![Bending Spoons: The Stealth Tech Giant Acquiring Eventbrite [2025]](https://tryrunable.com/blog/bending-spoons-the-stealth-tech-giant-acquiring-eventbrite-2/image-1-1769359098378.jpg)

Bending Spoons: The Stealth Tech Giant Acquiring Eventbrite and Reshaping Digital Products [2025]

You've probably used a Bending Spoons product without knowing it. Chances are you've swiped through photos enhanced by Remini, saved notes in Evernote, attended an event through Meetup, or shared files via WeTransfer. Yet ask most people what Bending Spoons is, and you'll get blank stares.

That's precisely the point. While other tech conglomerates trumpet their acquisitions and brand synergies on earnings calls, Bending Spoons operates in the shadows, quietly amassing one of the most impressive digital product portfolios in existence. In December 2024, the Milan-based company announced it would acquire Eventbrite for

This isn't private equity in the traditional sense. Bending Spoons doesn't flip companies or milk them for dividends. It doesn't create financial engineering masterpieces or strip assets. Instead, it's built something far more ambitious: a tech operating system for digital products. The company acquires underperforming but beloved internet properties, strips away bloat, cuts unnecessary costs, and optimizes them to serve users more efficiently. Sometimes this means layoffs. Sometimes it means controversial product changes. Sometimes it means converting freemium offerings into paid tiers. And sometimes it creates genuine value for users and creators.

After 12 years of acquisitions, Bending Spoons serves over a billion people across its portfolio. More than 300 million monthly active users rely on its products. It employs roughly 400-500 people (internally called "Spooners") to manage a collection of products that, on paper, should require ten times that headcount. The company has never sold a business. It claims it aims to hold forever.

This is the story of how a startup born from the ashes of a failed photo app became one of tech's most prolific acquirers and one of its most divisive forces. Here's what you need to know.

TL; DR

- Bending Spoons serves over 1 billion people across products like Meetup, Evernote, WeTransfer, and Eventbrite, yet remains largely unknown to the general public

- **The company acquired Eventbrite for 1.38B), Brightcove, and AOL

- It operates on an efficiency-focused model, acquiring mature but stagnant products and reorganizing them for profitability through cost cuts, team restructuring, and monetization changes

- Significant layoffs follow most acquisitions, with entire teams eliminated—raising ethical questions while also potentially improving product performance

- The business model works, with the company holding forever and never selling acquired businesses, creating a living digital product portfolio worth billions

