![SEC Considering Shift to Twice-Yearly Earnings Reports [2025]](https://tryrunable.com/blog/sec-considering-shift-to-twice-yearly-earnings-reports-2025/image-1-1773707680211.jpg)

SEC Considering Shift to Twice-Yearly Earnings Reports [2025]

The financial reporting landscape could be on the verge of a significant transformation. The U.S. Securities and Exchange Commission (SEC) is contemplating a shift from the traditional quarterly earnings reports to a semiannual system. This change is aimed at reducing the compliance burden on public companies and potentially encouraging more firms to go public, as detailed in a Wall Street Journal article.

TL; DR

- Potential Change: The SEC is considering moving from quarterly to twice-yearly earnings reports to alleviate the reporting burden, as reported by another Wall Street Journal report.

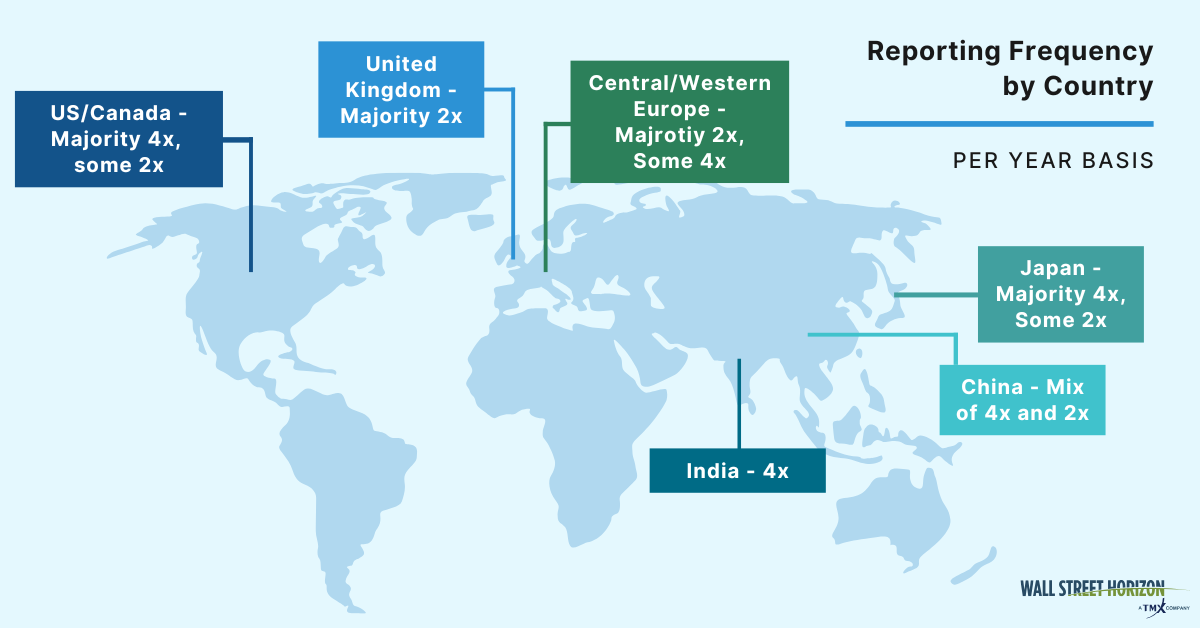

- Current Requirement: Companies have been reporting quarterly for over 50 years, but the practice is seen as costly and burdensome by many, as highlighted by Board Member.

- Public Company Attraction: A semiannual system may incentivize private companies to go public, increasing market participation, according to Benefits and Pensions Monitor.

- Criticism and Support: While some argue it may lead to less transparency, others believe it could foster long-term planning, as discussed in CFO Brew.

- Future Implications: If implemented, this shift could reshape financial strategies and investor relations, as noted by Morningstar.

