The North American EV Trade Landscape Is Shifting: Understanding Canada's Historic Deal with China

The automotive industry in North America has operated under relatively predictable assumptions for decades. Tariff walls have protected domestic manufacturers, supply chains have remained largely regional, and the competitive hierarchy among automakers seemed fairly established. That landscape changed fundamentally when Canada announced a groundbreaking trade agreement with China to dramatically reduce tariffs on electric vehicle imports. This wasn't a minor adjustment to existing trade policy—it represented a significant pivot in how North America approaches one of the world's fastest-growing automotive segments.

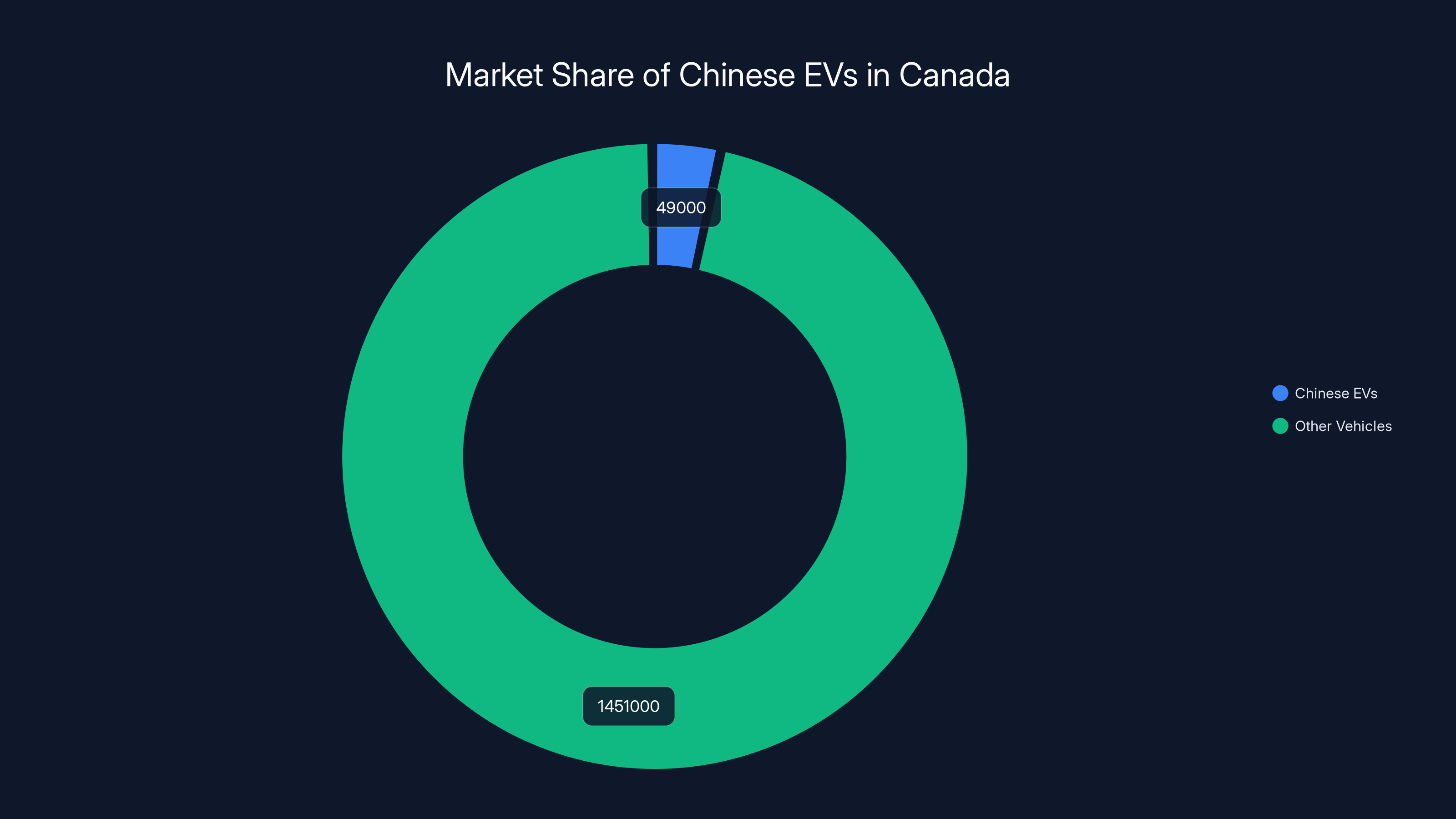

Prime Minister Mark Carney's announcement signaled that Canada would initially allow up to 49,000 Chinese electric vehicles into the country at a reduced 6.1 percent tariff rate, a substantial decrease from previous import duties. The exact timeline for implementation remains somewhat nebulous, but the direction is unmistakable. This development carries profound implications that extend far beyond Canada's borders, raising critical questions about whether the United States might follow suit and what the consequences would be for established automakers, emerging EV manufacturers, and consumers across North America.

The timing of this announcement is particularly significant given the broader geopolitical and economic context. President Trump has simultaneously signaled openness to Chinese automakers establishing manufacturing operations within the United States, provided they build factories domestically and employ American workers. This apparent contradiction—supporting tariff barriers while expressing willingness to allow Chinese competition—reveals the complex calculations occurring within the Trump administration regarding trade policy, domestic manufacturing, and economic competitiveness.

To understand the full implications of these developments, we need to examine multiple dimensions: the technical capabilities and cost advantages of Chinese EV manufacturers, the specific policy mechanisms being deployed, the competitive threat to established American and Canadian automakers, the consumer implications of potentially accessing dramatically cheaper vehicles, and the broader question of whether current tariff structures can withstand the pressure from a genuinely superior low-cost competitor. This analysis explores each of these dimensions in detail.

Understanding China's Dominant Position in Global EV Manufacturing

Why China Has Become the World's EV Powerhouse

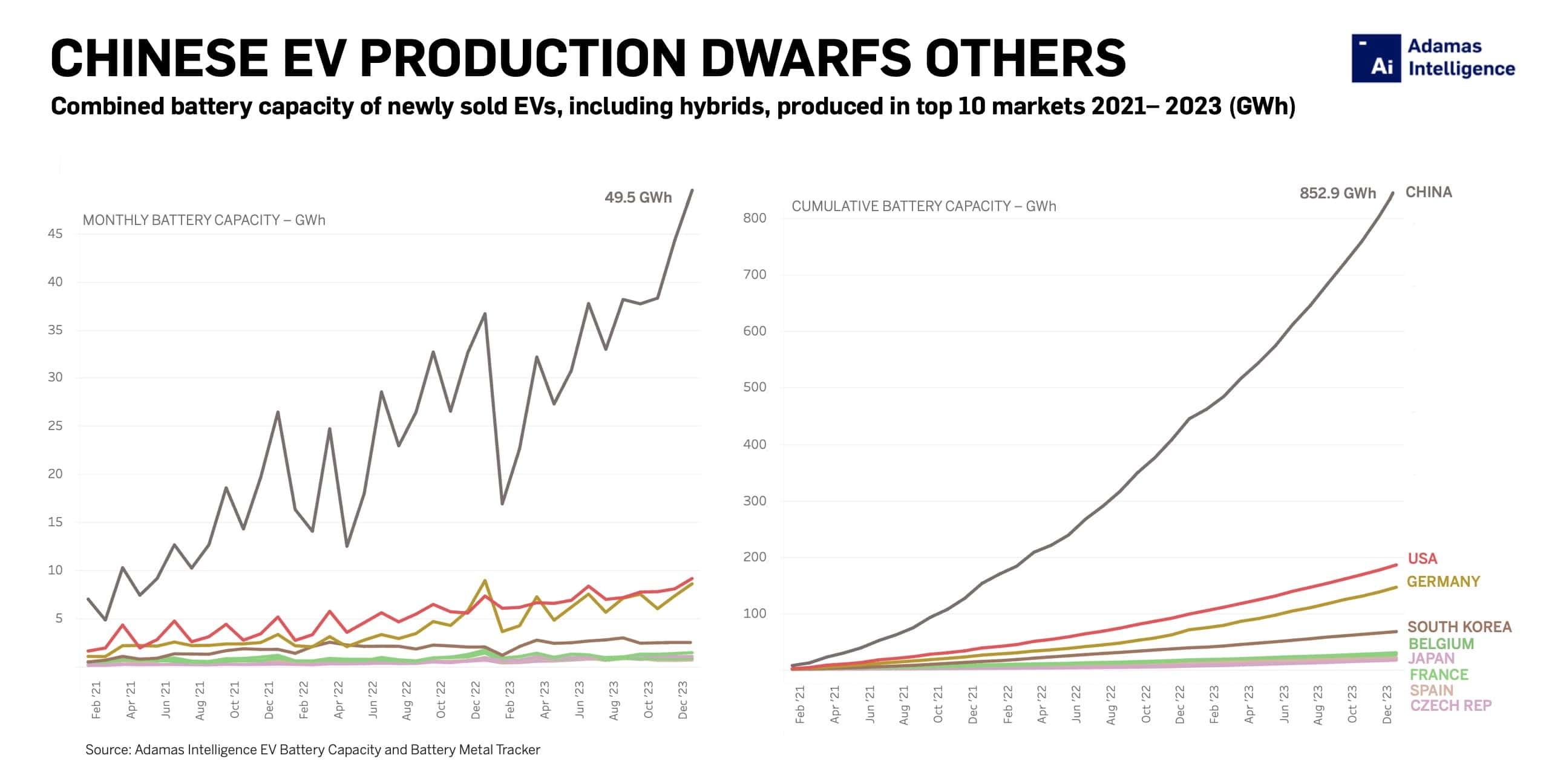

China's ascendancy in electric vehicle manufacturing didn't occur by accident—it resulted from systematic government investment, coordinated industrial policy, and a ruthlessly efficient domestic market that forced continuous innovation and cost reduction. The Chinese government recognized early that battery technology and electric propulsion would define the automotive future. Rather than allowing incumbent automakers to dictate the transition timeline, Chinese policymakers actively promoted the development of new manufacturers and aggressively subsidized both production and consumer adoption.

