What CIOs Are Most Looking to Replace with AI Today | SaaStr

The question every B2B exec should be asking right now is not whether CIOs are looking to replace software with AI. They are. The question is which software,...

TechnologyInnovationBest PracticesGuideTutorial

Listen to Article

0:00

0:00

0:00

What CIOs Are Most Looking to Replace with AI Today | Saa Str

Overview

Free e Books

e Book: Hiring a Great VP of Sales

e Book: Raising Capital

e Book: The First $1m ARR

University

All Posts

University

Podcasts

The Top CROs

VC Fundraising

Top Videos

Q&A

Best of Saa Str

#1 Bestselling Book

Search Everything

Join the Community

Details

Free e Books

e Book: Hiring a Great VP of Sales

e Book: Raising Capital

e Book: The First $1m ARR

London 2025

Annual 2026

Events Overview

Sponsors

Event Sponsorship

Media Sponsorship

Digital AI Day 2025 (Free)

Speaker Submissions

Speaker Requirements

Overview

What CIOs Are Most Looking to Replace with AI Today

by Jason Lemkin | Artificial Intelligence (AI), Blog Posts, Saa Str. Ai

The question every B2B exec should be asking right now is not whether CIOs are looking to replace software with AI. They are. The question is which software, and how fast.

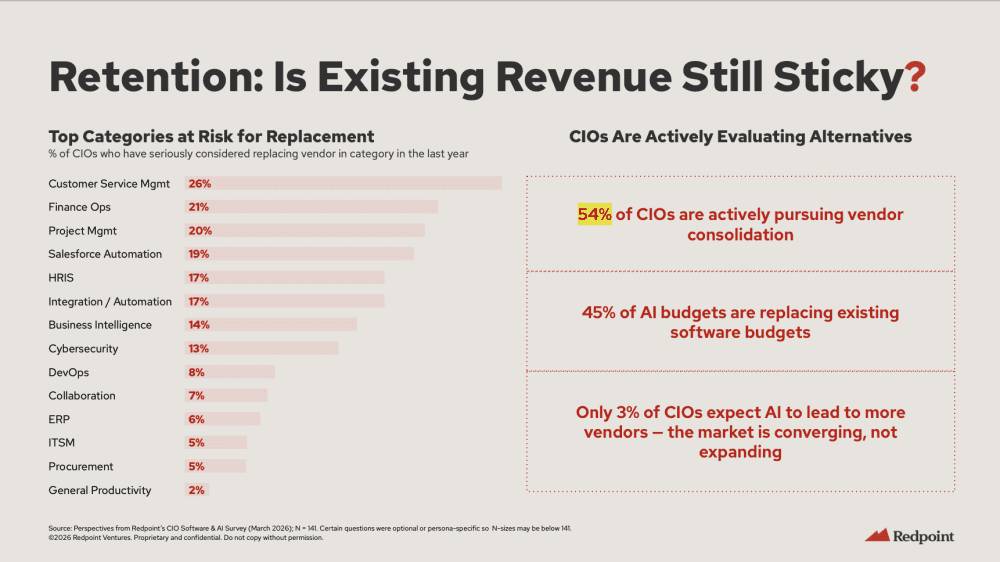

Redpoint surveyed 141 CIOs in March 2026 and asked a direct question: in which software categories have you seriously considered replacing your current vendor in the last year? The answers tell you where the real displacement pressure is building, and where incumbents are safer than the headlines suggest.

The Category Rankings: Where CIOs Are Actually Looking to Switch

Here is the full list, ranked by the percentage of CIOs who have seriously considered replacing their vendor in that category over the last twelve months:

Customer service management is the most vulnerable category by a meaningful margin.

One in four CIOs has seriously considered replacing their customer service vendor in the last year. This tracks with what is happening in the market — AI-native customer support tools like Sierra, Decagon, and Fin/Intercom are winning real enterprise contracts against established players, and the ROI case for replacing human-assisted support workflows with AI agents is the most mature of any category right now. A separate Gartner survey of 321 customer service and support leaders conducted in October 2025 found that 91% are under pressure to implement AI in 2026, with nearly 80% planning to transition at least some frontline agents into new roles. That is not a category on the edge of disruption — it is a category in the middle of it.

