Asus Exits Smartphone Market 2025: Why Zenfone & ROG Phones Are Done

Introduction: The End of an Era for Asus Mobile

The smartphone industry just witnessed another landmark moment: Asus has officially discontinued its mobile phone division, marking the exit of one of the last independent Android manufacturers with any meaningful market presence. CEO Jonney Shih's recent announcement confirmed that neither the Zenfone line nor the ROG Phone gaming series will receive new models moving forward, freezing both product families indefinitely. This decision was confirmed in a report by NotebookCheck.

This announcement resonates far beyond Asus enthusiasts. It signals a fundamental shift in how hardware manufacturers view the mobile market's profitability and sustainability. Unlike a typical product pause or market repositioning, Asus's decision carries permanent undertones—the company explicitly stated "no longer add new mobile phone models in the future," language that suggests this isn't a temporary strategic retreat but rather a recognition that smartphone manufacturing no longer aligns with corporate growth objectives, as noted by Android Police.

The decision wasn't made in isolation. Over the past eighteen months, we've witnessed cascading exits from major players: LG Mobile's shutdown in 2021, Microsoft's abandonment of Windows Phone, and most recently, Samsung's consolidation of its Galaxy lineup to core models only. These departures share a common denominator: the fundamental mathematics of smartphone profitability no longer works for manufacturers without world-dominating scale.

What makes Asus's exit particularly significant is the company's operational sophistication. Asus isn't a struggling startup; it's a diversified hardware conglomerate with strong positions in gaming laptops, networking equipment, and components. The company's decision to reallocate resources away from smartphones—despite operational competence—indicates that even well-managed, experienced manufacturers have determined that mobile devices represent a capital-intensive, margin-compressing business with limited upside.

This comprehensive analysis examines why Asus made this decision, what it reveals about smartphone market dynamics, how competing manufacturers are responding, and what consumers should expect moving forward. We'll also explore the broader implications for the industry and discuss alternatives for users who relied on Asus mobile devices.

