China's Renewable Energy Revolution: Global Impact & Grid Challenges 2025

Introduction: The Unstoppable Green Energy Tsunami

When science fiction enthusiasts imagine a utopian future powered by limitless clean energy, they typically envision fusion reactors harnessing the power of stars. Yet the actual transformation happening right now looks far less elegant and significantly more chaotic. China has unleashed a renewable energy revolution operating at scales that defy intuition, creating an unprecedented global scramble that's simultaneously solving climate challenges while destabilizing energy markets worldwide.

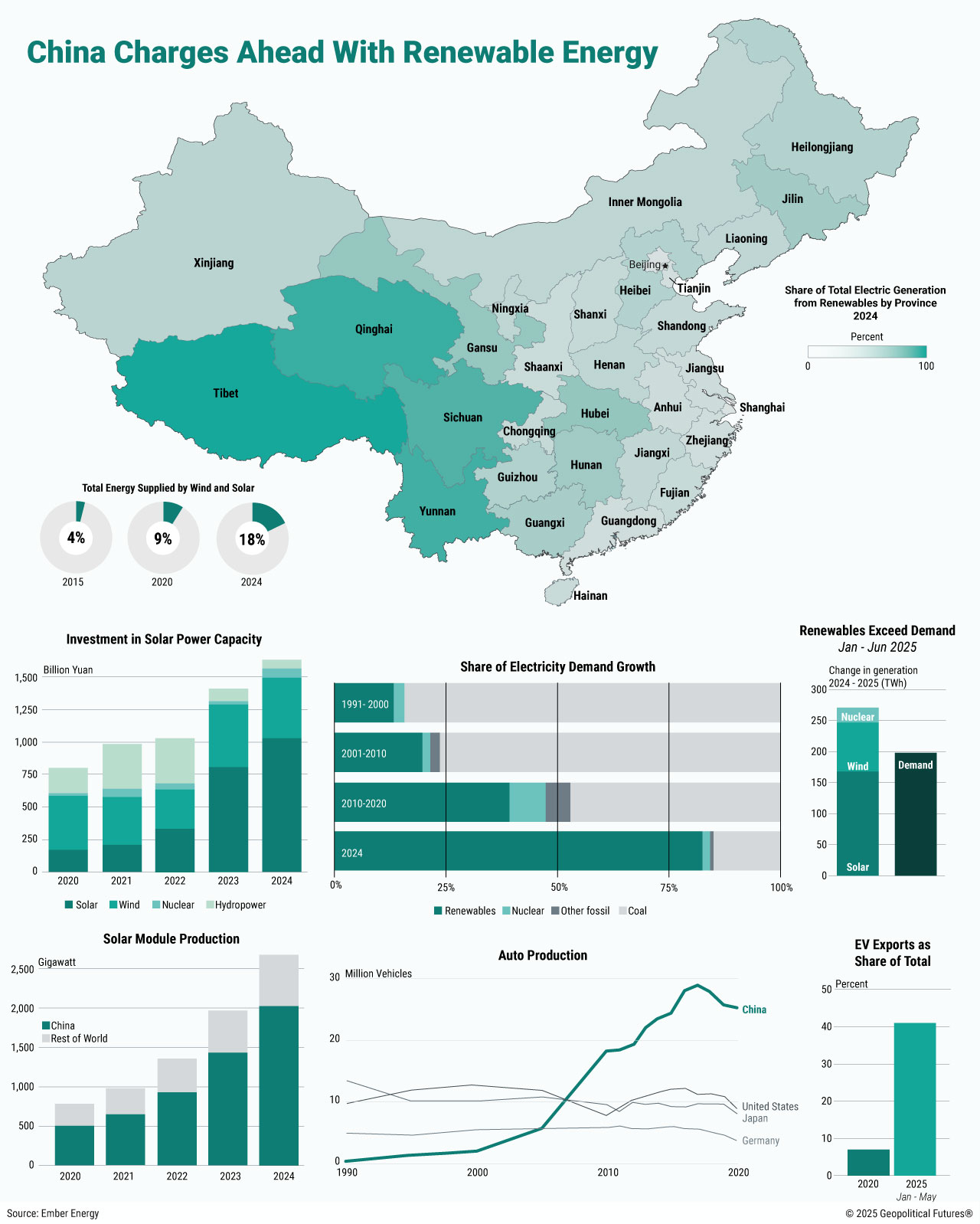

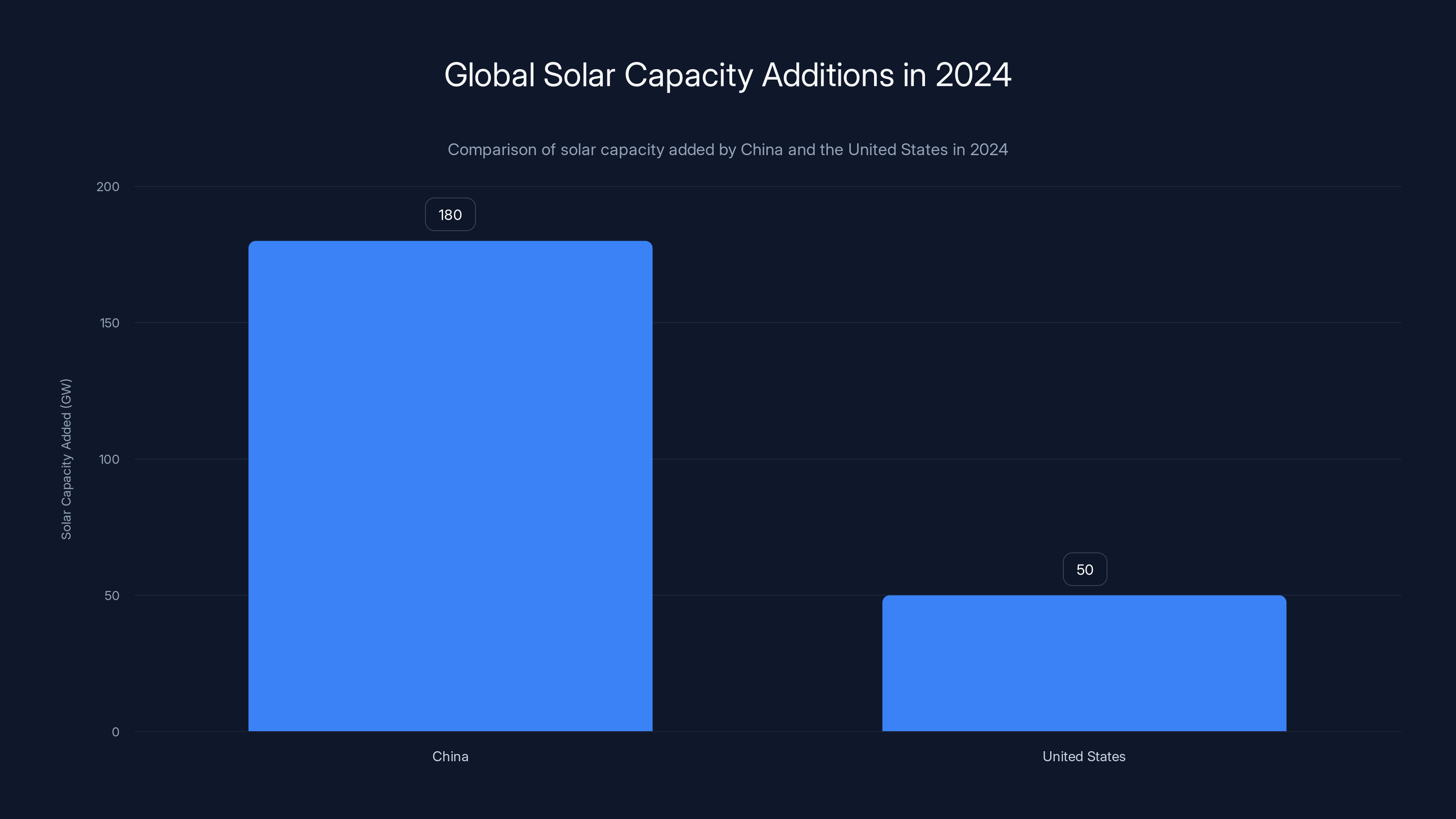

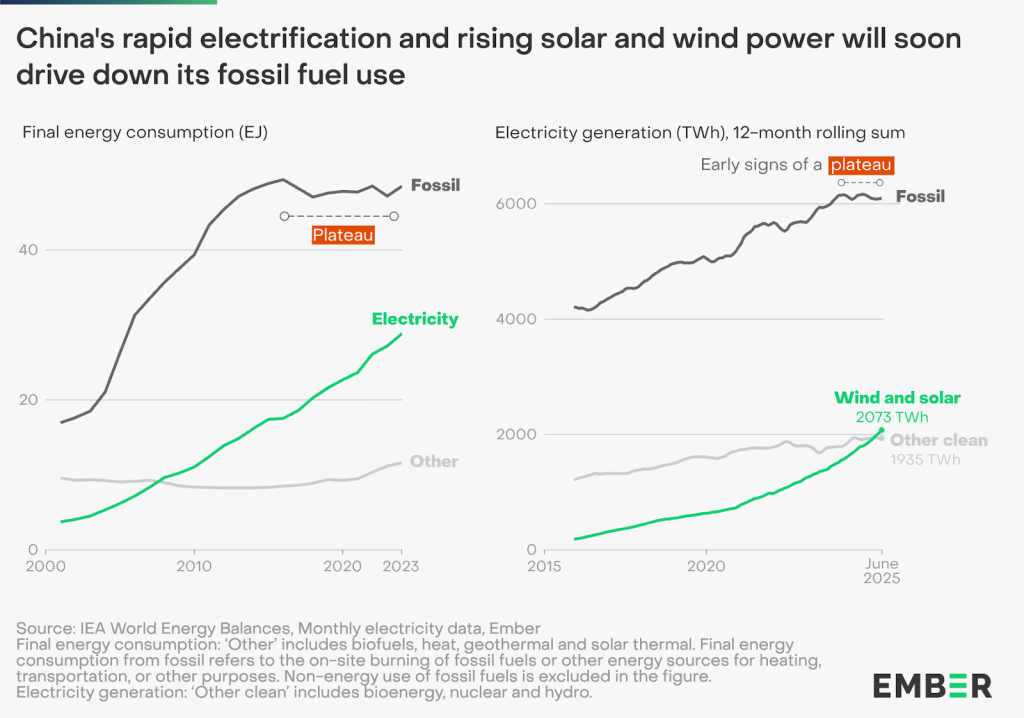

The statistics alone border on science fiction. In 2024, the planet's total installed electricity capacity—encompassing every coal plant, gas turbine, nuclear reactor, wind farm, and solar installation—totaled approximately 10 terawatts. Strikingly, China's solar manufacturing supply chain now produces enough photovoltaic panels annually to generate 1 terawatt of capacity every single year. To contextualize this: the United States, celebrating record renewable deployment in 2024, added approximately 50 gigawatts of solar capacity over twelve months. During the same period, China added over 180 gigawatts in just the first five months of 2025, driven by a manufacturing surge before policy changes took effect as reported by Electrek.

