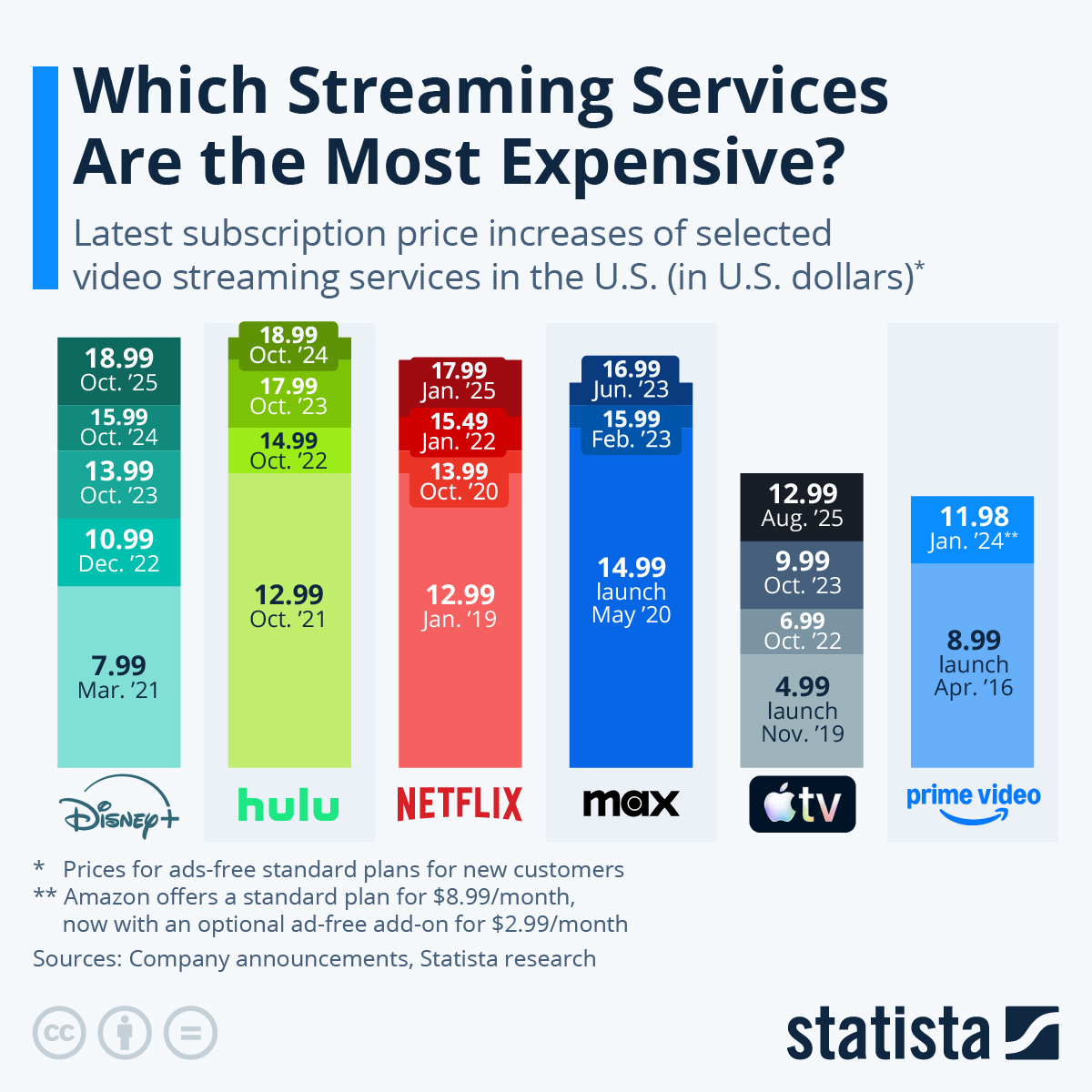

![Streaming Subscription Prices Soared 29% in 2025 [2026]](https://tryrunable.com/blog/streaming-subscription-prices-soared-29-in-2025-2026/image-1-1768421242018.jpg)

Streaming Subscription Prices Soared 29% in 2025: What Federal Data Really Shows

Something broke in the streaming economy last year. Not the technology. Not the business model. The social contract.

