The PE Software Backlog: Will 1,000+ Unicorns Ever Get Sold or Go Public? | Saa Str AI

Overview

AI VC AI Mentor: Digital Jason + Amelia AI Startup Benchmarking

AI Agent Playbook Free e Books

e Book: Hiring a Great VP of Sales

e Book: Raising Capital

e Book: The First $1m ARR

Details

University All Posts Podcasts The Top CROs VC Fundraising Top Videos Q&A Best of Saa Str #1 Bestselling Book Search Everything Join the Community

Free e Books

e Book: Hiring a Great VP of Sales

e Book: Raising Capital

e Book: The First $1m ARR

AI Annual 2026 Events Overview Sponsors

Event Sponsorship

Media Sponsorship

Digital AI Day 2026 (Free) Speaker Submissions Speaker Requirements Overview

The PE Software Backlog: Will 1,000+ Unicorns Ever Get Sold or Go Public?

Per the Wall Street this week, private equity will need about nine years to clear its backlog of unsold portfolio companies.

And that’s the conservative version. Bain’s 2026 Global Private Equity Report puts the whole industry at roughly 32,000 unsold companies worth

Add the venture unicorns and there are well over a thousand billion-dollar software companies that were bought or valued at 2021 peaks with no working way out.

OMERS takes nine-figure loss as Touch Bistro sold to Constellation Software for

OMERS takes nine-figure loss as Touch Bistro sold to Constellation Software for

About 13,500 U. S. companies sat in private equity portfolios as of June 30, up from roughly 13,300 at the end of 2025 (Pitch Book, via WSJ). Almost 4,000 have been held six or more years. About 1,500 have been held nine or more. The private equity model is to ideally exit them in 4 years or less.

Bain’s data says the same thing at industry scale. The average holding period at exit is now around seven years, up from five to six across 2010 to 2021. Almost 40% of all companies are held longer than five years, up from 29% in 2019. And the money isn’t coming back: distributions as a share of NAV have stayed below 15% for four straight years, which is an industry record.

PE firms used to target three-to-five-year holds. When the average drifts to seven and the backlog hits 33,000, the machine stops turning, and LPs stop writing checks. First-half 2026 fundraising came in at

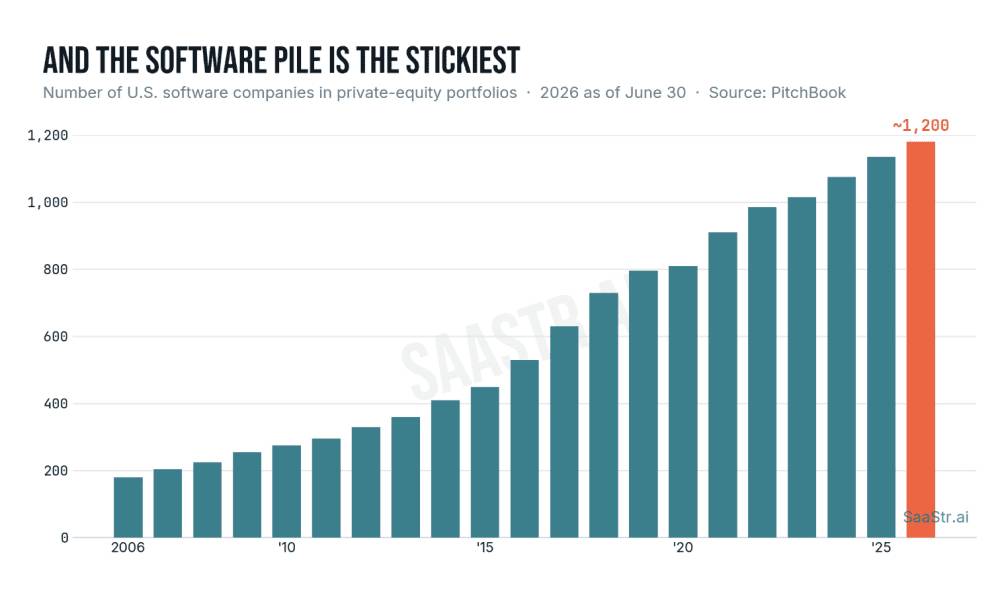

Importantly, Software Is Where It’s Frozen Hardest

Only about 1,200 of the 13,500 PE-owned companies are software. Small by count, but they lock up a larger share of the capital, because so many got bought at peak multiples in 2020 and 2021. Darius Craton at Raymond James told the WSJ the 2021 vintage is the toughest to exit given where valuations were then versus now, and there’s a wall of it building up that has to come through.

The Bain midyear report shows how hard that wall hit. Technology buyout deal value fell 70% between Q4 2025 and Q1 2026, and the number of tech deals over $1 billion dropped from 15 to just 4. That is the software market seizing up.

The Venture Side: 859 Unicorns and a Sub-1x Decade

The WSJ and Bain cover PE. The venture backlog is its own problem, and the numbers are just as stark from the primary source.

Per the 2026 NVCA Yearbook, U. S. venture deployed $320B in 2025, 65% of it into AI, with 859 unicorns waiting for an exit. Globally the World Economic Forum counts 1,920 privately held unicorns, and 59% of them were founded more than a decade ago. Most of these are aging private assets with investors who want their money back.

Pitch Book and NVCA report the median VC IRR for North American vintages since 2019 sits in the single digits, and the median DPI (cash returned) for the past decade’s vintages is still below 1x. A decade of funds, and the median one hasn’t yet returned the cash it took in.

A private company exits three ways, and all three got narrower.

IPOs are back, but through a keyhole. PE firms took 16 companies public in the first half of 2026 and raised $10.1B, the best six-month stretch since late 2021, and December’s Medline listing was the largest PE-backed IPO ever. Real progress. But the market got selective: 67% of the unicorns that went public in 2025 priced below their last private round.

