![GameStop's 400+ Store Closures: The Death of Physical Gaming [2025]](https://tryrunable.com/blog/gamestop-s-400-store-closures-the-death-of-physical-gaming-2/image-1-1768151170450.jpg)

The Beginning of the End: Game Stop's Seismic Store Closures in 2025

Something unprecedented is happening in the gaming retail world, and it's happening fast. Game Stop, once the undisputed king of physical video game sales, is shutting down over 435 stores across 42 states as we head into 2026. This isn't a minor adjustment or a strategic pivot. This is an existential reckoning for a company that, just a few years ago, seemed poised for resurrection. According to GamesIndustry.biz, these closures are part of a broader strategy to streamline operations and focus on profitability.

The numbers are staggering. As of mid-January 2026, Game Stop had already initiated or completed closures of 435 locations, according to tracking data. That's not just significant—it's cataclysmic for a company that had 2,325 US stores as of February 2025. We're talking about an 18.7% reduction in physical retail footprint in just one fiscal year. For context, that means nearly one in five Game Stop locations are disappearing.

But here's where it gets complicated. On the surface, this looks like a company in freefall. And in many ways, it is. But the narrative underneath is far more nuanced. The driving force behind these closures isn't entirely desperation—it's a calculated financial engineering play that reveals something deeper about how modern corporate incentives can clash with human consequences.

Game Stop CEO Ryan Cohen is sitting on stock options that could be worth up to

The question isn't whether Game Stop can survive the loss of 400+ stores. It's whether Game Stop, as we know it, should survive at all. And the company's leadership seems to have already answered that question.

TL; DR

- 435 stores closing across 42 states: Game Stop is shuttering roughly 18.7% of its US retail footprint in fiscal 2025, following 590 closures in 2024

- CEO compensation mega-package at stake: Ryan Cohen's 100 billion market cap, incentivizing aggressive cost-cutting

- International retreat accelerating: Game Stop has already exited Canada, Germany, Austria, Ireland, Switzerland, and Italy, with France departures planned within 12 months

- Thousands of jobs being eliminated: Conservative estimates suggest 6,000+ workers are losing employment due to store closures and winding down operations

- Physical gaming retail in structural decline: The shift to digital distribution, streaming, and digital-only platforms has fundamentally changed how people buy games

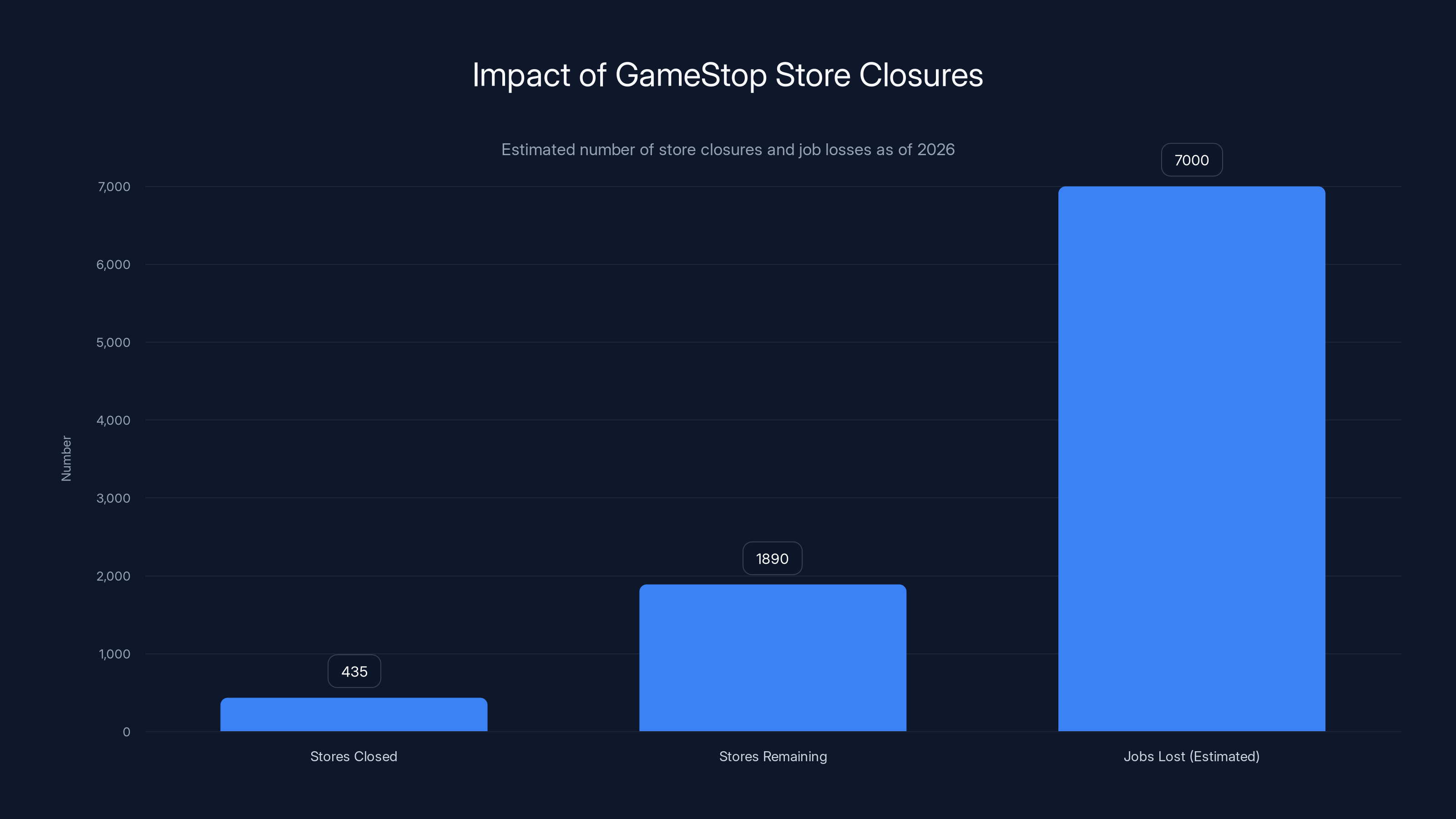

GameStop has closed 435 stores, leaving 1,890 operational. Estimated job losses range from 6,000 to 8,000.

