![Why Gaming's Biggest Publishers Are Betting Everything on Fewer, Bigger Games [2025]](https://tryrunable.com/blog/why-gaming-s-biggest-publishers-are-betting-everything-on-fe/image-1-1769089410637.jpg)

Why Gaming's Biggest Publishers Are Betting Everything on Fewer, Bigger Games

Something fundamental is shifting in how the world's largest gaming publishers make decisions. They're not just cautious anymore. They're terrified.

Last year, a game called Concord launched on PlayStation. It was beautiful. Expensive. And dead on arrival. Sony spent eight years and an estimated $200 million developing it, then shut the entire game and studio down just two weeks after launch. That's not a failure. That's a catastrophe.

Now, look at what's happening across the industry. Ubisoft announced a massive reorganization in late 2024, canceling six in-development games—including the long-awaited Prince of Persia remake—to focus exclusively on "billionaire franchises" and live service titles. EA is doing the same, pouring resources into sequels for Battlefield, EA Sports FC, and The Sims while abandoning mid-tier titles. Sony is following suit, betting on fewer games that either become massive franchises or disappear entirely.

This isn't strategy. It's triage.

The gaming industry has hit an inflection point. Development costs are astronomical. Player expectations are unrealistic. The window to recoup investment keeps shrinking. And when one major release underperforms, the financial damage cascades through the entire company. So the industry's biggest players are making a calculated bet: abandon the middle market entirely and swing for the fences with properties that either become global phenomena or vanish without a trace.

The problem? This strategy is fundamentally unsustainable, and nobody in the industry wants to admit it.

TL; DR

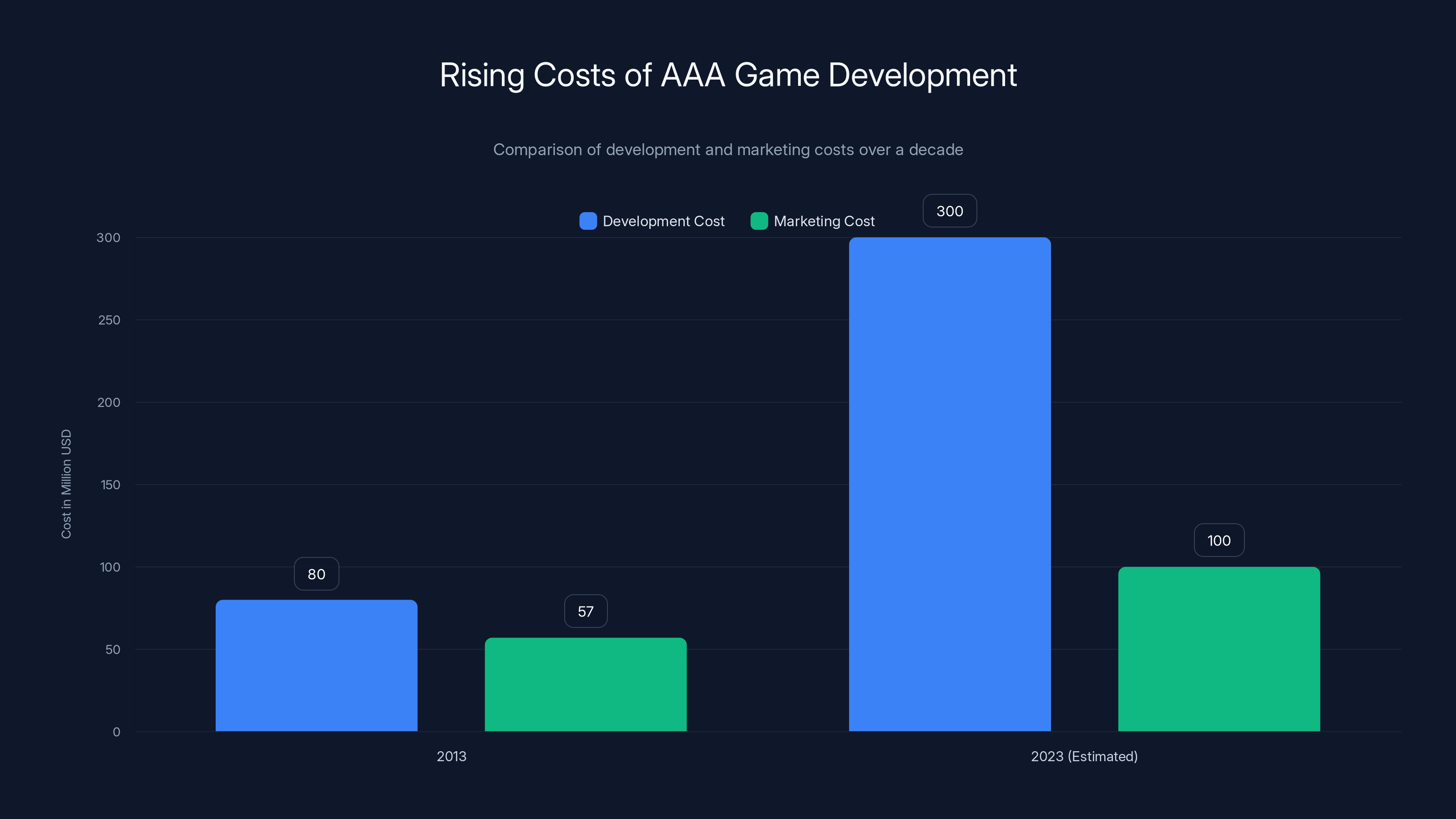

- Development costs are crushing the industry: AAA games now cost 300M+ to develop, forcing publishers to eliminate mid-tier titles

- Publishers are consolidating around proven franchises: Ubisoft, EA, and Sony are canceling new IPs and focusing exclusively on established brands like Assassin's Creed, Battlefield, and The Sims

- The Concord disaster changed everything: Sony's $200M loss on a game that lasted two weeks sent shockwaves through the entire industry

- Fewer games means higher stakes: When each release must be a blockbuster, one failure can destabilize an entire publisher

- Innovation is being sacrificed for safety: The industry is prioritizing proven formulas over creative risks, potentially stagnating game design for years

