The Leading Public Software Companies Are Now Down -50% in the Last 6 Months | SaaStr

The SaaStr.ai Index of the Top 25 Public Software Companies just hit -50.5% over the past six months. October 2025 to April 2026. Half the market cap of the...

TechnologyInnovationBest PracticesGuideTutorial

Listen to Article

0:00

0:00

0:00

The Leading Public Software Companies Are Now Down -50% in the Last 6 Months | Saa Str

Overview

Free e Books

e Book: Hiring a Great VP of Sales

e Book: Raising Capital

e Book: The First $1m ARR

University

All Posts

University

Podcasts

The Top CROs

VC Fundraising

Top Videos

Q&A

Best of Saa Str

#1 Bestselling Book

Search Everything

Join the Community

Details

Free e Books

e Book: Hiring a Great VP of Sales

e Book: Raising Capital

e Book: The First $1m ARR

London 2025

Annual 2026

Events Overview

Sponsors

Event Sponsorship

Media Sponsorship

Digital AI Day 2025 (Free)

Speaker Submissions

Speaker Requirements

Overview

The Leading Public Software Companies Are Now Down -50% in the Last 6 Months

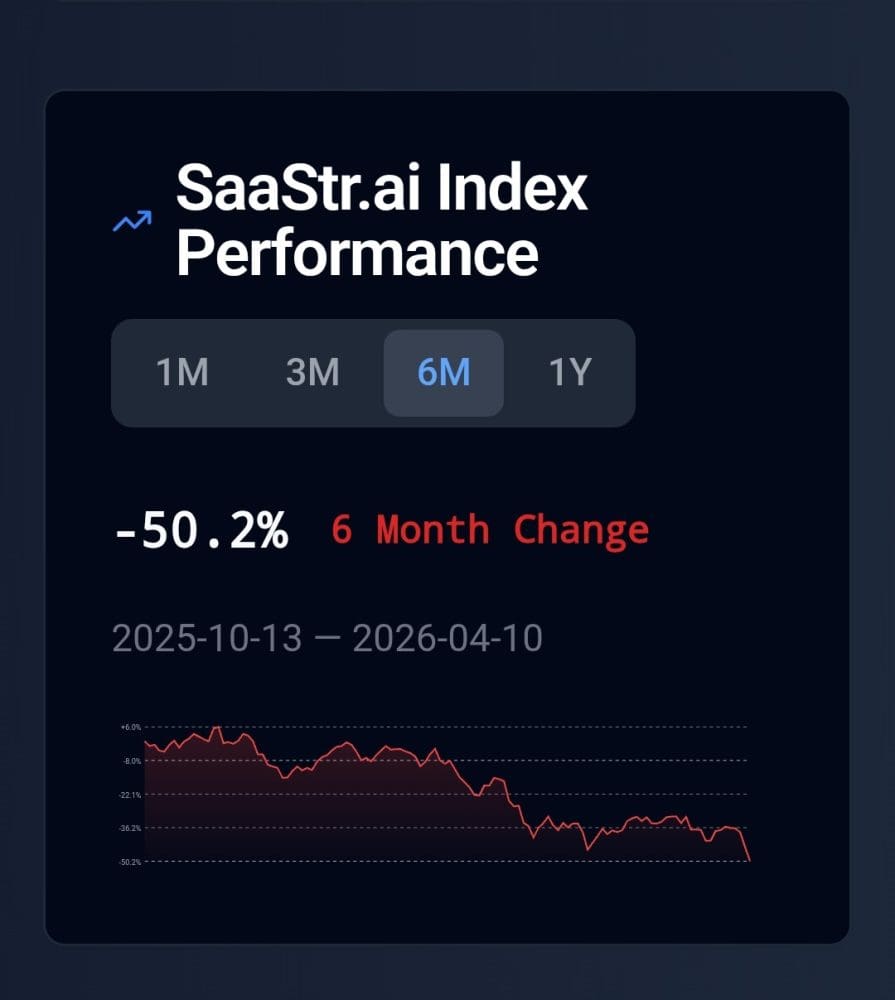

The Saa Str.ai Index of the Top 25 Public Software Companies just hit -50.5% over the past six months. October 2025 to April 2026. Half the market cap of the leading public B2B software companies — gone.