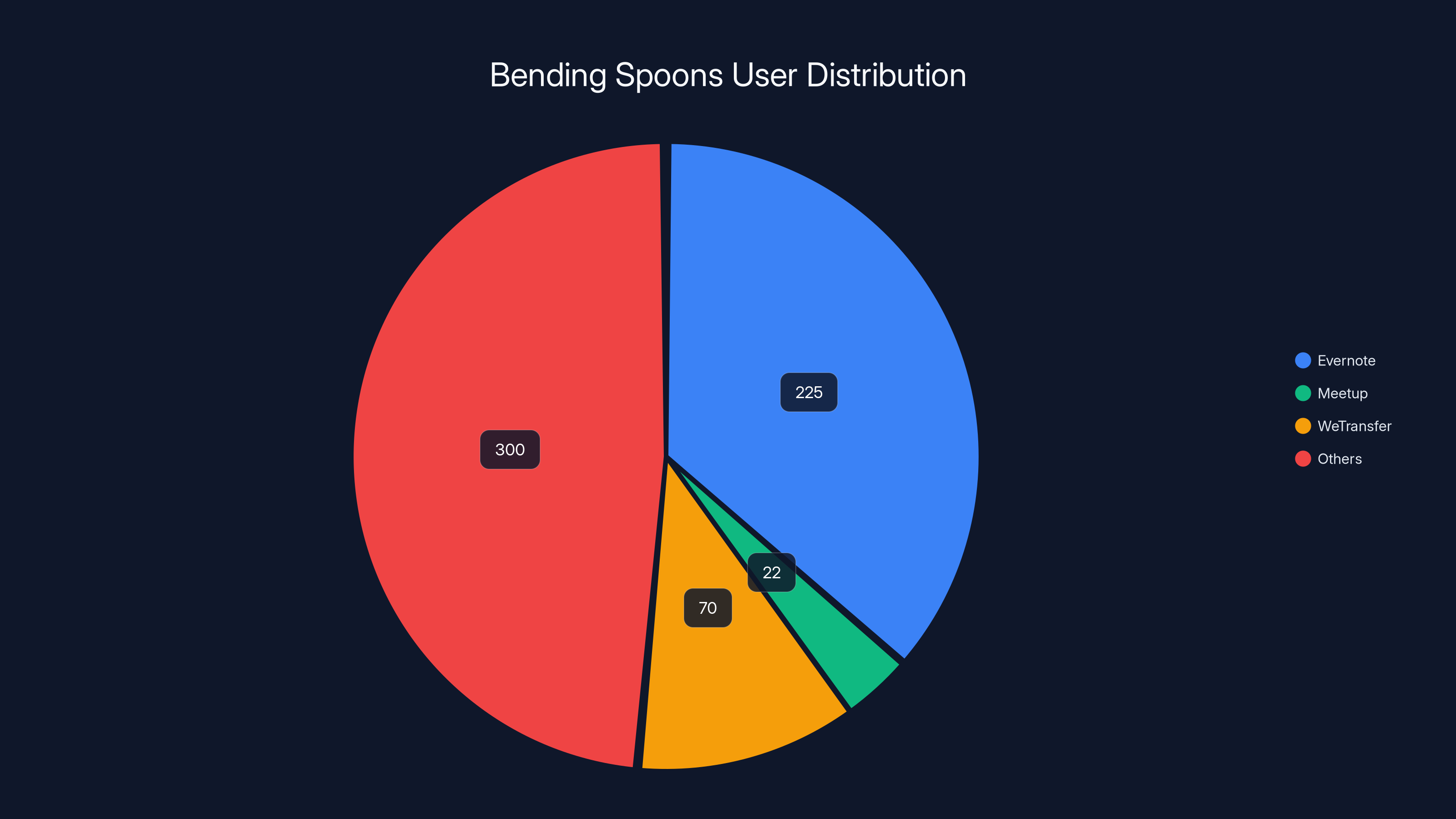

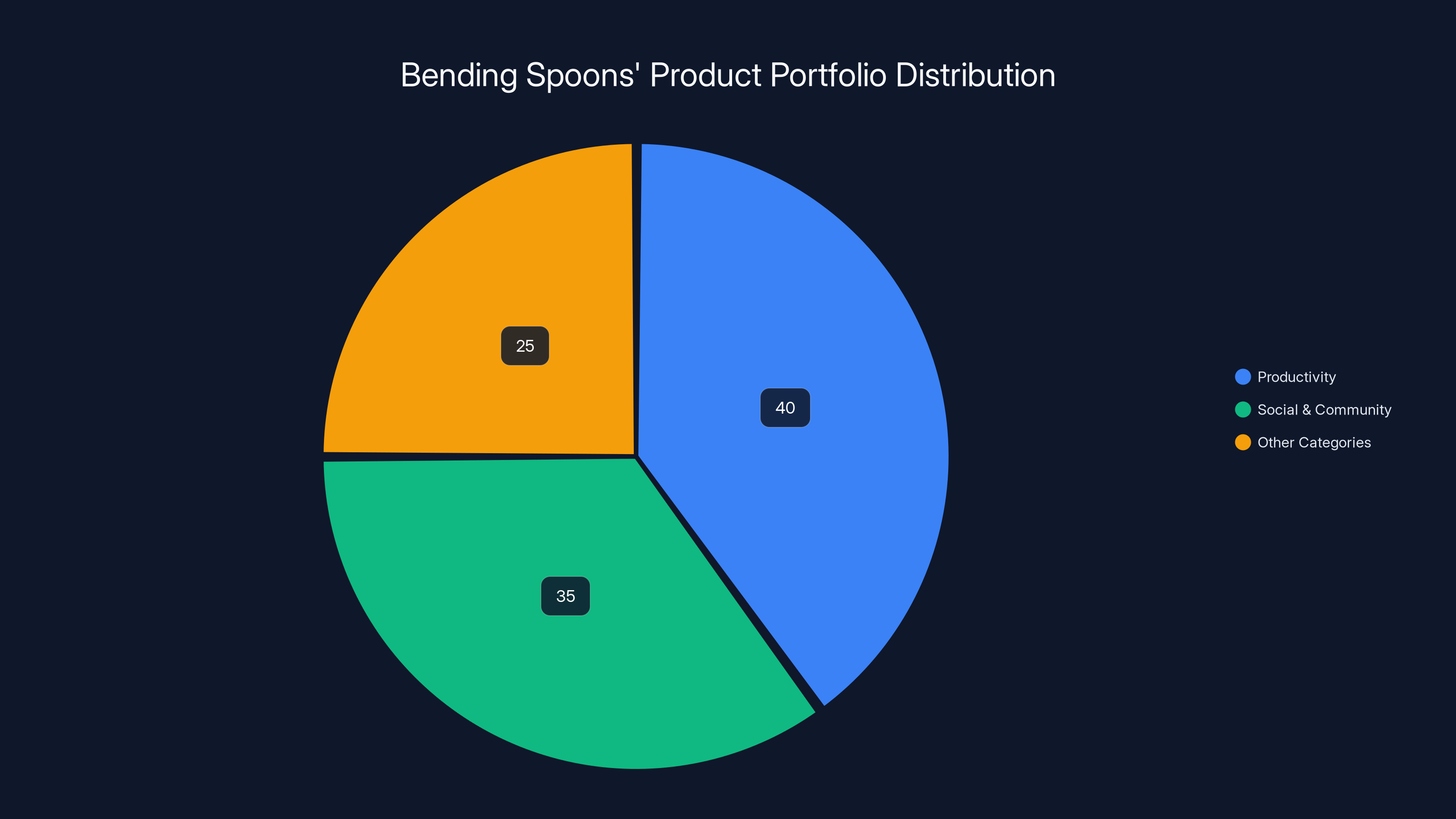

Bending Spoons' portfolio includes major platforms like Evernote, Meetup, and WeTransfer, with a significant portion of users spread across other products. Estimated data.

What Exactly Is Bending Spoons?

Bending Spoons is a digital product holding company that acquires, reorganizes, and optimizes established internet businesses. Unlike traditional venture capital, which funds startups and seeks exits through IPOs or acquisitions, or traditional private equity, which extracts value through leverage and operational improvements before selling, Bending Spoons operates with a simpler philosophy: buy good products that have stagnated, make them more efficient, and hold them indefinitely.

The company's core belief is that many successful digital products reach a plateau where their original founders or owners lose interest, resources become misallocated, or organizational bloat obscures the product's potential. Bending Spoons identifies these opportunities and moves in. What follows is aggressive restructuring: cost analysis, team reorganization, feature prioritization, and new monetization strategies.

The numbers tell the story. With 400-500 employees managing a portfolio that includes Meetup (22 million monthly active users), Evernote (225+ million downloads), WeTransfer (70 million monthly active users), Brightcove (a multi-billion-dollar video platform), and dozens of others, the company operates at a scale that would require thousands of workers at traditional tech companies. This efficiency isn't an accident. It's baked into Bending Spoons' DNA.

The company's approach also differs fundamentally in patience. In 2020, Bending Spoons created and donated Immuni, Italy's official COVID-19 contact-tracing app, a non-profit project that demonstrated the company's willingness to deploy resources for purposes beyond immediate profit. This contrasts sharply with the stereotype of startup acquisitions, where purchased teams are typically folded into acquirer infrastructure and original products are killed or neglected.

Instead, Bending Spoons maintains acquired products as independent entities, each with its own user base and revenue streams. The holding company provides financial backing, operational guidance, and strategic direction, but acquired products retain their brand identity and user experiences. This hands-off-ish approach paradoxically coexists with very hands-on restructuring after acquisition, creating a sometimes-confusing brand strategy.

The company is led by CEO and co-founder Luca Ferrari, who rarely gives interviews. In a rare appearance on the podcast 20VC, Ferrari explained that Bending Spoons was born from the ashes of a failed startup called Evertale, which had built a photo-sharing app called Wink. When Evertale failed around 2012, Ferrari and a handful of employees stayed together, initially building their own apps. They made their first acquisition in 2014 and have been acquiring ever since. What started as a small team trying to salvage something from failure has grown into one of tech's most prolific buyers.

