Medallia Is Just the Opening Act. Here’s the List of PE SaaS Deals Most at Risk. | SaaStr

Thoma Bravo handed the keys to Medallia over to its lenders yesterday. Blackstone, KKR, Apollo, and Antares are taking control of a company Thoma Bravo bough...

TechnologyInnovationBest PracticesGuideTutorial

Listen to Article

0:00

0:00

0:00

Medallia Is Just the Opening Act. Here’s the List of PE Saa S Deals Most at Risk. | Saa Str

Overview

AI VC

AI Mentor: Digital Jason + Amelia

AI Startup Benchmarking

AI Agent Playbook

Free e Books

e Book: Hiring a Great VP of Sales

e Book: Raising Capital

e Book: The First $1m ARR

Details

University

All Posts

Podcasts

The Top CROs

VC Fundraising

Top Videos

Q&A

Best of Saa Str

#1 Bestselling Book

Search Everything

Join the Community

Free e Books

e Book: Hiring a Great VP of Sales

e Book: Raising Capital

e Book: The First $1m ARR

AI Annual 2026

Events Overview

Sponsors

Event Sponsorship

Media Sponsorship

Digital AI Day 2026 (Free)

Speaker Submissions

Speaker Requirements

Overview

Medallia Is Just the Opening Act. Here’s the List of PE Saa S Deals Most at Risk.

Thoma Bravo handed the keys to Medallia over to its lenders yesterday. Blackstone, KKR, Apollo, and Antares are taking control of a company Thoma Bravo bought for

6.4billionin2021,wipingoutroughly

5.1 billion in equity held by the firm and its co-investors.

And it’s not a one-off. Medallia is the second giant Saa S equity wipeout in 18 months after Vista’s Pluralsight handover in 2024. It’s likely going to get worse before it gets better. Because there are many more software leaders PE acquired, that took on large debt positions, and now … don’t have the cash flow to pay back that debt.

Here’s the setup, then the list of deals most exposed.

The mechanics matter because the same mechanics apply to roughly a dozen other deals.

Medallia’s annual debt service had climbed to about

300millionbyearly2026,againstroughly

200 million in annual earnings.

The breaking point was the expiration of Payment-in-Kind relief at the end of 2025 — the arrangement that let Medallia defer cash interest by piling it onto principal. When Blackstone, holding $1.5B of the debt, declined to extend the PIK window again, there was no viable path other than restructuring.

Lenders had already been marking the debt down for months. FS KKR Capital Corp had it at 79 cents on the dollar. Apollo Debt Solutions had it at 74 cents. Once the biggest lender in the syndicate refused to extend, the rest followed.

This is the template. Peak-vintage LBO + aggressive leverage + revenue growth that stalled + PIK toggles expiring + no refinancing window because enterprise Saa S multiples collapsed. Median revenue multiples for mature Saa S platforms have dropped from 9x in 2021 to roughly 6x in 2026, which makes refinancing at a level that preserves equity essentially impossible.

From 2015 to 2025, PE bought more than 1,900 software companies in deals totaling over $440 billion. Roughly 20-25% of all private credit is now exposed to software. About one-fifth of that debt has to refinance by 2028.

So which deals are most at risk of going the Medallia way?

4 billion of equity held by Vista and co-investors. Lenders got an 85% stake after converting

1.2Bofdebttoequityandputtingin

275M of fresh capital. Vista got aggressive on the way down with a drop-down transaction that moved IP out of lenders’ reach, which created lasting damage to relationships.

