![Netflix, Warner Bros., and Paramount Merger War [2025]](https://tryrunable.com/blog/netflix-warner-bros-and-paramount-merger-war-2025/image-1-1771337149149.jpg)

The Streaming Wars' Biggest Gamble: Netflix vs. Paramount for Warner Bros. Discovery

Picture this. It's early 2025, and the streaming industry just exploded into chaos. Not the kind that kills companies (though that's happening too). The kind that reshapes entertainment forever.

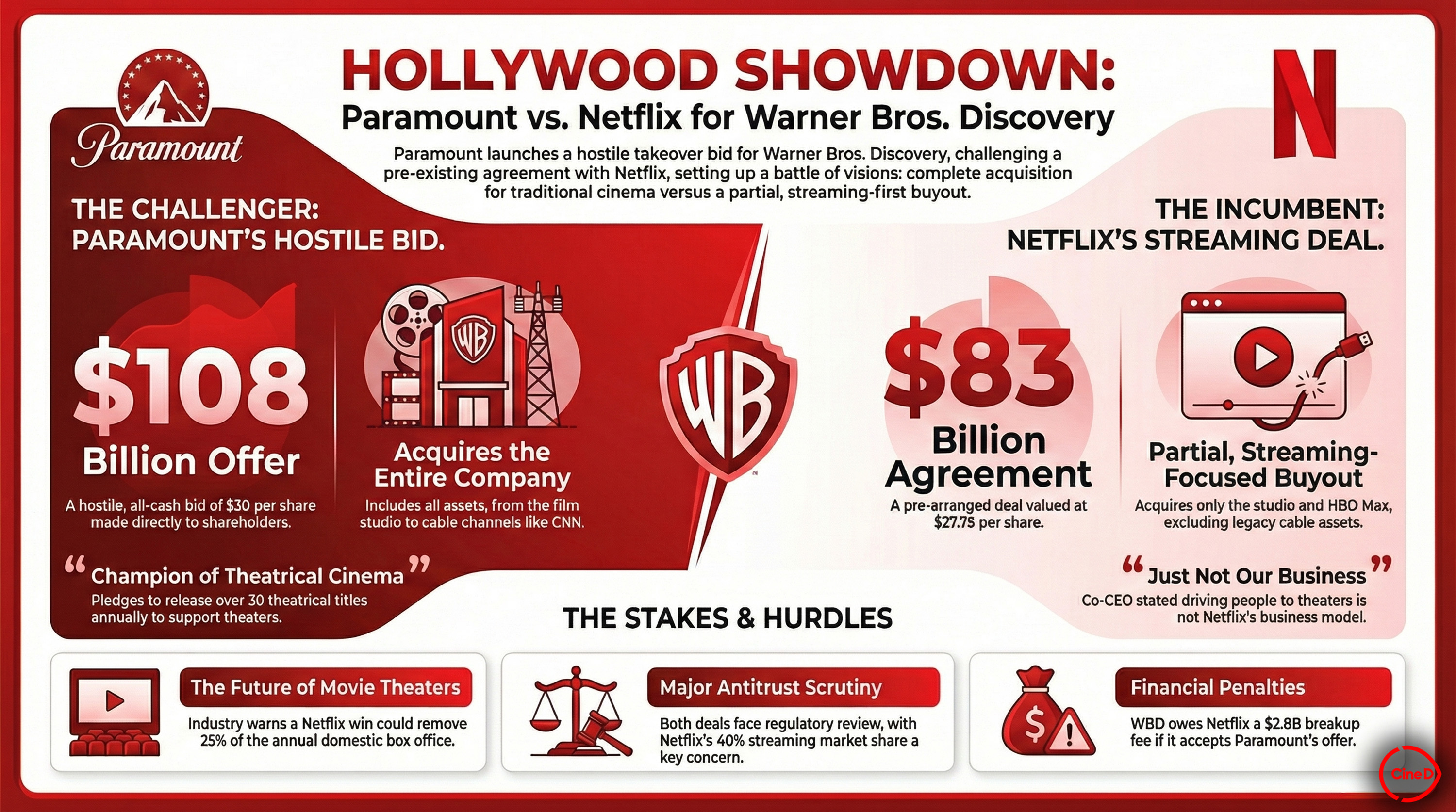

Netflix is trying to buy Warner Bros. Discovery for $82.7 billion. Not just the streaming service. The entire studio. HBO, Max, DC Comics, the whole thing. It's the biggest entertainment acquisition anyone's talked about in years.

But then Paramount, led by aerospace billionaire David Ellison, comes in swinging with a competing offer. And suddenly we're watching one of the most consequential corporate battles of the decade play out in real time.

Here's the thing: this isn't just about money or corporate egos. This deal will determine what you watch, how you watch it, and honestly, whether small studios survive in a streaming-dominated world. The winner gets a content empire. The loser gets knocked back to the minor leagues.

I've been following media deals for years. I've never seen stakes this high.

TL; DR

- Netflix offered $82.7 billion to acquire WBD's entire studio and streaming service in what could be the entertainment industry's biggest deal ever

- **Paramount countered with 2.8 billion Netflix termination fee to restart negotiations, as reported by Reuters.

- WBD gave Paramount one week to present its "best and final" offer, creating a ticking clock drama that will define streaming's future, according to Reuters.

- National security concerns emerged when Netflix raised issues about Middle Eastern funding backing Paramount's bid, specifically Saudi Arabia's Public Investment Fund, as noted by CNN.