This explosion isn't confined to distant desert installations. Across China's landscape, solar panels blanket rooftops in residential neighborhoods, industrial factories sprawl with photovoltaic arrays, and vast energy megabases combining solar and wind installations stretch across western deserts and Tibetan highlands for hundreds of miles. These singular installations generate power equivalent to multiple nuclear plants, transmitted eastward via ultrahigh-voltage power lines to population centers demanding constant electricity.

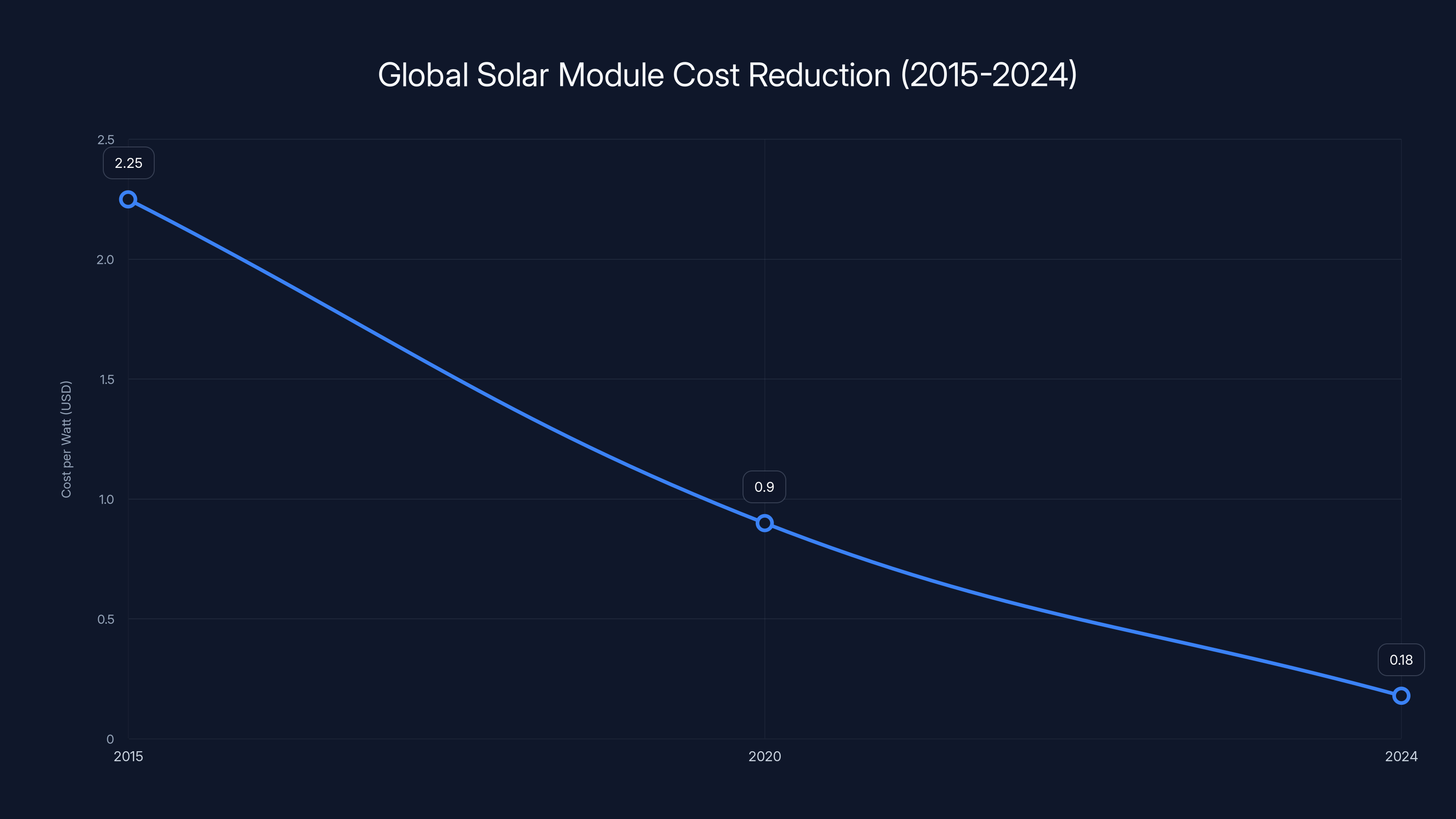

The global market impact proves equally dramatic. Chinese manufacturers have driven photovoltaic panel costs so low that in European markets, they now cost less than conventional fencing materials. Globally, the cascading price competition has compressed the average cost of solar-generated electricity to approximately 4 cents per kilowatt-hour—potentially the cheapest electricity ever produced by any technology, anywhere. This represents a stunning 90% cost reduction compared to solar pricing a decade ago according to Bloomberg.

Yet beneath this ostensible green energy success story lurks a fundamentally different narrative: one of market chaos, destabilized electrical grids, decimated coal communities, devastating price wars, and policy dysfunction that extends globally. While mainstream media increasingly acknowledges China's renewable dominance, coverage consistently understates the profound turbulence reshaping energy systems. This isn't a carefully orchestrated government program but rather a runaway competitive frenzy with consequences nobody anticipated and even fewer entities control. The resulting transformation presents simultaneously as an emerging utopia and an unfolding disaster.

