Panasonic Stops Making TVs: The End of an Era and What It Means for the Industry

Introduction: The Fall of Japan's TV Manufacturing Crown

In February 2025, Panasonic announced a seismic shift in its business strategy: it will no longer manufacture its own television sets. Instead, the Japanese electronics giant has handed over complete manufacturing, marketing, and distribution responsibilities to Skyworth, a Chinese television manufacturer headquartered in Shenzhen. This decision marks the effective end of one of Japan's most storied chapters in consumer electronics—a narrative that began in the era of plasma dominance and ended quietly in the age of flat-screen standardization.

For anyone who grew up watching television during the 2000s and early 2010s, Panasonic represented something aspirational: premium Japanese engineering, cutting-edge display technology, and uncompromising quality standards. The company controlled 40.7% of the global plasma TV market in 2010, a commanding position that seemed unassailable. Yet here we are, barely 15 years later, watching the company transform from manufacturer to brand licensee.

This development carries profound implications that extend far beyond Panasonic's balance sheet. It represents the final chapter in the decline of Japanese consumer electronics manufacturing. It demonstrates the relentless consolidation of the global TV industry under Chinese and South Korean control. And it raises critical questions about what "premium" means when your product is manufactured by a third party in a completely different country.

For consumers, the Skyworth partnership introduces both opportunities and uncertainties. Skyworth has positioned itself as a capable manufacturer with modern manufacturing capabilities and deep Android TV platform expertise. The company reportedly ranked in the top five global TV brands by sales revenue in Q1 2025, according to research from Omdia. Yet consumer familiarity with Skyworth remains limited, particularly in Western markets. When you buy a Panasonic TV going forward, you're essentially purchasing a Skyworth product bearing a Panasonic nameplate—a distinction with potentially significant implications for warranty support, long-term availability, and brand consistency.

This comprehensive guide explores the Panasonic announcement in exhaustive detail. We'll examine the historical context that led to this moment, analyze what the Skyworth partnership actually entails, consider the broader implications for the television industry, and help you understand what this means if you're considering purchasing a television. By the end, you'll have a complete picture of one of 2025's most significant consumer electronics developments.

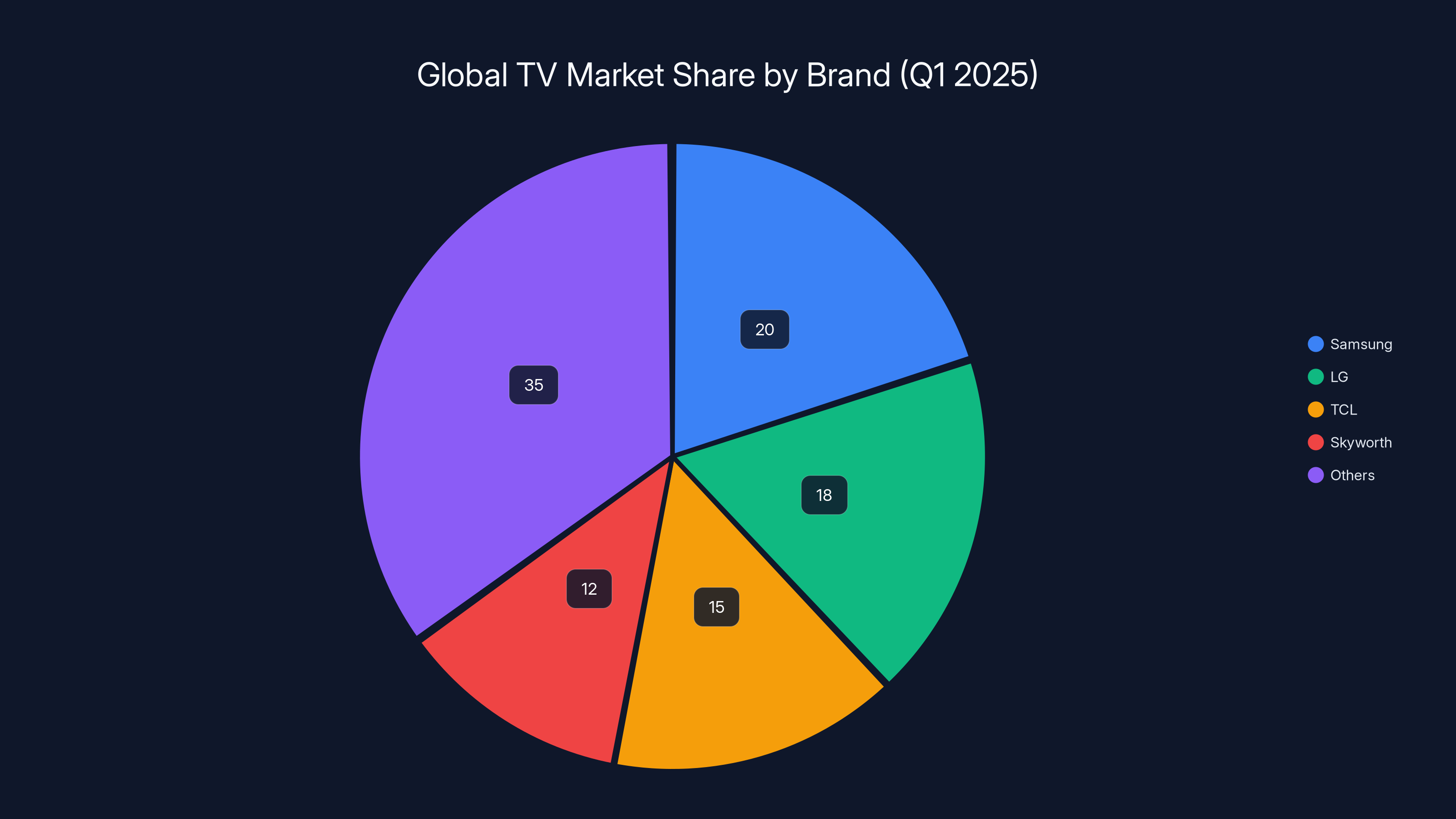

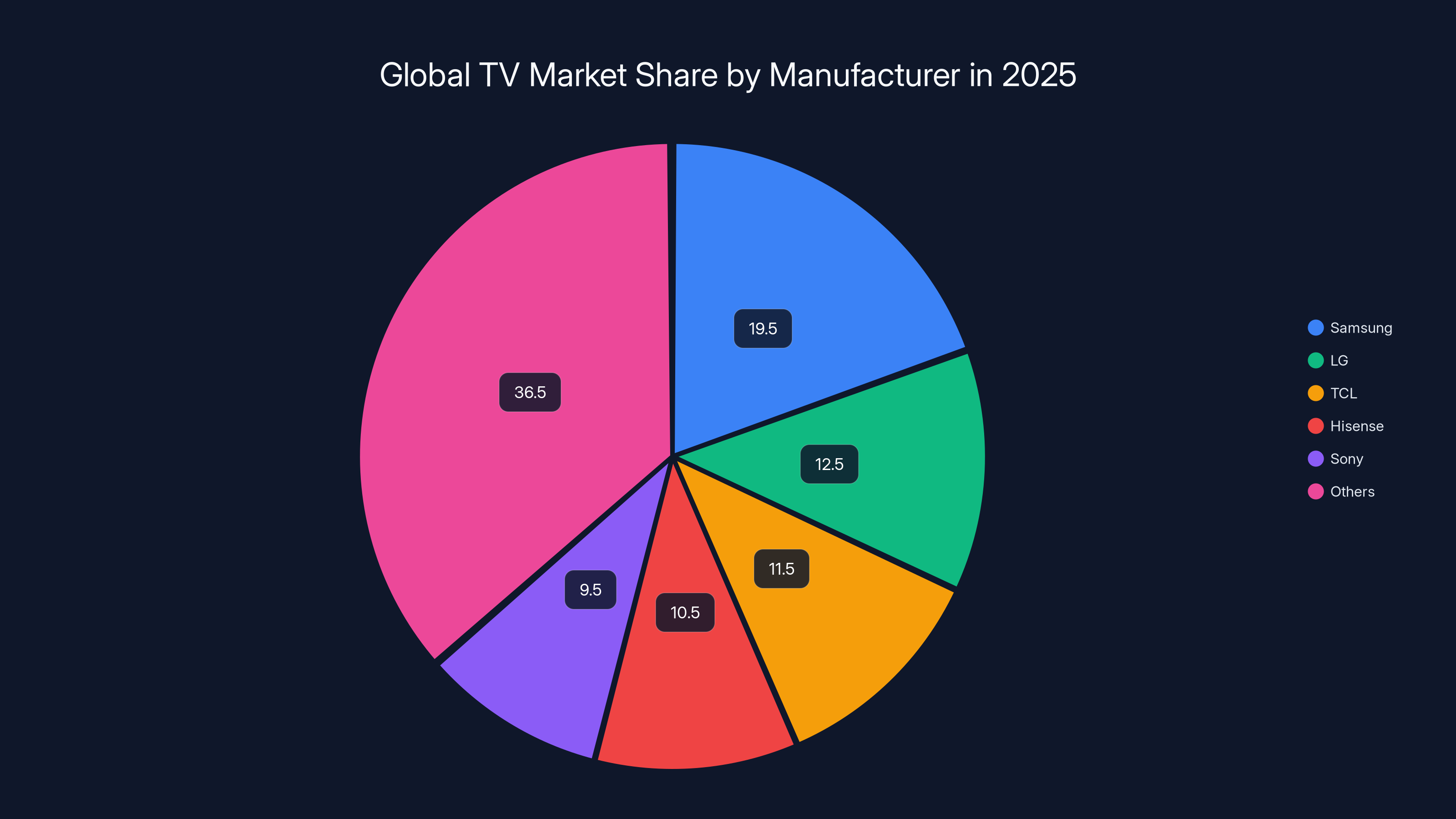

Skyworth ranks among the top five global TV brands by sales revenue, capturing 12% of the market in Q1 2025. Estimated data based on market trends.