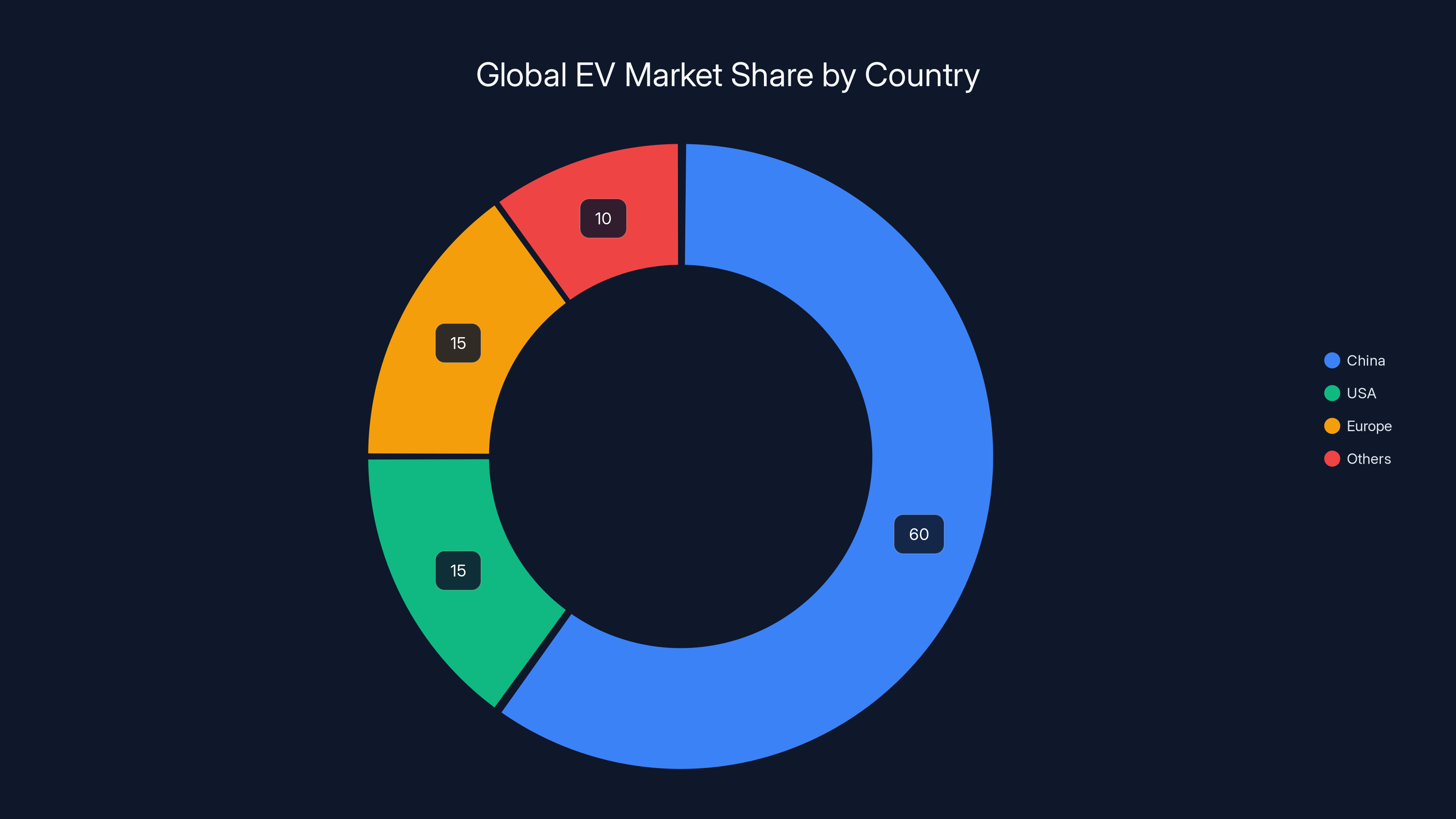

The results have been staggering. China currently manufactures more electric vehicles than every other nation combined. Chinese brands control roughly 60 percent of global EV market share, with companies like BYD, Li Auto, XPeng, NIO, and others achieving scale that their American and European counterparts only dream about. These manufacturers aren't merely assembling vehicles—they're developing sophisticated battery technologies, autonomous driving capabilities, and integrated software systems that in many cases exceed what's available in Western vehicles.

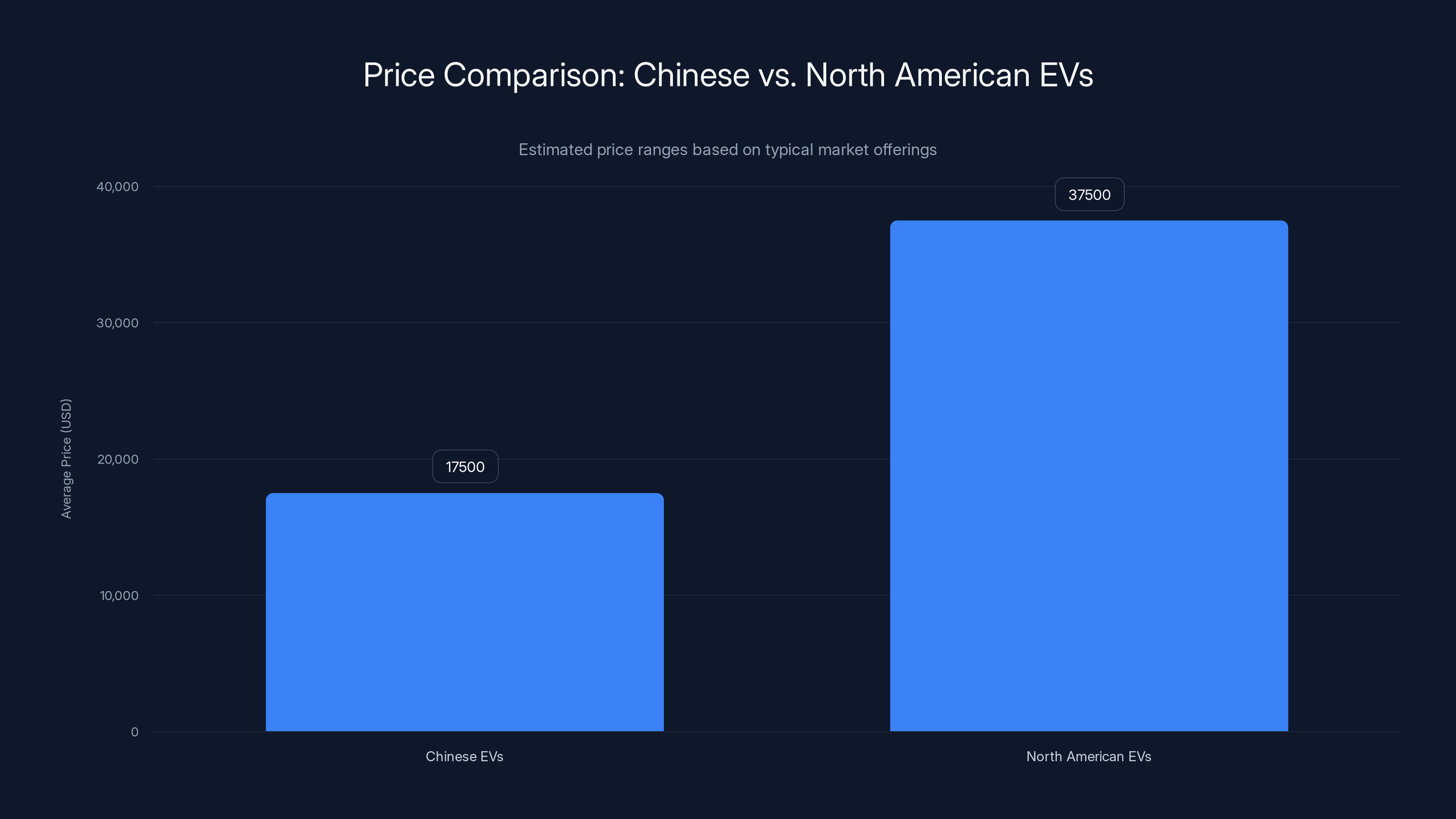

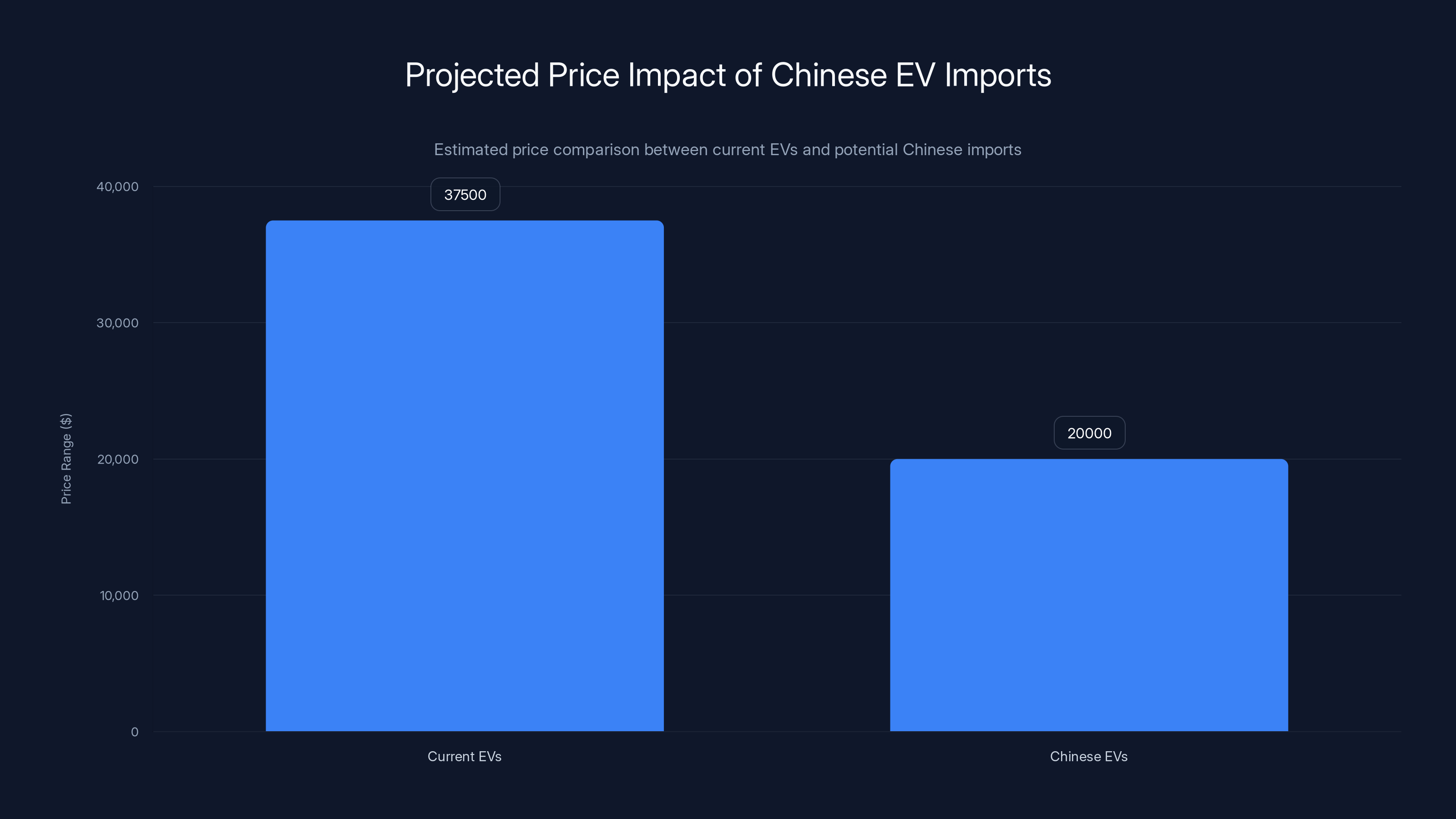

What makes Chinese EV dominance particularly significant is the cost structure these manufacturers have achieved. A Chinese EV that retails for

The Brutal Domestic Price War Driving Global Expansion

China's domestic EV market has become genuinely oversaturated. Manufacturers expanded production capacity aggressively, betting on continued rapid growth. When market growth plateaued in 2023 and 2024, Chinese automakers faced massive inventory backlogs and insufficient domestic demand to absorb production. This created intense pressure to export vehicles and seek international markets to maintain capacity utilization and revenue.