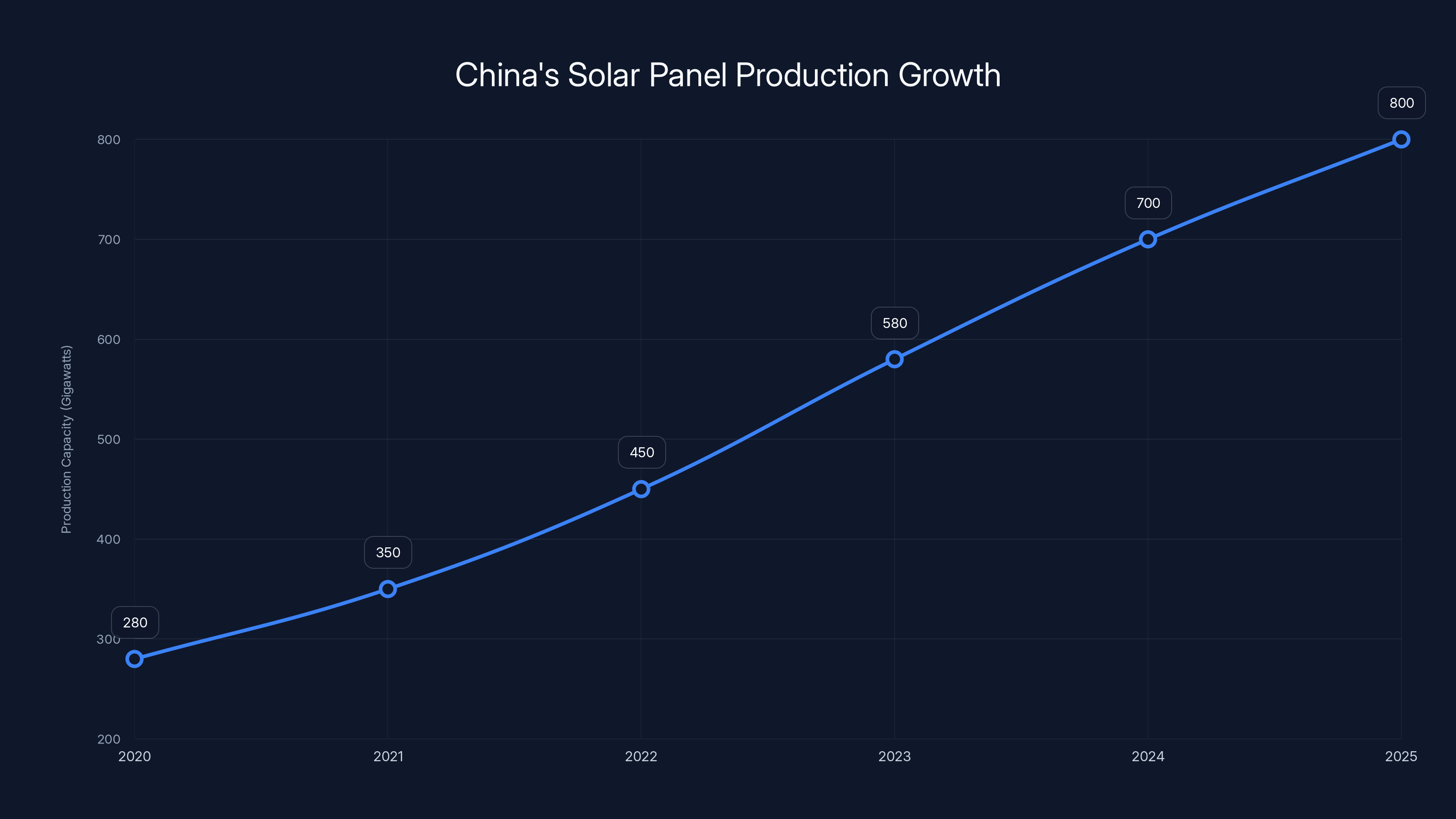

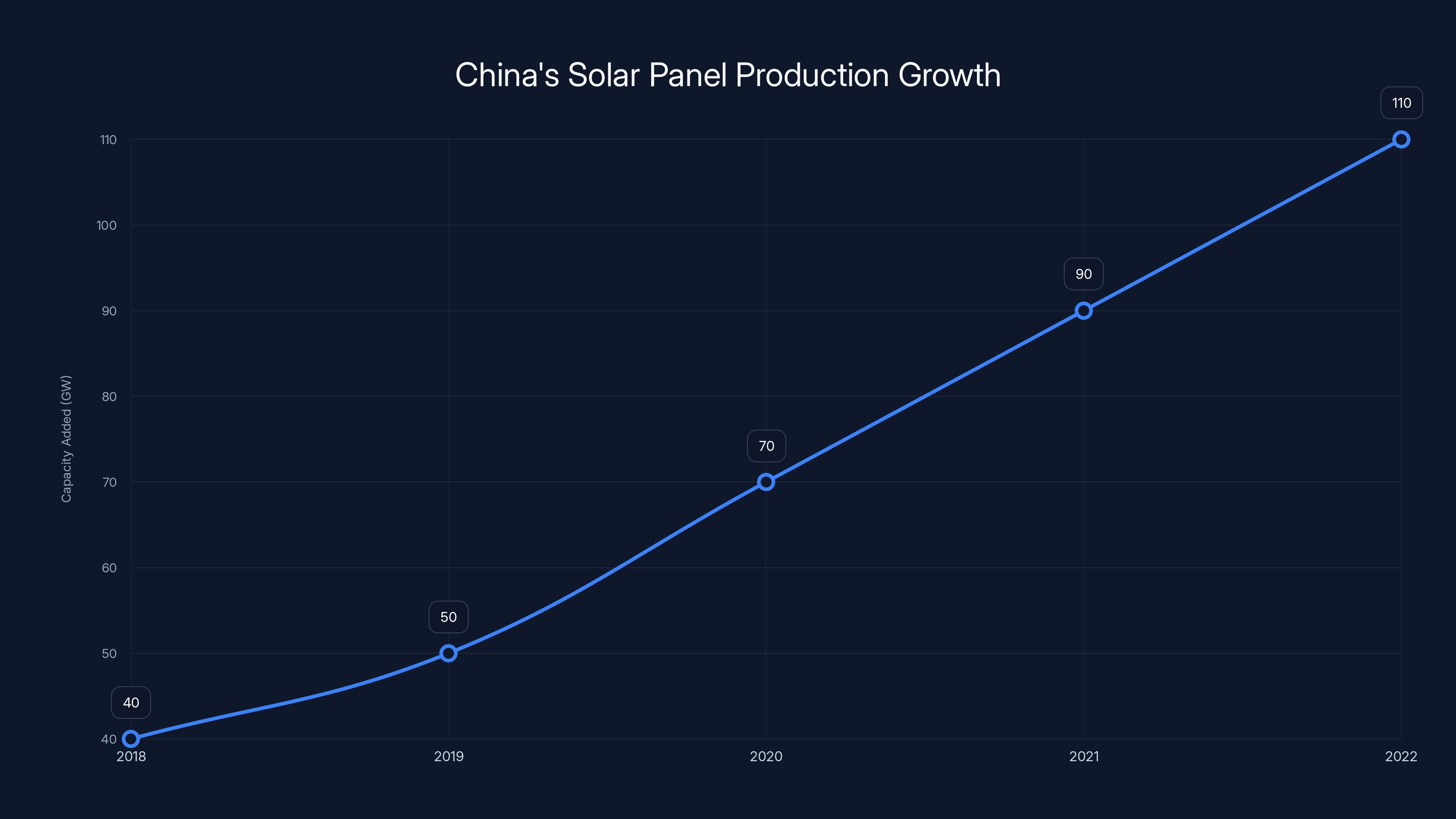

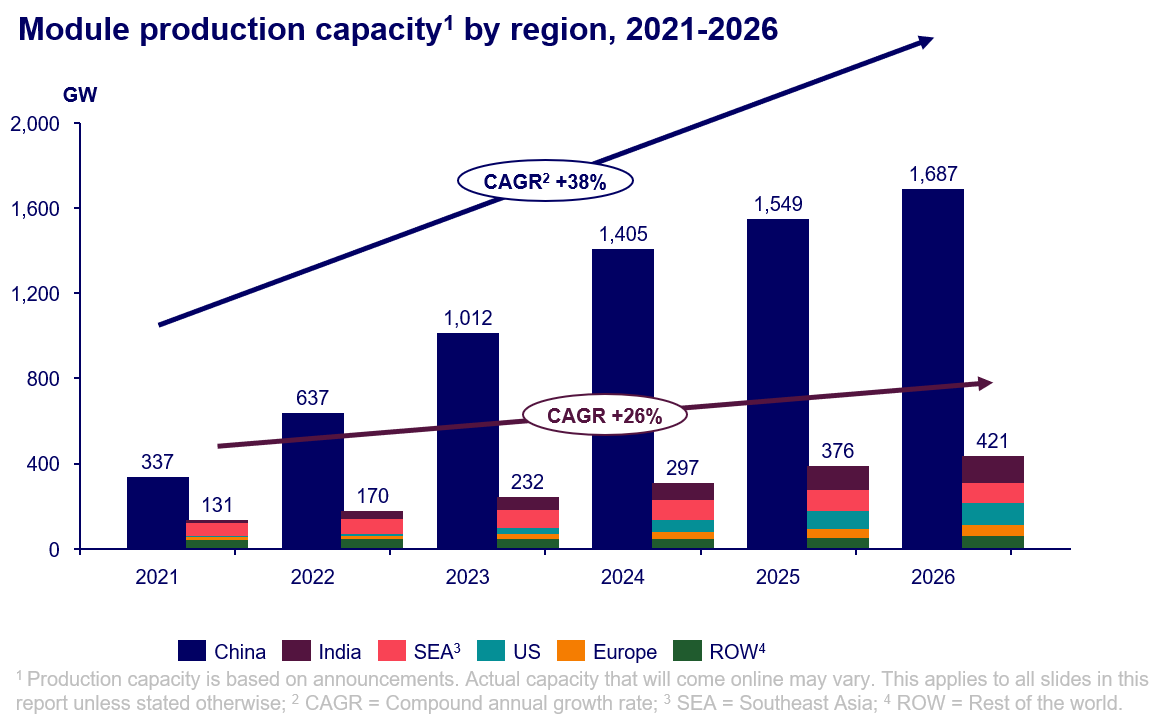

China's solar panel production capacity is projected to grow from 280 GW in 2020 to over 800 GW by 2025, reflecting a compound annual growth rate of 28-35%. Estimated data highlights China's strategic dominance in the solar manufacturing sector.

The Scale of China's Solar Manufacturing Dominance

Annual Production Capacity and Global Market Share

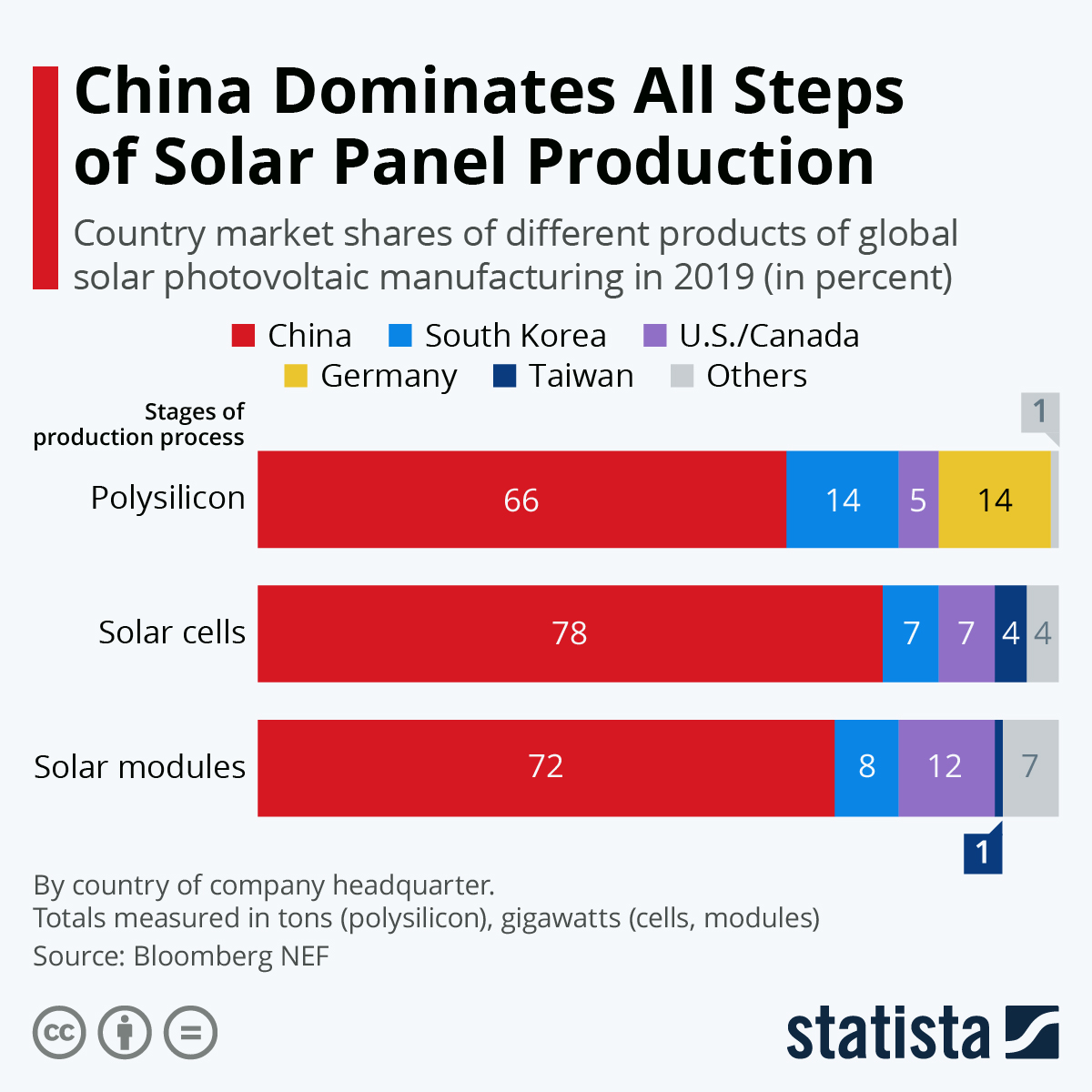

China's control over global solar manufacturing represents perhaps the most consequential industrial dominance in the 21st century energy sector. The Chinese solar supply chain doesn't simply lead the global market—it essentially comprises the entire market. With production capacity exceeding 1 terawatt annually, Chinese manufacturers control approximately 80% of global photovoltaic cell production and over 75% of module assembly capacity. This concentration emerged through decades of strategic government support, massive capital investments, technological innovation, and ruthless cost competition that eliminated virtually all international competitors as discussed by the Sasakawa Peace Foundation.