Part 1: Understanding Panasonic's TV Business Trajectory

The Plasma Era: When Panasonic Dominated Television

To understand the significance of Panasonic's exit from TV manufacturing, we must first understand the heights from which it fell. During the plasma television era—roughly from the early 2000s through the early 2010s—Panasonic wasn't just a participant in the TV market. It was the undisputed leader.

Plasma technology itself represented a genuine leap forward in display quality. Unlike LCD displays, which relied on backlighting and liquid crystal panels to create images, plasma TVs used ionized gas between two glass panels to generate light directly. This approach offered several advantages: superior contrast ratios, wider viewing angles, deeper blacks, and faster response times. For serious television enthusiasts and home theater professionals, plasma was the gold standard.

Panasonic recognized this opportunity early and invested heavily in plasma technology development. The company manufactured both the display panels and the complete TV sets, controlling the entire value chain from silicon to finished product. This vertical integration allowed Panasonic to maintain quality standards and capture higher profit margins than competitors who relied on third-party panel suppliers.

By 2010, this strategy had reached its apex. Panasonic controlled nearly 41% of the global plasma TV market, according to Display Search data. This wasn't just market leadership—it was market domination. Samsung held 33.7% and LG claimed 23.2%, but Panasonic's position was unquestionably superior. The company manufactured plasma TVs under its own brand while also supplying panels to other manufacturers. Revenue flowed from multiple channels, and Panasonic's plasma business represented a crown jewel in the company's consumer electronics portfolio.

Yet even at the height of its dominance, the seeds of decline were being sown. LCD technology, which had long been considered inferior, was improving at a relentless pace. Manufacturing processes were becoming more efficient. Display quality was approaching parity with plasma in many respects, while offering advantages in weight, thickness, and power consumption. The writing was on the wall, though few wanted to read it.

The Transition Period: From Plasma to LCD and Beyond

In March 2014—a pivotal moment in Panasonic's history—the company made an announcement that stunned the industry: Panasonic would cease plasma TV production entirely. The decision shocked even seasoned industry observers. This wasn't a gradual phase-out or a "strategic reorganization." It was a complete, unambiguous exit from a business Panasonic had built and dominated.

The official reasoning was straightforward: falling demand for plasma TVs as consumers increasingly adopted LCD technology, combined with persistent profitability challenges. More candid observers noted that Panasonic hadn't actually made money on plasma TVs for years despite their market dominance. The company was essentially manufacturing loss leaders—products that sold well but generated minimal or negative profit margins.

This paradox—dominant market share coupled with poor profitability—reveals a critical truth about commodity hardware manufacturing. Once a technology becomes commoditized, scale matters more than innovation. Panasonic's plasma expertise couldn't protect it from the reality that LCD displays were becoming "good enough" while being cheaper to produce. The company faced a choice: invest billions in reengineering manufacturing processes for a dying technology, or exit the business and redeploy capital elsewhere.

Panasonic chose the latter. The company began systematically reducing its TV business presence. By 2016, Panasonic had completely exited the US consumer TV market, the world's most profitable television market. The company retained some presence in Japan and other Asian markets, but its TV division had been reduced from a crown jewel to a struggling operation.

However, Panasonic's exit from the US market proved temporary. In 2024, the company returned with new OLED and Mini LED models, explicitly marketed as "designed and developed in Japan." This return signaled that Panasonic still saw value in the TV business, but under a fundamentally different business model. The company was no longer betting on volume sales and market dominance. Instead, it was positioning itself as a premium brand competing on quality and innovation rather than scale.

The Outsourcing Decision: From Manufacturer to Designer

In 2021, Panasonic made a crucial announcement that foreshadowed the February 2025 development: the company would outsource all TV production to an undisclosed third-party manufacturer. This decision represented a philosophical shift. Panasonic would no longer be a TV manufacturer. It would be a brand owner and product designer contracting with external manufacturers for actual production.

This outsourcing arrangement actually functioned reasonably well for several years. By decoupling product design and brand management from manufacturing, Panasonic gained flexibility to respond to market changes without the capital constraints of owning manufacturing facilities. The company could design TVs to its specifications, have them manufactured by partners, and maintain quality control without operating factories.

Yet the arrangement had inherent limitations. Panasonic was ultimately beholden to its manufacturing partner's capabilities, capacity, and strategic priorities. A third-party manufacturer might prioritize higher-margin products for their own brands at the expense of Panasonic-branded goods. Supply chain disruptions, quality variations, or changes in partner priorities could impact Panasonic's ability to deliver products to market.

The 2025 Skyworth arrangement represents an evolution of this outsourcing model—not a departure from it. What's different is the scope. Under previous arrangements, a third party manufactured TVs to Panasonic specifications. Under the Skyworth deal, Skyworth doesn't just manufacture—it "leads sales, marketing, and logistics." Panasonic essentially becomes a brand name affixed to Skyworth products, with some input on premium OLED models through joint development arrangements.

Part 2: The Skyworth Partnership Explained

Who Is Skyworth? Understanding the Manufacturing Partner

Before evaluating the implications of the Panasonic-Skyworth arrangement, it's essential to understand who Skyworth actually is and what capabilities the company brings to this partnership.

Skyworth Digital Holdings Limited is a publicly traded Chinese electronics manufacturer based in Shenzhen. The company manufactures televisions, set-top boxes, digital media players, and related consumer electronics equipment. Unlike many Chinese manufacturers that operate in relative obscurity, Skyworth has invested in building brand recognition, particularly in emerging markets where it competes directly against Samsung, LG, TCL, and other established television manufacturers.

According to Omdia research from July 2025, Skyworth ranked among the top five global TV brands by sales revenue in the first quarter of 2025. This is a significant position—the global TV market generates roughly $100+ billion annually, and maintaining a top-five position requires manufacturing at scale, reliable distribution networks, and market presence across multiple geographies. Skyworth has invested heavily in all three.

Skyworth also claims expertise with the Android TV platform, positioning itself as "a top three global provider" of Android TV implementations. This expertise matters because Android TV has become the dominant smart TV operating system globally. Unlike proprietary systems developed by individual manufacturers, Android TV provides a common foundation that app developers, streaming services, and consumers understand. Strong expertise with Android TV translates to ability to rapidly bring new products to market with current software features.

The company operates extensive manufacturing facilities in Shenzhen and maintains distribution partnerships across Asia, Europe, and North America. Skyworth doesn't just manufacture TVs for export—it actively sells televisions under its own brand globally, giving it direct experience with consumer preferences, distribution challenges, and market dynamics in different regions.

What the Partnership Actually Entails

The Skyworth-Panasonic arrangement represents a three-part division of responsibilities:

Manufacturing, Sales, and Logistics: Skyworth assumes complete responsibility for these operational functions. The company manufactures Panasonic-branded TV sets in its facilities, manages inventory, handles logistics and shipping, and leads sales efforts in targeted markets. Skyworth essentially treats Panasonic-branded televisions as one of its product lines.

Quality Assurance and Expertise Sharing: Panasonic maintains involvement in quality control and product development. According to the announcement, Panasonic will "provide expertise and quality assurance to uphold its renowned audiovisual standards." This means Panasonic engineers will presumably review designs, establish quality benchmarks, and conduct testing to ensure Skyworth-manufactured products meet Panasonic standards.

Premium Product Joint Development: For high-end OLED models, Panasonic and Skyworth will engage in "full joint development." This arrangement gives Panasonic greater influence over flagship products, ensuring these premium-tier televisions reflect Panasonic's engineering approach and quality standards.

So what does this actually mean in practical terms? When you purchase a Panasonic TV in 2026 or later, you're buying a television manufactured by Skyworth in Skyworth's factories, using Skyworth's supply chains and engineering, but bearing the Panasonic brand name and meeting quality standards that Panasonic has defined. It's a critical distinction.

Geographic Scope and Market Strategy

Skyworth-manufactured Panasonic TVs will initially be sold in the United States and Europe—the world's two largest TV markets. These markets represent roughly $40-50 billion in annual television spending, so the potential revenue is substantial.

In Europe specifically, Panasonic and Skyworth are targeting "double-digit market share." This is an ambitious goal. The European TV market includes strong competition from Samsung (typically the market leader with 20-25% share), LG, TCL, and various regional brands. Achieving double-digit market share would require capturing 10-15% of European TV sales, positioning Panasonic-branded sets as one of the three top brands in the region. Whether Skyworth can achieve this depends on product positioning, pricing strategy, and brand perception.

The fact that Panasonic is focusing on the US and European markets (rather than, say, expanding aggressively in Asia where Skyworth has stronger brand recognition) suggests the partnership is specifically designed to leverage the Panasonic brand name in Western markets where it retains equity and recognition.

Support Timeline and Transition Mechanics

Panasonic has committed to providing support for all TVs "sold up to March 2026 and all those available from April." This means:

- TVs purchased before April 2026 will receive Panasonic warranty support and service

- TVs purchased from April 2026 onward will technically be Skyworth products, though bearing the Panasonic brand

The transition suggests Panasonic will wind down its direct customer service obligations, with Skyworth presumably assuming responsibility for warranty claims, repairs, and customer support for future purchases. This is a significant change for consumers accustomed to dealing with Panasonic's established service networks.