The Ryan Cohen Factor: When CEO Incentives Drive Corporate Strategy

You can't understand Game Stop's current trajectory without understanding Ryan Cohen's compensation package. And you really can't understand it without doing the math.

Cohen's potential payday is structured around stock options that vest if Game Stop reaches a

And there's one quick way to improve those metrics: eliminate unprofitable assets. Close the stores that are dragging down your margins. Cut the headcount. Reduce the footprint. Make the remaining business leaner, meaner, and more efficient on a per-location basis.

This isn't new strategy. It's the playbook that's worked for retail optimization going back decades. When Circuit City faced competition from online retailers, did it expand stores or consolidate? When Blockbuster faced Netflix, did it double down on locations? No. Both companies rationalized their footprints aggressively. And both went bankrupt anyway.

But the dynamics are different for Cohen. He's not trying to save a dying retail chain. He's trying to trigger a stock price surge that turns his options into real money. Closing unprofitable stores is the fastest path there, regardless of what happens to the company's actual business long-term.

Let's look at the mathematics. If Game Stop can show improving unit economics at the store level—meaning the remaining stores generate better profits—then it can claim operational success. Analysts might upgrade the stock. Institutional investors might believe the turnaround narrative. And if enough momentum builds, the share price could actually climb, bringing that $100 billion market cap into the realm of possibility.

Is it a sustainable strategy? Almost certainly not. But sustainability isn't the goal. The goal is a stock price spike before the options vest. That's a materially different objective.

The irony is that Cohen hasn't been wrong about everything. Game Stop has actually stabilized. The company has reduced cash burn. It's not hemorrhaging money like it was a few years ago. There's a functioning business underneath this mass of store closures. But whether that business can sustain itself—and grow into a $100 billion valuation—is a different question entirely.

Closing 435 stores led to a 53% increase in operating profit despite a 23% drop in revenue, highlighting how margin improvements can mask underlying business issues. Estimated data.

The Math of Closure: Why 435 Stores Weren't Making Money

Game Stop's store closure pattern tells us something important about retail economics that's often overlooked in broader retail decline narratives. Not all stores are created equal. And in Game Stop's case, the surviving stores are likely generating disproportionately higher revenue per location than the stores being closed.

Let's think about the store closure calculus. Game Stop had approximately 2,325 US stores as of February 2025. It's closing 435 stores. That leaves roughly 1,890 stores. Now, here's the key question: what was the revenue and profitability distribution across those 2,325 locations?

In any mature retail chain, you'll typically see a power-law distribution. The top 20% of stores by revenue might generate 50-60% of total sales. The bottom 30-40% of stores might generate just 10-15% of sales. These bottom-quartile locations are often money losers or break-even operations that exist primarily for legacy reasons or geographic coverage.

Game Stop closing 435 stores (roughly 18.7% of its footprint) in a single year suggests the company has identified a specific subset of locations that are underperforming. The question is: by how much?

If those 435 stores were generating, say, $150 million in annual revenue but running at an operating loss (after accounting for rent, labor, inventory carrying costs, and corporate overhead), then closing them would immediately improve the company's operating margin. But it would reduce total revenue and further concentrate the customer base into a smaller store footprint.

There's also the inventory carrying cost factor. Physical retail requires holding inventory. Every store has capital tied up in stock. By closing stores, Game Stop reduces its total inventory obligations, which frees up cash and improves balance sheet metrics. That matters to institutional investors and credit rating agencies.

The labor angle is straightforward: fewer stores mean fewer employees. At an average of roughly 4-5 full-time employees per Game Stop location (based on typical mall store staffing), 435 store closures represent somewhere in the range of 1,740 to 2,175 direct job losses, not counting the corporate redundancies that often follow store rationalization.

But here's where the strategy gets interesting. Game Stop is simultaneously investing in digital capabilities and its loyalty program. The company is trying to shift customer acquisition away from foot traffic and towards direct-to-consumer channels. If that works, then the company becomes less dependent on physical store proximity. You don't need a Game Stop on every corner if you can deliver digital content and services to homes.

The problem is that strategy requires building a legitimate DTC business, which Game Stop hasn't really done. The company's web presence is still oriented around driving traffic to stores. Its loyalty program has some digital hooks, but it's not clear if that's generating meaningful incremental revenue.

The Digital Shift: Why Physical Games Are a Dying Category

The most important context for Game Stop's collapse isn't internal to Game Stop. It's external. It's the fundamental shift in how people acquire and play games.

Five years ago, physical game sales still represented a meaningful percentage of overall game revenue. Today? Physical is rounding toward zero.

The shift has three components. First, digital game sales. Platforms like the PlayStation Store, Xbox Game Pass, Nintendo eShop, and Steam now account for the majority of game purchases. A gamer doesn't need to visit a store. They buy the game online, download it to their device, and play. No physical medium required. No shipping wait times. No middle person required.

Second, subscription services. Game Pass, PlayStation Plus, Xbox Game Pass Ultimate—these services have fundamentally changed the game acquisition model. Instead of buying individual games, players pay a monthly subscription and get access to hundreds or thousands of titles. Why would you buy a game for

Third, mobile gaming and cloud gaming. A huge percentage of gaming now happens on phones. And cloud gaming services are emerging as real alternatives to local hardware gaming. You don't need to buy a game cartridge or disc if the game streams from a data center.

What does Game Stop sell? Physical games. Consoles. Accessories. Collectibles. These are all categories that have been in structural decline for years. The console market itself is shrinking. The big three—PlayStation, Xbox, Nintendo—are all seeing declining hardware sales year-over-year.

Game Stop has attempted to pivot into collectibles and apparel, but that's niche revenue. It's not going to replace the loss of physical game sales. It's a rounding error compared to the core gaming decline.

The company is caught between an industry paradigm shift and the inertia of its own cost structure. It has tens of thousands of employees, hundreds of millions in rent obligations across thousands of leases, and corporate overhead designed for a much larger business. You can't pivot that ship on a dime. You can only shrink it and hope something else emerges.

