![Beyond Meat's Protein Soda: Last Chance or New Direction [2025]](https://tryrunable.com/blog/beyond-meat-s-protein-soda-last-chance-or-new-direction-2025/image-1-1769614679755.jpg)

Beyond Meat's Protein Soda: Last Chance or New Direction [2025]

Beyond Meat just did something it's never really done before. It launched a product that makes absolutely no attempt to replicate meat. No burger patty pretending to sizzle like ground beef. No fake blood made from beetroot juice. Just a protein soda in three fruity flavors, coming in both 10g and 20g protein versions, promising to be crisp and refreshing instead of chalky and thick.

The product is called Beyond Immerse. And if you're paying attention to what's happening in the alt-protein space, it signals something profound: the company that built its entire identity on replacing beef, chicken, and pork is finally admitting that this strategy isn't working.

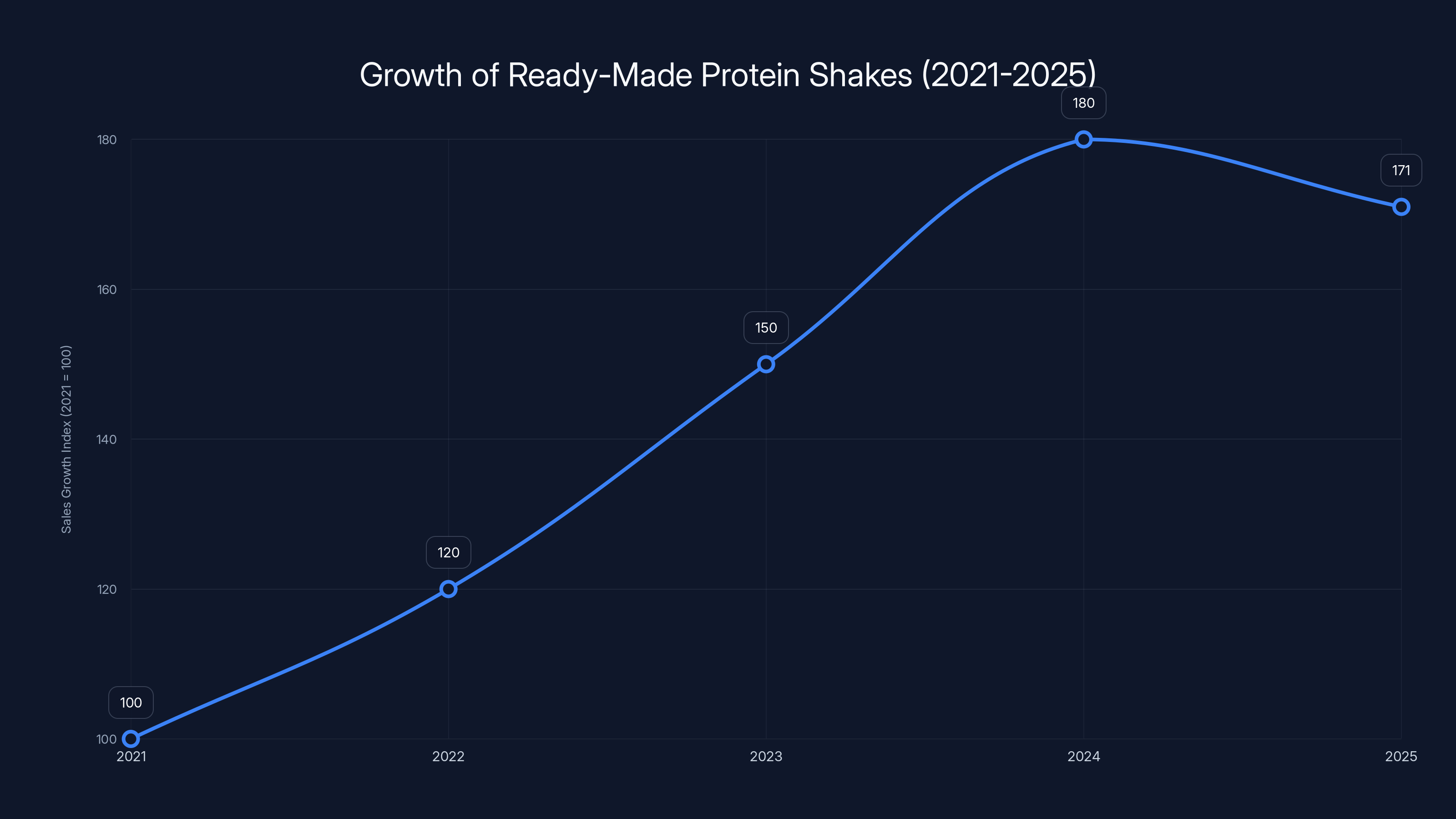

Beyond Meat's core problem isn't complicated. The plant-based meat market has contracted dramatically since its 2019 IPO hype, consumer enthusiasm has cooled, and the company has never turned an annual profit. Meanwhile, the beverage market—specifically functional drinks packed with protein, probiotics, fiber, and electrolytes—is booming. Ready-made protein shake sales grew 71% between 2021 and 2025. The functional drink category as a whole exceeded $200 billion in 2024 and continues accelerating.

So Beyond Meat is making a calculated bet: maybe it's not a plant-based company anymore. Maybe it's just a company that happens to use plants. And maybe the real money isn't in competing with Tyson Foods. It's in competing with Poppi, Liquid IV, and Celsius.

But here's what makes this pivot both hopeful and terrifying: it might already be too late.

The Plant-Based Meat Market Has Hit a Wall

Let's be clear about the situation Beyond Meat is facing. The plant-based meat category peaked around 2019-2021. That was the moment when every major food company was pouring billions into alt-protein, every grocery store was expanding its meatless section, and mainstream media was running breathless features about the future of food.

Then reality set in.

Consumer interest has flatlined. People tried plant-based burgers, discovered they didn't quite hit the mark, and went back to regular burgers. The price premium over conventional beef never made sense to price-conscious shoppers. And honestly, the products still don't taste exactly like meat—they taste like something trying very hard to taste like meat and almost getting there, which is not the same thing at all.

