Why Navan Is Up +30% in 2026. When So Many Other Public Software Leaders Are Down. | Saa Str AI

Overview

AI VC AI Mentor: Digital Jason + Amelia AI Startup Benchmarking

AI Agent Playbook Free e Books

e Book: Hiring a Great VP of Sales

e Book: Raising Capital

e Book: The First $1m ARR

Details

University All Posts Podcasts The Top CROs VC Fundraising Top Videos Q&A Best of Saa Str #1 Bestselling Book Search Everything Join the Community

Free e Books

e Book: Hiring a Great VP of Sales

e Book: Raising Capital

e Book: The First $1m ARR

AI Annual 2026 Events Overview Sponsors

Event Sponsorship

Media Sponsorship

Digital AI Day 2026 (Free) Speaker Submissions Speaker Requirements Overview

Why Navan Is Up +30% in 2026. When So Many Other Public Software Leaders Are Down.

by Jason Lemkin | 5 Interesting Things, Blog Posts, Scale

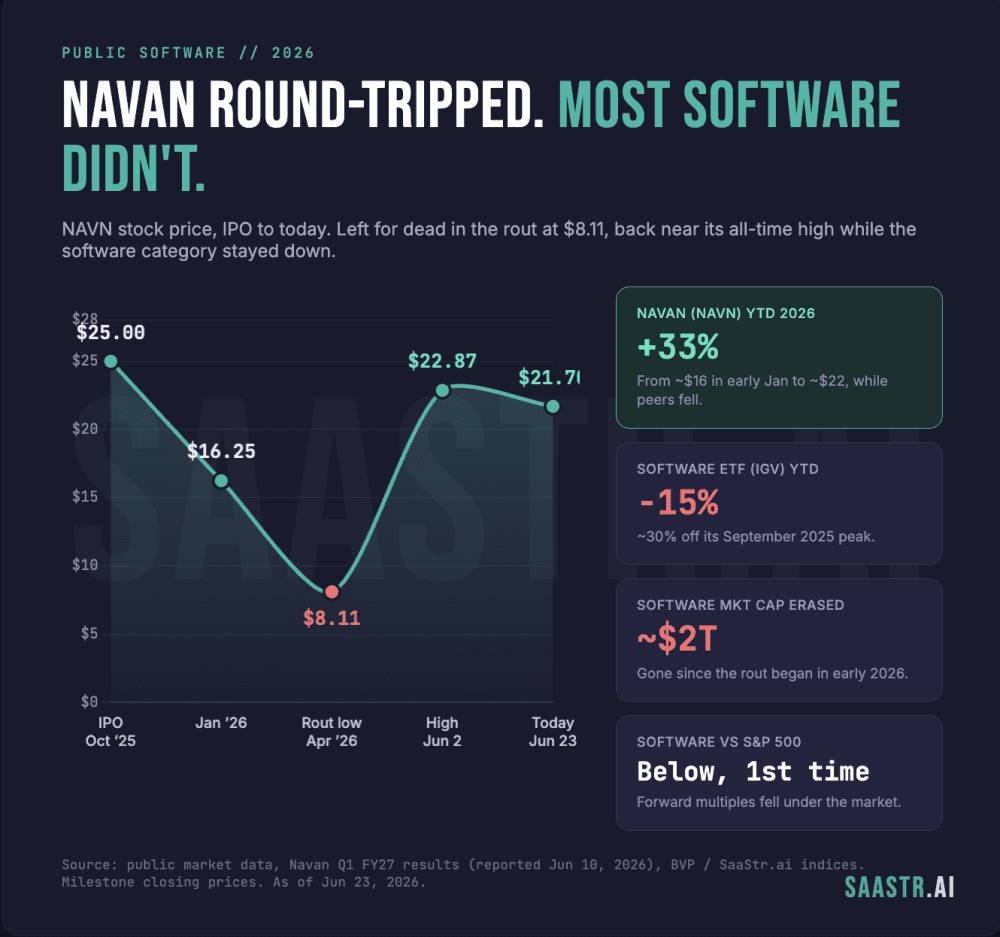

Pull up a chart of public B2B software in 2026 and it is a sea of red. IGV, the i Shares software ETF, is down more -15% year-to-date and off roughly 30% from its September 2025 peak. For the first time in history, software forward multiples dropped below the S&P 500.

