![Tiger Global's India Tax Loss: What It Means for Offshore Investment Structures [2025]](https://tryrunable.com/blog/tiger-global-s-india-tax-loss-what-it-means-for-offshore-inv/image-1-1768487914345.jpg)

Introduction: When Sovereign Power Trumps Tax Optimization

Tiger Global just got a very expensive lesson in geopolitics.

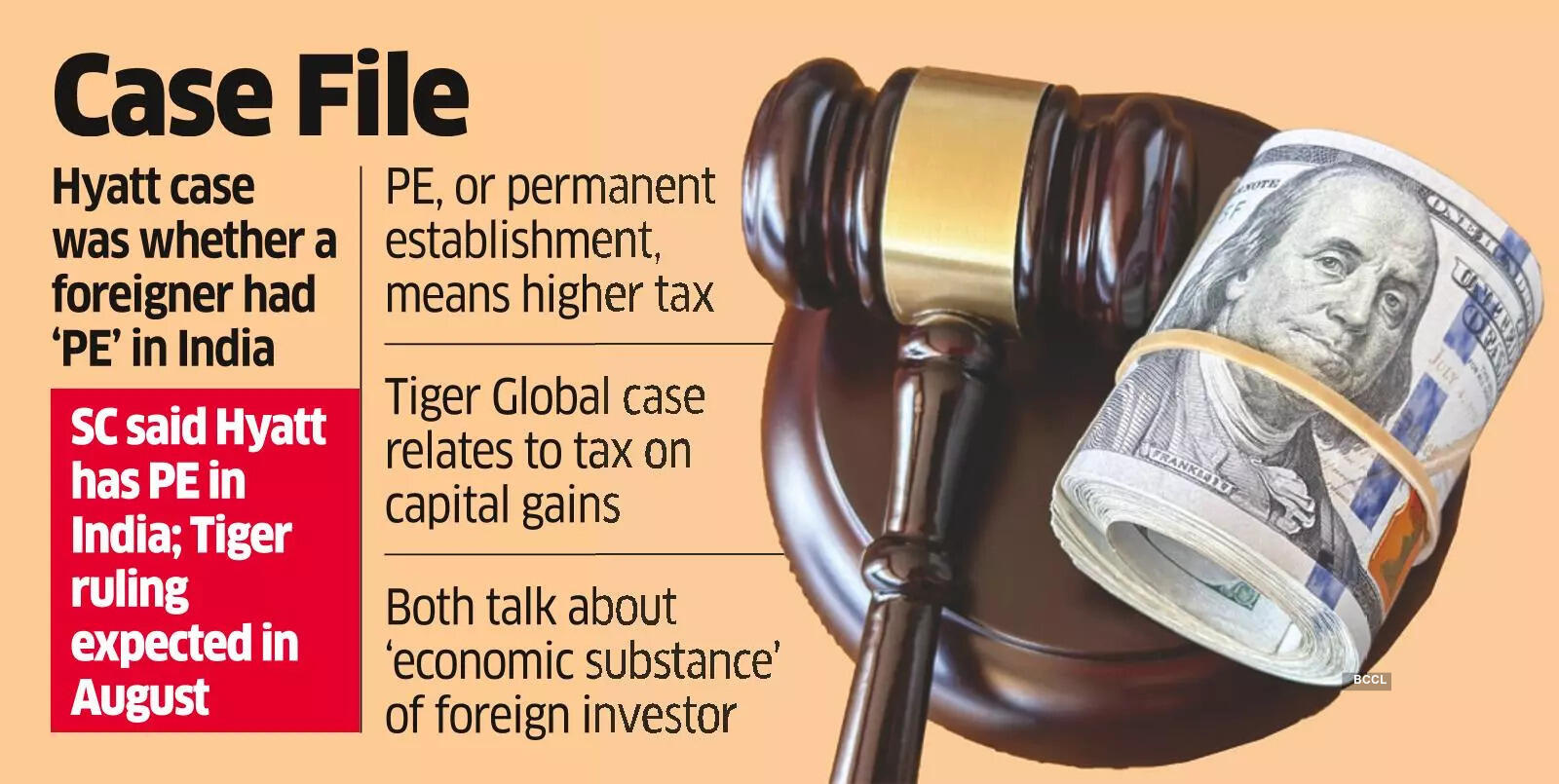

On a Thursday in early 2025, India's Supreme Court issued a ruling that sent shockwaves through the global investment community. The case wasn't about fraud or illegal activity. It was about something far more subtle, and far more consequential: whether a sophisticated offshore structure could shield an investment fund from paying taxes in the country where the actual value was created.

The case centered on Tiger Global's 2018 exit from Flipkart during Walmart's

It's a playbook that's worked for decades. In fact, it's become the gold standard for how sophisticated investors structure their exposure to fast-growing emerging markets. The logic is clean: invest through an offshore entity, structure it to qualify for treaty protections, and when you exit, minimize the tax friction.

Except this time, it didn't work. And that matters more than most people realize.

This ruling represents a fundamental shift in how countries are thinking about taxing rights, sovereignty, and the limits of legal tax optimization. It's not a technical tax detail for accountants. It's a signal that the old offshore playbook—the one that's worked for Tiger Global, Sequoia, and countless other global funds—is facing serious structural challenges.

What makes this particularly significant is the court's explicit framing of the issue around national sovereignty. The bench didn't just rule on Tiger Global's specific case. It issued a broader warning about structures designed "primarily to dilute" a country's taxing authority. That language matters. It suggests future rulings will look less at whether a structure is technically legal and more at whether its primary purpose is tax avoidance.

For Tiger Global, the stakes are enormous. The firm is considering a review petition, though such appeals rarely succeed. But more importantly, this ruling reshapes how global funds think about their India exposure. India represents one of the fastest-growing major capital markets in the world. Millions of startups and thousands of growth-stage companies operate in India. For any serious global investor, India is non-negotiable. The question is no longer whether you invest there. The question is how you structure that investment when you're facing a judiciary increasingly skeptical of aggressive tax planning.

Let's break down what happened, why it matters, and what it means for the future of offshore investment structures in high-growth emerging markets.

The Tiger Global-Flipkart Situation: A Case Study in Strategic Investment

Understanding Tiger Global's position requires understanding what Flipkart was and what it meant to investors in India's tech ecosystem.

Flipkart, founded in 2007 by Sachin Bansal and Binny Bansal, was India's answer to Amazon. At a time when most people doubted whether e-commerce could work in a country with inconsistent internet infrastructure and limited digital payment adoption, Flipkart proved skeptics wrong. The platform didn't just work. It became absolutely essential to how millions of Indians shopped online.