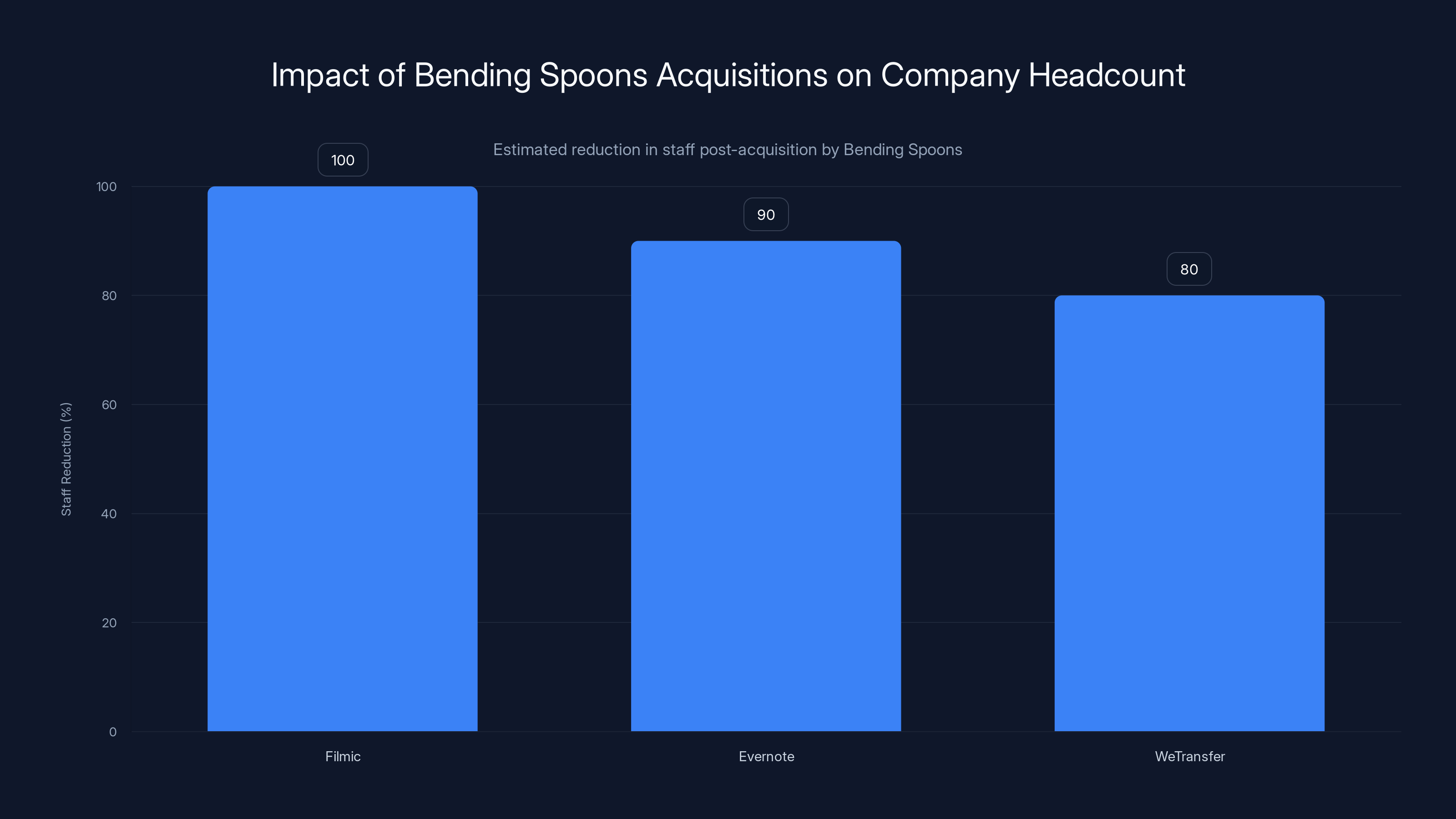

Bending Spoons significantly reduces staff in acquired companies, with Filmic seeing a 100% reduction, Evernote 90%, and WeTransfer 80%. Estimated data.

The Origin Story: From Evertale's Ashes

Every successful company has an origin story, and Bending Spoons' is more interesting than most. It begins not with a brilliant idea pitched to venture capitalists, but with the wreckage of a failed startup and the determination of its founders to keep working together despite that failure.

Evertale was a Copenhagen-based startup founded in the early 2010s. The company built Wink, a photo-sharing app, and raised seed funding to grow it. It even participated in Tech Crunch Disrupt SF 2011's Startup Alley, which gave it a modest amount of visibility and credibility in startup circles. But Wink never achieved traction. The photo-sharing space was already crowded with Instagram, which had launched in October 2010 and was growing explosively. Evertale couldn't compete.

The company failed, and its investors exited. Most teams would have dispersed. Founders would have moved to other startups. Employees would have joined larger companies. But Ferrari and his co-founders made a different choice: they stayed together and kept working.

Instead of trying to build the next great photo app or social network, they pivoted to something that would ultimately prove far more valuable: acquiring and improving existing digital products. This shift in thinking—from "how do we build something new" to "how do we make existing things better"—became the foundation of Bending Spoons' entire business model.

The team started by building apps in-house, trying to iterate on products they thought could succeed. But somewhere around 2013-2014, they began acquiring struggling digital properties. Their first acquisitions were relatively small, but each one taught them lessons about cost structure, user retention, and monetization. By 2022-2023, they had enough capital and operational expertise to start acquiring recognizable brands like Evernote.

What's remarkable about Bending Spoons' origin is that it wasn't premeditated. The company didn't launch with a master plan to become a digital product conglomerate. Instead, Ferrari and his team discovered an arbitrage opportunity: digital products that were losing money, neglected by their owners, or mismanaged could be purchased relatively cheaply, restructured by a lean team, and turned profitable. This discovery became a repeatable system.

In a 2023 interview, Ferrari described the philosophy simply: Bending Spoons acquires companies that have reached "their limits" but still have substantial user bases and potential. The previous owners might be founders who built something successful but tired of running it. They might be public companies like Yahoo, which held assets like AOL that didn't fit their core strategy. Or they might be well-funded startups that somehow lost their way.

The key insight is that Bending Spoons doesn't need to build products from scratch. Millions of people already use these products. The challenge isn't acquiring users—it's making those products valuable to both users and the company owning them. That requires a specific operational philosophy.

The Acquisition Strategy: How Bending Spoons Picks Its Targets

Bending Spoons acquires at scale. Since 2014, the company has purchased or taken stakes in dozens of digital products. This isn't random. The company has developed a clear acquisition thesis over 12 years of buying businesses.

First, the target must have an established user base. Bending Spoons isn't interested in early-stage startups with 100,000 users and dreams of growth. It's interested in products with millions of users, significant monthly active user counts, and real revenue. When Bending Spoons acquired Meetup, the platform already had 22 million monthly active users. When it acquired Evernote, the product had over 200 million downloads. These aren't startup plays—they're mature products with proven market product-market fit.

Second, the product should have reached a plateau or decline. The previous owner might have built something successful, but that success has plateaued. Revenue might be flat. User growth might have stalled. Product development might have become glacial. The owner might be focused on other priorities. These conditions create acquisition opportunities because the previous owner might be willing to sell at a discount to what the product could theoretically be worth.

Third, Bending Spoons must believe it can improve the product's economics. This might mean cutting costs by eliminating redundant teams, consolidating infrastructure, or closing unprofitable features. It might mean changing the monetization model—converting a freemium product to a paid-only product, for example. It might mean improving the user experience to increase retention. Or it might mean expanding the product into new markets or use cases. Whatever the specific lever, Bending Spoons must believe it can make the product more valuable and profitable than it currently is.

Fourth, the product's brand must be salvageable. Bending Spoons doesn't want to buy bankrupt companies or products so damaged that users have lost trust. It wants products that users still love, even if those users feel neglected by the current owner. This is why many of Bending Spoons' acquisitions generate controversy—the company inherits a beloved product with a loyal user base, then makes changes that those users dislike.

Looking at the acquisition timeline, several patterns emerge. In 2014-2021, Bending Spoons made acquisitions but remained relatively quiet. In 2022-2023, the pace accelerated dramatically. In 2024, acquisitions happened at breakneck speed. This acceleration suggests either that Bending Spoons obtained significant new capital (either from new investors or reinvested profits from earlier acquisitions) or that the company became more confident in its operational model.

The move into larger acquisitions is notable. Acquiring a 2-million-user app is fundamentally different from acquiring Evernote with 225 million downloads, or Meetup with 22 million monthly active users, or WeTransfer with 70 million monthly active users. Managing products at this scale requires different operational muscles. Yet Bending Spoons has demonstrated the ability to manage both small and large acquisitions simultaneously.

The company's most recent acquisitions—Eventbrite (

Yet Bending Spoons absorbed them all into its portfolio, presumably believing it could improve their operations and profitability despite their scale.

Bending Spoons prioritizes acquiring products with an established user base and potential for economic improvement. Estimated data based on acquisition strategy insights.

The Portfolio: What Bending Spoons Actually Owns

Understanding Bending Spoons requires understanding its portfolio. The company owns dozens of products across dozens of categories, serving different user bases and business models. This diversity is strategic—it allows Bending Spoons to spread risk and find synergies across different product types.

Productivity and Collaboration Products

Evernote is Bending Spoons' most famous productivity acquisition. The note-taking app was founded in 2000 and had reached a $1 billion valuation at its peak. By the time Bending Spoons acquired it in 2022-2023, the product had been stagnant for years. The app felt bloated. Product development had slowed. The free tier was generous but unprofitable. User sentiment had turned mixed—people loved the product's core functionality but felt abandoned by its owner.

Bending Spoons immediately restructured Evernote. The company cut staff, reduced the free tier's functionality (limiting users to just two devices instead of unlimited access), and refocused the product on core use cases. The moves were controversial. Long-time users complained about the free tier restrictions. Articles about the acquisition flooded tech news sites. But Bending Spoons' thesis was clear: a more profitable Evernote, even with fewer free users, was better than a money-losing Evernote.

Harvest, acquired in 2025, is another productivity play. The time-tracking and invoicing software serves freelancers and agencies. Like Evernote, Harvest had been successful but was showing signs of stagnation. Bending Spoons acquired it to consolidate with other productivity tools and presumably to rationalize its cost structure.

