![Rad Power Bikes Bankruptcy: $13.2M Acquisition Explained [2025]](https://tryrunable.com/blog/rad-power-bikes-bankruptcy-13-2m-acquisition-explained-2025/image-1-1769458060893.png)

Rad Power Bikes Bankruptcy: How a $1.65 Billion E-Bike Company Collapsed [2025]

It's hard to believe. Less than four years ago, Rad Power Bikes was valued at

Then reality hit hard.

In late January 2025, Rad Power Bikes agreed to sell its assets to Life Electric Vehicle Holdings for

This wasn't sudden. Rad Power's decline unfolded over 18 months of visible struggles: multiple rounds of layoffs, CEO changes, battery fire investigations by the Consumer Product Safety Commission, and dwindling sales momentum. But the bankruptcy auction and subsequent acquisition by a relatively unknown Florida-based company raises critical questions about the entire e-bike market, venture capital's role in inflating valuations, and whether the pandemic-fueled boom was built on unsustainable foundations.

The story of Rad Power Bikes is the story of modern venture capital excess meeting harsh market realities. It's a cautionary tale about growth-at-any-cost culture, mismanaged supply chains, quality control lapses, and the difficulty of sustaining hardware companies in competitive markets. But it's also a window into the broader e-bike industry, where several major players have faced similar troubles.

This article breaks down what happened, why it happened, and what it means for the e-bike industry and startups that raised billions on promises that never materialized.