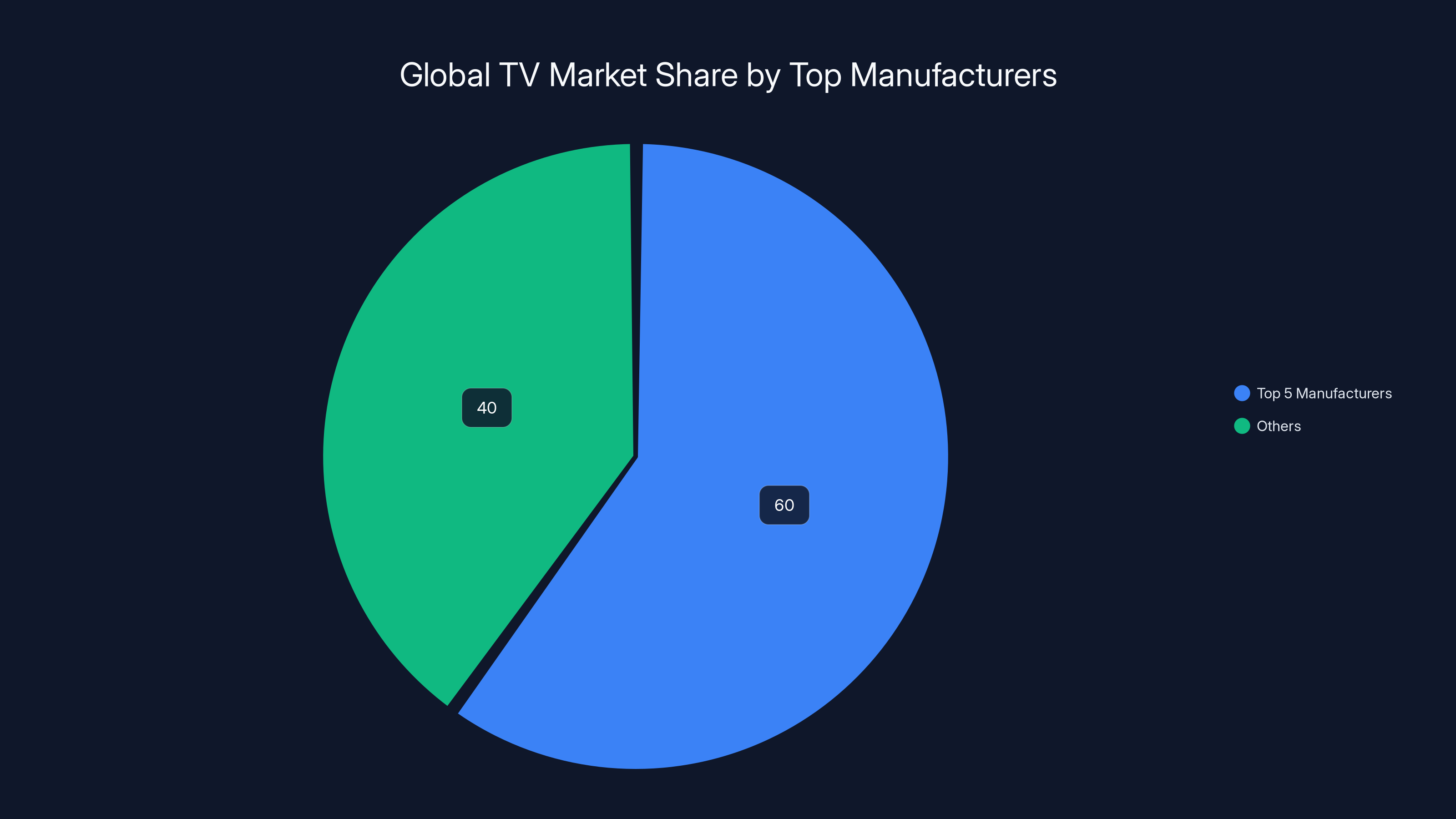

The global TV market has seen significant consolidation, with the top five manufacturers increasing their market share from 60% in 2010 to an estimated 75% in 2025. Estimated data.

Part 3: Why This Happened: The Structural Forces Behind Panasonic's Exit

The Economics of TV Manufacturing Today

To understand why Panasonic made this decision, it's essential to understand the current economics of television manufacturing. The TV industry in 2025 is radically different from the TV industry of 2010, and those differences explain why even dominant manufacturers exit the business.

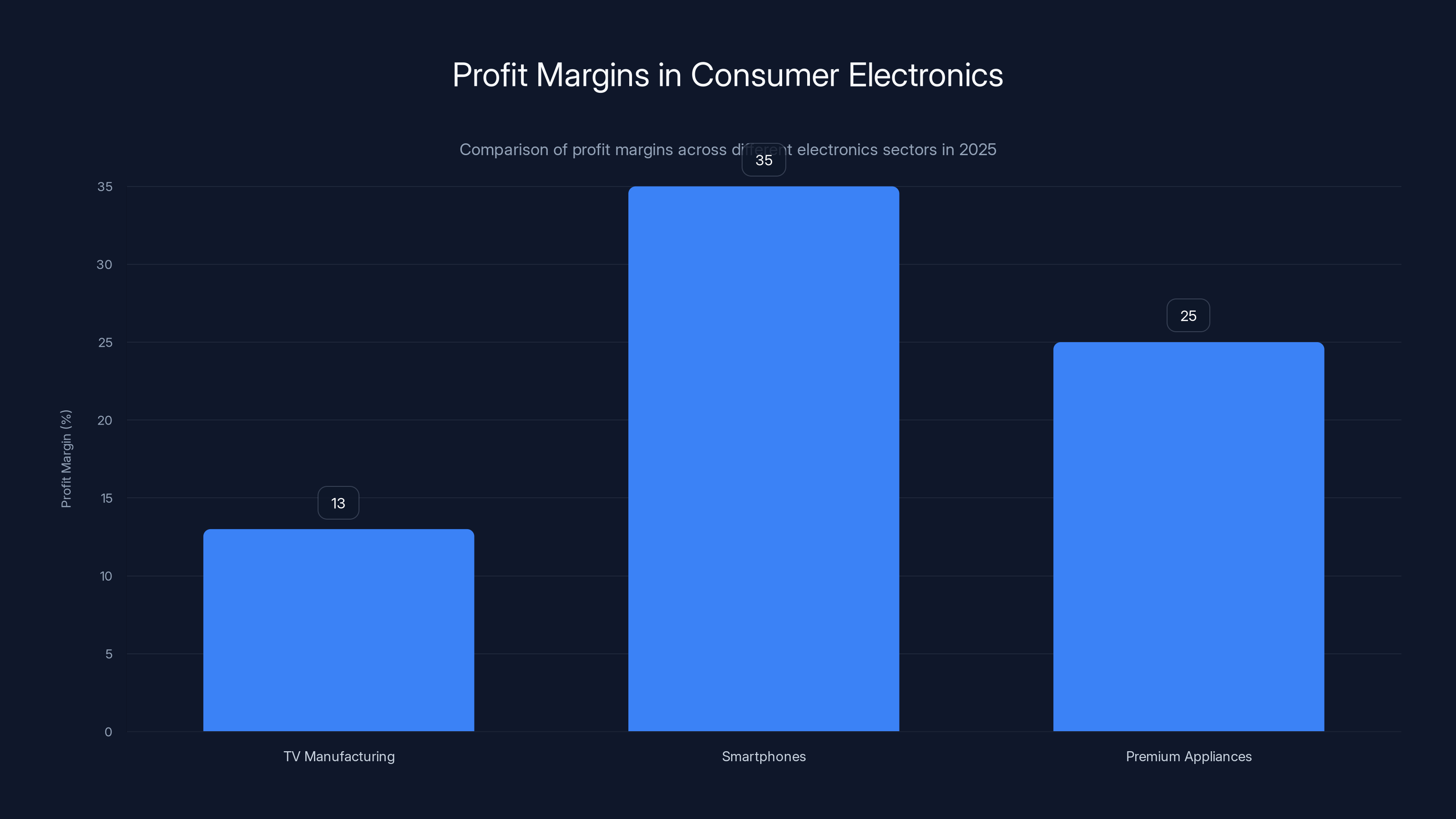

The Margin Compression Problem: Television manufacturing has become a low-margin, high-volume business. A typical TV retailer might purchase a 55-inch 4K TV from a manufacturer for

Compare this to smartphones, where manufacturers like Apple capture 30-40% margins, or to premium appliances where margins can exceed 25%. Television manufacturing is fundamentally less profitable than other consumer electronics categories, yet requires comparable engineering investment and capital expenditure.

The Commodity Display Panel Problem: Modern TVs are fundamentally commodity products built around commodity display panels. Samsung manufactures panels. LG manufactures panels. China's BOE manufactures panels. A TV manufacturer's margin depends less on the quality of their engineering and more on their ability to negotiate favorable panel pricing from suppliers.

Panasonic doesn't manufacture its own LCD or OLED panels anymore. The company must purchase panels from external suppliers, paying commodity prices. This removes a critical competitive advantage—vertical integration—that Panasonic enjoyed during the plasma era. Now Panasonic competes on the same terms as every other TV manufacturer: access to commodity panels plus software/user interface plus marketing.

The Scale Disadvantage: The TV market favors massive manufacturers that can achieve extreme scale. Chinese manufacturers like TCL, Hisense, and Skyworth manufacture tens of millions of units annually, allowing them to negotiate aggressively with panel suppliers, achieve extremely low manufacturing costs, and spread R&D expenses across enormous volume. Panasonic simply doesn't have the scale to compete on cost.

A Japanese manufacturer paying Japanese wages in Japanese factories can't compete with a Chinese manufacturer operating at 10-20 times the volume. It's not a question of engineering capability—it's a question of fundamental economics. The Chinese manufacturer wins through scale, period.

The Japanese Manufacturing Exodus

Panasonic's exit from TV manufacturing isn't isolated. It's part of a broader exodus of Japanese consumer electronics manufacturing that has been underway for over a decade.

Sharp: Once one of Japan's most respected electronics companies, Sharp exited the TV manufacturing business years ago. The company now licenses its brand to Chinese manufacturers, similar to the Panasonic-Skyworth arrangement.

Toshiba: Toshiba ceased manufacturing televisions and now operates primarily as a corporate conglomerate focused on infrastructure, semiconductors, and industrial products.

Hitachi: Exited television manufacturing years ago, having concluded the business was incompatible with the company's strategic direction.

