![Broadcom's VMware Partner Purge: What CSPs Need to Know [2025]](https://tryrunable.com/blog/broadcom-s-vmware-partner-purge-what-csps-need-to-know-2025/image-1-1770032418305.jpg)

The Broadcom Bulldozer: How VMware's Partner Collapse Changes Everything

Something significant just happened in the cloud infrastructure world, and most people barely noticed.

At the end of January 2026, Broadcom quietly ended the VMware Advantage Partner Program, which meant hundreds of European Cloud Service Providers (CSPs) lost the ability to resell VMware software. This isn't a minor policy adjustment. This is a consolidation bomb.

Here's what you need to understand: the Advantage Partner Program was the backbone of VMware's partner ecosystem. It allowed independent cloud providers across Europe, North America, and beyond to build businesses around VMware's virtualization technology. They managed customer relationships, handled support, customized deployments, and created differentiated services. It was a healthy, competitive market.

Now it's gone.

The ripple effects are already visible. CISPE (the Cloud Infrastructure Services Providers in Europe), the umbrella organization representing European cloud providers, has openly criticized Broadcom's moves as a "bulldozer" that's "rolling over" the remaining competition. One CTO called it exactly what it is: aggressive consolidation disguised as "evolving customer requirements."

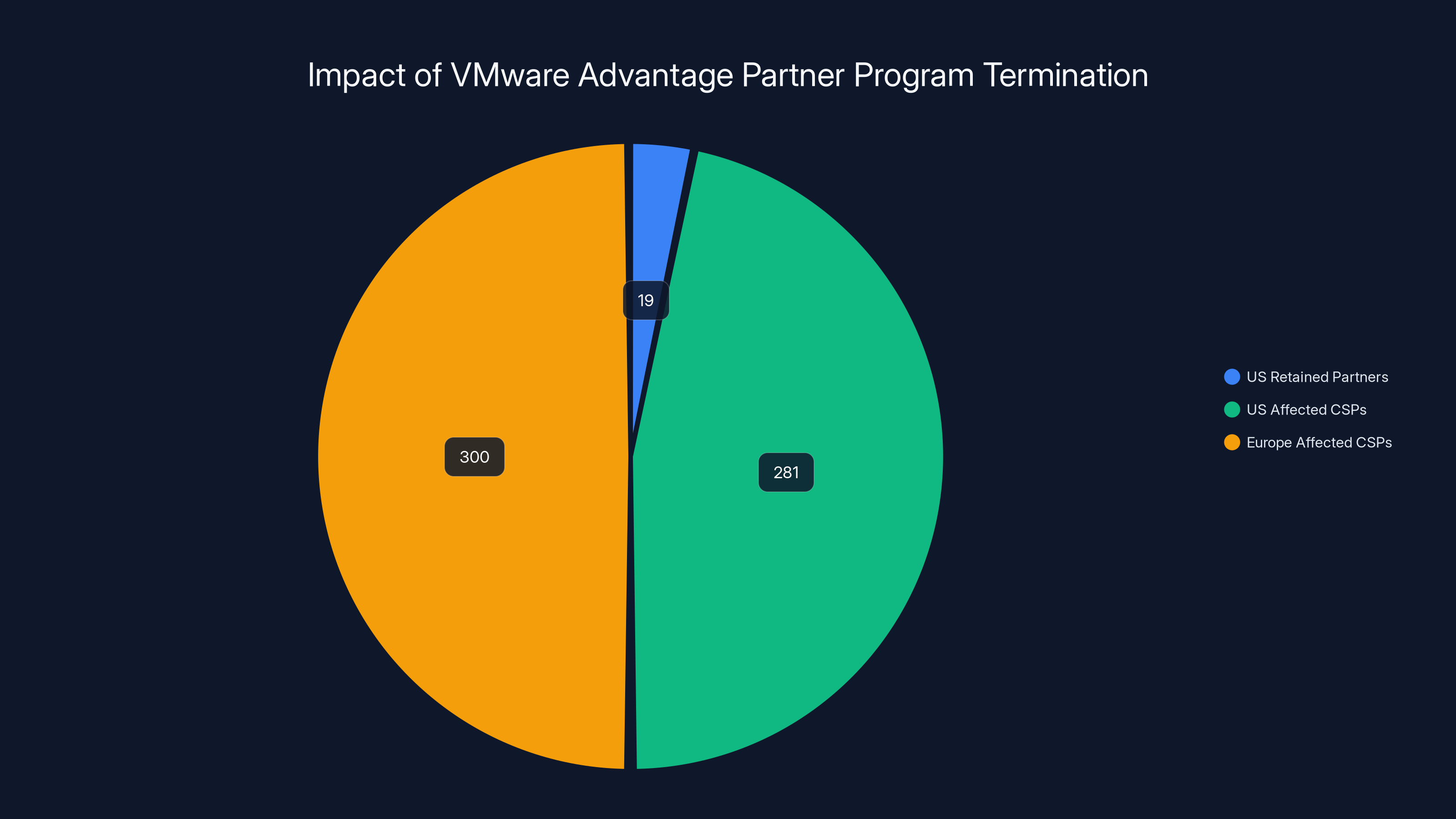

But here's where it gets worse. Only about 19 CSPs remain in the United States with VMware Advantage Partner status. In Europe, the same pattern is unfolding. The vendor that once championed channel partnerships is now narrowing its partner base to a selected few. This is what happens when a semiconductor giant buys a software company for $61 billion and decides the partner model doesn't fit their financial targets.

This matters because you might be one of those CSPs, or you might be a customer about to discover that your provider can't renew their VMware relationships. Either way, prices are about to get interesting. And not in a good way.

TL; DR

- Broadcom terminated the VMware Advantage Partner Program effective January 26, 2026, eliminating resale opportunities for hundreds of European CSPs

- Only a small subset of partners can join the new program, creating a bottleneck that reduces customer choice and increases competition for limited slots

- Market consolidation is accelerating, with just 19 CSPs remaining in the US and similar consolidation happening across Europe

- Higher prices and reduced competition are the likely outcomes, as fewer providers compete for VMware workloads

- Data sovereignty risks increase for European businesses, since fewer local providers means less flexibility and potential lock-in with multinational vendors

