How Disaster Preparedness Became Big Business: The Prepping Industry in 2025

Introduction: From Fringe Movement to Mainstream Market

When most people think of "preppers," they conjure images of extreme survivalists in remote compounds, obsessing over apocalyptic scenarios. But today's disaster preparedness market tells a far different story. Over the past two decades, what was once considered the domain of conspiracy theorists and doomsayers has evolved into a mainstream, multibillion-dollar industry that caters to everyone from suburban families worried about power grid failures to coastal homeowners concerned about hurricane preparedness. The shift reflects a fundamental change in how Americans view risk, resilience, and self-reliance in an increasingly unpredictable world.

The transformation didn't happen accidentally. It resulted from a convergence of factors: genuine increases in natural disasters and climate-related events, the rise of social media amplifying concerns about societal collapse, economic uncertainty following major recessions, and perhaps most significantly, the active participation of organized religious communities—particularly members of The Church of Jesus Christ of Latter-day Saints—who brought legitimacy, organizational sophistication, and sustained consumer bases to the industry.

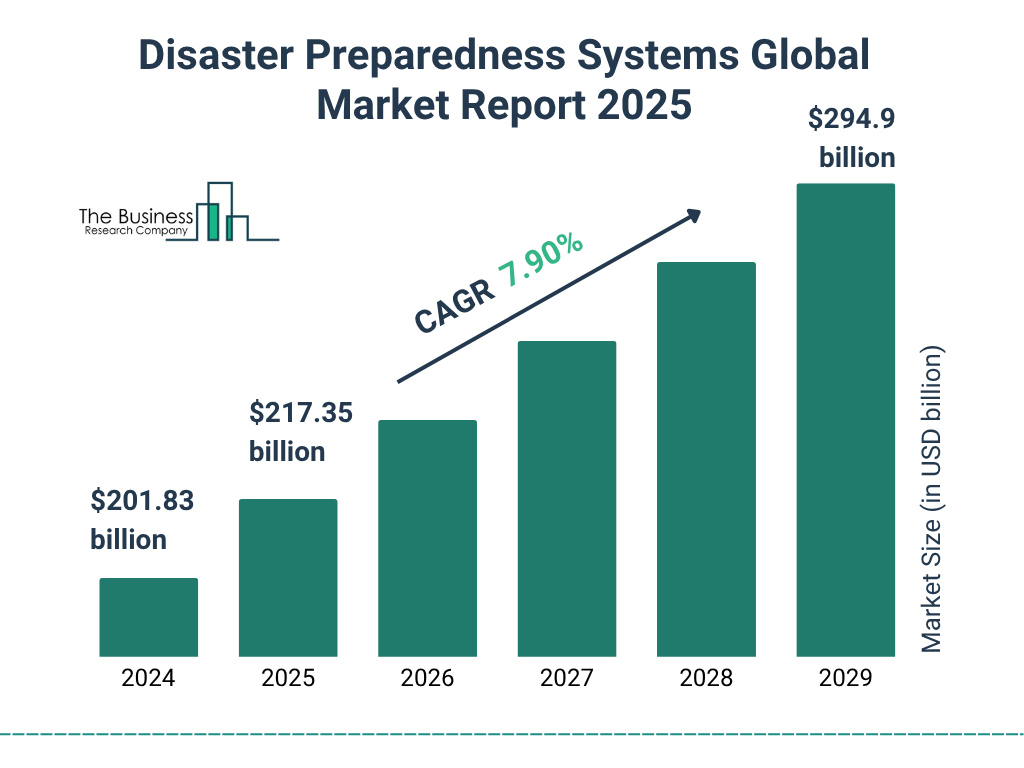

The prepping market has expanded from a niche focused on bunkers and canned goods into a sprawling ecosystem encompassing solar generators, water filtration systems, dehydrated food kits, communication devices, medical supplies, and digital preparedness apps. Market research indicates that the global disaster preparedness market was valued at approximately

Understanding this industry requires examining several interconnected narratives: the religious and cultural foundations that made prepping philosophically acceptable, the business innovations that brought preparedness products into the mainstream, the marketing strategies that normalized disaster preparation as a lifestyle choice rather than a symptom of paranoia, and the legitimate concerns about infrastructure resilience that drive consumer interest. This comprehensive analysis explores how disaster preparedness evolved from a fringe movement into a significant economic force, the key players dominating this space, the psychological factors driving consumer behavior, and what this trend reveals about American attitudes toward security, self-sufficiency, and institutional trust.