The surprise on this list is how high Finance Ops sits at 21%.

Historically, finance software is sticky to the point of being immovable. CFOs do not like change, auditors demand consistency, and the integration requirements are brutal. But 21% of CIOs have seriously considered replacing their finance operations vendor. That is a signal worth paying attention to.

The core value proposition of most project management tools — tracking who is doing what and when — is precisely the coordination problem that AI agents solve natively. When an AI can assign tasks, update statuses, surface blockers, and draft status reports automatically, the case for paying per seat for a tool that humans manually update gets harder to make.

This may go a long way toward explaining what has happened to Atlassian and Monday.com in 2026. Both stocks have been among the hardest hit in the software selloff. The market is not just pricing in weaker near-term growth — it is pricing in the specific concern that the coordination and workflow visibility use case, which is the core of both products, is exactly what AI agents do for free on top of whatever system of record a company already runs. When 20% of CIOs have seriously considered replacing their project management vendor in the last twelve months, the terminal value question for seat-based project management tools becomes very hard to answer confidently.

General Productivity at 2% is the number that should give pause to anyone declaring that Microsoft 365 or Google Workspace is about to get disrupted. Two percent. CIOs are not going to rip out their productivity suites. The switching costs are too high, the integration surface area is too broad, and the incumbent AI features — Copilot, Gemini — give buyers a reason to stay.

Salesforce Automation at 19% is worth highlighting separately. A Recognize survey of over 200 US IT executives conducted in late 2025 found that 55% anticipate replacing some commercial software with AI-generated tools, and self-built CRMs and workflow automation platforms were the most commonly cited examples. CRM is not just at risk from AI-native startups like Attio. It is at risk from enterprises deciding to build their own.

The category-level data only makes sense in the context of three macro numbers from the same survey.

54% of CIOs are actively pursuing vendor consolidation. This is the most important number in the entire dataset. More than half of your enterprise customers are not just evaluating whether to switch vendors — they are running active programs to reduce the number of vendors they work with. The average enterprise runs over 130 Saa S applications and typically finds 20 to 30% redundancy when they look closely. That redundancy is now a budget line item under active review.

45% of AI budgets are replacing existing software budgets, not adding to them. This is the zero-sum problem. AI spending is not incremental for most enterprises right now. IT budget growth is decelerating to 3.4% in 2026 per a January survey of CIOs. The money going into AI tools is coming from somewhere, and almost half of CIOs say it is coming directly from existing software line items. When your customer buys a new AI tool, there is a nearly one-in-two chance they are canceling or reducing something else to pay for it.

Only 3% of CIOs expect AI to lead to more vendors. The market is converging. The era of buying a best-of-breed point solution for every workflow is ending. CIOs are making decisions today about which platforms they will consolidate around, and the vendors who do not make that short list face a structural demand compression problem regardless of how good their product is.

Looking at the data, there is a clear pattern to which categories are most at risk and which are not.

The high-risk categories share a common characteristic: their core value is coordination and workflow visibility. Customer service routing, project task management, sales activity tracking, integration orchestration — these are problems AI agents handle well. They do not require years of proprietary data to be useful. They can be replicated with relatively low switching cost once the decision is made. And the ROI case for replacing them with AI is easy to model. This maps precisely to what Gartner’s AI strategy team identified as the jobs most at risk from AI: service desk roles, business analysts, and project managers — specifically because those roles are workflow-heavy, with outputs that are tickets, documentation, and status templates. The software built to serve those jobs is just as exposed as the jobs themselves.

The protected categories share a different characteristic: deep integration with financial, compliance, or workforce data that took years to accumulate. ERP at 6% and General Productivity at 2% are not immune to AI disruption, but they are not going to be ripped out based on a demo. Redpoint’s framework is useful here: vertical software that owns years of proprietary, industry-specific data carries switching costs that are existential rather than cosmetic. You do not replace your ERP because you saw an impressive agent demo.

Collaboration at 7% is interesting. Despite years of predictions that Slack would get disrupted by AI-native tools, CIOs are not moving. This is consistent with the buy-versus-build math Redpoint laid out — replacing Slack for a 1,000-person company costs roughly

220Kperyear.Buildinganequivalentin−houseruns

2M or more annually, and you get an inferior product. The economics of displacing deeply embedded collaboration tools do not work even in an AI-native world.