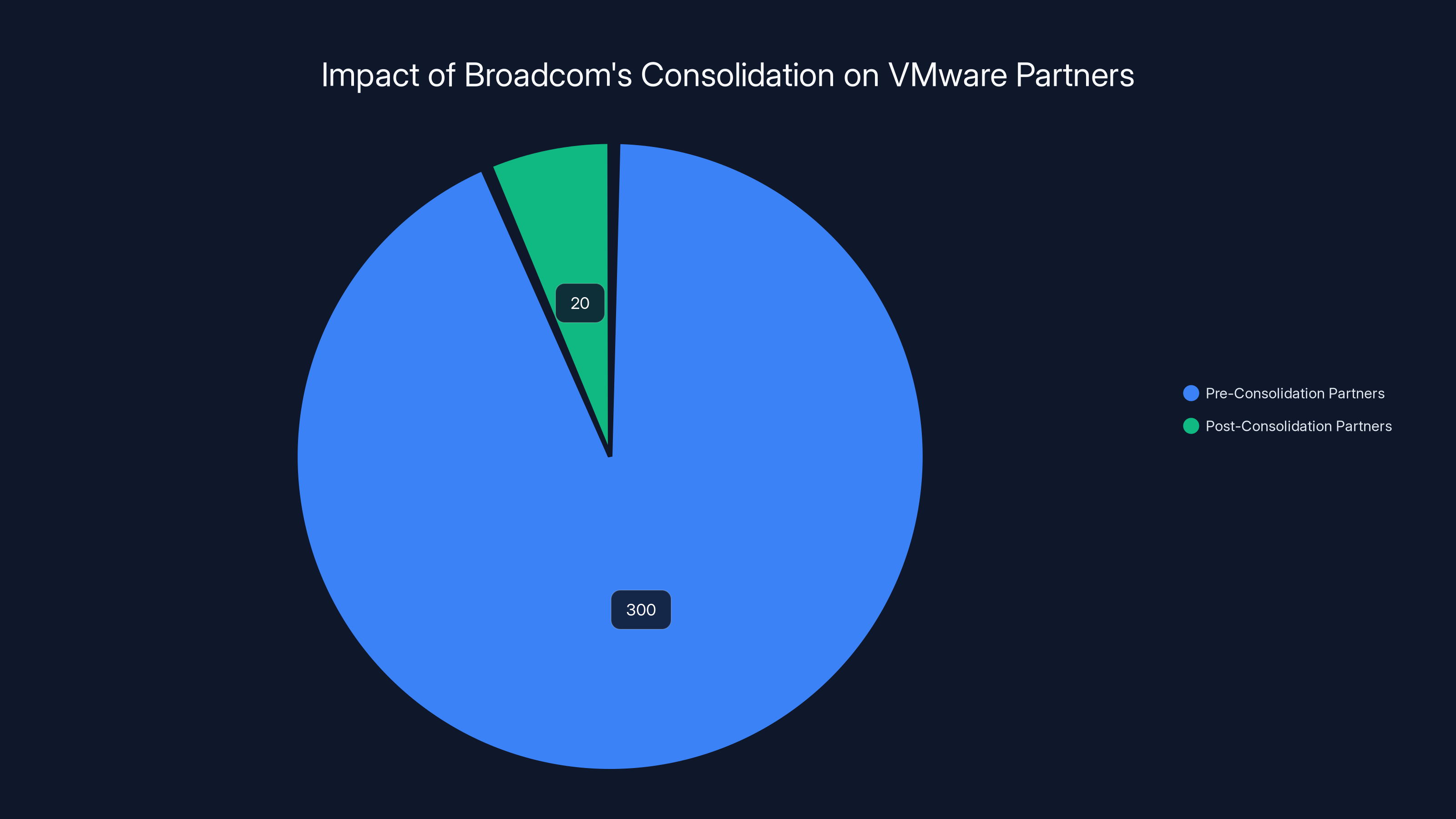

The termination of the VMware Advantage Partner Program significantly affected CSPs, reducing US partners from an estimated 300 to just 19 retained partners. Europe follows a similar pattern with approximately 300 affected CSPs. (Estimated data)

The Advantage Partner Program: What Just Died

Before we get into the fallout, let's understand what the Advantage Partner Program actually was.

The program was VMware's response to a fundamental problem in enterprise IT: customers don't always want to buy directly from the vendor. They want a trusted local partner who understands their infrastructure, their budget constraints, and their business goals. That partner becomes the single point of contact for everything from initial consulting through deployment, optimization, and ongoing support.

