![Chinese Battery Factories Are Reshaping Global Manufacturing [2025]](https://tryrunable.com/blog/chinese-battery-factories-are-reshaping-global-manufacturing/image-1-1769114274851.jpg)

Chinese Battery Factories Are Reshaping Global Manufacturing [2025]

When a Chinese battery factory announces plans to open in your town, the reaction is almost always mixed. There's excitement about jobs and economic investment. Then comes the skepticism. Will locals actually get hired? What about the environment? Who really benefits when a foreign company plants roots thousands of miles from home?

These questions aren't abstract anymore. They're happening right now across Europe, North America, and beyond. Over the past decade, Chinese battery manufacturers have announced or built 68 major factory facilities outside China. That's not a typo. Sixty-eight. These aren't small operations either. We're talking about multi-billion-dollar investments from companies like CATL, BYD, and Gotion.

This shift marks something fundamental about how global manufacturing works in the 2020s. The old narrative about "Made in China" centered on cheap labor and cutting corners. But the companies building these new factories? They're often more advanced, more efficient, and more competitive than the incumbents they're challenging. They can relocate production anywhere on the planet and still out-compete local manufacturers.

That's a game-changer for everyone involved: communities hoping for jobs, governments worried about energy independence, workers concerned about labor practices, and consumers driving the shift to electric vehicles. The batteries these factories produce will power millions of cars, trucks, and energy storage systems. The way these factories operate will shape labor relations, environmental standards, and technological transfer across entire regions.

But here's what makes this story complicated: the expansion isn't going as smoothly as anyone expected. Policy uncertainty is stalling projects. Consumer adoption of EVs is slower than manufacturers hoped. And everywhere these factories open, they're meeting resistance from people asking hard questions about who actually wins.

Let's dig into what's really happening when Chinese battery makers come to town.

The Scale of Chinese Battery Dominance

Before you can understand the international expansion, you need to grasp just how dominant China has become in battery manufacturing. This isn't about market share points. This is about fundamental control of a critical technology.

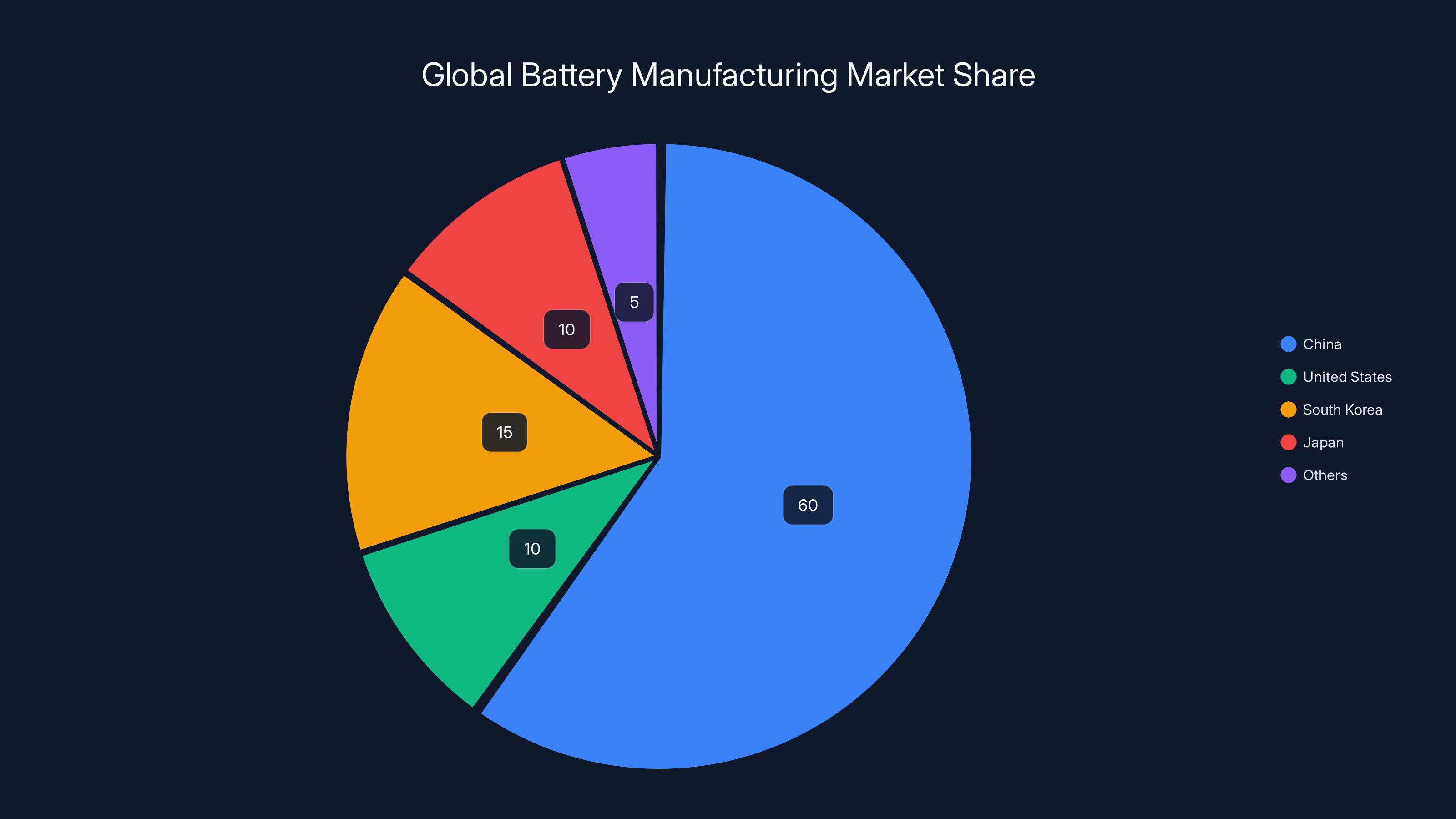

China produces roughly 75% of the world's lithium-ion batteries. That number alone doesn't capture the real picture. Chinese companies control the supply chains. They've invested heavily in refining, cathode production, anode materials, and everything else that goes into a battery. When you're looking at a Tesla, a BMW, or a Chevrolet Bolt, there's a good chance the battery inside it came from China or used Chinese-sourced components.

Companies like CATL have achieved scale that's genuinely difficult to compete against. CATL alone produces more batteries annually than all the battery manufacturers in the United States combined. Their factories operate with precision, efficiency, and cost structures that took years to develop. They've learned what works and what doesn't. When they move that knowledge to another country, they bring a proven playbook.

This isn't the result of accident or sudden innovation. Chinese manufacturers spent two decades establishing themselves as the world's battery hub. Government incentives helped. Access to raw materials helped. But what really matters is that they built competitive advantages that aren't easy to replicate. The supply chains, the manufacturing expertise, the worker training, the relationships with component suppliers, and the operational systems all compound over time.

Now they're exporting that advantage. When CATL or BYD opens a factory in Hungary or Mexico, they're not starting from zero. They're taking a proven operation and adapting it to a new location.