Pioneer: Ceased consumer TV manufacturing long ago, pivoting to professional and automotive electronics.

Sony: In early 2025, Sony announced it was selling 51% of its home entertainment business (including televisions) to TCL, a Chinese manufacturer. This represents a partial exit—Sony retains branding and some design input, but TCL assumes manufacturing responsibility.

The pattern is unmistakable: Japanese electronics companies have systematically exited consumer TV manufacturing over the past 15 years. Those remaining in the business are operating at minimal scale or have fundamentally restructured their business models. Meanwhile, South Korean manufacturers (Samsung, LG) and Chinese manufacturers (TCL, Hisense, Skyworth) have consolidated the market.

The Shift in Global Manufacturing Power

This exodus reflects deeper changes in global manufacturing. In 2000, Japan was a consumer electronics superpower. Japanese companies dominated televisions, cameras, audio equipment, and most consumer electronics categories. In 2025, the landscape has transformed completely.

China's Rise: Chinese manufacturers have invested $500+ billion in consumer electronics manufacturing over the past 20 years. They've built massive factories, trained millions of workers, and developed sophisticated supply chains. They can manufacture TVs at a cost point that Japanese manufacturers simply cannot match, even assuming equivalent quality.

The Cost Advantage: A typical TV manufactured in China might cost

Supply Chain Integration: Chinese manufacturers control or partner closely with panel makers, component suppliers, and logistics providers. They've created ecosystem advantages that allow them to reduce costs faster than competitors can match. Panasonic, operating outside this ecosystem, faces a structural disadvantage.

Labor Cost Realities: Japanese workers earn substantially more than Chinese workers, and manufacturing is labor-intensive despite automation. A factory producing TVs in Japan costs more to operate than a factory producing identical TVs in China, and this cost difference cannot be competed away through efficiency alone.

Part 4: The Broader Television Industry Landscape

The Global TV Market Structure in 2025

Understanding the Panasonic-Skyworth partnership requires understanding the current structure of the global television market. The industry has consolidated dramatically over the past decade.

Market Leaders by Volume:

- TCL (China) - Roughly 11-12% global market share

- Hisense (China) - Roughly 10-11% global market share

- Samsung (South Korea) - Roughly 19-20% global market share

- LG (South Korea) - Roughly 12-13% global market share

- Sony (Japan/TCL partnership) - Roughly 9-10% global market share

- Others including Skyworth, Panasonic, Vizio, Philips, etc. - Remaining 35-40% share

Two critical observations emerge from this market structure:

First, the market is dominated by Chinese and South Korean manufacturers. Japanese manufacturers that once represented perhaps 30-40% of the market now represent less than 10% combined (Panasonic has roughly 2-3% share independently, declining). This shift has occurred over roughly 15 years.

Second, the market remains fragmented. Unlike smartphones where Apple and Samsung dominate, or laptops where Lenovo, HP, and Dell lead, the TV market has numerous competitors with single-digit market shares. This fragmentation reflects the commodity nature of the product—there's limited differentiation between a Samsung TV and a TCL TV at the same price point, so consumers choose based on price, brand familiarity, and local availability.

Premium vs. Budget Market Dynamics

The television market has also segmented dramatically into premium and budget categories, with different dynamics in each segment.

Budget TVs ($200-400): These are essentially commodity products manufactured by anyone with access to panels and manufacturing capacity. Skyworth competes effectively in this segment. Panasonic cannot, because Japanese manufacturing costs are incompatible with budget TV margins. The Skyworth partnership allows Panasonic to access the budget segment through a low-cost manufacturer.

Mid-Range TVs ($400-800): This segment features growing competition from multiple manufacturers. Consumers at this price point show somewhat more brand preference and quality expectations, but the segment remains price-sensitive. This is where Skyworth likely positions Panasonic-branded products.

**Premium TVs (

The OLED Opportunity

One significant detail from the Panasonic announcement warrants emphasis: Panasonic showed off two OLED TV prototypes during the launch event, including one using LG Display's newest Tandem WOLED panel.

This is important because OLED technology represents the one segment where Japanese brands can still compete effectively. OLED displays offer superior picture quality compared to LED-lit LCD displays, justifying premium pricing. The technology is complex enough that consumers understand there's a quality difference, unlike budget LCD TVs where differentiation is minimal.

LG Display manufactures most of the world's OLED display panels used in televisions. Samsung manufactures some OLED panels for its own TVs. But LG Display remains the leader, supplying panels to multiple manufacturers including Panasonic (going forward through Skyworth). By focusing joint development efforts on OLED models, Panasonic and Skyworth are positioning their partnership to compete in the segment where brand and picture quality matter most.

The prototypes shown at the launch event suggest Panasonic intends for its OLED lineup to reflect genuine engineering innovation, not merely rebadged Skyworth products. This strategic focus makes sense: the OLED market can support higher margins and commands greater brand loyalty than budget TV segments.

Part 5: What This Means for Consumers

The Warranty and Support Question

For consumers who own Panasonic televisions or are considering purchasing them, the partnership raises immediate practical questions about warranty support and long-term reliability.

For Existing Panasonic TV Owners: If you purchased a Panasonic TV before April 2026, you'll receive warranty support through Panasonic's established channels. After April 2026, when those warranties expire, servicing may transition to Skyworth-authorized service centers. This transition could mean:

- Longer wait times if Skyworth has less developed service infrastructure in your region

- Different service quality standards if Skyworth's service partners aren't as rigorously trained as Panasonic's were

- Potentially higher service costs if Skyworth uses different pricing models

- Possible service discontinuation if Skyworth decides supporting older Panasonic TV models isn't profitable

For Future Panasonic TV Purchasers: Starting in April 2026, Panasonic TVs will technically be Skyworth products. Your warranty and support relationship will be with Skyworth, not Panasonic. This introduces some uncertainty:

- Service Network Quality: Skyworth's service networks in Western markets are less established than Panasonic's historical networks. You may have fewer service options available.

- Language and Communications: Skyworth is a Chinese company. While it presumably will establish English-language support channels for Western markets, communication clarity might be less polished than you'd expect from a long-established Japanese brand.

- Service Availability Horizon: How long will Skyworth support older Panasonic TV models? Chinese manufacturers typically focus on newer product generations more aggressively than Japanese manufacturers did.

The Brand Loyalty Question: For consumers who've purchased Panasonic televisions because they trust the brand, the partnership introduces risk. You're no longer purchasing products with Panasonic's reputation directly behind them. You're purchasing Skyworth products bearing a Panasonic brand license. If something goes wrong, Panasonic's historical reputation for quality becomes less relevant—your actual experience depends on Skyworth's quality and service.

Product Quality and Design Implications

Will Skyworth-manufactured Panasonic TVs be as good as Panasonic-manufactured Panasonic TVs?

This question requires nuance. For budget and mid-range models, Skyworth's manufacturing quality is likely to be roughly equivalent to what Panasonic was producing anyway. Panasonic wasn't manufacturing TVs domestically anymore—it was outsourcing production to third parties. Skyworth is a larger, more capable manufacturer than many third parties Panasonic previously worked with. So product quality for non-premium models might actually be acceptable or even slightly improved.

For premium OLED models, the story is different. The partnership includes joint development arrangements, meaning Panasonic engineers will presumably be involved in design and specification. This suggests premium models should maintain design quality standards, though manufacturing quality ultimately depends on Skyworth's execution.

However, there's a subtle but important distinction: Panasonic was a design-first company. Engineers at Panasonic were obsessed with display quality, color accuracy, and user interface refinement. Skyworth is a manufacturing-first company focused on cost optimization and volume production. Even with joint development arrangements, this fundamental difference in corporate culture could manifest in subtle quality differences—not necessarily worse, but different.

The Pricing Question

Will Panasonic TVs become cheaper now that Skyworth manufactures them?

Probably not in the short term. Panasonic is positioning itself as a premium brand, and pricing strategy will reflect that. The Panasonic brand name carries value in Western markets, so Skyworth will likely maintain price points comparable to previous Panasonic models. However, the lower manufacturing costs Skyworth achieves might translate into:

- Improved profit margins for Panasonic and Skyworth, not necessarily lower consumer prices

- More feature-rich models at the same price point as Panasonic previously offered

- Gradual price reductions as market share grows and Skyworth benefits from scale

Consumers shouldn't expect a dramatic "Skyworth effect" where prices plummet. Instead, expect pricing to stabilize at competitive market rates, with perhaps modest improvements in feature value over time.

TV manufacturing has significantly lower profit margins (13-20%) compared to smartphones (30-40%) and premium appliances (25%). This margin compression is a key factor in Panasonic's exit from the TV market.

Part 6: Competitive Implications and Market Positioning

How This Affects Samsung and LG

The Panasonic-Skyworth arrangement has interesting implications for Panasonic's primary competitors.

Samsung's Position: Samsung manufactures its own TVs and panels, maintaining vertical integration that Panasonic abandoned. Samsung's manufacturing costs are lower than Panasonic's were, but not dramatically lower, because Samsung operates massive facilities in South Korea and elsewhere. Samsung can still compete effectively on quality and innovation. However, the Panasonic-Skyworth deal means Skyworth (a company Samsung competes with globally) now has access to Panasonic's brand value and historical customer base in Western markets. From Samsung's perspective, this is mixed news—a competitor became somewhat stronger in the Panasonic brand-name market, but Panasonic's independent manufacturing capacity was minimal anyway.

LG's Position: LG operates similarly to Samsung, manufacturing its own TVs and panels. LG also manufactures OLED panels that Skyworth will use for Panasonic-branded TVs. So LG has a financial interest in this partnership—LG Display stands to earn revenue from selling OLED panels to Skyworth for Panasonic TV production. From a competitive standpoint, LG faces a stronger Skyworth through this partnership, but also benefits from panel sales revenue.