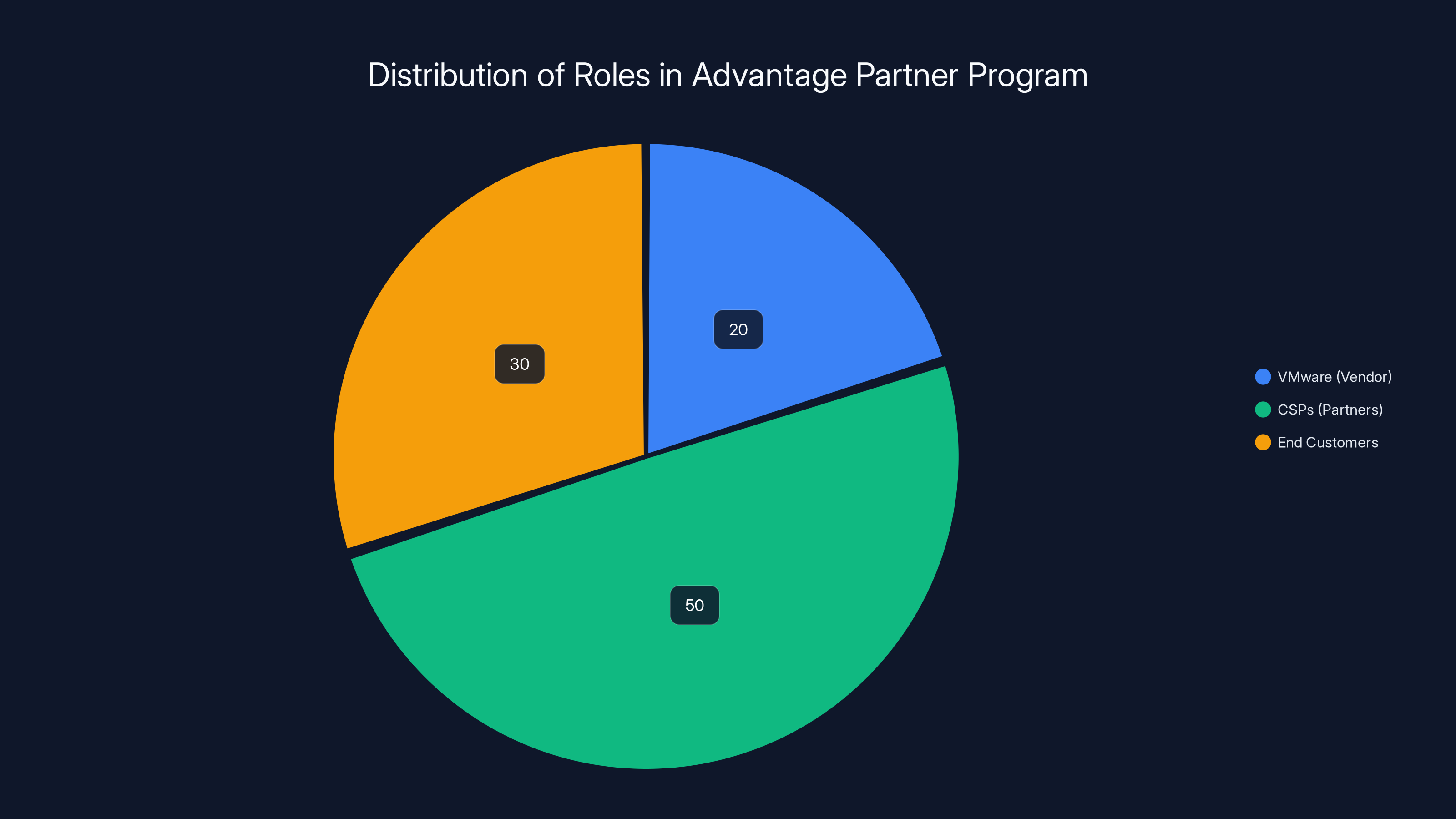

The Advantage Partner Program formalized this. Partners could purchase VMware licenses at partnership pricing, resell them to their own customers, and maintain those relationships over time. It created a three-tier ecosystem:

- VMware (vendor) - builds the software, manages licensing

- CSPs (partners) - resell licenses, handle customer relationships, provide localized support

- End customers - get choice in who they buy from and work with

This isn't unique to VMware. It's the channel model that drives the entire software industry. Microsoft, Cisco, and Oracle all use variants of this model because it works. Partners earn money, customers get service, vendors get distribution.

But Broadcom's acquisition of VMware changed the equation entirely.

When Broadcom closed its $61 billion acquisition of VMware in late 2023, the company inherited a mature partner network and a mature business. Mature businesses don't have the growth profiles that semiconductor companies like Broadcom need. Broadcom's investors expect expansion. They expect new revenue streams. They expect consolidation where it drives margin improvement.

The Advantage Partner Program termination is textbook consolidation. By narrowing the partner base, Broadcom can:

- Reduce the complexity of partner management

- Increase direct customer relationships (which generate higher margins)

- Pressure remaining partners into more exclusive, higher-volume commitments

- Control pricing and licensing terms more directly

It's aggressive. It's also predictable once you understand who owns VMware now.

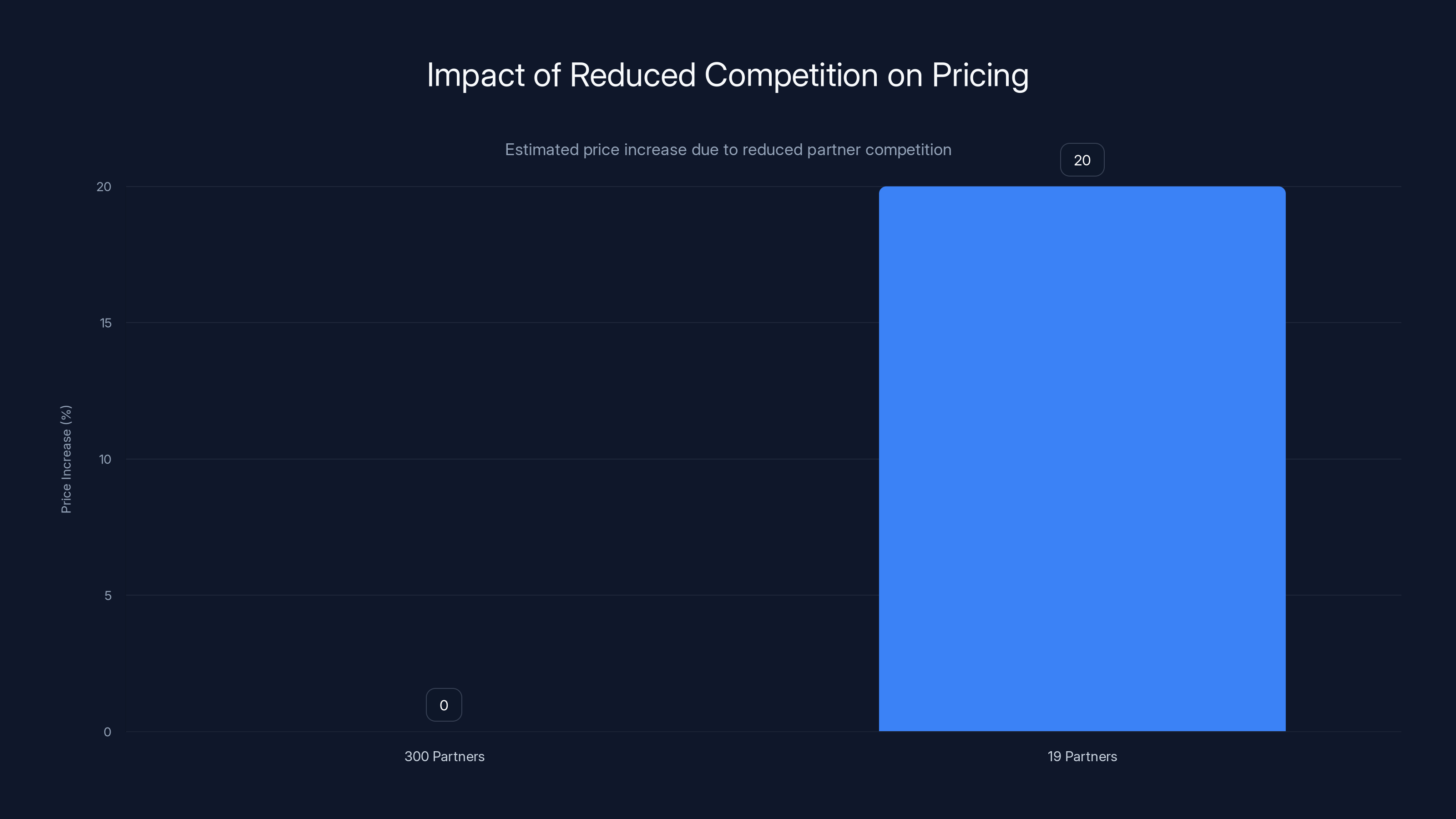

Estimated data suggests that reducing the number of partners from 300 to 19 could lead to a 15-25% price increase due to decreased competition.

The Numbers: How Many Partners Just Lost Their Business?

This is where things get concrete.

