![Employee Fraud in Retail: How Insiders Exploit Discount Systems [2025]](https://tryrunable.com/blog/employee-fraud-in-retail-how-insiders-exploit-discount-syste/image-1-1771274247468.jpg)

Employee Fraud in Retail: How Insiders Exploit Discount Systems

You'd think catching someone stealing hundreds of thousands of dollars would be easy. They leave a paper trail. They sell stolen goods. Someone talks. But here's what really happens: it takes months for the numbers to look weird enough that anyone notices.

In early 2024, a Best Buy manager in Florida started noticing something off. The sales numbers didn't add up. Certain items were moving through discounts at rates that made no sense. It seemed like a glitch in the system at first, but private investigators traced it back to a single employee. That employee, a 36-year-old experience manager named Matthew Lettera, had orchestrated one of the more brazen internal theft schemes in recent retail history.

He used a simple method: his manager's discount code. Over the course of several months, Lettera and his accomplices purchased nearly 150 items at discounts sometimes reaching 99 percent off. MacBooks that should have cost

Let's be clear about what this case really represents. It's not just one employee getting greedy. It's a window into a much larger problem that's costing American retailers somewhere between

This article breaks down how these schemes actually work, why retailers keep getting caught off guard, what's being done about it, and what this means for you as a consumer. Because when retailers lose this much money to fraud, prices go up. Everywhere.

TL; DR

- A Best Buy employee stole $118,000 using his manager's discount code to purchase nearly 150 items at up to 99% off

- Employee theft costs U.S. retailers $60-120 billion annually, making it a bigger loss category than external shoplifting

- Discount code exploitation is one of the easiest internal fraud vectors, requiring minimal technical knowledge and often going undetected for months

- Retail turnover and workplace stress directly correlate with fraud, with stressed employees more likely to participate in schemes

- Detection systems are catching up, but most retailers still rely on manual audits that happen weeks or months after the crime

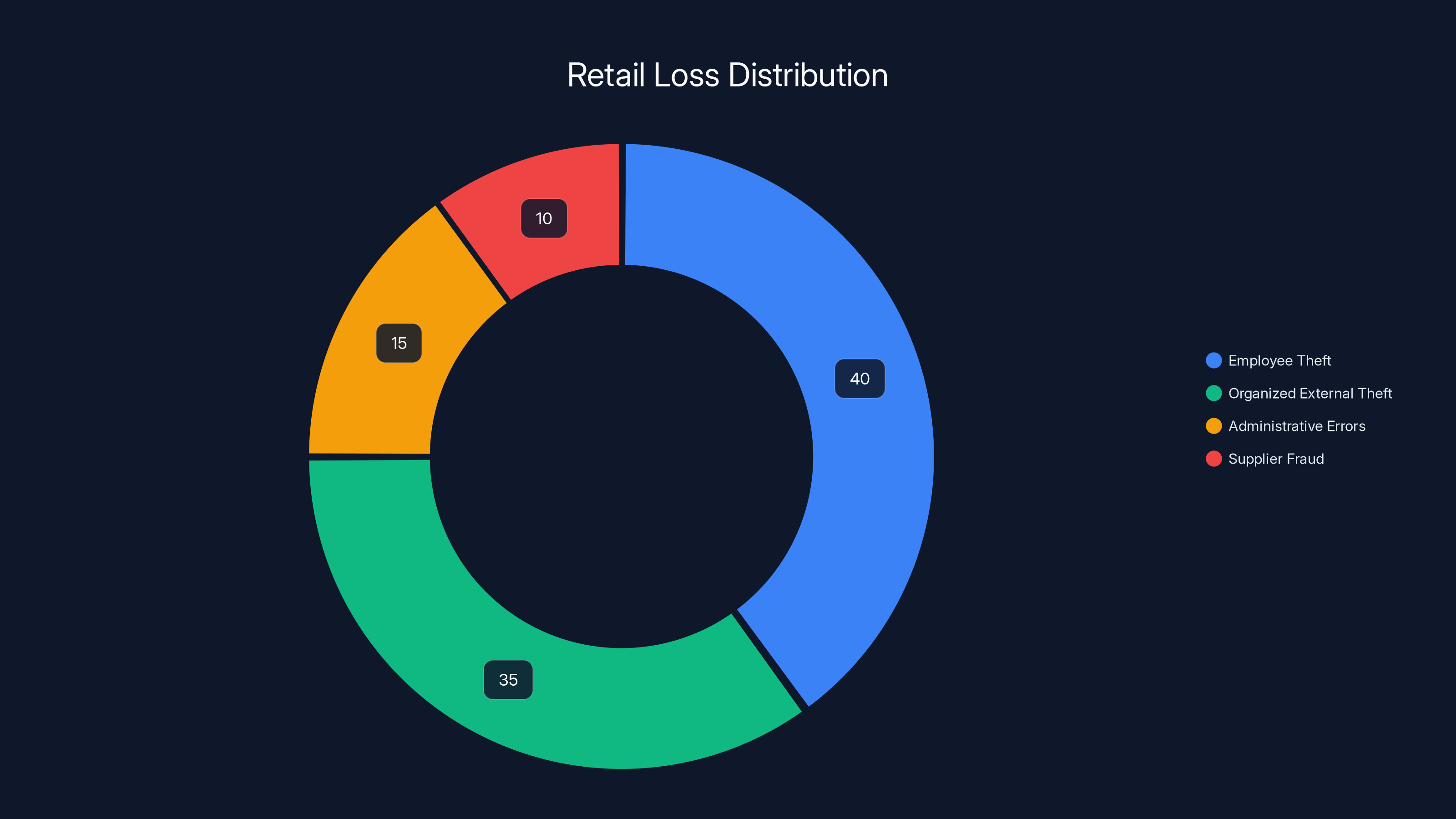

Employee theft accounts for a significant portion of retail losses, often surpassing organized external theft. Estimated data.

The Matthew Lettera Case: How One Employee Cost Best Buy $118K

Matthew Lettera seemed like an unremarkable employee. He'd been working at Best Buy's West Palm Beach location since January 2020. According to his LinkedIn profile, he'd transitioned from a career in culinary training to retail management. Nothing screamed "future fraud architect."

But in March 2024, something changed.

