![Public vs. Private AI SaaS: The Market Divergence Explained [2026]](https://tryrunable.com/blog/public-vs-private-ai-saas-the-market-divergence-explained-20/image-1-1768923536471.jpg)

Public vs. Private AI SaaS: The Market Divergence Explained [2026]

We're living through something genuinely unprecedented in B2B software. Not just unusual. Not just a correction. Unprecedented.

For 15+ years, I've watched venture markets cycle through waves of irrational exuberance and brutal corrections. Dot-com bubble. Mobile-first everything. Cloud hysteria. AI winter. All of it. But what's happening right now is different. It's not a simple reversion to the mean. It's a market actively rejecting one category of business while simultaneously throwing money at another with an intensity I've never seen before.

The thesis is stark: we're experiencing the worst time in modern history to own public software stocks while simultaneously living through the best time ever to invest in private AI-native businesses. These two trends shouldn't coexist. Logically, they shouldn't. But they're running parallel, diverging further every week.

This isn't sentiment. This isn't narrative. This is capital literally voting with its feet, creating the widest valuation divergence between public and private software in decades. Understanding what's actually happening—and why—matters if you're building a company, investing capital, or hiring great talent in this space.

Let's walk through the numbers first, then decode what the market is actually saying.

The Public B2B SaaS Bloodbath: Iconic Companies Cratering

We're barely into January 2026, and the damage is already significant. Not isolated. Not sector-specific. Systemic.

Take HubSpot. The company that literally defined inbound marketing. The textbook case for SMB SaaS success. Down 51% over the past year. Not a temporary dip. A 51% permanent revaluation of what the market thinks that business is worth. That's erasing roughly $30 billion in market value for a company that's still growing, still profitable, still printing cash.

ServiceNow is down 36%. This is the workflow automation company. The platform that replaced SAP and Oracle for half of corporate America. Analysts are openly calling it the "death of SaaS" narrative. Meaning, they're not saying ServiceNow is broken. They're saying the entire category is being repriced. According to KeyBanc analysts, this shift is significant.

Atlassian is down 26.9% just in the first 18 days of 2026. Jira is in every engineering organization on the planet. That's not hyperbole. It's verifiable. Yet the stock gets hammered by over a quarter in less than three weeks because the market is rotating out of software entirely.

Intuit, Adobe, Workday, Datadog, Monday.com—these aren't speculative bets. These are category-defining, moat-having, cash-generating software businesses. And they're all getting absolutely demolished. The average SaaS stock in the Nasdaq 100 is down double digits. Not some. The average.

Wall Street's language has shifted too. It's not "temporary headwinds" anymore. KeyBanc analysts are publishing reports with headlines about the "death of SaaS narrative." Morgan Stanley is suggesting software multiple compression will continue throughout 2026. The consensus, suddenly, is that software stocks are uninvestable.

Here's the thing that really matters: these companies are still growing. ServiceNow still has enterprise sales motion that works. HubSpot still owns SMB marketing. Datadog still has best-in-class cloud infrastructure monitoring. The businesses haven't changed. The market's willingness to pay for software businesses has.

Valuation multiples on public SaaS stocks have compressed to their lowest levels since 2008. Revenue multiples that were 8-12x just two years ago are now 2-4x. Enterprise value to free cash flow? Crushing downward. The market is essentially saying: we'll pay you what we'd pay for a stable utility, not a growth company.

For founders and investors in early-stage software, this creates a secondary effect that's genuinely dangerous. Public markets set the tone for exit expectations. When the comparable public companies are trading at 2-3x revenue, it's very hard to justify $50 million Series B rounds at 15x revenue assumptions. The comp story gets harder to tell. Valuations reset downward. Fundraising gets tougher even for well-run private companies.

But that's only half the story. And the other half is where things get genuinely strange.