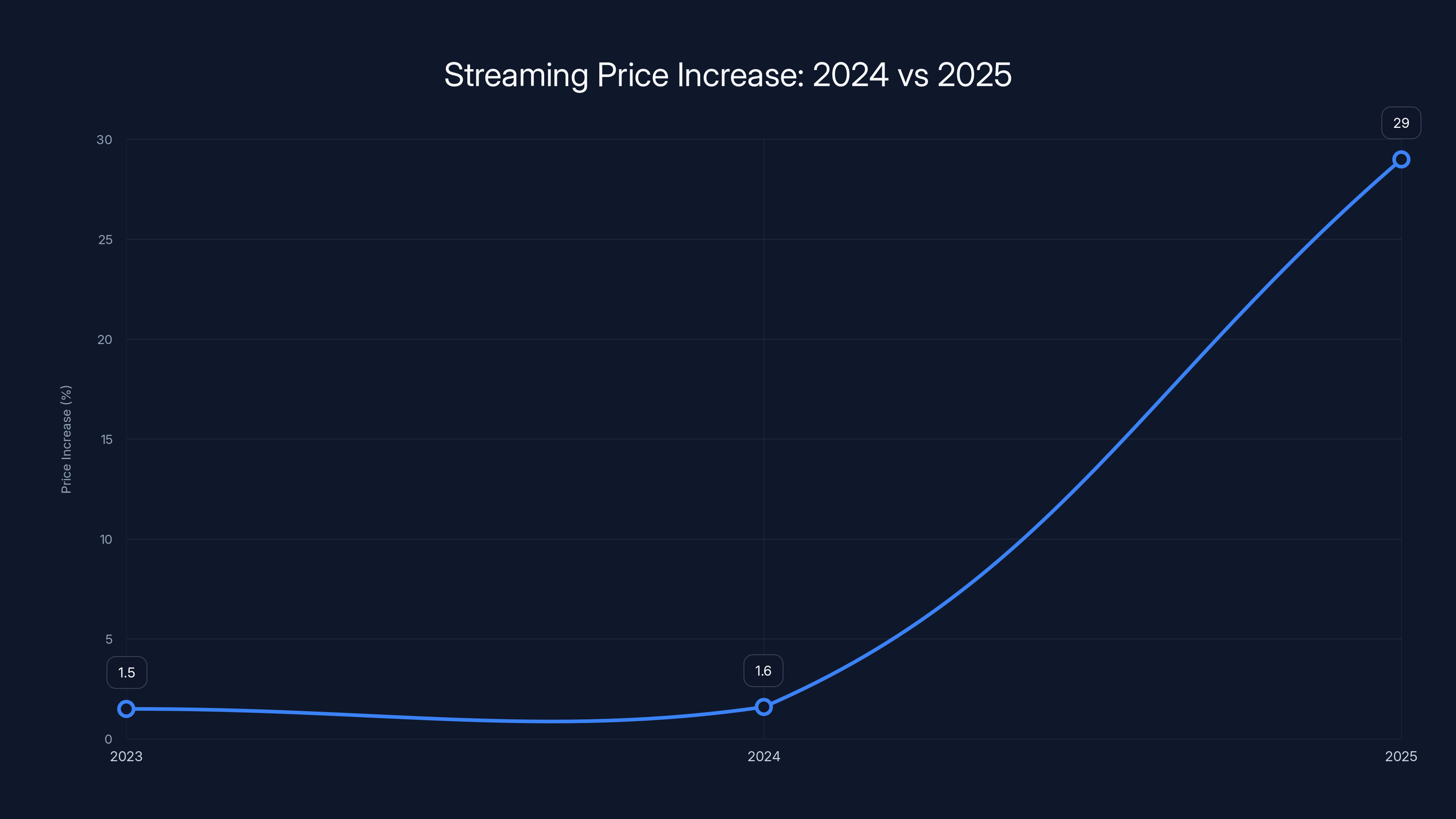

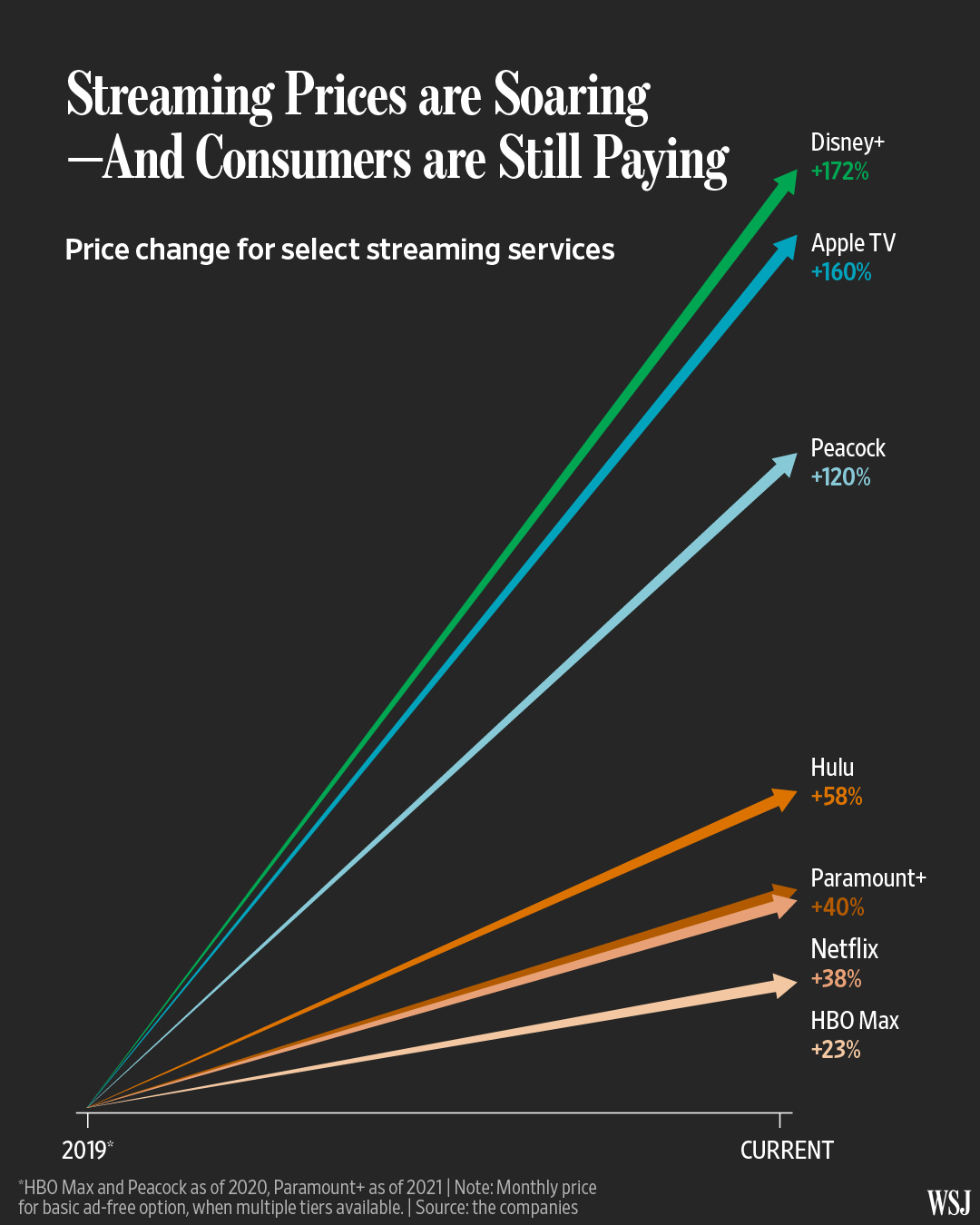

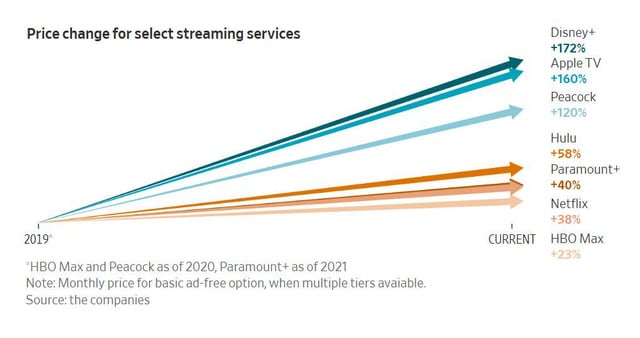

Americans woke up in 2025 to find that watching Netflix, Disney+, HBO Max, and Apple TV had become measurably more expensive. Not just by a few percentage points. Not by the typical inflation adjustment. The prices that Americans paid for subscription and rental access to video streaming services and video games jumped 29 percent from December 2024 to December 2025.

That number comes directly from the US Department of Labor's Bureau of Labor Statistics. It's not hyperbole. It's not extrapolation. It's official federal economic data.

To put that in perspective, overall inflation for the entire US economy—everything from housing to groceries to gasoline—was 2.7 percent that same year. Streaming services raised prices roughly ten times faster than the general rate of inflation. That's not a market correction. That's market power being wielded with confidence.

This shift didn't happen overnight, but the acceleration in 2025 marked a genuine inflection point. Streaming companies that spent their early years undercutting cable TV prices now price like they've become the dominant entertainment platform. Because they have. Television has fundamentally changed, and the companies that control the digital pipes realized they could charge accordingly.

The question isn't whether streaming prices rose. Federal data confirms that. The real question is why it happened so suddenly, what consumers are actually paying, and whether the industry overplayed its hand in 2025.

TL; DR

- 29% price surge: Streaming and video game subscriptions increased by 29% in 2025, nearly 11 times faster than overall inflation

- Compared to cable: Traditional cable saw only 4.9% inflation, making streaming the most aggressive price raiser in entertainment

- November to December spike: The final month of 2025 alone saw adjusted inflation of 19.5% for streaming services

- Every major service hiked: Netflix, Disney+, HBO Max, Apple TV+, and smaller services all raised rates simultaneously

- Subscriptions outpaced food inflation: Streaming price increases exceeded even volatile food categories like beef steaks and coffee

- Industry expects continued increases: Analysts predict more hikes in 2026, likely through premium tiers and feature-based pricing

