Google's Historic Antitrust Appeal: Understanding the Search Monopoly Case and Its Global Impact

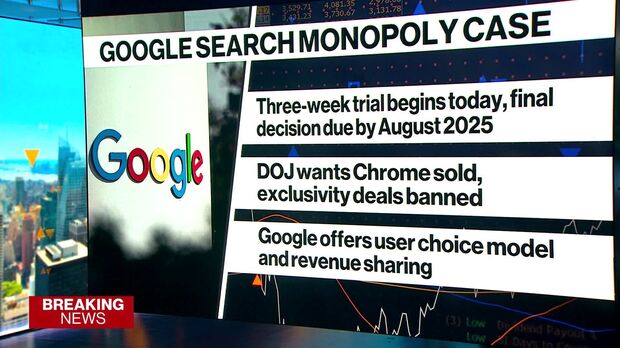

In a pivotal moment for digital competition and regulatory oversight, Google formally appealed a federal court's decision declaring it an illegal monopolist in online search services. This appeal, filed in late 2024 following Judge Amit Mehta's groundbreaking August 2024 ruling, represents one of the most significant antitrust battles since the United States versus Microsoft litigation of the 2000s. The case fundamentally challenges whether Google's dominance in search—commanding approximately 92% of the global search market share—results from superior products and innovation or from anticompetitive exclusionary practices.

The implications extend far beyond a single company's regulatory standing. At stake is the future structure of the internet itself, the definition of fair competition in digital markets, and whether the remedies ordered by the court can restore meaningful choice to billions of users worldwide. Google's appeal argues that the ruling "ignored the reality that people use Google because they want to" and that court-ordered remedies would "risk Americans' privacy and discourage competitors from building their own products." Conversely, the U. S. Department of Justice maintains that without intervention, Google's durable monopoly will continue to entrench itself, preventing innovation and limiting consumer choice.

This comprehensive analysis examines Judge Mehta's monopoly findings, the specific remedies under appeal, Google's strategic arguments for reversal, the timeline for resolution, and the broader implications for technology competition. We'll also explore how this case influences the search landscape and why alternative solutions matter in understanding future internet dynamics.

The August 2024 Monopoly Ruling: What Judge Mehta Decided

The Core Finding: Illegal Monopoly Status

Judge Amit Mehta's decision in August 2024 made an unambiguous pronouncement: Google maintained an illegal monopoly over "general search services" and "general search text advertising". This finding didn't emerge from speculation or theoretical arguments but from detailed examination of market dynamics, contractual arrangements, and competitive barriers. Mehta's analysis revealed that Google's dominance wasn't accidental but rather resulted from deliberate, anticompetitive conduct spanning two decades.

The ruling synthesized complex economic evidence showing that Google controlled the market through a combination of technical excellence and exclusionary agreements. Users gravitated toward Google because it provided superior search results—a point Google emphasized throughout the trial. However, Mehta found that Google simultaneously used its dominance to foreclose rivals from reaching consumers through contractual arrangements that made switching economically irrational for partners. The judge's language was particularly striking: "These are Fortune 500 companies, and they have nowhere else to turn other than Google."

This statement captured the essence of the monopoly finding. Apple, Mozilla, Samsung, and other major technology companies had theoretically concluded they could promote competing search engines. In practice, the economics made it impossible. The revenue sharing arrangements Google offered—reportedly worth billions annually to Safari and Mozilla alone—created dependency relationships that competitors couldn't overcome without years of independent research and development investment with uncertain returns.

Exclusive Default Arrangements and Distribution Control

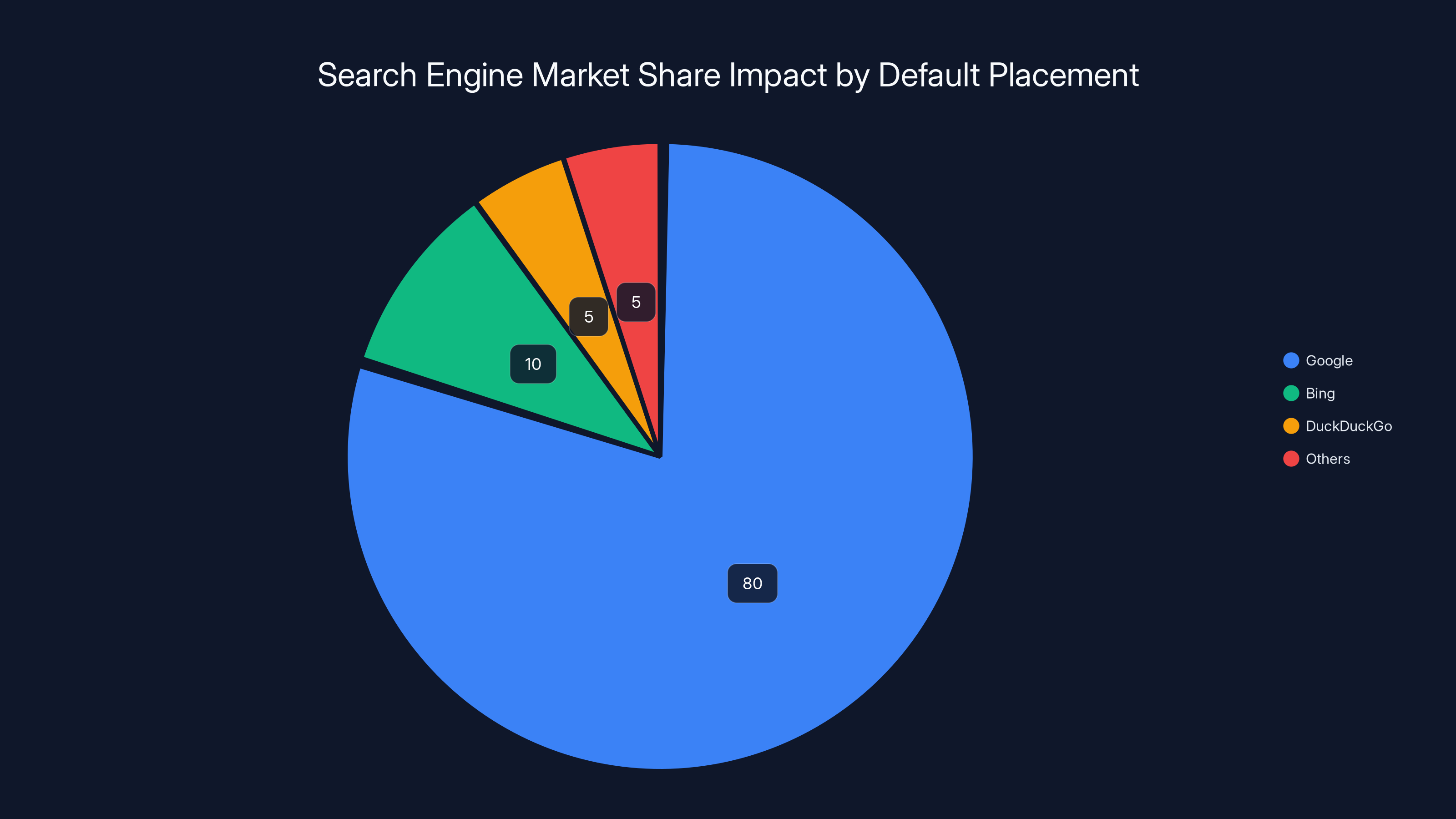

Mehta identified specific mechanisms through which Google maintained its monopoly. The most significant involved exclusive default search agreements with major browsers and device manufacturers. When you open Safari on an iPhone or Firefox on a computer, Google appears as the default search engine not by accident but because Apple and Mozilla signed agreements making it so. These defaults matter enormously—studies consistently show that 87% to 94% of search queries use the default engine, meaning that becoming the default essentially determines market share.

Google paid extraordinary sums for these positions. The government estimated that in 2021 alone, Google spent approximately $26.3 billion on default placements—roughly 15% of Google's total annual revenue. This wasn't spending on product development, customer service, or infrastructure. It was pure exclusionary spending designed to prevent rivals from accessing distribution channels. No competitor could afford to match these payments. Microsoft's Bing, despite backing from a company with nearly equivalent financial resources, struggled to gain traction partly because Microsoft couldn't match Google's default payments.

Judge Mehta found that these arrangements harmed competition in ways that ultimately hurt consumers. By ensuring no competitor could achieve scale through default placement, Google eliminated the pathway through which a rival might have developed competitive search technology. Bing exists because Microsoft possessed extraordinary resources and patience; smaller competitors attempting to challenge Google faced insuperable barriers.

The "Durability" Finding and Network Effects

One of Mehta's most important findings concerned the durability of Google's monopoly. The judge concluded that Google had created "enduring" market dominance that wouldn't erode even if competitors offered superior products. This durability arose from network effects and switching costs that created structural barriers to competition.

Network effects in search function differently than in social media. When more people use a search engine, more content creators optimize for it. More optimization means better results. Better results attract more users. This virtuous cycle can entrench market leaders. Additionally, Google's extended dominance meant it accumulated unprecedented amounts of search data—data showing what users searched, what results they clicked, and how they refined queries. This data, accumulated over two decades, provided advantages that newer competitors couldn't replicate quickly.

Switching costs reinforced durability. Users grow accustomed to Google's interface, search syntax, and result presentation. Trying a new search engine involves learning new approaches with no guarantee of better results. These psychological and practical switching costs, multiplied across billions of users, create friction that benefits incumbents. Mehta recognized that unless something changed—unless courts intervened—users would continue defaulting to Google, partners would continue signing with Google, and the monopoly would persist indefinitely.

