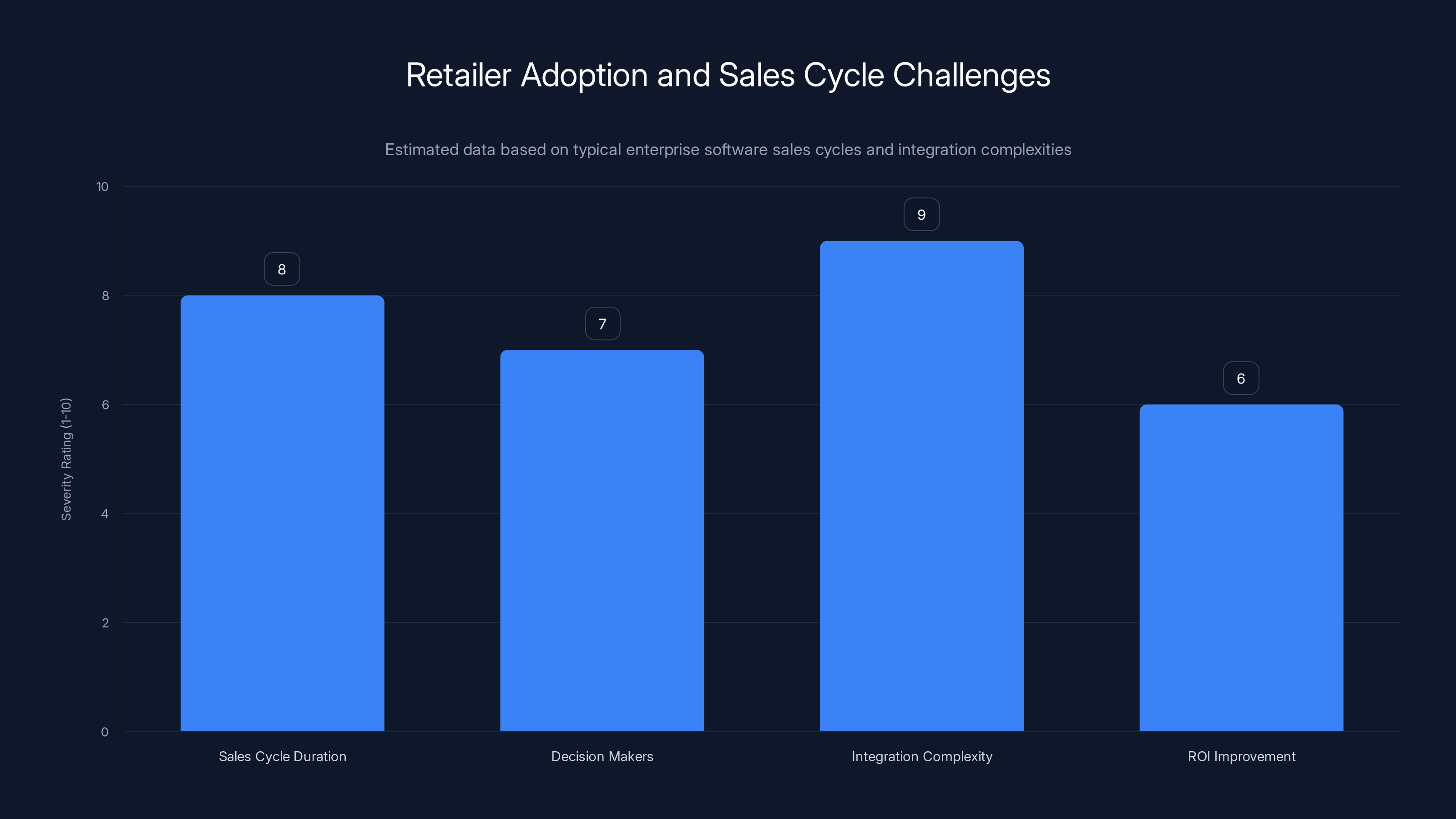

Integration complexity and lengthy sales cycles are the most severe challenges for Another, with high ratings of 9 and 8 respectively. Estimated data.