Navan, the corporate travel and expense platform formerly known as Trip Actions, IPO’d at

And then it did the thing few other non-infrastructure public software company managed in 2026. It went back up. On June 11, after reporting Q1 FY2027 results, Navan hit a fresh 52-week high of

So how is one company climbing while the category it lives in loses half its value? The answer is more interesting than “good quarter.” Navan is up because of the exact same force that is killing everyone else. Here is the analysis, and five learnings worth taking to your own business.

Start with the numbers from Q1 FY2027 (quarter ended April 30, 2026), reported June 10:

Revenue of

Gross Booking Volume of $3.1B, up 50% year-over-year. A record.

Non-GAAP operating income of $24M, an 11% margin, up 900 basis points year-over-year.

Non-GAAP net income of

Non-GAAP EPS of

Then Navan raised full-year FY2027 guidance to

In a year where the entire public software complex is guiding down and getting punished for it, Navan guided up and projects sustained 30%+ growth.

1. Navan never sold seats. That is why the Saa Spocalypse skipped it.

The thesis crushing public software in 2026 is specific. The market has decided that AI agents will replace headcount, and per-seat licensing models depend on headcount growing. If agents replace seats instead of filling them, the revenue model does not slow. It reverses. That fear is why Atlassian, Workday, Hub Spot, and the rest got cut in half.

The model the market is fleeing is the one Navan never had. The lesson for founders is blunt. In 2026, your pricing model is your risk model. Revenue that scales with customer activity survives the agent transition. Revenue that scales with customer headcount is now on trial.

For most public software, AI is the threat coming for the business model. For Navan, AI is the product getting better and the cost to serve getting lower at the same time.

Usage of Navan’s proprietary AI model jumped from 20% to 30% in a matter of weeks. That automation is what drove the 900 basis points of operating margin expansion. The company is orchestrating AI agents and human travel agents together through its Cognition platform, which matters most exactly when travel breaks down and pure automation is not enough.

And instead of waiting to be embedded, Navan embedded itself. Navan Anywhere puts its travel agents directly inside Alphabet’s Gemini Enterprise, so a company already running Gemini can book travel through Navan without ever opening Navan. That is the difference between riding the shift to agents and being replaced by it. Navan made AI a distribution channel, not a competitor.

3. Competitor consolidation is a gift, and Navan is collecting it.

Here is a number that does not get enough attention. 38% of Navan’s Q1 customer wins came out of the American Express Global Business Travel cohort. RFP volume was up more than 200% year-over-year. Fortune 500 customers grew to 45, up from 28 a year earlier.

When the legacy travel incumbents consolidate and stumble, the displaced demand has to land somewhere. Navan is the modern alternative in a category where the incumbents are genuinely old, and customers are reevaluating in waves. Management said it plainly. They are seeing more customers come to them rather than having to push into the market.

The general principle. In a frozen market, being the obvious modern replacement in a category full of tired incumbents is one of the few reliable growth engines left. Disruption flowing toward you is worth more than any demand gen budget.

4. The market re-rated Navan the moment it proved growth plus margin together.

In 2021, public software got paid for growth alone. In 2026, that trade is dead. The market now wants growth and durable margin in the same company, and it is brutal toward anyone offering only one.

Navan delivered both in the same quarter. 40% revenue growth, an 11% non-GAAP operating margin, a swing to non-GAAP profit, positive free cash flow, and raised guidance. That is a real Rule of 40-plus profile arriving at the exact moment the market decided it would only pay for that profile.

The takeaway for anyone planning a 2026 or 2027 exit. Growth gets you in the room. Margin and cash flow get you the multiple. The companies getting rewarded right now are the ones that can show both lines moving in the right direction at once.

5. Reacceleration is the single rarest and most valuable signal in software right now.

Public software growth rates have declined essentially every quarter since the 2021 peak. Deceleration is the default. The market has priced in a world where every software company is slowing down, which is most of why even 22x multiples are getting questioned.