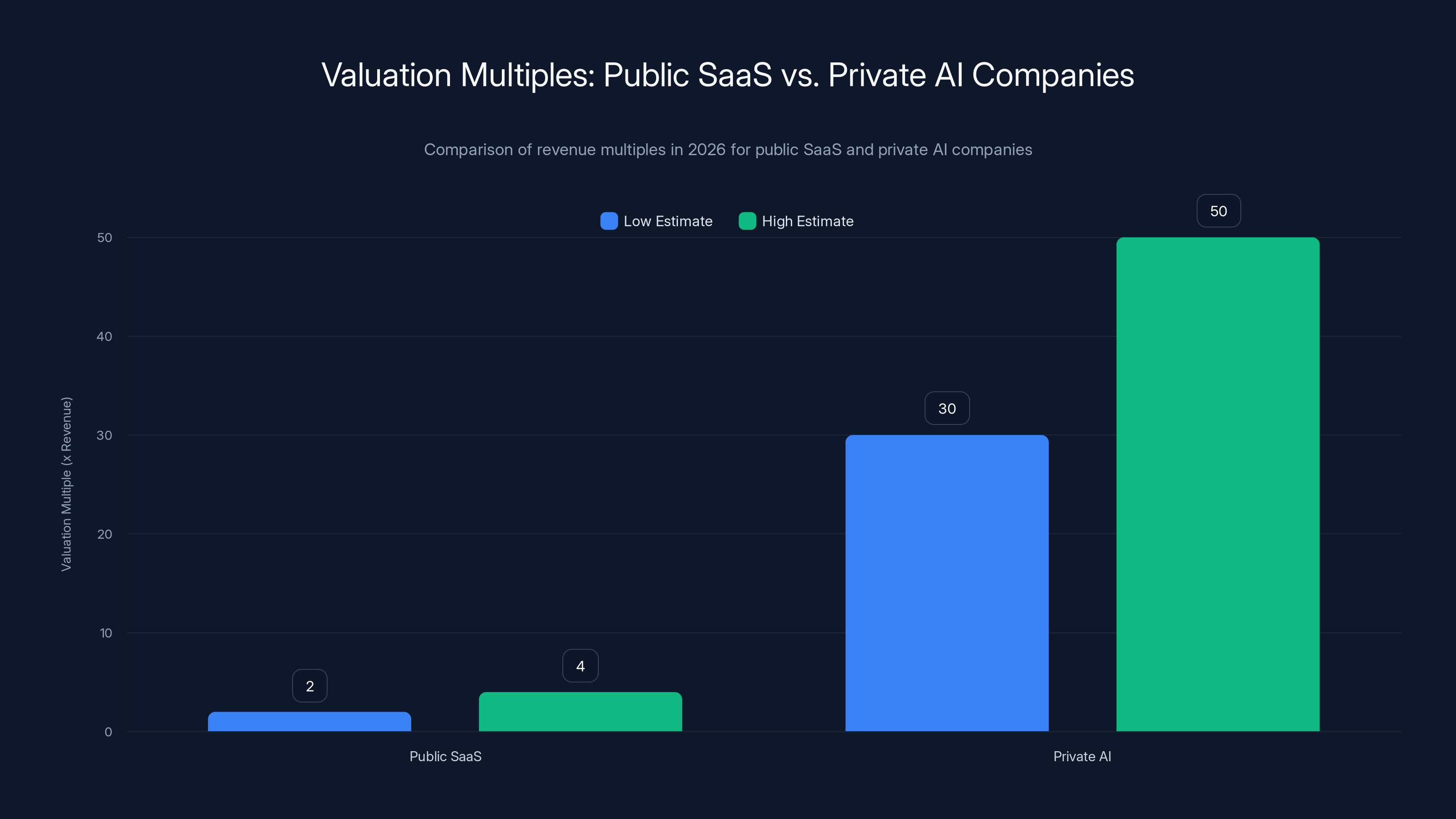

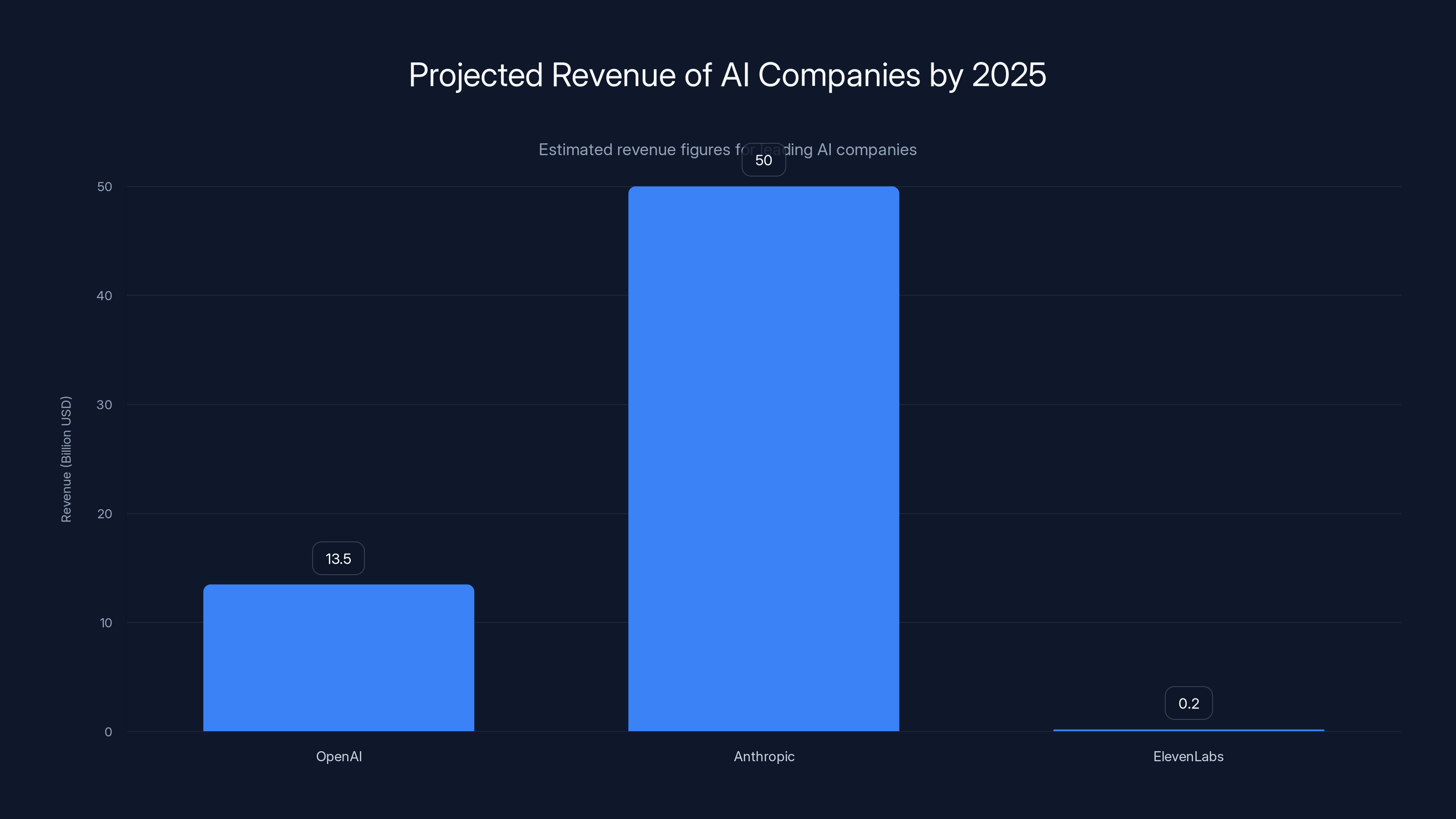

In 2026, public SaaS companies are valued at 2-4x revenue, while private AI companies are valued at 30-50x revenue, highlighting a significant divergence driven by investor confidence in AI-native companies. Estimated data.