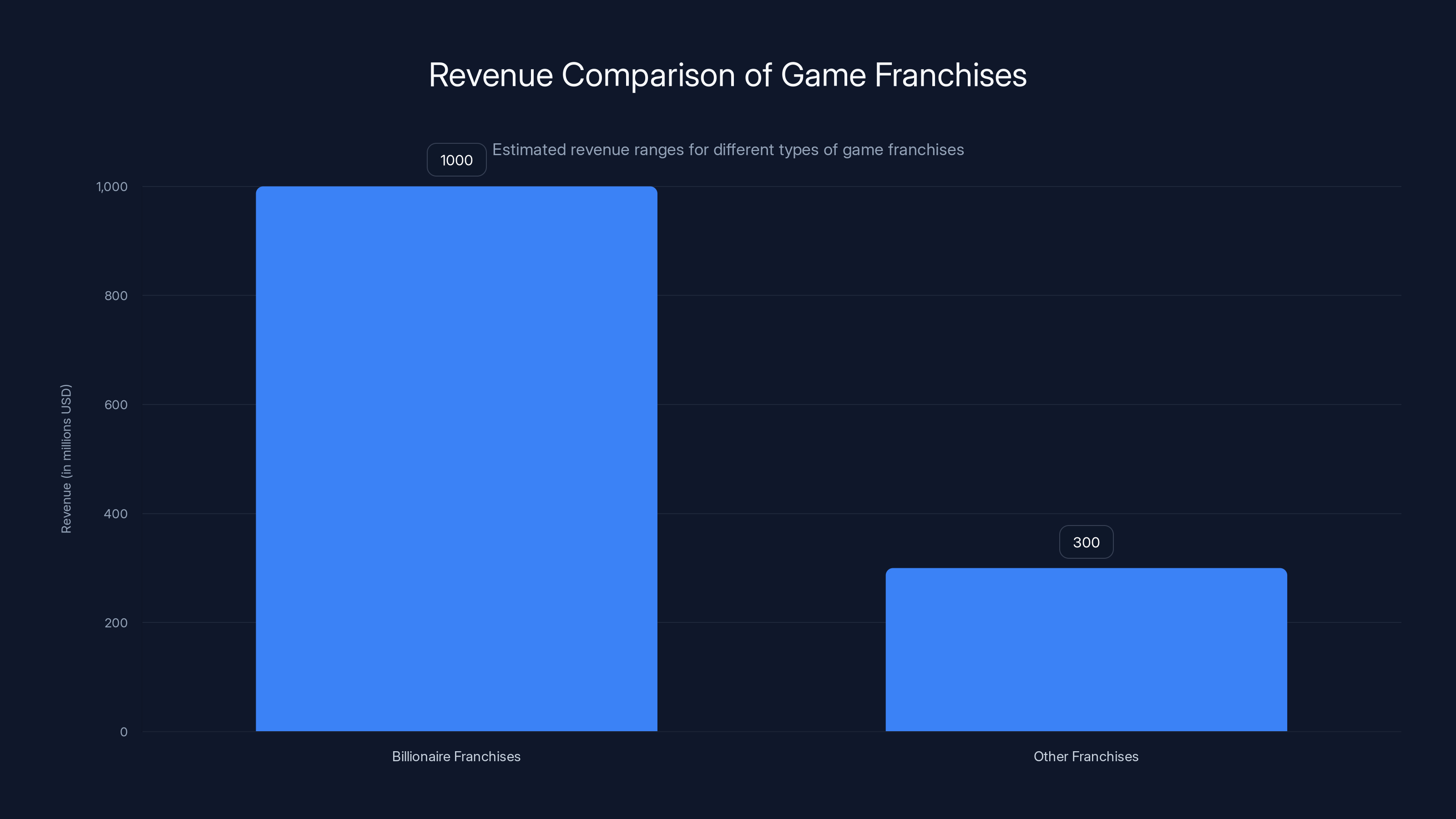

Billionaire franchises generate over

The Catastrophic Economics of Modern Game Development

Let's talk numbers, because this story doesn't make sense until you understand the financial reality crushing the industry.

A decade ago, a "big budget" game cost roughly

Rockstar Games' Grand Theft Auto V cost an estimated $137 million to develop and market—making it one of the most expensive entertainment products ever created at the time. But GTA V launched in 2013. Today's games spend even more.

Why did costs explode? Several converging factors:

First, player expectations evolved faster than technology did. When games moved to 64-bit consoles, developers could double the scale of environments. When HDR arrived, artists had to re-texture entire worlds. When motion capture became standard, studios needed mo-cap facilities, actors, and post-production pipelines that didn't exist before. Each technological generation forced publishers to rebuild their entire production infrastructure.

Second, the talent pipeline tightened. You can't hire 300 developers for a AAA project if only 50 qualified people exist in your region. So salaries skyrocketed. A senior game engineer in San Francisco now costs

Third, live service games created an entirely new cost category. Traditional games shipped and moved on. Live service games need continuous updates, balance patches, seasonal content, and permanent server infrastructure. That's not a one-time expense. It's a permanent drain on resources that extends 3 to 10 years post-launch.

The math doesn't work anymore. If you're spending **

How Ubisoft's Reorganization Reveals the Industry's Real Problem

Ubisoft's announcement in late 2024 wasn't just corporate restructuring. It was a public admission that the traditional game development model is broken.

Under the new structure, Ubisoft created five "Creative Houses," each focused on specific genres and franchises. This is corporate speak for: "We're throwing everything that doesn't fit into our proven franchises in the trash."

Here's what Ubisoft is keeping:

Vantage Studios will develop the company's "biggest franchises"—specifically Assassin's Creed, Far Cry, and Rainbow Six. These are the billionaire franchises, meaning each game in the series should theoretically generate $1 billion+ in lifetime revenue.

Other studios handle competitive shooters, live service games (the persistent, always-on titles that require continuous updates), fantasy and narrative-driven universes, and casual games.

Here's what Ubisoft is canceling:

Six games in development, including the Prince of Persia: The Sands of Time Remake. That game was in development for years. Resources were allocated. Teams were hired. And then, Ubisoft looked at the financial spreadsheet and realized: "This game might sell 3 to 5 million copies. That's not enough."

Beyond Good & Evil 2, another franchise that's been in development hell for over a decade, survives only because it's attached to an established IP with nostalgic value.

What's remarkable is what Ubisoft isn't saying: They're canceling three entire franchises. Not games. Franchises. Meaning there are entire intellectual properties—worlds, characters, stories—that Ubisoft invested in, only to determine they'll never be profitable enough to justify future investment.

This is the industry's dirty secret. For every Assassin's Creed, there are dozens of franchises that were either stillborn or died after one disappointing installment. The new business model requires publishers to make fewer bets, but those bets have to be absolutely certain winners.

