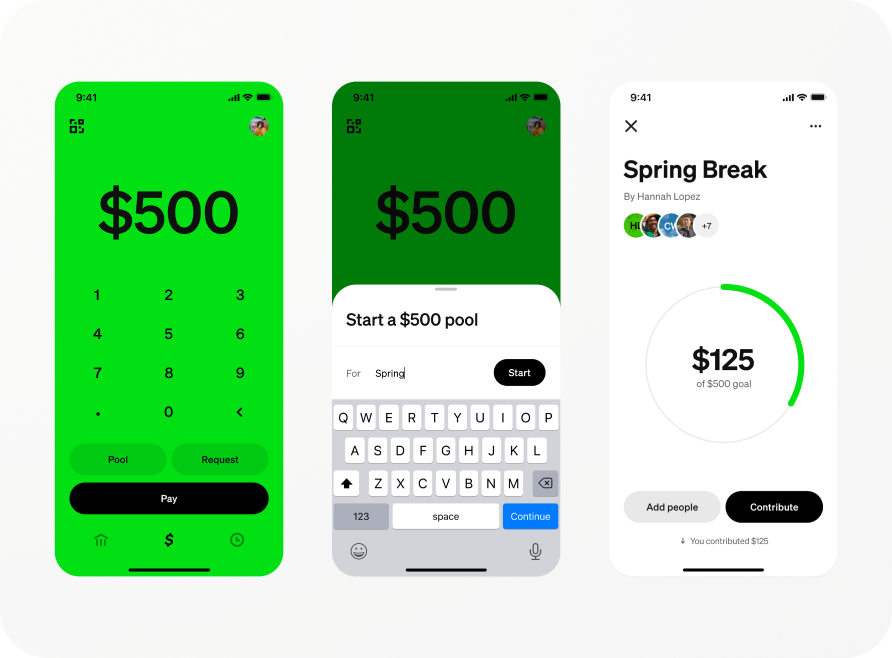

![Cash App Payment Links: Simplifying Digital Payments [2025]](https://tryrunable.com/blog/cash-app-payment-links-simplifying-digital-payments-2025/image-1-1770840469453.jpg)

How Cash App's Payment Links Are Changing the Way We Share Money Online

Remember when paying someone back meant a phone call, or worse, an awkward face-to-face conversation? The evolution of digital payments has been genuinely transformative, but there's always been friction in the process. You'd open an app, find a contact, request or send money, and hope the notification didn't feel too formal or demand-like. It's the kind of mundane interaction we've all experienced, yet it's remained surprisingly clunky for a technology that should feel effortless.

That's where Cash App's latest innovation enters the picture. The mobile payment platform, owned by Block, Inc., has introduced payment links, a feature that fundamentally reshapes how users request and send money to friends, family, and even strangers. Instead of navigating through traditional in-app interfaces, users can now generate shareable links that work seamlessly across text messages, emails, direct messages on social platforms, and any other digital communication channel.

What makes this development significant isn't just the feature itself. It's what it represents: a recognition that payment requests have become deeply embedded in social contexts. They're not purely transactional anymore. They carry emotional weight. A formal payment notification can feel passive-aggressive. A perfectly timed text with a payment link, though, feels human. It feels natural. It acknowledges that money conversations happen where people actually communicate.

This article explores the mechanics of Cash App's payment links, the strategic thinking behind the feature, how it compares to competing approaches, and what it means for the future of peer-to-peer payments. We'll examine the technical implementation, the psychology of payment requests, the competitive landscape, and practical use cases that demonstrate why this feature matters more than it might initially appear.

TL; DR

- Payment links work across any digital platform: Users generate a link in Cash App's payment tab that can be shared via text, email, DM, or any messaging service

- Reduces social awkwardness: The feature addresses a real pain point identified through Gen-Z user research showing that payment discussions often feel overly formal

- Supports recurring and group payments: Payment links aren't limited to one-time transactions; they handle split payments and subscription-style recurring transfers

- Preloaded with requested amounts: Recipients click the link and see the exact amount requested, eliminating negotiation friction

- Part of larger Cash App expansion: This feature joins an AI financial advisor chatbot and enhanced benefits programs in Block's recent product updates

- Signals a shift in payment UX design: Moving away from in-app notification models toward communication-first payment flows

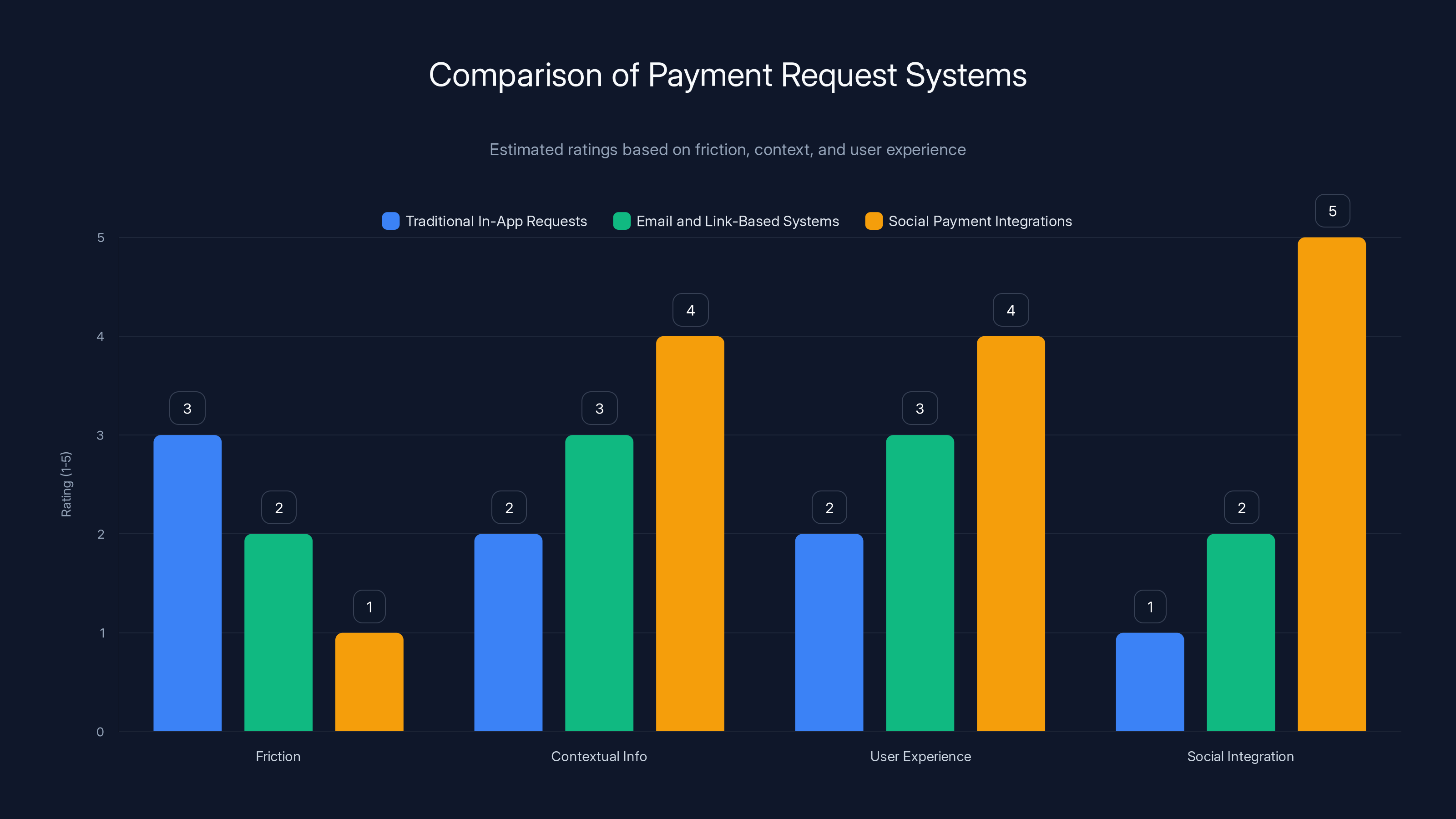

Social Payment Integrations score highest in user experience and social integration, while Traditional In-App Requests face the most friction. (Estimated data)

Understanding Cash App's Payment Links: The Basics

Let's start with what payment links actually are and how they function in practice. If you've used most modern payment apps, you've probably encountered payment requests through push notifications or in-app messages. These work, technically. But they're also interruptions. They arrive as notifications, sometimes feeling like demands, especially if the amount seems large or the context is vague.