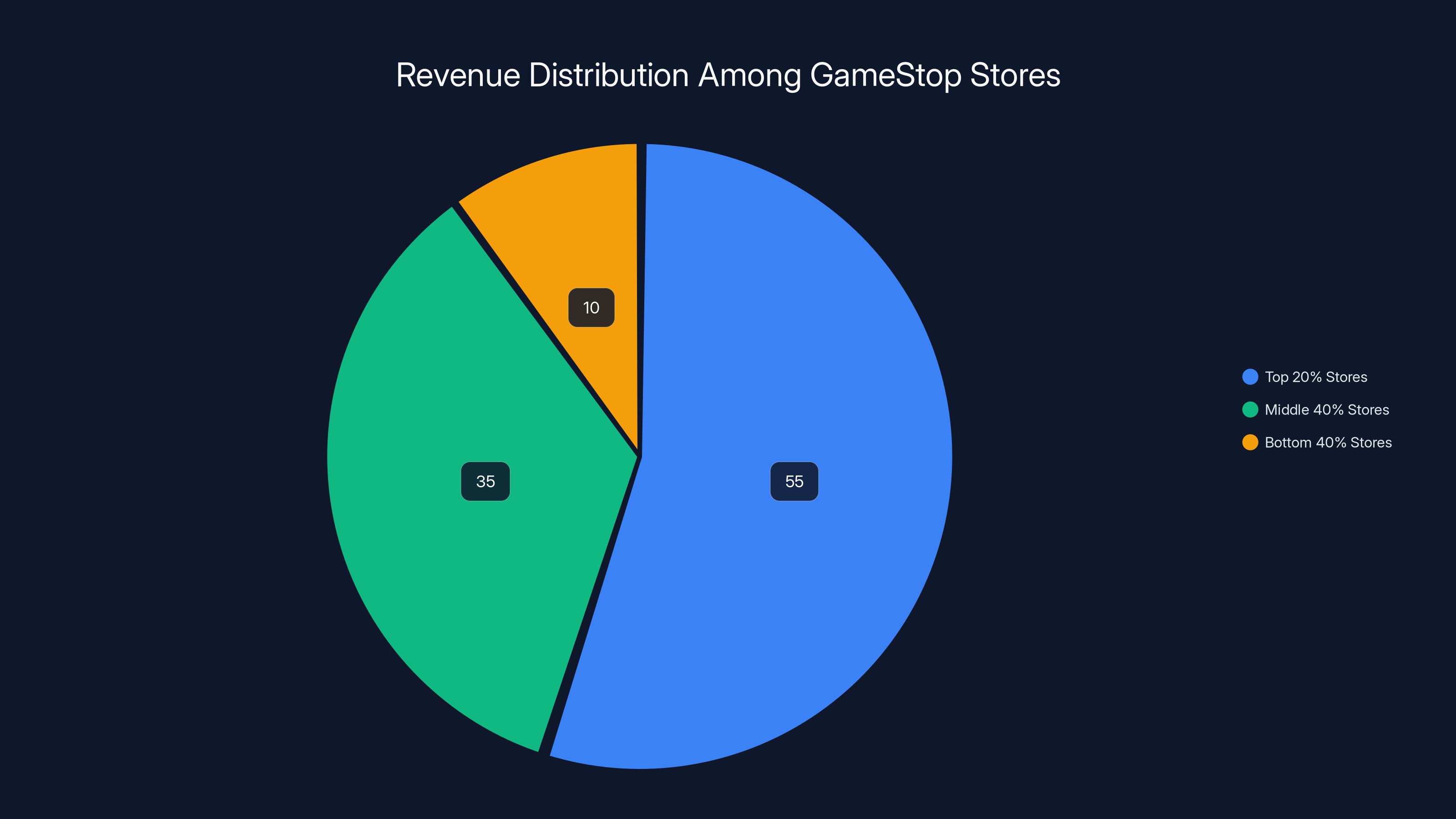

Estimated data shows that the top 20% of GameStop stores generate about 55% of total sales, while the bottom 40% contribute only 10%. Closing underperforming stores can improve overall profitability.

International Retreat: The Global Contraction Story

Game Stop's store closures aren't limited to the United States. The company is simultaneously winding down international operations with surprising speed.

According to recent filings, Game Stop has already exited Canada, Germany, Austria, Ireland, Switzerland, and Italy. The company has plans to exit France within the next 12 months. When you list out all the countries, it's clear: Game Stop is not interested in being a global retailer anymore. It's retreating to a fortress America strategy, and even that fortress is being aggressively downsized.

Why the rapid international retreat? The answer is likely twofold. First, international operations are complex. They require local management, local supply chains, local accounting, and compliance with different regulatory regimes. That complexity is costly and hard to manage when your core business is contracting.

Second, the digital shift is even more pronounced internationally. In many European countries, digital game distribution penetration is higher than in the United States. So the core business problem—physical game sales declining—is even more acute in those markets.

Closing international operations is a financial positive in the short term. It eliminates complexity, reduces overhead, and consolidates the business around a single geography. But it also signals a company that's given up on global scale. That's worth noting for what it implies about Game Stop's future trajectory.

The France exit is particularly interesting. Game Stop is planning to complete the exit within 12 months, which means the company is burning through European operations quickly. There's no long-term international strategy here. There's just cash-preservation through contraction.

The Employment Impact: 6,000+ Jobs in Jeopardy

Here's the part of this story that gets glossed over in financial narratives: thousands of people are losing their jobs.

Game Stop's store closures mean job losses across multiple layers. First, there's the direct impact: the store employees themselves. At an average of 4-5 employees per store, 435 closures represent somewhere between 1,740 and 2,175 direct job losses.

But that's just the tip of the iceberg. Behind every store is corporate infrastructure. Distribution centers. Logistical staff. Regional managers. Buyers. Human resources. Accounting. When you eliminate 435 stores, you're also triggering redundancies across the corporate structure.

International retreat adds another layer. Staff in Canadian, German, Austrian, Irish, Swiss, and Italian operations are being let go. The French exit over the next 12 months will trigger additional workforce reductions.

