![MrBeast's Step Acquisition: Why Creator Economics Met Fintech [2025]](https://tryrunable.com/blog/mrbeast-s-step-acquisition-why-creator-economics-met-fintech/image-1-1771032966838.webp)

The Creator Who Became a Fintech Player: Mr Beast's Step Acquisition Explained

When Mr Beast announced the acquisition of Step, a youth-focused financial platform, it marked a significant pivot point in creator economics. This wasn't just another celebrity endorsement deal or passion project. This was a strategic acquisition that brought 7 million users, a regulated financial product, and an entire fintech infrastructure into Beast Industries' expanding portfolio.

The announcement caught many off guard. Mr Beast, already dominating YouTube with over 450 million subscribers, had been building Beast Industries into something bigger than content creation. We're talking about a company that runs Feastables (a snack brand), Beast Philanthropy, Beast Games, and now financial services. The trajectory suggests something most people haven't fully processed yet: the world's largest creator isn't just making content anymore. He's building parallel infrastructure.

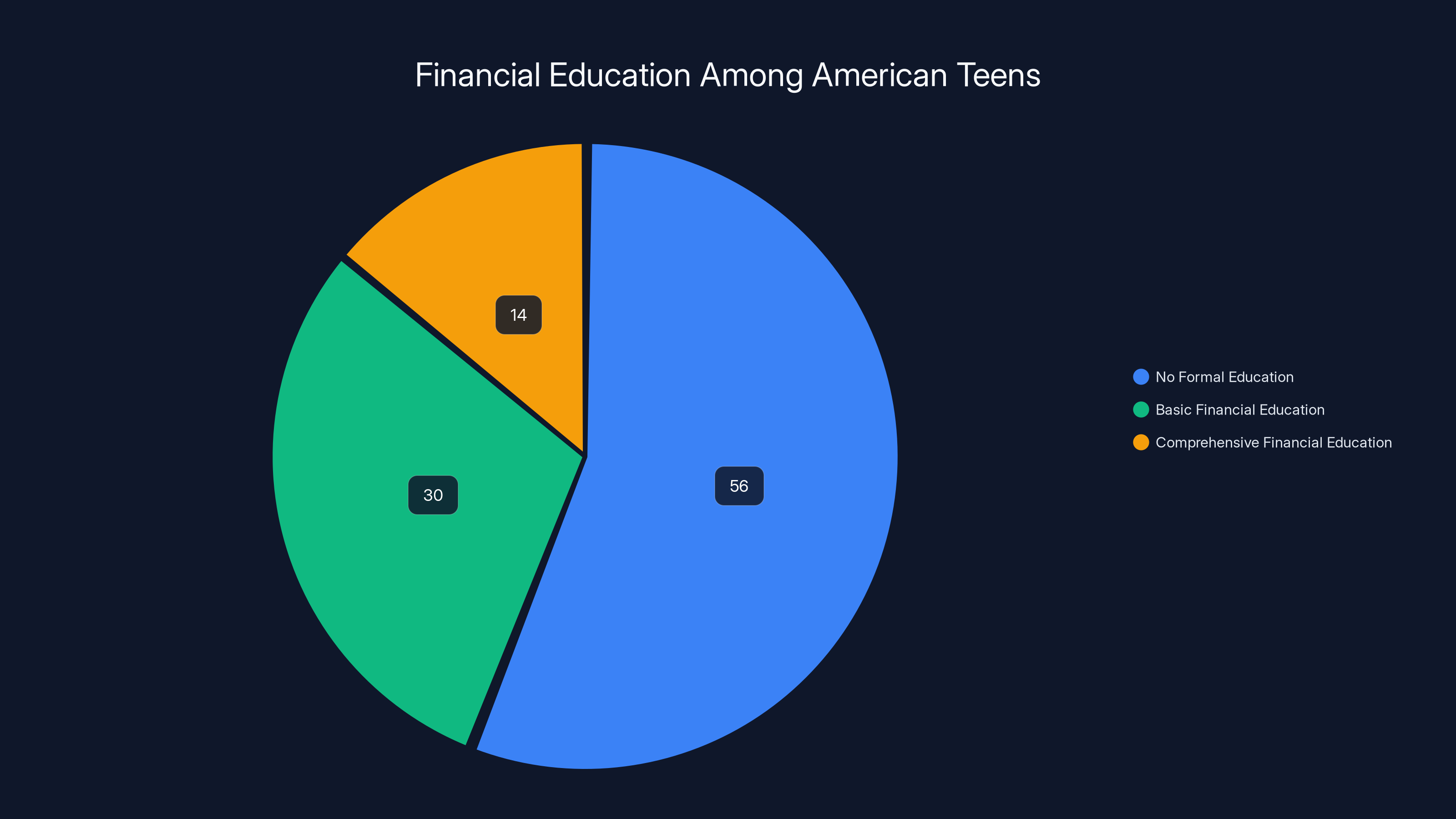

Mr Beast's statement about the deal reveals his actual motivation. He said he was never taught about investing, building credit, or managing money growing up. That's not just a personal anecdote—that's a market opportunity he spotted. According to recent data, roughly 56% of American teens have no formal financial education before turning 18. Most don't understand compound interest, credit scores, or how to invest. That gap exists because traditional financial institutions weren't designed for teenagers, and most parents can't teach what they never learned themselves.

The Step acquisition represents something deeper than celebrity entrepreneur enthusiasm. It's a collision between creator economics (where influence directly converts to audience) and fintech (where user acquisition is notoriously expensive and requires massive marketing budgets). What would cost a fintech startup $50 million to achieve through traditional marketing, Mr Beast could potentially reach in months through his existing audience.

Understanding Step: What It Actually Does

Step isn't a bank. This distinction matters more than you might think. Founded in 2018 by fintech veterans CJ Mac Donald and Alexey Kalinichenko, Step operates as a financial platform that partners with Evolve Bank & Trust for the actual regulated banking services. Step itself handles the user experience, customer acquisition, and product design, while Evolve manages the compliance nightmare.

The core product is a Visa debit card paired with mobile banking features. You'd think that description sounds ordinary—plenty of apps offer debit cards. But Step's positioning targets something specific: teenagers who need to learn financial habits without the complexity of traditional banking.