The Advantage Partner Program had hundreds of certified partners across Europe alone. When CISPE says "hundreds of European CSPs will lose their ability to resell VMware software," they're not being dramatic. They're being accurate.

In the United States, only 19 CSPs remain with Advantage Partner status. Think about that. The world's largest virtualization software platform, deployed in probably 60-70% of enterprise data centers globally, has exactly 19 partners in the US market. That's not a partner program. That's controlled distribution.

Europe is heading the same direction. Partners like Wave Com just joined CISPE specifically to oppose this consolidation. That's not a coincidence. These are providers who saw the writing on the wall and realized their VMware resale business was about to evaporate.

The financial impact varies by partner. Some CSPs built 20-30% of their revenue around VMware licensing. For them, this isn't just a policy change. It's an existential threat. They either pivot to other technologies (like Open Stack, Proxmox, or o Virt), find a new vendor, or consolidate with larger competitors.

Why Broadcom Did This: The Semiconductor Mindset

Understanding Broadcom's logic is critical to predicting what happens next.

Broadcom's core business is semiconductors. The company manufactures infrastructure chips, networking equipment, and storage controllers. It's an engineering-driven, margin-focused business. When you're designing chips, your unit economics are simple: engineer costs, manufacturing costs, gross margin. You optimize for scale and efficiency.

Software is different. Software has network effects. Software benefits from a diverse ecosystem of partners. VMware's success, over 20+ years, came from being the open platform that everybody built around. Third-party vendors integrated with VMware. Partners customized VMware for specific industries. This ecosystem created lock-in, but it was lock-in through value, not through restriction.

Broadcom doesn't think that way. Broadcom thinks in terms of direct relationships, direct sales, and direct margins.

CEO Hock Tan has already signaled this shift repeatedly. In earnings calls, he's talked about "streamlining" the VMware business, moving to more "direct customer engagement," and implementing "efficient go-to-market models." In corporate speak, that means: we're cutting out the middleman, consolidating partners, and taking customer relationships in-house.

It makes financial sense from Broadcom's perspective. Direct customer relationships generate higher margins. You don't share revenue with a partner. You control the entire customer relationship from licensing through support. You can implement aggressive price increases without negotiating with 500+ partners.

But here's the problem: this strategy only works if customers have nowhere else to go. And spoiler alert, they do.

The Advantage Partner Program involved VMware as the vendor, CSPs as partners, and end customers, with CSPs playing the largest role in maintaining customer relationships and providing localized support. Estimated data.

The European Backlash: CISPE's Warning

Europe is not happy about this.

CISPE released a formal statement in December 2025 (before the partner program termination) accusing the European Commission of "failing to properly assess the risks associated with Broadcom's acquisition." The organization called out the regulatory body for essentially rubber-stamping the deal without understanding the consolidation implications.

"By rubber stamping the deal, Brussels handed Broadcom a blank cheque to raise prices, lock-in and squeeze customers," wrote CISPE Secretary General Francisco Mingorence.

This isn't vague criticism. CISPE is predicting exactly what will happen: price increases, customer lock-in, and competitive squeezing. And they're blaming European regulators for not blocking or conditioning the acquisition.

Why should Europe care differently than the US?

Because data sovereignty matters more in Europe. The EU has GDPR, the Digital Markets Act, and other regulations that require European data to be processed and stored according to European standards. When you have hundreds of small to mid-sized CSPs, you have options. When you have 19 partners, you have a concentration risk.

A European bank might be comfortable with Customer A, a local CSP, managing their VMware infrastructure because Customer A is bound by EU regulations and can't offshore their data. If Customer A goes out of business (because they lost VMware resale rights), the bank has limited options. The remaining VMware partners might be owned by Broadcom or by multinational companies that are less constrained by European regulations.

That's the sovereignty argument. It's not theoretical. It's actively happening as European CSPs lose their ability to compete.

Market Consolidation: The US Pattern, Now Playing in Europe

Here's what happened in the United States, and it's instructive for where Europe is heading.

Broadcom didn't announce the Advantage Partner Program termination as a global policy. It started with the US market. Partners got individual letters saying their partnerships wouldn't be renewed. Some were offered paths to stay as "select partners," but the requirements increased dramatically (higher volume commitments, exclusive focus on Broadcom solutions, etc.). Others got polite rejection letters.

The result: from probably 200-300 partners in 2023, down to 19 by 2026. That's consolidation in real time.

Now the same pattern is rolling out in Europe. Partners are getting notified that their contracts won't renew. They're being told a "new program" exists, but participation is limited and requirements are steep. It's the same playbook.

Why does this happen? Because it's profitable, and there's limited recourse for partners.

When you have a successful business built on a vendor relationship, you're trapped. You can't sue. You can't appeal to regulators (they already approved the deal). Your only options are:

- Try to meet the new, stricter requirements (usually impossible)

- Exit the business

- Pivot to a different vendor (takes 2-3 years, costs money)

Most partners choose option 2 or 3. The market consolidates. Broadcom's partner count drops from 300 to 19. But Broadcom's direct revenue increases because customers have nowhere else to go.

It's not a bug in Broadcom's strategy. It's the feature.