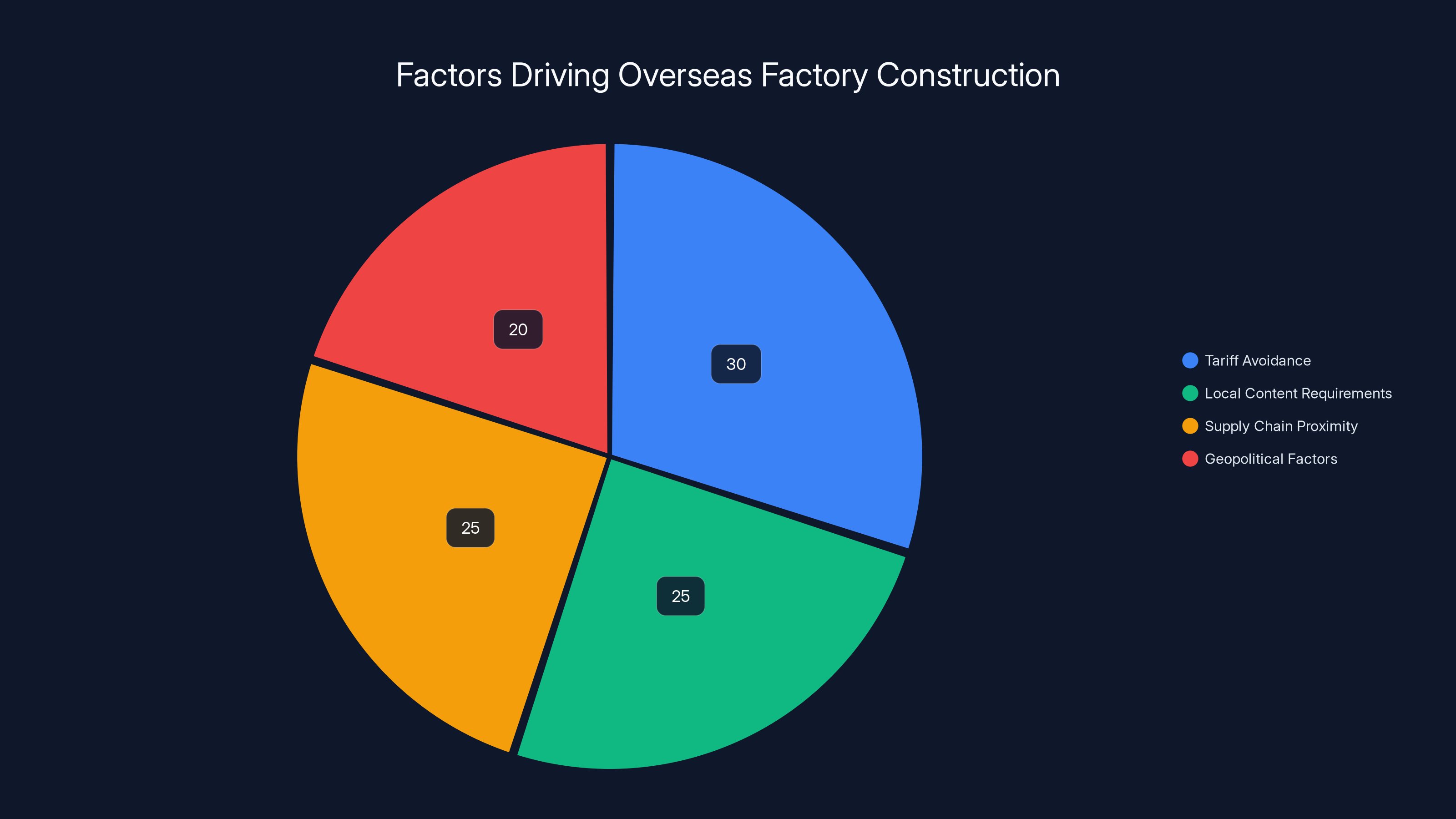

Tariff avoidance is the leading factor driving Chinese companies to build factories overseas, followed closely by local content requirements and supply chain proximity. Estimated data.

Why They're Building Overseas Now

If Chinese companies are already so dominant at home, why bother building factories anywhere else? The answer comes down to trade barriers, consumer preferences, and logistics.

First, there's the tariff problem. The United States, European Union, and other major markets have implemented or are considering significant tariffs on batteries and EVs made in China. These aren't small taxes either. We're talking 25% to 50%+ premiums on imported batteries. When you're competing on cost, that kind of tariff makes overseas production much more attractive. If you build a factory in Mexico or Hungary, you can avoid tariffs, access the local market, and still maintain your cost advantage.

Second, governments are increasingly requiring local content. The U. S. Inflation Reduction Act, for instance, provides subsidies to EV and battery manufacturers, but only if they meet domestic content requirements. Build your batteries in America, and you unlock billions in incentives. Keep production in China, and you lose access to those programs. This creates a straightforward economic incentive: relocate or lose market access.

Third, car manufacturers want to be close to their supply chains. Tesla, Ford, Volkswagen, and other automakers are building more EV production capacity in Europe and North America. If you're an automaker, you don't want to ship batteries across oceans. You want them made nearby, reducing shipping costs, improving delivery times, and managing supply chain risk. So battery makers follow the car makers.

Fourth, there's the geopolitical reality. Consumers and governments are increasingly uncomfortable with supply chain dependence on China. Framing battery production as local helps automakers market their vehicles as domestically made. It's partly politics, partly real logistics, but the effect is the same: battery makers need to build outside China.

Chinese companies understood these incentives early. They started making strategic investments in the early 2010s, building small pilot facilities in Europe and other markets. As tariff walls rose and local content requirements tightened, the pace of expansion accelerated dramatically.

But here's the complication: they invested in this expansion during a period of extraordinary optimism about EV adoption. Governments were throwing subsidies at both consumers and manufacturers. It seemed obvious that demand would grow exponentially. Battery makers planned massive factories betting on that growth. Then the policy environment changed, subsidies were reduced or eliminated, and suddenly those factories looked like expensive bets on a slower-growing market.

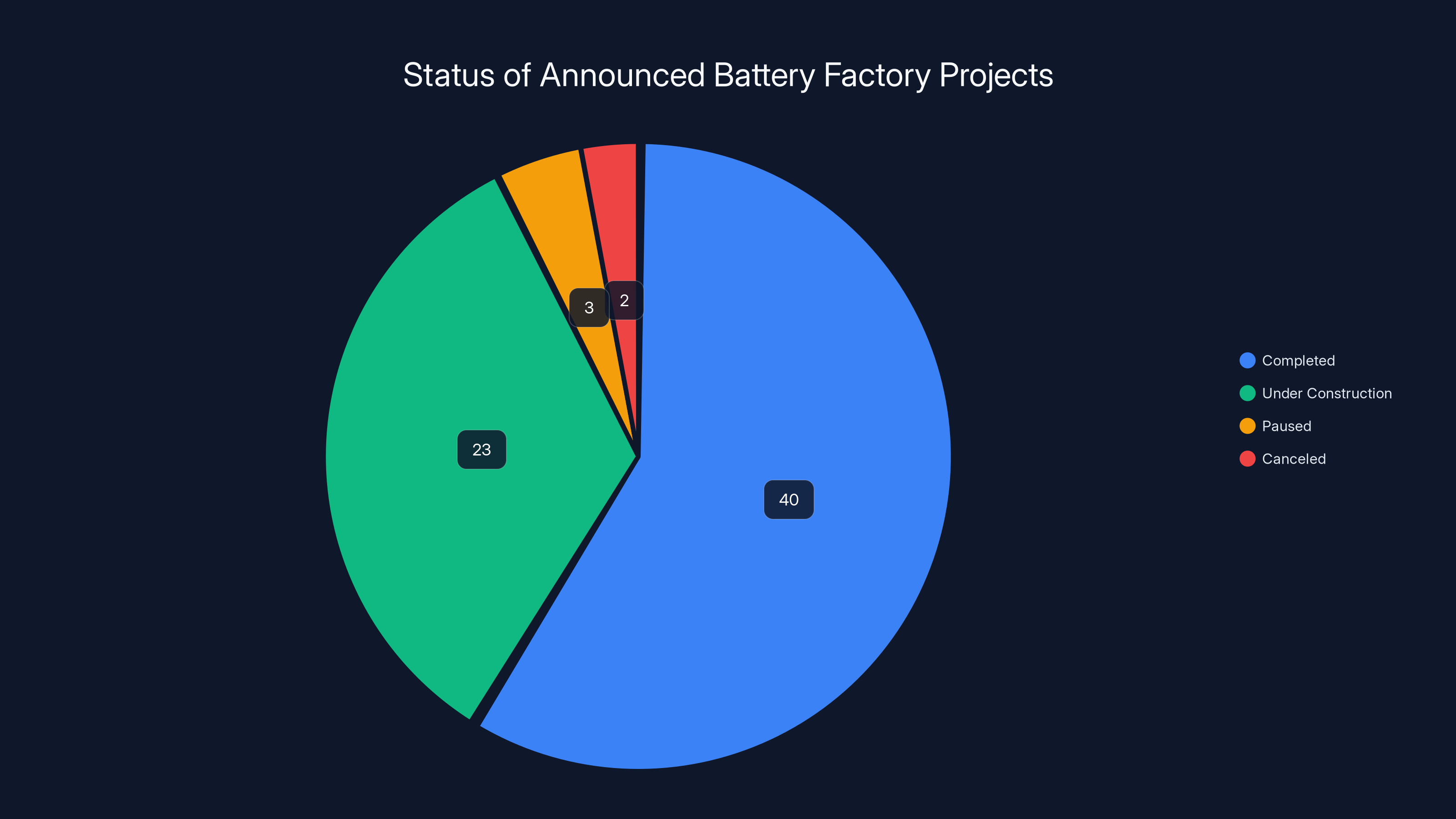

Out of 68 announced battery factories, 5 have been paused or canceled, highlighting the impact of shifting market demands and policy changes. (Estimated data)

Hungary as the Canary in the Coal Mine

If you want to understand what happens when Chinese battery factories come to a small European country, Hungary is your case study. It's the most striking example globally of both the opportunities and tensions that emerge.

Hungary isn't a random choice. The country sits strategically in Central Europe, near major German automakers and Western European markets. It has lower labor costs than Germany or Austria but access to EU infrastructure and regulations. The Hungarian government actively courted battery manufacturers, offering tax incentives and streamlined permitting. Over the past five years, at least four major battery plants have been announced or begun construction in Hungary, with CATL's facility representing an $8.5 billion investment.