What Step provides:

- Visa debit card with no monthly fees or minimum balance requirements

- Savings goals that let teenagers set targets and track progress

- Spending analytics showing exactly where money goes (this is the educational component)

- Money sending between friends and family

- Basic investing tools that introduce stock market concepts

- Credit building through reported payment history to credit bureaus

- Parental controls so guardians can set spending limits and monitor transactions

The genius here is that Step doesn't try to be everything. It's specifically designed for financial literacy through experience. When a 16-year-old sees their spending broken down by category, it creates immediate feedback loops that traditional banking never provided. They see that $200 in small coffee purchases adds up. That's behavioral change through data visualization.

The app has raised significant funding from reputable sources. Stripe invested in Step, which matters because Stripe is ruthlessly selective about fintech investments. Y Combinator backed them. These weren't random venture capitalists throwing money at a founder's resume—they were validating that Step solved a real problem for a real market.

By the time Mr Beast acquired Step, the app had 7 million users. For fintech, that's a meaningful scale. That's not unicorn-sized user base, but it's a proven product-market fit. The fact that Step was still growing despite being founded in 2018 (before the fintech explosion) suggests real retention and engagement rather than flash-in-the-pan trend.

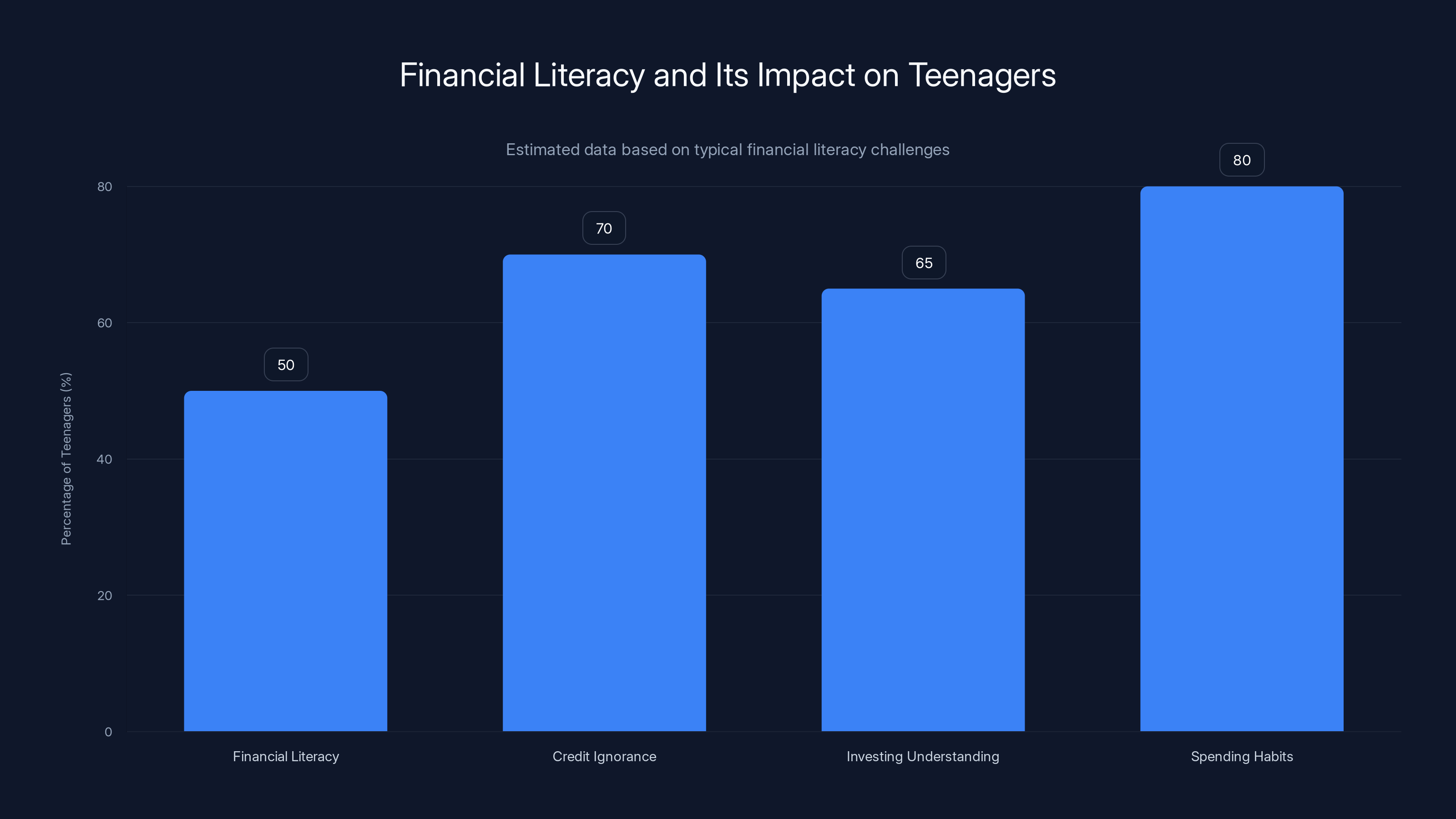

An estimated 50% of teenagers lack financial literacy, leading to issues like credit ignorance (70%), poor investing understanding (65%), and unchecked spending habits (80%). Estimated data.

The Beast Industries Strategy: Scaling Through Influence

Beast Industries exists because Mr Beast recognized something fundamental about content creation at scale: audience becomes infrastructure. When you have 450 million YouTube subscribers and billions of monthly views, you can launch products without traditional marketing budgets. The distribution channel is already built.

Look at what Beast Industries actually owns:

- Mr Beast Snapchat show: Broadcast rights and content creation

- Feastables: A snack brand selling through distribution partnerships

- Beast Games: A gaming competition platform with streaming rights

- Beast Philanthropy: Charitable organization with content tied to giving

- Now Step: Financial services for teenagers

There's a pattern here. Each of these isn't just a business—it's a business that feeds content back to Mr Beast's primary distribution channels. When you watch a Mr Beast video about fintech mistakes, there's now a financial product you can use. That's vertical integration of a sort, except instead of controlling supply chains, he's controlling audience attention.

The strategy makes economic sense when you run the math. Step's user acquisition cost in the traditional fintech market typically runs

Beast Industries also received a $200 million investment from Bitmine Immersion Technologies, a company with significant cryptocurrency exposure. This funding validates that institutional investors see Beast Industries as a legitimate business entity, not just a content brand. That's important for fintech credibility.

The acquisition also gave Beast Industries something intangible: a regulated fintech team. Building fintech from scratch requires deep expertise in banking regulations, compliance, fraud prevention, and payment processing. By acquiring Step, Mr Beast got all of that institutional knowledge without hiring and training.