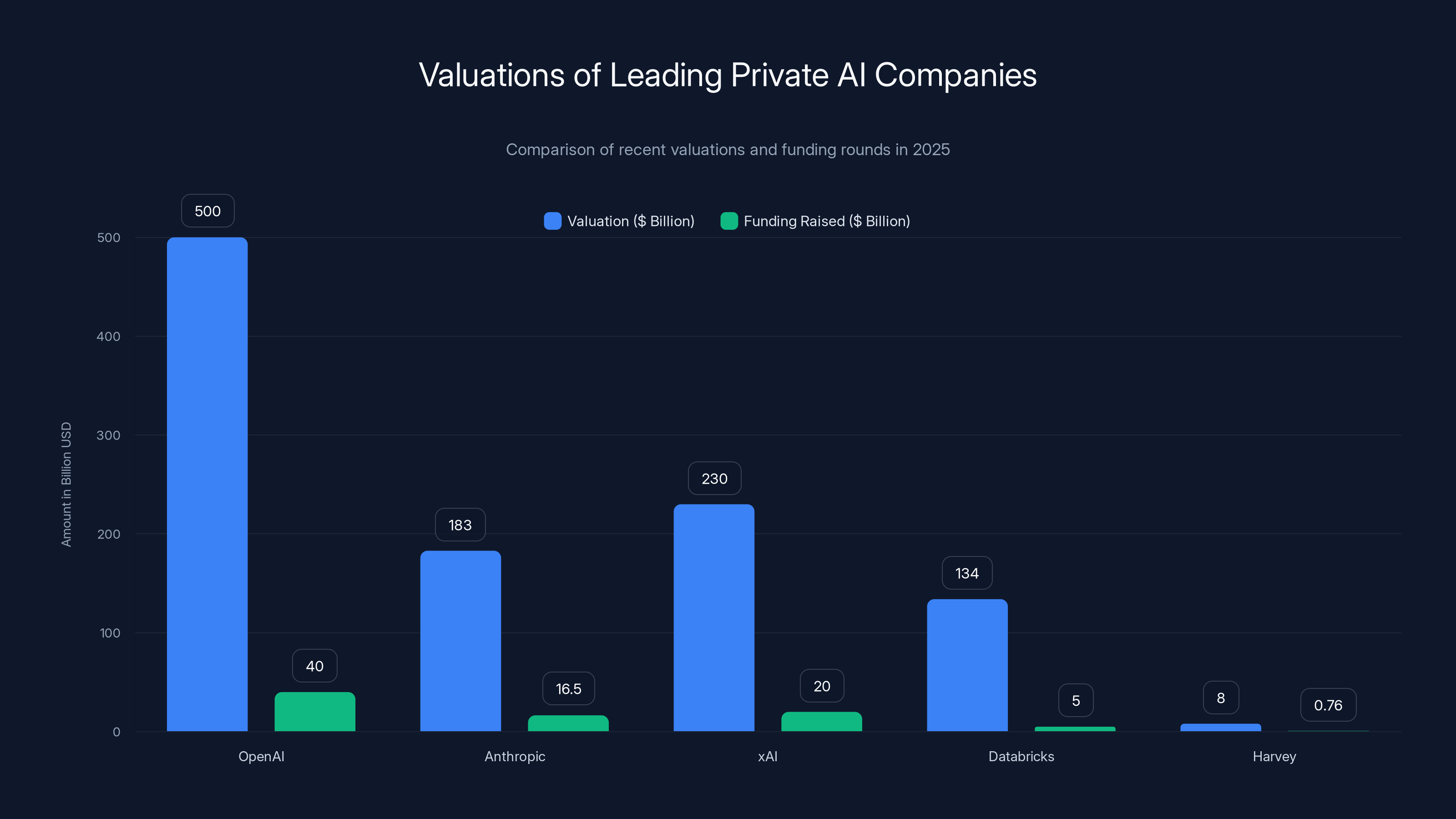

The Private AI Capital Explosion: Numbers That Defy Logic

Meanwhile, in the private markets, we're seeing something that's almost hard to articulate without sounding hyperbolic. It's not just euphoria. It's capital abundance that seems to come from another universe.

OpenAI raised

They're projecting $13.5 billion in revenue for 2025. Meaning, the market is paying 37x revenue for this company. While public SaaS trades at 2-4x.

Anthropic just raised

xAI hit a

Databricks raised

But here's where it gets really strange: it's not just foundation model companies. The application layer is following the same playbook.

Harvey, a legal AI platform, went from

Eleven Labs is now in talks to raise at an

Cursor, a coding tool, raised

Safe Superintelligence went from

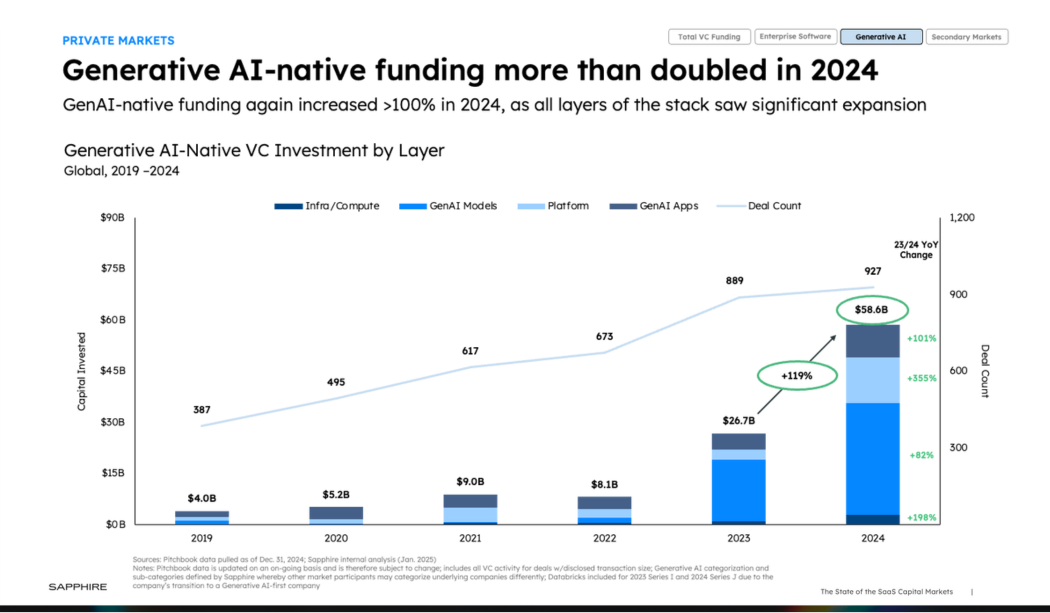

In 2025 alone, over

The venture dollars are moving into AI with a velocity that makes the dot-com bubble look cautious by comparison.

Iconic B2B SaaS companies like HubSpot and ServiceNow have seen significant declines in market value, with HubSpot down by 51% and ServiceNow by 36%. Estimated data for Intuit and Adobe.

What's Actually Happening: The Great Capital Migration

So the question becomes: why? Why is the market suddenly pricing public SaaS at 2-3x revenue while simultaneously paying 30-50x revenue for private AI companies with a fraction of the revenue?

There are several forces at work, and understanding each one matters.