Lettera accessed his manager's discount code. That's the kind of credential that legitimate managers use dozens of times per day to help customers with legitimate discounts on bulk purchases or employee benefits. But Lettera wasn't helping customers. He was using it to buy products for himself and his accomplices at fractional prices.

The pattern went like this: Lettera would ring up a MacBook Pro. Normal price: around

He didn't even try to hide it well. According to the arrest affidavit from the Palm Beach Police Department, Lettera conducted at least 97 discounted purchases for himself. But he got bolder. He started recruiting coworkers. The affidavit shows 52 additional transactions where Lettera sold discount codes or completed purchases for other people. Once someone else is involved, the scheme gets exponentially riskier. More witnesses. More people who know what's happening. More chances for someone to have a crisis of conscience or get caught.

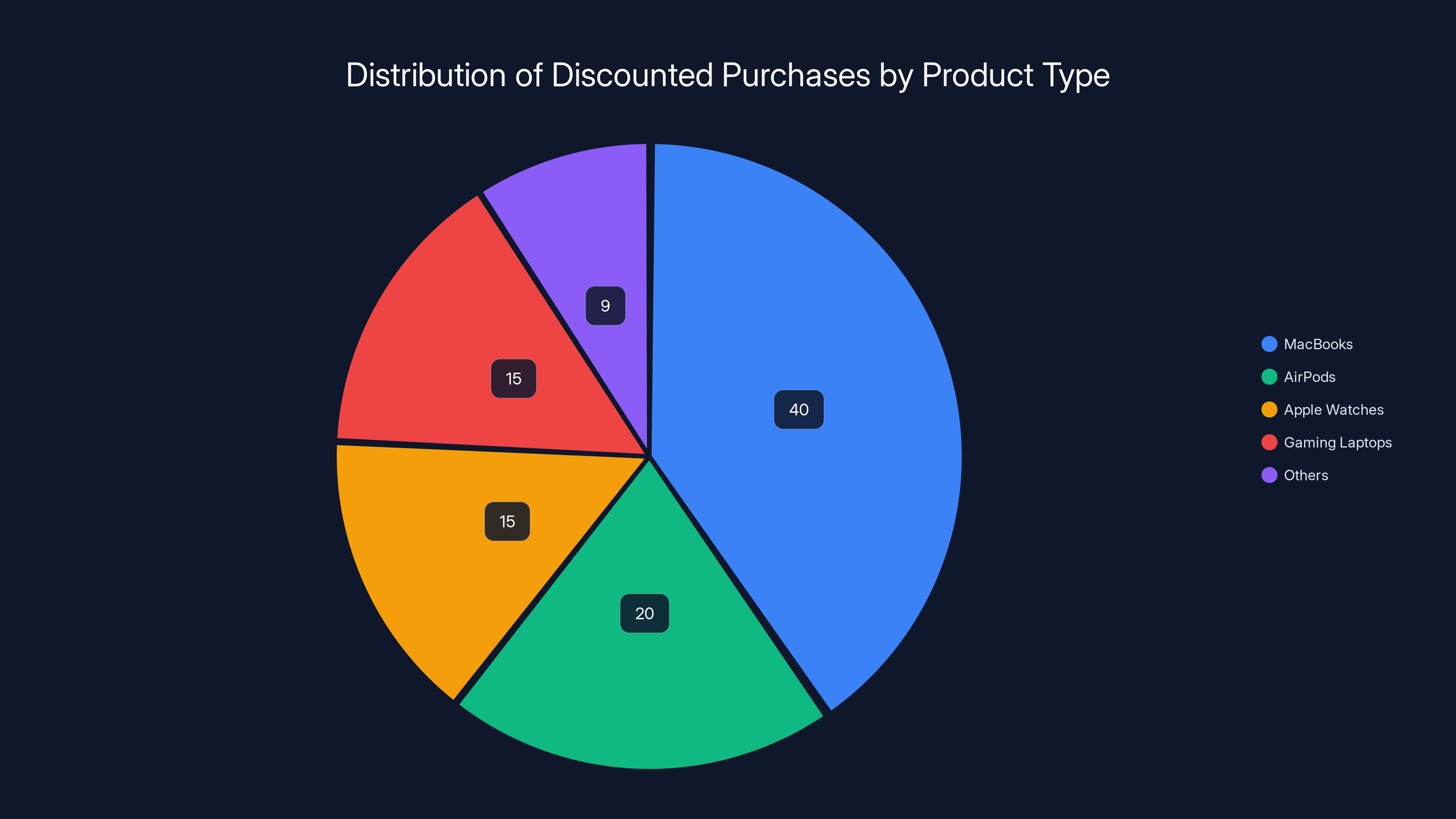

The items Lettera was pulling: MacBooks, obviously. Those are high-value, easily fenced. But also AirPods, Apple Watches, gaming laptops. Anything that could be sold at a pawn shop for close to retail value. And that's exactly where the trail led.

When Best Buy's managers finally got suspicious in December 2024, they didn't immediately catch Lettera. They called in private investigators. Those investigators did what detective work always requires: they pieced together records. Sales data. Transaction logs. They looked for the anomalies. They found them.

Then they went to the pawn shops. Pawn shops keep meticulous records. They have to. It's the law. So investigators showed up with descriptions of the products and dates. The pawn shops provided their own records. There was the MacBook. There was the gaming laptop. All sold by someone matching Lettera's description.

Lettera was arrested. He faced fraud charges. The case became yet another data point in a much larger trend that retail executives have been losing sleep over.

Why Employee Theft Is Actually Bigger Than Shoplifting

Here's something most people don't realize: employee theft costs retailers more money than customer shoplifting does. This seems counterintuitive. You hear about organized retail crime. Smash-and-grab thieves. Groups of people stealing $40,000 in merchandise in a single night. That gets media attention. That seems like the crisis.

But the numbers tell a different story. According to the National Retail Federation's most recent surveys, organized external theft accounts for maybe 35% to 40% of total retail losses. Employee theft makes up a similar or sometimes larger percentage. The rest comes from administrative errors, supplier fraud, and other internal issues.

Why is employee theft so effective? Because employees already have the access. They know the systems. They understand the security measures because they bypass them every single day. An employee doesn't need to plan an elaborate heist. They just need to clock in, do their job, and exploit one small vulnerability.

