![AWS's Copper Mining Deal: How AI Data Centers Are Reshaping Supply Chains [2025]](https://tryrunable.com/blog/aws-s-copper-mining-deal-how-ai-data-centers-are-reshaping-s/image-1-1768943298341.png)

How Amazon's Copper Deal Exposes AI's Hidden Infrastructure Crisis

When you think about AI, you probably picture algorithms, GPUs, and lines of code. What you don't picture is tons of copper getting pulled from Arizona mines to wire up data center cabinets. But that's exactly what's happening right now, and it's becoming a serious problem.

Amazon Web Services just signed a major deal with Rio Tinto to source newly mined copper from Arizona operations, marking the first domestic copper supply agreement of its kind in over a decade. This isn't a casual contract. It's a strategic move that signals something bigger: the infrastructure needed to power AI isn't just about electricity or land anymore. It's about raw materials, and we're starting to run out.

The problem is simple but alarming. Every hyperscale data center needs enormous amounts of copper. We're talking tens of thousands of metric tonnes per facility. AWS alone is building data centers faster than ever to support LLM training, inference, and the broader AI arms race. But the US copper mining industry has been dormant for years. Rio Tinto's deal includes around 14,000 metric tonnes of copper from its Nuton bioleaching process over four years, with another 16,000 metric tonnes from conventional leaching. That sounds like a lot until you realize a single large data center can consume 20,000 to 30,000 tonnes on its own. One deal. One data center's worth. That's the scale problem we're facing.

What makes this even more complex is the environmental angle. AWS has committed to reaching net-zero carbon emissions by 2040 under its Climate Pledge. But mining copper, even with newer methods, still generates emissions and consumes water. Rio Tinto's Nuton technology uses naturally occurring microorganisms to extract copper from sulfide ores, which the company claims reduces water usage and carbon footprint compared to traditional smelting routes. Yet only part of the deal relies on this lower-carbon method. The rest comes from conventional processing. So AWS is balancing sustainability promises against infrastructure realities, and neither side is winning cleanly.

This moment is worth understanding because it reveals something that tech companies don't talk about much: the physical constraints on AI scaling. You can build better algorithms, buy more GPUs, and hire more engineers. But you can't just wish copper mines into existence. Mining takes years to permit, billions to build, and environmental trade-offs that affect real communities. This is where the rubber meets the road for AI infrastructure.

TL; DR

- AWS's Rio Tinto deal covers only 30,000 metric tonnes of copper over four years, while a single large data center can consume 20,000-30,000 tonnes alone

- US copper mining capacity has been dormant for over a decade, creating a critical supply constraint for AI infrastructure buildout

- Rio Tinto's Nuton bioleaching process uses less water and generates lower emissions, but only part of the deal leverages this technology

- AI data centers require massive copper volumes for electrical systems, wiring, transformers, and cooling infrastructure, making material supply a practical constraint on scaling

- The AWS-Rio Tinto partnership signals that tech companies are beginning to address upstream supply chain resilience as a competitive advantage

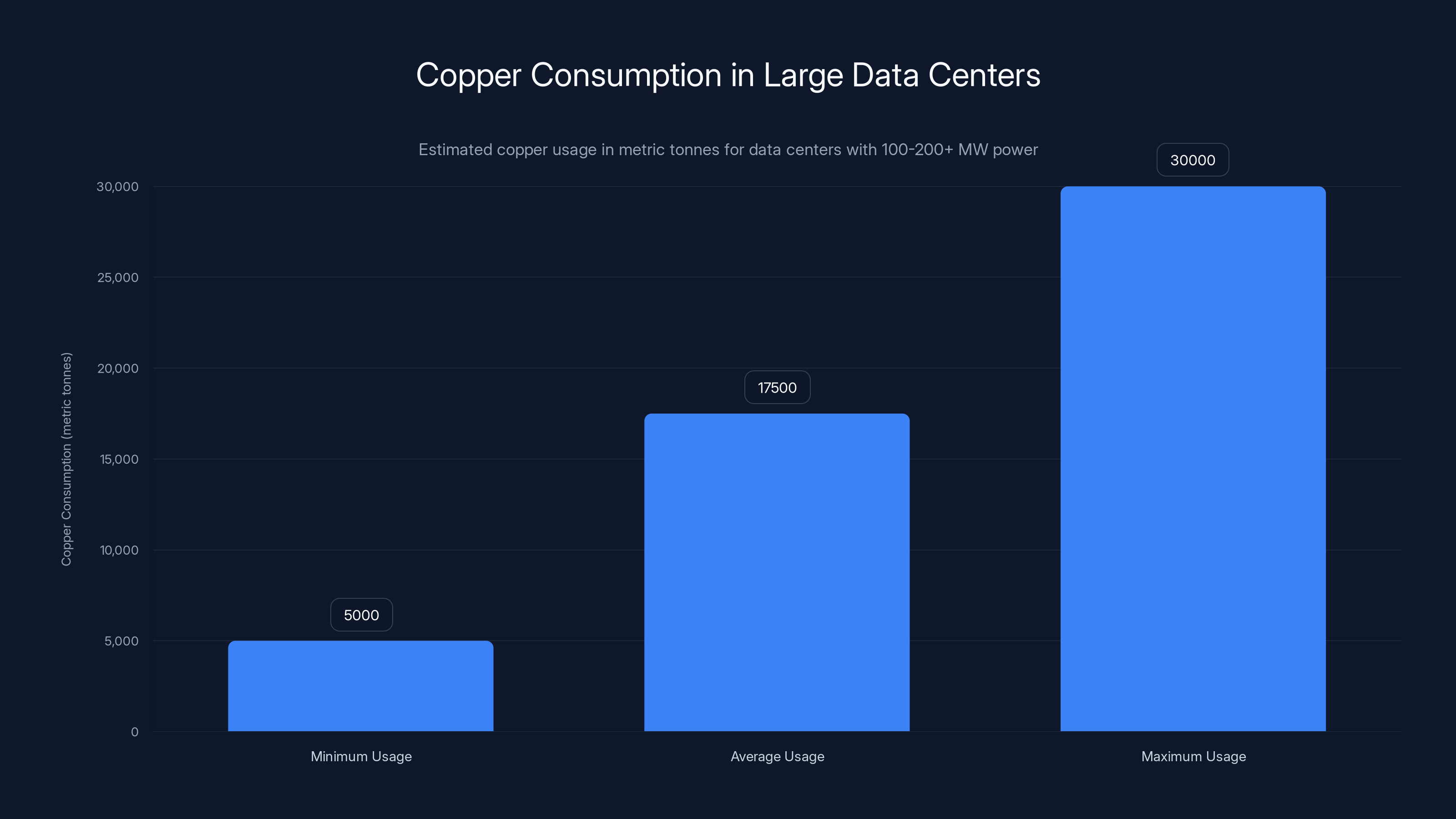

Large hyperscale data centers consume between 5,000 to 30,000 metric tonnes of copper, depending on their size and design. (Estimated data)

The Copper Problem Nobody's Talking About

Let's start with what copper actually does in a data center. It's not flashy. It's not on the roadmap slides investors see. But it's absolutely critical.

Copper is the foundational material for the entire electrical infrastructure of a hyperscale facility. Every cable running between servers, every transformer stepping down voltage, every switch connecting hardware, every cooling system pipe. Copper is in all of it. The metal conducts electricity with minimal resistance, doesn't corrode easily, and handles the thermal stress that comes with massive power loads. There's no real substitute at scale.