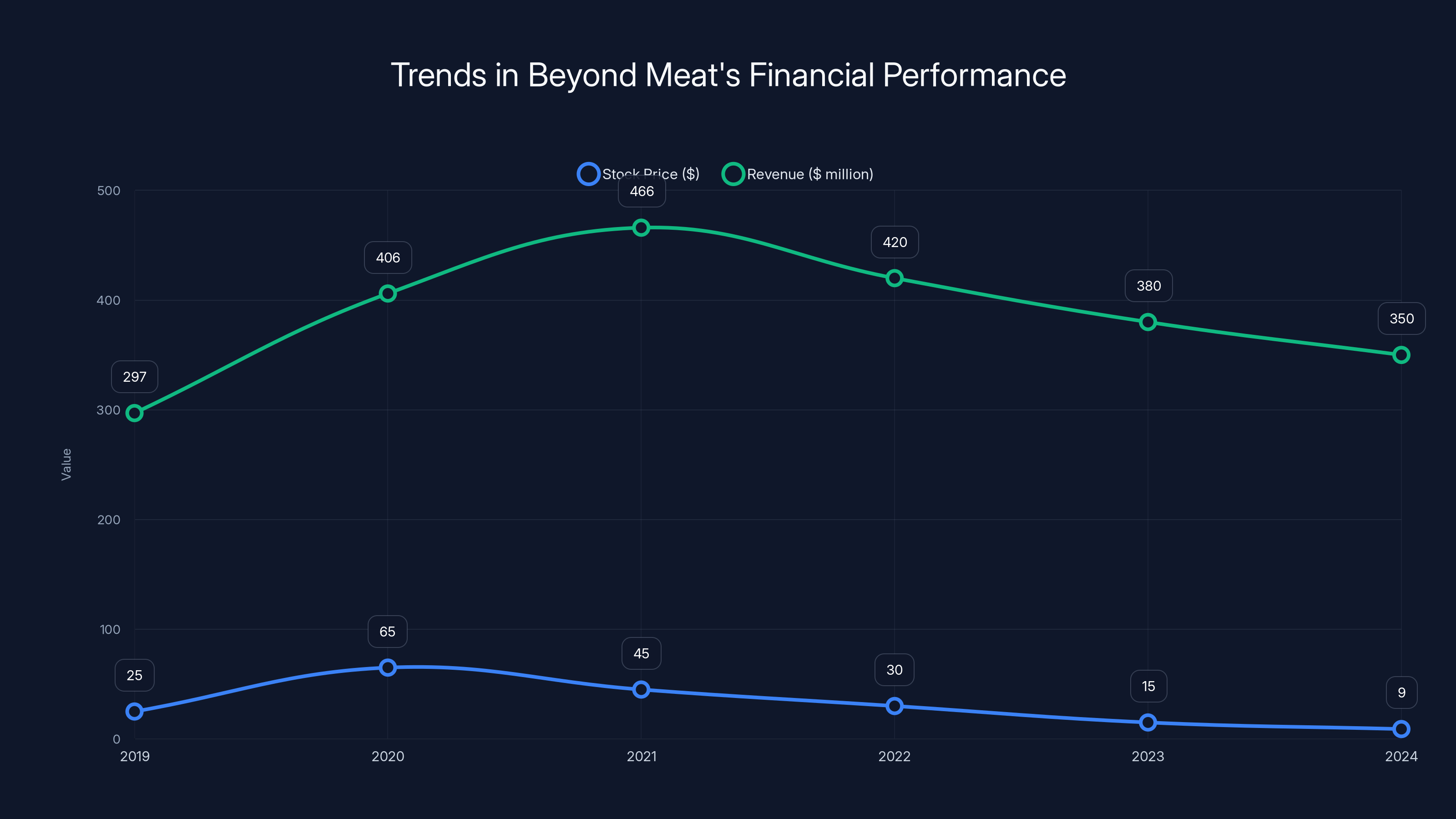

Beyond Meat's financial trajectory tells the whole story. The company went public at

By 2024, Beyond Meat's stock was trading in the single digits. The company has never posted an annual profit. It's burned through hundreds of millions in cash. Its net loss in 2023 was

More worrying than the numbers themselves is what they reveal about market dynamics. Plant-based meat isn't just struggling at Beyond Meat. The entire category is struggling. Sales of plant-based meat alternatives have been flat or declining across the US for the past three years, even as consumers have become more interested in plant-based eating overall. This suggests that the problem isn't people avoiding plants—it's that people don't actually want meat replacements as much as the industry believed.

The competitive landscape didn't help. Large food companies like Tyson, Perdue, and Nestlé all launched their own plant-based products, using their distribution advantages to undercut Beyond on price while leveraging established brand trust. Upstart competitors like Impossible Foods gained market share. And all the while, consumer novelty wore off.

The fundamental issue is that Beyond Meat built its entire business model on one specific insight: that consumers would pay a premium for a plant-based burger if it tasted good enough. But that insight turned out to be wrong. Most consumers will not pay the premium. And most people don't care that much whether their protein comes from animals or plants—they just want it to taste good and not cost too much.

This is why the shift toward beverages makes sense. In the protein drink market, consumers have already proven they're willing to pay premiums for different formulations, flavors, and functional benefits. The economics are better. The market is growing. And Beyond Meat's plant-based positioning is actually an asset rather than a liability.

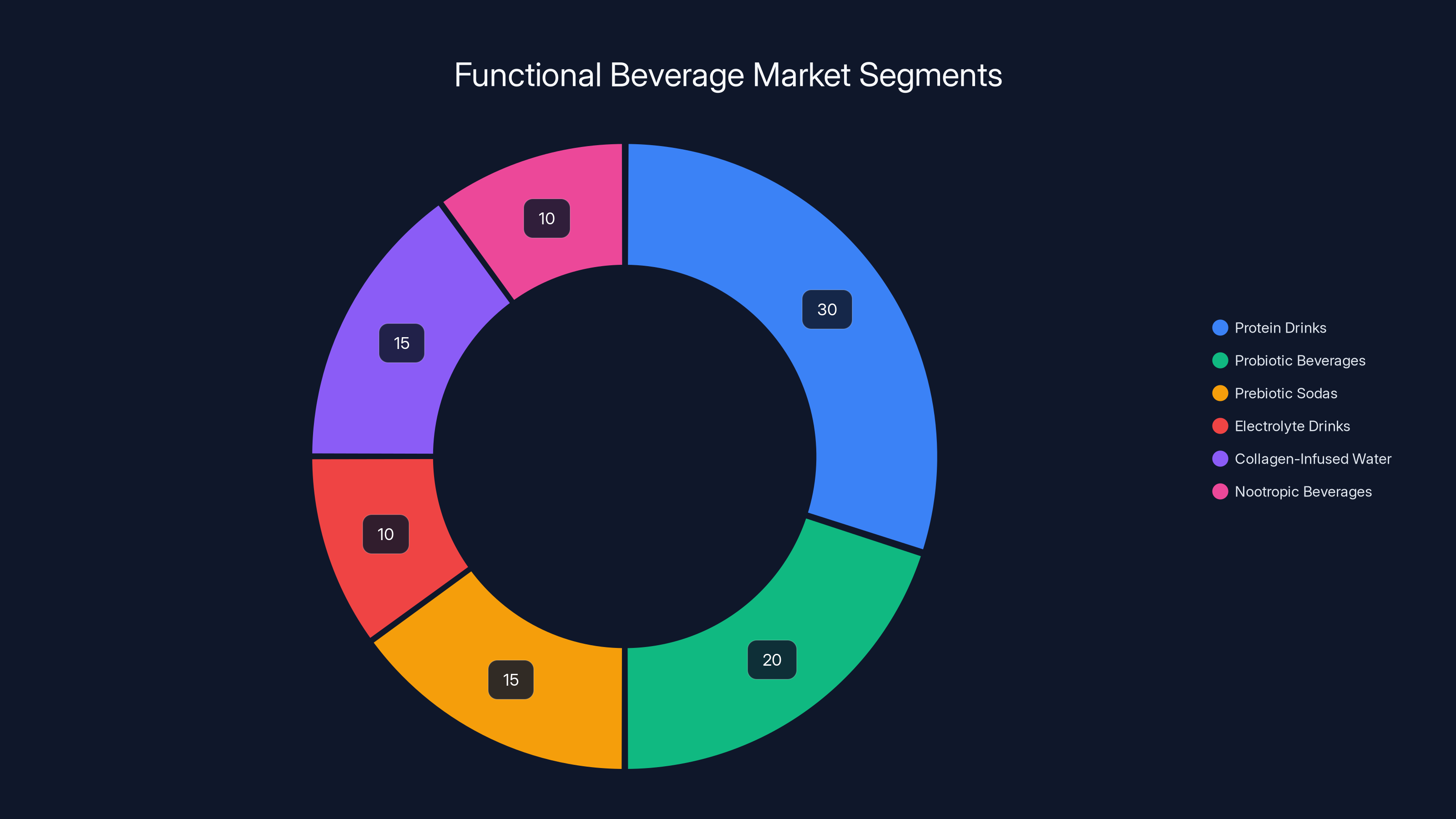

Protein drinks lead the functional beverage market with an estimated 30% share, followed by probiotic beverages at 20%. Estimated data based on market trends.