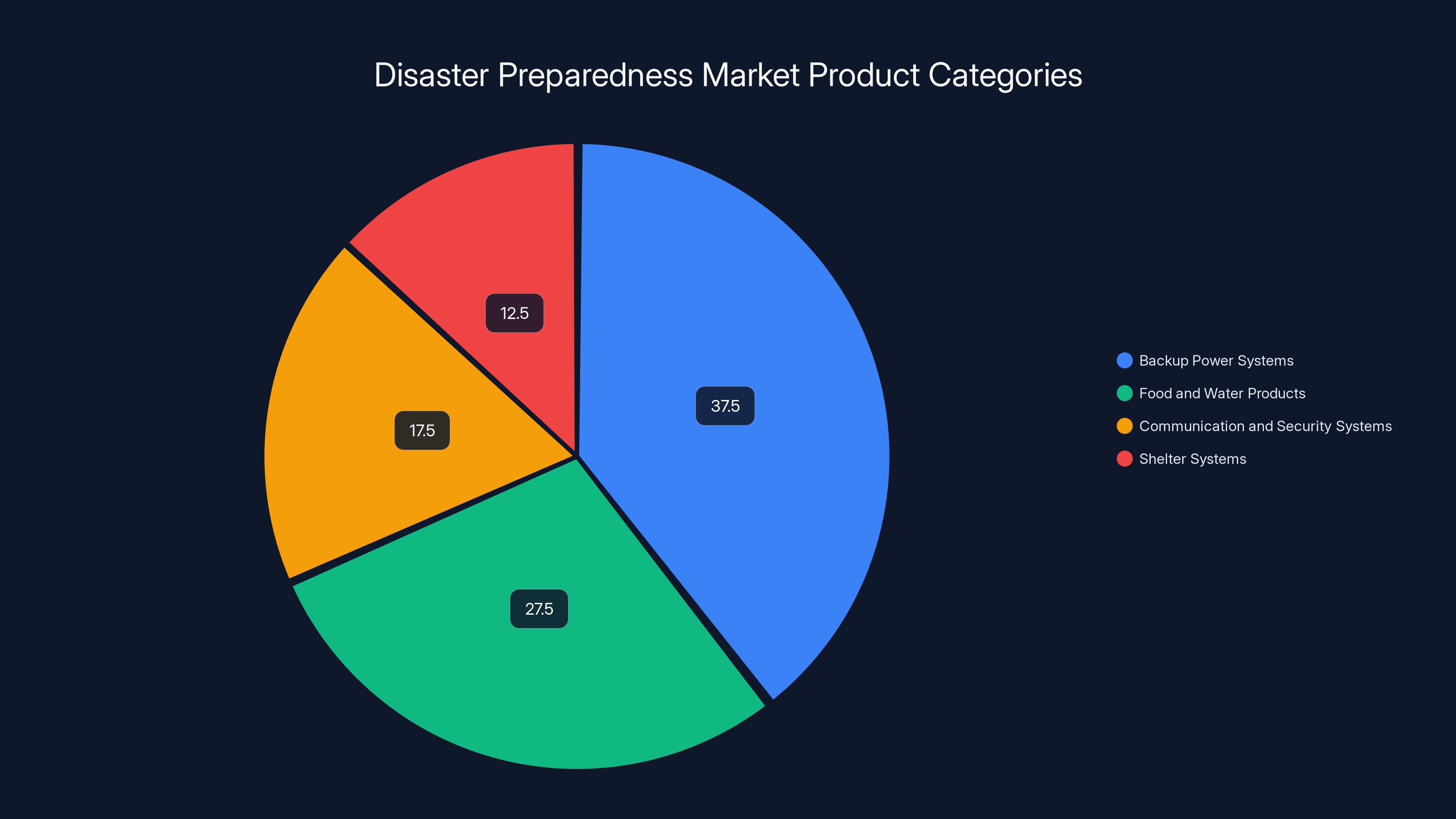

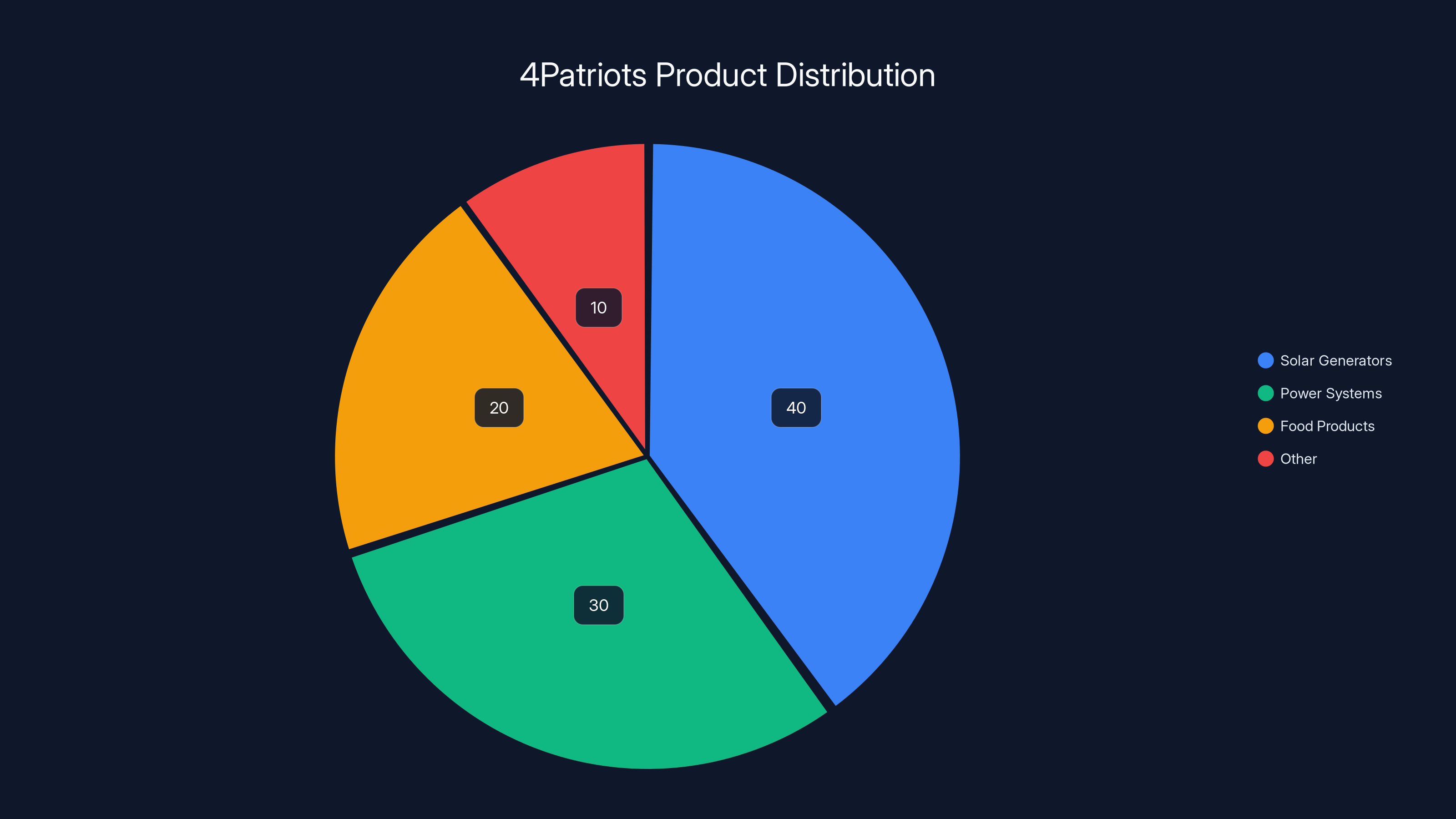

Backup power systems dominate the disaster preparedness market, accounting for approximately 37.5% of the market share, followed by food and water products at 27.5%. Estimated data.

The Religious Roots: How Mormon Theology Created a Consumer Base

The Doctrine of Self-Reliance and Preparation

The origin story of modern prepping in America begins not with doomsday prophets but with religious doctrine. Members of The Church of Jesus Christ of Latter-day Saints have maintained a formal preparation and self-reliance framework for over 150 years. The concept of being "Latter-day Saints"—saints living in the latter days before Christ's return—creates a theological imperative to prepare for significant upheaval. This isn't framed as paranoia but as spiritual responsibility.

The church's official teachings on preparedness are remarkably comprehensive. They emphasize maintaining at least a one-year supply of food, water, medicines, and personal hygiene items. Beyond emergency supplies, the doctrine extends to financial preparation, skill development, and what the church calls "temporal self-reliance." This theological framework has produced generations of Latter-day Saint families who view preparation not as optional paranoia but as fundamental religious practice. In practice, this means millions of families in the American West and increasingly across the country maintain stockpiles, develop self-sufficiency skills, and remain psychologically open to preparedness products and concepts.

The demographic concentration of this religious group in specific regions—particularly Utah, Idaho, and parts of Colorado—created geographic clusters of naturally receptive consumers. These areas also feature relatively high concentrations of engineers, technology professionals, and business-minded individuals, which proved crucial for transforming religious duty into commercial enterprise.

From Church Warehouses to Corporate Warehouses

What makes the Mormon connection to prepping unique is that an explicitly religious organization maintains significant infrastructure for disaster preparedness and food production. The Church of Jesus Christ of Latter-day Saints operates massive food production and storage facilities, farms, and distribution centers. These exist partially for humanitarian purposes but also to serve members' needs for preparedness products. For decades, church members could acquire bulk foods, water storage, and other supplies through official church channels, creating a captive, spiritually-motivated market.

However, the church's capacity couldn't meet growing demand, particularly as prepping trended beyond the religious community. This created a significant market opportunity. Entrepreneurs who understood both the theological motivations and the practical needs began establishing commercial enterprises to serve this market. Many of these founders were themselves Latter-day Saints with engineering backgrounds, business experience, and deep understanding of the values and concerns driving their potential customers. They could authentically communicate with this demographic while building companies that would eventually serve much broader markets.

The relationship between religious motivation and commercial expansion created a unique business dynamic. Early prepping companies could leverage authenticity with Mormon consumers while positioning themselves as mainstream solutions for all Americans concerned about preparedness. The religious underpinning provided initial legitimacy and a reliable customer base, while the broadening appeal created explosive growth potential.

Backup power systems dominate the disaster preparedness market with 37.5% share, followed by food and water products at 27.5%. Estimated data.

The Major Players: Industry Consolidation and Competition

4 Patriots: Engineering-Driven Preparedness

4 Patriots emerged as one of the industry's dominant forces through a combination of strategic positioning, product innovation, and sophisticated marketing. Founded by individuals with deep roots in the Mormon community and significant engineering expertise, the company built its reputation on solar generators, power systems, and food products specifically designed for the preparedness market. The company's headquarters near Salt Lake City and the presence of engineers like Tyler Stapleton (chief product engineer for off-grid power products) demonstrate how engineering talent concentrated in Utah's tech sector has been channeled into the preparedness industry.

The company's approach focuses on what company representatives frame as "energy independence"—a concept with both practical merit and aspirational appeal. Rather than emphasizing doomsday scenarios, 4 Patriots marketing emphasizes resilience against temporary grid failures, which have become increasingly common across the country. Solar generators, the company's flagship products, have genuine utility for camping, home backup power, and emergency situations. This real-world application makes the products less ideologically charged than older survival gear categories.

4 Patriots' product development reflects serious engineering ambition. The company invests in battery technology, solar efficiency, and portable power solutions. According to company claims, they have shipped over 5 million products to consumers over a three-year period, suggesting either very high market penetration or significant production volume across a broad product range. However, this scale also creates quality control challenges, as evidenced by consumer complaints regarding faulty water filters, defective generators, and potential food contamination issues.

Consumer Reports testing of a 4 Patriots 1,800-watt solar generator yielded a middling rating of 46 out of 100, suggesting the quality gap between marketed capabilities and actual performance. Additionally, a voluntary recall in 2016 involving several thousand generators due to fire hazards raised questions about quality assurance processes. Despite these challenges, the company maintains significant market position through aggressive marketing, competitive pricing, and products that serve genuine use cases beyond disaster scenarios.

My Patriot Supply: Warehouse-Scale Operations

My Patriot Supply represents a different approach to prepping market dominance—vertical integration and operational scale. The company operates massive warehouse facilities, with representatives indicating expansion from a 45,000-square-foot space pre-pandemic to a 428,000-square-foot facility by the early 2020s. This represents extraordinary scaling and suggests the company processes enormous volumes of dehydrated foods, water filtration systems, generators, and related products.

The company's aggressive marketing positioning against competitors—including labeling competitors as "fake patriots"—demonstrates intense competitive dynamics within the industry. This aggressive positioning reflects the zero-sum nature of market share in disaster preparedness, where brand loyalty and trust become paramount competitive factors. Consumers making preparedness purchases want to buy from vendors they perceive as reliable and authentic. The competitive claims suggest market pressures are driving increasingly polarized messaging.

My Patriot Supply's success appears driven by operational efficiency at scale, supply chain management capabilities, and aggressive digital marketing. The company has built significant market presence through social media, email marketing, and content marketing—converting general preparedness interest into committed customers. However, like 4 Patriots, the company has faced consumer complaints and quality control issues despite its massive operations.

Market Concentration and Industry Dynamics

The prepping industry is increasingly concentrated among a handful of major players, all with roots in Utah's Mormon community and all offering largely similar product assortments. Beyond 4 Patriots and My Patriot Supply, other significant players include e Foods Direct, Mother Earth Products, and regional competitors. The concentration of these companies in Utah reflects the historical convergence of religious motivation, engineering talent, and entrepreneurial opportunity.

The industry exhibits characteristics of winner-take-most markets. Marketing effectiveness and brand awareness become crucial competitive factors. This has driven increasing spending on digital advertising, social media marketing, and content creation designed to establish brand authority in preparedness. The competitive intensity appears to be increasing, with companies developing more sophisticated product lines, enhanced manufacturing capabilities, and more targeted marketing messages.

