![Why Lego Pokémon Sets Are $200–$650: The Collapse of Toys for Kids [2025]](https://tryrunable.com/blog/why-lego-pok-mon-sets-are-200-650-the-collapse-of-toys-for-k/image-1-1769341025093.png)

The $650 Question: When Did Toys Stop Being for Kids?

Remember when Lego was the thing you could just buy for your kid's birthday? When a $40 set felt like a splurge? Those days are functionally over.

Last year, Lego announced a partnership with The Pokémon Company that felt inevitable. Two cultural juggernauts colliding in a shower of nostalgia and commerce. The 30th anniversary of Pokémon was coming up in 2026. The timing was perfect. The execution? That's where things get weird.

When Lego unveiled the actual Pokémon sets in 2025, it became immediately clear: this collaboration wasn't designed for anyone under 18. Not a single set aimed at kids. Not one. Instead, the company launched three products with a single target audience: adult collectors with disposable income.

The entry point? A 587-piece Eevee model for

Six. Hundred. And fifty. Dollars. For plastic bricks.

Here's what made it worse. Lego bundled an exclusive badge set with the

And now? Those badge sets are going for

But this isn't just a Pokémon problem. This is a symptom of something bigger happening in the toy industry right now. The entire landscape is shifting. Toys aren't being manufactured for children anymore. They're being manufactured for adults who collected them as children, have money now, and are willing to spend it. The companies making toys figured this out years ago. They've been optimizing for it ever since.

The question that keeps nagging at industry observers is simple: at what point does pursuing the lucrative adult collector market start damaging the brand's foundational identity? When does maximizing profit with existing fans begin alienating the next generation?

TL; DR

- Lego's Pokémon line has zero kid-focused sets at launch, with prices ranging from 650

- **The flagship 30 million in day-one revenue

- Exclusive collectibles are fueling scalper markets, with resellers listing items for 3–5x retail prices

- The toy industry is fundamentally shifting toward adult collectors as the primary revenue driver

- This strategy risks alienating children and undermining brands built on multi-generational appeal

Lego's pricing for its most expensive sets has increased significantly from

The Lego-Pokémon Partnership: A Timeline of Escalation

Lego announced the Pokémon partnership in March 2025 without revealing the actual product lineup. Industry observers assumed this was standard play: a couple of small sets for kids, maybe a medium-tier collector's item, probably a

Then the official lineup dropped, and people started doing math.

The partnership wasn't surprising in concept. Pokémon licensing is everywhere. It's on everything from energy drinks to fashion collaborations. Lego, meanwhile, has been aggressively pursuing adult collector markets since the early 2000s, when the "Adult Fans of Lego" (AFOL) community started organizing conventions and building increasingly complex models.

But the execution of the Pokémon line revealed something troubling about where the toy industry's priorities actually sit.

Lego positioned all three Pokémon sets as "display pieces." They're not designed to move. The Pikachu can't really flex. The Venusaur trio can rotate and display in different arrangements, but that's about it. They're meant to sit on a shelf. They're meant to be looked at. They're meant to appreciate in value like trading cards or collectible figurines.

That's the entire design philosophy. Not "fun to build and play with," but "carefully preserved after assembly and placed somewhere climate-controlled."

For context, Lego's other major licensed collaborations tell a different story. The Super Mario line, for example, launched with playsets explicitly designed for children. You could buy a Mario Kart set with vehicles you could actually move around. The Luigi's Mansion haunted house had interactive elements. Yes, there were premium collector sets too, but the range started with kids.

The Pokémon line? It started with nostalgia-baiting adults and went up from there.

Katriina Heljakka, a senior researcher specializing in toy and play cultures at the University of Turku in Finland, pointed out something crucial in analysis of the strategy: "Pokémon and Lego have multi-generational fanbases, yet there's no explicit narrative about multigenerational play. The new sets emphasize novelty, collectability, and fandom, which aligns with AFOL preferences, but provide little substantive commentary on how people actually play together."

In other words, Lego deliberately constructed a product line that prevents families from building together. The most accessible set, the Eevee, is supposedly compatible with Lego's "Build Together" feature through the mobile app. That feature splits instructions so multiple builders can work on different sections simultaneously. Theoretically brilliant. Practically, only one out of three sets supports it.

It's a choice. A deliberate one.

The Adult Collector Economy: How Nostalgia Became a Revenue Stream

This didn't happen overnight. The adult toy collector market has been growing for two decades.

In the early 2000s, Lego noticed something interesting: adults who'd grown up with Lego in the 1980s and 1990s were buying Lego. Not for kids. For themselves. They were building elaborate dioramas, attending conventions, trading pieces online, and documenting their collections.

Someone at Lego headquarters had an epiphany: what if we make products specifically for these people?

They started with modest collector sets. A

The economics are irresistible. An adult collector willing to drop

So Lego optimized. They hired product designers who understood display aesthetic. They collaborated with influencers—the "Lego YouTuber" is now a legitimate professional category. They created scarcity by limiting production runs. They bundled exclusive pieces that couldn't be bought separately. They created FOMO (fear of missing out) through limited-time preorders.

And it works. It works so well that the entire industry started copying it.

Hot Wheels, the die-cast car brand, started releasing premium "collector series" vehicles that cost

The toy industry figured out what the sneaker industry learned in the 2000s: scarcity plus nostalgia plus social status equals unlimited spending potential.

Adults don't just want toys. They want investments. They want status symbols. They want bragging rights. And they're willing to pay accordingly.