The Protein Drink Boom: Where the Real Money Is

The functional beverage market has become one of the fastest-growing segments in CPG (consumer packaged goods). We're talking about drinks that aren't just designed to taste good—they're engineered to deliver specific health benefits.

Protein drinks are just one slice of this pie. Other functional categories include probiotic beverages, prebiotic sodas, electrolyte drinks, collagen-infused water, nootropic beverages, adaptogens, and more. Walk into any major grocery store's beverage section and you'll see entire shelves dedicated to products that would have seemed ridiculous five years ago.

The numbers are compelling. The global protein drink market was valued at approximately

Why the difference? Several factors converge. First, beverage pricing is psychologically divorced from traditional protein sources. A consumer thinks nothing of paying

The category has attracted serious capital and talent. Pepsi Co acquired the prebiotic soda brand Poppi for $1.95 billion in 2025, validating that functional beverages are worth premium valuations. Mondelēz has been expanding its functional drink portfolio. Coca-Cola launched multiple functional beverage lines. Even energy drink companies like Red Bull and Monster are diversifying into functional categories.

Beyond Meat is entering this space with some actual advantages. The company has legitimate expertise in plant-based formulation. It understands how to work with pea protein, create pleasant mouthfeel, and manage the flavor profile challenges that have plagued plant-based beverages in the past. It has brand recognition as a pioneer in the space. And it has existing distribution relationships with major retailers that have already granted shelf space to its products.

The functional beverage market also benefits from genuine consumer trends around health consciousness, fitness, and wellness. Unlike the plant-based meat trend, which was partially driven by hype and novelty, interest in functional beverages is rooted in demonstrated consumer behavior. People genuinely want to optimize their nutrition, recovery, and energy levels. They're willing to experiment with products that promise tangible benefits.

Beyond Immerse's positioning directly targets this sentiment. The product promises protein, fiber, antioxidants, and electrolytes in a refreshing format. The macros (up to 20g protein and 7g fiber at 100 calories) are competitive with leading products. The flavor approach—fruity, crisp, and not trying to taste like anything other than a soda—is actually smart positioning. It's a product that says "I'm a functional beverage that happens to be plant-based," not "I'm a plant-based product that happens to be a beverage."

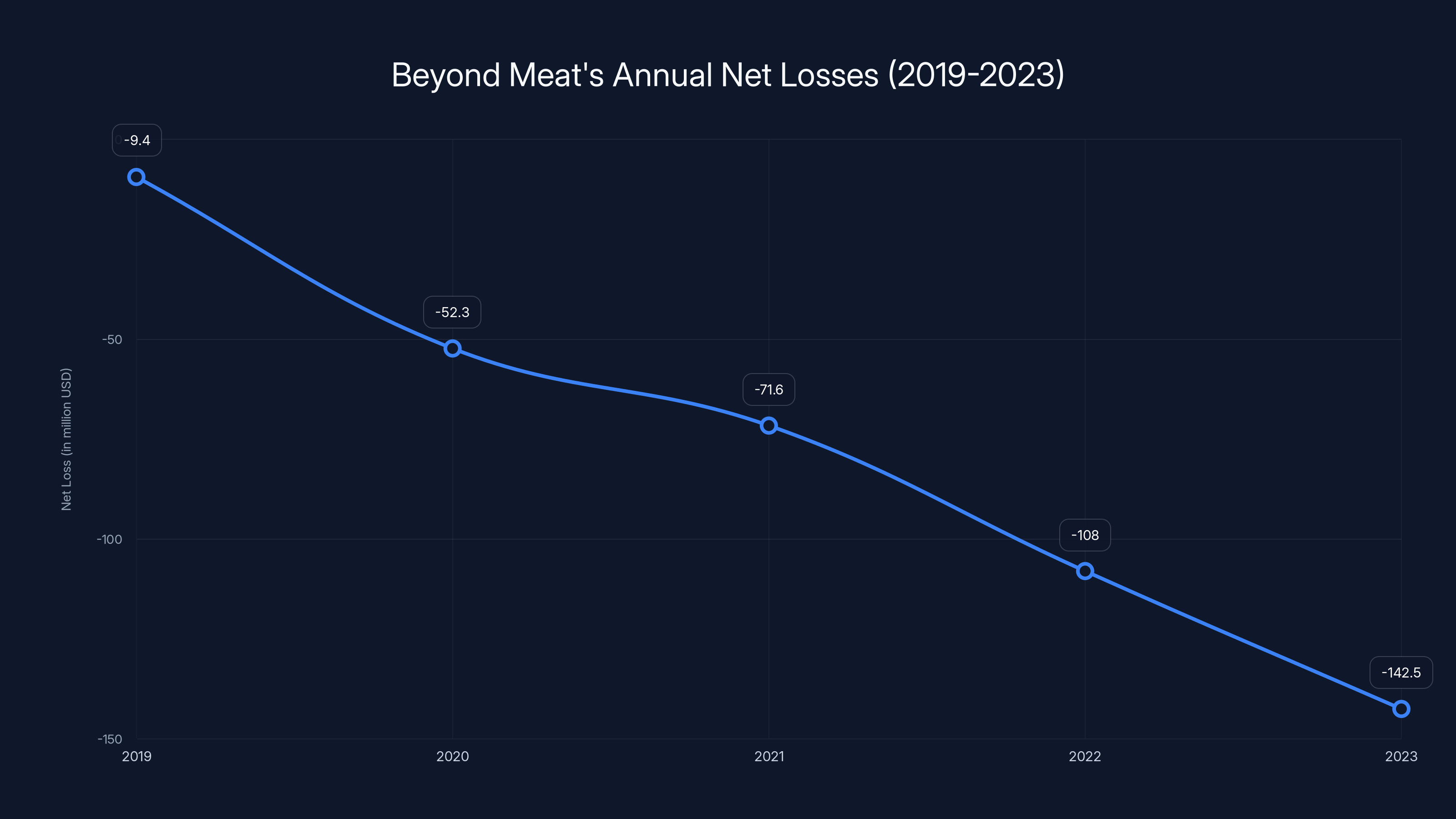

Beyond Meat's net losses have increased significantly from 2019 to 2023, highlighting the financial challenges the company faces. Estimated data suggests that entering the beverage market could improve margins.

Beyond Immerse: The Product That Shows Both Promise and Desperation

Let's talk about what Beyond Immerse actually is, because the product itself is revealing.

Immerse comes in three flavors: Peach Mango, Lemon Lime, and Orange Tangerine. Each flavor is available in two protein levels—10g or 20g—and two calorie targets—60 calories or 100 calories respectively. The product uses pea protein for amino acids and tapioca fiber for the, well, fiber. The flavor profile relies on fruit juice concentrates and stevia as the sweetener, with a handful of added electrolytes, antioxidants, and natural flavors to round things out.