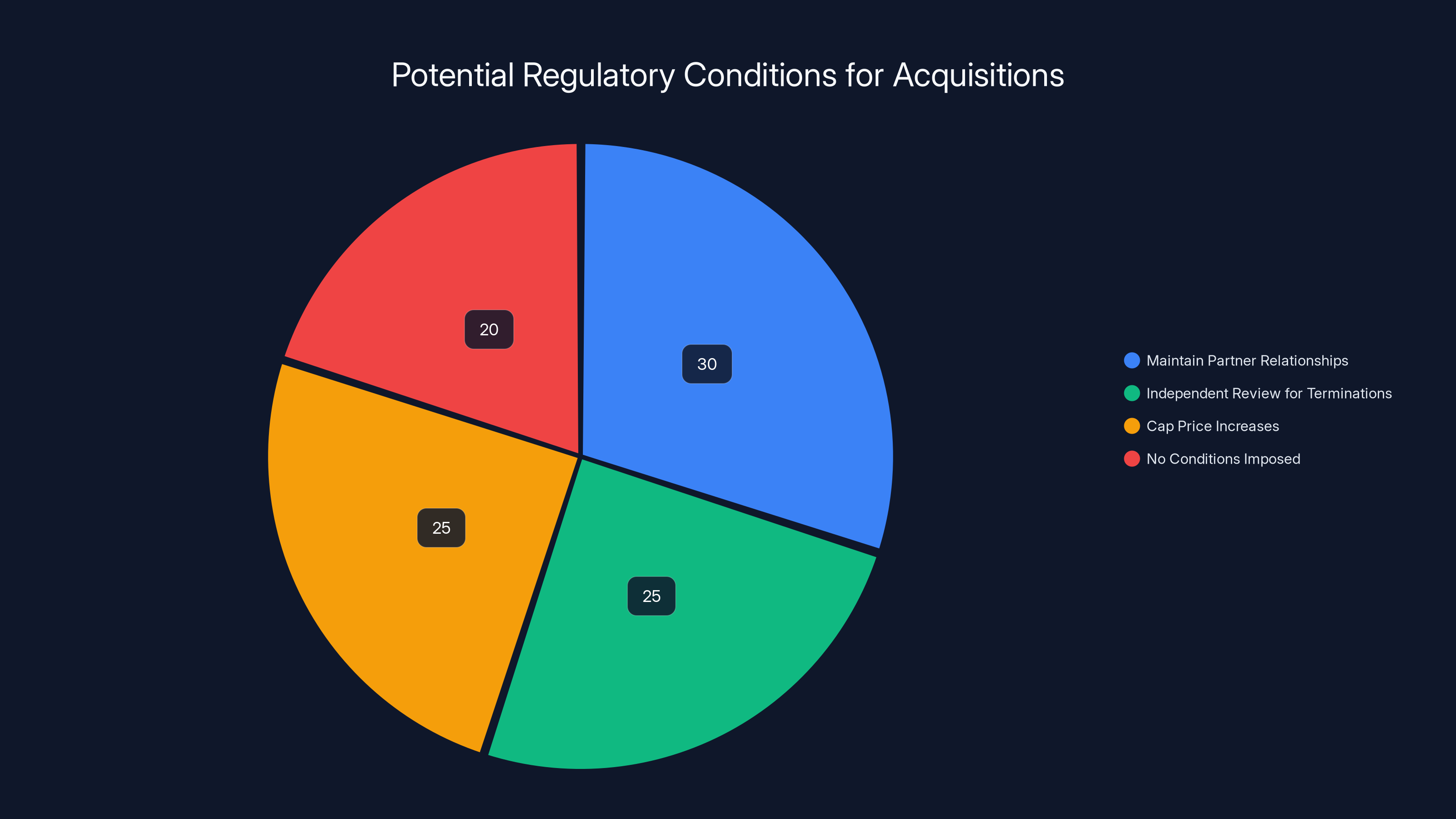

Estimated data showing potential conditions the EU could have imposed on Broadcom's acquisition of VMware. No conditions were imposed, leading to market consolidation.

Pricing Implications: The Consolidation Tax

Let's talk about what this means for prices.

When you have 300 competing partners, price pressure is constant. Partner A undercuts Partner B. Customer C shops around. Everybody's chasing market share, which means discounts, flexible terms, and competitive packages.

When you have 19 partners, there's no shopping around. You contact the partner that serves your region or industry. They quote you. You either accept or you switch to a different hypervisor (which takes months and costs money). That's not a negotiation. That's a take-it-or-leave-it scenario.

Broadcom has already demonstrated pricing aggressiveness. When they took over VMware, they implemented new licensing models that confused customers and, in many cases, doubled costs for existing customers. VMware Cloud Foundation, Broadcom's new "strategic" product, costs significantly more than v Sphere under the old pricing model.

With fewer partners, Broadcom can push these new models harder. Partners can't negotiate volume discounts because they're competing with 18 other partners for the same pool of customers. And customers can't leverage competitive pressure because there's no competition.

Historically, industry analysts have estimated that partner competition creates 15-25% pricing pressure compared to vendor direct models. Losing that competitive friction could translate to 15-25% price increases for VMware workloads over 2-3 years.

For a mid-sized enterprise running 50-100 v Sphere hosts, that could mean

The Sovereignty Trap: European Businesses at Risk

Europe has a unique problem that the US doesn't: sovereignty requirements.

When a German bank stores customer data in a VMware infrastructure, there are regulatory expectations that this infrastructure is controlled by a German or European entity. When you consolidate from 50 European partners to 5, you lose that diversity. You end up with vendors that might be subsidiaries of US companies, or companies that have complex multinational ownership structures.

This creates vendor lock-in with a sovereignty dimension. A German bank can't easily switch their infrastructure because:

- They're committed to a multi-year contract with their CSP

- Most CSPs are now affiliated with larger multinational corporations

- Switching to another hypervisor (Open Stack, Proxmox, etc.) takes 18+ months and costs millions

- They're stuck

The sovereignty risk goes deeper. If a European CSP wants to negotiate better terms with Broadcom, they can't. Broadcom controls the licensing. The CSP is just a reseller. But the CSP is also the customer's primary relationship manager and infrastructure operator. If the CSP goes out of business (because they lost Advantage Partner status), the customer loses their trusted advisor.

EU regulators should have anticipated this. Some did. But the approval process happened anyway, and now the consolidation is real.

Broadcom's consolidation reduced VMware partners from over 300 to fewer than 20, significantly concentrating the market. (Estimated data)

How Partner Consolidation Affects End Customers

Let's get practical: how does this actually impact you if you're running VMware in production?

Choice narrows. You probably had 3-5 CSP options in your region. Now you have 1-2. Your next renewal conversation will be different. Your current CSP might not exist. The new partner might require different terms, higher minimums, or exclusive commitments.

Support quality varies. Not all 19 remaining US partners are equal. Some are strong on infrastructure, weak on application-layer support. Some are regional, others national. Consolidation means you might end up with a partner that's good in one area but not yours. Broadcom doesn't care. They got paid.

Pricing rigidity increases. When you have competition, you can negotiate. When you have limited options, negotiating leverage disappears. CSPs might argue they need better terms with Broadcom to serve you better, but Broadcom just got more direct and more expensive. That cost passes through.

Innovation slows. Competitive partners innovate because they need differentiation. They build custom solutions, develop industry-specific expertise, create services that partners offer, not Broadcom. When partners consolidate, you lose this innovation layer. Broadcom's direct model is efficient but generic.

Transition costs spike. If you want to switch off VMware, you need help. A good CSP provides expertise for migration, understands your workloads, and can guide you to alternatives. When partners are scarce, finding migration help becomes expensive. Broadcom won't help you switch off their product. Your new partner might be unfamiliar with your infrastructure.

None of this is catastrophic immediately. But over 2-3 years, the cumulative effect is substantial. Customers pay more, get less choice, receive worse service, and experience higher switching costs.

The Broadcom Justification: What They Actually Say

Broadcom hasn't issued a formal statement defending the Advantage Partner Program termination, but the company's messaging has been consistent in other contexts.

Broadcom's line: "We're focusing on customer requirements and delivering the best possible VMware Cloud Foundation experience."