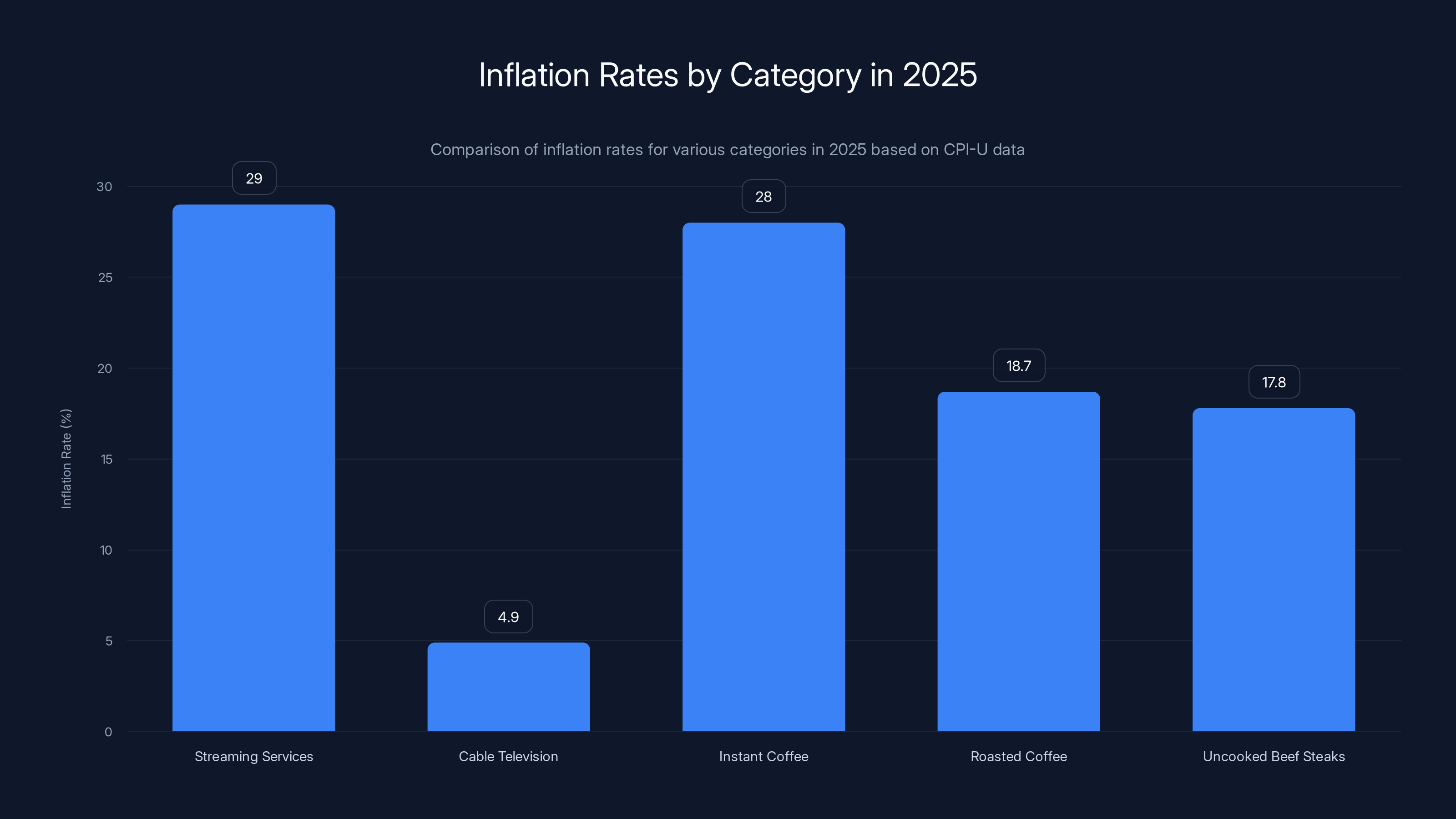

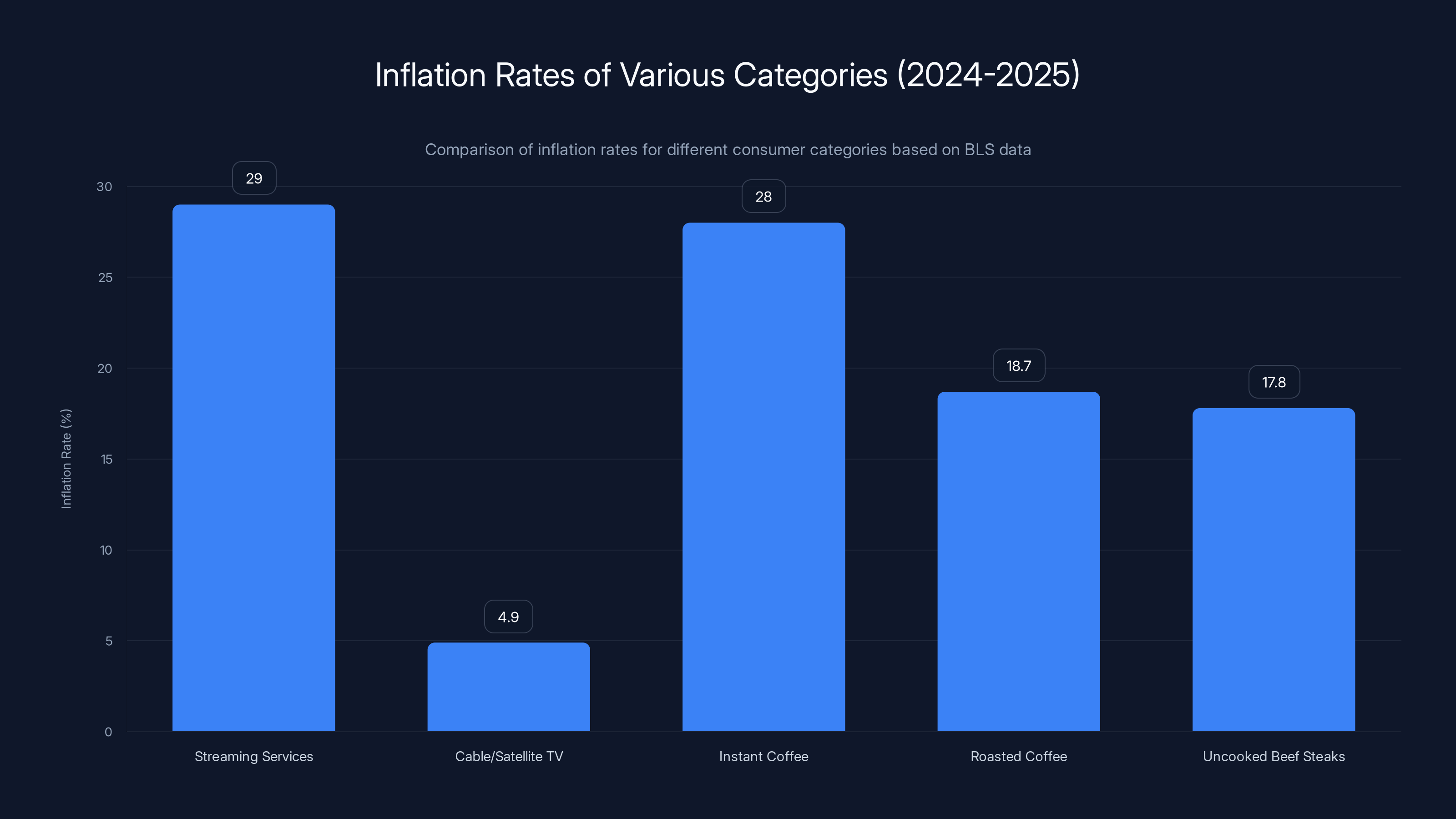

In 2025, streaming services experienced the highest inflation rate at 29%, significantly outpacing other categories like cable television (4.9%) and instant coffee (28%).

The Federal Data That Changed Everything

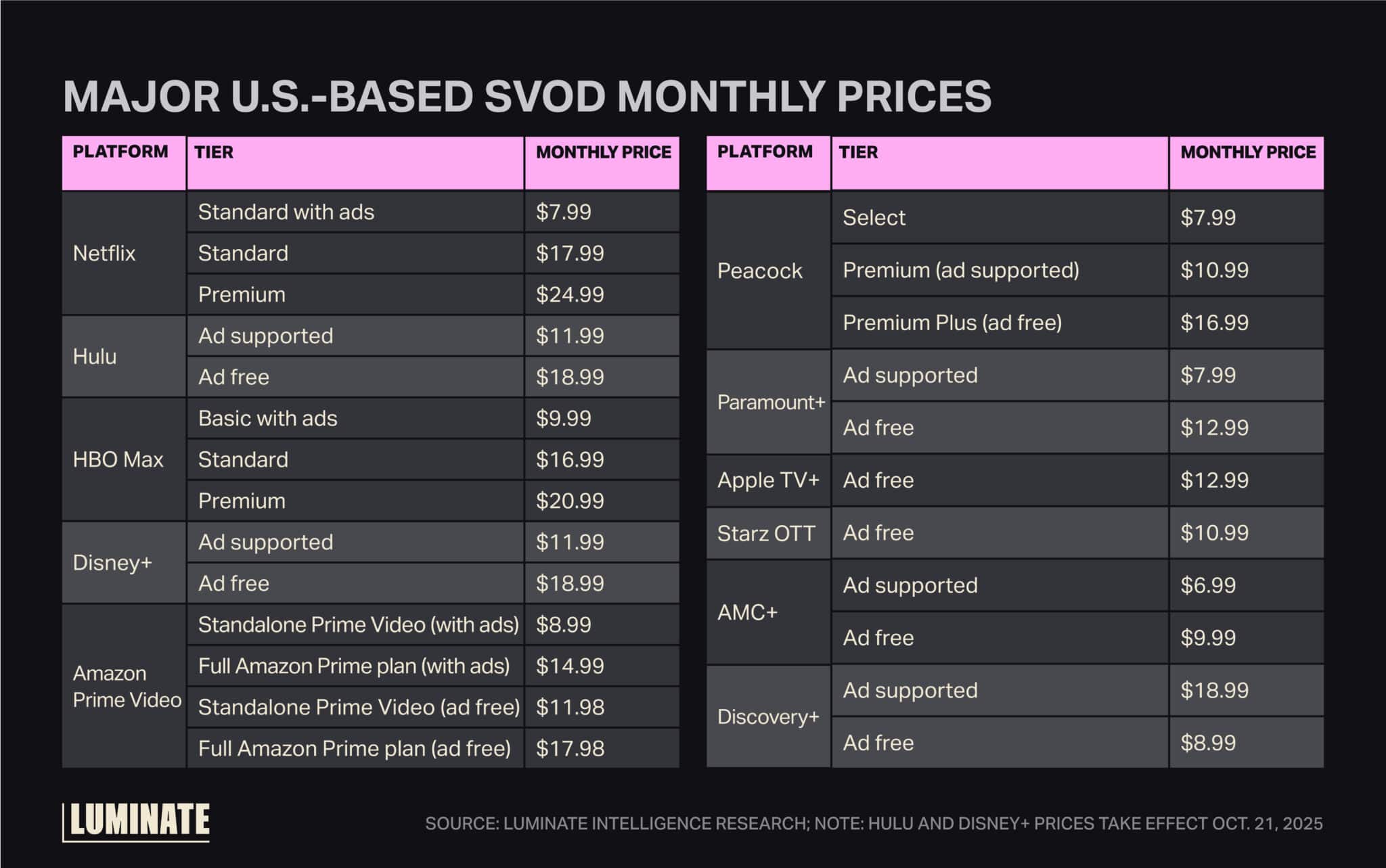

Here's what actually happened with the numbers. The US Department of Labor's Bureau of Labor Statistics tracks prices for everything Americans buy. They break down these categories into subcategories. One of those subcategories is "subscription and rental of video and video games." This includes Netflix, Disney+, HBO Max, Apple TV+, and any service where you pay to stream content or rent videos.