Market Challenges and Risks

Retailer Adoption and Sales Cycles

The primary risk facing Another is achieving customer adoption at a pace that supports sustainable growth. Selling enterprise software to large retailers is notoriously difficult. Sales cycles run 6-12 months. Procurement processes are rigid. Budget cycles are annual. The number of decision-makers is large (merchandising, operations, finance, IT all have opinions).

Another must overcome skepticism that a startup can handle integrations with enterprise systems that have often been modified and customized by multiple generations of operators. A 50-year-old retailer with legacy systems built in the 1990s might reasonably worry about data quality, security, and operational risk.

Sucking in customers also depends on their perceiving clear ROI. Another's value proposition depends on demonstrating that using the platform generates more value from off-channel inventory than manual processes. If a retailer currently recovers 35% of original retail value on excess inventory and Another can demonstrate the improvement to 42%, the value is clear. But if a retailer has already optimized this process through other means, Another's value might be unclear.

Integration Complexity and Technical Risk

Another's business model depends on being able to integrate with diverse retailer systems at reasonable cost and time. But retail technology environments are notoriously complex and idiosyncratic. A retailer might use Oracle for financial systems, SAP for supply chain, Salesforce for CRM, and a custom-built system for returns management, all poorly integrated with each other.

If integration takes significantly longer than anticipated, or if certain retailers' systems are incompatible with Another's approach, this creates customer acquisition headwinds and integration cost overruns. A single difficult customer with expensive, time-consuming integration can dramatically impact unit economics.

Competitive Response

Larger retail technology vendors could theoretically enter this market. A company like SAP or Oracle could add off-channel inventory optimization as a module to their existing suite. Marketplace platforms like Shopify could build off-channel inventory management features into their platform. If a larger vendor enters the market aggressively, Another could face competitive pressure on pricing and customer acquisition.

Ghost, Another's named competitor, could also accelerate its development efforts and expand its platform capabilities, potentially creating a more direct competitive threat.

Marketplace Relationship Risk

Another's value depends partly on maintaining strong relationships with secondary marketplaces like Nordstrom Rack, TJ Maxx, and liquidation platforms. If these marketplaces build their own inventory management solutions or restrict access to marketplace APIs, this could undermine Another's ability to deliver value.

Future Roadmap and Potential Expansion

Adjacent Markets and Expansion Opportunities

Once Another establishes market leadership in off-channel inventory management for retailers, several adjacent markets represent expansion opportunities. The core competency—intelligently routing inventory to secondary channels based on real-time data—applies to other contexts.

Third-Party Logistics and Fulfillment: 3PL companies that manage inventory for multiple retail brands could use a similar platform to optimize how they route their clients' excess inventory. Instead of each brand having to implement Another separately, a 3PL using Another could serve multiple brands and optimize across their collective inventory.

Outlet Operations: Large retailers that operate their own outlet stores could use a similar platform to optimize inventory distribution between main retail stores and outlet stores based on demand signals and pricing dynamics.

Reverse Logistics and Returns Management: Another could expand from off-channel inventory management into broader returns and reverse logistics, offering retailers a complete solution for managing product lifecycle once it leaves the customer.

International Operations: Currently Another likely focuses on domestic off-channel operations. Expanding to help retailers manage international secondary markets—cross-border resale, local discount retailers in different countries—represents significant expansion opportunity.

Technology Roadmap Considerations

Based on the market and Another's positioning, the likely technology roadmap priorities probably include:

Enhanced Predictive Analytics: Moving from reactive ("here's your current inventory and here's where you should send it") to predictive ("based on historical demand patterns, seasonal trends, and external signals, here's where this inventory will be most valuable").

Marketplace Expansion: Adding integrations with additional marketplaces and secondary distribution channels, increasing the universe of options Another can route inventory toward.