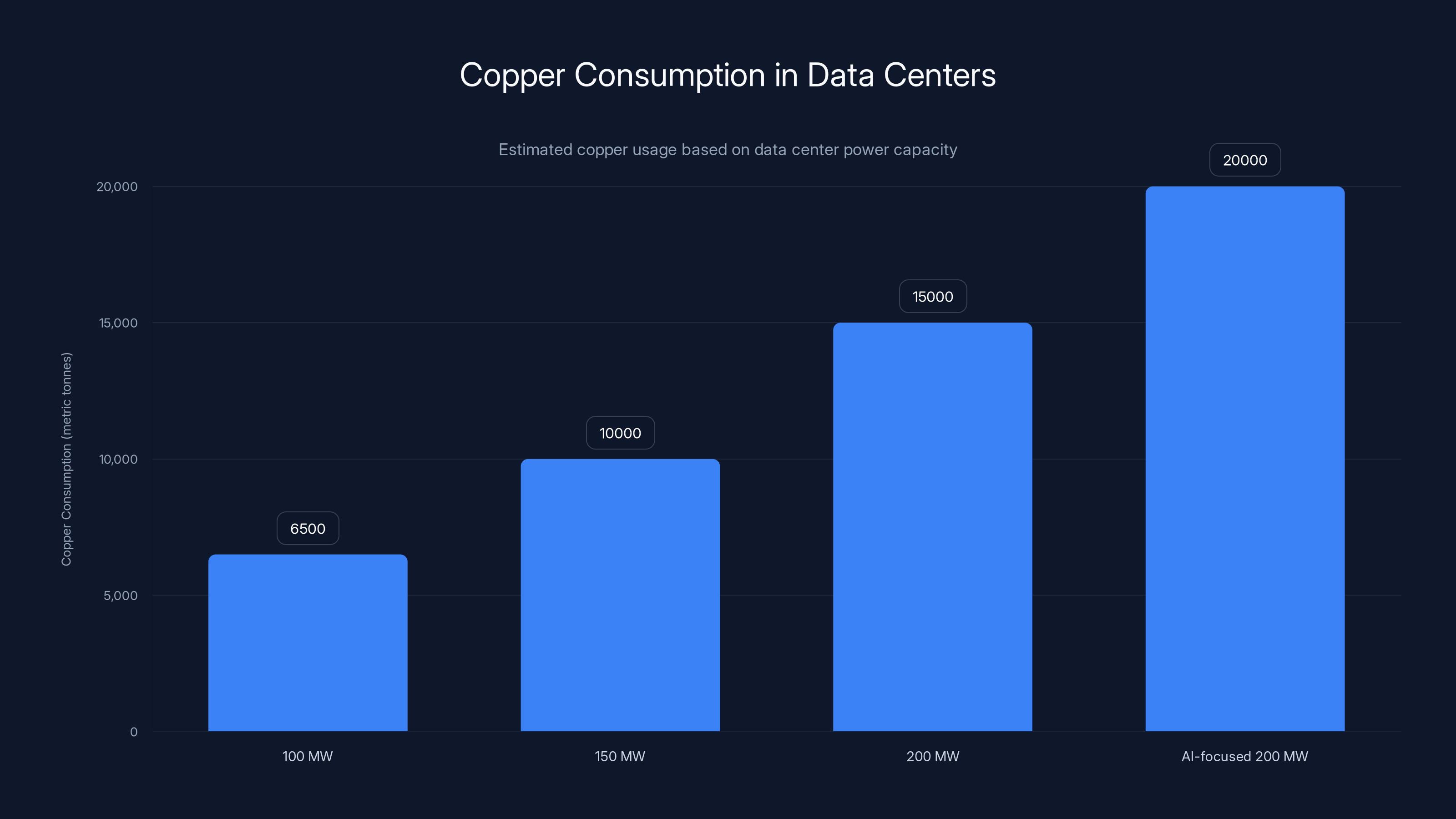

A single large data center pulling 100+ megawatts of power needs staggering amounts of copper. We're talking thousands of tonnes just for the main distribution infrastructure. Add in redundancy, backup systems, and the tens of thousands of individual server connections, and you're looking at 20,000 to 30,000 metric tonnes of copper per facility.

Now multiply that by the number of data centers AWS is building right now. The company announced in 2024 that it's accelerating infrastructure investment to support AI workloads. Not just maintaining existing capacity. Building new facilities. Lots of them. Microsoft is doing the same. Google too. Every hyperscaler is racing to expand data center footprint because demand for AI inference and training is accelerating faster than they anticipated.

Here's where the crisis emerges: the US copper mining industry largely shut down over the past fifteen years. Environmental regulations, permitting delays, community opposition, and competition from cheaper foreign mining all contributed. The last major new domestic copper mine opened years ago. Supply has been relatively flat while global demand climbed steadily. Now you have AI data center construction accelerating the timeline, and suddenly copper availability becomes a bottleneck.

Rio Tinto's Johnson Camp mine restart is significant, but it's also limited. The company is using it as a proving ground for Nuton technology, not as a full-scale production facility yet. The 30,000-metric-tonne commitment over four years works out to about 7,500 tonnes annually. That's real supply, but it's also a drop in an increasingly empty bucket.

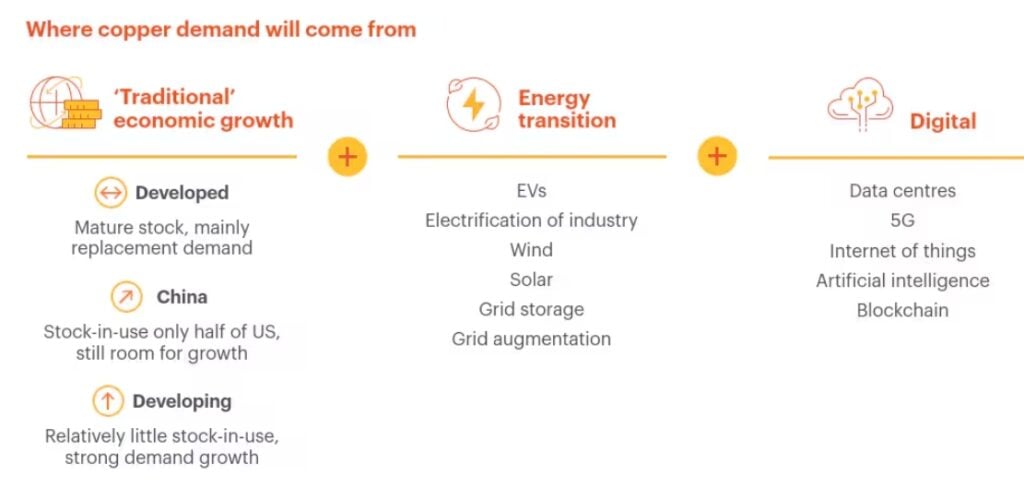

The broader US copper supply is around 1.2 million tonnes annually. Data centers alone are starting to consume tens of thousands of tonnes per year when you add up all the hyperscalers' buildout. It's not the only copper use, either. Construction, manufacturing, telecommunications, automotive, renewable energy systems. Everyone needs copper. And AI infrastructure is arriving at the worst possible time, when supply is constrained and demand is explosive.