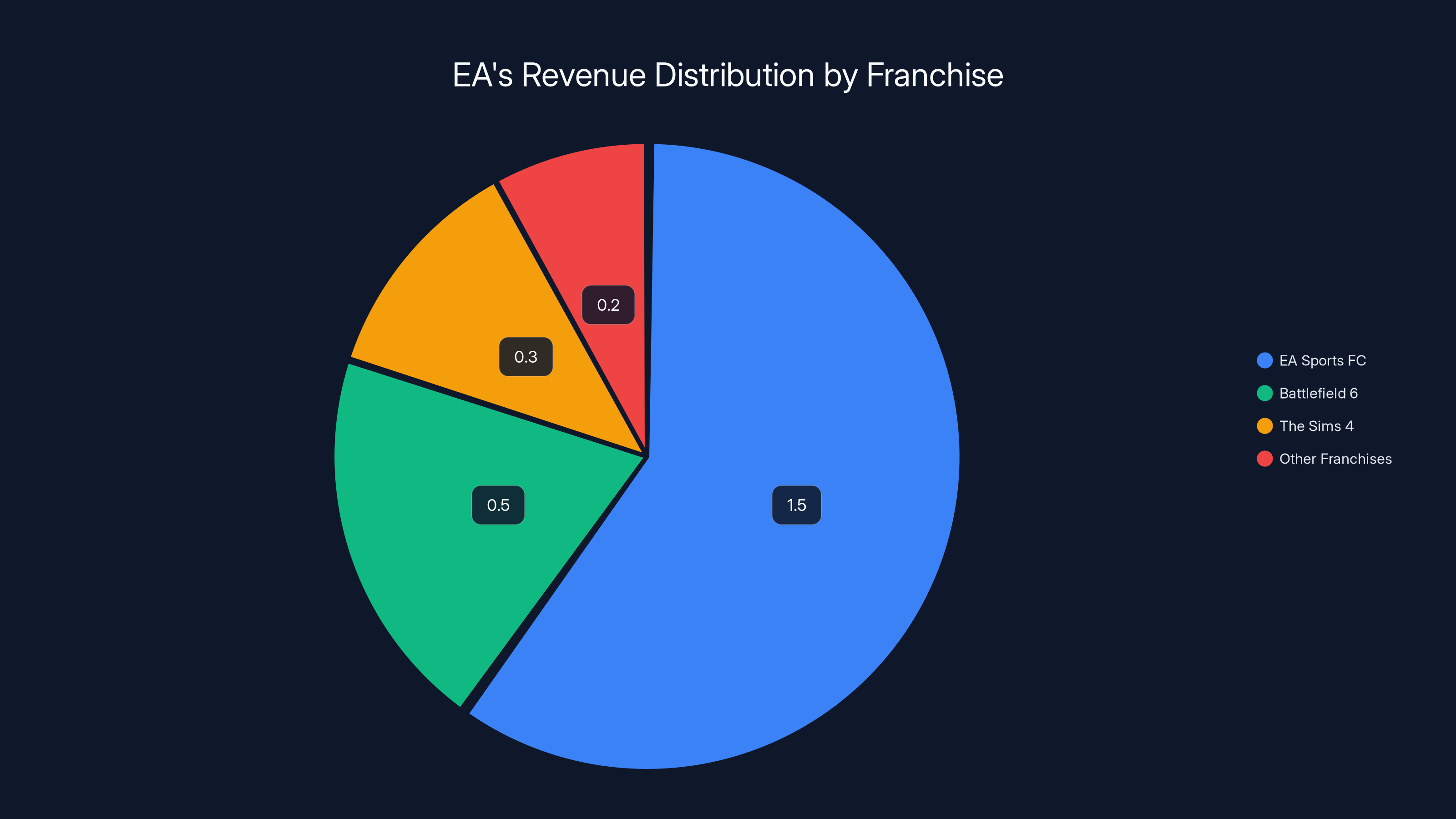

EA Sports FC dominates EA's revenue with $1.5 billion annually, followed by Battlefield 6 and The Sims 4. Estimated data.

The Concord Disaster: A $200 Million Lesson That Changed Everything

Concord deserves its own section because it's the event that crystallized the industry's fear and accelerated this consolidation trend.

Sony's new hero shooter launched in August 2024. By September, it was dead. The game shut down, and Firewalk Studios, the developer, was dismantled. Some reports suggest the project cost upwards of $200 million across eight years of development.

What happened? Everything that could go wrong, did.

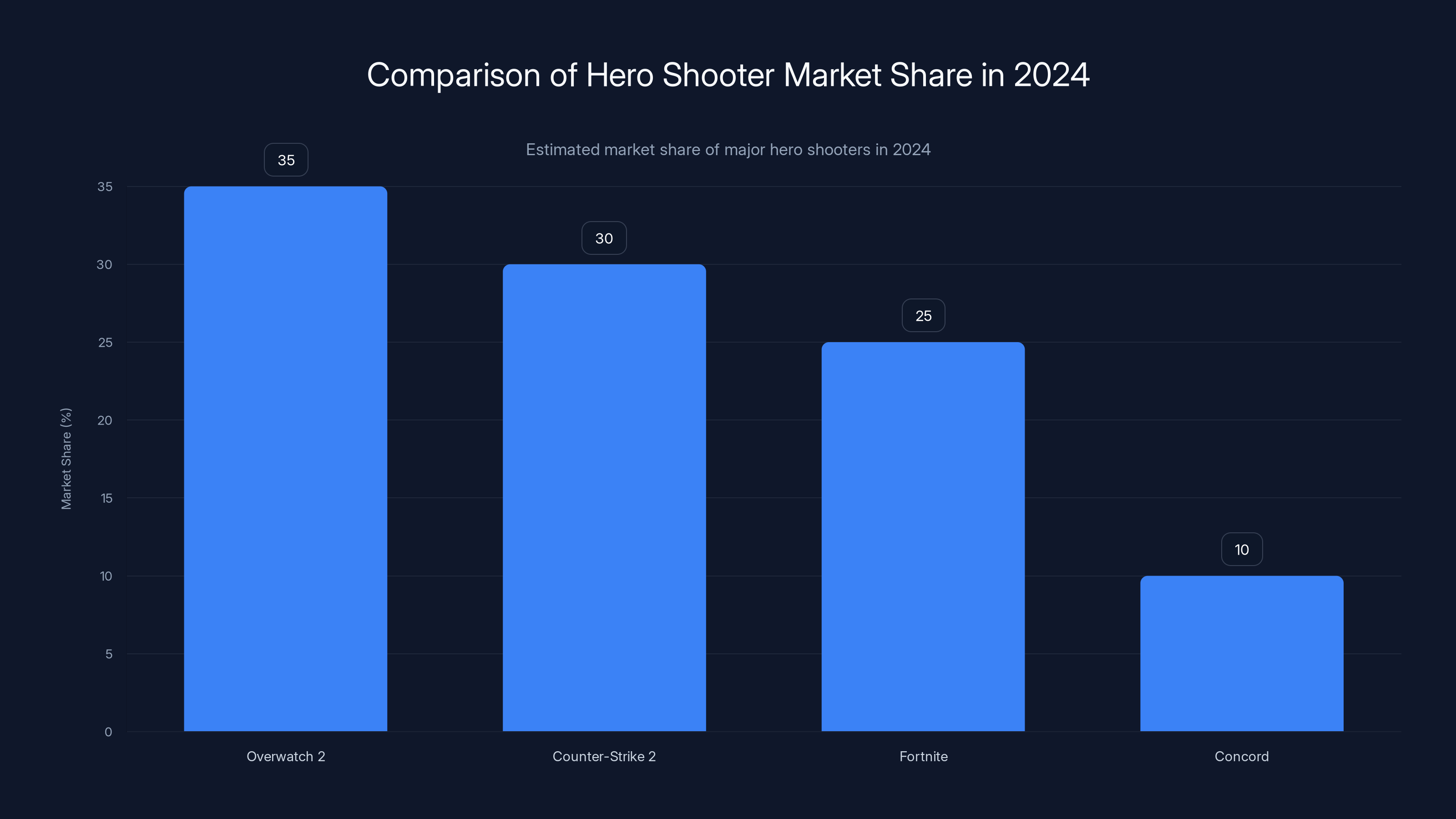

First, the market was saturated. In 2024, hero shooters were dominated by Overwatch 2 (free-to-play), Valve's Counter-Strike 2 (free-to-play), and Fortnite (free-to-play). Concord charged $40 upfront, then expected players to spend more on cosmetics. Why would a new player jump into an 8-year-old community of Overwatch 2 players when they could play the established game for free?

Second, the monetization model was out of step. Free-to-play games are the norm. A paid entry fee feels archaic. Even established franchises like Halo Infinite struggled with similar monetization friction.

Third, the game launched with minimal differentiation. If you've played Overwatch, you've essentially played Concord. The hero archetypes were familiar. The gameplay loop was familiar. There was no compelling reason to switch.

Fourth, Sony pulled the plug immediately rather than iterate. Instead of trying to salvage the game with free-to-play conversion or aggressive content updates, Sony simply deleted it. Two weeks. Gone. The decision made financial sense—continuing to operate a failing game would only burn more money—but it also sent a terrifying message to the industry: "If your game doesn't catch fire in the first 30 days, we're killing it."

The Concord failure had ripple effects. Publishers looked at their own pipelines and realized: If a company with Sony's resources, distribution power, and existing player base can't make a hero shooter work, what hope do we have? The response wasn't to innovate or take strategic risks. It was to abandon the category entirely and retreat to proven franchises.

EA's Tentpole Strategy: Why Sequels Are Safer Than Innovation

Electronic Arts has been executing this consolidation strategy longer and more aggressively than anyone else. They're the template the industry is copying.

EA's portfolio now centers on what they call "tentpole franchises"—games that are so established that they can carry an entire publisher's revenue. For EA, those are:

Battlefield: A military multiplayer franchise that's been around since 2002. After a catastrophic launch in 2042, EA dedicated massive resources to Battlefield 6, treating it almost like a complete reboot. The investment paid off. Battlefield 6 reportedly became the best-selling shooter of 2025, generating hundreds of millions in revenue.