The resulting price war within China's domestic market has been fierce, with manufacturers cutting prices repeatedly to maintain market share. BYD, historically known for serving mid-market customers, has aggressively expanded downmarket with ultra-low-priced vehicles that deliver surprising quality and capability. Li Auto, originally positioned as a premium brand, has launched sub-$10,000 vehicles to compete with mass-market alternatives. This competitive intensity has forced continuous innovation while simultaneously driving down profitability per unit.

Exporting vehicles represents the logical response to this overcapacity situation. Mexican markets have already absorbed significant numbers of Chinese vehicles from brands like BYD, Chery, and Neta. Other developing nations have similarly opened their doors to Chinese imports. Now Canada's tariff reduction opens another substantial market, and the United States represents an even larger prize—if political obstacles can be overcome.

Battery Technology and Supply Chain Advantages

China's dominance in EV manufacturing extends deeply into battery technology and supply chains. Chinese manufacturers have invested heavily in lithium, cobalt, and rare earth element processing, giving them unprecedented control over raw materials and component costs. Companies like CATL and BYD have developed advanced battery chemistries, manufacturing processes, and quality control systems that provide genuine competitive advantages.

This vertical integration—where manufacturers control or have preferential access to battery supply, raw materials processing, and component manufacturing—creates cost structures that Western manufacturers cannot easily replicate. When Tesla builds vehicles in Shanghai, it achieves production costs per unit that are substantially lower than equivalent vehicles built in Germany or the United States, primarily because of supply chain advantages and manufacturing efficiency rather than simply lower labor costs.

The battery technology gap has also narrowed significantly. Chinese manufacturers now produce lithium iron phosphate (LFP) batteries that deliver comparable performance to more expensive NCM (nickel-cobalt-manganese) chemistries used in many Western vehicles, but at substantially lower cost. These batteries are more stable, less prone to thermal runaway, and increasingly sophisticated in their battery management systems.

China holds an estimated 60% of the global EV market share, significantly outpacing the USA and Europe. Estimated data.

Canada's Trade Agreement: What Changed and Why

The Specific Terms of Canada's Tariff Reduction Deal

Canada's deal with China represents a carefully structured agreement that addresses multiple concerns simultaneously. The arrangement allows up to 49,000 Chinese-made electric vehicles to enter Canada annually at a 6.1 percent tariff rate—dramatically lower than the previous rate that had effectively excluded most Chinese vehicles from the Canadian market. In exchange, China agreed to lower tariffs on Canadian agricultural products, particularly canola, which represents a significant export for Canadian farmers.

This structure reveals something important about modern trade negotiations: they're rarely about a single product category. Canada's agricultural sector—particularly canola producers—had been pressuring the government to find a resolution to previous trade disputes. By linking EV tariff reductions to agricultural market access, the Carney government created a political calculus where agriculture beneficiary constituencies could support what might otherwise be unpopular policy that harms domestic automakers.

The 49,000 vehicle annual quota is significant but not overwhelming. For context, Canada's total vehicle market is approximately 1.5 million units annually. Even if the quota filled completely, Chinese vehicles would represent roughly 3-4 percent of the market. However, the quota mechanism itself is notable—it establishes a framework for potentially expanding access if deemed successful. Once consumers experience Chinese EV quality and affordability, political pressure to maintain or expand the quota could become substantial.

Why Canada Moved First Among North American Nations

Canada's decision to negotiate independently rather than maintaining unified North American tariff policy reflects genuine tensions within the continental trade framework. The Trump administration's approach to trade negotiations has been more confrontational and less multilateral than previous administrations. Rather than coordinating with Canadian or Mexican policymakers on a shared approach to Chinese competition, Trump administration officials have prioritized bilateral relationships and sometimes contradictory strategic objectives.

Canada, as a smaller economy than the United States but with significant automotive manufacturing capabilities, faces a different competitive calculus. Canadian automakers produce approximately 5.3 million vehicles annually, with about 70 percent destined for the American market. This dependency on US market access limits Canada's negotiating leverage with the Trump administration. By moving independently on trade policy, Canada signaled both willingness to pursue its own interests and frustration with the unpredictability of Trump-era trade negotiations.

The political economy also matters. Canadian consumers have become increasingly frustrated with EV pricing. Traditional North American automakers have struggled to match Chinese EV prices and have focused their electric vehicle offerings on premium market segments. Opening market access to Chinese vehicles appeals to Canadian voters seeking affordable climate-friendly transportation options. Unlike the United States, where automotive manufacturing remains highly concentrated in several states with significant political power, Canadian auto production is more geographically dispersed and less dominant in the overall economy.

The Broader Context: Mexico's Earlier Chinese Vehicle Imports

Canada wasn't the first North American jurisdiction to allow Chinese vehicle imports. Mexico has imported Chinese vehicles for several years, with brands like BYD, Chery, and Neta establishing distribution networks and building consumer awareness. Notably, BYD had considered establishing a manufacturing facility in Mexico to serve North American markets, though those plans have been put on hold—possibly due to uncertainty around American trade policy.

Mexico's earlier openness to Chinese vehicles provided valuable market research for other potential importers. Mexican consumers have shown genuine interest in Chinese EVs, particularly in lower price segments where incumbent manufacturers struggle to compete. The absence of catastrophic consequences in the Mexican market—in terms of job losses, dramatic market disruptions, or quality scandals—probably increased Canadian confidence that similar policies would be manageable.

However, Mexico's situation differs from Canada's in important ways. Mexico has less established automotive manufacturing than Canada, and the American market is less critical to Mexico's auto sector. Canada's decision to move forward despite greater potential disruption to domestic manufacturing suggests genuine confidence that the agreement provides net benefits, or at minimum, that the political benefits outweigh the manufacturing sector costs.

Chinese EVs are priced significantly lower, with an average range of

Trump's Openness to Chinese Manufacturing in the United States: A Strategic Pivot?

The Detroit Speech and Chinese Factory Investment

President Trump created substantial surprise when he suggested at a Detroit event that Chinese automakers would be welcome to establish manufacturing operations in the United States. The conditions Trump articulated were straightforward: build factories in America and hire American workers. This statement seemed to contradict the Trump administration's combative approach to Chinese trade policy and raised immediate questions about whether this represented official policy or improvisational thinking.

The strategic logic underlying Trump's position, however, becomes clearer with examination. Trump has consistently prioritized manufacturing job creation and reshoring as a central policy objective. From his perspective, Chinese automakers investing in American factories represents exactly the type of job creation he has championed. Chinese companies establishing operations in the United States would bring capital investment, create manufacturing employment, and potentially generate additional economic activity in host communities.

This framing also addresses a fundamental challenge for American automakers: Chinese competitors have achieved superior cost structures and manufacturing efficiency. If American policy prevents Chinese manufacturers from competing domestically while simultaneously being unable to prevent Chinese imports from undercutting American manufacturers, the net effect is to harm American consumers and workers. Trump's approach suggests that allowing Chinese manufacturing in the US, subject to American employment requirements, might be preferable to ineffective tariff barriers that simply raise prices for consumers without protecting jobs.

Historically, American policy has favored allowing foreign manufacturers to establish US operations rather than relying purely on tariff protection. This approach drove Japanese automaker investment in the 1980s and 1990s—Toyota, Honda, and Nissan built massive manufacturing operations in America that now employ hundreds of thousands of workers. From this historical precedent, Trump's suggestion that Chinese manufacturers be allowed similar access isn't as radical as initial reactions suggested.

Tensions and Contradictions in Trump's Trade Approach

That said, Trump's willingness to accommodate Chinese manufacturing sits uneasily with other aspects of his trade philosophy and policy. The Trump administration has aggressively maintained existing tariffs on Chinese goods and threatened additional tariffs on a broad range of products. These actions have raised costs for American manufacturers and consumers while generating substantial revenue for the federal government.

The contradiction becomes apparent when considering battery manufacturing and automotive components. If Chinese automakers establish US factories but source batteries and critical components from China—which they almost certainly would, given supply chain advantages—the policy would fail to achieve the goal of genuine domestic manufacturing. Alternatively, if the United States insists that Chinese manufacturers source batteries and components domestically, this would eliminate much of the cost advantage that makes Chinese EVs attractive, potentially making the entire exercise economically unviable.

Moreover, allowing Chinese automakers unfettered access to American manufacturing would almost certainly trigger intense political opposition from American automakers, their suppliers, and union leadership. The United Auto Workers union has historically been a powerful political force, and the prospect of substantial Chinese manufacturing capacity in America would likely generate fierce resistance from labor organizations that have long opposed competitive threats to American jobs.

These contradictions suggest that Trump's openness to Chinese manufacturing may be more limited than initial statements suggested. More likely, the statement was designed to signal flexibility to China's leadership while preserving the option to maintain restrictive policies if political opposition becomes too intense. Trump's track record suggests he values the appearance of strength and unpredictability in negotiations, even when underlying policy remains relatively consistent.