The National Retail Federation started tracking this more carefully after 2023. That year, they surveyed hundreds of retailers about their biggest losses. Inflation was creating stress in the economy. Wages weren't keeping up. Retail jobs were already notorious for low pay and high turnover. The NRF's report warned that this combination was creating a perfect environment for internal fraud.

When employees are stressed, when they feel underpaid, when they're constantly dealing with understaffing and having to pick up extra shifts, some of them start thinking differently about the rules. Not all of them. Most retail workers are honest. But the percentage who aren't increases dramatically under financial pressure.

Then there's the turnover problem. Retail has one of the highest turnover rates of any industry. Some studies show 60% to 75% annual turnover depending on the region and company. When someone knows they're going to be fired in three months anyway, or when they know nobody cares enough to actually check the details, the friction for committing fraud drops to almost zero.

Lettera had been at Best Buy for four years when he started his scheme. He wasn't desperate or newly hired. He was established. He had a manager's credentials. He understood the system well enough to know that discount transactions might not get audited immediately. He knew the pawn shop ecosystem. The whole operation suggests a level of planning and understanding that only comes from someone who's been inside the system for a while.

Weak oversight is the most significant factor contributing to employee theft in retail, with an impact score of 9. Estimated data based on industry insights.

The Mechanics: How Discount Code Fraud Actually Works

Discount code fraud is deceptively simple. You need three things: access to a legitimate discount code, a transaction system that doesn't flag unusual patterns, and a way to move the stolen goods quickly.

Lettera had all three.

First, the access. Discount codes come in different types. Some are for specific promotions. Buy two, get one free. 20% off all electronics this weekend. Those are hard to abuse because they're tied to specific products or timeframes. But manager discretionary codes? Those are broader. They're designed so that a manager can help a customer with a pricing issue. Maybe the customer bought something yesterday at regular price and it went on sale today. The manager can adjust the price. Or maybe a customer is buying a bulk order for a business and qualifies for a discount that the regular customer doesn't.

The system trusts the manager to use good judgment. But the system doesn't actively prevent a manager from using that code every single time they scan a product. Technically, there's nothing stopping a manager from putting a 50% discount on every item they touch. The system only catches you if someone notices. And noticing requires actively auditing transactions.

Most retail audit systems are reactive, not proactive. They flag transactions that exceed certain thresholds. Maybe if someone discounts more than

Second, the sale itself. Lettera just bought the products. He walked into Best Buy, put the item on the counter, applied the discount, paid cash or used a card, and left. Some retailers have procedures where you have to get supervisor approval for large discounts. Best Buy apparently doesn't have that, or he found a way around it. The transaction completes. The inventory system shows a sale. From the system's perspective, this is a legitimate transaction.

Third, the fence. Pawn shops don't ask a lot of questions when someone brings in a MacBook. They'll do a quick check to make sure it's real. They'll offer cash on the spot. The person walks out with money. The pawn shop sells it at a markup, usually 30% to 50% above what they paid. By the time Best Buy realizes they were defrauded, the product has already moved twice.

What's fascinating about Lettera's approach is that he didn't need to be sophisticated. He didn't need to manipulate code. He didn't need to do anything technical. He just needed access and patience.

The Broader Pattern: Best Buy Isn't Unique

One month before the Lettera case became public, a different Best Buy in Georgia experienced a related but distinct fraud. A 20-year-old employee named Dorian Allen allegedly allowed a shoplifting ring to steal more than $40,000 in merchandise over a period of weeks.

Surveillance footage showed shoplifters coming into the store, loading items into carts, and walking straight out without paying. Allen was stationed at the exits. He just let them go. Over 140 transactions. PlayStations. Xbox Series S consoles. VR headsets. High-end headphones. A Segway, for crying out loud. All walking out the door while an employee watched.

Allen's defense was unusual: he claimed he was being blackmailed by a hacker group. They had nude photos he'd shared on Instagram. They threatened to release them unless he cooperated with the theft ring. Under that duress, he helped coordinate which items the shoplifters should target. He memorized descriptions so he'd know when to let them pass.

Whether the blackmail story is true or a convenient excuse, the outcome is the same. Best Buy lost $40,000. The security systems that were supposed to prevent this kind of loss failed. An employee with legitimate access was the vulnerability.

These aren't isolated incidents. A quick search of retail fraud cases shows similar patterns everywhere. Target. Walmart. GameStop. Home Depot. It doesn't matter how big the retailer is or how sophisticated their systems are. If you have an employee willing to commit fraud and even a moderately designed opportunity to do so, the fraud happens.

