Steam Machine $700 Price Crisis: How Component Costs Could Reshape Gaming Hardware

Introduction: The Perfect Storm for Valve's Living Room Dream

Valve's Steam Machine represents one of the most ambitious hardware plays by a software-first company in modern gaming history. As a living room-focused PC gaming device designed to bring the flexibility of PC gaming into the traditional console space, the Steam Machine promised to offer something unique: the power of Steam's massive library with the convenience of a dedicated gaming appliance.

However, the company now faces an existential pricing challenge that could fundamentally alter the viability of this strategic initiative. In a critical blog post, Valve acknowledged that skyrocketing prices for essential components—particularly RAM and storage—have forced the company to "revisit our exact shipping schedule and pricing" for the Steam Machine. This seemingly technical supply chain announcement masks a deeper problem: Valve may be caught between market demands for affordability and the brutal economics of component sourcing.

The stakes couldn't be higher. According to industry analysts, a price point approaching $700 for the base model could prove catastrophic for market adoption. Meanwhile, component costs continue climbing in ways that larger console manufacturers can better absorb through sheer purchasing power. This convergence of technical challenges and market dynamics has created what industry observers are calling a potential "death sentence" for the platform—though the story is far more nuanced than that alarming headline suggests.

Understanding this situation requires examining not just the immediate pricing pressures, but the fundamental structural advantages and disadvantages Valve faces compared to established console makers, the psychology of gaming hardware purchasing, and the broader implications for innovation in the gaming industry. This article provides a comprehensive analysis of the Steam Machine pricing crisis, exploring how component costs shape hardware economics, what analysts expect for final pricing, and what this means for the future of PC gaming in the living room.

The

The Component Cost Explosion: Understanding the Technical Crisis

RAM Price Volatility in the Gaming Hardware Market

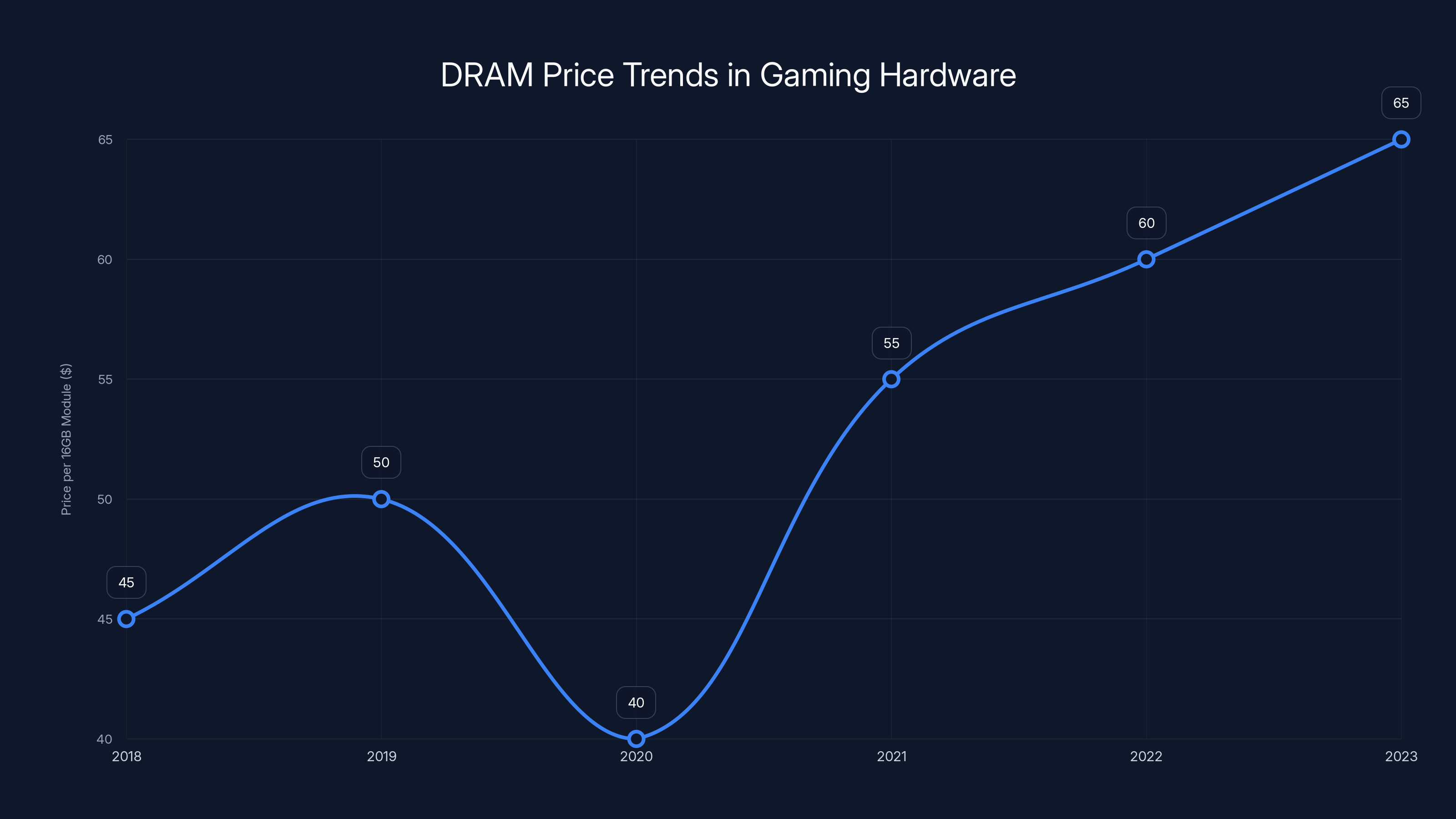

RAM pricing represents one of the most volatile factors in gaming hardware economics. Dynamic random-access memory (DRAM) prices follow cyclical patterns influenced by manufacturing capacity, demand across consumer electronics, and geopolitical supply chain disruptions. The gaming hardware market has historically benefited from periods of DRAM oversupply, allowing manufacturers to source memory at favorable rates.

The current pricing environment represents a significant departure from these historical patterns. Memory manufacturers have reduced production capacity in response to earlier demand weakness, creating supply constraints exactly when demand for gaming hardware components has intensified. A device like the Steam Machine, which requires high-capacity, low-latency memory for smooth 1080p or 4K gaming performance, is particularly sensitive to these price movements.

The difference between sourcing DRAM at

Storage Density and NAND Flash Economics

Solid-state drive (SSD) costs involve different but equally challenging dynamics. NAND flash memory, the fundamental technology enabling high-capacity SSDs, experiences its own supply and demand cycles. The shift toward larger storage capacities in gaming—modern AAA titles routinely exceed 100GB—means that gaming hardware manufacturers must provide increasingly generous storage to avoid creating poor user experiences from constant storage management.

The Steam Machine's design philosophy, emphasizing local storage rather than relying on cloud gaming or constant downloads, makes it particularly susceptible to NAND flash price fluctuations. Offering both 512GB and 2TB variants compounds this sensitivity. When NAND flash pricing increases by 15-25%, as has occurred in recent quarters, the cost difference between these tiers expands dramatically. A 2TB SSD might jump from

Additionally, gaming consoles and PC manufacturers compete for NAND flash supplies. When production capacity tightens, suppliers prioritize customers with long-term volume commitments and established relationships. Valve's newcomer status in hardware manufacturing puts the company at a disadvantage in negotiating favorable allocation terms.

The Multiplier Effect of Supply Chain Constraints

Component costs don't exist in isolation. A shortage of specific DRAM or NAND flash variants doesn't just raise unit costs—it creates cascading effects throughout the supply chain. Manufacturers competing for scarce components bid prices upward, encouraging yield optimization investments that increase non-component costs. Longer lead times necessitate larger inventory positions, tying up working capital and creating obsolescence risks.