The Competitive Threat: How Chinese EVs Could Disrupt North American Markets

Cost Advantages and Consumer Appeal

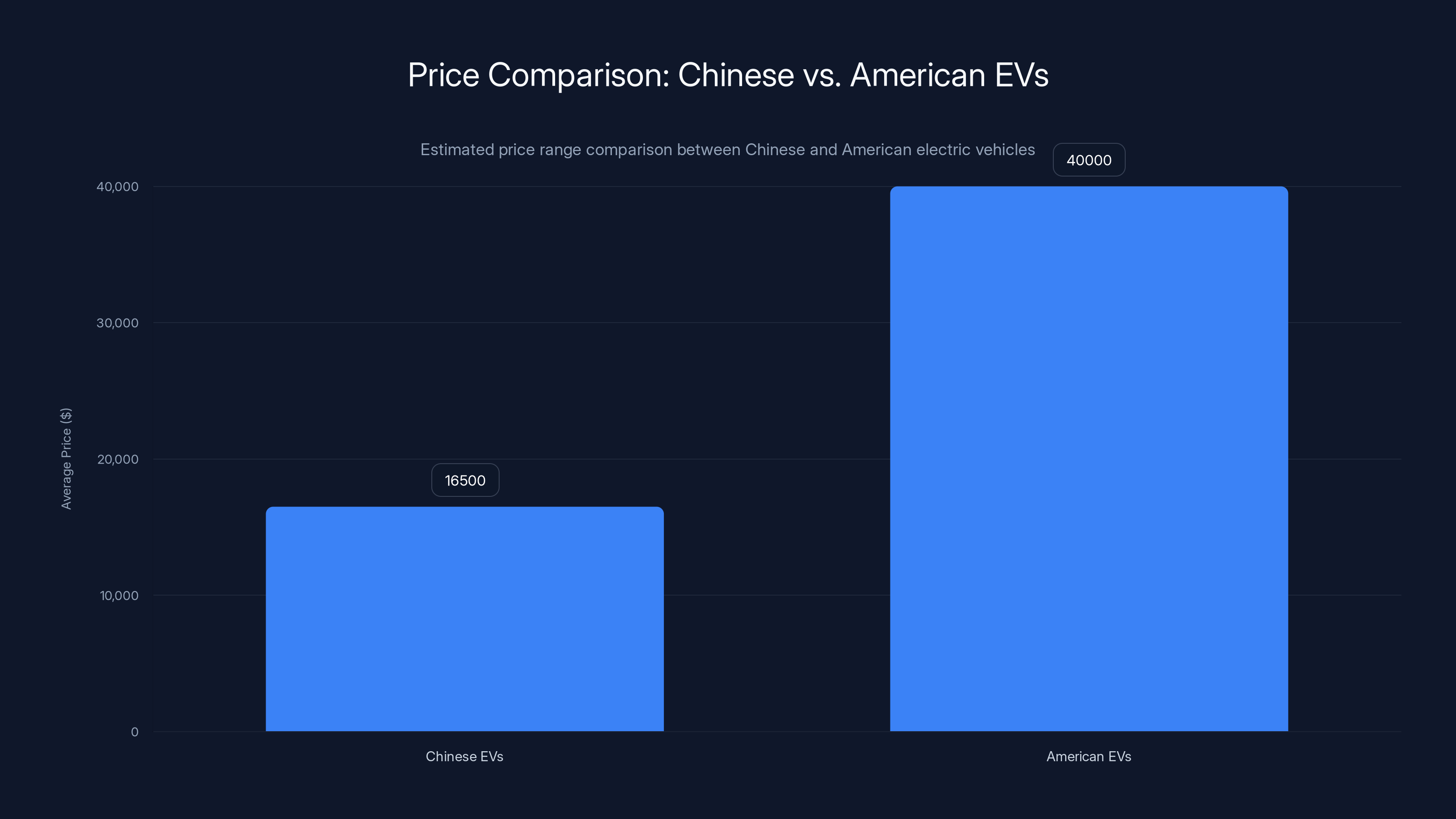

The fundamental driver of potential Chinese EV market penetration is straightforward economics: Chinese manufacturers can produce vehicles at dramatically lower cost while delivering competitive quality and impressive technical capabilities. A Chinese EV priced at

Consumer appeal extends beyond price. Chinese EVs generally offer sophisticated battery management systems, reasonably advanced autonomous driving capabilities (though not at the level of Tesla's most advanced systems), attractive interior design, and reliability that matches or exceeds many Western vehicles. Chinese manufacturers have invested heavily in design capabilities, software development, and quality control, and these investments are evident in the final products.

For price-sensitive consumers—particularly in Canada and potentially in the United States—the availability of credible, feature-rich vehicles at half the price of equivalent Western offerings represents genuinely transformational choice. Over time, as Chinese brands develop reputation and brand recognition, the price advantage alone could drive substantial market penetration. Chinese manufacturers have been aggressively marketing vehicles through influencers and social media, building awareness and positive associations among younger consumers who are early adopters of electric vehicles.

Tesla's Competitive Position and Elon Musk's Concerns

Tesla occupies an unusual position in this competitive landscape. Tesla built much of its early dominance on having no serious competitors in the premium EV segment. The company's cost advantages, manufacturing efficiency, and technological sophistication made it nearly impossible for traditional automakers to compete effectively. Tesla's Model 3 and Model Y became the world's best-selling vehicles in their respective segments, not just among EVs but across all vehicle categories.

Chinese competition threatens this position in several ways. Chinese manufacturers have achieved cost structures that allow them to undercut Tesla significantly on price while offering competitive features. BYD's battery manufacturing operations give it advantages in battery cost and quality that rival or exceed Tesla's. Chinese software development capabilities have advanced rapidly, making the gap between Tesla's autonomous driving features and those offered by Chinese competitors smaller than many Western observers realize.

Elon Musk has been remarkably candid about this threat. Musk has stated that Chinese automakers would "demolish" American automakers if given unfettered access to US markets. This assessment isn't hyperbole designed to justify protectionist policies—it appears to reflect Musk's genuine analysis of competitive dynamics. Musk has also indicated that Tesla's advantages are primarily in software and brand—areas where Chinese competitors are advancing rapidly—rather than manufacturing, where Chinese competitors have achieved parity or superiority.

Notably, Musk hasn't advocated for tariff protection against Chinese competition. Instead, Tesla has focused on innovation, cost reduction, and expanding into segments where it can compete effectively. This approach implicitly acknowledges that tariff protection is ultimately ineffective against genuinely superior competitors. The question isn't whether Tesla can maintain dominance against Chinese competition—that appears unlikely—but whether Tesla can maintain profitable market share in a more competitive environment.

Ford and Traditional Automakers' Vulnerability

Traditional American automakers like Ford, General Motors, and Stellantis face a more severe competitive threat from Chinese EV manufacturers than Tesla does. These manufacturers are in the midst of expensive transitions from internal combustion engines to electric powertrains. The transition requires enormous capital investment, retooling of manufacturing facilities, retraining of workforces, and rebuilding of supply chains optimized for battery and electric components rather than traditional automotive systems.

Ford CEO Jim Farley has publicly acknowledged the severity of this competitive threat. In interviews, Farley has essentially admitted that if Chinese manufacturers gained unrestricted access to American markets, they would capture substantial market share because Ford and other traditional manufacturers simply cannot match Chinese cost structures given their legacy cost burdens—pensions, healthcare obligations, aging manufacturing facilities, and established supplier relationships that factor in traditional costs.

This competitive disadvantage stems partly from labor costs but primarily from structural inefficiencies accumulated over decades. A Ford manufacturing facility built in the 1980s or 1990s, even after modernization, carries overhead burdens that a greenfield Chinese manufacturing facility built in 2020 simply doesn't have. Legacy supplier relationships often embed higher costs than alternatives available to Chinese manufacturers. Healthcare and pension obligations for existing workers increase labor costs beyond the hourly wages paid to new employees.

The vulnerability is particularly acute in lower price segments. Chinese manufacturers have demonstrated expertise in the sub-$25,000 EV market—a segment where American manufacturers struggle to achieve profitability. Ford's attempts to compete in this segment with vehicles like the upcoming affordable EV model face inherent disadvantages against Chinese competitors with lower cost structures. The question for Ford and similar manufacturers is whether they can reduce costs enough to compete or whether they will be forced to concede lower-priced segments to Chinese competitors and focus on premium segments where they retain advantages in brand prestige and performance.

Chinese electric vehicles are significantly cheaper, costing 40-60% less than North American counterparts, primarily due to efficient supply chains and manufacturing processes. Estimated data.

