![Exploring Cash App's 'Buy Now, Pay Later' Feature for P2P Transfers [2025]](https://tryrunable.com/blog/exploring-cash-app-s-buy-now-pay-later-feature-for-p2p-trans/image-1-1775088262752.png)

Exploring Cash App's 'Buy Now, Pay Later' Feature for P2P Transfers [2025]

Cash App, a popular peer-to-peer (P2P) payment platform owned by Block, has introduced a groundbreaking feature that reshapes how users handle everyday transactions. Known as the 'buy now, pay later' (BNPL) option, this feature allows users to defer payments for P2P transfers, adding a new layer of flexibility to digital transactions. According to Yahoo Finance, this diversification strategy aims to boost Cash App's growth.

TL; DR

- Cash App's BNPL feature: Offers deferred payment options for P2P transfers with a 7.5% fee.

- Eligibility: Transfers of $25 or more; repayable in weekly increments up to six weeks.

- User benefits: Flexibility in cash flow management and budgeting.

- Potential pitfalls: Users should be aware of fees and repayment schedules.

- Future trends: Growing adoption of BNPL in everyday financial transactions.

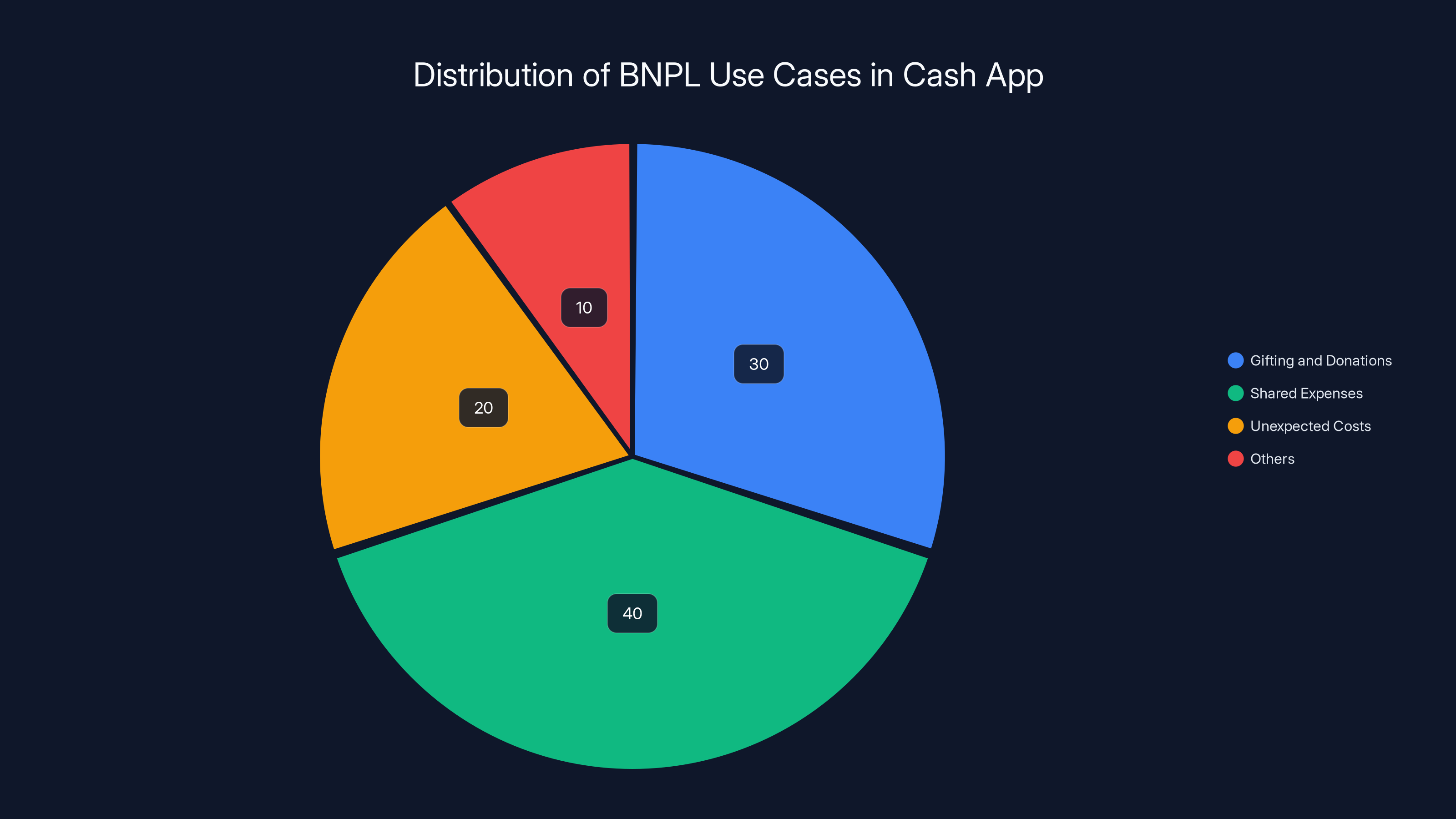

Estimated data shows that shared expenses and gifting/donations are the most common use cases for BNPL in Cash App, highlighting its role in managing everyday financial transactions.