Social and Community Products

Meetup is perhaps Bending Spoons' most important acquisition. The platform, acquired in early 2024, facilitates in-person social gatherings across thousands of communities. With 22 million monthly active users, Meetup is one of the largest community platforms on the internet. The acquisition price wasn't disclosed, but estimates ranged from $200-300 million.

Meetup had been owned by WeWork parent The We Company (formerly WeWork), which had acquired it for $196 million in 2017. WeWork's implosion in 2019 left Meetup orphaned within a conglomerate focused on office real estate. For years, Meetup was neglected, receiving minimal investment or product development. The platform still worked, users still organized and attended events, but the product felt stuck in time.

Bending Spoons immediately began restructuring Meetup. The company consolidated its infrastructure, cut staff, and introduced new monetization features. Users began seeing changes almost immediately—not all of them positive. But Bending Spoons' bet was that Meetup's core value proposition (helping people find and organize events) was strong enough to survive restructuring and emerge more profitable.

File Transfer and Sharing Products

WeTransfer is one of Bending Spoons' most controversial acquisitions. The file-sharing service, founded by Dutch entrepreneurs Nalden and Rinse, was built on a philosophy of simplicity and generosity. You could send up to 2GB of files for free, no registration required. The service was beloved by creatives, designers, and professionals who valued its elegant user experience.

Bending Spoons acquired WeTransfer in July 2024 for a reported $205 million. Within months, the company began making changes: stricter limits on the free tier, new paid tiers, and eventual staff reductions. The changes triggered a backlash. Founder Nalden publicly criticized the acquisition in December 2025, announcing he was building a new file transfer service to replace WeTransfer.

This is the Bending Spoons paradox: the company acquires beloved products but then changes them in ways that alienate users. WeTransfer was profitable and sustainable as designed. Bending Spoons believed it could be more profitable with restrictions and paid tiers. Whether that's true depends on how many users stick around after the changes.

Creative and Media Products

Filmic, a maker of professional video and photo editing apps, was acquired in 2022. In December 2023, Bending Spoons laid off Filmic's entire staff while maintaining the apps themselves. This move—keeping the product but eliminating the team—became a template for future acquisitions. If you can keep a product running with minimal ongoing development, why pay for a full team?

Remini, an AI-powered photo enhancement app, was acquired earlier in Bending Spoons' history. The app has become one of the most successful products in the portfolio, with hundreds of millions of users. This suggests that not all Bending Spoons acquisitions turn into cautionary tales. Some actually become valuable, growing businesses.

Issuu, a publishing platform acquired in July 2024, serves millions of creators and publishers. The platform allows anyone to publish interactive documents online. It's a niche product in some respects, but a lucrative one for the creators who use it.

Video and Broadcasting Products

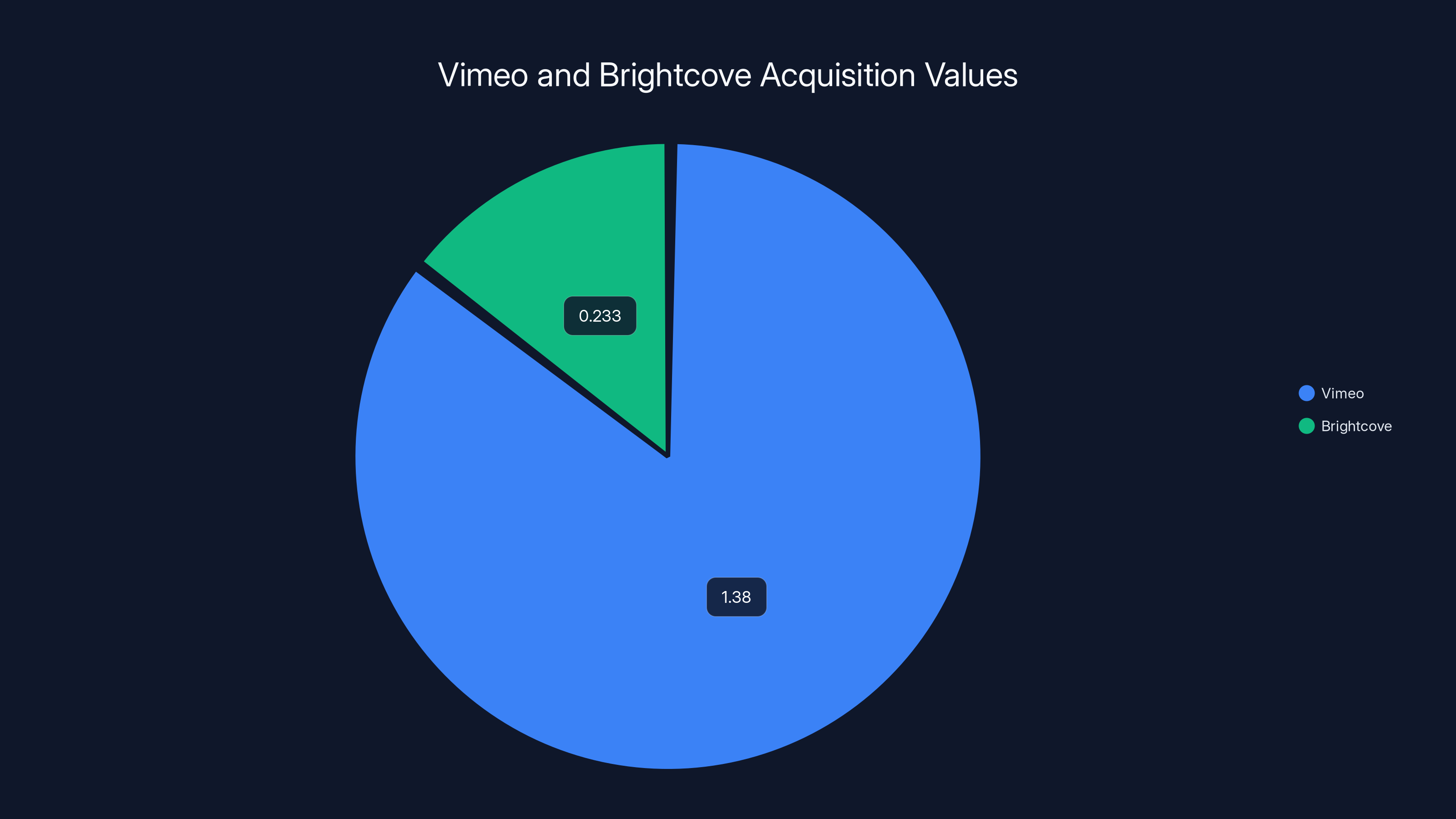

Brightcove, acquired in November 2024 for $233 million in an all-cash deal, is a professional video platform used by thousands of enterprises. The acquisition was significant because Brightcove is a multi-billion-dollar company by revenue. It serves corporations, media companies, and large content creators.

Vimeo, which Bending Spoons announced it would acquire for $1.38 billion in 2025, is an even larger prize. Vimeo is a public company (it's traded on Nasdaq) with hundreds of millions in annual revenue. It serves both individual creators and enterprises. The acquisition signals that Bending Spoons is now playing at the public-company acquisition level.

Events and Ticketing

Eventbrite, acquired for $500 million in December 2024, is the world's largest ticketing platform. The company facilitates billions of dollars in ticket sales annually. It's where most people buy concert tickets, event tickets, and conference passes. The acquisition makes Bending Spoons a controlling interest in a critical piece of internet infrastructure.

Eventbrite was a public company before the acquisition. It's still a public company, but Bending Spoons now owns it. This matters because it signals that Bending Spoons is willing to take companies private and re-optimize them for profitability rather than public market performance.