Conservative estimates suggest total employment impact is somewhere in the range of 6,000 to 8,000 jobs. And these aren't high-margin professional jobs. These are retail workers, logistics workers, middle-management positions in regional markets. These are people in communities where Game Stop was often one of the major employers.

The broader narrative around retail consolidation often treats job losses as inevitable casualties of market forces. "Disruption," the narrative goes. "Creative destruction." Amazon disrupted retail. Digital disrupted physical media. That's just how capitalism works.

But there's a human cost to that narrative that's worth acknowledging. Someone had a job at a Game Stop, a distribution center, or corporate headquarters. They're losing that job not because they performed poorly, but because their employer made a strategic calculation that eliminating their position was necessary to hit a stock valuation target.

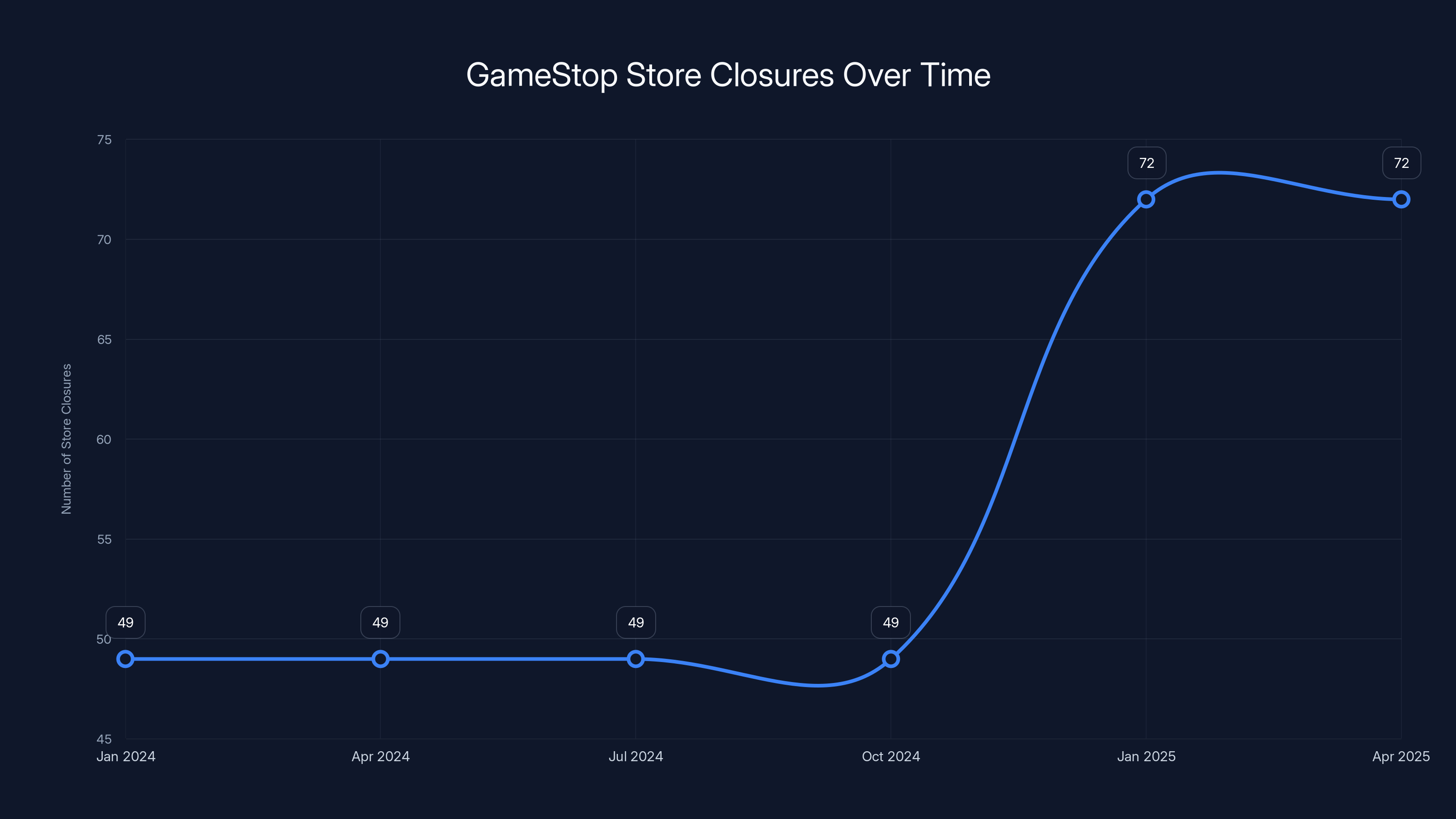

GameStop accelerated its store closures from an average of 49 per month in 2024 to approximately 72 per month by early 2025, indicating a strategic shift towards rapid downsizing. Estimated data.

The Game Stop Meme Stock Legacy: How Hype Met Reality

It's worth remembering where Game Stop was just a few years ago, because it provides crucial context for understanding the current situation.

In January 2021, Game Stop stock became a sensation. Reddit retail investors organized around the stock, driving it to unprecedented valuations. The stock hit $480 per share. The company briefly had a higher market cap than companies with orders of magnitude more revenue and profitability. For a few weeks, Game Stop was the hottest story in investing.

The meme stock rally attracted massive media attention and celebrity investors. Celebrity entrepreneurs talked about disrupting the gaming industry from within. Retail investors believed Game Stop could become the next great tech company. The stock was a vehicle for anti-establishment sentiment, a way to stick it to institutional investors who'd bet against the company.

Then reality hit. Game Stop's business fundamentals didn't change. The store closures continued. Revenue contracted. Losses accumulated. The stock inevitably crashed back to earth.

But during that period when the stock was soaring, something important happened: Game Stop and its then-CEO raised capital. The company issued new stock at inflated valuations, raising cash that provided a runway. That cash runway enabled the company to survive long enough to do exactly what it's doing now—aggressive cost-cutting and store rationalization.

So in a strange way, the meme stock era actually prolonged Game Stop's existence. The euphoria gave the company time and resources to remake itself, even if that remake involves shuttering the majority of its physical footprint.