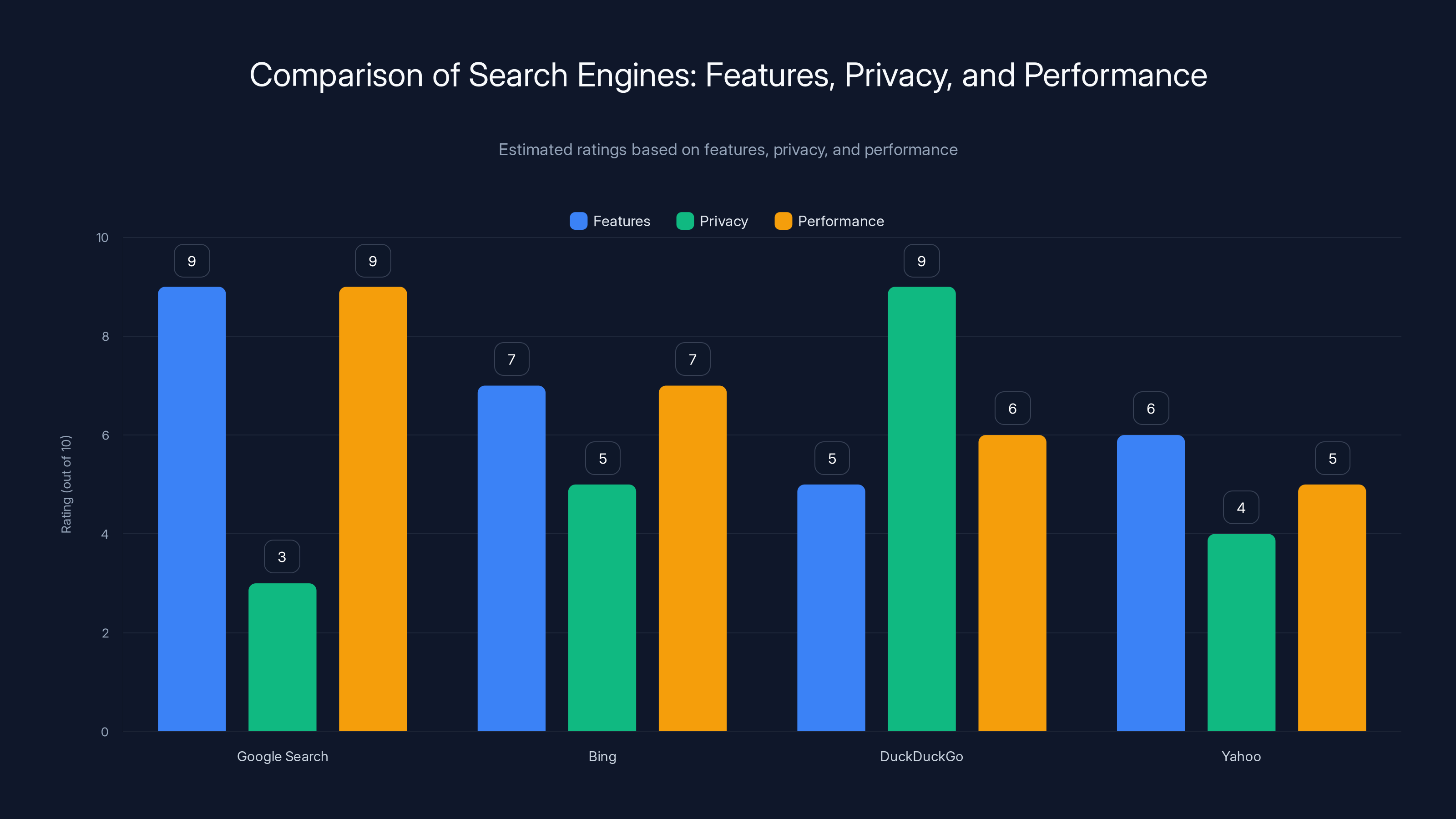

Google Search leads in features and performance but lags in privacy, while DuckDuckGo excels in privacy. Estimated data based on general perceptions.

The September 2024 Remedies Decision: What Google Must Do

Data Sharing Requirements and Search Syndication Obligations

Following his monopoly findings, Judge Mehta issued a detailed remedies decision in September 2024 designed to restore competition. Rather than break up Google—which the government had requested—Mehta imposed what he considered a more measured approach: forced data sharing and search syndication obligations.

The most significant remedy requires Google to share search data with competitors in standardized formats. This data includes user search queries, click behavior, and result relevance signals. Competitors have long argued that Google's data advantages represent insurmountable barriers. A new search engine needs to understand what queries mean, what results users find relevant, and how search patterns evolve over time. Google accumulated this understanding through decades of operation. New competitors start from zero.

By requiring Google to share anonymized, aggregated search data, Mehta aimed to level the playing field. Competitors could use this data to train machine learning models, understand search intent, and identify gaps in current search results. The remedy didn't hand competitors Google's proprietary algorithms or ranking systems, but it provided the information necessary to build competitive alternatives.

The second major remedy involves search syndication obligations. Google would be required to offer its search results to other platforms—news aggregators, travel sites, job boards—on non-exclusive, reasonable terms. Currently, many platforms compete with Google or lack sufficient traffic to negotiate favorable terms. Forced syndication would allow more competition in specialized search categories while giving smaller platforms access to high-quality search results.

Restrictions on Search Default Practices

Mehta also imposed restrictions on how Google can arrange default placements. The specific provisions included requirements that Google negotiate separately with different platforms rather than bundling services, limits on exclusive dealing arrangements, and transparency obligations regarding revenue sharing. These restrictions aimed to create space for competitors to reach users through default channels.

The judge rejected the government's request to force Google to divest Chrome, concluding that the remedy of data sharing and syndication requirements could achieve competitive effects without the disruption of a forced sale. This decision represented a significant victory for Google, as forced divestiture would have fundamentally restructured the company. However, the remaining remedies remained substantial and costly to implement.

Google's Appeal Strategy: The Core Arguments

The "People Choose Google" Argument

Google's primary appeal argument centers on user choice. The company contends that billions of people use Google Search not because they're forced to but because they prefer it. Google Vice President Lee-Anne Mulholland stated: "The decision failed to account for the rapid pace of innovation and intense competition we face from established players and well-funded start-ups."

This argument contains statistical grounding. Google's share of search has remained stable or grown because users consistently choose it, even when alternatives exist. On most devices, changing the default search engine takes seconds—yet users rarely do so. If Google's dominance resulted purely from anticompetitive default arrangements, wouldn't users switch once they discovered superior alternatives? The fact that they don't suggests that exclusive defaults aren't the entire explanation.

Google also emphasizes that it faces genuine competition from established players like Microsoft (Bing), Amazon, and emerging AI-powered search providers. Chat GPT, despite being fundamentally different from traditional search, diverts search queries. Specialized search services (job boards, travel sites, shopping platforms) cannibalize specific categories of Google Search queries. In this view, Google's market share reflects success in competition, not anticompetitive conduct.

Privacy and Innovation Concerns

Google argues that data sharing requirements would harm user privacy by forcing the company to distribute sensitive search information more broadly. The company contends that forcing it to syndicate search results on non-exclusive terms would reduce incentives for competitors to develop their own search capabilities, thereby stifling innovation.

These arguments deserve serious consideration. Search data is sensitive—it reveals intimate information about users' health conditions, financial situations, legal problems, and personal interests. Distributing this data, even in anonymized and aggregated form, creates risks. Competitors who receive this data might not implement equivalent privacy protections. Privacy breaches could harm the very users the remedies are intended to protect.

The innovation argument operates similarly. If competitors can license Google's search results rather than building their own capabilities, they have less incentive to invest in fundamental research. The remedy might preserve competition at the margin while reducing innovation in search technology itself.