- WBD shareholders vote March 20th, making this the most critical moment for the streaming industry's consolidation strategy.

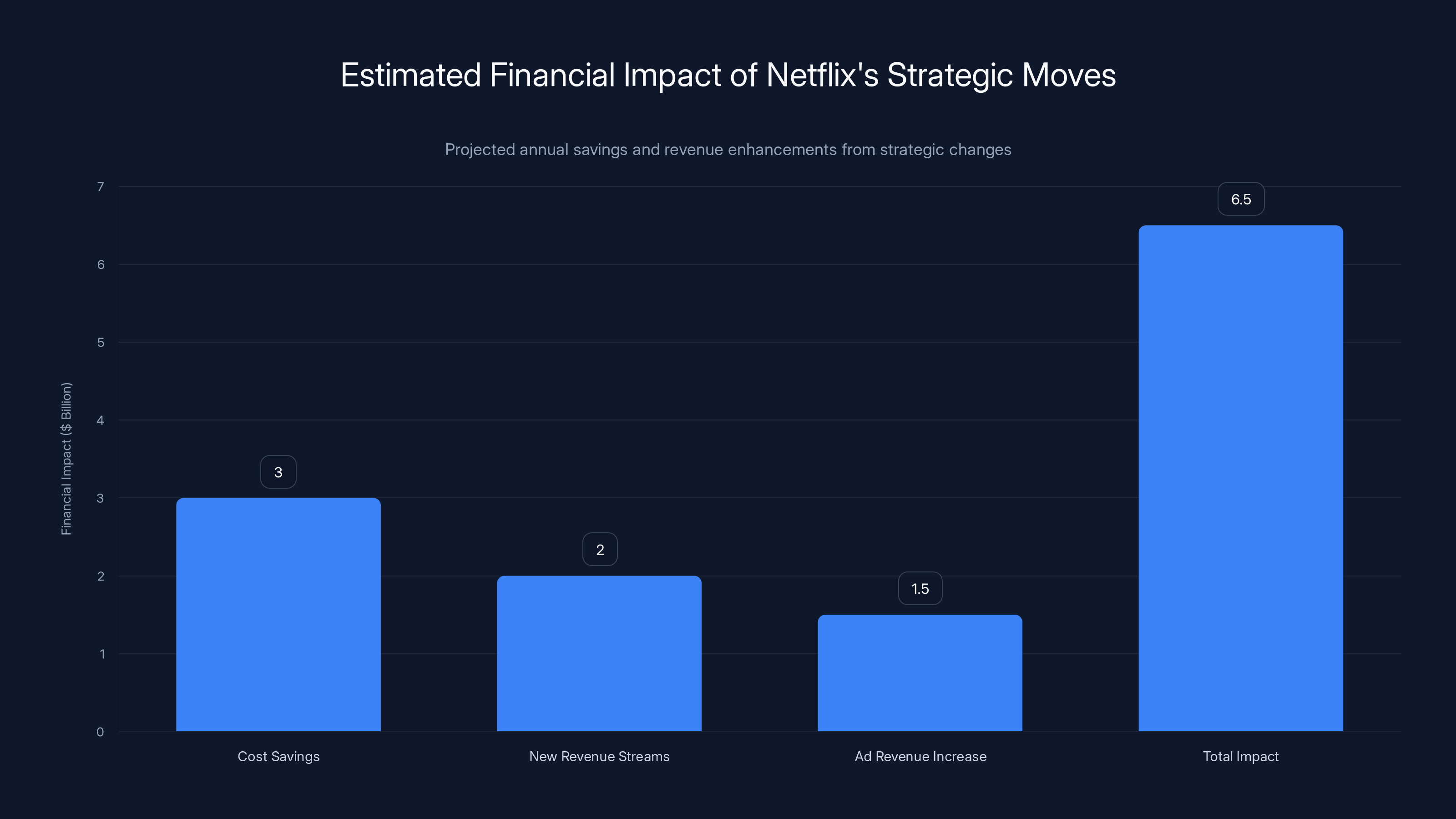

Estimated data suggests Netflix could achieve a total financial impact of $6.5 billion annually through cost savings, new revenue streams from HBO and DC content, and increased ad revenue. Estimated data.

Why $82.7 Billion Isn't Just a Big Number

Let's start with the Netflix offer. $82.7 billion sounds abstract. Let me make it real.

That's more than Apple paid for Beats Electronics. More than Microsoft paid for Activision Blizzard, which held the record for biggest tech deal ever at $69 billion. More than most countries' annual GDP.