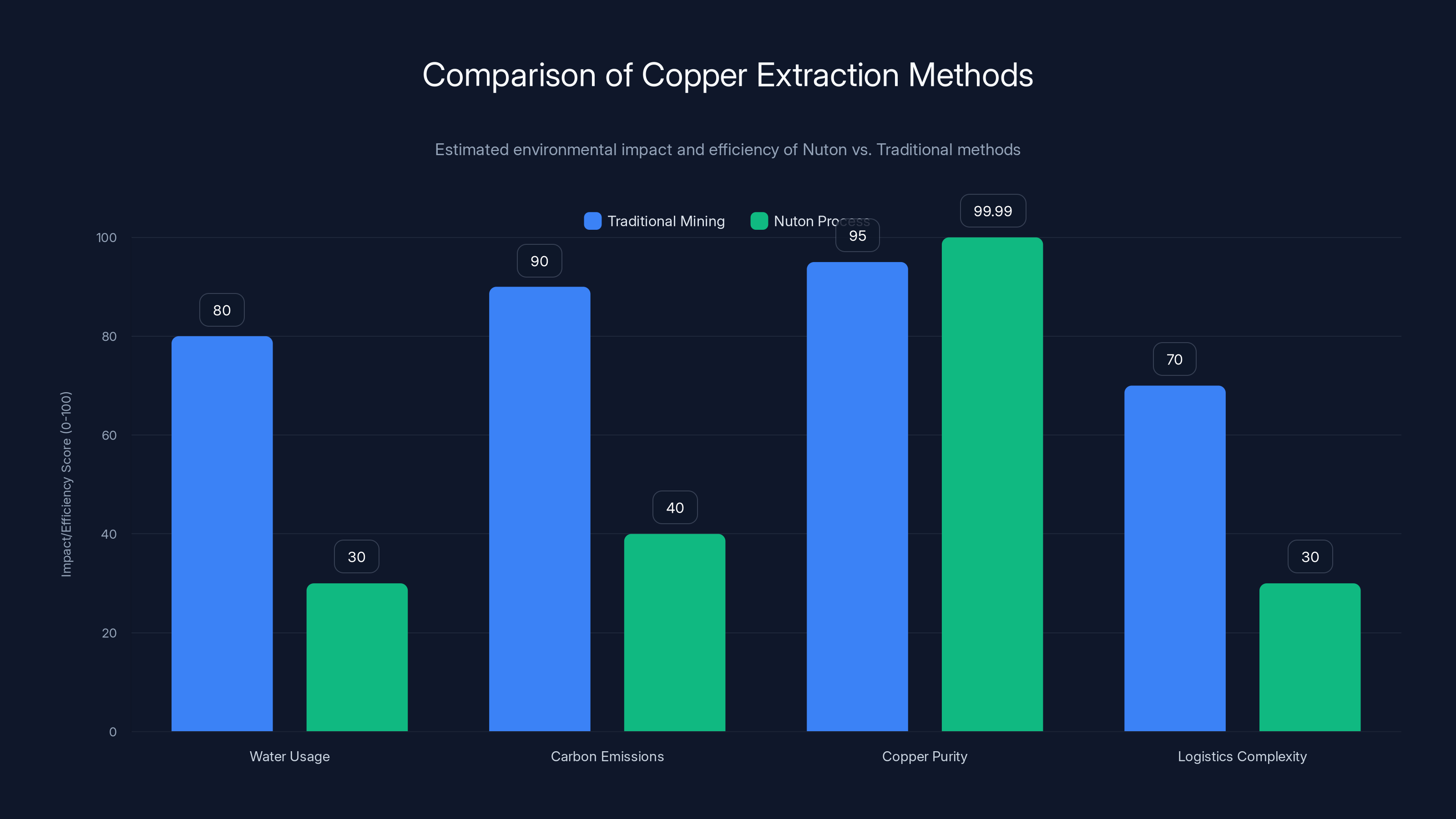

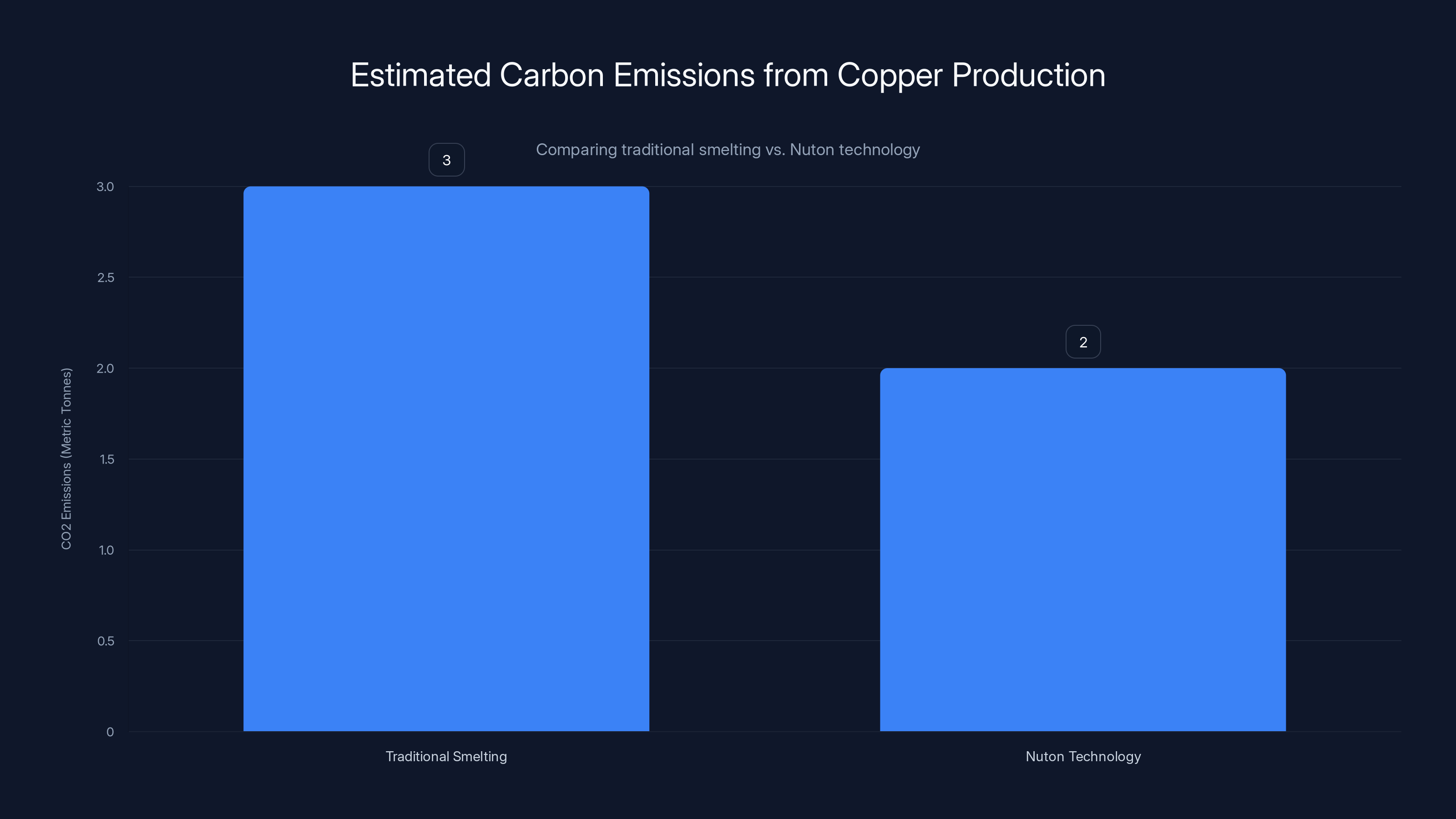

The Nuton process significantly reduces water usage and carbon emissions while delivering higher purity copper and simplifying logistics. Estimated data.

Why Rio Tinto's Nuton Technology Matters (And Why It's Not Enough)

Rio Tinto's Nuton process represents a genuine innovation in copper extraction, and it's worth understanding what makes it different from conventional mining.

Traditional copper mining from sulfide ores involves several energy-intensive steps. You dig up ore, crush it, process it through concentrators to separate copper-bearing minerals, then send it to smelters where heat and chemicals refine it further. Each stage generates emissions, consumes water, and produces waste. The process works, but it's resource-heavy and creates environmental costs that mining companies increasingly need to justify to regulators and communities.

Nuton takes a different approach. The process leverages naturally occurring microorganisms to biologically extract copper from primary sulfide ores. Essentially, the bacteria do the chemical work that would normally require industrial equipment and heat. The bacteria consume the ore and produce copper that can be harvested more directly. Rio Tinto operates the system at the mine site, producing copper cathode on location rather than shipping raw ore to distant smelters.

The environmental argument is compelling on paper. Nuton reportedly uses significantly less water than conventional smelting routes. Water is precious in Arizona and the broader Southwest, where the Johnson Camp mine operates. The process also generates lower carbon emissions because you're not running massive smelters and refineries. Plus, Rio Tinto claims the process can recover copper from ore previously classified as waste, which means more total copper extracted without expanding the mining footprint.

The purity angle is also important for AWS. Nuton delivers 99.99% pure copper cathode at the mine site. That simplicity reduces logistics complexity. AWS doesn't need to buy cathode from intermediaries or deal with refining. It's a more direct supply chain, which matters when you're trying to secure strategic materials.

But here's the critical limitation that AWS and Rio Tinto don't emphasize: only a portion of the deal actually relies on Nuton technology. Rio Tinto's commitment includes 14,000 metric tonnes of Nuton copper and around 16,000 metric tonnes from conventional run-of-mine leaching. So you've got roughly 50-50 split between the innovative, lower-carbon process and conventional mining.

Why not go all-in on Nuton? The answer is scale and certainty. Nuton is still being proven at commercial scale. It works in testing and pilot operations, but ramping a new biological process to full production capacity takes time, optimization, and troubleshooting. Rio Tinto included conventional methods to guarantee AWS would actually receive the full 30,000 tonnes promised over four years. If Nuton hit unexpected issues, conventional backup supply ensures the contract gets fulfilled.