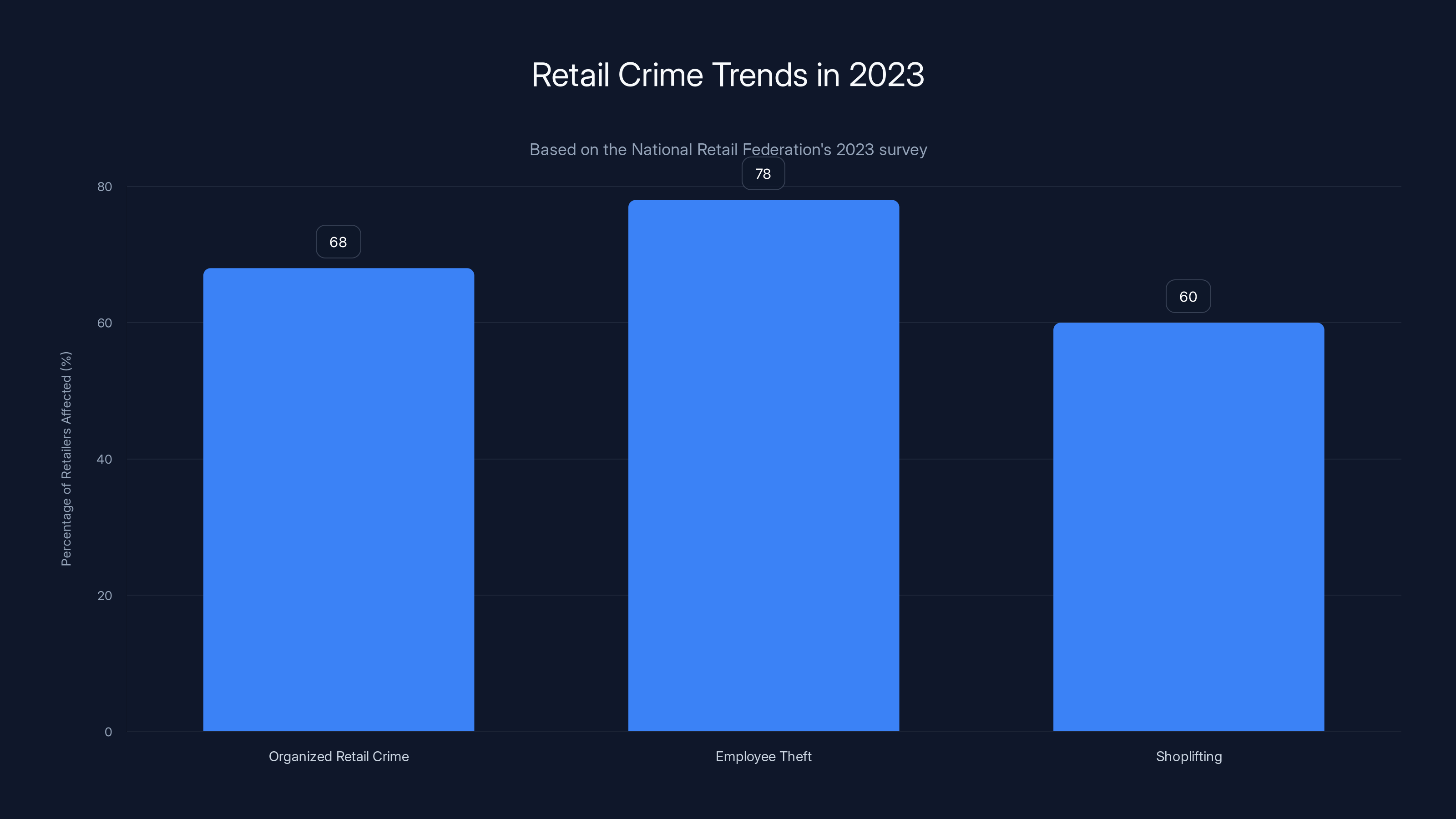

The retail industry has known this for years. The National Retail Federation publishes annual "Organized Retail Crime" surveys. In the 2023 survey, they found that 68% of retailers experienced organized retail crime that year. But they also found something else: 78% reported increases in employee theft. That number is actually rising faster than shoplifting rates.

Why Detection Systems Are Failing

Here's what should have caught Lettera: the system should have noticed that a single employee was applying manager discounts at a statistically impossible rate. If the average manager discount is used twice per week per manager, and there are 10 managers in a store, that's maybe 20 legitimate discount transactions per week. Lettera was doing several per day.

Any competent audit system should flag that. But either Best Buy didn't have that system, or it wasn't monitoring the right metrics, or the alerts went to someone who didn't care or didn't understand what they were seeing.

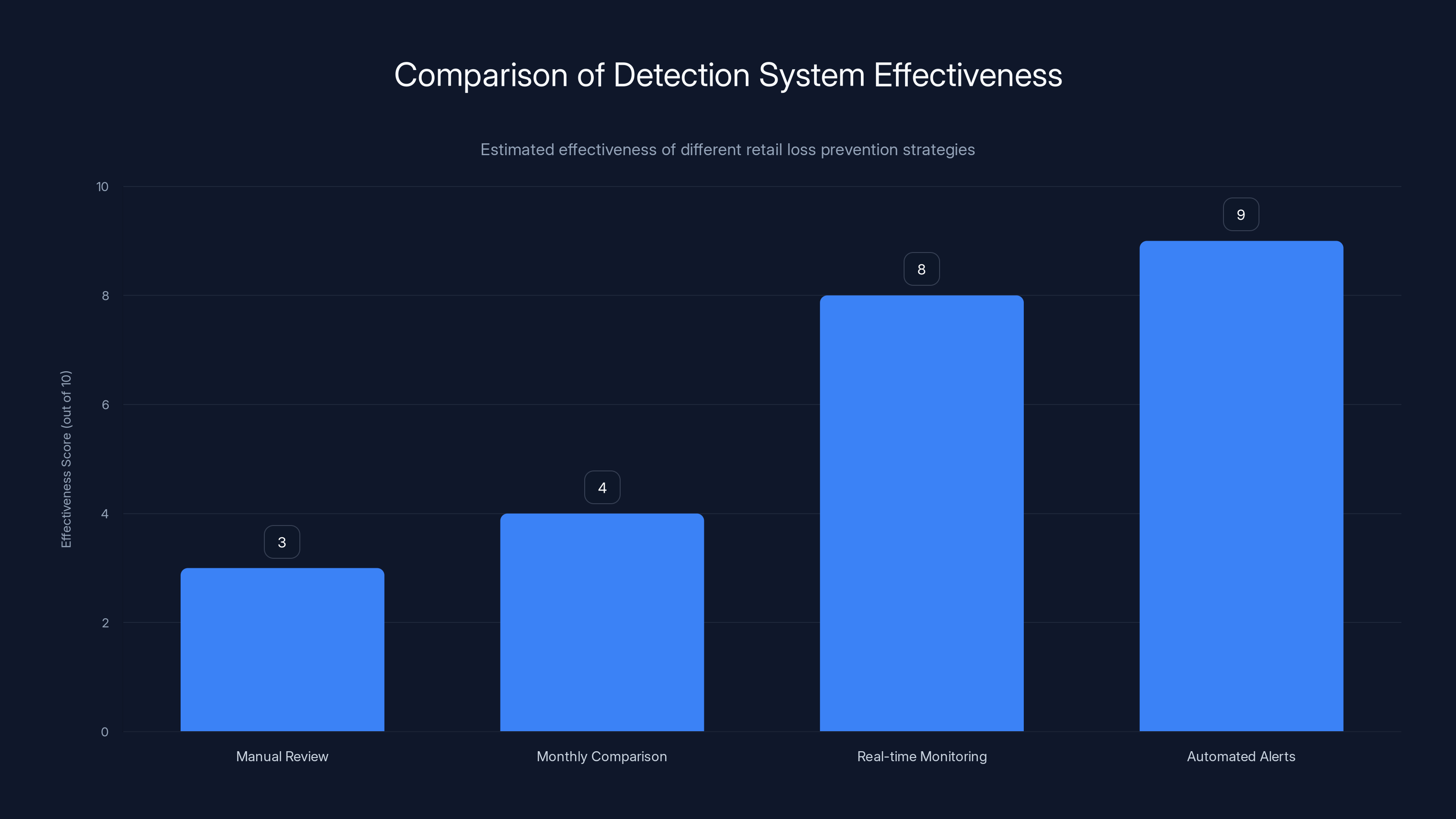

Most retail loss prevention systems are still built on manual reviews. An analyst looks at reports. They compare this month to last month. They look for big anomalies. But that's backward-looking. By the time you're comparing this month to last month, the fraud has already happened. You're detecting it weeks or months late.