Payment links flip this dynamic entirely. Instead of the app initiating the request, the user does. They generate a link that encodes the payment request itself. This link can then be embedded into any communication medium. Think of it like the difference between a formal invoice and a casual text saying "hey, here's the thing." The mechanism is the same, but the feeling is completely different.

Here's how the technical flow works. A user opens Cash App and navigates to the payment tab. Instead of selecting a recipient and sending a payment request through the app's notification system, they click a new option: "share link." Cash App generates a unique URL that contains the payment request details. This includes the requested amount, any memo or description the user adds, and the recipient identifier. The user can then copy this link and paste it anywhere.

When a recipient clicks the link, they're taken to a page that preloads the payment information. They don't have to manually enter the amount or figure out who the request is from. Everything is already there. They authenticate through their Cash App account and confirm the payment. The transaction settles with the same security and speed as any other Cash App transfer.

The elegance of this approach lies in its simplicity. It removes friction at multiple points. There's no searching for contacts. There's no manual amount entry. There's no confusion about what's being requested. And critically, there's no formal notification landing in someone's inbox that might feel like a demand.

Cash App designed payment links to address a specific observation: Gen-Z users engage in frequent payment discussions outside of dedicated payment apps. They're already in group chats, DMs, and text threads. Payment requests that happen in these spaces feel more natural than those arriving as formal app notifications. By allowing users to initiate requests from within the app but deliver them through users' preferred communication channels, Cash App meets people where they already are.

The Psychology Behind Payment Requests and Social Friction

Before diving deeper into features, it's worth understanding why Cash App made this particular design choice. The decision wasn't arbitrary. It came from explicit user research focused on how Gen-Z users actually handle money conversations.

Here's the core insight: payment requests trigger social anxiety in ways most other digital interactions don't. When you send a formal payment notification, you're making a demand. That word might sound harsh, but it's accurate. You're asking someone to take action, and there's an implicit expectation of compliance. Some users experience this as passive-aggressive, especially if the payment is sizeable or the relationship is casual.

Text messages and DMs carry entirely different social weight. They're how friends communicate. They're informal. They allow for context, humor, and negotiation. You can say, "Hey, remember that dinner? I paid for your drink. Can you Venmo me five bucks?" That sentence feels casual and natural. The same request through a formal app notification feels cold and transactional.

This isn't just a feeling. Psychology research on communication and social dynamics shows that context matters enormously. When a request arrives through a channel associated with casual conversation, recipients perceive it differently than when it arrives through formal notification systems. Tone matters. Spontaneity matters. The feeling that you could negotiate or joke about it matters.

Cash App's product team listened to this. They realized that designing the perfect in-app payment request experience doesn't solve the actual problem users face. The problem isn't technical. It's social. Users want to send payment requests without feeling weird about it. They want the recipient to accept without feeling put on the spot. Payment links enable this by allowing requests to flow through established social communication channels.

This design philosophy represents a broader shift in how fintech companies think about user experience. Rather than trying to be the communication channel, successful payment apps increasingly recognize that they're tools embedded within communication. They should integrate with how people actually talk, not demand that people change their communication patterns to accommodate payment flows.

Blockchain and Web 3 communities learned this lesson several years ago when they realized that crypto wallets sending transactions felt weird and impersonal to most people. The most successful implementations—like payment protocols on Discord and Telegram—work because they integrate payment into existing social infrastructure. Cash App's payment links follow this same principle, just applied to traditional mobile payments.

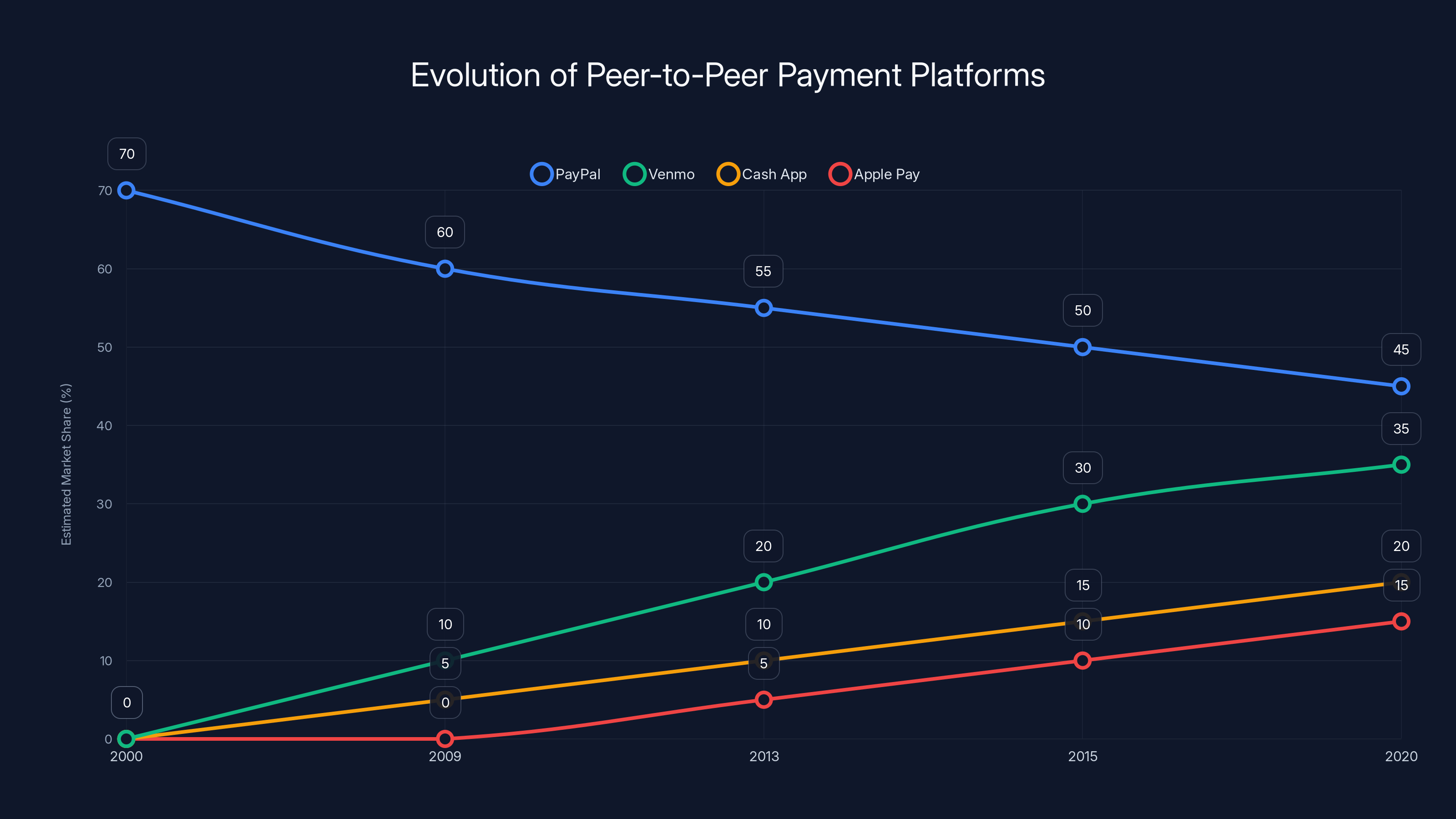

The P2P payment market has evolved with PayPal initially dominating, but Venmo and Cash App have gained significant market share, especially among younger users. (Estimated data)