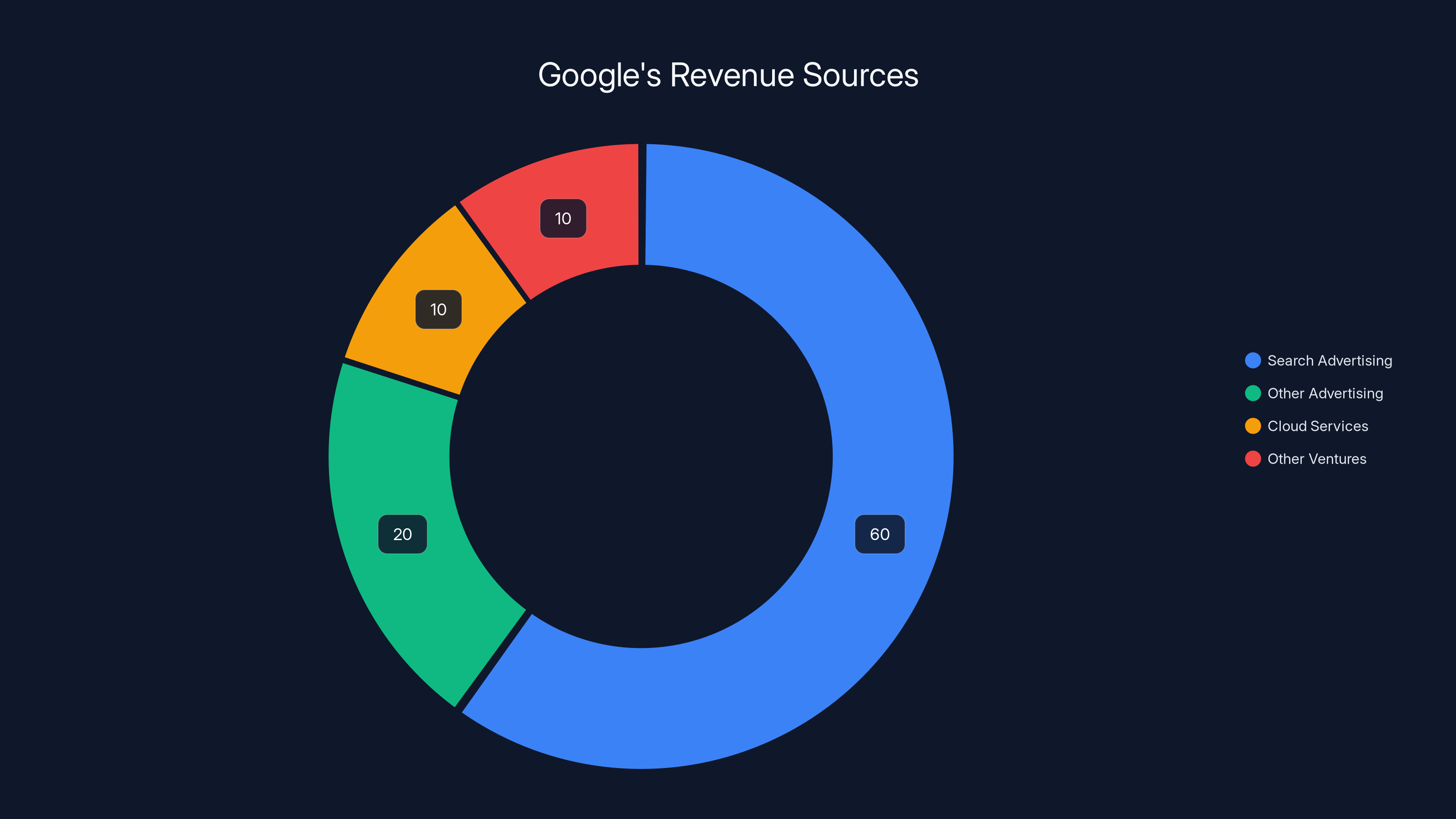

Search advertising constitutes approximately 60% of Google's revenue, highlighting its critical role in the company's financial model. Estimated data.

The Timeline: How Long Will This Case Take?

Appeal Process and Expected Duration

Google's appeal will almost certainly extend the case several additional years. The company filed a notice to appeal in late 2024, initiating a process that typically requires 18 to 36 months before appellate courts issue decisions. Given the case's complexity and significance, timelines at the longer end of that range are more likely.

First, the case goes to the U. S. Court of Appeals for the District of Columbia Circuit. This appeals court handles federal regulatory matters and understands antitrust law deeply. The court will review whether Judge Mehta correctly applied antitrust principles to the facts he found. Google will argue that the judge misapplied law; the Department of Justice will defend the decision.

The D. C. Circuit doesn't retry the case or re-examine evidence. Instead, it asks whether the lower court's legal analysis was sound and whether findings of fact had adequate support in the record. For Google's appeal to succeed, it must convince a three-judge panel (or potentially the full court in an "en banc" review) that Mehta committed legal error.

Most observers expect the D. C. Circuit process to take 18 to 24 months, followed by potential Supreme Court review if either party files a petition. The Supreme Court receives thousands of petition applications annually and accepts approximately 70 to 80 cases. An antitrust case of this magnitude and public importance would likely attract Court attention, but the Justices might also view it as a matter better left to lower courts and Congress.

If the Supreme Court accepts the case, another two to three years would elapse before a decision. This means the entire appellate process could extend until 2027 or 2028—roughly a decade after the original Department of Justice lawsuit.

Interim Remedies and Pausing Provisions

Google has asked courts to pause or stay the remedies pending appeal. This is a crucial request—if granted, Google wouldn't have to implement the data sharing and syndication requirements while appeals proceed. The company argues that implementing costly measures, then reversing them if the appeal succeeds, would waste resources.

Courts rarely stay remedies in antitrust cases, as doing so allows alleged monopolists to continue harmful conduct indefinitely. However, Google's arguments about implementation difficulty and the risk of irreversible disruption carry some weight. Courts might stay some remedies while allowing others to proceed, or might allow limited, supervised implementation while the case continues.

The practical effect of any stay would be to preserve Google's current market position unchanged, giving the company continued opportunities to entrench its monopoly through continued exclusive default payments and contractual arrangements.