Navan went the other way. It guided Q1 to around 30% growth and printed 40%. GBV accelerated to 50%. Then it raised the full year. In a market where the entire peer group is guiding down, the one company guiding up does not get a small reward. It gets re-rated, because reacceleration breaks the model the market is using to price everyone else.

If you can credibly show your growth rate going up and not down in 2026, you are in a category of one. That is the scarcest thing in public software today, and it is most of why Navan is the exception on the chart.

92% of revenue is usage-based. Usage revenue hit

2% to 11% non-GAAP operating margin in a single year, with gross margin up from 72% to 75%. The growth did not cost efficiency.

Negative

28 to 45 Fortune 500 customers, up 61% year-over-year, across roughly 12,500 total customers. The mix is moving upmarket.

Reed & Mackay migrations are underway and Smartrips in Brazil is signed, Navan’s first acquisition as a public company. M&A is a growth lever, not a side project.

+202% off the bottom, from the

6x forward sales and roughly 100x forward earnings after the run. The Street-high target is $38, so the price already assumes near-perfect execution. The risk is now the valuation, not the business.

The Revenue Multiple is Still … Low. At Least by Historical Standards. And By What VCs Look For.

Navan is reaccelerating. The stock is back near its highs. AI is helping, not harming. Times are good for Navan.

But step back and the bigger picture is sobering. B2B multiples for public companies are not what they were, and Navan lives in the same market as everyone else.

The median public software company now trades around 3.4x ARR. That is the Saa S Capital Index reading as of May 2026, and Aventis lands at the same 3.4x on its own data. The large-cap cloud leaders do better, with the BVP Cloud Index averaging 6.6x, but that same index peaked at 28x revenue back in late 2021. Software forward earnings multiples are still sitting below the S&P 500, something that had never happened before this cycle.

So even the best story in public B2B right now is being told in a market that pays a fraction of what it paid four years ago. Navan trades at a premium to that 3.4x median, around 6x forward sales, precisely because it is doing the one thing the market still rewards. But a premium in 2026 is a smaller number than a premium in 2021. The entire curve reset lower.

You can do everything Navan did, reaccelerate, swing to profit, turn AI into a tailwind, and still get valued against a 3.4x baseline instead of a low-double-digit one. The bar to earn a premium went up. The size of the premium came down. Navan cleared the bar. Most companies will not. And even the winners are getting paid on a smaller scale than the last generation of B2B leaders.

The Real Lesson: Navan Didn’t Dodge AI Disruption. It’s on the Winning Side of It.

Navan is not up because it dodged the AI disruption that is repricing software. It is up because it is built on the winning side of that exact disruption:

AI as a margin and distribution engine instead of a threat.

Competitor consolidation flowing in instead of out.

The market is not being irrational about Navan while being rational about everyone else. It is being consistent. It is rewarding the company whose model points the same direction the future is pointing, and selling everything pointed the other way.

The AI model is a commodity. The business model is the moat. Navan is what it looks like when a company is on the right side of both.

Gartner: AI Software Spending to Grow 60% to

Gartner: Software Spend Now $1.44 Trillion in 2026, Revised Back Up to 15.1%. The Slowdown Never Came. Are You Grabbing That Budget?

The Saa S Rout of 2026 Is Even Worse Than You Think. For the First Time Ever, Software Now Trades at a Discount to the S&P 500.

Gartner: AI Software Spending to Grow 60% to

Gartner: Software Spend Now $1.44 Trillion in 2026, Revised Back Up to 15.1%. The Slowdown Never Came. Are You Grabbing That Budget?

The Saa S Rout of 2026 Is Even Worse Than You Think. For the First Time Ever, Software Now Trades at a Discount to the S&P 500.

Get from

Key Takeaways

-

AI VC AI Mentor: Digital Jason + Amelia AI Startup Benchmarking

-

AI Agent Playbook Free e Books

e Book: Hiring a Great VP of Sales e Book: Raising Capital e Book: The First $1m ARR -

University All Posts Podcasts The Top CROs VC Fundraising Top Videos Q&A Best of Saa Str #1 Bestselling Book Search Everything Join the Community

-

Free e Books

e Book: Hiring a Great VP of Sales e Book: Raising Capital e Book: The First $1m ARR -

AI Annual 2026 Events Overview Sponsors

Event Sponsorship Media Sponsorship