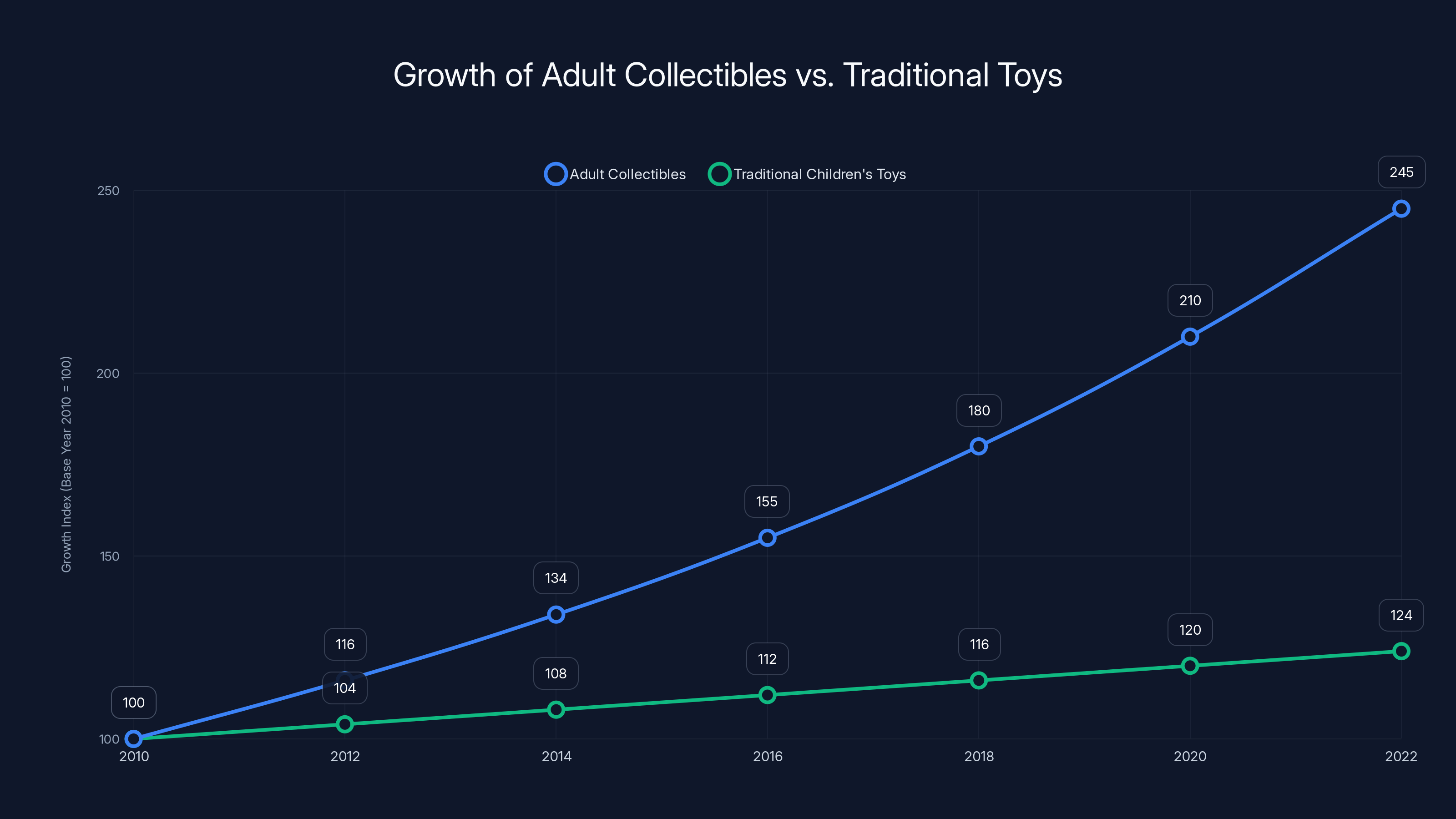

The adult collectibles segment has grown significantly faster than the traditional children's toy market, highlighting a shift in industry focus. Estimated data based on compound annual growth rates.

Price Points That Would've Been Unthinkable Five Years Ago

Let's zoom in on what $650 actually means in the context of Lego's pricing history.

In 2015, Lego's most expensive set was the $400 Parisian Restaurant. Considered outrageous at the time. Industry observers predicted it would tank.

It didn't. It sold well. That signaled something to the board.

By 2020, the

Then 2025 happened, and Lego released a thousand-dollar Death Star. People bought it. Actual people, with actual money, clicked purchase. The resale market immediately valued it at $1,200+.

Now a Pokémon set at $650 doesn't even raise eyebrows. It's aggressive, sure, but it's not shocking.

What's the actual content difference between a

That's pure market extraction. That's pricing what the market will bear, which apparently is quite a lot.

Here's the calculation: if the AFOL market is willing to spend

So you stop making the $30 sets. You don't need them. They cannibalize your premium offerings. They're a waste of production capacity.

Except here's the problem: kids aren't in that

The Scalper Problem: When Exclusivity Meets Artificial Scarcity

Here's where the strategy gets actively harmful.

Lego didn't just price the Pokémon sets high. They also made the badge set—the eight-piece collectible featuring the original game's gym badges—only available as a "gift with purchase" for people who preordered the $650 flagship set.

Limited quantity. Only during preorder. No second chance.

This is a classic scarcity play. Create desire by making something rare. Lego has done this before with other exclusives. The problem is that scarcity creates opportunity for speculation.

Within hours of the set selling out, eBay listings appeared. The badge set alone:

Think about that. Someone paid

Scalpers aren't buying these to collect them. They're buying them as financial instruments. They're treating Lego sets like cryptocurrency or penny stocks—pure speculation plays.

And the worst part? There's no way for legitimate collectors to stop them. You can't make purchases earlier. You can't bypass the preorder window. The scarcity is built into the product strategy.

Lego said, in a statement to media inquiries, that they would reserve some stock of the gift-with-purchase badge set for launch day in-store purchases. Great. But "some stock" is vague. And if you're not near a Lego store at 10 a.m. on launch day, you're competing with people who've made it their job to camp out and resell.

Meanwhile, kids? Kids have no chance at any of this. Not because they don't want it—kids absolutely want Lego Pokémon sets—but because they have no purchasing power and no way to get to a store before scalpers do.

Why Kids Weren't Even Considered in the Product Planning

This is the thing that really bothers industry analysts. Pokémon is fundamentally a kids' property.

Yes, there are adult fans. Absolutely. The franchise wouldn't be worth $100 billion+ without nostalgic adults buying things. But the core audience, the reason Pokémon exists, is children. Kids aged 5–15 are the primary demographic.