Market Size, Growth Projections, and Economic Impact

Current Market Valuation and Growth Trajectories

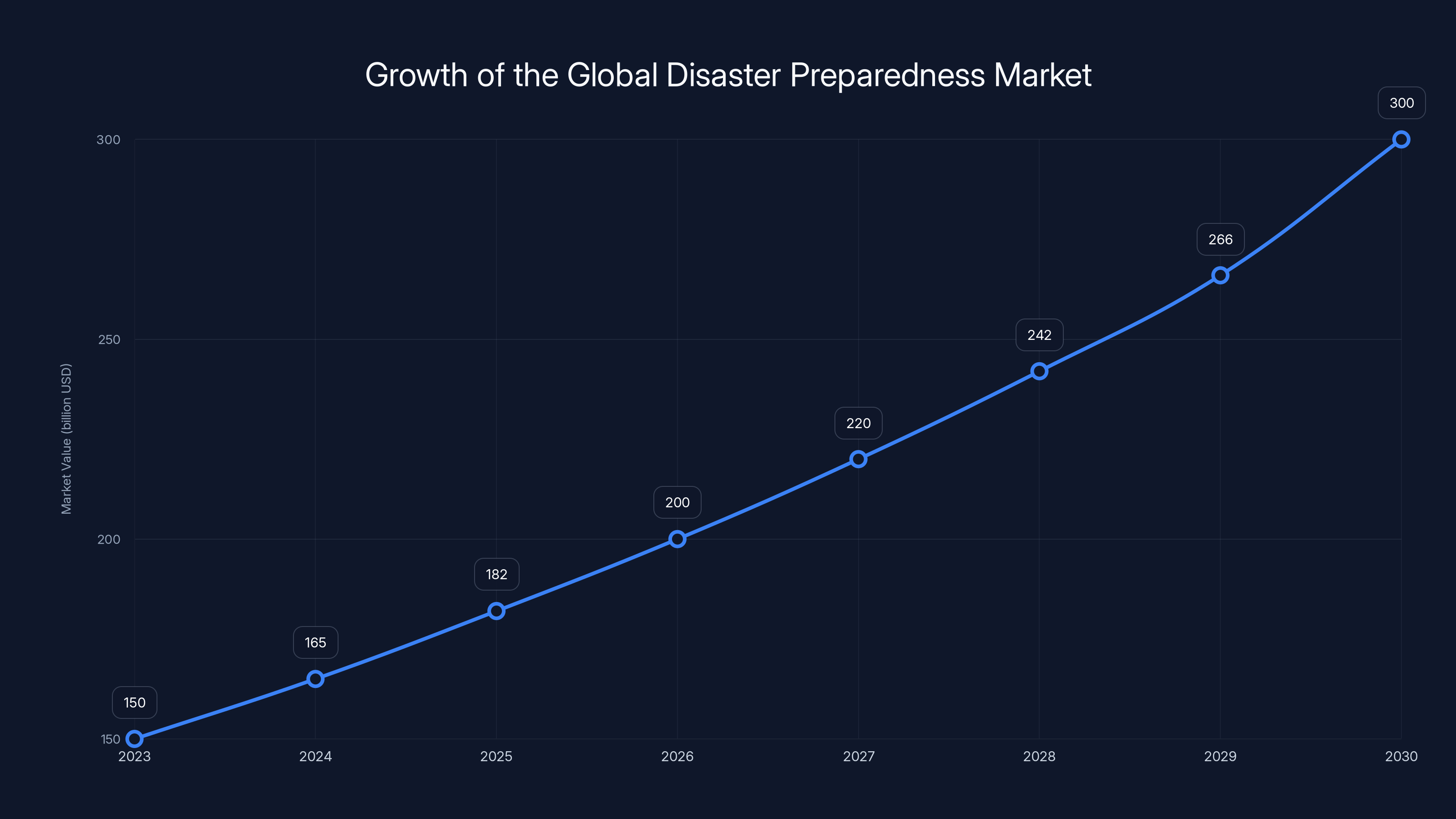

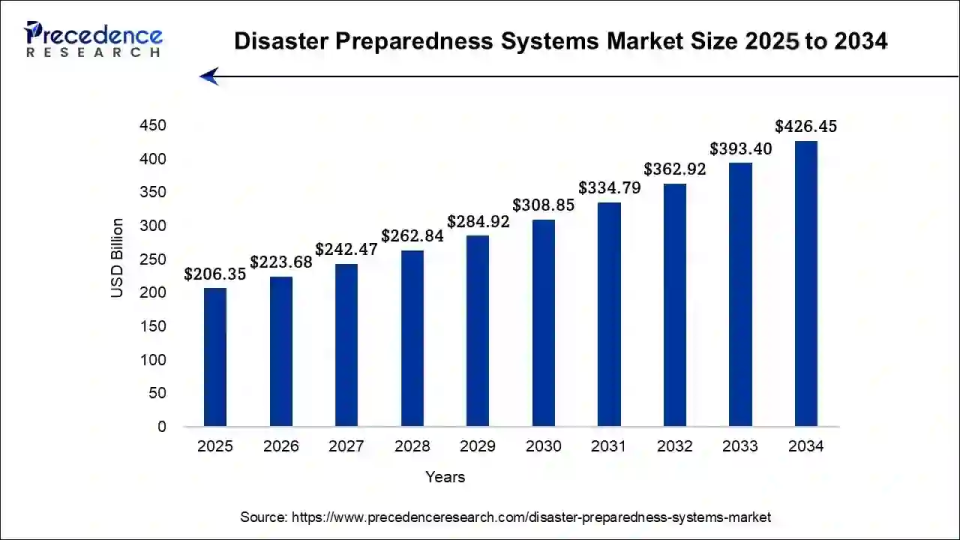

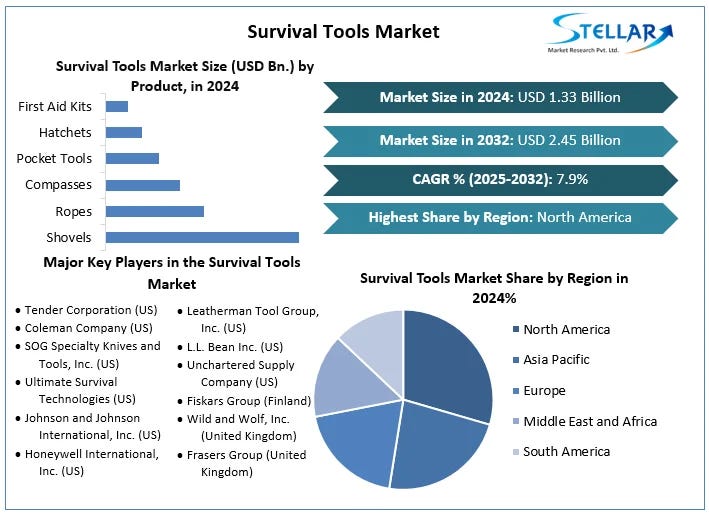

The disaster preparedness market represents one of the fastest-growing consumer sectors in contemporary America. Current market analysis suggests the industry was valued at approximately

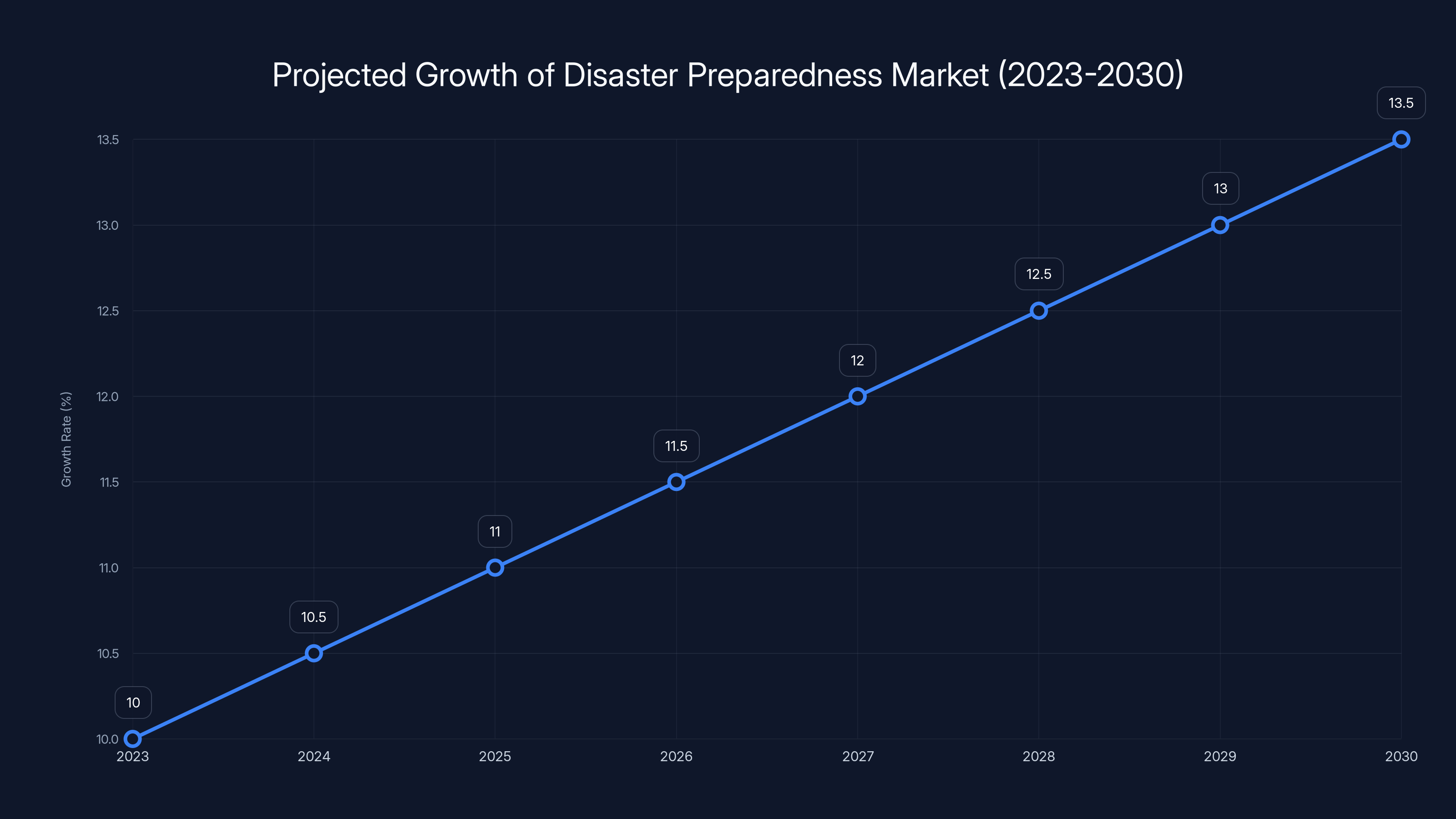

Market growth projections through 2030 consistently forecast expansion to $280-320 billion globally, representing a compound annual growth rate of 10-12%. This growth rate significantly exceeds general consumer goods growth and even outpaces technology sector growth. The acceleration is driven by several converging factors: increasing frequency and severity of weather-related disasters, visible infrastructure failures in major metropolitan areas, political and economic uncertainty, and the demonstrated success of preparedness marketing in normalizing disaster preparation as a mainstream consumer behavior.