So the environmental benefit, while real, is partial. AWS is getting some lower-carbon copper, which supports its Climate Pledge narrative. But it's also getting conventional copper, which comes with traditional mining impacts. The company is threading a needle between sustainability commitments and infrastructure realities.

The Math Behind Data Center Copper Consumption

Let's get specific about copper usage because the numbers illustrate how constrained the supply chain actually is.

A hyperscale data center—the kind AWS, Microsoft, and Google build—typically spans 100,000 to 500,000 square feet. The largest facilities push toward 1 million square feet. These buildings house tens of thousands of servers generating enormous power loads, often 50 to 150 megawatts per facility. Some newer AI-focused centers approach 200+ megawatts.

Copper requirements scale with power delivery complexity. The more megawatts you're running through a facility, the more copper infrastructure you need to distribute that power safely and efficiently. Here's the breakdown:

Main distribution feeds from substations to the data center typically use cables with 500-1000 MCM copper (1 MCM is roughly 0.5 square millimeters of cross-section). A single large feed might contain multiple conductors, each requiring thousands of pounds of copper. You might have 10-20 separate main feeds entering a large facility, each to provide redundancy and load balancing.

Within the data center, power is distributed through increasingly smaller copper busbars and cables. Server rows, cabinet feeds, and PDU (power distribution unit) connections all require copper. The density of copper in a data center electrical room is actually stunning if you've ever seen it in person—copper bus bars stacked, color-coded cables running everywhere, transformers the size of refrigerators.

Additionally, cooling systems require massive amounts of copper. Chillers, heat exchangers, water loops, and refrigerant circuits all rely on copper tubing and components. Large data centers consume hundreds of tons of copper in cooling infrastructure alone.

Adding it up: a 100-megawatt data center with typical architecture needs somewhere in the range of 5,000 to 8,000 metric tonnes of copper. A 200-megawatt AI-focused facility could require 10,000 to 20,000 tonnes. The largest hyperscale centers? 20,000 to 30,000 tonnes is realistic.

AWS's 30,000-tonne commitment from Rio Tinto covers roughly one to four large data centers, depending on their size and design. AWS is planning dozens of new facilities over the next few years to support AI. The supply math gets grim quickly.

Here's another angle: copper prices have been volatile. In 2023, copper traded around

Using rough coefficients: a 100 MW facility with standard distribution might calculate as 100 × 70 + 1500 = 8500 metric tonnes of copper.

Copper consumption in data centers scales significantly with power capacity, with AI-focused centers requiring up to 20,000 metric tonnes. Estimated data.

AWS's Climate Pledge and the Carbon Copper Paradox

Amazon committed to reaching net-zero carbon emissions across its entire business by 2040 under its Climate Pledge. That's a massive undertaking. AWS generates enormous carbon footprints through electricity consumption, data center construction, and supply chain operations.

Mining and refining copper produces significant carbon emissions. Traditional smelting operations are energy-intensive and often powered by fossil fuels. A metric tonne of copper production can generate 2-4 metric tonnes of CO2 equivalent when you account for mining, crushing, concentration, smelting, and refining. These are industrial processes built over decades using established infrastructure, and much of that infrastructure still relies on conventional power.

AWS's partnership with Rio Tinto on Nuton technology is directly intended to lower the carbon footprint of copper supply. By using biological extraction instead of high-temperature smelting, Rio Tinto claims Nuton reduces emissions per tonne of copper produced. The company hasn't released exact numbers, but industry estimates suggest 30-40% emission reductions compared to conventional concentrate smelting operations.

But here's the paradox: to reach net-zero by 2040, AWS would need to do more than just reduce the carbon intensity of copper. It would need to eliminate emissions entirely, or offset them through carbon credits and renewable energy investments. Nuton copper might be lower-carbon, but it's not zero-carbon. And the conventional half of the deal definitely isn't.

Further, AWS is rapidly expanding its data center footprint specifically to support AI workloads. More data centers mean more copper consumption. Even if each tonne of copper comes from lower-carbon sources, the total volume consumed still climbs. You're playing a game where demand is accelerating faster than the efficiency gains you can achieve.

This reveals the deeper tension in AWS's strategy. The company wants to scale AI infrastructure aggressively to compete with Microsoft, Google, and others. It also wants to maintain a Climate Pledge commitment that increasingly looks difficult to achieve. The Rio Tinto deal is a partial solution: it addresses supply and partly addresses carbon. But it doesn't solve the fundamental issue that massive AI infrastructure buildout and net-zero commitments are in tension.

AWS spokesperson Kara Hurst, the company's Chief Sustainability Officer, framed the deal as essential to decarbonizing at scale. The language suggests AWS believes this partnership is part of the path to 2040. But the math says otherwise. Even lower-carbon copper sourced from one mine can't offset the emissions from dozens of new data centers powered by electricity that, while increasingly renewable, still partially comes from fossil fuels.

What AWS is really doing is signal that it takes supply chain sustainability seriously, differentiate against competitors who ignore the issue, and reduce carbon intensity incrementally while accepting that net-zero by 2040 requires much broader systemic changes outside the scope of any single supply agreement.

The Broader Copper Supply Chain and Global Competition

The US represents only a small fraction of global copper production. Understanding the global picture explains why AWS pursuing domestic supply is strategic beyond just reducing transportation distance.