For a company manufacturing gaming hardware for the first time at scale, these secondary effects prove particularly disruptive. Established console manufacturers have sophisticated supply chain management systems refined over decades of hardware launches. They maintain multiple supplier relationships, have invested in strategic inventory reserves, and have contractual arrangements that protect against extreme price volatility. Valve, by contrast, must navigate these complexities while simultaneously managing the technical challenges of bringing an entirely new product to market.

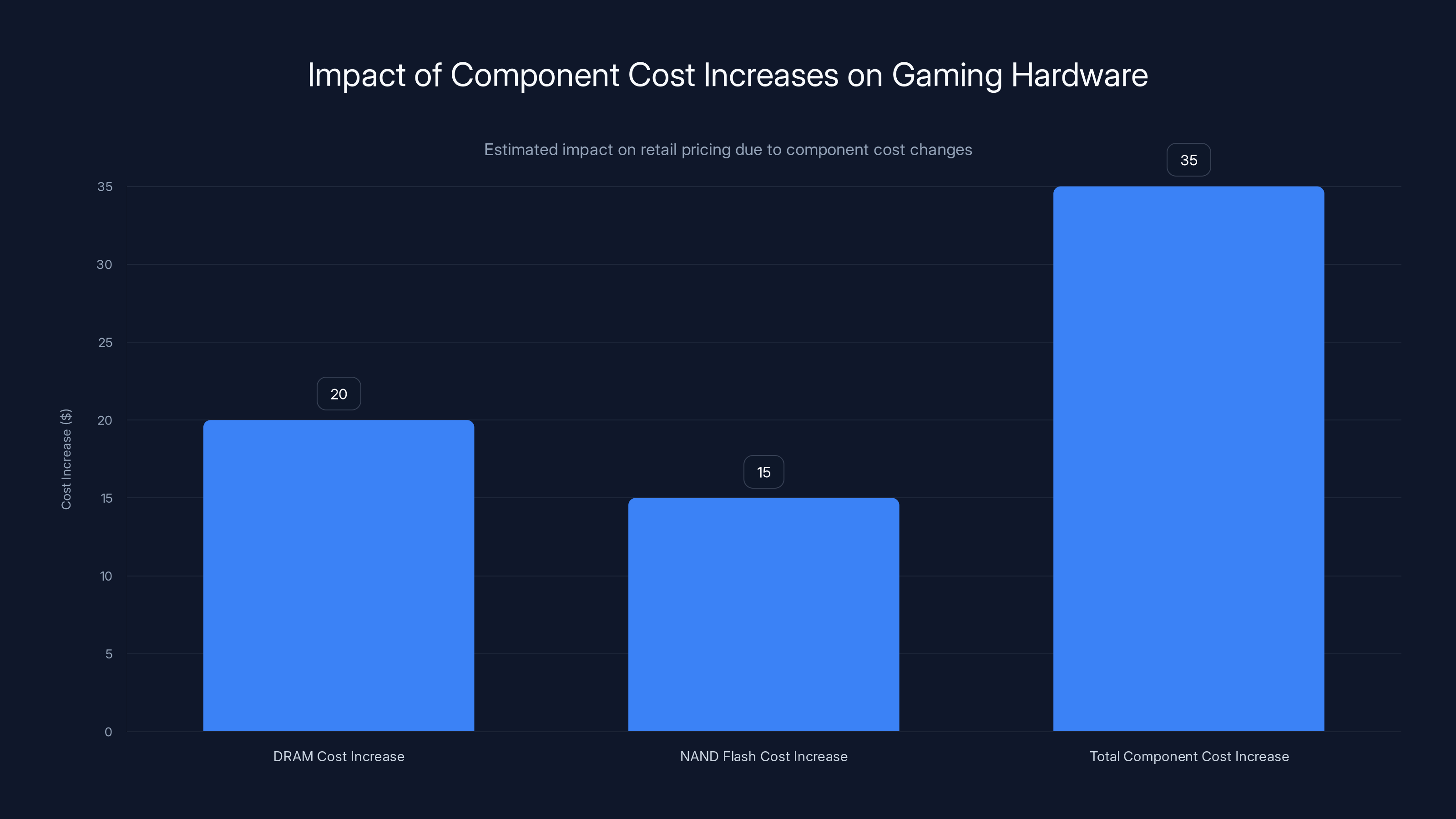

Estimated data shows that a

Analyst Price Projections: From Optimism to Reality

The $599 Baseline and Why It Matters

Wedbush Morgan analyst Michael Pachter initially provided a framework for understanding Steam Machine pricing that centered on a

However, Pachter now describes any price above

The DFC Intelligence Analysis: Approaching Premium Pricing

DFC Intelligence analyst David Cole offered a more pessimistic assessment based on current trajectory. Cole indicated that component prices have "just gotten worse" despite expectations they would moderate. More significantly, Cole's analysis suggested that plausible Steam Machine pricing has "approached

This projection implies a pricing structure looking something like: 512GB at

Cole's assessment reflects the reality that component costs aren't stabilizing—they're likely to remain elevated through at least the next 18-24 months based on current manufacturing trends and demand forecasts. A company hoping for short-term relief is likely to be disappointed.

The Most Pessimistic Scenario: F-Squared Analysis

F-Squared analyst Michael Futter provided what many would consider an outlier perspective, but one grounded in specific technical analysis. Futter projected that the 512GB model could exceed

However, Futter's analysis considered several specific factors: the potential for Valve to absorb fewer component cost increases than other manufacturers due to lack of negotiating power, the possibility that Valve might prioritize profit margins over market penetration, and the scenario where component price pressures extend longer than optimistic forecasts suggest. Additionally, Futter's analysis may reflect a scenario where Valve's initial supply contracts locked in prices at the beginning of the cost escalation cycle, making current pricing reflective of more expensive foundational commitments.

While Futter's projections represent the more pessimistic end of the analyst spectrum, they serve an important function: they establish boundary conditions for thinking about Steam Machine economics. They illustrate that under plausible scenarios, the device could price itself entirely out of the mass consumer market and into a niche enthusiast category with fundamentally different competitive dynamics.

Valve's Structural Disadvantage: Why Large Console Makers Have Pricing Power

Volume Commitments and Supplier Negotiations

The semiconductor and storage component industries operate on principles fundamentally favorable to large-volume purchasers. When Sony manufactures Play Station 5 consoles at a rate of 20+ million units annually, the company negotiates component prices for those volumes. The supplier knows that losing Sony's business means losing a predictable, enormous revenue stream. This creates genuine negotiating leverage.

Valve's situation differs dramatically. Even optimistic projections suggest the company might sell 5 million Steam Machines across the entire product lifecycle. While this represents significant volume, it pales compared to the annual Play Station or Xbox production runs. More problematically, Valve's negotiating position is weaker because the supplier knows that if negotiations fail, Valve has extremely limited alternatives. A component shortage means a delayed or canceled product. For Sony, a single supplier dispute might result in slightly higher costs but production continues. For a new entrant like Valve, supplier conflicts threaten the entire venture.

This structural imbalance appears throughout the component supply chain. DRAM manufacturers have established relationships with Sony, Microsoft, Nintendo, and major PC manufacturers like Dell, HP, and Lenovo. When Valve enters the market with an unfamiliar request, the supplier's first calculation is whether serving this new customer is worth diverting limited capacity from established, high-volume relationships. The answer, economically, is often "no"—unless Valve agrees to premium pricing that compensates the supplier for this opportunity cost.