Tariff Structures and Their Effectiveness Against Cost-Advantaged Competitors

Current American Tariff Regimes Against Chinese Vehicles and Components

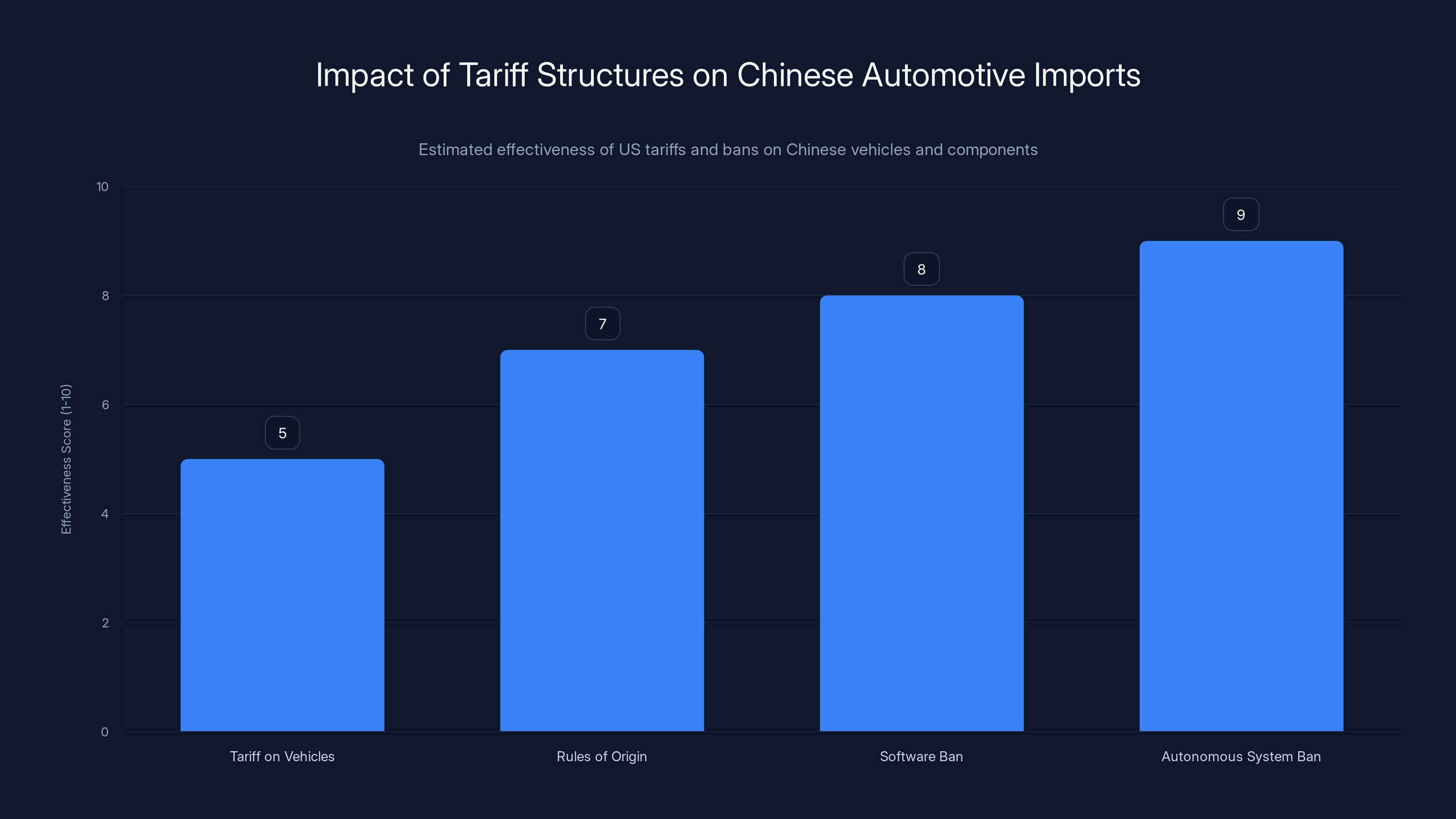

The United States currently maintains extremely high tariffs on imported automobiles—approximately 2.5 percent on vehicles, which is standard under trade agreements, but the Trump administration added additional tariffs specifically targeting Chinese-related supply chains. More significantly, the US maintains complex rules of origin requirements that effectively exclude many foreign components from vehicles. These rules specify that vehicles built in North America with high levels of North American content receive preferential treatment compared to vehicles with higher foreign content.

Beyond tariff rates themselves, the US has implemented complete bans on automotive software and autonomous driving systems from China. These bans reflect both competitive concerns and national security considerations. The bans are particularly significant because modern vehicles—especially electric vehicles—are increasingly software-dependent. Vehicles require sophisticated battery management systems, autonomous driving software, charging optimization algorithms, and infotainment systems. Chinese automakers have developed sophisticated capabilities in these areas, but American policy prohibits their incorporation into vehicles sold domestically.

The rationale for these restrictions involves both economic and security arguments. Economically, American policymakers want to preserve advantages for American technology companies in automotive software. Security arguments focus on concerns that Chinese automakers might incorporate surveillance capabilities into vehicles or create vulnerabilities that could compromise vehicle safety or provide data access to foreign governments. Whether these security concerns are exaggerated or legitimate is a matter of genuine debate, but they represent substantial political barriers to policy change.

Why Tariffs Alone May Fail Against Truly Superior Cost Structures

Musk's comment about Chinese automakers "demolishing" American manufacturers reflects an uncomfortable reality: tariffs alone cannot prevent competition from genuinely cost-advantaged competitors. Basic economics suggests that tariffs raise prices without addressing underlying cost differences. If a Chinese EV costs

Moreover, very high tariffs create political and economic costs. Consumers face higher prices. Domestic manufacturers lacking strong competitive pressures may have less incentive to innovate and improve efficiency. Tariffs generate political resentment from consumers and can trigger retaliation from trading partners. The history of trade protection suggests that while tariffs can provide temporary relief to affected industries, they rarely enable those industries to develop genuinely competitive advantages—instead, they tend to preserve inefficiency and delay necessary adjustments.

This economic reality explains why some American and Canadian business leaders have become more open to allowing Chinese competition. Rather than trying to exclude superior competitors, the alternative approach involves ensuring that competition occurs within a shared regulatory framework where vehicles must meet safety, emissions, and data security standards. The framework preserves important objectives—safety, environmental protection, security—while allowing competition on price and features to proceed.

Another consideration involves consumer welfare. From a consumer perspective, access to Chinese EVs would provide dramatically more affordable options for vehicle electrification. This could accelerate EV adoption overall by making electrified transportation accessible to middle and lower-income consumers who cannot currently afford available options. In a world where climate change is a serious concern, accelerating electrification even if it occurs through Chinese vehicles rather than American or Canadian manufacturers might represent the net-better outcome for broader societal goals.

Regional Manufacturing Implications and Supply Chain Restructuring

If Chinese vehicles entered North American markets at scale, the implications for existing automotive manufacturing would be substantial. Plants would close. Workers would be displaced. Suppliers would face demand reductions. These aren't abstract economic concepts—they represent real human costs that deserve serious policy consideration. Entire regions have economies built around automotive manufacturing, and wholesale disruption to that sector would create genuine hardship.

At the same time, the current automotive manufacturing base in North America is heavily concentrated in a handful of regions. Ontario in Canada and the American Midwest disproportionately depend on automotive employment. Political power within these regions is substantial, which explains the intense opposition to policies that might threaten automotive manufacturing. This concentration of political power means that even economically rational policies that would benefit broader consumer populations face intense opposition from concentrated, organized interests.

The long-term dynamic is also important. If Chinese manufacturers continue to improve and develop new technologies while American and Canadian manufacturers struggle to transition to electric powertrains, the competitive gap may widen rather than narrow over time. Current tariff protection might preserve existing jobs temporarily while preventing the organizational restructuring and innovation that would be necessary to compete long-term. Alternatively, allowing competition might force rapid innovation and restructuring that improves long-term competitiveness but creates short-term disruption.

Consumer Implications: Affordability, Choice, and Market Access

The Potential Price Impact on the EV Market

The most immediate consumer impact of allowing Chinese EV imports would be dramatic price reductions across the electric vehicle market. When Chinese manufacturers entered markets in other developed nations, they almost immediately forced price reductions from incumbent manufacturers. The presence of credible, well-reviewed alternatives at half the price creates competitive pressure that manufacturers cannot ignore.

For consumers, this price reduction would have profound consequences. Electric vehicles would become accessible to middle and lower-income households that currently find the technology financially out of reach. First-time EV buyers who might otherwise spend

The price reduction would likely accelerate overall EV adoption rates. Current EV penetration in North America, while growing rapidly, remains constrained partly by price. Consumers who would prefer electric vehicles but cannot justify the premium price would suddenly find affordable options. The resulting market expansion could actually benefit some incumbent manufacturers if they can compete in expanded market segments, while displacing others who cannot match Chinese cost structures.

Price competition might also extend to charging infrastructure and related services. As EV markets expand due to Chinese imports, charging networks would likely expand to serve larger customer bases, potentially reducing charging costs and improving availability. This infrastructure expansion would create positive feedback loops supporting additional EV adoption.

Quality, Warranty, and Service Concerns

A legitimate concern regarding Chinese EV imports involves quality, warranty coverage, and service availability. American and Canadian consumers are accustomed to extensive warranty coverage, easily accessible service networks, and straightforward repair processes. Chinese manufacturers, even those with solid reputations in their home markets, would need to establish comparable service infrastructure to compete effectively in North America.

Some Chinese manufacturers have already begun establishing North American service networks in preparation for potential market access. BYD has explored service arrangements and facility locations. Other manufacturers have partnerships with existing dealers or are planning dedicated service centers. However, establishing service infrastructure comparable to that of established manufacturers would require substantial investment and time. During a transition period, consumers purchasing Chinese vehicles might face warranty concerns, service delays, or difficulty finding qualified technicians.

Quality concerns have largely diminished as Chinese manufacturers have matured. Modern Chinese EVs undergo rigorous quality control and testing. Battery durability and reliability match or exceed Western vehicles. However, perception lags reality—many North American consumers remain skeptical about Chinese manufacturing quality even though objective evidence suggests the concern is overstated. Building consumer confidence would require positive ownership experiences, independent quality reviews, and consistent warranty coverage.

Accessibility for Lower and Middle-Income Consumers

Perhaps the most significant consumer benefit of Chinese EV access would be dramatically improved affordability. For lower and middle-income consumers, vehicle purchases represent one of the largest financial decisions. Adding

This accessibility matters both economically and environmentally. Economically, it reduces transportation costs—electricity to charge a vehicle is substantially cheaper than gasoline per mile. Environmentally, it accelerates the transition to zero-emission vehicles in lower-income segments where adoption has lagged. It also reduces transportation cost burdens on lower-income households, effectively representing a transfer of wealth from oil companies to consumers in the form of reduced energy costs.

The social implications are also noteworthy. Access to new, reliable vehicles improves quality of life for lower-income households. New vehicles reduce maintenance needs, improve reliability, and provide better safety features compared to older vehicles that lower-income consumers often drive due to affordability constraints. Electrified new vehicles combine reliability benefits with dramatically lower operating costs.

Estimated data suggests that bans on software and autonomous systems are more effective than tariffs and rules of origin in limiting Chinese automotive imports.

The Question of Trade Dynamics: Will the United States Follow Canada?

Policy Tensions and Political Calculation

Whether the United States follows Canada's example by allowing Chinese EV imports remains deeply uncertain and heavily dependent on political dynamics. The Trump administration has simultaneously signaled both openness to Chinese manufacturing (contingent on US factory investment) and maintaining protectionist tariff barriers. These positions aren't obviously compatible, which suggests the administration hasn't settled on a final policy approach.

The political economy of automotive trade heavily favors protection. Automotive manufacturing unions, particularly the United Auto Workers, have extraordinary political influence in key states like Michigan, Ohio, and Pennsylvania. American automakers have spent decades building relationships with political figures and agencies that tend to support industry protection. Regional economies heavily dependent on automotive manufacturing face economic decline if domestic production is reduced due to Chinese competition.

These concentrated political interests oppose Chinese competition far more intensely than diffuse consumer benefits support it. Individual consumers benefit from cheaper vehicles, but that benefit is individually modest—perhaps

At the same time, the Trump administration has shown willingness to pursue unorthodox policies and overturn established precedents. Trump's unpredictability on trade matters could work in either direction—he might maintain tariff protection to satisfy auto industry constituencies and labor unions, or he might pursue openness to Chinese manufacturers to signal strength and claim credit for lower consumer prices.

Regulatory Harmonization and Standards

A potential pathway toward allowing Chinese vehicles in US markets would involve harmonizing safety, emissions, and autonomous vehicle standards between Chinese and American regulators. Rather than maintaining absolute bans on Chinese vehicles or imposing punitive tariffs, the US could establish technical requirements that Chinese vehicles would need to meet. If Chinese manufacturers can meet these requirements—and many can—vehicles would be allowed market access.