The Semi/Chip Boom: Picks and Shovels

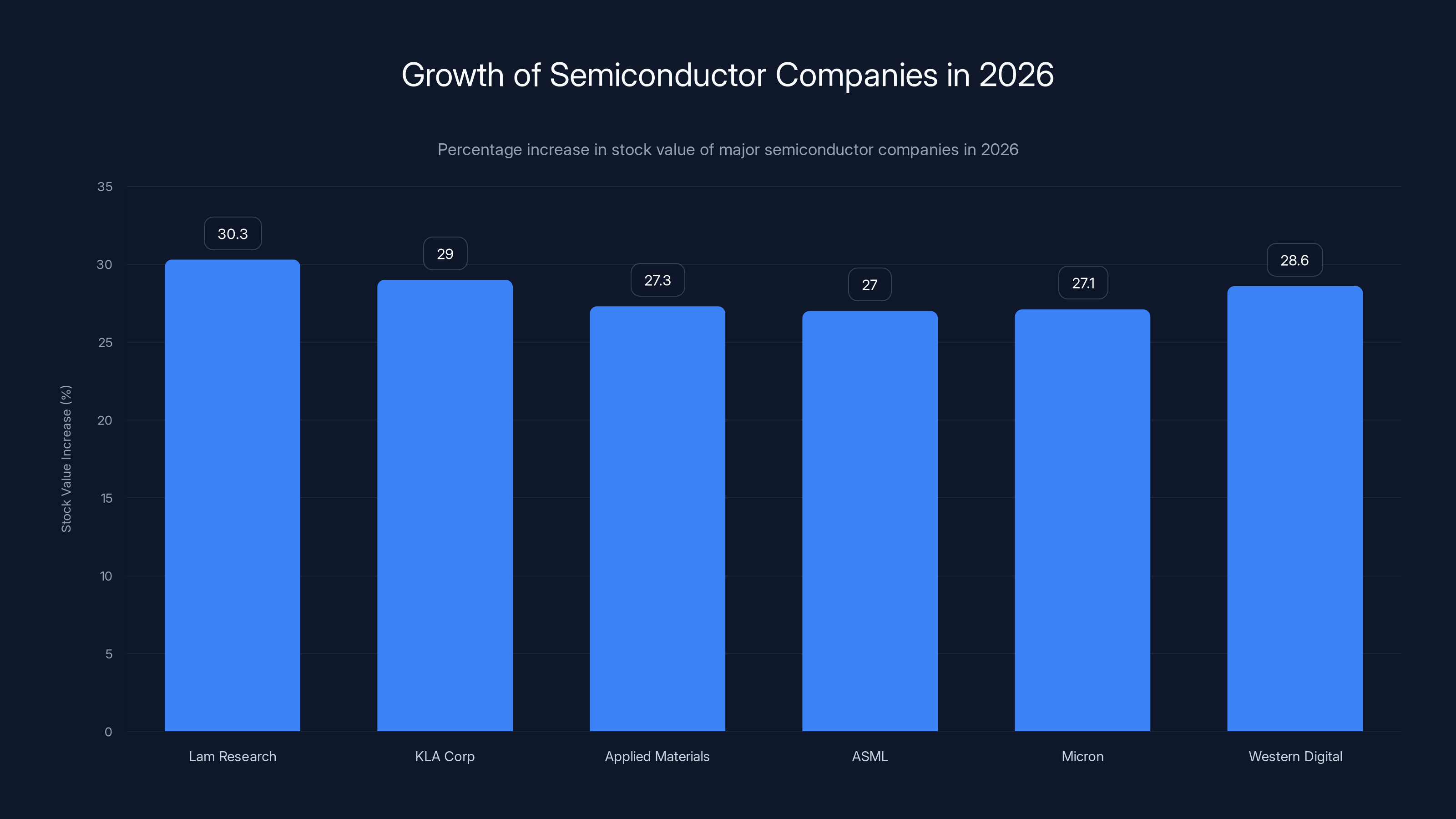

First, look at what's actually up in 2026. It's not software. It's semiconductors and infrastructure.

Lam Research is up 30.3%. KLA Corp up 29%. Applied Materials up 27.3%. ASML up 27%. Micron up 27.1%. Western Digital up 28.6%. These are chip makers. Chip testing companies. Chip manufacturing equipment suppliers. The picks and shovels of the AI gold rush.

Why? Because every AI company needs chips. Lots of them. And chip supply is bottlenecked. NVIDIA is sitting at roughly $3.5 trillion market value because AI compute demand is unlimited while chip supply is constrained. When supply is constrained and demand is infinite, prices go up, margins expand, and valuations compress upward.

Traditional software doesn't benefit from this dynamic. It doesn't need physical infrastructure in the same way. It doesn't have supply constraints driving margin expansion. So while the picks-and-shovels companies are printing money, traditional software is stuck.

The Application Layer Bifurcation: AI-Native vs. AI-Adapted

Second, there's a fundamental split happening at the application layer that the market is recognizing.

There's the "AI-native" category: companies building their primary value proposition around AI from inception. Cursor is an AI coding assistant. Eleven Labs is an AI voice company. Harvey is an AI legal platform. These companies aren't "adding AI features." They are AI features. The entire business model depends on having world-class models, fine-tuned data, and user workflows optimized for AI outputs.

Then there's the "AI-adapted" category: traditional software companies that are bolting AI features onto existing products. HubSpot adds AI writing assistants. Salesforce adds Einstein. Workday adds AI insights. These are real features. They're genuinely useful. But they're not the primary value proposition.

The market is betting—heavily—that AI-native companies will capture the upside of AI, while AI-adapted companies will watch their TAM get disintermediated by AI-native competitors.

That's a logical bet. It's not guaranteed to be true, but it's coherent. If AI becomes the primary way you interface with your domain (writing, coding, design, legal research, voice), then the companies that were built around AI from the start probably have better product-market fit than companies that were built around something else and are trying to graft AI on top.

Why would you use Intuit's AI accounting when you could use an AI accounting assistant trained specifically on your data? Why would you use Adobe's AI design tools when you could use an AI design platform built from the ground up for that?

This is the core thesis driving the valuation divergence. The market believes AI will eat software from the inside out, and the winners will be AI-native companies, not incumbent software companies trying to adapt.

The Enterprise Motion Collapse (Or Apparent Collapse)

Third, there's something happening with enterprise software sales motions that's worth examining closely.

Traditional enterprise SaaS works like this: long sales cycles (6-18 months), high ACV (average contract value

But that motion requires a certain relationship with your customer: the belief that you're enabling them to do something they couldn't do before. Once you're embedded, once you're the standard tool, you have pricing power.