The Importance of Long-Term Supply Contracts

Analyst James Sanders emphasized a critical but often-overlooked factor: when Valve locked in component supply contracts. Gaming hardware manufacturers typically establish supply agreements 12-18 months before product launch. These contracts specify component volumes, pricing, and delivery schedules. A company that secured DRAM and NAND flash contracts 18 months ago at pre-escalation prices could launch at planned price points despite current market conditions. A company forced to negotiate replacement contracts or adjust orders now faces current market rates.

Large console manufacturers negotiate these agreements with sophistication honed through previous generations. Sony planned Play Station 5 component procurement during the transition from Play Station 4 to PS5, giving executives visibility into component trends. Microsoft brought similar experience from the Xbox One to Xbox Series X transition. Nintendo benefited from component expertise developed across Switch, 3DS, and Wii generations.

Valve, despite the success of the Steam Deck, lacked this embedded institutional knowledge when planning Steam Machine component sourcing. The Steam Deck is a mobile gaming device with different component requirements—it needs lower-power processors, less memory bandwidth, and smaller storage capacities. The expertise doesn't directly transfer to a living room device competing on processing power and graphical fidelity. This meant Valve had to build supply chain competence during a period when the market was working against newcomers.

Strategic Inventory Positioning

Established console manufacturers maintain strategic inventory reserves of key components. These reserves serve multiple purposes: they buffer against supply shocks, provide negotiating leverage when disputes arise, and allow companies to spread purchasing across multiple quarters to reduce exposure to price volatility. Building such reserves requires capital that companies invest expecting long-term returns.

Valve, preparing for what should theoretically be a one-time hardware launch (though the company has since discussed potential future hardware iterations), might not have justified extensive inventory investments. Each component sitting in inventory represents capital that could be deployed elsewhere in Valve's more profitable software business. The incentive structure differs fundamentally from what established hardware manufacturers face.

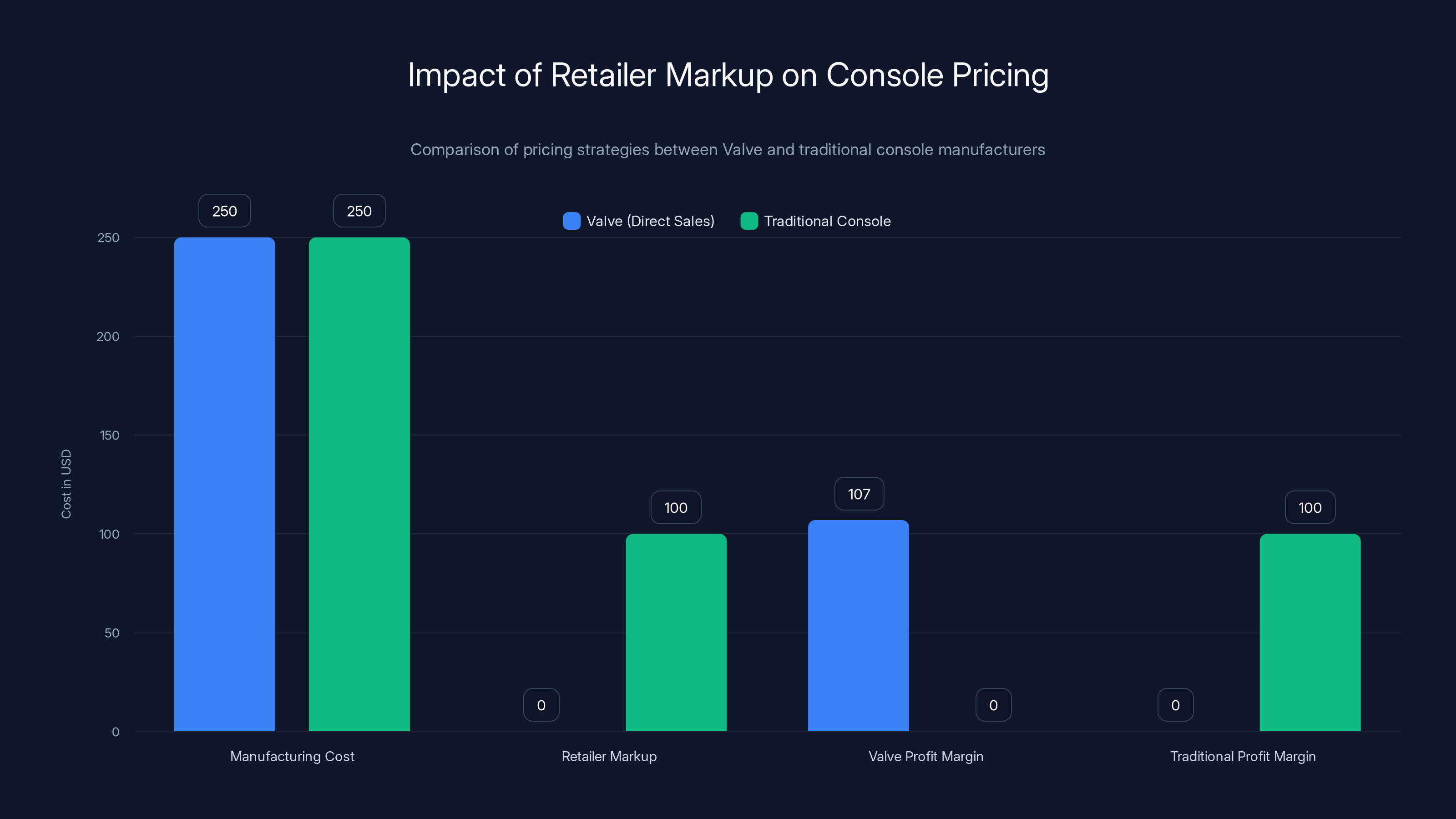

Valve's direct sales model avoids retailer markups, allowing for competitive pricing or higher profit margins. Estimated data based on typical markup and profit margins.

Market Psychology: The Price Sensitivity Threshold in Gaming Hardware

Understanding Console Pricing Elasticity

Gaming hardware pricing exists within specific psychological and competitive windows. Research in consumer electronics indicates that gaming devices operate under different demand dynamics than general computing products. A

The Steam Machine's challenge becomes more complex because it doesn't have a true analog. It's not quite a console (lacks the exclusive game library certainty), not quite a PC (lacks the upgrade flexibility), and not quite a streaming device (requires local hardware). This ambiguous positioning makes price perception particularly important. Consumers lack an established mental model for evaluating value. Without that model, price becomes the primary decision factor.

The $599 Psychological Anchor

Current-generation consoles established

Analyst projections suggesting

Core Audience Price Elasticity

DFC Intelligence analyst David Cole noted that the Steam Machine has "a fairly niche built-in audience that will not be too price sensitive." This observation captures an important nuance: the device's core market—existing PC gamers wanting a living room experience without the complexity of full custom builds—might tolerate $100-150 price increases reasonably well. These are consumers who've already invested in PC gaming, may own multiple gaming devices, and are motivated by convenience and integration rather than absolute minimizing cost.

However, "not too price sensitive" doesn't mean "price insensitive." Even an enthusiast audience has limits. The difference between a

Comparative Cost Structures: Sony, Microsoft, and Valve

Sony's PS5 Economics and Scale Advantages

Sony manufactures Play Station 5 units at staggering scale. In typical years, the company produces and ships 20+ million units annually across all Play Station products, with console production regularly exceeding 5-10 million units per year. This volume provides extraordinary leverage with component suppliers. When Sony commits to purchasing 50 million DRAM modules for a new console generation, suppliers prioritize fulfilling that order because failure to do so means losing a guaranteed, decade-spanning revenue stream.