Some retailers have moved to real-time monitoring. Transaction happens. Algorithm analyzes it within seconds. If it matches a fraud pattern, an alert goes out to a human or to an automated system that can take action. But that requires investment. It requires that someone decided loss prevention was important enough to budget for it.

Retailers have been consolidating for decades. Stores are cutting staff. Training is minimal. Loss prevention departments have been squeezed. So you get situations where a single analyst is responsible for monitoring fraud across 50 stores. They're not going to catch everything.

There's also a culture problem. Loss prevention is expensive. It's a cost center. It doesn't make money. So when budgets get tight, it gets cut first. But then you get situations like Lettera's where a single employee steals $118,000 before anyone notices.

Allen's case is different. That's not a system failure. That's a culture failure. Allowing shoplifters to just walk out requires either active assistance or aggressive passivity. For weeks. That means managers saw it and didn't stop it, or employees saw it and nobody reported it. Somewhere in that store, the sense of security or accountability broke down.

In 2023, 78% of retailers reported increases in employee theft, surpassing organized retail crime and shoplifting rates. Estimated data based on trends.

The Economics of Retail Fraud: Who Actually Pays

When Best Buy loses $118,000 to fraud, they don't just absorb it. They factor it into their margins. Retailers typically build in what's called "shrink" into their pricing. Shrink is the difference between the inventory that should exist and the inventory that actually exists. It comes from theft, from errors, from fraud. Industry estimates put average retail shrink at 1% to 3% of sales.

That might not sound like much. But 1% of the

But every dollar of shrink eventually comes out of your pocket. It comes out when prices are set higher than they'd otherwise need to be. It comes out when fewer employees are hired because the productivity metrics don't support it. It comes out when a retailer's profit margins shrink, which makes it harder for them to invest in better systems or pay employees better.

It's a weird economic chain. Lettera's theft didn't just cost Best Buy $118,000. It likely cost Best Buy customers money too, spread across millions of transactions in the form of slightly higher prices.

For the pawn shop that bought the stolen goods, it was a profit play. They bought MacBooks for

For Lettera, the math is even simpler. He walked away with cash. The scheme ran from March to December 2024, so roughly nine months. If the total theft was

Until he got caught.

Why Employees Commit Fraud: The Psychology

There's a framework in fraud psychology called the "Fraud Triangle." It states that fraud generally requires three components: pressure, opportunity, and rationalization.

Pressure is the financial need or want. Maybe Lettera was in debt. Maybe he wanted something he couldn't afford on his salary. Maybe he was bored and wanted to prove he could pull something off. The arrest affidavit doesn't specify.

Opportunity is what we've already discussed: access to the manager code, a system that doesn't actively prevent it, and a fence for the goods.

Rationalization is how people convince themselves that what they're doing is okay. "Best Buy is a huge company, they can afford it." "The company doesn't pay me enough, this is just getting what I deserve." "Everybody does this." (They don't, but it helps to believe it.) "I'm just helping my friends out." The specific rationalization matters less than the fact that every fraudster develops one.

What's interesting about Allen's case is that his claimed rationalization was different. He said he was coerced. Maybe that's true. The psychology of someone who's being actively threatened is different from someone who's motivated by greed. But the outcome is the same.

Retailers have been thinking about this more in recent years because the National Retail Federation's research showed a direct correlation between employee stress and fraud rates. When employees are overworked, underpaid, and feel unappreciated, fraud goes up. When there's good management, reasonable hours, and a sense of being part of a team, fraud goes down.

That doesn't excuse fraud. But it explains it. And it suggests that part of the solution isn't just better systems, it's better working conditions.

Red Flags: What Actually Indicates Fraud

If Best Buy had been watching for these specific patterns, they might have caught Lettera earlier.

Unusual Discount Rates: A manager who consistently applies discounts at unusual rates. If the store average for manager discounts is 15%, and one manager is doing 50% or more regularly, that's suspicious.

High Transaction Velocity: Legitimate manager discretionary codes might be used 2-3 times per shift. If someone's using them 5-10 times per shift, especially on high-value items, that's a pattern.

Cash Purchases: Legitimate customers usually put big purchases on cards. If a manager is consistently ringing up large purchases that are paid in cash, especially with big discounts, that's notable.

No Customer Present: In-store surveillance could show a transaction occurring with no actual customer. Or with a customer who doesn't seem to match the items being purchased.

Inventory Mismatches: If the inventory system shows the item was sold, but nobody ever delivered it to a customer, that's a disconnect.

Pawn Shop Patterns: If items from a specific store start appearing in local pawn shops at higher rates than normal, that's a data point.

Coworker Complaints: Sometimes other employees know. They see something odd happening. They might complain to management or HR. Those complaints should be logged and taken seriously.

The problem is that most retailers aren't actively monitoring for these red flags. They're relying on year-end audits or monthly reviews of loss data. By then, if the fraud is well-distributed, it's hard to spot.

Estimated data shows that external shoplifting and employee theft are the largest contributors to retail shrink, impacting pricing and employment decisions.

What's Changing in Loss Prevention Technology

The retail industry has been waking up to this problem, and some retailers are investing in better systems.