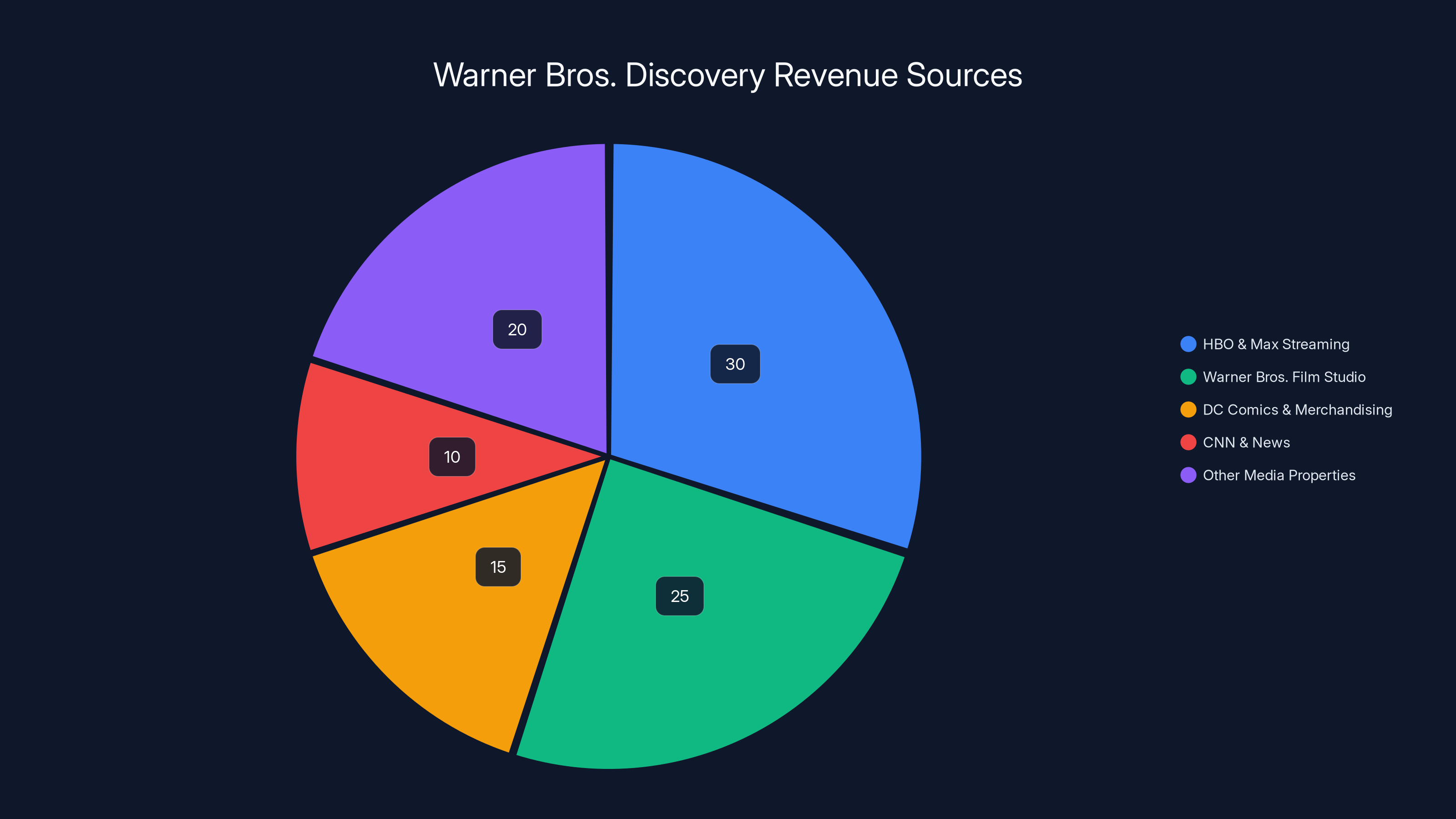

For that money, Netflix gets everything WBD owns. The HBO brand that's synonymous with premium television. The DC Comics universe, which has fumbled recently but still owns characters worth billions. CNN's vast news archive. Thousands of hours of Warner Bros. films. The Max streaming platform, which competes directly with Netflix today.

Why would Netflix want all this? Because streaming economics have shifted dramatically. When Netflix started making originals, the model was simple: spend billions on content, keep subscribers paying $15/month forever.

That stopped working.

Subscribers got cheaper tastes. Costs got higher. Competitors multiplied. Netflix's profit margins compressed. Suddenly, content libraries matter more than ever. Old films drive new subscriber interest. Franchises generate multiple revenue streams—streaming, merchandise, theme parks, theatrical releases.

WBD's assets solve this. HBO's prestige drama library brings cultural credibility Netflix sometimes lacks. DC Comics creates franchise opportunities. The studio itself produces films that can go theatrical first, maximize revenue, then come to streaming. It's vertical integration in its purest form.

Estimated data shows HBO & Max Streaming as the largest revenue source for Warner Bros. Discovery, followed by Warner Bros. Film Studio. Estimated data.

The Paramount Counter-Punch Nobody Expected

Here's where it gets interesting. Most people assumed WBD and Netflix would announce the deal, shareholders would vote yes, and by late 2025, Netflix would own the largest entertainment conglomerate outside Disney.

Then David Ellison decided otherwise.

For those unfamiliar, Ellison isn't a media executive. He's a billionaire tech entrepreneur who led Skydance Media into major studio territory through smart acquisitions and partnerships. He's backed by enormous pools of capital, including Saudi Arabia's Public Investment Fund.

Paramount came back with a

Here's the catch: Paramount explicitly said this wasn't their best offer. It was basically a conversation starter. A way of saying, "Hey WBD, let's actually talk." And it worked. WBD reopened negotiations with Paramount and gave them one week to present the real offer, as detailed by Reuters.

Why would Paramount even try? Because if Netflix buys WBD, Paramount becomes the industry's clear third player. Netflix gets the content fortress. Disney already has its empire (Disney+, Hulu, ESPN+). Paramount would be running to stay in place, competing against companies with way more resources.

Buying WBD lets Paramount consolidate. HBO Max (soon to be Max, if it isn't already) merges with Paramount+. Suddenly you're looking at a streaming platform with HBO's prestige, Paramount's franchises, and coverage across drama, comedy, reality, news, and sports.

It's the kind of move that makes strategic sense if you believe streaming consolidation is coming. And honestly, it probably is.