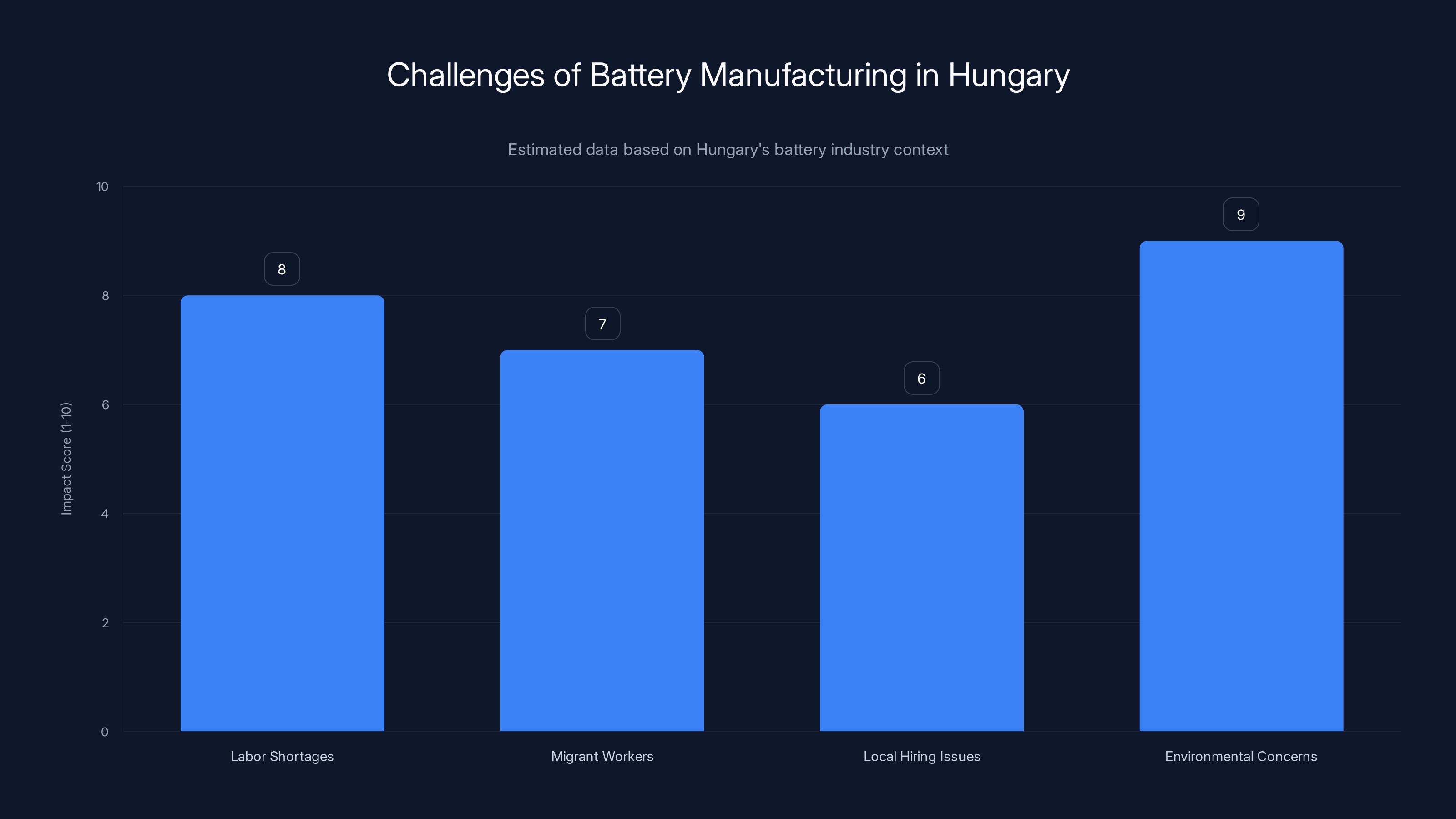

But the situation reveals deep tensions. Hungary was already struggling with labor shortages before these factories arrived. Many Hungarians had moved to Western Europe seeking higher wages and better opportunities. There aren't enough local workers to fill factory positions. So Chinese companies partnered with the Hungarian government to bring in migrant workers from Central Asia, Southeast Asia, and other regions. That triggered backlash from local residents who worried about job displacement and cultural change.

When CATL laid off more than 100 workers at its planned factory site in the summer, the local municipality launched an investigation into whether the company had honored commitments to hire locally. The optics were terrible. A foreign company had promised jobs and investment. Instead, there were layoffs and questions about workforce planning.

Environmental concerns made things worse. Battery manufacturing requires significant amounts of water. Hungary, already facing water stress from drought and climate change, became the focus of protests about resource depletion. Samsung, a Korean battery manufacturer, had already faced similar criticism. When Chinese companies announced plans in the same drought-prone regions, they immediately inherited the existing environmental debate.

Hungarian courts had recently ordered Samsung's battery plant to suspend production over pollution concerns. Now Chinese companies faced similar scrutiny. Groundwater contamination during battery production wasn't a new issue, but it was becoming more visible and contested.

There's also a fundamental mismatch between who makes batteries and who uses them. Most batteries produced in Hungary are destined for wealthy consumers in Germany, France, and other Western European countries. The average Hungarian doesn't have the purchasing power for a new electric vehicle. They drive used cars imported from Germany. So the local community experiences the environmental costs and labor disruption but misses the consumer benefits of the clean energy transition. The benefits flow elsewhere.

Andras Bartok, who studies Hungary's relationship with China, points out that this creates a perception problem. Local residents feel disconnected from the global green energy transition. They see factories, environmental concerns, and migrant workers but don't see themselves as participants in the clean energy future. That's a genuinely difficult political problem with no easy solution.

Despite these tensions, Hungary has become a hub for Chinese battery investment. The government sees it as economic development. The companies see it as market access. But the residents living near these facilities are grappling with real costs and uncertain benefits.

Environmental Impact and Water Stress

Battery manufacturing is not a clean industry. That's worth stating plainly. While batteries enable cleaner transportation, the process of making them requires substantial resources, energy, and generates waste.

Water consumption is the biggest environmental concern. Lithium extraction, cathode production, and battery assembly all require significant water. In water-stressed regions, this creates real conflicts between industrial development and community needs. Hungary, Chile, Australia, and parts of the American Southwest all face water scarcity, and they're also prime locations for battery manufacturing.

Chilean lithium mining, which supplies material for batteries worldwide, has consumed so much groundwater that it's affected local communities and ecosystems. When battery companies want to expand lithium extraction, they're competing for resources with agricultural communities and indigenous populations. The environmental cost isn't hypothetical. It's experienced by people who depend on groundwater for survival.

This is where the story gets genuinely complicated. Battery manufacturing contributes to climate change in the short term through energy consumption and resource extraction. But batteries enable electric vehicles, which reduce climate change in the long term. The net benefit depends on how you account for the environmental costs of production and the benefits of EVs over their lifetime.

Manufacturers aren't always transparent about these trade-offs. They market batteries as green technology without equally emphasizing the environmental costs of production. That's understandable from a marketing perspective, but it creates a credibility problem when communities discover the real impacts.

Pollution concerns go beyond water. Battery manufacturing involves chemicals, particulates, and emissions that affect air and soil quality. Communities near battery factories report respiratory issues and other health concerns. Are these issues definitively caused by the battery factories? Sometimes the evidence is clear. Sometimes it's contested. But the concern is real, and it shapes how people perceive these investments.

The irony is that Chinese manufacturers often bring better environmental standards than local competitors. Their factories operate under tighter controls than some regional alternatives. But "better than the worst alternative" isn't the same as "good." Communities are comparing Chinese battery factories to their idealized vision of clean industry, not to the alternative of having no factory. That gap between expectations and reality fuels frustration.

China dominates global battery manufacturing with an estimated 60% market share due to strategic investments and supply chain control. Estimated data.

Labor and the Migration Question

One of the sharpest tensions surrounding Chinese battery factory expansion involves labor. Who gets hired? What do they earn? How are they treated? These questions matter intensely to communities and workers.

When battery factories open in developed countries like Hungary or the United States, they're often in regions with labor shortages or regions where local wages are lower than in major cities. The factories need workers. Lots of them. But there aren't always enough local candidates, especially for semi-skilled manufacturing roles.