Moreover, Sony's supply chain operates through layers of established relationships built across previous console generations. The Play Station 4 taught the company lessons about component sourcing, supplier relationships, and inventory management. The PS5 benefited from that institutional knowledge. Sony can credibly threaten to move production of next-generation hardware to different suppliers if current suppliers don't meet pricing or availability requirements. Valve lacks this credible threat.

Sony also distributes hardware costs across multiple product lines. Play Station VR equipment, Play Station Portables, and other devices share component sourcing strategies. A favorable DRAM deal that benefits the PS5 can be optimized across the entire product ecosystem, creating additional negotiating leverage.

Microsoft's Cross-Platform Component Efficiency

Microsoft manufactures gaming hardware across multiple categories: home consoles (Xbox Series X and Series S), handheld devices (anticipated future mobile gaming hardware), and PC components sold through partners. Additionally, Microsoft operates extensive data center infrastructure requiring processors, memory, and storage. The company's negotiations with suppliers span not just gaming, but cloud infrastructure, enterprise computing, and consumer electronics.

When Microsoft's procurement division negotiates with Intel or AMD for processors, they're negotiating billion-unit commitments across gaming, cloud, and consumer products. They're negotiating with DRAM suppliers for memory used in everything from consoles to data centers to computers. This aggregate purchasing power dwarfs what any single-purpose gaming hardware manufacturer can achieve.

Similarly, Microsoft can more easily absorb component price increases because the company can offset gaming hardware margin pressure through software and services revenue. If Xbox hardware margins compress by 5-10%, Microsoft can maintain overall profitability through Xbox Game Pass subscriptions, which continue generating revenue per customer throughout the device's lifecycle. Valve, while having profitable software through Steam, lacks an equivalent services revenue stream tied to Steam Machine adoption.

Valve's Structural Disadvantages and Limited Mitigation Options

Valve's negotiating position is substantially weaker across multiple dimensions. The company is a newcomer to console hardware with no precedent for multi-generational relationships with suppliers. Steam Deck production, while successful, occurred at lower volumes and targeted a different market segment. The company has no track record of meeting supply commitments across hardware generations—suppliers must evaluate Valve as an unknown quantity in hardware reliability and long-term partnership value.

Valve also cannot distribute component costs across multiple product lines or leverage aggregate purchasing power from non-gaming divisions. Unlike Sony's consumer electronics empire or Microsoft's enterprise and cloud operations, Valve's revenue is concentrated in software (Steam) and the Steam Deck. The company has no existing data center business, no enterprise computing division, no consumer electronics heritage. Each component negotiation stands alone.

The direct sales model, while offering some advantages discussed later, also eliminates the negotiating leverage that retailers like Best Buy or Game Stop provide. Those retailers represent additional volume to component suppliers. When Valve sells direct-to-consumer through its website and Steam client, suppliers see Valve's total volume and no more. There's no "channel partner" component that could suggest the Steam Machine might reach different market segments through different distribution mechanisms.

High-End Gaming PCs offer the most customization but at a higher cost, while Cloud Gaming Services provide maximum convenience with no hardware cost. Estimated data.

Potential Pricing Scenarios and Market Implications

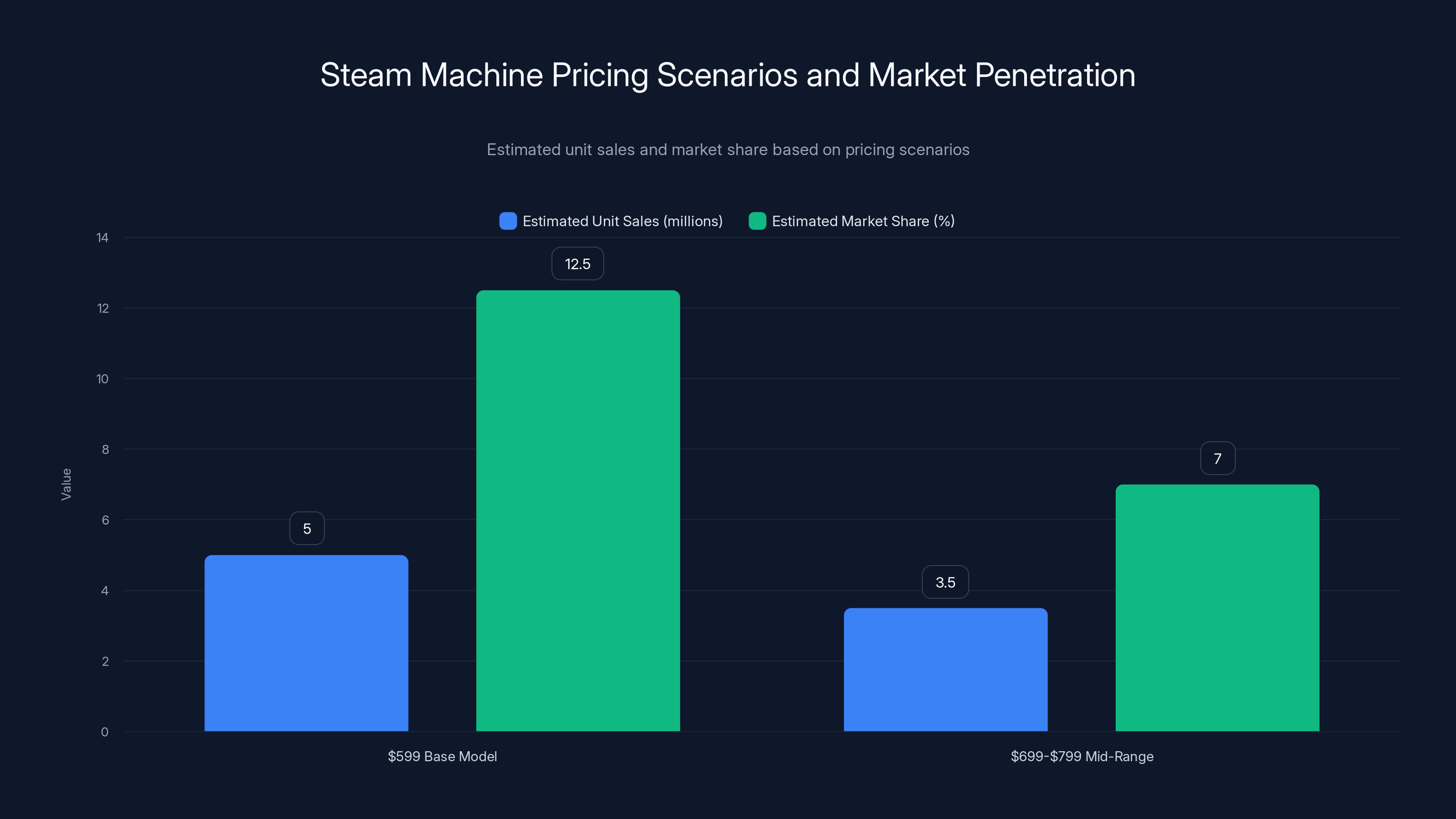

Scenario One: The $599 Base Model Path

If Valve successfully navigates component pricing and launches the Steam Machine at

Market penetration under this scenario would depend heavily on execution in other areas: game availability, user interface design, performance consistency, and marketing effectiveness. Analyst Pachter suggests this scenario might achieve 5 million unit sales across the product's lifecycle—meaningful but not transformative. The device becomes a credible option for perhaps 10-15% of the console gaming market, appealing primarily to existing PC gamers and technology enthusiasts.