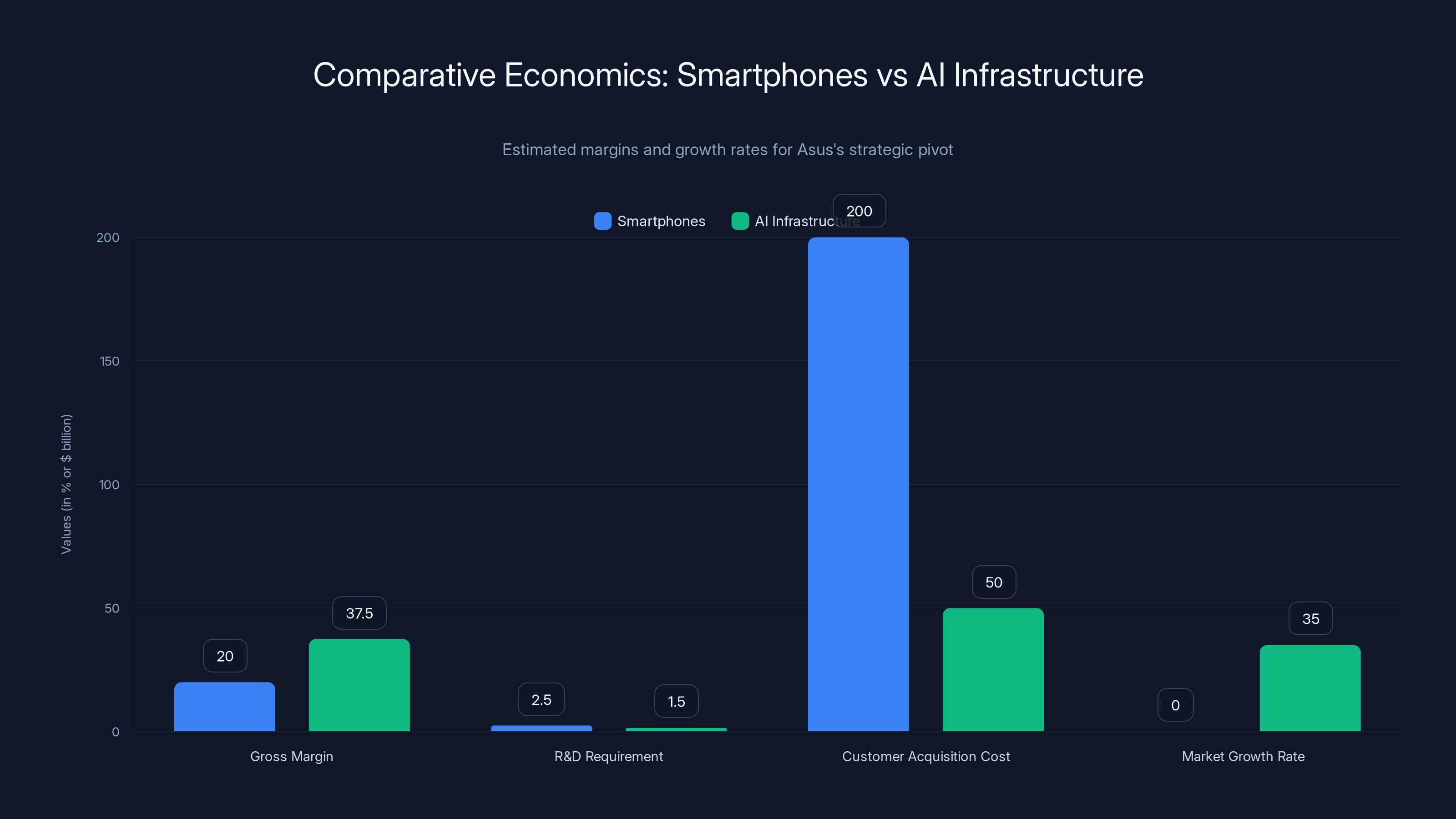

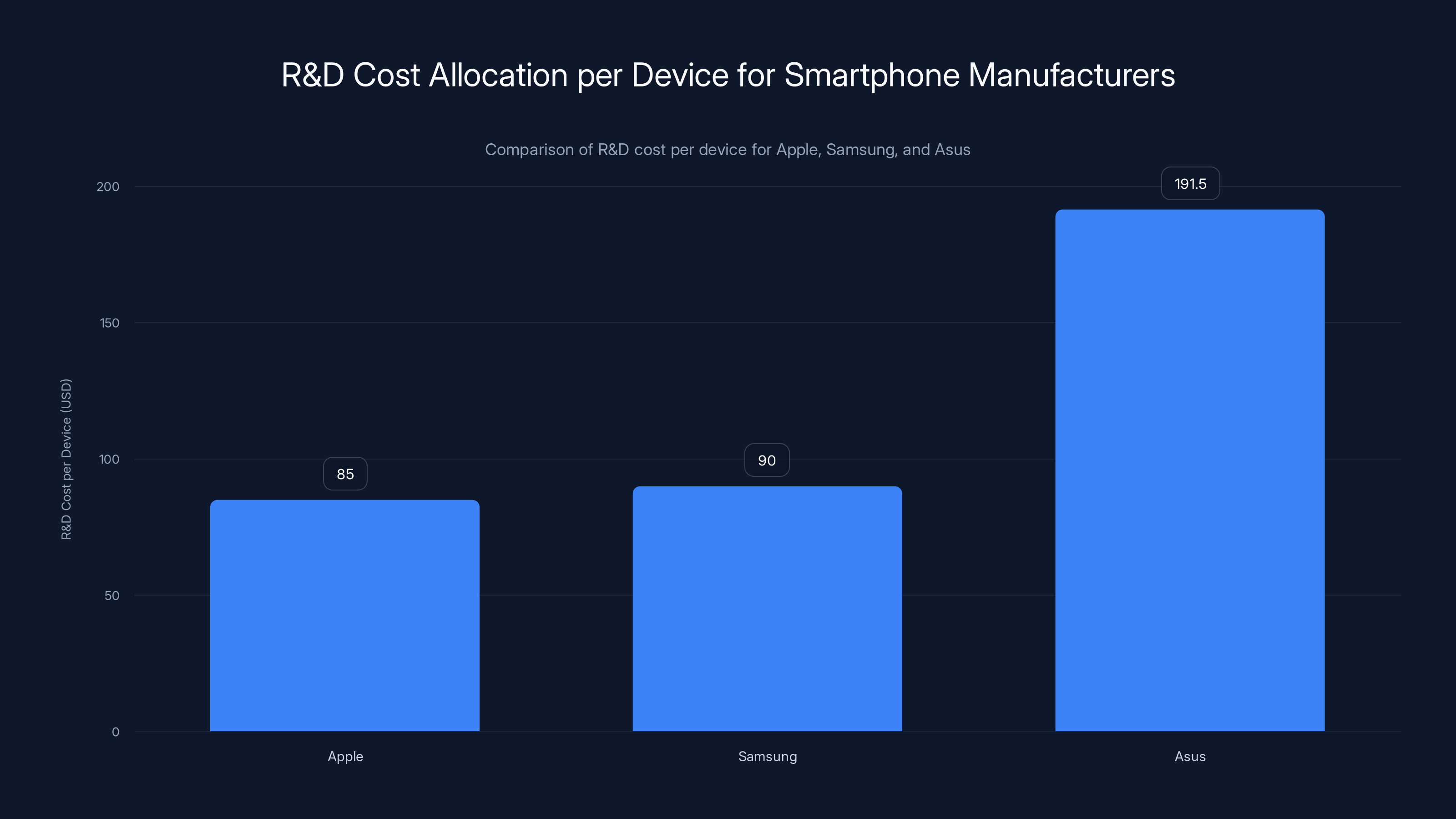

Asus faced challenges with low smartphone shipments (13.5 million) and lower margins (20%) compared to AI opportunities with higher margins (37.5%) and growth (35%). Estimated data.

The Smartphone Profitability Crisis: Why Even Strong Brands Are Exiting

Understanding the Economics of Modern Smartphone Manufacturing

Smartphone manufacturing looks deceptively simple from a consumer perspective: companies design chips, assemble components, sell finished devices. The reality involves exponentially more complexity. Each new smartphone generation demands investments across multiple domains: proprietary chip development, manufacturing tooling updates, software optimization, supply chain establishment, regulatory compliance in 150+ countries, and marketing campaigns to differentiate commoditized hardware.

These costs have grown substantially over the past decade. When Samsung released the Galaxy S8 in 2017, the company spent approximately

Here's where the mathematics breaks down for mid-tier manufacturers: these R&D investments must be amortized across unit sales. Apple can justify massive R&D spending because the company sells 230-240 million iPhones annually. Samsung moves 250-270 million Galaxy devices yearly. But Asus? In its best years, Asus shipped perhaps 12-15 million devices globally—roughly 5-6% of Apple's volume.

This creates a brutal unit economics problem. If Asus needs to invest

The Replacement Cycle Collapse

Historically, smartphone profitability relied on rapid replacement cycles. Through 2014-2017, consumers regularly upgraded devices every 18-24 months, driven by meaningful performance improvements, camera advances, and battery life enhancements. This created predictable cash flows: companies could launch annual flagships with confidence that 20-30% of their user base would upgrade immediately.

That paradigm has fundamentally shifted. Current smartphone replacement cycles have extended to 36-48 months, according to industry analysis. Why? Because performance saturation has arrived. A flagship Android processor from 2021 handles 99% of real-world tasks identically to 2024 models. Battery improvements are incremental—perhaps 5-10% better in ideal conditions. Camera quality matters, but computational photography has reached a plateau where further improvements yield diminishing returns.

Consumers have internalized this reality. They're keeping phones longer because manufacturers have optimized performance to a point where further investment generates insufficient value perception. This directly impacts the revenue models that sustained smartphone manufacturers for fifteen years. Annual device launches become harder to justify when devices remain functional and competitive for 4+ years.

For Asus specifically, this presented an acute problem. The company never achieved the marketing dominance or ecosystem lock-in that Apple and Samsung established. Asus customers could switch to competitive devices without losing anything—no proprietary services, no ecosystem integration, no switching costs. This meant Asus had to compete purely on hardware features, where differentiation opportunities were increasingly marginal.

Chinese Competition and Margin Compression

Asus faced another structural headwind: intensifying competition from Chinese manufacturers who operate under fundamentally different business models. Companies like Xiaomi, OPPO, Vivo, and Realme compete aggressively on price, accepting lower per-unit margins in exchange for market share and scale. These companies achieve profitability through extreme volume, supply chain optimization, and reduced marketing spend.

Xiaomi's approach exemplifies this strategy. The company operates with gross margins of 10-12% on many device lines—roughly half the margins Apple achieves. But Xiaomi compensates through volume scale (180+ million devices annually) and services revenue from China's massive installed base. This creates a competitive environment where Asus's mid-market positioning becomes untenable.

Asus couldn't compete on price because the company lacked Xiaomi's manufacturing scale and Chinese domestic market dominance. Asus couldn't compete on premium positioning because Samsung and Apple owned that space. This left Asus squeezed in the middle—exactly where smartphone manufacturers go to die.

For context, Asus's Zenfone line achieved roughly 2-3% global market share at peak, while ROG Phones captured perhaps 0.5-1% of the gaming-specific segment. These weren't catastrophic market shares, but they weren't sufficient to justify the required R&D investment and infrastructure costs.