Yet Lego made a conscious decision to create zero products for that audience.

Why? Let's walk through the internal logic that probably happened at a Lego product strategy meeting.

First, someone pointed out the success of the adult collector market. The Death Star sold a million copies. Star Wars sets are consistently top revenue generators. AFOLs have conventions, YouTube channels, spending budgets in the thousands.

Second, someone pointed out Pokémon's massive nostalgic pull. Millennials who grew up with the original games are now 30–40 years old with disposable income. They have the Pokémon card collection nostalgia itch. This is untapped market.

Third, someone did market research and found out that the highest-value Pokémon collector audience is aged 25–45, with household incomes above

Fourth, someone ran the numbers and realized that a

Fifth, someone probably said, "Why even bother with kids' sets? It's extra production complexity, lower margins, and cannibalization of the premium line."

And nobody in the room argued.

That's how you end up with an 18+ product line for a franchise whose primary audience is children.

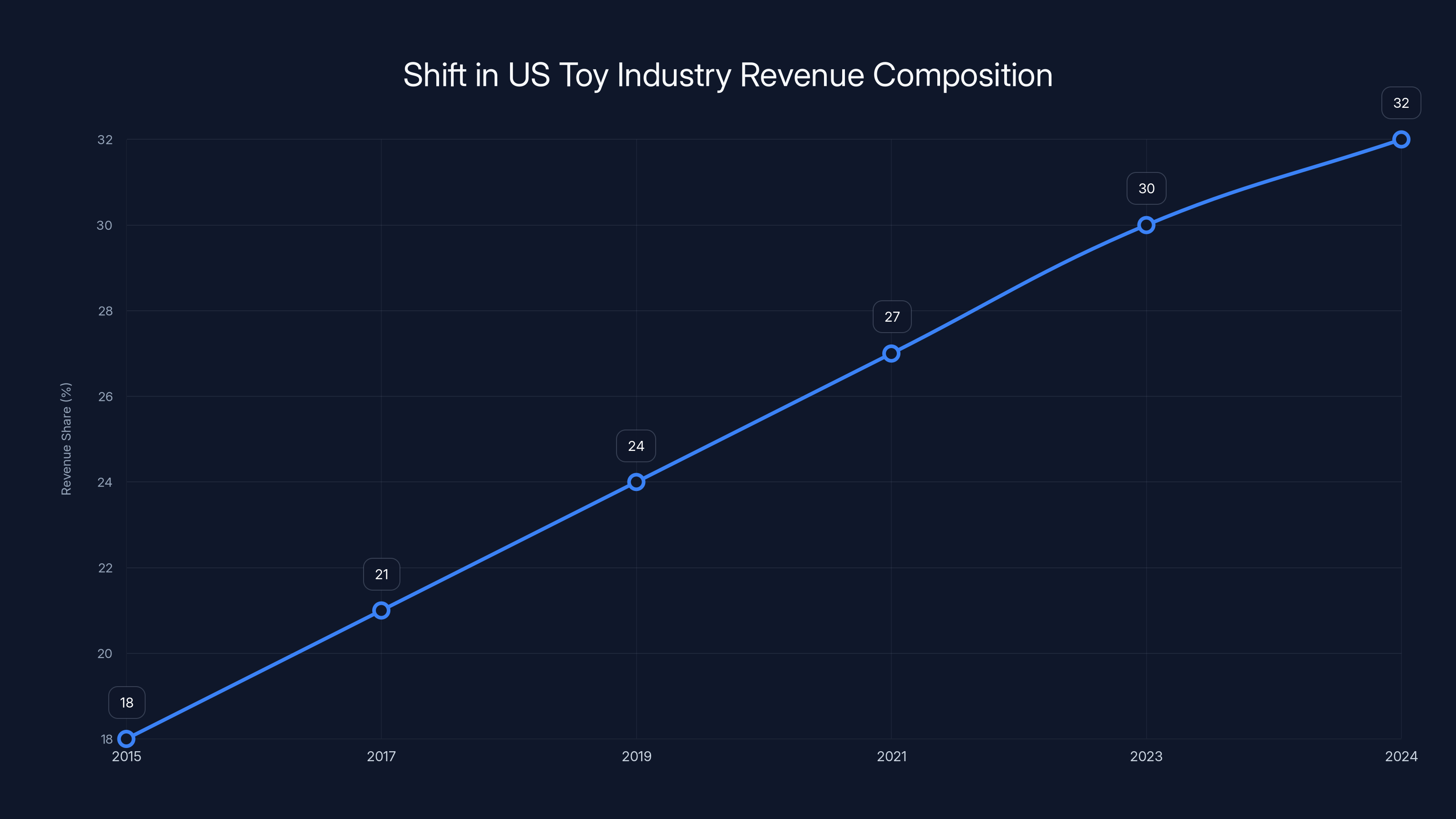

The share of adult collectibles in the US toy industry revenue has increased from 18% in 2015 to an estimated 32% in 2024, reflecting a shift towards premium pricing and affluent customers. Estimated data.

The Multi-Generational Appeal Problem: Lego's Core Identity Crisis

Lego's entire brand identity is built on "the toy for everyone." For seven decades, the message has been consistent: Lego is for kids of all ages. It's for families. It's for grandparents building with grandchildren. It's for date nights. It's for team-building exercises.

That's the brand promise. That's why Lego commands premium pricing. People trust it because it's been a constant, accessible part of childhood.

But what happens when a major product line explicitly excludes children?

Katriina Heljakka notes that the Pokémon line represents a departure from Lego's foundational values: "The new sets emphasize novelty, collectability, and fandom, which aligns with AFOL preferences, but provide little substantive commentary on how people actually play together. Licensed collectibles risk being perceived as display pieces for solitary play rather than as tools for shared play."

In simpler terms: Lego is abandoning the idea of building together.

The company even has a feature specifically for this. The Lego Builder app includes a "Build Together" mode that splits large sets into smaller sections. Multiple people can build simultaneously. You divide and conquer, then combine the pieces. It's collaborative. It's social. It's supposed to be the future of Lego.