This approach offers several advantages. It preserves important regulatory objectives around safety and environmental protection while eliminating ineffective tariff barriers. It allows consumer choice while maintaining standards that protect public welfare. It creates competitive pressure on American and Canadian manufacturers to improve efficiency and innovation while preserving their option to compete on quality, brand, and features rather than relying purely on trade protection.

Regulatory harmonization has precedent. The US has harmonized automotive standards with other developed nations through various forums. Chinese automakers have demonstrated capability in meeting international standards—vehicles sold in Europe, Australia, and elsewhere meet rigorous regulatory requirements. Establishing comparable requirements for the American market is technically feasible, though politically contentious.

The obstacle involves political resistance from incumbent manufacturers and their supplier networks. From their perspective, regulatory requirements are preferable to tariff barriers because they level the playing field somewhat—if Chinese vehicles must meet the same standards as American vehicles, the cost of compliance might reduce Chinese cost advantages. Strict autonomous vehicle and cybersecurity requirements could be particularly effective at increasing Chinese manufacturer costs, though this approach raises questions about whether such requirements are genuinely necessary or are protectionist measures disguised as safety standards.

Timeline and Policy Scenarios

The trajectory of American policy toward Chinese vehicles will likely depend on several factors: the success of Canada's experiment with Chinese imports, evolution of the Trump administration's thinking on trade and manufacturing, political pressure from affected constituencies, consumer demand for affordable EVs, and technological developments in autonomous vehicles and battery technology.

A base-case scenario suggests that the US maintains high tariffs and restrictive policies on Chinese vehicles for the near term, particularly given political sensitivities around automotive manufacturing employment. However, within 5-10 years, several factors might shift this position. If Canadian consumers successfully adopt Chinese EVs at scale and experience no negative consequences, American political resistance would likely weaken. If Chinese manufacturers achieve significant technological leadership in autonomous driving or battery technology, maintaining a complete ban might appear increasingly economically irrational. If American consumers increasingly demand access to affordable EVs and perceive tariff barriers as harmful to their interests, political pressure for change would build.

Alternatively, if American and Canadian manufacturers successfully complete their transition to electric powertrains while achieving significant cost reductions, the competitive threat from Chinese vehicles might diminish or disappear. Manufacturers might develop new competitive advantages through advanced autonomous driving systems, superior software, or features particularly appealing to North American consumers. In this scenario, tariff barriers could gradually be reduced as competitive pressures ease.

Manufacturing Implications for North American Auto Plants

Capacity Utilization and Production Forecasts

North American automotive manufacturing operates at specific capacity levels planned years in advance. Automakers invest billions in manufacturing facilities based on demand forecasts and production plans. The introduction of Chinese EV competition that captures unexpected market share would disrupt these plans, creating excess capacity, underutilized facilities, and difficult decisions about production and employment.

Currently, American and Canadian automakers are in the midst of major capital investments to transition manufacturing capacity from internal combustion engines to electric vehicles. Ford, General Motors, and Stellantis are retooling facilities, investing in battery manufacturing partnerships, and restructuring supply chains. These investments are predicated on assumptions about market share and demand levels. Unexpected Chinese competition would invalidate many of these assumptions, potentially requiring expensive facility restructuring or early obsolescence of investments.

The capacity problem is particularly acute for battery manufacturing. American battery manufacturing capacity is being built through partnerships with companies like LG, SK Innovation, and others, with significant government support through the Inflation Reduction Act and other incentives. These facilities are designed to supply specific vehicle production volumes. If Chinese vehicles capture market share faster than anticipated, battery overcapacity would develop, potentially making some American battery manufacturing uneconomical. Alternatively, if Chinese batteries are allowed to be imported, American battery manufacturers face direct competition and potential failure.

Geographic Concentration and Regional Economic Risk

Automotive manufacturing in North America is heavily concentrated geographically, creating regional vulnerability to sector disruptions. Ontario, Michigan, Ohio, Kentucky, Tennessee, and a handful of other regions depend disproportionately on automotive employment. In some communities, automotive manufacturing represents 20-30 percent of employment. Pension systems for public employees and teachers in these regions depend partly on tax revenue from automotive manufacturing.

Chinese competition that significantly reduced vehicle production in North America would create regional economic distress with political consequences. Unemployed autoworkers would seek retraining and relocation. Communities would face declining tax revenues and economic contraction. Schools and public services would suffer funding reductions. These human and economic costs cannot be ignored in policy decisions, even if they don't represent optimal economic outcomes in narrow efficiency terms.

This geographic concentration also creates political incentives for trade protection. Automotive-dependent regions have substantial representation in Congress and significant influence over presidential elections (particularly Michigan and Ohio). Politicians from these regions face intense pressure to protect domestic manufacturing. The concentrated nature of the political interest in protection explains why trade barriers persist even when they generate broader economic costs.

Supply Chain and Supplier Network Disruption

Automotive supply chains are complex, deeply integrated systems involving thousands of suppliers, many of which are small to medium-sized companies with specialized capabilities and limited ability to adapt to dramatic market changes. These suppliers depend on contracts with major automakers to maintain operations and employment. If major automakers reduce North American production due to Chinese competition, suppliers face demand reductions that threaten viability.

Many suppliers have invested heavily in specific manufacturing capabilities tailored to particular vehicle platforms or powertrains. These investments become stranded assets if demand disappears. Suppliers in lower-value segments—plastic components, fasteners, rubber products—have limited ability to transition to other industries. Workers in these supplier companies often have limited alternative employment opportunities in their regions.

The disruption would extend to supporting services: trucking companies moving vehicle components, logistics providers, parts warehouses, dealer networks. An entire ecosystem of economic activity depends on automotive manufacturing at current volumes. Sudden disruption would create cascading effects throughout these supplier networks.

At the same time, the introduction of Chinese vehicles might create opportunities for new supply chain participants if Chinese manufacturers establish manufacturing operations in North America. Chinese batteries, powertrains, and electronics could be sourced from Chinese companies establishing North American operations. This would create opportunities for new suppliers while displacing existing ones—a genuine restructuring rather than simply loss and decline. However, during transition periods, the disruption would be real and painful for affected communities and workers.

Estimated data shows that Chinese EV imports could reduce average EV prices from

International Trade Law and Regulatory Frameworks

World Trade Organization Obligations and Disputes

American and Canadian trade policy operates within frameworks established by international trade law, particularly World Trade Organization (WTO) rules. These rules limit the ability of countries to impose arbitrary tariffs or discriminate against products based on country of origin. Excessive tariffs or protectionist measures face legal challenges through WTO dispute mechanisms.

China has previously challenged American tariffs through WTO dispute processes, with some success. If the United States maintains or increases tariffs on Chinese vehicles while allowing vehicles from other countries to enter at lower rates, China would likely file WTO complaints. Ultimately, a WTO dispute panel might rule that such tariffs violate trade rules, creating pressure to change policies or face retaliatory tariffs from China.

Canada's tariff reduction agreement is presumably structured to comply with WTO rules—it appears to be a bilateral agreement reducing tariffs, not a discriminatory action that violates most-favored-nation principles. The US would have more difficulty maintaining restrictions specifically on Chinese vehicles if other countries are allowed vehicle imports. Any American policy limiting Chinese vehicles would face potential legal challenges both through WTO mechanisms and through provisions of trade agreements like USMCA (the updated NAFTA).

These legal frameworks provide some pressure toward policy harmonization. If Canada allows Chinese vehicles, the US faces legal pressure to do the same rather than maintaining unilateral restrictions. Maintaining distinct policies creates legal risk and potentially triggers retaliatory measures.

National Security Exceptions and Autonomous Driving Standards

Trade law includes exceptions for national security concerns, which could justify restrictions on Chinese vehicles if structured carefully. The Trump administration has invoked national security exceptions for various trade actions, and similar reasoning could apply to automotive restrictions if tied to autonomous driving capabilities and cybersecurity concerns.

Arguments for national security restrictions would focus on potential Chinese government access to vehicle telemetry, autonomous driving systems creating vulnerability to cyberattacks, or information gathering capabilities embedded in Chinese vehicles. If structured as general autonomous driving and cybersecurity standards rather than discriminatory restrictions on Chinese vehicles specifically, such requirements might survive legal challenge while effectively limiting Chinese vehicle access.

However, this approach raises questions about whether legitimate security concerns are being used to justify protectionism. American and European vehicles increasingly incorporate extensive telemetry, autonomous driving systems, and internet connectivity that create comparable security concerns. If American policymakers impose rigorous cybersecurity standards on Chinese vehicles but not on American vehicles, the discriminatory nature becomes apparent and potentially challengeable.

USMCA and Continental Trade Framework

The United States-Mexico-Canada Agreement (USMCA), which replaced the original NAFTA, establishes a continental trade framework that should theoretically coordinate policy on Chinese vehicle imports. However, Trump administration policies have sometimes operated outside or contrary to USMCA provisions, and the agreement's provisions on automobiles and related trade are complex and sometimes ambiguous.

Canada's independent move to reduce tariffs on Chinese EVs without coordinating with the US raises questions about USMCA compliance. Mexico had already allowed Chinese imports, so Canada's move continues a pattern of unilateral national policy rather than coordinated continental approach. The framework doesn't appear to require exact tariff harmonization across the three countries, but it does establish principles about non-discrimination and most-favored treatment.

If the US maintains high tariffs on Chinese vehicles while Canada and Mexico allow imports, the effective result is that vehicles can enter the North American market through lower-tariff entry points and potentially be sold across borders. This creates incentives to establish distribution networks in Mexico or Canada to serve American consumers. Enforcement of border restrictions becomes complex and potentially uneconomical.

Battery Technology and Supply Chain Considerations

China's Dominance in Battery Manufacturing and Raw Materials

China controls a disproportionate share of global battery manufacturing and dominates processing of raw materials critical for battery production. CATL manufactures roughly 37 percent of the world's battery capacity. Chinese companies control significant refining capabilities for lithium, cobalt, and nickel—the critical elements in battery chemistry. This dominance creates fundamental cost advantages that are difficult for Western manufacturers to overcome quickly.

American policy has recognized this strategic vulnerability and has invested heavily in developing domestic battery manufacturing and supply chains through the Inflation Reduction Act. The law provides substantial subsidies for battery manufacturing, critical mineral processing, and EV assembly in the United States. The goal is to reduce dependence on Chinese batteries and minerals and develop domestic capacity.

However, even with substantial subsidies, American and European battery manufacturing cannot quickly match Chinese capacity or cost structures. Chinese manufacturers achieved their dominance through decades of incremental development, massive volumes, and ruthless competition. American manufacturers are starting from a base of essentially zero battery production a decade ago. Even accelerated development will take years to achieve parity with Chinese capabilities.