Ryan Cohen's arrival as CEO in 2022 came with expectations that he'd apply his Chewy playbook to gaming retail—building a DTC juggernaut that could compete with Amazon and digital platforms. That hasn't happened. Instead, we've gotten aggressive store rationalization and cost-cutting. Which is fine. It's a legitimate strategy. But it's very different from the growth story that animated the meme stock narrative.

Store Profitability Paradox: When Closing Stores Improves Metrics

Here's a counterintuitive reality about retail economics that's crucial to understanding what Game Stop is doing: closing unprofitable stores can actually make a company look financially healthier.

Consider two scenarios. In Scenario A, Game Stop operates 2,325 stores and generates

In Scenario B, Game Stop operates 1,890 stores (after closing 435 locations) and generates

To a financial analyst or investor looking at margin improvement, Scenario B looks like operational success. "Game Stop turned around its profitability," they might say. "The company found operational efficiencies."

But what actually happened? The company eliminated its lowest-margin stores. That's not a business turnaround. That's profit through subtraction.

The danger is that investors conflate margin improvement with business health. And sometimes those things are correlated. If a company improves margins through genuine operational efficiency—better supply chain, reduced overhead, technological improvements—then margin improvement is a sign of a healthy, improving business.

But if a company improves margins purely through store closures and cost-cutting, it's masking an underlying structural decline. The customer base is shrinking. The market position is eroding. But the financial statements look better because you've eliminated the parts of the business that made the statement look bad.

For Game Stop, this matters because it affects how the market values the stock. If investors believe Game Stop is on a profitability turnaround, they might bid up the stock price, getting Cohen closer to that $100 billion valuation threshold. But if the improvement is just accounting sleight-of-hand—profit through subtraction rather than addition—then the stock rally would be based on false premises.

GameStop plans to close 435 stores in 2025, following 590 closures in 2024, affecting over 6,000 jobs. Estimated data based on company announcements.

The Loyalty Program Bet: Can Direct-to-Consumer Save Game Stop?

Amidst all the store closures, Game Stop is simultaneously investing in its loyalty program. The company is trying to build a direct-to-consumer relationship with customers that doesn't depend on physical store proximity.

This is theoretically sound. If Game Stop can convert its customer base into a DTC community, it could eventually operate more like a content platform and less like a retail store chain. Customers would engage with Game Stop online, through the app, or through email and social media. They'd buy digital content, physical collectibles shipped to their homes, and maybe some hardware.

The loyalty program is the entry point for that strategy. Get customers to enroll, track their behavior, understand their preferences, and then market to them directly.

But here's the problem: Game Stop's customer base is primarily interested in physical games. That's what brought them to the stores. And the market for physical games is shrinking. So Game Stop is trying to build a DTC business around a declining customer base interested in declining product categories.

That's possible to execute, but it requires significant customer acquisition beyond the existing base. It requires building brand equity around things like collectibles, apparel, and community that go beyond gaming. It requires becoming something more like Hot Topic or Spencer's—a pop culture destination—than a gaming retailer.

There's no evidence Game Stop has successfully executed that transformation. The loyalty program exists, but metrics around its effectiveness aren't particularly compelling. The company talks about it in investor communications, but the growth trajectory suggests it's not driving meaningful incremental revenue.

The danger is that Game Stop closes stores to improve financial metrics while its DTC business is still in early, unproven stages. If the loyalty program doesn't scale, then Game Stop has eliminated stores without building a viable replacement revenue channel. That's a contraction death spiral.

The Lease Landscape: Why Store Closures Take Time

One thing that often gets overlooked in retail closures is the lease situation. Retailers don't own most of their stores. They rent them. And lease agreements aren't easy or cheap to exit.

Game Stop has 1,890 remaining stores after closures, but it likely has lease obligations on many of those locations for several more years. That's operating leverage working in the opposite direction. The company has to pay rent even as sales decline and the store becomes a financial drain.

Store closures involve lease termination negotiations, buyout fees, and sometimes just continuing to pay rent on empty spaces while looking for subleasing opportunities. None of that is cheap.

This is one reason Game Stop's path to profitability is more difficult than it might appear. The company can close 435 stores, but it still has rent obligations on the remaining 1,890 stores. If foot traffic is declining and comp sales are negative (which they almost certainly are), then the cost basis of those remaining stores becomes even more problematic.

The ideal endgame for Game Stop would be to shrink to a much smaller footprint—maybe 500-700 core locations in high-traffic areas—and then supplement with a dominant DTC business. But getting from 1,890 stores to 700 stores requires breaking or renegotiating hundreds of leases. That's expensive and time-consuming.