TL; DR

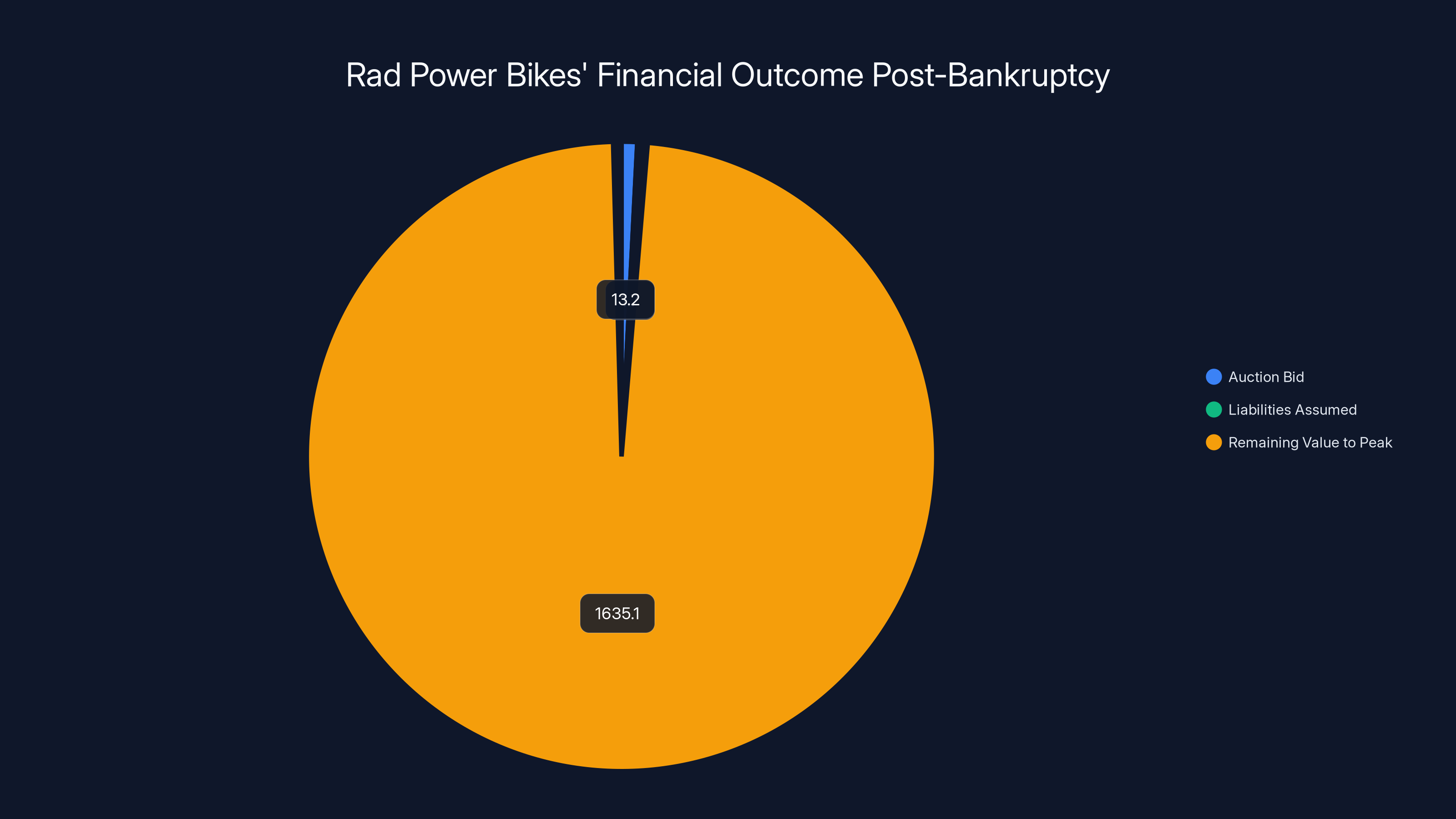

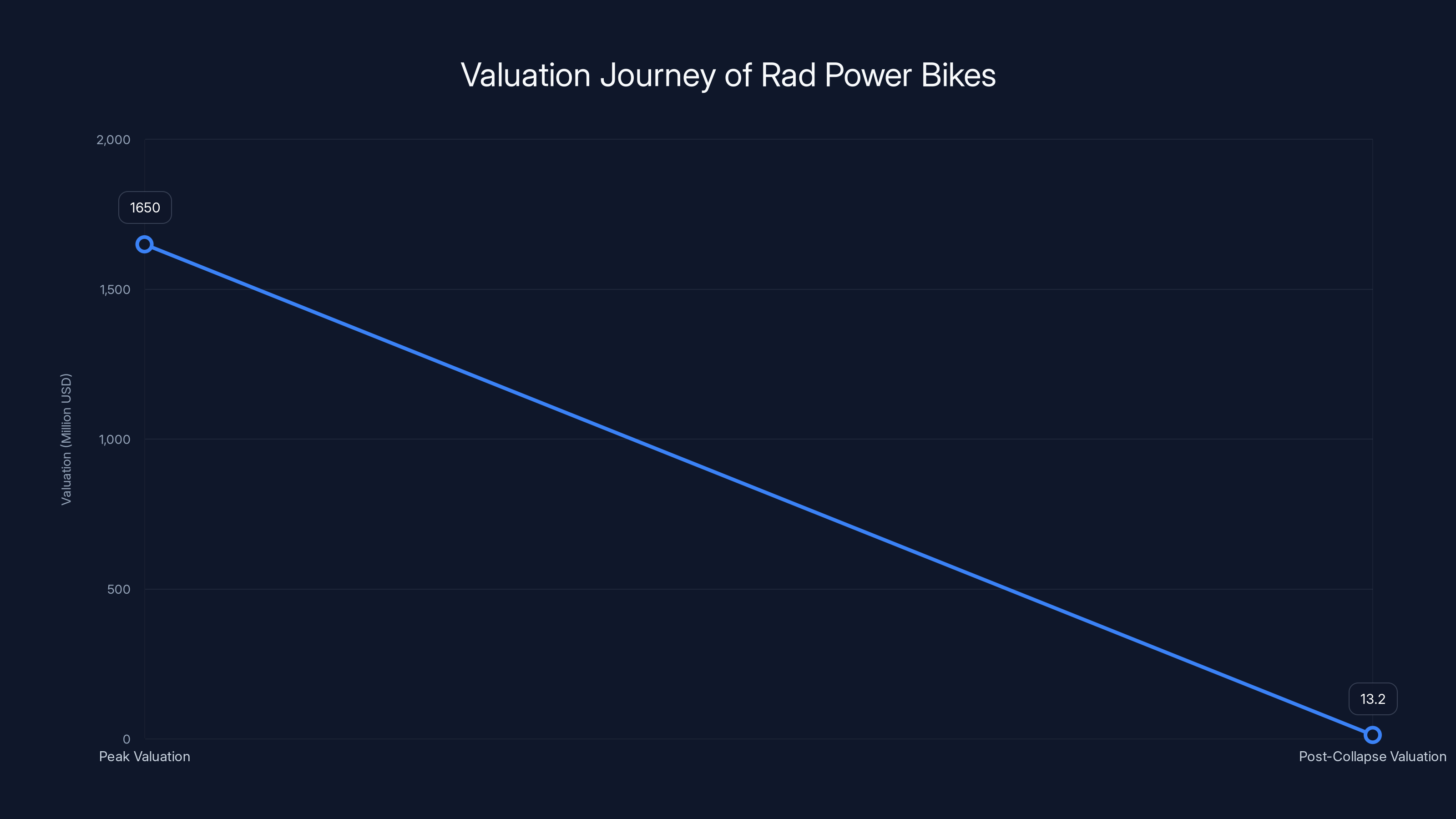

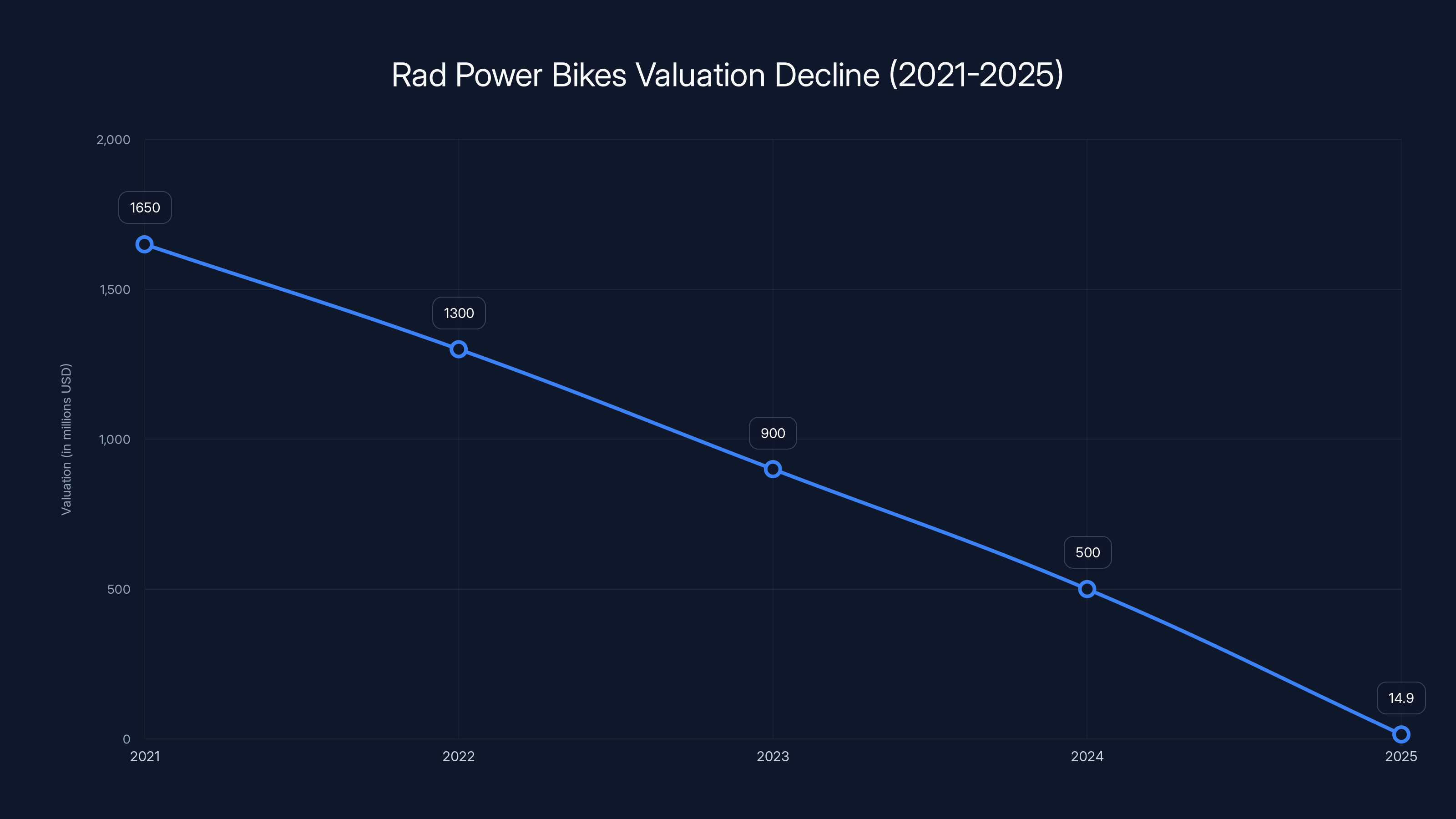

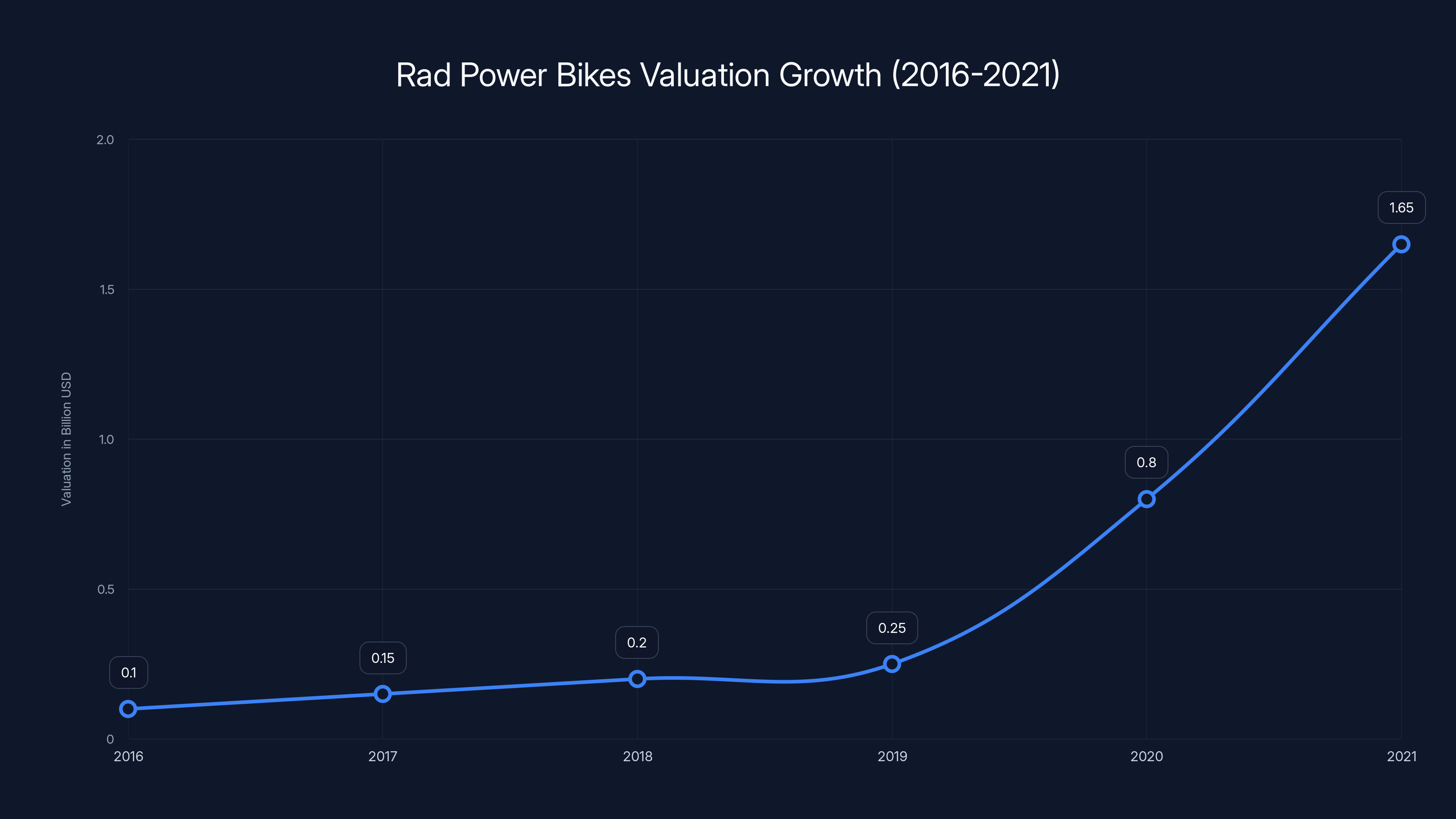

- Valuation Collapse: Rad Power Bikes sold for 1.65 billion peak valuation in October 2021—a 99% decline in value

- Pandemic Boom, Then Bust: Massive sales growth during COVID-19 lockdowns masked underlying operational and product quality issues

- Safety Issues: Battery fire investigations by the CPSC and product recalls damaged brand trust and consumer confidence

- Competitive Pressure: Oversaturation in the e-bike market and more established competitors eroded margins and market share

- Takeaway: The e-bike industry boom was driven by speculation and pandemic-era spending, not sustainable demand fundamentals

The total deal value of

The Rise: How Rad Power Became a Unicorn (2016-2021)

Rad Power Bikes wasn't always a failure story. It started as a genuine success.

Founded in 2007 by Mike Radenbaugh and Ty Collins, the company began as a maker of electric bikes focused on practical transportation rather than luxury recreation. In the early days, they sold directly to consumers through their website, avoiding the traditional bicycle retailer model that had long margins and slow inventory turns.

For over a decade, the company grew steadily but without fanfare. Most people had never heard of Rad Power Bikes. They were profitable, lean, and focused on the actual product.

Then the pandemic changed everything. In 2020 and 2021, as lockdowns kept people indoors and concerned about public transportation, demand for e-bikes exploded. Suddenly, riding outside became a viable recreation and transportation option. Supply chains couldn't keep up. Prices climbed. And companies that made e-bikes printed money.

Rad Power Bikes capitalized on this moment perfectly. They had brand recognition in online communities, a proven product, direct-to-consumer distribution channels, and access to capital at historically low interest rates. Between 2020 and 2021, the company raised multiple funding rounds at skyrocketing valuations.

By October 2021, Rad Power Bikes had raised