Breakdown by product category reveals interesting market dynamics. Backup power systems (generators, solar power, batteries, inverters) represent approximately 35-40% of total market value and are the fastest-growing segment with 13-15% annual growth. Food and water products represent 25-30% of market value with more modest 8-10% annual growth as the market matures. Communication devices and security systems represent 15-20% of market value with 12-14% annual growth driven by technological advancement and new use cases. Shelter and structural systems (bunkers, safe rooms, generators) represent 10-15% of market value with variable growth rates.

The economic impact extends beyond direct consumer spending. The prepping industry has created significant employment in manufacturing, logistics, marketing, and distribution. Warehouse operations like My Patriot Supply's 428,000-square-foot facility require hundreds of employees for storage, packing, and logistics management. Manufacturing facilities in Utah and other regions employ engineers, technicians, and production workers. Digital marketing agencies have built entire service divisions around preparedness marketing. The industry has become economically significant at both regional and national levels.

Seasonal Patterns and Consumer Spending Dynamics

Preparedness market analysis reveals distinct seasonal patterns in consumer spending. Spending typically peaks in late summer (July-August) preceding hurricane season and in early fall (September-October) after significant weather events occur. Following major disasters—hurricanes, wildfires, or winter storms—affected regions experience 300-500% increases in preparedness product searches and purchases. These patterns demonstrate that disaster preparedness purchases are significantly influenced by current events and visible risks.

Interestingly, preparedness spending also shows increasing baseline levels year-round, suggesting the market is transitioning from purely event-driven behavior to more constant consumer interest. This is partially attributable to successful marketing normalization of preparedness as a responsible consumer behavior rather than an extreme lifestyle choice. The shift represents a maturation of the market from novelty to normalized consumer category.

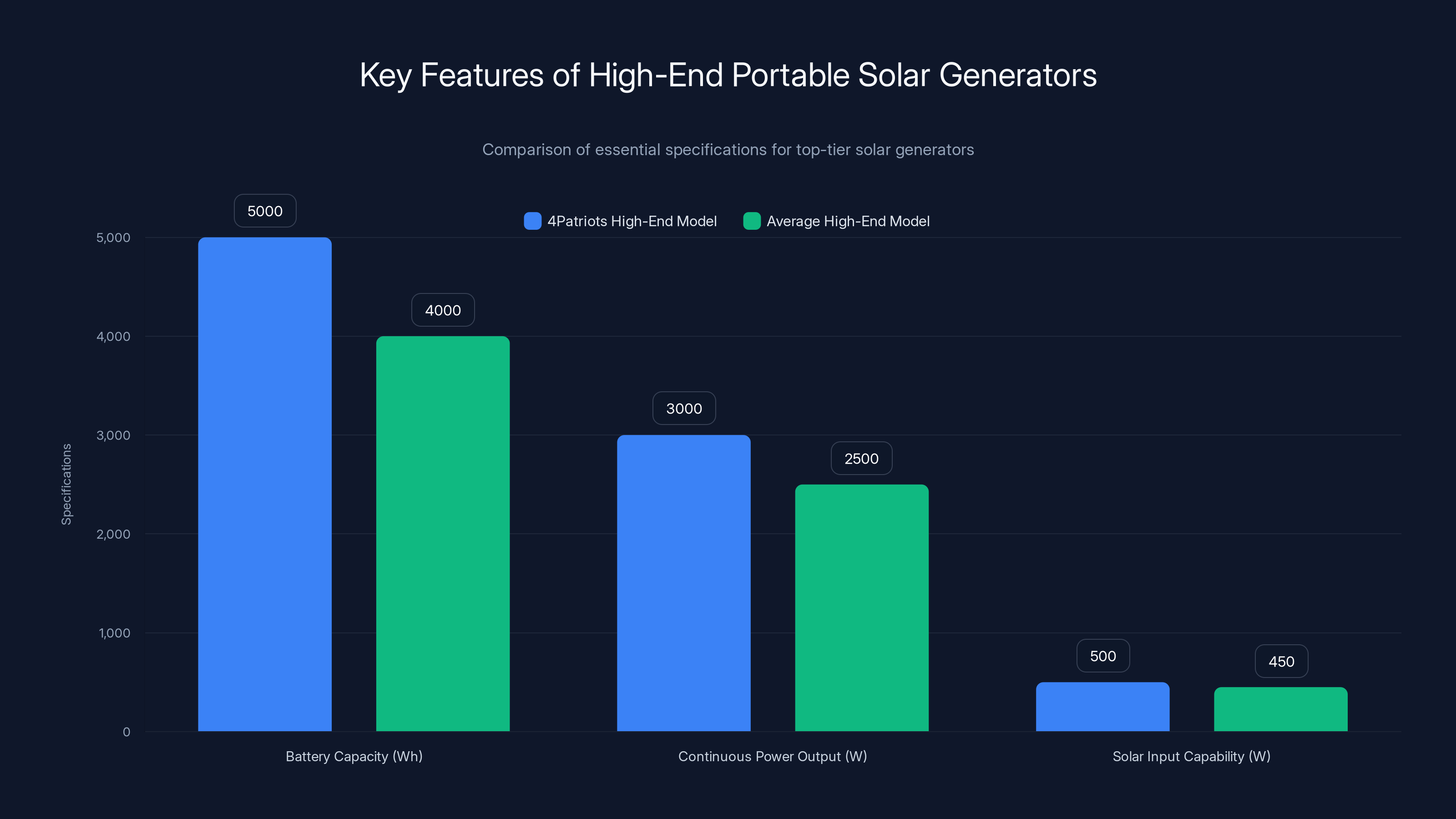

High-end portable solar generators offer significant battery capacity, power output, and solar input capabilities, making them suitable for various applications from home backup to off-grid recreation. Estimated data based on typical high-end models.

The Psychology of Fear and Marketing: How Anxiety Became Commerce

Cognitive Biases in Risk Perception

The explosive growth of the preparedness industry reflects fundamental aspects of human psychology around risk, uncertainty, and control. Psychologists identify several cognitive patterns that drive preparedness spending, particularly in contemporary environments characterized by visible infrastructure challenges and mediated catastrophe awareness.

Availability heuristic significantly influences preparedness spending. When individuals are exposed to media coverage of disasters—particularly disasters that appear preventable through personal action—they tend to overestimate the probability of experiencing similar events. Extensive media coverage of power grid failures, wildfires destroying homes, or water contamination creates vivid, accessible examples in people's minds, increasing perceived risk. This psychological mechanism isn't irrational; it's an adaptation to environments where catastrophic risks are genuinely present. However, it can drive purchasing behavior that exceeds rational risk assessment.

Illusion of control motivates significant spending on preparedness products. Individuals feel psychological comfort when they believe they can take action to mitigate risks, even when the actual risk reduction is marginal. Purchasing a backup generator doesn't substantially reduce the probability of grid failure, but it creates a sense of personal agency and control. This psychological benefit, independent of practical protection value, drives consumer willingness to pay substantial sums for preparedness products. The sense of personal preparation creates measurable psychological comfort and reduced anxiety.

Social proof and conformity bias have become increasingly important as preparedness transitions to mainstream consumer behavior. When preparedness moves from fringe concern to normalized behavior—when neighbors, coworkers, and social media connections discuss their preparedness planning—individual resistance to preparedness spending decreases. The behavior becomes normalized rather than eccentric. This creates self-reinforcing market growth patterns where media coverage drives consumer awareness, which drives purchases and testimonials, which drives additional media coverage.

Marketing Strategies and Narrative Framing

Successful preparedness companies have developed sophisticated marketing strategies that emotionally engage consumers while maintaining plausible deniability about fear-mongering. Rather than explicitly emphasizing catastrophic scenarios, modern preparedness marketing frames disaster preparation as "responsible family planning" or "energy independence." This subtle reframing makes preparedness consumption feel responsible rather than paranoid.

Multi-channel marketing campaigns combine digital advertising, social media content, email marketing, and affiliate partnerships to create comprehensive brand presence. Companies produce content that educates consumers about specific risks ("Hurricane Season Preparation Guide," "Backup Power for Home Medical Equipment") while subtly reinforcing the message that professional preparedness solutions provide the optimal response. This content marketing approach builds authority and trust while driving purchase intent.