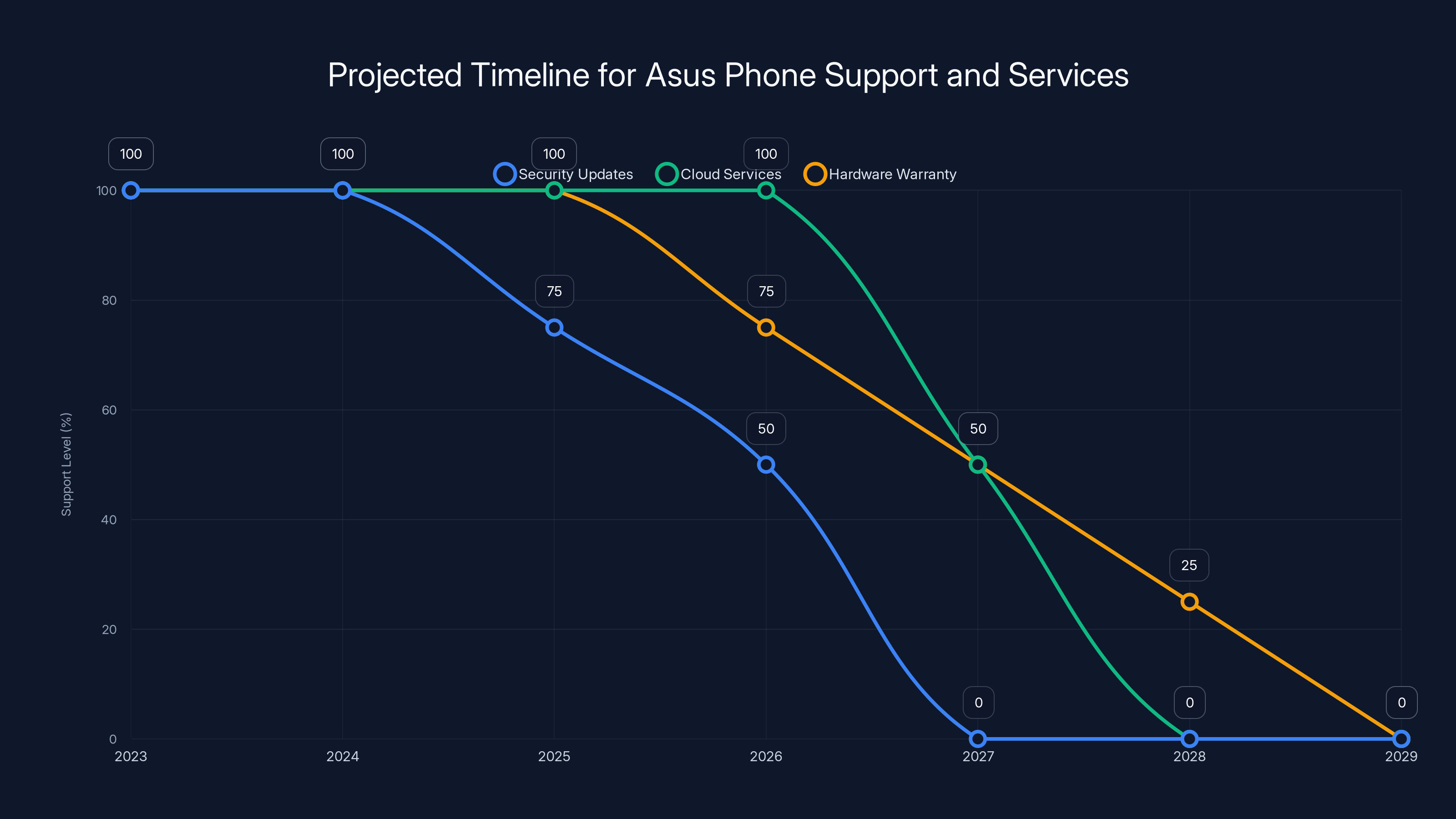

Estimated data shows a decline in support for Asus phones, with security updates possibly ending by 2026 and cloud services by 2028.

The Zenfone Story: Compact Design and Budget Positioning That Couldn't Sustain

What the Zenfone Represented in the Market

The Zenfone line, which debuted in 2014, carved out a specific market position: compact, feature-rich smartphones at aggressive prices. During the Zenfone 2 era (2015), Asus devices delivered flagship processors and solid cameras at price points $100-200 below equivalent Samsung or Apple offerings. This positioning resonated with budget-conscious consumers and tech enthusiasts who valued component value over brand prestige.

The Zenfone 2 specifically achieved meaningful commercial success, shipping 10+ million units annually at its peak. The device offered a 5.5-inch display, Intel Atom processor, 4GB RAM, and a 13MP camera for roughly $350-400—genuinely competitive specifications for the 2015 timeframe. Asus's design philosophy emphasized practical features: dual SIM slots, expandable storage, and respectable battery capacity, which appealed to international users and power users.

However, Asus failed to establish the software differentiation and update commitment that sustained competitors' market positions. Samsung and Apple built loyal user bases partly through lengthy software support guarantees and regular feature updates. Asus committed to updates more conservatively. The Zenfone 2, launched with Android 5.0, received updates to Android 6.0 but didn't achieve the update longevity that Samsung's flagships garnered.

This created a perception problem: Asus devices were commodities with corporate branding, not investments with long-term value propositions. Budget-conscious consumers could buy a Xiaomi Redmi device at identical price points with comparable specs, or stretch budget for a Samsung device with superior software support commitment. The middle ground that Zenfone occupied proved increasingly squeezed.

The Mid-Market Positioning Trap

By the Zenfone 5 generation (2018), Asus had abandoned aggressive pricing and moved upmarket—attempting to compete at $500-700 price points where Samsung Galaxy A and Galaxy S devices dominated. This repositioning abandoned the budget segment where Asus had some differentiation while simultaneously refusing to match premium competitors' features or brand equity.

The fundamental error: Asus attempted to compete in every market segment simultaneously. The company's portfolio included budget Zenfones (Z0001-Z5), mid-range devices (Zenfone 5-7), and premium variants (Zenfone Max series with extended batteries). This sprawl meant R&D investment spread thin across incompatible market segments, with insufficient scale in any individual segment to justify independent development.

Contrast this with Samsung's approach: Samsung concentrates development effort into core Galaxy S flagships and Galaxy A budget line, achieving sufficient scale within each segment to justify differentiated R&D. Asus attempted this strategy but with 10x lower volumes, creating a unit economics disaster.

By 2022-2023, Zenfone devices had largely disappeared from major markets. Best Buy removed Zenfone stock. Amazon's Zenfone selection diminished to discontinued models. Carrier partnerships evaporated. Without retail visibility, Asus couldn't build brand momentum, perpetuating a death spiral: fewer retail partners → fewer consumers aware of devices → lower sales → less leverage for retail partnerships.

Software Support and Consumer Expectations

A critical factor in Zenfone's decline was software update inconsistency. Consumers increasingly demanded long-term support guarantees. Apple promised 5-6 years of iOS updates. Samsung began offering 3-4 years of OS updates and 5 years of security patches. Asus typically committed to 2-3 years maximum, sometimes shorter.

For consumers making multi-year device investments, this represented an unacceptable risk. A $600 Zenfone purchased in 2020 might receive only 18-24 months of OS updates, while Samsung's equivalent device would receive 36+ months. The financial calculus favored Samsung despite higher initial cost.

This reflects a broader reality: software support has become a primary purchasing criterion for informed consumers. Asus never fully embraced this reality, continuing to treat software as a commodity feature rather than a core value proposition. The company's Zen UI customization, while feature-rich, never achieved the polish or consistency of Samsung's One UI or Google's Android implementations.

The ROG Phone Chronicles: Gaming Ambitions in a Specialized Niche

The Gaming Smartphone Opportunity That Wasn't

Asus's ROG (Republic of Gamers) brand represents decades of gaming hardware credibility—the company dominates high-end gaming laptops and has significant presence in gaming peripherals. The ROG Phone line, launched in 2018, seemed to be a natural extension: Android gaming devices optimized for demanding mobile titles with specialized cooling, haptic feedback, and gaming-oriented accessories.

The strategic logic appeared sound. Mobile gaming represents the largest segment of the gaming industry by revenue. Games like PUBG Mobile, Call of Duty Mobile, and Genshin Impact demonstrate that console-quality gaming experiences can run on smartphones. Gaming enthusiasts represent a premium consumer segment willing to pay substantial prices for specialized hardware.

ROG Phones embodied this vision: devices with thermal management systems worthy of gaming laptops, vapor chambers, specialized cooling fans, high refresh rate displays (144 Hz on later models), and customizable RGB lighting. Later iterations introduced side-mounted gaming buttons, specialized cases, and cooling docks—accessories that leveraged Asus's gaming peripheral expertise.

The ROG Phone line achieved meaningful innovation. The integration of Qualcomm's Snapdragon processor with custom thermal engineering produced genuinely superior gaming performance compared to standard flagship devices. Benchmarks consistently showed 10-15% higher sustained performance in demanding games due to superior thermal management preventing thermal throttling.

The Fundamental ROG Phone Problem: Niche Within a Niche

Despite technical excellence, ROG Phones never achieved significant commercial success. Why? The market for specialized gaming smartphones proved dramatically smaller than anticipated. Here's the brutal economics:

The total smartphone gaming market is worth $100+ billion annually, but that's distributed across 1.5+ billion devices. Gaming is one of many activities users perform on smartphones. Conversely, true hardcore gamers represent maybe 2-3% of smartphone users—individuals who would prioritize frame rates, thermal performance, and specialized controls.

For this audience, ROG Phones made technical sense. But Asus charged premium prices—

The ROG Phone thus occupied an awkward position: too expensive for casual gamers, too specialized for enthusiasts who preferred dedicated gaming hardware. Casual gamers—the actual massive market—upgrade smartphones every 3-4 years based on general-purpose needs. They don't prioritize gaming performance because any modern flagship plays any mobile game fluidly.

Market data supports this analysis. Peak ROG Phone shipments reached perhaps 500,000-800,000 units annually—less than 0.3% of global smartphone shipments. Compare this to Samsung's gaming-optimized Galaxy Z Fold (which sold 1+ million units annually) or even OnePlus's gaming-focused devices (which exceeded ROG shipments despite less specialized hardware).