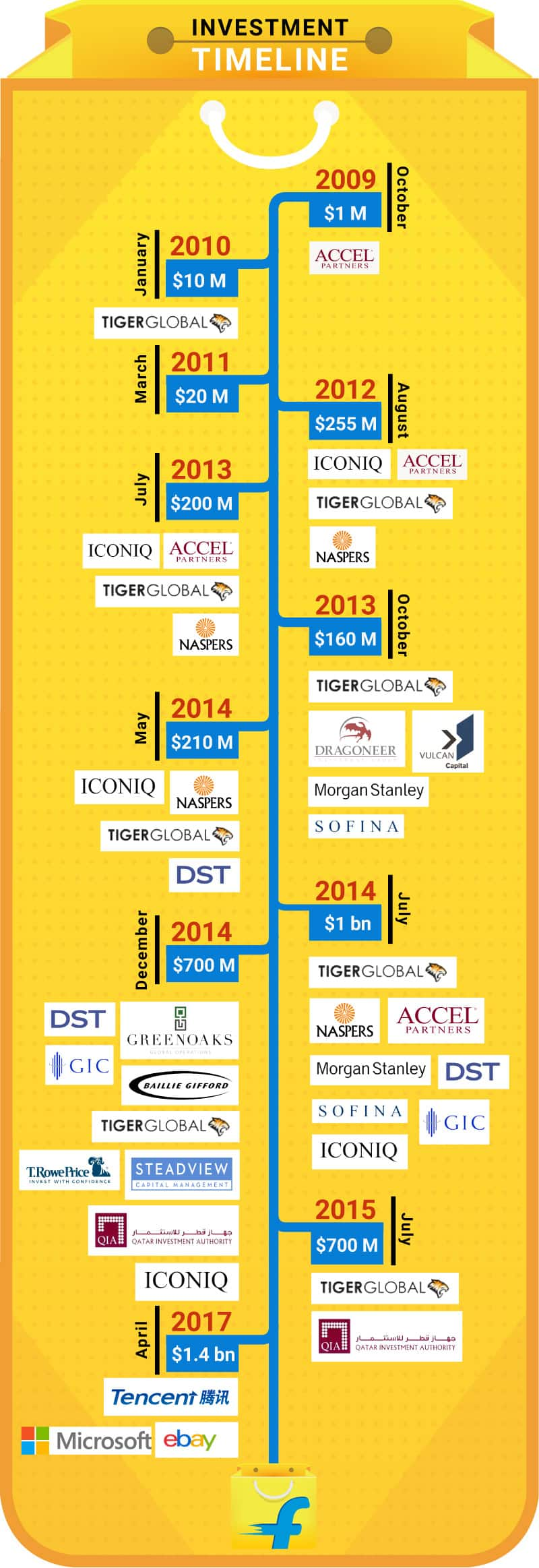

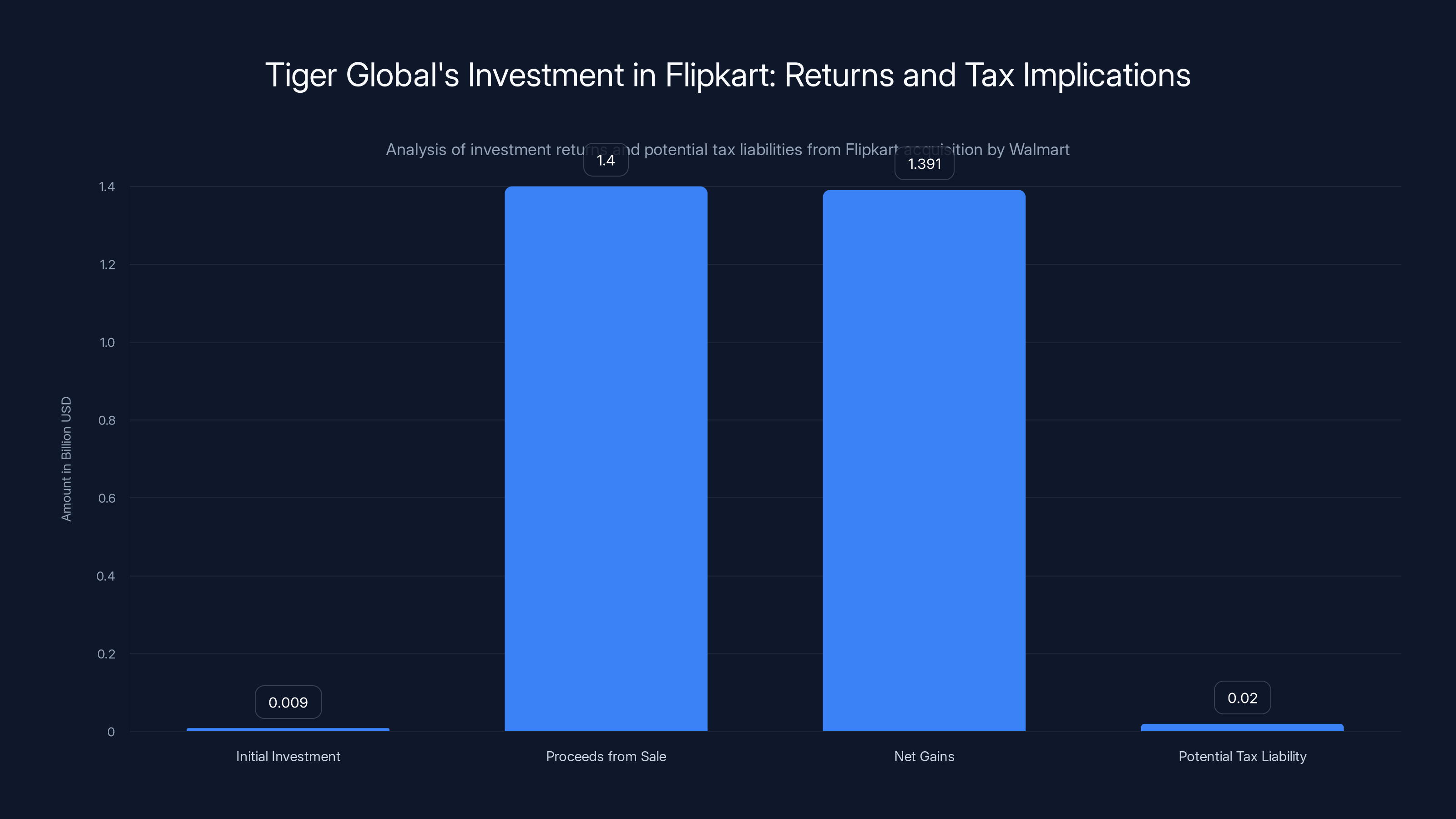

Tiger Global recognized this early. An initial

That

In India's tax system, when you realize gains on investments, those gains are subject to capital gains tax. The rate depends on how long you held the asset and what category it falls into. For investments held for more than two years, there's "long-term capital gains tax." Depending on the structure and timing, rates can range from 10% to 20% or higher.

On gains of roughly

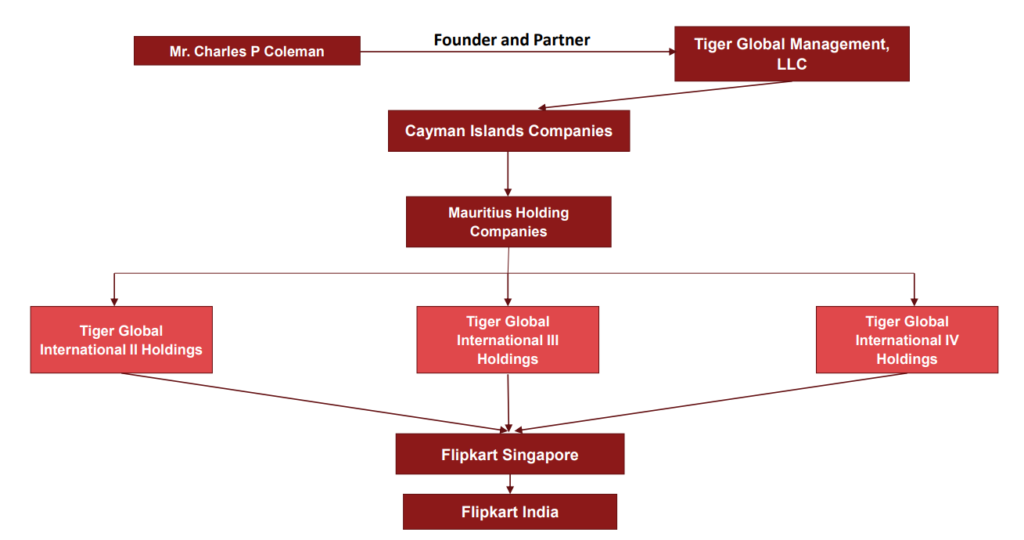

But Tiger Global had structured its Flipkart investment through Mauritius-based entities. This wasn't accidental. The structure was deliberate, and it was based on a legitimate tax treaty between India and Mauritius designed to promote investment between the two countries. Under that treaty, certain capital gains realized by Mauritius residents on the sale of shares in Indian companies are exempted from Indian tax.