Sustainability Reporting: Building comprehensive reporting that shows retailers the environmental impact of their inventory decisions—units saved from destruction, waste prevented—supporting their sustainability commitments and storytelling.

AI-Driven Insights: Integrating more sophisticated AI and machine learning to identify patterns, anomalies, and opportunities in off-channel inventory data that humans might miss.

How Another Compares to Alternative Approaches

Build vs. Buy vs. Partner Decision

Retailers facing off-channel inventory management challenges face a classic "build vs. buy vs. partner" decision. Building in-house means developing custom software and hiring specialized talent. This maximizes customization but minimizes speed and creates ongoing maintenance burden. Buying from a vendor like Another means accepting some standardization but gaining faster implementation and vendor support. Partnering with consulting firms to improve processes means potentially improving without technology.

Another's value proposition sits on the buy side of this spectrum—it's faster than building, cheaper than extensive consulting, and more integrated than generic supply chain platforms. This positioning works well for mid-market retailers but might be less compelling for massive enterprises that have already built custom solutions or very small retailers where the problem isn't severe enough to justify investment.

Another vs. Cross-Functional Optimization

Some retailers attempt to solve off-channel inventory optimization through process improvement and organizational change rather than technology. Better cross-functional collaboration between warehouse operations, merchandising, and marketplace management sometimes generates meaningful improvements.

However, process improvement has inherent limits. Human decision-makers cannot access, process, and act on real-time market data with the speed and accuracy of automated systems. A software system can continuously monitor marketplace demand, pricing trends, and inventory characteristics to make optimal routing decisions. Human managers making weekly decisions simply cannot match this responsiveness.

Another's technology approach complements organizational improvements. Process optimization gets some of the way; technology gets retailers the rest of the way.

Estimated data shows that a significant portion of unsold retail inventory remains stored in warehouses, while a smaller percentage is destroyed, highlighting inefficiencies in inventory management.

Strategic Implications for the Retail Industry

The Professionalization of Off-Channel Operations

The emergence of specialized software companies like Another signals the broader professionalization of off-channel inventory management. For decades, off-channel inventory operations were treated as a necessary evil—something retailers had to do but didn't invest heavily in optimizing. Leading companies are shifting to viewing this as a strategic, optimizable business function.

This shift has several implications. First, it means retailers will increasingly expect predictable, improving returns from off-channel inventory. Rather than accepting 30-35% recovery rates, retailers will increasingly demand 40-45% or better. Second, it means off-channel operations will attract better talent as the business becomes more sophisticated and strategic. Third, it means the technology layer supporting off-channel operations will become more valuable and more competitive.

Data-Driven Decision Making in Retail Operations

Another represents a microcosm of broader trends in retail operations—the shift from intuition and experience to data-driven decision making. Rather than having experienced buyers make judgment calls based on gut feel about inventory allocation, retailers are increasingly implementing systems that guide decisions with data.

This trend will likely accelerate. Retailers face intense cost pressures from e-commerce and will invest in efficiency opportunities anywhere they can find them. Off-channel inventory management might seem like a small opportunity, but it's one of many operational areas where data-driven optimization can drive meaningful margin improvement.

Sustainability as Business Imperative

Another's emphasis on waste reduction signals something important about where the retail industry is heading. Brands increasingly view sustainability not as nice-to-have corporate responsibility but as integral to business strategy. Investors increasingly penalize brands that produce massive waste. Consumers increasingly prefer brands with sustainability commitments.

This means the market for solutions that help brands be more sustainable while maintaining profitability will only grow. Another benefits from this tailwind, but it also benefits companies solving inventory waste in other contexts (resale platforms, rental services, donation management systems).

Lessons from Another's Funding and Positioning

Why This Company and This Problem Matter

Another's successful fundraising at the seed stage demonstrates several things about the current venture capital landscape. First, specialized solutions addressing specific operational challenges in large industries remain compelling investment opportunities. The VC market increasingly looks for companies solving specific problems deeply rather than companies attempting broad market transformation.