Influencer marketing and testimonial campaigns leverage customers who visibly benefit from preparedness products. When prepared customers share their experiences during actual power outages or weather events, it provides authentic evidence of product value. These testimonials become more persuasive than direct advertising because they come from peers rather than companies with obvious commercial interests.

Social media algorithms amplify preparedness content in ways that exacerbate fear and concern. Users showing interest in preparedness-related content receive increasingly concentrated exposure to similar content, creating filter bubbles where disaster and catastrophe concerns become normalized and dominant. Preparedness companies leverage these algorithmic dynamics through targeted advertising and viral content strategies designed to maximize algorithmic distribution.

The Ethical Dimensions of Preparedness Marketing

The relationship between legitimate disaster preparedness and fear-based marketing remains contentious. Genuine risks exist—grid failures, water contamination, extreme weather, and infrastructure vulnerabilities are real problems affecting real communities. Preparedness products address genuine needs. However, the question remains whether marketing strategies sometimes amplify fears beyond warranted levels to drive incremental consumption.

Evidence suggests marketing strategies sometimes cross from risk-awareness into fear-amplification. Companies face incentive structures that reward alarming content, crisis-focused messaging, and increasingly extreme preparedness scenarios. A company marketing reasonable hurricane preparedness faces less growth potential than a company marketing comprehensive societal collapse scenarios. This creates structural incentives toward escalating fear narratives.

Consumer protection agencies and the Better Business Bureau have received complaints suggesting some preparedness companies engage in deceptive marketing practices—making performance claims about products that don't materialize, overselling capabilities, and using fear-based pressure tactics to drive purchases. While complaints don't prove systematic fraud, they suggest industry practices sometimes cross ethical boundaries in pursuit of sales growth.

Product Categories and Innovation: From Canned Goods to Smart Systems

Backup Power and Energy Independence

Backup power represents the fastest-growing and highest-value segment of the preparedness market. This growth reflects genuine infrastructure challenges, the falling cost of battery and solar technology, and legitimate consumer interest in energy independence beyond disaster scenarios. Solar generators—portable power systems combining lithium batteries, solar panels, and inverter technology—represent the category's apex product.

These systems offer genuine utility for multiple use cases. Homeowners use them for backup during grid outages. Campers use them for off-grid recreation. Homesteaders use them to reduce utility bills and achieve partial energy independence. This multi-use application creates broader consumer interest than purely disaster-focused products. The technological improvements in battery capacity, charging speed, and system efficiency reflect genuine engineering advancement rather than marketing hype.

Market leaders like 4 Patriots compete intensely on product features: charging speed, battery capacity (measured in watt-hours), solar input capability, and form factor. A high-end portable solar generator system might feature 3000-5000 watt-hours of battery capacity, 2000-3000 watts of continuous power output, and 400+ watts of solar input capability. These specifications allow operation of essential home appliances during extended outages. The technology directly descends from innovations developed by Tesla and other battery manufacturers who created these capabilities for automotive and grid storage applications.

However, quality control challenges emerge at scale. Generators failing due to electrical defects, batteries degrading faster than specifications suggest, and power output falling short of claims represent common complaints in consumer reviews. The gap between engineering specifications and real-world performance in consumer-grade devices remains a persistent industry challenge.

Water Filtration and Purification

Water represents humanity's most critical survival need—roughly 5-7 days without water produces fatal dehydration. Water filtration products have become essential components of preparedness kits. The category includes pitcher-style filters, portable filtration systems, and large-scale purification solutions. The market has expanded from basic carbon filters to sophisticated systems including reverse osmosis, ultraviolet purification, and multi-stage filtration designed to handle diverse contamination scenarios.

Leading preparedness companies offer filtration systems claiming to eliminate bacteria, viruses, parasites, and chemical contaminants from various water sources. The effectiveness of these systems varies significantly based on initial water quality, maintenance, and specific contaminants present. Consumer complaints about faulty filters that fail to reduce contamination to claimed levels or that clog excessively suggest quality control challenges in this category as well.

Water storage represents a complementary market. Guidelines from the Federal Emergency Management Agency recommend 1 gallon per person per day for a minimum of 3 days, which for a family of four means maintaining 12+ gallons of stored water. This requires dedicated storage space and rotation to prevent contamination. Preparedness companies have developed space-efficient water storage solutions, from collapsed bladders that expand for use to modular storage systems designed to integrate with home infrastructure.

Dehydrated and Freeze-Dried Foods

Food products represent the longest-established category in the preparedness market, tracing back decades before prepping became mainstream. However, the category has evolved dramatically. Rather than basic survival foods emphasizing shelf-life over taste, modern preparedness companies offer diverse, palatable meal options designed to appeal to mainstream consumers.

Market leaders have transitioned from canned goods toward dehydrated and freeze-dried food products that offer longer shelf life, lighter weight, and superior nutritional retention compared to traditional canned goods. These products require only water and heat to prepare, making them suitable for scenarios where conventional cooking isn't possible. The category has expanded to include diverse cuisines and meal types—not just survival rations but familiar foods in convenient preserved formats.

Consumer complaints about food products reveal quality and safety concerns. Reports of insect contamination, spoilage despite claimed shelf-life, and questionable food safety practices suggest some companies cut corners in sourcing or storage practices. The Federal Food and Drug Administration has investigated preparedness food companies, and recalls have occurred for various products. This reveals a gap between marketing claims about food safety and storage duration versus actual product performance.

Communication and Security Systems

Modern preparedness has expanded into communication and security domains. Products in this category include satellite messengers (devices that transmit messages without cellular coverage), emergency radios, backup phone charging systems, and water purification systems designed for emergency scenarios. As more people become concerned about cellular infrastructure failures or internet outages, demand for communication independence has grown.

Two-way radios and satellite messengers represent high-value products addressing specific vulnerabilities. Personal locator beacons and satellite messengers from manufacturers like Garmin provide emergency communication capabilities when standard infrastructure fails. These products have legitimate utility beyond preparedness—outdoor enthusiasts, boaters, and remote workers use them routinely. The crossover between mainstream functionality and preparedness appeal has expanded this market category.

The global disaster preparedness market is expected to double from

The Infrastructure Reality: Are Concerns About Grid Failure and Contamination Justified?

Power Grid Vulnerabilities and Increasing Outages

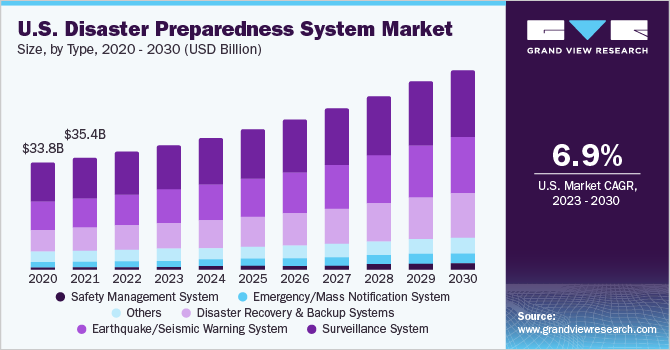

The motivation driving backup power purchases isn't purely psychological. The American electrical grid has demonstrated increasing vulnerability to various disruption sources. Data from the Department of Energy indicates that power outages affecting 50,000+ customers have increased from approximately 15-20 annually in the 1980s to 30-40 annually in recent years. These major outages cause cascading economic damage, disrupt essential services, and create genuine hardship for affected communities.

Climate change appears to be increasing outage frequency and severity. Extreme heat, severe winter storms, and hurricane activity have all caused significant grid failures. The 2021 Texas winter storm that failed to winterize the grid caused rolling blackouts affecting millions. The 2020 Derecho in Iowa downed transmission lines across a wide geographic area. California's rolling blackouts during extreme heat in 2020-2022 demonstrated grid capacity limitations during peak demand periods. These aren't theoretical concerns but documented failures affecting millions of people.

Beyond weather-related failures, the grid faces aging infrastructure challenges. Significant portions of American electrical infrastructure date to the 1960s-1980s and are reaching or exceeding design lifespans. The American Society of Civil Engineers rates electrical infrastructure conditions as "C-plus," indicating moderate deterioration. Upgrading this infrastructure requires massive capital investment that utility companies have been slow to implement. This aging infrastructure becomes increasingly vulnerable to various disruption mechanisms.

The grid also faces cybersecurity vulnerabilities. As grid operations become increasingly digital, they become susceptible to digital attacks. A 2015 incident in Ukraine demonstrated that coordinated cyberattacks could cause widespread power outages. While the American grid has significant security protections, vulnerabilities almost certainly remain. The potential for attacks—whether by foreign actors, domestic extremists, or common criminals—represents a genuine risk vector that backup power mitigates.

Water Quality and Contamination Risks

Water contamination represents another genuine concern motivating filtration product purchases. The Flint, Michigan water crisis demonstrated how municipal water systems can fail to protect public health due to corrosion of water infrastructure and inadequate treatment. Lead contamination from aging water pipes affects many American communities. Chemical contamination from industrial activity, agricultural runoff, and legacy pollution affects water systems across the country.

Several factors increase water contamination risks. Climate change increases flooding that can overwhelm water treatment systems and contaminate supplies. Aging water infrastructure—like electrical infrastructure—requires massive capital investment to replace. Drought can concentrate contaminants in water supplies. Industrial activity near watersheds can introduce chemicals. These aren't speculative risks but documented problems affecting real communities.

The Environmental Protection Agency tracks water contamination incidents, and the data suggests various water systems regularly experience quality challenges. While major cities maintain relatively robust water treatment and distribution systems, many smaller communities operate on aging infrastructure with limited redundancy. Private wells, which serve roughly 20% of American households, lack the treatment systems of municipal supplies and are vulnerable to bacterial and chemical contamination.