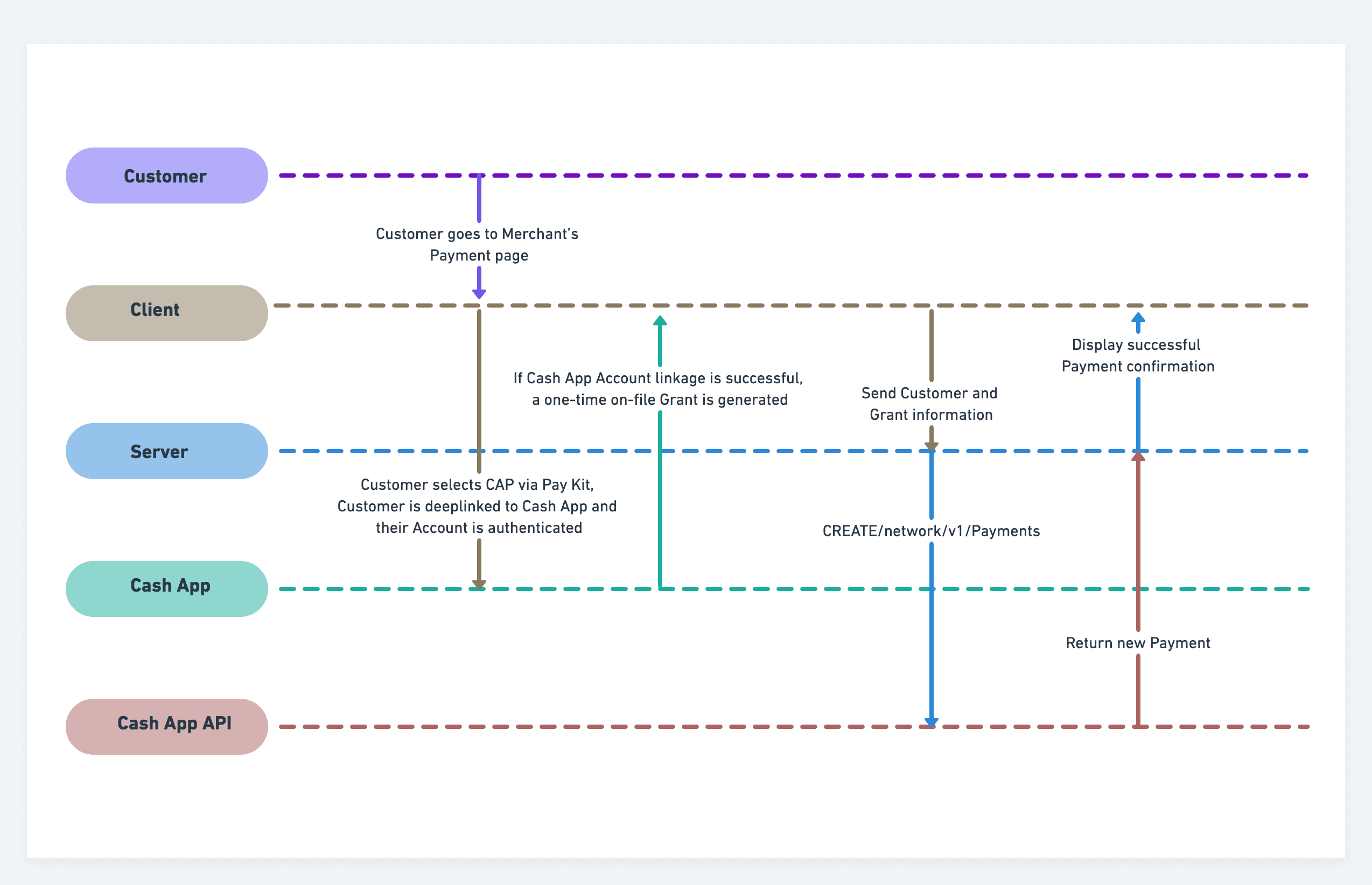

Technical Architecture: How Payment Links Actually Work

Let's get into the technical details of how payment links function. Understanding the engineering gives you insight into why this feature is more sophisticated than it might initially appear.

When a user generates a payment link in Cash App, several things happen server-side. First, the app creates a payment request object containing the following data: sender ID, requested amount, currency, optional memo or description, creation timestamp, and expiration parameters. This object gets assigned a unique identifier.

Cash App then generates a URL that includes this identifier. The URL structure is something like cashapp.com/request/[unique-id]. This URL is what the user copies and shares. Critically, the sensitive details (like the sender's full account information or security credentials) aren't encoded in the URL. Only the request ID is. This is a security best practice that prevents sensitive data from being exposed in browser history, email logs, or accidentally forwarded messages.

When a recipient clicks the link, several verification steps occur. The server looks up the payment request by ID. It validates that the request hasn't expired. It checks whether the recipient is already authenticated in Cash App. If they're not, it prompts them to log in or create an account. Once authenticated, the system confirms that the request is still valid and hasn't been fulfilled.

Then comes the preloading step. Instead of showing a blank payment form, the recipient's browser or app loads all the request details: the exact amount, who it's from, any memo text, and payment history if applicable. This preloading is crucial because it eliminates friction. Recipients don't have to enter amounts or search for contacts. They just confirm and pay.

The architecture handles recurring payments through a slightly different flow. When a user creates a recurring payment link, Cash App stores additional metadata: frequency, maximum number of recurrences, and authorization parameters. Recipients can authorize the recurring payment once, after which Cash App charges them at the specified intervals without requiring additional clicks. This is similar to how subscription services work, but initiated by the payment requester rather than the payee.

For group payments, the mechanics become more complex. A user can generate a single payment link that applies to multiple recipients or request contributions toward a specific total. Cash App tracks how much each recipient has paid, what remains, and manages the overall transaction flow. This is particularly useful for situations like splitting rent among three roommates or collecting contributions for a group gift.

Security is embedded throughout this process. Cash App uses encryption for data in transit. Payment links expire after a certain period (typically 30 to 90 days depending on settings). Users can revoke links at any time through their Cash App dashboard. Recipients are verified through Cash App's standard authentication mechanisms. And all payment links are tied to verified accounts, not anonymous transactions.

The architecture also includes analytics. Cash App can track when links are created, how many times they're clicked, whether they're completed, and where they're shared (based on click patterns). This data helps the company understand how users are actually using the feature, which informs future refinements.

Comparing Payment Links to Traditional Payment Request Systems

To understand why Cash App's payment links represent a significant evolution, it helps to compare them to how payment requests have traditionally worked in the fintech space.

Traditional In-App Payment Requests (used by most payment apps for years) function through push notifications and in-app messaging. The sender opens the app, finds the recipient, enters an amount, and hits send. This generates a notification that lands on the recipient's phone or appears in their app's message center. The recipient then opens the app to view and respond to the request.

This approach has significant friction points. First, it requires the recipient to have the app installed and open it. Second, notification overload means requests can get lost or ignored among dozens of other notifications. Third, the formal notification structure creates the social awkwardness Cash App identified. Fourth, there's no contextual information unless the sender includes a memo, and even then, the memo appears in isolation from any conversation.

Email and Link-Based Payment Systems (like payment buttons embedded in email receipts) work similarly to Cash App's approach but arrive through email rather than generating standalone links. Someone sends you an email invoice with a "Pay Now" button. You click it, get taken to a payment page, and complete the transaction. The advantage is that payment sits within communication context. The disadvantage is that you're tied to email as the delivery mechanism, and it feels commercial rather than casual.

Social Payment Integrations (like Venmo comments or Facebook Pay in Messenger) embed payment functionality directly into social platforms. You can request money within a conversation thread, and both parties get context about why the payment was needed. This solves the social awkwardness problem elegantly. The disadvantage is fragmentation—different platforms have different payment features and capabilities.

Cryptocurrency and Web 3 Approaches (like Lightning Network or blockchain-based payment requests) allow link-based transactions but require technical sophistication and often involve transaction fees or settlement complications that traditional payment systems avoid.

Cash App's payment links occupy a unique position in this spectrum. They combine the contextual benefits of social platform integration (requests can be sent through any communication channel) with the reliability and security of traditional payment systems. They're simpler than cryptocurrency approaches and more casual than formal email invoicing. They don't require recipients to have the app open when the request is made, just when they're ready to pay.

The comparison to Venmo specifically is instructive. Venmo requires both parties to be Venmo users. It works best when integrated into Venmo's social feed where transactions and comments are visible. Venmo solved the social awkwardness problem by making payments public and adding humor through comment sections. Cash App's payment links solve it differently: by moving requests out of formal app channels entirely.