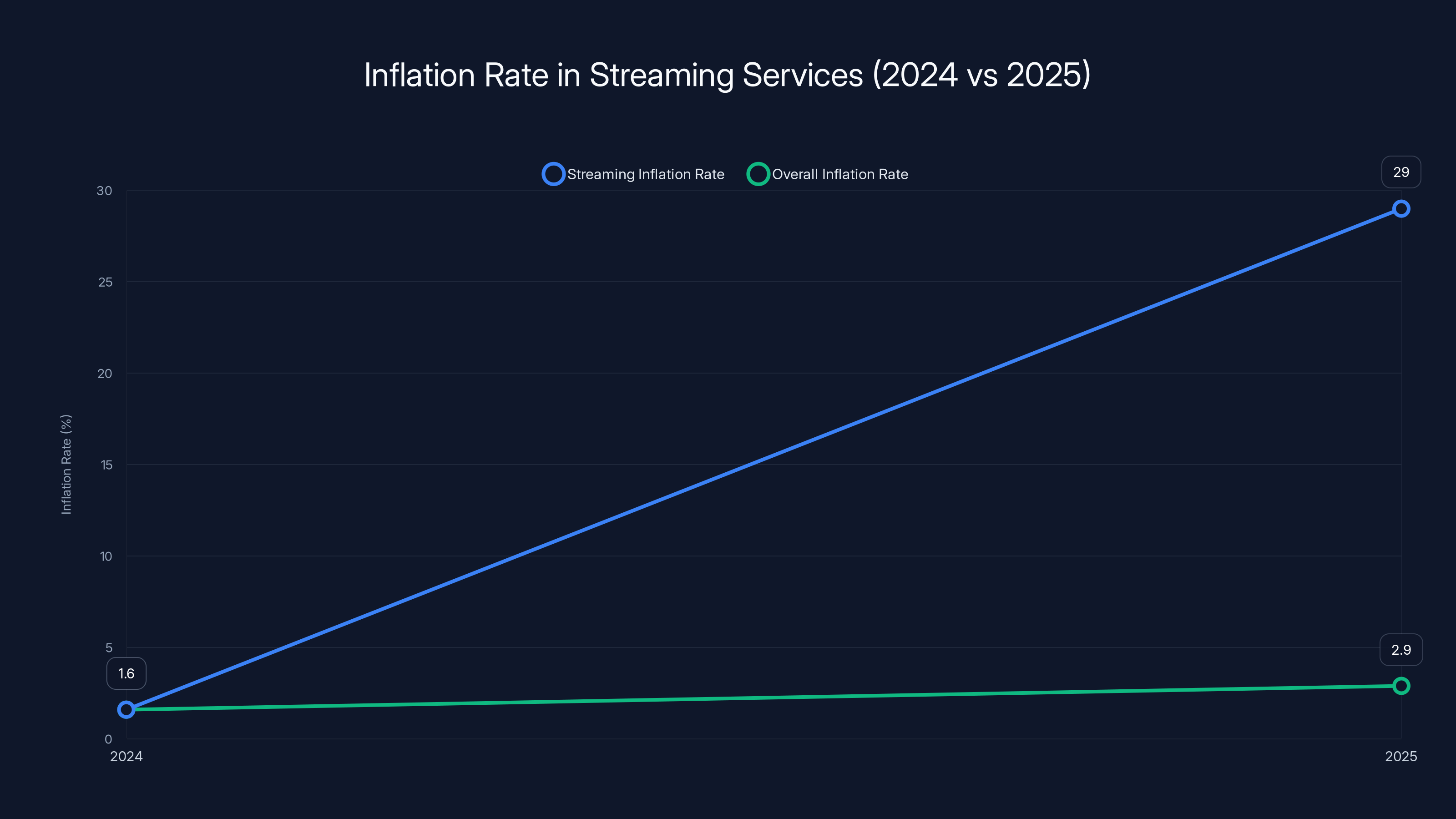

The Consumer Price Index for All Urban Consumers (CPI-U) that BLS releases represents over 90 percent of the US population. When it moves, it matters. On Tuesday, January 28th, 2026, the BLS released data showing that this category saw 29 percent unadjusted inflation from December 2024 to December 2025.

Unadjusted data matters because it reflects what consumers actually pay. Adjusted data removes seasonal variations and expected yearly shifts. But if you're paying more for Netflix every month, the unadjusted number is the one that hits your wallet. That 29 percent number is what real people experienced.

To understand how extreme this was, consider the context. The overall CPI-U for all items increased just 2.7 percent that year. Different categories of goods and services performed differently. Cable, satellite, and live streaming television services like YouTube TV and Sling TV saw 4.9 percent inflation. That's high, but it's not streaming-high.

Now zoom out even further. What else in the American economy saw similarly aggressive price increases? Instant coffee saw 28 percent inflation. Roasted coffee saw 18.7 percent. Uncooked beef steaks saw 17.8 percent. These are volatile categories where commodity prices and supply chains create year-to-year swings. Streaming services—where the marginal cost of adding one more subscriber is near zero—somehow kept pace with agricultural commodities. That tells you something about market power and pricing strategy.

Why November-to-December Was the Real Shock

Zoom in on the final month of 2025. From November to December alone, streaming and gaming subscriptions saw adjusted inflation of 19.5 percent. Adjusted inflation means BLS removed seasonal variations. They weren't expecting that kind of shift. December typically sees some price adjustments and year-end billing changes, but 19.5 percent in a single month was extraordinary.