Not -20%, which would feel like a correction. Not -30%, which we’ve seen before. Fifty percent.

This is not a blip. This is a structural re-rating of an entire asset class.

The Saa Str.ai Index tracks 25 leading B2B and software companies — the names founders and investors have benchmarked against for a decade. Companies like Datadog, Zscaler, Git Lab, Rubrik, Klaviyo, Ui Path, Workday.

In March, the index had declined approximately 23.6% year-to-date, with Digital Ocean as the lone standout at +49.6% YTD, and Atlassian as the biggest laggard at -53%. By April 10, the 6-month cumulative loss hit -50.5%.

That number represents something that has never happened in our industry before.

For the first time ever, public software companies now trade at a P/E discount to the S&P 500. Not at parity. Below. We’ve never seen this. Not in 2022 when rates spiked. Not in 2008. Not even in the dot-com unwind, which was a speculative bubble collapsing — not a structural attack on the business model itself.

The forward P/E multiple for application software has collapsed from 84x in 2021 to 22.7x today. The market’s implied long-term growth rate for a representative public Saa S company has dropped from 4.7% just three months ago to 1.1% today.

The market is effectively saying: we no longer believe software is a premium business.

The Saa S Rout of 2026 Is Even Worse Than You Think. For the First Time Ever, Software Now Trades at a Discount to the S&P 500.

The Saa S Rout of 2026 Is Even Worse Than You Think. For the First Time Ever, Software Now Trades at a Discount to the S&P 500.

It’s important to separate these, because conflating them leads to bad strategy.

450 billion, is targeting AI infrastructure. That money used to flow to Salesforce seats, Service Now modules, Hub Spot licenses, Datadog tiers. It is being redirected right now, this quarter, measurably.

AI agents may make traditional software structurally less valuable over time. Seat-based models depend on headcount growth. If agents replace seats rather than complement them, the revenue model doesn’t just slow — it reverses. The market is pricing this in at the terminal value level, which explains why current earnings don’t fully explain the magnitude of the decline. Roughly 85-95% of enterprise value in a Saa S DCF comes from terminal value. Investors aren’t debating this quarter. They’re debating whether this business has a sustainable moat at all.

Both forces are real. The second one may be more fear than reality at this exact moment. But when $2 trillion in market cap disappears, the market has made a judgment.

Look at what’s happened to the category leaders over the past 6-12 months:

Atlassian (TEAM): Down 50%+ YTD. A company that basically built developer collaboration. Jira is in virtually every engineering org on the planet.

Hub Spot (HUBS): Down 50%+ over the past year. Wrote the book on inbound. Grew to $2B+ ARR on the back of one of the best go-to-market motions in B2B history.

Workday (WDAY): Down 30%+ in Q1 2026 alone. Owns HCM at the Fortune 500. Deeply embedded workflows.

Salesforce (CRM): Down 30%+ in Q1. The defining CRM platform of the last 20 years.

Service Now (NOW): Down 30%+ in Q1. Despite actually accelerating — RPO growth outpacing revenue, Agentforce-style AI positioning arguably the most credible in enterprise software.

Adobe (ADBE): Down from

638tounder

350. The creative cloud monopoly. Every designer, every marketer.

Ui Path (PATH): Down dramatically from its highs. The RPA leader that was supposed to be the automation winner.

These are not speculative bets. These are cash-generating, deeply embedded, category-defining businesses. And the market is treating them like they face existential risk.

Not everything is down equally. Within the wreckage, a clear pattern has emerged.

The companies holding their own — or in some cases still growing — share a few characteristics:

Palantir (PLTR): +135% in 2025, now cooling with the broader market but still dramatically outperforming peers on a multi-year basis. Their Rule of 40 score hit 127 in Q4 2025. Revenue growth at 70% Yo Y, U. S. commercial up 137%. They guided 2026 at 61% growth as a floor. The market is doing them no favors right now, but the underlying business has definitively proven it is not just another seat-based Saa S vendor.