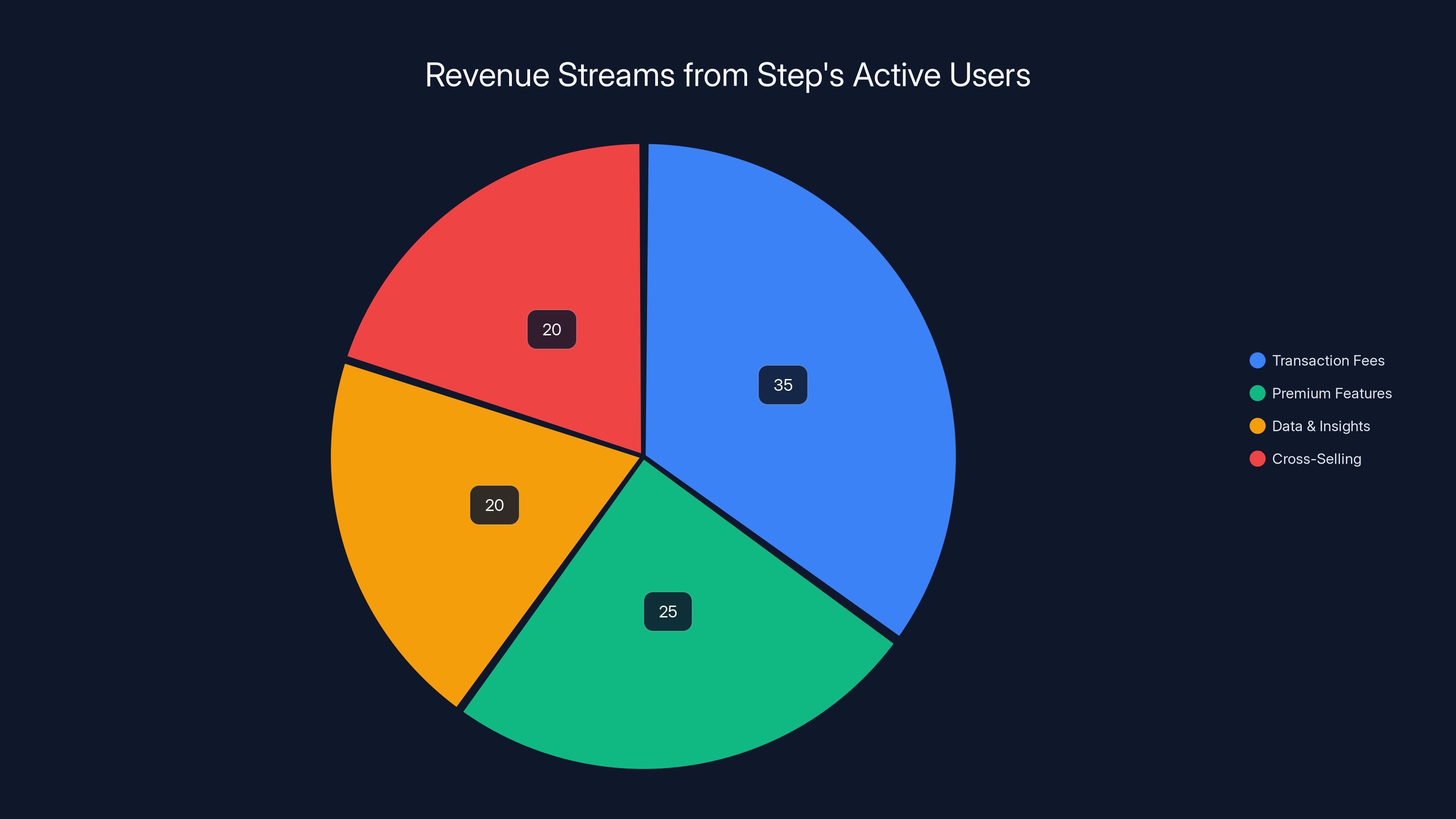

Estimated data shows that transaction fees and premium features are major revenue sources, but data insights and cross-selling also hold significant potential.

Teen Financial Literacy: The Real Problem Step Solves

Here's what most adults won't admit: they were never taught to manage money either. The financial education system in America is broken. Most schools treat money management like an optional elective, not a core life skill.

The statistics are grim. According to the Financial Industry Regulatory Authority (FINRA), only 57% of American adults are financially literate. That means nearly half of adults can't answer basic questions about interest rates, inflation, or risk diversification. If half of adults are financially illiterate, what chance do teenagers have without intervention?

This creates a cascade of problems:

Problem 1: Credit ignorance leads to debt spirals. Most teenagers get their first credit card or loan without understanding how interest compounds. They see "low APR" but don't understand that 18% APR on a

Problem 2: No understanding of investing means missed wealth building. If you start investing

Problem 3: Spending habits are never questioned. Most people adopt spending patterns by age 25 and stick to them for decades. Without early feedback about where money actually goes, teenagers develop expensive habits that compound into expensive lifestyles. A

Step attempts to solve these problems through direct experience. By giving teenagers a real debit card with real spending analytics, it creates immediate cause and effect. They see their spending. They build credit history. They understand what investing means through actual small positions. This is experiential learning, which research shows is 75% more effective than traditional instruction.

The Regulatory Framework: How Step Actually Works Legally

This is where things get complex. Step is not a bank and doesn't claim to be. The app is the interface, but Evolve Bank & Trust is the actual bank. This structure matters for compliance and user protection.

Here's how the regulatory chain works:

Layer 1: The App (Step). This is what users see and interact with. It handles customer interface, transaction initiation, customer service, fraud detection at the application layer, and user data management. Step does not hold deposits or transfer money directly.

Layer 2: The Payment Network (Visa). This is the infrastructure that actually moves money. Visa provides the card rails, the merchant network, and transaction security. Visa is regulated by the Federal Reserve and government banking authorities.

Layer 3: The Bank (Evolve Bank & Trust). This is where deposits actually sit and are protected by Federal Deposit Insurance Corporation (FDIC) insurance up to $250,000 per account holder. Evolve is the regulated entity that reports to the Office of the Comptroller of the Currency (OCC) and undergoes regular audits.

This three-layer structure is important because it means Step users have FDIC protection despite the app being owned by Mr Beast. Your money in Step is as protected as money in Chase or Bank of America, at least from a regulatory standpoint. That matters when a creator brand acquires a fintech product.