Pay Pal's "Request Money" feature works similarly to traditional in-app systems, sending notifications rather than shareable links. Square Cash (which merged with Cash App) had some link functionality, but Cash App's implementation is more comprehensive and user-friendly.

Use Cases: Where Payment Links Actually Shine

Theoretically, payment links sound useful. In practice, there are specific situations where they're genuinely transformative for user experience.

Group Expenses and Split Payments represent one of the most common use cases. Imagine you're organizing a dinner with six friends. You pay the entire

Recurring Shared Expenses like rent, utilities, or HOA fees benefit enormously from payment links. If you're splitting rent with roommates, you can send the same payment link each month. Recipients can save it or create recurring payments. This eliminates the awkward "Hey, rent is due" conversation. The payment link is just a standing mechanism that doesn't feel accusatory.

Freelance and Gig Work creates scenarios where casual service providers need payment collection systems without formal invoicing infrastructure. A photographer might send a payment link after a photo shoot. A dog walker might share a link after a week of walks. These are semi-formal relationships where traditional invoicing feels overblown, but in-app payment notifications feel impersonal. Payment links hit the right tone.

Marketplace and Secondhand Sales are surprisingly common payment contexts. Someone's selling a used bookshelf on Facebook Marketplace. They can send the buyer a payment link, which feels more trustworthy than asking for Venmo directly (because it's in the app), but doesn't require setting up Square or Stripe. The buyer can pay through a familiar interface. The seller knows exactly how much was requested.

Event and Trip Planning frequently involve payment collection. Planning a group weekend trip? Send payment links for deposit amounts to confirm attendance. Organizing a wedding and need contributions from family? Payment links feel more personal than formal invoices but handle the logistics cleanly.

Bet Settlement and Game Stakes are interesting edge cases. Friends play poker, go on fantasy sports leagues, or make casual bets. Payment links let the winner send a request that feels more like "you owe me" than formal billing. The loser can pay with minimal friction.

Payment links significantly enhance user acquisition and activation, with high impact scores of 8 and 9 respectively. This leads to increased engagement and monetization opportunities. (Estimated data)

Cash App's Broader Product Strategy and Recent Innovations

Payment links don't exist in isolation within Cash App's product roadmap. Understanding the broader context shows how this feature fits into Block's larger vision for the platform.

Cash App has been aggressively innovating beyond basic payment transfers. In recent months, the company introduced an AI-powered financial advisor chatbot that debuted late in 2024. This tool provides financial guidance to users, answering questions about budgeting, investing, and money management. The chatbot represents a shift toward Cash App becoming not just a payment platform but a comprehensive financial wellness tool.

Alongside this, Cash App launched enhanced benefits programs with higher borrowing limits. This suggests Block is positioning Cash App as a more comprehensive financial services platform, not just a peer-to-peer payment tool. Users can access credit, financial advice, and payment services all in one place.

Payment links fit into this ecosystem by improving the core payment experience. Block recognizes that payment remains the foundation of its business. Before users engage with investing, borrowing, or financial advice, they need to trust and enjoy the basic payment functionality. Payment links make payments frictionless and social, which drives more frequent usage and deeper engagement.

This also reflects a recognition that younger users (Gen-Z and younger millennials) have different payment expectations than older demographics. These users grew up with social media and digital communication as primary channels. They expect integration between social and financial functions. Payment links bridge that gap. Rather than forcing users to switch to a dedicated app for payments, Cash App lets payments flow through the communication channels users already prefer.

Block's broader strategy involves creating a "super app" experience where Cash App becomes central to users' digital financial lives. Payment links are a piece of this puzzle. They make payments so frictionless that they happen more frequently. More frequent payments mean more app engagement. More engagement means better data for understanding user behavior. Better data means more targeted features and services.

It's worth noting that this strategy isn't unique to Block. We Chat in China pioneered this approach years ago, embedding payments so deeply into social communication that the app became essential for daily life. Stripe, Pay Pal, and other fintech companies are all trying to replicate this success in different ways. Payment links represent Cash App's specific answer to this challenge.

Market Context: The Evolution of Peer-to-Peer Payments

The P2P payment market has evolved significantly since services like Pay Pal launched in the late 1990s. Understanding this evolution provides context for why payment links are strategically important.

In the early 2000s, online payment was complex. Setting up a Pay Pal account required multiple verification steps. Transactions took days to settle. Security was questionable. But it solved a real problem: moving money between people over the internet without writing checks or meeting in person.

Venmo arrived in 2009 and fundamentally changed the category. It made sending money to friends feel social. The public transaction feed turned payments into a social activity. Users could comment on transactions, make jokes, and see what their friends were spending money on. This made Venmo feel like a social network, not just a financial tool. It became the default for payments among younger users, particularly in cities.

Square Cash (later merged into Cash App) launched around the same time with a focus on simplicity. Square understood that not everyone wanted their transactions public. They built Cash App around one-click payments, minimal friction, and privacy. Square also owned the merchant side through Square (now Block, Inc.), giving it unique insights into how payments flowed through the economy.

In 2013, Apple launched Passbook (later Wallet), which didn't handle payments initially but positioned the phone itself as a payment device. In 2014, Apple Pay launched, enabling tap-to-pay everywhere. This didn't eliminate P2P payment apps but shifted expectations around speed and security.

By 2015-2016, the P2P market had consolidated around a few major players. Venmo dominated among younger users. Pay Pal dominated among older users and businesses. Cash App was strong but secondary. Stripe and Square dominated merchant payments.

Over the past five years, the competitive dynamics have shifted. Cryptocurrency and blockchain emerged as alternative payment infrastructure. Cross-border payments became more prominent. Regulation increased. Fraud and scams in P2P payment became more visible. And most importantly, user expectations shifted dramatically toward seamless, omnichannel payment experiences.

Payment links represent the natural evolution of this market. They're a response to several market realities: users want payments to happen in conversation contexts, they want them to be private, they want them to work everywhere, and they want minimal friction. Payment links address all of these needs.

The competitive response will be instructive. Venmo will likely implement something similar (they may already be testing it). Pay Pal will add payment links to its ecosystem. Square and Block's other properties will integrate this capability. Within 12 months, payment links will probably be a standard feature across all major P2P payment platforms.

Generational Expectations: Why Gen-Z Users Drove This Feature

Cash App explicitly researched Gen-Z users to understand payment friction. This wasn't random. Gen-Z's expectations about digital life are fundamentally different from older generations, and they're now the fastest-growing demographic segment and a key target market for fintech companies.

Gen-Z grew up with social media as a primary communication channel. They spent their teenage years messaging friends, sharing moments, and coordinating plans through digital platforms. They developed strong expectations about how communication should work: it should be immediate, it should be visual, it should be casual, and it should happen where they already are.

When Gen-Z encounters a requirement to leave a communication channel to perform a transaction, it feels jarring. They don't think, "Oh, I need to open the payment app." They think, "Why isn't this integrated here?" This attitude reflects deeper cultural expectations about frictionless digital experiences.

It's also worth noting that Gen-Z is genuinely more comfortable discussing money openly than previous generations. They grew up with friends sharing personal information on social media. They're more likely to split expenses in group settings. They're more likely to move in shared housing. They're more likely to engage in side hustles and gig work. All of these behaviors require frequent payment transfers among friends and acquaintances.

These behaviors create unique friction points. A group chat discussing a trip might involve multiple payment discussions: deposits, flight cost shares, accommodation splits, daily expense coverage. Each of these could be a separate payment request through traditional channels. That's overwhelming. But integrating payments into the existing conversation through payment links makes it seamless.

Gen-Z also values authenticity and casualness in brands and products. They're suspicious of overly polished experiences and corporate language. When something feels designed to sell to them, they often reject it. Payment links feel authentic because they originate from genuine user feedback about social friction, not from marketing strategies. And they integrate into casual communication rather than creating formal processes.

This generational insight is significant because it signals how fintech companies should think about product development going forward. The most successful innovations will be those that recognize how different age cohorts actually want to interact with digital tools. For Gen-Z, that means meeting them in communication contexts, not demanding they switch contexts to perform transactions.