Translation: We're moving from a distributed partner model to a concentrated direct model because it's more profitable and we think customers will pay for it.

Broadcom also argues that consolidation means faster decision-making. With fewer partners, the company can communicate changes more efficiently, roll out new features faster, and maintain consistent customer experience.

There's a grain of truth here. Sometimes centralization is more efficient. But there's a cost: you lose the diversity of thought that comes from 300+ independent organizations thinking about how to apply your product.

Broadcom's growth targets also matter. When you acquire a mature company like VMware, investors expect you to dramatically increase profitability. You don't do that by maintaining the status quo. You do it by consolidating costs, raising prices, and reducing complexity. The Advantage Partner Program termination is a move toward those financial targets.

It's not surprising. It's inevitable when a semiconductor-focused acquirer takes over a software company with a distributed ecosystem.

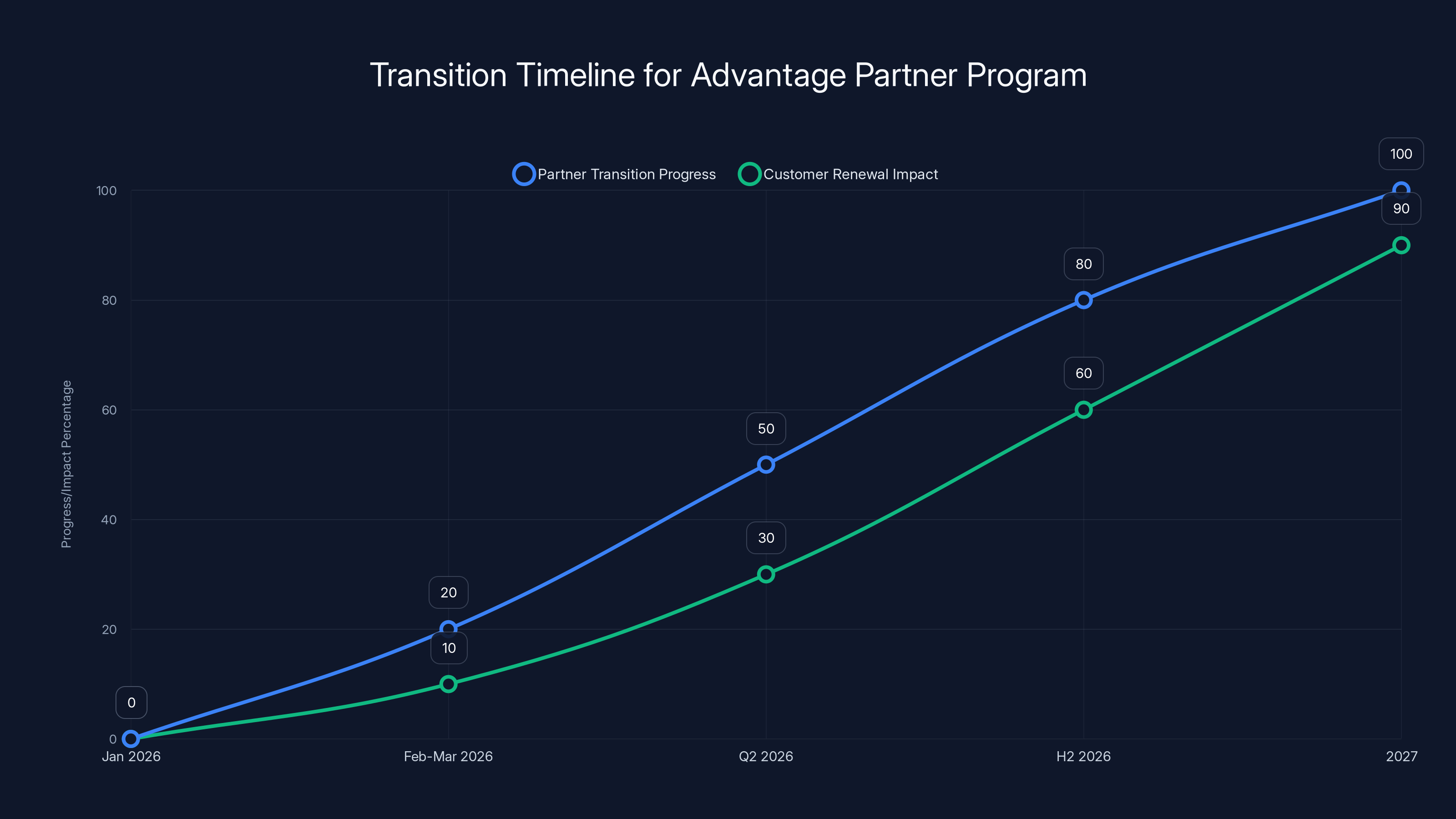

The timeline shows the transition progress of partners and the impact on customer renewals. By 2027, the full effects of the transition are expected to be visible. Estimated data.

Alternatives to VMware: The Realistic Options

For CSPs and customers looking for exit strategies, here are the real alternatives.

Open Stack. The nonprofit organization has been building an open-source cloud computing platform for 15 years. It's complex, requires deep expertise, but offers complete architectural freedom. If you're a CSP considering moving away from VMware, Open Stack is credible. But migration is hard. You're retraining staff, adopting new tools, and managing a multi-year project.

Proxmox. A simpler alternative focused on small to mid-sized virtualization. Proxmox is easier to deploy than Open Stack, has a much smaller learning curve, and is significantly cheaper. It's not as feature-rich as VMware, but for many workloads, it's sufficient.

Public cloud hyperscalers. AWS, Microsoft Azure, and Google Cloud all offer migration programs for VMware customers. They'll help you move workloads, co-invest in migration costs, and provide infrastructure you control through their platforms. It's not a purely technical alternative (you're moving to managed services), but it solves the vendor lock-in problem by switching to a bigger lock-in.

KVM-based platforms. o Virt, Red Hat Virtualization, and other KVM derivatives offer another path. They're less mature than VMware but significantly cheaper and open-source-friendly.

None of these are simple swaps. They all require investment in training, tooling, and migration. But they all offer an escape from the Broadcom consolidation trap.

The reality: customers aren't trapped. They're just facing a non-trivial cost to escape. And that cost is expensive enough that many will stay, accept higher prices, and grumble. Which is exactly what Broadcom is betting on.

The Regulatory Question: Did European Authorities Miss Something?

This is the hard question CISPE raised.

When Broadcom acquired VMware, the European Commission had authority to block or condition the deal. The EU's merger regulations allow intervention if a deal threatens "effective competition" in relevant markets.

Did Broadcom's acquisition threaten effective competition in the virtualization market? Arguably yes. The company controls the dominant hypervisor (v Sphere), now controls the strategic evolution of VMware software, and can unilaterally change licensing, pricing, and partner policies.