The regulatory reality becomes trickier around financial advice. Step can provide educational content about investing and financial management, but it cannot provide personalized investment advice without becoming a registered investment advisor. This is the line that separates education from advice, and it's crucial for compliance.

Mr Beast could theoretically use his platform to recommend investments, but if Step recommends specific stocks based on user profile, that crosses into investment advice territory and requires licensing. It's a boundary that fintech companies dance around constantly.

Step offers a comprehensive suite of features tailored for teenagers, with high emphasis on financial literacy and parental controls. Estimated data based on feature descriptions.

Why This Acquisition Surprised (and Didn't) Industry Observers

The fintech community had mixed reactions to the Mr Beast-Step acquisition. Some saw it as inevitable. Others questioned whether a creator brand should control financial products for teenagers.

The "inevitable" argument goes like this: Fintech has a customer acquisition problem. Regulatory requirements make financial products inherently complex and expensive to build. But distribution (acquiring users) is expensive and unpredictable. Creator brands solve the distribution problem. Mr Beast's audience is younger, digitally native, and already trusts him. Step needed scale. Mr Beast had unlimited scale. The combination was logically obvious.

The skepticism focused on different concerns. When a creator brand owns financial products, does that cloud judgment? Will Mr Beast promote Step even when it's not the best choice for his audience? Will he use his platform to inflate valuations or hide product deficiencies? These are conflicts of interest that traditional banking never had because banking was boring. Now a creator owns the bank.

There's also the question of audience vulnerability. Mr Beast's audience skews young. Average age estimates suggest 35% of his viewers are under 18. Teenagers are susceptible to influence and make impulsive financial decisions. Giving them financial tools via a creator they trust could amplify poor financial choices rather than prevent them.

Industry analysts also noted that the acquisition signals something bigger: creator economics is moving upstream into infrastructure. If Mr Beast can acquire fintech, what's next? Health tech? Legal services? Real estate platforms? The precedent suggests that influence can substitute for regulatory moat and brand trust in ways that traditional business never could.

From Beast Industries' perspective, the acquisition makes sense for another reason: hedging against platform risk. YouTube could change policies, algorithm changes could tank views, or controversies could damage the brand. But if Mr Beast owns financial products, payment processing networks, and banking relationships, he's no longer purely dependent on YouTube for revenue and reach. That's the logic of vertical integration applied to creator economics.

The Financial Architecture: Who Profits From This Deal

Mr Beast didn't disclose how much Beast Industries paid for Step. Industry estimates suggest somewhere between

But the financial logic becomes clearer when you model the unit economics. Step has 7 million users. If even 20% maintain active accounts and conduct regular transactions, that's 1.4 million active users. Revenue comes from several streams:

Transaction fees: When teenagers use their Step card at merchants, Visa charges a merchant discount rate (typically 1.5% to 2.5% of transaction value). Visa rebates roughly 50% of that to the card issuer, which in this case is Evolve Bank. Step likely negotiated a revenue share with Evolve.

Premium features: While the basic card is free, premium features (enhanced investment tools, priority customer service, accelerated savings goals) could generate subscription revenue. At even 5% penetration with a

Data and insights: This is where it gets interesting. Step accumulates spending data from teenagers. That data has value for understanding youth consumer behavior, marketing insights, and trend prediction. Beast Industries could monetize this through partnerships with brands wanting to understand Gen Z spending patterns.

Cross-selling opportunities: Every teenager with a Step account is a potential customer for Feastables, Beast Games, and other Beast Industries products. Financial products become acquisition channels for the broader ecosystem.

The real profit opportunity for Beast Industries isn't primarily from Step's transaction revenue. It's from the user acquisition channel that Step represents. Those 7 million teenagers become access points for other products and services. That's the strategic value of the acquisition.

If Beast Industries increases Step's monetization from

An estimated 56% of American teens lack formal financial education, highlighting a significant market opportunity for youth-focused financial platforms like Step.

Competitive Landscape: How Step Compares to Alternatives

Step isn't alone in the teen fintech space. Several competitors exist, and Mr Beast's acquisition should be understood in the context of an emerging market.

Greenlight is probably the closest competitor. It offers a debit card for kids with parental controls and financial education tools. Greenlight has raised significant venture funding and serves roughly 5 million users. The key difference: Greenlight is positioned as a parental tool (parents sign up and create cards for children), while Step positions itself as a tool for teenagers. That positioning difference affects everything from user acquisition to feature design.

Fidelity Youth offers investment education with small amounts of real money. It's more investment-focused than Step and appeals to teenagers interested in market participation. But it requires parental account opening, which creates friction.

Chime is a traditional online bank that happens to have good functionality for younger users. It has 20+ million users but targets the full spectrum of ages, not specifically teenagers. Chime's advantage is brand recognition and maturity. Step's advantage is focus on the specific needs of teenagers.

Dave is aimed at financial assistance and offers overdraft protection. It's popular with millennials and Gen Z but skews older than Step's target demographic.

The market for teen fintech is still forming. Census data shows roughly 35 million teenagers in America. If the market penetration for teen fintech reaches even 20%, that's 7 million users. Step already has most of that addressable market captured. The question is whether Mr Beast's ownership accelerates that penetration or whether it causes some users to switch out due to trust concerns.

Content Creator Trust and Financial Credibility

Here's the uncomfortable question nobody wants to ask directly: Should teenagers trust Mr Beast with their money?

Mr Beast has built an empire on entertainment and generosity. His content demonstrates financial sophistication (he discusses budgets, ROI, scaling content operations). But entertainment talent and financial services expertise are different skill sets. Being good at content creation doesn't make someone qualified to oversee financial products for millions of teenagers.

That said, Mr Beast hasn't mismanaged his own finances or engaged in financial fraud. He's not a known grifter. He's built a legitimate business empire. The trust he enjoys with his audience isn't baseless.

But there's a structural problem worth considering: Mr Beast's incentives are entertainment first and financial well-being second. If promoting Step requires keeping teenagers engaged with the app, not necessarily giving them sound financial advice, incentives misalign. A traditional bank regulator would intervene. A creator brand operates with different governance.

Beast Industries did appoint Jeff Housenbold as CEO. Housenbold has legitimate business credentials as former CEO of Shutterfly and has fintech experience. This suggests Beast Industries is taking the regulatory and operational aspects seriously, not treating Step as a side project. That matters for legitimacy.