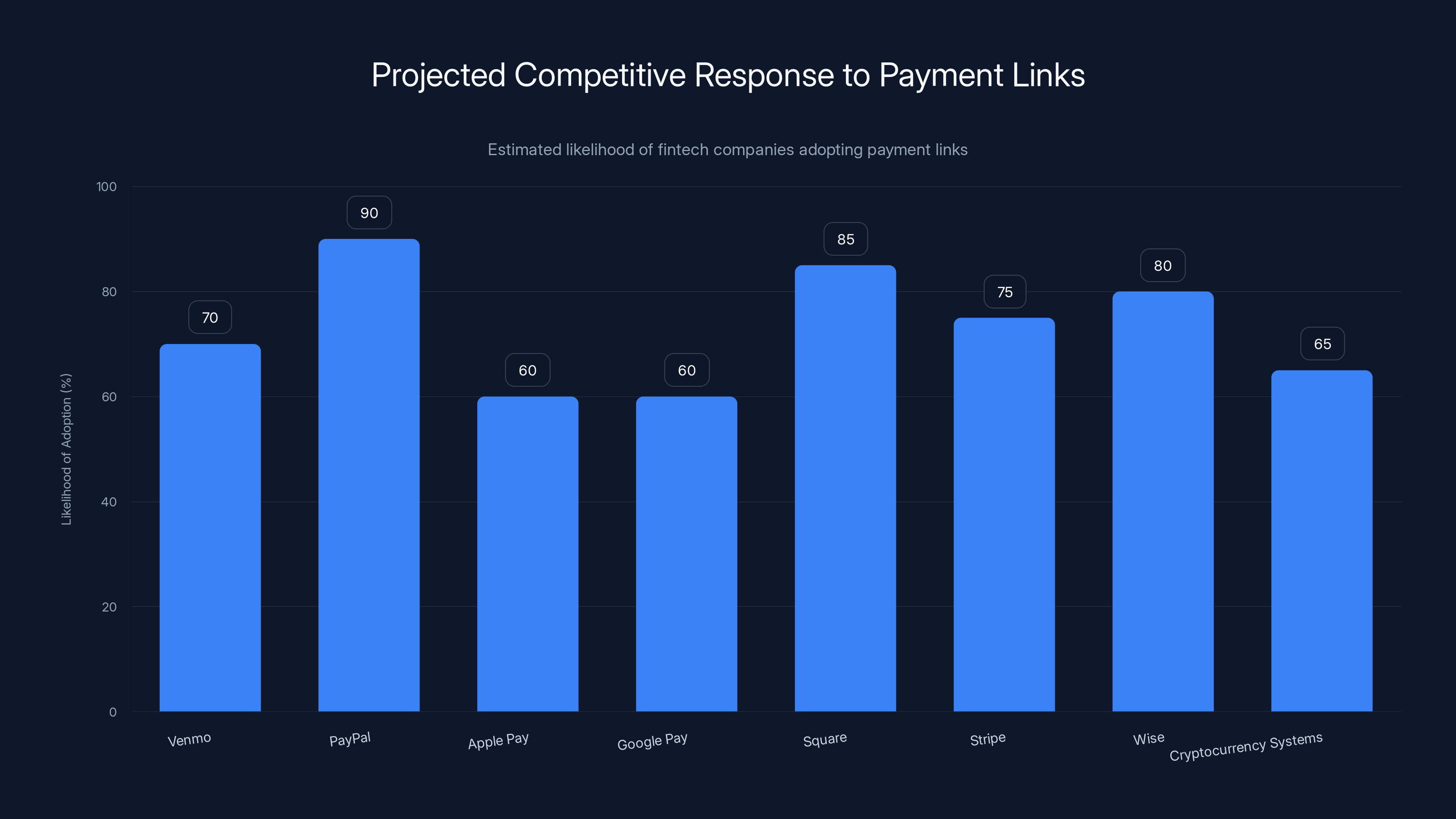

PayPal and Square are most likely to adopt payment links due to existing infrastructure, while Apple Pay and Google Pay may be more cautious. Estimated data.

Security Considerations and Fraud Protection

Payment links introduce interesting security dynamics that differ from traditional in-app payment requests. Understanding these is important for users deciding whether to adopt the feature.

Address bar spoofing is a potential concern. A fraudster could create a link that looks like a Cash App payment link but actually directs users to a fake site designed to steal credentials. This is a known attack vector for many link-based payment systems. Cash App mitigates this through several mechanisms: they use verified domain and SSL certificates to ensure users can verify they're on the legitimate site. They include authentication requirements, so users must log into their real Cash App account before payments process. And they employ machine learning to detect suspicious links that are being shared.

Unauthorized link generation is another vector. Could someone generate payment links using another person's account? Cash App's architecture requires that payment links be created by authenticated users, so this would require account compromise. However, if an account is compromised, the attacker could indeed generate payment links that victims might trust because they appear to come from a known contact. The mitigation here is the same as for any account compromise: strong passwords, two-factor authentication, and immediate notification if suspicious activity is detected.

Link sharing and interception creates different risks. If someone shares a payment link through insecure channels (unencrypted email, unprotected messaging), the link could be intercepted. An attacker could potentially modify the link or use it to phish for information. However, this requires intercepting the link in transit, which is difficult for most internet communications. And even if intercepted, the link only contains the request ID, not sensitive payment information.

Expired link exploitation is lower risk. Cash App implements link expiration, so a link that's been sitting in an email or chat for 90 days might no longer work. This is actually a security feature—it prevents old links from being reused in phishing attacks. However, it can be frustrating if you want a recurring link for legitimate purposes.

Recipient fraud and unauthorized payments represent a different category of concern. Could someone click a payment link and claim they didn't authorize it? This is theoretically possible but mitigated by the fact that the link preloads the amount, who it's from, and recipients must authenticate before payment. Cash App's fraud detection systems also monitor for unusual patterns that might indicate account compromise or fraud.

Cash App's broader security infrastructure applies to payment links. The company uses encryption for all data in transit. It implements fraud detection algorithms that can flag suspicious payment patterns. It offers buyer and seller protection programs. And it operates within regulatory frameworks that mandate security standards.

That said, payment links do introduce new user education requirements. Users need to understand that they should only click payment links from trusted sources. They should verify that they're on legitimate Cash App domains before entering credentials. They should be skeptical of unsolicited payment links from unknown contacts. Cash App will likely invest in education content around safe payment link usage.

Technical Integration: How Payment Links Work Across Devices and Platforms

A key strength of Cash App's payment links is their cross-platform compatibility. Unlike features that require the app to be open, payment links work on any device with a web browser.

When someone shares a payment link via text message, the recipient receives the URL as text. They can click it on their phone, tablet, or computer. The link takes them to a mobile-optimized web page that displays the payment request. If they don't have Cash App installed, they can download it. If they do, they can authorize the payment directly from the app.

This is technically more sophisticated than it might appear. Cash App needs to detect whether a user has the app installed and handle each case appropriately. If the app is installed, they typically redirect to the app to complete the payment. This preserves the security advantages of in-app authentication. If the app isn't installed, they provide a web-based payment interface.

The redirect mechanism is important. When someone clicks a payment link on their phone, Cash App can detect the device type, check whether the app is installed, and route accordingly. This seamless experience means users don't have to manually open the app, navigate to a payment section, and find the request. It all happens automatically.

Cross-browser support means that links work in Safari, Chrome, Firefox, and any other browser. This is particularly important for SMS links, which might be opened in the default browser on older phones or feature phones that don't have modern browsers.

Mobile payment optimization ensures that the payment flow works smoothly on small screens. The request details display clearly, buttons are finger-friendly, and the authentication process doesn't require extensive typing or complex interactions.

Desktop experience is also considered, though less common. Someone might receive a payment link via email and open it on their laptop. Cash App's interface should adapt to the larger screen and different interaction patterns (mouse vs. touch).

Integration with wallet apps might also be relevant. Apple Wallet and Google Wallet can store payment information. Payment links might eventually integrate with these systems, allowing users to add payment links to their wallet for quick access. This would be a natural evolution.