How a 7-Day Deadline Changed Everything

Let's talk about the timeline, because timelines matter in these deals.

WBD shareholders are voting on the Netflix merger March 20th. That's the hard deadline. Before that vote happens, WBD gave Paramount exactly seven days to present its best offer.

Why seven days? Because Netflix's deal comes with protections. If a competing bidder emerges (which Paramount did), Netflix gets a waiver period to renegotiate. Seven days is the window.

This creates incredible pressure. Paramount can't do two months of due diligence. They can't model out every scenario carefully. They have to move fast or lose the window completely.

WBD knows this. It's why they gave one week instead of two. They want to force Paramount's hand while still appearing to negotiate in good faith. If Paramount comes back with a real offer that beats Netflix, then WBD shareholders face a genuine choice. If Paramount can't get the numbers right in seven days, WBD has cover to go with Netflix.

The mathematics matter here too. Let's do some quick calculation.

For Paramount to beat Netflix's offer, they'd need to price WBD significantly higher than

Paramount has backing from Saudi Arabia's PIF, which manages over $900 billion in assets. So capital availability isn't the constraint. Demonstrating that the deal makes financial sense is the constraint. Paramount has to show WBD shareholders that they'll actually finance this, close this, and create value from the combined entity.

Paramount's

The National Security Curveball

Then Netflix played what might have been the smartest move in the entire negotiation.

They raised national security concerns about Paramount's bid.

Specifically, Netflix pointed out that Paramount's financing includes Middle Eastern investment, primarily from Saudi Arabia's PIF. They suggested this creates security issues because you'd have a foreign government sovereign wealth fund partially owning a major American media company.

It's a fascinating move because it's not wrong, but it's also not the reason Netflix is upset. Netflix is upset because they're losing a deal. But the national security angle is real enough that it can influence regulators.

Congress has increasingly scrutinized foreign investment in American media and technology. Saudi Arabia's PIF already has stakes in golf leagues and other American entities. Another major media play could trigger real regulatory resistance.

In a representative's letter, Rep. Sam Liccardo (D-CA) specifically questioned whether a Saudi-backed Paramount owning WBD creates appropriate security guardrails. It's not a blocking move, but it's a caution light. Deals have died for less.

This is where the deal gets weird. Because here's the thing: if Paramount wins the auction, they'll still have to deal with these concerns. They can address them. Sovereign wealth funds own stakes in all kinds of American companies. Disney's board includes people with Saudi connections. It's not impossible to navigate.

But it adds complexity. It adds regulatory uncertainty. It potentially delays the deal or adds conditions that make it less attractive financially.

Netflix knows this. By raising it publicly, they're essentially saying to regulators: "Hey, something worth thinking about here." It's not playing dirty, exactly, but it's definitely playing smart.

The Warner Bros. Dilemma: Money vs. Certainty

Here's where we need to think like WBD's board of directors.

You're sitting on this board. You have fiduciary duty to shareholders. Netflix offers you $82.7 billion in a deal that's basically already approved by your board. Your shareholders can vote yes or no, but you're recommending yes.

The deal is slightly complicated but doable. Netflix is solid financially. They've got the cash or financing lined up. Regulators probably approve this (there are some antitrust questions, but nothing deal-killing). The deal closes, probably by late 2025.

Then Paramount comes in. They say they'll beat this. But they need a week to prove it.

What's your play?

If you say no immediately, you're gambling Netflix stays interested at $82.7 billion. You're betting the deal closes clean. You're reducing downside risk for shareholders.

If you say yes to Paramount's week, you might get $85-90 billion. You might get a better synergy story for shareholders. But you also introduce risk. What if Paramount's financing falls through? What if regulators block it? What if the deal dies and Netflix walks?

WBD's board chose the cautious middle path. Give Paramount the week. Keep Netflix at the table. Make sure both bidders know you're serious about best value, but Netflix is the fallback.

WBD chairman Samuel Di Piazza Jr. made this clear in the official statement. WBD still believes Netflix is the better deal because it's lower risk, faster to close, and more certain to get regulatory approval. But they're open to being surprised if Paramount brings enough value to justify the uncertainty.

Netflix's offer stands at

Streaming's Consolidation Reckoning

Let me zoom out and talk about what this deal means for the entire streaming industry.

Since 2015, we've watched streaming expand from "Netflix and maybe HBO" to dozens of platforms competing for your attention. Disney+, Amazon Prime Video, Paramount+, Peacock, Apple TV+, Max, Roku, and seventeen others I'm forgetting.

The economics fell apart. Too many services, not enough subscribers. Everyone loses money. Consolidation becomes inevitable.

WBD+Netflix merger is step one of that consolidation. It's Netflix saying: "Okay, competing on content budget alone doesn't work. We need a studio. We need an archive. We need scale." It's vertical integration, which should theoretically make Netflix more profitable and more able to invest in new content.

If Paramount wins instead, it's a different kind of consolidation. Skydance gets bigger. Paramount gets stronger. But Netflix still exists as a standalone competitor. The market gets more concentrated but less integrated.

Either way, you're looking at a future where maybe four or five streaming platforms dominate. Netflix or Netflix+WBD. Disney with its three services. Amazon (which barely tries). Maybe Apple. Maybe someone else.

Smaller players die or get acquired. Content creators have fewer buyers. Consumer choice paradoxically gets worse even as competition gets "fiercer." Everyone pays more and has more services (as ads become standard).