The reality is that teens will trust Mr Beast more than traditional banks. His generation grew up with him and finds banks boring and inaccessible. From a financial inclusion perspective, if Step serves teenagers who would otherwise ignore financial planning entirely, that's net positive even if the ownership structure is unconventional.

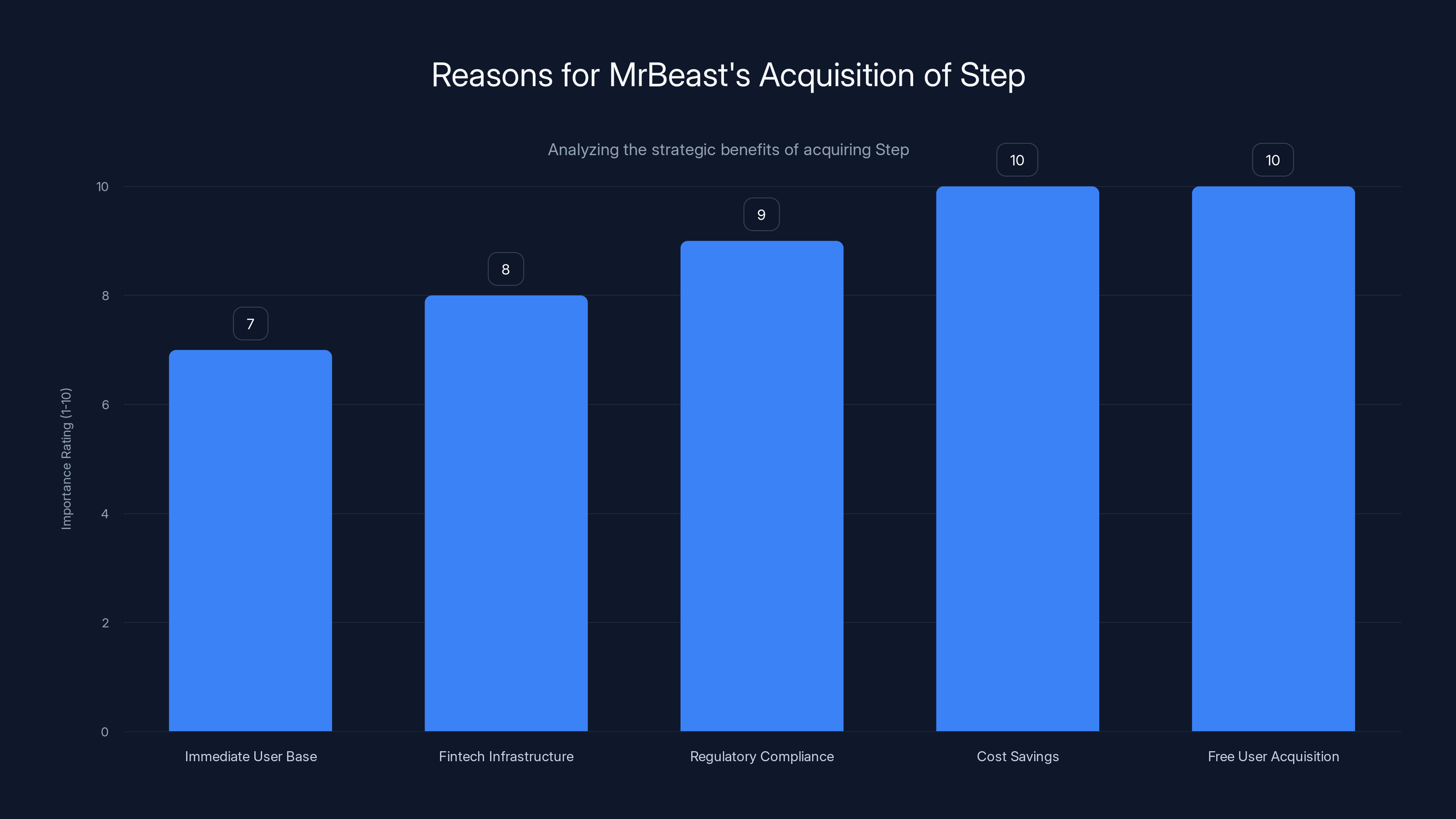

MrBeast acquired Step to leverage its existing 7 million users, established fintech infrastructure, and regulatory compliance, saving significant time and costs compared to building from scratch. Estimated data.

Regulatory Risks and Compliance Challenges

Mr Beast now operates in one of the most heavily regulated industries. That comes with obligations and risks that don't exist in content creation.

Step must comply with:

Anti-Money Laundering (AML) regulations: The Bank Secrecy Act requires financial institutions to know their customers and report suspicious transactions. This applies to Step. If teenagers are using Step accounts for anything questionable, Beast Industries has legal obligations to report it.

Know Your Customer (KYC) rules: Financial institutions must verify customer identity. For teenagers, this means verifying parent or guardian consent for minors. Step must maintain documented proof of identity and age.

Payment Card Industry (PCI) compliance: Card data must be encrypted and secured to industry standards. A breach could result in massive regulatory fines and civil liability.

Securities regulations: To the extent Step offers investment features, it must comply with SEC regulations about investment education versus investment advice. This is a narrow line that requires careful legal management.

Gramm-Leach-Bliley Act: This requires financial institutions to protect customer privacy and disclose data practices. Step cannot use customer data however it wants. Certain uses require explicit opt-in consent.

State-level banking regulations: Different states have different requirements for money transmission and banking services. Step must comply with regulations in all states where it operates.

Breach or violation of any of these could result in regulatory action, fines, criminal charges, or even loss of license to operate. This is serious infrastructure, not a content creation playground.

The good news is that Step already operates under these regulations through Evolve Bank. The acquisition doesn't change the regulatory framework. The bad news is that Beast Industries now inherits the compliance obligations and regulatory risks. One major breach or enforcement action could damage the entire Beast Industries brand.

The Cryptocurrency Connection and Financial Industry Skepticism

Here's something that deserves attention: the $200 million investment in Beast Industries came from Bitmine Immersion Technologies, which has deep cryptocurrency ties. This matters for understanding the full context of Mr Beast's fintech play.

Bitmine is a company with significant Ether holdings. That suggests investors with strong cryptocurrency conviction are funding Beast Industries. This raises questions: Is Beast Industries being positioned as a bridge between traditional finance and crypto? Will Step eventually offer cryptocurrency features? Is this acquisition part of a larger strategy to bring fintech to younger audiences who are more crypto-curious?