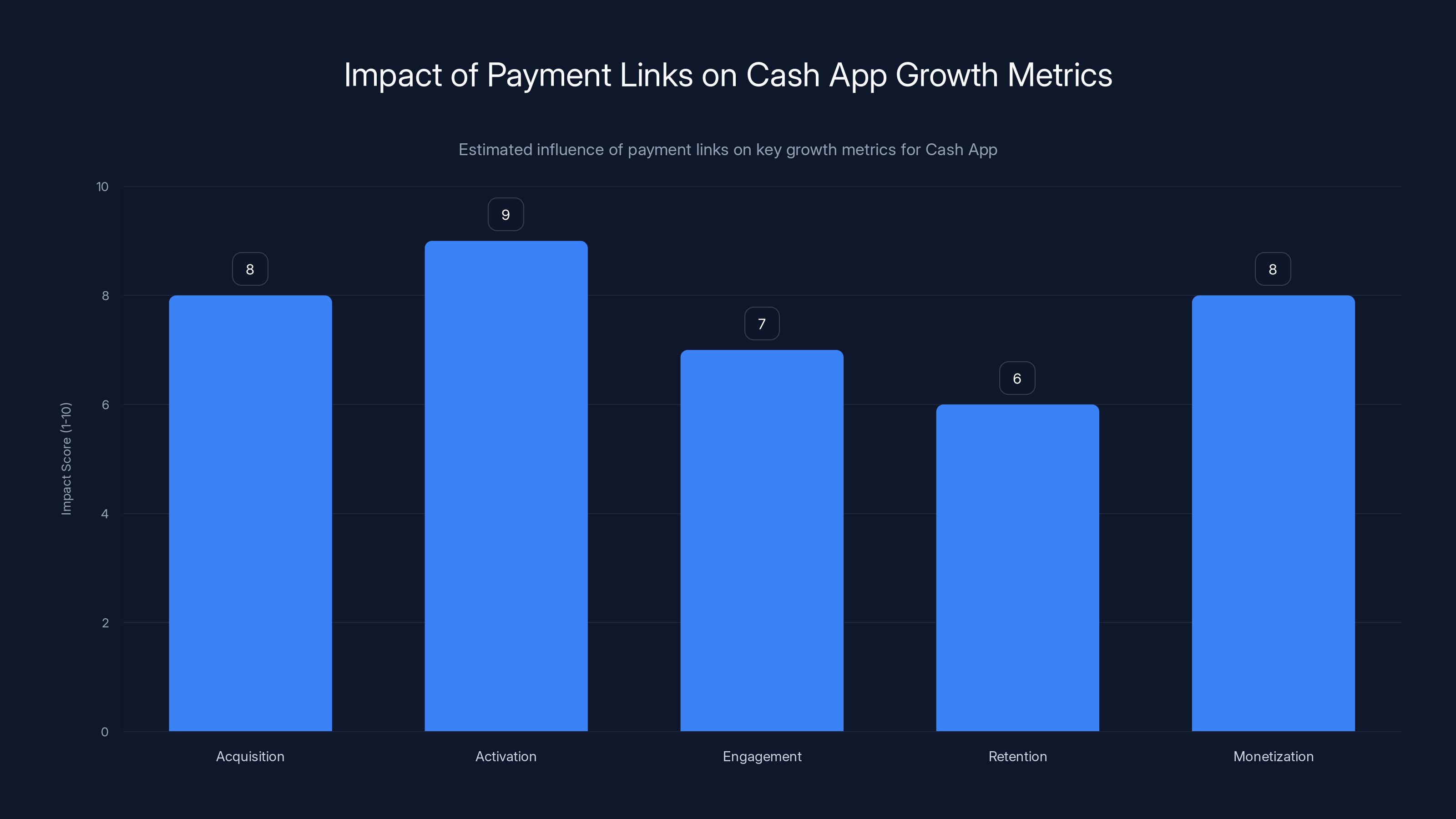

The Role of Payment Links in Cash App's Growth Strategy

From a business perspective, payment links represent a strategic lever for driving several key metrics that matter to Block, Inc.

Acquisition is the first lever. Payment links enable frictionless onboarding for new users. Someone doesn't have Cash App? A payment link can redirect them to the download page with context about why they need it. The link encodes the payment amount and who it's from, making the value proposition immediately clear. This is more effective marketing than generic app store listings.

Activation (getting users to actually use the platform) is the second lever. For many people who download Cash App, it sits unused. They never set up a payment. Payment links change this dynamic. If someone receives a payment link, they're immediately motivated to complete the transaction. They're activated in one step rather than needing discovery and education.

Engagement (how frequently users return to the platform) increases through payment links. Users who can send payments through their preferred communication channels will send more payments, more frequently. They don't have to overcome the friction of opening the app. Payments become ambient to their communication flow.

Retention improves as users develop payment habits. The more frequently someone uses Cash App, the more invested they become. They start to explore other features: investing tools, budgeting features, financial advice. They're more likely to maintain an active account.

Monetization follows from engagement. Cash App makes money through multiple mechanisms: interchange fees on card transfers, interest on Cash App savings, spreads on currency conversions, and lending products. More engaged users generate more opportunities for monetization.

For Block, Inc., these metrics cascade upward to company valuation and investor confidence. Each improvement in user acquisition, activation, engagement, or retention directly impacts company growth and profitability. Payment links are a relatively low-cost way to move these metrics in positive directions.

It's also worth noting that payment links generate network effects. As more users adopt payment links, they become more valuable to everyone. A user is more likely to send a payment link if they expect recipients to be able to easily use it. As adoption increases, the value proposition strengthens, driving further adoption. This positive feedback loop is exactly the kind of dynamic that creates sustainable competitive advantages.

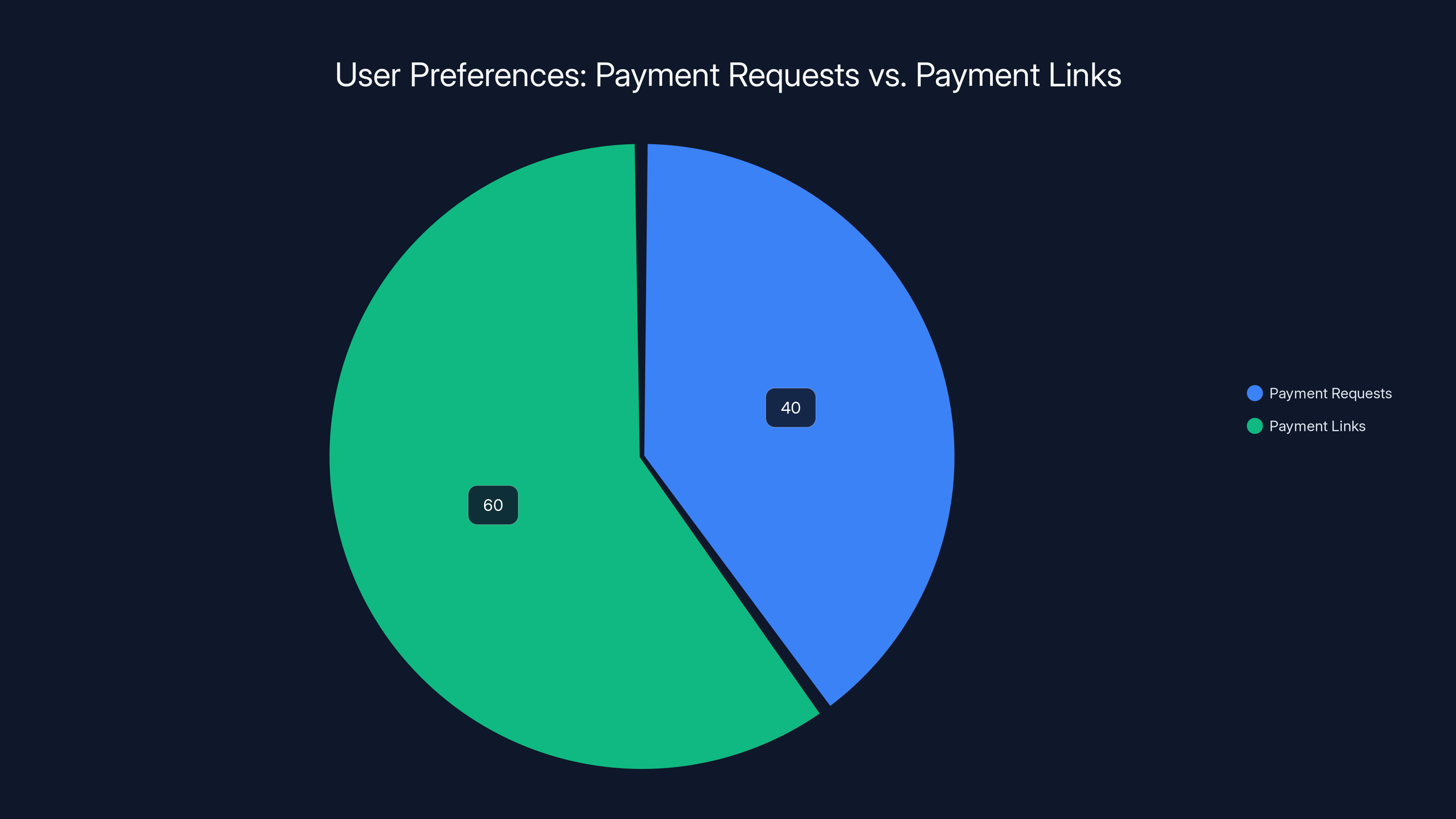

Estimated data suggests that users prefer payment links (60%) over traditional payment requests (40%) due to increased control and convenience.