AI companies are disrupting that in two ways:

First, they're often cheaper. If you can replace a

Second, they move faster. Enterprise software sales move at the pace of procurement and risk management. AI companies are moving at the pace of product development. A new AI feature ships in weeks. Enterprise software features ship in quarters. By the time enterprise software ships a feature to compete with AI, the AI has already shipped three new features and raised another $5 billion.

The market is recognizing that the enterprise sales motion advantage—which was the competitive moat for companies like ServiceNow and Workday—is becoming a liability. It's slow. It's expensive. It creates friction.

AI companies are proving that you can build billion-dollar ARR businesses with freemium/viral motion and land-based expansion. No expensive sales teams required. No 18-month sales cycles. Just good product and word-of-mouth.

That's a fundamental threat to the traditional enterprise software economics that the public market is pricing in.

The Venture Capital Allocation Shift: Where the Smart Money Actually Is

Here's something that matters more than it seems: look at where the actual venture capital allocation is moving.

Your Sequoia Capital, Andreessen Horowitz, Kleiner Perkins, Benchmark—all the tier-one firms that have historically backed enterprise SaaS—are now mostly investing in AI. A16z's recent mega-funds? Explicitly AI-focused. Sequoia's new strategy? AI and its infrastructure layer. The traditional venture playbook was to find a smart founder, pick an underserved market, and back them for 7-10 years as they built an enterprise motion.

Now the playbook is: find a smart founder, give them $100 million, and see if they can build an AI product that goes viral before their runway ends.

It's not a better playbook. But it's faster. It's more capital-efficient at finding product-market fit. And it rewards founders who can move quickly more than it rewards founders who can navigate long sales processes.

When the smartest capital stops flowing to traditional enterprise SaaS and starts flowing to AI, that's a signal. It's saying: we think the future of software is different than the past. We're moving our chips accordingly.

In 2026, semiconductor companies like Lam Research and KLA Corp saw significant stock value increases, driven by high demand for AI-related infrastructure. Estimated data.

The 10x Bet Asymmetry: Why Investors Are Chasing AI

Here's the honest math that drives venture allocation:

A traditional SaaS company might return 5-10x investor capital over 10 years. That's an amazing outcome. Seriously. A 50% IRR. That's venture success.

An AI company, if it works, might return 100x in 5 years. If ChatGPT or Anthropic make it to trillion-dollar valuations, early investors make 1,000x.

That's not a small difference. That's an order-of-magnitude difference in expected return.

Now, the probability of AI companies hitting those targets is lower than traditional SaaS. Risk-adjusted, they might have similar expected value. But venture capital doesn't allocate based on risk-adjusted expected value. It allocates based on the size of the upside if you're right.

Why back a company that might be worth

That's the venture allocation story. It's not that SaaS is broken. It's that AI has asymmetric upside that SaaS doesn't have. And capital follows asymmetry.

The Public Market Repricing: Multiple Compression and the Death of SaaS Narrative

What's happening in public markets is a different mechanism, but it leads to the same place: capital rotation out of software.

When analysts start talking about the "death of SaaS," they're not being literal. SaaS isn't dying. But the thesis that SaaS is a good long-term investment—the thesis that's driven valuations for 15 years—is being questioned.

Public market investors are fundamentally asking: if AI can do what SaaS does, but better and cheaper, why am I holding SaaS stock? Why am I not holding AI stocks instead?

And when public market investors start asking that question en masse, you get the valuation compression we're seeing. It's not forced selling. It's rational reallocation.

The problem is: you can't easily buy AI stocks in the public market. OpenAI, Anthropic, xAI—all private. Eleven Labs, Cursor, Scale AI—all private. So public investors who want to chase the AI thesis have two choices:

-

Sell their SaaS holdings and buy semiconductor companies (picks and shovels), which are trading at reasonable valuations and benefiting from the AI infrastructure boom.

-

Stay in software and hope that legacy SaaS companies successfully transition to AI-native businesses.

Most are choosing #1. Because #2 is hard. It requires betting that companies like Salesforce and Workday, which built their entire business around a different value proposition, can successfully reinvent themselves as AI companies. That's hard. The incentives aren't aligned. The org structure isn't built for it. The culture isn't designed for rapid iteration.

So the public market is rotating: out of software, into semiconductors, and into the few listed AI infrastructure companies (like Super Micro Computer, which builds AI servers). That rotation is creating the divergence we're seeing.

This chart highlights the staggering valuations and funding rounds of leading private AI companies in 2025, with OpenAI leading at a $500 billion valuation. Estimated data based on narrative.

Why This Matters: The Secondary Effects

This divergence doesn't just matter to public investors and venture capitalists. It has ripple effects through the entire ecosystem.