The theory was clean. Tiger Global's Mauritius entities would claim treaty protection, argue that the gains qualified for exemption under a "grandfathering" clause protecting investments made before April 1, 2017, and therefore no Indian tax would be due. The fund would request a no-tax-withholding certificate from Indian authorities, complete the transaction, and pocket the full proceeds.

It's exactly how hundreds of similar deals have been structured. For decades, it's been the standard playbook.

Then Indian tax authorities said: No.

Tiger Global's initial

The Tax Authority's Challenge: Substance Over Form

In 2020, the Indian Authority for Advance Rulings (AAR) rejected Tiger Global's request for tax-withholding relief. The authority's reasoning was direct: the offshore structure appeared designed primarily to avoid Indian income tax. Therefore, it didn't qualify for treaty protection.

This is where the case gets interesting from a tax policy perspective.

The AAR didn't argue that Tiger Global violated any law. It didn't claim the fund committed fraud. Instead, it applied a principle that's becoming increasingly central to global tax enforcement: substance-over-form analysis. The principle is simple in theory but profound in practice. When evaluating whether a tax structure qualifies for preferential treatment, authorities should look at the economic substance of the transaction, not just its legal form.

In other words: Does this structure serve a legitimate business purpose beyond tax savings? Or is it engineered primarily to reduce tax liability?

For treaty structures, this is particularly important. Tax treaties are negotiated between countries specifically to encourage investment and commerce. They're not meant to be used as mechanisms to eliminate tax entirely where the underlying activity generates real economic value in a treaty country.

Let's think about this concretely. Imagine two scenarios:

Scenario 1: A Mauritius-based fund invests in Flipkart because it genuinely believes in Indian e-commerce and wants exposure to India's consumer growth story. It partners with local investors, contributes expertise, and maintains meaningful presence in the market. When it exits profitably, it's reasonable that treaty protection might apply because the investment created real economic value in India.

Scenario 2: The same fund invests in Flipkart because it's a high-return opportunity, but it structures the investment through Mauritius for no reason other than tax optimization. The Mauritius entity isn't a real operating entity. It exists purely to claim treaty benefits. When exiting, the fund's primary motivation is minimizing tax, not realizing legitimate investment returns.

The distinction seems obvious in theory. But in practice, it's rarely that clear. Most sophisticated investments fall somewhere in the middle.

Tiger Global's structure was sophisticated enough that for four years, from 2020 to 2024, the Delhi High Court actually agreed with the fund. In 2024, the Delhi High Court overturned the AAR's original decision, ruling in Tiger Global's favor. The court suggested that Tiger Global's Mauritius entities did have some substance beyond pure tax optimization.

But then the Indian Supreme Court intervened.

The Supreme Court's Sovereignty Argument: A New Framework

What makes the Supreme Court's ruling significant isn't just the outcome. It's the reasoning.

The two-judge bench framed the dispute explicitly around national sovereignty. Here's the key language from the judgment: "Taxing an income arising out of its own country is an inherent sovereign right of that country. Any dilution of this power through artificial arrangements is a direct threat to its sovereignty and long-term national interest."

That language is remarkable. It shifts the discussion from technical tax law into constitutional territory.

When courts frame issues in terms of national sovereignty, they're not just resolving a single dispute. They're establishing a principle that will guide future cases. The bench is saying: Indian courts will interpret tax law in ways that protect India's sovereign right to tax income generated within its borders. When structures appear designed to dilute that authority, courts should be skeptical.

This has implications far beyond Tiger Global's Flipkart exit.

Think about what this means for future deals. Global funds investing in Indian companies will now face an uncomfortable calculus. If they structure investments through offshore entities to claim treaty benefits, they risk having those benefits challenged. The burden effectively shifts. Rather than tax authorities needing to prove the structure is illegitimate, investors essentially need to prove it's legitimate.

The court also explicitly rejected the idea that an advance-ruling mechanism can be used to seek protection for structures that appear designed to avoid tax. Advance rulings are procedures where taxpayers can get pre-approval for how a transaction will be taxed. Normally, if you get an advance ruling, you're protected—you can proceed knowing your tax treatment in advance.

But the Supreme Court said: If a transaction appears designed primarily to avoid tax, the advance-ruling process itself cannot be used to legitimize it.

This is subtle but consequential. It removes a pathway that sophisticated investors have used to gain certainty about aggressive tax positions.

The increase in assumed Indian tax rate from 5% to 20% significantly reduces expected returns on a

Why This Matters: The Broader Implications for Global Investment Structures

Okay, so a sophisticated hedge fund lost a tax case in India. Why should anyone outside the tax advisory world care?

Because this case signals something fundamental about how high-growth emerging markets are thinking about foreign investment, tax policy, and economic sovereignty.

For decades, the global investment playbook has relied on tax optimization as a core feature. When funds invest in emerging markets, they structure those investments through low-tax jurisdictions to minimize tax friction on exit. The logic made economic sense: emerging markets need foreign capital, so they negotiate tax treaties that offer preferential treatment. Investors use those treaties as designed.

But India's Supreme Court is suggesting the game has changed.

India is in a unique position. It's the world's most populous country. It has a young, growing workforce. Its startup ecosystem is producing world-class companies at scale. For any global investor with serious ambitions, India is non-negotiable.

Exactly because India is so valuable, and because capital flows into India are so significant, the country's government is reconsidering its tax approach. The fundamental question is: Why should India allow foreign investors to structure deals in ways that minimize India's tax take on profits generated by Indian companies and Indian workers?

Tiger Global's loss suggests India's judiciary is aligned with this question.

Consider the scale. If Tiger Global had successfully claimed treaty relief, it would have avoided perhaps $30-50 million in Indian tax on a transaction worth billions. That's not unusual. Hundreds of similar transactions structure investments through offshore entities, many achieving tax optimization that produces similar savings.

Multiply that across thousands of transactions and billions in foreign investment, and you're talking about tens of billions in tax that India forgoes annually.

For a developing country trying to fund infrastructure, education, and healthcare, that's a genuine economic priority. The Indian government is explicitly signaling that it intends to be more aggressive about collecting tax on gains from Indian investments.

Treaty-Routing and Its Evolution

Tiger Global's strategy relied on what's called "treaty-routing." It's not a technical term of art, but it captures an important concept: structuring investments to route them through a treaty jurisdiction to access preferential tax treatment.

Treaty-routing isn't inherently illegal. Tax treaties explicitly permit investors from one treaty country to claim benefits when investing in another. But over the last decade, there's been a global shift in how countries view aggressive treaty-routing.

The shift started with the OECD's Base Erosion and Profit Shifting (BEPS) initiative, launched in 2015. BEPS was an explicit recognition that countries were losing enormous tax revenue because multinational companies were using treaty structures and other mechanisms to route profits to low-tax jurisdictions.

Out of BEPS came several key principles. One is the "Principal Purpose Test," which essentially states that treaty benefits should be available only if the principal purpose of an arrangement is not to obtain treaty benefits. Sounds circular, but it's powerful in practice. It means you can't structure a deal with treaty optimization as the primary goal.