Competitive Responses and Market Evolution

Historically, when one fintech company introduces an innovative feature, competitors quickly respond. We should expect payment links to follow this pattern.

Venmo is the most obvious competitor that needs to respond. Venmo's architecture is primarily built around in-app transactions with social features. Adding payment links would require product development but isn't technically infeasible. Venmo might struggle more with the social angle—payment links are inherently less social than Venmo's comment-based transaction feeds. But Venmo could position payment links for situations where privacy is desired.

Pay Pal already has payment infrastructure that could support payment links. Indeed, Pay Pal's "pay later" features and invoice payment links already exist in some forms. Pay Pal might integrate these more deeply into their platform and actively market them as competitors to Cash App's offering.

Apple Pay and Google Pay operate at a different layer (point-of-sale) but could theoretically extend into P2P payments through payment links. Both companies have interest in P2P payments but have been cautious about competing too aggressively with banks and payment processors.

Square (Block's other property) will likely integrate payment links across its ecosystem. Square merchants might be able to generate and share payment links. Square's point-of-sale systems might default to payment links for follow-up payments or deposits.

Stripe and Wise might implement similar features for their customer bases. Wise, in particular, focuses on international transfers where payment links could significantly reduce friction.

Cryptocurrency-based systems might also respond. Lightning Network and other blockchain payment systems already support payment requests through links. As these systems mature, they could compete directly with traditional fintech solutions.

The competitive response will likely accelerate adoption of payment links across the industry. Within 18-24 months, payment links might become a baseline expected feature in payment apps, much like push notifications are now. At that point, differentiation shifts to other factors: user experience quality, feature breadth, integration depth, and brand strength.

Privacy and Data Concerns Around Payment Links

While payment links offer convenience, they also raise privacy and data collection questions that both users and regulators might scrutinize.

Click tracking is a fundamental capability of link-based systems. Cash App can track when payment links are clicked, where they're opened from, and what device types are used. This data could be valuable for product analytics—understanding where and how users are sharing links informs feature improvements. But it also represents data collection that some users might find invasive.

Recipient identification requires that Cash App know whether a payment link is being used by the intended recipient or someone else. This could involve IP address tracking, device fingerprinting, or other identifying information. Again, this is necessary for security but does create privacy implications.

Communication pattern data emerges from payment links. Cash App can infer social connections based on who sends and receives payment links. It can understand which users frequently exchange money. It can identify patterns in payment behavior. This data could be monetized, shared with advertisers, or used for lending decisions. Users might object if they understood the extent of this tracking.

Regulatory implications are significant. Financial regulators are increasingly focused on data privacy and consumer protection. If payment links enable new forms of data collection, they'll likely require explicit user consent and transparency. The Financial Consumer Protection Bureau and similar agencies in other countries might require Cash App to provide clear disclosures about what data is collected and how it's used.

GDPR and international compliance also apply if Cash App users are in Europe or other jurisdictions with strong privacy protections. Generating shareable payment links could be considered creating persistent identifiers that track individuals. Cash App would need to ensure compliance with these frameworks.

It's worth noting that traditional in-app payment requests also generate similar data. Cash App already tracks when payment notifications are sent and received. Payment links don't introduce entirely new privacy concerns, but they might enable more granular tracking because they exist outside the app's controlled environment.

Implementation Timeline and Rollout Strategy

Block, Inc. would have considered carefully how to roll out payment links to maximize adoption while minimizing technical issues and user confusion.

Initial testing likely involved internal testing and limited external beta testing with select user groups. This is standard practice for fintech features because bugs or security issues can directly impact user money. Block probably tested extensively with various scenarios: different amounts, international payments, edge cases, and error conditions.

Staged rollout is the likely approach. Rather than enabling payment links for all users simultaneously, Block would probably enable them for a subset first. They'd monitor usage, collect feedback, and identify any technical issues. Once they're confident, they'd expand to larger user groups.

Regional variations might occur if specific regions have regulatory or technical considerations. For example, payment links might roll out in the US first, then expand to other countries after ensuring compliance with local regulations.

Feature flags in the Cash App codebase allow Block to enable or disable payment links for specific users without deploying code changes. This enables rapid experimentation and rollback if issues emerge.

User communication needs to be handled carefully. Users need to understand what payment links are, how to use them, and why they're useful. Block probably invested in creating educational content: tutorial videos, help center articles, and in-app guidance.

The rollout strategy reflects a broader principle in fintech product development: shipping features fast is valuable, but not at the expense of stability, security, or user experience. Payment links affect core financial operations, so careful rollout is essential.

Payment links are most frequently used for group expenses, followed by recurring shared expenses and freelance work. Estimated data based on typical scenarios.

Integration with Emerging Payment Trends

Payment links don't exist in isolation from broader trends in payment technology and user behavior.

Open Banking enables payment apps to integrate more deeply with banking infrastructure. Open standards mean that Payment links could connect directly to bank accounts, credit cards, and financial data. This makes payments faster and enables richer features.

Embedded Finance is the trend of financial services being embedded into non-financial applications. Payment links could enable merchants or social platforms to embed Cash App payment functionality without redirecting users away. This could expand payment links from direct transfer context to transactional commerce contexts.

Conversational Commerce positions payments within text-based interactions. AI chatbots, virtual assistants, and voice-based payment systems are emerging. Payment links could integrate into these contexts, allowing users to authorize payments through conversation.

Biometric Authentication increasingly replaces passwords. Payment links could require facial recognition, fingerprint verification, or other biometric authentication rather than traditional credentials. This strengthens security while maintaining simplicity.

Distributed Ledger Technology and blockchain could eventually power payment links. While traditional payment links use Cash App's centralized infrastructure, blockchain-based alternatives might offer different trust models or cost structures.

Cash App's payment links are positioned to evolve with these broader trends. The foundational architecture—shareable URLs that encode payment requests—is flexible enough to accommodate emerging technologies and use cases.

Best Practices for Using Payment Links Effectively

For users looking to maximize the utility of payment links, several best practices emerge from early usage patterns and user feedback.

Create context-specific links for different scenarios. You might have one link for splitting rent, another for splitting dinners, another for shared utilities. This makes it clear what each payment is for and prevents confusion. Naming these links in your notes or shared documents makes them even more useful.

Use recurring links for predictable, repeated expenses. Rent, subscriptions, shared bill payments—these happen regularly and don't change amount. A recurring payment link can handle this without requiring a new request each time.

Combine links with conversation for maximum effectiveness. Don't just send a link without context. Add a message: "Hey, here's the dinner split link" or "Our rent is due! Here's the link." The context makes the request feel more human and less demanding.

Verify link addresses before clicking, especially if you received them through unexpected channels. While Cash App links should be legitimate if they come from official Cash App communications, fraudsters might create fake links that look similar. Always verify you're on the legitimate Cash App domain.

Save links you use frequently in secure locations like note apps or password managers. If you have a link for a recurring expense, keeping it saved means you can access it quickly without searching your message history.

Set expiration dates on sensitive links. If you're requesting payment for a one-time expense, setting the link to expire after 30 days prevents it from hanging around indefinitely in chat histories.