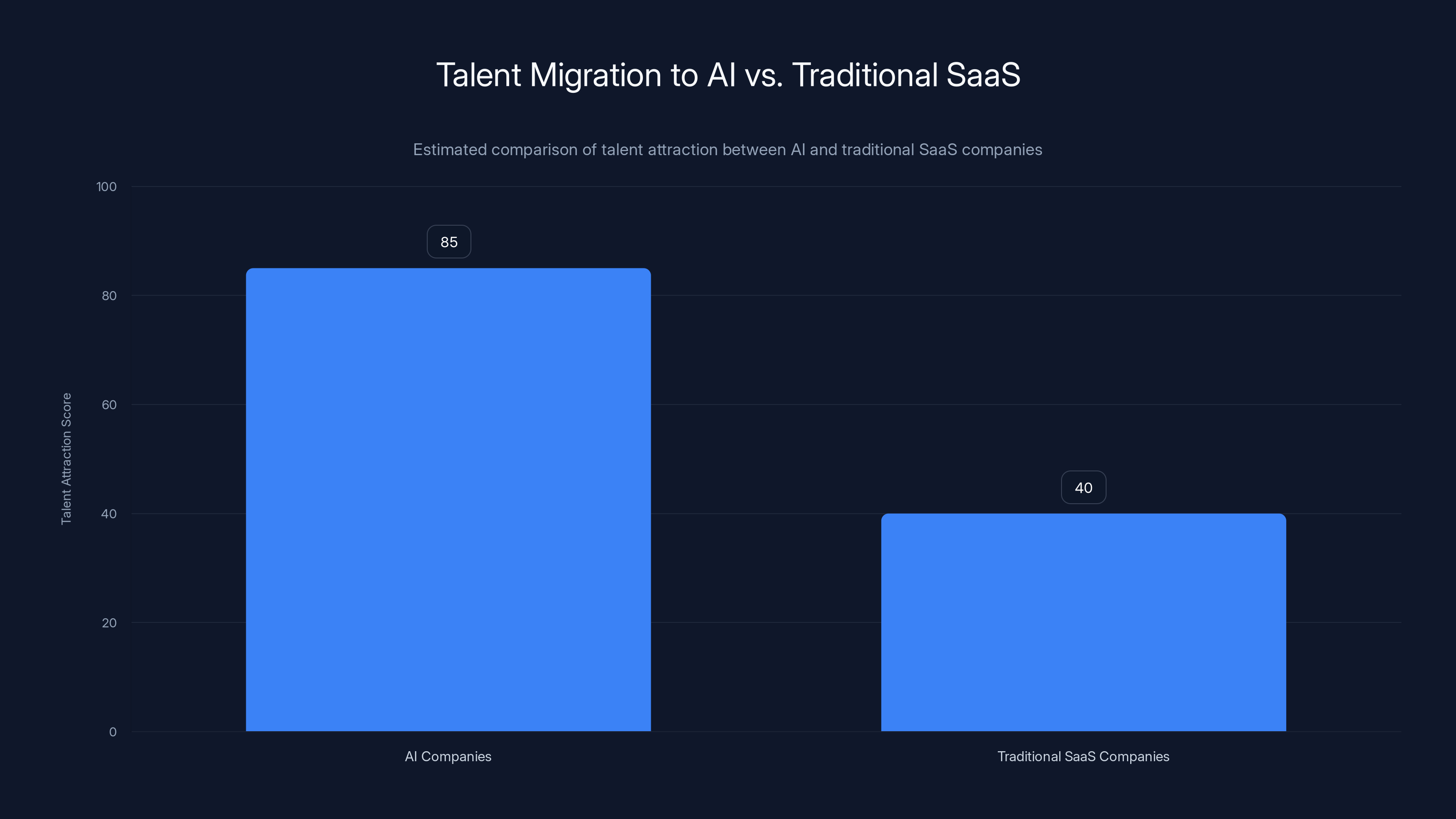

Talent Migration

When AI companies are raising at 10x the valuation and moving 10x faster, talent flows there. The best engineers who could go to Google or Stripe or Notion are now choosing Cursor or Anthropic. The best product managers are choosing Harvey or Eleven Labs.

This creates a secondary moat for AI companies: they're attracting the talent that would've built the next generation of SaaS companies. Instead, those people are building the next generation of AI companies.

For traditional SaaS companies, this is a compounding problem. Talent leaves. Product velocity slows. The company feels less innovative. More talent leaves. Eventually, you're a maintenance product, not a growth company.

The Down Round Problem

When public comps are trading at 2-3x revenue, it becomes very hard for private SaaS companies to raise funding. A Series B company raising at 8x revenue looks expensive when the public company in the same category is at 3x.

This forces companies into a choice: raise at significantly lower valuations (down rounds), accelerate to profitability (constrain growth), or pivot to AI (hard and risky).

Many companies are trying the pivot. It's not working consistently. AI is genuinely hard. You can't just add a neural network to your existing architecture and expect it to compete with purpose-built AI companies.

M&A Activity Shifts

Historically, large software companies acquire smaller software companies. Salesforce buys Slack. Adobe buys Figma (attempts to). ServiceNow buys process mining companies.

When your stock is down 36%, you don't have the currency to do strategic acquisitions. You're defending your own valuation. You're not out shopping for deals.

Instead, we're seeing software companies selling assets to private equity. We're seeing founder-led acquisitions where a hot founder buys up smaller software companies at the bottom. We're seeing strategic assets get separated and recombined in unexpected ways.

The M&A market is seizing up because public SaaS companies no longer have the currency to be aggressive acquirers.

The Counter-Narrative: Why Public SaaS Might Not Actually Be Broken

Now, I want to pause and acknowledge the other side of this thesis, because it matters.

It's entirely possible that public SaaS stocks are simply undervalued. That's happened before. In 2020, software stocks were trading at 15-20x revenue. They weren't all overvalued. Many were fairly valued. It just took time for the market to recognize it.

ServiceNow is still growing 25%+ YoY. HubSpot is still growing 20%+. These are not declining businesses. They're profitable. They have customer retention. They have pricing power.

It's possible that in 2028 or 2029, we look back at early 2026 SaaS stock prices and realize they were steals. The public market gets things wrong all the time. It overreacts to narratives.

There's also the argument that AI isn't actually going to replace most of what SaaS does. AI is great at specific, narrow tasks. But running your entire company on an AI that hallucinates sometimes? That's not a realistic near-term outcome. So maybe Workday still owns the HCM market in 2030. Maybe Salesforce still owns CRM. Maybe the disruption thesis is overstated.

Third, there's the argument that traditional software has network effects and switching costs that are underpriced. Once Jira is everywhere, moving to Cursor (a coding tool) doesn't eliminate Jira. They might exist side-by-side. So SaaS doesn't go to zero. It might just get smaller multiples.

That's a coherent narrative. And it might be true.

But the market isn't pricing for that narrative right now. The market is pricing for disruption. And until that changes, the divergence will likely continue.

OpenAI and Anthropic are projected to have significant revenues by 2025, justifying high valuations. Estimated data.

The AI Valuation Bubble Concerns: Is This Actually Different?

Let me also acknowledge the obvious: these AI valuations seem insane.

A $12 billion seed round? A company worth more than most of the Fortune 500 before shipping a product? Revenue multiples at 50x when profitable public companies trade at 3x? That looks like a bubble.

And it might be. Bubbles happen. The dot-com bubble happened. The WeWork/SoftBank bubble happened. Venture is prone to exuberance.

But here's the difference: some of these AI companies actually have revenue. OpenAI has

If Anthropic grows to

So it's not a bubble in the traditional sense. It's forward-looking pricing of genuine business potential. The risk is that the growth rate doesn't continue. The risk is that competition intensifies and margins compress. The risk is that the market for AI services turns out to be smaller than expected.

But the business model risk is lower than it was for the dot-com bubble. These are real businesses, not betting on eyeballs.

The Structural Divergence: Why This Might Persist for Years

Here's what I think matters most: this divergence might not be temporary.