For creators, this is complicated. More money consolidates at major platforms, which sounds good for big studios. But less competition means lower bidding on projects. Independent creators get squeezed harder. The economics shift against anyone not making content for Netflix, Disney, or Paramount.

For consumers, the paradox deepens. We abandoned cable because streaming was cheaper. Now we've got six streaming subscriptions costing $100+/month. We're right back where we started, except now we're paying different companies and watching on our phones instead of TV.

Netflix's Strategic Rationale

Why is Netflix willing to spend $82.7 billion?

Let's think like their CEO. Netflix's core business is stable but not growing fast. Subscriber growth has slowed. Average revenue per user plateaus in developed markets. Stock price depends on convincing investors they have a growth story. What's the growth story if you're just Netflix?

You run out of room. You can raise prices (which causes churn). You can add ads (which makes the service worse and attracts lower-value subscribers). You can expand internationally (where economics are worse). Or you can fundamentally change the business.

WBD changes the business. HBO content gives Netflix prestige shows they can't build from scratch. DC Comics opens merchandising and franchise revenue streams. The studio lets Netflix make theatrical films that maximize revenue before coming to streaming. It's not just more content. It's more profitable content.

Netflix also gets more leverage with advertisers. Right now, Netflix ads are valuable because Netflix is Netflix. Add HBO's audience. Add DC movies. Add the studio's theatrical pipeline. Suddenly you're not selling ads on Netflix. You're selling ads on HBO, Netflix, DC, and a studio's theatrical releases. That's way more valuable.

The financial math works if Netflix can extract synergies. Which is corporate speak for "they need to cut costs and overlap." There will be layoffs. There will be duplicate roles eliminated. WBD and Netflix will consolidate streaming platforms (probably onto Max or something new). They'll rationalize their content spend.

If Netflix executes this right, they could save $2-4 billion annually. That's real money. Over five years, that justifies much of the acquisition cost.