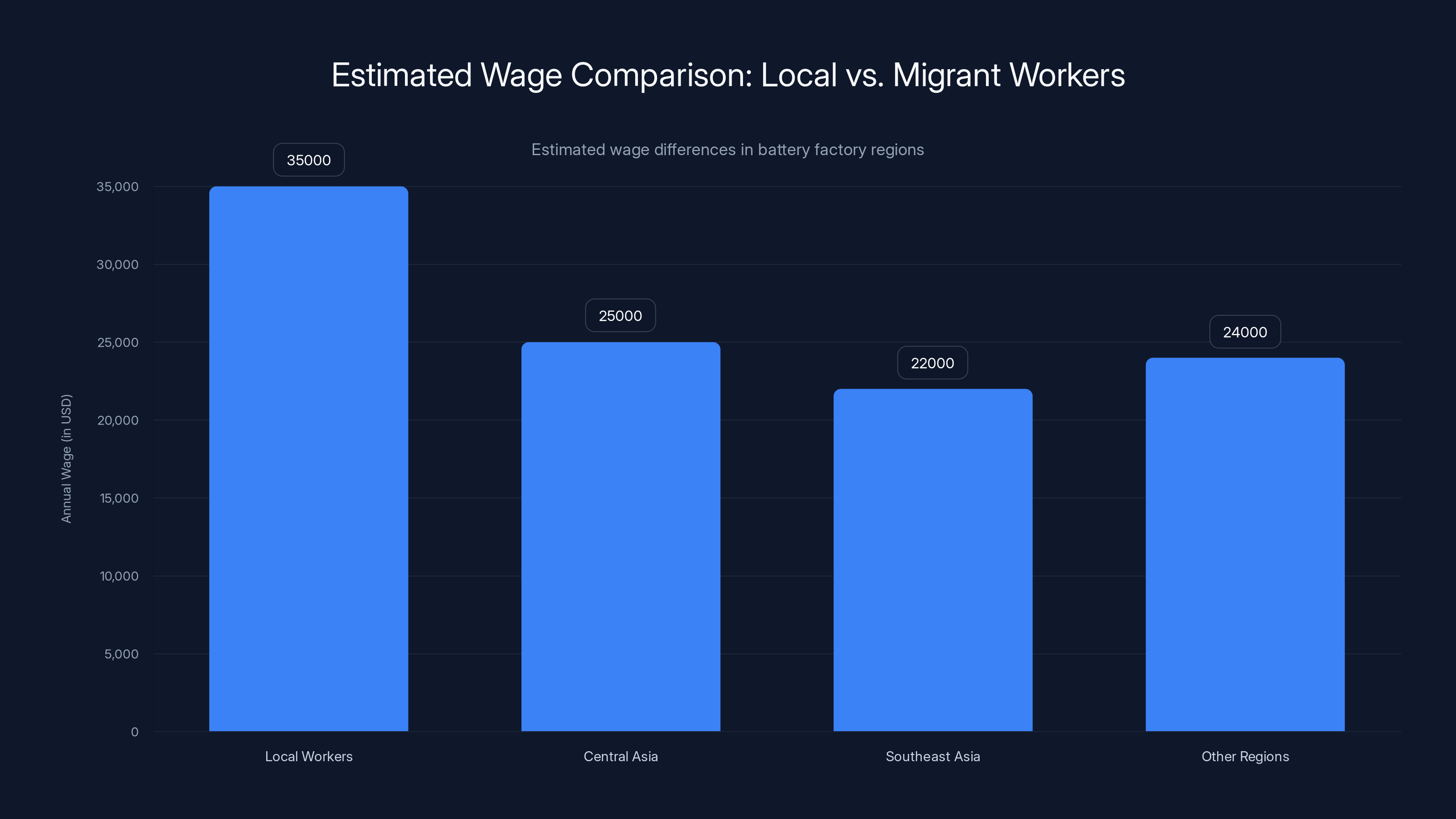

Chinese manufacturers have traditionally solved this problem by bringing workers from countries with lower wage expectations. CATL and other companies have brought workers from Central Asia, Southeast Asia, and other regions where annual wages are significantly lower than local standards. This approach maximizes cost efficiency but creates social friction.

When migrant workers arrive in communities that haven't experienced significant immigration, the cultural and economic impacts are visible and contested. Long-term residents worry about wages being suppressed. They worry about housing costs rising as new workers move in. They worry about strains on local services and cultural change.

Are these concerns justified? Sometimes. Labor markets are real. If you bring in workers willing to work for lower wages, it can depress local wage expectations. But the overall economic impact is more complex. The workers also spend money in local communities, rent housing, and use local services. They contribute to economic activity even as they potentially affect wage dynamics.

Manufacturers argue they bring in migrant workers because they can't find enough local candidates. That's often true in regions with labor shortages. But it's also true that bringing in lower-wage workers improves the company's financial position. The incentives are misaligned between what's good for the company and what's good for local labor markets.

Some communities have negotiated agreements requiring manufacturers to hire minimum percentages of local workers. This helps but doesn't eliminate the tension. A German battery factory might commit to hiring 60% locally. That still means 40% migrant workers, which is substantial in a small town.

Wages at battery factories are often decent compared to regional alternatives but lower than comparable manufacturing jobs in wealthy countries. A worker in Hungary earning €800/month at a battery factory is earning more than they would in many alternative jobs but far less than someone doing similar work in Germany or Austria. That creates its own form of economic inequality, even if it's an improvement for the individual worker.

The labor question also intersects with gender. Battery manufacturing has traditionally been male-dominated, like most manufacturing industries. Chinese manufacturers are beginning to hire more women, but gender pay gaps and workplace safety concerns persist. In some regions, migrant women workers report exploitation and poor treatment.

This isn't unique to Chinese companies. It reflects broader manufacturing industry practices. But when Chinese manufacturers come to communities, they inherit the scrutiny that comes with being new, foreign, and large.

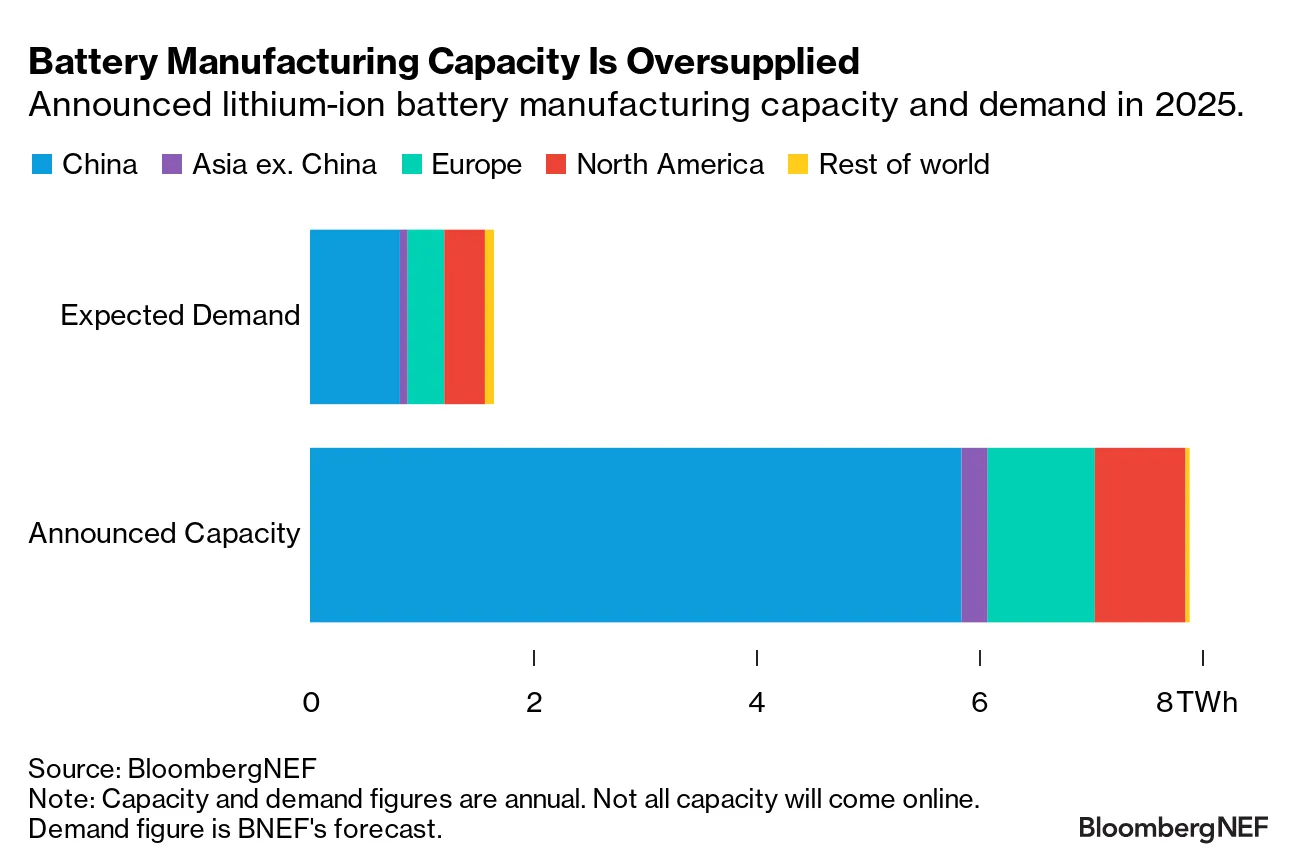

The Investment Pipeline and Project Cancellations

Not every announced battery factory actually gets built. In fact, quite a few don't. Of the 68 major battery facilities announced by Chinese companies outside China, at least five have been paused or officially canceled. Some cancellations happened after construction had already begun.

Why would a company announce a major factory investment, begin construction, and then cancel? The primary reason is market demand uncertainty. Chinese manufacturers made aggressive global expansion plans during a period of extreme policy support. Governments were subsidizing battery production and offering tax credits for EV purchases. It seemed inevitable that demand would grow exponentially.