Historically, stock market cycles are self-correcting. When growth stocks get too expensive, they underperform, and capital rotates into value stocks. When value gets too cheap, the same thing happens in reverse. It's cyclical.

But the AI/SaaS divergence might not be cyclical. It might be structural.

Why? Because the businesses are actually becoming different. AI companies are building different products, with different unit economics, requiring different skill sets, with different distribution models.

If AI companies actually are better at solving problems that traditional SaaS solves, then the divergence isn't a valuation anomaly. It's a market reallocating capital from inferior to superior products. That doesn't revert. That trend continues.

The semiconductor companies that are up 27-30% in 2026 might stay up. The SaaS companies that are down 15-50% might stay down. Not forever. But for years. Until the old business model completely gives way to the new one.

That's the scary part for traditional software investors. It's not that this is a cycle. It's that this might be an era.

AI companies are attracting significantly more talent compared to traditional SaaS companies, creating a competitive advantage. (Estimated data)

What This Means for Founders: The Strategic Implications

If you're a founder building a new company in 2026, this divergence shapes your strategic choices in real ways.

First, the clear play is AI. The capital is there. The investor interest is there. The value creation thesis is there. If you can build a genuinely good AI product, the fundraising environment is as good as it gets. At least for now.

But if you're building traditional SaaS—a better project management tool, a better HR system, a better accounting platform—you need to acknowledge that you're swimming upstream. The capital isn't flowing to you. The public comps are terrible. The acquisition targets are constrained.

You can still build a successful company. Profitable businesses get built all the time. But your exit options are limited. You're probably getting acquired by PE or a strategic buyer (if one exists). You're probably not going public at a good valuation. You're probably not getting acquired by a mega-cap SaaS company for a venture-grade return.

That's not saying: don't build software. It's saying: understand the environment you're building in. Build accordingly.

Second, if you're building within the traditional SaaS space, the differentiation needs to be defensive. You need to be focused on things that AI can't easily disrupt: enterprise sales motion, customer lock-in, network effects, data advantages. You need to be building moats, not just features.

A new project management tool without major defensibility gets crushed by Claude with a good prompt. A new project management tool that's embedded in an enterprise's entire workflow, with millions of integrations, years of data history, and irreplaceable team workflows—that has a chance.

Third, if you're an AI company founder, the challenge is different. You have capital. You have investor interest. Your challenge is actually delivering on the hype. Building products that work. Achieving product-market fit. Scaling economically.

Many AI companies will fail at this. The hype will outpace reality. Margins will compress. Competition will intensify. The companies that succeed will be the ones that focus on real utility, not narrative.

The Venture Capital Implications: Mega-Funds and Concentration

What's happening to venture capital itself matters too.

Traditional venture capital works through diversification. You back 20 companies, hope 3 work out, and those 3 return your entire fund and then some. It's a portfolio game.

But when you're deploying

That's different. That concentrates risk. If those companies succeed massively, the venture firms win massively. If they stumble, the venture firms face serious problems.

It also changes the incentive structure. If I'm a partner at a venture firm and I've committed $500 million to a mega-fund focused on AI infrastructure, I'm incentivized to back more AI companies. Even if they're not the best opportunities. The fund's performance depends on AI companies succeeding.

That's creating a feedback loop: more capital chasing AI companies, which drives valuations up, which makes it harder to find good SaaS companies to back (because they're no longer there), which pushes even more capital toward AI.

This could eventually correct. But not before billions of dollars are misallocated.

The Public Market Endgame: Where Does This End?

Where does the public market divergence end?

Really, there are three plausible scenarios:

Scenario 1: SaaS Recovery (30% probability)

Public SaaS companies successfully transition to AI-native businesses, or they defend their markets and integrate AI successfully enough that they remain dominant. Valuations recover to 5-8x revenue. The multiple compression was overdone. In 2028 or 2029, investors realize they sold winners at the bottom.

This requires: SaaS companies to move faster than they historically have. To cannibalize their own products. To invest heavily in AI R&D. To hire away talent from AI companies. It's hard, but not impossible. Salesforce and Workday have the capital to do it.

Scenario 2: Continued Compression (50% probability)

Public SaaS becomes a stable, low-multiple business. Similar to what happened to Oracle. It's a profitable cash cow. Investors hold for dividends and modest growth. But it's no longer a growth category. Multiples stay at 3-5x revenue indefinitely. The companies aren't destroyed. They're just not exciting anymore.

This is the base case. Mature software becomes mature software. It's a good business. Just not a high-multiple business.

Scenario 3: Structural Decline (20% probability)

AI genuinely does disintermediate most software. Multiples compress further to 1-2x revenue. The public SaaS market shrinks. Companies get delisted or taken private at depressed valuations. It's a worst-case scenario, but it's possible if AI moves faster than expected.

Most likely, the truth is Scenario 2: stable compression, mature business, lower multiples, nobody really wins or loses, market moves on. But the risk of Scenario 3 is what's driving the capital flight right now.

The Private Market Endgame: The Inevitable Reckoning

For private AI companies, the endgame is different but equally uncertain.

Right now, we're in a capital abundance phase. Investors will fund almost anything with "AI" in the pitch. Valuations are inflated by the sheer availability of capital looking for a home.

But that ends. It always does. Either the companies hit growth and profitability targets (and the valuations get justified), or they don't (and the valuations get crushed).

I'd estimate 90% of the AI companies being funded at mega-valuations won't hit their targets. Their growth will slow. Their margins will compress. The business models will turn out to be harder than they looked. Those companies will end up as acqui-hires or wind down.

But 10% will be absolute monster successes. OpenAI will probably be a

When those winners emerge—really emerge, not just hype-driven—the valuations will look cheap in retrospect. The investors who believed will get returns that look insane.

That's what's driving the mega-raises and mega-valuations right now. It's lottery ticket thinking at massive scale. Most tickets are losers. But a few are winners so big that the expected value is positive.

That's venture. Just at 10x the scale of 2015 venture.

Cross-Sector Implications: Beyond Just SaaS

Where this really gets interesting is the downstream effects on other sectors.

If AI can automate software engineering, why would you be bullish on human software engineers? The labor market for mid-level engineers—who've done okay for 15 years—gets threatened. The bar goes up. You need senior engineers who can use AI to build 10x faster. The mediocre ones? They're competing against Claude.

That's already happening. Hiring for mid-level engineering roles is getting harder. Not because there are fewer candidates. Because companies are asking: why hire a mid-level engineer for

Same thing applies to copywriting, graphic design, data analysis, strategy consulting. The jobs that software was supposed to augment—the white-collar jobs that SaaS was created to enhance—are getting directly threatened by AI.