The company had also expanded far beyond its origins. They offered a wider range of e-bikes, entered new product categories, and accelerated marketing spend dramatically. They hired aggressively. Mike Radenbaugh, the co-founder, stepped back from the CEO role to let professional managers take the wheel.

Everything looked bullish. Everything felt inevitable.

But here's the thing about pandemic booms: they're temporary by definition.

The Momentum Reversal: When Growth Stalled (2022-2023)

By early 2022, it was clear that the pandemic e-bike boom had peaked. People returned to offices. Public transportation resumed. The novelty and necessity that drove pandemic-era purchases faded.

Demand collapsed. Not gradually—sharply.

Companies that had built operations to sustain pandemic-level volume suddenly found themselves with massive inventory, bloated cost structures, and significantly lower orders. The math became brutal fast: if you hired staff for 200,000 units per year but you're selling 100,000 units per year, your per-unit costs climb, your margins compress, and your path to profitability disappears.

Rad Power Bikes faced this directly. In late 2022, the company announced its first major layoffs, cutting roughly 10 percent of its workforce. Management blamed "global supply chain disruptions and uncertain market conditions." That was corporate language for "we overhired for demand that evaporated."

But the inventory problem persisted. E-bikes are physical products. They take up warehouse space. They depreciate in value if you're forced to discount them to clear stock. Retailers and direct-to-consumer companies holding too much inventory face terrible choices: hold the line on price and watch products sit, or discount aggressively and destroy margins.

Rad Power chose some of both, and neither worked well.

Their sales declined noticeably through 2023. The company was still operating, still selling bikes, still viable—but the growth narrative had completely inverted. Investors who bought at the $1.65 billion valuation saw that investment become worth significantly less, and the path back to growth looked distant.