The macronutrient profile is actually compelling. If you consume the 20g/100 calorie version, you're looking at a product that delivers:

- 20g of protein (equivalent to about 2.3oz of cooked chicken breast)

- 7g of dietary fiber (roughly 28% of the recommended daily value)

- 100 calories

- Added electrolytes

- Added antioxidants

- Zero sugar (stevia-sweetened)

For context, this is materially better than what most ready-to-drink protein beverages deliver. Most RTD protein shakes hit around 20g protein and 150-200 calories. Many traditional protein drinks are either chalky or overly sweet or both. If Beyond can actually deliver the texture and flavor profile it promises, Immerse becomes genuinely competitive.

There's a critical note here: the limited first run sold out almost immediately through Beyond's Test Kitchen direct-to-consumer channel. This matters because it suggests genuine consumer interest rather than morbid curiosity. People aren't buying it to see what a desperate company is doing. They're buying it because the product seems credible.

But here's where desperation shows through. Beyond Meat is launching Immerse in the direct-to-consumer channel first, not through traditional retail distribution. This is a classic pattern for companies in trouble. They launch through DTC to generate buzz, prove demand, and collect consumer feedback before asking retailers to dedicate precious shelf space to an unproven category extension.

It's the right move tactically. But it also reveals that Beyond Meat doesn't have the distributor leverage or retailer relationships necessary to secure premium shelf placement at scale. If the company had confidence in this product and access to the retail infrastructure it built over five years, it would be launching in Whole Foods and Kroger simultaneously, not hoping that positive DTC sales eventually convince retailers to stock it.

The product positioning itself—emphasizing that Immerse is plant-based but not trying to be meat—is a departure from how Beyond has typically positioned itself. For years, the company's entire identity was "the plant-based meat pioneer." Now it's rebranding to "a plant-based company with expertise in plant-based nutrition." This is necessary repositioning, but it also implies that the original positioning stopped working.

The Beverage Market's Expanding Competitive Landscape

Beyond Meat isn't entering an empty market. The protein drink space is becoming crowded, and many competitors have significant advantages.

Established brands like Muscle Milk, Premier Protein, Fairlife, and Isopure have been in this category for years and have strong distribution, proven formulations, and loyal consumers. Gatorade and Powerade are leveraging their massive distribution networks to add protein variants. Core has become a lifestyle brand. Trim has positioned around fitness culture.

In the plant-based protein drink specific category, Beyond Meat is competing against Soylent, Vega, Orgain, and a growing number of DTC-first brands. Many of these have the advantage of being born in the functional beverage era—they understand the category, the consumer expectations, and the distribution challenges more intuitively than a company pivoting from meat alternatives.

What Beyond Meat does have is brand recognition and distribution relationships. Most people have heard of Beyond Meat. Most major grocery stores already carry Beyond Meat products. That's valuable, but it's also not a durable competitive advantage in beverages. Consumers discover new drink brands constantly, and brand affinity doesn't transfer automatically from one category to another.

The competitive threat gets worse when you consider that major beverage companies have the scale to compete on price, the marketing budgets to compete on awareness, and the innovation resources to compete on product performance. If Beyond Meat successfully launches Immerse and proves the market, expect Pepsi Co to launch a plant-based protein drink. Expect Coca-Cola to announce one. They have the advantages of incumbency, and they'll extract them ruthlessly.

Beyond Meat's window to establish itself in the beverage category is narrow. The company needs to:

- Prove that Immerse can deliver on its taste and texture promises

- Build consumer loyalty before major competitors enter the category

- Secure retail distribution at scale

- Establish the product's unique positioning (plant-based, functional, refreshing) in consumer consciousness

- Generate enough scale to achieve profitable unit economics

All of that needs to happen within 12-24 months. If it doesn't, the window closes and the category gets dominated by competitors with more resources.

Beyond Meat's stock price and revenue peaked around 2019-2021 but have since declined, reflecting broader struggles in the plant-based meat market. Estimated data.

The Plant-Based Protein Drink Category: Is There Actually a Difference?

Here's a question that doesn't get asked enough: can consumers actually taste the difference between plant-based and dairy-based protein drinks?

The answer is complicated. For some consumers, the answer is yes—and they have legitimate reasons to prefer plant-based. They might be vegan, lactose intolerant, or simply concerned about animal welfare. But for the broader market, the difference is much smaller. A well-formulated plant-based protein drink should be functionally similar to a dairy-based equivalent in terms of texture, mouthfeel, and taste if the formulation is correct.

The problem is that most plant-based protein drinks haven't been formulated correctly. Pea protein, which is the most common plant-based protein source, has a beany flavor that's notoriously hard to mask. It creates a grainy mouthfeel if you're not careful. The fiber additions that make plant-based drinks functional can add unpleasant texture. And stevia, the preferred sweetener for plant-based products, has a distinctive aftertaste that some people find off-putting.

Beyond Meat claims to have solved these problems through proprietary formulation, using pea protein but combining it with juice concentrates and natural flavors to create a genuinely refreshing experience. This is plausible—Beyond has invested years in plant-based formulation, and the company employs food scientists who understand how to manage these flavor and texture challenges.

But here's the thing: consumers don't care whether the solution is proprietary or proven. They just care whether the drink tastes good. And plant-based positioning, while it appeals to some consumers, is actually a liability for many others. Some people actively want to avoid plant-based products. Others are simply indifferent to the plant-based angle and will choose whatever tastes best and delivers the best macros.

So Beyond Meat's advantage here is limited. The company's plant-based expertise is real, but it's not something that most consumers will ever notice. From a taste and texture perspective, Immerse is competing on the same basis as every other protein drink: does it taste good, does it deliver the promised macros, and is it worth the price?

That's both an opportunity and a threat. It's an opportunity because Beyond doesn't need to be "the plant-based drink" to succeed—it just needs to be a great protein drink. It's a threat because being great at something you've never done before is hard, and being great at something while your company is in financial distress is even harder.

Why the Timing Matters: Market Conditions in 2025

Beyond Meat's decision to enter the protein beverage market in 2025 is notably different from what the company might have done even two years ago. The beverage market landscape has shifted in ways that matter.

First, the functional beverage category has reached sufficient scale and maturity that major retailers now dedicate meaningful shelf space to these products. Five years ago, functional drinks were niche products found in natural food stores. Now they're mainstream, available in every supermarket, convenience store, and even vending machines. This makes retail distribution easier than it would have been in 2019.

Second, consumer mindset around health and fitness has become more sophisticated. The pandemic accelerated interest in wellness and immunity-boosting products. Gen Z consumers have normalized talking about biohacking, optimization, and functional nutrition. Sports nutrition and fitness are no longer niche—they're culturally mainstream. A plant-based protein drink fits naturally into this consumer conversation.

Third, plant-based eating as a category has matured past the early-adopter phase. Plant-based is no longer novel or countercultural. It's just another option. This actually helps Beyond Meat because the company no longer has to spend marketing dollars explaining why plant-based matters. It can just make a good product and let the plant-based positioning add a layer of appeal without being the entire value proposition.

Fourth, the investment environment around CPG (consumer packaged goods) has stabilized after several years of volatile funding. Private equity and strategic investors have proven willing to fund beverage brands that demonstrate scale potential. This means if Beyond Immerse succeeds, the company might have easier access to growth capital than would have been available in 2022-2023.

Fifth, and perhaps most importantly, the cautionary tale of plant-based meat has made investors and consumers skeptical of category claims. The hype has dissipated. This is actually good for Beyond Meat in some ways—it means the company's beverage launch will be evaluated on product quality and market performance rather than on category enthusiasm. But it's also bad because it means Beyond Meat starts from a position of distrust rather than excitement.