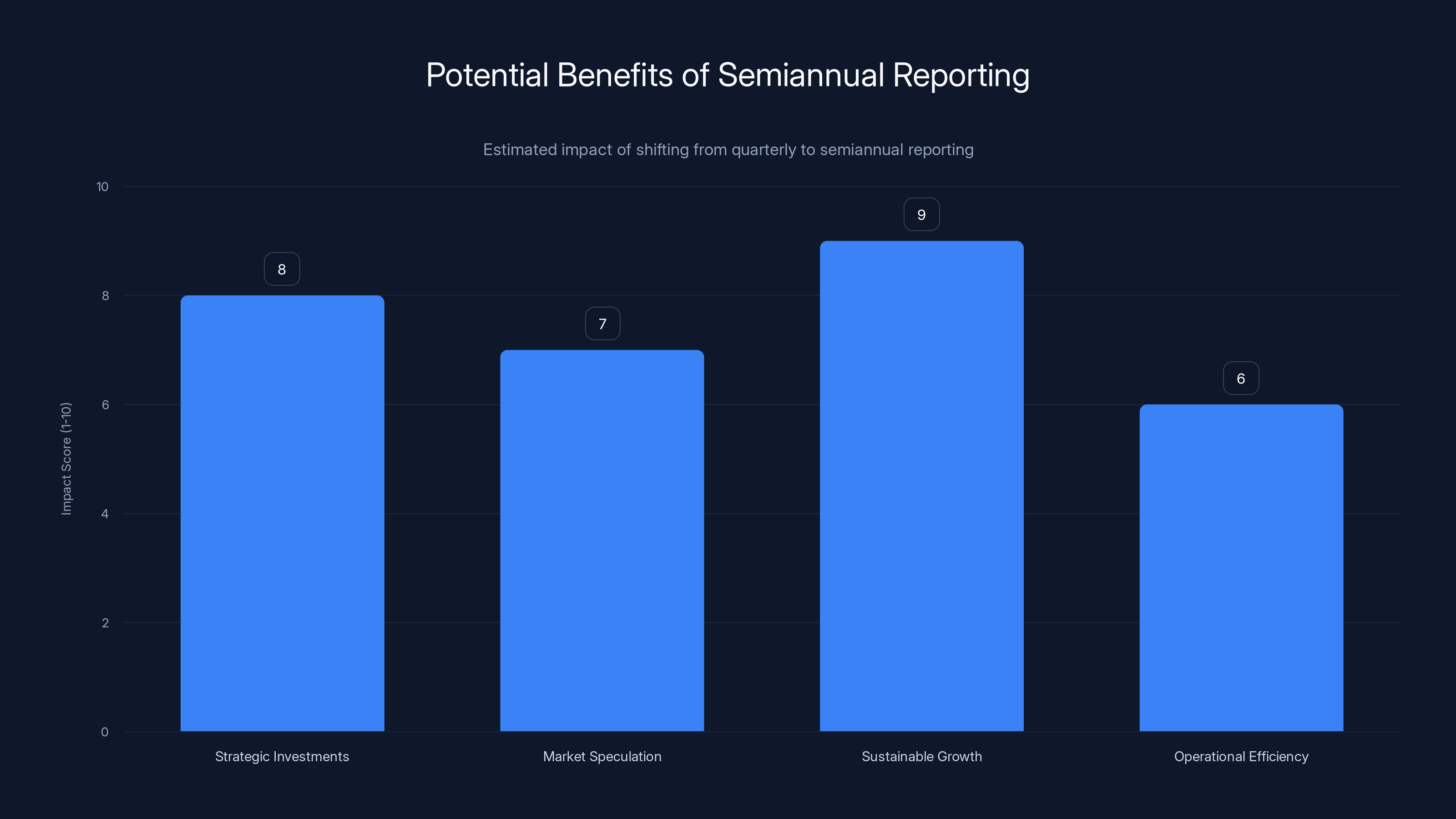

Estimated data suggests that semiannual reporting could significantly enhance strategic investments and sustainable growth by reducing short-term pressures.

The Current State of Quarterly Earnings Reports

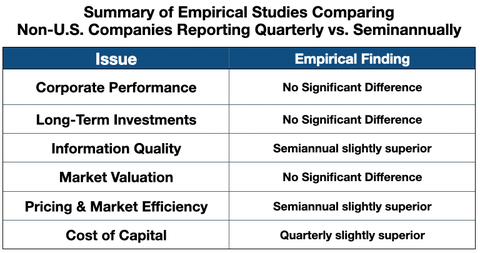

Quarterly earnings reports have been a cornerstone of financial transparency for over five decades. These reports provide investors with regular updates on a company's financial health, influencing investment decisions and stock prices. However, they come with significant costs and pressures for the companies involved, as noted by Calgary's Financial Task Force.

The Burden of Quarterly Reporting

For many companies, preparing for quarterly earnings reports is a resource-intensive process. Finance teams must compile detailed financial data, prepare comprehensive reports, and often engage in extensive auditing processes. This can divert resources from other strategic initiatives, as highlighted by Adobe's insights.

Key Challenges:

- Resource Allocation: Companies must allocate significant resources to ensure accurate and timely reporting.

- Market Pressure: The need to meet short-term expectations can lead companies to prioritize immediate results over long-term strategies.

- Volatility: Frequent reporting can lead to increased stock price volatility, as investors react to each quarterly update.

Estimated data shows that companies could benefit most from reduced compliance costs, while investors might face increased uncertainty. Estimated data.

Why the SEC is Considering a Shift

The discussion around moving to twice-yearly earnings reports is driven by several factors. Proponents argue that reducing the frequency of reports could mitigate some of the challenges associated with quarterly reporting, as discussed in WHBL's report.

Encouraging Long-Term Planning

One of the main arguments for semiannual reporting is that it could encourage companies to focus more on long-term strategic planning rather than short-term performance. By reducing the frequency of earnings reports, companies might have more freedom to pursue sustainable growth strategies, as suggested by Ramaco Resources.

Benefits of Long-Term Focus:

- Strategic Investments: Companies might be more willing to invest in R&D and capital projects without the pressure of quarterly scrutiny.

- Reduced Market Speculation: With fewer reports, there could be less opportunity for speculative trading based on short-term financial performance.

Potential Impacts on the Market

Transitioning to a semiannual reporting system could have widespread implications for the market, investors, and companies themselves.