Group expense management becomes easier with payment links. Designate one person to create links and share them with the group. This person becomes the "payment coordinator," making the process more organized than random requests.

The Future of Payment Links and P2P Payments

Looking ahead, payment links will likely become increasingly sophisticated and integrated into broader financial systems.

AI-powered payment routing could eventually recommend when to send payment links versus other payment methods. An AI assistant might suggest the optimal payment approach based on who you're paying, how urgent it is, and what the recipient prefers.

Predictive payment suggestions could identify situations where you'll likely need to request payment (like shared expenses coming up) and proactively suggest creating links. "Hey, you're going to dinner with three friends Thursday. Want to create a split payment link?"

Cross-platform payment links might eventually work across multiple payment providers. Instead of each company having its own payment link system, standardized links could work with Cash App, Venmo, Pay Pal, or any other provider. This would maximize convenience and flexibility.

Real-time settlement could accelerate as infrastructure improves. Currently, payments might settle within 24 hours or longer. Future payment links might enable instant settlement, making the experience even more seamless.

Global payment links would extend the feature to international transfers. Currently, Cash App's cross-border functionality is limited. But payment links could facilitate international payments more easily, particularly for remittances and travel-related expenses.

Integration with smart contracts (blockchain-based) could automate payment conditions. A payment link might be conditional on specific events, include automatic splitting, or execute complex payment logic.

Regulatory evolution will also shape payment links. Governments might require additional documentation for payment links (though probably not for small personal transfers). They might mandate certain security standards. Payment links could become the default mechanism through which governments identify and track payments for tax compliance.

The trajectory suggests that payment links are a foundational innovation that will evolve for years. The basic concept—shareable URLs that encode payment requests—is simple but powerful. As supporting infrastructure improves and regulatory frameworks mature, payment links will likely become even more central to how people move money.

Conclusion: Why Payment Links Matter More Than They Appear

On the surface, payment links might seem like a modest feature update. You can share requests in more places. That's useful. But the significance runs deeper.

Payment links represent a fundamental shift in how financial services companies think about user experience. Rather than demanding that users adapt to financial infrastructure, payment links acknowledge that payments happen within social contexts. They meet users where they are: in text messages, in group chats, in emails, in social platform DMs.

This philosophy has implications beyond payment itself. It suggests that future fintech innovation will increasingly focus on breaking down barriers between financial services and everyday digital life. It suggests that the most successful payment solutions won't be specialized financial apps that users visit occasionally, but tools that integrate seamlessly into communication and commerce flows.

Cash App's payment links also signal something important about generational expectations. Gen-Z users didn't ask for apps; they asked for frictionless experiences. They didn't ask for notifications; they asked for integration into their existing communication channels. They didn't ask for formality; they asked for casualness and authenticity. When fintech companies listen to these preferences and build products accordingly, they create solutions that resonate.

From a competitive perspective, payment links represent the kind of feature that's easy to copy but difficult to establish first-mover advantages from. Within 18-24 months, every major payment app will likely offer something similar. At that point, competition shifts to other factors: which app is easiest to use, which has the best customer service, which has the broadest feature set, which integrates best with the rest of users' digital lives.

For Cash App, payment links are a solid move that improves the core product and addresses legitimate user friction. Combined with recent additions like the AI financial advisor and enhanced benefits programs, they position Cash App as a comprehensive financial platform rather than just a payment app. This matters for retention, engagement, and long-term value.

For users, payment links are worth trying. They genuinely do reduce friction in a common scenario. They make requesting money feel more natural and less awkward. They integrate into communication flows that already exist. The combination of these factors makes them worth adopting as your default mechanism for most peer-to-peer requests.

The broader lesson is that user experience innovation often comes from listening to real pain points and designing solutions that align with how people actually want to interact with digital tools. Cash App did this with payment links. The fintech industry will likely continue down this path, resulting in increasingly seamless and natural financial interactions.

As digital life continues to evolve, expect more of these kinds of innovations: features that blur the boundary between communication, commerce, and financial services. Payment links are just the beginning of a broader shift toward truly integrated digital experiences.

FAQ

What are Cash App payment links?

Cash App payment links are shareable URLs that encode payment requests. Users generate a link in the Cash App payment tab and share it through text messages, emails, DMs, or any other digital communication channel. When recipients click the link, they see the preloaded payment amount and can complete the transaction with one tap.

How do I create a payment link in Cash App?

Open Cash App and navigate to the payment tab. Instead of selecting a recipient and using the traditional payment request feature, click the "share link" option. This generates a unique URL that you can copy and paste into any communication platform. Customize the amount and add a memo if desired before sharing.

Can payment links be used for recurring payments?

Yes, Cash App payment links support recurring payments. When creating a recurring link, you specify the frequency and maximum number of recurrences. Recipients can authorize the recurring payment once, and Cash App charges them automatically at the specified intervals without requiring additional confirmations.

Are payment links secure?

Cash App payment links use encryption and authentication security measures. Links contain only a request ID, not sensitive financial information. Users must authenticate through their Cash App account before completing payments. Cash App also implements fraud detection and expiration mechanisms to prevent unauthorized use. However, users should still be cautious about clicking links from unknown sources and verify they're on legitimate Cash App domains.

Do both parties need to have Cash App installed to use payment links?

Not necessarily. While having Cash App installed enables faster in-app processing, users can also complete payments through a web interface if they don't have the app. The link adapts to the device and whether the app is installed, routing users to the most convenient payment method.

Can I use payment links for group payments or splitting bills?

Yes, payment links handle group payments and expense splitting. You can generate a single link that applies to multiple recipients or a request that contributes toward a specific total. Cash App tracks how much each recipient has paid and what remains, making it easy to manage shared expenses like split rent, divided dinner bills, or collected contributions.

What happens if I don't pay a payment link?

Payment links don't expire immediately, so you can pay them at your own pace. However, Cash App typically sets expiration dates (usually 30-90 days) after which the link stops working. You can check the remaining balance and when the link expires by clicking it. The payment requester can revoke links at any time through their Cash App dashboard.

Can payment links be used for international payments?

Currently, Cash App's international functionality is limited, and payment links follow these same limitations. You can typically use payment links for payments within the United States. Cross-border functionality may be available in the future as Cash App expands its international capabilities, but this isn't yet a primary feature of payment links.

How does Cash App prevent fraud with payment links?

Cash App uses multiple fraud prevention mechanisms: encrypted links, authentication requirements, IP and device fingerprinting, machine learning-based fraud detection, and monitoring for suspicious patterns. Users also play a role by verifying that links come from trusted sources and checking URLs before providing credentials or completing payments.

Are payment links better than traditional payment requests?

Payment links offer several advantages over traditional in-app payment requests: they work across any communication platform, they feel more casual and less formal, they don't rely on the recipient having notifications enabled, and they add context to payment requests by keeping them within existing conversations. However, both methods are secure and effective, so choosing between them depends on your specific situation and preferences.

Suggested Internal Links

These internal links would be relevant if your site has related content:

- Digital Payment Security: Best Practices for Safe Mobile Transactions

- The Future of Fintech: Emerging Trends in P2P Payments

- Gen-Z Financial Habits: How Younger Users Prefer to Manage Money

- Mobile Payment Apps Compared: Venmo vs. Cash App vs. Pay Pal

- Building Trust in Financial Apps: What Users Really Want

Suggested Pillar Topics

These broader topics would make excellent pillar pages:

- The Complete Guide to Mobile Payment Platforms and Solutions

- Financial Innovation in the Digital Age: Emerging Payment Technologies

- User Experience in Fintech: How Apps Win Loyalty Through Design

Key Takeaways

- Payment links generate unique URLs that encode payment requests, shareable across any communication platform and eliminating app notification friction

- Feature addresses genuine social friction identified through Gen-Z user research showing that payment discussions often feel overly formal or passive-aggressive

- Supports recurring and group payments, making it useful for split rent, shared expenses, and freelance payment collection scenarios

- Security relies on encrypted links, authentication requirements, fraud detection, and expiration mechanisms, making links safer than they might initially appear

- Represents broader shift in fintech philosophy toward contextual payments that integrate into existing communication flows rather than demanding app context switching

- Competitive response from Venmo, PayPal, and other platforms likely within 18-24 months, making payment links a baseline feature across industry