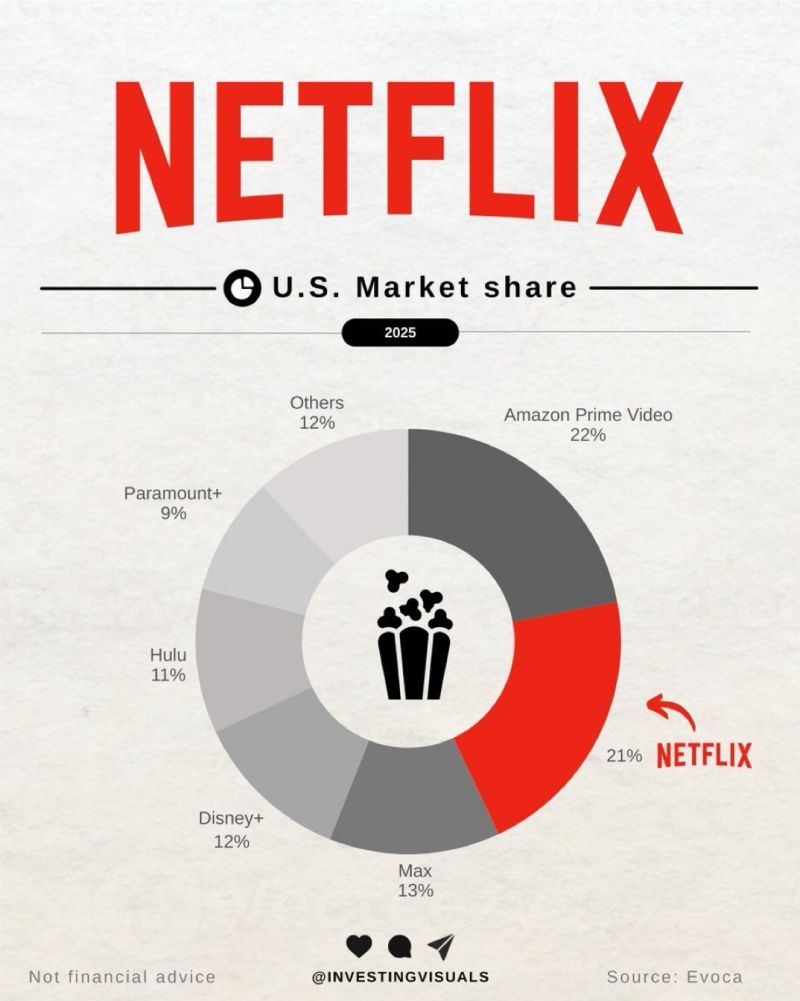

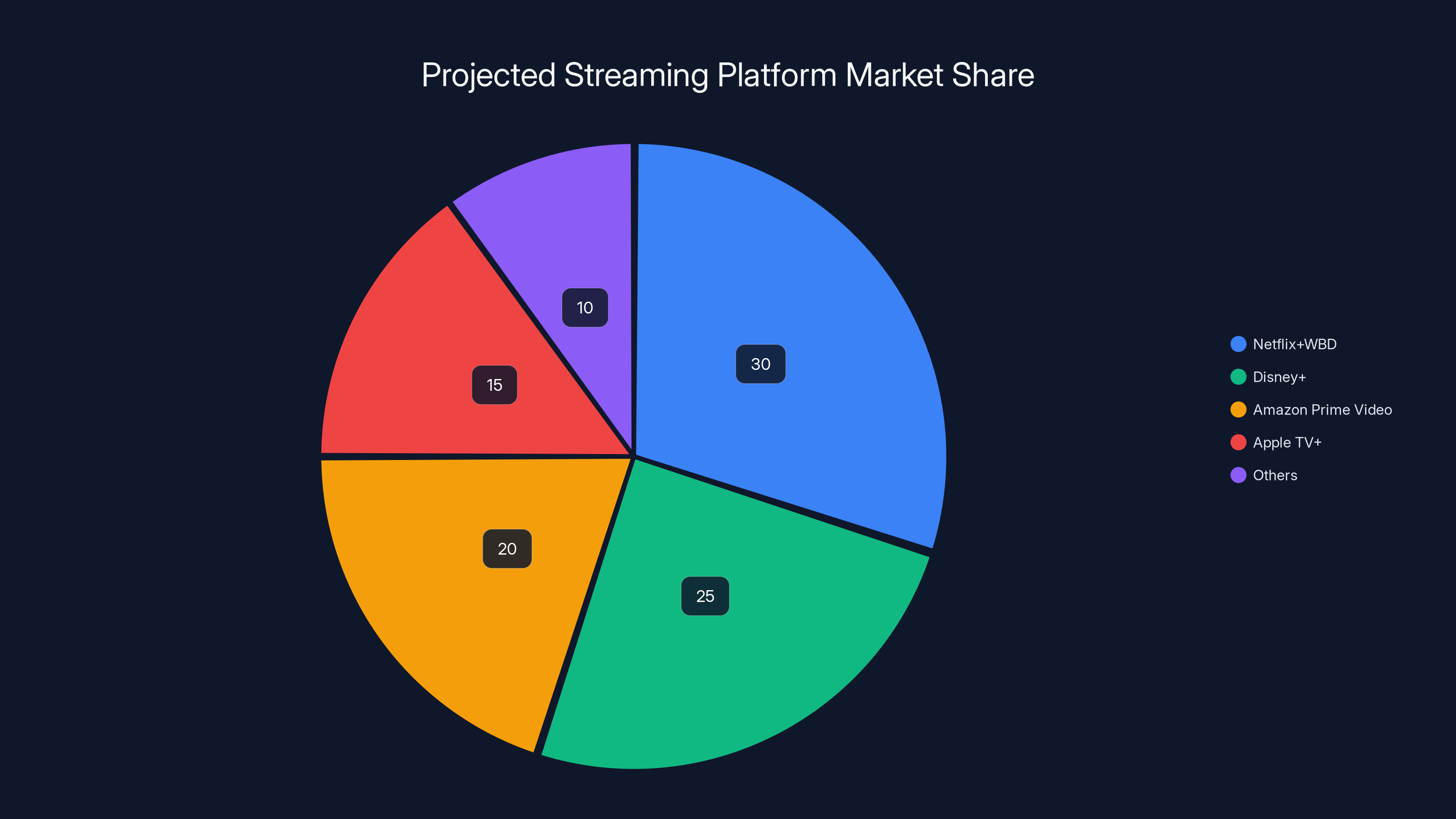

Estimated data suggests that post-consolidation, Netflix+WBD could hold the largest market share at 30%, followed by Disney+ and Amazon Prime Video. Smaller platforms may either merge or be acquired.

Paramount's Gamble

Now let's think like Paramount.

Paramount's current situation: they own a profitable studio, but Paramount+ is losing money and losing market share. They're number three in streaming after Netflix and Disney. They're getting crushed.

Option A: Stay independent. Keep trying to make Paramount+ work. Probably fail in 5-10 years. Get acquired cheap, or just fade.

Option B: Buy someone else. Get scale. Get a better streaming platform. Have a shot at competing.

Buying WBD is option B on steroids. WBD has HBO, which already has premium content and a subscriber base. WBD has the DC Comics franchise. WBD has a massive studio. If Paramount acquires this, suddenly they're not just a mid-tier streamer. They're a genuine competitor to Netflix and Disney.

The problem is it's insanely expensive. Paramount would have to finance $80+ billion in debt or equity. That's manageable for Skydance (which has Saudi backing), but it's a huge bet. If the combined Paramount+WBD doesn't work, if they can't integrate systems or content, if Netflix and Disney crush them anyway, Skydance/Paramount is in trouble.

But it's a reasonable gamble. If it works, you've got a top-two streaming platform. If it doesn't, you're not worse off than you were.

The Regulatory Minefield

Here's where this gets really complicated: neither deal is guaranteed to pass antitrust review.

Netflix acquiring WBD is less obviously problematic because Netflix is a different company in some ways. They're a distributor buying a studio. Traditional vertical integration. The Department of Justice usually allows that.

But it's not straightforward. If Netflix+WBD becomes so dominant that they can dictate terms to theaters, talent, and competing platforms, regulators might block it. It's unlikely, but not zero probability.

Paramount acquiring WBD is arguably more problematic from an antitrust angle. You're merging two studios. Two streaming platforms. It's horizontal consolidation, which regulators view more skeptically. You're also adding foreign sovereign wealth fund ownership, which creates national security questions.

However, Paramount's deal probably survives antitrust review too. They're number three in streaming (Disney and Netflix are bigger). Merging number three (Paramount) with number five or six (WBD) to create a stronger number two doesn't obviously violate antitrust law.

The bigger risk for Paramount is that Congress or the administration decides foreign sovereign wealth fund ownership of American media is too concerning. That's not a traditional antitrust argument. It's a political argument. And politics can kill deals.

March 20: The Shareholder Reckoning

Here's where this story reaches its climax.

March 20th, 2025, WBD shareholders vote. That's when all this becomes real.