Investor Reactions

Investors rely on quarterly reports to make informed decisions. A move to twice-yearly reports might necessitate changes in how investors gather and interpret information, as noted by Benefits and Pensions Monitor.

Potential Investor Concerns:

- Reduced Transparency: Some investors fear that less frequent reporting could lead to a lack of transparency.

- Increased Uncertainty: Longer gaps between reports might increase uncertainty about a company's performance.

Company Strategies

Companies might adjust their strategies if the reporting frequency changes. This could influence everything from financial planning to communication with investors, as discussed in CFO Brew.

Strategic Adjustments:

- Enhanced Communication: Companies may need to enhance their communication strategies to keep investors informed between reports.

- Operational Flexibility: Reduced reporting frequency could grant companies more operational flexibility to pursue strategic goals.

Estimated data shows that resource allocation is the most significant challenge in quarterly earnings reporting, followed by market pressure and volatility.

Case Study: Impact on Tech Companies

Tech companies, often characterized by rapid growth and innovation, could be significantly affected by this change, as noted in NVIDIA's financial results.

Example: A Hypothetical Tech Firm

Consider a tech company focused on developing cutting-edge AI technology. With quarterly reports, the company might feel pressured to demonstrate immediate returns on its R&D investments.

Potential Benefits of Semiannual Reporting:

- Freedom for Innovation: The company could invest more heavily in innovative projects without the quarterly pressure to show immediate results.

- Strategic Partnerships: With a longer reporting cycle, the company might have more leeway to pursue strategic partnerships that align with its long-term vision.

Common Pitfalls and Solutions

While the shift to twice-yearly reports offers potential benefits, it also presents challenges that companies must navigate.

Pitfall 1: Reduced Investor Confidence

Solution: Companies can implement more robust investor relations programs, providing regular updates and insights even between formal reports, as suggested by Board Member.

Pitfall 2: Increased Market Speculation

Solution: Transparent communication and proactive engagement with analysts and investors can help mitigate speculation, as recommended by Calgary's Financial Task Force.

Future Trends and Recommendations

As the SEC explores this potential shift, several future trends and recommendations emerge for companies and investors.

Trend 1: Enhanced Digital Reporting

Companies might leverage digital platforms to provide more dynamic and interactive reporting methods, keeping investors engaged, as suggested by Adobe's insights.

Trend 2: Focus on ESG Reporting

With less frequent financial reporting, there may be a greater emphasis on Environmental, Social, and Governance (ESG) factors, offering a more holistic view of a company's performance, as noted by Morningstar.

Recommendation: Companies should integrate ESG metrics into their reporting frameworks to offer a comprehensive view of their operations.

Conclusion

The SEC's consideration of moving to twice-yearly earnings reports represents a potential shift in the financial reporting paradigm. While this move could reduce burdens on companies and encourage long-term planning, it also requires careful consideration of transparency and investor needs. As discussions continue, companies, investors, and regulators must work together to ensure that any changes benefit the broader market ecosystem.

FAQ

What is the current requirement for earnings reports?

Public companies are currently required to file earnings reports quarterly, providing regular updates on their financial performance, as outlined by Wall Street Journal.

Why is the SEC considering a shift to twice-yearly reports?

The SEC is exploring this change to reduce the compliance burden on companies and potentially encourage more private companies to go public, as discussed in WHBL.

How might this change affect investors?

Investors may face increased uncertainty with less frequent reporting, but it could also reduce short-term market volatility, as noted by Board Member.

What are the potential benefits for companies?

Companies could benefit from reduced reporting costs and the ability to focus more on long-term strategies, as highlighted by Ramaco Resources.

How can companies maintain transparency with less frequent reports?

Companies can enhance their investor relations strategies, providing regular updates and insights through digital platforms, as recommended by Adobe.

Will this change impact all public companies?

If implemented, the shift would affect all public companies, but specific impacts may vary based on industry and company size, as noted by Morningstar.

Key Takeaways

- The SEC is contemplating a shift to twice-yearly earnings reports to alleviate reporting burdens, as reported by Wall Street Journal.

- This change could encourage more private companies to go public by easing compliance requirements, as noted by WHBL.

- While it may foster long-term planning, there are concerns about reduced transparency and increased uncertainty for investors, as discussed in Board Member.

- Companies should enhance communication strategies to maintain investor confidence, as recommended by Adobe.

- Future trends may include a focus on digital and ESG reporting to provide a comprehensive view of company performance, as suggested by Morningstar.

Related Articles

- The Consequences of Misleading Revenue Claims in Tech Startups [2025]

- Navigating Turbulence: The Challenges and Future of xAI Amidst Constant Upheaval [2025]

- Unpacking the Sudden Closure of Digg's Open Beta: The AI Bot Spam Dilemma [2025]

- The Surge of Unicorns: Understanding the Rise of New Billion-Dollar Startups in 2026

- Meta's Deepfake Moderation: Challenges and Future Directions [2025]

- CEO Compensation: Google and Nvidia's Strategic Pay Increases [2025]