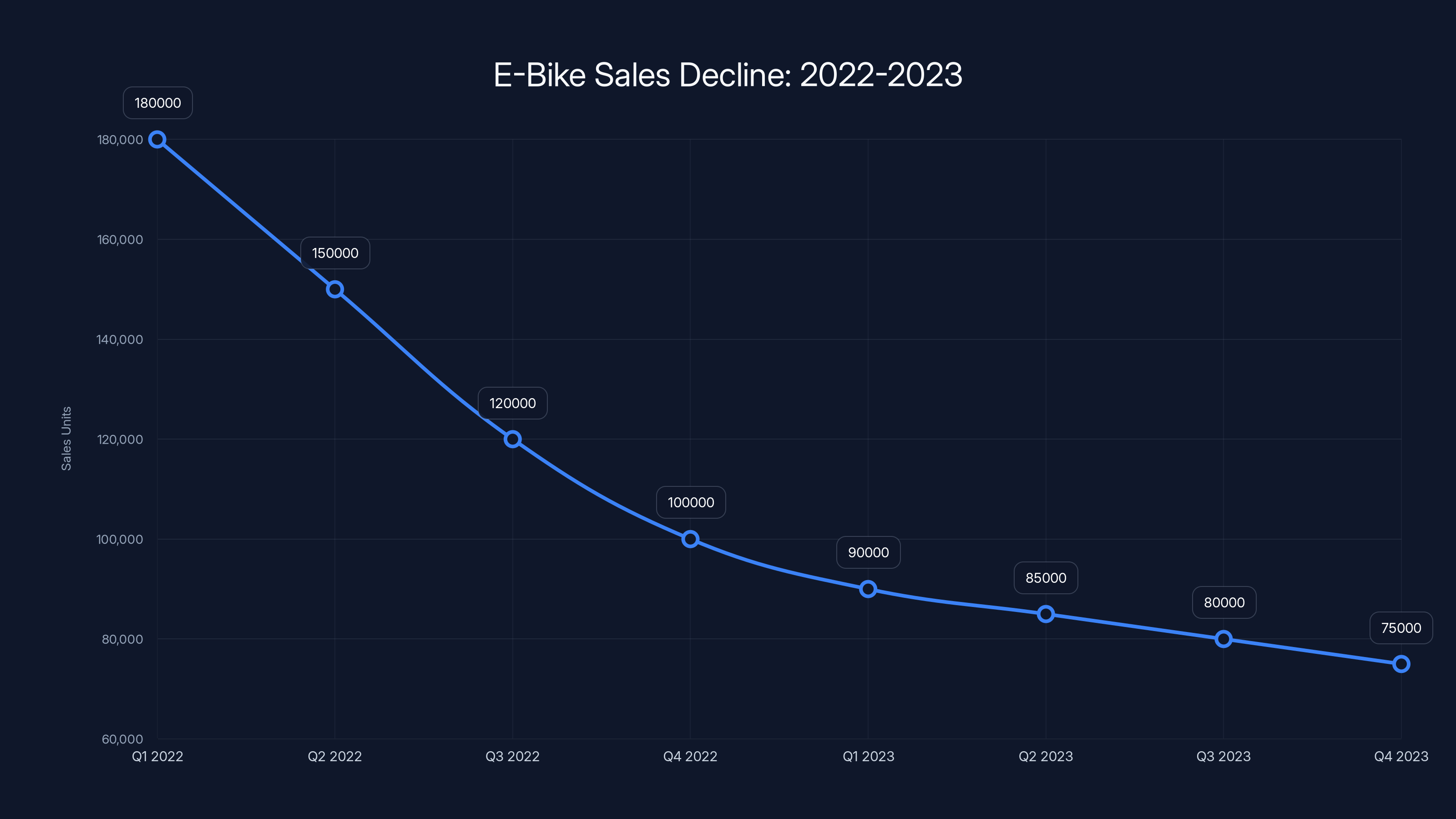

Estimated data shows a sharp decline in e-bike sales for Rad Power Bikes from 2022 to 2023, reflecting the post-pandemic market adjustment.

Product Quality Issues: Battery Fires and Brand Erosion

While demand challenges mounted, Rad Power Bikes faced a crisis that no amount of marketing or discounting could solve: product safety issues.

Starting in late 2023, reports emerged of Rad Power e-bikes catching fire. The fires appeared to be connected to the lithium-ion battery systems used in their bikes. These weren't isolated incidents—reports accumulated. By the time the Consumer Product Safety Commission investigated, they had documented 31 reported fires linked to Rad Power batteries.

The CPSC issued a statement characterizing certain Rad batteries as presenting a "hazard." The specific language suggested the batteries were defective or unsafe under normal use conditions.

For a hardware company, this is a catastrophic event. Brand trust, once eroded by safety concerns, is extraordinarily difficult to rebuild. A customer who experiences a product fire doesn't just stop buying—they tell everyone they know. They post on social media. They warn friends. They return the product and demand refunds.

Rad Power's response didn't help. The company issued a statement saying it "firmly stands behind our batteries and our reputation as leaders in the e-bike industry, and strongly disagrees with the CPSC's characterization." This response was dismissive of customer safety concerns. It read like the company was more concerned with defending its reputation than addressing the underlying issue.

What compounded the problem: Rad Power had been dealing with earlier battery issues in previous generations of products. This wasn't a new problem. It suggested systematic quality control failures across multiple product lines and multiple years.

For customers who'd already bought the bike, paid good money, and now worried about their home catching fire if they charged their bike overnight, Rad Power's defensive stance felt insulting.

The Competitive Landscape Shifts: New Players, Price Pressure

Even before battery fires and demand collapse, Rad Power Bikes faced intensifying competition.

The pandemic e-bike boom attracted massive capital and new entrants. Amazon began selling e-bikes directly. Giant and Trek, the legacy bicycle manufacturers with decades of distribution and brand strength, entered the e-bike market with superior supply chains and retail relationships. Specialized, Cannondale, and other established brands did the same.

These weren't scrappy startups. They had existing customer relationships, established retail networks, brand heritage, and capital. When they decided e-bikes were a priority, they could move faster and cheaper than Rad Power in many ways.

Then there were new entrants specifically focused on e-bikes. Companies like Retrospec, Juiced Bikes, and others raised capital and scaled aggressively. The market that Rad Power had largely to itself (or shared only with a few competitors) became crowded.

Crowded markets mean price pressure. If you're Rad Power and you're holding inventory while demand drops and new competitors are undercutting your prices, your margins evaporate quickly. You can't just sit on inventory hoping demand recovers—carrying costs force you to move product, even at lower margins.

Furthermore, the direct-to-consumer distribution model that had been Rad Power's advantage in 2015-2020 became less defensible. As e-bikes became mainstream, consumers wanted to see them in person, test them, and buy from trusted retailers. This required building retail relationships—the exact thing Rad Power had avoided for years.

They tried to adapt, but adaptation requires capital and organizational agility. By 2023, they were fighting a two-front war: defending their direct-to-consumer advantage while building retail presence they didn't have.

CEO Turnover and Organizational Chaos

A telling sign of trouble at any startup is executive instability.

In 2022 and 2023, Rad Power Bikes went through multiple CEO changes. The company replaced its CEO and struggled to find stability in leadership. This typically indicates either a failure by the board to properly assess the market situation, or a failure by new leadership to execute against those assessments—or both.

When a company is growing rapidly and confidently, CEO transitions are planned and measured. When a company is struggling and burning through capital, CEO transitions often signal panic and miscalculation.

Multiple CEO changes mean multiple strategic shifts, unclear direction, and organizational confusion. Employees don't know who to report to or what the actual priorities are. Customers see inconsistent messaging. Partners feel uncertain about the company's direction.

By the time a company has cycled through two or three CEOs in two years, the organization is effectively broken from a trust and execution standpoint.

Rad Power experienced exactly this. The management carousel sent clear signals to employees, customers, and investors alike: nobody really knows how to fix this company.