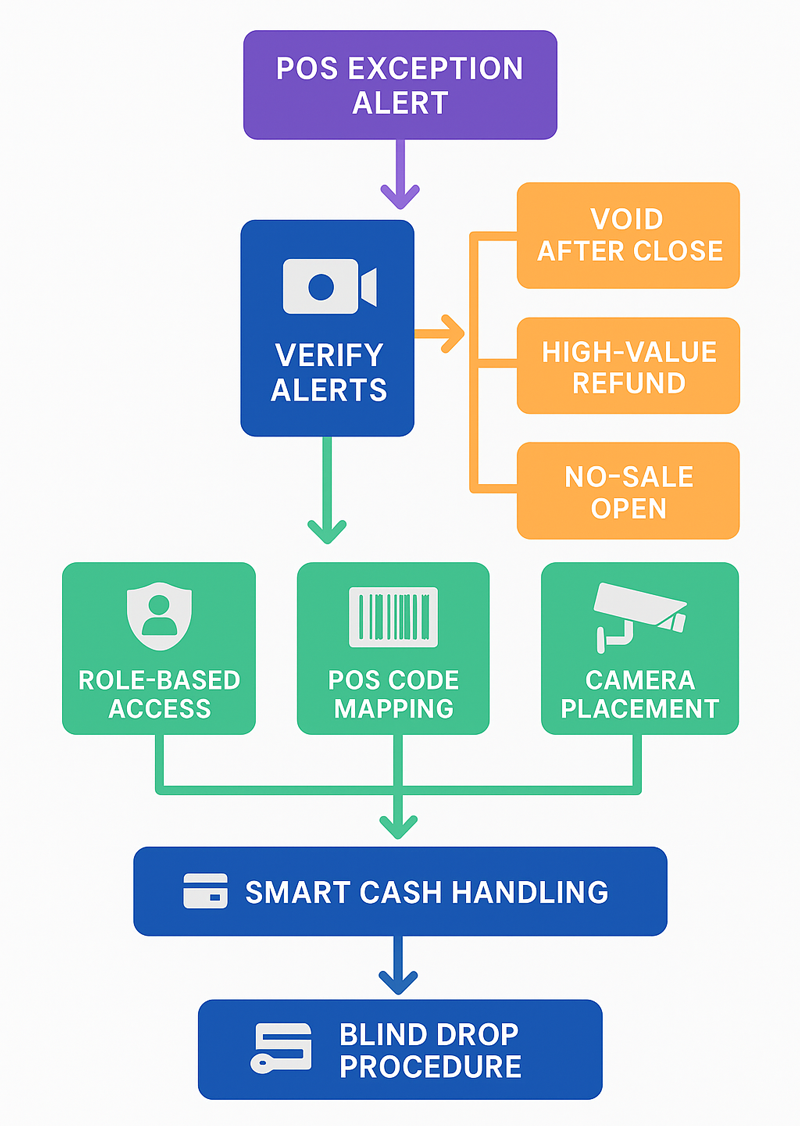

Real-Time Transaction Monitoring: Platforms that analyze every transaction as it happens, looking for patterns that match known fraud schemes. These can flag an unusual discount in seconds rather than months.

Employee Behavior Analytics: Using AI to identify unusual patterns in how employees interact with the system. If someone typically scans 200 items per day but suddenly scans 500, that's an anomaly worth investigating.

Integrated Inventory Systems: When the point-of-sale system is directly integrated with inventory management, discrepancies show up faster. If a MacBook is rung up as sold but never leaves the store, that's an immediate alert.

Video Analytics: Computer vision can watch surveillance footage and flag unusual patterns. An employee accessing the manager code station at unusual times, for instance, or letting someone leave without scanning their items.

Geofencing: Tracking that stolen items appear in unusual locations. If a MacBook is sold at one store and then appears at a pawn shop five miles away the same day, that's a pattern.

But here's the catch: these systems are expensive. They require technical expertise to set up and maintain. They require training for the staff who'll respond to alerts. A lot of retailers, particularly smaller chains or independent stores, simply don't have the budget.

The Coworker Factor: How Schemes Recruit

Lettera didn't just steal for himself. The police affidavit notes that he also processed transactions for other employees and acquaintances. That's how a small fraud scheme becomes a big one. Once you've recruited one person, you can recruit another. Once two people know about it, you can tell a third.

This is actually where schemes often collapse. More people means more risk. It takes only one person with a crisis of conscience, or one person who gets caught and decides to talk in exchange for a lighter sentence, to bring the whole thing down.

In Allen's case, he didn't recruit anyone. But the shoplifting ring recruited him. That's a different dynamic. A ring of professional shoplifters came into the store, identified Allen as a potential weak point, and applied pressure. That's sophisticated. That's organized retail crime, which is a different threat category than a single employee acting alone.

Management failure shows up at every level when you look at these cases. If the store manager isn't building a team that feels ownership and accountability, fraud is easier. If loss prevention isn't doing regular audits, fraud goes undetected longer. If HR isn't following up on complaints or concerns from other employees, the company misses warning signs.

Best Buy's Response and Industry Implications

Best Buy didn't immediately comment on lessons learned from either case, but the company's general loss prevention approach has been evolving. Like many major retailers, they've increased investments in surveillance, analytics, and training.

But here's the reality: no system is perfect. As long as there are human beings involved, there will be fraud. The goal isn't zero fraud, which is impossible. The goal is to make it risky enough, costly enough, and likely-to-be-caught enough that most people don't try it.

Lettera apparently miscalculated that last part. He thought he could pull this off for longer, or that the pawn shop records wouldn't matter, or that investigators wouldn't care about $118,000 in stolen goods. He was wrong. But the fact that he tried at all, and that it took months to catch him, shows that Best Buy's existing systems had gaps.

For the industry, the implication is clear: invest in loss prevention or pay for it in different ways. Some retailers are moving toward more automated checkout, which reduces the number of human transactions that could be manipulated. Some are increasing surveillance. Some are testing geofencing technology to track high-value items. Some are just paying people better and building a culture where employees feel invested in the company's success.

MacBooks were the most frequently discounted items in the scheme, accounting for an estimated 40% of the fraudulent purchases. Estimated data based on narrative.

The Role of Workplace Culture

One detail from the Lettera case is striking: it took four years for him to start the fraud. He was employed in January 2020 and didn't start until March 2024. What changed? We don't know. But it's a reminder that fraud often isn't a hiring problem. It's a management problem.

Somewhere along the way, Lettera decided that the risk was worth it. Maybe his manager changed. Maybe the store culture shifted. Maybe he developed a financial emergency. Maybe he just got bored and decided to test the system.

Retailers that take seriously the connection between employee satisfaction and loss prevention have figured something out: people who feel valued, who have reasonable hours, who are paid decently, and who have growth opportunities commit less fraud. Not zero fraud. But less.