Cloudflare (NET): Guided 2026 at $2.79B revenue, 28-29% growth. Their infrastructure sits behind 20%+ of the web. AI agents are generating an order of magnitude more outbound requests than traditional user-driven apps, and all of that flows through Cloudflare. This is what “becoming infrastructure for AI” looks like.

Digital Ocean (DOCN): Up nearly 50% YTD in an index down 50%. Smaller companies, simpler stack, and apparently a product that developers building AI apps actually want.

Crowd Strike (CRWD) and Zscaler (ZS): Cybersecurity is non-discretionary. You can be in budget freeze and still have to fund your security stack. These companies are down from 2025 peaks but have held far better than application software.

The winners are infrastructure plays — companies where AI workloads create demand rather than substitute for their product. The losers are horizontal workflow software, productivity tools, anything where the core value proposition is “help humans do their job more efficiently” and the obvious question is: what if agents do that job instead?

The public markets are a leading indicator, not just a scoreboard.

The repricing happening at the public level is coming to the private market. It already is. The Redpoint data shows median NTM revenue multiples for public Saa S now at 4.1x, down from 22x at the 2021 peak. Private markets at Series B/C are still pricing at 60x ARR for the highest-growth AI-native companies — a 528% premium over public software. That gap will narrow. Some of it will close because public software recovers. More of it will close because private valuations come in as the AI-native winners separate from the pretenders.

Three things to take from this if you’re a founder right now:

Seat-based growth is over as a primary growth thesis. If your business plan says “we’ll grow as customer headcount grows,” that assumption is broken. The CFOs know it. Investors know it. You need to be able to articulate a growth vector that doesn’t depend on companies hiring more humans.

Infrastructure beats application. The companies holding up are the ones where AI runs on top of their product, not the ones where AI replaces their product. If you sit in the workflow layer and you don’t have proprietary data or years of embedded integration, your category is in play.

The budget is moving, not disappearing. $40-50B in new annual enterprise spend has materialized in two years flowing to Anthropic and Open AI. That money came from somewhere — traditional B2B software. But it didn’t evaporate. It went to AI infrastructure and foundation models. Which means if you’re building AI-native, the budget exists. CIOs have already started authorizing it. The question is whether your product captures a piece of that shifted spend.

A Buying Opportunity Still? Or a Lost Generation?

Here’s what I keep asking: is this a buying opportunity or a fundamental re-rating?

In February 2016, Linked In dropped 44% and Tableau dropped 50% in a single day. Salesforce fell 13%. It felt like the end of the world. Four months later, Microsoft bought Linked In for $26B. The whole sector recovered within a year.

But that crash was fear-driven. Growth rates at those companies were intact. The business model was not under structural attack.

This one is different. Public Saa S growth rates have declined every single quarter since the 2021 peak. Not one quarter of reacceleration. Every quarter, slower. The AI narrative gave the market permission to reprice what the numbers had been saying for three years. The 2026 decline isn’t fully manufactured panic. It’s the market finally catching up to reality.

The bull case is that software companies still have the data, the enterprise relationships, the integrations, and 10-20 years of workflow lock-in. At 22x forward earnings — below the broader market — you’re not paying for growth anymore. If these businesses stabilize at even moderate growth, they’re cheap.

The bear case is that if seat expansion is gone as the growth engine, and pricing power gets squeezed as buyers renegotiate, the earnings trajectory for many companies is genuinely uncertain. A fair multiple on decelerating earnings is not 22x.

I don’t know how this resolves. But the Saa Str.ai Index at -50.5% in six months is the market telling you something important.

The public companies that survive and thrive from here will be the ones that answer this question clearly: am I infrastructure for AI, or am I competing with it?

The ones that can’t answer it — or worse, are pretending the question doesn’t apply to them — are the ones who will keep falling.

The Hardest Truth: Private Unicorns Have Fallen Further

Here’s what nobody says out loud: most private B2B unicorns — the ones marked at

1B,

2B, $5B valuations from 2020 and 2021 — have declined more than the public companies. Not less. More.

There’s no ticker. No daily price. The last round closed at

Xandthedeckstillsays

X. But if those companies went to market today — truly went to market for a new primary round at arms length — the marks would be brutal. The public comps are down 50%. The revenue multiples have compressed from 20x+ to 4x. The growth rates have slowed. The math does not produce the same number it did three years ago.