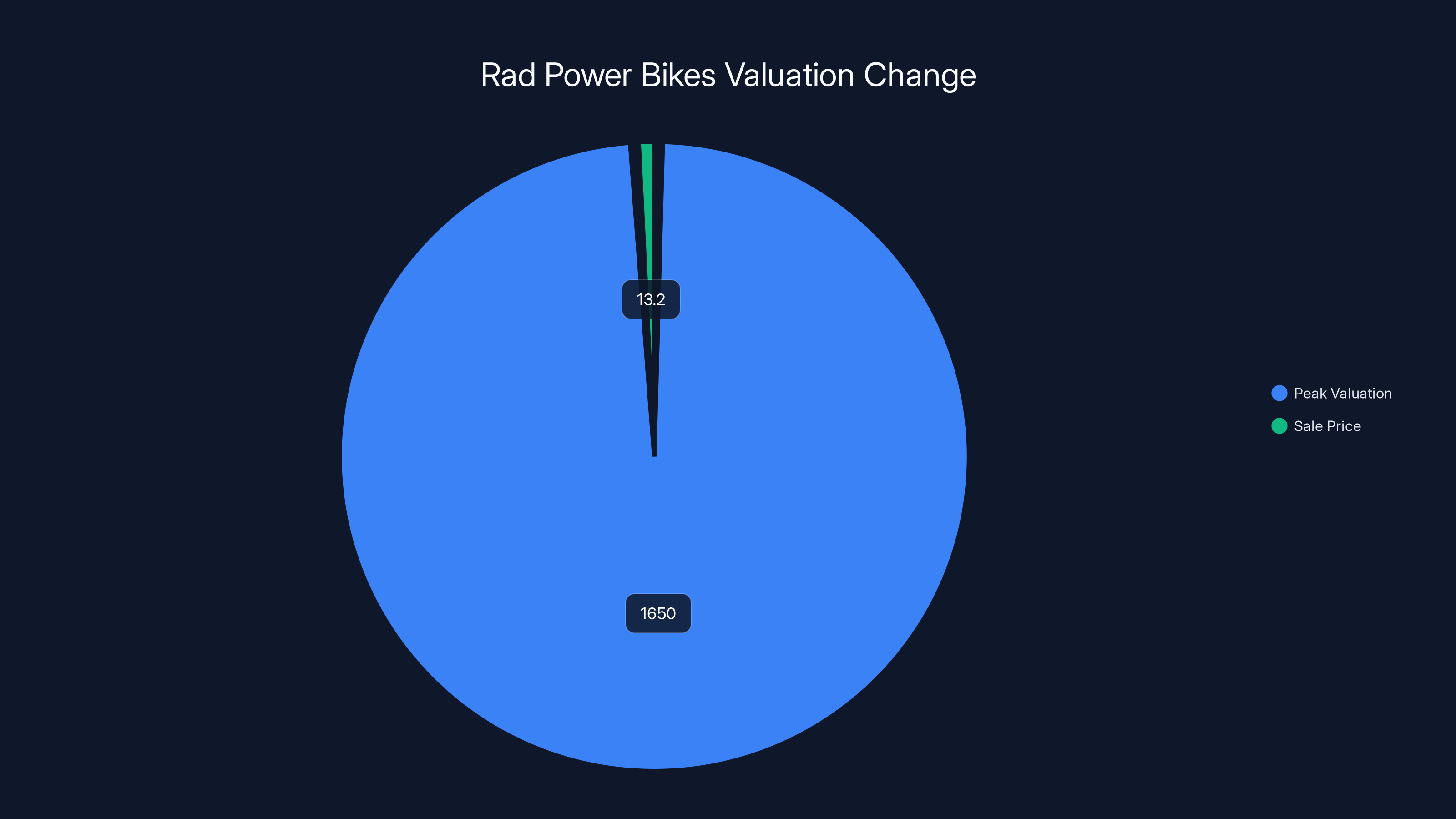

Rad Power Bikes experienced a dramatic 99% decline in valuation from its peak of

Supply Chain Mismanagement: Inventory That Wouldn't Move

Hardware companies live or die by supply chain management. Get it right, and you can scale smoothly. Get it wrong, and you accumulate inventory that destroys your balance sheet.

Rad Power Bikes made classic supply chain mistakes. During the pandemic boom, when demand was skyrocketing and capital was cheap, the company over-ordered components and built too much inventory. This is an understandable mistake—you don't want to miss sales due to stockouts—but it's still a mistake when the market is about to collapse.

When demand fell in 2022, Rad Power was left holding massive quantities of components, finished bikes, and batteries. These assets were supposed to generate revenue. Instead, they sat in warehouses, depreciating in value and consuming cash through storage and handling costs.

The company faced an ugly choice: sit on inventory hoping demand recovered, or discount aggressively to free up cash and warehouse space. Either choice was painful. The second choice—aggressive discounting—signals to the market that the company is desperate. It also trains customers to wait for sales rather than buying at full price.

Furthermore, e-bikes have a limited shelf life. Technology improves. New models launch. A 2021 model gathering dust in a warehouse in 2023 is competing against newer, fresher 2023 models from competitors. You can't sell 2021 inventory at 2023 prices.

Rad Power's supply chain problems weren't just operational—they were financial. Companies with poor inventory discipline burn through cash rapidly, and cash is survival for struggling startups.

The Bankruptcy Filing: When Options Run Out

By late 2024, Rad Power Bikes had exhausted most options.

The company had cut costs through layoffs. It had discounted inventory. It had cycled through CEOs. It had apologized for (or defensively justified) battery issues. But none of it stemmed the underlying problem: demand had evaporated, the company was burning cash, and the path to profitability was no longer visible.

Sometime in late 2024, Rad Power's board and management made the decision to file for bankruptcy protection. Bankruptcy isn't a failure to file—it's a legal tool that gives companies breathing room to reorganize, negotiate with creditors, and either restructure or sell their assets.

When a company files for bankruptcy, it's usually because the alternative (continuing to operate without bankruptcy protection) looks worse. The company likely had debt obligations it couldn't meet, obligations to investors it couldn't honor, and a balance sheet that was underwater.

Bankruptcy protection allowed Rad Power to halt immediate debt payments, discharge some obligations, and organize an asset sale process. In this case, that process took the form of an auction.

The Auction: Life EV Wins for $13.2 Million

In late January 2025, Rad Power Bikes held an auction for its assets. This is a common process in bankruptcy. The company's assets—inventory, intellectual property, brand, manufacturing relationships, customer lists, domain names, and anything else of value—are put on the market.

Five entities participated in the auction. Bidding opened at $8 million and moved upward as participants competed for the assets.

Life Electric Vehicle Holdings, a Florida-based company, emerged as the winning bidder with an offer of

Retrospec, another e-bike company, was the second-highest bidder at $13 million and is being held as the "backup bidder" in case the Life EV deal falls through for some reason.

The winning bid of

Investors who put money into Rad Power at high valuations will recover only cents on the dollar (if anything). Early investors who got out when valuations were high are fine. Late-stage investors who bought at

This is the harsh reality of venture capital: sometimes companies fail, and sometimes they fail catastrophically.

Rad Power Bikes' valuation plummeted from

Life Electric Vehicle Holdings: Who's Buying Rad Power?

This is where the story gets murky. Life Electric Vehicle Holdings, the winning bidder, is not a household name. The company is based in Florida and bills itself as a "developer, manufacturer, and distributor in the light electric vehicle industry."

Life EV sells e-bikes on its own website, though many of those products were listed as "sold out" at the time the acquisition was announced. This raises questions: Is Life EV an established, stable company, or is it also struggling?

The company's CEO, Robert Provost, declined to explain the company's plans for Rad Power, telling Tech Crunch that "there is still a process underway and there is an exciting future being planned for Rad Power." That's corporate language for "we're not saying anything specific right now."