Then the policy environment shifted. The U. S. reduced or eliminated some EV subsidies under the Trump administration. Europe has become more cautious about aggressive EV transition timelines. Consumers have proven more price-sensitive than manufacturers expected. An EV that costs

EV adoption hasn't stopped. It's growing globally. But it's growing more slowly in many developed markets than battery manufacturers projected. A factory built for 100 GWh of annual capacity becomes uneconomical when demand is only 60 GWh. You can't just abandon a half-built factory. The capital costs are sunk.

Some companies have delayed projects indefinitely. Others have pivoted. Ford announced it would shift a battery plant from EV batteries to energy storage batteries. Energy storage is growing faster than EV production in some markets, so that makes financial sense. Envision AESC paused U. S. expansion but is exploring energy storage opportunities.

This creates a problem for communities that have already begun benefiting from factory investment. In some cases, local governments have invested in infrastructure improvements, training programs, and incentive packages. When projects get canceled or significantly delayed, the community is left with unused capacity and unfulfilled economic expectations.

For investors and companies, project cancellation is a normal part of business. Plans change. Markets shift. Investors understand this. But for communities, it feels like broken promises. A mayor campaigns on bringing jobs and investment. Construction begins. Workers are hired or retrained. Then the project pauses indefinitely. Trust is damaged.

The canceled projects also reveal something important about the broader expansion strategy. Chinese manufacturers didn't necessarily do fine-grained market analysis for each location. They made broad bets that EV demand would grow globally and profitably. Some bets worked out. Others didn't. The markets that got burned are learning to be more skeptical about the next wave of announcements.

Estimated data shows that environmental concerns and labor shortages are the most significant challenges faced by Hungary due to the influx of battery manufacturing investments.

Policy Uncertainty and Subsidy Dependence

Large-scale manufacturing investment requires confidence about the future. Battery factory decisions involve billions of dollars committed over decades. That kind of capital only flows when there's clarity about policy direction, tariffs, subsidies, and regulations.

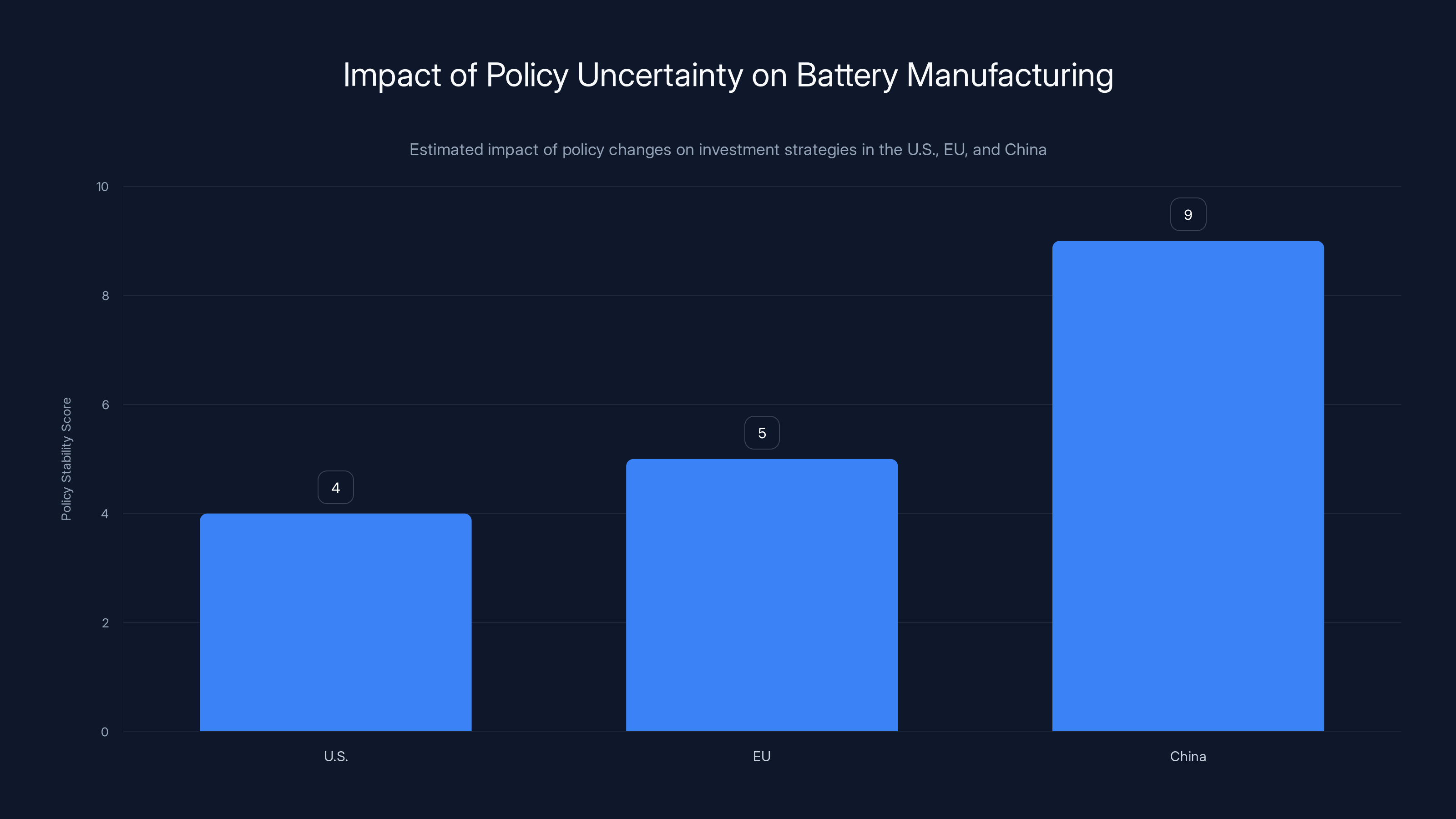

The problem is that policy is increasingly uncertain. The U. S. Inflation Reduction Act was a huge signal that battery production was a priority. But then the Trump administration moved into 2025 signaling different priorities. Would subsidies be maintained? Would tariffs increase? Would local content requirements be strictly enforced? Suddenly, the future looked murkier.

Europe similarly sent mixed signals. The EU was aggressively pushing EV adoption and committed to eliminating gas-powered vehicles by 2035. Then cost pressures and consumer pushback caused the EU to reconsider that timeline. If the 2035 deadline slips to 2040 or 2045, battery demand projections change significantly. Manufacturers have to recalibrate their expansion plans.

China itself is taking a different approach. Battery manufacturers can rely on predictable government support, consistent subsidy levels, and strategic planning horizons measured in decades. They're comfortable making massive investments because they expect policy consistency.

Western governments are less predictable. Administrations change. Priorities shift. Subsidies get cut or expanded based on political considerations. From a manufacturer's perspective, that creates risk. It makes smaller, more modular expansion strategies more rational than the huge factory bets that were being made in 2020-2023.

Battery manufacturers are learning to hedge their bets. Instead of one massive factory, build multiple smaller facilities. Instead of betting everything on EVs, diversify into energy storage, stationary power systems, and other applications. Instead of assuming subsidies will continue forever, build business models that work without them.

The policy uncertainty also creates incentives for manufacturers to lobby for continued support. The irony is that by making expansion decisions dependent on subsidies, manufacturers have locked themselves into supporting government policies that favor their sector. If subsidies disappear, their investment thesis breaks down.

This dependency creates a feedback loop. Manufacturers announce massive investments based on subsidy expectations. Governments see those investments and feel more committed to supporting the battery industry. Eventually, though, voters or fiscal constraints force policy changes. Then manufacturers scramble to adapt.

For communities hoping to host battery factories, policy uncertainty is a real concern. A factory that's profitable with subsidies might not be viable without them. Local economic development plans built on factory expansion can collapse if policy changes. It's not something communities can control, but it's something they should understand before celebrating factory announcements.

The Energy Storage Pivot

Something interesting is happening as EV demand growth slows: battery manufacturers are increasingly interested in energy storage. This represents a potential pivot in the global battery industry that could reshape where factories are built and how they operate.

Energy storage is different from EV batteries. Instead of powering vehicles, energy storage systems store electricity from the grid, solar panels, wind turbines, or other sources. The electricity is then released when it's needed. This solves one of the fundamental problems with renewable energy: it's intermittent. Solar panels don't generate power at night. Wind turbines don't generate power on calm days. Energy storage bridges those gaps.

As countries transition to renewable electricity, energy storage demand grows. Utilities need batteries to manage grid stability. Businesses need backup power systems. Homeowners want to store solar energy for nighttime use. The market is smaller than EV batteries today, but it's growing faster in many regions.

From a manufacturer's perspective, energy storage has different economics than EV batteries. EV batteries are manufactured to strict specifications, optimized for weight and performance. Energy storage batteries can be heavier and bulkier. Manufacturing requirements are less stringent. But energy storage batteries need to be highly reliable and durable because they operate continuously, not just when someone is driving.