And the pipeline is thin. Pitch Book notes that Space X, Open AI, and Anthropic alone could generate close to $2.5 trillion in exit value, more than every VC-backed IPO this century combined, but as of this week’s Q2 report, beyond Anthropic and Open AI there’s no real IPO pipeline built behind them. A handful of giants clearing does not reopen the market for the other 800-plus.

M&A is the usual backup, and it’s narrowed too. Antitrust reviews drag, fewer strategics are active, and a lot of the backlog is stranded in the worst possible spot, too big to get acquired easily and too richly marked for public buyers.

Secondaries and continuation vehicles are where the liquidity actually moves now. On the venture side, Pitch Book pegs U. S. direct secondary volume at roughly 2% of total unicorn value, growing fast and shifting from fallback to core strategy. On the PE side, GPs are running continuation vehicles that let LPs cash out while the sponsor keeps the asset. Useful tools, both. They’re also the market routing around a front door that stopped working.

What’s Getting Out: AI, Defense, and Down Rounds

What’s clearing tells you what the market wants. Outside healthcare, roughly 90% of this year’s IPOs came from AI, crypto, fintech, defense, and space. Those sectors have the growth and, in some cases, the government tailwind. The market is moving toward fewer, larger offerings.

Two more things stand out. The roll-up model is back in favor. Bending Spoons, which has been buying up brands including AOL, raised $1.68B in its debut last week and jumped 40%. Its playbook is buying tired businesses, fixing them, and holding, and public investors clearly like it. Expect more capital chasing that approach, because there are tens of thousands of stranded assets sitting at reset prices.

Down-round IPOs also went mainstream. That 67% of 2025 unicorn listings priced below their peak, and the market absorbed them fine. The stigma faded. For a lot of founders, a clean down-round exit beats waiting five more years for a number that isn’t coming back.

A few takeaways if you’re building or investing right now.

Assume liquidity is a decade out and run the company that way. The three-to-five-year hold is gone on the PE side, and the venture clock runs longer. If your plan needs a clean exit inside five years, it needs a market that doesn’t exist. Get to real profitability, because “12 is the new 5” applies to you too. Public buyers now want growth you can actually show.

Stop treating your 2021 valuation as a floor. The companies most stuck are the ones whose owners can’t accept the reset. The 5% rule that traps GPs traps founders too. Mark to reality, raise flat or down when you have to, and take a fair exit when it shows up.

Get good at secondaries. Whether you’re a founder giving early employees liquidity or a GP managing DPI, you need a real view on the secondary market. That’s where the volume is, and it isn’t going back in the box.

Being AI-native is the line between an exit and a holding pattern. The market is sorting companies into the AI, defense, and fintech names that clear and everything else that sits, and the sort keeps getting sharper. The best protection against the backlog is being a company the 2026 market wants to buy.

WSJ: “Private-Equity Firms Are Sitting on a Nine-Year Backlog,” The Wall Street Journal, July 7, 2026

Global Private Equity Report 2026 (the 32,000 companies / $3.8T, ~7-year holds, sub-15% NAV distributions, “12 is the new 5”): https://www.bain.com/insights/topics/global-private-equity-report/

Full report PDF: https://www.bain.com/globalassets/noindex/2026/bain-report_global-private-equity-report-2026.pdf

Private Equity Midyear Report 2026 (the 70% tech-buyout drop, $1B deals 15→4, Saa Spocalypse, MSCI marks, ILPA 5% rule, ~33,000 count): https://www.bain.com/insights/private-equity-midyear-report-2026/

Midyear press release version: https://www.bain.com/about/media-center/press-releases/2026/winning-firms-will-focus-on-what-they-can-control-weather-the-rest-as-triple-shock-brakes-private-equitys-latest-revival-bain–company-2026-midyear-pe-report/

Q2 2026 Pitch Book-NVCA Venture Monitor (this week’s report, “no IPO pipeline beyond Anthropic and Open AI”): https://pitchbook.com/news/reports/q 2-2026-pitchbook-nvca-venture-monitor

Q1 2026 Venture Monitor (median DPI below 1x, single-digit IRRs, ~$2.5T potential from Space X/Open AI/Anthropic): https://pitchbook.com/news/reports/q 1-2026-pitchbook-nvca-venture-monitor

2026 NVCA Yearbook (859 unicorns, 67% down-round IPOs, $320B / 65% AI): https://nvca.org/2026-nvca-yearbook/

By Year-End, Anthropic Will Out-Earn Every Public Software Company Except Microsoft

Coatue: We Have a 25 Year IPO Backlog. But Software Will Bounce Back Soon.

Dear Saa Str: How Much Do Founder-CEOs Own at Time of Exit?

By Year-End, Anthropic Will Out-Earn Every Public Software Company Except Microsoft

Coatue: We Have a 25 Year IPO Backlog. But Software Will Bounce Back Soon.

Dear Saa Str: How Much Do Founder-CEOs Own at Time of Exit?

Get from

Key Takeaways

-

AI VC AI Mentor: Digital Jason + Amelia AI Startup Benchmarking

-

AI Agent Playbook Free e Books

e Book: Hiring a Great VP of Sales e Book: Raising Capital e Book: The First $1m ARR -

University All Posts Podcasts The Top CROs VC Fundraising Top Videos Q&A Best of Saa Str #1 Bestselling Book Search Everything Join the Community

-

Free e Books

e Book: Hiring a Great VP of Sales e Book: Raising Capital e Book: The First $1m ARR -

AI Annual 2026 Events Overview Sponsors

Event Sponsorship Media Sponsorship