Second, experienced operators with deep domain expertise continue to be valuable. Corina Marshall spent over a decade in retail digital marketing, understood the off-channel inventory problem intimately, and built a company directly addressing that problem. This domain expertise probably mattered significantly in impressing investors.

Third, the intersection of business optimization and sustainability creates compelling value propositions. Investors are increasingly looking for solutions that improve financial metrics while improving environmental metrics. Companies that can credibly claim both benefit from strong tailwinds.

The Importance of Market Selection

Another's success to date likely reflects smart market selection. Off-channel inventory management is a specific enough problem that competitors haven't saturated the market, but common enough that meaningful opportunity exists. The problem is acute enough that companies will pay for solutions, but not so acute that they've already solved it comprehensively. This represents an ideal market for an early-stage company.

For entrepreneurs considering starting companies, Another represents a template worth studying. The company didn't try to revolutionize retail; it identified a specific, high-value problem that existing solutions don't address well, and built a focused solution for that problem.

Practical Considerations for Retailers Evaluating Solutions

Assessing Fit for Your Organization

Retailers considering off-channel inventory management solutions like Another should ask several diagnostic questions. First: How much excess inventory does your organization manage annually? If the answer is fewer than 500,000 units, the ROI might not justify software investment. If it's 5+ million units, the case is much stronger.

Second: How manual is your current process? If off-channel inventory management happens through spreadsheets and emails, there's significant opportunity for improvement. If you already have enterprise software managing the process, the opportunity might be more limited.

Third: What's your current recovery rate? If you're recovering 25-30% of original retail value, you're probably leaving money on the table. If you're already recovering 45%+, you're probably closer to optimal.

Fourth: How many secondary marketplaces do you currently sell through? If you work with only one or two, there might be optimization opportunity through diversification. If you already work with many, another tool for optimization might be valuable.

Implementation Readiness

Before implementing any off-channel inventory platform, retailers should ensure they're ready from an organizational perspective. This means having executive sponsorship (off-channel operations should not be implemented at a project team level without leader commitment), having clear KPIs (what success looks like should be defined upfront), having data readiness (your underlying systems should be in reasonable shape), and having change management (staff need to be trained and bought into the new process).