Ford's announcement that it would shift production at its Michigan battery plant from EV batteries to energy storage batteries signals this transition. Envision AESC's recent announcements about energy storage expansion point in the same direction. If this trend accelerates, it could change which regions are attractive for battery manufacturing.

Energy storage demand is growing faster in developed countries with high renewable penetration. Germany, California, Australia, and other regions need substantial energy storage to manage renewable integration. That means battery factory locations might shift from EV-focused regions to electricity transmission hubs.

This is also where Chinese manufacturers' technological advantage becomes even more important. Building energy storage systems is partly about batteries but also about power electronics, software, and system integration. Chinese companies have invested heavily in these areas. They're not just battery manufacturers. They're energy technology companies.

The pivot to energy storage also changes the sustainability narrative. Manufacturing a battery for energy storage contributes directly to renewable energy integration. There's no debate about whether it contributes to climate action. It obviously does. That makes energy storage battery factories potentially more acceptable to communities concerned about environmental impact.

But it also means that factory locations, wages, environmental practices, and labor standards will remain contested. Energy storage doesn't eliminate the fundamental tensions around manufacturing in developed countries with high environmental standards and high labor costs.

Estimated data shows that migrant workers from Central and Southeast Asia earn significantly less than local workers, highlighting potential wage suppression concerns.

Global Supply Chain Implications

When Chinese battery manufacturers build factories outside China, they're not just relocating production. They're beginning to reshape global supply chains. This has implications for everything from mineral sourcing to technology transfer to economic dependence.

Battery manufacturing depends on a supply chain of inputs. You need lithium, cobalt, nickel, manganese, and other materials. You need separators, electrolytes, and other chemical components. You need manufacturing equipment and expertise. China has advantages in all of these areas.

But the supply chain isn't just within China anymore. Chinese mining companies are extracting lithium in Chile, Argentina, Australia, and other countries. Chinese companies are building refining capacity in multiple countries. Chinese equipment manufacturers are selling to battery factories worldwide. The supply chain is becoming distributed, but it's still heavily controlled by Chinese companies.

This creates a strategic reality: even if a battery factory is located in the United States or Europe, it might still be dependent on Chinese supply chains for key inputs. That's not necessarily problematic, but it means that reshoring battery production doesn't fully eliminate supply chain dependence on China. It relocates assembly but maintains material and equipment dependence.

Technology transfer is another critical element. When Chinese manufacturers build factories in developed countries, they're bringing production expertise and technical knowledge. That knowledge gradually transfers to local workers, equipment suppliers, and related industries. Over time, the local ecosystem becomes more capable of competing in battery manufacturing.

This happened historically with Japanese manufacturing. When Japanese companies built auto factories in the United States, they brought manufacturing expertise that ultimately improved American manufacturing practices. The same is happening with battery manufacturing. Chinese companies are inadvertently raising the competence level of the regions where they operate.

For developed countries, that's potentially good. For China, it's a strategic risk. As technical knowledge diffuses and local competitors develop, Chinese manufacturers' cost advantages might erode. Some Chinese companies are beginning to protect proprietary technology more carefully when they build overseas factories. But knowledge transfer is hard to prevent when you're employing local workers and selling to local suppliers.

The supply chain implications also affect geopolitics. Countries that host battery factories become more enmeshed with China economically. They depend on Chinese expertise, investment, and supply chains. That creates political leverage for China. If tensions rise, China could potentially restrict access to critical battery components or withdraw investment. That's not typically discussed explicitly, but it's understood by strategic planners in developed countries.

For developing countries, Chinese battery manufacturing investment offers opportunities for technology transfer and economic development. Workers and companies learn manufacturing practices. Infrastructure improves. Capital flows into the local economy. But it also creates dependencies on Chinese companies and potentially locks regions into battery manufacturing without developing more diversified industries.

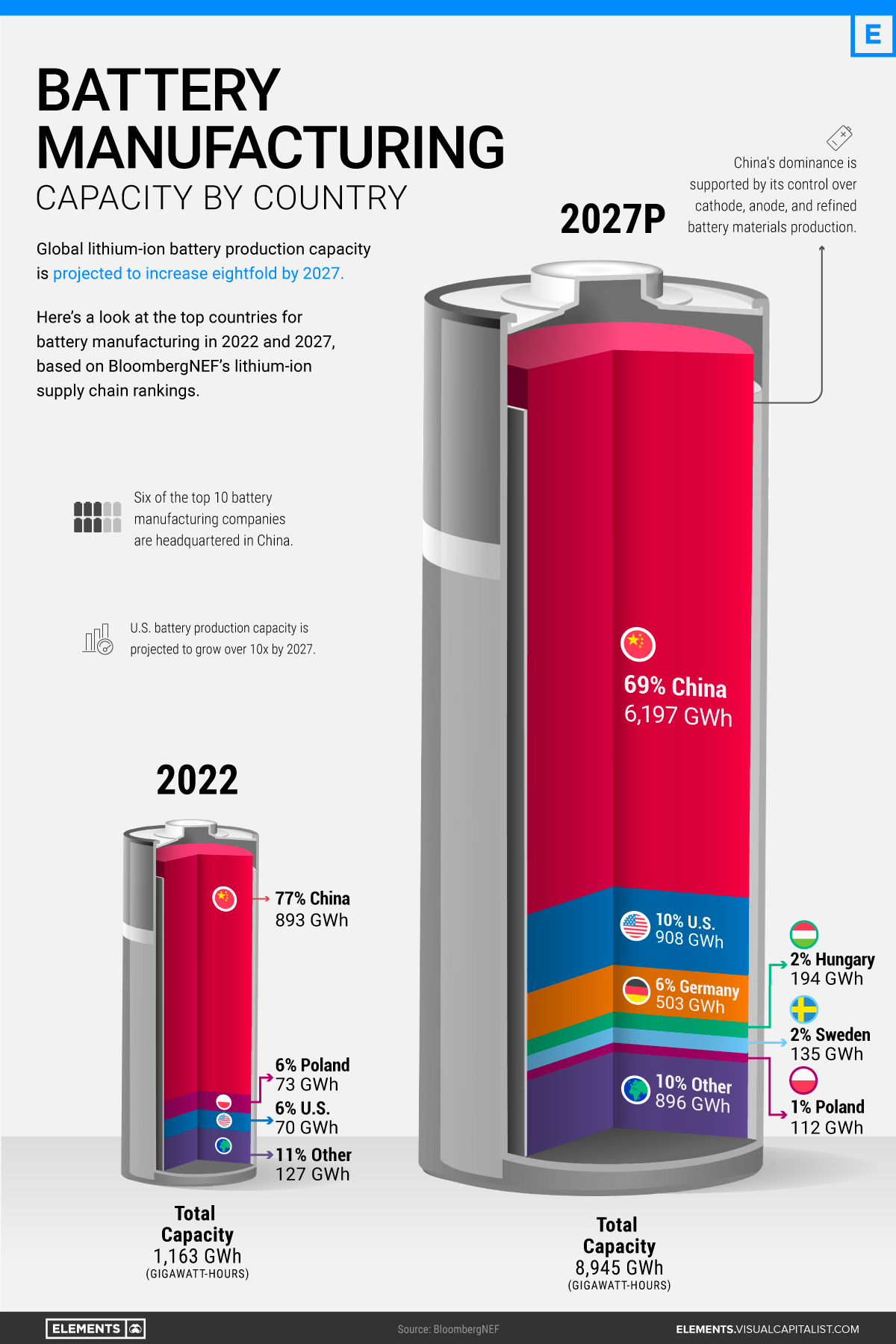

The United States Battery Strategy

The United States has begun implementing a distinct battery and EV strategy in response to Chinese dominance. The Inflation Reduction Act, Bipartisan Infrastructure Law, and other policies aim to rebuild American battery manufacturing capacity. It's a direct challenge to Chinese dominance and a recognition that battery supply chains are strategically important.

The goal is clear: shift battery production from China to the United States. Create domestic manufacturing capacity. Build local supply chains. Reduce dependence on imports. These are reasonable strategic objectives, but they're also economically difficult to achieve.

The problem is cost. Chinese manufacturers have achieved scale, efficiency, and cost structures that American manufacturers can't easily match. Building a competitive American battery industry requires either subsidies or tariffs (or both). The Inflation Reduction Act provides both. Companies building batteries in America get substantial tax credits. Companies importing batteries face tariffs. That changes the economics.

But subsidies are expensive. The IRA dedicates hundreds of billions to EV and battery manufacturing support. Over time, that creates political pressure to reduce spending. Once subsidies are reduced, the cost advantage disappears unless American manufacturers can match Chinese efficiency.

Chinese companies understand this. Some are building factories in the United States to access IRA subsidies while maintaining cost advantages through operational expertise and supply chain sophistication. It's a way of capturing government support while preserving competitive advantages.