How This Affects TCL and Hisense

For TCL and Hisense, the Panasonic-Skyworth partnership is largely neutral to slightly negative. These companies compete directly with Skyworth and benefit from fragmenting the market further (more competitors = harder for any single competitor to gain scale advantages). However, Skyworth gaining access to the Panasonic brand name in Western markets does strengthen one of their competitors.

How This Affects Sony

Sony's situation is particularly interesting. In early 2025, Sony sold 51% of its TV business to TCL, a Chinese manufacturer. Sony retained 49% ownership and maintains design/branding authority over Sony-branded TVs. The Panasonic-Skyworth arrangement is actually less extensive than the Sony-TCL arrangement—Panasonic has less control over the manufacturing process than Sony does.

Sony's willingness to sell its TV business to TCL in 2025, combined with Panasonic's announcement in February 2025, suggests a clear trend: Japanese TV manufacturers are concluding that direct manufacturing is no longer strategically viable. Sony and Panasonic will henceforth compete primarily through branding and design, not manufacturing excellence.

Part 7: The End of Japanese Electronics Manufacturing

A Historical Perspective

The Panasonic announcement marks the effective end of Japanese consumer electronics manufacturing as a significant force in the television market. To appreciate the magnitude of this shift, some historical context helps.

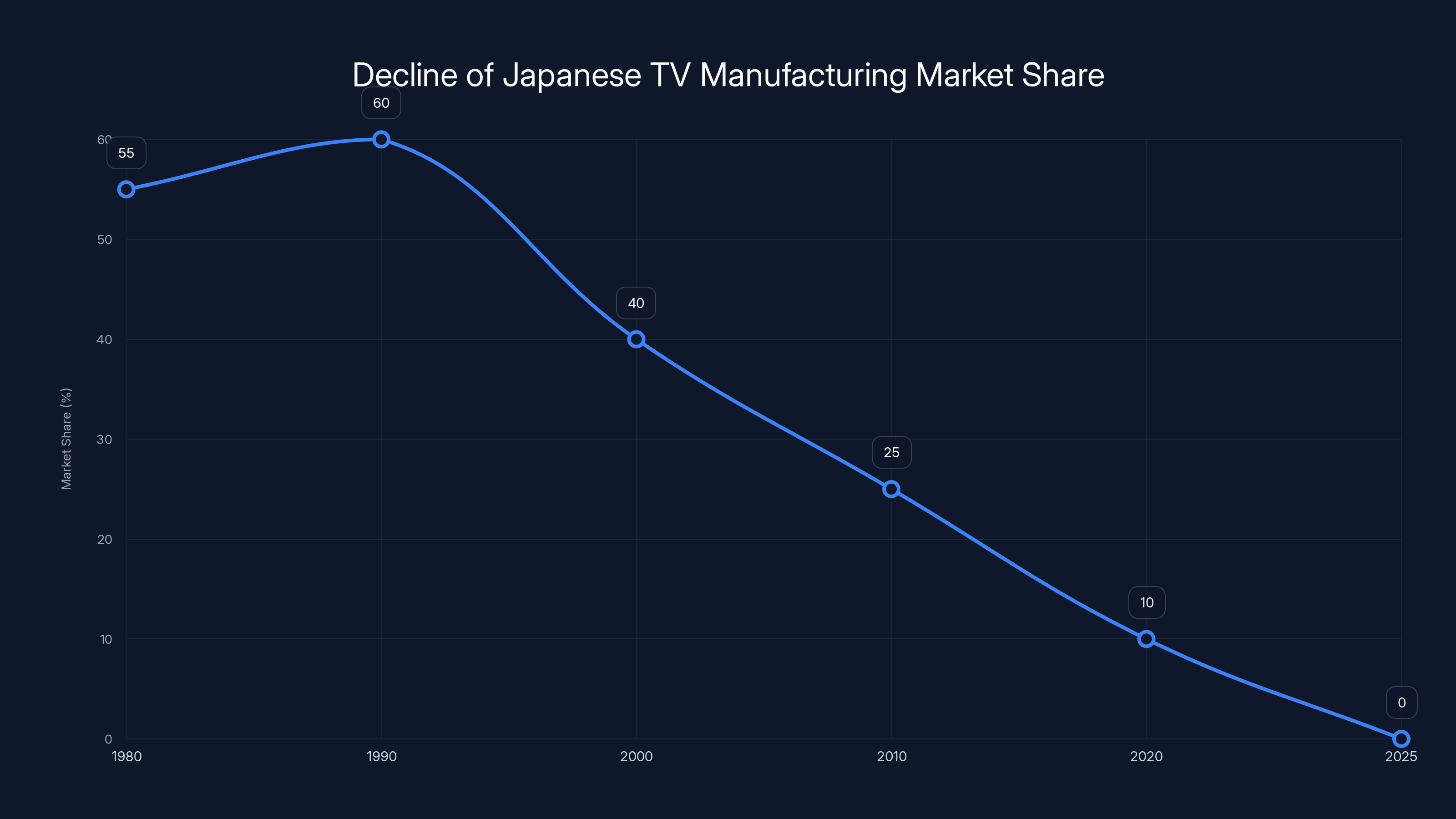

In the 1980s and 1990s, Japanese electronics companies represented perhaps 50-60% of global television manufacturing. Sony, Panasonic, Toshiba, Hitachi, Pioneer, and others manufactured TVs that defined the premium market globally. Japanese brands were synonymous with quality, reliability, and innovation. Japanese engineers invented many of the technologies that made modern televisions possible.

By 2010, Japanese manufacturers had lost the budget and mid-range market entirely to Chinese competitors, but still dominated the premium segment. Panasonic's 41% share of the plasma market represented the last bastion of Japanese TV manufacturing dominance.

By 2025, Japanese manufacturers have effectively exited the market entirely. Panasonic is now outsourcing to a Chinese manufacturer. Sony is outsourcing to a Chinese manufacturer. Toshiba, Sharp, Hitachi, and Pioneer have already exited.

This transformation has occurred in less than 40 years—a blink of an eye historically. Japanese electronics manufacturers went from global dominance to irrelevance in consumer televisions within a single generation.

Why Japanese Manufacturing Lost the Television War

Several interconnected factors explain this dramatic decline:

1. Capital Intensity: Television manufacturing requires massive capital investment in factories, equipment, and inventory. Japanese companies, operating with higher labor costs, needed greater volume to justify this capital. When Chinese competitors started producing 50 million TVs annually at 1/3 the cost, Japanese manufacturers couldn't justify the capital investment required to compete.

2. Technology Commoditization: The technology underlying modern TVs—LCD/LED panels, power supplies, circuits, processors—became standardized and available from multiple suppliers. Innovation mattered less; scale and cost mattered more. Japanese companies excelled at innovation but struggled at commodity-scale production.

3. Labor Cost Advantages: Chinese workers earning

4. Vertical Integration Disadvantages: Japanese companies owned factories, manufacturing facilities, and component makers. These were assets that required maintenance and generated ongoing costs. Chinese competitors, unburdened by legacy assets, could shift manufacturing locations quickly and optimize for lowest-cost production. Flexibility mattered more than asset ownership.

5. Supply Chain Geography: As panel manufacturing shifted to Taiwan, South Korea, and China, Japanese manufacturers became geographically disadvantaged. Chinese TV manufacturers could receive components the next day; Japanese manufacturers faced shipment times and logistics costs.

6. Brand Loyalty Decay: In the premium market, Japanese brands like Panasonic commanded loyalty through reputation. But this loyalty proved fragile when consumers discovered that a TCL TV at 60% of the Panasonic price offered 95% of the picture quality. Over time, brand premium eroded, and price became the primary purchasing criterion.

The Broader Pattern in Japanese Electronics

The television industry story is part of a much broader pattern affecting Japanese electronics generally. Japan's share of global electronics manufacturing has declined from 20-25% in 2000 to less than 10% in 2025.

Japanese companies remain strong in niche premium segments (high-end cameras, professional audio equipment, automotive electronics), but have largely ceded the consumer mass market to Chinese and South Korean competitors. This shift has profound implications for Japan's economy and technology leadership.

Part 8: Understanding the TV Manufacturing and Technology Landscape

Display Technology Overview

To appreciate the nuances of the Panasonic-Skyworth partnership, understanding modern TV display technology is helpful.

LCD/LED Displays: The dominant display technology, LCD (Liquid Crystal Display) uses a backlight to illuminate liquid crystals that create images. LED (Light Emitting Diode) refers to the backlighting technology. LED-backlit LCDs are the industry standard for budget and mid-range TVs. Cost-effective but suffer from inferior contrast ratios and viewing angles compared to newer technologies.

Mini LED: A stepping stone between traditional LED-backlit LCD and OLED, Mini LED uses thousands of tiny LEDs for backlighting instead of a few larger LEDs. This allows for better local dimming and improved contrast. Panasonic specifically mentioned Mini LED models in its 2024 US market return, suggesting the company sees this technology as an opportunity to differentiate from pure LCD competitors.

OLED (Organic Light Emitting Diode): Each pixel generates its own light, eliminating the need for backlighting. This allows perfect blacks (when pixels are off, no light emits), superior contrast, faster response times, and better viewing angles. OLED technology is more expensive to manufacture, requires more careful handling, and historically has suffered from burn-in issues (permanent image retention). However, OLED TVs provide the best picture quality available, and burn-in has become less significant with modern panel improvements.

Tandem WOLED: LG Display's latest OLED innovation, Tandem WOLED represents an evolution where OLED panels are stacked to improve brightness and efficiency. According to the Panasonic announcement, the company's premium prototypes use LG Display's Tandem WOLED panels, indicating a focus on cutting-edge display technology for premium models.

QD-LED and Quantum Dot: Samsung's approach to premium picture quality, QD-LED (Quantum Dot LED) combines LED backlighting with quantum dot materials that enhance color. Not as superior to OLED as OLED's marketing suggests, but a legitimate technology providing improved color performance vs. standard LED-backlit LCDs.