Other Notable Products

StreamYard, acquired in early 2024, is a live streaming platform. Komoot, acquired in 2025, is a hiking and cycling app with millions of outdoor enthusiasts. These acquisitions highlight the breadth of Bending Spoons' thesis—essentially any digital product with an established user base and sub-optimal margins is a potential target.

The portfolio's diversity is striking. Bending Spoons isn't building a vertical stack or creating a coherent platform. It's not trying to achieve synergies through integration like typical conglomerates. Instead, it's collecting digital properties like a collector might gather art—each piece valuable in its own right, but the real value in the collection itself.

The Operational Model: How Bending Spoons Runs Acquired Companies

Bending Spoons' operational model is the key to understanding the company. It's not what the company acquires that matters most—it's how the company runs acquired businesses afterward.

The model can be summarized in a few principles: cost rationalization, team consolidation, product focus, and new monetization strategies.

Cost Rationalization

Every acquired company arrives with inherited costs. There might be redundant teams, unnecessary tools, inefficient infrastructure, or bloated headcount. Bending Spoons' first task is to analyze these costs and eliminate waste.

This often means layoffs. In many cases, it means substantial layoffs. When Bending Spoons acquired Filmic, it laid off the entire team but kept the apps running. When it acquired Evernote, it cut staff significantly. When it acquired WeTransfer, it reduced headcount. These decisions generate headlines and criticism, but they're central to how Bending Spoons improves profitability.

The company's philosophy appears to be that many digital products require far fewer people to maintain and improve than companies typically employ. If Evernote was employing, say, 300 people before acquisition, Bending Spoons might believe that the product could be maintained and incrementally improved by 30 people. That's a 90% cost reduction, which transforms economics.

This isn't universally applicable. Products in active development or rapid growth need larger teams. But for mature, stable products that have reached a plateau, smaller teams might actually be sufficient.

Product Focus and Rationalization

Acquired products often contain features that don't contribute meaningfully to user value or revenue. Bending Spoons analyzes what users actually use and what drives engagement, then ruthlessly prioritizes.

Evernote's free tier restructuring is an example. The original free tier allowed unlimited devices and unlimited note creation. Bending Spoons' new free tier limits users to two devices. This change is annoying for users, but it's designed to drive conversions to paid tiers. By restricting the free tier, Bending Spoons makes it more likely that users who want to use Evernote across multiple devices will upgrade.

WeTransfer's free tier changes followed a similar pattern. By restricting free file sizes and transfer speeds, Bending Spoons made paid tiers more attractive.

This is a core tension in Bending Spoons' model: the company improves profitability by reducing free offerings, but this often frustrates long-time users who valued the original generosity.

Monetization Redesign

Bending Spoons looks at how each acquired product makes money and asks whether the approach is optimal. This might mean introducing paid tiers where none existed. It might mean eliminating features from free tiers. It might mean increasing prices. It might mean moving to a usage-based pricing model instead of a subscription model.

The goal is to maximize lifetime value per user while maintaining sufficient users to sustain the business. There's a balance—if you monetize too aggressively, users leave. But if you're too generous with free access, the business becomes unprofitable.

Infrastructure Consolidation

When Bending Spoons acquires multiple products, there are inevitable infrastructure synergies. If you own both Evernote and Harvest, you might consolidate their cloud infrastructure. If you own multiple apps, you might consolidate authentication systems, data analytics, or customer support.

These consolidations can reduce costs and improve reliability. They can also enable knowledge-sharing and best practices across the portfolio. But they also risk introducing single points of failure and losing product-specific optimizations.

Maintaining Product Independence

Despite consolidations, Bending Spoons maintains acquired products as independent entities. Evernote remains Evernote. Meetup remains Meetup. WeTransfer remains WeTransfer. This is different from many acquisitions, where the acquired product is folded into the acquirer's brand.

Maintaining independence makes sense strategically. The products have established brands and loyal user bases. Merging them into a Bending Spoons brand would alienate users and waste the value of the original acquisition. It also allows each product to serve specific use cases and communities without being diluted by merger with other products.

But it also requires operational sophistication. Managing dozens of independent brands, each with their own users and businesses models, requires different operational muscles than managing a single unified product.

Estimated data shows that productivity and social/community products make up the majority of Bending Spoons' portfolio, reflecting their strategic focus on diverse user bases.

The Controversial Side: Layoffs, Product Changes, and User Backlash

Bending Spoons' operational model generates controversy. This is inevitable when you restructure beloved products and eliminate entire teams.

When Bending Spoons acquired Evernote, users immediately noticed the free tier restrictions. The reaction was mixed. Some users had been waiting for the company to improve (they felt Evernote was neglected), but others felt the restrictions were heavy-handed. Long-time free users who had been using Evernote for a decade suddenly had to choose between paying $15/month or limiting themselves to two devices.

WeTransfer's changes generated similar backlash. Founder Nalden's December 2025 public criticism was significant. It signaled that the creator of the product disagreed with Bending Spoons' direction. This is a challenging position for Bending Spoons to navigate—you want to optimize a product, but if the creator publicly criticizes the changes, it calls into question whether the optimization is actually an improvement.

Filmic's acquisition and subsequent staffing elimination were controversial but noteworthy for a different reason: the company kept the products running without the team. This demonstrated that, in some cases, mature digital products don't require continuous active development. They can be maintained in a sort of "steady state" with minimal ongoing investment.

These controversies raise a genuine question: is Bending Spoons improving products or just extracting value from them? The answer probably depends on how you measure success.

The Efficiency Argument

Bending Spoons would argue that it's improving products by eliminating waste. A company that was losing money is now profitable. Users still have access to the product they love, but it's no longer subsidized by desperate venture capital. The product is sustainable long-term.

This argument has merit. Many venture-backed products burn massive amounts of money to acquire users while the business model remains uncertain. Bending Spoons often acquires after this period of profitless growth. By cutting costs and implementing sensible monetization, the company makes the product viable long-term.

Furthermore, Bending Spoons' claim that it never sells acquired businesses suggests a long-term commitment. If the company were just extracting value before selling, it would be behaving like private equity. Instead, by holding forever, Bending Spoons signals that it's making permanent improvements, not temporary optimizations.

The User Experience Argument

Users often argue that Bending Spoons' changes damage the products. Free tiers become restrictive. Ads proliferate. Features get removed. Interfaces change. These aren't improvements—they're downgrades disguised as operational optimization.

This argument also has merit. Product improvements shouldn't be measured solely by profitability. User happiness, retention, and satisfaction matter too. If Bending Spoons' changes increase profitability at the cost of user satisfaction, that's a trade-off, not an unambiguous improvement.

The Reality in the Middle

Most likely, the truth is somewhere in the middle. Some of Bending Spoons' changes are genuine improvements. Some are compromises. Some might be mistakes that the company learns from. Running digital products at scale is difficult. Balancing profitability with user satisfaction is the central challenge of the business.

What's clear is that Bending Spoons isn't hiding its philosophy. Users know the company is optimizing for profitability. They can choose to stick with the products if they believe Bending Spoons' version is still valuable, or leave if they think it's been degraded. That transparency is more than many acquirers offer.

Eventbrite Acquisition: A Case Study in Scale

The Eventbrite acquisition for $500 million represents a significant moment in Bending Spoons' history. It's the company's most ambitious acquisition yet in terms of the platform's importance to internet infrastructure.

Eventbrite is the world's largest ticketing platform. It's where you buy concert tickets, festival passes, conference registrations, and event access. The platform processes billions of dollars in ticket sales annually. It's integrated into thousands of venues, bands, conferences, and event organizers' workflows.