The challenge for American manufacturers is building competitive capacity from scratch. Tesla and other companies are trying. They're building factories, developing expertise, and improving efficiency. But they're starting from behind. A factory built in 2024 is competing against factories built over two decades with cumulative improvements.

The long-term outcome is uncertain. It's possible American manufacturers will eventually achieve cost parity with Chinese manufacturers. It's possible they'll always be dependent on subsidies. It's possible Chinese manufacturers will dominate American battery production despite tariff walls and local content requirements. The outcome depends on execution, technological progress, and policy stability.

What's clear is that battery manufacturing is now recognized as strategically important by governments. It's not just a commercial market. It's a domain of industrial policy and geopolitical competition. That recognition shapes investment decisions, policy choices, and factory locations.

Estimated data shows China offers the most stable policy environment for battery manufacturers, encouraging larger investments compared to the U.S. and EU, where policy uncertainty leads to more cautious strategies.

Mexico as the Next Frontier

While Hungary is the European battleground for Chinese battery manufacturing, Mexico is becoming the critical battleground in the Western Hemisphere. Mexico has advantages that make it attractive to Chinese manufacturers and American automakers alike.

Geography is one advantage. Mexico shares a border with the United States and is close to North American automotive production centers. Building a battery factory in Mexico puts the product close to American and Canadian automakers and consumers. Transportation costs are lower. Supply chain coordination is easier. From a logistics perspective, Mexico makes sense.

The other advantage is labor. Mexican manufacturing wages are higher than in China but lower than in the United States or Canada. Mexican workers have manufacturing experience. The Mexican government is interested in attracting battery manufacturing investment. All of this makes Mexico an attractive location for factories serving the North American market.

China recognizes this. Chinese battery manufacturers have announced or begun construction on multiple facilities in Mexico. Some are joint ventures with Mexican companies. Others are wholly owned by Chinese firms. The scale of investment is substantial.

This creates strategic concerns for the United States. If Chinese battery manufacturers establish dominant positions in Mexico, they can serve the North American market through Mexican facilities, potentially avoiding some tariff and local content requirements. It's a way of getting around American trade barriers by locating just across the border.

The U. S. strategy is to either prevent Chinese battery factories in Mexico or ensure that North American supply chains are deeply integrated. If batteries are made in Mexico but sourced with North American materials and sold to North American automakers, the strategic concern is reduced. If batteries are made in Mexico using Chinese supply chains and sold to Chinese-controlled entities, the concern is higher.

Mexico, meanwhile, is playing its own game. The Mexican government wants battery manufacturing investment because it creates jobs and economic development. Whether that investment comes from China, America, Japan, or Europe is less important to Mexico than the fact that it comes.

The Mexico story is still developing. Factory announcements are being made. Communities are reacting. Environmental and labor concerns are emerging. Over the next few years, Mexico will become the testing ground for how battery manufacturing plays out in North America. The tensions that emerged in Hungary will likely emerge in Mexico as well, but with different political and economic contexts.

Technology and Competitive Advantages

Why are Chinese battery manufacturers so dominant? What specific advantages do they have? Understanding this helps explain why Chinese factories can operate competitively anywhere in the world.

The first advantage is manufacturing expertise. Chinese manufacturers have built thousands of facilities, optimized production processes, and trained hundreds of thousands of workers. They understand how to minimize waste, maximize throughput, and maintain quality at scale. This expertise compounds over time. Each factory built is slightly better than the last.

The second advantage is supply chain integration. Chinese battery manufacturers often own or have close relationships with suppliers of key components. They control the supply of separators, electrolytes, and other materials. This vertical integration reduces costs and improves supply reliability. Western manufacturers often buy components from specialized suppliers, which adds costs and complexity.

The third advantage is automation and robotics. Chinese manufacturers have invested heavily in automation. Modern battery factories use robots for dangerous, repetitive tasks. This improves safety, consistency, and efficiency. Chinese manufacturers have the capital and expertise to implement automation at scale.

The fourth advantage is talent. Battery manufacturing requires engineering expertise, chemistry knowledge, and technical skill. Chinese universities produce enormous numbers of engineering graduates. Chinese companies have built recruiting and training systems to develop technical talent. They can staff large, complex facilities with qualified people.

The fifth advantage is research and development. Chinese battery companies invest heavily in R&D. They're not just copying old designs. They're developing new battery chemistries, new manufacturing processes, and new applications. This innovation maintains their competitive advantage as technology evolves.

The sixth advantage is government support. Chinese companies have benefited from government subsidies, industrial policy, and strategic support. That support enabled them to make long-term investments and develop capabilities that private markets might not have funded. Now that they're established, they maintain advantages even without continued subsidies.

When these advantages are combined, they create a competitive moat that's difficult to breach. A new battery factory competing against Chinese manufacturers faces companies with more experience, better supply chains, more automation, better talent, more innovation, and historical support advantages.

Can these advantages be replicated? Partially. New factories can implement similar technologies. They can hire talented people. They can invest in supply chain integration. But they're starting from behind, competing against companies that have been optimizing for decades.

The competitive dynamics will likely shift over time as technology evolves and supply chains mature. But in the near term, Chinese manufacturers will likely maintain significant advantages even when operating outside China.

Environmental Regulation and Standards

When Chinese battery manufacturers operate in developed countries, they encounter environmental regulations that are often more stringent than in China. This affects production costs, facility design, and operational practices. Understanding how manufacturers navigate these regulations is important for assessing the real environmental impact of their facilities.

Developed countries typically have strict regulations around emissions, wastewater discharge, chemical handling, and waste management. Europe's environmental standards are particularly rigorous. China's standards have improved significantly but are generally less stringent than European standards.

When Chinese manufacturers build factories in Europe, they must comply with European standards. They can't import Chinese operational practices that wouldn't meet European regulations. This is actually a positive thing for environmental outcomes. Chinese factories operating under European standards will have lower environmental impact than Chinese factories operating under Chinese standards.

But this creates a cost penalty. Compliance with strict environmental standards requires investment in pollution control equipment, wastewater treatment systems, and monitoring infrastructure. These investments increase capital costs and ongoing operational expenses.

Some Chinese manufacturers try to minimize these compliance costs. They argue for regulatory flexibility or delays in meeting standards. This has created friction with European regulators and environmental advocates. But ultimately, European standards typically prevail. Companies operating in Europe must meet European environmental requirements.

The irony is that environmental regulations in developed countries, while potentially increasing battery manufacturing costs, reduce the environmental impact of battery production. A battery produced in a European factory with strict environmental standards has lower environmental cost than a battery produced in a factory with minimal controls.

This raises an important question: how do we measure the environmental impact of batteries? Do we only count the factory emissions? Do we include supply chain impacts? Do we compare factory emissions in different countries? These are genuinely difficult accounting questions, but they matter for assessing the true environmental cost of battery manufacturing.

Chinese manufacturers are gradually improving environmental practices and investing in cleaner technology. Newer factories often have better environmental performance than older facilities. But the question of whether advanced environmental standards in developed countries make battery production meaningfully cleaner or just more expensive is genuinely contested.

Consumer Perception and Brand Challenges

China's battery manufacturers face a branding and perception challenge in developed markets. "Made in China" carries connotations that aren't always favorable. Quality perceptions have improved over decades, but skepticism remains.

When a consumer sees that their EV has a CATL or BYD battery, what do they think? In China, these companies are seen as advanced, high-quality manufacturers. In the United States or Europe, many consumers aren't familiar with the company names. Others might have concerns about Chinese manufacturing or Chinese companies generally.

Manufacturers address this by emphasizing technical quality, testing, and warranty coverage. They highlight that their batteries power vehicles from major global automakers like Tesla, Ford, and Volkswagen. The implicit argument is: these batteries are good enough for major brands, so they're good enough for you.

But perception is sticky. Chinese manufacturers building factories overseas is partly a strategy to address brand concerns. A battery made in the United States, even by a Chinese company, is more acceptable to American consumers than a battery imported from China. It's the same product with different origins, but the perception changes.

This is an example of how manufacturing location shapes consumer perception independently of actual product quality. A factory in Mexico makes batteries more acceptable to North American consumers. A factory in Hungary makes batteries more acceptable to European consumers. The technology is the same, but where it's made shapes how it's perceived.

Over time, consumer perception will likely shift as Chinese manufacturers prove reliability and quality in overseas markets. But in the near term, local manufacturing helps address skepticism and builds brand equity.

The Future of Battery Manufacturing Geography

Where will battery manufacturing be located in 2030 or 2040? The answer depends on how policy evolves, how technology develops, and how consumer preferences shift.

If current trends continue, battery manufacturing will become more geographically distributed. Factories will be located closer to major markets to reduce shipping costs and improve supply chain resilience. This means more factories in North America, Europe, and Asia. Fewer batteries shipped across oceans.

China will likely remain the dominant center of battery manufacturing, but its share of global production will decline as other regions develop capacity. The absolute volume of Chinese production might increase, but the percentage will decrease.