The speed of capacity expansion defies historical industrial precedent. In 2020, Chinese solar panel production totaled approximately 280 gigawatts annually. By 2024, this figure doubled to 580 gigawatts. Projections for 2025 exceed 800 gigawatts—a compound annual growth rate of 28-35% over five years. This extraordinary expansion occurred despite global oversupply, collapsing prices, and repeated warnings from industry analysts about irrational overcapacity as noted in a study published in Nature.

Manufacturers maintained this expansion through continuous automation improvements, supply chain optimization, and ruthless price competition. Vertical integration accelerated, with leading companies controlling polysilicon production, ingot manufacturing, wafer slicing, cell production, module assembly, installation, and balance-of-system components. This integration enabled Chinese manufacturers to operate at margins that would bankrupt Western competitors, with some reports suggesting module production at cost margins below 3%—meaning producers essentially break even on hardware sales while capturing profits through volume, system integration, and downstream services.

Technological Innovation and Cost Reduction Mechanisms

Behind the production volume surge lies relentless technological innovation driving systematic cost reduction. Chinese manufacturers pioneered mass production of perovskite solar cells, achieving laboratory efficiency ratings exceeding 33%—compared to traditional silicon panel efficiencies around 22-23%. Multiple manufacturers achieved commercial production of heterojunction cells and TOPCon (Tunnel Oxide Passivated Contact) technologies, improving conversion efficiencies by 0.5-1.5% compared to conventional monocrystalline designs. These incremental improvements, replicated across billions of panels, compound into substantial cost savings through improved kilowatt-hour generation per installed watt.

Factory automation accelerated cost reduction exponentially. Contemporary Chinese manufacturing facilities operate with minimal human labor, featuring robotic systems for wafer handling, automated testing protocols, and AI-driven quality control systems. Production speeds reached unprecedented levels: modern facilities produce 600-800 cells per minute per production line. By comparison, Western manufacturers operating at lower volumes typically achieve 200-300 cells per minute, substantially increasing per-unit overhead allocation.

Supply chain logistics optimization contributed equally to cost reduction. By 2024, polysilicon prices—traditionally the manufacturing cost bottleneck—dropped from

In 2024, China added 180 GW of solar capacity, significantly outpacing the United States' 50 GW. Estimated data for 2025 shows China's continued dominance.

The Domestic Deployment Frenzy: China's Internal Energy Transformation

The May 2025 Policy-Driven Installation Surge

China's renewable energy deployment tells a story of policy-driven competition rather than organic market development. The critical inflection point occurred in early 2025 when Beijing announced the discontinuation of a decades-long subsidy mechanism pegging renewable energy prices to provincial "baseline" coal power rates. This policy had effectively ensured renewable generators received guaranteed returns, providing investment security that incentivized massive capacity additions as covered by The New York Times.

Recognizing this policy change, China's renewable energy sector responded with unprecedented urgency. Developers accelerated project timelines to complete installations before the May 2025 deadline, triggering a competitive frenzy concentrated in spring 2025. January through March saw 60 gigawatts of new solar capacity additions. April added 45 gigawatts. May delivered a staggering 92 gigawatts of new solar capacity—equivalent to 3 gigawatts per day, every single day, for an entire month. This single month's deployment exceeded the United States' entire annual solar capacity addition by nearly 100%.

The policy change proved devastatingly effective at halting deployment. Post-May, monthly solar additions collapsed to approximately 10 gigawatts—a 90% reduction from peak rates. This illustrated both the policy mechanism's power and the sector's underlying structural weakness: installations depend critically on subsidy maintenance. Without guaranteed pricing, developers faced genuine uncertainty regarding project returns, substantially dampening investment appetite as noted by the National Observer.

Distributed Solar and Rooftop Revolution

Beyond massive utility-scale farms, China pioneered distributed solar deployment at residential and commercial scales. Policy mechanisms standardized installation requirements, streamlined grid interconnection processes, and reduced bureaucratic overhead that traditionally impeded rooftop installations in other markets. Standardized equipment specifications, simplified permitting, and presumed approval mechanisms accelerated residential adoption.

Rooftop panels now blanket urban apartment buildings, industrial facilities, and rural village homes across eastern China's population centers. This distributed approach distributed generating capacity geographically, reducing transmission requirements and grid stress concentrations compared to centralized megabase installations. Simultaneously, it enabled small-scale commercial and household participation in renewable energy economics, creating microeconomic incentives for grid optimization and demand response.

Battery storage integration followed distributed solar deployment. As rooftop capacity expanded, the intermittency problem—solar generation's fundamental limitation—became increasingly acute at local grid levels. Residential battery systems, typically 5-10 kilowatt-hour capacity, store midday solar generation for evening consumption, reducing grid stress during evening peak demand periods. By 2024, residential battery installations exceeded 15 million units, with cumulative storage capacity approaching 20 gigawatt-hours as reported by The Invading Sea.

Grid Instability: The Technical Crisis Nobody Anticipated

The Physics of Renewable Intermittency at Scale

Electrical grids operate on a fundamental physics principle: instantaneous power generation must equal instantaneous power consumption plus transmission losses. This balance requirement, maintained within narrow frequency tolerances (typically ±0.2 hertz), enables grid stability. Traditional power plants—coal, nuclear, natural gas—maintain generation capacity regardless of demand fluctuations, providing inertia and frequency stability that grids depend upon.

Renewable sources operate fundamentally differently. Solar generation follows solar irradiance patterns: it peaks at solar noon and disappears entirely after sunset. Wind generation depends on weather patterns, fluctuating unpredictably across hours and minutes. Neither can be throttled on demand. This creates unprecedented grid management challenges when renewable capacity exceeds 50% of generation infrastructure.

China encountered these challenges directly. As renewable generation expanded, grid operators faced increasingly acute balancing problems. During sunny, windy periods, renewable generation exceeds demand, creating surplus power that must either be stored, transmitted to distant load centers, or curtailed—essentially wasted. During evening peaks or calm weather, renewables contribute minimally while demand peaks, forcing reliance on dispatchable power sources.

The Xinjiang Blackout: A Canary in the Coal Mine

In August 2024, these technical challenges manifested catastrophically in Xinjiang, China's western renewable energy megabase. Poor voltage management from solar and wind generation caused regional voltage fluctuations that cascaded through the regional electrical grid. The resulting blackout affected millions of consumers and threatened cascading failures throughout the national grid. Engineering investigations revealed that solar and wind generation's fast voltage changes exceeded grid protection systems' adaptive capabilities, creating instability that conventional grids—designed around stable, dispatchable power sources—weren't architected to manage as reported by Reuters.

This incident exposed a fundamental architectural problem: China's electrical grid, designed and built around centralized, dispatchable power generation, couldn't accommodate renewable generation at the scales being deployed. Grid protection systems, relay timing, voltage regulation equipment, and frequency stability mechanisms all assumed relatively stable voltage and frequency profiles maintained by large synchronous generators. Solar and wind installations—operating as power electronic converters without synchronous inertia—violated these assumptions, creating novel failure modes that existing protection systems couldn't manage.

Following the Xinjiang incident, grid operators implemented emergency measures: frequency-responsive control systems, advanced voltage regulation equipment, and grid-forming inverter requirements for new renewable installations. These technologies, adapted from power electronics research, enable solar and wind installations to behave more like conventional generators, providing voltage support and frequency stability. However, retrofitting existing installations proved technically complex and economically challenging, leaving millions of existing solar panels operating with suboptimal grid stability contributions.

Negative Electricity Prices: Economics Inverted

Beyond technical instability, renewable oversupply created bizarre economic conditions. Electrical markets operate on fundamental supply-demand principles: prices rise when demand exceeds supply; prices fall when supply exceeds demand. The natural endpoint of this cycle—where price approaches zero at maximum supply—doesn't exist in electricity markets because power must be generated continuously and consumed instantaneously.

China encountered negative electricity prices—a paradoxical condition where generators pay consumers to accept power. This emerged in Shandong Province, the most renewables-dense region, where massive solar and wind capacity additions created chronic oversupply. During periods of peak renewable generation—particularly midday and windy nights—the marginal cost of accepting additional power fell below zero. Nuclear plants couldn't reduce output due to safety constraints. Coal plants operating for heating couldn't throttle generation. Energy-intensive industries—particularly aluminum smelting and steel production—positioned themselves to capture these negative prices, effectively purchasing electricity at negative rates.

Weiqiao Aluminum, a major Shandong metals producer, relocated substantial production capacity to capture persistent negative pricing. By accepting power at rates where generators paid for consumption, the company's effective electricity cost dropped to nearly zero. This arbitrage—essentially getting paid to consume power that would otherwise be wasted—made energy-intensive production arbitrarily profitable, attracting hundreds of gigawatts-equivalent of industrial load migrations to renewable-rich regions.

Negative pricing created perverse economic incentives: it rewarded grid oversupply rather than incentivizing demand reduction or generation throttling. Markets designed to penalize excess supply instead rewarded it when applicable technology made continued generation cheaper than shutdown. This inverted pricing mechanism threatened the fundamental market signals that traditionally incentivized supply-demand balancing as noted by Business.com.