This scenario represents Valve absorbing significant component cost increases without passing them fully to consumers. The company would likely operate at lower margins on hardware than it initially planned, betting that volume, brand reputation, and Steam integration would eventually drive profitability. It's the scenario most favorable to consumers and most challenging for Valve's hardware margin structure.

Scenario Two: The 799 Mid-Range Positioning

If component costs force Valve to price the base model at

Market size under this scenario would likely contract to 3-4 million units across the product lifecycle. The core PC gaming audience—perhaps 20-30% of the broader gaming market—would still consider the device, but casual gamers would likely choose cheaper console options. Valve would be betting that the PC gaming market is valuable enough to sustain profitability at lower unit volumes but premium margins.

This scenario presents real business viability but represents a fundamental repositioning from the original vision. Instead of a "console alternative for the living room," the Steam Machine becomes a "premium gaming appliance for the PC enthusiast market." These are different products with different marketing strategies and different audience expectations.

Scenario Three: The $900+ Premium Hardware Category

If component costs force prices above

Market size under this scenario would likely fall to 1-2 million units, with sales concentrated among hardcore enthusiasts. Profitability would depend entirely on healthy hardware margins—the volume simply couldn't sustain a business model based on thin margins and ecosystem profitability. Valve would essentially be operating a niche hardware business rather than attempting to drive mainstream living room gaming adoption.

While this scenario seems least desirable, it's worth noting that profitability at low volume with premium pricing is actually viable in the gaming hardware market. Companies have succeeded with premium controllers, specialized peripherals, and high-end gaming devices by accepting limited market size while maintaining strong margin structure.

Supply Chain Alternatives and Valve's Options

Reducing Component Specifications to Lower Costs

One available path for Valve involves accepting lower-tier specifications to reduce component costs. Gaming hardware always involves specification tradeoffs: more storage, better processor, more memory, better graphics. If Valve accepted some compromises in these areas, component costs would decline, potentially enabling better pricing.

For example, moving the base model from 512GB to 256GB storage would reduce NAND flash costs by roughly

However, this path involves real tradeoffs in perceived value. If the Steam Machine offers inferior specifications to Play Station 5 at a premium price, the value proposition collapses. Consumers would ask: "Why should I pay

Staggered Launch Strategy

Valve could adopt a staggered launch approach, initially bringing a high-end 2TB Steam Machine to market at premium pricing (

This strategy is common in gaming hardware but carries risk. If early adopters encounter issues or provide negative reviews, it becomes harder to attract mainstream buyers later. Conversely, if the high-end launch succeeds, it establishes brand perception and might allow broader market entry later with more credibility and market understanding than an initial premium launch would provide.

Direct Component Manufacturing Investment

Very large technology companies sometimes vertically integrate component manufacturing when suppliers prove unreliable or expensive. Apple, for example, designs custom processors for i Phones and has explored custom memory solutions. However, this path is extremely capital intensive—establishing new semiconductor manufacturing capacity requires billions of dollars and multi-year timelines. It's not a practical option for Valve in the near term.

Strategic Partnerships and Co-Manufacturing

Valve could explore partnerships with established console manufacturers or contract manufacturers. If Sony or Microsoft have excess production capacity and favorable component supply agreements, they could theoretically co-manufacture Steam Machines, allowing Valve to benefit from their supplier relationships. While this seems unlikely given competitive dynamics, it represents a potential path Valve hasn't explicitly ruled out.

Alternatively, Valve could partner with contract manufacturers like Foxconn, Pegatron, or others who have relationships across multiple device manufacturers and might negotiate component discounts through aggregate volume. This is similar to how the Steam Deck is manufactured and represents a potential efficiency gain compared to managing component sourcing entirely in-house.

DRAM prices have shown significant volatility, with recent increases due to supply constraints and heightened demand. Estimated data reflects typical market trends.

Market Timing and the Consumer Expectation Cycle

When Did Consumers Form Expectations?

Valve first announced the Steam Machine in 2013, though the device never shipped as envisioned. The company has discussed potential hardware iterations periodically since then. When Valve announced renewed Steam Machine development plans, it created expectations about pricing, specifications, and availability that are now being tested against component cost reality.

Consumers who have been following the Steam Machine news for months have formed mental price anchors. Industry reporting, analyst commentary, and Valve's own positioning likely created expectations in the

The Competitive Landscape in 2025-2026

The gaming hardware landscape has evolved significantly since the Play Station 5 and Xbox Series X launched at $499 in 2020. New processor architectures from AMD, Nvidia, and Intel offer better performance at equivalent price points. SSD technology has matured, providing faster access at lower cost. The market now has multiple gaming device options: high-end consoles, mid-range devices, cloud gaming services, and high-end gaming PCs.

Into this landscape, the Steam Machine arrives as a newcomer. The device needs to offer genuine value differentiation—not just equivalent specifications at higher pricing. If the device offers meaningful advantages in terms of specifications, game library access, or user experience, it can command a pricing premium. If it offers equivalent specifications at premium pricing, it's difficult to justify consumer adoption.

The good news for Valve is that the company has genuine advantages to offer. Steam's game library contains over 70,000 titles. The flexibility of open-source Steam OS operating system offers advantages over closed console ecosystems. The device can function as both a console replacement and a traditional PC, providing dual-purpose value. If Valve can deliver on these value propositions while containing pricing pressure, the Steam Machine has a credible path to market success despite component cost challenges.

Direct Sales Economics: Where Valve Has Advantages

Eliminating Retailer Markups

Traditional console manufacturers distribute through retailers: Best Buy, Game Stop, Target, Walmart, and international equivalents. These retailers require markups—typically 20-35%—to cover operating costs and provide profit margin. When Sony manufactures a Play Station 5 for

Valve's direct-to-consumer sales model eliminates this intermediary layer. The company sells through its website and the Steam client directly to consumers. This removes the retailer markup from the pricing equation. If the Steam Machine costs

This difference is substantial enough to materially impact competitive pricing. Direct sales could allow Valve to price a device 15-20% lower than competitors with equivalent component costs and margin targets. Alternatively, Valve could maintain equivalent pricing while capturing higher margins than traditional manufacturers. Both approaches create strategic options for navigating component cost pressures.

Reduced Logistics and Fulfillment Costs

Direct sales also enable optimization of logistics and fulfillment infrastructure. Rather than shipping devices to thousands of retail locations across multiple distribution channels, Valve coordinates shipment from manufacturing partners directly to customers. This consolidation reduces the number of shipment touches, warehousing locations, and supply chain intermediaries.

Additionally, Valve has invested extensively in logistics optimization for Steam Deck fulfillment. The company has developed processes and relationships with fulfillment partners that can theoretically be scaled for Steam Machine distribution. This existing infrastructure provides a cost advantage over companies building direct sales capabilities from scratch.

Customer Data and Personalization Opportunities

Direct sales provides Valve with direct customer relationships and purchasing data. The company can track which customers purchased Steam Machines, what peripherals they purchased, what games they played, how they used the device. This data enables sophisticated personalization, targeted marketing, and customer retention strategies unavailable to manufacturers selling through traditional retail channels.

For instance, Valve could offer customized game recommendations based on Steam Machine usage patterns, provide targeted sales on complementary products (controllers, headsets, storage upgrades), or develop new features specifically addressing how customers use Steam Machines. This information advantage creates ongoing value beyond the initial hardware sale.

Consumers expect the Steam Machine to be priced between

The Broader Implications: What Steam Machine Pricing Reveals About Hardware Economics

Centralization of Hardware Manufacturing Power

The Steam Machine pricing crisis illustrates a deeper trend in technology hardware: the increasing centralization of manufacturing power among large, established companies. Companies like Apple, Sony, Microsoft, and Samsung have invested decades in supply chain expertise, component sourcing relationships, and manufacturing infrastructure. These advantages compound over time, making it increasingly difficult for newcomers to achieve cost parity.