Before the Bending Spoons acquisition, Eventbrite was a public company. It had raised hundreds of millions from venture capital. It was traded on Nasdaq under the ticker symbol EB. Its valuation had fluctuated based on public market sentiment, but it was a recognized public company.

The acquisition de-listed Eventbrite from public markets and brought it under private ownership. This is significant. It means Bending Spoons' operational thesis—that publicly traded companies often prioritize short-term metrics over long-term value creation—is being tested on one of the internet's most important platforms.

The question is whether Bending Spoons can improve Eventbrite. The platform faces genuine challenges. Venue operators sometimes complain about Eventbrite's fees. Users sometimes complain about the interface. And there's always the competitive threat from other ticketing platforms like Ticketmaster.

Bending Spoons' approach would likely focus on cost optimization (reducing headcount, consolidating infrastructure) and monetization improvements (potentially increasing fees to venues or adding new revenue streams). The company would analyze what features drive the most value and ruthlessly prioritize around them.

If successful, Eventbrite under Bending Spoons could become more profitable while maintaining its user base. If unsuccessful, the platform could become degraded through cost-cutting while losing users to competitors. Both scenarios are possible.

The Eventbrite acquisition is also significant because it demonstrates Bending Spoons' ability to access capital at scale. Acquiring a public company for $500 million requires serious capital availability. This suggests that either Bending Spoons has raised new funding, or the company's earlier acquisitions have generated enough profits to self-fund new acquisitions.

The acquisition of Vimeo at

The Vimeo and Brightcove Acquisitions: Moving Into Billion-Dollar Deals

Bending Spoons' recent acquisitions of Vimeo (

Brightcove, valued at $233 million in an all-cash deal, is a professional video hosting and publishing platform. Thousands of enterprises use Brightcove to manage, host, and stream video content. The platform generates significant revenue, but it had stagnated. Growth had slowed. The company had become a classic "cash cow" generating profits but not exciting investors.

Bending Spoons' acquisition of Brightcove makes sense given its playbook. The platform has an established user base, clear revenue streams, and substantial profitability. Bending Spoons can acquire it and immediately begin optimizing costs while defending the revenue base.

Vimeo's acquisition is more ambitious. Vimeo is a public company (traded on Nasdaq under the ticker VMEO) with hundreds of millions in annual revenue. It's both a consumer platform (where creators host and share videos) and an enterprise platform (where businesses use Vimeo's tools). The company generates real revenue from millions of paid subscriptions.

The $1.38 billion acquisition price represents a significant bet. It suggests that Bending Spoons either has access to substantial capital (from new investors or accumulated profits) or is willing to take on debt to fund the acquisition. Either way, it signals confidence in the company's ability to operationalize a billion-dollar acquisition.

Why would Bending Spoons want Vimeo? Several reasons. First, the platform has a large, established user base—millions of creators and hundreds of thousands of paying subscribers. Second, Vimeo generates substantial revenue, which creates immediate profitability potential. Third, the company had become somewhat less focused under public market ownership. Bending Spoons believed it could improve Vimeo's operations.

But the Vimeo acquisition also tests Bending Spoons' model at its limits. Vimeo is a complex platform serving two different markets (creators and enterprises). It's not obvious how you "optimize" a company at this scale without damaging the product. Previous Bending Spoons acquisitions were smaller and simpler. Vimeo is neither.

AOL and the Yahoo Exit: Acquiring an Internet Legend

In a stunning move that shows how much Bending Spoons has evolved, the company announced it would acquire AOL from Yahoo. The acquisition price wasn't disclosed, but AOL—once the world's largest internet service provider and communication platform—is being absorbed into Bending Spoons' portfolio.

This acquisition is symbolic. AOL was founded in 1985 and was the gateway to the internet for millions of people. At its peak, AOL was worth nearly

Bending Spoons acquiring AOL signals that the company sees value in legacy internet properties that others have written off. AOL still has hundreds of millions of email accounts. It still provides email and web services to millions of people. It's not growing, but it's still functional and utilized.

The AOL acquisition also demonstrates Bending Spoons' ambition. Acquiring an internet legend, even one that's fallen on hard times, is a bold move. It shows the company isn't afraid of challenging acquisitions or complex legacy platforms.

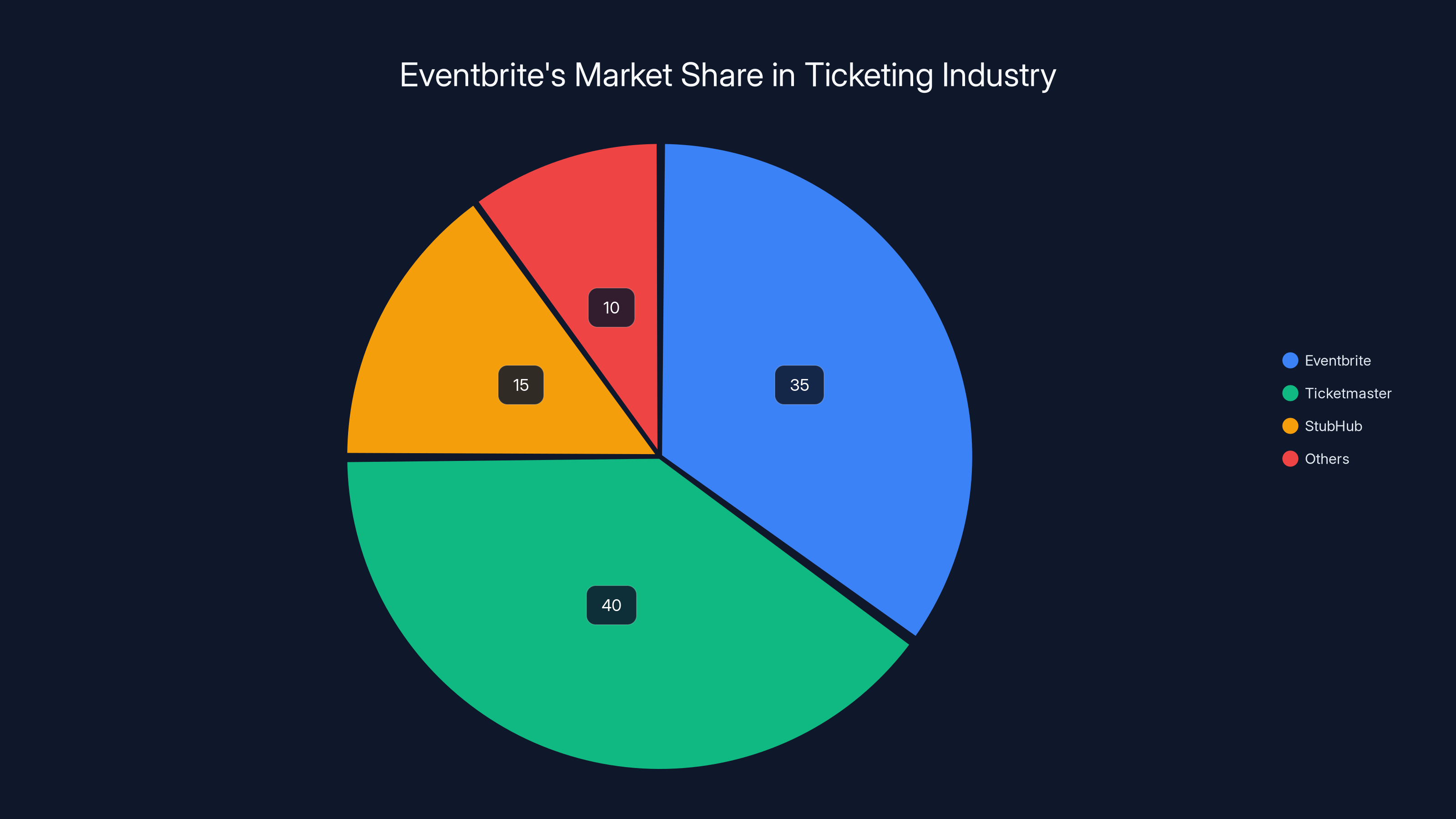

Eventbrite holds an estimated 35% market share in the ticketing industry, trailing behind Ticketmaster. Estimated data based on industry insights.