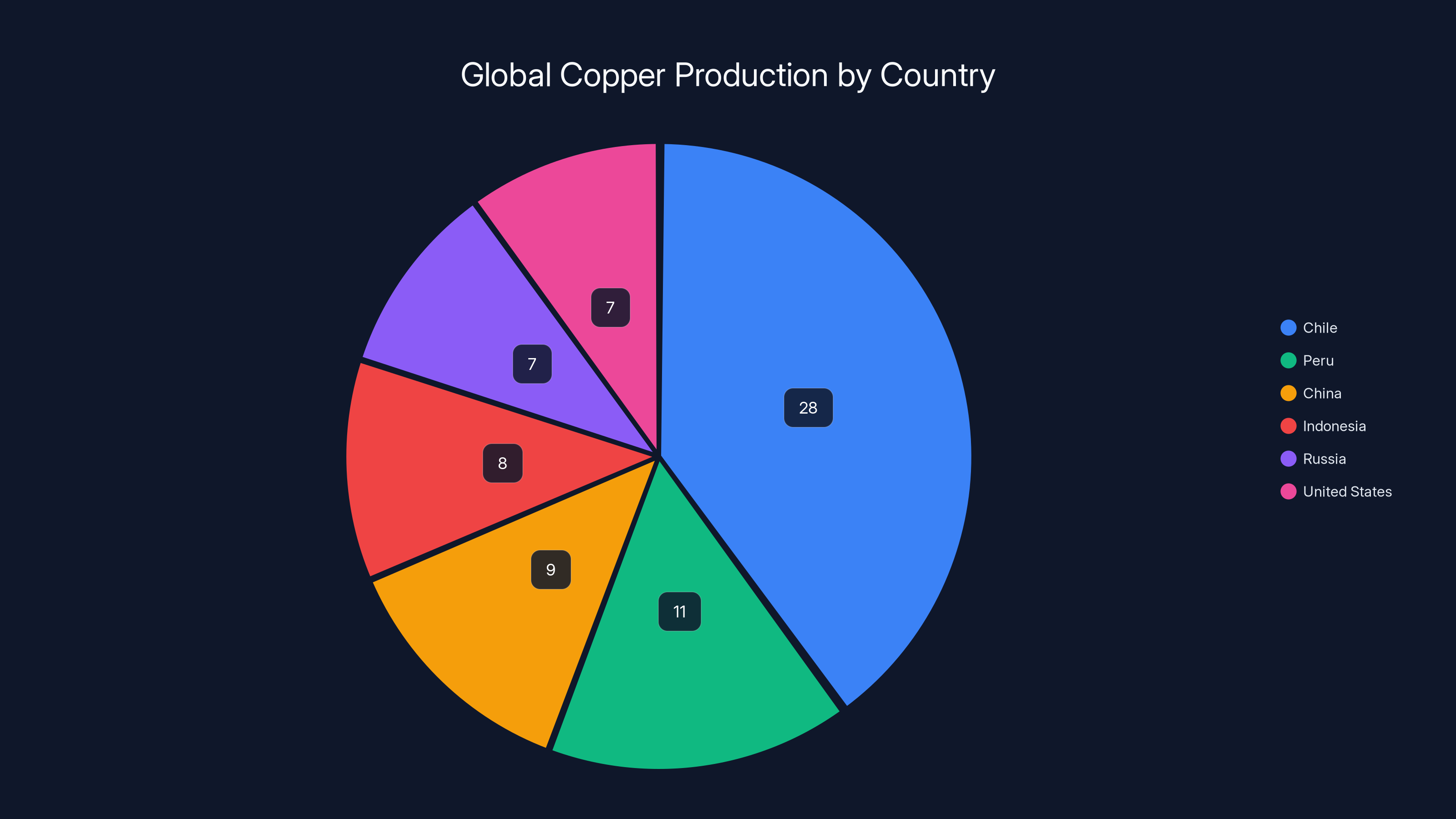

Chile is the world's largest copper producer, providing roughly 25-30% of global supply. Peru is second at around 10-12%. Indonesia, China, Russia, Zambia, and Australia round out the major producers. The US, despite having copper reserves, accounts for only about 7-8% of global production, and that figure has been declining.

Why does geography matter? Three reasons: supply concentration risk, geopolitical dependency, and cost dynamics.

First, supply concentration. When most of the world's copper comes from a handful of countries, disruptions in those regions ripple globally. Chile experienced political turmoil in recent years. Peru has faced labor strikes and community opposition to mining expansion. Indonesia's copper reserves are significant, but the country has regulatory uncertainty. When supply is politically concentrated, big consumers like AWS become vulnerable to price spikes and allocation decisions they can't control.

Second, geopolitical tension. Trade relationships between the US and China have deteriorated. Tariff threats, semiconductor export controls, and restrictions on advanced technology all reflect broader strategic competition. Copper is less politically sensitive than semiconductors, but it's still a strategic material. US dependence on Chinese or Russian copper would create vulnerability. Domestic supply, even if it costs slightly more, reduces that exposure.

Third, cost dynamics. Copper costs are linked to global spot prices, which fluctuate based on worldwide supply and demand. If global supply tightens due to mining disruptions or geopolitical events, prices spike everywhere. Domestic supply under a long-term contract locks in costs and provides price certainty. AWS probably negotiated fixed or capped pricing with Rio Tinto, protecting the company against future market volatility.

China has been actively securing copper supply globally, making deals in Africa and South America. The country recognizes that copper is critical to EV manufacturing, renewable energy, and data center expansion. AWS and other US tech companies are essentially playing catch-up, realizing they need to secure strategic materials directly rather than relying on global spot markets.

The Rio Tinto deal should be understood in this context. It's not just about mining. It's about supply chain resilience in an era where critical materials are increasingly contested.

Chile leads with 28% of global copper production, followed by Peru at 11%. The US contributes about 7%, highlighting its strategic interest in domestic supply. Estimated data.

How AI Infrastructure Is Reshaping Mining Economics

Historically, copper mining investment decisions were driven by automotive demand, construction, and electrical utilities. AI data centers are introducing a new demand driver that's reshaping how mining companies think about capacity expansion.

Traditional mining projects have long lead times. Identifying a viable deposit takes years. Securing environmental permits can take a decade or more. Building a new mine another five to ten years. Then you're operating the mine for decades, hopefully profitably, before eventual depletion.

Rio Tinto evaluated the Johnson Camp deposit years ago and determined it wasn't economically viable for conventional mining. The ore grades weren't high enough, the processing costs were too steep, and demand didn't justify the investment. It sat dormant.

Enter Nuton technology. The innovation made processing lower-grade ore economical. Rio Tinto could develop the deposit with lower costs and environmental impact. But even that improvement might not have triggered development if demand remained flat.

AI changed that calculus. Suddenly, AWS and other hyperscalers are promising large, multi-year copper contracts. AWS's commitment gave Rio Tinto demand certainty. That certainty makes the investment in Nuton development and Johnson Camp reactivation financially justified.

This creates a virtuous cycle for Rio Tinto and similar mining companies. AI infrastructure growth signals sustained demand for copper. Companies like Rio Tinto respond by investing in new capacity and new technologies. That increased supply helps meet AI infrastructure needs while also benefiting other copper consumers.

But the cycle has limits. Mining development timelines are measured in years. AWS is building data centers measured in months. The supply response lags the demand surge. That's why AWS pursued the Rio Tinto deal even though 30,000 tonnes only covers a few data centers. It's a down payment on future security.

From Rio Tinto's perspective, the deal is strategically valuable beyond the immediate copper revenue. Nuton success at Johnson Camp can be replicated at other deposits globally. Rio Tinto operates copper mines in Australia, Mongolia, Chile, and elsewhere. If Nuton works at scale, the company can apply the technology to increase production across its global portfolio. AWS's early commitment effectively subsidizes Rio Tinto's proof-of-concept for a technology that could reshape global copper economics.

It's a symbiotic relationship. AWS gets supply security and lower-carbon copper. Rio Tinto gets demand certainty and customer validation for an unproven technology. Both companies benefit from the partnership.

The Role of AWS Infrastructure Management Systems

One overlooked aspect of this deal is the technological layer AWS brings to mining operations.

AWS is providing infrastructure management and analytics systems to monitor Johnson Camp operations. The article mentions that AWS is running simulations of heap leach behavior and feeding data analytics into operational decisions. This resembles AI tools used to optimize software systems, though applied to geological and mining processes.

What does that actually mean? Mining is increasingly data-driven. Ore grade, moisture content, microorganism health (in biological leaching), extraction rates, water usage, and chemical composition all vary. Managing these variables in real-time requires massive amounts of sensing, data collection, and analytics.

AWS is essentially applying cloud infrastructure expertise to optimize mining operations. Sensors deployed throughout the Johnson Camp mine feed data to AWS systems that model leach behavior, predict extraction efficiency, and suggest operational adjustments. It's industrial optimization at scale.

This adds another dimension to why AWS pursued the partnership. It's not just securing copper supply. It's creating a strategic relationship that allows AWS to pilot advanced data analytics and optimization tools in a physical industrial setting. The company gains real-world validation of infrastructure management systems that could eventually be sold to other mining, manufacturing, and industrial customers.

Rio Tinto gets operational efficiency and real-time visibility into the Nuton process. The partnership accelerates learning about how to run the novel process at scale. For a company trying to prove that biological copper extraction is commercially viable, having the world's largest cloud infrastructure provider optimize your operations is invaluable.

It's worth noting that Rio Tinto is not exclusively dependent on AWS. The company runs its own substantial data and analytics operations. But the partnership suggests Rio Tinto values AWS's expertise and wants the company embedded in optimizing Johnson Camp. That's a significant strategic win for AWS beyond just securing copper.