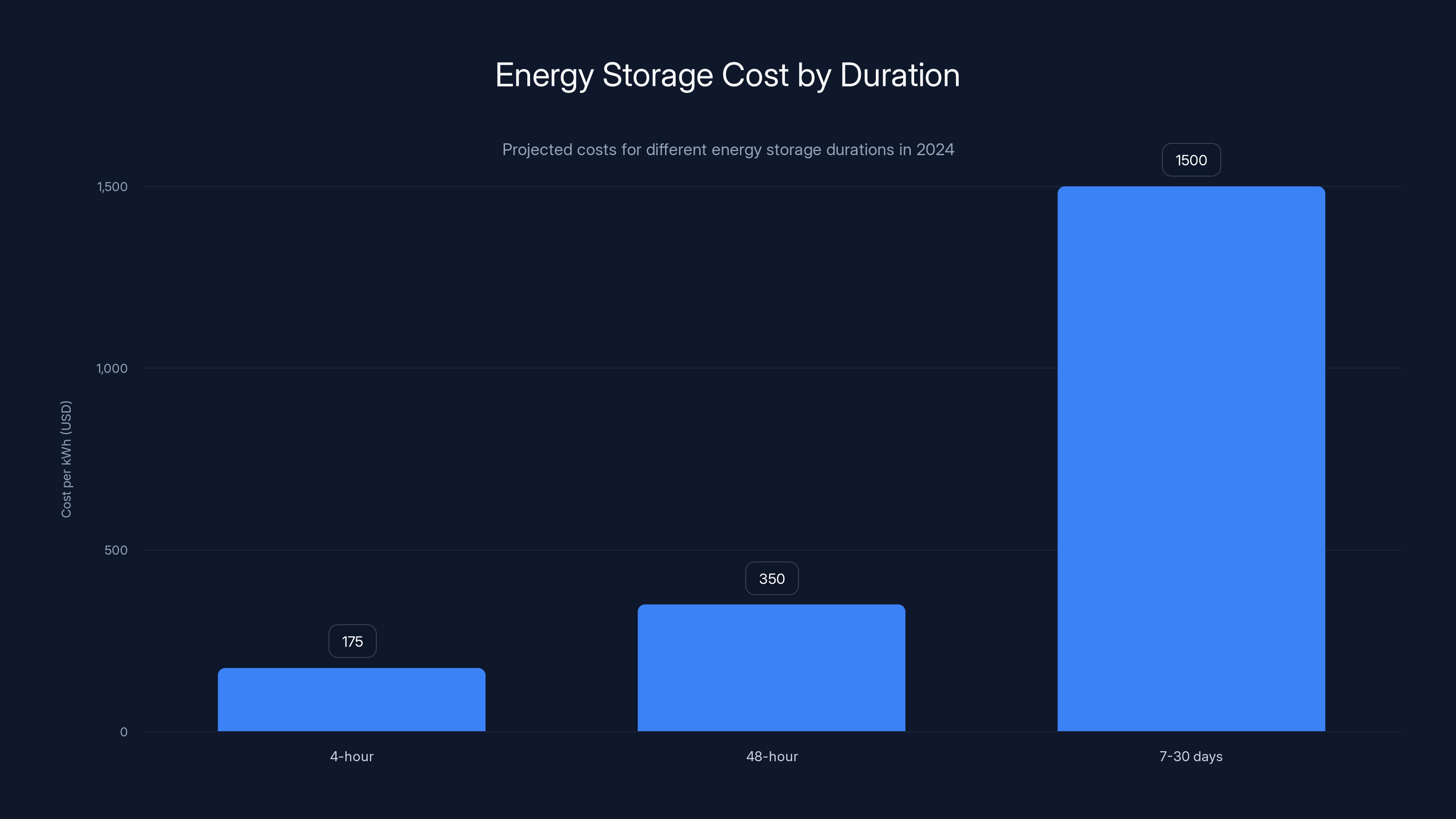

Energy storage costs increase significantly with duration. While 4-hour storage costs

The Global Market Revolution: Price Wars and Competitive Destruction

Cost Compression and Margin Elimination

China's renewable manufacturing dominance triggered global price wars that systematically compressed margins across the entire solar industry. In 2015, installed solar costs globally averaged

European manufacturers, particularly German and Swiss companies that dominated early solar manufacturing, couldn't compete at Chinese price points while maintaining Western labor costs and environmental standards. Most European solar cell and module manufacturers either exited the market, consolidated with Chinese companies, or shifted operations to lower-cost jurisdictions. By 2024, European solar manufacturing capacity declined to less than 5% of global production, from approximately 40% in 2010.

American solar manufacturers faced similar challenges. Despite tariffs, subsidies, and industrial policy initiatives, Chinese manufacturers maintained price advantages through superior manufacturing scale, more aggressive margin compression, and lower capital costs. American manufacturers focused increasingly on upstream polysilicon production and downstream system installation rather than competing directly on module manufacturing. Sun Power, once America's leading solar manufacturer, shifted to premium residential systems and system design rather than competing on volume or cost.

Dumping Allegations and Trade Tensions

The aggressive pricing triggered international trade disputes and dumping accusations. Indian manufacturers claimed Chinese solar exports violated fair trade principles, filed antidumping cases, and advocated for protectionist import barriers. European manufacturers pursued similar strategies, claiming predatory pricing and state-subsidized competition. The United States maintained tariff regimes against Chinese solar imports, yet imports continued growing as Chinese manufacturers routed products through Southeast Asia to circumvent tariff regimes.

By 2024, these trade tensions remained unresolved. Chinese manufacturers maintained market dominance through sheer scale and efficiency advantages—not primarily through state subsidies, despite persistent allegations. Investigation by international trade bodies revealed that Chinese manufacturers' cost advantages derived primarily from manufacturing efficiency, economies of scale, and supply chain integration rather than explicit subsidies. Yet political pressure for protectionist barriers remained intense in developed markets.

Emerging Market Electrification: Distributed Solar Economics

Globally collapsing solar costs transformed energy access in emerging markets, enabling unprecedented distributed electrification. In sub-Saharan Africa, India, and Southeast Asia, solar microgrids and distributed installations provided electricity access to populations previously reliant on diesel generators or lacking grid connection entirely. Chinese manufacturers captured 60-70% of this emerging market, with vendors often providing turnkey installation and financing alongside hardware.

Indian markets experienced particularly dramatic transformation. With solar costs approaching

Wind Energy: The Parallel Revolution

Offshore Wind Dominance and Technology Leadership

While solar captured media attention, China simultaneously dominated global wind energy development. Chinese manufacturers controlled approximately 65% of global wind turbine manufacturing capacity, with leading companies like State Power Investment Corporation, China General Nuclear Power, and China Three Gorges Corporation producing turbines for both domestic deployment and global export. China led technological advancement in offshore wind, commercializing 12-15 megawatt floating platform turbines while Western manufacturers remained at 10-12 megawatt fixed installations.

Offshore wind deployment accelerated particularly in Southern China and coastal regions. The South China Sea's consistent wind patterns and abundant ocean space enabled massive offshore farm development. By 2024, China had installed approximately 55 gigawatts of offshore wind capacity—exceeding the entire global offshore wind capacity of all other countries combined. Floating platform turbines enabled deployment in deeper waters previously inaccessible, opening new regions for development.

Manufacturing advantages paralleled solar dominance. Chinese offshore wind turbines cost approximately

Integration with Solar: Complementary Generation Patterns

Solar and wind generation patterns complement each other seasonally and diurnally. Summer solar peaks when winter wind generation is minimal. Daily solar peaks at midday when evening wind speeds typically remain calm. Geographic distribution amplifies complementarity: coastal regions experience consistent wind year-round, while inland and southern regions receive intense solar resource. Strategic geographic combination of solar and wind capacity optimized total renewable generation patterns.

China's energy megabases deliberately combined solar and wind installations, creating more consistent combined output than either resource alone. Shandong Province's renewable installations combined both resources to reduce variability. Northwestern deserts hosted massive solar farms while coastal regions emphasized offshore wind. This geographic diversification reduced the storage and transmission capacity required to accommodate renewable intermittency.

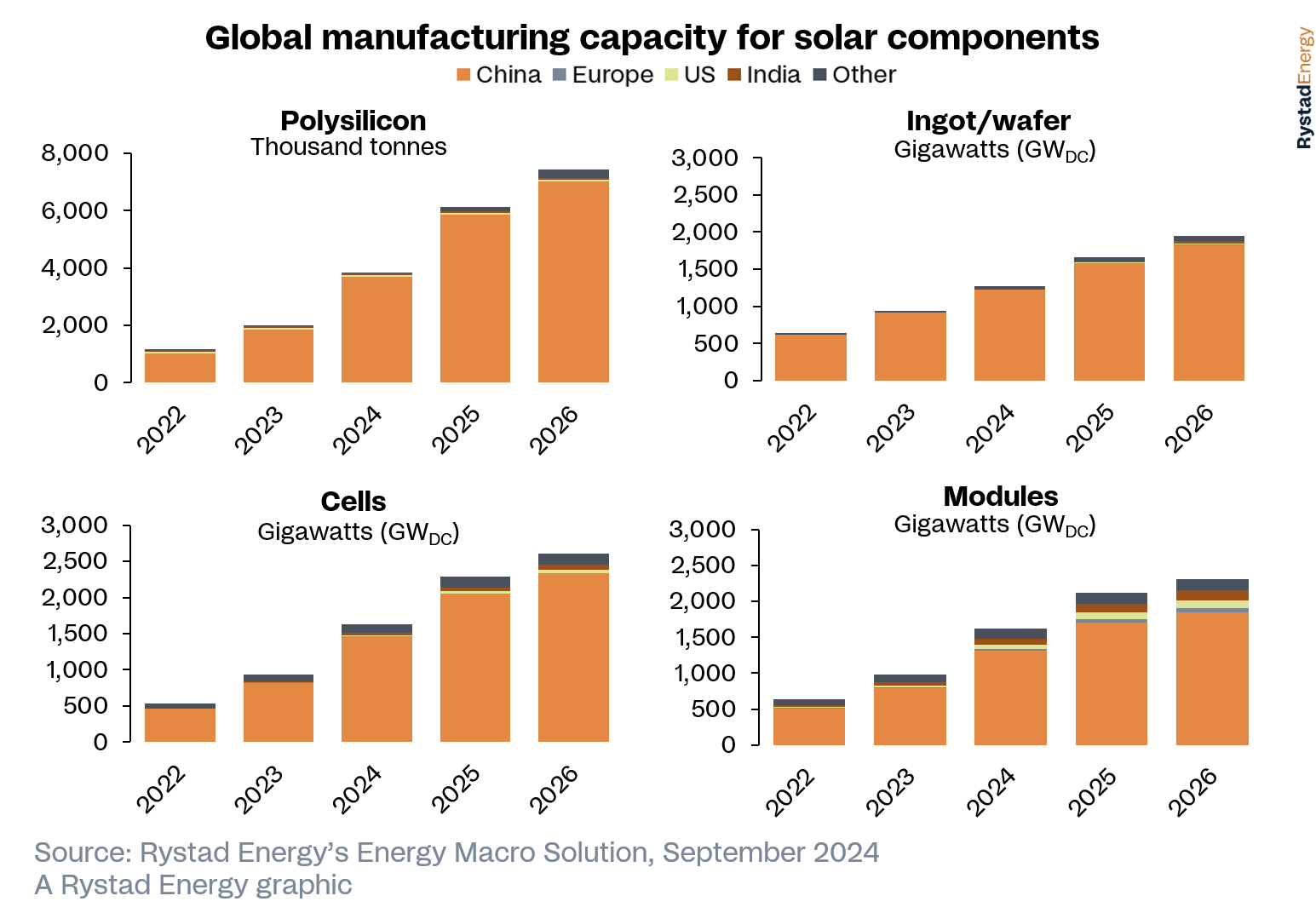

China's solar panel production has seen rapid growth, adding significant capacity annually. Estimated data highlights the scale of this transformation.