The Business Model and Profitability Question

How does Bending Spoons actually make money? And is the company actually profitable?

The business model is straightforward in theory. Bending Spoons acquires products, reorganizes them for profitability, and collects the earnings. Over time, as products become more profitable and new acquisitions are made, the overall portfolio's profitability should grow.

But several questions remain unanswered. How much profit does each acquired product generate? How much does Bending Spoons spend on infrastructure and corporate overhead? Are some products subsidizing others? Is the company as a whole profitable?

Bending Spoons is privately held and doesn't disclose financial information. So the true profitability picture remains opaque. The company claims it's sustainable and profitable, but without audited financials, investors and users have to take the company at its word.

What we can infer from Bending Spoons' behavior suggests profitability. The company continues to acquire new products, which requires either profitability from existing products or access to capital from investors. The acquisitions are increasingly large (Eventbrite, Vimeo, Brightcove), which requires serious financial resources. And the company claims never to have sold a business, which suggests that the portfolio is valuable enough to hold.

But profitability at the portfolio level doesn't mean every product is profitable. Some products might be loss-leaders that drive engagement with other products. Some might be acquisition candidates that Bending Spoons bought cheaply and is still optimizing. Some might be mature cash generators.

The Comparison to Traditional Private Equity

Bending Spoons is often compared to private equity firms, but there are significant differences.

Traditional private equity acquires companies, improves them (or sometimes just extracts value), and then sells them at a profit. The holding period is typically 5-10 years. The goal is to generate a return for investors. This requires eventually exiting the investment—either through a sale, IPO, or special dividend.

Bending Spoons claims a fundamentally different approach: buy and hold forever. The company never sells businesses. There's no exit strategy. The goal is to build a sustainable, profitable portfolio of digital properties that generates returns indefinitely.

This difference is significant. It changes incentives. In private equity, you might be tempted to cut costs aggressively to maximize the sale price, even if it damages the business long-term. But if you're holding forever, you have to care about the product's long-term sustainability.

Of course, this could also be a marketing narrative. Without seeing Bending Spoons' actual financial statements and acquisition agreements, it's impossible to verify that the company truly intends to hold forever. But the company's behavior is consistent with this philosophy—it doesn't exit acquisitions, and it maintains products as independent entities rather than consolidating them into a unified platform.

The comparison to traditional conglomerates is also instructive. Companies like Berkshire Hathaway or 3M buy diverse businesses and hold them as a portfolio. But these companies typically extract value through consolidation, shared services, and cross-selling. Bending Spoons maintains independence while consolidating infrastructure. That's a different model.

The Immuni Exception: Bending Spoons' Non-Profit Work

In 2020, Bending Spoons broke from its acquisition strategy to develop Immuni, Italy's official COVID-19 contact-tracing app. The company created the app, donated it to the Italian government, and made it available for free to all Italian citizens.

This project is significant because it demonstrates that Bending Spoons isn't purely profit-driven. The company allocated substantial resources to a public health project with no direct revenue generation. The app processed tens of millions of data points and served millions of Italian citizens.

The Immuni project also demonstrated Bending Spoons' technical capabilities. Building a national-scale contact-tracing app requires significant engineering talent and operational expertise. Bending Spoons successfully delivered.

But the project also revealed the challenges of building at scale. Contact-tracing apps faced adoption challenges across the world, including in Italy. Privacy concerns, technical barriers, and user skepticism limited Immuni's ultimate impact. The app was eventually discontinued as the COVID-19 emergency receded.

The Immuni experience suggests that Bending Spoons, for all its operational prowess, faces the same challenges that all tech companies face when trying to build new products or launch in new markets. The company's expertise in optimizing existing products doesn't automatically translate to building new ones successfully.

The Culture and Organization: How Bending Spoons Operates Internally

Bending Spoons employs approximately 400-500 people, whom the company calls "Spooners." This relatively small headcount for managing a portfolio of dozens of products worth billions of dollars is remarkable. It suggests either that Bending Spoons has achieved exceptional operational efficiency, or that the company relies heavily on automated systems and outsourced contractors.

The company is based in Milan, Italy, which gives it a different cultural perspective than Silicon Valley or other major tech hubs. Milan is known for fashion, design, and classical tradition—not necessarily for tech entrepreneurship. This location choice might influence how the company approaches product design and optimization.

Bending Spoons' culture appears to prioritize efficiency and pragmatism over growth at all costs or user delight at any price. The company makes difficult decisions about layoffs and cost-cutting relatively quickly. This suggests a different cultural orientation than many venture-backed companies, where growth and user expansion are paramount.

The company's rare public communications—primarily through CEO Luca Ferrari's occasional interviews—emphasize the long-term vision and commitment to the portfolio. Ferrari presents Bending Spoons as a company focused on sustainable, profitable businesses rather than rapid growth or trend-chasing.

This operational culture is both a strength and potential weakness. The strength is that Bending Spoons can make unpopular decisions quickly and execute them ruthlessly. The weakness is that this approach can alienate users and employees who value different priorities.

The Future: Where Is Bending Spoons Heading?

Basing predictions on limited public information is always risky, but several things seem clear about Bending Spoons' future direction.

First, acquisitions will continue. The company has demonstrated that it can acquire at scale and operationalize large, complex products. The portfolio will likely grow to 50+ products, if it hasn't already. Bending Spoons will likely acquire other large, established digital properties.

Second, monetization will remain a priority. As Bending Spoons optimizes existing products, the next frontier is generating more revenue from users. This might mean more aggressive pricing, fewer free users, or new revenue streams like advertising or partner programs.

Third, infrastructure consolidation will continue. As the portfolio grows, the company will likely find more opportunities to consolidate infrastructure, share engineering resources, and reduce costs. This might eventually lead to some products sharing code or services, which could improve reliability and efficiency.

Fourth, the company might eventually seek outside capital or investors. If Bending Spoons wants to acquire even larger products (think: Slack, Notion, or other major platforms), it might need to access capital markets. This could mean raising a large institutional fund, accepting outside investors, or even potentially going public.

Fifth, Bending Spoons might eventually face regulatory scrutiny. As the company accumulates more digital properties and user data, regulators might ask questions about monopolistic behavior, user privacy, or fair competition. This is still a theoretical concern, but as the portfolio grows, it becomes more likely.

The biggest question is whether Bending Spoons' model actually works long-term. The company claims it's profitable and sustainable, but without seeing financials, investors and users are taking a leap of faith. If the portfolio is actually profitable, Bending Spoons might become one of the most successful business models of the decade—a way to create value by efficiently running digital products. If it's not, the company might eventually run out of capital and face pressure to change its strategy.

The Ethical Dimension: Is This Good for Users?

Ultimately, the Bending Spoons question reduces to an ethical one: is the company good for users and the digital ecosystem?

The case for Bending Spoons is straightforward. The company acquires products that were neglected or mismanaged, reorganizes them for sustainability, and keeps them alive. WeTransfer would not exist in its current form if Bending Spoons hadn't acquired it. Evernote was stagnating before the acquisition. Meetup was orphaned within a larger conglomerate. By acquiring these products and optimizing them, Bending Spoons keeps them available for millions of users.