India is increasingly applying these BEPS principles. The Supreme Court's language about structures designed "primarily to dilute" India's taxing authority echoes BEPS logic.

What's significant is that India is doing this through its courts, not just through tax administration. The Supreme Court's ruling suggests courts will apply principle-based reasoning to strike down aggressive treaty-routing structures.

For global investors, this is a major change. You can't rely on technical legal structures anymore. Courts will look at economic substance.

The 2024 Delhi High Court Ruling: Why It Mattered and Why It Didn't

Before the Supreme Court intervened, Tiger Global actually won. In 2024, the Delhi High Court ruled in the fund's favor, overturning the 2020 Authority for Advance Rulings decision.

The Delhi High Court's reasoning was more traditional. It looked at the specific structure Tiger Global created and found that the Mauritius entities had some economic substance beyond pure tax avoidance. The court seemed to accept that treaty protection could apply.

For Tiger Global and other investors, that ruling provided hope. It suggested that well-structured offshore arrangements could still claim treaty benefits, provided they had some legitimate business rationale.

That hope lasted less than a year.

The Supreme Court's decision to overturn the Delhi High Court ruling and back the tax authority is noteworthy because India's Supreme Court doesn't typically intervene in technical tax cases. Allowing the Delhi High Court ruling to stand would have been the normal course.

The fact that the Supreme Court chose to reverse suggests the court viewed this as raising issues of fundamental constitutional importance around national sovereignty. When courts do that, it's a signal that the issue transcends technical tax law.

For global investors, the lesson is clear: Don't assume a favorable ruling at a lower court level will stick if higher courts think you're challenging the government's core taxing authority.