Market Analysis: Google's Current Dominance and Competitive Landscape

Global and Regional Search Market Share

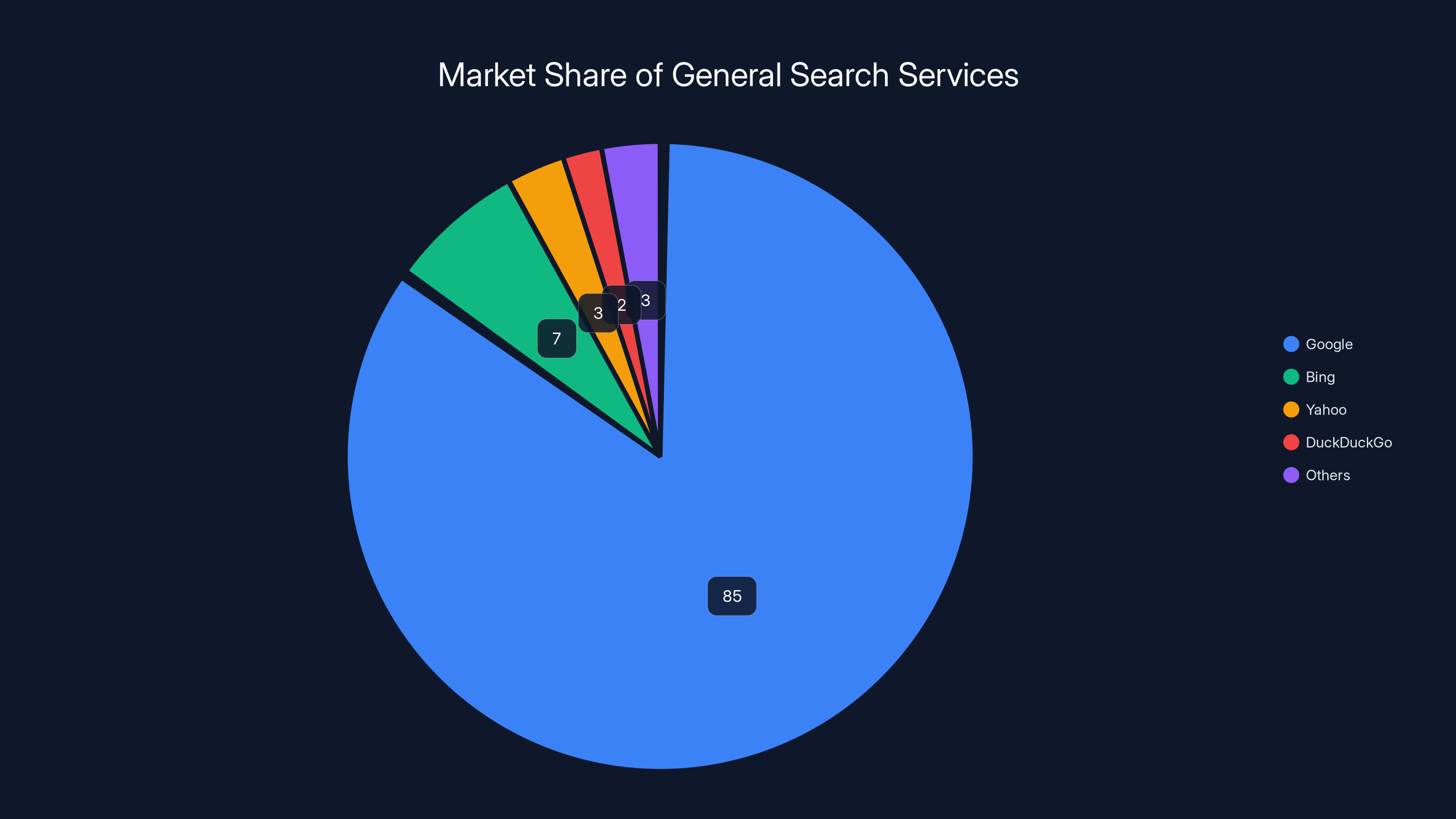

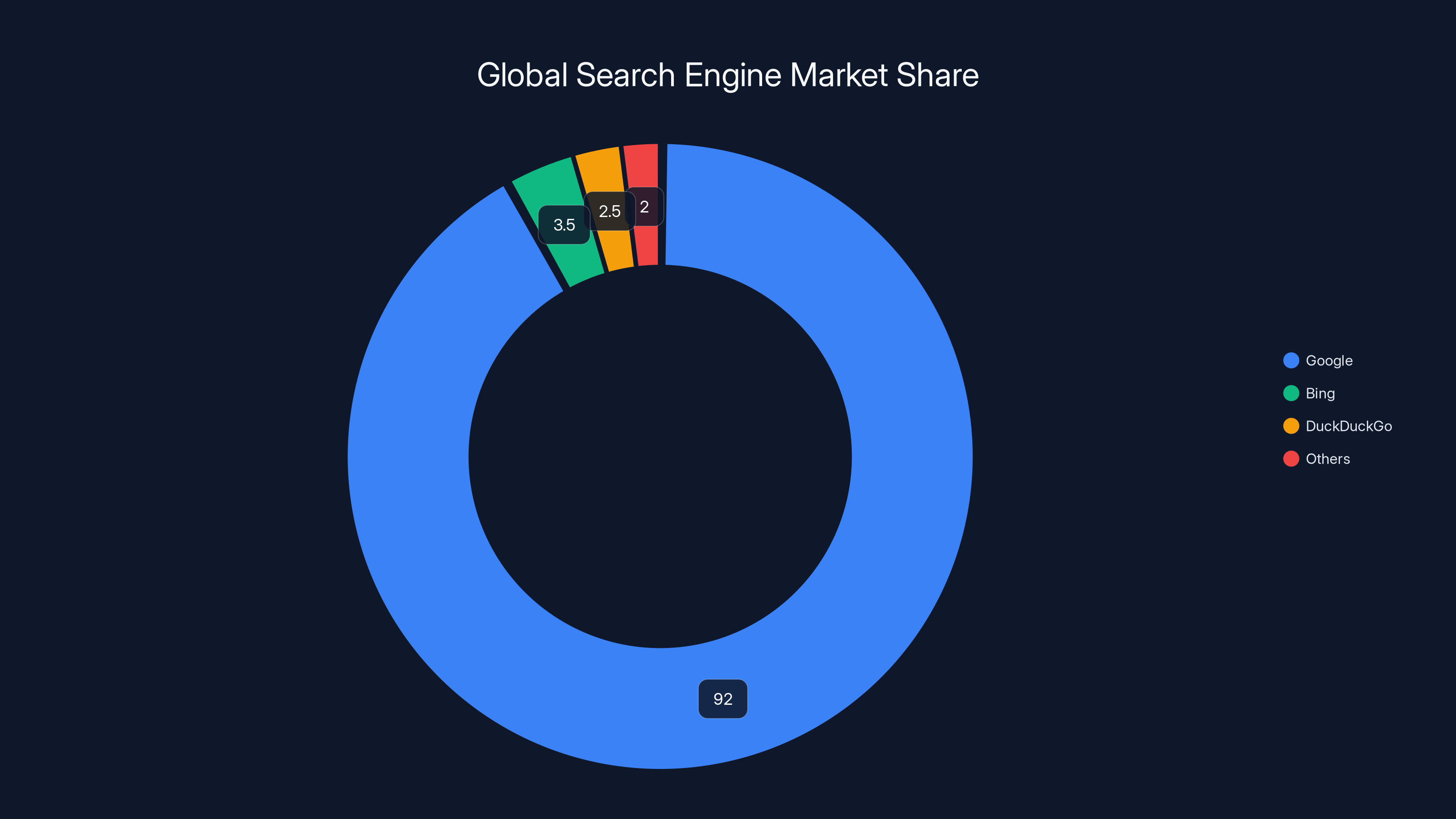

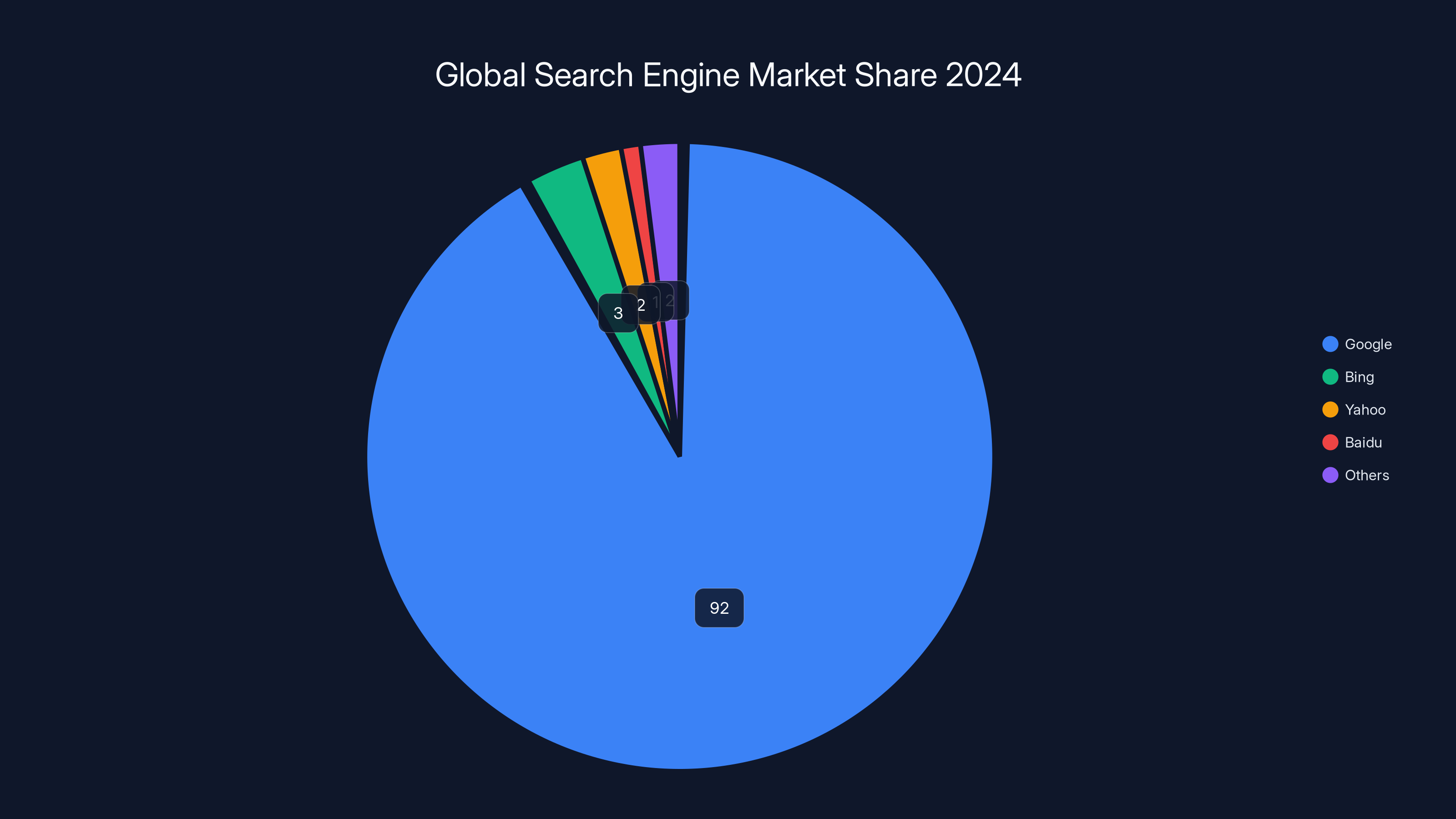

Google's market dominance extends across virtually every geographic region and device category. Globally, Google commands approximately 92% of search engine market share, a figure that has remained stable for over a decade despite dozens of attempted competitors. This stability is remarkable—in most technology markets, dominance is temporary, eroded by new entrants with superior offerings.

In the United States, Google's share is approximately 88-90%, slightly lower than the global average but still overwhelming. Bing, Microsoft's search engine, captures approximately 3-4% despite Microsoft's technical capabilities and massive financial resources. Duck Duck Go, which emphasizes privacy, has grown to capture roughly 2-3%. All other search engines combined account for the remaining small percentage.

On mobile devices, Google's dominance is even more pronounced. Approximately 95% of mobile search queries route through Google, reflecting both the exclusivity of Apple's Safari default and Android's deep integration of Google Search. This mobile dominance matters enormously, as mobile now represents more than half of all internet traffic globally.

Different regions show modest variations but consistent patterns. In Russia and China, government-controlled search engines dominate, reflecting political rather than competitive factors. In Europe, Google maintains approximately 90% market share. In India, where smartphone adoption has exploded, Google accounts for approximately 98% of mobile searches.

Emerging Competitors and Alternative Search Models

Despite Google's dominance, alternative search models have begun emerging, particularly in artificial intelligence-powered search. Chat GPT, despite being fundamentally a language model rather than a search engine, attracts search-like queries. Open AI's new Search GPT product attempts to compete more directly with Google by combining language generation with real-time information retrieval.

Perplexity AI, a startup founded in 2022, offers AI-powered search that generates answers rather than simply ranking pages. The platform has grown rapidly, attracting hundreds of millions of queries monthly. Unlike Google, which returns a list of potentially relevant pages, Perplexity generates synthesis answers, citations included, providing a fundamentally different user experience.

Google itself has responded by integrating AI-powered summaries into its search results through its "AI Overviews" feature. This response demonstrates that Google recognizes the competitive threat posed by AI-powered alternatives, even if these alternatives haven't significantly eroded its market share.

Regional search engines persist in specific markets. Baidu dominates in China, Yandex in Russia, Naver in South Korea. These regional leaders succeeded not through superior technology but through local dominance strategies and, in some cases, government favoritism. They demonstrate that search engines can be competitive where distribution advantages exist.

Legal and Economic Arguments: The Antitrust Debate

Defining the Relevant Market

A fundamental question in antitrust analysis involves defining the relevant product market. Is "search" a single market where Google competes against Bing, Duck Duck Go, and AI-powered alternatives? Or are there multiple markets—general search, image search, news search, video search, local search—where different competitors might dominate?