When a company like Valve, despite significant software industry resources, struggles to achieve favorable component pricing, it reveals the depth of the structural advantage large hardware manufacturers possess. This trend suggests that future gaming hardware categories may increasingly be dominated by a small number of major players rather than enabling new entrants to succeed.

For consumers, this centralization could reduce innovation and increase pricing power for established manufacturers. For industry newcomers with compelling visions—like Valve's Steam Machine—the path to success requires either competing on differentiation substantial enough to overcome cost disadvantages, accepting smaller market share at premium pricing, or finding ways to disrupt the supply chain itself.

The Role of Software in Hardware Competitiveness

Valve's primary advantage in navigating the Steam Machine pricing crisis is software. The company's deep integration with Steam, the massive game library, and the ability to optimize the operating system specifically for hardware represent competitive advantages that don't depend on supply chain favorability. A Steam Machine running Steam OS can offer experiences unavailable on Play Station 5 or Xbox Series X precisely because Valve controls both the hardware and the primary software ecosystem.

This dynamic suggests that future hardware competitiveness will increasingly depend on software advantages. Companies competing primarily on hardware specifications and manufacturing efficiency will face structural headwinds competing against companies that also control the software and services ecosystem. Valve's path to Steam Machine success requires emphasizing these software advantages to justify any pricing premium required by component costs.

The Fragility of Hardware-First Strategies

The Steam Machine situation also illuminates risks in hardware-first business strategies. Valve is ultimately a software company. The company's profits, engineering talent, and strategic resources come from Steam and PC gaming software. The Steam Machine represents a hardware bet—an attempt to extend Valve's software dominance into the hardware category.

When component costs threaten hardware viability, the company faces a strategic choice: accept lower margins and push hardware through, or accept higher pricing and risk market failure. Neither option is ideal. This fragility suggests that companies should view hardware carefully as a means to software and services dominance, rather than as an end in itself. Valve's success with Steam Deck, which benefits from the software advantages of Steam integration, may prove more sustainable than a more independent hardware play.

Expert Perspectives on Navigating the Pricing Crisis

The Case for Strategic Patience

Some industry observers suggest Valve should accept component cost pressures patiently, recognizing that pricing will eventually moderate as manufacturing capacity expands. This perspective notes that peak component prices are likely temporary—within 18-24 months, DRAM and NAND flash production capacity should increase, driving costs down. A company willing to absorb margin pressure initially could reposition pricing downward over time, capturing market share from competitors unwilling to invest in early losses.

This strategy requires confidence in long-term demand and acceptance of near-term margin pressure. It's workable for a profitable company like Valve but is incompatible with venture capital business models that expect near-term profitability. It also requires a multi-generational hardware commitment—if Steam Machine is a one-off product, strategic patience doesn't make business sense.

The Case for Niche Positioning

Alternatively, some analysts suggest Valve should embrace the premium positioning that component costs force. Rather than competing with consoles at console price points, Valve positions the Steam Machine as a premium gaming appliance for the PC enthusiast market. This repositioning acknowledges reality rather than fighting against it.

Under this approach, Valve accepts that the Steam Machine won't achieve 10+ million unit sales. Instead, the device targets 2-3 million dedicated PC gamers willing to pay premium prices for a device optimized specifically for their use case. Margins would be healthier, allowing continued hardware development. The marketing shifts from "alternative to consoles" to "ultimate PC gaming appliance." This positioning is honest about the market and potentially sustainable despite component costs.

The Case for Specification Compromise

A third perspective suggests Valve should negotiate component costs downward through specification compromises. By accepting slightly reduced storage, memory, or processing capability, the company could achieve pricing closer to its original targets. This requires confidence that specifications remain sufficient to satisfy customer expectations and deliver strong gaming performance.

The challenge here is that specification compromise can damage market positioning. If the Steam Machine offers 8GB of memory where competitors offer 16GB, or 256GB storage where competitors offer 512GB, consumers perceive the device as inferior even if the performance difference is minimal. Specification numbers drive market perception as much as actual user experience.

The Competitive Response: How Consoles Navigate Similar Pressures

Sony's Play Station 5 Pro Strategy

Sony responded to component costs and market dynamics by introducing the Play Station 5 Pro—a higher-specification console positioned at premium pricing (

This two-tier strategy avoids the binary choice between accepting margin pressure or implementing system-wide price increases. Instead, Sony offers choice: consumers budget-conscious enough to value the $500 base model choose that option; consumers willing to invest more in specifications choose the Pro. Both products coexist without directly cannibalizing each other.

Valve could adopt a similar two-tier approach with the Steam Machine. Offering a base model at

Microsoft's Approach: Pricing Flexibility Across Tiers

Microsoft has historically offered multiple Xbox tiers—base S model and high-end X model—at different price points. This strategy provides pricing flexibility and allows consumers to self-segment based on budget and specification requirements. Both products are in market simultaneously, not sequentially.

For the Steam Machine, a similar approach—offering both

The Role of Component Cost Trends: Future Outlook

DRAM Price Trajectory

DRAM pricing is notoriously cyclical, with prices reflecting fundamental supply-demand dynamics. Current price elevation reflects both strong demand (driven by AI infrastructure buildouts, data center expansion, and consumer electronics demand) and constrained supply (manufacturers maintaining deliberate capacity discipline to avoid oversupply cycles).

Industry forecasts suggest DRAM prices will likely remain elevated through 2025, potentially moderating slightly in 2026 as additional manufacturing capacity comes online. However, expectations of moderation are often disappointed by unexpectedly strong demand or capacity constraints. A realistic expectation is that DRAM pricing remains 20-30% above historical levels through at least the first half of 2026.

For the Steam Machine, this means component costs locked in today will likely remain the baseline for the next 18+ months. There's limited near-term relief available through waiting for prices to drop.

NAND Flash Price Trends

NAND flash pricing follows different cycles than DRAM, driven by specific architectural transitions and manufacturing process improvements. Current NAND flash pricing benefits from competitive market dynamics—multiple manufacturers (Samsung, SK Hynix, Kioxia, Micron) maintain strong capacity and competition keeps pricing moderate.

However, recent consolidation in the NAND industry (fewer major players than existed five years ago) has reduced competitive pressure. Some analysts suggest NAND pricing could actually increase if current market conditions persist or consolidation continues. This suggests less relief available from waiting on NAND flash costs compared to DRAM.

Processor and GPU Pricing

Processor and GPU costs involve partially different economics. Competition between AMD, Intel, and Nvidia, along with custom ARM designs from Apple and others, creates competitive pressure that moderates pricing. However, leading-edge process nodes remain expensive to manufacture, so high-performance processors command premium prices.

For the Steam Machine, the primary choice is between using current-generation AMD RDNA 2 architecture (mature, increasingly affordable) or waiting for next-generation RDNA 3 or newer architecture (more expensive but offering better performance-per-watt). Current indications suggest the Steam Machine uses RDNA 2 architecture, which should see modest price declines over the next 12-18 months but likely remains expensive in absolute terms.

Business Model Implications: Profitability and Long-Term Sustainability

Hardware Margin Targets in the Gaming Industry

Gaming hardware manufacturers typically target hardware gross margins of 15-25%, depending on product positioning and business model. Premium products like the Play Station 5 Pro target higher margins (25-35%) while mainstream products target lower margins (10-20%). Companies offset thin hardware margins through software, services, and ecosystem monetization.