This creates a strategic dilemma: if American automakers are forced to source batteries domestically due to tariff barriers on finished vehicles but Chinese batteries, they face higher costs that reduce competitiveness. If Chinese batteries are allowed to be imported, American battery manufacturers cannot compete. If Chinese vehicles with Chinese batteries are excluded through tariffs, American consumers face higher prices and fewer options.

Raw Materials Security and Supply Chain Resilience

America and Europe have become concerned about strategic dependence on Chinese-controlled supply chains for critical materials. China controls processing of rare earth elements and other materials essential for advanced technologies. This dependence creates vulnerability: China could theoretically restrict supplies of critical materials for strategic or political purposes.

This concern extends to batteries. If Chinese vehicles dominate North American markets and Chinese companies control battery supply chains, American dependence on Chinese supply chains actually increases rather than decreases. Even if vehicles are manufactured in America, if batteries are sourced from Chinese companies using Chinese-processed raw materials, American strategic dependence doesn't change substantially.

The resolution involves investing in Western supply chains for raw material extraction, processing, and battery manufacturing. This requires substantial capital investment and time. American and allied companies are developing critical mineral extraction in the US, Australia, and allied nations. Processing capabilities are being developed. Battery manufacturing capacity is expanding. However, these efforts require years to mature and significant capital investment before approaching Chinese scale.

EV Cost Reductions and Long-Term Technology Development

China's dominance in battery manufacturing and EV production has paradoxically driven down global EV costs faster than would have occurred in a Western-dominated manufacturing environment. Chinese competition has forced manufacturers globally to innovate in cost reduction and efficiency. Battery prices have fallen far more rapidly than many experts predicted, primarily driven by Chinese manufacturing scale and competition.

From a consumer and environmental perspective, this cost reduction accelerates EV adoption worldwide. Lower battery costs make EVs more affordable and more competitive with internal combustion engines. This acceleration is genuinely valuable for addressing climate change. From an economic nationalism perspective, however, this cost reduction also shifts manufacturing and economic benefits toward Chinese companies and away from Western manufacturers.

Policies that exclude Chinese competition might slow this cost reduction by reducing competitive pressure on Western manufacturers to innovate. Protected incumbents have less incentive to invest in revolutionary new approaches if they're not facing pressure from superior competitors. Conversely, policies that allow Chinese competition ensure rapid cost reduction and technology advancement, even if it occurs primarily through Chinese companies rather than Western ones.

Under the new trade agreement, Chinese electric vehicles could occupy up to 3-4% of the Canadian vehicle market, highlighting a significant yet controlled market entry.

Labor, Jobs, and Economic Transition

Employment Impacts and Worker Transition Challenges

If Chinese EVs captured substantial North American market share, employment impacts would be significant. Automotive manufacturing employs roughly 1.6 million workers in the United States and Canada combined. These are relatively high-wage jobs—manufacturing employment in automotive typically pays

Worker transition is also complicated. Many automotive manufacturing workers are in midcareer or late career stages. Retraining for different occupations is difficult and often results in lower-wage employment. Geographic relocation is challenging—manufacturing jobs are concentrated in regions where workers have roots, family, and social networks. Expecting 50-year-old manufacturing workers to retrain and relocate is unrealistic for many affected individuals.

This reality explains why unions and worker organizations oppose policies that might reduce automotive employment. The concerns aren't abstract economic theory—they represent genuine human welfare implications. Workers and communities face real, substantial costs from trade disruption. These costs should be weighed seriously in policy decisions, even if narrower economic efficiency calculations suggest that trade barriers are economically inefficient.

Policy Options for Managing Transition

If trade policy were to shift toward allowing more Chinese competition, effective transition assistance would require substantial public investment. Education and retraining programs would need to help displaced workers develop new skills. Wage insurance could replace lost income during transition periods. Geographic mobility assistance could help workers relocate to regions with better employment opportunities. These programs are expensive but arguably more humane and economically efficient than maintaining ineffective trade barriers that create broad consumer costs without effectively protecting affected workers.

Historically, the US has underinvested in worker transition assistance. Trade Adjustment Assistance (TAA) programs exist but are often underfunded and limited in scope. If trade policies were to shift toward greater openness, policymakers would presumably need to invest more substantially in transition assistance to provide political sustainability for the policy change.

Alternatively, if American automakers develop genuinely competitive advantages through innovation and efficiency improvements, they might be able to compete effectively against Chinese imports even without tariff protection. This scenario would require sustained investment in technology development, manufacturing efficiency, and developing vehicles that appeal to consumers for reasons beyond price. Some American manufacturers might achieve this position while others decline—resulting in a restructured rather than eliminated automotive sector.

Skills Development and Workforce Evolution

The shift from internal combustion to electric vehicles is inherently different in manufacturing requirements. EV manufacturing is less labor-intensive than traditional automotive manufacturing. Battery pack assembly is increasingly automated. Fewer components are required in an EV powertrains compared to traditional combustion engines. These structural differences mean that even if American manufacturers maintain significant market share, employment levels would likely decline compared to historical norms.

Workers displaced from traditional manufacturing could transition to electric vehicle manufacturing if they develop appropriate skills. Battery manufacturing, power electronics, advanced materials processing, and software development offer employment opportunities. However, these roles often require different skill sets than traditional automotive assembly work. Community colleges and training organizations would need to develop curricula to train workers in these new competencies.

Long-term, the automotive sector may be able to absorb displaced workers through new roles, but transition periods would involve genuine disruption and hardship. Some workers would successfully transition while others would face permanent income reductions. Communities would experience population decline if younger workers relocate for employment opportunities while older workers remain in declining regions.

The Environmental and Climate Dimension

Accelerated EV Adoption Through Affordability

One underappreciated aspect of Chinese EV competition involves climate and environmental benefits. If Chinese vehicles reduce EV prices significantly, they would accelerate electrification of transportation, which is critical for climate change mitigation. Transportation accounts for roughly 25 percent of US greenhouse gas emissions, with light-duty vehicles responsible for about half of that. Decarbonizing transportation is essential for achieving climate goals.

Current EV prices limit adoption to relatively affluent consumers. Lower prices achieved through Chinese competition would enable lower and middle-income households to access electric vehicles. This would accelerate the overall rate of fleet electrification, potentially reducing transportation emissions decades earlier than current trajectories suggest. For climate objectives, this acceleration represents substantial value.

Of course, environmental benefits depend on the electricity grid's carbon intensity. In regions with largely renewable or nuclear electricity, EV adoption provides immediate emissions benefits. In regions still dependent on fossil fuel generation, benefits are more modest but still substantial since electric powertrains are more efficient than combustion engines even when powered by fossil generation. Over time, as electricity grids transition to renewables, the environmental benefits of EVs increase.

Manufacturing Carbon Intensity and Lifecycle Assessments

A more complex environmental consideration involves manufacturing carbon intensity. Chinese manufacturing might use more coal-based electricity than equivalent American manufacturing, depending on facility locations and power sources. Lifecycle carbon assessments of vehicles manufactured in China versus North America would need to account for these differences. Some studies suggest that manufacturing in high-carbon-intensity regions could offset operational emissions benefits of electric powertrains.

However, Chinese manufacturing emissions intensity has been improving. Chinese companies increasingly have access to renewable electricity through grid expansion. New manufacturing facilities are more efficient than older ones. Over lifecycle analysis periods of 10-15 years, manufacturing location becomes less significant as operational emissions (which heavily favor EVs) accumulate. The overall lifecycle carbon advantage of an affordable Chinese EV over an expensive American EV produced from fossil fuel electricity likely remains positive from an environmental perspective.

This calculation gets complicated quickly and depends on numerous assumptions about electricity sources, manufacturing processes, and vehicle lifespans. The general point is that environmental considerations don't clearly argue for or against allowing Chinese vehicles. They argue for rapid EV adoption whatever the source, which favors affordable vehicles from whatever manufacturer can provide them most cost-effectively.

Regulatory Standards and Environmental Compliance

A potential framework for allowing Chinese vehicles while preserving environmental objectives would involve requiring compliance with North American emissions standards. Chinese vehicles would need to meet equivalent tailpipe emissions standards, fuel economy standards, and other environmental requirements. If structured this way, environmental protection would be maintained while consumer choice would expand.

China's environmental standards have been evolving and are increasingly stringent. Chinese EV manufacturers have demonstrated capability in meeting rigorous international emissions standards. This suggests that requiring Chinese vehicles to meet North American standards would be technically feasible without substantially increasing costs or reducing competitiveness.

A regulatory approach would be superior to tariff-based approaches from an environmental perspective because it would allow cost competition while preserving environmental objectives. Rather than using trade barriers to discourage Chinese vehicles, North American policymakers could use environmental standards to ensure that vehicles meet rigorous performance requirements while allowing competition to drive innovation and cost reduction.

Market Access and Consumer Rights Considerations

Transparency and Information Availability

Consumers making vehicle purchase decisions benefit from transparent information about quality, reliability, safety features, warranty coverage, and service availability. Incumbent manufacturers have established reputations and extensive information available through publications, consumer reviews, and dealer networks. Chinese manufacturers, even those with strong reputations in their home markets, would need to establish equivalent information availability for North American consumers.

Independent testing organizations like NHTSA and IIHS provide safety ratings for vehicles sold in North America, helping consumers evaluate safety features. These organizations would need to test Chinese vehicles to provide consumers with reliable safety information. Without this information, consumers would face information asymmetries that could lead to poor decisions or distrust of unfamiliar brands.

Transparency is also important for warranty and service commitments. Would Chinese manufacturers honor warranties if companies fail or withdraw from markets? Would service be available in consumers' regions or only in major metropolitan areas? Would recalls be handled effectively? These questions need clear answers before consumers should trust purchasing Chinese vehicles. Regulatory frameworks would need to establish requirements for warranty coverage, service network availability, and recall procedures before allowing Chinese vehicles to be sold.

Consumer Protection and Product Liability

North American legal frameworks establish consumer protection through product liability laws, warranty requirements, and fraud protections. Vehicles must meet safety standards and manufacturers can be held liable for defective products that cause injury. These protections help ensure that manufacturers have incentives to maintain quality and safety.

Extending these protections to Chinese manufacturers raises questions. If a Chinese manufacturer sells vehicles in North America but doesn't maintain sufficient assets in North American jurisdiction, can injured consumers effectively pursue product liability claims? If a manufacturer exits the market, can warranty obligations be fulfilled? These legal frameworks would need to be adapted to ensure that consumer protections extend equally to Chinese as to American manufacturers.