Google argues for a broad market definition that includes all forms of information retrieval. In this view, traditional search engines compete with specialized search services, AI assistants, social media platforms (users find information on Tik Tok and You Tube), and direct navigation (users go directly to Amazon when searching for products). By this definition, Google's share of "information retrieval" is substantially lower—perhaps 30-40%—which wouldn't constitute monopoly dominance.

The Department of Justice and Judge Mehta define the market more narrowly as "general search services," essentially the service of retrieving web pages in response to written queries. By this definition, Google's 92% share clearly constitutes monopoly dominance. The choice of market definition heavily influences the case's outcome.

Perfect Competition vs. Monopoly Leveraging

Google also argues that its business model—providing search for free while monetizing through advertising—isn't anticompetitive because users pay nothing. If Google were truly monopolistic, customers would face higher prices. Instead, they receive a free service with consistent quality and constant feature improvements.

This argument contains truth but obscures important economics. In digital markets with network effects, "free" services can be more damaging to competition than expensive ones, because the value proposition isn't price but convenience and quality. When users get search for free and that free service has superior quality due to network effects and data advantages, users have little reason to try alternatives. The absence of direct price suggests absence of monopoly harm, but this conclusion confuses consumer harm with monopoly harm.

Monopoly harm in digital markets often manifests not as high prices but as reduced innovation, limited consumer choice, and foreclosure of rival business models. Judge Mehta found that Google's exclusive default arrangements prevented rivals from achieving the scale necessary to invest in search innovation. By this logic, the harm isn't that Google charges high prices for search (it doesn't) but that it prevents competitors from developing alternatives.

The Presumption of Legality for High Market Share

Google's appeal will almost certainly argue that high market share alone doesn't establish monopoly liability. A company can legally achieve 92% market share if it does so through superior products, innovation, and customer service. Antitrust law distinguishes between monopolies earned through efficiency (legal) and monopolies maintained through anticompetitive conduct (illegal).

Google contends its market share results from the former. Its search algorithm is genuinely superior. Its machine learning capabilities are unmatched. Users choose Google because they prefer it, not because they're forced to. The company invested billions in developing search excellence, and this investment created legitimate competitive advantages.

The government counters that while Google's product is good, its market dominance results substantially from exclusionary agreements. A competitor with a comparably good search engine couldn't reach users because Google ensured that Safari, Chrome, and other major distribution channels defaulted to Google Search. This foreclosure of distribution, not product inferiority, maintains Google's monopoly.

Google's dominance in the search engine market is evident, with an estimated 85% share, highlighting the monopoly concerns addressed in the ruling. (Estimated data)

The Department of Justice's Perspective and Enforcement Arguments

Original DOJ Case and Continuing Involvement

The Department of Justice filed the original antitrust lawsuit in October 2020, during the Trump administration. The case continued and expanded under the Biden administration, which intensified antitrust enforcement against technology giants. The DOJ's case represented the culmination of a multi-year investigation examining Google's conduct across search, advertising, Android, Chrome, and Maps.

The DOJ team, led by antitrust lawyers with decades of experience, built a comprehensive case demonstrating how Google's various businesses reinforced each other to maintain and extend monopoly dominance. Chrome, ostensibly a browser, served as a distribution channel for Google Search. Android, Google's mobile operating system, came pre-configured with Google Search. Each Google service directed traffic toward other Google services, creating an interconnected ecosystem that rivals couldn't replicate.

Judge Mehta's monopoly finding vindicated the DOJ's core argument: Google's dominance resulted substantially from anticompetitive conduct rather than inevitable efficiency. The government has now argued before the court that remedies must be substantial enough to restore meaningful competition while any appeal proceeds.

Remedy Adequacy and Implementation Oversight

The DOJ faces a challenging situation as Google appeals. If courts stay the remedies pending appeal, Google continues operating unchanged, potentially deepening its monopoly. If remedies proceed immediately, implementing costly measures that might later be reversed creates business uncertainty.

The government has signaled that it believes even the implemented remedies may prove insufficient. Data sharing alone might not enable competitors to achieve scale, particularly if Google's superior machine learning systems produce search results that, even with shared data, competitors can't match. Search syndication requirements might not incentivize competitors to build independent search capabilities if licensing Google's results remains the faster path to market.

The DOJ may argue that more aggressive remedies—potentially including Chrome divestiture that Judge Mehta rejected—would be necessary if appeal processes extend indefinitely. The government's implicit threat is that failure to implement substantial remedies now suggests more dramatic restructuring will be necessary later.

International Regulatory Perspectives and Parallel Actions

The European Union's Parallel Investigation

While the United States pursued its antitrust case, the European Union simultaneously conducted its own investigation into Google's search practices. EU competition authorities, traditionally more aggressive than their U. S. counterparts, had already fined Google billions of euros for various anticompetitive practices.

The EU investigation focused specifically on Google's conduct in search and search advertising—the exact domains of the U. S. case. EU investigators examined whether Google's preferential treatment of its own services (Google Shopping, Google Hotels, Google Flights) in search results constituted abuse of dominance. They also investigated exclusive default arrangements, particularly with Apple and Mozilla.

The EU's potential remedies could be more aggressive than Judge Mehta's decision. EU competition law includes a robust right to break up monopolies, and EU regulators have demonstrated willingness to impose severe penalties and structural remedies against dominant tech platforms. Google faces the prospect of defending its monopoly across multiple jurisdictions simultaneously, with different legal standards and remedy approaches.

Broader Implications for Big Tech Regulation

Google's case is part of a wave of antitrust enforcement against major technology platforms. Apple faces scrutiny regarding its App Store practices, Meta faces investigations regarding acquisitions, and Amazon faces challenges regarding its dual roles as marketplace operator and competitor. Google's appeal, and its outcomes, will influence how aggressively regulators pursue these other cases.

If Google's appeal succeeds, it suggests that current antitrust frameworks struggle to address digital dominance, potentially leading to legislative reforms. If the appeal fails, it establishes precedent that exclusive default arrangements and foreclosure of distribution channels constitute illegal monopolistic conduct even when products are superior.

The Mechanics of Search Monopoly: How Distribution Determines Market Share

Why Default Matters More Than Quality

The empirical evidence overwhelmingly demonstrates that default search engine placement determines market share. Research consistently shows that changing a default search engine causes immediate and substantial traffic shifts, despite no changes to search quality or functionality.

When Mozilla briefly tested setting Bing as the default in Firefox, Bing's market share increased by approximately 2-3 percentage points. When Duck Duck Go expanded its default placements on some browsers, its traffic surged. These experiments demonstrate that the default isn't merely a convenient option users accept; it's effectively a determinative factor in market share.

This dynamic reflects both rational and irrational behavior. Rationally, users might default to the default because they haven't evaluated alternatives—the benefits of switching are uncertain while the costs of learning a new interface are concrete. Irrationally, users might default to the default simply because it's default, a status quo bias that researchers have documented extensively in consumer behavior.

Google has leveraged this reality by ensuring that its search dominates default placements across virtually every major distribution channel. This dominance doesn't result from technical superiority of defaults but from exclusive agreements and financial incentives making Google the rational choice for platforms to select.

Revenue Sharing Economics and Dependency

Google's default payments create financial dependencies that make switching economically irrational. The company allocates approximately 80% of advertising revenue from search to distribution partners through revenue sharing arrangements. For Safari, this arrangement generated an estimated $20 billion annually as of 2021, representing a massive portion of Apple's services revenue.

This revenue scale creates dependency. Apple couldn't replace Google Search without sacrificing billions in annual revenue—revenue that flows to Apple's bottom line and funds corporate operations. Short of antitrust intervention, no competitor could match Google's payment offers because no competitor generates the advertising volume that search generates.

This creates a chicken-and-egg problem for competitors. They can't achieve sufficient search volume to generate the advertising revenue necessary to compete with Google's payments. They can't obtain the default placements necessary to achieve sufficient volume. They're trapped in a competitive position where they lack access to the mechanisms necessary to compete.

Default search engine settings significantly impact market share, with Google maintaining dominance due to strategic default placements. Estimated data based on typical market behavior.

Consumer Welfare and Innovation Effects: Evaluating Harm

Direct Consumer Harm vs. Structural Harm

The monopoly harm in Google's case isn't direct consumer harm through high prices but structural harm through foreclosure of competition. Google Search remains free, provides high-quality results, and has continuously improved. By these metrics, consumers appear well-served.

However, antitrust law recognizes that monopolists can harm consumers through mechanisms beyond pricing. When monopolists foreclose distribution channels, they prevent new technologies from reaching consumers. If a superior search engine emerges—better at understanding questions, more accurate results, stronger privacy protections—and that search engine can't reach users because Google controls all distribution channels, consumers are harmed by being unable to access superior alternatives.

Judge Mehta found that Google's conduct precisely created this harm. By ensuring that Safari, Chrome, Android, and other distribution channels defaulted to Google, Google prevented potentially superior competitors from achieving the scale necessary to develop and market their services.

Innovation Effects and Long-Term Competition

The monopoly also affects innovation incentives. If entrepreneurs recognize that even superior search products can't reach consumers without defeating Google's exclusive default arrangements, they won't invest in search innovation. Instead, investment flows toward areas where distribution isn't controlled—social media, e-commerce, specialized services.

This dynamic may already be visible in search innovation trends. Major innovations in search—AI-powered synthesis, privacy-first search, specialized search categories—have emerged outside Google or at smaller scales where dominant positions don't exist. If distribution competition were functioning, we might expect more search innovation, more experimentation with different search paradigms, and faster diffusion of emerging technologies.