EA Sports FC: The rebranded version of FIFA (EA lost the licensing agreement with FIFA after decades of partnership). EA Sports FC is now the dominant soccer simulation game and generates over $1.5 billion annually just from Ultimate Team packs and seasonal passes.

The Sims: A life simulation franchise that's been running since 1997. The Sims 4 is approaching 15 years old and still generates massive revenue through expansion packs and seasonal content. There's essentially no competition in this space.

What EA has abandoned or deprioritized: Mid-tier franchises, new IP experiments, and games that don't have built-in franchise potential.

This includes canceling a Black Panther game in development, which represented years of work with Marvel. The game probably would've been good. It might have sold 3 to 5 million copies. But 3 to 5 million copies isn't enough when your development costs are $150M+.

EA's formula is brutal in its efficiency: Identify which franchises are likely to become multi-generational cash cows. Allocate massive resources to those properties. Ignore everything else. Repeat.

The formula works financially—EA's stock price reflects strong shareholder returns—but it creates massive creative constraints. Every Battlefield game needs to iterate in ways that feel fresh to players while maintaining the core loop that made the franchise successful. Every EA Sports game needs to add just enough new features to justify a full-price annual release while not alienating players who spent thousands on previous versions.

Innovation becomes incremental. Risk becomes unacceptable.

Sony's Strategic Pivot: Fewer Games, Bigger Bets

Sony is in an interesting position. As a hardware manufacturer (PlayStation), they benefit from strong exclusive games that drive console sales. But as a software publisher, they're subject to the same economic pressures as EA and Ubisoft.

Sony's response has been to divide their game portfolio into two distinct categories:

Blockbuster franchises: These are games that either generate massive revenue or drive hardware adoption. This includes God of War, Spider-Man, Horizon, and Gran Turismo—franchises that sell 5 to 10+ million copies and command prices of

Live service experiments: These are the riskier bets, and they're getting riskier. Concord was supposed to be a live service hit. It wasn't. And Sony's response was to essentially abandon live service innovation for PlayStation for at least the next few years.

Sony's first-party studios are now structured around these two categories. And notably, first-party studios that can't contribute to either category are seeing reduced funding or being consolidated with other teams.

What's interesting about Sony's position is that they can actually afford to take more risks than EA or Ubisoft, because console sales and PlayStation Plus subscription revenue provides a cushion. But instead of using that advantage to fund experimental projects, Sony is applying the same risk-aversion logic: fewer swings, but each swing aims for the fences.

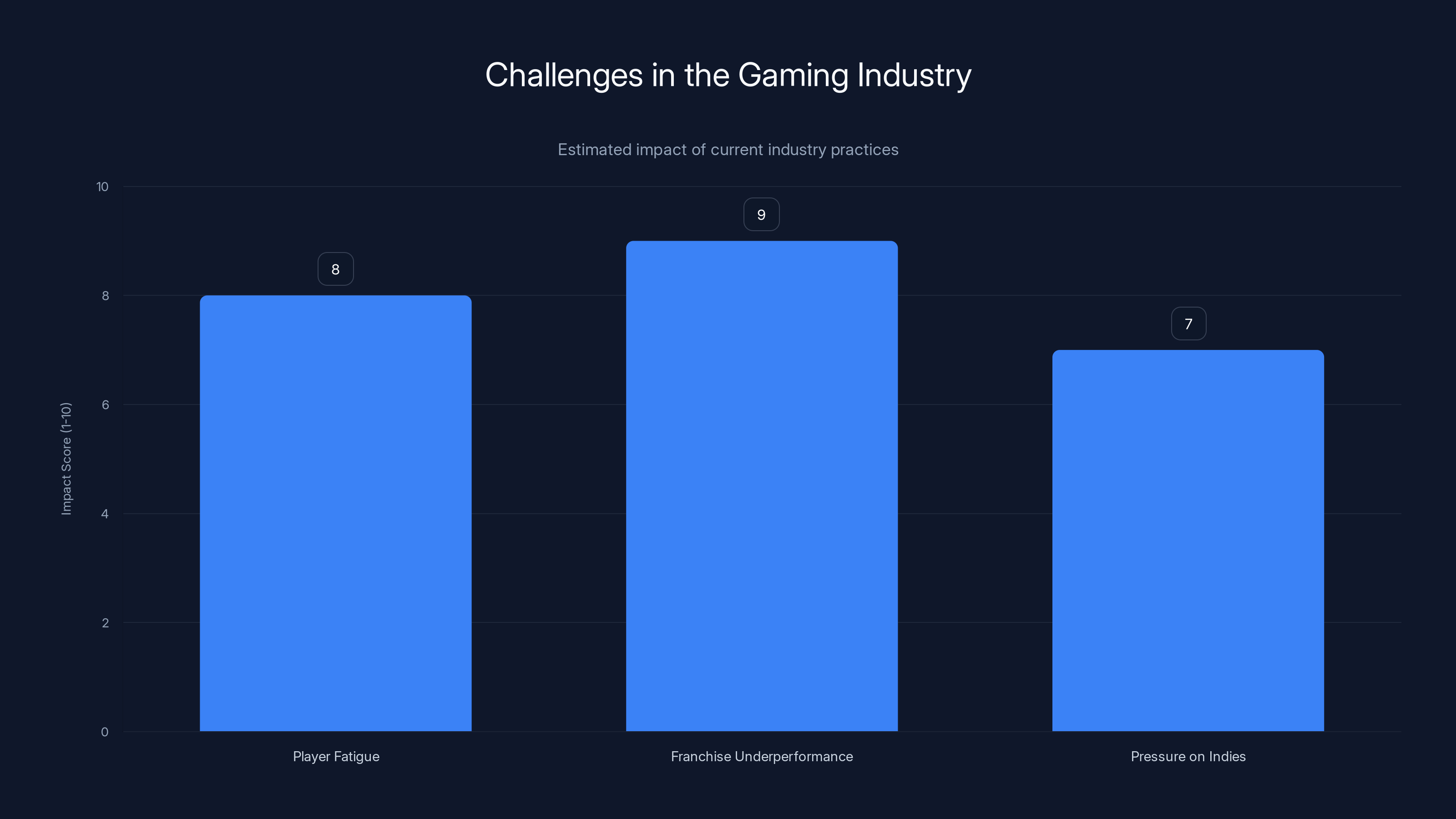

The gaming industry faces significant challenges, including high player fatigue, catastrophic risks from franchise underperformance, and pressure on smaller studios. Estimated data highlights these impacts.

Why This Strategy Is Fundamentally Unsustainable

Here's the thing that keeps economists and industry analysts awake at night: The industry is optimizing for short-term financial returns while destroying the conditions that create those returns.

The consolidation around proven franchises means fewer new IPs are getting developed. Fewer new IPs means fewer opportunities to discover the next massive hit. The gaming industry's best franchises—Minecraft, Fortnite, Among Us, PUBG—emerged from studios taking risks on experimental projects. Minecraft was developed by one person. Fortnite was originally a save-the-world PvE game that nobody cared about until Epic pivoted it to battle royale.

Now imagine those games being developed under current industry conditions. Minecraft would never get funded because "indie sandbox games don't have franchise potential." Fortnite would get canceled halfway through because the original PvE concept wasn't hitting engagement targets.

The industry is slowly painting itself into a corner where:

First, player fatigue sets in faster. If every game is either a sequel or iterative live service content, players burn out. The window to monetize shrinks. The pressure to add aggressive battle pass mechanics, cosmetics, and seasonal content intensifies. The games become more cynically designed, less fun, more predatory.