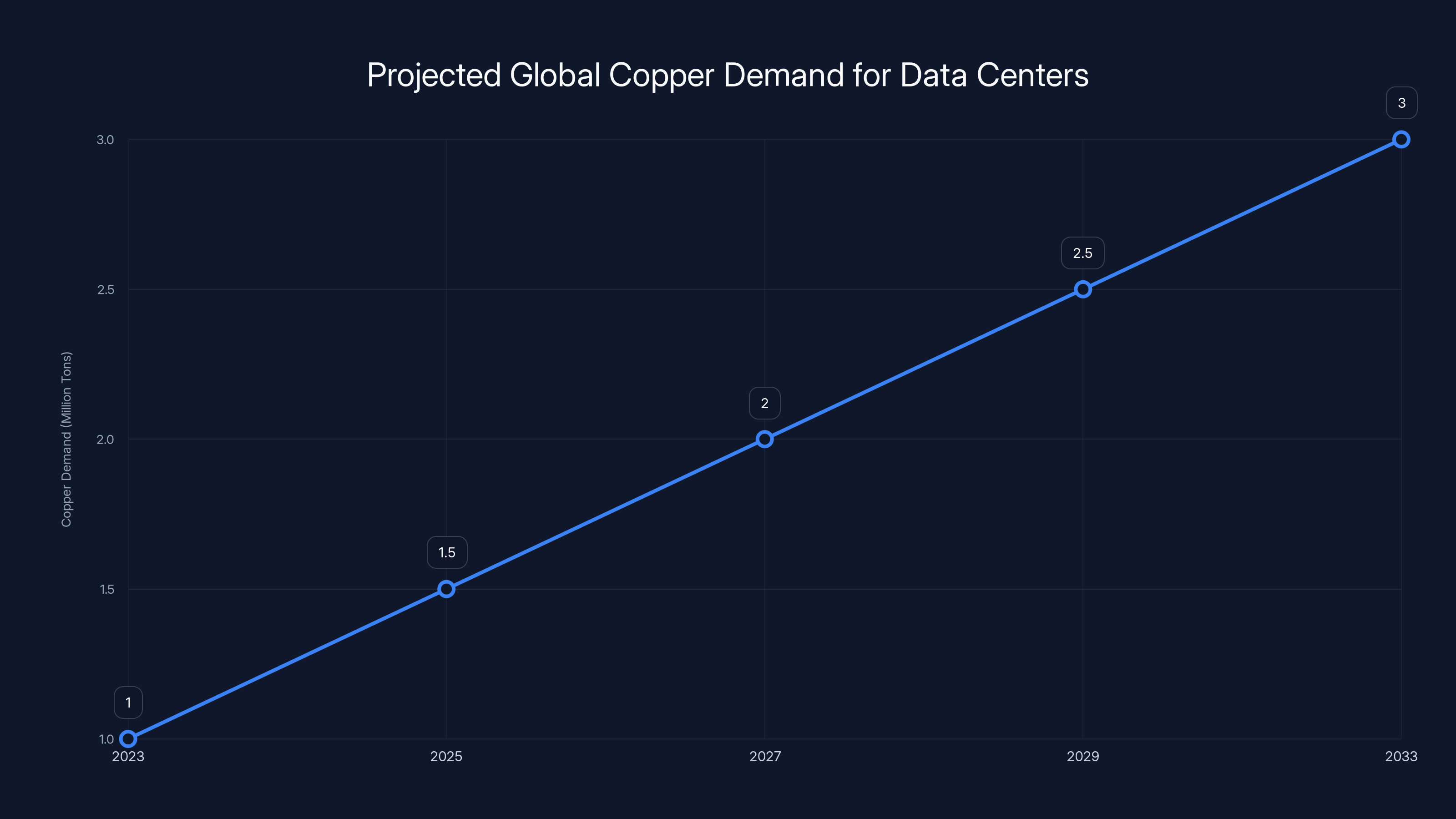

Estimated data suggests that global copper demand for AI data centers could triple by 2033, driven by the rapid expansion of AI infrastructure. Estimated data.

Water Usage and Southwestern Drought Realities

Arizona's water situation is dire. The Colorado River, which supplies roughly 80% of Arizona's water, is in structural deficit. Lake Mead and Lake Powell reservoirs have dropped to historically low levels. The state has faced mandatory water cuts in recent years.

Into this water-constrained environment comes copper mining. Traditional mining and smelting are water-intensive. Rio Tinto's claim that Nuton uses significantly less water is therefore critical to community acceptance and regulatory approval.

But the numbers matter. How much less water does Nuton actually use compared to conventional processing? Rio Tinto hasn't released detailed comparative data. Industry estimates suggest Nuton could reduce water consumption by 70-90% compared to traditional smelting-based routes. If true, that's dramatic.

For context, traditional copper smelting can consume 1-2 gallons of water per pound of copper produced. Nuton reportedly reduces this to 0.1-0.2 gallons per pound. For the 30,000 tonnes AWS is sourcing, that difference represents hundreds of billions of gallons of water over the contract period. That's not trivial in a desert state.

However, the water equation is more complex than just processing efficiency. Mining itself consumes water. Dust suppression, ore leaching, and heap management all require water. The Johnson Camp mine site isn't getting water from nowhere. It's drawing from Arizona aquifers and potentially from Colorado River allocations.

Rio Tinto and AWS have framed the partnership as environmentally responsible given the water efficiency gains. Environmental groups have been more skeptical, arguing that even lower-water copper mining still creates water stress in an already stressed region.

This tension reveals something important about how tech companies think about supply chains. AWS's Climate Pledge and sustainability commitments are real. The company wants lower-carbon, lower-water copper. But the company also needs copper to build data centers. The Rio Tinto deal represents an optimization within constraints: get the most environmentally responsible supply possible while still securing the material required to scale AI infrastructure.

That's a reasonable business decision, but it's not solving the underlying constraint. Arizona's water situation will worsen over the next decade as climate change alters precipitation patterns and snowpack in the Rockies. Even efficient mining will struggle to justify itself if water becomes genuinely scarce. The Rio Tinto partnership is a near-term answer to a medium-term problem that doesn't have a good solution.

The Competitive Advantage of Vertical Supply Chain Integration

AWS's deal with Rio Tinto represents a subtle but important shift in how tech companies think about supply chain strategy.

Historically, AWS and other hyperscalers treated copper like any other commodity. Buy it on the spot market or through standard supply contracts. Optimize price and delivery logistics. The metal was fungible; the source didn't matter much.

That's changing. AWS, Microsoft, and Google are increasingly recognizing that controlling upstream material supply creates competitive advantage. If you can secure copper, silicon, rare earths, and other critical materials, you reduce cost volatility, ensure capacity to scale, and potentially gain pricing advantages.

AWS's Rio Tinto partnership is part of this vertical integration strategy. The company isn't just buying copper. It's partnering with a mining company to develop new production methods, investing in mine optimization, and securing long-term supply commitments. It's the kind of relationship that historically would have been unusual for a software company.

But AWS isn't really a software company anymore. It's an infrastructure company. And infrastructure companies need to control their material supply chains.

This has competitive implications. If AWS secures reliable copper supply at predictable costs, it can underbid competitors who rely on volatile spot markets. If Microsoft or Google face copper shortages, they face delays expanding data center capacity. AWS builds on schedule. That operational advantage compounds over time.

It also signals something to other tech companies: you need to think about supply chain resilience now, not later. The first companies to secure strategic materials will have advantages. The companies that wait risk getting squeezed as supply tightens and prices rise.

From Rio Tinto's perspective, the partnership provides similar advantages. The company gets an anchor customer, long-term demand certainty, and investment in new technology. That combination makes Rio Tinto more attractive to investors and more resilient to commodity price downturns.

This kind of vertical integration could reshape how both mining and technology industries operate. Rather than separate markets, you get strategic partnerships between resource companies and infrastructure companies. The companies that best integrate these relationships will likely outcompete those that don't.

Nuton technology is estimated to reduce carbon emissions by 30-40% compared to traditional smelting, lowering emissions from 3 to 2 metric tonnes per tonne of copper. Estimated data.

Permitting, Regulation, and the Speed of Change

One reason AWS pursued a domestic copper deal is precisely because new mines take forever to develop.

Opening a copper mine in the US requires extensive environmental review, community consultation, permitting from multiple agencies, and often litigation from environmental groups. The timeline from exploration to production easily spans 10-15 years. Sometimes longer.

Rio Tinto's Johnson Camp restart is advantageous because the site was previously mined. Permitting is faster for expanding an existing mine than developing a new one. Environmental baselines are established. The local community has historical experience with mining. There's precedent for operations.

Still, restarting Johnson Camp required environmental review, permits, and regulatory approvals. Rio Tinto likely spent years navigating this process before AWS's supply agreement was finalized.

The speed challenge is real. AWS wants to build data centers now. Copper constraints exist now. But new US mining capacity won't materialize for many years. The Rio Tinto deal buys time by reactivating existing capacity, but it doesn't solve the longer-term problem.

For other potential mining projects, the regulatory timeline is even more daunting. The US has vast copper reserves, but developing them requires something the industry hasn't had much practice with recently: quickly permitting new mines in an era of climate consciousness and environmental litigation.

This creates a policy opportunity. If the government recognized critical mineral supply as strategically important, it could streamline permitting for domestic mining projects. But that's politically contentious. Environmental groups oppose mining expansion. Communities worry about local impacts. Indigenous tribes have treaty rights over some lands with copper deposits.