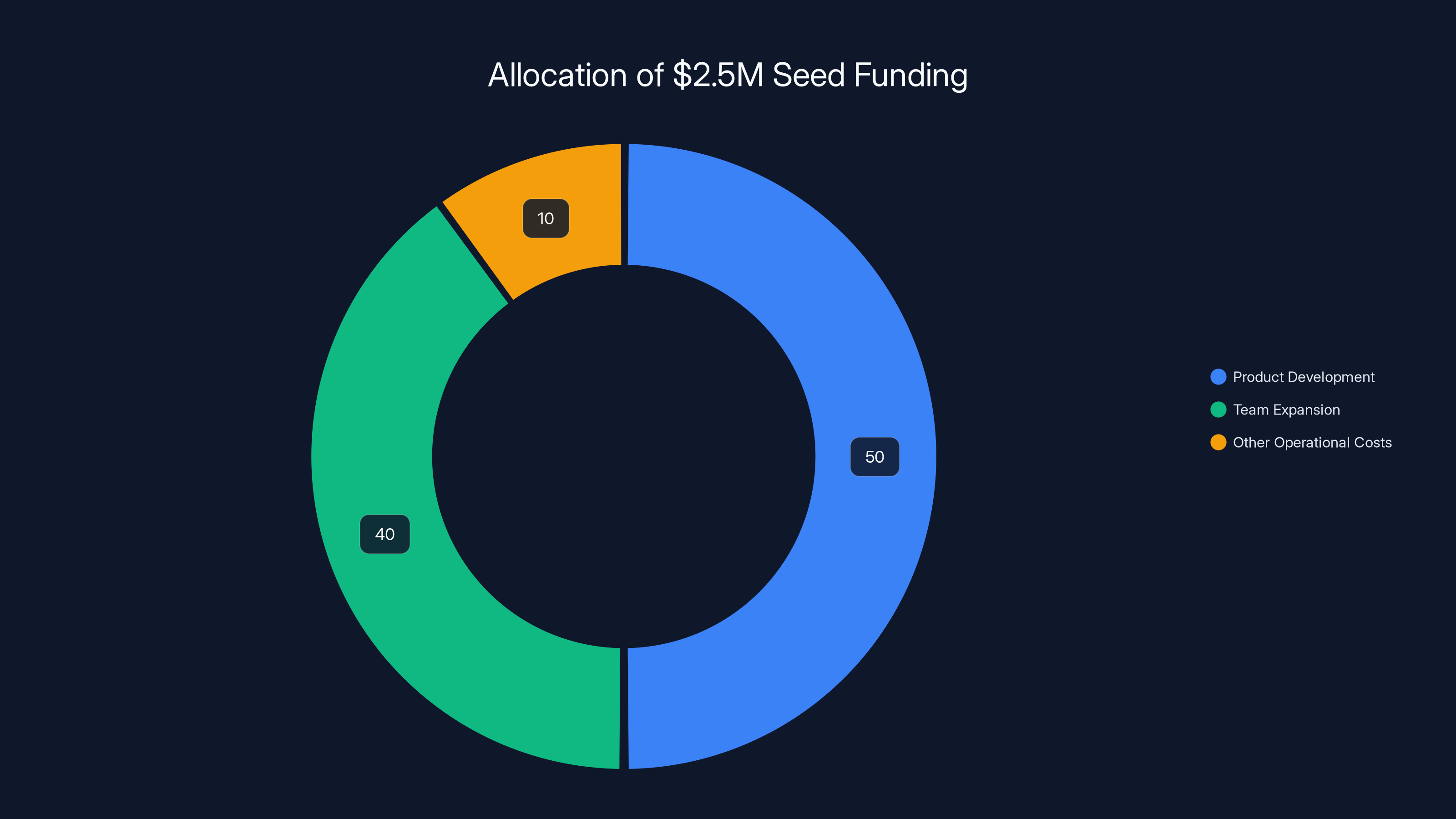

Estimated data: The $2.5M seed funding is primarily allocated to product development (50%) and team expansion (40%), with a small portion (10%) reserved for other operational costs.

The Competitive Landscape Today

Direct Competitors

Ghost remains the most direct competitor, though as discussed their approach differs from Another's. Ghost has the advantage of being an established marketplace with existing buyer demand and seller relationships. Ghost has the disadvantage of operating as a marketplace rather than as operational software integrated into a retailer's existing processes.

Other potential competitors include liquidation software platforms, though most of these operate as marketplaces rather than as optimization platforms for existing secondary market relationships.

Indirect Competitors and Threat Categories

Retailers' existing systems vendors represent indirect competition. If Oracle or SAP adds sophisticated off-channel inventory optimization as a feature to their suite, it could create competitive pressure. These large vendors have the advantage of existing customer relationships and massive sales infrastructure; they have the disadvantage of being slow to move and often prioritizing breadth over depth.

Internal development represents another form of competition. Large retailers like Walmart or Target could theoretically develop their own off-channel optimization systems. However, the cost and time to build is significant, and most retailers prefer to leverage specialized vendors for non-core functionality.

Third-party logistics and fulfillment providers could enter this space. If major 3PLs develop their own off-channel optimization platforms for their clients, this could fragment the market.

Emerging Trends Impacting Off-Channel Inventory

E-Commerce Growth and Complexity

The continued growth of e-commerce amplifies inventory management challenges and creates more off-channel inventory. E-commerce features higher return rates than physical retail (30%+ vs 10-15%). E-commerce creates demand forecasting challenges as brands experiment with new channels and product lines. E-commerce reduces inventory visibility as goods move through multiple fulfillment networks. All of these factors mean more excess inventory needs to be managed.