Second, when a franchise underperforms, the fallout is catastrophic. If you're betting everything on Assassin's Creed, and the next installment is received poorly, Ubisoft loses $300M+ and hundreds of jobs. There's no portfolio diversification. No safety nets. One bad release can spiral the company toward crisis.

Third, smaller studios and independent developers face existential pressure. Gamers have limited time and money. If the biggest publishers are releasing 10 AAA games per year, there's less attention and money for indie games. This concentrates market power, raises barriers to entry, and ultimately reduces the diversity of games being created.

Fourth, the talent pool shrinks. Junior developers, artists, and designers learn from working on diverse projects. If the only games being greenlit are sequels to established franchises, there's nowhere for junior talent to experiment, fail safely, and grow. Over time, this creates a cohort of designers with narrower experiences and less creative range.

The Risk-Aversion Feedback Loop

Joost van Dreunen, a games industry researcher at New York University, described the industry's current strategy perfectly: "It's a classic risk-aversion strategy. When markets get choppy, large publishers retreat to what they know works. It's a rational response to uncertainty, but it comes with real costs."

This is the feedback loop:

Step 1: One game fails. Concord launches and dies. Or Anthem underperforms. Or Cyberpunk 2077 launches with bugs and reputational damage.

Step 2: Financial analysis reveals the failure. The development costs were

Step 3: CFOs and boards get nervous. Shareholders demand explanations. Earnings calls become hostile. Stock prices decline. The CEO gets fired or steps down.

Step 4: Publishers become more risk-averse. The new leadership implements strict criteria for game greenlight: minimum franchise potential, minimum expected revenue of $500M+, maximum development risks.

Step 5: Experimental projects get killed. Promising games that don't fit the framework get canceled. Teams working on innovative but risky concepts get reassigned.

Step 6: The industry becomes more homogeneous. With fewer experimental games being made, trends cycle faster. Everyone copies the latest success. Games start feeling like variations on the same themes.

Step 7: Players notice and become fatigued. When every release feels like a reskinned version of something you've already played, engagement declines. Time-to-peak-users shrinks. Peak concurrency drops.

Step 8: Financial projections miss targets. The games that should have been hits underperform because players are burned out. Engagement falls below expectations. Revenue misses forecast.

Step 9: Loop repeats. Another game fails, and the feedback loop intensifies.

This isn't speculation. This is exactly what happened in the 1980s. The video game market was dominated by arcade publishers and console makers making sequel after sequel after sequel. Games became repetitive and exhausted. Player interest collapsed. The market crashed in 1983, and it took Nintendo's careful, quality-focused relaunch to rebuild trust. Recovery took nearly a decade.

What Games Are Being Sacrificed on the Altar of Franchises

When Ubisoft canceled six games, they sacrificed more than projects. They sacrificed potential.

One of those canceled games was the Prince of Persia: The Sands of Time Remake. That game was in development for years. It was supposed to be a high-quality, AAA reinterpretation of a beloved classic. By most accounts, it was shaping up to be good.

But "good" isn't good enough anymore. "Good" means selling 3 to 5 million copies. That generates maybe

Compare that to Assassin's Creed, which routinely sells 10+ million copies per installment, generating

From a spreadsheet perspective, killing the Prince of Persia remake is rational. From a creative industry perspective, it's devastating. Players who loved that original game now have no new experience to look forward to. A creative team that spent years developing something loses their project. The franchise essentially goes dormant.

Multiply this across six canceled games, and you start to understand the creative desert that the industry is creating.

What makes this even more frustrating is that some canceled games were from experienced, talented studios. Ubisoft has brilliant people working on projects that will never see light. Those developers will be reassigned, fired, or will leave for companies that still take creative risks.

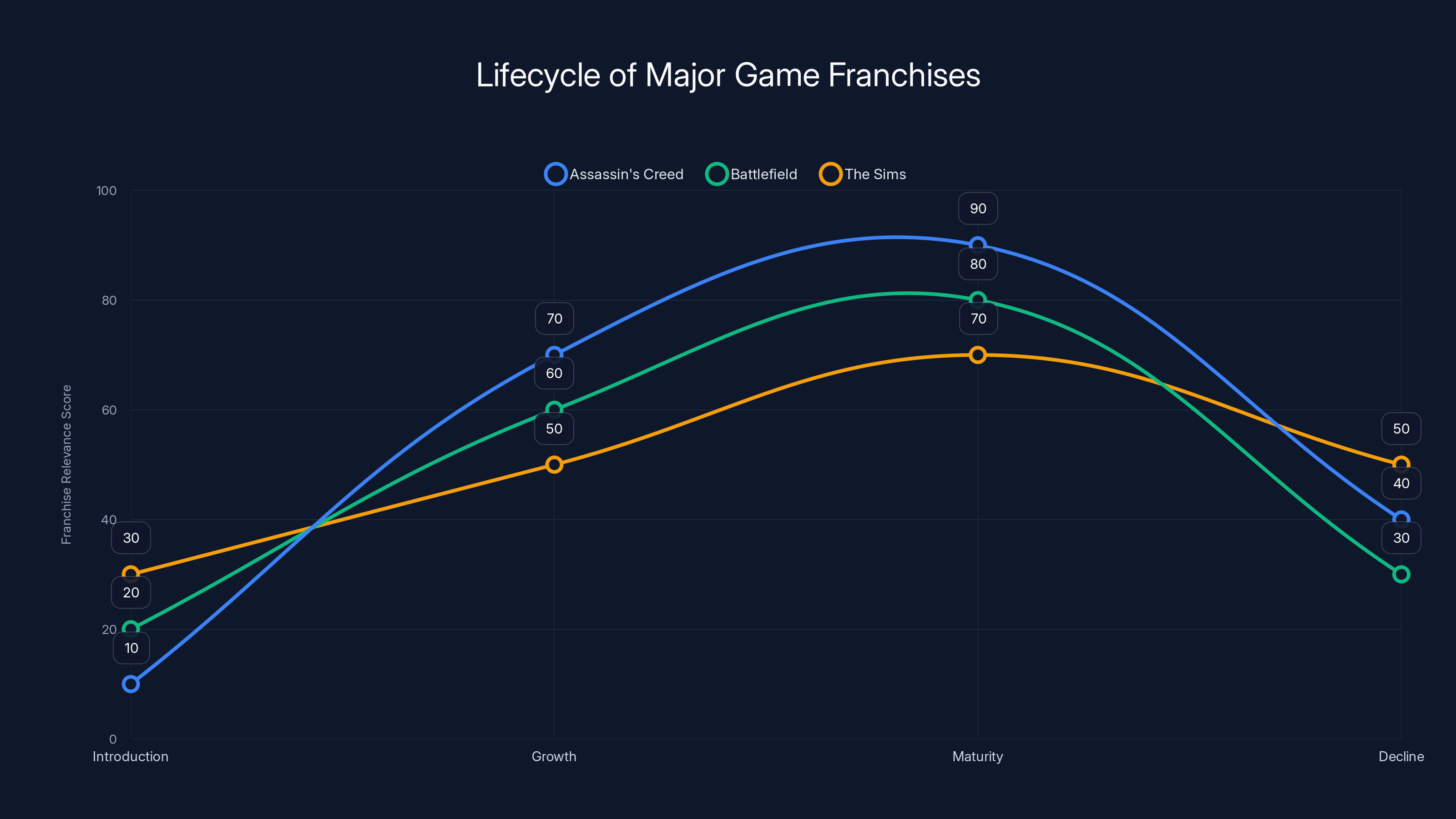

Estimated data shows that major game franchises follow a lifecycle with introduction, growth, maturity, and decline phases. Even successful franchises like Assassin's Creed, Battlefield, and The Sims face eventual decline, highlighting the risk of over-reliance on established franchises.