AWS likely recognizes that pursuing one Rio Tinto deal is more politically feasible than advocating for broad mining deregulation. The company gets supply, Rio Tinto gets validation and customer demand, and both avoid the political firestorm of pushing broader mining policy changes.

But this is a short-term solution to a structural problem. If AI infrastructure demand continues accelerating, and if the US wants to maintain domestic mining capacity rather than rely entirely on imports, something will eventually have to give on the regulatory front. That's a conversation happening slowly in Washington, but not yet with the urgency the supply chain constraints suggest is warranted.

Copper Alternatives and Why They Don't Exist at Scale

You might wonder: why is copper irreplaceable? Why not use aluminum, fiber optics, or some newer material?

The answer is physics and economics. Copper has properties that are difficult to replicate at the scales and costs required for data center infrastructure.

Copper's electrical conductivity is excellent: only silver conducts electricity better, but silver is far more expensive and rarely used for infrastructure. Copper's thermal conductivity is also outstanding, which matters for cooling applications. The metal is ductile, allowing it to be drawn into fine wires and cables. It doesn't corrode easily in most environments, reducing maintenance requirements.

Aluminum is cheaper and more abundant, so why not use it instead? Aluminum's conductivity is only about 60% that of copper. To achieve the same current-carrying capacity, you need thicker aluminum conductors or more of them. The cost savings from aluminum's lower price get erased by needing more material. Plus, aluminum corrodes more easily, requiring more protective coatings and maintenance.

Fiber optics handle data transmission beautifully, replacing copper for long-distance networking. But data center infrastructure involves power distribution, not just data. Fiber can't carry electricity. You still need copper for all the power infrastructure.

Recently, there's been research into superconductors for power transmission. If superconductors were practical at data center temperatures and costs, they could theoretically reduce copper requirements dramatically. But that technology is decades away from commercial deployment, and the cooling costs might negate the copper savings.

The practical reality is that copper has no close substitute for data center power infrastructure at current costs and scales. The industry tried optimizing around copper constraints during previous supply crunches, and copper usage evolved incrementally, not fundamentally. You can't wire a 200-megawatt data center with aluminum or fiber optics. The physics and economics simply don't work.

This explains why AWS is willing to partner with Rio Tinto and secure long-term copper supply. The company has no choice. There's no material revolution coming that solves the copper problem. The only solution is securing supply from actual mines.

Future Copper Demand and the Growth Trajectory

Let's project forward. If AI data center buildout continues accelerating, what happens to copper demand over the next 5-10 years?

AI infrastructure is becoming a separate category of data center from traditional cloud infrastructure. AI requires higher power density, more sophisticated cooling, and different architectural approaches. Companies are building these specialized facilities globally, not just in the US.

Microsoft's data center expansion is massive. Google's infrastructure buildout is equally aggressive. Chinese tech companies are building data centers domestically. Regional cloud providers in Europe, Asia, and elsewhere are all expanding to meet AI demand.

If this trend continues, global copper demand specifically for data center infrastructure could double or triple over the next five years. That's on top of existing demand from construction, automotive, renewable energy, and manufacturing.

Global copper supply grows much more slowly than demand. Mining projects operate for decades, but capacity additions are incremental, not step-change improvements. New mines are difficult to develop, as discussed. Recycling copper from old equipment helps, but recycling rates are only around 50% globally, and recycled copper can't meet all demand.

The math suggests copper is going to be tight. Prices will likely rise. Companies that haven't secured supply through long-term contracts will face cost increases and potentially allocation challenges during supply crunches.

Rio Tinto and similar mining companies will likely see pressure to expand capacity. AWS and other tech companies will likely pursue additional supply agreements with other mines. Some might even invest directly in mining ventures, following AWS's model.

This creates a fascinating dynamic: tech companies becoming more like resource companies, and resource companies becoming more like tech companies (adopting advanced analytics and optimization). The convergence reflects the reality that AI infrastructure requires secure material supply, and mining companies need technology partners to operate efficiently.

One variable that could change everything: a breakthrough in battery technology or superconductors that dramatically reduces copper requirements. Or a shift toward distributed AI inference reducing data center buildout. Or an economic recession cutting demand. These are possible, but none are guaranteed. The prudent assumption is that copper supply tightens significantly in the next decade, which justifies AWS's partnership with Rio Tinto and suggests similar deals will proliferate.

Implications for Data Center Siting and Strategy

Copper availability might eventually influence where tech companies build data centers.

Historically, data center location decisions were driven by electricity availability (ideally cheap, renewable), cooling (proximity to cool climates or water), fiber connectivity (being near network hubs), and tax incentives. Copper supply wasn't on the list.

But if copper becomes increasingly constrained, geographic proximity to copper supply could become a location factor. Building a massive data center in a region with no nearby copper supply means massive transportation costs to bring the material in. Building near copper mines and refineries reduces that cost.

Arizona is emerging as a copper hub by default. It has existing copper mines, Rio Tinto's operations, and Arizona State University's strong materials science research community. It's also in the Southwest, close to California's massive data center footprint.

AWS might find Arizona increasingly attractive for data center siting, not just because of electricity costs or climate, but because copper is close. Microsoft and Google might make similar calculations. This could accelerate data center growth in Arizona while slowing growth in regions without copper proximity.

There's also a question about whether tech companies might invest in copper refining capacity near data centers. Instead of buying finished copper, they might partner with refiners to optimize for specific applications. This would further vertically integrate supply chains.

It's speculative, but supply chain logic suggests that over a 10-year horizon, copper availability could influence data center site selection and infrastructure development strategies significantly.

ESG Implications and Shareholder Pressure

AWS's Rio Tinto partnership is attracting attention from environmental and social governance advocates.

Shareholders increasingly pressure tech companies on environmental impact. AWS's Climate Pledge is a competitive differentiator, and the company wants to be seen as serious about emissions reduction. Securing lower-carbon copper supports that narrative.

But there's also scrutiny of mining operations broadly. Mining creates environmental damage, water stress, and impacts on indigenous communities and local ecosystems. Some ESG advocates argue that tech companies pursuing AI growth through mining partnerships are externalizing environmental costs.

AWS has tried to balance this by emphasizing Nuton's lower environmental impact. But the reality is nuanced. The mine still operates. It still uses land, water, and energy. It still has impacts.

From an ESG perspective, the Rio Tinto deal signals that AWS takes supply chain sustainability seriously. It's not the perfect solution, but it's better than ignoring the issue or sourcing copper from mines with worse environmental records.

Investors and ESG evaluators will likely reward AWS for this partnership while still pushing the company to continue improving. The bar for corporate sustainability keeps rising. Today's innovative solution becomes tomorrow's minimum requirement.

For Rio Tinto, the partnership helps defend mining against ESG criticism. If the company can demonstrate that its copper is being bought by a major sustainability-focused tech company for lower-carbon reasons, it strengthens the company's ESG positioning. It's mutually beneficial for both companies to highlight the environmental benefits of their partnership.

The Broader Industrial Implications

Beyond AWS and Rio Tinto, this partnership signals a broader transformation in how tech and resource companies relate.

For decades, tech companies have focused on digital innovation while outsourcing material production to traditional industries. That separation is eroding. As tech infrastructure becomes increasingly critical to economic activity, and as material constraints emerge, tech companies are engaging upstream.

AWS investing in mining optimization, Microsoft potentially securing rare earth supply, Google partnering with renewable energy projects. These aren't traditional tech company activities. But they're becoming necessary as infrastructure scaling requires secure material sources.

Similarly, resource companies are becoming more tech-sophisticated. Rio Tinto, BHP, Glencore, and other major mining companies are investing heavily in AI, robotics, and advanced analytics. The old model of mining company as industrial operator is evolving toward mining company as technology-enabled operation.

This convergence has competitive implications. Mining companies that don't adopt technology will become less efficient and less attractive to customers like AWS. Tech companies that don't secure material supply will face constraints scaling infrastructure. The winners will be the companies that integrate both capabilities effectively.

For governments and policymakers, this trend raises questions about strategic autonomy. If US tech companies are dependent on foreign mining companies for critical materials, do we have sufficient domestic capability? The Rio Tinto deal helps, but it's one company, one mine. Broader supply chain resilience might require more aggressive domestic mining development or international partnerships with aligned governments.