But the Pokémon line barely uses it. Only the entry-level Eevee set supports it. The two premium sets don't.

Is this a technical limitation? No. Is it a cost-cutting measure? Probably not. It's a deliberate design choice that says, "These sets are for you, the individual collector, to build in solitude and display in your room."

Compare this to the Super Mario line, Lego's other major Nintendo collaboration. Those sets explicitly support collaborative building. You can build Mario Kart tracks together. You can construct levels in parallel. The messaging is, "Buy this and play with people you love."

The Pokémon line's messaging is, "Buy this and flex on social media."

These are two very different value propositions. One builds community and strengthens the brand across generations. The other extracts maximum value from existing fans while providing no on-ramp for new ones.

Lego's growth targets are presumably still ambitious. The company wants to keep scaling. But if you're not creating young collectors today, where are the adult collectors coming from in 15 years?

The Broader Toy Industry Shift: Adults Only

The Pokémon Lego situation isn't isolated. It's emblematic of a broader transformation in the toy industry that started maybe ten years ago and is now in full swing.

Market research firms have been tracking this. Statista data shows that the "adult collectibles" segment of the toy market grew at a compound annual growth rate of roughly 8–10% for most of the 2010s and 2020s. Meanwhile, the traditional children's toy market grew at maybe 2–3%.

The math is obvious. Investors prefer faster growth. Faster growth comes from adults. So investment flows to adult products.

This affected everything:

Trading cards: The Pokémon Trading Card Game generates more revenue now from adult "collectors" buying sealed boxes and chasing rare variants than from kids actually playing the game. Booster box prices have tripled since 2019. A sealed first edition base set box now costs $10,000+. Kids literally can't participate in this market.

Action figures: Hot Toys, S. H. Figuarts, and other premium figure makers charge

Sneakers: Resale market for limited-release sneakers regularly hits hundreds of millions. Kids can't compete with adults camping outside stores.

Manga and anime figures: Nendoroids and other collectible figures regularly price above $100. The accessibility ceiling is high.

The pattern is consistent: scarcity + nostalgia + adult wealth = premium pricing, scalper activity, and kids priced out of their own culture.

Toy companies aren't evil. They're just following incentive structures. A CFO looks at the AFOL market, sees growth, sees margins, and green-lights investment. A product manager sees a successful competitor charging

Each individual decision is rational. The cumulative effect is irrational. You end up with an industry that's optimized for extracting maximum value from existing fans while actively discouraging the creation of new ones.

Eventually, that catches up to you. But it doesn't catch up immediately. And in the meantime, the money's great.

Scarcity as Strategy: The Gift-With-Purchase Model Explained

Lego's decision to make the badge set a "gift with purchase" exclusive deserves its own analysis because it's a brilliant piece of marketing that also happens to be kind of predatory.

Here's how it works:

You want the badge set. It's cool. It's exclusive. It's Pokémon nostalgia in eight pieces. You can't buy it directly. The only way to get it is to buy the $650 trilogy set during the preorder window.

So you do. You commit to

This is loss leader strategy taken to the extreme. The badge set costs Lego maybe

That's marketing genius. That's also extremely effective scarcity-based selling, which is why it immediately triggered scalper activity.

Because here's what scalpers understood immediately: the badge set is the actual valuable piece. It's irreplaceable. It's limited. It can't be bought separate. If you own it, you're in an exclusive club.

So scalpers didn't buy the sets to keep. They bought them to extract the badge set and immediately flip it. They knew they could sell the badges for

Which is exactly what happened. Within days, eBay had listings. Within a week, the secondary market was fully functional. Within a month, a legitimate collector trying to buy a badge set was facing

Lego said they'd reserve some stock for launch day in-store sales. Cool. But "some" is the operative word. It's a token gesture. If you can't get to a store at 10 a.m. on launch day—if you have work, or school, or literally any other commitment—you're buying on the secondary market from a scalper.

Lego probably doesn't mind. The secondary market proves the exclusivity and desirability of the product. Which means the next exclusive they release will command even higher premiums, leading to even more scalper activity, leading to even more hype, leading to even more sales.

It's a self-reinforcing cycle. And it works until it doesn't. The question is whether Lego's brand reputation survives being perceived as a speculation vehicle rather than a toy company.