The company also benefits from having more data about what works and what doesn't in plant-based formulation. Five years of building plant-based products have generated knowledge about consumer preferences, flavor profiles, and product performance. Beyond Meat is leveraging that knowledge, not starting from scratch.

But here's the complication: 2025 is also when the window is closing for companies that need to pivot or die. Beyond Meat's cash runway isn't infinite. The company is still burning substantial amounts of capital. Investor patience for turnarounds is limited. Institutional pressure to show a path to profitability is intense.

Beyond Meat launched Immerse at almost exactly the right time—not too early when the beverage category seemed saturated, not too late when investor patience had fully evaporated. But the timing is also cutting it close. The company needs this to work, and it needs it to work soon.

Ready-made protein shake sales grew 71% from 2021 to 2025, indicating a strong market trend towards functional beverages. Estimated data based on industry reports.

The Financial Question: Can Beverages Be Profitable for Beyond?

Let's talk numbers, because ultimately this story is about whether Beyond Meat can generate profit.

The company has never been profitable on an annual basis. Let's state that clearly. Since going public in 2019, Beyond Meat has generated the following results:

- 2019: Net loss of $9.4 million

- 2020: Net loss of $52.3 million

- 2021: Net loss of $71.6 million

- 2022: Net loss of $108.0 million

- 2023: Net loss of $142.5 million

The trend is moving in the wrong direction. The company continues to burn more cash than it generates in profit. Gross margin on existing plant-based meat products is in the 20-30% range, which leaves insufficient money to cover SG&A (selling, general, and administrative) expenses, R&D, and interest.

Beverage products typically have better gross margins, usually 50-70% depending on formulation and manufacturing scale. This is because beverages have lower per-unit manufacturing costs, higher price points, and better packaging economics. A beverage that retails for

Here's a simplified math model for Beyond Immerse:

Assuming:

- Retail price: $4.50 per 12oz can

- Wholesale price to retailer: $2.70 (40% discount)

- Manufacturing and packaging cost: $0.90

- Gross profit per unit: $1.80 (at wholesale)

- Gross margin: 67%

This is significantly better than plant-based meat products. With this margin structure, Beyond Meat could potentially achieve profitability if it can scale Immerse to sufficient volume. According to industry analysis, a beverage brand needs to reach approximately 50-100 million units annually to justify the fixed costs of distribution, marketing, and manufacturing.

For context, Poppi was doing approximately 60-80 million units annually when Pepsi Co acquired it. Liquid IV has achieved similar scale. These are the benchmarks Beyond Meat would need to hit.

At 50 million units annually and 67% gross margin, Beyond Immerse would generate approximately $46 million in annual gross profit (before considering fixed costs). That's not enough to cover a company-wide cost structure, but it would represent meaningful progress toward profitability if combined with improved performance from other product lines.

The challenge is getting from zero to 50 million units. Scaling a beverage requires:

- Manufacturing capacity (bottling facilities, production agreements with co-manufacturers)

- Distribution infrastructure (getting into stores, managing logistics)

- Marketing and awareness (consumers need to know the product exists)

- Competitive pricing (balancing margin with accessibility)

- Product superiority (the drink actually needs to be better than alternatives)

Beyond Meat has some advantages here (existing distribution relationships, brand recognition) but also significant disadvantages (limited capital, lower brand power in beverages, no history in this category).

The mathematics suggest that beverages could help Beyond achieve profitability, but only if the company can execute flawlessly. The margins are better, the market is larger, and consumer interest is genuine. But the execution bar is very high, and failure is entirely possible.

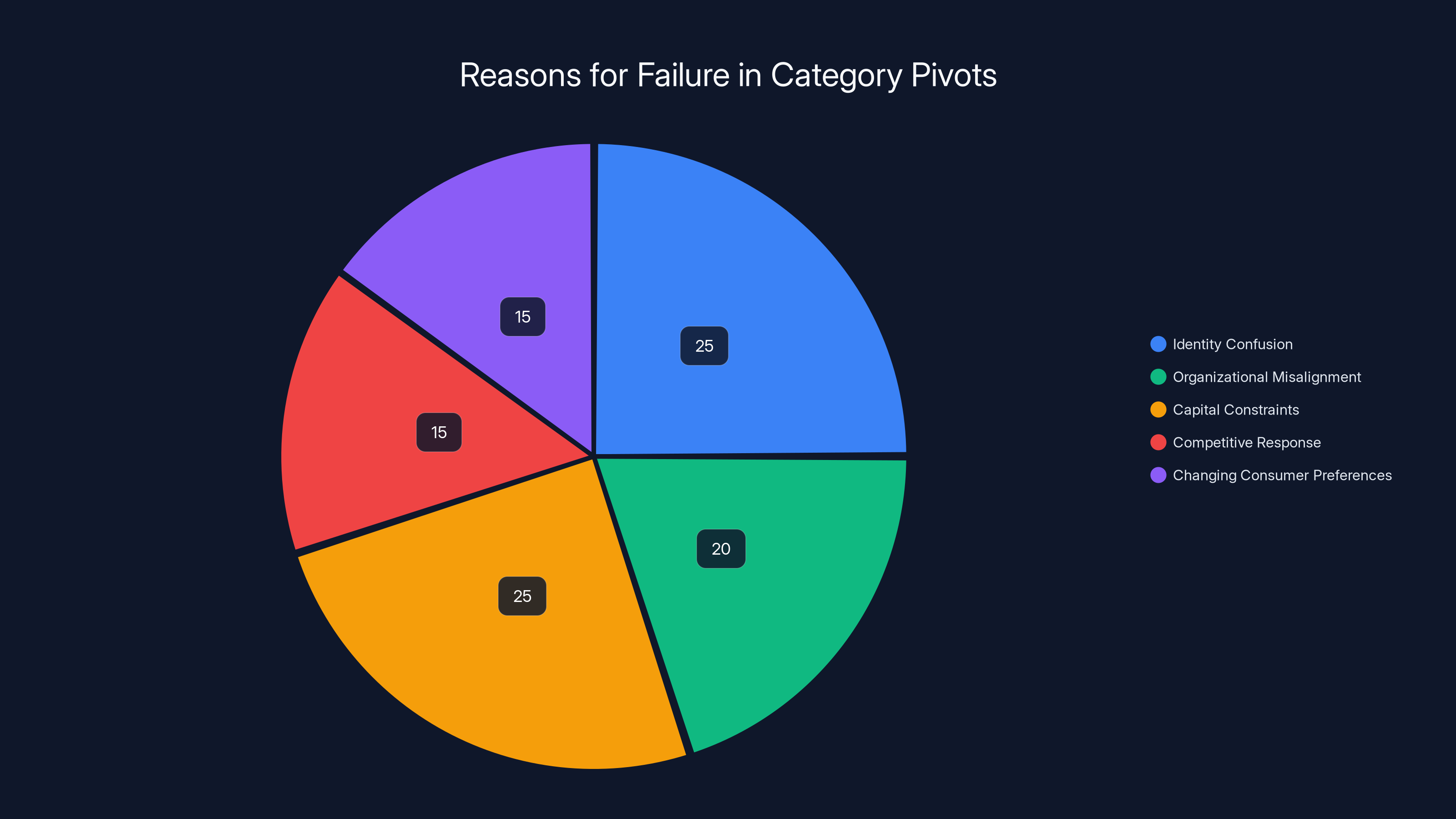

Execution Risk: Why Many Category Pivots Fail

Companies pivot all the time. Sometimes it works. Often it doesn't. The success rate for major category pivots in CPG is probably lower than 40%, and that's being generous.