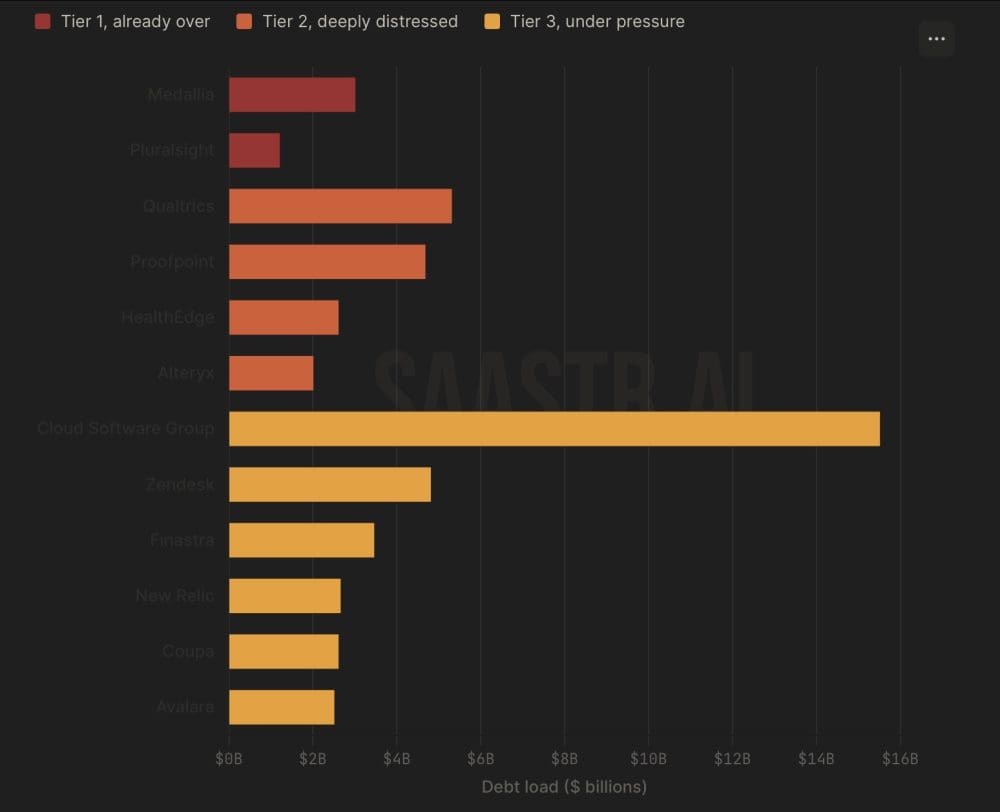

Medallia — Thoma Bravo, 2021, $6.4B. As of April 22, 2026: done.

Thoma Bravo claims Proofpoint has doubled revenue and nearly quadrupled EBITDA under its ownership, which may well be true. But with rates where they are, even doubled EBITDA has to cover a much bigger debt stack. Watch for any PIK conversion or covenant relief discussion — that’s always the first signal.

5.3 billion Qualtrics debt deal on March 17 after failing to win over investors amid deepening anxiety around AI disruption. That’s the same “lenders won’t extend” signal that preceded Medallia. Qualtrics is also the direct category leader over Medallia in experience management — if Medallia is broken, Qualtrics is in the same line of fire. 15% workforce cuts already happened in 2023. In October 2025 they stacked the $6.75B Press Ganey acquisition on top of existing debt. Same category, same vintage, same playbook, and now lenders are publicly backing away.

Health Edge (Bain Capital). Bain bought Health Edge from Blackstone at 30x EBITDA — roughly 4x what Blackstone had paid — financed with

2.6billionofdebtat8.72

226 million. Adjacent to Saa S but similar structure: peak multiple, peak leverage, AI disruption risk in revenue cycle management.

Alteryx (Clearlake + Insight,

4.4B,2024).

2B debt at SOFR + 650 bps. Analytics automation is arguably the single most AI-exposed Saa S category — “data prep for business analysts” is exactly the seat AI agents replace first. Clearlake is already managing 11 portfolio companies with underperforming debt, including Quest Software at 25¢ and Cornerstone On Demand. So the sponsor’s bandwidth and willingness to inject fresh equity into Alteryx specifically is a real question. Clearlake is triaging.

Quest Software (Clearlake). Clearlake’s lowest-graded Quest Software debt is trading around 25 cents on the dollar. When debt trades at 25 cents, the equity is already economically zero. The only question is timing and structure.

Cornerstone On Demand (Clearlake). Multiple term loans underperforming. Corporate learning is squarely in the path of AI disruption.

These aren’t in restructuring talks yet, but the leverage is heavy and the facts are moving the wrong way.

Cloud Software Group (Vista + Elliott,

16.5BCitrix+TIBCO,2022).About

15-16B of new leverage. Late-2022 loan pricing near SOFR+475-600 bps. Citrix’s Daa S/VDI business is structurally squeezed by Microsoft Windows 365 and Azure-native alternatives. This is the single largest software LBO by debt quantum and the one most exposed to platform displacement rather than AI displacement.

Coupa (Thoma Bravo, $8B, 2022). Debt-to-equity ratio roughly 65:35, with up to 30% of the workforce reportedly cut post-acquisition. Procurement and spend management is exactly the category where autonomous agents threaten seat-based pricing most directly. Thoma Bravo is reportedly pushing an agent-first re-architecture, but it’s a race against debt service.

2.65 billion debt package for the buyout, with Blackstone also participating — priced at SOFR + 6.75%. That’s roughly $300M of annual interest against a business still mid-transition to consumption pricing. Observability is one of the most directly AI-exposed categories (agents write their own telemetry, Datadog and Grafana are already cannibalizing entry points). No public distress signals yet, but the coverage math is thin.