The Android TV Operating System

Skyworth specifically highlighted its expertise with Android TV, which warrants explanation because the operating system is crucial to modern TV functionality.

Android TV is Google's smart TV platform based on the Android operating system. It allows TVs to run streaming applications (Netflix, Hulu, Disney+, etc.), access online content, and update software features. Most mid-range and budget TVs sold globally run some version of Android TV or similar smart TV platforms.

Advantages of Android TV:

- Open ecosystem: Developers create apps for Android TV because it's widespread

- Rapid updates: Google provides regular security and feature updates

- Familiar interface: Users who have Android phones recognize the interface

- Cost-effective: Google provides the operating system; manufacturers pay minimal licensing fees

Skywort's claimed expertise as "top three global provider of the Android TV platform" suggests the company has:

- Deep knowledge of the underlying Android TV codebase

- Ability to customize the interface and user experience

- Relationships with Google and content providers

- Expertise bringing new Android TV features to market rapidly

This expertise translates to better software performance, faster feature rollout, and smoother user experience for Panasonic-branded TVs. It's one significant advantage Skyworth brings to the partnership.

Manufacturing Complexity

While TVs appear simple (rectangular box with screen), manufacturing involves surprising complexity:

Panel Sourcing: Securing adequate supply of display panels from Samsung, LG Display, or BOE at favorable prices. Panel costs are typically 25-35% of the final product cost, so this is critical.

Logistics: Managing supply chains across multiple countries, shipping components to manufacturing facilities, and shipping finished products to regional warehouses and retailers.

Quality Control: Testing panels, components, and finished products for defects. Defect rates must be maintained below 2-3% for profitability.

Software Integration: Loading the operating system, configuring the user interface, testing streaming services and apps.

Certification and Compliance: Ensuring products meet regulatory requirements for electrical safety, electromagnetic emissions, and environmental standards in different markets.

Skyworth's scale allows the company to optimize each of these processes for cost and efficiency. Panasonic was attempting to do this while competing on a much smaller volume basis—an impossible situation economically.

Samsung leads the global TV market with a 19.5% share, followed by LG and TCL. The market remains fragmented with a significant portion held by 'Others', highlighting the competitive landscape. Estimated data.

Part 9: Strategic Alternatives Panasonic Considered

What Panasonic Could Have Done Differently

When evaluating the Panasonic-Skyworth partnership, it's worth considering what alternatives Panasonic had and why this arrangement was superior to other options.

Continue Independent Manufacturing: Panasonic could have continued manufacturing its own TVs, attempting to compete on quality and brand value. This would have required accepting minimal margins, competing primarily in the premium OLED segment, and gradually shrinking market share as volume-driven competitors undercut pricing. Eventually, the business would likely become so small as to be unviable. This option was economically untenable.

Compete on Technology Innovation: Panasonic could have attempted to develop breakthrough display technologies or features that justified premium pricing. However, innovation in TV technology has slowed dramatically. OLED represents the last major innovation (and LG Display leads there). Further innovation is likely to be incremental. Betting the business on breakthrough innovation is high-risk when the market demands commoditized products.

Pursue Premium Market Dominance: Panasonic could have exited the budget and mid-range market entirely, focusing exclusively on premium OLED TVs. However, the premium OLED market is relatively small (perhaps 15-20% of total TV unit sales) and dominated by Samsung, LG, and Sony. Panasonic would be competing for tiny market share against entrenched competitors. This would have been viable but would have meant a much smaller TV business.

Partner with a South Korean Manufacturer: Panasonic could have partnered with Samsung or LG, allowing one of these companies to manufacture Panasonic-branded TVs. This might have provided access to better technology (Samsung and LG both manufacture their own panels). However, Samsung and LG have little incentive to strengthen a competitor's brand, and they'd likely withhold their best technologies. Additionally, this arrangement would potentially violate antitrust regulations in some markets.

Exit the TV Business Entirely: Panasonic could have simply stopped making/selling TVs, as several other Japanese manufacturers have done. This would have eliminated ongoing losses but would also have meant abandoning a business with some positive cash flow, even if margins are modest. The Skyworth arrangement allowed Panasonic to maintain a TV business without bearing manufacturing costs.

Given these alternatives, the Skyworth arrangement emerges as a reasonable middle path: Panasonic exits capital-intensive manufacturing while remaining in the TV market through branding and design. This minimizes losses while maintaining revenue streams and brand presence.

Part 10: The Future of Television Manufacturing and Consumer Electronics

Where Television Manufacturing is Heading

The Panasonic-Skyworth partnership provides insight into the direction television manufacturing is heading globally.

Consolidation Around Chinese and South Korean Manufacturers: The long-term trajectory is clear: Chinese manufacturers (TCL, Hisense, Skyworth, others) and South Korean manufacturers (Samsung, LG) will manufacture nearly all televisions. Japanese and European manufacturers will increasingly become brand/design companies licensing their names to Asian manufacturers.

Premium/Commodity Bifurcation: The market will increasingly separate into budget/commodity products (manufactured by the lowest-cost provider, minimal differentiation) and premium products (emphasizing design, picture quality, and innovation). Mid-range products will gradually disappear as price competition pushes budget buyers toward commodity options and quality buyers toward premium options.

Location Consolidation: Manufacturing will increasingly concentrate in China, Taiwan, and South Korea—geographies with the best supply chains, lowest costs, and most developed ecosystems. Manufacturing elsewhere becomes uneconomical.

Technology Stagnation: With declining innovation and commoditization, TV technology will advance more slowly. OLED will remain the premium option; LED-backlit LCD will remain the budget option. Incremental improvements will continue, but breakthrough innovations are unlikely for the foreseeable future.

Implications for Consumers

These trends have concrete implications for consumers shopping for televisions:

1. Brand Reliability Declining: Traditional brand reliability advantages erode when your television is manufactured by Skyworth regardless of whether it bears a Panasonic or Skyworth nameplate. Consumers increasingly can't rely on brand reputation as a quality signal.

2. Warranty Support Becoming Uncertain: As manufacturing shifts to multiple countries and third-party contract manufacturers, warranty support chains become complex. Service quality will likely decline from historical averages.

3. Price Competition Intensifying: With manufacturing consolidated around low-cost providers, price competition will intensify, but so will commoditization. Price differences between brands will narrow as feature differences narrow.

4. Model Continuity Decreasing: Third-party manufacturers can discontinue product lines more aggressively than vertically integrated companies can. You might struggle to find replacement parts or service for a three-year-old TV.

5. Premium Segment Sustaining Value: The one area where brand value sustains is premium OLED TVs, where technology and design create genuine differentiation. Consumers seeking long-term value should focus on premium OLED models from established brands rather than budget options.

Part 11: Skyworth's Global Strategy and Brand Building

Who Skyworth Is Really Trying to Reach

Understanding why Skyworth pursued the Panasonic partnership requires understanding Skyworth's broader global strategy.

Skyworth is a major television manufacturer by volume, but outside Asia, the brand recognition is minimal. Most North American and European consumers have never heard of Skyworth. When they shop for TVs, they recognize Samsung, LG, Sony, TCL, maybe Hisense. Skyworth barely registers.

This visibility gap matters. In consumer electronics, brands with historical equity can command price premiums. A Samsung TV priced 10% higher than a Skyworth TV of identical specs will likely outsell it substantially because consumers recognize Samsung. Skyworth faces a structural disadvantage in Western markets despite manufacturing capability comparable to or superior to Samsung's.

The Panasonic partnership solves this problem. Skyworth manufactures televisions bearing the Panasonic nameplate—a brand that still resonates with Western consumers who remember Panasonic's quality during the plasma era. Skyworth gets to piggyback on Panasonic's brand equity while providing the manufacturing and volume that Panasonic needs.

For Skyworth, this arrangement potentially opens the US and European markets in a way that selling under the Skyworth nameplate never could. The company can build volume, establish distribution networks, and eventually translate that presence into Skyworth-branded sales down the road. It's a strategic foothold in premium markets Skyworth has historically had difficulty penetrating.

Skyworth's Competitive Position

While Skyworth operates at significant scale globally, the company faces limitations in Western markets that this partnership addresses:

Market Share: Skyworth captures roughly 5-8% of global TV market share by volume, placing it outside the top five globally. This is respectable scale but far below Samsung (20%+) or TCL (12%). In Western markets, Skyworth's share is even smaller—perhaps 2-3% if that.

Brand Awareness: Outside Asia, few consumers know Skyworth. The company invests in brand building but struggles against established competitors with historical presence.

Premium Segment Access: Skyworth's strength lies in budget and mid-range products. Premium OLED segments are dominated by Samsung, LG, and Sony. The Panasonic partnership, with joint development on premium OLED models, gives Skyworth access to the premium segment it otherwise couldn't penetrate.

Technology Access: Through the partnership, Skyworth gains exposure to Panasonic's design processes and can benefit from Panasonic's historical expertise in display technology—knowledge that translates into better product design and engineering.

This chart compares key specifications across Budget, Mid-Range, and Premium TVs. Premium TVs generally offer superior refresh rates, brightness, and color gamut, enhancing viewing experience. (Estimated data)

Part 12: Real-World Implications and What Consumers Should Know

Should You Buy a Panasonic TV Going Forward?

For consumers considering Panasonic televisions after the Skyworth partnership takes effect, several practical questions arise.

Arguments For Panasonic TVs:

- Skyworth is a capable manufacturer: The company produces quality products at scale and has the resources to support products globally.

- Panasonic maintains design input: The partnership includes Panasonic expertise and quality assurance, so products should maintain reasonable quality standards.

- Competitive pricing: Skyworth's manufacturing costs enable competitive pricing without sacrificing reasonable quality.

- OLED quality: For premium OLED models with joint development, you're getting products designed by Panasonic engineers using cutting-edge panels.

Arguments Against Panasonic TVs:

- Support uncertainty: Warranty service transitions from Panasonic to Skyworth, introducing uncertainty about service quality and duration.