The Live Service Trap: Perpetual Content Treadmill

One consequence of this franchise consolidation is the explosion of live service games. If you're going to bet everything on one IP, you need to maximize its lifetime value. The way to do that is to keep the game alive with continuous content updates, seasonal passes, and cosmetics for 5 to 10 years post-launch.

Live service games sound great in theory. Players keep playing. Revenue streams never stop. The game evolves over time based on player feedback.

In practice, live service games are brutal for developers.

First, the content treadmill is relentless. Every season needs fresh cosmetics, new game modes, rebalanced mechanics, and bug fixes. This requires maintaining a full team post-launch indefinitely. If a live service game has 10 million active players, you need maybe 200+ developers, artists, and support staff working on it full-time, year after year.

Second, the pressure to monetize intensifies. As the game ages and novelty wears off, getting players to spend money on cosmetics or battle passes becomes harder. Publishers respond by making cosmetics more exclusive, battle passes more grindy, and seasonal content more aggressively time-gated. This erodes player goodwill and accelerates burnout.

Third, failed live service games become anchor points for failure. If you launch a live service game and it fails to reach engagement targets in the first 3-6 months, shutting it down becomes inevitable. But shutting down a live service game means every player who bought cosmetics or seasonal passes loses access to their purchases. The legal and reputational liability is massive.

Look at the disaster that was Anthem, BioWare's live service attempt. The game had fundamental design problems. Rather than iterate quickly, BioWare spent years trying to fix it. Eventually, EA pulled the plug, wasting years of developer effort and potentially hundreds of millions in investment.

The current trend is that publishers are doubling down on live service for established franchises while abandoning it for new concepts. This makes sense financially but creates a two-tier game market: either massive franchises with live service components, or small indie games. Everything in the middle dies.

How This Affects Game Design and Player Experience

When the industry is optimizing for franchise safety, game design itself changes in predictable ways.

Games become more formulaic. If your game needs to sell 10 million copies to justify its budget, you can't take risks with core game mechanics. You optimize for mass appeal. You dial back innovation. You make sure the game feels familiar enough that players understand it within the first hour.

Cosmetic monetization becomes aggressive. Without innovative gameplay to encourage continued engagement, games rely on cosmetics and seasonal battle passes to keep players invested. This means every character design, weapon skin, and cosmetic item is gated behind microtransactions.

Story takes a backseat. Narrative-driven games struggle in the live service model because linear stories end. You can't keep players engaged for five years on a story that concludes. So franchises like Call of Duty and Fortnite minimize story. The narrative becomes a backdrop to the multiplayer treadmill.

Graphics become the primary differentiator. If you can't innovate mechanically, you innovate visually. The industry invests heavily in ray tracing, uncompressed textures, and visual fidelity. This creates a graphics arms race where visual quality becomes the primary reason to upgrade to the next console generation. But graphical improvements have diminishing returns on player enjoyment.

Single-player experiences shrink. Live service games are multiplayer-focused because that's where monetization happens. Single-player campaigns become shorter, more linear, less ambitious. A game like The Witcher 3, which had a massive 100+ hour single-player experience with meaningful choices, would never get greenlit today. It's too big, too risky, requires too much development time, and doesn't have built-in recurring revenue.

The net effect is that games are becoming increasingly standardized. Visit any gaming forum, and you'll hear players complain that all new AAA games feel derivative, that innovation is dead, that gaming is less fun than it was five or ten years ago.

They're not entirely wrong. The industry's economic incentives are now actively working against innovation.

The Catch: Why Playing It Safe Isn't Actually Safe

Here's what van Dreunen says that most industry analysts won't: "This strategy might work for publishers with deep catalogs of beloved franchises, but it's not a guarantee of survival. It's more like buying time than building a sustainable future."

This is the critical insight that nobody in the industry wants to confront. The consolidation around franchises feels safe, but it's actually incredibly fragile.

Why? Because every franchise has a shelf life.

Assassin's Creed has been around since 2007. That's 18 years of annual releases and spin-offs. Player interest in the franchise has cycled multiple times. Some entries like Origins and Odyssey were massive hits. Others, like Syndicate, underperformed. If Ubisoft releases an Assassin's Creed game that reviews poorly or doesn't capture the zeitgeist, that franchise is suddenly worth significantly less.

Battlefield has been around since 2002. The franchise has had multiple false starts (2042 was widely considered a disaster). Players are fatigued with military shooters. How many more iterations can the franchise sustain before it becomes irrelevant?

The Sims hasn't had a new mainline entry since 2014 (Sims 4). It survives purely on expansion packs and seasonal content. But that revenue model depends on an ever-shrinking playerbase of people with decades-long emotional investment in the franchise. New players aren't jumping into a 10-year-old game when there are dozens of newer experiences available.

Even the biggest franchises have mortality dates. Not because they become bad, but because the market eventually moves on.

The industry's current strategy is betting everything on the assumption that these franchises will remain relevant and profitable indefinitely. But franchises are like any consumer product. They have adoption curves, peak periods, decline phases, and eventual obsolescence.

If you're a publisher with five major franchises and one of them becomes irrelevant, you've lost 20% of your revenue base. Now imagine that happening to two franchises simultaneously. Or three. You're looking at a crisis.

Compare this to a publisher with 20+ diverse franchises and properties. If two of them decline, you've only lost 10% of revenue, and you still have 18 others generating income. The risk is distributed.

The industry is doing the exact opposite. They're concentrating risk into fewer franchises. When one fails, the fallout is catastrophic.

Estimated data shows Concord held a minor 10% market share compared to established games like Overwatch 2 and Fortnite, which dominated the market in 2024.

Smaller Studios and Indies: The Wild Card

While EA, Ubisoft, and Sony consolidate around franchises, something interesting is happening at the edges of the industry.

Independent studios and smaller publishers are taking the risks that big publishers won't. This is where game innovation is actually happening right now.

Games like Baldur's Gate 3 (developed by Larian Studios, a relatively small studio), Elden Ring (from From Software, which is medium-sized but fiercely independent), and Hollow Knight (a tiny indie team) have become some of the most critically acclaimed and commercially successful games of recent years.

These games succeeded because they did something different. They took creative risks. They had distinct visions. They weren't trying to be everything to everyone. They found specific niches and dominated those niches with exceptional execution.

This creates an interesting market dynamic: Big publishers are consolidating around safe bets. Indie developers are filling the vacuum with innovative, risky, niche games. Players who want genuine novelty are increasingly turning to indie titles. This gradually shifts mindshare and revenue away from AAA publishers toward indie developers.

Over 10-20 years, this could fundamentally reshape the industry. The AAA market becomes a stable, mature market of franchise sequels. The indie market becomes the primary source of innovation and growth.

But this transition comes with a cost. Indie games generally have smaller budgets, which means less sophisticated technology, smaller teams, and fewer resources for marketing. The barrier to entry for indie developers is lower, but the barrier to profitability is still high.

The Future: Either Consolidation Collapses or Creativity Dies

The industry is heading toward one of two futures.

Future One: The Consolidation Fails. Publishers bet too heavily on aging franchises. One or two major franchises decline or become irrelevant. Revenue crashes. Publishers lay off massive numbers of staff. The industry contracts sharply. Investors lose confidence. A few survivors emerge from the wreckage, hopefully having learned that risk diversification is more sustainable than franchise concentration.

This happened in 1983. The industry crashed hard and took years to recover. There's a reasonable chance it happens again.