The Rise of 'Buy Now, Pay Later' in Everyday Transactions

In recent years, BNPL has transformed from a niche offering into a mainstream financial tool, especially popular among younger consumers. Traditionally associated with retail purchases, BNPL allows consumers to split payments into manageable installments without the immediate financial burden. A report by Precedence Research indicates that the BNPL market is expected to continue growing significantly.

Cash App's introduction of BNPL for P2P transfers signifies a major shift in how these transactions are perceived and managed. This feature is particularly appealing to users who need to manage cash flow without incurring high credit card debt. According to Quartz, this move could potentially enhance user engagement and retention.

The Mechanics of Cash App's BNPL Feature

Cash App's BNPL feature is straightforward yet impactful. Users can opt to pay for transactions over time by paying a 7.5% fee on the transaction amount. For instance, a

Implementing BNPL in Your Cash App Experience

To use Cash App's BNPL feature, users must first ensure they have the latest version of the app. Here's a step-by-step guide to get started:

- Open Cash App: Ensure your app is updated to the latest version.

- Select Payment: Choose the P2P transfer you wish to defer.

- Choose BNPL Option: Opt for 'buy now, pay later' at checkout.

- Review Terms: Understand the 7.5% fee and repayment schedule.

- Confirm Transaction: Complete the process and manage repayments via the app.

Use Cases and Real-World Applications

Cash App's BNPL feature is versatile, catering to various financial scenarios:

- Gifting and Donations: Spread the cost of gifts or donations over weeks.

- Shared Expenses: Manage shared living expenses with roommates or family.

- Unexpected Costs: Cover emergency expenses without immediate financial strain.

Pros and Cons of Using BNPL for P2P Payments

Pros:

- Financial Flexibility: Offers users the ability to manage cash flow efficiently.

- No Immediate Full Payment: Avoids the financial burden of lump-sum payments.

Cons:

- Fees: The 7.5% fee can add up over time, increasing overall costs.

- Potential Debt Accumulation: Users might accumulate more debt if not managed properly.

Common Pitfalls and How to Avoid Them

- Over-reliance: Users might become too dependent on BNPL, leading to debt accumulation.

- Missed Payments: Missing a payment can lead to additional fees and impact credit scores.

To avoid these pitfalls, users should set reminders for repayment dates and ensure they have a financial plan in place.

Future Trends: The Growing Impact of BNPL

The integration of BNPL into everyday transactions is expected to grow, with more fintech companies exploring similar features. As consumer demand for financial flexibility increases, BNPL can expand beyond P2P and retail into areas like utilities and rent. A survey by Inside Radio found that nearly half of consumers use BNPL services weekly, underscoring its rising popularity.

Best Practices for Managing BNPL Payments

- Budget Wisely: Include BNPL payments in your monthly budget.

- Track Payments: Use financial apps or calendars to track due dates.

- Communicate: If using BNPL for shared expenses, communicate with all parties involved to ensure smooth transactions.

Expert Opinions and Industry Insights

Financial experts suggest that while BNPL offers convenience, it requires disciplined financial management. According to a study by McKinsey, consumers should weigh the benefits against potential long-term costs.

"BNPL is a powerful tool for financial management, but like any credit service, it demands responsibility," — Financial Advisor, Sarah Johnson

Technical Considerations for Developers and Fintech Innovators

For developers looking to implement similar features, consider the following:

- User Interface Design: Ensure the process is intuitive and user-friendly.

- Security Measures: Implement strong security protocols to protect user data.

- Integration with Existing Systems: Ensure seamless integration with existing payment gateways.

Looking Ahead: The Future of BNPL in Fintech

As fintech continues to evolve, BNPL is poised to become a staple in financial transactions. Companies are exploring AI-driven solutions to better assess creditworthiness and tailor BNPL offerings to individual users. According to Yahoo Finance, this trend is likely to continue as companies seek to diversify their offerings.

Conclusion

Cash App's 'buy now, pay later' feature is a significant step forward in the evolution of P2P payments, offering users unparalleled flexibility in managing their finances. By understanding the mechanics, benefits, and potential pitfalls of this feature, users can make informed financial decisions that align with their needs.