The Incumbent Advantage Is Real, But Being Wasted

Here is the tension in this data. The same survey that shows 54% of CIOs pursuing vendor consolidation also shows that 61% of CIOs prefer investing in AI features from vendors they already use. When given the choice, most buyers would rather have their existing vendor add AI than switch to an AI-native alternative.

That incumbent advantage is real. But based on the feedback CIOs are giving in the market right now, many incumbents are squandering it. The verdict on Salesforce Agentforce from enterprise buyers is that it was oversold and underdelivered. Microsoft Copilot pricing — which effectively doubles an E3 license — has caused large enterprises to pause or pull back enterprise-wide rollouts. Service Now is perceived as expensive enough that buyers say they would not think twice about switching if a credible AI-native alternative appeared.

The implication for AI-native founders is that the window for attacking these categories is open precisely because incumbents have the relationship advantage but are not executing on AI fast enough to lock buyers in. That window is not permanent. Once a major incumbent ships a genuinely capable AI layer and prices it reasonably, the consolidation logic works against the new entrant, not the incumbent.

If your product competes in customer service management, project management, sales automation, or finance ops — the categories where 19% to 26% of CIOs are actively evaluating alternatives — you are operating in an environment where buyer intent to switch is at a multi-year high. That is genuinely good news for challengers. The question is whether you can close before buyers consolidate around a different platform.

The data on speed matters here. Enterprises that are seeing real proof points from AI are cutting experimentation budgets, rationalizing overlapping tools, and deploying savings into the AI technologies that have actually delivered. The consolidation decisions are being made now. A company that ran five pilots in 2025 is making its platform bets in 2026. Getting in front of buyers before those decisions are finalized is a different sales motion than the one most B2B companies ran two years ago.

If your product is in the bottom half of the list — collaboration, ERP, ITSM, general productivity — the displacement pressure is lower but the consolidation pressure is the same. Your risk is not that a buyer replaces you with an AI-native alternative. Your risk is that you get cut in a rationalization exercise because you are a redundant point solution that overlaps with a platform the buyer is doubling down on.

The categories with the lowest replacement risk are not safe from the consolidation wave. They are just safe from a different kind of disruption.

The enterprise software budget is contracting in real terms while AI spend is rising. The math means every dollar going to a new AI tool is taking a dollar from something that already exists. CIOs have told us which categories they are most willing to pull that dollar from.

Customer service software is the most contested category in enterprise right now. Finance ops and project management are more exposed than most people expected. ERP and general productivity are genuinely sticky.

And 54% of CIOs are running active consolidation programs, which means even categories that are not on the replacement list face meaningful churn risk simply from being the fourth or fifth tool in a category that a buyer decides to collapse into one.

Your VCs May Be Giving Up on You Right About Now. Don't Let That Stop You.

Your VCs May Be Giving Up on You Right About Now. Don't Let That Stop You.

RSS Industry News

Get from

0to

100 Million in ARR

with less stress and more success.

Key Takeaways

Free e Books

e Book: Hiring a Great VP of Sales

e Book: Raising Capital

e Book: The First $1m ARR

University

All Posts

University

Podcasts

The Top CROs

VC Fundraising

Top Videos

Q&A

Best of Saa Str

#1 Bestselling Book

Search Everything

Join the Community

Free e Books

e Book: Hiring a Great VP of Sales

e Book: Raising Capital

e Book: The First $1m ARR

London 2025

Annual 2026

Events Overview

Sponsors

Event Sponsorship

Media Sponsorship

Digital AI Day 2025 (Free)

Speaker Submissions

Speaker Requirements

Overview

Cut Costs with Runable

Cost savings are based on average monthly price per user for each app.

Which apps do you use?

Apps to replace

ChatGPT

$20 / month

Lovable

$25 / month

Gamma AI

$25 / month

HiggsField

$49 / month

Leonardo AI

$12 / month

TOTAL$131 / month

Runable price = $9 / month

Saves $122 / month

Runable can save upto $1464 per year compared to the non-enterprise price of your apps.