Future Two: The Consolidation Works, But Creativity Suffers. Publishers successfully manage their franchise portfolios. Revenue remains stable or grows. But the cost is industry-wide stagnation. New ideas become rarer. Games feel increasingly derivative. The industry becomes more like Hollywood: a small number of massive studios making expensive franchises, while creativity happens primarily in independent and international projects.

This isn't necessarily a bad outcome for players who enjoy AAA franchises. But it closes doors for developers who want to experiment, innovate, and take risks at scale.

What makes this particularly frustrating is that the risk-aversion strategy isn't based on player demand. Players consistently ask for fresh IPs, innovative gameplay mechanics, and creative risks. Publishers respond by making more sequels. This mismatch between what players want and what publishers deliver suggests that the industry's decision-making is driven by financial engineering, not creative vision or player satisfaction.

The video game industry is at an inflection point. The current strategy maximizes short-term returns at the cost of long-term innovation and sustainability. It's a viable strategy for the next 5-10 years, but eventually—and maybe sooner than anyone expects—it will hit a wall.

What This Means for Game Developers

If you're a game developer, this consolidation trend has direct implications for your career.

First, opportunities are narrowing. The number of major game projects being greenlit is shrinking. Games that don't fit into franchise slots are being canceled. This means fewer job openings, more competition for remaining positions, and less opportunity for junior developers to break in.

Second, creative freedom is declining. Most of the remaining jobs are on established franchises where the core mechanics, narrative themes, and gameplay loops are already defined. You're implementing within constraints, not creating from scratch. This can be satisfying work, but it's less creatively fulfilling for many developers.

Third, stability is questionable. When a game ships and underperforms, entire studios get shut down. The Concord shutdown eliminated Firewalk Studios entirely. These aren't small teams. These are hundreds of people who suddenly have no job. Working for a AAA publisher increasingly feels like a high-wire act where one failure can end your tenure.

What's interesting is that developers with this understanding are increasingly leaving AAA studios for indie projects, middle-tier publishers, or completely different industries. This exodus of experienced talent further erodes the creative capacity of AAA studios, which then accelerates the creative decline.

For aspiring developers, the message is: If you want creative freedom and stable employment, consider indie development, middle-tier publishers, or international studios. The AAA industry is becoming increasingly hostile to both.

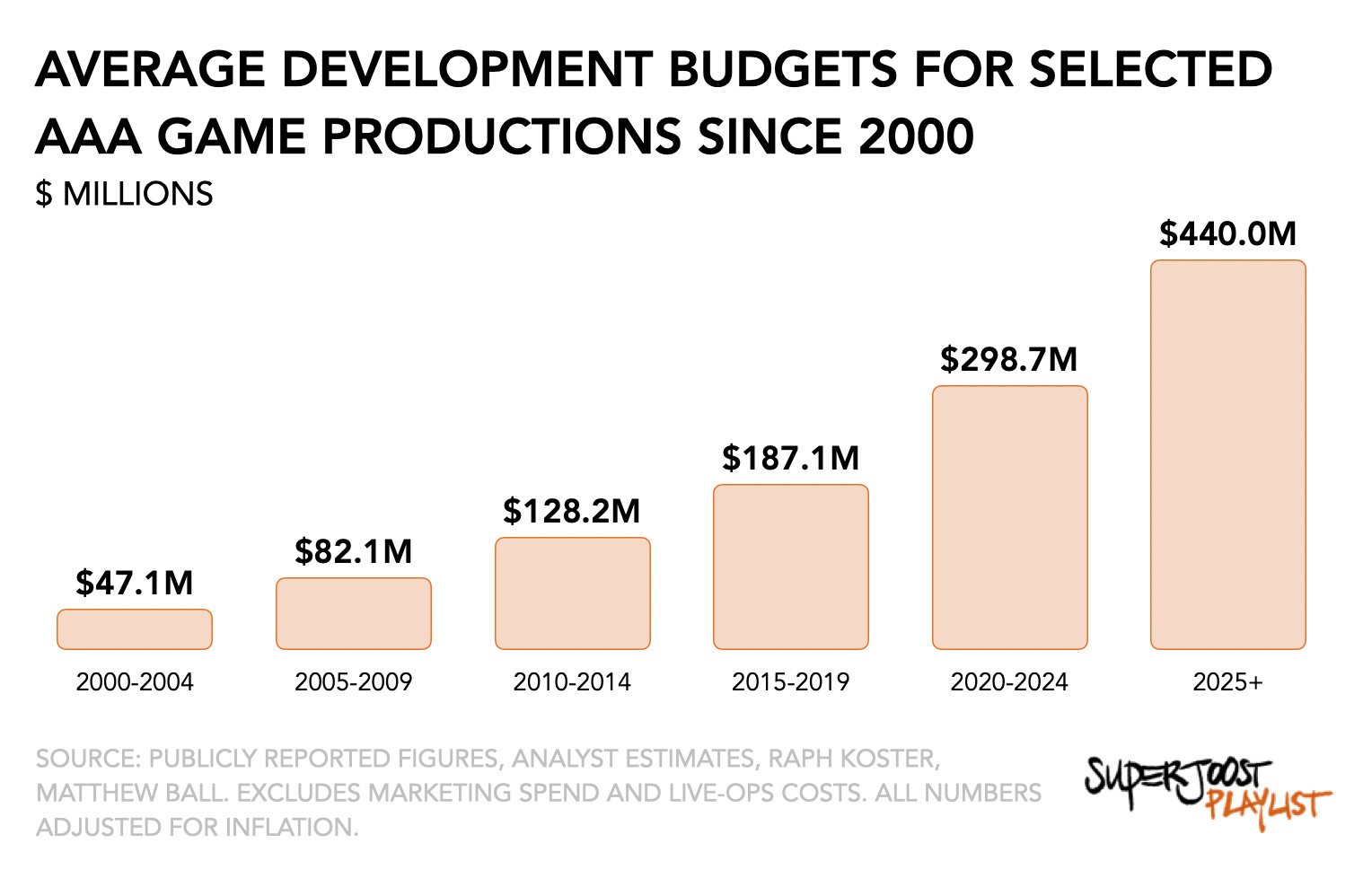

The cost of developing and marketing AAA games has significantly increased over the past decade, with development costs rising from

How Players Are Responding

Player sentiment is shifting in response to this industry trend. Several signals indicate growing frustration:

Franchise fatigue is real. Players are tired of annualized sequels with minimal innovation. Call of Duty, Sports games, and Assassin's Creed entries are seeing declining first-month sales and decreasing engagement as the games age. Players are explicitly saying they don't want annual releases anymore.

Indie games are gaining mindshare. Games like Baldur's Gate 3, Hades, Stardew Valley, and Valheim have attracted massive audiences partly because they offer something different from AAA franchises. The success of these titles proves there's enormous demand for novel experiences.

Live service games are declining in trust. After years of aggressive monetization, failed live service shutdowns, and poor balance changes, players are increasingly skeptical of live service promises. They're less likely to invest heavily in cosmetics or battle passes for games they don't trust will exist in 3 years.

Game Pass and subscription services are changing purchase patterns. As players increasingly access games through subscription services rather than purchasing individually, the importance of owning specific games declines. This reduces the revenue pressure on individual titles and makes it easier to take risks on smaller franchises or new IPs.

These trends suggest that player expectations are diverging from what publishers are offering. Over time, this creates an opportunity for publishers willing to serve those unmet demands. The question is whether the AAA industry will adapt or whether the void will be filled entirely by indie developers and mid-tier studios.

The Role of Development Tools and Technology

One factor that could disrupt this trend is the evolution of game development tools and technology.

If game development becomes significantly cheaper and faster—because of improved engines, better automation tools, or more efficient pipelines—the economics of the industry change dramatically. Suddenly, you can make AAA-quality games with smaller budgets. That enables more creative risk-taking.