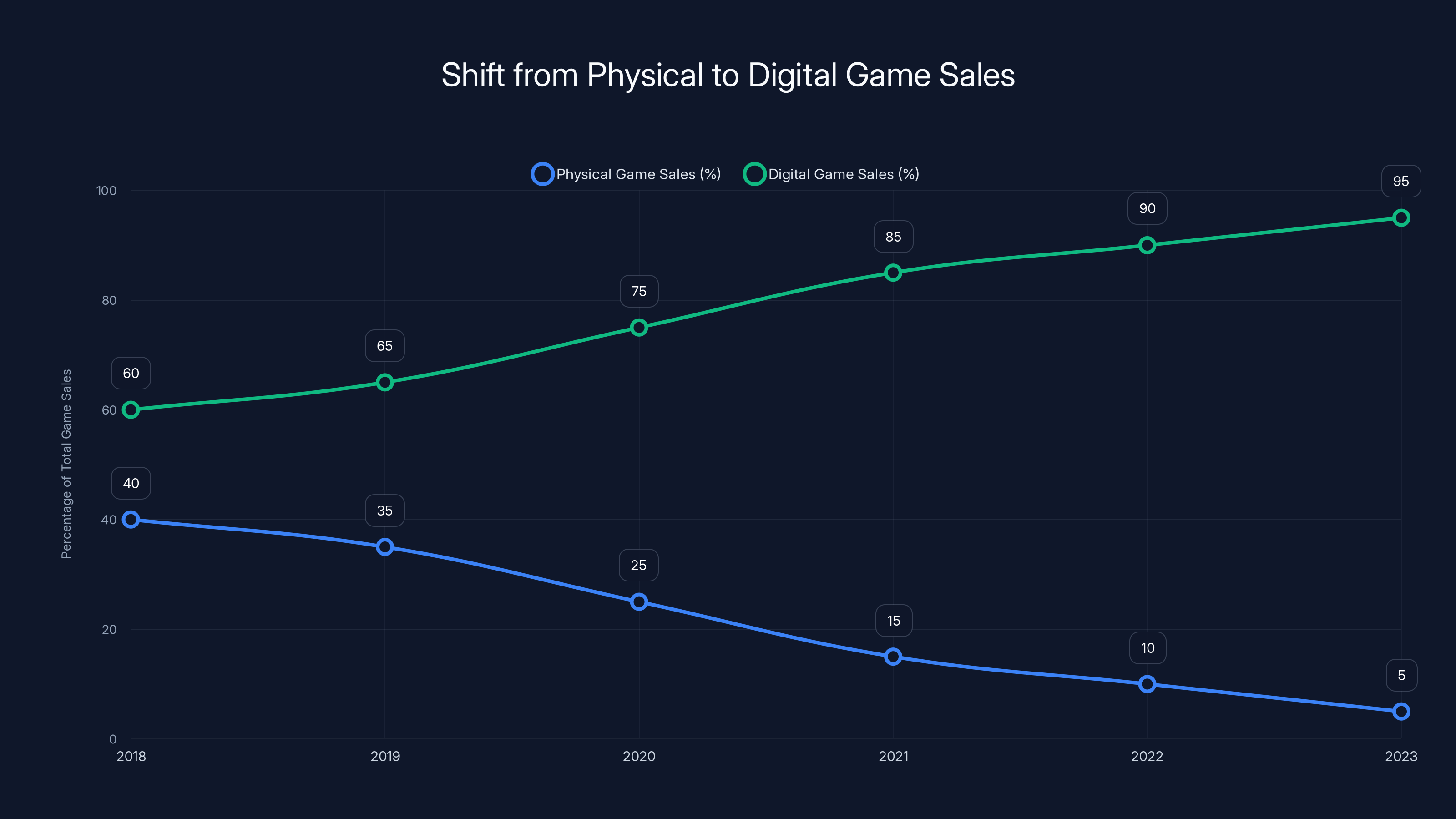

The chart illustrates the dramatic decline in physical game sales from 40% to 5% over five years, with digital sales rising to dominate the market. Estimated data.

Competitive Landscape: What's Game Stop Competing Against?

Understanding Game Stop's current situation requires understanding what it's competing against. And the answer is: everything.

Game Stop is competing against Amazon for hardware and physical media sales. It's competing against the PlayStation Store, Xbox Game Pass, Steam, Epic Games Store, and Nintendo eShop for game sales. It's competing against Twitch streamers and YouTube creators for entertainment attention. It's competing against mobile gaming for casual gaming hours. It's competing against subscription services and cloud gaming for how people access entertainment.

And Game Stop is competing with all of this using a business model built on selling physical games in physical stores. That model made sense in 1998. In 2025, it's fighting against fundamental industry trends.

The question isn't whether Game Stop can survive—it probably can, at least for a while longer. The question is what Game Stop is actually competing on. If it's competing on convenience, it loses to digital platforms. If it's competing on selection, it loses to Amazon. If it's competing on price, it loses to competitors with lower cost bases. If it's competing on experience, it's struggling because the store experience is often just a place to browse before buying elsewhere.

Game Stop's one potential competitive advantage is community. Gaming communities are real, and Game Stop locations could theoretically be gathering spaces. But that requires investment in-store experience, events, and community management. And Game Stop's strategy is to close stores, not invest in them.

So the competitive situation is bleak. Game Stop occupies a niche in the retail landscape—physical games—that's structurally declining. No amount of store closures or cost-cutting changes that fundamental dynamic.

Financial Engineering vs. Business Building: The Cohen Strategy

Ryan Cohen's approach to Game Stop reveals something important about modern corporate strategy: sometimes financial engineering wins out over business building.

A business-building approach would involve identifying a new market opportunity, investing in it, building it up, and then optimizing it. That's what Cohen did with Chewy—he started with an insight (pet owners spend lots of money on supplies), built a company around it, and sold it to PetSmart for $3.35 billion.

A financial engineering approach involves taking an existing asset, restructuring it to improve key financial metrics, and then triggering a stock price increase by getting investors excited about the improved metrics.

Game Stop's current trajectory is clearly financial engineering. Close stores. Reduce costs. Improve margins. Show operational improvement. Get the stock price to rise. Cash in stock options.

There's nothing inherently wrong with financial engineering. It's a legitimate business strategy. But it's a strategy optimized for the short term, not the long term. And it has very different implications for everyone involved.

For shareholders who bought in during the meme stock period and are still holding: financial engineering might work out if the stock price actually rises. For employees being laid off: financial engineering means they lose their job. For customers: financial engineering might mean fewer locations and worse service. For creditors: financial engineering can sometimes work out, but it often presages eventual bankruptcy.

The ethical question isn't whether financial engineering is legal—it usually is. The ethical question is whether it's the right approach for a company that was once an employer of tens of thousands, a cultural institution in gaming, and a trusted place for gamers to explore their hobby.

Cohen's playbook is working, at least in the short term. The stock has rebounded from its lows. The company's balance sheet is improving. Financial metrics look better. If he can get the stock to $300+ per share, his options would be in-the-money, and he'd have access to billions in value.

But the business underneath that financial engineering is still shrinking. That's not a problem for Cohen's options. It is a problem for Game Stop's long-term viability.

The Broader Retail Trend: Is This Unique to Game Stop?

Game Stop's store closures are dramatic, but they're not unique. They're part of a broader trend in retail where companies are rationalizing physical footprints in response to structural industry shifts.