Cost pressures will remain constant. Battery manufacturing will continue to concentrate in regions with lower labor costs and favorable policy support. This might mean continued growth in Mexico, Eastern Europe, and Southeast Asia. It might mean contraction in high-cost regions if subsidies are reduced.

Technology evolution will reshape manufacturing. Solid-state batteries, lithium iron phosphate chemistries, and other emerging technologies require different manufacturing processes. Companies that can adapt manufacturing facilities to new technologies will maintain advantages. Companies locked into current technologies might struggle.

Energy storage will grow faster than EV batteries. This will reshape factory locations and configurations. Regions with substantial renewable energy generation and grid challenges will be particularly attractive for energy storage battery manufacturing.

Geopolitical considerations will increasingly shape manufacturing locations. Countries want to reduce dependence on China, which means building alternative capacity. But alternative capacity is expensive to develop. This tension will create pressure for subsidies, tariffs, or regulations that shape where batteries are made.

The wildcard is labor. If automation continues advancing, labor costs become less important. Factories could be located based on other factors: energy costs, proximity to raw materials, proximity to markets. If automation plateaus, labor costs remain critical and manufacturing concentrates in lower-wage regions.

Overall, battery manufacturing is likely to become more geographically distributed but remain concentrated in regions with scale advantages, favorable policy environments, and technical expertise. China will remain important, but it won't be as dominant as it is today. Multiple regional hubs will develop.

For communities considering hosting battery factories, the lesson is clear: the long-term viability of these facilities depends on competitiveness, policy support, and market conditions. Factories built on subsidies alone are vulnerable to policy changes. Factories built on genuine cost or technical advantages are more durable.

Key Lessons and Takeaways

The global expansion of Chinese battery manufacturing raises important questions about manufacturing, trade, environment, labor, and geopolitics. A few key lessons emerge from examining where factories are being built and what's actually happening in these communities.

First, manufacturing location matters. Where something is made affects its cost, its environmental impact, the jobs it creates, and its political significance. For batteries, location affects whether factories are economically viable and whether local communities benefit or bear costs.

Second, policy shapes investment decisively. Subsidies, tariffs, local content requirements, and other policy tools redirect capital and reshape manufacturing geography. But policy uncertainty undermines investment. Companies need confidence about the future policy environment to make billion-dollar commitments.

Third, communities experience batteries as local impact. Manufacturing jobs, environmental concerns, water use, labor practices, and infrastructure impacts are felt locally. But batteries themselves are global products serving global consumers. This mismatch between local costs and global benefits creates persistent tensions.

Fourth, technology concentrates advantage. Companies with better manufacturing expertise, supply chains, automation, and R&D capabilities maintain advantages even when operating outside their home countries. Building competitive capacity requires sustained investment and operational excellence, not just copying existing designs.

Fifth, geopolitics are becoming more important. Battery manufacturing is strategically important for energy security and EV transition. Countries increasingly view battery manufacturing as a matter of national interest, not just commercial enterprise. This shapes policy, investment, and international competition.

Sixth, both concerns and opportunities are real. Chinese factory expansion creates genuine opportunities for economic development, job creation, and industrial advancement. It also creates real concerns about environmental impact, labor practices, and community influence over decisions that affect their futures.

Looking forward, battery manufacturing will be a contested domain. Different stakeholders want different outcomes. Communities want jobs without environmental costs. Companies want profitability without constraints. Governments want energy security without excess subsidies. Workers want good jobs with fair treatment. These interests don't always align.

The challenge is navigating these tensions constructively. Communities can demand transparency and accountability. Companies can invest in genuine local partnerships and environmental stewardship. Governments can design policies that create broad benefits, not just manufacturing capacity. Workers can organize collectively to advocate for fair treatment.

None of this is inevitable. Outcomes depend on choices made by communities, companies, governments, and workers. The battery factories coming to towns worldwide aren't externally imposed. They're the result of decisions made by multiple actors. Understanding those decisions and their implications is the first step toward shaping outcomes in ways that serve broader interests.

FAQ

What exactly is a lithium-ion battery and why are they used in electric vehicles?

Lithium-ion batteries are rechargeable batteries that use lithium ions moving between a positive and negative electrode to generate electrical current. They're used in electric vehicles because they have high energy density (storing lots of energy in a compact space), can be recharged hundreds of times without significant degradation, and have proven reliable in automotive applications. They're also used in smartphones, laptops, and grid-scale energy storage systems.

Why is China so dominant in battery manufacturing globally?

China achieved dominance through decades of cumulative investment, government support, supply chain integration, manufacturing expertise, and labor availability. Chinese companies like CATL and BYD invested heavily in production capacity, R&D, and operational optimization when other countries were skeptical about EV adoption. That investment created advantages in cost, quality, and scale that persist today. Additionally, China controls significant portions of the supply chain for key battery materials and components, further reinforcing competitive advantages.

What are the main environmental concerns around battery factory operations?

The primary environmental concerns are water consumption (which can deplete local groundwater in arid regions), air and soil pollution from manufacturing chemicals, electricity consumption (which has environmental impacts depending on the energy source), and waste management from production processes. Additionally, mining for lithium, cobalt, and other raw materials that go into batteries creates environmental impacts. However, batteries themselves enable cleaner transportation by powering electric vehicles, so the environmental trade-off is complex.

How do tariffs and subsidies affect battery manufacturing location decisions?

Tariffs and subsidies dramatically shape where factories are built. High tariffs on imported batteries make local production more economically attractive. Subsidies for factory construction and tax credits for battery production directly reduce the cost of manufacturing investment. The U. S. Inflation Reduction Act, for example, provides substantial tax credits for batteries produced domestically with certain sourcing requirements. These policies can shift investments from one country to another almost immediately. However, when subsidies are reduced or eliminated, the economic fundamentals change and factories might become unviable.

What is the difference between EV batteries and energy storage batteries?

EV batteries are optimized for high power output, light weight, and performance while operating under variable demand from driving patterns. Energy storage batteries are optimized for long-duration storage, reliability, and durability while operating continuously and predictably. Energy storage batteries can be heavier and larger because they don't need to fit in a vehicle. They're used to store electricity from renewable sources and release it when needed. Growing renewable energy adoption is driving rapid growth in energy storage demand.

How do communities negotiate with battery manufacturers to ensure they benefit from factory investment?

Communities can negotiate agreements that include commitments to hire local workers, invest in training programs, meet environmental standards, and contribute to local infrastructure. Some communities have required minimum percentages of local hiring or local content sourcing. However, enforcement of these agreements requires ongoing monitoring and accountability mechanisms. Without enforcement, commitments are often unmet. Communities can also demand environmental impact assessments and regular monitoring to ensure companies meet their environmental commitments.

What happens to a battery factory when EV market demand is lower than expected?

When demand is lower than expected, battery factories operate below capacity, which reduces efficiency and increases per-unit production costs. If demand remains weak for an extended period, companies might reduce production, temporarily shut down the factory, or cancel planned expansions. In extreme cases, companies might abandon projects entirely, even after construction has begun. This leaves communities with unused infrastructure and unfulfilled economic promises. Some companies have pivoted to energy storage instead of EV batteries when energy storage demand outpaces EV demand.

Are Chinese battery factories cleaner or dirtier than competitors when located in developed countries?

Chinese battery factories operating in developed countries generally must meet the same environmental standards as competitors. In Europe, for example, Chinese manufacturers must comply with EU environmental regulations. This means their environmental performance is comparable to other manufacturers operating under the same regulations. However, Chinese factories built in countries with less stringent environmental standards might have worse environmental performance. The quality of environmental practice depends more on the regulatory environment than on the company's nationality.

Could battery manufacturing ever shift significantly away from China in the future?

Possibly, but slowly. Building significant battery manufacturing capacity outside China requires sustained investment, technological development, and policy support. Some capacity will shift to other regions, particularly for supplying local markets. However, China's cumulative advantages in supply chains, expertise, and scale mean it will likely remain the dominant battery manufacturer for the foreseeable future. The more likely scenario is geographic diversification rather than China's dominance being completely displaced.

How does battery manufacturing fit into the broader clean energy transition?

Batteries are critical infrastructure for the clean energy transition. They enable electric vehicles to replace fossil fuel-powered cars, reducing transportation emissions. They enable renewable energy sources like solar and wind to reliably power grids by storing energy when renewable sources aren't generating and releasing it when needed. Without batteries, a renewable-powered grid and an electrified transportation system aren't feasible. This makes battery manufacturing strategically important for climate goals and energy security.

Key Takeaways

- Chinese battery manufacturers operate 68 major facilities outside China, fundamentally reshaping global manufacturing and energy supply chains

- Policy support through subsidies and tariffs is critical to factory investment decisions, creating vulnerability to policy changes

- Communities experience local costs (environmental impact, labor tensions) while consumers elsewhere enjoy global benefits of batteries

- Chinese manufacturers maintain cost and technology advantages even when operating outside China due to supply chain integration and manufacturing expertise

- Energy storage is growing faster than EV batteries, likely reshaping which regions attract manufacturing investment in coming years