Why do so many fail? Several reasons:

Identity Confusion: When a company has been famous for one thing, pivoting to something different creates identity confusion. Consumers think of Beyond Meat as a burger company. Asking them to think of it as a beverage company requires breaking and rebuilding mental associations. This is expensive and difficult.

Organizational Misalignment: The skills and incentive systems that made a company successful in one category often don't transfer. Beyond Meat's expertise in plant-based meat formulation doesn't directly translate to beverage formulation. The company's relationships with burger-focused retailers might not help with beverage distribution. The sales force trained to sell to burger-focused chains might not be effective selling to beverage channels.

Capital Constraints: Pivots require investment. You need to build manufacturing capacity, invest in marketing, perhaps hire new talent. Companies in financial distress often don't have the capital to invest adequately. Beyond Meat could spend $50-100 million trying to scale Immerse and still fail if execution is imperfect. That's a lot of capital to spend when you're already burning cash.

Competitive Response: If Beyond Immerse succeeds, it won't stay uncontested for long. Large beverage companies will respond with their own plant-based offerings. Once that happens, Beyond's first-mover advantage dissipates, and the category becomes a war of scale and capital. Beyond probably loses that war.

Changing Consumer Preferences: Categories shift. Protein drinks are hot in 2025, but what if consumers pivot to something else by 2026? What if functional beverages face regulatory scrutiny around health claims? What if a new category emerges and cannibalizes the functional drink space? Beyond Meat would be caught with significant investment in a category that's no longer exciting.

The history of consumer brands pivoting categories is filled with failures. Kodak made excellent digital cameras but failed to pivot away from film because the organization was designed around film. Go Pro built an iconic action camera brand but struggled to expand into other device categories. Nokia dominated phones but couldn't successfully pivot to smartphones when that category emerged (though their downfall also involved licensing their brand to a company with different capabilities).

Beyond Meat's pivot is smart from a strategic perspective—the company needs to find a more profitable business model. But execution risk is substantial. The company is trying to enter a new category while simultaneously managing the decline of its existing business, all while in financial distress. That's an extremely difficult needle to thread.

The positive signal is that Immerse sold out quickly in the initial DTC release. This suggests product-market fit potential. But one successful limited release doesn't prove the company can scale. We'll need to see:

- How many customers reorder

- How the product performs when retail distribution begins

- Whether the company can maintain product quality while scaling manufacturing

- How consumers respond when the marketing hype settles

- Whether the company can remain solvent long enough to reach profitability

All of these are open questions.

Identity confusion and capital constraints are major reasons for the failure of category pivots, each contributing an estimated 25% to the failure rate. Estimated data.

The Existential Question: Is Beyond Meat a Plant-Based Company or a Technology Company?

Here's a deeper question that Immerse's launch raises: what actually is Beyond Meat?

For the first decade of its existence, Beyond Meat had a clear identity. The company was a plant-based protein company focused on creating alternatives to meat. The value proposition was simple: taste like meat, be healthier than meat, require fewer resources than meat. The business model was direct and understandable.

But that identity has become a liability. It has locked the company into a category that's not growing at the rate required to build a billion-dollar business. It's created investor and consumer expectations that the company can't meet. It's made it difficult for Beyond Meat to be acquired by a strategic buyer because any acquirer would be buying into a declining market.

Immerse represents a different identity: Beyond Meat as a plant-based nutrition company. The core insight isn't "replace meat with plants." It's "use plants to deliver superior nutrition." This is a broader positioning that could encompass many product categories—beverages, supplements, snacks, meal replacements, functional foods. It's not tied to any specific product form.

This is actually a smart identity to pursue. It's more defensible. It opens more market opportunities. It positions the company as a nutrition innovator rather than a novelty burger company.

But there's a problem: it's not clear whether Beyond Meat has the organizational DNA to execute this broader identity. The company was built by people who understood meat alternatives. Its culture, values, and institutional knowledge are all organized around that mission. Remaking the company into something broader requires not just launching new products—it requires changing what the company fundamentally is.

That's hard. Cultural transformations of this magnitude often fail because they're not really about new products. They're about identity, purpose, and organizational structure. They require different leadership, different incentive systems, different values, and often different employees at various levels.

Beyond Meat would benefit from this kind of transformation. But there's no evidence yet that it's willing to undertake it. The company has maintained most of its original leadership. It hasn't signaled major organizational changes. Immerse feels like a product launch, not a transformation.

That might be fine if the launch is successful. But if it's not, Beyond Meat doesn't have a plan B. The company has gone all-in on beverages working without having fully transformed itself to become a beverage company. That's optimistic at best, reckless at worst.

Consumer Behavior: Who Actually Buys Plant-Based Protein Drinks?

Let's think about the actual consumer for Beyond Immerse.

It's not the core plant-based consumer. That person is probably already committed to plant-based protein options and has found favorites. Beyond Immerse might appeal to them, but they're not the growth opportunity.

The real opportunity is the person who doesn't particularly care whether their protein is plant-based or dairy-based. They just want a good-tasting, functional beverage that delivers promised macros at a reasonable price. Maybe they're a fitness enthusiast. Maybe they're a health-conscious consumer. Maybe they're someone who's trying to lose weight or build muscle. They've probably tried multiple protein drink brands and will judge Immerse on whether it's better than what they're currently using.

For this consumer, plant-based positioning is a nice-to-have, not a must-have. The product lives or dies on whether it's genuinely crisp and refreshing, whether the macros are real, whether it tastes good, and whether the price is right.

This is a very different consumer than the early plant-based movement attracted. That consumer was motivated by ideology—concern about animal welfare, environmental impact, health benefits of plant-based eating. The new consumer is motivated by utility—they want a good product at a good price.

Beyond Meat's success with Immerse depends on whether the company can appeal to utility-driven consumers rather than ideology-driven ones. The early sales success suggests this might be possible. But sustained success requires that the product actually be better than alternatives in ways that matter to the target consumer.

There's also a question about consumption occasion. When does someone buy a protein drink? Usually when they're trying to optimize nutrition around fitness, weight management, or general wellness. This is a scheduled, intentional consumption pattern. The consumer doesn't grab a protein drink on impulse because it's next to the soda—they buy it because they've decided they need protein in their diet.

This means Immerse's success depends heavily on consumer education and marketing. The company needs to convince people that this drink is worth buying and worth paying the premium price. That's a heavy lift, especially for a brand that's currently associated with failing plant-based burgers.