- Brand assurance fading: You're no longer purchasing a product with Panasonic's full reputation behind it—you're purchasing a Skyworth product with a Panasonic brand license.

- Cheaper alternatives available: You could purchase a TCL or Hisense TV for similar or lower prices from manufacturers with established Western presence.

- Quality assurance fade risk: If Skyworth decides supporting Panasonic TVs is unprofitable, the company could exit the market quickly, stranding consumers without service options.

The Practical Recommendation: If you have affinity for the Panasonic brand based on historical experience, Skyworth-manufactured Panasonic TVs are likely acceptable for budget and mid-range purposes, recognizing they're essentially Skyworth products with Panasonic branding. For premium OLED models, the joint development arrangement means you're potentially getting a better product than you'd get from pure Skyworth. However, don't pay a significant premium for the Panasonic nameplate—you're not getting the support infrastructure that historical Panasonic brand equity implied.

Budget Allocation Recommendations

For Budget TVs ($200-400): Brand matters minimally. Buy the TCL, Hisense, Skyworth, or Panasonic with the best features at the lowest price. All will provide acceptable performance. Service is unlikely to matter because these TVs are typically replaced rather than repaired.

For Mid-Range TVs ($400-800): Consider brand familiarity and local service availability. Panasonic makes sense if you have positive prior experience and local service is available. Otherwise, TCL or Hisense offer similar value. Don't overpay for brand.

For Premium TVs ($800+): Invest in established premium brands (Samsung, LG, or Sony for OLED) rather than Panasonic-branded sets. These brands can better sustain premium positioning through technology differentiation and established service networks. Panasonic-branded premium TVs might offer good value, but you're taking on execution risk with a partnership-manufactured product.

Part 13: Broader Economic and Competitive Implications

What This Means for Japan's Economy

The exodus of Japanese electronics manufacturers from televisions has broader implications for Japan's economy and global competitiveness.

Loss of Manufacturing Capacity: Each exiting manufacturer represents factories closed, workers laid off, and manufacturing expertise relocated. Japan's share of global consumer electronics manufacturing has declined by roughly 70% over the past 20 years.

Technology Leadership Transition: Japan's identity as a global technology leader is increasingly difficult to sustain when consumer electronics manufacturing—historically a foundation of that leadership—has moved to other countries.

Labor and Wage Implications: Television manufacturing was historically high-wage, stable employment in Japan. Manufacturing relocation means these workers transition to lower-wage service sector jobs or struggle to find employment.

Supply Chain Dependency: Japan has become dependent on imports for many consumer electronics, creating trade deficits and reducing economic resilience.

Niche Positioning: Japanese companies increasingly occupy premium niches (luxury goods, professional equipment) rather than mass-market segments. This is economically viable but represents a smaller addressable market.

These dynamics have contributed to Japan's economic challenges over the past two decades—the "lost decades" where growth stagnated and aging demographics compounded economic problems.

Competitive Lessons for Other Industries

The television industry provides case studies relevant to other industries facing similar pressures.

When Cost Competition Becomes Commoditization: Once a technology becomes mature and available from multiple suppliers, cost becomes the primary competitive variable. Companies with high cost structures cannot compete unless they fundamentally restructure. Panasonic learned this lesson late.

The Importance of Ecosystem Control: Chinese manufacturers benefit from ecosystem advantages (proximity to panel suppliers, component makers, logistics infrastructure) that competitors outside the ecosystem struggle to overcome. Building ecosystem leadership is more important than individual company innovation.

Scale Advantages in Manufacturing: Modern manufacturing economics heavily favor scale. A manufacturer producing 50 million units annually can achieve cost structures that a manufacturer producing 5 million units simply cannot match. This creates natural industry consolidation.

Brand Value Erosion Under Commoditization: In commoditized markets, brand premium erodes because consumers understand that functional differences are minimal. Panasonic's brand couldn't sustain its premium when TCL offered equivalent functionality at much lower prices.

Part 14: Technical Specifications and Product Comparisons

Key Specifications for Modern TVs

When evaluating television purchases, understanding key specifications helps ensure informed decisions.

Resolution: Modern TVs are primarily 4K (3840 × 2160 pixels), with 8K available at premium price points but with minimal content. 4K represents the practical standard.

Refresh Rate: Typically 60 Hz standard, with 120 Hz available on higher-end models. 120 Hz matters for gaming and sports viewing but less critical for general content.

Brightness (nits): Measured in peak brightness. Budget TVs: 300-400 nits. Mid-range: 500-800 nits. Premium OLED: 1000+ nits. Higher brightness is better for well-lit rooms.

Contrast Ratio: The ratio between brightest whites and darkest blacks. OLED TVs have infinite contrast (blacks are truly black when the pixel is off). LED-backlit LCDs have finite contrast ratios, typically 5,000:1 or higher for decent quality.

Color Gamut: The range of colors a TV can display. Standard is DCI-P3 color space. Wider gamut = more accurate colors. Premium TVs approach 90-95% DCI-P3. Budget TVs might achieve 85% or less.

Response Time: How quickly pixels change from one color to another, measured in milliseconds. Matters primarily for gaming. OLED TVs have <1ms response time. LED TVs typically 4-8ms. Insufficient for most viewers to notice.

Viewing Angles: Measured in degrees. OLED TVs have superior viewing angles (178 degrees) compared to LED-backlit LCDs (typically 170 degrees). Practical difference is minimal for typical viewing scenarios.

Smart TV Operating System: Increasingly important as TVs become internet-connected. Android TV (Google), web OS (LG), Tizen (Samsung), and others. Features and app availability vary.

Comparison Framework

When comparing TVs, evaluate across these dimensions:

| Factor | Budget TVs | Mid-Range | Premium |

|---|---|---|---|

| Price Range | $200-400 | $400-800 | $800-3000+ |

| Panel Type | LED-backlit LCD | LED or Mini LED | OLED |

| Peak Brightness | 300-400 nits | 500-800 nits | 1000-2000 nits |

| Contrast Ratio | 5000:1-8000:1 | 8000:1-15000:1 | Infinite (OLED) |

| Color Accuracy | 85-90% DCI-P3 | 90-95% DCI-P3 | 95%+ DCI-P3 |

| Design Quality | Plastic, basic bezels | Metal frame, better aesthetics | Premium materials, refined design |

| Smart Features | Android TV basic | Full-featured Android TV | Premium smart platform |

| Audio Quality | Basic stereo | Improved stereo/2.1 | Premium surround (some models) |

| Warranty | 1 year typical | 2 years typical | 3-5 years premium |

| Longevity | 4-6 years average | 6-8 years average | 8-10+ years potential |

Japanese TV manufacturers' market share plummeted from 55% in the 1980s to 0% by 2025, highlighting a rapid decline in global influence. Estimated data.

Part 15: Future Outlook and Predictions

What's Next for Panasonic and Television Manufacturing

Looking forward, several developments seem likely based on current trends.

Panasonic's TV Business Will Stabilize but Shrink: The Skyworth arrangement removes the immediate existential threat to Panasonic's TV business. The company will generate some revenue and maintain brand presence. However, without aggressive investment in design and innovation, Panasonic's share will likely decline. Panasonic becomes a mid-tier TV brand globally—present but not dominant.

Skyworth Will Invest in Panasonic Brand Development: The company has incentive to build the Panasonic brand in Western markets, as market share growth directly increases Skyworth's revenue. Expect improved service networks, expanded product lines, and marketing investments.

OLED Will Remain the Differentiation Point: Panasonic-Skyworth will likely focus joint development efforts on OLED models, where differentiation and margin are viable. Budget and mid-range LCD models will become increasingly commoditized and undifferentiated.

Manufacturing Consolidation Will Continue: Expect additional mergers among Chinese and South Korean TV manufacturers. Skyworth might acquire other brands or be acquired itself. The ultimate endgame is likely a smaller number of global manufacturers supplying most of the world's TVs.

Premium Brands Will License More Aggressively: Following Panasonic and Sony's leads, expect additional Japanese and European brands to outsource manufacturing entirely, competing purely through design and branding.

The Broader Consumer Electronics Landscape

The television industry is merely one example of a broader trend reshaping consumer electronics:

Manufacturing Moving to Asia: Whether TVs, laptops, smartphones, or appliances, manufacturing increasingly concentrates in China and Southeast Asia where costs are lowest and ecosystems are most developed.

Japanese Brands Retaining Premium Niches: Japanese companies increasingly retreat to premium segments (luxury goods, professional equipment, specialized applications) where design and brand value sustain profitability.

Chinese Brands Rising Globally: Chinese manufacturers, having built massive scale and efficient cost structures, are aggressively pursuing market share in Western markets. TCL, Hisense, and others are household names now globally.

South Korean Brands Sustaining Leadership: Samsung and LG maintain technology advantages (particularly in displays) that allow them to command premium positioning despite lower cost Asian competitors.

Part 16: Investment and Business Model Implications

Strategic Lessons from the Television Industry Shift

The television industry transition provides valuable lessons for investors, business leaders, and economists.

Vertical Integration vs. Asset-Light Models: Panasonic's integrated manufacturing model provided quality control and margins during growth phases but became a liability during commoditization. Asset-light models (design + outsourced manufacturing) are increasingly superior in mature markets. However, asset-light models sacrifice control and long-term strategic flexibility.

The Danger of Late Transitions: Panasonic didn't transition to outsourced manufacturing until 2021, after the market had already shifted toward Chinese manufacturers. Earlier transitions might have preserved greater market share. Late strategic transitions often fail because competitors have already established dominance.

Geography Matters More Than You Think: Skyworth's location in Shenzhen, proximate to panel suppliers, component makers, and logistics hubs, provides structural advantages that engineering excellence alone cannot overcome. Geography and ecosystem effects are underestimated in business strategy.

Technology Leadership Requires Scale: Innovating faster than competitors requires resources that only come from substantial revenue/profitability. As Panasonic's TV business declined, innovation became impossible—the declining business couldn't fund the innovation needed to reverse decline.