Failed Ecosystem and Accessory Strategy

Asus attempted to build a ROG Phone ecosystem similar to how Apple creates ecosystem lock-in around iPhones. The company developed specialized cooling fans, gaming triggers, protective cases with integrated controls, and gaming docks. These accessories theoretically differentiated ROG Phones from standard devices.

However, accessory-driven differentiation only works if the core device already achieved massive adoption. Apple can sell accessory ecosystems because 1+ billion iPhone users represent a viable market. Asus could never accumulate sufficient ROG Phone installed base to justify accessory development. The company essentially invested in ecosystem infrastructure before establishing baseline device adoption—a backwards-looking strategy that doomed the initiative.

Additionally, third-party gaming controllers became commodified. Companies like Backbone and Razer developed universal smartphone gaming controllers compatible with any device. These eliminated ROG Phone's accessory advantage while costing less than Asus's proprietary solutions. Consumers could buy a $100 universal controller and use it across smartphones, making proprietary ROG gaming hardware economically irrational.

The Thermal Management Innovation That Still Couldn't Save ROG

From a pure engineering perspective, ROG Phones represented sophisticated thermal management. Later-generation models incorporated vapor chamber cooling systems, variable fan speeds, and active heat sinks—technology borrowed from gaming laptop design. In sustained gaming tests, ROG Phones demonstrated thermal performance advantages that translated to meaningful FPS improvements in demanding titles.

Yet even this technical excellence couldn't overcome market realities. Consumers chose devices based on ecosystem, brand recognition, software support, and general-purpose capability—not thermal margin advantages invisible in everyday usage. The ROG Phone's cooling superiority mattered only during extended gaming sessions, which represented perhaps 1-2% of daily device usage for even dedicated gamers.

Moreover, smartphone SoC (System-on-Chip) efficiency improved dramatically over ROG Phone's lifecycle. By 2023-2024, standard Snapdragon and Apple processors achieved such efficiency that thermal management became less critical. An iPhone 15 Pro or Samsung Galaxy S24 Ultra handled demanding games without throttling despite lacking ROG Phone's specialized cooling—because chip efficiency improvements eliminated the necessity.

Asus's pivot to AI infrastructure is driven by higher gross margins and market growth rates compared to smartphones, with lower R&D and customer acquisition costs (Estimated data).

The Broader Industry Context: When Scale Becomes Everything

The Smartphone Industry's Winner-Take-Most Dynamics

Smartphone manufacturing exhibits extreme winner-take-most economics. The top 3-5 manufacturers control 70-75% of global smartphone volume and an even higher proportion of profits. This concentration happens because smartphones require massive scale to amortize infrastructure investments.

Consider Apple's position: with 230+ million annual iPhone sales, the company can justify:

- $20+ billion annual R&D investment for custom chip design

- Vertical integration of components including display technology, modem design, sensor manufacturing

- Global supply chain infrastructure with direct relationships with component suppliers

- Manufacturing investments across multiple Asian countries

- Software development spanning iOS, chipset drivers, and optimization

- Customer service infrastructure with 500+ retail locations globally

These investments create a virtuous cycle: superior products justify premium pricing → premium pricing funds continued R&D → continued R&D produces superior products → repeat. Apple's gross margins on iPhones exceed 40% globally because manufacturing at scale enables both volume advantages and pricing power.

Compare this to Asus's situation with 12-15 million devices: the company couldn't justify vertical integration, couldn't maintain proprietary supply chains, and couldn't fund R&D at comparable levels. Asus attempted to compete with Samsung's strategy while operating at 5% of Samsung's volume—structurally impossible.

Why Samsung Survives (Barely) While Asus Doesn't

Samsung, with 250-270 million annual smartphone shipments, maintains smartphone operations despite structural profitability challenges. How? Through diversification and component vertical integration. Samsung manufactures display panels, DRAM, NAND storage, and processors for its devices—and sells excess capacity to competitors. This generates profitable revenue streams independent of smartphone sales.

When Samsung's smartphone business faces margin pressure, display and memory divisions remain profitable. Apple has undertaken similar vertical integration (chips, custom silicon for services). Asus lacks this component manufacturing base. The company makes motherboards, graphics cards, and system components, but none of these integrate backward into smartphone component manufacturing.

This explains why Asus exited while Samsung continues: Samsung's business model supports smartphones even at reduced profitability because component sales offset losses. Asus's business model lacks this advantage. Smartphone operations drain resources from higher-margin segments (gaming laptops generating 25-30% gross margins, server boards generating 20%+ margins).

The LG Mobile Precedent and Pattern Recognition

LG Electronics provides a direct historical precedent. LG once represented a significant smartphone manufacturer—the world's third-largest in 2011 with 150+ million devices shipped annually. Yet LG exited mobile in 2021 after accumulating $4+ billion in losses over 10 years.

LG's smartphone history follows an instructive pattern:

- 2011-2012: Position as third-largest manufacturer, reasonable profitability

- 2013-2015: Margin compression as Samsung and Chinese competitors intensify competition

- 2016-2018: Attempts at niche positioning (G series premium phones, V series with specialized features)

- 2019-2020: Accelerating losses, brand deterioration, retail channel collapse

- 2021: Formal exit announcement; final devices shipped

Asus's trajectory mirrors this pattern almost exactly, compressed into a shorter timeframe. Where LG took 10 years to accumulate losses and finally exit, Asus accelerated the timeline by reducing investment earlier and recognizing the unsustainable mathematics more quickly. This arguably represents better management—cutting losses earlier rather than subsidizing a doomed division for a decade.

The Chinese Manufacturer Exception and Ecosystem Lock-In

Chinese manufacturers (Xiaomi, Oppo, Vivo, Realme) continue smartphone operations despite margins that would be unacceptable to Western companies. Why?

These companies operate fundamentally different business models:

- Domestic market dominance: Xiaomi controls roughly 15% of China's massive domestic market—150+ million units annually just from China. This scale supports infrastructure investments.

- Services integration: Xiaomi, Oppo, and Vivo offer cloud services, digital payments, smart home ecosystems, and content services that generate profits independent of device sales.

- Manufacturing integration: These companies operate factories and supply chains optimized for volume, achieving cost structures Western manufacturers cannot match.

- Lower labor costs: Smartphones manufactured in China benefit from regional labor advantages compared to manufacturing elsewhere.

- Government support: Chinese manufacturers receive indirect support through domestic market protection and supply chain preferences.

Asus lacked all of these advantages. The company couldn't generate ecosystem lock-in because no comparable Asus ecosystem existed. Consumers bought Asus laptops or peripherals independently of mobile devices—no platform integration motivated cross-ecosystem purchases.

The AI Pivot: Where Asus Is Actually Making the Strategic Bet

Why AI Infrastructure Became More Attractive Than Smartphones

Asus's strategic reorientation toward AI infrastructure reflects rational capital allocation decisions. The company's statement emphasized investments in "AI tools, servers, robotics, and smart wearables." This pivot isn't random—it's driven by fundamentally superior business dynamics compared to smartphones.

Asus's server and infrastructure business operates on completely different economics than consumer smartphones. Enterprise customers purchasing AI server infrastructure don't price-shop as aggressively as consumers. A company investing $50 million in GPU clusters for AI training makes purchasing decisions based on performance, reliability, and vendor support—not cost optimization. This enables significantly higher gross margins (35-40%+) compared to smartphone manufacturing (15-25%).

Moreover, AI infrastructure represents an expanding market with secular growth, while smartphones face replacement cycle maturation. The global AI server market is projected to grow 30-40% annually through 2027, while smartphone shipments remain essentially flat or slightly declining.

Asus's board of directors logically concluded:

Allocate capital toward high-margin, growing markets (AI infrastructure) rather than low-margin, mature, intensely competitive markets (smartphones).

This is rational business strategy, not corporate whim.