This tells us the price increases didn't happen evenly throughout the year. Companies didn't gradually inch up prices month by month. Instead, they coordinated a late-year push. This is deliberate strategy. Streaming companies timed their increases for maximum collection impact while consumers are distracted by holidays and year-end accounting.

The November-to-December data point matters because it shows acceleration, not deceleration. If streaming companies were moderating their increases, you'd see the year-to-date 29 percent spread relatively evenly. Instead, you see a massive concentration at the end of the year. Consumers woke up on New Year's Day 2026 to find their favorite services cost significantly more.

Streaming services experienced the highest inflation rate at 29%, surpassing both traditional TV services and various food commodities, indicating significant market power and pricing strategy shifts.

The Comparison to 2024 Shows Clear Acceleration

Context matters. In December 2024, streaming prices had increased just 1.6 percent year-over-year. That was already above the overall inflation rate of 2.9 percent for that year, but it wasn't shocking. Companies were taking small price increases. It seemed sustainable. It seemed reasonable.

Then 2025 happened. From 1.6 percent to 29 percent is not a continuation of a trend. It's a fundamental shift in strategy. Something changed in how streaming companies viewed their market position and their ability to raise prices without losing customers.

This 18-fold acceleration in a single year tells you the increase wasn't driven primarily by cost pressures. If labor, licensing, or infrastructure costs had suddenly increased 29 percent, that would be visible in the broader economy. Instead, it shows that streaming companies—having consolidated their market position and having become the primary way Americans watch television—started pricing like a mature, profitable industry rather than a growth-stage disruptor.

They stopped competing on price. They started competing on content and features. And they used their existing subscriber base as a monetization opportunity.

Why Every Major Service Hiked Simultaneously

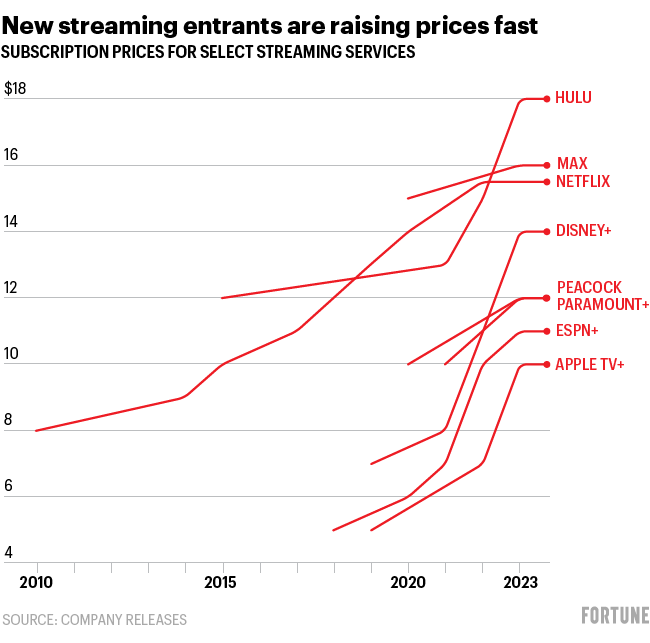

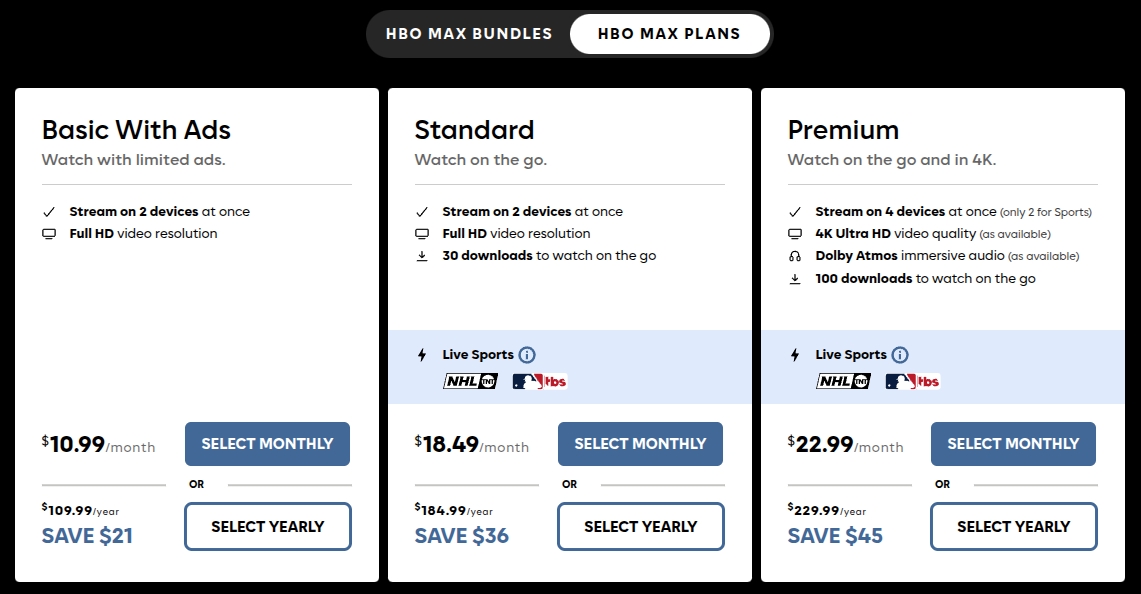

Netflix raised prices. Disney+ raised prices. HBO Max raised prices. Apple TV+ raised prices. Smaller services like Dropout and Discovery+ also increased rates. This wasn't one company breaking ranks and raising prices while competitors held steady. It was an industry-wide strategy.