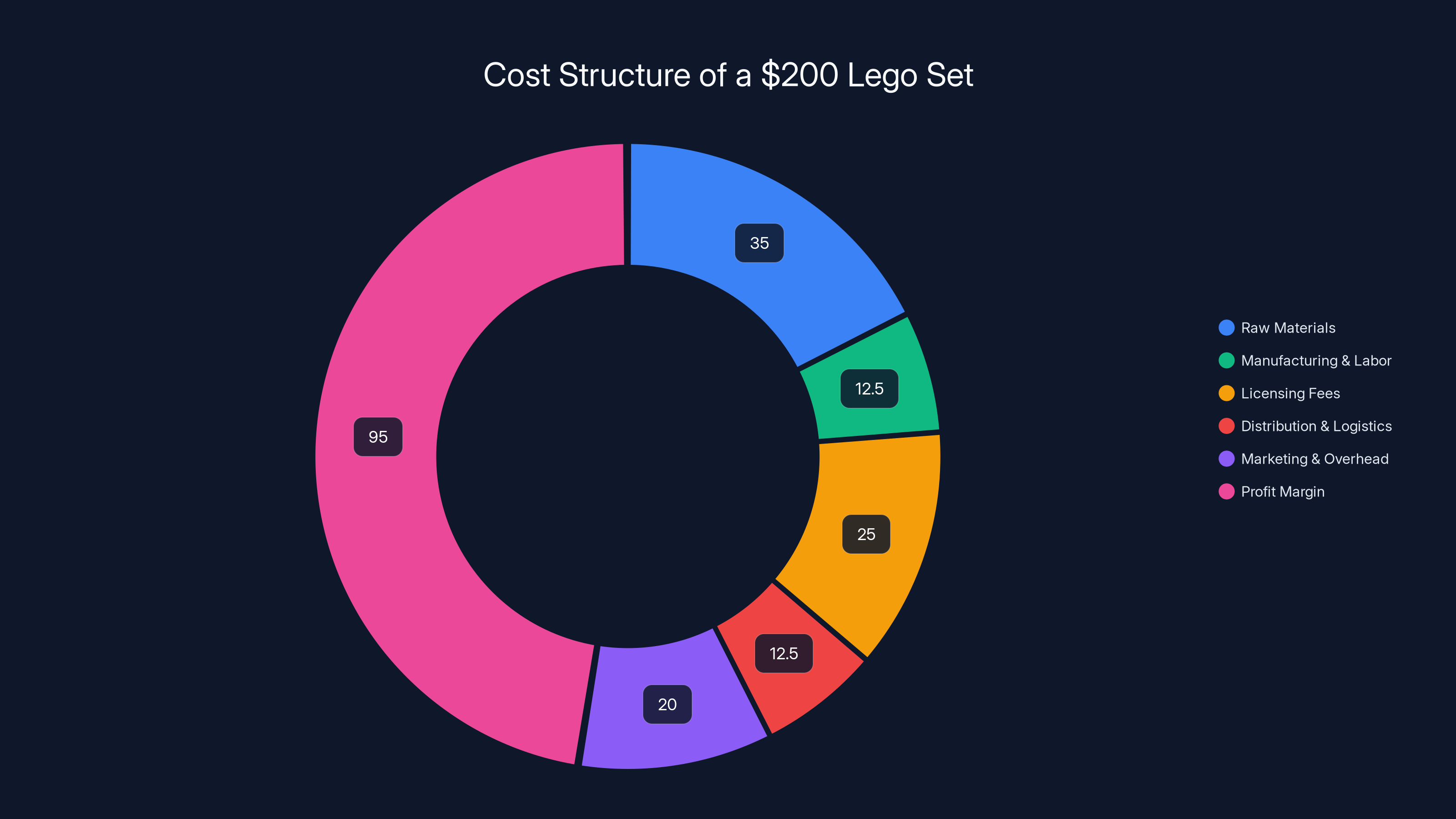

The profit margin for a $200 Lego set is significant, accounting for nearly half of the retail price. This highlights the premium pricing strategy that maximizes profit per unit.

The Super Mario Comparison: How Lego Used to Handle Licensed Properties

Lego's Super Mario partnership, announced in 2020, took a completely different approach. It's worth examining because it shows what responsible multi-generational product strategy actually looks like.

The Mario line launched with sets at multiple price points:

- Starter packs around 70 designed for kids aged 6+

- Expansion sets in the 60 range for building out the world

- Premium dioramas and display pieces in the 200 range for collectors

- Occasional exclusive collector sets that got special treatment

Crucially, the entire line was designed with the game in mind. Sets featured moving parts. Tracks could be built and rebuilt. Levels could be modified. The whole concept was "build your own Mario level," which explicitly encourages play and creativity.

Yes, there were collector pieces. Yes, there was scarcity marketing. But the floor was accessible. A kid with $50 and parental consent could walk into a Lego store and buy a Mario set today. That same kid can't do that with Pokémon.

The difference is philosophical. Mario says, "Everyone can participate." Pokémon says, "Only people with significant disposable income."

Which one do you think builds more loyal customers across generations?

The Mario strategy also proved profitable. The line has been successful by any measure. It's generated hundreds of millions in revenue. But it did so while maintaining accessibility and introducing new audiences to Lego.

That's the road not taken with Pokémon.

Supply Chain Economics: Why Premium Pricing Makes Sense (Even If It Sucks)

Let's talk economics for a moment, because understanding the decision-making process helps explain (if not justify) why we're here.

Assuming a typical Lego cost structure:

- Raw materials (ABS plastic, packaging): 40 for a $200 set

- Manufacturing and labor: 15

- Licensing fees (Pokémon Company gets paid): 30

- Distribution and logistics: 15

- Marketing and overhead: 25

- Profit margin: 95 (roughly 40–50%)

Now, if Lego tried to make a $50 set with the same profit margin:

- Raw materials: 12

- Manufacturing: 5

- Licensing: 8

- Distribution: 5

- Marketing/overhead: 10

- Profit margin: 17 (roughly 22–34%)

Same work. Exponentially lower profit per unit. So from a pure business perspective, why would you make the $50 set?

You wouldn't. You'd only make premium sets where you can justify manufacturing because the margins are thicker.

This is how you optimize for profit short-term. It's also how you accidentally kill your business long-term by cutting off the pipeline of new customers.

But if you're a mid-level product manager with quarterly earnings targets, you're not thinking about the pipeline. You're thinking about this quarter's revenue.

That's the incentive structure. That's why we're here.

Will Lego Ever Make Kid-Friendly Pokémon Sets?

The question haunting the industry right now is whether Lego will eventually release child-friendly Pokémon products. The answer is: probably, but not soon.

Here's why: if Lego announces a

That's bad marketing. That's worse for customer trust.

So Lego will let the premium line breathe for at least a year or two. They'll let collectors feel special. They'll let scalpers extract value. They'll let the secondary market stabilize at elevated prices.

Then, probably 18–24 months from launch, they'll announce a $40 Pokémon beginner set. Totally separate line. Different branding maybe. Clearly positioned as entry-level.

But by then, the cultural perception of Lego Pokémon will be "this is premium, exclusive, expensive." That anchor will stick. A $40 set will feel like the consolation prize.

And the kids who could've had Lego Pokémon from day one? They'll have moved on. They'll want something else. The window closes.

This is strategic patience. This is knowing that you have a limited amount of time to extract maximum value from the early adopter AFOL market, and you're going to squeeze every dollar before pivoting to accessibility.

It's smart business if you're measuring in quarters. It's terrible strategy if you're measuring in decades.

The Trilogy Set is the most expensive and has the highest piece count, reflecting its premium positioning in the Lego Pokémon lineup.

The Slippery Slope: What Happens When Every Licensed Product Is Premium?

Here's the concerning scenario that keeps industry observers up at night:

Lego successfully executes the Pokémon premium strategy. Makes hundreds of millions. Investors are thrilled. Stock price rises. Board members get bonuses.