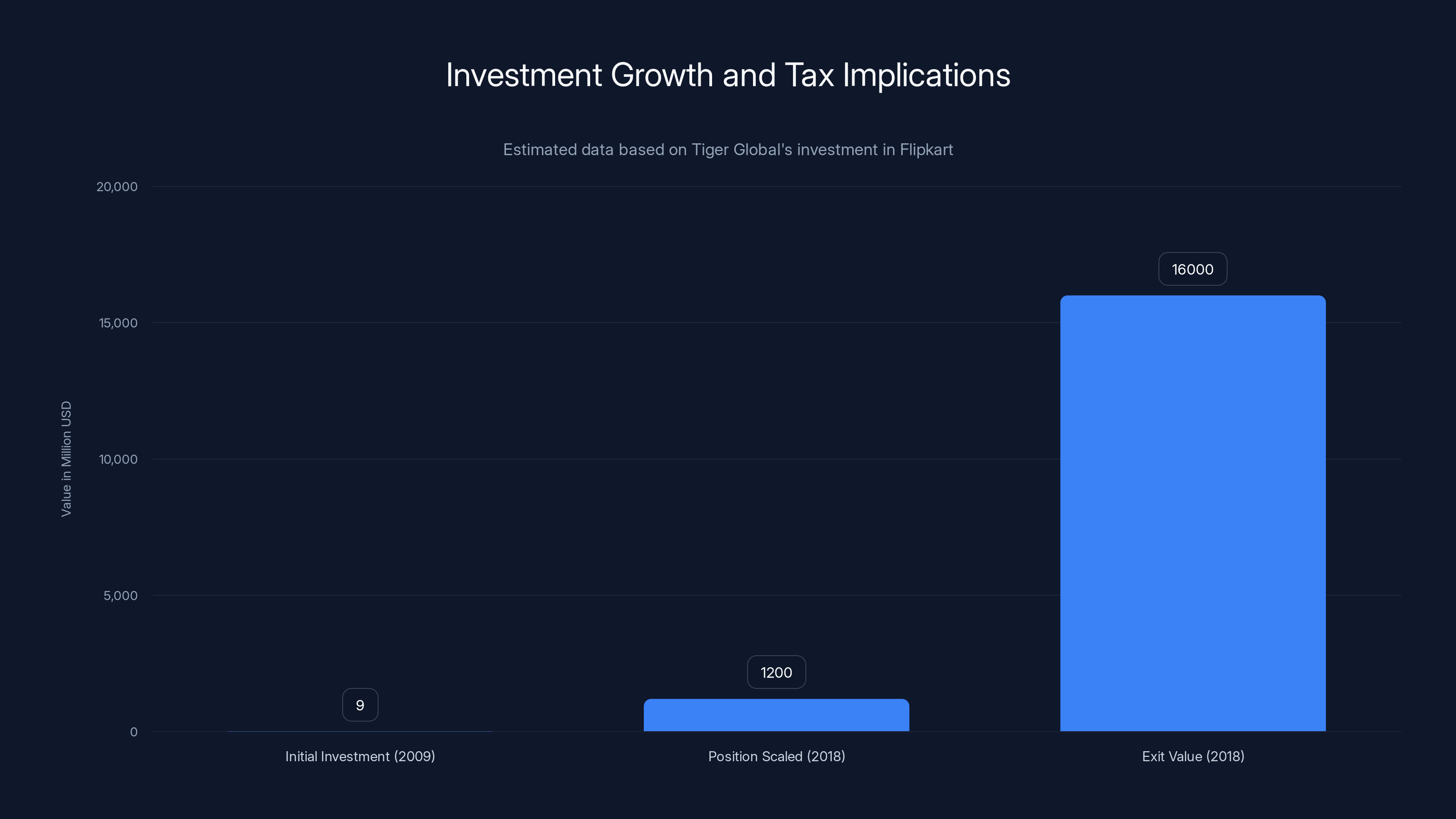

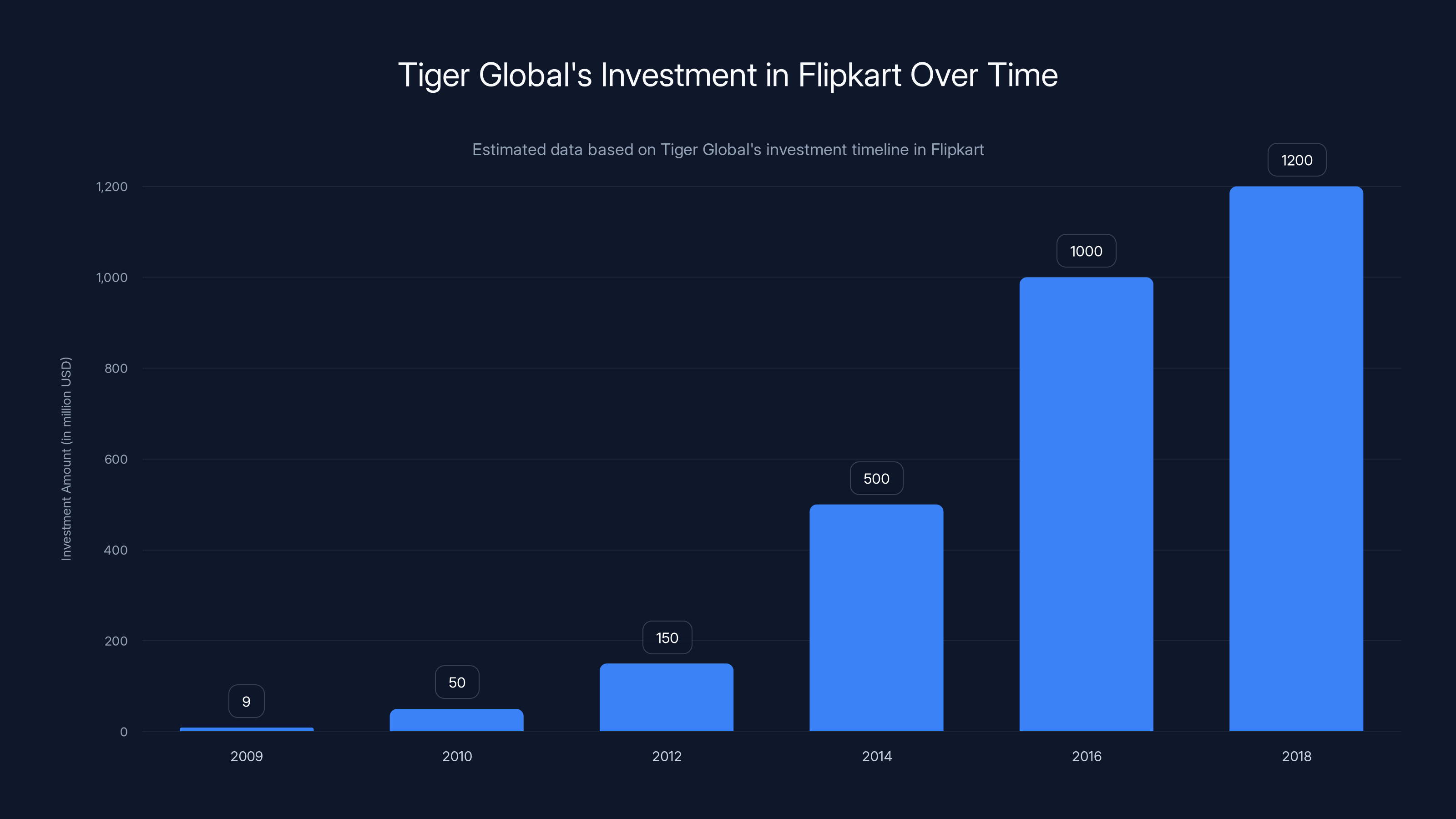

Estimated data showing Tiger Global's investment growth in Flipkart from an initial

The Grandfathering Question: Timing and Transition

One element of Tiger Global's argument relied on a "grandfathering" clause. India implemented new capital gains tax rules effective April 1, 2017. For investments made before that date, India's tax treaty with Mauritius appeared to provide exemption for gains.

Tiger Global had invested in Flipkart well before April 1, 2017, so it argued it qualified for grandfathering.

This is a legitimate argument in theory. Governments often grandfather existing arrangements when introducing new tax rules, precisely to avoid disrupting established investments.

But the Supreme Court essentially said: Grandfathering doesn't matter if the structure itself appears designed to avoid tax.

The court's logic is: You can't grandfather something that was never legitimate to begin with.

This is particularly important because it suggests Indian courts will apply substance-over-form analysis even to transition provisions. In other words, the date of the investment doesn't protect an aggressive structure.

For investors with pre-April 2017 investments, that's concerning. It suggests that even if a structure qualified for tax benefits when it was established, courts reserve the right to revisit that qualification if the structure appears primarily motivated by tax avoidance.

Cross-Border M&A and Deal Structuring: New Uncertainty

The Tiger Global case has immediate implications for how cross-border M&A deals get structured in India.

When a global fund invests in an Indian company with the intention of exiting through an acquisition, the exit structure becomes a critical element of the investment decision. Fund managers model returns by projecting what the exit price might be and what taxes might apply.

Tiger Global likely structured its Flipkart investment with specific assumptions about Indian tax liability. Those assumptions were based on industry practice, prior precedent, and advice from tax advisors.

All of that changed with the Supreme Court ruling.

Now, deal teams at global funds need to assume higher Indian tax risk on exits. That means lower expected returns. Which means deals that looked attractive before might not look attractive now.

Consider the math: Assume a fund expects to make a

For a fund making allocation decisions across geographies, that kind of risk premium shift could actually redirect capital away from India to other high-growth markets that offer more predictable tax treatment.

Which, perversely, might not be what India's government actually wants. India wants foreign capital. The government benefits from that capital because it funds innovation, creates jobs, and builds the country's technology ecosystem.

But if foreign investors face substantially higher tax risk on exits, they might reduce their India allocation. That's a genuine tradeoff policymakers face.

Substance-Over-Form: The Permanent Shift in Tax Enforcement

The Supreme Court's decision reflects a global trend toward substance-over-form analysis in tax enforcement.

For decades, tax law worked differently. You could structure a transaction with specific legal forms. If the legal form qualified for certain tax treatment, you got that treatment. Substance didn't matter as much.

But over the last fifteen years, that's changed fundamentally. The OECD's BEPS initiative, multilateral conventions, and domestic tax reforms across developed economies all moved toward substance-over-form reasoning.

India is importing this logic.

Under substance-over-form analysis, courts ask: What's the economic reality here? Does the structure serve legitimate business purposes? Or is it engineered primarily to access tax benefits?

When courts apply this standard, structures that look fine under old legal analysis can get struck down.

For sophisticated investors, this is a permanent shift. You can't rely on technical legal form anymore. You need genuine economic substance.

What does that mean practically? It means:

- Offshore entities holding Indian investments need to have real operations, real decision-making, real economic activity. Not paper entities serving purely for tax purposes.

- The primary motivation for a structure needs to be business rationale, not tax optimization. If tax savings are the primary motivation, courts will scrutinize heavily.

- Transaction documentation needs to reflect legitimate business purposes. If internal emails reveal the structure was designed purely for tax savings, that kills the case.

- Timing matters. Structures implemented specifically to react to tax law changes look suspicious.

None of this means global funds can't invest in India. It means they need to think more carefully about how they structure those investments.

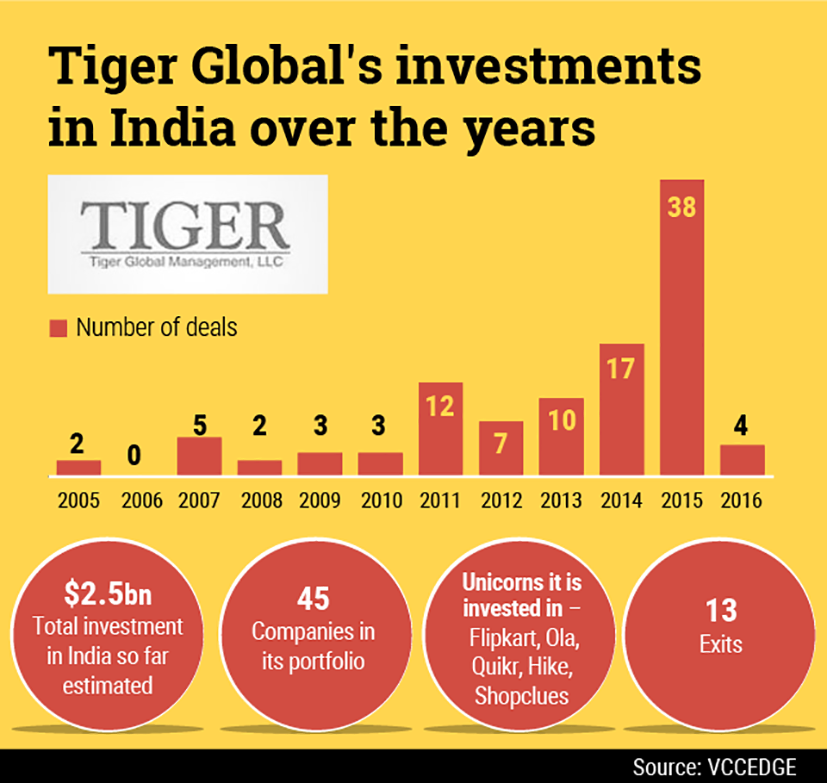

Tiger Global's investment in Flipkart grew from an initial

Other Offshore Jurisdictions in the Crosshairs

One reason this case attracted such global attention is that it's not really about Mauritius specifically. It's about a broader pattern.