Target, for instance, has been explicitly trying to build better workplace culture in their stores. Better pay, clearer scheduling, and less aggressive pressure on metrics. It's not purely altruistic; it's because they've done the math and realized that a 10% reduction in theft through better culture and lower turnover more than pays for slightly higher wages.

Of course, there's a limit. You can't raise wages to the point where the company isn't profitable. But there's a sweet spot where better working conditions reduce fraud and turnover enough to offset the costs.

What Customers Should Know

These fraud cases don't directly harm individual customers in the moment. Your MacBook still costs the same whether it's purchased at a discount or full price. But the indirect effects are real.

When retailers lose $118,000 to internal fraud, they factor that into their margin expectations. They adjust their prices upward slightly across the board. They reduce the budget for customer service. They make the store less pleasant to work in by cutting staff. All of these effects ripple through the customer experience.

Also, fraud affects the brand. Best Buy's reputation wasn't destroyed by these cases, but they're negative press. Customers hear that employees are ripping the company off and wonder about security, returns fraud, and other integrity issues.

Finally, customers should be aware of pawn shop dynamics. If you're buying high-end electronics at a pawn shop, there's always a small risk that the item is stolen. Pawn shops are supposed to check ID and keep records, which can help identify stolen goods. But if something seems priced way too low, it might be stolen merchandise that the original owner will trace and recover.

Systemic Issues in Retail Loss Prevention

The Lettera and Allen cases expose some fundamental weaknesses in how retail loss prevention is structured.

First, Loss Prevention Is Understaffed: Most retailers have one or two loss prevention personnel per district covering dozens of stores. That's an impossible workload for catching active fraud.

Second, Audits Are Delayed: Monthly or quarterly audits mean fraud can run for months before detection. By then, the merchandise is gone and the money is spent.

Third, Systems Aren't Integrated: Point-of-sale, inventory, surveillance, and employee access control are often separate systems. A sophisticated fraud that spans multiple systems can hide because no one tool sees the full picture.

Fourth, Training Is Minimal: Most retail employees receive almost no training on loss prevention. They don't know what to watch for or how to report concerns.

Fifth, Management Accountability Is Unclear: When a manager's credentials are used to commit fraud, is that manager responsible? Are they fired? Or is it considered a system security issue? Unclear accountability enables more fraud.

Real-time monitoring and automated alerts are significantly more effective in preventing fraud compared to manual reviews and monthly comparisons. Estimated data.

The Future of Retail Loss Prevention

Large retailers are moving toward more sophisticated approaches. Machine learning models that learn what normal looks like and flag anomalies. Integration between systems so that a single unified platform sees all activity. Automated response systems that can take action without waiting for human decision-making.

Some are experimenting with blockchain-based transaction logging, which creates an immutable record that's harder to manipulate. Others are using advanced biometrics tied to employee access, so that when the manager code is used, the system knows exactly which manager, at which terminal, at what time.

But there's a privacy tradeoff. The more surveillance and control a retailer implements, the more oppressive it can feel for legitimate employees. Some employees will leave if they feel they're being treated like criminals. So there's a balance.

The most effective approach seems to be combining good technology with good management. Use systems to catch what you can automatically, but invest equally in culture and training so that employees feel motivated to maintain integrity.

International Perspectives on Employee Fraud

Retail fraud isn't just an American problem. In the UK, the British Retail Consortium reports similar issues. In Australia, the National Retailers Association tracks internal fraud as a major loss category. In Japan, even with different cultural norms around loyalty, employee theft is tracked and addressed.

The common thread is that wherever there's opportunity and pressure, some people will commit fraud. The percentages might vary by culture. The methods might be different. But the basic dynamics are universal.

Interestingly, some European retailers have been ahead of the curve on loss prevention technology. IKEA, for instance, which has stores worldwide, uses sophisticated integrated systems that track movement of high-value items in real time. But IKEA also pays above-average retail wages and invests heavily in employee culture.

Legal Consequences and Prosecution

Matthew Lettera faced fraud charges. The prosecution would have used the evidence from the police investigation: transaction records, pawn shop documentation, surveillance footage if available, and testimony from Best Buy personnel. If convicted, he'd face federal charges given the dollar amount involved, which could mean significant prison time and restitution.

The interesting question is restitution. Best Buy wants its $118,000 back. But Lettera might not have that much to pay. He'd have spent a lot of it. He might have no assets. So even if he's convicted and sentenced to pay restitution, Best Buy might never see most of the money.

Allen faced different charges given that his case involved external shoplifting, though his role was crucial to enabling it. His case would focus on aiding and abetting, plus whatever crimes he was coerced or bullied into participating in.

The prosecution of these cases serves as a deterrent. If everyone knows that employee fraud gets investigated, prosecuted, and results in jail time, that changes the calculation for would-be fraudsters. But the deterrent only works if prosecution actually happens and is visible.

Why This Keeps Happening

Retail fraud is so persistent because the basic equation doesn't change. As long as retail stores exist, they'll have employees with access, systems with vulnerabilities, and fences willing to buy stolen goods. As long as wages feel inadequate, some employees will be tempted. As long as audit systems lag behind transactions, opportunities exist.

The Lettera case is notable not because it's unique, but because it's typical. It's a regular employee with regular access exploiting a regular vulnerability. The fact that it took nine months to catch might actually be faster than average.

What might actually change things is if the calculus shifted. If detection became faster, prosecution became more certain, penalties became steeper, but simultaneously working conditions and compensation improved, the incentive structure would shift. Some fraud would still happen, but less of it.

But that requires coordinated action across many retailers, which is difficult to organize. Each retailer is trying to optimize for their own profitability, not the industry as a whole.

The Ripple Effects on Trust

When employees commit fraud and it becomes public, it affects the trust that customers place in the retailer. Not dramatically, not enough to destroy the company. But it accumulates. Best Buy's brand is still strong, but this incident adds to a pattern of negative stories. Over time, a brand that's associated with loss and inefficiency loses its premium positioning.

For investors, these cases matter more. A company that can't control internal fraud is a company with poor management and inadequate systems. That affects stock price and borrowing costs. It affects ability to hire talent because good people want to work for well-run companies.

For employees at Best Buy stores nationwide, these cases might create a chilling effect. If you're thinking about bending the rules, seeing coworkers get arrested makes you think twice. If you're an honest employee, it might make you feel more alienated if you work hard while others cut corners.