The case against Bending Spoons is equally straightforward. The company prioritizes profitability over user experience. It cuts teams ruthlessly, sometimes eliminating products' original creators and visionaries. It restricts free offerings, forcing users to pay or leave. It makes changes to beloved products that users dislike. For users of Bending Spoons products, the experience can feel like the product has been stripped down and monetized aggressively.

The reality is probably that Bending Spoons is neither wholly good nor wholly bad—it's a pragmatic business approach with trade-offs. Some of those trade-offs benefit users and the ecosystem. Some damage them.

What's clear is that Bending Spoons represents a different model than either venture-backed startups (which prioritize growth over profitability) or traditional conglomerates (which seek synergies and consolidation). The company's approach—acquiring, optimizing, and holding—is neither selfless nor purely exploitative. It's a business model designed to generate returns while keeping products alive and serving users.

Whether that's ultimately good or bad is a question each user has to answer for themselves.

FAQ

What exactly does Bending Spoons do?

Bending Spoons is a digital product holding company that acquires established internet platforms and applications, then restructures and optimizes them for profitability. The company buys products like Evernote, Meetup, and WeTransfer, analyzes their cost structures and business models, and makes changes—including layoffs, feature restrictions, and monetization adjustments—to improve the products' financial performance. The company claims to hold acquired businesses indefinitely and never sells them.

How many users does Bending Spoons reach across its portfolio?

Bending Spoons serves over a billion people across its portfolio of products. The company claims more than 300 million monthly active users and 10 million paying customers. These numbers span dozens of products including Evernote (225+ million downloads), Meetup (22 million monthly active users), WeTransfer (70 million monthly active users), and many others. The portfolio's reach is massive, yet most users never interact with the Bending Spoons brand.

Why does Bending Spoons cause so many layoffs when it acquires companies?

Bending Spoons believes that many digital products are overstaffed relative to the core value they deliver. When the company acquires a product, it analyzes the team structure and cuts positions it deems unnecessary. In some cases—like Filmic—the entire team is eliminated while the product continues to operate with minimal ongoing development. This approach prioritizes financial efficiency over maintaining headcount, and it allows Bending Spoons to dramatically reduce costs while supposedly maintaining product functionality. Whether these layoffs actually improve products long-term is debated.

Is Bending Spoons good for users?

Whether Bending Spoons is good for users depends on how you measure "good." The company keeps beloved products alive that might otherwise be abandoned or shut down. But it also makes changes—restricting free tiers, removing features, increasing prices—that many users dislike. For some users, Bending Spoons' optimization preserves products they couldn't live without. For others, the changes damage products they loved. The answer probably differs from product to product and user to user.

How did Bending Spoons get all this capital to acquire major companies like Eventbrite and Vimeo?

Bending Spoons' source of capital isn't entirely clear, but likely sources include reinvested profits from earlier acquisitions, investor backing, and potentially debt financing. The company has been operating since 2012 and has made dozens of acquisitions. As earlier products became profitable, that cash could fund new acquisitions. The company likely also has investors or backers willing to provide capital for acquisitions. Without seeing financial statements, it's impossible to know the exact capital structure, but the scale of recent acquisitions (Eventbrite

Will Bending Spoons eventually go public?

It's possible, though Bending Spoons has never indicated plans to do so. Going public would require disclosing financial information and reporting to public markets—something the company has avoided so far. If Bending Spoons wants to continue acquiring large companies or raise capital at scale, going public might become necessary. But the company's philosophy of long-term value creation over quarterly metrics might be incompatible with public market pressures.

What's the difference between Bending Spoons and traditional private equity?

The key difference is the exit strategy. Traditional private equity acquires companies, improves them, and sells them within 5-10 years to generate a return. Bending Spoons claims it never sells acquired companies—it holds them forever. This fundamentally changes incentives. Private equity might cut costs aggressively to maximize the sale price. Bending Spoons must balance short-term profitability with long-term sustainability because it's not planning to exit. Both models can be profitable, but they optimize for different outcomes.

Are there products Bending Spoons has actually failed with or shut down?

Public information about Bending Spoons' failures is limited, but the company's claims suggest it hasn't shut down acquired products. Some products may operate in "maintenance mode" with minimal development (like Filmic after the team was eliminated), but the company claims never to have sold or discontinued an acquired business. This makes Bending Spoons' portfolio theoretically durable—even if a product stops growing, it stays alive.

How does Bending Spoons compare to other product holding companies?

Bending Spoons' model is relatively unique. Most conglomerates seek synergies through integration. Bending Spoons maintains product independence. Most private equity firms have exit strategies. Bending Spoons claims to hold forever. Most acquirers immediately re-brand or consolidate. Bending Spoons lets products keep their identities. This distinctive approach makes Bending Spoons hard to compare directly to other companies—it's something of a hybrid between traditional private equity, conglomerates, and a tech incubator.

Conclusion: The Stealth Giant Reshaping Digital Products

Bending Spoons remains one of tech's best-kept secrets. A company with over a billion users across its portfolio operates almost entirely outside public awareness. Its CEO rarely gives interviews. Its acquisitions generate headlines primarily when they're announced or when layoffs follow. Yet the company's impact on the digital landscape is enormous.

The acquisitions of Eventbrite for

Whether Bending Spoons ultimately proves to be a brilliant innovation in digital commerce or an exploitative model that strips products of their soul remains to be seen. The company's philosophy—optimizing for efficiency and profitability while holding products indefinitely—is neither inherently noble nor inherently extractive. It's a business model with trade-offs.

What's clear is that Bending Spoons has demonstrated a sustainable approach to managing digital products at scale. The company acquires products that others have abandoned or mismanaged, reorganizes them for profitability, and keeps them alive serving millions of users. Whether you think that's good or bad depends on whether you value efficiency and sustainability over the user experience ideals of the products' original creators.

For users of Bending Spoons products, the implication is straightforward: expect changes after acquisition. Expect payoff of free tiers. Expect ruthless cost-cutting. Expect aggressive monetization. But also expect the product to survive and potentially thrive long-term. For creators and founders who've sold to Bending Spoons, the implication is equally clear: you've joined a system optimized for efficiency, not growth or creative vision.

The next frontier for Bending Spoons is consolidation. With dozens of products in the portfolio, the company will eventually find infrastructure synergies, shared services, and cross-selling opportunities. This might improve the portfolio's overall profitability but could also risk creating the kind of conglomerate bloat that Bending Spoons was originally designed to eliminate.

Bending Spoons' ascent is one of the tech industry's most important and least noticed stories. As the company continues acquiring digital properties—and increasingly large ones—understanding the Bending Spoons model becomes crucial for anyone who uses digital products, invests in tech, or cares about how the internet is shaped and operated.

The company that was born from the ashes of a failed startup has quietly become one of the internet's most important infrastructure providers. Whether it will ultimately prove to be a force for good or a cautionary tale about putting efficiency above everything else remains one of tech's most important open questions.

Key Takeaways

- Bending Spoons serves over a billion people across its portfolio of products including Meetup, Evernote, WeTransfer, and Eventbrite, yet remains virtually unknown to the general public

- The company's acquisition strategy focuses on mature digital products with established user bases but stagnant growth, which it then restructures for profitability through cost cuts and monetization changes

- Recent acquisitions of Eventbrite (1.38B), and Brightcove ($233M) signal the company's expansion into billion-dollar platform territory and larger-scale operations

- Bending Spoons' operational model emphasizes efficiency and long-term holding over growth or user experience, often resulting in significant layoffs and controversial product changes

- The company claims to never sell acquired businesses and aims to hold its portfolio indefinitely, fundamentally distinguishing it from traditional private equity models