For years, certain jurisdictions became known as "tax-treaty hubs." Mauritius is one. So is the Netherlands. Singapore is another. Luxembourg. Ireland. These are countries that have negotiated broad tax treaties and offer low corporate tax rates, making them attractive as intermediate holding locations for global investment structures.

The logic is straightforward: Route your investment through one of these jurisdictions, access treaty benefits, and minimize your tax exposure in the destination country.

But countries are increasingly saying: We're not going to let that happen.

India's case against Tiger Global is one high-profile example. But similar challenges are happening in other markets.

Mexico challenged treaty structures. Brazil is doing the same. Even developed markets like the US are scrutinizing treaty-routing more carefully.

When courts in major markets start disallowing treaty benefits for aggressive structures, it cascades. Fund managers looking at Indian deals start assuming higher tax risk. That assumption changes how they structure deals across the board.

For Mauritius and other treaty-hub jurisdictions, that's concerning. Their value proposition depends on being recognized as legitimate intermediate holding points. If major investment destinations start routinely denying treaty benefits, the value proposition erodes.

Investor Sentiment and Capital Flows: Real Impacts

Here's where this case moves from tax technicality into real economic impact.

Global investment funds make allocation decisions based partly on expected return, and expected return depends on tax assumptions. If India suddenly becomes a higher-tax jurisdiction for offshore investors, some capital will flow elsewhere.

We're unlikely to see dramatic capital flight from India. The country's growth fundamentals are too compelling. But we might see more conservative allocations. We might see fewer mega-rounds in Indian startups. We might see more Indian founders shifting incorporation to Singapore or other jurisdictions with more predictable tax treatment.

In other words, Tiger Global's loss could ripple through India's entire startup ecosystem.

Tiger Global itself has deployed over $3 billion in Indian companies and may continue to do so, but on different terms. Fund managers will likely demand higher ownership percentages or clearer control rights to offset the increased tax risk. That changes negotiation dynamics between founders and investors.

For Indian entrepreneurs, this could be negative. Higher tax uncertainty for foreign investors means less competitive capital markets and potentially less favorable terms.

Which, again, might not be what India's government intends. The government wants a thriving startup ecosystem. Aggressive tax challenges against foreign investors might feel good politically but create unintended consequences.

How Other Countries Have Handled Similar Situations

India's approach isn't unique, but the extremity matters.

Australia's tax authority has aggressively challenged offshore treaty structures, particularly involving treaty hubs. Over the last decade, Australia collected billions in additional tax from multinational companies adjusting their structures to avoid Australian tax. But Australia did this through administrative action and guidance documents, not through Supreme Court decisions invalidating entire classes of structures.

The UK scrutinizes treaty-routing structures but generally allows them if they have legitimate business substance.

Canada's courts have applied substance-over-form analysis but somewhat inconsistently.

The US applies strict rules through its tax code, particularly around foreign investment corporations and passive foreign investment companies.

What's notable about India's Supreme Court approach is its constitutional framing. By grounding the decision in national sovereignty rather than technical tax principles, the court is suggesting future courts will apply even stricter scrutiny.

Compare that to Australia or the UK, where courts have generally been more restrained in invalidating structures that technically comply with tax law.

India's approach is more aggressive.

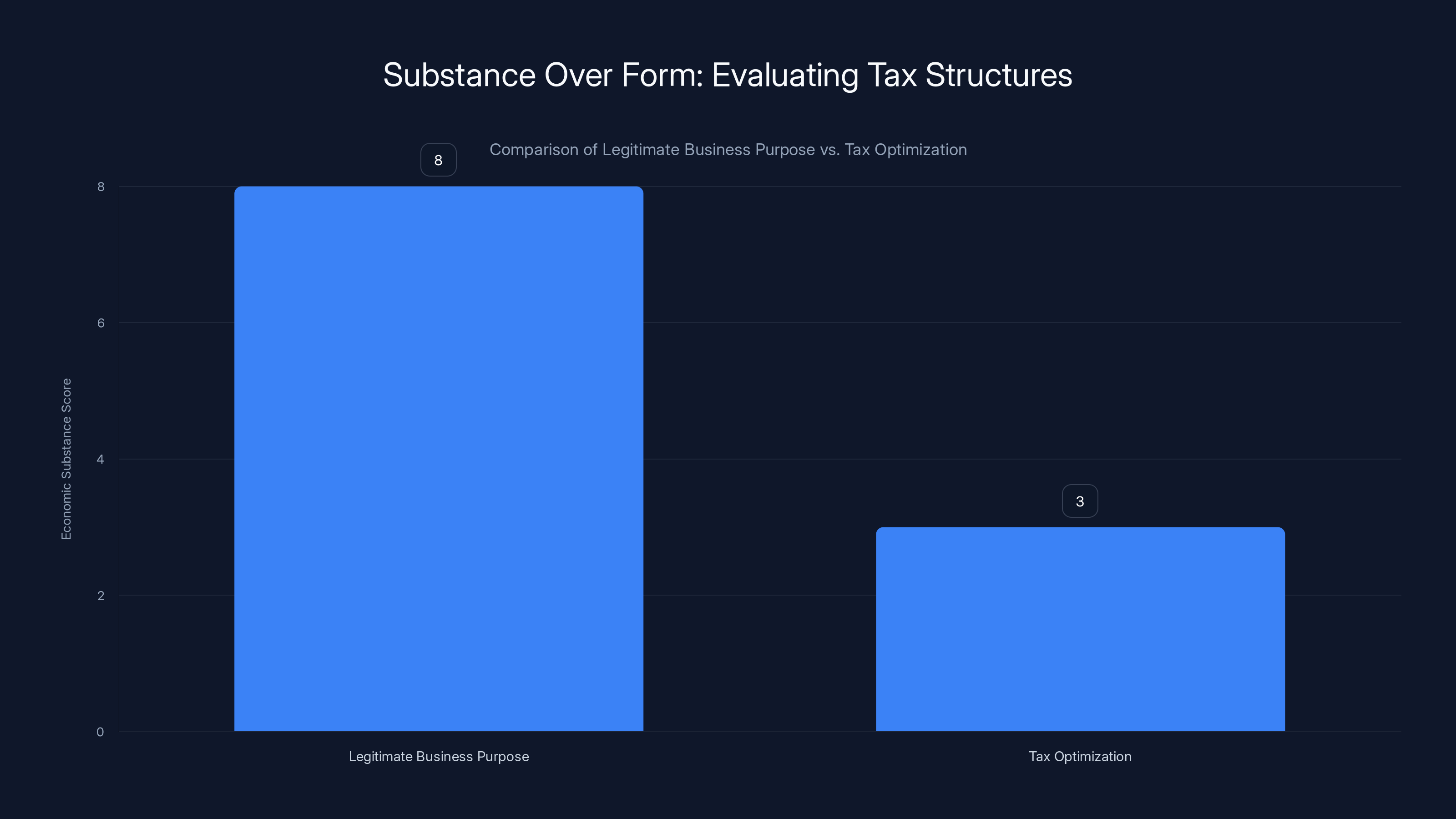

Investments with a legitimate business purpose score higher in economic substance, aligning with treaty intentions. Estimated data based on typical tax authority evaluations.

Compliance and Restructuring: What Existing Investors Need to Do

For global funds that already hold Indian investments through offshore structures similar to Tiger Global's, this ruling creates some uncomfortable questions.

The good news is that Tiger Global's case is specifically about exits. If you hold the investment and don't trigger the realization event, you don't immediately face tax. The bad news is that when you do exit, you might face challenges similar to what Tiger Global experienced.