WBD's board is recommending the Netflix deal. But shareholders aren't just rubber stamps. If Paramount comes back with a materially better offer, shareholders might vote it down and tell the board to negotiate with Paramount instead.

Paramount has until the shareholders vote to make their pitch. They've got one week from whenever they officially started negotiating. After that, they need to convince WBD shareholders directly that a Paramount deal is better than Netflix.

This is where the deal could really turn. Because WBD shareholders include hedge funds that buy stocks based on deal value, activist investors who care about specific outcomes, and long-term investors who care about the company's strategic future.

The hedge funds want maximum bid value. If Paramount bids $85 billion and Netflix won't go higher, hedge funds vote Paramount. The activists might care about gaming this (Paramount owns DC and has gaming potential Netflix doesn't). Long-term investors might prefer Netflix's financial stability.

It's genuinely uncertain. And that uncertainty is exactly why Paramount's bid matters.

The Content Implication

Let's talk about what this deal means for the shows you watch.

If Netflix wins: You get HBO content on Netflix. You lose the Max platform as a separate app (unless Netflix keeps it). HBO shows have more money for production. Netflix's franchises get integrated into a longer content pipeline. You pay more (Netflix already said it's raising prices). You get more ads on cheaper tiers.

If Paramount wins: You get HBO on Paramount+. Paramount+ gets better (HBO's quality helps). You get DC content integrated with Paramount's franchises. Paramount gets more cash to invest in originals. But they're probably less stable than Netflix, so there's execution risk.

Either way, the number of streaming platforms in your TV menu gets smaller. Cord-cutting doesn't look as appealing anymore. The idea of "cutting the cord to save money" becomes laughable when you're paying $100+/month to eight streaming services.

Why This Deal Matters Beyond Entertainment

I know this sounds dramatic, but this deal is bigger than just "who owns HBO."

This is about whether consolidation in media is good or bad. It's about whether tech companies should buy media companies. It's about whether foreign investment in American media is acceptable. It's about whether streaming actually disrupted the media business or just recreated it online.

Netflix winning suggests tech disruption succeeds, but requires scale and integration. A tech company can own Hollywood. Paramount winning suggests media people still matter, foreign money can buy American assets, and consolidation is the only survival strategy.

Shareholders care because both outcomes affect profit potential. But consumers should care because it affects what we watch, how we watch it, and how much we pay.

This deal is where streaming's chaotic growth phase becomes its oligopoly phase.

The Week Ahead

Paramount has about seven days from the board's announcement to present an offer that actually works.

They need to:

- Finalize financing terms with their banks and Saudi backing

- Model out the combined entity's revenue and cost structure

- Present a bid that's higher than $82.7B but not so high it's financially irresponsible

- Make a convincing case that they can actually close this deal without regulatory intervention

- Show WBD shareholders why Paramount+WBD is better long-term than Netflix+WBD

It's a lot to do in a week. But Paramount's had months to prepare contingently. This might look rushed on the outside while being planned on the inside.

The odds? I'd say Netflix's deal is probably 60-65% likely to close as-is. Paramount maybe 30-35% likely to win an auction. Something else (deal dying, compromise emerges) maybe 5%.

But those odds shift based on Paramount's bid. If they come in at

The Cascading Effects

Here's what happens to the broader industry if Netflix wins:

Immediately: WBD announces integration plans. Layoffs happen fast. Platform consolidation starts. HBO Max probably becomes "Netflix Max" or just Max (depending on branding). Stock prices adjust. Other studios watch nervously.

In 6 months: Netflix has absorbed WBD's assets. They're announcing cost synergies. They're showing Wall Street why this deal justifies the price. They're probably raising prices or introducing new ad tiers.

In 1-2 years: Netflix+WBD starts generating combined value. Theatrical releases come to streaming faster. HBO prestige content sits next to Netflix originals. You're watching DC movies that go HBO-on-Max instead of premium VOD windows.

In 3-5 years: Other streaming platforms accelerate consolidation to compete. Amazon might buy MGM+ or similar. Apple might acquire more studios. Disney+ and Hulu fully merge. The "seven streaming services" era ends. We're back to three or four major platforms that own everything.

If Paramount wins, the timeline is similar but Paramount is the integrator instead of Netflix.

FAQ

What exactly is Warner Bros. Discovery?

Warner Bros. Discovery is a media conglomerate formed in 2022 when Warner Media merged with Discovery, Inc. It owns the HBO network, the Max streaming platform, Warner Bros. film studio, DC Comics, CNN, the Warner Bros. archives of thousands of films and TV shows, and other media properties. The company generates about $50-55 billion in annual revenue but has struggled with streaming losses.

Why would Netflix want to buy Warner Bros. Discovery?

Netflix wants WBD for vertical integration. Owning a major studio gives Netflix access to an established content library, theatrical film releases that maximize revenue before coming to streaming, the HBO brand for prestige content, and the DC Comics franchise for merchandising and spin-offs. It also dramatically increases Netflix's advertising value because they'd own more content across more platforms. Essentially, Netflix transforms from a pure distributor to a studio-distributor, which should improve profitability.

What's Paramount's advantage in competing for WBD?

Paramount's advantage is that they're a media company trying to stay relevant, so they could integrate WBD into their ecosystem more naturally than Netflix could. They already own Paramount+, the Paramount studio, CBS, and other assets. Buying WBD would make Paramount a genuine competitor to Netflix and Disney by combining their streaming platform with HBO's superior content. However, their disadvantage is execution risk. They have less cash than Netflix and more integration complexity.