Climate Change and Disaster Frequency

Disaster preparedness concerns are rooted in documented increases in severe weather events and climate change impacts. The data unambiguously shows increasing frequencies of extreme heat events, severe storms, and in some regions, drought conditions. The National Oceanic and Atmospheric Administration reports that extreme weather events have increased significantly since the 1980s, with 2020-2023 featuring record-breaking severe weather activity in the United States.

Insurance industry data provides compelling evidence of increasing disaster costs. Property and casualty insurers report continuously increasing claims from weather-related disasters. Multiple insurers have exited certain markets due to unsustainable loss ratios. This suggests genuine increases in risk, not merely perception. When profit-driven businesses reduce exposure to specific risks, it indicates those risks are increasing and becoming more costly.

Consumer Demographics and Market Segmentation

The Primary Preparedness Market

Market analysis reveals distinct demographic profiles of preparedness consumers. Contrary to common stereotypes, the primary market isn't exclusively rural, ideologically extreme, or economically marginal. Instead, the market spans multiple demographic segments with different motivations and purchasing patterns.

Affluent suburban homeowners represent a significant and growing market segment. These consumers, typically with household incomes exceeding $100,000, purchase preparedness products as part of broader home security and resilience investments. They install backup generators, water storage systems, and power backup solutions alongside home security systems and emergency medical equipment. Their motivation combines practical protection against specific risks they perceive as likely (power outages, storm damage) with insurance-like psychological peace of mind. This segment has expanded dramatically as preparedness has become normalized among upper-middle-class suburban communities.

Homeowners in disaster-prone regions represent another major market segment. Residents of coastal areas prone to hurricanes, western regions prone to wildfires, and areas with geological hazards naturally gravitate toward preparedness products. For these consumers, preparedness isn't paranoia but rational response to visible, recurring risks. This segment shows particularly strong demand following major disaster events that affect their regions.

Off-grid and rural homeowners have always represented a core preparedness market segment. These consumers purchase backup power and water systems out of practical necessity rather than disaster concern. Rural areas often lack reliable grid access and municipal water systems, making independent power and water systems essential rather than optional. This segment's purchasing is driven by utility considerations rather than disaster anxiety.

Technology enthusiasts and "early adopters" represent another demographic segment increasingly entering the preparedness market. For these consumers, backup power systems represent interesting technology applications combining renewable energy, battery innovation, and smart control systems. This segment purchases based on technological specifications and capabilities rather than disaster concerns. The positioning of solar generators alongside camping and outdoor equipment appeals to this demographic.

Secondary and Growing Market Segments

Beyond primary segments, preparedness products increasingly appeal to broader consumer bases. Climate-conscious consumers concerned about reducing carbon footprint and achieving energy independence represent a growing segment. Homeowners managing chronic health conditions requiring power-dependent medical equipment purchase backup systems out of practical necessity. Outdoor recreation enthusiasts purchase portable power and water systems for camping and remote activities. This diversification of consumer motivation and demographic characteristics has driven market expansion beyond traditional preparedness markets.

Geographic analysis reveals concentrated preparedness markets in specific regions. The Intermountain West (Utah, Idaho, portions of Colorado and Wyoming) shows the highest per-capita preparedness spending, driven by the concentrated Mormon population and associated cultural values around self-reliance. The Pacific Coast (California, Oregon, Washington) shows strong preparedness markets driven by earthquake, wildfire, and storm concerns. The Atlantic and Gulf Coasts show strong demand driven by hurricane risks. Midwestern regions show moderate preparedness spending except in areas prone to tornado activity. This geographic variation suggests preparedness consumption is significantly driven by perceived local risks rather than uniform cultural attitudes.

Estimated data shows solar generators as the leading product category, comprising 40% of 4Patriots' shipments, followed by power systems and food products.

Quality Control Challenges and Consumer Protection Issues

Product Reliability and Performance Gaps

As the preparedness industry has expanded, quality control challenges have become increasingly apparent. The sector attracts entrepreneurs and venture capital seeking high-growth market opportunities, but not all entrants maintain rigorous quality standards. Consumer complaints reveal recurring patterns of product failures contradicting marketing claims.

Backup power systems receive complaints about battery degradation, electrical defects, and power output falling significantly short of specifications. Lithium battery technology is complex, and quality control requires sophisticated testing and manufacturing processes. Some manufacturers source cells from questionable suppliers or cut corners in circuit design, resulting in systems that fail when needed. Reports of generators that overload under moderate loads, stop charging properly after limited cycles, or develop dangerous electrical faults suggest systematic quality issues in some product lines.

Water filtration systems receive complaints about contamination failing to meet claimed removal rates, filters degrading quickly and becoming impossible to clean, and systems breaking down after limited use. The complexity of multi-stage filtration systems and the variety of possible contaminants creates challenges for manufacturers in ensuring products function across diverse scenarios. Some complaints suggest companies make overly broad contamination claims their products can't actually achieve.

Food products receive complaints about contamination despite claimed preservation, taste quality failing to match descriptions, and actual shelf-life falling short of claimed storage duration. Food safety requires rigorous manufacturing and storage protocols. Evidence suggests some companies fail to maintain these standards, resulting in products that spoil or become contaminated despite marketing claims.

Regulatory Environment and Oversight Gaps

The preparedness industry operates in a regulatory environment with significant gaps. Backup power systems fall under various regulations (electrical codes, product safety standards) but oversight is fragmented across federal agencies and state regulators. The Food and Drug Administration oversees some preparedness foods but has limited capacity to test all products. Water filtration systems lack comprehensive federal certification requirements, allowing companies to make claims difficult to verify.

The Better Business Bureau has received numerous complaints against preparedness companies. My Patriot Supply maintains a Better Business Bureau rating of approximately B to B+, while 4 Patriots maintains a rating in similar range. These ratings suggest moderate consumer satisfaction but persistent complaint patterns that haven't been fully resolved. Common complaints include difficulty obtaining refunds, shipping delays, and billing issues alongside product quality concerns.

Class action lawsuits have been filed against preparedness companies in some cases, alleging deceptive marketing, misrepresentation of product capabilities, and consumer fraud. While the legal outcomes remain mixed and many cases haven't reached final resolution, they suggest systematic patterns of complaints that extend beyond isolated consumer dissatisfaction.

Improving Quality Standards

Industry leaders are beginning to implement more rigorous quality standards and third-party testing. Manufacturers working with Consumer Reports and other independent testing organizations are subjecting products to rigorous evaluation. Some companies have begun implementing more rigorous manufacturing standards and supply chain audits. The industry is gradually professionalizing, though significant quality variation remains between market leaders and smaller competitors.

Consumer advocacy organizations recommend that preparedness product purchasers: conduct independent research on specific products rather than relying on manufacturer claims; read verified customer reviews on independent platforms; look for products that have undergone third-party testing; verify warranty terms and return policies; and begin with pilot purchases of smaller quantities before committing to large bulk orders. These practices help mitigate quality control risks that remain endemic to the industry.

Digital Transformation and the Future of Preparedness

Mobile Apps and Digital Planning Tools

The preparedness market is expanding into digital tools and software platforms complementing physical products. Mobile applications guide users through emergency planning, track supply inventories, provide real-time disaster information, and maintain digital records of important documents. Companies like Ready.gov (a Federal Emergency Management Agency initiative) and various private preparedness apps provide digital frameworks for household disaster planning.

These digital tools address a genuine need—most households lack formal emergency plans, don't know what supplies they actually possess, and struggle to maintain important documents in ways accessible during emergencies. Digital solutions make disaster planning accessible and systematic. The market for preparedness planning software and apps is growing at 15-20% annually, faster than traditional product markets.

Integration between physical products and digital systems is advancing. Smart backup power systems now include mobile app controls allowing users to monitor battery levels, power consumption, and system performance in real-time. This data-driven approach appeals to technology-oriented consumers and provides genuine value by optimizing system usage and alerting users to potential problems.

Internet of Things and Smart Preparedness Systems

The convergence of preparedness products with Internet of Things (Io T) technology creates opportunities for integrated smart systems. Backup power systems connected to home automation platforms can automatically prioritize essential loads during power outages, manage power distribution intelligently, and provide real-time status monitoring. Water systems can monitor quality and alert users to contamination risks. Security systems can integrate with backup power to maintain operation during grid outages.

These integrated approaches appeal to consumers willing to invest in comprehensive home resilience systems. Smart home integration makes backup power seamlessly part of home infrastructure rather than a visibly separate emergency item. This normalization process contributes to mainstream adoption of preparedness technology.

Artificial Intelligence and Predictive Preparedness

Emerging applications of artificial intelligence to disaster preparedness include predictive modeling that identifies specific household vulnerabilities and recommends targeted preparedness investments. AI analysis of household characteristics, geographic location, and historical disaster patterns can generate customized preparedness recommendations rather than generic guidance. This personalization increases relevance and purchase intent while helping consumers make more informed investment decisions.

Data analytics applied to preparedness product performance provides valuable feedback loops. Companies collecting anonymized data on product failure rates, usage patterns, and performance under real conditions can continuously improve product design and manufacturing. This data-driven improvement cycle has potential to address quality control challenges that currently plague the industry.

The disaster preparedness market is projected to grow steadily at an annual rate of 10-13.5% through 2030, driven by increasing disaster events and climate change impacts. Estimated data.