Energy Storage: The Missing Puzzle Piece

Battery Technology Advancement and Cost Reduction

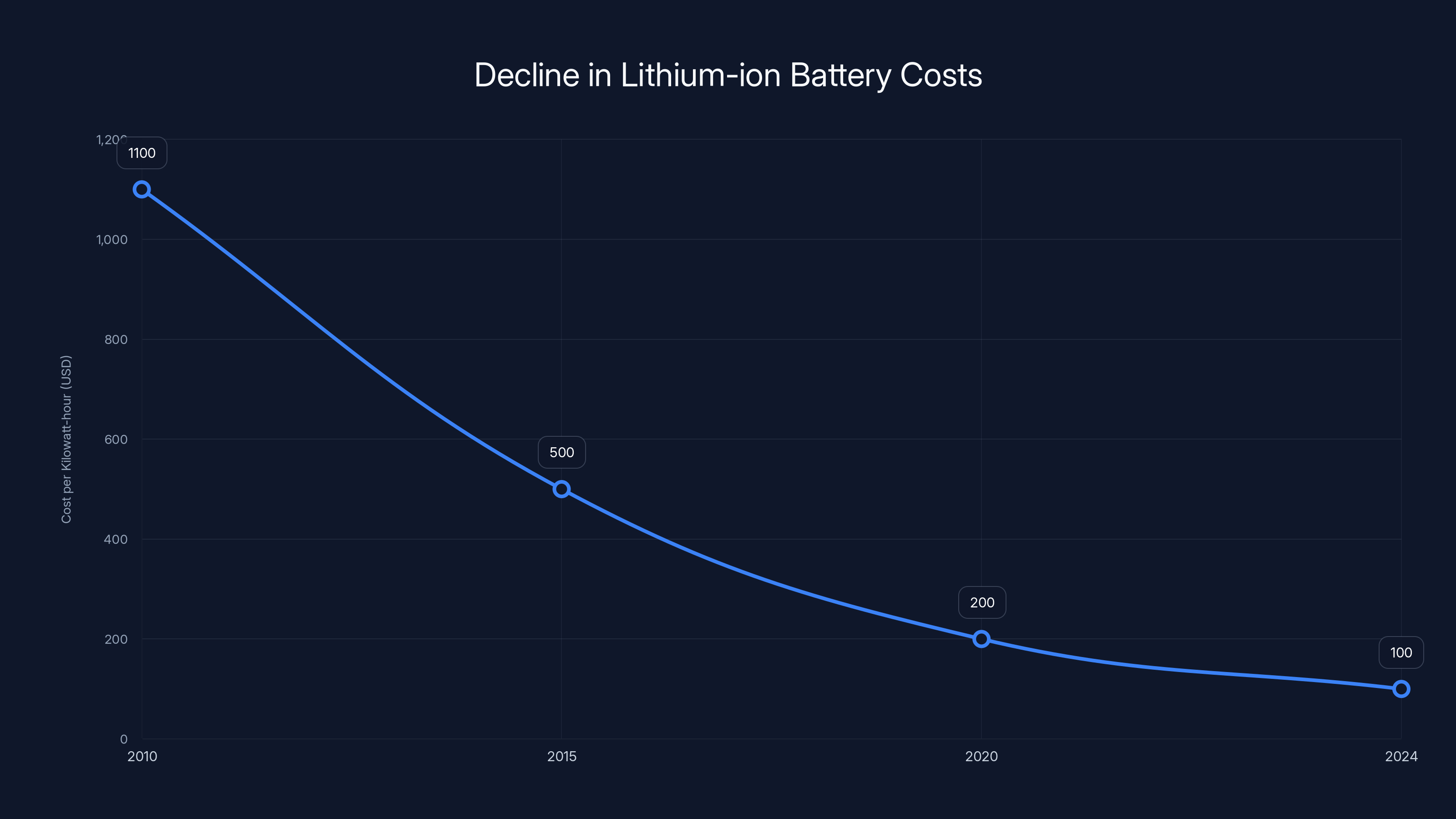

Renewable energy storage emerged as the critical missing infrastructure element enabling high-renewable grids. Lithium-ion battery costs declined dramatically—from approximately

Community and grid-scale battery storage—typically 100 megawatt-hour installations to multi-gigawatt-hour systems—emerged as transformative infrastructure. By 2024, China had deployed approximately 30 gigawatt-hours of utility-scale battery storage, with deployment accelerating toward 100+ gigawatt-hour annual additions by 2025. These installations smoothed renewable generation variability, storing midday solar and windy-period generation for evening peak demand consumption.

Battery storage economics improved continuously. A utility-scale 4-hour duration battery storage system—sufficient to store peak solar generation for evening peak demand—cost approximately

Hydrogen Storage and Long-Duration Options

Battery storage addressed daily and weekly variability effectively but couldn't economically manage seasonal variations—summer solar excess or winter wind deficit. Hydrogen storage emerged as theoretical long-duration solution: excess renewable electricity electrolyzes water into hydrogen, which stores indefinitely and can be converted back to electricity via fuel cells or burned in turbines. Multiple Chinese facilities constructed green hydrogen pilot facilities, though commercial viability remained distant at 2024-2025 price points.

Compressed air energy storage and other mechanical storage technologies received research investment but demonstrated limited commercial deployment. Thermal storage—using excess solar heat to warm salt tanks or other thermal masses—proved more practically deployable at moderate scales. By 2024, thermal storage contributed only 2-3 gigawatt-hours nationally, a minimal fraction compared to battery storage expansion.

Coal Communities and Regional Economic Disruption

The Decimation of Coal-Dependent Regions

Renewable energy's expansion triggered economic devastation in coal-dependent communities across China. Entire regions built around coal mining, thermal power plants, and associated industries faced economic contraction as renewable electricity displaced coal generation. Shanxi Province, historically dependent on coal mining, experienced particularly acute disruption: coal mining employment declined from approximately 280,000 workers in 2015 to under 120,000 by 2024, representing 57% employment loss in a single sector.

Coal plant retirements accelerated dramatically. China closed approximately 250 gigawatts of coal generation capacity between 2020-2024, representing roughly 25% of existing capacity. Mining communities faced unemployment cascades as mines closed and power plants shuttered. Simultaneously, renewable energy manufacturing and installation—while creating employment overall—concentrated in industrial regions and coastal areas rather than traditional coal communities, leaving displaced coal workers geographically isolated from new opportunities.

Government transition programs attempted to address dislocation through retraining initiatives, economic diversification encouragement, and modest transition support, but deployment remained inconsistent and underfunded relative to disruption scale. Displaced workers in their 50s and 60s couldn't easily retrain for renewable energy sector employment. Early retirement packages offered to some workers proved insufficient for workers requiring 10-20 additional years of income.

Stranded Asset Challenges

Beyond employment disruption, coal power plants transformed into economic dead weight. Thermal power plants typically operate for 40-50 years, representing multi-billion-yuan capital investments amortized over decades. As renewable generation expanded, coal plant utilization factors—the percentage of capacity actually generating electricity—declined from historical averages of 70-80% to 40-50% or lower in some provinces. This forced plants to operate at substantially reduced utilization, spreading fixed costs across diminished revenue, pushing many facilities toward operating losses.

Some coal plants, particularly those providing heating to communities through steam distribution, couldn't fully retire despite reduced electricity demand. These plants maintained operation to provide thermal energy even when electricity generation became uneconomical. This created perverse economics: maintaining expensive infrastructure for a secondary service neither market-competitive nor economically rational.

The cost of solar modules has dramatically decreased from

Policy Mechanisms and Government Control

The Feed-In Tariff Era and Subsidy Structure

China's renewable energy revolution depended historically on government policy support and subsidies. Feed-in tariffs, established in the early 2000s, guaranteed renewable generators specific electricity prices, ensuring investment returns and incentivizing capacity additions. These guaranteed rates made renewable investment essentially risk-free—investors could predict returns with certainty, attracting massive capital flows.

As renewable costs collapsed, these subsidies became extraordinarily expensive. By 2024, accumulated renewable energy subsidy obligations exceeded 200 billion yuan annually—approximately $28-30 billion per year. These subsidies, funded through utility surcharges distributed across all consumers, represented escalating fiscal burdens that government budgets struggled to sustain. Renewable energy investors, expecting continued subsidies, faced policy reversal shock when Beijing announced subsidy phase-out plans.

The May 2025 Policy Shock: Market Transition

Beijing's May 2025 announcement—discontinuing guaranteed renewable pricing and pegging renewable rates to coal generation costs—represented a dramatic policy reversal. Rather than gradual subsidy phase-out, the policy eliminated pricing guarantees immediately for post-May installations. This created perverse incentives for developers to rush installations before the deadline, leading to the unprecedented deployment surge and subsequent collapse.

The policy signaled government intent to transition renewable energy from subsidy-dependent to market-competitive. Implicit messaging suggested that solar and wind—now cost-competitive with coal—didn't require subsidies and should compete on economics alone. This transition reflected legitimate fiscal pressures but ignored renewable energy's inherent intermittency, grid integration costs, and market design requirements that markets alone couldn't address.

Grid Pricing Mechanisms and Market Design Deficiencies

China's electrical market design proved inadequate for accommodating high-renewable penetration. Wholesale electricity prices, set through centralized bidding mechanisms, typically reflected marginal generation costs but couldn't properly value grid stability services that renewables couldn't provide. Battery storage, voltage support equipment, and dispatchable reserves required for renewable integration generated costs that market pricing didn't capture, creating underinvestment in complementary infrastructure.

Ancillary services markets—designed to compensate providers for grid stability services—remained underdeveloped. Markets couldn't properly price frequency regulation, voltage support, or reactive power compensation that renewables' power electronics struggled to provide compared to synchronous generators. This created systematic underpricing of grid services that renewable integration demanded, distorting investment incentives throughout the electrical system.

Global Energy Market Transformation

The End of Energy Scarcity Economics

China's renewable dominance fundamentally challenged traditional energy economics predicated on resource scarcity. Fossil fuels—coal, oil, natural gas—operate on supply constraints and geological depletion timelines that historically ensured scarcity premiums and sustained pricing. Renewable energy resources—solar irradiance, wind patterns—operate at essentially unlimited supply, creating economic conditions previously reserved for computational resources and manufactured goods: marginal cost approaching zero with deployment at sufficient scale.