AI Server Economics: The Profitability Difference

Here's where the economics diverge dramatically between smartphones and AI infrastructure:

Smartphone segment:

- Gross margin: 15-25%

- R&D requirement: $2-3 billion annually for competitive devices

- Customer acquisition cost: $100-300 per device (marketing + distribution)

- Upgrade cycle: 36-48 months

- Competitive intensity: Extreme (100+ manufacturers)

- Market growth rate: -2% to +2% annually

AI Infrastructure segment:

- Gross margin: 35-45%

- R&D requirement: $500 million annually (significant but lower than smartphones)

- Customer acquisition cost: $5,000-50,000 per enterprise deal (minimal per-unit cost)

- Upgrade cycle: 3-5 years

- Competitive intensity: Moderate (20-30 significant manufacturers)

- Market growth rate: 30-40% annually

The financial case is decisive. A

This represents 50-100% better return on capital for AI infrastructure compared to smartphones. When capital is scarce and opportunity cost is high, rational companies allocate toward superior returns.

Robotics and AI-Powered IoT Devices

Beyond server infrastructure, Asus's pivot toward robotics and smart IoT devices represents another strategic reorientation. These segments share common characteristics that make them more attractive than smartphones:

Robotics market dynamics:

- Global market size: $60+ billion annually, growing 12-15% yearly

- Gross margins: 25-35% (substantially higher than smartphones)

- Customer concentration: Enterprise/industrial purchasers with long sales cycles

- Differentiation opportunities: Software, AI integration, specialized capabilities

- Competitive landscape: Less saturated than smartphones

Asus previously developed collaborative robots and manufacturing automation equipment. Redeploying smartphone engineering talent toward robotics represents a higher-value application of engineering capabilities. A software engineer who optimized Android thermal management could optimize robot operating systems and control software—applying similar expertise toward higher-margin products.

Smart wearables and IoT:

- Market size: $100+ billion annually (and expanding rapidly)

- Growth rate: 8-12% annually

- Gross margins: 30-40% (higher than smartphones)

- Differentiation: Through AI integration and software capabilities

- Competitive intensity: Moderate (unlike smartphones which feature 100+ competitors)

Asus's previous wearable efforts (smartwatches, fitness trackers) were modest, but integrating AI capabilities into wearables creates opportunities for meaningful differentiation. AI-powered health monitoring, predictive analytics, and personalized recommendations generate value that justifies premium pricing.

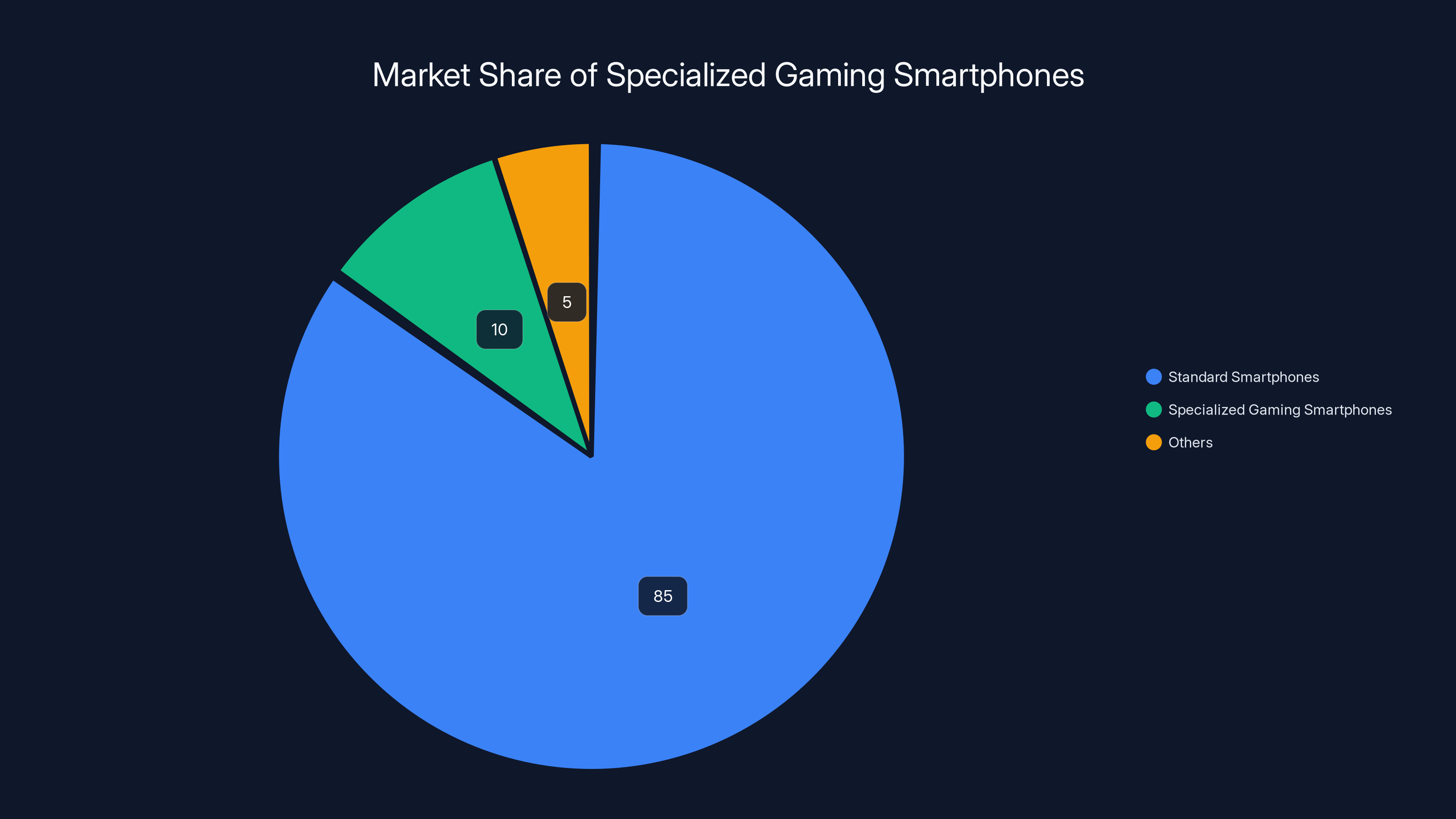

Estimated data shows specialized gaming smartphones hold a small market share within the $100 billion smartphone gaming industry, highlighting the niche appeal of devices like the ROG Phone.

Consumer Impact: What Happens to Existing Asus Phone Users?

Software Support for Existing Devices

Asus has not explicitly addressed software support for existing Zenfone and ROG Phone users, but historical patterns suggest limited expectations. When manufacturers exit segments, they typically:

- Continue security updates for 12-18 months (if customers are vocal enough)

- Discontinue feature updates immediately

- Shut down cloud services and online features within 2-3 years

- End hardware warranty service within 3-5 years

For users who purchased Zenfone or ROG Phones in 2023-2024, this timeline means:

- 2025-2026: Security updates possible but not guaranteed

- 2026+: No updates; devices become increasingly vulnerable to security issues

- 2027-2028: Cloud services (backup, Asus account features) shut down

- 2029+: Hardware repairs become impossible through official channels

This isn't unique to Asus—it reflects how technology companies manage legacy products. However, it creates genuine hardship for users who invested $400-1,200 in devices now entering 2-3 year usage periods.

Repair and Parts Availability

Asus will likely maintain parts availability through official channels for 2-3 years following the exit announcement, though repair pricing may increase as inventory becomes scarce. Third-party repair shops may offer longer-term support as they source used parts from devices entering the secondary market.