Next year, Lego announces a Zelda partnership. Guess how many kid-focused sets launch? Zero. All premium, all adult-focused, all priced accordingly.

The year after that, a Dragon Ball Z partnership. Same story.

Gradually, every licensed partnership becomes a play for adult collectors. Every major franchise gets segmented into premium-only offerings. The brand position shifts from "toys for everyone" to "collectibles for affluent adults."

At some point, you look up and realize that the toy industry has completely bifurcated. There's the premium collectible segment, dominated by adults with money. And then there's the budget segment, which is disposable garbage made in factories with minimal quality control, sold at drugstores.

The middle market—the accessible, quality products for regular families—gets squeezed out.

This is already happening in some toy categories. High-end collectible figures versus cheap anime knockoffs. Limited-edition Funko Pops versus dollar-store figures.

It's not inevitable that Lego goes this direction. The company has enough brand equity and profit to make different choices. But the incentive structures all point this way. And if nobody pushes back—if parents don't vote with their wallets, if collectors don't demand more accessibility, if the industry stays silent—then this is the direction we go.

Nostalgia as a Trap: Why Millennials Are Funding This

Let's be honest about what's happening here. Lego and Pokémon aren't just marketing to adults. They're exploiting nostalgia.

If you grew up in the 1990s, Pokémon Red and Blue are not just games. They're core memories. They're simpler times. They're childhood joy distilled into 8-bit graphics. When you see a Pikachu, you don't just see a fictional character. You see yourself at age ten.

That's powerful. That's vulnerable. That's where $650 comes from.

Companies know this. They've built entire product strategies around it. The Pokémon Company, Lego, and every other major nostalgia brand has done market research showing that Millennials (aged 30–44 in 2025) have significant disposable income and high emotional attachment to their childhood brands.

So they optimize for that. They make products that hit that emotional nerve. They price them at the ceiling of what this demographic will pay. They create scarcity and exclusivity to amplify the emotional stakes.

It's not malicious. It's just very effective capitalism. They've identified a market segment with high emotional motivation and low price sensitivity, and they've built products for that segment.

But there's a cost. The cost is that the next generation doesn't get to have the same experience. Ten-year-olds today can't afford Lego Pokémon. They can't build it with their parents. They can't experience the joy of construction and imagination that made Lego special in the first place.

So in 20 years, when those kids are adults, they won't have the same nostalgic pull for Lego. They won't have that foundational memory. They won't spend

The industry is essentially mortgaging its future to maximize its present. And it's doing it under the guise of "serving adult collectors."

What Experts Are Actually Saying About This Shift

Katriina Heljakka's research on toy cultures is particularly relevant here. Her analysis of the Pokémon line highlights something crucial: these sets are "closed-object products that behave more like 3D jigsaw puzzles than platforms for co-play by building together."

In plain language: they're not toys. They're display pieces. The distinction matters.

Toys are tools for play, imagination, and social interaction. Display pieces are objects for collection and appreciation. Lego used to make toys. Now they're making display pieces and calling them toys.

The language matters because it shapes expectations. If you buy a toy, you expect your kid to play with it. If you buy a display piece, you expect to assemble it once and leave it alone.

Most people are operating under the toy mental model when they buy Lego. They expect multi-generational appeal. They expect buildability and rebuildability. They expect shared experiences.

Lego Pokémon delivers none of that. It's display pieces priced like toys but positioned as collectibles.

Other experts point out the cannibalization risk. If Lego is successfully capturing hundreds of millions from the premium AFOL market, why would they ever go back to the kids' market? Once you've trained your customer base to accept premium pricing, going backward creates perception problems.

So Lego has an incentive to never go back. To keep chasing higher price points. To keep targeting older, wealthier demographics. To keep emphasizing collectability over playability.

This is the path dependency problem. One decision leads to another. Before you know it, you've architected your entire business around a model that explicitly excludes children.

The question is whether the board room realizes the long-term cost of that architecture.