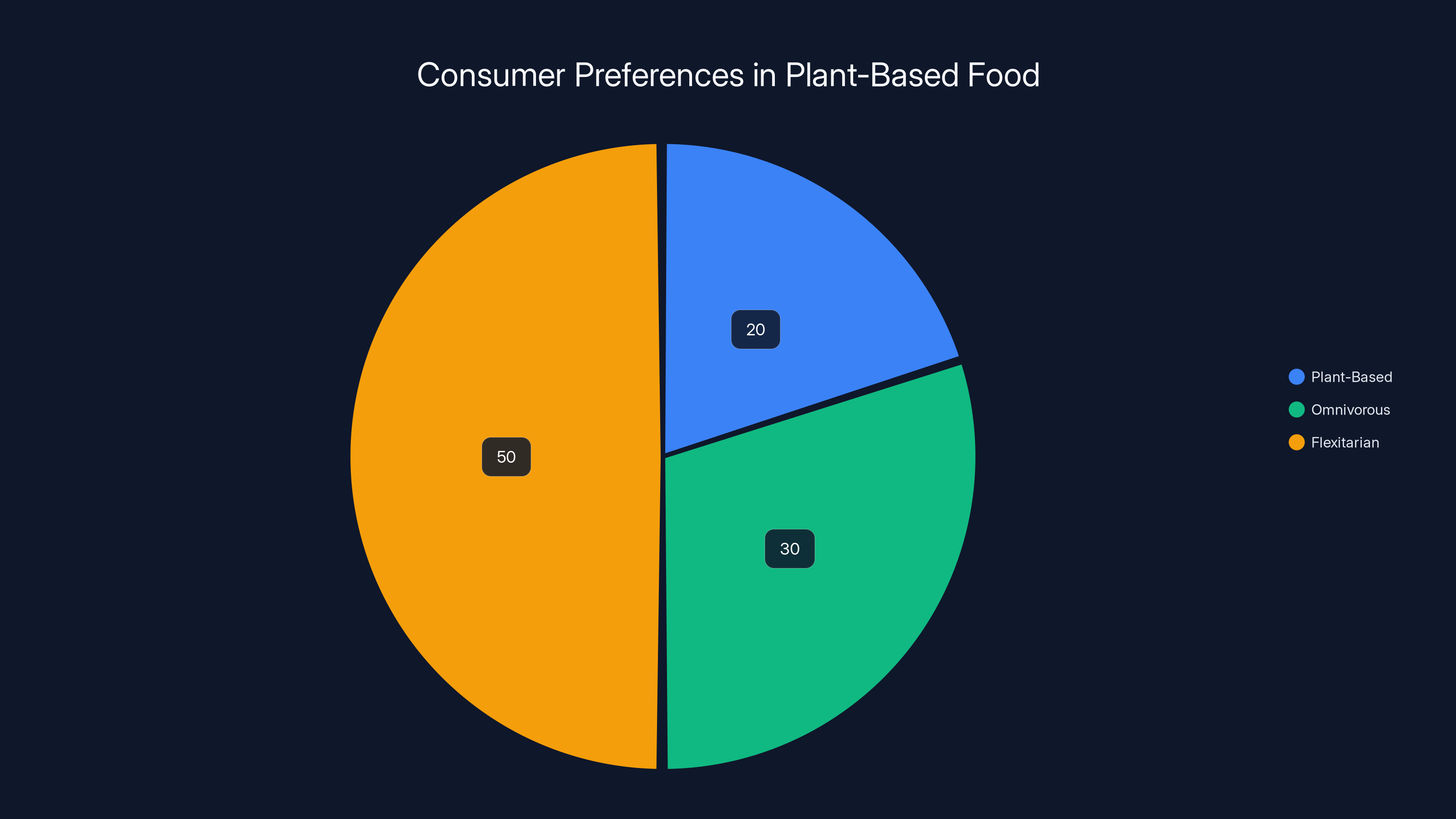

Estimated data suggests that flexitarians, who consume both plant-based and animal products, make up the largest segment of the market, highlighting the integration of plant-based eating into broader consumer behavior.

The Broader Plant-Based Protein Ecosystem

Beyond Meat isn't the only plant-based protein company trying to stay relevant. The entire ecosystem is under pressure.

Impossible Foods is in a similar position—it built its brand on plant-based burgers and is now exploring other categories. The company has been testing plant-based sausages, nuggets, and other formats to diversify away from burgers. But it's facing similar market dynamics: the plant-based burger category is not growing at the rate needed to build a sustainable, profitable business.

Smaller plant-based companies have been acquired or gone out of business. Lightlife, owned by Maple Leaf Foods, has largely exited the plant-based space in favor of conventional products. Field Roast, which made plant-based deli meats, was acquired and then largely dismantled. The venture capital money that was flowing into plant-based startups in 2019-2021 has largely dried up.

This suggests that the plant-based food movement has hit a maturity plateau earlier than many expected. It's not that consumers have rejected plant-based products—it's that they've selected the specific formats and brands that work for them, and the total addressable market is smaller than the hype suggested.

Within this ecosystem, Beyond Meat's move to beverages makes sense. The company has brand recognition and distribution capabilities that smaller startups don't have. It has access to capital that allows it to invest in new categories. And it has legitimate expertise in plant-based formulation that translates across categories.

But the broader point is that plant-based food as a category is undergoing consolidation. The winners will be companies that figure out profitable niches. The losers will be companies that remain committed to categories that aren't economically viable.

For Beyond Meat, the gamble is that beverages are a viable niche. The math suggests they could be. But execution risk is real.

Regulatory and Labeling Considerations

There's another layer of complexity that doesn't get discussed much: regulation and labeling.

Functional beverages exist in a regulatory gray area. They're not quite dietary supplements, but they're not quite conventional beverages either. The FDA has been increasingly scrutinizing functional beverage claims. If a company claims that a product improves health in specific ways, the FDA might require substantiation that would be difficult or impossible to provide.

Poppi, the prebiotic soda that sold for $1.95 billion, had to settle litigation around misleading health claims. The company claimed the product had specific gut-health benefits that allegedly weren't substantiated. This is a cautionary tale for any company launching a functional beverage with health-related claims.

Beyond Immerse makes specific promises: it contains protein, fiber, antioxidants, and electrolytes. These are fact-based claims about what's actually in the product, which is low-risk. But the product's positioning implies functional benefits—that these ingredients will improve health outcomes. If Beyond Meat makes those implications too explicit, it could face regulatory scrutiny.

This might actually be an advantage for Immerse. By positioning the product as a refreshing soda that happens to have good macros and functional ingredients, rather than as a health beverage making specific health claims, Beyond Meat avoids the regulatory and litigation risks that have plagued other functional beverage companies.

The labeling question also matters for retail. How will Immerse be shelved? In the beverages section next to sodas and sports drinks? Or in the health and wellness section next to protein powders and supplements? The placement affects who sees it and how consumers evaluate it. This is a decision that will vary by retailer and region, which could create execution challenges for Beyond Meat.

Looking Forward: What Success Looks Like for Beyond Immerse

For Beyond Immerse to be genuinely successful—not just as a product launch but as a salvage plan for the company—several things need to happen.

First, the product needs to perform well in limited direct-to-consumer distribution. This means high repeat purchase rates, strong customer satisfaction, and positive word-of-mouth. The initial sellout is a good sign, but it's not sufficient. The company needs to see that people love the product enough to repurchase consistently.

Second, the company needs to secure retail distribution at meaningful scale within 12-18 months. This means getting into major chains like Whole Foods, Kroger, Target, and Walmart. Without retail distribution, Immerse remains a niche product that will never achieve scale.

Third, the company needs to build brand awareness among the target consumer. Most people don't know Beyond Meat is launching a protein drink. The company will need to invest in marketing to make the product visible. This is expensive and requires sustained investment over multiple quarters.

Fourth, the product needs to maintain quality and consistency while scaling manufacturing. This is harder than it sounds. Many beverage companies have stumbled at this point—the product that tasted perfect in the limited initial run tastes different when made at scale in a co-manufacturing facility.

Fifth, the company needs to achieve unit economics that work at scale. The product needs to remain profitable even after accounting for distribution costs, marketing, and retail margins. If the math doesn't work, neither does the business.