For comparison, LG phones continue receiving third-party repairs 3-4 years after company exit, but availability and pricing are substantially worse than contemporary devices. Users should anticipate:

- Display replacements: 100-200 for Samsung or iPhone)

- Battery replacements: 50-100 for mainstream devices)

- Parts scarcity: Availability diminishes each quarter

- Repair expertise decline: Independent shops gradually stop offering repairs as device volume decreases

Trade-In and Resale Market Implications

Asus's exit will suppress resale values for Zenfone and ROG Phones. Devices currently trading at 40-50% of retail value will likely decline to 25-35% as:

- Buyers become aware that software support is ending

- Alternative devices prove more economical despite higher initial prices

- Brand perception deteriorates

- Repair infrastructure diminishes

Users holding current Zenfone or ROG Phones should consider selling before values plummet further. Within 6-12 months, secondary market values will likely stabilize at depressed levels (35-50% lower than current resale prices).

Migration Path for Current Asus Users

Current Asus smartphone users should evaluate migration options based on use case:

For Zenfone users prioritizing budget and practical features:

- Xiaomi Redmi series offers similar positioning (compact, practical, budget-friendly) with better software support commitment

- Samsung Galaxy A series provides slightly higher prices but superior update guarantees

- Google Pixel 7a or Pixel 8a offer best-in-class software support (guaranteed 3+ years OS updates, 4+ years security patches) at comparable price points

For ROG Phone users prioritizing gaming performance:

- OnePlus flagships (OnePlus 12) offer strong gaming performance at lower prices than ROG Phone equivalents

- iPhone 15 Pro/Pro Max deliver superior gaming experience through Apple Arcade and optimized game support

- Samsung Galaxy S24 Ultra provides competitive gaming performance with superior software ecosystem

For users valuing Asus's build quality and design:

- Nothing Phone offers distinctive industrial design with transparent back

- OnePlus devices maintain similar design philosophy with excellent build quality

- Samsung Galaxy devices offer proven durability and parts availability

Broader Industry Implications: The Smartphone Market's Maturation

The Death of Independent Smartphone Manufacturers

Asus's exit represents a broader pattern: independent smartphone manufacturers are functionally extinct. The industry has consolidated to companies with sufficient scale or strategic advantages to sustain operations:

Companies with mass-market presence:

- Apple (230+ million annual units)

- Samsung (250+ million annual units)

- Chinese manufacturers (Xiaomi, Oppo, Vivo, Realme collectively 500+ million units)

Companies with strategic differentiation:

- Google (Pixel) - leverages search ecosystem, software optimization

- OnePlus - maintains cult following and design-focused positioning

- Nothing - positions as design innovator

Companies operating at extreme scale:

- Huawei (mainland China focus despite Western restrictions)

- Motorola (ultra-budget positioning)

Notably absent: independent manufacturers without vertical integration, ecosystem advantage, or extreme scale. HTC exited smartphone manufacturing in 2018. LG exited in 2021. Asus exits in 2025. This is not coincidental—it reflects structural market forces eliminating companies without sufficient advantages.

The implication: smartphone manufacturing is permanently consolidating toward companies with 50+ million annual units minimum or strategic ecosystem advantages. Mid-scale manufacturers cannot sustain operations.

The Role of Ecosystem Lock-In

Successful smartphone manufacturers increasingly rely on ecosystem integration rather than hardware differentiation. Apple succeeds through ecosystem lock-in (iPhone, iPad, Mac, AirPods, Apple Watch all integrate seamlessly). Samsung benefits from Android ecosystem but differentiates through custom software (One UI) and services.

Asus never established comparable ecosystem lock-in. Unlike Apple, Asus consumers don't necessarily use Asus laptops alongside Asus phones. Unlike Samsung, Asus didn't develop compelling software experiences that justified staying within the brand ecosystem.

This lesson suggests that future smartphone viability increasingly depends on ecosystem breadth. Companies selling only smartphones face structural disadvantages against diversified manufacturers with multiple product categories.

Software Support as Core Value Proposition

As hardware differences diminish, software support duration has become a primary purchasing criterion. Apple's 5-6 year update cycle, Samsung's 3-4 year commitment, and Google's 3-year OS + 4-year security update guarantee differentiate these brands from manufacturers offering 18-24 month support.

Asus failed to establish similar update commitments, which depressed brand perception. This suggests future manufacturers must make explicit, lengthy software support guarantees as a core value proposition—not an afterthought.

The Rise of Services-Based Revenue Models

Profitable smartphone operations increasingly require services revenue streams independent of device sales. Apple generates

Asus attempted minimal services integration. The company had no app store, no cloud service comparable to Samsung Cloud, and minimal content partnerships. This meant Asus depended entirely on device hardware margin—insufficient in modern competitive landscape.

Future successful manufacturers will likely bundle services (cloud storage, AI features, productivity tools, entertainment access) as standard with device purchases, generating recurring revenue streams that offset hardware margin compression.

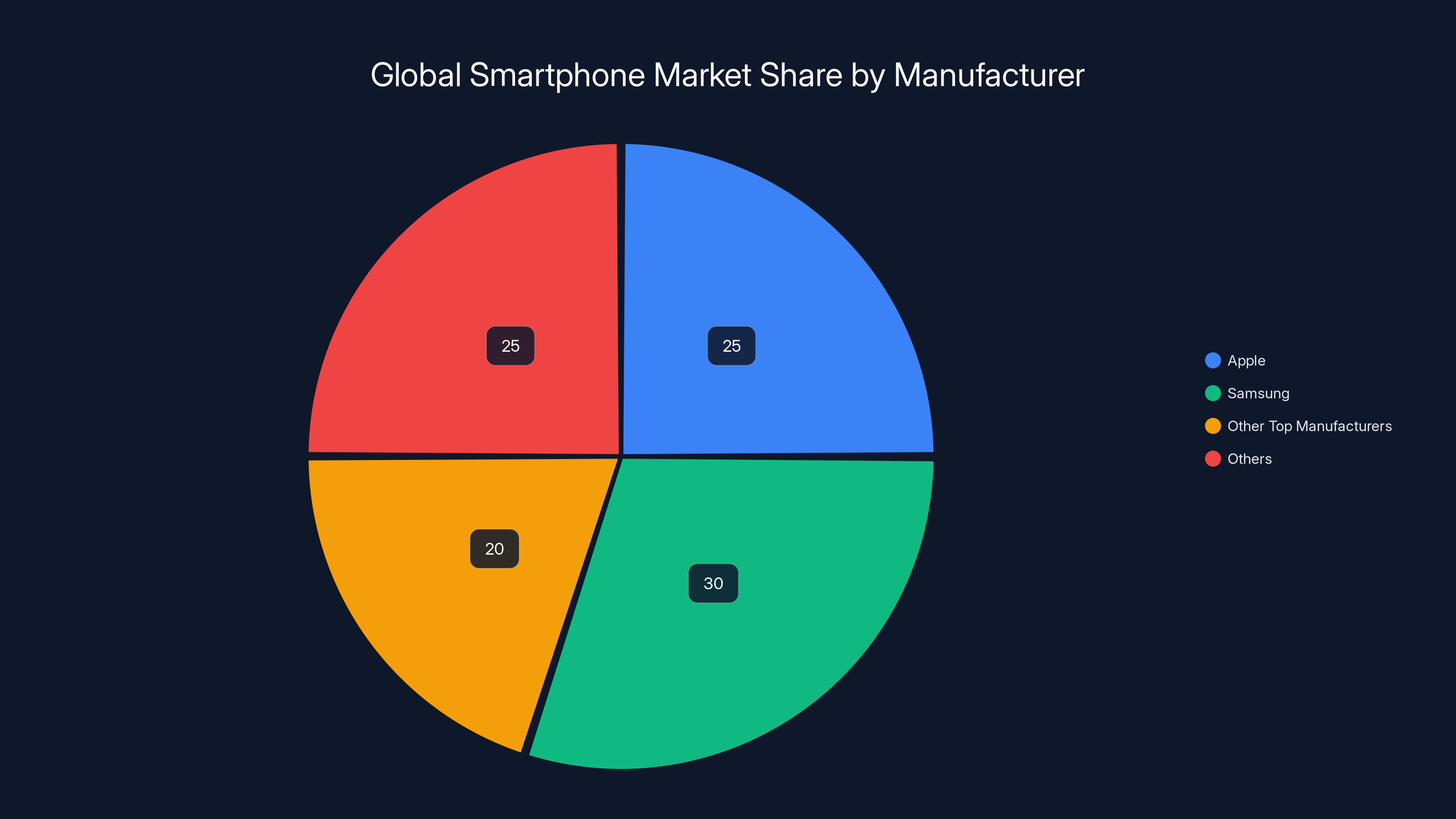

Apple and Samsung together control over half of the global smartphone market, highlighting the winner-take-most dynamics in the industry. Estimated data based on shipment volumes.