One approach would require Chinese manufacturers to establish legal entities and maintain assets sufficient to meet potential liability obligations. This adds costs to Chinese manufacturers and potentially reduces their competitive advantage. However, it also ensures that consumers have effective remedies for defective products, which is important for market functioning and consumer welfare.

Competitive Dynamics and Market Evolution

Tesla's Strategic Position in a More Competitive Market

Tesla occupies a unique position in the EV market as a software-focused company competing on technology and brand rather than low cost. In a world where Chinese competitors dominate low-cost segments, Tesla would likely maintain substantial market share in premium segments where consumers prioritize advanced autonomous driving, performance, and brand prestige. Tesla's advantages in software development and autonomous driving capabilities would remain significant even against capable Chinese competitors.

However, the competitive environment would be more challenging. Tesla's current market dominance depends partly on lack of competition in the EV segment. With Chinese competitors entering the market, Tesla would face pressure to maintain innovation pace, reduce costs in lower-price segments, and defend market share. These competitive pressures would ultimately benefit consumers through faster innovation and more choices, but would reduce Tesla's unprecedented profitability and market dominance.

Elon Musk's candid assessment that Chinese competitors would "demolish" American automakers suggests his recognition of this competitive reality. Musk appears to have acknowledged that superior competition ultimately serves consumer interests even if it reduces Tesla's specific advantages. This pragmatic perspective might influence Trump's thinking—if even Tesla's CEO acknowledges that Chinese competition would be good for consumers, maintaining protectionist policies becomes harder to justify.

Traditional Automakers' Restructuring Scenarios

Traditional automakers face fundamentally different challenges. Ford, General Motors, and Stellantis have massive legacy cost structures and are in the midst of expensive transitions to electric vehicles. Chinese competition would accelerate the pain of this transition by forcing cost reductions, production adjustments, and facility closures.

In a scenario where Chinese vehicles gain substantial market share, American automakers might focus on premium segments, specialized vehicles (trucks, SUVs), and markets where they maintain brand advantages. Lower-cost segments would likely be dominated by Chinese competitors. Over time, American automakers would shrink in absolute size but might maintain profitability by focusing on higher-margin segments. This would represent significant restructuring from historical norms where major manufacturers competed across all price segments.

Alternatively, American automakers might develop specialty competencies in autonomous driving or software capabilities that differentiate them from Chinese competitors and justify premium pricing. If they successfully develop autonomous vehicle technology superior to Chinese competitors, they could compete effectively on features even if unable to match on price. This path would require sustained investment in technology development and innovation.

New Entrants and Market Disruption

The introduction of Chinese vehicles might also accelerate the emergence of new entrants and market disruption. Startups focused on specific vehicle types (commercial vehicles, robotaxis, delivery vehicles) might find it easier to compete in a market where price pressures favor new competitors and incumbent advantages are weaker. Chinese vehicle platforms could be adapted for North American markets by new competitors with innovative business models.

Alternatively, Chinese manufacturers might establish North American subsidiaries and compete directly using North American-based facilities and supply chains. This would gradually transition from "Chinese vehicles imported to North America" to "Chinese companies manufacturing vehicles in North America," which aligns with Trump's expressed openness to Chinese factory investment. Over 10-20 years, the relevant distinction wouldn't be where vehicles are manufactured but rather company ownership and control of technology.

Policy Recommendations and Strategic Options

A Framework for Managed Competition

Rather than absolute exclusion of Chinese vehicles or unmanaged market opening, a strategic approach would establish a regulatory framework that permits competition while preserving important policy objectives. This framework would require Chinese vehicles to meet North American safety, emissions, and cybersecurity standards. Vehicles meeting these standards would be permitted to compete on price and features.

This approach preserves environmental and safety objectives while enabling consumer choice and cost competition. It avoids the ineffectiveness of tariff barriers while also avoiding the regulatory capture risks that might emerge if Chinese companies gain unmanaged access. Requirements for warranty coverage, service network availability, and product liability compliance would ensure that consumer protections extend equally to all manufacturers.

Implementing this framework would require coordination between federal transportation safety agencies, environmental regulators, and cybersecurity officials. Standards would need to be developed, testing procedures established, and Chinese manufacturer compliance verified. This process would take time, but would provide a logical path forward that acknowledges competitive realities while maintaining important protections.

Investment in American Competitive Capabilities

Simultaneously with opening to Chinese competition, American policy should accelerate investment in developing genuinely competitive American manufacturers. This requires sustained funding for battery manufacturing, autonomous vehicle development, charging infrastructure expansion, and workforce development. The Inflation Reduction Act represents a start, but substantially more investment would be needed to develop competitive capabilities matching Chinese competitors.

Specifically, American policy should:

- Expand battery manufacturing subsidies to achieve parity with Chinese battery costs within 10 years

- Invest in autonomous vehicle development to maintain American leadership in software and autonomous driving

- Establish critical mineral processing capabilities to reduce dependence on Chinese supply chains

- Fund workforce development in batteries, power electronics, and EV manufacturing

- Support charging infrastructure expansion to ensure seamless EV adoption across North America

- Maintain R&D funding for next-generation battery technologies and powertrain innovations

These investments would position American manufacturers to compete on innovation and capabilities rather than relying on trade protection. Over time, a well-funded approach might develop American competitive advantages that justify premium positioning compared to lower-cost Chinese alternatives.

Managed Transition Support for Affected Workers and Communities

If trade policies shift toward allowing more Chinese competition, comprehensive support for affected workers and communities becomes essential from both ethical and political sustainability perspectives. This includes:

- Expanded Trade Adjustment Assistance providing longer-term income support and retraining

- Wage insurance helping workers transition to lower-wage employment

- Community economic development assistance for regions heavily dependent on automotive manufacturing

- Education and training programs preparing workers for new roles in EV manufacturing and related sectors

- Relocation assistance helping workers move to regions with better employment opportunities

These programs would be expensive—potentially billions annually if implemented comprehensively. However, the cost would be justified by providing genuine support for affected people and communities rather than maintaining expensive and ultimately ineffective tariff barriers that benefit concentrated industries at the expense of general consumers.

Looking Forward: Scenarios for 2025-2030

Base Case: Gradual Opening with Protective Measures

The most likely scenario involves gradual opening to Chinese vehicles with continued protective measures that slowly relax over time. The Trump administration might initially maintain tariff barriers while negotiating with Chinese manufacturers about establishing American manufacturing operations. Companies like BYD or others might invest in American factories, creating vehicles manufactured domestically but owned and designed by Chinese companies.

This scenario would gradually expand Chinese-controlled automotive capacity in North America while maintaining tariffs on imported vehicles. Over time, as Chinese manufacturers prove successful and domestic opposition moderates, tariffs might be reduced. Canadian and Mexican market access would gradually increase, creating pressure for American policy alignment.

In this scenario, North American automotive employment would gradually decline but wouldn't experience sudden collapse. Existing American and Canadian manufacturers would restructure toward premium segments where they retain competitive advantages. Chinese manufacturers would dominate lower-price segments but would face tariff barriers limiting market penetration. Within 10 years, Chinese vehicles would represent 15-25% of the North American market.

Optimistic Case: Rapid Transition to Open Competition

An optimistic scenario involves American policymakers recognizing that Chinese competition ultimately benefits consumers and accelerates technological advancement. Trade barriers are reduced significantly, and Chinese vehicles compete openly with American and Canadian manufacturers. American companies invest heavily in developing competitive capabilities, focusing on premium segments and advanced autonomous vehicles where they maintain advantages.

In this scenario, North American vehicle prices decline substantially, EV adoption accelerates, and manufacturing employment declines but restructures toward higher-technology, higher-wage roles. American manufacturers maintain meaningful but reduced market share, competing on innovation and premium positioning rather than low cost. Within 10 years, Chinese vehicles might represent 30-40% of the market, but employment would be stabilized at lower levels with higher-wage manufacturing jobs.

This scenario requires substantial adjustment but ultimately creates more innovative, efficient automotive industries. Consumers benefit through lower prices and more choices. American competitiveness in advanced technologies improves as manufacturers are forced to innovate. Environmental benefits accrue through accelerated EV adoption.

Pessimistic Case: Sustained Trade War and Market Fragmentation

A pessimistic scenario involves the Trump administration and potentially future administrations maintaining aggressive protectionism, escalating trade conflicts with China, and fragmenting North American automotive markets. High tariffs persist, Chinese vehicles are excluded from American markets, and trade relations deteriorate. In this scenario, consumers face high vehicle prices, innovation slows due to reduced competitive pressure, and manufacturing employment gradually declines anyway due to automation despite trade protection.

Canada and Mexico might maintain more open policies toward Chinese vehicles, creating unequal market access across North America. Supply chains become increasingly fragmented. American automakers focus on the protected American market while ceding international markets to Chinese competitors. Over time, American manufacturers fall further behind in innovation because lack of competitive pressure removes incentives for rapid development of advanced technologies.

This scenario represents the worst of both worlds: high consumer costs, reduced innovation, and ultimate manufacturing decline anyway due to inability to compete in global markets. Employment declines occur anyway due to automation, while consumers pay premium prices and have limited choices.

The Broader Context: Technology, Innovation, and Market Competition

Software, Autonomous Driving, and Competitive Differentiation

Increasinglly, vehicle competitiveness depends on software capabilities, autonomous driving systems, and integrated technology rather than traditional automotive manufacturing metrics. Chinese companies have invested heavily in autonomous driving research, battery management software, and artificial intelligence applications in vehicles. These capabilities represent genuine innovations that shouldn't be ignored in assessing competitive threats.

American advantages in software development remain real but eroding. Tesla's autonomous driving capability represents a genuine advantage, but Chinese companies are advancing rapidly. BYD's latest models incorporate sophisticated autonomous features. XPeng has been developing advanced autonomous capabilities. The technical gap between American and Chinese autonomous driving capabilities is narrowing faster than most Western observers expected.

This software competition dimension argues against tariff protection and for allowing open competition. If American companies are to maintain leadership in autonomous vehicle technology, they need to compete directly with Chinese competitors, driving innovation pace. Tariff protection would reduce competitive pressure and potentially slow American innovation. The long-term American interest is in winning the autonomous vehicle software competition, not in maintaining cost advantages through trade barriers.

Global Supply Chains and Economic Integration

Modern vehicles incorporate components from global supply chains. A vehicle labeled "Made in America" likely contains components from multiple countries, including China. Similarly, vehicles manufactured in China often incorporate American and European components. Tariffs and trade barriers complicate these integrated supply chains, raising costs without effectively protecting anything meaningful.