Some funds are likely considering proactive restructuring. Rather than waiting for a tax authority challenge at exit, they're thinking about modifying their structures now.

What might that look like? A few options:

First, some funds might shift investments to operate through Indian entities rather than offshore entities. This eliminates the treaty-routing question entirely because Indian entities are subject to Indian tax anyway. The downside is loss of tax treaty benefits.

Second, some funds might establish meaningful economic substance in their treaty-jurisdiction entities. If the Mauritius entity actually has employees, makes investment decisions, and conducts real business operations related to the Indian portfolio, substance-over-form analysis becomes less damaging.

Third, some funds might hold assets longer to demonstrate that the investment was long-term conviction rather than short-term tax optimization. If you can show you held the asset for ten years because you believed in the company, not to manipulate tax, courts might be more sympathetic.

None of these options is particularly attractive. Restructuring costs money. Operating real entities costs money. Holding assets longer delays exits and return realization.

But those costs might be lower than losing tax disputes.

The Role of Tax Advisors and Reputational Risk

When Tiger Global structured its Flipkart investment, it almost certainly relied on advice from major tax advisory firms. These firms likely provided opinions that the structure qualified for treaty relief.

Those opinions now look wrong.

For the tax advisory industry, this creates reputational risks. If their advice structures are being systematically invalidated by courts, clients lose confidence.

We might see tax advisory firms becoming more conservative about what structures they'll support. That means fewer aggressive tax optimization strategies. Which could create a second-order effect: global investors have fewer options for tax-efficient structuring, making investing in India even less attractive.

It's a feedback loop that could reduce capital flows beyond what the tax case itself would suggest.

Future Supreme Court Cases: Anticipating the Next Test

Tiger Global is unlikely to be the last case testing whether India will enforce aggressive treaty-routing structures.

There are hundreds of similar structures out there. When other funds exit Indian investments, they might face similar challenges. The next case could involve different treaty jurisdictions, different companies, or different time periods.

Each new case gives the courts another opportunity to refine and tighten the rules. The trend will almost certainly be toward stricter enforcement.

Funds should expect that Indian tax authorities will become more aggressive in challenging treaty structures across the board. The Supreme Court has essentially blessed that aggressiveness by framing it as protecting national sovereignty.

What might the next test case look like? Perhaps a fund trying to claim treaty benefits for a structure where the offshore entity explicitly exists only for tax purposes. Or a structure where internal documents reveal the motivation was pure tax optimization. Or a case involving a different treaty jurisdiction that hasn't been tested yet.

Each case will likely produce rulings that further restrict treaty-routing opportunities.

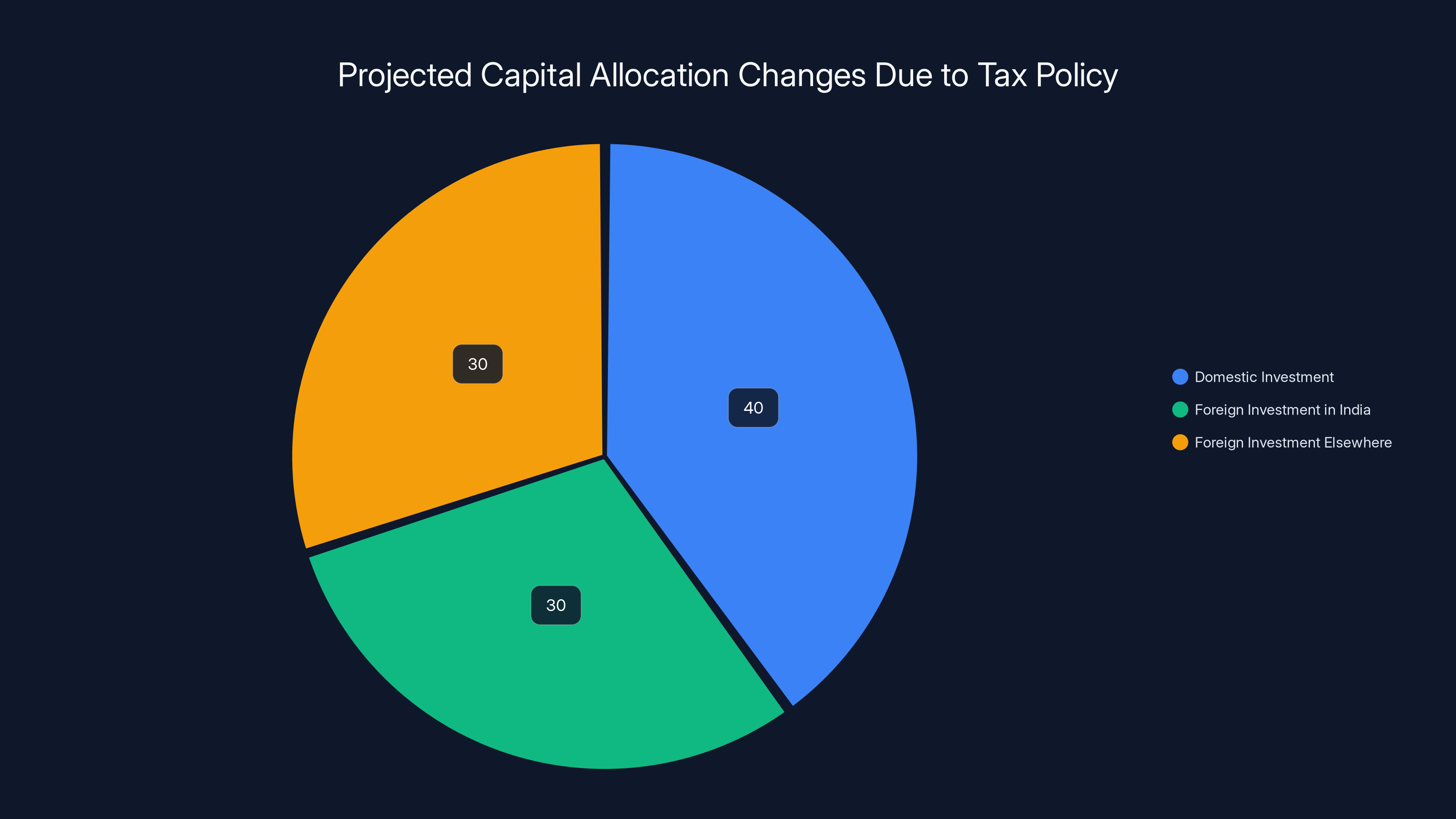

Estimated data shows potential shifts in capital allocation due to tax policy changes, with a possible decrease in foreign investment in India.

The Broader Conversation: National Sovereignty vs. Treaty Benefits

Tiger Global's loss forces a genuine policy question: How should countries balance the desire to attract foreign investment against the right to tax income generated within their borders?

There's a real tension here.

On one hand, countries negotiate tax treaties specifically to promote investment. Lower tax uncertainty should theoretically attract more capital.

On the other hand, why should countries deliberately tax themselves out of revenue when that revenue could fund development priorities?

Developing countries especially face that tension acutely. India needs tax revenue more urgently than most developed countries. But India also needs foreign capital to fund its startup ecosystem and technology sector.

Tiger Global's loss tips the balance decisively toward protecting India's taxing authority. The question is whether that's the right balance.

Economically, the loss might be negative. Higher tax risk could reduce capital flows and slow Indian growth. Politically, it might be positive—Indian taxpayers and policymakers might prefer that foreign investors pay meaningful tax on their profits.

How this tension resolves will shape India's investment environment for decades.

Implications for Mauritius and Small Treaty Jurisdictions

One major implication of this case is for Mauritius itself.