If component costs force the Steam Machine to price significantly higher than planned, hardware margins might actually improve despite lower volumes. A

However, ecosystem monetization becomes more challenging at lower volumes. If the Steam Machine sells 2-3 million units instead of the optimistic 5+ million projections, the platform represents a smaller ecosystem for software partners and Valve itself. Lower volume makes software optimization more difficult and reduces the installed base that third-party developers want to optimize for.

Cross-Subsidization and Platform Strategy

Valve's strategy likely involves cross-subsidization: using hardware as a platform to drive Steam ecosystem engagement, game sales, and services adoption. If hardware volume is constrained by pricing, this strategy becomes less effective. The Steam Machine becomes less valuable as a platform if it only reaches 2-3 million dedicated enthusiasts rather than 5+ million mainstream consumers.

In this scenario, the Steam Machine's primary value becomes serving existing PC gamers rather than expanding the PC gaming market. The device deepens engagement with people already committed to Steam, rather than converting console gamers to the PC ecosystem.

Marketing and Positioning Strategies for a Premium Priced Product

Emphasizing Software Advantages

If the Steam Machine must price above direct console competition, marketing must emphasize advantages that justify the premium. These include access to Steam's 70,000+ game library versus the 300-500 new exclusive titles per generation on consoles, the flexibility of PC gaming architecture, the ability to run non-gaming software, and integration with existing Steam libraries for customers who have invested in Steam game purchases.

These advantages are real and meaningful for PC-focused consumers. The challenge is communicating them effectively to mainstream audiences who may not understand technical distinctions between PC gaming and console gaming.

Positioning the Device as an Appliance, Not a Computer

Marketingshould position the Steam Machine as an appliance—a device you turn on and play games, not a computer you need to maintain. This positioning reduces the perception of technical complexity and justifies premium pricing by emphasizing convenience. The message becomes: "Why buy a $1,500 gaming PC and deal with setup, updates, and troubleshooting when you can buy this optimized gaming appliance?"

This positioning acknowledges that the device is premium-priced but frames the premium as paying for convenience and optimization. It's similar to how Apple markets Macbooks as premium-priced compared to Windows PCs.

Leveraging Early Adopter Enthusiasm

The core Steam Machine audience consists of early adopters enthusiastic about new gaming hardware. These consumers influence broader market perception through reviews, social media discussions, and recommendations. Strong execution and positive early reviews can create word-of-mouth momentum that sells the device despite premium pricing.

Conversely, early problems or negative reviews would be damaging. Premium-priced products held to higher quality standards, and any perception that consumers are overpaying generates significant negative momentum.

Scenarios for Long-Term Hardware Strategy

Scenario A: Premium Gaming Appliance

Valve positions the Steam Machine as a premium option for PC enthusiasts, accepts lower volumes (2-3 million), and uses the device as a flagship for Steam OS and PC gaming in the living room. Over time, successful Steam OS implementations on lower-cost devices (potentially through partnerships with third-party manufacturers) expand the reach without Valve bearing all the manufacturing challenges. The Steam Machine becomes a reference design—proof that Steam OS delivers excellent gaming experiences.

This strategy requires patience and acceptance that the Steam Machine itself may never be a blockbuster seller. But it could seed a broader ecosystem of Steam OS-based devices from multiple manufacturers, similar to how Android operates.

Scenario B: Revised Timeline and Specifications

Valve delays the Steam Machine launch by 12-18 months, allowing component costs to moderate and manufacturing capacity to increase. The company uses additional development time to refine Steam OS, improve optimization, and incorporate customer feedback. When the device finally launches at higher specifications and lower component costs, it might hit original pricing targets while offering better specifications than initially planned.

This strategy trades timing risk for cost and specification advantages. The danger is that additional delays further erode consumer interest and give competitors additional time to innovate.

Scenario C: Ecosystem Expansion Through Partnerships

Valve licenses Steam OS and Steam Machine designs to third-party manufacturers (similar to how Android operates). These manufacturers build their own variants, competing on price, specifications, and design. Valve monetizes through OS licensing and Steam ecosystem software sales rather than hardware margins.

This strategy addresses Valve's structural disadvantage in manufacturing scale by leveraging others' manufacturing capability. However, it requires Valve to accept less control over the product and to compete with multiple Steam OS-based devices from other manufacturers.

Conclusion: Navigating Structural Challenges and Market Realities

The Core Challenge: Structure vs. Ambition

The Steam Machine pricing crisis crystallizes a fundamental challenge in technology business: structural advantages matter enormously. Valve's software capabilities and Steam ecosystem represent genuine advantages in gaming—advantages that should enable hardware success. Yet structural disadvantages in manufacturing, supply chain negotiation, and component sourcing create friction that no amount of software excellence fully overcomes.

This tension between software advantage and hardware disadvantage isn't unique to Valve. Many software-first companies have attempted hardware ventures with mixed results. Success requires acknowledging structural realities while leveraging software advantages to overcome them. The Steam Machine faces that exact challenge: Can Valve's software and ecosystem advantages justify a pricing premium required by structural hardware disadvantages?

Pricing as a Strategic Statement

Fundamentally, the Steam Machine's pricing decision communicates strategic intent. A

Each positioning is viable from a business perspective, but they communicate different strategic ambitions. Valve's actual pricing choice, when announced, will clarify whether the company is attempting to displace consoles in the living room or to serve the existing PC gaming audience more effectively.

What Steam Machine Pricing Reveals About Industry Consolidation

The difficulty Valve faces in achieving attractive Steam Machine pricing despite significant resources suggests that hardware manufacturing power has become increasingly concentrated. The ability to negotiate favorable component pricing, secure manufacturing capacity, and navigate complex supply chains represents an enormous advantage that few companies possess. This consolidation favors established hardware manufacturers and creates barriers for new entrants.

For the broader gaming industry, this has implications. If new hardware platforms can only be launched by companies with pre-existing hardware expertise and manufacturing relationships, innovation may be constrained to improvements within existing categories rather than fundamentally new approaches. This isn't necessarily bad—established players can innovate effectively—but it does raise questions about how novel gaming platforms emerge.

The Real Outcome Scenarios

Realistic assessments suggest the Steam Machine will likely fall into one of three categories:

Success Case: Valve launches at

Moderate Case: Valve launches at

Challenged Case: Valve struggles to achieve satisfactory pricing and either delays the launch indefinitely or releases a device at $1,000+ that fails to gain meaningful market traction. Component cost challenges, combined with execution issues or market skepticism, prevent the Steam Machine from achieving critical mass. The project becomes a learning experience rather than a business success.

A Broader Perspective on Gaming Hardware Economics

The Steam Machine situation is ultimately about constraints. Every product faces constraints—cost constraints, technical constraints, market constraints. Hardware especially reveals these constraints because manufactured goods have immutable cost structures. You cannot engineer away the cost of memory and storage. You can only decide whether to absorb the costs yourself or pass them to consumers.

Valve's challenge is deciding which constraints to accept and which to fight. Fighting all constraints simultaneously isn't viable. Accepting all constraints means potentially launching an uncompetitive product. Strategic choices involve picking which constraints to accommodate and which to navigate creatively.

The component cost crisis doesn't make the Steam Machine unviable. It makes success more difficult and requires clearer value differentiation or acceptance of smaller market scale. Both are manageable for a company like Valve. The real question isn't whether the Steam Machine can succeed at any price point, but rather what price point allows both viable business returns and meaningful market impact. That's the decision Valve faces, and pricing alone won't determine the outcome—execution, software quality, and marketing will matter just as much.

FAQ

What caused the Steam Machine pricing pressure?