Omnichannel Retail Complexity

Retailers increasingly operate across multiple channels—owned stores, third-party marketplaces, social commerce, wholesale distribution. This complexity creates more inventory coordination challenges. A brand selling on Amazon, Shopify, and in physical stores needs to intelligently allocate inventory across these channels and manage what to do with inventory that doesn't sell in any of them. This creates more need for sophisticated off-channel inventory management.

Demand for Circular Economy Solutions

The circular economy—keeping products in use rather than destroying them—is transitioning from a nice-to-have principle to an increasingly mandatory requirement for major brands. European regulations, investor pressure, and consumer expectations all push toward companies minimizing waste. Off-channel inventory management that keeps products in secondary markets rather than sending them to landfills or destruction represents a form of circular economy solution.

Investment Perspective: Why Investors Like This

The Venture Capital Case for Another

From a venture capital perspective, Another represents an attractive investment thesis for several reasons. First, the company addresses a pain point in a large, established industry (retail). Second, the market hasn't yet been dominated by a single vendor, so there's room for market leadership. Third, the founding team has domain expertise and credibility. Fourth, the business model (B2B SaaS with enterprise customers) aligns well with venture capital's preferred model (high margins, recurring revenue, scalable sales). Fifth, the company sits at the intersection of two powerful trends (operational efficiency and sustainability).

The Anthemis and Westbound investors likely evaluated Another against these criteria and found it compelling. Both investors have track records in supply chain and fintech, suggesting they understand the business deeply.

What Investors Will Watch Going Forward

As Another raises future funding rounds, investors will scrutinize specific metrics. Customer acquisition cost (what does it cost to land each customer) will matter significantly. Churn rate (what percentage of customers cancel annually) will be critical—high churn signals that customers don't perceive the value. Expansion revenue (how much do existing customers increase their spending annually) will indicate whether Another is creating ongoing value or just one-time implementation value.

Investors will also watch competitive developments. If Ghost raises massive funding and becomes dominant, that changes Another's opportunity. If a large vendor enters the market aggressively, that's a risk signal.

The Broader Startup Ecosystem Implications

Opportunity for Specialized B2B SaaS

Another's successful funding demonstrates continued opportunity for specialized B2B SaaS companies serving specific functions within large industries. The "enterprise software" market is not dead; rather, it's evolving. Startups that can identify specific operational pain points and build focused solutions have good odds of success.

This contrasts with the early 2000s venture capital model, which often favored broad platforms attempting to replace entire categories of software. Modern venture capital increasingly recognizes that specialized, best-of-breed solutions often outperform general platforms because they can go deeper, move faster, and create more user value.

The Retail-Tech Opportunity

Retail technology remains an attractive venture capital domain despite the perception that e-commerce has disrupted traditional retail. The reality is that most retail still happens in physical stores; e-commerce is growing but hasn't displaced brick-and-mortar. Retail represents 4-5% of US GDP. Even small operational improvements generate significant value.

Retail software companies tend to have strong unit economics (retailers are willing to pay for solutions that save money or increase revenue) and reasonable sales cycles (though longer than SaaS for startups). Another represents a proof point that retail-focused startups can raise capital and build meaningful companies.

Conclusion: What Another Means for Retail and Beyond

The Opportunity to Transform Off-Channel Operations

Another's emergence and successful funding round validates something that has been true for years but is only now becoming operationalized: off-channel inventory management represents a huge, underserved operational opportunity for retailers. Billions of dollars in inventory value flows through secondary markets annually, yet the technology supporting these operations has lagged compared to primary channel retail technology. Another is working to close this gap.

The impact of successful off-channel inventory optimization extends beyond any single company. When retailers can recover 40-45% of original retail value from excess inventory instead of 25-30%, this represents meaningful margin improvement at scale. For a retailer with

The Sustainability Imperative

What makes Another particularly compelling is its positioning at the intersection of business optimization and environmental impact. The company isn't asking retailers to choose between profitability and sustainability; it's showing them how to improve both simultaneously. This alignment of business incentives with environmental outcomes is increasingly powerful and will likely be even more powerful in the future as environmental concerns intensify.