Regulatory Framework and Government Initiatives

Federal Disaster Preparedness Guidance

The Federal Emergency Management Agency and other federal agencies provide guidance on disaster preparedness. A 2023 Federal Emergency Management Agency survey found that 51% of Americans reported being "prepared for a disaster" in some way. This baseline provides a market anchor—the government has established preparedness as a public health priority, legitimizing preparedness products and services.

Federal guidance emphasizes household emergency planning, supply stockpiling, and infrastructure resilience. These themes align closely with preparedness company messaging, creating synergy between government objectives and commercial interests. However, government guidance emphasizes basic preparedness (72-hour emergency kits, family communication plans) while commercial products push toward comprehensive household resilience requiring significantly larger investments.

State and Local Regulations

State and local governments have increasingly developed disaster preparedness initiatives and in some cases have provided incentives for residential preparedness investments. Tax credits, rebates, and utility company incentive programs for residential solar and backup power systems have proliferated in recent years. These programs simultaneously promote energy resilience, accelerate clean energy adoption, and create market expansion for preparedness products.

California and other states with significant natural disaster risks have developed comprehensive preparedness initiatives. These initiatives don't explicitly advocate for private preparedness products but create environments where preparedness becomes normalized and government resources are stretched toward community-scale rather than household-scale preparedness. This creates market opportunities for private sector solutions addressing household-level resilience needs.

International Perspectives

Disaster preparedness markets are developing in other countries, though the intensity varies significantly based on natural hazard exposure and cultural factors. Japan, with significant earthquake and typhoon risks, has developed substantial preparedness markets. New Zealand, Australia, and other disaster-prone regions show strong preparedness markets. However, the integration of religious motivations with commercial preparedness markets is relatively unique to the Mormon-influenced American context.

Environmental and Sustainability Considerations

Resource Consumption and Manufacturing Impact

The preparedness industry's rapid growth creates environmental considerations worth examining. Producing millions of backup power systems, water storage containers, and food products consumes substantial raw materials and energy. Battery manufacturing—central to backup power systems—requires mining for lithium, cobalt, and other materials with associated environmental and social impacts. The scale of preparedness product manufacturing represents significant resource consumption.

Additionally, the preparedness industry contributes to consumer culture patterns of accumulating possessions. Storage of stockpiled goods requires home space, potentially driving larger home construction. Replaced or discarded preparedness products contribute to electronic waste (particularly batteries and electronic devices) and other waste streams. The environmental footprint of household-scale preparedness systems deserves more thorough analysis than it currently receives.

Renewable Energy Alignment

Backup power systems, particularly solar generators and solar + battery systems, align with renewable energy and carbon reduction objectives. Consumers purchasing solar-powered backup systems simultaneously reduce reliance on grid electricity and fossil fuel consumption. This convergence between preparedness needs and environmental objectives has been remarkably successful in driving solar product adoption and market growth.

However, the preparedness framing can obscure more practical approaches to energy resilience. A consumer motivated by preparedness concerns might purchase an expensive portable solar system, while a more cost-effective approach would involve home solar installation (providing continuous benefit) plus modest battery storage. The preparedness framing sometimes drives less economically rational purchasing than pure energy resilience planning would produce.

Lifecycle and Circular Economy Considerations

Preparedness products have extended lifecycles as they're consumed slowly or maintained for extended periods. A backup generator purchased for emergency use might sit unused for years or decades. This extended lifecycle without usage differs from typical consumer products with regular use patterns. The environmental implications are complex—stored products consume no energy through use but do consume embodied energy in manufacturing and transportation.

Recirculation and reuse of preparedness products remains underdeveloped. Most consumers either exhaust stockpiled foods or discard spoiled goods rather than redistributing to other users. Backup power systems accumulate in households after technology obsolescence but aren't routinely recycled. Greater focus on product lifecycle management and circular economy approaches to preparedness could reduce environmental impact while improving economic efficiency.

Socioeconomic Dimensions and Equity Concerns

Access and Affordability Challenges

Preparedness products vary enormously in cost, from inexpensive (

Federal and state disaster assistance programs provide support following disasters, but preventive preparedness remains primarily a private responsibility. This creates a form of preparedness inequality where wealthier households invest in protective infrastructure while lower-income households depend on public sector response and assistance. This pattern has become particularly apparent following major disasters affecting low-income communities with limited private preparedness investments.

Preparedness as Social Status

As preparedness has moved into mainstream consumer markets, it has acquired elements of status consumption. High-end solar systems, sophisticated backup power solutions, and premium preparedness products have become status markers among affluent consumers. This transformation of practical preparedness into consumption signaling further distances preparedness from lower-income consumers who lack the economic capacity for status-level preparedness investments.

This dynamic creates distinct preparedness cultures where affluent communities have invested substantially in household resilience while vulnerable communities remain dependent on public sector response capacity that may be insufficient during major disasters. The 2021 Texas winter power crisis exemplified this dynamic—affluent households with backup power maintained comfort and safety while vulnerable populations suffered in homes without heat or clean water.

Community-Scale Preparedness

Public health and disaster preparedness experts increasingly emphasize community-scale preparedness as potentially more effective and equitable than household-scale approaches. Community-scale approaches involve shared resources, mutual aid frameworks, and public infrastructure resilience. However, these community approaches receive significantly less policy attention and investment than household-scale preparedness promoted through private markets.

The emphasis on household-scale preparedness through market-based solutions creates uneven resilience where wealth determines disaster recovery capacity. Alternative approaches emphasizing community resilience, mutual aid, and public infrastructure investment might produce more equitable outcomes, but these approaches don't generate the commercial opportunities that private preparedness markets do.

The Preparedness-Conspiracy Pipeline: Radicalization and Extremism Concerns

From Risk Awareness to Extremism

Disaster preparedness exists on a spectrum. At one end, government-endorsed basic preparedness (72-hour kits, emergency planning) represents responsible behavior. At the other end, elaborate bunker construction, weapons stockpiling, and preparation for societal collapse ventures into extremist territory. The concerning dynamic is the radicalization pipeline where individuals drawn to preparedness through legitimate disaster concerns gradually encounter increasingly extreme narratives and adopt more extreme ideologies.

Social media algorithms exacerbate this pipeline. An individual seeking information about hurricane preparedness encounters related content including broader disaster scenarios, which leads to civil unrest preparation content, which eventually leads to extremist militia preparation narratives. The algorithmic amplification of increasingly extreme content combined with the psychological comfort of preparedness community membership creates conditions where individuals gradually drift toward extremism.

This pattern has been documented in radicalization research. Individuals recruited into extremist movements often begin with legitimate preparedness concerns before being introduced to extremist ideologies through community membership. The preparedness community, while primarily mainstream and non-ideological, provides social infrastructure where extremist recruitment can occur.

Company Responsibility and Community Moderation

Preparedness companies face questions about responsibility for how their products are used and what ideological communities they serve. Some preparedness companies have been criticized for appearing to court militia communities through marketing messaging emphasizing resistance to government authority and personal armed capability. Other companies have explicitly disavowed extremist associations and avoided messaging that could fuel radicalization.

The challenge is complex because legitimate preparedness concerns can be separated from extremist ideologies only with difficulty. A company marketing energy independence to customers might attract both solar enthusiasts and anti-government extremists. A company marketing backup power systems might attract both families seeking resilience and militia members preparing for imagined civil conflict. Drawing clear lines between responsible marketing and inadvertent extremist recruitment remains difficult.

Future Outlook: Trends and Predictions

Continued Market Growth and Consolidation

Market projections suggest continued strong growth in disaster preparedness through 2030 and beyond. Growth drivers include increasing frequency of disaster events, greater political polarization and institutional distrust reducing reliance on government disaster response, ongoing climate change impacts, and the normalization of preparedness as mainstream consumer behavior. Annual growth rates of 10-12% seem sustainable through the decade, potentially accelerating if major disaster events affect major metropolitan areas.

Market consolidation appears likely as well. Larger companies with sophisticated supply chains, manufacturing capabilities, and marketing resources will likely dominate market share, while smaller competitors struggle with profitability in a capital-intensive industry. We should expect continued acquisition and consolidation with perhaps 3-5 major companies controlling 60-70% of the market by 2030.

Internationalization represents another growth frontier. Preparedness markets in other developed nations remain underdeveloped compared to the American market. Companies are beginning to export American preparedness concepts and products to other developed nations, particularly those with visible disaster risks or growing climate change concerns. International expansion could double addressable markets over the coming decade.

Technological Advancement and New Product Categories

Technological advancement will continue driving product innovation. Improvements in battery technology will increase backup power system capacity and reduce costs, making these systems accessible to broader market segments. Advances in water purification technology will enable more sophisticated contamination removal in portable systems. Artificial intelligence applications will enable more sophisticated disaster prediction and preparedness planning.

Emerging product categories will likely develop around emerging risk perception. As cyber attack risks against infrastructure gain prominence, demand for network-independent communication systems and digital resilience products will grow. As pandemic preparedness remains elevated following COVID-19 experience, products addressing disease transmission and biological hazards will likely expand. Emerging threats drive emerging preparedness products.

Integration with Smart Home and Io T Ecosystems

Increasing integration between preparedness products and broader smart home ecosystems will accelerate. Backup power systems will become standard components of home automation platforms. Water quality monitoring will integrate with home health and wellness tracking. Emergency communications will integrate with smart home security systems. This integration makes preparedness seamlessly part of home infrastructure rather than a visibly separate emergency system, further normalizing preparedness in mainstream households.