Why would a company spend $13.2 million on a failing competitor's assets without a clear public strategy? Several possibilities:

-

Acquisition of brand and customer base: Rad Power still has brand recognition and an existing customer base. Life EV might want to expand by absorbing Rad's customers and converting them to Life EV products.

-

Manufacturing and supply chain relationships: Rad Power has relationships with manufacturers, component suppliers, and logistics partners. Life EV might want to leverage these relationships to improve its own operations.

-

Inventory and intellectual property: The $13.2 million might be primarily for inventory, patents, and design IP that Life EV can use in its own products.

-

Market consolidation: Life EV might be betting that the e-bike market will eventually recover and wants to build scale for that recovery.

-

Asset stripping: In worst-case scenarios, a buyer might acquire assets at bankruptcy prices with the intention of selling off components individually, liquidating inventory, and keeping anything valuable. This would be a financially motivated acquisition rather than a strategically motivated one.

Without more transparency from Life EV, the true intent remains unclear. The bankruptcy court will need to approve the deal before it closes, which adds another layer of oversight.

Retrospec's Backup Bid: Another Player in the E-Bike Wars

Retrospec, which submitted the second-highest bid at $13 million, is worth noting. Retrospec is a fellow e-bike company and a direct competitor to Rad Power.

The fact that Retrospec was willing to pay nearly the same amount as Life EV suggests they saw real value in acquiring Rad Power's assets. They likely valued Rad Power's brand, customer list, manufacturing relationships, and inventory at or near the winning bid price.

If Retrospec had won, the outcome would have been different: they would likely integrate Rad Power's customer base into their own operations, potentially rebrand some products under the Rad Power name if it still carries market value, and consolidate operations to improve margins and efficiency.

Instead, Retrospec gets to be the backup bidder. If Life EV's deal falls apart for any reason, Retrospec has the right of first refusal at their bid price. This is actually valuable optionality for Retrospec—they got a chance to bid, and if Life EV stumbles, they get another shot.

The presence of multiple serious bidders suggests the market does see potential in Rad Power's assets, even if the company itself is defunct.

The Broader E-Bike Bust: It's Not Just Rad Power

Rad Power Bikes isn't alone in its struggle. The broader e-bike industry has been contracting sharply since 2021.

Van Moof, a Dutch e-bike company that was once valued at

Cake, a Swedish maker of electric motorcycles and bikes, also went through bankruptcy and restructuring, eventually being acquired by other entities.

Bird, the scooter company (a different category of micromobility but similar dynamics), went through bankruptcy proceedings. It had raised over $700 million and was once valued at billions.

The pattern is clear: the pandemic created a massive, temporary boom in micromobility companies. Venture capitalists funded them aggressively. Companies scaled too fast. Demand crashed when the pandemic subsided. Companies couldn't adjust quickly enough. Bankruptcies and asset sales followed.

This isn't unique to e-bikes. It's a pattern that repeats whenever new technologies boom and then face reversion to normal demand levels.

Rad Power Bikes' valuation plummeted from

The Role of Venture Capital: Inflated Valuations Meet Market Reality

Rad Power Bikes' collapse raises uncomfortable questions about venture capital and how valuations are determined.

Rad Power raised

Four years later, the company is bankrupt, and its assets sold for $13.2 million.

How does this happen? A few factors:

Extrapolation from temporary conditions: During the pandemic boom, Rad Power's growth was extraordinary. Early-stage venture capitalists often extrapolate recent growth rates into the future, assuming they'll continue. When they bet on Rad Power at peak pandemic demand, they were betting that demand would stay high or continue growing. It didn't.

Capital abundance distorts decision-making: In 2020-2021, venture capital was historically abundant. Interest rates were near zero. Institutional investors (pension funds, endowments, corporations) were aggressively seeking high-growth bets. This created a competitive environment among VCs to fund the "hottest" companies. Higher valuations helped VCs win deals against other VC firms. Eventually, valuations disconnected from fundamentals entirely.

Ignoring market saturation: By 2021, the e-bike market was becoming saturated. Legacy bike manufacturers were entering with superior distribution. Amazon was selling e-bikes. New startups were being funded constantly. Rad Power was losing its competitive advantage. But unicorn valuations were still being granted, suggesting investors weren't fully accounting for competitive dynamics.

Overlooking operational execution: Rad Power's battery issues, supply chain mismanagement, and later management chaos were strategic red flags. Yet valuations continued to be high because VCs were focused on top-line growth, not operational efficiency or product quality.

When a company goes from a

What Happens to Rad Power Now? Brand, Assets, and Customers

With Life EV as the new owner, several questions emerge:

What happens to existing Rad Power customers? Rad Power has shipped hundreds of thousands of bikes. Owners will need support: warranty claims, spare parts, technical assistance, and repairs. Will Life EV honor Rad Power's warranty commitments? Will they stock spare parts for older models? These are critical for customer satisfaction.

What about the battery fire recalls? If Life EV inherits liability for the battery fires that were documented with the CPSC, they could face significant ongoing costs and legal exposure. They might need to implement a replacement program or settlement.

Will the Rad Power brand continue? Rad Power has brand recognition, especially in online communities. Life EV could maintain the brand name and gradually migrate Rad Power customers to Life EV products. Or they could fold the brand entirely and liquidate remaining inventory under clearance sales.

Will manufacturing continue? Rad Power manufactured bikes in various locations. Will Life EV continue those operations, or will they consolidate manufacturing into their own facilities? This affects supply chain relationships and potentially the pricing and availability of Rad Power bikes.

What about the Rad Power community? Rad Power built a loyal online community through social media, forums, and content. Life EV could try to maintain and grow that community, or they could let it dissipate as the company transitions.

These are not small questions. They directly impact every person who owns a Rad Power bike, who works for Rad Power, or who was counting on the company for future products and support.

Lessons for Startups: What Went Wrong

Rad Power Bikes' collapse offers several hard-earned lessons for founders and investors:

1. Temporary demand booms can look permanent. When growth is accelerating rapidly, it's easy to believe it will continue. It won't. Build your cost structure and hiring plans around sustainable demand, not peak demand.

2. Operational excellence matters more than marketing. Rad Power had great marketing and brand recognition, but they failed on basic execution: product quality, inventory management, and supply chain efficiency. No amount of marketing can overcome those failures for long.

3. Customer trust is fragile. Battery fires aren't a PR problem—they're a customer safety and brand trust problem. Defensive responses and minimization of customer concerns accelerates brand decay.

4. Legacy competitors aren't dead. Established companies like Trek, Giant, and Specialized have distribution networks, supply chain relationships, manufacturing expertise, and brand heritage. When they decide to enter a new market, startup competitors with none of those things face headwinds.

5. Hardware is harder than software. E-bikes are physical products. They have supply chains. They have customer support costs. They have quality issues. Margins are lower and more competitive than in software. The economics don't match the hype.

6. High valuations create internal pressure. When you raise at a $1.65 billion valuation, your investors expect you to build a multi-billion-dollar company. That pressure can lead to reckless spending, aggressive growth targets, and poor decision-making when reality doesn't match expectations.

7. Management stability matters. CEO turnover, especially multiple cycles, signals organizational dysfunction. It often precedes collapse.

Rad Power Bikes experienced rapid valuation growth during the pandemic, reaching unicorn status by 2021 with a valuation of $1.65 billion. Estimated data based on funding rounds.