Mauritius's entire economic model, to some degree, depends on being a recognized intermediate jurisdiction for global investment structures. If major investment destinations like India routinely deny treaty benefits that investors are trying to claim, Mauritius's value proposition diminishes.

We're unlikely to see Mauritius collapse as a financial center. But we might see it become less central to global investment structures.

Moreover, Mauritius's relationship with India could deteriorate. India might become more skeptical of the India-Mauritius tax treaty itself, potentially seeking to renegotiate its terms.

For other small treaty jurisdictions with similar models (Netherlands, Luxembourg, Singapore), this case is a warning. If courts in major investment destinations start systematically invalidating treaty structures, the entire premise of these jurisdictions shifts.

Precedent and the Doctrine of Stare Decisis

One important question is whether the Tiger Global ruling is binding on lower courts in future cases.

In India's legal system, Supreme Court rulings are binding on lower courts. So the Delhi High Court and other appellate courts must follow the principles laid out in Tiger Global when they decide similar cases.

That doesn't mean every future case reaches the same outcome. Different facts might support different conclusions. But the legal framework established by Tiger Global will guide all subsequent decisions.

What was the framework? Essentially: When a transaction appears designed primarily to avoid tax, courts should be skeptical of treaty protection claims, particularly if those claims threaten a country's core taxing authority.

That's a fairly broad framework. It gives courts significant discretion to strike down structures that feel aggressive.

Future cases will likely narrow or refine this framework. But it will remain the governing principle for treaty-routing cases in India.

The Path Forward: Options for Investors

For global investors with Indian exposure, what's the right response to this ruling?

There's no one-size-fits-all answer, but a few principles seem clear:

First, don't assume historical tax treatments will remain available. Just because similar structures worked for prior exits doesn't mean future exits will have the same tax treatment. Courts are explicitly overruling past practice.

Second, ensure genuine economic substance in any offshore structures. Don't create paper entities. If you're using a Mauritius entity as an intermediate holding company, make sure it has real operations and real decision-making.

Third, model higher tax risk in your return assumptions. Don't assume you'll win treaty battles. Assume you might lose and need to pay substantial tax on exits.

Fourth, consider the full range of structuring options. That might include Indian entities, dual-hold structures, or other approaches that don't depend on treaty optimization.

Fifth, engage early with tax authorities and advisors. Don't wait until you're at the exit door to get clarity on tax treatment. Seek advance rulings, get official guidance, and create documentation showing legitimate business purposes.

None of these options is free or frictionless. But they're better than the alternative, which is discovering at exit that your tax structure doesn't work.

Conclusion: A Watershed Moment in Emerging Market Taxation

Tiger Global's loss in India's Supreme Court marks a genuine watershed moment. It's not just about one fund and one investment. It's about how high-growth emerging markets are fundamentally reframing their relationship with foreign capital and tax optimization.

For decades, the playbook was clear: Invest through offshore entities, access treaty benefits, minimize tax on exit. It worked because countries negotiated treaties that enabled it, and courts respected those treaties.

That playbook is breaking down.

India's Supreme Court explicitly grounded its reasoning in national sovereignty. That language matters. It signals that courts will construe tax law in ways that protect a country's fundamental right to tax income generated within its borders. When structures appear designed to dilute that right, courts will strike them down.

This matters because India isn't alone. Other high-growth emerging markets are applying similar logic. The global investment environment is shifting toward more aggressive tax enforcement.

For global funds, that shift requires rethinking how they structure investments. It means assuming higher tax risk, incorporating more genuine economic substance, and being more conservative about treaty optimization.

For India, the shift offers both opportunities and risks. Opportunity: India can capture more tax revenue from foreign investors, funding development priorities. Risk: Higher tax uncertainty might reduce capital flows and slow growth in the startup ecosystem.

The Supreme Court's decision suggests India's government believes the opportunity outweighs the risk. We'll see if that judgment proves correct as capital flows and deal-making patterns respond.

One thing is certain: The offshore playbook that worked for Tiger Global for over a decade is fundamentally disrupted. What replaces it will shape how global investors approach India—and by extension, emerging market investing more broadly—for the next decade.

FAQ

What was Tiger Global's original investment in Flipkart?

Tiger Global made an initial

How did Tiger Global structure its investment to minimize taxes?

Tiger Global structured its Flipkart investment through Mauritius-based entities to claim protection under the India-Mauritius tax treaty, attempting to avoid capital gains tax on profits realized during Walmart's 2018 acquisition by leveraging grandfathering provisions that supposedly exempted pre-April 2017 investments.

What is treaty-routing and why is it significant?

Treaty-routing involves structuring investments to pass through jurisdictions with favorable tax treaties to access preferential tax treatment. It's significant because the Supreme Court's decision signals courts will scrutinize these structures for economic substance rather than accepting them based purely on legal form.

Why did the Supreme Court frame this as a sovereignty issue?

The Supreme Court explicitly grounded its decision in national sovereignty, arguing that a country's fundamental right to tax income generated within its borders cannot be diluted through "artificial arrangements." This framing elevates the case beyond tax law into constitutional territory and suggests future courts will apply stricter scrutiny.

What is the "substance-over-form" principle in tax law?

The substance-over-form principle requires that when evaluating tax structures, courts and authorities look at the economic reality and legitimate business purposes behind the arrangement rather than simply accepting its legal form. If a structure's primary purpose appears to be tax avoidance rather than legitimate business activity, it can be disallowed even if technically compliant with tax law.

How might this ruling affect other global investors in India?

The ruling creates higher tax uncertainty for offshore investors, potentially increasing modeled tax risks on exits and reducing expected returns. This may prompt some funds to restructure existing holdings, demand higher ownership stakes to compensate for tax risk, or reduce allocation to India in favor of markets with more predictable tax treatment.

Can Tiger Global appeal or seek review of the Supreme Court decision?

Tiger Global can technically petition for a review of the verdict, but such petitions are rarely successful in India's legal system. The Supreme Court's decision effectively establishes binding precedent that will guide lower courts in future treaty-routing cases.

What does this mean for investments made before April 1, 2017?

While India's tax rules included grandfathering protections for pre-April 2017 investments, the Supreme Court suggested that grandfathering doesn't protect structures that appear designed primarily to avoid tax. The timing of the investment doesn't necessarily shield an aggressive structure if its substance is questioned.

How will this impact Mauritius as a financial center?

The ruling potentially diminishes Mauritius's attractiveness as an intermediate jurisdiction for Indian investment structures. If major investment destinations routinely deny treaty benefits that investors have traditionally claimed through Mauritius entities, the value proposition of the jurisdiction erodes significantly.

What should global investors do now to protect themselves?

Global investors should model higher tax risk in return assumptions, ensure genuine economic substance in any offshore structures rather than creating paper entities, seek advance rulings and official guidance early, consider restructuring options, and engage with tax advisors proactively rather than waiting until exit to address tax treatment questions.

Key Takeaways

- India's Supreme Court ruled against Tiger Global, disallowing treaty benefits for offshore investment structures that appear designed primarily to avoid tax, reshaping the entire offshore playbook

- The court framed the issue around national sovereignty, suggesting future rulings will prioritize India's fundamental taxing authority over technical treaty interpretations

- The substance-over-form principle now dominates Indian tax enforcement, requiring that investments demonstrate genuine economic substance and legitimate business purposes beyond tax optimization

- Global investors must assume higher tax risk on Indian exits and recalibrate return models, potentially reducing capital flows to India despite its strong growth fundamentals

- Similar aggressive enforcement patterns are emerging across emerging markets, suggesting this case reflects a permanent shift in how developing countries approach foreign investment taxation