It's a complex policy question that's getting more urgent as AI infrastructure buildout accelerates.

What This Means for You as a Developer or IT Professional

If you work in infrastructure, data centers, or cloud operations, the copper supply story affects you more than you might realize.

First, it explains why your company might face increased infrastructure costs over the next few years. Copper prices are likely to rise, which increases data center construction costs. If you're planning major infrastructure expansions, the math gets harder as material costs increase.

Second, it signals that infrastructure supply chain resilience is becoming strategic competitive advantage. Companies that secure material supply early will have cost and capacity advantages. This might translate to better infrastructure services and pricing for their customers.

Third, it suggests that data center location decisions might shift over time. If your company is evaluating new office locations or infrastructure hubs, proximity to reliable electricity, cooling, and increasingly, material supply, all matter. Phoenix and Arizona might become more attractive data center hubs if copper proximity becomes a factor.

Finally, it highlights that infrastructure sustainability is real and complex. The Rio Tinto partnership shows that major companies are thinking about carbon footprint in material sourcing. But it also shows the compromises involved: getting lower-carbon copper while still accepting real mining impacts. Understanding these trade-offs helps you evaluate corporate sustainability claims more critically.

For your career, recognizing that infrastructure increasingly touches upstream supply chains might open interesting opportunities. Infrastructure planning, supply chain optimization, and material sourcing are becoming more technology-focused and strategic.

FAQ

What is copper's role in data center infrastructure?

Copper is the foundational material for electrical distribution in hyperscale data centers. It's used in main distribution feeds from substations, power cables connecting servers, transformers stepping down voltage, cooling systems, and countless smaller connections throughout the facility. Copper's superior electrical and thermal conductivity, combined with its durability and cost-effectiveness compared to alternatives like silver or aluminum, make it irreplaceable for data center power infrastructure at current scales and costs.

How much copper does a single large data center consume?

A large hyperscale data center pulling 100-200+ megawatts of power typically requires 5,000 to 30,000 metric tonnes of copper, depending on facility size, design architecture, and cooling systems. This figure encompasses main distribution cables, sub-distribution infrastructure, cooling systems, and all the power-related components throughout the facility. AWS's 30,000-tonne commitment from Rio Tinto covers approximately one to four large data centers, illustrating just how constrained the supply currently is relative to buildout demand.

What makes Rio Tinto's Nuton technology different from conventional copper mining?

Nuton uses naturally occurring microorganisms to biologically extract copper from primary sulfide ores, rather than relying on energy-intensive smelting and refining. The process produces 99.99% pure copper cathode at the mine site, reducing reliance on distant smelters and refineries. Rio Tinto claims Nuton uses significantly less water and generates lower carbon emissions compared to traditional concentration-based smelting routes, though only about half of the AWS supply deal actually relies on Nuton technology, with the remainder coming from conventional leaching methods.

Why does AWS care about domestic copper supply instead of buying on the global market?

Domestic supply provides three strategic advantages: supply concentration risk reduction (the US is less vulnerable to disruptions in Chile, Peru, or other major copper producers), geopolitical independence (the company reduces reliance on imports from countries with uncertain trade relationships), and price certainty through long-term contracts rather than volatile global spot markets. Additionally, securing lower-carbon copper through Rio Tinto supports AWS's Climate Pledge commitment to reach net-zero emissions by 2040, which is increasingly important for corporate competitive positioning.

How does this copper deal affect AWS's climate commitments?

The partnership allows AWS to source some copper from lower-carbon production methods, which reduces the carbon intensity of data center construction. However, it represents a partial solution rather than a complete answer. Only about half of the 30,000-tonne commitment comes from Nuton's lower-carbon process, and even that is lower-carbon, not zero-carbon. Meanwhile, AWS is rapidly expanding data center footprint to support AI workloads, so total copper consumption and associated emissions will still rise despite improved sourcing.

What are the water implications of mining in Arizona?

Arizona faces severe water scarcity due to Colorado River depletion and ongoing drought conditions. Rio Tinto's Nuton process reportedly uses 70-90% less water than traditional copper smelting, which is significant in a water-constrained region. However, mining itself still consumes water for dust suppression and heap management. The partnership represents an optimization within constraints—getting the most water-efficient copper supply possible—rather than eliminating the water impact entirely. This tension highlights the reality that even innovative mining still creates environmental trade-offs.

Why can't tech companies simply use alternative materials instead of copper?

Copper has no viable substitute for large-scale data center power infrastructure. Aluminum costs more to use in larger quantities due to lower conductivity, silver is prohibitively expensive, and fiber optics can't carry electrical power. Superconductors could theoretically reduce copper needs but are decades away from practical commercial deployment. The physics and economics of materials science mean that copper remains the only practical choice for data center electrical infrastructure, making secure supply a genuine bottleneck rather than a problem that innovation can quickly solve.

What happens if copper supply continues to tighten?

Increasing copper scarcity would likely drive prices higher, increase data center construction costs, and potentially create allocation challenges for companies without long-term supply contracts. This could accelerate vertical integration, with more tech companies pursuing direct partnerships with mining companies and potentially investing in mining operations themselves. Data center siting decisions might shift toward locations near copper supply. Global AI infrastructure buildout could slow if copper becomes a true bottleneck rather than just an expensive constraint, though this depends on whether mining companies can expand capacity sufficiently.

How does this partnership affect competition between AWS, Microsoft, and Google?

AWS securing long-term copper supply with Rio Tinto provides a competitive advantage in cost certainty, infrastructure expansion speed, and potentially pricing for infrastructure services. If Microsoft and Google don't secure equivalent supply agreements, they face vulnerability to copper price spikes and potential constraints expanding data center capacity. This creates incentive for all hyperscalers to pursue similar partnerships. The company that best secures strategic material supply while also managing costs will have operational advantages that compound over time.

Could this deal influence where tech companies build data centers?

Potentially, yes. Historically, data center locations were decided based on electricity cost, cooling availability, and fiber connectivity. If copper becomes increasingly constrained, geographic proximity to copper supply could become an additional factor. Arizona and regions with copper mining proximity might become more attractive for data center siting. This could accelerate infrastructure development in some regions while slowing it in others, potentially reshaping the geographic distribution of AI infrastructure over the next decade.

Key Takeaways

-

AWS's Rio Tinto copper partnership addresses a real infrastructure constraint: data center power systems require massive amounts of copper, and US mining capacity has been dormant for years, creating supply vulnerability.

-

The 30,000-tonne agreement covers only 1-4 large data centers depending on their size, illustrating how constrained copper supply is relative to hyperscaler buildout ambitions.

-

Rio Tinto's Nuton bioleaching technology genuinely reduces water usage and carbon emissions compared to traditional smelting, but only about half the deal relies on this lower-carbon method, the other half uses conventional leaching.

-

AWS is balancing competing pressures: it wants to scale AI infrastructure aggressively, maintain Climate Pledge commitments, and secure material supply resilience. The Rio Tinto deal threads this needle partially but doesn't fully resolve the tensions.

-

This partnership signals a broader trend of tech companies engaging upstream in supply chains, becoming more vertically integrated and less reliant on pure outsourcing. Mining companies are simultaneously adopting technology capabilities. The convergence will reshape both industries.

-

Copper supply is likely to be tight for the next decade as AI data center buildout accelerates and competing demand from renewable energy, electric vehicles, and construction all increase. Prices will likely rise, and companies without secured supply could face constraints.

-

The precedent of this deal will likely inspire similar partnerships between tech companies and mining firms globally. This is the beginning of a broader transformation in how infrastructure supply chains organize.

Related Articles

- Trump and Governors Push Tech Giants to Fund Power Plants for AI [2025]

- AI Data Center Infrastructure Upgrades: The Engineering Boom [2025]

- Taiwan's $250B US Semiconductor Deal Reshapes Global Supply Chains [2025]

- Prebiotics for Copper Mines: How One Startup is Solving a Critical Shortage [2025]

- Copper Shortage Crisis: How Electrification Is Straining Global Supply [2025]

- Microsoft's $0 Power Cost Pledge: What It Means for AI Infrastructure [2025]