This transition threatened the geopolitical foundation of energy markets. Oil price volatility drove international conflicts, shaped political alignments, and enabled resource-rich autocracies to finance geopolitical ambitions. As renewable electricity approached zero marginal cost, the geopolitical leverage of fossil fuel control diminished. Conversely, countries controlling rare earth elements, battery manufacturing capacity, and renewable technology intellectual property gained geopolitical influence, with China already dominating these emerging strategic resources.

Stranded Asset Risk for Fossil Fuel Infrastructure

Globally, trillions of dollars in fossil fuel infrastructure faced accelerating obsolescence. Coal plants, oil refineries, and natural gas distribution systems—capital assets amortized over decades—confronted competing economic technologies with zero marginal costs and rapidly improving competitiveness. Financial markets increasingly recognized this stranded asset risk, driving capital reallocation from fossil fuel companies toward renewable energy developers and storage technology providers.

Insurers, increasingly aware of climate risk and transition risk, adjusted premium pricing and coverage availability for fossil fuel infrastructure. Pension funds and institutional investors implemented environmental, social, and governance criteria restricting fossil fuel investments. These financial market pressures accelerated obsolescence timelines beyond technological fundamentals—not because fossil fuel technologies stopped functioning but because financial capital increasingly viewed them as poor long-term investments.

Electricity as Commodity and Energy Abundance Paradigm

As solar and wind costs collapsed toward near-zero marginal cost, electricity transformed from scarce commodity with sustained premium pricing into increasingly commodified, abundant resource. In regions with high renewable penetration, wholesale electricity prices approached zero during peak generation periods, eliminating profitability for marginal generation and making electricity virtually abundant during renewable peak hours.

This energy abundance paradigm shifted consumption patterns. Industrial processes typically scheduled for off-peak hours to minimize electricity costs increasingly operated flexibly, shifting to peak renewable periods and consuming electricity at near-zero cost. Data centers, computing systems, and electrochemical processes located strategically in high-renewable regions to capture cheap electricity economics. This created secondary economic incentives for renewable deployment—not just electricity generation but industrial relocation and manufacturing economics transformation.

Lithium-ion battery costs have decreased by 90% from 2010 to 2024, making renewable energy storage more economically viable. Estimated data.

Environmental and Climate Implications

Carbon Emission Reductions and Climate Trajectory Impact

China's renewable energy deployment directly displaced fossil fuel consumption and reduced carbon emissions. In 2024, renewable electricity generation avoided approximately 1,200 megatons of carbon dioxide equivalent emissions compared to historical coal-based generation patterns. This represented roughly 12% of China's total energy-related carbon emissions, a substantial but still limited fraction of economy-wide decarbonization required for climate stabilization.

Globally, cheap Chinese solar panels accelerated renewable deployment worldwide, enabling developing nations to skip fossil fuel infrastructure entirely and build renewable-first electrical systems. This development pattern transformation potentially prevented centuries of coal-dependent growth that historical developed nations followed. Cumulative global carbon emission reductions from Chinese renewable exports may exceed 500-800 megatons annually by 2030, representing meaningful climate trajectory improvement.

Manufacturing and Supply Chain Environmental Costs

Aggressive renewable deployment came with significant environmental costs concentrated in upstream manufacturing. Polysilicon production—the silicon feedstock for solar cells—requires energy-intensive processing involving hazardous chemicals and generates toxic waste. Xinjiang's polysilicon facilities, while achieving remarkable cost efficiency, operated with varying environmental controls and raised geopolitical concerns regarding labor practices alongside environmental standards.

Battery manufacturing similarly concentrated environmental impacts in upstream production rather than operational phases. Lithium extraction, cobalt mining, and cathode material processing in China, Congo, and other developing nations created localized environmental degradation and health impacts. Life cycle assessments of renewable systems demonstrated that while operational phases generated negligible environmental impact, manufacturing phases created concentrated impacts in production regions—typically lower-income countries with limited environmental enforcement.

Long-Term Grid and Ecosystem Impacts

Massive renewable deployment created novel ecological impacts. Large-scale solar farms and wind installations altered local land-use patterns, affecting agricultural productivity and wildlife habitats. Shandong's dense solar development, while displacing coal generation, concentrated land-use changes affecting local ecosystems. Offshore wind development altered marine environments and affected fishing activities. These tradeoffs—between climate benefits and localized environmental impacts—remained inadequately addressed in policy frameworks and investment decisions.

Technological Innovation Frontiers

Advanced Inverter Technology and Grid Services

Renewable energy integration spurred innovation in power electronics and grid management technology. Grid-forming inverters—advanced power electronic converters enabling solar and wind installations to behave increasingly like conventional synchronous generators—emerged as critical enabling technology. These inverters provided voltage support, frequency regulation, and fault current capability that traditional renewable inverters couldn't supply, partially addressing grid stability challenges exposed by the Xinjiang incident.

Multiple Chinese companies advanced grid-forming inverter technology: Huawei's renewable energy division commercialized sophisticated grid-forming solutions, as did Sungrow and other power electronics manufacturers. By 2024, grid-forming inverter costs declined to $0.05-0.10 per watt, approaching marginal production economics. Mandatory grid-forming inverter requirements for new installations accelerated deployment, fundamentally improving renewable integration capabilities.

Artificial Intelligence and Predictive Grid Management

Artificial intelligence increasingly enabled sophisticated renewable grid integration. Machine learning algorithms trained on years of solar irradiance, wind speed, and consumption data enabled increasingly accurate generation forecasting. Probabilistic forecasting systems provided grid managers with confidence intervals for renewable generation 24-48 hours ahead, enabling improved scheduling of dispatchable resources. Real-time AI systems controlled battery charging and discharging based on anticipated renewable generation and consumption patterns, optimizing storage utilization.

Demand response systems, enabled by smart grid technology and AI optimization, enabled automated consumption adjustment in response to renewable availability. Air conditioning systems, water heaters, and industrial processes could shift operational timing flexibly, consuming electricity when renewable generation peaked. This demand flexibility, coordinated through AI optimization systems, provided virtual storage capacity complementing physical battery systems.

Next-Generation Solar Technologies

China's renewable manufacturing dominance enabled rapid commercialization of advanced solar technologies. Perovskite solar cells—theoretically capable of 30%+ efficiencies—progressed from laboratory demonstrations toward commercial production. Tandem solar cells, combining perovskite with crystalline silicon layers, exceeded 30% efficiency in commercial products by 2024. While still representing modest production volumes compared to traditional monocrystalline panels, these technologies signaled continuous cost and efficiency improvements sustaining renewable energy advancement.

Thermophotovoltaic cells and concentrated photovoltaic systems, emerging from research institutions, approached commercial viability. These technologies potentially enabled higher energy density solar generation, though remained substantially more expensive than conventional panels. Manufacturing scale and cost reduction following successful commercialization could enable broader deployment.

Global Competitiveness and Industrial Policy Implications

Chinese Industrial Leadership and Strategic Dominance

China's renewable energy dominance extended beyond manufacturing to technology standards, supply chain control, and intellectual property. Chinese standards for inverter technology, battery chemistries, and system integration increasingly became global de facto standards through sheer market dominance. International standards bodies increasingly aligned standards with Chinese manufacturer capabilities rather than alternative approaches, concentrating technological direction.

This competitive dominance positioned China as the emerging energy superpower of the 21st century. While oil and natural gas previously defined strategic resource competition, solar panel and battery production capacity increasingly determined which nations could electrify energy systems. China's commanding market position enabled pricing power, supply chain leverage, and geopolitical influence analogous to historical petroleum dominance.

Western and Developing Nation Response Strategies

Developed nations pursued various strategies responding to Chinese renewable dominance. The United States implemented substantial renewable energy subsidies, manufacturing tax credits, and protectionist tariffs attempting to rebuild domestic solar and battery manufacturing. The Inflation Reduction Act committed $369 billion toward clean energy deployment and manufacturing, explicitly targeting Chinese competition. European Union adopted similar strategies, emphasizing domestic manufacturing resilience and supply chain diversification.

These industrial policy initiatives faced fundamental challenges: China's decade-long manufacturing head start, integrated supply chains, and cost advantages proved enormously difficult to overcome through subsidies alone. Domestic manufacturing could only compete for premium market segments or protected markets where tariffs created cost protection. Globally, Chinese manufacturers maintained decisive competitive advantages.

Developing nations, meanwhile, captured extraordinary benefits from cheap Chinese renewable exports. Rather than building expensive domestic manufacturing capacity, developing nations purchased turnkey solar systems, batteries, and wind turbines at globally competitive Chinese prices, accelerating electrification at radically reduced costs compared to historical alternatives. This dynamic created tension: rich nations pursued manufacturing resilience and industrial development objectives while poor nations optimized for electrification speed and cost minimization.

Challenges and Future Uncertainties

Energy Storage Requirements and Economic Viability

High renewable penetration grids fundamentally require extensive energy storage to manage intermittency. Mathematical modeling suggested that grids approaching 80%+ renewable penetration required storage capacity equal to 3-5 days of demand, effectively storing seasonal variations. For a grid consuming 3,000 gigawatt-hours daily, this implied 9,000-15,000 gigawatt-hour storage requirements—approximately 300-500 times current global battery storage capacity.

Battery storage economics improved dramatically but remained economically challenged for multi-day applications. A 4-hour battery storage system cost approximately

China accelerated storage deployment but acknowledged storage requirements would remain cost-constraining for decades. Hybrid approaches combining limited battery storage with dispatchable backup capacity and demand flexibility appeared more pragmatic than pure storage-based solutions, at least through 2030-2035.

Electrification Requirements and Demand Growth

Decarbonization demanded not merely replacing electricity generation but expanding electricity supply to displace fossil fuels from heating, transportation, and industrial processes. Current electricity demand represented only 20% of total energy consumption globally—the remaining 80% came from direct fossil fuel burning. Fully electrified economies would require total electricity supply 2-3 times current levels.

China's electricity consumption growth continued accelerating due to air conditioning expansion, electric vehicle adoption, and industrial growth. Demand growth of 3-4% annually meant electricity consumption doubled every 20 years. This demand growth, overlaid on renewable transition requirements, implied electricity supply requirements doubling or tripling over coming decades. This massive supply expansion opportunity represented the economic engine sustaining renewable investment and industrial expansion.