Regulatory Evolution and Standards Development

As the preparedness industry matures, we should expect increasing regulatory attention and standards development. Federal Trade Commission enforcement against deceptive preparedness marketing will likely increase. Product safety standards will become more rigorous. Environmental regulations governing battery disposal and manufacturing will impose greater requirements on manufacturers. This regulatory professionalization will likely improve quality standards while potentially increasing product costs and reducing market growth rates from current projections.

Critical Evaluation: Balancing Rational Preparedness with Market Concerns

When Preparedness Makes Sense

Household disaster preparedness is sensible and appropriate in many circumstances. Maintaining a basic emergency kit, developing family communication plans, and securing backup power for homes with power-dependent medical equipment represents responsible planning. In disaster-prone regions (coastal areas vulnerable to hurricanes, regions vulnerable to earthquakes or severe winters), additional preparedness investments make logical sense.

Backup power systems make economic sense in regions with frequent power outages or for households with power-dependent medical equipment. Solar power systems make economic sense for households seeking to reduce electricity costs or achieve energy independence. Water filtration systems make sense for households with water quality concerns. These are rational investments addressing specific household circumstances and risks.

Where Preparedness Intersects with Problematic Consumption

The preparedness market becomes problematic when it encourages excessive consumption poorly matched to actual risk levels, when marketing strategies exploit fear and anxiety to drive purchasing beyond reasonable preparation levels, when quality control failures result in products failing when genuinely needed, and when preparedness becomes a vehicle for conspiracy thinking and extremism.

Forcing consumers with very low risk profiles to develop elaborate preparedness systems doesn't represent efficient resource allocation. A household with reliable utility service, stable employment, and solid social support might rationally spend preparedness resources on non-financial emergency preparation (training in first aid, developing evacuation plans, maintaining community relationships) rather than purchasing expensive backup systems. Marketing that encourages excessive preparedness consumption beyond this rational level represents misallocation of consumer resources.

Recommendations for Consumers

Consumers evaluating preparedness products should conduct honest assessment of actual household risks, develop baseline preparedness addressing genuine vulnerabilities, implement preparedness gradually rather than through panic purchasing, prioritize resilience approaches aligned with actual risk profiles, verify product quality claims through independent testing, and be skeptical of marketing emphasizing catastrophic scenarios. Starting with basic 72-hour emergency kits, developing family communication plans, and ensuring backup power for essential equipment represents sensible baseline preparedness. Expanding from this baseline should be deliberate and risk-based rather than driven by marketing or social media anxiety.

Conclusion: Preparedness as a Cultural and Economic Phenomenon

The transformation of disaster preparedness from fringe concern to multibillion-dollar industry reflects fundamental shifts in how Americans perceive risk, institutional trust, and personal responsibility for security. The growth is rooted in genuine vulnerabilities—aging infrastructure, increasing disaster frequency, and visible failures of public systems to protect citizens. These are real challenges deserving real attention and solutions.

However, the commercialization of preparedness has created dynamics where marketing incentives sometimes drive consumption beyond what rational risk assessment would suggest. Fear-based marketing, algorithmic amplification of disaster content, and the intersection between preparedness and extremism create concerning patterns worth examining. The industry's quality control challenges and deceptive marketing practices by some companies undermine trust in preparedness products and create risks that emergency equipment will fail when genuinely needed.

The industry is likely to continue growing substantially. Market fundamentals are sound, technological advancement is real, infrastructure challenges are genuine, and mainstream cultural acceptance of preparedness is solid. Market consolidation will likely produce a more professionalized industry with better quality standards and more rigorous marketing practices. Integration with smart home ecosystems will further normalize preparedness as part of home infrastructure rather than visible emergency preparation.

Ultimately, preparedness represents a reasonable individual response to genuine risks. The challenge is maintaining this rationality in the face of market incentives and media dynamics that encourage excessive anxiety and consumption. Households should evaluate preparedness through a lens of specific risks and vulnerabilities, implement solutions addressing these risks cost-effectively, and resist marketing pressures encouraging excessive consumption. Communities should explore complementary community-scale preparedness approaches alongside household-scale preparation, ensuring resilience benefits aren't limited to affluent households capable of large preparedness investments.

The prepping industry has evolved from extreme niche to mainstream market force, reflecting both genuine preparedness needs and the power of marketing to shape consumer behavior around fear and anxiety. Understanding this industry requires acknowledging both its legitimate contributions to household safety and its problematic dynamics around commercial exploitation of uncertainty and fear. As the industry continues growing, these tensions will become increasingly important to navigate effectively.

FAQ

What is the disaster preparedness market?

The disaster preparedness market encompasses all commercial products and services designed to help individuals and households prepare for and survive emergencies, including backup power systems, water filtration, dehydrated foods, communication devices, and emergency planning software. The global market was valued at approximately

How has disaster preparedness become mainstream?

Disaster preparedness transitioned from a fringe concern to mainstream consumer behavior through several factors: increasing actual disaster frequency and infrastructure failures, normalization through social media and content marketing, religious communities providing cultural legitimacy through formal preparedness doctrine, and sophisticated marketing strategies positioning preparedness as responsible family planning rather than paranoia. The Federal Emergency Management Agency's endorsement of household disaster preparation further legitimized the market.

What are the main product categories in the preparedness industry?

The preparedness market encompasses several major categories: backup power systems (solar generators, batteries, inverters) representing approximately 35-40% of market value; food and water products representing 25-30%; communication and security systems representing 15-20%; and shelter systems representing 10-15%. Within each category, products range from basic emergency supplies to sophisticated integrated systems.

How much does household preparedness cost?

Preparedness investment costs vary dramatically based on intended protection level. Basic emergency kits cost

What quality control issues affect preparedness products?

Consumer reports indicate recurring quality control challenges across the industry including backup power systems with electrical defects or battery degradation, water filtration systems failing to achieve claimed contamination removal, and food products containing contaminants or spoiling despite claimed shelf-life. The Better Business Bureau and consumer advocacy groups recommend purchasing small quantities initially to verify product quality before making large bulk orders.

How should households determine appropriate preparedness levels?

Rational preparedness planning should begin with honest assessment of specific household risks—considering geographic disaster exposure, infrastructure reliability in your area, health vulnerabilities requiring backup power, and actual probability of events requiring emergency supplies. Baseline preparedness typically includes a 72-hour emergency kit, family communication plan, and relevant-specific preparation (hurricane preparation for coastal residents, wildfire preparation for rural residents, etc.). Expanding beyond this baseline should address specific identified vulnerabilities rather than being driven by general anxiety or marketing pressure.

How do religious communities influence the preparedness market?

Members of The Church of Jesus Christ of Latter-day Saints have strongly influenced preparedness market development through theological emphasis on preparation for end-times events, cultural values around self-reliance and independence, and organizational infrastructure providing disaster preparedness guidance. Many major preparedness companies were founded by Mormon entrepreneurs and maintain headquarters in Utah regions with high Mormon concentrations. The religious foundation provided initial legitimacy and consumer base allowing companies to expand into mainstream markets.

What infrastructure vulnerabilities are driving preparedness market growth?

Legitimate infrastructure vulnerabilities driving preparedness include aging electrical grid infrastructure reaching or exceeding design lifespans, increasing frequency and severity of weather-related disasters linked to climate change, aging water infrastructure vulnerable to contamination and failure, and cybersecurity vulnerabilities in increasingly digitized critical infrastructure. Federal Emergency Management Agency data indicates major power outages have increased significantly over recent decades, and multiple major infrastructure failures have affected millions of Americans.

How do preparedness companies market products to consumers?

Modern preparedness marketing employs multi-channel strategies including content marketing positioning preparedness as responsible family planning, social media advertising targeting consumers showing preparedness interest, influencer testimonials from customers benefiting from products during actual emergencies, email marketing campaigns, and organic social media content designed for algorithmic amplification. Marketing typically emphasizes energy independence and resilience rather than catastrophic scenarios, though some companies employ fear-based tactics exaggerating risk levels.

What role do artificial intelligence and technology play in preparedness?

Emerging technologies including artificial intelligence, Internet of Things integration, and data analytics are transforming preparedness. AI-powered applications analyze household characteristics and geographic risks to generate personalized preparedness recommendations. Smart backup power systems integrate with home automation to intelligently manage power distribution during outages. Data analytics applied to product performance enables continuous improvement in design and manufacturing. These technological advances are expected to accelerate preparedness market growth by improving product functionality and user experience.

Key Takeaways

- The $150B disaster preparedness market grew from religious doctrine to mainstream consumer behavior through cultural normalization and genuine infrastructure vulnerabilities

- Mormon theological emphasis on self-reliance and preparation provided the initial market foundation and concentrated entrepreneurial talent in Utah

- Backup power systems represent the fastest-growing segment with 35-40% of market value and 13-15% annual growth driven by real grid reliability concerns

- Quality control challenges persist across product categories with consumer complaints about performance gaps between marketed and actual capabilities

- Market consolidation and regulatory professionalization will likely improve quality standards while reducing growth rates from current projections

- Preparedness consumption patterns reveal concerning socioeconomic divides where affluent households invest in protection while vulnerable populations remain dependent on public assistance

- Marketing strategies sometimes exploit fear beyond warranted levels, and algorithmic amplification of disaster content creates radicalization pathways toward extremism

- Infrastructure vulnerabilities including aging electrical systems, increasing disaster frequency, and water contamination risks provide legitimate foundations for preparedness growth

- Emerging technologies including AI-powered risk assessment and smart home integration will transform preparedness from standalone products to integrated household systems

- Rational household preparedness addressing specific identified risks represents prudent planning, while excessive consumption driven by marketing anxiety indicates market dysfunction