We're seeing hints of this. Unreal Engine 5 introduced features that reduce animation work, asset creation work, and optimization work. Unity continues to improve performance and ease-of-use. Blender, an open-source 3D creation tool, has become sophisticated enough to compete with expensive professional tools.

If these tools continue improving at their current rate, we might see a bifurcation: expensive, high-end AAA experiences that require massive budgets, and high-quality mid-tier games that can be made with teams of 50-100 people instead of 300+.

This would be healthy for the industry. It would expand the middle market, create more opportunities for developers, and reduce the risk concentration in the hands of a few franchises.

But this requires tool developers and independent studios to execute flawlessly while major publishers remain focused on franchise management. That's a lot to expect.

International and Independent Market Dynamics

While Western AAA publishers consolidate around franchises, something different is happening internationally.

miHoYo (now Hoyoverse), a Chinese game studio, created Genshin Impact and Honkai: Star Rail, both of which have become global phenomena. These games are AAA in scope and visual quality but were developed with philosophy more aligned with player experience than Western publishers.

Japanese studios like Nintendo have consistently prioritized creative innovation over franchise consolidation. Games like Breath of the Wild and Tears of the Kingdom broke genre conventions and became some of the most successful games ever made.

South Korean and Southeast Asian studios are producing high-quality games that compete with Western AAA titles but with more innovative mechanics and different cultural influences.

This international diversity is healthy for the overall gaming ecosystem. It means that even as Western publishers consolidate, there are alternative creative centers producing fresh experiences. Players can seek out these alternatives. Developers can find opportunities outside of EA, Ubisoft, and Sony.

Over the next decade, the balance of power in the gaming industry might shift toward international publishers that are willing to take creative risks. This would fundamentally reshape the industry and could break the franchise consolidation trend.

The Sustainability Question: Can This Last?

Let's address the fundamental question: How long can the gaming industry sustain this consolidation strategy?

The honest answer is: Probably not more than 10-15 years before it hits serious problems.

Here's why:

Franchise lifespans are finite. Every franchise eventually becomes irrelevant or oversaturated. When major franchises start declining (and they will), publishers won't have a portfolio of alternatives to fall back on. They'll face revenue crises with few options.

Player sentiment is shifting. Players want new experiences, not more sequels. Long-term, publishers that ignore this preference risk losing audience trust and relevance.

Creative talent is exhausted. Game development is already a high-burnout industry. Making annual sequels to established franchises is less creatively fulfilling than working on original projects. Developers will continue leaving AAA studios, which erodes the creative capacity needed to maintain franchises effectively.

Indie competition is intensifying. As more talented developers join indie studios, the quality gap between AAA and indie games shrinks. Players increasingly ask: "Why pay $70 for an Assassin's Creed sequel when I can buy five innovative indie games for the same price?"

Technology is democratizing. Better tools mean smaller teams can create higher-quality games. This reduces the cost advantage that drives AAA consolidation.

The current strategy works as a financial optimization model, but it's not sustainable long-term. The industry is effectively harvesting existing IP at the cost of developing new IP. Eventually, that harvest will decline.

When it does, publishers that have invested in diverse franchises and creative talent will be better positioned than publishers that have consolidated everything into a few tentpole series.

FAQ

What is a "billionaire franchise" and how does it differ from other game franchises?

A billionaire franchise is a video game series that has generated over

Why did Concord fail so catastrophically, and what lesson did the industry learn?

Concord failed because it was a premium hero shooter (requiring a

What is the difference between live service games and traditional single-player games, and why are publishers favoring live service?

Traditional games have a defined endpoint. You complete the story, finish the campaign, reach max level. The game ends. Publishers then move on to the next title. Live service games are designed to never end. They receive continuous updates, seasonal content, new characters, and cosmetics indefinitely. Publishers prefer live service games because they generate recurring revenue. A player might spend

How does development cost inflation affect game design and player experience?

When development costs rise from

What happened to other big gaming companies like Activision and Blizzard during this industry consolidation?

Activision Blizzard has faced unique challenges beyond the industry consolidation trend. The company faced serious workplace misconduct allegations and scandal, which damaged its reputation with players and employees. Their flagship franchises (Call of Duty, World of Warcraft, Overwatch) all faced declining engagement or failed launches during this period. In January 2023, Microsoft completed a $68.7 billion acquisition of Activision Blizzard, making it the largest video game acquisition in history. Microsoft's consolidation of Activision further concentrated industry power in the hands of a few mega-corporations. The acquisition itself reflects the trend toward consolidation, though it's driven more by corporate strategy than the franchise-focused strategy we're discussing with Ubisoft and EA.

Are there any successful recent games that broke the "proven franchise" rule and launched as new IP?

Yes, but they're increasingly rare. Baldur's Gate 3 is a recent example—though technically it's based on Dungeons & Dragons, which is established IP, the game was a fresh entry in that universe. Hades, developed by Supergiant Games, was entirely new IP and became wildly successful—but it was developed by a relatively small indie studio with modest budget. At the AAA level, genuinely new IP launches are vanishingly rare. Most AAA games now either iterate on established franchises or build on IP from other media (movies, books, comics). This suggests that the consolidation toward proven franchises is real and structural, not temporary.

How does the consolidation trend affect game prices and the cost to consumers?

Consolidation toward blockbuster franchises creates pressure to raise prices to justify increasing development budgets. Standard AAA game prices have increased from

What role do engine licensing fees play in the high costs of AAA game development?

Unreal Engine 5 charges a 5% royalty on gross game revenue (after the first

Conclusion: The Industry's Reckoning Is Coming

The gaming industry's shift toward fewer, bigger, safer games is economically rational in the short term. It's a perfectly logical response to rising costs, market uncertainty, and financial pressure from shareholders.

But it's unsustainable.

Every industry that has pursued this consolidation path—relying on a shrinking number of tentpole products while abandoning the middle market—has eventually faced reckoning. Publishers that fail to innovate eventually lose player interest. Franchises that become stale get replaced by fresh competitors. And when the reckoning comes, it comes hard.

The good news is that the gaming industry has proven it can recover and evolve. The bad news is that recovery requires acknowledging the problem before catastrophe strikes, and most of the industry leadership is too focused on quarterly earnings to make that acknowledgment.

So the consolidation will continue. More franchises will be killed. More experimental projects will be canceled. More developers will be laid off. More creative talent will leave AAA studios. And slowly, almost imperceptibly, the industry will become less innovative, less diverse, and less interesting.

Until it breaks.

When it does, the studios that invested in creative talent, diverse franchises, and genuine innovation will emerge stronger. The studios that consolidated everything into a few tentpole franchises will face existential crises.

The question isn't whether this cycle will happen. The question is when, and which publishers will survive it.

For now, the industry keeps swinging harder with fewer, bigger bets. We're all watching to see if the final swing connects or if the entire house of cards comes crashing down.

One thing is certain: the status quo can't last forever. The laws of economics and human nature eventually reassert themselves, and when they do, the gaming industry will transform in ways nobody currently predicts.

Key Takeaways

- AAA game development costs have ballooned from 80M a decade ago to300M today, forcing publishers to consolidate around proven franchises

- Concord's $200M failure and rapid shutdown terrified the industry into abandoning live service innovation and consolidating around safe bets

- Ubisoft, EA, and Sony are now exclusively greenlight games attached to established franchises, canceling new IP and mid-tier projects

- This risk-aversion strategy feels safe short-term but creates fragility: when one major franchise declines, publishers have no alternatives

- The consolidation trend is destroying industry innovation, driving talent away from AAA studios, and creating opportunity for indie developers