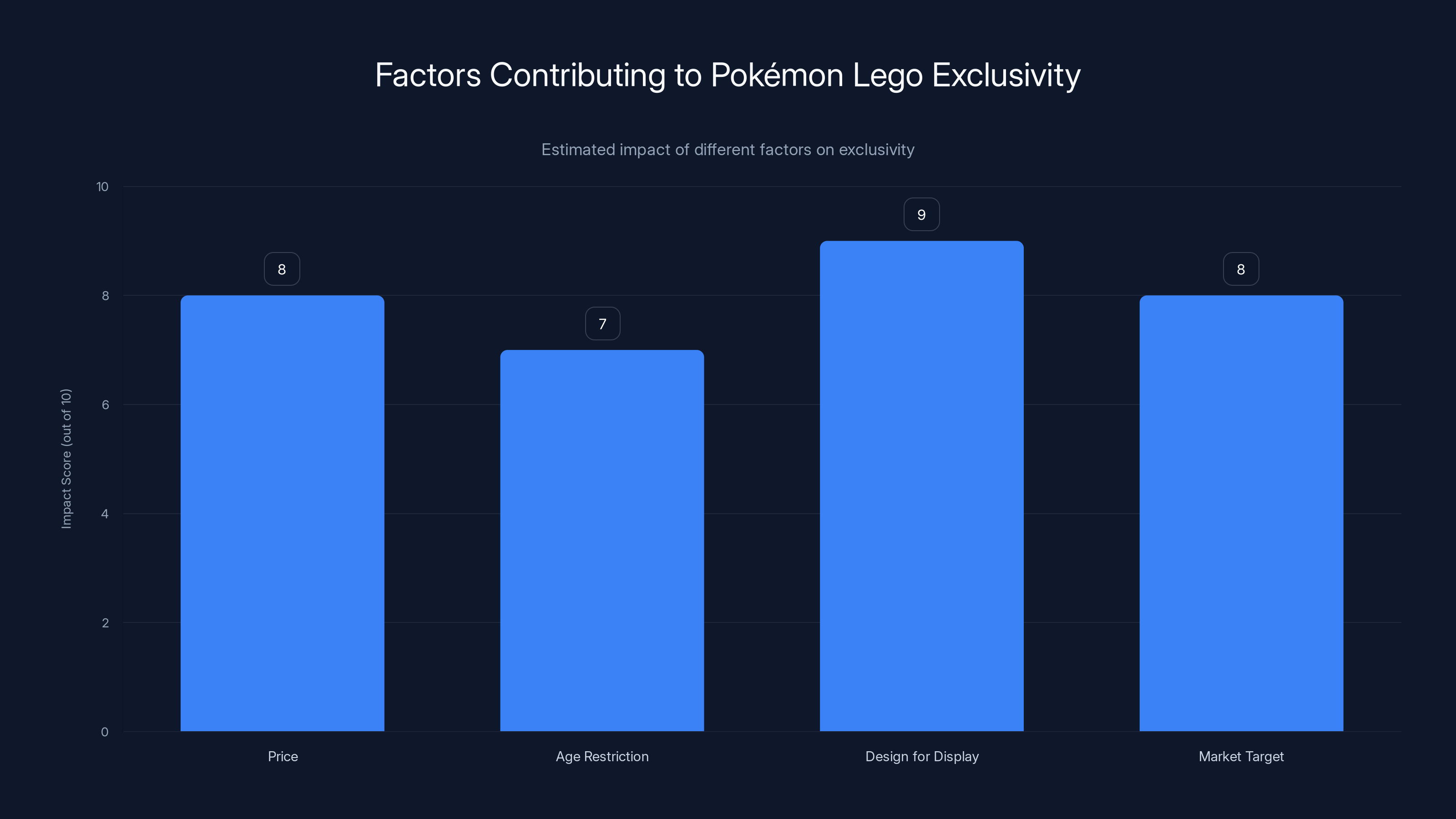

Estimated data shows that design for display and pricing have the highest impact on the exclusivity of Pokémon Lego sets, making them less accessible to children.

The Numbers Behind the Scarcity: Production Volumes and Market Reality

Lego hasn't publicly released production numbers for the Pokémon sets, but industry analysts have some data points.

JANGBRIKKS' calculation suggested roughly 50,000–75,000 units of the trilogy set were produced for initial release. That generated the estimated

For context, a typical Lego Star Wars set produces 200,000–400,000 units. The Mario line produces even higher volumes because it's designed for broader accessibility.

The Pokémon trilogy had maybe 1/5 to 1/3 the volume of comparable licensed sets. That's a deliberate scarcity strategy.

Why? Because volume and exclusivity have an inverse relationship. The more units you produce, the more common the set becomes, the less special it feels, the lower the resale value.

So Lego constrained supply to maintain exclusivity. This was almost certainly intentional. Not "we ran out," but "we only made exactly as many as we estimated the premium market could absorb."

Which is brilliant for short-term revenue. It's terrible for brand accessibility and intergenerational appeal.

Note also that the initial production run wasn't infinite. The sets sold out. Lego announced restocks later, but the initial scarcity was managed. Some units will eventually return to shelves, but the perception of scarcity has already taken hold.

Secondary market prices reflect that perception. Even as new stock arrives, the resale market stays elevated because the narrative of "limited edition" is already set.

The Regulatory Question: Is This Actually a Problem?

Should governments regulate this? Should there be laws requiring toy companies to maintain children's product lines?

This is where it gets philosophically murky.

On one hand, toys are ostensibly products designed for children. There's an implicit social contract: toy companies make things kids can access and enjoy.

On the other hand, companies have the right to make business decisions about their product mix. If Lego decides to prioritize profitability over accessibility, that's their prerogative.

Some countries have toy safety regulations. The EU has strict standards. The US has CPSIA guidelines. But none of these address pricing or accessibility. They address safety and quality.

There's no regulatory framework that says, "You must make a product line accessible to children if you want to use the toy branding."

Should there be? That's a policy question beyond the scope of business analysis. But it's worth noting that the lack of regulation is allowing this to happen unimpeded.

Some people argue for market correction. If parents get mad about price and accessibility, they'll vote with their wallets. Lego will adjust. But that assumes parents even know about this. Most people don't pay attention to toy pricing strategies. Most kids just ask for the thing they want, and parents buy it or don't based on sticker shock.

Meanwhile, Lego banks on the parents who do buy it, and those numbers are strong enough to justify the strategy.

So nothing changes, absent external pressure.

The Larger Context: How the Entire Retail Landscape Shifted Toward Affluence

This isn't just a toy story. The entire retail landscape has shifted toward serving wealthy customers and abandoning the middle market.

Consider fast fashion. Twenty years ago, the industry served everyone. You could buy jeans for

Now? Fast fashion has fragmented. There's ultra-cheap garbage made in places with minimal labor protections, marketed toward people with very low budgets. And there's premium fast fashion, where a basic t-shirt costs

The $30 jeans are gone. That middle market got hollowed out.

The same thing happened in restaurants. Casual dining died. Now you have food courts with fast casual (Chipotle, Panera) at one end, and fine dining at the other. The sit-down restaurant with moderate pricing is nearly extinct.

The same thing happened in cars. Middle-market sedans died. Now it's either used economy cars or premium luxury vehicles. The affordable new car for a regular family is getting harder to find.

This is a broader economic trend. The hollowing out of the middle. Pricing is polarizing. You serve either the wealthy or the poor. The middle gets squeezed out.

Lego Pokémon is a microcosm of that macroeconomic trend. It's not unique. It's part of a larger pattern where companies increasingly optimize for high-value customers and abandon the mass market.

Whether that's sustainable long-term is an open question. But it's definitely the direction we're trending.

What Happens Next: Predictions and Scenarios

Here's where this probably goes:

Scenario One: Premium Strategy Continues

Lego doubles down. Every major licensed partnership becomes premium-only at launch. They milk the AFOL market for maximum value. Volumes constrain, prices climb. The secondary market thrives. Scalper activity increases. Eventually, some regulatory body or parent group pushes back on predatory pricing, but probably not until there's broader public awareness.