Comparing Different Search Engines: Features, Privacy, and Performance

Google Search: Dominance, Features, and Limitations

Google Search dominates through a combination of superior relevance, comprehensive indexing, and continuously improving AI features. Google's search results are widely considered more relevant than competitors', reflecting decades of algorithm refinement and access to enormous amounts of relevance feedback data. Google indexes the entire web comprehensively, ensuring that obscure but relevant content appears in results. Google's integration of AI through features like featured snippets and AI-powered overviews represents the frontier of search technology.

However, limitations exist. Google's results can be dominated by commercial content, as the company monetizes search through advertising. Google's ranking algorithms have been criticized for favoring large publishers and making it difficult for small creators to gain visibility. Privacy concerns persist—Google aggregates search data across services, creating detailed profiles of user interests and behavior.

Bing: Microsoft's Long-Challenged Alternative

Microsoft Bing, despite tremendous investment and genuine technical capability, has struggled to gain significant market share despite offering comparable quality to Google. Bing's results are respectable, its features are competitive, and Microsoft has invested heavily in integration with Windows and Office. Yet Bing remains stuck at approximately 3-4% market share, suggesting that product quality alone is insufficient to overcome Google's distribution advantages.

Bing's situation illustrates the case's core issue. If Bing, backed by a company with Microsoft's financial resources and technical expertise, can't significantly dent Google's dominance, smaller competitors face impossible odds. This isn't because Bing is inferior but because Bing lacks distribution. Microsoft can't match Google's default payments, can't arrange exclusive agreements with Apple or Mozilla, and lacks alternative channels to reach users at scale.

Privacy-Focused Alternatives: Duck Duck Go

Duck Duck Go offers search with a privacy-first approach, promising not to track user behavior or store personal data. The service has attracted users concerned about privacy, growing to approximately 2-3% market share despite having far fewer resources than Google or Microsoft.

Duck Duck Go's limitations illustrate why alternative business models struggle. By refusing to track users, Duck Duck Go cannot develop machine learning systems that learn from user behavior feedback. Its search results, while respectable, don't improve as much as Google's, which benefits from continuous feedback about which results users find relevant. Additionally, Duck Duck Go's privacy-first approach limits advertising monetization, constraining its ability to pay for default placements.

AI-Powered Search: New Entrants

Emerging AI-powered search services like Perplexity AI and Search GPT represent a fundamentally different approach to search. Rather than returning ranked lists of web pages, these services synthesize information into coherent answers, generating responses that combine information from multiple sources.

These services appeal to users seeking concise answers rather than lists of pages to evaluate. They've grown rapidly, attracting hundreds of millions of queries. However, they face the same distribution challenge as traditional search engine alternatives. Without default placement on major browsers and devices, they remain niche services.

Comparison Table: Search Engine Features

| Feature | Bing | Duck Duck Go | Perplexity | Search GPT | |

|---|---|---|---|---|---|

| Market Share | 92% | 3-4% | 2-3% | <1% | <1% |

| Privacy Focus | Minimal | Moderate | Extensive | High | High |

| AI Features | Advanced | Advanced | Basic | Central | Central |

| Real-time Data | Excellent | Good | Good | Excellent | Excellent |

| Ranking Quality | Excellent | Good | Good | Very Good | Excellent |

| Default on Safari | Yes | No | No | No | No |

| Default on Chrome | Yes | No | No | No | No |

| Free Service | Yes | Yes | Yes | Yes | Yes |

| Ad-Supported | Yes | Yes | No | Limited | Limited |

The Case's Impact on Search Innovation and Future Technologies

How Monopoly Power Stifles Search Innovation

Google's monopoly position may be stifling innovation in search through two mechanisms: reduced investment incentives for competitors and reduced experimentation within Google itself. Competitors, facing the distribution barriers discussed above, have limited incentives to invest heavily in search innovation. Why develop superior technology if you can't reach consumers? This diverts innovation resources toward areas where distribution isn't monopolized.

Within Google, monopoly position might reduce innovation incentives. Without competitive pressure, organizations often slow innovation cycles. Google continues improving search, but competitive pressure might accelerate improvement. Bing's inability to gain scale means it can't pressure Google in meaningful ways. This apparent paradox—that lack of competition reduces innovation even when the monopolist is technically sophisticated—has support in economic research.

Opportunities for AI-Powered Search Alternatives

Recent breakthroughs in large language models have created unprecedented opportunities for alternative search models. Unlike traditional search, which requires specific distribution advantages to gain scale, AI-powered search powered by LLMs benefits from a different advantage: computational power and training data.

Companies without access to traditional search distribution can build competitive AI-powered search by investing in model training. Open AI demonstrated this by creating Search GPT despite lacking search distribution. If distribution competition were restored through antitrust remedies, we might see a explosion of specialized search services optimized for different user needs—medical search, legal search, scientific search, coding search—each leveraging AI to provide superior domain-specific results.

Google dominates the global search engine market with a 92% share, followed by Bing and DuckDuckGo with minor shares. Estimated data.

Financial Implications: Google's Business Model and Advertising Economics

Search Advertising Revenue Concentration

Search advertising generates approximately 60% of Google's total revenue, with search advertising generating approximately $175-200 billion annually. This revenue concentration creates powerful incentives to maintain search dominance. Losing search market share directly threatens Google's most profitable business.

Google's profit margins on search advertising exceed those of any other business segment. The combination of dominant market position, exclusive default arrangements, and switching costs creates pricing power. Advertisers pay more per click in search than in other advertising formats precisely because search traffic has higher commercial intent and faces less competition for placement.

The monopoly's financial value is enormous. If Google lost even 10 percentage points of search market share—dropping from 92% to 82%—the company would lose approximately $20-25 billion in annual revenue at current pricing. This explains why Google fights aggressively to defend its monopoly. The financial stakes are among the largest in any antitrust case ever filed.

Advertiser Economics and Consequences of Competition

Monopoly power over search gives Google extraordinary advantages in dealing with advertisers. Advertisers cannot cheaply access competitor platforms because competitor platforms lack comparable reach. Advertisers must accept Google's terms regarding pricing, data access, and algorithmic control.

If search competition were restored, advertisers could distribute spending across multiple platforms based on ROI. This would likely reduce advertiser spending per platform, reducing per-click prices, and improving advertiser returns. In this scenario, users benefit indirectly through lower advertising costs driving lower prices on goods and services.

Regulatory Landscape and Legislative Considerations

Congressional Antitrust Activities

Congress has held numerous hearings regarding big tech dominance and has considered various legislative proposals to address antitrust concerns. Some proposals would establish new rules specifically for large digital platforms, others would strengthen traditional antitrust law, and still others would create separate regulatory frameworks for tech companies.

The challenge facing Congress is balancing innovation incentives against fair competition. Aggressive antitrust enforcement against dominant firms might reduce innovation by removing lucrative acquisition targets and creating regulatory uncertainty. Minimal enforcement might preserve monopoly rents and prevent new entrants from disrupting incumbents.

Google's appeal process occurs in this uncertain legislative context. A substantial appellate victory might reduce pressure on Congress to act. Conversely, continued antitrust success might accelerate legislative action, as Congress concludes that current law is insufficient.

International Regulatory Divergence

Different jurisdictions are adopting different approaches to tech regulation, creating a complex compliance landscape for global platforms. The EU's Digital Markets Act establishes clear designation standards for "gatekeeper" platforms and mandates specific behaviors. The UK, while implementing the Online Safety Bill, takes a different approach. China's regulations are more restrictive, India's are still developing.

Google must navigate these divergent regulatory frameworks while an antitrust case proceeds in the United States. If it loses the U. S. case, it will likely face similar actions internationally, making compliance even more complex.

The Case for and Against Breaking Up Google

Arguments for Structural Remedies

The Department of Justice argued that nothing short of forcing Google to divest Chrome would adequately remedy the monopoly. Chrome, bundled with Android, dominates distribution channels and directs users to Google Search. Chrome represents Google's greatest leverage point for ensuring that users default to Google Search.

Forced divestiture would require Google to separate Chrome into an independent company, preventing the bundling of services that creates distribution power. If Chrome were independent, it could no longer preferentially direct users to Google Search. Other search engines could arrange distribution deals directly with Chrome, restoring competition.

This approach has precedent. The breakup of AT&T in the 1980s, while controversial, is credited with enabling innovation and competition in telecommunications. Similarly, breaking up Standard Oil created companies that competed with each other while contributing to industrial productivity.

Arguments Against Breaking Up Google

Judge Mehta declined to impose forced divestiture, concluding that less aggressive remedies could achieve competitive effects. Breaking up Google would be tremendously disruptive, potentially harming users and innovation through transition costs. Chrome, integrated with Google's other services, benefits from synergies that separation would eliminate.

Additionally, breakup doesn't guarantee lasting competitive effects. Separated companies might merge, and without ongoing regulation, new monopolies could re-form. Behavioral remedies requiring Google to share data and offer syndication might achieve competitive effects while preserving beneficial integration.

Breakup also raises international concerns. If the U. S. breaks up Google while other countries don't break up their dominant tech companies, U. S. technology companies face global competitive disadvantage. Google's integrated services compete against similar integrated offerings from Chinese and European companies. Breakup might weaken Google relative to international competitors.

Google holds an overwhelming 92% of the global search market, underscoring its dominance and the antitrust concerns raised. Estimated data.

The Broader Implications for Technology and Society

Search as Infrastructure and the Neutrality Debate

The case raises a fundamental question: Should dominant search platforms be treated as neutral infrastructure or as private companies with rights to organize their services? If search is essential infrastructure upon which commerce and communication depend, perhaps it should be regulated similarly to utilities—with net neutrality principles ensuring equal treatment of all content.