But here's the challenge: predicting ecosystem behavior after an acquisition is hard. The Commission can't say, "We think Broadcom might consolidate partners in 2-3 years." They need evidence now. And at the time of approval (2023), Broadcom was publicly committed to supporting VMware's partner ecosystem.

Two years later, Broadcom is systematically dismantling that ecosystem.

Was this foreseeable? Probably. Broadcom's CEO has been clear about his acquisition philosophy: buy growing companies, integrate them, and optimize for profitability. That philosophy is incompatible with distributed partner ecosystems.

Should the Commission have blocked the deal? That's a policy question. But at minimum, it could have imposed conditions: "Broadcom must maintain X number of partner relationships for Y years," or "Partner terminations must be approved by independent review," or "Price increases are capped at Z% for P years."

None of those conditions were imposed. The deal closed. And now consolidation is happening.

This is a test case for how regulators approach acquisitions of ecosystem-dependent companies. The EU might be learning a lesson: when you approve an acquisition, the acquirer has the power to reshape entire ecosystems. Better to condition that power upfront than to complain about it afterward.

What Broadcom Should Have Done (And Why They Didn't)

Here's the counterfactual: what if Broadcom took a different approach?

Imagine if Broadcom had announced: "We're investing $2 billion in partner enablement. We're expanding the Advantage Partner Program, adding partners in emerging markets, and creating dedicated support for partners. We believe VMware's strength comes from ecosystem diversity."

That would have:

- Signaled commitment to partners

- Reduced consolidation risk

- Created goodwill with regulators

- Potentially increased market share (new partners = new customers)

But it wouldn't have maximized short-term profitability. Broadcom's financial targets require the opposite strategy: consolidation, direct customer relationships, and margin expansion.

This is the tension between sustainable business strategy and financial optimization. Broadcom chose optimization. The cost is competitive risk, regulatory scrutiny, and customer dissatisfaction. The benefit is higher near-term margins.

For Broadcom's shareholders, that might be the right trade. For customers and partners, it's clearly not.

Timeline: What's Happening When

Let's get specific about the calendar.

January 26, 2026. The Advantage Partner Program officially terminates. Existing contracts expire. Partners can either transition to the new "select partner" program (if approved) or exit the business. This date already passed (as of the information provided), so we're now in the transition period.

February-March 2026. Partners are scrambling to understand the new program, negotiate new terms (or accept they won't), and figure out transition plans. Some are joining CISPE to coordinate response. Others are already planning migrations to alternative platforms.

Q2 2026. The new partner base stabilizes. A subset of the 300 original partners have been approved for the new program (probably 15-30% of the original base). The rest are exiting. Customers are beginning renewal conversations with either their existing partner (if approved) or new vendors.

H2 2026. Price increases become visible. The first major contract renewals under the consolidated partner model happen. Customers see the impact of reduced competition. Early migration projects to alternative platforms begin.

2027. We see the full impact. Market share data shows whether customers stuck with VMware or moved to alternatives. If too many move, Broadcom might adjust strategy. If most stay, consolidation succeeded and becomes the template for future acquisitions.

This isn't speculation. This is how these things work in enterprise IT. Change takes time. Impact is lagged. But it's coming.

How to Prepare: Actionable Steps

If you're affected by this consolidation, here are concrete steps.

For CSPs who lost partner status:

-

Immediately audit your customer base. Understand who depends on VMware, how much of their infrastructure is VMware, and what their contract terms look like. This is your bargaining position.

-

Approach customers proactively. Don't wait for them to hear about your partner status change from Broadcom. Call them. Explain the situation. Offer alternatives (migration planning, architecture review, competitive analysis).

-

Build an escape plan. Evaluate Proxmox, Open Stack, KVM, or public cloud migrations for your customer base. Get certified or trained on alternatives. You're no longer "VMware-focused." You're "virtualization-agnostic."

-

Join industry groups. CISPE is the obvious choice in Europe. But also consider technology-specific groups (Open Stack Foundation, etc.). You need allies and visibility.

-

Document the impact. Keep detailed records of lost revenue, affected customers, and transition costs. If regulators eventually open an investigation, this data matters.

For customers with VMware infrastructure:

-

Know your vendor landscape. Who's your CSP partner? Did they keep Advantage Partner status? If not, who's your next option? Don't find out during contract renewal.

-

Assess alternatives. Evaluate what it would cost to move off VMware. What's the migration timeline? What's the resource cost? Know your options before you're forced to make a decision.

-

Negotiate now. If your current contract expires soon, negotiate multi-year terms before consolidation drives prices up. Lock in rates while you have leverage.

-

Explore cost optimization. Broadcom's new pricing model might mean your existing v Sphere infrastructure is more expensive than you think under the new licensing. Work with your partner to understand the real cost of your infrastructure.

-

Invest in diversity. Don't build your entire infrastructure around VMware. Mix in KVM, containers, or public cloud. Reduce your vendor concentration risk.

These aren't dramatic steps. They're risk management. But they matter more now than they did a year ago.

The Bigger Picture: Consolidation As an Industry Trend

This isn't unique to Broadcom and VMware.

We're seeing similar consolidation across enterprise software:

- Salesforce has been consolidating its partner channel, pushing more customers toward direct relationships

- Oracle has steadily reduced the number of partners it works with, focusing on larger strategic partners

- Microsoft has the most diverse partner network in the industry, but even Microsoft is consolidating around strategic partnerships

The pattern is clear: mature software companies under financial pressure consolidate their channels. It's profitable short-term. It creates risk long-term.

For enterprise customers, this means vendor consolidation should be a major strategic concern. When you adopt a new software platform, ask: "What's this company's historical approach to partners?" If they're consolidating, you're on the wrong side of that consolidation.

For partners, diversification is increasingly critical. Don't build a business around a single vendor. Mix multiple platforms, develop specialized services, and maintain customer relationships through value, not vendor dependency.

Broadcom's partner consolidation is a symptom of a broader trend: enterprise software margins are being squeezed, so companies are consolidating cost and increasing pricing. You need to plan for that.

FAQ

What exactly is the VMware Advantage Partner Program?

The VMware Advantage Partner Program was Broadcom's (previously VMware's) framework that allowed independent Cloud Service Providers (CSPs) to purchase VMware licenses at partnership pricing and resell them to their own customers. The program enabled hundreds of regional and mid-sized providers to build businesses around VMware virtualization technology, offering localized support, customization, and relationship management. Partners could maintain long-term customer relationships while VMware accessed broader market distribution.

Why did Broadcom end the Advantage Partner Program?