Practical Safeguards for Retailers

If you run a retail operation or manage one, here are practical steps to reduce fraud risk:

Automate What You Can: Use software to flag unusual transactions in real time, not months later.

Rotate Access: Don't let the same person have the same elevated access for years. Rotate manager codes and credentials frequently.

Audit Randomly: Don't let audits be predictable. Random audits catch more.

Train Employees: Let people know that fraud is monitored, prosecuted, and costly.

Pay Competitively: If your wages are so far below market that employees feel desperate, you're asking for fraud.

Build Culture: Make people feel like they're part of a team with shared goals.

Trust but Verify: Good relationships with managers don't mean you don't audit them.

Track Inventory Physically: Do regular physical counts, not just system counts.

Monitor Exits: High-value items should have security tags and monitoring.

Work with Pawn Shops: Build relationships where pawn shops call you if your products show up.

FAQ

What exactly did Matthew Lettera do to commit fraud?

Lettera accessed his manager's discount code and used it to purchase nearly 150 items at heavily discounted prices, sometimes at 99% off. He and his accomplices then sold these products, primarily to local pawn shops, for cash. The scheme ran from March to December 2024 and resulted in losses exceeding $118,000 for Best Buy before he was caught.

How did Best Buy finally discover the fraud?

Best Buy managers noticed unusual sales patterns and declining inventory numbers in December 2024. They hired private investigators who traced the transactions to Matthew Lettera. The investigators then contacted local pawn shops and recovered sales records showing that the discounted products had been sold to those shops, providing concrete evidence of the theft.

Why is employee theft becoming more common in retail?

The National Retail Federation identified several contributing factors: high employee turnover rates (60-75% annually), financial stress among workers due to inflation, understaffing that creates stress, and inadequate investment in loss prevention systems. When employees feel underpaid and overworked, and when they perceive weak oversight, some become more willing to commit fraud.

What red flags should retailers watch for to catch fraud earlier?

Retailers should monitor unusual discount rates (managers applying discounts at much higher percentages than normal), high transaction velocity (same manager using discount codes repeatedly throughout a shift), cash payments on large purchases, discrepancies between sales records and inventory, employee transactions with no visible customer, and higher-than-normal appearance of store products at local pawn shops.

How much does retail fraud actually cost the industry annually?

Employee theft alone costs American retailers between

What technological solutions are retailers implementing to prevent fraud?

Advanced loss prevention systems now include real-time transaction monitoring with AI analysis, employee behavior analytics that flag unusual patterns, integrated inventory systems that catch discrepancies immediately, video analytics that can identify unusual behavior in surveillance footage, and geofencing technology that tracks high-value items. However, these systems require significant investment that not all retailers can afford.

Can employees charged with retail fraud actually serve jail time?

Yes. Employee fraud charges can result in federal prosecution depending on the amount stolen. Sentences can include significant prison time plus restitution orders to repay the stolen amount. However, collecting restitution is often difficult if the employee lacks assets or has already spent the money.

How does workplace culture affect fraud rates in retail?

Research shows a direct correlation between employee satisfaction and fraud rates. Retailers that invest in better working conditions, competitive pay, reasonable scheduling, and employee development see measurably lower fraud rates. Conversely, stores with high stress, low pay, and poor management experience higher fraud. This suggests that addressing the underlying conditions that create pressure to commit fraud is as important as implementing surveillance systems.

Why do pawn shops play a role in retail fraud?

Pawn shops are a primary fence for stolen retail goods because they operate on a cash basis with relatively simple verification procedures. An employee can quickly convert stolen merchandise to cash at a pawn shop, and the pawn shop can resell the goods at a markup. Pawn shops are required to keep records, which helps law enforcement trace stolen merchandise, but they're still attractive to fraudsters because the transaction is quick and anonymous.

What should a customer do if they suspect an employee is committing fraud at a retail store?

Report observations to store management or the retailer's fraud hotline if one exists. Most major retailers have ethics hotlines or fraud reporting mechanisms. Provide specific details: what was observed, when, and which employee. Let the company's loss prevention team investigate rather than confronting the employee directly, which could escalate the situation or provide a heads-up to allow evidence destruction.

Conclusion: The Ongoing Battle Against Internal Fraud

Matthew Lettera's $118,000 fraud scheme didn't happen because Best Buy was careless about security. It happened because he was a clever insider who understood the system and had enough access to exploit it over an extended period. By the time the fraud was detected, months had passed. The merchandise was gone. He'd recruited others. The damage was done.

Dorian Allen's case is different in method but similar in outcome. An external threat identified him as a vulnerability and exploited him through coercion. The result was still massive loss, still slow detection, still customers affected through higher prices and reduced service.

These cases represent a broader trend in retail that most customers never see. Behind every store's balance sheet is an ongoing tension between trust and verification. Retailers need to trust employees enough to give them meaningful work and responsibility. But they also need to verify and audit in ways that prevent that trust from being abused.

The future will likely feature more technology: better analytics, faster detection, more sophisticated monitoring. But technology alone won't solve the problem because the fundamental issue is human behavior. Some people will always be tempted by opportunity and pressure. The goal isn't zero fraud, which is impossible. The goal is to make it risky and costly enough that the clear-eyed calculation shows more fraud isn't worth it.

For now, retailers will keep learning hard lessons through cases like Lettera's and Allen's. They'll invest in better systems. Some will improve working conditions. Some won't. The fraud will continue, occasionally getting caught, usually going unnoticed until it's too late.

And you, as a customer, will pay for all of it, spread across thousands of transactions in the form of slightly higher prices and slightly fewer employees on the store floor. That's the hidden cost of retail fraud. It's invisible, but it's real.

Key Takeaways

- A single Best Buy employee's nine-month fraud scheme cost the retailer $118,000 through systematic exploitation of manager discount codes

- Employee theft costs U.S. retailers $60-120 billion annually—more than external shoplifting—making it the largest loss category

- Real-time transaction monitoring could have caught this fraud in days; delayed monthly audits allowed it to continue for months

- Workplace stress, high turnover (60-75% annually), and inadequate wages directly correlate with increased employee fraud rates

- Future fraud prevention requires both advanced technology (AI analysis, real-time alerts) and improved workplace culture (better pay, reasonable hours)