As regulations around textile waste tighten, as consumer expectations around sustainability sharpen, and as investor scrutiny of waste and destruction increases, solutions that help brands be more sustainable while maintaining profitability will become increasingly important. Another benefits from these trends.

The Broader Startup Lesson

For entrepreneurs and investors, Another provides a useful template. The company identified a specific, valuable problem that affects a large industry. The founding team had domain expertise and credibility. The company built focused, specialized software addressing that problem rather than attempting to solve everything. The company's positioning at the intersection of business value and social value (sustainability) creates strong tailwinds. These factors combined to create a compelling investment thesis.

Another is early in its journey. The company must still achieve meaningful customer adoption, demonstrate strong unit economics, and maintain competitive positioning. But the strong seed round funding from Anthemis FIL and Westbound suggests that experienced investors believe Another is well-positioned to succeed.

Evaluating Solutions for Your Organization

For retailers and retail-adjacent organizations reading this analysis, the key takeaway is not that Another is necessarily the right solution for your organization (that depends on your specific circumstances), but rather that recognizing off-channel inventory management as an important, optimizable business function is valuable. Whether you build in-house, partner with Another, Ghost, a consulting firm, or another vendor, focusing strategic attention on this area can generate meaningful value.

The technology is advancing; solutions are improving. The time when off-channel inventory management was a back-office function managed by spreadsheets and email is ending. The next era will feature sophisticated technology, data-driven decision making, and optimization of every step of the process.

Another is positioned to be part of this transformation. Whether it becomes the dominant platform in this space remains to be seen, but the company is clearly on an interesting trajectory with strong backing and a clear value proposition. As the company executes on its roadmap and grows its customer base, it will likely create meaningful value for retailers, investors, and the broader ecosystem.

FAQ

What is off-channel inventory management and why do retailers need it?

Off-channel inventory refers to products that don't sell through a retailer's primary sales channels, including overstock items, returns, clearance merchandise, and damaged goods. Retailers need specialized management for this inventory because secondary markets operate with tight timelines and dynamic pricing. Without optimization, products get sold at deep discounts, destroyed, or liquidated for pennies on the dollar. Effective management helps brands recover 40-45% of original retail value instead of just 25-30%, representing significant profit recovery annually.

How does Another's platform actually connect to existing retail systems?

Another functions as middleware that integrates with retailers' existing systems like returns management systems (RMS) and warehouse management systems (WMS). Rather than replacing these systems, Another aggregates data from multiple sources into a centralized hub, creating unified visibility across inventory location, condition, pricing, and marketplace opportunities. The platform then automates routing decisions based on real-time market conditions and historical performance data, connecting inventory to the optimal secondary marketplace for each item.

What are the main benefits of using AI-powered inventory management like Another?

AI-powered inventory management delivers three primary benefits: Real-time optimization through continuous analysis of market conditions and dynamic pricing; Reduced manual work by automating routing, pricing, and coordination decisions that previously required human judgment; and Improved financial outcomes by directing inventory to the highest-value marketplace rather than defaulting to liquidation or destruction. For teams seeking AI-powered automation capabilities across their operations, platforms like Runable offer comparable workflow automation features that extend beyond inventory into documentation and reporting.

Who are the main competitors to Another in off-channel inventory management?

Ghost represents the most direct competitor, operating as a marketplace for off-channel inventory rather than as optimization software for existing marketplaces. Ghost facilitates direct buyer-seller relationships but lacks integration with retailers' existing systems and processes. Other indirect competitors include general supply chain platforms (like Blue Yonder) that offer off-channel management as one feature among many, and custom solutions built in-house by large retailers. Alternative automation platforms like Runable address broader workflow optimization but not specialized inventory management.

How much does off-channel inventory management software typically cost?

Pricing varies significantly based on the vendor and the retailer's scale. Typical SaaS models charge either per-unit fees (

How long does it take to implement off-channel inventory management software?