Brand Licenses Provide Optionality: The Panasonic-Skyworth arrangement allows Panasonic to maintain a TV presence without capital investment. While brand equity decays over time, brand licensing provides a lower-risk middle path between full exit and full commitment.

Part 17: Consumer Choice and Decision Framework

Evaluating Television Options in 2025

Given the Panasonic-Skyworth development and broader industry trends, here's a framework for evaluating television purchases:

Step 1: Determine Your Budget

- Budget tier: $200-400

- Mid-range: $400-800

- Premium: $800+

Step 2: Assess Your Viewing Conditions

- Well-lit room? Prioritize brightness. OLED less ideal for bright environments.

- Dark room for movies/gaming? OLED superior for contrast and color.

- Typical broadcast TV/streaming? Any modern TV is acceptable.

Step 3: Evaluate Technology Preferences

- Budget: LED-backlit LCD is standard. Accept commodity quality.

- Mid-range: Consider Mini LED or entry OLED if budget allows. Meaningful quality improvement.

- Premium: Invest in high-end OLED from established brands (Samsung, LG, Sony).

Step 4: Consider Brand and Support

- For budget/mid-range: Brand is less critical. Verify local service availability.

- For premium: Prioritize brands with established service networks (Samsung, LG, Sony) over new entrants (Panasonic-Skyworth).

Step 5: Evaluate Long-Term Value

- Are you keeping the TV 3-5 years? Budget/mid-range TVs are fine.

- Are you keeping 7-10 years? Invest in premium quality from established brands. Service and parts availability matter more.

Step 6: Make Your Decision

- Budget tier: Buy the TCL/Hisense/Panasonic with best features at lowest price

- Mid-range: Balance brand familiarity, features, and price. Samsung, LG, or Panasonic reasonable choices.

- Premium: Invest in Samsung OLED, LG OLED, or Sony OLED from established premium manufacturers.

Part 18: Conclusion and Key Takeaways

Panasonic's announcement that it will no longer manufacture its own televisions marks the culmination of trends that have been unfolding for over a decade. The Japanese electronics giant, once revered as the "plasma king" and a global leader in television innovation, has concluded that independent TV manufacturing is no longer economically viable.

The partnership with Skyworth represents a pragmatic solution to an intractable problem: Panasonic could not compete on cost with Chinese manufacturers while maintaining its quality standards and profitability requirements. By outsourcing manufacturing to Skyworth, Panasonic exits the capital-intensive manufacturing business while maintaining a revenue stream through brand licensing and joint development on premium products.

For consumers, this development carries implications both positive and negative. On the positive side, Skyworth is a capable manufacturer with modern facilities and expertise in Android TV platforms. Panasonic-branded TVs should maintain acceptable quality standards. On the negative side, the Panasonic brand no longer carries the direct quality assurance it once did—consumers are purchasing Skyworth products with Panasonic branding, not Panasonic-engineered products.

The broader significance of this announcement is the final eclipse of Japanese consumer electronics manufacturing. Virtually no major consumer electronics are manufactured in Japan anymore. Those that bear Japanese brand names are increasingly manufactured by Chinese or South Korean companies. This represents a dramatic reversal from the 1980s when Japan dominated consumer electronics globally.

This shift reflects fundamental economic forces: labor cost advantages, supply chain geography, ecosystem effects, and manufacturing scale advantages concentrated in Asia (particularly China). These forces cannot be overcome through superior engineering or brand reputation alone. The television industry demonstrates this reality with particular clarity.

For investors and business leaders, the lesson is clear: In commodity hardware markets, cost structure and manufacturing scale dominate. Companies without these advantages cannot sustain competitive positions indefinitely, regardless of brand equity or historical innovation. Panasonic learned this lesson late, but it learned it thoroughly.

For consumers shopping for televisions, the practical lesson is equally important: Brand names provide diminishing assurance in a world of outsourced manufacturing. A Panasonic TV is a Skyworth TV. A Sony TV is increasingly a TCL TV. The brand name indicates design and software features more than it indicates manufacturing quality or service support.

Going forward, the television market will likely continue consolidating. Chinese manufacturers will capture increasing share through cost advantages and scale. South Korean manufacturers (Samsung, LG) will maintain leadership through technology advantages (particularly OLED display manufacturing). Japanese brands will occupy premium niches with outsourced manufacturing. This structure is likely to stabilize around 2030, with roughly three Chinese manufacturers, two South Korean manufacturers, and several licensed Japanese/European brands controlling 70-80% of global TV market share.

The Panasonic-Skyworth partnership is a milestone in this inevitable restructuring. It's the moment when a former global leader formally acknowledged that its manufacturing heyday is over. The company now focuses on design, branding, and quality assurance—critical functions, but fundamentally different from the manufacturing excellence that once defined Panasonic.

For those who remember Panasonic as "the plasma king," the news carries a note of nostalgia. The era of Japanese TV dominance is definitively closed. The future belongs to manufacturers with cost advantages, scale, and geographic proximity to supply chains. Panasonic's partnership with Skyworth is simply accepting this reality.

FAQ

What does it mean that Panasonic will no longer make its own TVs?

Panasonic has partnered with Skyworth, a Chinese manufacturer, to handle all TV manufacturing, sales, and logistics. Instead of producing TVs in its own factories, Panasonic now focuses on design, quality assurance, and branding. This means Panasonic-branded TVs will be manufactured by Skyworth but designed to Panasonic specifications, with Panasonic maintaining quality control oversight, particularly for premium OLED models.

Who is Skyworth and why did Panasonic choose this partner?

Skyworth Digital Holdings is a major Chinese television manufacturer headquartered in Shenzhen, ranking in the top five global TV brands by sales volume. Panasonic chose Skyworth for its manufacturing expertise, cost efficiency, and distribution capabilities in Western markets. Skyworth benefits from access to the Panasonic brand name in markets where Skyworth has minimal recognition, while Panasonic gains manufacturing capability without capital investment.

When will this partnership take effect and what happens to existing Panasonic TV owners?

The transition takes effect in April 2026. Panasonic will support all TVs sold before March 2026 under existing warranty terms. For TVs purchased from April 2026 onward, Skyworth assumes responsibility for warranty and customer service. Existing Panasonic TV owners should expect warranty coverage to continue through the remaining warranty period, after which support may transition to Skyworth service channels.

Will Skyworth-manufactured Panasonic TVs be the same quality as previous Panasonic TVs?

Quality should be comparable or potentially improved for budget and mid-range models, as Skyworth is a capable manufacturer with modern facilities. However, the quality assurance framework is different—you're no longer relying on Panasonic's direct manufacturing oversight but rather on Panasonic's quality review of Skyworth products. For premium OLED models, joint development arrangements should ensure quality consistency with previous Panasonic standards.

Why did Panasonic decide to stop manufacturing TVs?

Television manufacturing has become a low-margin, commodity business where cost structure and manufacturing scale determine profitability. Panasonic could not compete economically with Chinese manufacturers operating at massive scale with lower labor costs. The company maintained losses despite market dominance in plasma TVs because production costs exceeded profit margins. Outsourcing manufacturing to a low-cost producer allows Panasonic to maintain a TV business without bearing manufacturing costs.

What does this mean for other Japanese TV manufacturers?

Panasonic's partnership follows Sony's announcement of selling 51% of its TV business to TCL and reflects a broader trend of Japanese manufacturers exiting TV production. Sharp, Toshiba, Hitachi, and Pioneer have already exited TV manufacturing. This consolidation reflects the fundamental economics of the television industry—Japanese labor costs and manufacturing approaches cannot compete with Chinese manufacturers operating at higher volume and lower cost.

Should I buy a Panasonic TV after April 2026?

For budget and mid-range TVs, Panasonic represents a reasonable option if you have affinity for the brand and local service is available. However, don't pay a significant premium for the Panasonic nameplate—you're purchasing a Skyworth product with Panasonic branding. For premium OLED models, Panasonic may offer competitive value due to joint development arrangements. For the longest-term value and reliable service support, established premium brands like Samsung, LG, or Sony OLED models may be safer choices.

What is OLED and why does Panasonic emphasize this technology?

OLED (Organic Light Emitting Diode) technology creates pixels that generate their own light, enabling perfect blacks, superior contrast ratios, and wider viewing angles compared to LED-backlit LCD TVs. OLED represents the premium segment where technology differentiation and brand value sustain higher margins. The partnership includes joint development on OLED models, allowing Panasonic to compete in the premium segment where manufacturing cost advantages matter less and design/technology matter more.

How will warranty and customer support work for future Panasonic TVs?

Starting April 2026, Skyworth assumes responsibility for warranty claims and customer service for new Panasonic TV purchases. This means you'll likely contact Skyworth-authorized service centers rather than Panasonic directly. Support quality and availability will depend on Skyworth's service infrastructure in your region. Existing Panasonic TV owners retain Panasonic support until their warranty expires, after which they may transition to Skyworth service channels.

Does this affect the television market for consumers?

This development reflects broader consolidation of television manufacturing under Chinese and South Korean manufacturers. For consumers, it means traditional brand names (Panasonic, Sony, etc.) provide less direct assurance of manufacturing quality. It also suggests ongoing industry consolidation—expect fewer independent TV manufacturers and more outsourced manufacturing arrangements. For consumers, this creates opportunities to purchase quality TVs at competitive prices but requires more careful evaluation of actual manufacturing and support capabilities rather than relying on brand reputation.

Additional Resources and Industry Context

Key Market Trends

Market Consolidation: The global TV market has consolidated dramatically. In 2010, the top five manufacturers controlled roughly 60% of market share. In 2025, the top five control approximately 75%, with Chinese and South Korean manufacturers comprising 65% of the total.

Price Deflation: TV prices have declined roughly 60-70% over the past 15 years (adjusted for quality/size improvements). This reflects commoditization and