These questions are speculative, but they matter for credibility. The fintech industry is already skeptical of crypto-adjacent investments because of the association with fraud and volatility. If Beast Industries starts pushing cryptocurrency features through Step, trust with regulators and parents could erode quickly.

Mr Beast has been careful to avoid the fintech-crypto overlap explicitly. He hasn't mentioned cryptocurrency in connection with the Step acquisition. But the financial backing suggests someone's thinking about that trajectory.

For parents and teenagers using Step, the prudent approach is to recognize this uncertainty and monitor carefully. If Step introduces cryptocurrency features without proper disclosures and age-appropriate controls, that's a red flag. For now, the app functions as a straightforward financial tool without crypto exposure.

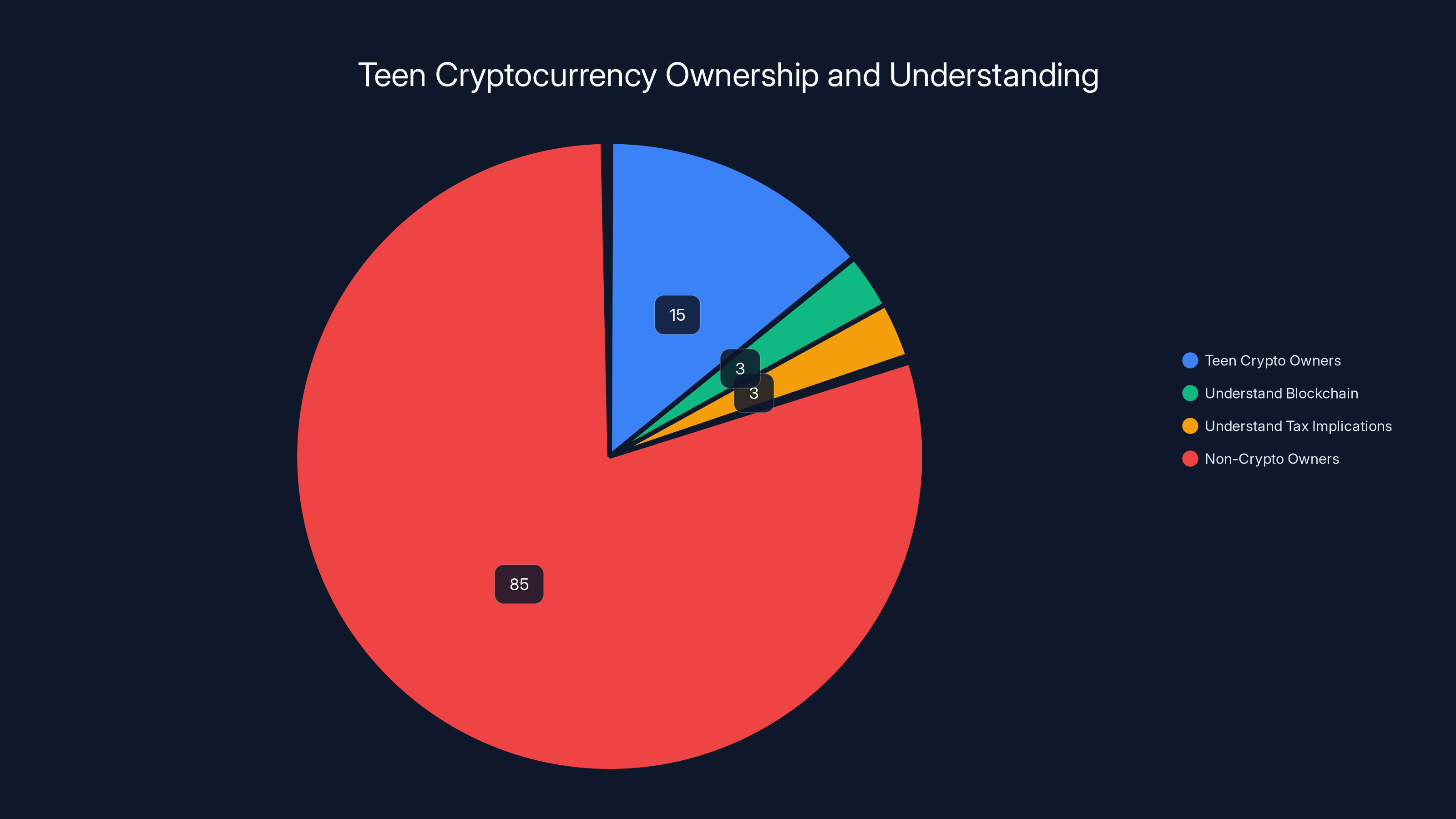

Estimated data shows that while 15% of teenagers own cryptocurrency, very few understand blockchain technology or tax implications, highlighting a significant knowledge gap.

Content Marketing and the Blurred Lines Between Promotion and Education

When Mr Beast makes videos about Step, he'll blur a line that traditional financial institutions maintain very carefully: the distinction between marketing and education. A bank can't say "use our product" in advertising without disclaimers. But content creators operate with different norms.

When Mr Beast makes a video titled "I Gave My Subscribers Money and They Invested It Using Step," is that marketing? Education? Entertainment? Probably all three. And that's where things get ethically complex.

If the video is honest about Step's actual features and limitations, it's valuable education for teenagers who would otherwise learn nothing. But if the video emphasizes success stories and downplays limitations, it's marketing dressed as education. The line is subjective.

Beast Industries could solve this by implementing strict policies: All financial content gets reviewed by compliance. All promotional content includes disclaimers. All educational content is clearly separated from promotional content. But enforcing that while maintaining entertainment value is genuinely difficult.

Industry observers should watch for whether Mr Beast maintains editorial integrity about Step or if the app becomes another promotional vehicle. That tells you whether Beast Industries is serious about fintech or just capitalizing on influence.

The Broader Shift: Creator Economies Moving Into Infrastructure

The Step acquisition isn't an isolated event. It's part of a larger pattern where creators with massive audiences are building business infrastructure beyond content.

Kim Kardashian has ventured into beauty, fashion, and now private equity. Oprah built a media empire. Joe Rogan negotiated direct licensing with Spotify. These are all creators leveraging audience into business platforms.

Mr Beast is doing the same thing, but differently. He's building operational infrastructure rather than licensing content. He owns a snack brand's production. He owns a gaming platform. Now he owns a fintech company. That suggests a long-term vision beyond YouTube celebrity.