Implementation timelines typically range from 4-12 weeks depending on system complexity. Retailers with modern, well-integrated systems and consistent data practices can often go live in 4-8 weeks. Retailers with legacy systems, custom integrations, and inconsistent data approaches might require 3-6 months of integration, data cleanup, and testing before full deployment. Implementation usually involves dedicated customer success resources from the vendor working with IT, operations, and merchandising teams at the retailer.

What sustainability benefits does off-channel inventory optimization provide?

Off-channel inventory optimization reduces waste by helping retailers sell excess products through secondary markets rather than destroying them. Industry estimates suggest tens of billions of clothing items are destroyed annually when they fail to sell. By recovering inventory through secondary markets, retailers extend product lifecycles, reduce landfill waste, and minimize the environmental impact of overproduction. This aligns with circular economy principles and helps brands meet increasingly stringent sustainability commitments, while also recovering revenue that would otherwise be lost.

What metrics should retailers track to measure off-channel inventory performance?

Key performance metrics include: Recovery rate (percentage of original retail value recovered through secondary sales), Sell-through rate (percentage of inventory that actually sells vs. remaining in market), Time-to-market (how quickly inventory moves from assessment to secondary marketplace), Cost per unit (total operational costs divided by units managed), and Markdown rate (average discount from target pricing). Retailers should also track waste prevented (units saved from destruction) and environmental impact (carbon equivalent prevented through extending product life).

How does Another position itself against larger enterprise software vendors?

Another differentiates through focus and specialization rather than breadth. Larger vendors like SAP or Oracle offer off-channel inventory as one minor feature among thousands. Another goes deeper, specifically optimizing for off-channel operations with specialized pricing algorithms, marketplace integrations, and workflow automation. Another can move faster and innovate more quickly because it's not constrained by managing backwards compatibility across massive, complex systems. Another's trade-off is lower feature breadth but higher feature depth.

What types of retailers see the highest ROI from off-channel inventory software?

Mid-sized to large fashion/apparel retailers typically see the highest ROI because their inventory depreciates rapidly over time, creating urgency and high value in optimization. Multi-channel retailers managing inventory across numerous distribution centers, store locations, and marketplaces also see strong ROI because they have complexity that software can help coordinate. Large retailers with seasonal inventory challenges (winter vs. summer inventory overages) benefit significantly. Small retailers with minimal excess inventory volume might not generate sufficient ROI to justify implementation costs.

Key Takeaways

- Another raised $2.5M seed from Anthemis FIL and Westbound to solve off-channel inventory management for retailers

- Off-channel inventory represents $350-450B annual value in retail, yet remains operationally inefficient and manual

- Another integrates with existing retailer systems to centralize data and optimize inventory routing to secondary markets

- Retailers can improve excess inventory recovery rates from 25-30% to 40-45% through intelligent marketplace matching and pricing optimization

- Ghost represents the main direct competitor but uses a marketplace model versus Another's integration-focused operational software approach

- Sustainability benefits (waste reduction) align Another's business case with environmental imperatives reshaping retail

- Implementation typically requires 4-12 weeks depending on system complexity; ROI justifies costs through 5-10 point recovery rate improvements

- Mid-sized to large fashion retailers see highest ROI due to rapid inventory depreciation and complexity in managing multiple secondary channels

- The market remains early with significant opportunity for market leadership before larger vendors enter with feature-based competition

Related Articles

- Eat App India Expansion: Restaurant Reservation Market Analysis 2025

- Garmin tactix 8 Cerakote Coating: Ultimate Durability Guide [2025]

- UK Electric Car Campaign: 5 Critical Roadblocks the Government Ignores [2025]

- ExpressVPN Deal: 78% Off Two-Year Plans [2025]

- Hyatt Ransomware Attack: NightSpire's 50GB Data Breach Explained [2025]

- Netflix's Star Search Live Voting: How Interactive TV Is Reshaping Competition Shows [2025]