Alternative Smartphone Options for Enterprise and Developer Audiences

Enterprise-Grade Smartphone Requirements

Asus previously marketed phones to business customers, positioning Zenfone's durability and battery life as business-appropriate. Companies evaluating replacements should prioritize:

Security and Update Commitment:

- Apple iPhone (5-6 year guarantee)

- Samsung Galaxy (3-4 year guarantee)

- Google Pixel (3 years OS, 4 years security)

Durability and Repairability:

- iPhone 15 Pro: Industry-leading durability, officially supported repairs through Apple Care+

- Samsung Galaxy S24 Ultra: Excellent durability, extensive parts availability

- Framework Phone (upcoming): Designed for repairability, though not yet released

Cost Optimization:

- Samsung Galaxy A series: Lower prices than flagships, solid reliability

- Google Pixel 8a: Exceptional value, guaranteed 3 years updates

- OnePlus 12: Strong performance at moderate prices

Developer-Focused Smartphone Alternatives

Developer communities that supported Asus phones (through custom ROMs, developer mode features, and enthusiast communities) should consider:

For Android development and customization:

- Google Pixel: Direct Android updates, excellent developer tools, bootloader flexibility

- OnePlus: Historically developer-friendly, good Oxygen OS customization

- Nothing Phone: Open to customization, active developer community

For Gaming and Performance:

- iPhone 15 Pro Max: Unmatched GPU performance, excellent sustained gaming performance

- Samsung Galaxy S24 Ultra: Powerful GPU, excellent thermals, gaming optimizations

- OnePlus 12: Strong performance, cooling technology, gaming partnerships

For Productivity and Work:

- iPhone 15 Pro: Best-in-class productivity apps, seamless integration with Mac/iPad

- Samsung Galaxy S24 Ultra: Largest display options, excellent S-Pen support, desktop-class productivity features

- Google Pixel 8 Pro: Best AI integration, excellent computational photography, clean Android experience

Cost-Effective Smartphone Automation Solutions

For teams and developers looking to automate smartphone-related workflows and content generation, platforms like Runable offer AI-powered automation at accessible price points ($9/month). Rather than maintaining custom smartphone tools, teams can leverage Runable's AI agents for:

- Automated device documentation generation

- Testing report creation and analysis

- API documentation automation for mobile development

- Workflow automation for smartphone deployment pipelines

- Content generation for mobile app documentation

Development teams previously reliant on Asus phones for testing can streamline their testing and documentation workflows through automation platforms, reducing reliance on specific hardware brands while improving efficiency.

The Smartphone Industry's Future Trajectory

Predicted Consolidation Timeline

Based on current market dynamics, we can predict smartphone manufacturer consolidation over the next 3-5 years:

2025-2026:

- OnePlus potentially faces pressure unless parent company BBK funnels sufficient resources

- Samsung consolidates to core Galaxy and Galaxy A lines only

- Mid-tier Chinese manufacturers merge or specialize

2026-2028:

- Motorola potentially divested or consolidated as market share erodes

- Only companies with 50+ million annual units or strategic advantages remain independent

- Google Pixel potentially divested if profitability targets aren't met

2028-2030:

- Smartphone market resembles auto industry: dominated by 3-4 major players with strong market positions

- Specialty/gaming phones extinct except as premium variants of flagship lines

- Services integration becomes standard rather than optional

This consolidation reflects fundamental market economics where extreme scale becomes mandatory for profitability.

Hardware Differentiation Becomes Harder, Software/Services Become Critical

As processor, display, and camera commoditize further, smartphone differentiation increasingly depends on:

- Software experience and customization (Samsung's One UI, Apple's iOS, Pixel's Android)

- Services integration (Apple Ecosystem, Google services, Samsung ecosystem)

- Design and aesthetics (though diminishing relevance)

- Brand ecosystem breadth (laptops, watches, tablets, smart home integration)

Companies competing on pure hardware innovation have failed. Future smartphone viability requires integrated software/services ecosystems and broader product category presence.

The Role of AI in Future Smartphone Strategy

Asus's pivot toward AI infrastructure implicitly acknowledges that consumer smartphones are becoming increasingly AI-dependent. Features like:

- Computational photography

- Real-time translation

- Voice recognition and synthesis

- Predictive assistance

- On-device AI processing

...require manufacturer competence in AI model development, hardware optimization for AI, and continuous model updates. Asus lacked these capabilities compared to Apple (A-series neural engine optimization), Google (Pixel neural processing), and Samsung (custom NPU development).

Future smartphone manufacturers must invest substantially in AI model development, hardware-software co-optimization for AI features, and on-device AI capabilities. Companies lacking AI expertise or infrastructure will struggle to compete.

Apple and Samsung have lower R&D costs per device due to higher sales volumes, while Asus faces higher per-device costs due to smaller sales figures. Estimated data based on provided ranges.

Learning from Asus's Exit: Strategic Lessons for Technology Companies

Market Concentration and Winner-Take-Most Dynamics

Asus's exit validates a critical principle: markets with extreme scale requirements and heavy R&D burdens naturally concentrate toward winner-take-most outcomes. Smartphones exemplify this dynamic:

- Entry requires $2-5 billion annual R&D minimum

- Differentiation requires proprietary components or software

- Profitability requires 50+ million annual unit scale

- Scale advantages compound (supply chain leverage, marketing efficiency, ecosystem effects)

Companies evaluating entry into such markets should recognize that mid-market positioning is functionally unviable. Success requires either:

- Dominant scale (100+ million units annually)

- Unique ecosystem integration (Apple, Google)

- Strategic geographic dominance (Chinese manufacturers in China)

- Extreme cost structure advantage (not available to Western manufacturers)

Without one of these advantages, market entry represents capital destruction.

The Importance of Exit Strategy and Capital Reallocation

Asus made a sophisticated decision: recognizing unsustainable market dynamics and reallocating capital toward higher-return opportunities (AI infrastructure). This approach prevented the LG scenario where tens of billions in losses accumulated before formal exit.

Organizations should develop mechanisms for regular strategic market participation reviews. Questions to address:

- Are we competing in markets with structural profitability challenges?

- Do we possess sufficient scale/differentiation to sustain profitability?

- Are capital returns in this market superior to alternative investments?

- What would full exit cost versus continued marginal losses?

Asus's leadership likely asked these questions honestly and concluded smartphone operations weren't justifiable.

Building Defendable Market Positions

Asus's failure to build ecosystem lock-in or sustained brand loyalty demonstrates that hardware-only differentiation is insufficient in competitive markets. Successful technology companies build on multiple layers:

- Hardware excellence (necessary but not sufficient)

- Software customization and optimization (Samsung's approach)

- Services ecosystem (Apple's approach)

- Broader product integration (Apple, Google, Samsung all integrate across categories)

Asus attempted hardware-only differentiation and failed. Future entrants must recognize that competitive advantage requires multiple reinforcing layers.

Conclusion: Understanding Market Maturity and Strategic Reorientation

Asus's official exit from smartphone manufacturing, while notable, reflects broader industry maturation rather than company-specific failure. The smartphone market has matured to the point where only companies with extreme scale, strategic differentiation, ecosystem integration, or geographic dominance can sustain profitability. Mid-market positioning has become structurally unviable.