Industry Outlook: Will E-Bikes Survive?

The collapse of Rad Power and other startups raises a critical question: is the e-bike market dead?

The answer is no, but with important caveats.

The pandemic created a temporary, unsustainable demand spike. When that demand normalized, a lot of companies that were built for the boom got crushed. That doesn't mean e-bikes are inherently unviable—it means the market was massively overheated and oversupplied.

Established bicycle manufacturers like Trek, Giant, Cannondale, and Specialized are still making e-bikes and selling them profitably. They have the distribution, the customer relationships, the manufacturing scale, and the brand heritage to compete effectively.

Smaller, scrappy e-bike companies can also succeed—but they need to find sustainable niches. Maybe that's a specific geography, a specific use case (cargo bikes, folding bikes, performance e-bikes), or a specific customer segment (kids, seniors, urban commuters).

What won't work is the VC model applied to e-bikes: raise massive capital, scale aggressively, build for exponential growth, achieve a multi-billion-dollar valuation. The unit economics don't support that model. E-bikes have 40-45% gross margins at best, tough supply chain economics, and a market that's finite and increasingly competitive.

The e-bike market will exist and probably grow slowly from here. But it will be dominated by established manufacturers and profitable specialists, not venture-backed unicorns.

What This Means for Consumers

For people who own Rad Power bikes, the bankruptcy and acquisition create some uncertainty. The good news: Life EV has acquired the assets and is continuing (in some form) to support the brand. The bad news: there's no guarantee that service, warranty support, and spare parts will be as available as they were when Rad Power was well-capitalized.

For people considering buying an e-bike, the Rad Power story is instructive: buy from established manufacturers (Trek, Giant, Cannondale, Specialized) who have deep pockets and will be around for warranty and support long-term. Startup e-bike companies are riskier because they might not be around in five years to honor warranty commitments or supply spare parts.

This is a fundamental economics lesson: hardware businesses need stable long-term capital and efficient operations. Venture capital can fund growth, but it can't guarantee survival. Choose partners you trust to outlast market cycles.

The Bankruptcy Auction Process: How Asset Sales Work

Understanding how bankruptcy auctions work helps explain what happened to Rad Power.

When a company files for bankruptcy, the court appoints a trustee to manage the liquidation process. In many cases, the company's assets are put up for auction. The auction is designed to get the maximum value and distribute proceeds to creditors in order of priority: secured creditors first, then unsecured creditors, then preferred stockholders, then common stockholders.

For Rad Power, the bankruptcy court held an auction with five participants. Bidding started at

When a sale occurs in bankruptcy, the company's liabilities are typically assumed by the buyer. In Rad Power's case, Life EV is assuming

The proceeds from the sale go to creditors. Rad Power likely had significant debt from investors, bank loans, and trade creditors. Secured creditors (those with collateral) are paid first. Unsecured creditors (vendors, employees owed back wages) are paid from remaining proceeds.

Equity investors—the VCs who funded Rad Power—typically get nothing. Their investment is wiped out.

Competitive Analysis: How Rad Power Stacks Against Survivors

Why did some e-bike companies survive while Rad Power collapsed?

The answer lies in fundamentals:

Trek and Giant: These are legacy bicycle manufacturers with 40+ years of history, established retail distribution in thousands of bike shops, manufacturing expertise, and efficient supply chains. They don't need venture capital. They're profitable. They have customer loyalty. When they enter the e-bike market, they're not learning to ride—they're leveraging existing capabilities.

Specialized and Cannondale: Similar story. They have heritage brands, retail distribution, and manufacturing expertise. E-bikes are a new product category, but the underlying business model is the same.

Smaller startups that survived: Companies like Riese & Müller (German cargo bikes) and some regional players survived by focusing on specific niches where they could command premium prices and build customer loyalty. They didn't try to be everything to everyone.

What Rad Power lacked: No retail distribution (they were pure DTC). No manufacturing expertise (they outsourced production). No brand heritage to draw from. No way to compete with legacy manufacturers on supply chain efficiency or cost.

Rad Power was betting that direct-to-consumer distribution and aggressive marketing could overcome those structural disadvantages. When demand collapsed, those marketing advantages evaporated, and the structural weaknesses became fatal.

Investor Losses and the Venture Capital Reality Check

Let's do the math on investor losses.

Rad Power raised

The company is now selling for $13.2 million.

This means equity investors are losing roughly 93-95 percent of their capital. For VCs who bought into the company at later rounds (when valuations were highest), losses are total or near-total.

For early investors who got out in secondary sales during the peak, they're fine. But most of the capital invested at high valuations is simply gone.

This is a hard lesson for the venture capital industry and for founders: raising a large valuation doesn't guarantee success. Execution and market conditions matter more than capital.

It's also a lesson about the limits of venture capital in certain industries. Hardware has different economics than software. Software can scale indefinitely with minimal marginal costs. Hardware requires supply chains, manufacturing, inventory, and customer support. The unit economics are very different.

The Role of COVID-19: Artificial Demand and Market Distortion

This story cannot be fully told without acknowledging the pandemic's role.

COVID-19 created unprecedented disruption: lockdowns, work-from-home mandates, fear of public transportation, and stimulus spending. For a few years, e-bikes benefited from all of these tailwinds simultaneously.

But these conditions were temporary by definition. Vaccines were deployed. Life returned to normal. Public transportation resumed. Stimulus spending ended. These temporary conditions that had inflated e-bike demand evaporated.

Companies that planned for those temporary conditions to persist made a strategic error. They built cost structures, hired aggressively, and invested in scaling for demand that was fundamentally unsustainable.

The pandemic did something similar to other sectors: cloud infrastructure, video conferencing software (before consolidation), and delivery services all experienced pandemic booms that didn't stick. Companies that treated those booms as permanent made costly mistakes.

The lesson: distinguish between temporary disruptions and structural shifts. Temporary disruptions create false signals. When the conditions change, the signals reverse. This is a difficult forecasting problem, and many smart people got it wrong with e-bikes.

What About Employees? The Human Cost of Failure

While most of the discussion around Rad Power's collapse focuses on financial and strategic issues, there's a human dimension worth acknowledging.

Rad Power employed hundreds of people at its peak. Through multiple rounds of layoffs starting in 2022, those employees lost their jobs. The bankruptcy final nailed shut any hope they had of cashing out through equity appreciation.

For employees who received equity compensation (stock options or RSUs), those holdings are likely worthless. They worked for years anticipating those equity grants would provide financial upside when the company exited or went public. Instead, the equity was diluted down to nothing.

This is a risk of working for startups, especially hardware startups in competitive markets. The upside potential is real, but so is the downside. Rad Power employees who joined when the company was a darling and were promised riches are instead walking away with experience and a story about how even "successful" companies can collapse.

The CPSC Investigation: Regulatory Risk in Hardware

The battery fire investigation by the Consumer Product Safety Commission deserves more focus.

When a federal agency investigates consumer safety issues with your product, that's a massive red flag. It signals that the product is creating genuine harm (or perceived risk of harm) to consumers. It also signals regulatory risk: the agency could mandate recalls, require product redesigns, impose fines, or take other actions.

For Rad Power, the CPSC's findings were damaging:31 reported fires, a characterization of the batteries as presenting a "hazard," and implicit criticism of the company's approach to battery safety.