Best Buy closed 250 stores over a period of years. Circuit City went completely bankrupt. Blockbuster went bankrupt. Toys "R" Us went bankrupt. Barnes & Noble nearly did. All of these companies faced similar dynamics: digital disruption of their core business, oversupanded store footprints, and the need to right-size their operations.

When a company faces that situation, it has a few options. It can invest heavily in digital and omnichannel capabilities while maintaining a smaller physical footprint. That's what Best Buy did—it downsized stores but maintained a strong online presence. It survived.

It can pivot to adjacent categories or experiences. That's what Barnes & Noble did—it shifted focus to books as a cultural experience and events as a community gathering. It's doing better now than it was five years ago.

Or it can aggressively rationalize and cost-cut while hoping something changes. That's what Game Stop is doing. And historically, that approach doesn't end well.

The difference is that Best Buy had higher margins on its products and broader market positioning. Electronics retail has better fundamentals than gaming retail, even post-disruption. Barnes & Noble has cultural cachet and community value that extends beyond just book sales. Game Stop is primarily dependent on a category—physical games—that's in structural decline.

Game Stop hasn't found a comparable diversification strategy. Collectibles and apparel are nice, but they're not big enough to replace gaming revenue.

The 2026 Acceleration: Why This Year Is Different

The timing of these 435 closures—happening in January 2026, just as fiscal 2025 is ending—reveals something important about the strategy. This isn't a normal retail rationalization happening over several years. This is an acceleration.

Game Stop closed 590 stores in fiscal year 2024. It's closing 435 in just the first month of fiscal 2025. That's a pace of roughly 5,000+ stores annually if sustained, which would eliminate the entire US footprint in less than five months.

Obviously, the pace won't sustain. The company needs to maintain some store base for continued revenue. But the acceleration is notable. It suggests management feels urgency around hitting financial targets before a specific deadline.

What's the deadline? It could be related to investor meetings or quarterly earnings. It could be related to Cohen's compensation vesting. It could be related to debt covenants or other financial obligations.

The acceleration also might indicate that management has simply given up on the turnaround narrative. For the first couple of years after Cohen's arrival, there was talk of transformation, repositioning, and new direction. Now? The narrative is just contraction.

What Happens Next: Three Possible Futures

So what's actually going to happen to Game Stop? There are roughly three scenarios.

Scenario One: Stabilization and Managed Decline. Game Stop closes stores until it reaches a sustainable footprint of maybe 500-700 locations in high-traffic areas, builds a functional DTC business around collectibles and niche gaming, and operates as a small, profitable specialty retailer. The company wouldn't be big, but it would be viable. This assumes the loyalty program and digital business actually work, which is far from guaranteed.

Scenario Two: Bankruptcy and Restructuring. Game Stop's store closures accelerate, but the DTC business never materializes. The company's revenue contract faster than costs decline. The company eventually becomes insolvent, files for bankruptcy, gets reorganized, and emerges as a much smaller company. This is the most likely scenario if the loyalty program doesn't scale.

Scenario Three: Acquisition or Strategic Partnership. Game Stop eventually gets acquired by a larger company—perhaps Microsoft, which wants gaming retail presence, or Amazon, which wants to complete its retail dominance—or partners with another company to become part of a larger platform. This could happen as a voluntary transaction or as a fire sale during financial distress.

None of these scenarios is particularly bullish for Game Stop as an independent company. Even Scenario One requires the company to successfully execute a business model transformation it hasn't yet demonstrated an ability to execute.

The most likely outcome is Scenario Two—continued contraction until the company either stabilizes at a tiny scale or goes through bankruptcy. But nothing about the current trajectory suggests management is successfully building toward viability.

Workforce Transition and Community Impact

Beyond the financial metrics and corporate strategy, there's a human story here that deserves attention.

Game Stop employees in the 435 closing stores are facing job loss. For many, this is their primary income. For some, Game Stop might be their only job experience. The company offers severance to some employees, but severance is never equivalent to continued employment.

In smaller markets, losing a Game Stop might mean losing one of the few retail employers in the area. Communities that depend on a handful of retail establishments face economic disruption when those establishments close.

State and local governments in those 42 states are also affected. Game Stop stores generate tax revenue and sales tax. Store closures mean reduced tax revenue, requiring local governments to either cut services or increase taxes elsewhere.

There's also a cultural component. Game Stop was a gathering place for a generation of gamers. It was where you went to discuss games, trade titles, and find community with people who shared your interests. That's less critical now that gaming communities exist online, but for many people, their local Game Stop was a meaningful space.

There's no good outcome here for the people affected by these closures. The best case is that workers transition to other jobs in reasonable time. The worst case is that workers face extended unemployment, particularly in areas with limited retail opportunities.

Corporate cost-cutting generates benefits for shareholders (especially those like Cohen who benefit from stock appreciation). Those benefits come at a cost to workers and communities. That's a trade-off worth acknowledging even if you believe the business decision is sound.

The Collector and Nostalgia Factor

One aspect of Game Stop's potential future is its positioning as a collectibles destination. Physical game collectors still exist. Retro gaming has become a genuine hobby with dedicated followers.

Game Stop is attempting to lean into this, stocking collectibles, vintage games, and merchandise. This is actually a more viable business than selling new physical games. Collectors have brand loyalty and willingness to pay premium prices. It's a high-margin business. And it's not directly competing against digital platforms.

But collectibles retail is a very different business from game retail. It requires deep knowledge, curation, and community engagement. It's more similar to comic book shops or specialty retail than to mainstream electronics retail. Success requires smaller, carefully managed locations in high-traffic areas, not a chain of 1,890 stores scattered across mall spaces.

If Game Stop can successfully transform into a collectibles-focused retailer with maybe 200-300 strategically located stores, that's actually viable. But that requires significant shift in operational capability, merchandising philosophy, and employee training. And there's no evidence Game Stop is building that capability.

Investor Sentiment and Stock Dynamics

Game Stop's stock performance will ultimately determine Cohen's options outcome. The stock has recovered significantly from its lows, but whether it can reach the $100 billion market cap required for Cohen's options to be worth billions is still uncertain.

The current investor narrative is something like: "Game Stop is in turnaround mode. Management is executing cost-cutting. Financial metrics are improving. The stock could surge." That narrative sustains stock prices during periods of operational decline.