The pattern is recognizable: creators with sufficient audience scale can build businesses more efficiently than traditional entrepreneurs because customer acquisition costs approach zero. That's a fundamental advantage. A startup founder spending $100 million on marketing might acquire 2 million users. Mr Beast can acquire 2 million users with a video and a mention.

This trend will likely accelerate. Expect more creator brands to move into infrastructure ownership. The question isn't whether this happens, but whether regulatory bodies force creators to separate entertainment from financial services or whether they allow the overlap to continue.

The answer to that question will shape how creator economies evolve over the next decade. If regulators block the overlap, creator businesses will face the same compliance and governance requirements as traditional companies. If they permit it, creator brands could become the dominant financial services providers for Gen Z.

What Parents Should Actually Consider About Step

Parents evaluating whether to set up Step for their teenagers should focus on specific questions rather than trusting (or distrusting) the Mr Beast brand.

Does your teenager currently track spending? If not, that's the primary benefit of Step. The spending analytics feature is genuinely valuable for developing financial awareness. That alone justifies consideration.

Are you comfortable with your child having a debit card? Some parents prefer young teenagers use cash to feel spending physically. Others think debit cards help develop good spending habits. This is a personal parenting choice that Step doesn't change.

Will you use parental controls? Step offers parental controls that let you set spending limits, see transactions, and restrict certain types of purchases. These are tools for financial oversight. If you won't use them, Step offers less value.

What's your teenager's age? Step works better for teenagers 15-18 than for younger kids. The investing features and credit building don't matter for a 13-year-old, but financial awareness through spending tracking matters at any age.

Are there better alternatives? Compare Step to Greenlight (more parental control focused), Chime (traditional banking with good teen features), or even a regular checking account at your bank with a linked debit card. Different tools fit different needs.

What's your comfort level with fintech products? If you prefer traditional banking relationships, Step might feel risky even if it's regulated. If you're comfortable with fintech, Step offers better functionality than traditional banking for teenagers.

The Mr Beast ownership shouldn't be the primary factor in your decision. The features, the regulatory framework, and your family's financial philosophy should drive the choice.

Future Implications: What the Step Acquisition Signals

Looking forward, the Mr Beast-Step acquisition signals several trajectories worth considering.

Consolidation in teen fintech: Expect more creator brands or traditional companies to acquire fintech startups with established user bases. User acquisition efficiency is the most valuable asset in fintech. Acquisitions that provide that efficiency will accelerate.

Feature expansion in Step: Beast Industries will likely push Step to add features that increase engagement and monetization. Expect enhanced investing tools, premium subscription tiers, and integrations with other Beast Industries products. The app will become less specialized and more comprehensive.

Regulatory scrutiny: Expect regulatory bodies to scrutinize creator-owned financial products more closely. The SEC and banking regulators will want to understand incentives and potential conflicts of interest. This could result in stricter policies for how creators can promote financial products.

Creator financial services becoming mainstream: Within five years, expect 15-20% of teenagers to use at least one creator-backed financial product. The model works too well for distribution to ignore. Regulatory frameworks will adapt to accommodate this.

Privacy concerns escalating: As creator brands accumulate more user data through financial products, privacy advocates will increase pressure for stronger protections. Expect legislation requiring explicit consent for data sharing and limiting commercial use of financial data.

Integration of entertainment and finance: The separation between content creation and financial services will continue to blur. Mr Beast might fund videos through Step accounts. He might create investing games with real money. The boundaries that traditionally kept entertainment and finance separate will dissolve.

For teenagers in 2025 and beyond, this means financial tools will increasingly come from creators rather than banks. That's not inherently good or bad—it's different. It offers benefits (accessibility, engagement, focus on their needs) and risks (misaligned incentives, conflicts of interest, data privacy).

The teenagers who thrive financially will be those whose parents help them navigate this landscape thoughtfully, using the best tools (whether creator-backed or traditional) for their specific situations.

TL; DR

- Mr Beast acquired Step, a youth-focused fintech app with 7 million users, signaling Beast Industries' expansion beyond content into financial services and regulated products

- Step addresses a real gap: 56% of American adults are financially illiterate, and most teenagers receive no formal financial education before age 18

- The business logic is sound: Mr Beast's 450+ million subscriber audience provides distribution that would cost $50-150 million to achieve through traditional marketing

- Regulatory framework is solid: Step operates through Evolve Bank & Trust for FDIC-insured deposits, maintaining the same protections as traditional banks despite creator ownership

- Conflicts of interest exist: Creator brands have entertainment incentives that may not perfectly align with financial well-being, requiring careful governance and transparency

- The bigger signal: This acquisition represents creator economies moving into infrastructure ownership, suggesting significant changes to how Gen Z accesses financial services

FAQ

What is the Step app and who owns it now?

Step is a youth-focused fintech platform founded in 2018 that provides teenagers with a Visa debit card, spending analytics, saving tools, and basic investing features. It's regulated through a partnership with Evolve Bank & Trust. Mr Beast (Jimmy Donaldson) acquired Step through Beast Industries in 2025, combining the app's 7 million users with his 450+ million subscriber audience across YouTube and other platforms.

How does Step actually work, and is it safe?

Step operates as a fintech platform that partners with Evolve Bank & Trust, a regulated bank insured by the FDIC. When you deposit money into Step, it's held at Evolve Bank and protected by FDIC insurance up to $250,000 per account holder. Step handles the user interface, transaction processing at the application layer, and customer service, while Evolve manages the actual banking and regulatory compliance. Your money is as protected as it would be at Chase or Bank of America, even though Mr Beast owns the app. Transactions go through the Visa network for merchant purchases.

Why did Mr Beast buy Step instead of building a financial app from scratch?

Mr Beast acquired Step to gain immediate access to 7 million users, a full fintech infrastructure, and regulatory compliance already in place. Building fintech from scratch would take 3-5 years and cost

What does Step offer that regular banks don't for teenagers?

Step provides features specifically designed for teenage financial literacy: automated spending analytics showing exactly where money goes by category, savings goals with visual progress tracking, the ability to send money to friends instantly, basic investing tools that let teenagers own fractional shares of stocks, and parental controls for guardians to set limits and monitor transactions. Traditional banks offer none of these features because teenagers aren't their target market. Banks focus on adults and don't build interfaces or features for teenagers' specific educational needs.

Is my teenager's data being sold, and what happens to spending information?