This perspective suggests that Google, controlling 92% of search, shouldn't be able to preferentially rank its own services or those of partners who pay for default placement. Instead, ranking should be determined purely by relevance, with no possibility of leveraging search dominance to advantage other services.

Opponents argue that search isn't infrastructure but a service, and Google has rights to organize its service as it sees fit. Google invested in developing search excellence and deserves to benefit from that investment. Treating Google as infrastructure would set a precedent requiring continuous regulation, reducing incentives for further innovation.

Long-Term Competitive Dynamism and Creative Destruction

One critical question concerns whether competition law should preserve today's dominance or enable tomorrow's disruption. Google now seems inevitable, but every dominant platform eventually faces disruption from new technologies. Yahoo was once dominant, Microsoft seemed unbeatable, and AT&T appeared permanent before antitrust action.

Artificial intelligence is already changing how people seek information. Within ten years, AI-powered synthesis might fully replace list-based search results. If this transition occurs, the dominance of traditional search engines becomes less relevant. Google could maintain 92% of traditional search market share while losing the more important market for AI-powered information discovery to competitors with better AI systems.

This perspective suggests that antitrust enforcement focusing on Google's search dominance might miss a broader dynamic in which distribution competition matters less as new paradigms emerge. Alternatively, it suggests that remedies should focus on enabling competition in emerging information technologies rather than purely addressing today's dominance.

Alternative Models for Search and Information Retrieval

Decentralized Search Architectures

Some advocates propose decentralized search architectures where index content and ranking algorithms are openly shared, enabling any developer to build search services without central control. These proposals, inspired by blockchain and decentralized web principles, would fundamentally restructure how search operates.

Decentralized search would eliminate the need for default placement on browsers and devices, as users could select services based on preference rather than installation convenience. It would reduce barriers to entry for new competitors, as they wouldn't need to build search indexes from scratch but could use shared, open infrastructure.

However, decentralized search faces significant challenges. Building comprehensive indexes requires massive computing investment. Determining which content should rank highly requires sophisticated algorithms and user feedback mechanisms. Decentralizing these functions across many entities risks duplication and inefficiency. Additionally, decentralized systems can be more difficult to moderate, potentially increasing harmful content visibility.

Vertical Integration vs. Horizontal Competition

Another approach proposes restricting Google's ability to integrate services vertically. Under this model, Google could operate search as a service, but couldn't also operate Google Shopping, Google Hotels, Google News, or other vertical services. Separating these services would prevent leveraging search dominance to dominate adjacent categories.

This approach preserves beneficial integration where it exists while preventing the most egregious anticompetitive effects. Google's search could still work smoothly with Chrome and Android, but couldn't preferentially rank Google Shopping results over competitors' shopping results.

Syndication Models and Content Neutrality

Syndication-based approaches, which Judge Mehta endorsed, require dominant platforms to offer their services to competitors on reasonable terms. Rather than breaking up the company or restricting its operations, these approaches recognize that consumers benefit from integrated services while ensuring that competitors can access necessary inputs.

Under syndication, Google would offer its search results to other browsers and devices on non-exclusive terms. Other platforms could integrate Google search without being locked into exclusivity, and could more easily offer competing search products alongside or instead of Google.

Case Precedents and Legal Framework

The Microsoft Case: Historical Parallel

The Microsoft antitrust case, resolved in the early 2000s, provides the most direct precedent for the Google case. Microsoft faced similar allegations: that it maintained an illegal monopoly over operating systems and abused that monopoly to dominate internet browsers (Internet Explorer) and other applications.

The Microsoft case, like Google's, involved exclusive default arrangements. Microsoft bundled Internet Explorer with Windows, ensuring that users defaulted to IE rather than Netscape Navigator. The government argued this was anticompetitive; Microsoft argued its product was superior. The case ultimately settled with behavioral remedies rather than breakup, though Microsoft's dominance did eventually face disruption from other technologies.

The Microsoft precedent suggests that judge-ordered remedies might have limited long-term effectiveness against determined monopolists. However, it also shows that antitrust enforcement, even if not ultimately determining market outcomes, can constrain monopolistic practices and create space for competition.

The AT&T Divestiture Case

The breakup of AT&T in 1982, following decades of antitrust litigation, provides precedent for structural remedies in technology. AT&T operated a telecommunications monopoly with integrated local and long-distance services. The government successfully argued that separation was necessary to enable competition in long-distance and equipment manufacturing.

AT&T's breakup is widely credited with enabling competition and innovation in telecommunications. Separated "Baby Bells" competed on local service, long-distance providers like MCI and Sprint could enter, and equipment manufacturers could compete with AT&T's Western Electric subsidiary. However, the breakup was also disruptive, and over subsequent decades, telecommunications consolidation partially reversed initial competitive effects.

What Could Go Wrong: Implementation Challenges and Risks

Data Sharing Complexity and Privacy Risks

Data sharing remedies, while less disruptive than breakup, face significant implementation challenges. Google must share search data with competitors without violating user privacy. Creating datasets that are useful for training competitor systems while being sufficiently anonymized to protect privacy is technically complex.

If data sharing is implemented inadequately, competitors won't gain meaningful access to useful signals, and remedies will fail. If anonymization is inadequate, privacy risks materialize. Courts must oversee this balance, monitoring both whether competitors receive useful data and whether privacy is protected.

Innovation Stagnation and Transition Costs

Forced data sharing and syndication might reduce innovation incentives. If competitors can license Google's search results, they have less incentive to develop independent search capabilities. Google, aware that its data will be shared, might reduce investment in search improvement if reduced quality wouldn't significantly damage market share.

Transition costs are also substantial. Google must develop systems to share data at required volumes and frequencies. Competitors must integrate this data into their systems. During transition, search quality might suffer, harming users. These transition costs don't obviously benefit consumers and might not be justified if remedies ultimately fail to produce sustainable competition.

Regulatory Capture and Ongoing Compliance

If complex behavioral remedies are implemented, they require ongoing regulatory oversight. Monitors must constantly assess whether Google is complying with data sharing obligations, whether data quality is adequate, and whether syndication terms are reasonable. This requires building permanent regulatory structures overseeing technological companies' internal operations.

Regulatory capture is a risk—over time, the regulated company and the regulator may develop relationships that reduce enforcement vigor. Additionally, ongoing regulation might entrench Google's position by making it too expensive for competitors to emerge. If compliance with complex rules requires expensive legal and technical infrastructure, smaller competitors might find entry impossible despite remedies aimed at helping them.

The Future of Search and Information Access

AI-Powered Transformation and Shifting Paradigms

The future of search may be determined not by the resolution of Google's current antitrust case but by fundamental technological shifts toward AI-powered information systems. As large language models improve, synthesizing information into coherent answers becomes the dominant search paradigm rather than ranking lists of pages.

If this transformation occurs, Google's dominance of traditional search becomes less important. Google can leverage its resources to build superior AI-powered search, but it competes on more level ground with competitors like Open AI, Anthropic, and startups with strong AI teams. The distribution advantages that preserve Google's traditional search dominance matter less in AI-powered paradigms.

Specialized Search and Vertical Integration

The future may also involve multiplication of specialized search services optimized for specific domains. Medical search, legal search, scientific research search, code search, and job search might all evolve into specialized services with different ranking criteria and result presentations optimized for each domain.

This development could happen naturally as AI enables easier vertical service creation. Alternatively, it could be encouraged through antitrust remedies that restrict Google's ability to integrate vertically. In either case, the broad "general search" market that Google dominates might fragment into specialized verticals where various competitors operate.

Privacy, Data, and User Expectations

Emerging user concerns about privacy and data usage might reshape search competition. As privacy becomes more valued, search services promising stronger privacy protections might gain share despite lacking distribution advantages. This would represent a shift from product quality and distribution as primary competitive factors toward privacy and ethical practices.

Google has acknowledged privacy concerns through features like incognito search and privacy-focused updates. However, its fundamental business model depends on data collection and personalization. Competitors genuinely focused on privacy might have structural advantages as user preferences shift, even if current evidence suggests most users default to Google despite privacy concerns.

Lessons for Antitrust in Digital Markets

Market Definition and Digital Dominance

The Google case reveals challenges in applying traditional antitrust frameworks to digital markets. Traditional market definition focuses on product characteristics and consumer behavior. But digital markets are characterized by network effects, switching costs, and winner-take-all dynamics that make traditional analysis inadequate.

Future antitrust enforcement must grapple with market definition in environments where high market share can coexist with genuine consumer satisfaction. Users truly prefer Google, yet Google's dominance forecloses competition. Resolving this apparent paradox requires antitrust theory that acknowledges both that Google is preferred today and that competitive alternatives might be preferred tomorrow if available.

Behavioral vs. Structural Remedies in Tech

The Google case represents an experiment in behavioral remedies for digital monopolies. Rather than breaking up the company, courts imposed ongoing compliance obligations. This approach preserves integration benefits while constraining anticompetitive conduct.

However, behavioral remedies require ongoing regulatory oversight. Structural remedies, while more disruptive, create clearer rules and require less monitoring. Future enforcement might favor structural remedies despite short-term disruption, concluding that long-term competition requires clear separation rather than manageable monopolists.

The Global Regulatory Coordination Problem

Tech companies operate globally while antitrust is jurisdictional. Google must navigate antitrust cases in the U. S., EU, UK, India, and potentially other jurisdictions, each with different legal standards and remedy approaches. This fragmentation creates compliance complexity and might result in contradictory mandates.