The company's response—defending the batteries rather than owning the problem—was tone-deaf. When you have a safety issue, the appropriate response is to investigate root causes, take responsibility, and implement fixes. Rad Power did none of that publicly.

Regulatory risk is often underestimated in venture capital. A startup can be growing fast with great unit economics, but if regulators are concerned about the product, that regulatory risk can become existential.

This is especially true in hardware industries where safety is a factor: e-bikes, electric vehicles, robots, etc. Regulatory approval and safety certification can make or break companies.

FAQ

What was Rad Power Bikes' original business model?

Rad Power Bikes was a direct-to-consumer e-bike manufacturer that sold bikes primarily through its website rather than through traditional retail channels. The company focused on practical, affordable electric bikes and built a strong online community and brand identity. Their direct sales model allowed them to avoid retailer markups and maintain lower prices than legacy bicycle manufacturers.

Why did Rad Power Bikes fail if it was so successful during the pandemic?

Rad Power Bikes failed because the pandemic boom was temporary. When lockdowns ended, public transportation resumed, and stimulus spending dried up, demand for e-bikes collapsed. The company had scaled operations for peak pandemic demand and couldn't adjust quickly enough. Additionally, the company faced battery fire issues, management instability, and intense competition from established manufacturers entering the e-bike market.

How much did Life Electric Vehicle Holdings pay for Rad Power's assets?

Life Electric Vehicle Holdings won the bankruptcy auction with a bid of

What happened to Rad Power's battery fire investigation?

The Consumer Product Safety Commission documented 31 reported fires linked to Rad Power batteries and characterized certain Rad batteries as presenting a "hazard." The company disputed the CPSC's findings but did not publicly announce a comprehensive recall or remediation program. This issue significantly damaged customer trust and brand reputation.

Will Rad Power Bikes continue to exist under Life Electric Vehicle Holdings?

It's unclear what Life EV's plans are for the Rad Power brand. Life EV's CEO stated that "there is an exciting future being planned for Rad Power," but provided no details. Life EV could maintain the brand and gradually integrate Rad Power customers into its product line, rebrand the assets, or liquidate the inventory. The bankruptcy court must approve the deal before it closes.

Is the e-bike market dead because of Rad Power's failure?

No, the e-bike market still exists and is growing, but at a much slower and more sustainable pace than during the pandemic boom. The collapse of Rad Power and other venture-backed e-bike startups reflects overheating and oversupply, not the death of the category. Established manufacturers like Trek, Giant, Cannondale, and Specialized continue to sell e-bikes profitably. The market is likely to be dominated by these established companies and profitable niche players rather than venture-backed startups.

What happened to the employees of Rad Power Bikes?

Rad Power went through multiple rounds of layoffs starting in 2022, cutting approximately 10% of its workforce initially and additional employees in subsequent rounds. Employees with equity compensation (stock options or RSUs) likely lost their holdings as the company's valuation collapsed and ultimately filed for bankruptcy. The final bankruptcy eliminated any potential for equity value recovery.

How does a bankruptcy auction work?

When a company files for bankruptcy, its assets are typically auctioned to the highest bidder. The bankruptcy court sets a reserve price and manages the auction process. Proceeds from the sale go to creditors in order of priority: secured creditors (those with collateral) first, then unsecured creditors, then preferred stockholders, and finally common stockholders. Equity investors typically receive nothing in bankruptcy sales like Rad Power's.

What is Van Moof and how is it similar to Rad Power?

Van Moof is a Dutch e-bike company that raised

Why didn't Rad Power compete effectively against Trek, Giant, and Cannondale?

Legacy bicycle manufacturers have structural advantages over startups: established retail distribution networks, manufacturing expertise, efficient supply chains, brand heritage, and access to capital without extreme dilution. When these companies entered the e-bike market, they could leverage all of these advantages. Rad Power had none of them. Their advantage was direct-to-consumer marketing and brand identity, but those advantages disappeared when demand collapsed and customers could buy from trusted established brands instead.

Conclusion: Lessons That Will Echo Through Venture Capital

The collapse of Rad Power Bikes is a watershed moment for venture capital, hardware startups, and the e-bike industry. It's a story of exceptional execution meeting impossible market conditions, of capital abundance distorting rational decision-making, and of the fundamental difference between software and hardware business models.

For founders, the lesson is clear: sustainable business fundamentals matter more than growth rates. You can't spend your way out of unfavorable unit economics or structural competitive disadvantages. When demand normalizes, those fundamentals become everything.

For investors, the lesson is harder: valuations disconnected from market reality will eventually be corrected. The correction is painful. Companies that raised at peak valuations see their equity wiped out. Investors who bought into unicorn narratives without stress-testing assumptions lose their capital.

For consumers, the lesson is practical: buy from companies likely to survive and support your products long-term. Early-stage hardware startups are higher risk than established manufacturers with deep pockets and existing distribution networks.

For the e-bike industry, the lesson is that the pandemic boom was a gift that masked underlying operational challenges. Companies that used that time to build sustainable competitive advantages (manufacturing excellence, customer service, brand loyalty) survived. Companies that treated the boom as permanent didn't.

Rad Power Bikes at

It's a story that will be taught in MBA programs for years. And most importantly, it's a story that will make investors slightly more skeptical and slightly more rigorous the next time they see a company with extraordinary growth and an even more extraordinary valuation.

That skepticism might prevent the next Rad Power from raising too much capital too fast and building an unsustainable cost structure for temporary demand. Or it might not. History suggests that venture capital will cycle through boom and bust regardless of lessons learned. But hopefully, a few founders and investors will remember Rad Power Bikes and make slightly better decisions because of it.

The e-bike industry will recover from this bust. E-bikes are a legitimate category with real customer demand. But the recovery will be built on established manufacturers and profitable specialists, not venture-backed unicorns burning through capital and pretending temporary demand is structural. That's the real lesson of Rad Power's fall.

Key Takeaways

- Rad Power Bikes sold for 1.65 billion peak valuation in 2021, representing a 99% value collapse

- Pandemic demand boom created unsustainable growth trajectories that founders and VCs mistook for permanent market shifts, leading to aggressive scaling

- Battery fire investigations by the CPSC and subsequent product safety concerns eroded customer trust when the company took a defensive stance instead of owning the problem

- Established bicycle manufacturers (Trek, Giant, Cannondale, Specialized) proved structurally superior competitors with existing retail distribution, brand heritage, and manufacturing expertise

- Direct-to-consumer distribution advantage evaporated when demand fell and consumers preferred buying from trusted established brands with retail presence and warranty support

- Hardware business unit economics can't support the venture capital growth model that works in software SaaS, limiting how large and valuable e-bike companies can become

- Multiple CEO changes and layoffs signaled organizational dysfunction that preceded bankruptcy, showing management instability is a leading indicator of collapse

- Supply chain mismanagement resulted in massive inventory accumulation that destroyed cash flow when pandemic-driven demand normalized

- The pattern repeats: VanMoof, Cake, Bird, and other venture-backed micromobility companies filed for bankruptcy in similar fashion after pandemic boom ended

- Investors lost 93-95% of capital deployed at high valuations as equity was wiped out in bankruptcy asset sales favoring creditors