Why does national security matter in this deal?

Paramount's bid is partially backed by Saudi Arabia's Public Investment Fund, a sovereign wealth fund that manages over $900 billion. Congress has increasingly scrutinized foreign ownership of American media companies on national security grounds. Having a Saudi-controlled entity partially own major American media assets (HBO, Warner Bros., CNN) creates regulatory complications. Netflix raised this concern specifically to create doubt about Paramount's deal, though the national security argument is legitimate enough that regulators would consider it.

What happens to me as a viewer if Netflix wins?

If Netflix wins, HBO content becomes part of Netflix's platform, likely ending Max as a separate app. You'd watch HBO shows on Netflix instead of Max. Netflix would probably raise prices or reduce ad-free tier availability to offset acquisition costs. You'd get access to a larger content library immediately, but potentially pay more for it. Streaming becomes more consolidated, with fewer competing platforms.

What if Paramount wins instead?

If Paramount wins, you'd likely see HBO integrated into Paramount+, which would become a much stronger streaming platform. Paramount+ would have HBO's prestige content, better financial backing, and more investment in originals. The downside is Paramount's less financially stable than Netflix, so there's execution risk. Your experience depends on whether Paramount successfully integrates and competes, or whether the combined entity struggles under the debt load and eventually gets acquired by someone else.

Could this deal actually fail?

Yes. Regulatory issues, financing problems for Paramount, or a change in market conditions could kill either deal. However, the Netflix deal is more likely to close because they have clearer financing, lower regulatory risk, and WBD's board support. The Paramount deal is riskier but not impossible. Most likely scenario is Netflix wins, but there's a genuine 25-35% chance Paramount's bid succeeds if they come in significantly higher than $82.7 billion.

When will we know the outcome?

WBD shareholders vote March 20th, 2025. Paramount has until then (officially about a week from the announcement) to present their competing offer. If they come with a compelling bid, shareholders might vote it down and force the board to negotiate with Paramount. If not, they vote for Netflix. The deal closes later in 2025, probably by late Q3 or Q4.

Why should I care about this deal?

You should care because this determines what streaming looks like for the next decade. It's the turning point from fragmented streaming to consolidated streaming. It affects pricing, content availability, and whether tech companies or media companies control your entertainment. It also signals to the industry what consolidation looks like, which will drive similar deals down the line.

What's the realistic play here?

My read: Netflix closes this deal at $82.7 billion or slightly higher (if Paramount pushes the bid up). WBD shareholders vote yes. Integration begins. By 2026, HBO's on Netflix, Max either becomes a Netflix product or disappears, and streaming consolidation accelerates. Paramount stays independent but weaker. Another five years, we're probably down to Netflix, Disney, Amazon, and one other player (maybe Apple or a consolidated Paramount). Streaming prices reflect that consolidation. Consumers lose the "cord-cutting is cheaper" narrative.

The Endgame

This deal represents the end of streaming's wild west phase.

For five years, we watched every media company and their cousin launch a streaming platform. It was chaos. It was exciting. It was also unsustainable. Too many platforms, not enough viewers, not enough profit.

Consolidation was always coming. The only question was how fast and who would survive.

WBD is the first mega-consolidation. Netflix buying an entire studio is the moment the industry matures. After this, expect Amazon to make moves. Expect Apple to accelerate its media strategy. Expect Disney to strengthen their position. Expect smaller players to realize they can't compete and get bought or die.

In ten years, your TV menu might look like: Netflix+HBO, Disney+, Amazon Prime Video, maybe Apple TV+, maybe sports-specific platforms. That's it. Cord-cutting saved money for a moment. Then we recreated the old system online and called it progress.

The irony is perfect. We hated cable's bundling and pricing. Streaming promised freedom. Now we're back to paying $100+/month for bundled streaming services with rotating content. We've traded remote controls for apps, but the fundamentals stayed the same.

What changed? Netflix and everyone else realized that disruption is expensive. You can't disrupt an industry by charging less and losing money forever. You have to build sustainable business models. Sustainable business models require scale. Scale requires consolidation.

Paramount's bid is a last gasp of competition. Netflix's bid is the consolidation winner proving they can handle the future. One of them will own Warner Bros. Either way, the era of independence ends.

March 20th will tell us which direction this goes. But the direction itself is already determined. Consolidation is coming. This deal just accelerates it.

We're not disrupting media anymore. We're reorganizing it. That's less exciting, but far more profitable. And that's what Wall Street has wanted all along.

Key Takeaways

- He's a billionaire tech entrepreneur who led Skydance Media into major studio territory through smart acquisitions and partnerships

- Here's the catch: Paramount explicitly said this wasn't their best offer

- Before that vote happens, WBD gave Paramount exactly seven days to present its best offer

- For Paramount to beat Netflix's offer, they'd need to price WBD significantly higher than $82

- Market conditions matter, but let's say they'd need to reach $90+ billion to even get WBD shareholders interested

Related Articles

- Indian Pharmacy Chain Data Breach: How Millions Were Exposed [2025]

- Best Fitness Earbuds to Keep You Motivated Through Workouts [2025]

- Solar Thermal Energy Storage: How Molecules Store Heat for Months [2025]

- NYT Strands Answers & Hints Game #716 Feb 17 [2025]

- PS5 Presidents' Day Deals 2025: $100 Off + Fortnite Bundle [2025]

- 2026 TechRadar Australian PC Awards Finalists: Complete Guide [2025]