Anaplan (Thoma Bravo, $10.7B, 2022). Loans near par for now, but same vintage, same sponsor concentration, same AI-exposed category as Coupa. The difference is operational: Anaplan is executing better. If execution slips, the leverage is still there.

Zendesk (Hellman & Friedman + Permira,

10.2B,2022).

4.6-5B in private credit. Customer support is ground zero for agent replacement of seats. To its credit, Zendesk is reportedly generating $200M+ in ARR from its own AI offering — the question is whether that grows faster than legacy seat revenue shrinks.

Avalara (Vista,

8.4B).

2.5B in private credit led by Blue Owl. Tax compliance is more defensible than most Saa S categories, but the leverage assumptions were still peak-vintage.

Smartsheet (Vista + Blackstone, $8.4B, late 2024). Loans have already appeared on private credit secondary bid/offer lists. That’s unusual this soon after a buyout and it’s a tell.

Hyland Software (Thoma Bravo). Loans showing up on JPMorgan’s private credit secondary trading lists.

Finastra (Vista). Placed a

2.95Bfirst−lientermloanand

500M second-lien in July 2025. Loans recently fell from high 90s to about 93-94.5 as sentiment cracked.

The Three Signals That Say a Deal Is About to Break

Watching a dozen of these over the past few years, the sequence is almost always the same:

Sponsor asks lenders for covenant relief (Vista did this on Pluralsight in Q1 2023, a full 18 months before the handover).

PIK toggle gets activated or extended (Medallia ran this playbook until the PIK window expired).

Lenders mark the debt below 80 cents (the distress threshold), then below 75 cents. At that point, the sponsor’s equity is economically worthless and it’s just a question of when, not if.

A fourth signal worth adding: banks pull a planned syndication. That’s what just happened to Qualtrics on March 17. It doesn’t always mean restructuring is imminent, but it means the market has repriced the risk faster than the sponsor can restructure the capital stack.

For Proofpoint specifically, no covenant relief request has surfaced publicly. That’s the thing to watch.

Three things matter for operators, not just observers:

PE exits are shrinking as a destination. If sponsors can’t refinance existing portfolio companies, they’re not buying new ones at reasonable prices. Secondary sale multiples are already compressed. If you were modeling an 8-10x revenue exit to a PE sponsor in 2027, rebuild the model at 4-6x.

PE-backed competitors are cutting, not investing. If you’re competing against a 30x EBITDA buyout loaded with private credit debt, they’re managing to a debt service number, not to a product roadmap. That’s an opening for well-capitalized AI-native challengers — and a meaningful one.

Venture debt needs a real stress test. The private credit funds under pressure are cousins of the venture debt providers. Lines of credit will get renegotiated, not renewed, for anything that looks shaky. If you have venture debt, model a scenario with growth down 10-15 points and see what happens to your covenants. Have the conversation with your lender now, not when you trip a covenant.

Medallia is not the canary. Pluralsight was the canary, in 2024. Medallia is the second bird down. Qualtrics, Proofpoint, Health Edge, Alteryx, Quest, and Cornerstone are the ones most likely to be the third.

The rest of the list has time to figure it out — but only if AI disruption of seat-based Saa S doesn’t accelerate, and multiples don’t compress any further from here. Neither is a great bet.

Almost Everyone's Gotten Radically More Efficient in Saa S

The Most Important Saa S Metric of All: Net New Customer Growth

Almost Everyone's Gotten Radically More Efficient in Saa S

The Most Important Saa S Metric of All: Net New Customer Growth

RSS Industry News

Get from

0to

100 Million in ARR

with less stress and more success.

Key Takeaways

AI VC

AI Mentor: Digital Jason + Amelia

AI Startup Benchmarking

AI Agent Playbook

Free e Books

e Book: Hiring a Great VP of Sales

e Book: Raising Capital

e Book: The First $1m ARR

University

All Posts

Podcasts

The Top CROs

VC Fundraising

Top Videos

Q&A

Best of Saa Str

#1 Bestselling Book

Search Everything

Join the Community

Free e Books

e Book: Hiring a Great VP of Sales

e Book: Raising Capital

e Book: The First $1m ARR

AI Annual 2026

Events Overview

Sponsors

Event Sponsorship

Media Sponsorship

Cut Costs with Runable

Cost savings are based on average monthly price per user for each app.

Which apps do you use?

Apps to replace

ChatGPT

$20 / month

Lovable

$25 / month

Gamma AI

$25 / month

HiggsField

$49 / month

Leonardo AI

$12 / month

TOTAL$131 / month

Runable price = $9 / month

Saves $122 / month

Runable can save upto $1464 per year compared to the non-enterprise price of your apps.