Sixth, the company needs to establish Immerse as a standalone brand with equity. Over time, consumers should think of Immerse as its own product, not just as "Beyond Meat's protein drink." This requires marketing investment and product success.

Finally, and most importantly, Beyond Meat needs to reach profitability within 3-4 years. If the company is still burning cash by 2028, investors will lose patience. The company will become a takeover candidate for a buyer looking to strip assets, or it will become a distressed situation.

If all of this happens, Immerse could be a success and could help Beyond Meat return to profitability. If any of these elements fail—if the product disappoints at scale, if retail won't take it, if marketing doesn't generate awareness, if manufacturing gets expensive—Immerse becomes another failed pivot in the company's history.

The company is essentially betting its future on one product launch. That's simultaneously desperate and potentially brilliant, depending on execution.

The Bigger Picture: What This Means for Plant-Based Food

Beyond Meat's pivot to beverages tells us something important about the state of plant-based food.

It tells us that the original hypothesis—that consumers wanted plant-based alternatives to meat that tasted like meat—was partially wrong. Some consumers wanted this. But not enough to build a sustainable, profitable business.

It also tells us that the plant-based food movement was, in many ways, a venture capital-driven hype cycle. Billions of dollars flowed into companies making plant-based meat because the narrative was exciting and the market seemed enormous. But narratives don't create sustainable demand, and enormous potential markets don't guarantee profitability.

What seems to be happening instead is that plant-based eating is becoming integrated into normal consumer behavior rather than existing as a separate category. Some consumers are plant-based, some are omnivorous, and many are flexitarians who eat both. But the idea that there would be one massive "plant-based food" category with massive scale seems increasingly unlikely.

Within this context, Beyond Meat's pivot makes sense. Rather than being "the plant-based meat company," the company is repositioning to be "a company that uses plants to create nutritious products that consumers want." Burgers were the first product category. Beverages are the second. If beverages work, there could be a third, fourth, or fifth category.

This is a more defensible long-term strategy than remaining committed to a declining category.

But it's also a strategy that fundamentally changes what Beyond Meat is. The company is no longer building a "food company of the future" based on a specific ingredient. It's trying to become a general food and beverage company that happens to focus on plant-based ingredients. That's a lower-margin, lower-multiple business, but it might be the only viable path forward.

A Company in Transition

Beyond Meat stands at a crossroads. The business model that created the company—selling plant-based alternatives to meat at premium prices—has stopped working. The company has never been profitable. Cash is being burned. Investor confidence is shaken.

Beyond Immerse represents a bet that the company can transition to a different business model before the current one collapses completely. It's a bet on beverages, on better margins, on a category that's growing, and on the company's ability to execute something it's never done before.

Is it the right bet? Maybe. Beverages have better economics. The market is growing. Beyond Meat has some relevant expertise and distribution advantages. The product seems credible based on initial reception.

But there's also substantial risk. Category pivots are hard. Beyond Meat has limited capital to invest. The beverage category is increasingly competitive. And the window for proving success is narrow.

Most likely, we'll know within 18-24 months whether this gamble works. If Immerse achieves meaningful retail distribution and strong consumer reception, Beyond Meat has a path to profitability. If it doesn't, the company faces a much darker future.

What's certain is that the company that was supposed to represent "the future of food" is now fighting for its survival. That's a long fall from the IPO hype of 2019, when it seemed like anything was possible.

Beyond Meat's protein soda might not be the company's last chance. But it's definitely one of its last chances.

FAQ

What is Beyond Meat's Immerse protein soda?

Beyond Immerse is a ready-to-drink protein beverage launched by Beyond Meat in 2025, available in three fruity flavors (Peach Mango, Lemon Lime, and Orange Tangerine). Each flavor comes in two protein levels (10g or 20g) and two calorie targets (60 or 100 calories), made entirely from plant-based ingredients including pea protein and tapioca fiber. The product is designed to be crisp and refreshing while delivering competitive macronutrients compared to traditional protein drinks.

Why is Beyond Meat launching a protein drink now?

Beyond Meat's plant-based burger business has declined significantly since 2021, with the company never achieving annual profitability despite going public. The beverage category, particularly functional drinks, has grown substantially while maintaining better profit margins (50-70%) compared to plant-based meat products (20-30%). This pivot represents the company's attempt to enter a larger, more profitable market before the current business model becomes unsustainable.

How does Immerse compare to other plant-based protein drinks?

Immerse differentiates itself through a focus on taste and texture, positioning as a crisp, refreshing alternative to chalky traditional protein drinks. The macronutrient profile is competitive, offering up to 20g of protein and 7g of fiber at 100 calories, which compares favorably to established brands. However, it faces competition from established plant-based brands like Vega and Soylent, as well as major beverage companies that could enter the plant-based segment.

What are the profit margin implications for Beyond Meat?

Beverages typically generate 50-70% gross margins compared to plant-based meat's 20-30% margins, which creates potential for profitability at scale. For Immerse to meaningfully impact company finances, it would need to reach 50-100 million units annually—a substantial scale similar to what brands like Poppi achieved before acquisition. The improved margins could allow Beyond Meat to approach profitability if the company can achieve this volume, though achieving such scale remains challenging.

Is plant-based positioning an advantage or liability for the drink?

Plant-based positioning is both. It appeals to consumers who actively seek plant-based products and aligns with Beyond Meat's brand identity and manufacturing expertise. However, for the broader protein drink market, plant-based positioning is largely neutral—most consumers care primarily about taste, macros, and price. The strategic advantage lies in manufacturing capability and ingredient expertise rather than marketing positioning.

What happens if Immerse doesn't succeed?

Failure of the Immerse launch would leave Beyond Meat with severely limited options. The company would be forced to rely on declining plant-based meat sales, potentially face further investor losses, and might become a takeover target for a strategic buyer looking to acquire its distribution infrastructure and brand assets. The company's cash runway would determine whether it could attempt additional pivots or whether financial pressure would force more drastic measures.

How long does Beyond Meat have to make Immerse work?

The company likely has 18-24 months to demonstrate meaningful progress—this includes achieving positive consumer reception, securing retail distribution, and showing signs of a path to profitability. Beyond this window, investor patience typically exhausts itself, and the company faces increasing pressure from creditors and stakeholders. Success requires demonstrating consumer demand, retail acceptance, and viable unit economics within this timeframe.

What's the broader significance of this pivot?

Beyond Meat's shift from plant-based meat alternatives to functional beverages signals that the plant-based food movement, while real, is smaller and more niche than early venture capital projections suggested. It also demonstrates that sustainable food companies need to be built on economic fundamentals (profitability, margin structure) rather than on category enthusiasm or narrative excitement. For the food industry broadly, it suggests that ingredient-based positioning ("plant-based") is less valuable than product-based or functional positioning ("protein drink").

Key Takeaways

- Beyond Meat's pivot to beverages signals that the plant-based meat category has hit a maturity plateau with insufficient profitability potential

- Functional beverages offer 50-70% gross margins compared to plant-based meat's 20-30%, creating a sustainable path to profitability

- Immerse sold out immediately in limited DTC release, suggesting product-market fit potential, but scaling to profitability requires 50-100 million units annually

- The company has 18-24 months to demonstrate success before investor patience exhausts and the company faces existential risk

- Plant-based food as a category is consolidating, with winners being companies that find profitable niches rather than pursuing category-wide dominance