That's a different market dynamic than just SaaS valuation compression. That's wholesale sector disruption.

The Flywheel: Why Divergence Compounds

Here's why this divergence is likely to continue compounding for at least another 2-3 years:

Talent flows to AI companies because valuation multiples are higher. Higher valuations mean more capital to spend on talent. Capital spent on talent means better products. Better products mean faster growth. Faster growth justifies even higher valuations.

Meanwhile, SaaS companies lose talent, which slows product development, which slows growth, which crushes valuations, which reduces capital for talent acquisition, which causes more talent to leave.

It's a positive feedback loop on the AI side and a negative feedback loop on the SaaS side.

Compounding dynamics take years to fully play out. I'd expect the divergence to persist through 2026 and probably into 2027. At some point, the mathematical extremes force a reversion. But not yet.

Investment Implications: What Rational People Should Do

If you're managing capital and you want to actually make money, here's what the current market is saying:

For aggressive investors (venture capital, hedge funds with high risk tolerance):

AI is the place. The expected returns are asymmetric. Yes, 90% of AI companies will fail. But 10% will be 100x winners. That's a positive expected value bet if you have the risk capacity. Deploy capital here.

For institutional investors (pensions, endowments, 401k):

This is trickier. You need returns, but you can't afford to lose. Buying SaaS at depressed multiples is actually defensible. These are real businesses. 15-20 year time horizon? SaaS probably outperforms from here. It's been hammered. It's got embedded competitive advantages. It's probably mispriced.

But you also want exposure to the AI winners, because if AI really does transform everything, you want to own the transformation, not just the disrupted incumbents.

For regular people with 401ks:

Honestly? Don't overthink this. Broad index funds are probably fine. They own both the AI upside (through mega-cap tech) and the SaaS downside (through concentrated positions). Over 20 years, this probably works out. The market will price things correctly eventually.

The Honest Take: We Actually Don't Know

Let me be direct: nobody actually knows how this ends.

I have a strong opinion that AI-native companies will capture the most value. I think public SaaS valuations are probably going to stay compressed. I think AI will disrupt more than people expect.

But I'm working with imperfect information. It's possible that by 2030, most of the AI companies fail, and ServiceNow and Salesforce are still the dominant players in their categories. It's possible that AI turns out to be less economically transformative than we think. It's possible that the regulatory environment changes everything.

What I'm confident about is this: the divergence you're seeing right now is real. Capital is flowing differently than it did in 2015 or 2020. The valuation gap between public and private is legitimately historic. And something has to give.

When something is structurally misaligned, markets tend to resolve it eventually. Either through convergence (prices meeting) or separation (the two tracks diverge completely). We'll find out which over the next 18-36 months.

For founders, investors, and employees in this space, the next few years are going to be incredibly interesting. If you can survive the next cycle without getting washed out, you're going to do fine. But some people are going to catch a wave. And some people are going to wipe out.

Build something useful. Capital will follow eventually.

FAQ

What is the main divergence between public and private SaaS markets in 2026?

The market is pricing public software stocks at 2-4x revenue while simultaneously valuing private AI companies at 30-50x revenue. Public SaaS companies like HubSpot (down 51%), ServiceNow (down 36%), and Atlassian (down 27%) are experiencing historic valuation compression, while private AI companies like OpenAI (

Why are public software stocks crashing while private AI companies are raising at record valuations?

The market believes AI will disintermediate traditional software. AI-native companies (built from the ground up around AI) are seen as having better product-market fit and faster execution than traditional SaaS companies trying to bolt AI features onto existing products. Additionally, venture capital is allocating 46% of all 2025 VC funding to AI (versus traditional software), creating a capital abundance that drives private valuations up while public market investors rotate out of SaaS and into semiconductor picks-and-shovels companies like NVIDIA and ASML.

Are public SaaS stocks actually overvalued or undervalued at current prices?

That depends on your time horizon and risk tolerance. Valuation multiples are at historic lows (2-4x revenue), which means either they're deeply undervalued (scenario: they survive the AI transition and see multiples expand back to 5-8x) or they're correctly priced (scenario: they become mature utilities trading at low multiples indefinitely). The honest answer is nobody knows, but the market is currently pricing in structural decline rather than cyclical undervaluation.

What should founders building new SaaS companies do in this environment?

If you're building traditional software, acknowledge you're swimming upstream. Capital isn't flowing to you. Your exit options are limited. You need to build defensible advantages (enterprise moats, switching costs, network effects) rather than just features. Alternatively, pivot to AI if you can genuinely build something better than purpose-built AI companies. If you're building AI, focus on actually delivering value, not just narrative, because most AI companies will fail once capital becomes selective.

How long will this divergence between public and private valuations persist?

Likely 18-36 more months before something structurally gives. Either public SaaS companies successfully transition to AI and recover valuations, or they accept their role as mature utilities and stay at low multiples, or AI companies stumble and their valuations compress. The current misalignment can't persist indefinitely because it creates economic incentives (talent arbitrage, acquisition targets, capital rotation) that will eventually force convergence.

Is this an AI bubble similar to the dot-com bubble?

Partially. The valuation euphoria is real, and many AI companies won't survive. But unlike dot-com, some AI companies actually have significant revenue. OpenAI has

What's the investment implication for different types of investors?

Venture capitalists should deploy capital to AI (asymmetric returns justify the risk). Institutional investors should consider overweighting depressed SaaS stocks (they're probably mispriced) while maintaining some AI exposure (transformation risk). Regular people with broad index funds are probably fine—they own both the upside and downside. The risk is concentrated bets in either direction without understanding that nobody actually knows how this ends.

Key Takeaways

- Public SaaS stocks have compressed to 2-4x revenue (historic lows) while private AI companies command 30-50x multiples, creating an unprecedented valuation divergence

- Capital allocation has shifted dramatically: 46% of all 2025 venture funding went to AI, with just five companies raising 225B deployed

- AI-native companies built from the ground up around AI are displacing traditional SaaS companies that are trying to bolt AI features onto legacy products

- Talent migration toward AI companies creates compounding negative effects for traditional SaaS: lost product velocity, slower innovation, further valuation compression

- The divergence likely persists 18-36 months more before structural realignment occurs through either traditional software recovery or complete market shift to AI-native alternatives