Public market founders are living in the reality in real time. The stock price is there every morning when you open your phone. It is humbling, clarifying, and ultimately useful.

Private unicorn founders are often living in the last round. The board deck shows the old valuation. The team still talks about the billion-dollar milestone. The LP statement hasn’t moved. But the underlying value has. Quietly, without announcement, without a press release.

First, the next fundraise. If you’re a 2020 or 2021 vintage company that has not raised since, you are going to face a reality check when you do. The sooner you internalize what the public comps are saying, the better positioned you’ll be to navigate it — whether that’s tightening your burn, finding a path to profitability, or building the AI growth story that earns a new premium.

Second, the exit window. M&A at inflated valuations is essentially closed. Strategic buyers are not paying 2021 prices. They’re using public comps, which are now at historic lows. If you were counting on an exit at your last round valuation or above, that plan needs to be rebuilt.

A B2B software company growing at 10-15% in 2026 is not a stable business. It is a slowly dying one. The multiples tell you that. The talent market tells you that — the best engineers and salespeople are leaving for companies actually winning. The customer conversations tell you that — buyers are consolidating vendors and your contract is on the list.

You have to grow. And the only place the growth budget exists right now is AI.

CIOs have authorized AI spend. That budget line exists, it is growing, and in many organizations it is the only budget line that is growing. The rest of enterprise software spend is flat to declining. Security is non-discretionary. Everything else is getting cut or held.

If your product is not tapping into that AI budget line — if a CIO can’t categorize your purchase as part of their AI transformation — you are competing for dollars that don’t exist. You are fighting over a shrinking pool while the new pool sits right there.

This doesn’t mean slap “AI” on your marketing deck. Buyers have seen that. It means genuinely rethinking what your product does and how you price and package it in a way that solves the problem CIOs are actually trying to solve in 2026: how do I deploy AI agents into my workflows, reduce headcount costs, and show my board I’m not getting disrupted?

If your product answers that question, you access the budget. If it doesn’t, you’re asking for money that isn’t there.

The Saa Str.ai Index at -50.5% is a public market signal. The private market is sending the same signal — just more quietly. Grow or die. Tap the AI budget. There is no option three.

And join us at Saa Str AI Annual, May 12–14 in the SF Bay Area, where 10,000+ B2B + AI founders and investors will be digging into exactly these questions.

2025 Should Be Better Than 2024 For Almost All Leading Public Saa S Companies

About 70% of Saa S Public Companies Are New Versions of Existing Categories of Software (Updated)

What Are Public Saa S Companies Taken Private At? 7.7x ARR On Average Per Saa Somomics

2025 Should Be Better Than 2024 For Almost All Leading Public Saa S Companies

About 70% of Saa S Public Companies Are New Versions of Existing Categories of Software (Updated)

What Are Public Saa S Companies Taken Private At? 7.7x ARR On Average Per Saa Somomics

RSS Industry News

Get from

0to

100 Million in ARR

with less stress and more success.

Key Takeaways

Free e Books

e Book: Hiring a Great VP of Sales

e Book: Raising Capital

e Book: The First $1m ARR

University

All Posts

University

Podcasts

The Top CROs

VC Fundraising

Top Videos

Q&A

Best of Saa Str

#1 Bestselling Book

Search Everything

Join the Community

Free e Books

e Book: Hiring a Great VP of Sales

e Book: Raising Capital

e Book: The First $1m ARR

London 2025

Annual 2026

Events Overview

Sponsors

Event Sponsorship

Media Sponsorship

Digital AI Day 2025 (Free)

Speaker Submissions

Speaker Requirements

Overview

Cut Costs with Runable

Cost savings are based on average monthly price per user for each app.

Which apps do you use?

Apps to replace

ChatGPT

$20 / month

Lovable

$25 / month

Gamma AI

$25 / month

HiggsField

$49 / month

Leonardo AI

$12 / month

TOTAL$131 / month

Runable price = $9 / month

Saves $122 / month

Runable can save upto $1464 per year compared to the non-enterprise price of your apps.