Broadcom terminated the program to consolidate its go-to-market strategy and increase direct customer relationships, which generate higher margins. The acquisition of VMware gave Broadcom a mature software business that didn't align with the company's financial optimization targets. By narrowing the partner base from 300+ partners to approximately 19 in the US, Broadcom reduced operational complexity, increased direct pricing control, and created conditions where fewer competitors can pressure pricing downward. This strategy prioritizes short-term profitability over ecosystem diversity and customer choice.

How many CSPs were affected by the partner program termination?

Hundreds of Cloud Service Providers were affected, particularly in Europe where CISPE (Cloud Infrastructure Services Providers in Europe) represents the interests of regional providers. In the United States, only 19 CSPs retained or gained Advantage Partner status, down from an estimated 200-300 previously. Europe is following the same consolidation pattern, with partner numbers dropping dramatically as the new "select partner" program limits entry criteria and volume requirements increase significantly.

What does this mean for VMware pricing?

Pricing is likely to increase 15-25% over the next 2-3 years as partner competition diminishes. With fewer vendors competing for customers, the pricing pressure that partners previously created (through discounts, competitive packages, and flexible terms) disappears. Broadcom has already demonstrated aggressive pricing through new licensing models like VMware Cloud Foundation, which costs substantially more than legacy v Sphere pricing for equivalent features. Consolidation gives Broadcom the leverage to push these pricing models harder without customer alternatives.

What are the alternatives to VMware for customers?

Practical alternatives include Open Stack (open-source, feature-complete but complex), Proxmox (simpler, more affordable, suitable for SMBs), public cloud hyperscalers like AWS or Azure (managed services with different pricing models), and KVM-based platforms like o Virt. Each alternative requires significant investment in migration, training, and tooling, making them non-trivial switches but realistic escape routes from VMware lock-in.

How does this affect European data sovereignty?

European data sovereignty becomes riskier under consolidation because fewer CSPs remain as options for customers subject to GDPR and other EU regulations. A consolidated partner base means European businesses have fewer "trusted local provider" options, potentially forcing them to work with larger multinational corporations less constrained by European regulatory requirements. Additionally, if a primary CSP partner exits due to lost partner status, European customers lose continuity with their infrastructure operator, creating compliance and operational risk.

Could European regulators reverse or modify this decision?

Theoretically, the European Commission could investigate the consolidation under the Digital Markets Act (DMA) or existing competition law, but reversing an already-approved acquisition is difficult. More likely, regulators might impose conditions on future Broadcom conduct or use this case as a precedent for conditioning acquisitions of ecosystem-dependent companies. CISPE has called for regulatory action, but by the time any intervention occurs, the consolidation will likely be complete, making remedies difficult to implement.

Should my company migrate away from VMware now?

Not necessarily immediately, but you should develop a migration plan as insurance. If your current CSP partner retained Advantage Partner status, you have time. Negotiate multi-year contracts at favorable rates while you can. But simultaneously evaluate alternatives and begin tactical migrations (test environments, non-critical workloads) to understand the real cost and complexity of switching. Don't wait until contract renewal forces a decision under time pressure and consolidation has driven prices even higher.

How does this affect companies already using VMware Cloud Foundation?

Companies using VMware Cloud Foundation face less CSP partner choice but potentially smoother operations, since VCF is Broadcom's strategic product (it's what Broadcom wants to push). Consolidation might actually accelerate VCF adoption as the path of least resistance. However, VCF customers are locked more deeply into the Broadcom ecosystem, with fewer providers capable of specialized support or customization. This creates both operational benefits (standardization) and strategic risk (vendor lock-in).

The Path Forward: What Happens Next

Broadcom's partner consolidation will have ripple effects for years.

In the next 12 months, expect customer confusion as partner transitions happen. Some won't know their CSP lost status until renewal conversations start. Broadcom will frame this as a positive ("we're focused on quality partners"), customers will see it as negative ("fewer options, higher prices"), and IT departments will start concrete migration evaluations.

In 18-24 months, you'll see measurable migration away from VMware toward alternatives. It won't be massive (VMware has too much installed base), but the trend will be visible. Hyperscaler cloud migrations will accelerate as customers use consolidation as a forcing function to finally make the infrastructure decisions they've been postponing.

By 2027-2028, Broadcom will have optimized VMware for profitability, consolidated the partner base, and extracted higher margins. The company will claim success. Meanwhile, VMware's market share will have eroded 5-10% to alternatives, and competitive dynamics will have shifted. New vendors will have gained visibility. The ecosystem will have diversified away from VMware lock-in.

This is how consolidation plays out in enterprise software. It's profitable for the acquirer. It's painful for partners and creates friction for customers. But the fundamental trend is inevitable when financial optimization becomes the driver.

The question for customers and partners isn't whether consolidation will happen. It's whether they'll be ready when it does.

Key Takeaways

Here's what actually matters:

-

Consolidation is real. Broadcom didn't just slightly adjust VMware's partner program. The company dramatically reduced the available partners from 300+ to fewer than 20, creating a concentrated market.

-

Prices will increase. When partner competition disappears, pricing leverage disappears with it. Expect 15-25% cumulative price increases over the next 2-3 years as consolidation takes full effect.

-

Customer choice diminishes. Fewer partners means fewer options for customers evaluating VMware relationships. Shopping around becomes impossible when only 2-3 providers exist in your region.

-

European sovereignty is at risk. The EU's regulatory framework assumes diverse market participants. Consolidation reduces that diversity, creating compliance and operational risk for regulated businesses.

-

Alternatives exist, but migration is expensive. Open Stack, Proxmox, public cloud, and KVM alternatives are real escape routes, but they require significant investment and time. They're not simple plug-and-play replacements.

-

This is industry trend, not anomaly. Broadcom isn't unique. Enterprise software companies under financial pressure are consolidating channels across the industry. This is a signal to audit your vendor relationships broadly.

-

Preparation matters more than panic. Whether you're a CSP or customer, the time to act is now, while you still have leverage. Waiting until consolidation is complete means negotiating from a position of weakness.

Broadcom's "bulldozer" will continue rolling. It won't stop because it's profitable. But you can prepare for it.

Related Articles

- A Knight of the Seven Kingdoms Episode 4 HBO Max Release Date [2025]

- Best Noise-Canceling Earbuds for 2025: Expert Reviews [2025]

- Surfshark One at $2.29/Month: Best VPN Deal [2025]

- Best Home Theater Projectors for 2026: 4K, Laser & UST Guide

- AI Notetaking Devices: The Complete Guide to Smart Recording Hardware [2025]

- Dyson Clean+Wash Hygiene Review: Is This Hybrid Vacuum Worth It? [2025]