Step's privacy policy governs what happens to user data. The app does collect spending data, which has commercial value for understanding youth consumer behavior. Most fintech apps share anonymized, aggregated data with partners (brands, market research firms, etc.), but individual transaction data should remain private under GDPR and similar regulations. Beast Industries will almost certainly monetize this data through partnerships, but it should be anonymized and require opt-in consent for sensitive uses. Read Step's privacy policy carefully—data practices are a legitimate concern with any fintech product.

Could Mr Beast use his platform to promote Step even if it's not the best choice for teenagers?

Yes, that's a genuine conflict of interest. Content creators have entertainment incentives that don't perfectly align with financial well-being. However, Mr Beast also benefits from his audience trusting him long-term, which requires maintaining credibility. If he promotes Step when it's not appropriate, he damages trust. Regulators monitor financial product marketing, so overt conflicts would likely be flagged. The best protection is for parents to review products independently and not assume creator endorsements are impartial recommendations.

How does Step compare to Greenlight, and which is better?

Step and Greenlight are the two leading teen fintech apps, but they emphasize different things. Greenlight focuses on parental control and financial education through parent-initiated setup, appealing to families where guardians want oversight. Step positions itself as a tool for teenagers themselves, emphasizing spending awareness and personal financial management. Greenlight has roughly 5 million users, while Step has 7 million. Neither is objectively "better"—they solve different problems. Greenlight works better for younger teenagers and parents who want strong oversight. Step works better for teenagers 15+ who want to manage their own money with optional parental controls.

Will Step eventually offer cryptocurrency features through Mr Beast's connections?

That's speculative, but possible. Beast Industries received funding from Bitmine Immersion Technologies, which has cryptocurrency exposure. Mr Beast hasn't announced crypto features for Step, and introducing them would complicate regulation significantly. Any crypto features would require separate licensing and clear age-appropriate controls. For now, Step functions as a straightforward fintech product without cryptocurrency. If and when crypto gets added, it would be a significant product pivot that requires careful regulatory review.

What are the risks of using Step compared to a traditional bank?

Step's primary risks aren't regulatory (it's FDIC-insured like traditional banks) but operational and strategic. Beast Industries could mismanage the product, prioritize entertainment over financial health, or make decisions that harm teenagers' financial interests. There's also concentration risk: if anything damages Beast Industries' reputation, it could affect Step. Traditional banks are boring but stable. Creator-owned fintech is more innovative but more volatile. The best protection is monitoring product quality and being ready to switch if something changes for the worse.

Is starting financial literacy with Step better than traditional banking?

Yes, if your teenager will actually engage with the app. Step's strongest feature is spending analytics with visual feedback, which creates real behavioral change. Traditional banks offer none of this. However, Step only works if it's used. A teenager with a Step card they ignore learns nothing. The success depends entirely on engagement and parental guidance. Step provides the tools and data, but parents provide the actual financial education through conversation.

What should parents actually look for when evaluating teen fintech apps?

Focus on these factors: Does the app make spending visible? Does it offer parental controls that match your oversight style? Is it FDIC-insured or equivalent? How is user data handled? What's the fee structure? Can you easily switch if you're unsatisfied? Trust in the brand (including creator brand) should be a minor factor compared to actual functionality. Use features and governance as your primary evaluation criteria.

Conclusion

Mr Beast's acquisition of Step represents more than a celebrity entrepreneur expanding his portfolio. It's a signal that creator economies are moving infrastructure-upstream, fundamentally changing how audiences access financial services.

From a pure business standpoint, the acquisition is sound. Mr Beast gained 7 million users, a regulated fintech product, and a full technology team. In return, Beast Industries provided Step with distribution that would cost tens of millions to achieve conventionally. Both sides benefit.

But the implications extend beyond this single transaction. We're watching the emergence of a new category: creator-led financial services. These products have genuine advantages (accessibility, engagement, focus on younger audiences) and genuine risks (conflicts of interest, data privacy, regulatory uncertainty).

For teenagers, this is mostly positive. Financial products designed for them are rare. Most fintech treats teens as afterthoughts. Step focuses on their actual needs: spending awareness, credit building, and basic investing. Whether it's owned by Mr Beast or a traditional bank matters less than whether the product works.

For parents, the key is treating creator-backed financial products the same way you'd treat any financial product: evaluate on features, governance, and alignment with your family's values. Don't assume celebrity endorsement means quality. Don't assume institutional backing means safety. Use the same decision-making framework for both.

For regulators, this acquisition should trigger careful thought about how financial services are evolving. The traditional gatekeepers (banks, investment firms) are being supplemented by creator brands with direct audience access. That's not inherently bad, but it requires new frameworks for oversight and consumer protection.

The Step acquisition won't be the last time a creator moves into regulated financial services. If anything, it's the beginning of a wave. The teenagers who thrive financially will be those whose parents help them use these tools thoughtfully, maintaining the same skepticism and due diligence they'd apply to traditional financial institutions.

Beast Industries has a significant opportunity here. If they build a genuinely valuable product for teenagers and maintain ethical standards around conflicts of interest, Step could become the default financial app for Gen Z. If they prioritize entertainment over financial well-being or monetize user data aggressively, they'll lose credibility quickly.

Mr Beast's stated goal was simple: give millions of teenagers a financial foundation he never had. Whether Step actually delivers on that promise depends entirely on execution, governance, and maintaining alignment between creator incentives and user well-being.

For now, the product exists, works, and improves financial awareness. That's a solid start. Everything else is still being written.

Key Takeaways

- MrBeast acquired Step to solve fintech's primary problem: customer acquisition. His 450M+ subscriber audience provides near-zero cost user acquisition that would cost $50M-150M conventionally.

- Step addresses a real gap in teen financial education. 56% of American adults are financially illiterate, and most teenagers receive no formal financial training, creating a massive addressable market.

- The regulatory structure is solid. Step operates through FDIC-insured Evolve Bank & Trust, meaning teenagers' deposits are protected identically to traditional banks despite creator ownership.

- Creator-owned financial products introduce conflicts of interest that traditional banks don't face. Entertainment incentives may not align with financial well-being, requiring careful governance and transparency.

- This acquisition signals a broader trend: creator economies are moving into infrastructure ownership. Expect more creators to acquire or build financial services, fundamentally changing Gen Z's relationship with banking.

- For teenagers, Step's primary value is spending analytics that create immediate financial awareness through data visualization—something traditional banks never provided to young users.