But there's a tipping point where that narrative breaks. If the company closes too many stores, if revenue declines accelerate, if the DTC business never materializes, then investors will eventually lose faith. When that happens, the stock price could collapse, and Cohen's options would be worthless.

The window for the narrative to hold is probably a year or two, maybe three. Management needs to show some evidence of stabilization and positive direction within that timeframe. Otherwise, the market moves on.

FAQ

Why is Game Stop closing so many stores?

Game Stop is closing 435 stores primarily because they're generating insufficient revenue relative to their cost structure. Physical game sales have declined dramatically due to digital distribution, subscription services, and cloud gaming. The company is rationalizing its footprint to eliminate low-performing locations and improve overall financial metrics. CEO Ryan Cohen's compensation package, which could be worth up to

How many Game Stop stores are still operating?

After closing 435 stores, Game Stop has approximately 1,890 stores remaining in the United States as of early 2026. This represents a reduction of roughly 18.7% from the approximately 2,325 stores the company had as of February 2025. The company is also winding down international operations, having already exited Canada, Germany, Austria, Ireland, Switzerland, and Italy, with plans to exit France within 12 months.

Is Game Stop going bankrupt?

Game Stop is not currently bankrupt, but it faces significant long-term viability challenges. The company has reduced cash burn and improved balance sheet metrics through aggressive cost-cutting, but its core business—selling physical games—is in structural decline. Whether Game Stop can stabilize as a smaller, profitable company depends primarily on whether it can successfully build a viable direct-to-consumer business and pivot toward collectibles and niche gaming. If the loyalty program and DTC strategy fail to scale, bankruptcy becomes increasingly likely within the next 3-5 years.

How many Game Stop employees are losing their jobs?

Conservative estimates suggest that between 6,000 and 8,000 jobs are being eliminated due to store closures and international operations wind-down. The 435 store closures directly impact approximately 1,740 to 2,175 store employees (at 4-5 employees per location), but the company is also eliminating corporate positions in areas like distribution, logistics, regional management, and international operations. These job losses are concentrated across 42 US states and six countries where Game Stop is exiting operations.

What is Ryan Cohen's incentive structure and how does it affect Game Stop's strategy?

Ryan Cohen holds stock options that could be worth up to

Can Game Stop survive as a collectibles and specialty retailer?

It's theoretically possible, but Game Stop hasn't demonstrated the capabilities required. Successful collectibles retail requires deep curation, community engagement, specialized knowledge, and smaller, strategically located stores in high-traffic areas. Game Stop's infrastructure was built for mass-market game sales in mall locations, which is very different from specialty retail. The company would need to significantly retrain its workforce, completely restructure its merchandising and inventory systems, and build brand equity in a new category. There's limited evidence Game Stop is executing this transformation successfully.

What's the timeline for Game Stop's next major decision point?

The most critical timeline is the next 12-24 months. Management needs to show evidence that store closures are improving financial metrics and that the DTC/loyalty program is generating meaningful revenue. Quarterly earnings reports will be key indicators of whether the strategy is working. If revenue continues to decline faster than costs, or if the DTC business fails to scale, investor sentiment will likely shift negatively and the stock price could collapse. Cohen's options have varying vesting schedules, but the window for achieving a viable turnaround narrative is probably 18-36 months.

What happened to the meme stock narrative around Game Stop?

Game Stop's brief moment as a meme stock in January 2021 created a window of opportunity. The stock's surge to $480 per share allowed the company to raise capital at inflated valuations, giving management runway to execute turnaround plans. When the stock inevitably crashed back to earth, the meme stock era ended. However, that capital raise was crucial to Game Stop's survival. The meme stock enthusiasm extended the company's lifespan by years, even though the business fundamentals continued deteriorating. So while the meme stock narrative didn't prove true (Game Stop didn't become a high-growth tech company), it provided enough resources for the company to attempt a new strategy.

How does Game Stop's situation compare to other retailers facing digital disruption?

Game Stop's situation is similar to what Best Buy, Barnes & Noble, and other retailers faced during digital disruption, but with important differences. Best Buy survived by downsizing while maintaining a strong omnichannel presence and building service-based revenue through Geek Squad. Barnes & Noble pivoted toward books as cultural experience and community gathering. Game Stop is primarily using aggressive cost-cutting without a clear new value proposition. Unlike Best Buy, which operates in electronics (broader category with more resilience), Game Stop is dependent on physical games, a category in structural decline. That makes Game Stop's path forward more difficult than what Best Buy faced.

What should employees and customers expect?

Employees in closing stores should expect job loss and the need to transition to other employment. The company offers severance, but it's not equivalent to continued wages. Customers should expect fewer locations and potentially reduced local availability of physical games and hardware. For collectors, niche gamers, and loyalty program members, Game Stop will likely continue operating, but with a smaller footprint and greater emphasis on online ordering and delivery. The customer experience will likely shift from browsing physical stores to online shopping and occasional special events at remaining locations.

Key Takeaways

Game Stop is closing 435 stores across 42 states as fiscal 2025 ends, reducing its US footprint by 18.7% and eliminating an estimated 6,000-8,000 jobs. The closures are driven by structural decline in physical game sales (caused by digital distribution, subscriptions, and cloud gaming), CEO Ryan Cohen's $35 billion options compensation package (which incentivizes aggressive cost-cutting to improve financial metrics), and the company's inability to build a viable alternative business model. While margin improvement through store closures might trigger short-term stock price appreciation, it masks underlying business deterioration. Game Stop is simultaneously winding down international operations and betting on a direct-to-consumer loyalty program that hasn't yet proven successful. The company faces three possible futures: stabilization as a small specialty retailer, bankruptcy and restructuring, or acquisition. None of these scenarios suggest a return to Game Stop's former dominance or size. The most likely outcome is continued contraction, either toward viability at a much smaller scale or toward financial distress. For employees and communities, the impact is immediate and negative. For shareholders and especially Cohen, the strategy might work financially if stock prices rise. But for Game Stop as a company, the current trajectory is simply managed decline, not turnaround.