Long-term solutions might require international coordination on antitrust standards for digital platforms. Absent such coordination, tech companies will continue navigating contradictory requirements, and regulatory arbitrage might reduce enforcement effectiveness.

Preparing for Uncertainty: What Comes Next

Timeline for Appeals and Decision Points

Google's appeal faces a multi-year timeline. The company filed in late 2024; the D. C. Circuit will likely issue a decision in 2026 or 2027. Supreme Court review, if pursued, would extend the timeline to 2027-2029. Throughout this period, uncertainty about remedies will persist. Google will likely seek to stay remedies pending appeal, potentially preventing implementation.

Key decision points will come when the appeals court issues its decision, when Google might petition for Supreme Court review, and when the Supreme Court decides whether to accept the case. At each point, the competitive landscape could shift dramatically depending on rulings.

Strategic Responses from Competitors and Allies

Google's appeal will provoke responses from competitors and allies. Microsoft might increase Bing investment or explore partnership opportunities with appeal outcomes. Smaller search alternatives might prepare for scenarios where they gain distribution access if remedies are implemented. Device manufacturers and browser operators might lobby regarding specific remedy provisions.

Google's allies—Apple, Mozilla, and other companies receiving search revenue—will lobby to preserve their revenue streams. These companies might argue that forced data sharing or syndication would harm their interests, creating interesting dynamics where companies currently benefiting from Google's dominance argue against remedies.

Potential Legislative Responses

Congress might not wait for appeals to conclude. If antitrust enforcement seems slow, legislators might propose new rules specifically addressing tech platform dominance. Potential legislative responses could include requirements for interoperability, data portability, or restrictions on exclusive arrangements.

Legislative action would likely prove more aggressive and faster than litigation. A Democratic Congress combined with an administration prioritizing antitrust enforcement might produce legislation substantially restructuring tech markets before Google's appeals complete.

Conclusion: The Future of Digital Competition

Google's appeal of Judge Mehta's monopoly ruling marks a pivotal moment for digital competition, regulatory authority, and the future structure of the internet. The case synthesizes two decades of concerns about tech platform dominance into a specific legal determination: Google maintains an illegal monopoly over general search services through anticompetitive conduct, and remedies are necessary to restore competition.

The appeal process will likely extend for several years, potentially reaching the Supreme Court and ultimately requiring nearly a decade of litigation from the original lawsuit's filing in 2020. During this extended process, uncertainty about Google's obligations will persist, competitors will remain constrained by existing barriers, and the question of what remedies are adequate to restore competition will remain unresolved.

Google's arguments—that users choose Google because it's superior, that exclusive defaults benefit consumers by ensuring quality, and that data sharing would harm privacy—deserve serious consideration. Judge Mehta's findings don't establish that Google's product is inferior, only that Google's distribution dominance wasn't earned purely through product excellence and that this dominance has anticompetitive effects.

The case's ultimate impact extends beyond Google. It will determine whether tech platforms can maintain dominance indefinitely through exclusive arrangements, whether antitrust law adequately addresses digital markets, and whether behavioral remedies can restore competition or whether more aggressive structural solutions are necessary. The answers will reshape not just search, but the entire trajectory of digital competition.

Regardless of appeal outcomes, technological shifts toward AI-powered information systems may alter the case's practical importance. Google might maintain dominance in traditional search while losing ground in emerging paradigms. Alternatively, AI-powered alternatives might overcome distribution barriers through superior technology, making antitrust intervention unnecessary.

For now, the case remains unresolved, competitors remain constrained by existing barriers, and billions of users continue defaulting to Google Search as the result of both genuine preference and structural factors beyond their control. The appeal process will determine whether this status quo persists indefinitely or whether competition returns to digital search.

FAQ

What is the Google search monopoly ruling?

In August 2024, U. S. District Judge Amit Mehta ruled that Google maintains an illegal monopoly over general search services and search text advertising through anticompetitive conduct. The judge found that Google used exclusive default arrangements with browsers and device manufacturers to foreclose rival search engines from reaching consumers, creating a durable monopoly that prevented fair competition.

Why did Judge Mehta decide Google has a monopoly?

Mehta found that Google controls approximately 92% of search market share, which constitutes dominance. More importantly, the judge determined that this dominance wasn't achieved purely through superior products but through exclusionary contracts with Safari, Firefox, and other distribution channels that made switching to competitor search engines economically irrational for these platforms. The judge emphasized that major companies had "nowhere else to turn other than Google" due to the financial dependency created by Google's default payments.

What are the remedies that Google is appealing?

Judge Mehta ordered Google to share search data with competitors, offer search results through syndication on reasonable non-exclusive terms, and restrict exclusive default arrangements. Specifically, Google must provide competitors with access to search query data, click-through data, and result relevance signals in standardized formats to help them build competitive search systems. These remedies aim to level the competitive playing field without breaking up the company.

How long will Google's appeal process take?

Google's appeal will likely take 18-24 months to reach a decision from the U. S. Court of Appeals for the District of Columbia Circuit. If either party petitions the Supreme Court and it accepts the case—likely given the magnitude of the issues—another 2-3 years would be added. The entire appellate process could extend to 2027-2029, meaning nearly a decade will have elapsed from the original 2020 lawsuit filing to final resolution.

What are Google's main arguments in the appeal?

Google argues that the ruling "ignored the reality that people use Google because they want to," contending that high market share reflects genuine user preference, not anticompetitive conduct. The company emphasizes that it faces competition from established players like Microsoft Bing and well-funded startups, and that forcing data sharing would harm user privacy while discouraging competitors from building independent products. Google also argues that the court misapplied antitrust law to digital markets.

Could Google be broken up like Microsoft?

Judge Mehta rejected the Department of Justice's request to force Google to divest Chrome, concluding that behavioral remedies like data sharing could achieve competitive effects without the disruption of forced breakup. However, Google's appeal could ultimately result in different judges reaching different conclusions. If higher courts believe that behavioral remedies prove insufficient, they might impose structural remedies. The legal precedent for breaking up dominant tech companies exists from the AT&T divestiture case.

How does this case affect search alternatives like Bing and Duck Duck Go?

The remedies could significantly help search alternatives by requiring Google to share data and offer syndication on reasonable terms. If data sharing provisions are implemented, competitors could use this data to improve their search algorithms. If syndication is enforced, they might gain distribution through major browsers and devices. Currently, Bing remains constrained to approximately 3-4% market share despite Microsoft's resources, largely due to lack of default placement on Safari and other major platforms.

What is the Department of Justice's position on the appeal?

The Department of Justice has defended Judge Mehta's ruling and will argue against Google's appeal. The DOJ contends that Google's exclusive default arrangements constitute anticompetitive conduct that maintains its monopoly, and that the ordered remedies are necessary and appropriate to restore competition. The government will likely argue that even the implemented remedies may prove insufficient, potentially suggesting that more aggressive structural separation might ultimately be necessary.

How does artificial intelligence affect this case?

Emerging AI-powered search services like Chat GPT and Perplexity represent alternatives to traditional search that might be less constrained by distribution barriers. If AI-powered synthesis becomes the dominant search paradigm, Google's traditional search dominance becomes less important. However, AI-powered search faces similar challenges reaching users without distribution advantages. The case's outcomes might influence whether remedies extend to emerging search technologies or focus purely on traditional search services.

What happens if Google wins the appeal?

If Google wins the appeal, the monopoly ruling would be reversed, remedies would be canceled, and Google could continue its current practices without restriction. The company could maintain exclusive default arrangements, continue controlling distribution channels, and operate without forced data sharing or syndication obligations. This outcome would suggest that current antitrust law is insufficient to address tech platform dominance, likely prompting congressional action toward new legislative frameworks.

What international implications does this case have?

The European Union has conducted parallel investigations into Google's search practices and has previously fined Google billions for anticompetitive conduct. EU remedies could be more aggressive than U. S. orders, potentially including forced divestiture. China and India are developing their own tech regulation approaches. Google's case outcomes in the U. S. will influence regulatory approaches globally, either emboldening aggressive enforcement or suggesting that current legal frameworks lack adequate tools for addressing digital dominance.

How would data sharing remedies actually work?

Google would provide competitors with anonymized, aggregated search data including query patterns, result click-through rates, and relevance signals. Competitors could use this data to train machine learning systems, understand what queries mean, and identify where their search results could improve. Implementing this requires technical infrastructure ensuring data security, adequate anonymization, and sufficient volume and quality for competitors to meaningfully improve their search capabilities without violating user privacy.

Key Takeaways

- Judge Mehta ruled Google maintains an illegal search monopoly through exclusive default arrangements and distribution control

- Google commands 92% of search market share, with 87-94% of users accepting default search engine placements

- Google's remedies require data sharing with competitors and search result syndication on reasonable terms

- The appeal process will likely extend 4-5 years with potential Supreme Court involvement pushing timeline to 2027-2029

- Alternative search engines like Bing face distribution barriers rather than product quality issues, preventing scale

- Data sharing remedies must balance competitive benefits against privacy risks from distributing sensitive search data

- AI-powered search alternatives represent potential disruption but face identical distribution barriers as traditional competitors

- Google's distribution dominance generates $175-200 billion in annual search advertising revenue driving aggressive defense

- Failed appeals could trigger legislative action with potentially more aggressive remedies than current court orders

- Case outcomes will reshape how antitrust law addresses digital platform dominance globally