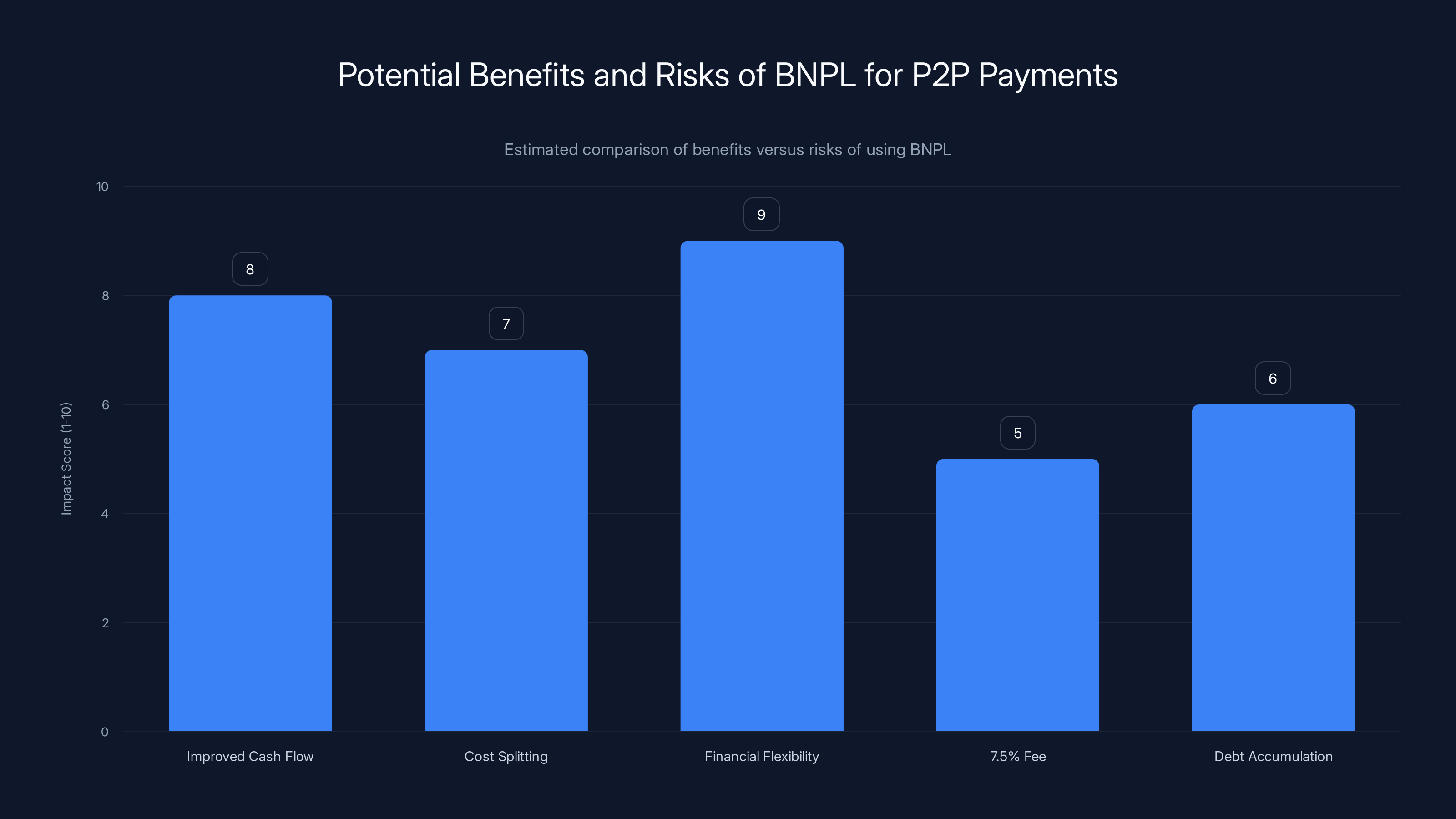

Estimated data shows that while BNPL offers significant benefits like improved cash flow and financial flexibility, users must be cautious of the 7.5% fee and potential debt accumulation.

FAQ

What is Cash App's 'buy now, pay later' feature?

Cash App's 'buy now, pay later' feature allows users to defer P2P payments over time, paying a 7.5% fee for the service.

How does the repayment process work?

Users can repay the amount in weekly increments over six weeks or in full by the due date, starting from transfers of $25 or more.

What are the benefits of using BNPL for P2P payments?

Benefits include improved cash flow management, the ability to split costs over time, and flexibility in managing finances.

Are there any risks associated with BNPL?

Yes, users should be aware of the 7.5% fee and potential for debt accumulation if payments are missed or mismanaged.

How can users avoid pitfalls with BNPL?

Users can avoid pitfalls by budgeting wisely, setting payment reminders, and not relying too heavily on BNPL services.

What is the future of BNPL in fintech?

BNPL is expected to expand into new sectors, driven by increasing consumer demand for flexible financial solutions.

Key Takeaways

- Cash App introduces BNPL for P2P transfers, enhancing payment flexibility.

- Users can defer payments with a 7.5% fee, repayable over six weeks.

- BNPL's popularity is rising among millennials and Gen Z consumers.

- Managing BNPL requires financial discipline to avoid debt accumulation.

- BNPL is expected to expand into new financial sectors in the future.

- Developers should focus on security and user-friendly interfaces for BNPL.

- Financial experts advise weighing BNPL benefits against costs.

- Cash App's BNPL is a response to growing demand for flexible payments.

Related Articles

- Understanding X Money: The Future of Payments with William Shatner and Elon Musk [2025]

- The Future of PayPal: Navigating Market Dynamics and Strategic Decisions [2025]

- Cash App Payment Links: Simplifying Digital Payments [2025]

- AI Fraud: The $400 Billion Threat Outpacing Banks [2025]

- Understanding Banking App Glitches: Lessons from Lloyds and Beyond [2025]

- How Global Tensions Impact IPO Strategies: The Case of PhonePe [2025]