Geopolitical Competition and Trade Tensions

China's renewable energy dominance created increasing geopolitical tensions. Western nations viewed renewable supply chains concentrated in Chinese control as strategic vulnerability, motivating reshoring and diversification strategies. Trade tensions around tariffs, forced technology transfer, and supply chain restrictions escalated. China conversely viewed Western attempts to develop independent renewable manufacturing as threatening to Chinese strategic interests.

These tensions risked fragmenting global renewable supply chains into regional blocks—Chinese-dominated Asian systems, European independent systems, American tariff-protected systems—rather than integrated global markets. Such fragmentation would reduce efficiency, increase costs, and slow global decarbonization compared to unified global supply chains optimizing for lowest cost and highest efficiency.

Investment Opportunities and Market Dynamics

Downstream Integration and Systems Opportunities

As upstream solar and battery manufacturing matured and margins compressed toward single digits, investment opportunities shifted downstream toward system integration, installation, financing, and optimization software. Companies positioning themselves in solar farm development, battery storage deployment, grid modernization, and demand response optimization captured better margins than commodity hardware manufacturing.

Developing nations in particular represented massive opportunity for distributed solar deployment. Approximately 750 million people globally lacked reliable electricity access. Solar microgrids offered economically viable electrification at costs lower than extending centralized grid infrastructure. Financing innovations—pay-as-you-go systems enabling customers to pay for solar gradually—enabled broad consumer participation previously inaccessible due to capital constraints.

Energy Software and Artificial Intelligence Solutions

Energy management software, demand forecasting systems, and AI optimization platforms emerged as high-value opportunities as renewable penetration increased. Companies developing sophisticated control systems coordinating distributed renewable resources, storage systems, and flexible loads captured premium valuations. Grid modernization software, advanced metering infrastructure, and cybersecurity solutions for electrical systems represented additional substantial opportunities.

Storage Technology Companies and Advanced Battery Research

Battery storage remained capacity-constrained despite rapid growth. Companies advancing alternative storage technologies—sodium-ion batteries offering lower cost per kilowatt-hour despite lower energy density, long-duration iron-air batteries, compressed air systems—received substantial investment. Commercialization of any emerging long-duration storage technology could prove transformative, enabling high-renewable grids without massive storage capacity buildouts.

Conclusion: The Uncontrolled Transition

China's renewable energy revolution represents perhaps the most consequential industrial transformation of the 21st century, yet it fundamentally differs from the carefully managed policy narratives most accounts present. Rather than a coordinated government program implementing predetermined objectives, the revolution emerged as a chaotic competitive explosion exceeding government planning capacity, generating both unprecedented climate opportunity and profound economic and technical chaos.

The statistics alone strain comprehension. A single nation now produces solar panel capacity equivalent to the planet's total installed electricity system, adding 3 gigawatts daily in peak months, driving electricity costs toward historic lows and destabilizing electrical grids globally. Simultaneously, this expansion delivers unprecedented electrification access to populations lacking reliable power, threatens fossil fuel industries with technological obsolescence, and creates new pathways toward energy-abundant futures.

Yet this transformation occurs chaotically, with policy mechanisms failing, electrical grids destabilizing, coal communities decimated, and market signals increasingly inverted. Negative electricity prices, grid blackouts, and stranded asset cascades alongside unprecedented cost reductions characterize this contradictory landscape. Nobody genuinely controls this transition—neither China's government, despite its policy instruments and planning apparatus, nor Western governments attempting to respond, nor markets theoretically optimizing allocation. The transition operates largely independently of deliberate direction, driven instead by technological progress, competitive dynamics, and policy reactions to emerging crises.

This uncontrolled revolution paradoxically offers climate stabilization pathway that deliberate policy coordination has repeatedly failed to achieve. While governments debated carbon pricing and slowly negotiated international climate agreements, China's competitive dynamics and cost reduction curves achieved decarbonization faster and more comprehensively than any policy framework could engineer. The chaos proves simultaneously the mechanism enabling rapid transition and source of stability risks that will require decades resolving.

Looking forward, the critical uncertainties center on grid stability mechanisms, storage technologies, and geopolitical responses. Can electrical grids accommodate 80%+ renewable penetration through advanced power electronics, storage expansion, and demand flexibility innovations? Will long-duration storage technologies achieve commercial viability before capacity constraints trigger grid instability crises? Can international relations accommodate Chinese strategic dominance over renewable supply chains, or will geopolitical fragmentation undermine transition efficiency?

These questions lack definitive answers. What remains clear: the renewable energy transition is unfolding at unprecedented pace, driven by uncontrolled competitive dynamics rather than deliberate policy coordination, producing both transformative opportunity and profound challenges that societies have barely begun addressing. The next decade will determine whether this messy, chaotic revolution succeeds in transforming global energy systems before stability crises demand fundamental restructuring, or whether the very dynamics enabling rapid transition ultimately undermine the grids and economic systems that transition depends upon.

The world watches, largely unprepared, as China's renewable explosion continues expanding regardless of global readiness to accommodate it. The consequences—whether salvation or calamity or most likely some complicated mixture—will define global energy systems, geopolitical competition, and climate trajectory for generations.

FAQ

What is China's renewable energy revolution?

China's renewable energy revolution refers to the dramatic acceleration of solar and wind energy deployment, driven by technological innovation and manufacturing dominance that produced over 1 terawatt of annual solar capacity and created global markets where renewable electricity costs less than traditional fossil fuels. This transformation occurred through both policy incentives and competitive market dynamics that created unprecedented overcapacity in renewable generation equipment.

How has China achieved such dominance in solar manufacturing?

China's solar dominance emerged through decades of strategic government support, massive capital investments, technological innovation, and ruthless cost competition that eliminated international competitors. Chinese manufacturers benefit from integrated supply chains controlling polysilicon production, cell manufacturing, module assembly, and installation, enabling costs 70-80% lower than Western manufacturers while maintaining similar quality standards.

What causes negative electricity prices in renewable-heavy grids?

Negative electricity prices occur when renewable generation exceeds demand during peak production periods, and dispatchable power plants cannot reduce output due to physical constraints (coal plants providing community heating, nuclear safety requirements). Rather than wasting power or paying shutdown costs, generators pay consumers to accept electricity—creating arbitrage opportunities for industrial users positioned to shift consumption to negative-price periods.

Why is grid instability occurring in China's renewable-heavy regions?

Electrical grids were designed around large synchronous generators providing stable voltage and frequency. Solar and wind generate power through power electronic converters lacking synchronous inertia, creating fast voltage fluctuations that exceed traditional grid protection systems' adaptive capabilities. When renewable generation comprises 50%+ of capacity, voltage instability and frequency deviation risks escalate dramatically without advanced power electronics and storage infrastructure.

What percentage of global solar manufacturing does China control?

China controls approximately 80% of global photovoltaic cell production and over 75% of module assembly capacity, with production capacity exceeding 1 terawatt annually by 2024. This dominance extends throughout supply chains, including approximately 60% of global polysilicon production and substantial control over downstream installation and integration services.

How does China's renewable deployment compare to the United States?

In 2024, the United States added approximately 50 gigawatts of solar capacity for the entire year. China added that capacity every three days during peak 2025 deployment periods—92 gigawatts in May 2025 alone. Even after policy changes reduced post-May deployment rates to 10 gigawatts monthly, China maintains installation pace roughly double U. S. historical records while implementing domestic electrification alongside global supply provision.

What happened to coal industry workers during China's renewable transition?

Coal industry employment in Xinjiang and Shanxi provinces declined 50-70% between 2015-2024 as coal mines closed and thermal power plants retired. Government transition programs provided limited retraining and early retirement support, though displaced workers in their 50s-60s faced particular challenges finding employment in renewable energy sectors that concentrated in industrial and coastal regions rather than traditional coal communities.

How do negative electricity prices affect industrial competitiveness?

Industries positioned to consume power during negative-price periods effectively receive subsidized electricity, dramatically improving economic competitiveness in energy-intensive production. Energy-intensive aluminum smelting, steel production, and data centers relocated to high-renewable regions to capture negative-price electricity, creating secondary economic incentives for renewable deployment beyond environmental objectives.

What energy storage capacity would high-renewable grids require?

Electrical grids approaching 80%+ renewable penetration would require storage capacity equivalent to 3-5 days of total demand—approximately 300-500 times current global battery storage capacity. This would necessitate either revolutionary long-duration storage technology breakthroughs or fundamental electricity market restructuring emphasizing demand flexibility over supply-side storage solutions.

Will renewable energy prices continue declining, or have they reached cost floors?

Solar module costs may approach asymptotic minimums around $0.10-0.15 per watt within 2-3 years, but system-level costs including balance-of-system components, installation, interconnection, and land acquisition will remain 2-3 times module costs. Further cost reductions depend on storage breakthroughs, installation efficiency improvements, and land-use optimization rather than module manufacturing advances.

How does renewable dominance affect geopolitical energy competition?

China's renewable dominance shifts strategic competition from fossil fuel resource control toward manufacturing capacity and supply chain control. Nations historically benefiting from petroleum geopolitical leverage face diminished influence as renewable electricity becomes globally abundant. Simultaneously, Chinese control over critical supply chains creates new dependencies and geopolitical leverage, fundamentally reshaping energy-based international relations.

Key Takeaways

- China produces 1 terawatt of annual solar capacity—equivalent to 20x U.S. annual deployment—driving global electricity costs toward historic lows

- Grid instability from renewable intermittency threatens electrical system reliability, requiring fundamental infrastructure redesign and advanced power electronics

- Negative electricity prices create economic paradoxes where generators pay consumers to accept power during peak renewable generation periods

- Coal industry displacement decimates regional economies while renewable manufacturing concentrates geographically, creating uneven transition impacts

- Renewable dominance represents geopolitical power shift from fossil fuel resource control toward manufacturing capacity and supply chain dominance

- Storage technology remains capacity-constrained for high-renewable grids, requiring breakthroughs or demand-side flexibility approaches

- Supply chain fragmentation into regional blocks threatens global decarbonization efficiency as geopolitical tensions increase

- Downstream opportunities in system integration, software optimization, and installation services capture better margins than commodity manufacturing

Related Articles

- Spotify's Page Match: Syncing Audiobooks with Physical Books [2025]

- Google Clock's New Alarm Features Make Sleeping Through Alerts Impossible [2025]

- Philips Hue Bridge Update Makes Smart Light Automations Easier [2025]

- Sony's TV Business Takeover: Why TCL's Partnership Changes Everything [2025]

- Xbox Cloud Gaming Free Tier With Ads: Everything You Need to Know [2025]

- Segway Navimow's Crab Walk Technology Explained [2025]