Component costs for critical hardware elements—particularly DRAM and NAND flash storage—have increased significantly due to supply constraints and strong demand across consumer electronics and data center markets. These component costs represent 40-50% of the total manufacturing expense for gaming hardware, making price increases directly impact retail pricing. Manufacturing companies like Valve that lack the negotiating power of established console makers face particular difficulty absorbing these increased costs.

How do component costs affect gaming hardware pricing?

Component costs flow directly through to consumer pricing. When DRAM costs increase from

Why does Valve struggle with component pricing compared to Sony or Microsoft?

Large manufacturers like Sony and Microsoft negotiate component pricing for tens of millions of annual units across multiple product lines. This volume creates leverage with component suppliers who prioritize maintaining relationships with guaranteed, massive-volume customers. Valve, as a newcomer to hardware manufacturing with limited aggregate purchasing volume, cannot credibly threaten to move to alternative suppliers. Component suppliers have less incentive to offer favorable pricing to Valve compared to Sony or Microsoft, forcing the company to accept less favorable terms.

What pricing would make the Steam Machine uncompetitive?

Industry analysts suggest

How might Valve address component cost challenges?

Potential responses include: launching at premium pricing and accepting lower volume, reducing device specifications to lower component costs, delaying the launch to allow component prices to moderate, licensing Steam OS to other manufacturers to leverage their supply chain advantage, and partnering with contract manufacturers experienced in negotiating component pricing. Each approach involves tradeoffs between speed to market, pricing competitiveness, and device specifications.

What advantages does Valve have in competing despite higher component costs?

Valve controls the Steam ecosystem, which provides genuine value differentiation through a library of 70,000+ games optimized for Steam integration. The company can sell directly to consumers, eliminating retailer markups that traditional console manufacturers must accommodate. Direct sales also enable Valve to gather customer data and implement sophisticated personalization. Finally, Steam OS provides a flexible, open operating system competing against locked console ecosystems—a meaningful advantage for certain customer segments.

Would a higher Steam Machine price make it unviable?

Not necessarily. While higher prices reduce potential market size, they can improve per-unit profitability and potentially align the product with customer expectations for premium performance devices. A smaller market of paying customers—say 2-3 million units instead of 5+ million—can still generate healthy business returns if managed correctly. The key is matching pricing to customer expectations and market positioning rather than treating price as the sole competitive factor.

How do console pricing increases affect Steam Machine positioning?

Recent Play Station 5 Pro pricing at

What percentage of gaming hardware costs come from components?

For devices like the Steam Machine, component costs (processor, GPU, memory, storage, power supply, thermal management) typically represent 40-55% of total manufacturing expenses, with the remainder including labor, packaging, logistics, and manufacturer margin. This means that 15-20% increases in component costs translate directly to 6-11% increases in total manufacturing costs, requiring either margin reduction or retail price increases of similar magnitude to maintain profitability.

How might the Steam Machine pricing decision affect future Valve hardware?

The Steam Machine establishes precedent for Valve's hardware strategy going forward. If Valve succeeds with premium pricing and smaller market volume, future devices might follow the same model. If the company pursues mainstream pricing despite margin pressure, future hardware investments would follow that pattern. The pricing decision essentially commits Valve to a particular positioning in the hardware market—whether as a premium provider serving enthusiasts or as a mainstream provider competing directly with established console makers.

Competitive Alternatives and Other Solutions

While the Steam Machine represents Valve's entry into dedicated gaming appliances, other solutions offer similar or complementary approaches for consumers interested in PC gaming in the living room.

High-End Gaming PCs: Custom-built systems costing

Pre-Built Gaming Systems: Companies like ASUS, Corsair, and others offer pre-built gaming PCs optimized for living room use, typically priced

Cloud Gaming Services: Microsoft Game Pass for Cloud, Play Station Plus Premium with cloud features, and other services allow console-quality gaming through internet streaming, eliminating local hardware constraints for players with high-speed connections.

Existing Consoles: Play Station 5, Xbox Series X, and Nintendo Switch remain proven alternatives with mature software ecosystems, exclusive game libraries, and established consumer confidence. Price increases on these platforms create some competitive positioning room for alternatives.

For teams and organizations evaluating automation and productivity solutions alongside gaming hardware investments, platforms like Runable offer AI-powered automation capabilities at competitive pricing ($9/month for core features), enabling teams to build automated workflows and generate AI-assisted content. While not directly competitive with gaming hardware, Runable complements hardware productivity through intelligent automation—relevant for content creators and developers interested in streamlining workflows alongside gaming experiences.

The Steam Machine ultimately competes less directly with these alternatives and more against the broader question: How much should consumers invest in gaming hardware given their budget constraints, preferred game library, and technical tolerance? The device's success depends not on becoming the objectively best option, but on offering sufficient value at the right price point for its target audience.

KEY TAKEAWAYS

- Component costs (particularly DRAM and NAND flash) have increased 15-25%, forcing significant pricing adjustments for gaming hardware manufacturers like Valve

- Analyst projections range from 900+ for premium enthusiast positioning, with each scenario implying different market volume and strategic intent

- Valve faces structural disadvantages in component sourcing compared to Sony and Microsoft due to lower purchasing volume and lack of established supplier relationships

- Direct-to-consumer sales eliminate retailer markups, providing potential 15-20% pricing advantage compared to traditional console distribution but requiring investment in fulfillment infrastructure

- Software advantages through Steam integration, the massive game library, and open Steam OS architecture provide competitive differentiation that can partially offset hardware cost disadvantages

- Market segmentation suggests a "core audience" of PC gamers may accept premium pricing while mainstream console buyers require competitive pricing—forcing Valve to choose between broad market appeal and profitability

- Long-term sustainability requires either achieving volume sufficient to improve component sourcing leverage, licensing Steam OS to partners with better manufacturing advantage, or accepting niche positioning as a premium gaming appliance

- Component costs will likely remain elevated through 2025 with modest moderation possible in 2026, limiting near-term relief through waiting for prices to drop

- Gaming hardware pricing reflects broader industry consolidation trends that advantage established manufacturers with decades of supply chain expertise and manufacturing relationships

- Strategic positioning through pricing communicates whether Valve intends mainstream console market disruption or serving existing PC gamers more effectively—a choice with different implications for long-term hardware strategy

Key Takeaways

- Component costs (DRAM, NAND flash) increased 15-25%, forcing significant pricing adjustments for gaming hardware

- Analyst projections range from 900+ (premium enthusiast positioning)

- Valve lacks supply chain leverage compared to Sony and Microsoft due to lower purchasing volume

- Direct-to-consumer sales provide 15-20% pricing advantage over traditional retail distribution

- Steam ecosystem and open SteamOS offer competitive differentiation partially offsetting hardware cost disadvantages

- Market segmentation suggests different strategies needed for core PC gamers versus mainstream console buyers

- Component costs likely remain elevated through 2025 with only modest moderation expected in 2026

- Hardware pricing reflects broader industry consolidation favoring established manufacturers with decades of expertise

- Strategic pricing choice determines whether Valve pursues mainstream disruption or niche premium positioning

- Success requires matching pricing to market positioning rather than treating price as sole competitive factor

Related Articles

- Steam Machine Delayed: RAM Crisis & Price Shock [2025]

- Best Xbox Controllers 2026: Complete Buyer's Guide & Comparisons

- Chinese EV Imports to Canada & US: Trade Deal Analysis 2025

- Nvidia's AI Upscaling Revolution: How PC Gaming is Fundamentally Changing [2025]

- Steam Machine Pricing Leak: What $950 Really Means for Gaming [2025]

- Lenovo Legion Go 2 SteamOS: Everything You Need to Know [2025]