In this scenario, Lego's profitability stays high for 5–10 years. Then, the next generation of adult collectors doesn't materialize because today's kids didn't grow up with accessible Lego. Revenue eventually declines.

Scenario Two: Market Correction

Parents and consumer advocates push back hard enough that Lego feels pressure to introduce kid-friendly product lines. They do, but it feels like a consolation prize. The messaging is confused. The product quality is lower. The AFOL market fractures between people who feel betrayed by accessibility and people who appreciate the inclusion.

Lego's revenue stays stable but doesn't grow. They've optimized themselves into a niche.

Scenario Three: Bifurcation

Lego creates completely separate brands. "Lego Classic" for kids and families. "Lego Collector" for AFOLs. Completely different product lines, different manufacturing standards, different price points. Each optimized for its audience. This is cleanest long-term but requires admitting the strategy was problematic.

Scenario Four: Regulatory Intervention

Some government body mandates that licensed toy products maintain accessible price points. Toy companies have to balance premium and entry-level offerings. Lego adjusts. Profitability declines slightly but the brand's generational equity improves.

Most likely? Scenario One in the short term, then a slow drift toward Scenario Two as reality hits.

The Bigger Question: What Do We Actually Want Toys to Be?

Ultimately, this isn't really about Lego or Pokémon specifically. It's about what we collectively want toys to represent.

Are toys tools for play, imagination, and family bonding? Or are they collectibles for investment and status?

Can they be both? Probably. But the current trajectory suggests we're answering that question in ways that exclude children.

Lego was special because it was accessible. Because a kid could have the same experience as a millionaire, building something cool with bricks. The economics were the same. The joy was the same. The imagination was the same.

That's no longer true. Now, the Pokémon Lego experience is reserved for people with significant disposable income. Everyone else gets something else.

That's not evil or wrong. It's just a choice. But it's a choice with consequences. The consequence being that the next generation grows up with different toy brands, different memories, different loyalties.

Maybe that's fine. Maybe there will be new toy companies that understand multi-generational appeal and seize the market. Maybe the next Lego will be a company that remembers what it's like to be a kid without much money.

Or maybe the toy industry continues bifurcating, and we get used to the idea that quality toys are for the wealthy, and everyone else gets whatever they can afford.

Based on current trajectories, I'd guess we're heading toward the latter. Which is sad, but probably inevitable given how incentives are structured.

FAQ

What is the Lego Pokémon partnership?

The Lego Pokémon partnership is a collaboration between Lego and The Pokémon Company announced in March 2025. The partnership produced three buildable sets featuring iconic Pokémon from the original generation games: an Eevee set (587 pieces,

Why are the Lego Pokémon sets so expensive?

The pricing reflects Lego's strategy to target the "Adult Fan of Lego" (AFOL) market rather than children. The sets use premium materials, complex engineering, and licensed IP from The Pokémon Company. Additionally, Lego deliberately constrained production volumes to maintain scarcity and exclusivity, which supports premium pricing. The highest-priced set generated an estimated $30 million in revenue within 24 hours of launch.

Are there any Pokémon Lego sets designed for children?

At the launch of the partnership, no. All three initial sets are age-rated 18+ with no announced child-friendly products. This contrasts sharply with Lego's Super Mario partnership, which launched with products at multiple price points and age ratings. Industry analysts speculate that Lego may eventually release kid-focused Pokémon sets, but probably not for 18–24 months to preserve the exclusivity perception of the premium line.

How did scalpers affect the Pokémon Lego market?

The limited availability of the exclusive Kanto Region Badge Collection (available only through preorder of the

How does this compare to other Lego licensed partnerships?

Lego's Super Mario partnership took a significantly different approach, launching with products at multiple price points (

What does this mean for future toy industry trends?

The Pokémon Lego strategy reflects a broader industry shift toward premium adult collectibles and away from mass-market accessibility. Similar trends appear in trading cards (sealed boxes targeting collectors rather than children playing the game), premium action figures, and limited-edition merchandise. This creates a bifurcated market where quality toys are primarily accessible to affluent adults, while children are served by cheaper alternatives. Whether this is sustainable long-term remains an open question, particularly regarding the pipeline for next-generation adult collectors.

Conclusion: The Inevitability of Exclusion

Lego didn't set out to create a product line that excludes kids. That framing is too conspiratorial. What Lego did was follow incentive structures. They identified a profitable market segment. They optimized for it. They executed well.

The problem is that the cumulative effect of these optimizations is exclusion. Not intentional, just inevitable.

The Pokémon Lego line is expensive because expensive is profitable. It's exclusive because exclusivity supports premium pricing. It's 18+ because adults have money and lower price sensitivity. It's designed for display, not play, because display pieces support longevity in the secondary market.

Every decision is rational. The totality is irrational.

And now we're in a world where a ten-year-old who loves Pokémon can't afford Pokémon Lego. They can look at pictures online. They can watch unboxing videos. They can admire from a distance. But they can't participate.

Meanwhile, a 35-year-old nostalgic millennial can drop $650 without blinking. And Lego is perfectly happy with that arrangement.

Is that the toy industry we want? The one where toys are status symbols for adults, not tools for childhood imagination?

Maybe. We'll probably find out. But that's the direction we're heading, and the Pokémon Lego sets are just the most visible example of a trend that's reshaping the entire landscape.

The question facing the toy industry now is whether it wants to be remembered for multi-generational joy and accessibility, or for extracting maximum value from nostalgic adults before moving on.

Based on current strategies, it seems we're choosing the latter. And that's a choice with consequences we won't fully understand for another decade.

But don't worry. There will probably be a Pokémon NFT collection to fill the gap.

Key Takeaways

- Lego's Pokémon partnership excludes children entirely, with all three sets rated 18+ and priced from 650

- The 30 million in 24-hour revenue through strategic scarcity and exclusive bundling

- Exclusive badge sets immediately triggered secondary market scalping, with resale prices inflating to 500 within days

- This strategy represents a systematic shift in the toy industry toward premium adult collectibles and away from multi-generational accessibility

- The industry risks damaging long-term brand equity by eliminating the pipeline of young collectors who would become affluent adult customers