For consumers, Asus's exit means:

- Existing Zenfone/ROG Phone users should anticipate shortened software support timelines (18-24 months of updates at most)

- Repair and parts availability will diminish significantly within 2-3 years

- Secondary market values will decline as buyers become aware of limited support

- No new Asus smartphones are coming, eliminating any hope for devices that captured previous user loyalty

For the broader industry, Asus's departure represents continued consolidation toward fewer, larger competitors with superior scale economics. By 2030, expect smartphone manufacturing to resemble the automotive industry: dominated by 3-5 major players, with specialty devices existing only as premium variants.

For Asus specifically, the reorientation toward AI infrastructure, robotics, and IoT devices represents rational capital allocation. These markets offer superior margins, faster growth rates, and opportunities for technology company diversification. The resources previously allocated to sustaining unviable smartphone operations can now fund higher-return strategic initiatives.

Users who invested in Asus smartphones should evaluate migration strategies now rather than waiting for support deterioration to force decisions. Organizations evaluating smartphone platforms should recognize that brand diversity will continue declining—and plan accordingly. And technology entrepreneurs should internalize the lesson that market scale requirements create winner-take-most dynamics that eliminate mid-market competitors.

The smartphone market's era of diverse manufacturers has definitively ended. The age of consolidated smartphone makers has begun.

FAQ

What was Asus's decision regarding smartphone manufacturing?

Asus announced it will no longer develop new smartphone models in any category, effectively discontinuing both the Zenfone and ROG Phone product lines indefinitely. CEO Jonney Shih stated the company will focus resources on AI infrastructure, robotics, and smart wearables instead. The company clarified that this represents a permanent strategic shift rather than a temporary pause, providing no timeline for potential smartphone re-entry.

Why did Asus decide to exit the smartphone market?

Asus exited because smartphone manufacturing exhibits extreme winner-take-most economics requiring 50+ million annual units for profitability—a scale Asus never achieved. The company shipped only 12-15 million devices annually at peak, making R&D investments ($2-3 billion annually) structurally unaffordable. Additionally, replacement cycles have lengthened to 36-48 months, reducing predictable upgrade revenue. Chinese competitors compress margins through aggressive pricing and massive scale advantages Asus cannot match. Meanwhile, AI infrastructure markets offered superior margins (35-40% gross margin vs. 15-25% for smartphones) and faster growth rates (30-40% annually vs. flat smartphone markets).

Will Asus provide software updates for existing Zenfone and ROG Phone users?

Asus has not made formal commitments regarding software support timelines. Historical patterns suggest the company will likely provide security updates for 12-18 months following exit announcement, then discontinue updates entirely. Feature updates will likely cease immediately. Cloud services and online features will shut down within 2-3 years. Users should not expect long-term software support comparable to Samsung (3-4 years) or Apple (5-6 years) offerings.

How will Asus's exit affect smartphone repair availability?

Repair parts and services will remain available through official Asus channels for approximately 2-3 years following the exit announcement, then availability will diminish significantly. Third-party repair shops may continue offering services longer using salvaged components, but pricing will increase as inventory becomes scarce. Users should anticipate display replacements costing

What smartphone alternatives should Zenfone users consider?

Zenfone users prioritizing budget pricing and practical features should consider Xiaomi Redmi series (comparable pricing and features), Samsung Galaxy A series (slightly higher prices with guaranteed 3-4 year software support), or Google Pixel 8a (excellent software support guarantee for 3+ years OS updates and 4+ years security patches). All three options offer superior software support commitments compared to Asus's historical practices.

What smartphone alternatives should ROG Phone gaming users consider?

ROG Phone users prioritizing gaming performance should consider OnePlus 12 flagships (strong gaming capabilities at lower prices), iPhone 15 Pro/Pro Max (unmatched GPU performance and gaming ecosystem support through Apple Arcade), or Samsung Galaxy S24 Ultra (competitive gaming performance with superior software ecosystem integration). None offer ROG Phone's specialized thermal cooling, but modern SoC efficiency improvements minimize the practical performance difference.

Is Asus abandoning the wearables and IoT market as well?

No—Asus is actually expanding wearables and IoT product development. The company specifically mentioned focusing on "smart wearables" and IoT devices as part of its strategic pivot away from smartphones. This includes smartwatches, fitness trackers, and connected home devices integrated with AI capabilities. Asus views this segment as higher-margin and faster-growing than smartphones.

Will Asus develop phones again in the future?

Asus's official language provides "no hope of returning" according to available statements. The company stated it will "no longer add new mobile phone models in the future" without specifying conditions for resuming smartphone development. Historical precedent (LG, HTC) suggests that once manufacturers exit smartphone markets, they rarely re-enter successfully. Asus provides no timeline or conditions suggesting potential future re-entry.

How does Asus's exit compare to LG's smartphone exit?

Asus's exit closely mirrors LG's exit pattern but on an accelerated timeline. LG accumulated $4+ billion in smartphone losses over 10 years before formally exiting in 2021. Asus appears to have made the decision more quickly (3-4 years of declining investment versus LG's decade-long decline) and earlier (before accumulating enormous losses). Strategically, both companies recognized similar fundamental issues: unsustainable economics for mid-scale manufacturers lacking ecosystem advantages or vertical component integration.

Should current Asus smartphone owners be concerned about software security?

Yes—devices will eventually reach end-of-life status where security updates cease entirely. Users should plan to migrate to alternative devices within 18-36 months to avoid operating obsolete software with unpatched security vulnerabilities. Remaining on outdated software beyond the support cutoff date exposes devices to known exploits. Users with sensitive data or business applications should prioritize migration immediately.

How will Asus's AI infrastructure focus impact its other business divisions?

Asus can theoretically leverage AI infrastructure expertise across gaming laptops, professional workstations, and networked systems. The company's gaming laptop division could integrate AI acceleration hardware. Professional systems could incorporate AI-optimized processors. However, smartphone exit reduces the company's ability to cross-sell devices to consumers—a strategic disadvantage compared to Samsung and Apple that maintain continuous consumer touchpoints. Asus's business-to-business focus (servers, infrastructure) differs fundamentally from smartphone consumer markets, potentially limiting ecosystem integration benefits.

Takeaway Summary

Asus's official exit from smartphone manufacturing reflects structural market forces eliminating manufacturers without sufficient scale, ecosystem advantage, or strategic differentiation. The company's decision to reallocate resources toward higher-margin AI infrastructure represents rational capital allocation. For existing Asus phone users, this means anticipated support timelines of 18-24 months before devices reach obsolescence. The smartphone industry continues consolidating toward 3-5 dominant players with global scale, leaving no viable position for mid-market manufacturers. Asus's strategic pivot toward AI, robotics, and IoT devices positions the company toward faster-growing, higher-margin markets better suited to its capabilities and capital constraints.

Key Takeaways

- Asus officially discontinued Zenfone and ROG Phone lines permanently, exiting smartphone manufacturing entirely

- Smartphone economics favor only 50+ million unit-per-year manufacturers due to R&D requirements exceeding $2-3 billion annually

- Replacement cycles extended to 36-48 months versus 18-24 months historically, eliminating predictable upgrade revenue

- Chinese manufacturers compress margins through scale and cost advantages independent smartphone makers cannot match

- AI infrastructure offers superior margins (35-40%) versus smartphones (15-25%) and grows 30-40% annually versus flat smartphone markets

- Only companies with ecosystem integration (Apple/Google), extreme scale (Samsung/Chinese makers), or geographic dominance survive smartphone competition

- Existing Asus phone users should expect 12-24 months maximum software support before device obsolescence

- Repair costs will increase significantly as parts availability diminishes within 2-3 years

- Samsung Galaxy, Google Pixel, and OnePlus devices offer superior software support guarantees compared to historical Asus commitments

- Smartphone industry continues consolidating toward 3-5 dominant players by 2030, following automotive industry pattern