When competitors all raise prices simultaneously in the same category, economists call that oligopolistic price leadership. It's not explicitly coordinated (which would be illegal), but it achieves the same effect. One company raises prices, others follow within weeks. No one undercuts because they've realized that undercutting isn't a path to profit. It's a path to customer acquisition, and these companies already have plenty of customers.

Netflix moved first with confidence. In late 2024 and early 2025, they announced increases on their ad-free tiers and premium plans. They'd built a track record of raising prices while maintaining subscriber numbers. Their investors rewarded price increases more than subscriber growth. So they kept doing it.

Disney+ looked at Netflix and thought: if they can do it, so can we. HBO Max and Apple TV+ came next. The smaller services had no choice. If they didn't raise prices, they couldn't justify their existence to investors. So they did.

What's remarkable is how little consumer pushback stopped these increases. Some people complained on social media. Some canceled subscriptions. But the vast majority paid the new prices. The services counted on this. They probably modeled the cancellation rate, calculated the revenue impact, and determined that raising prices on 95 percent of their base more than offset losing 5 percent of subscribers.

The Business Model Shift Behind the Prices

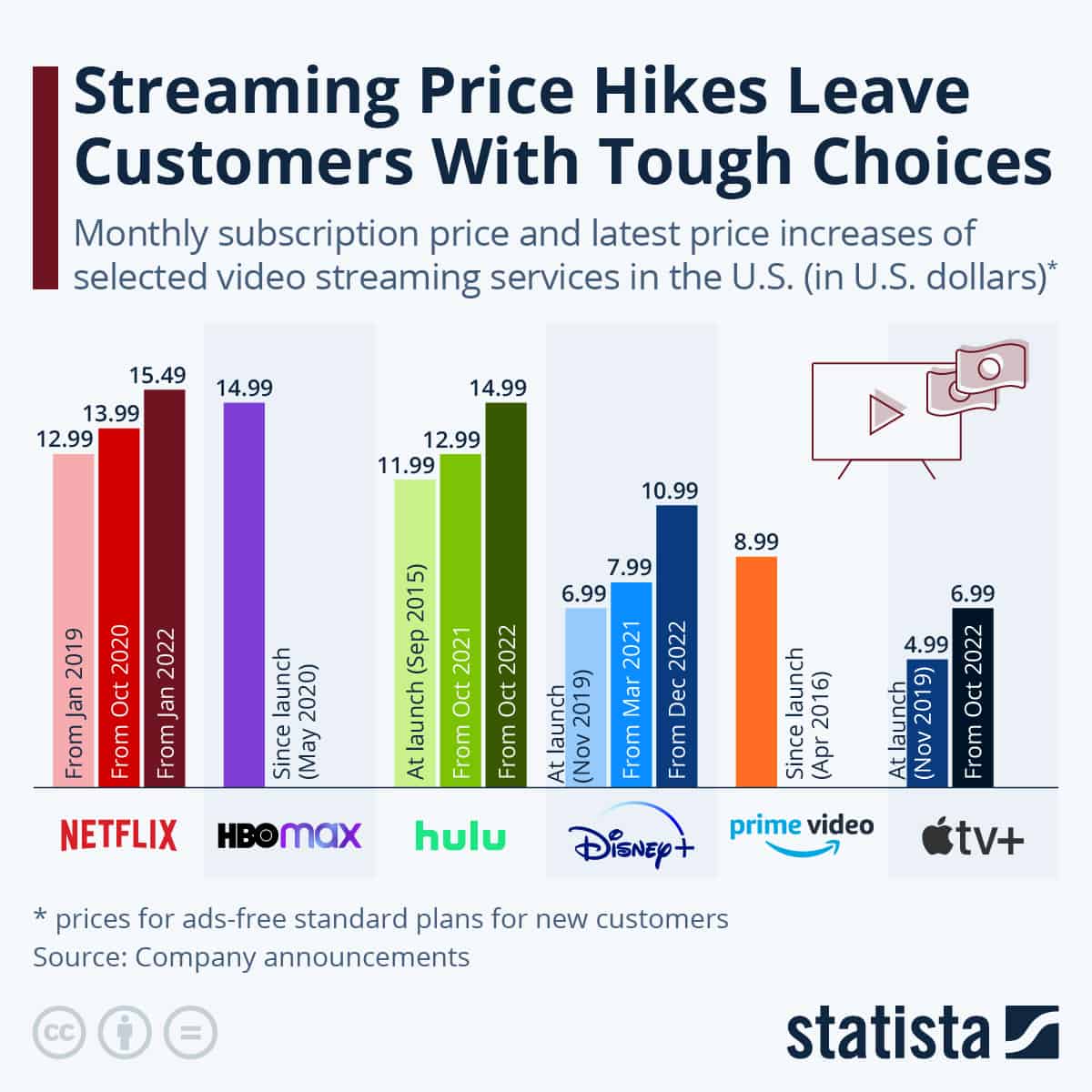

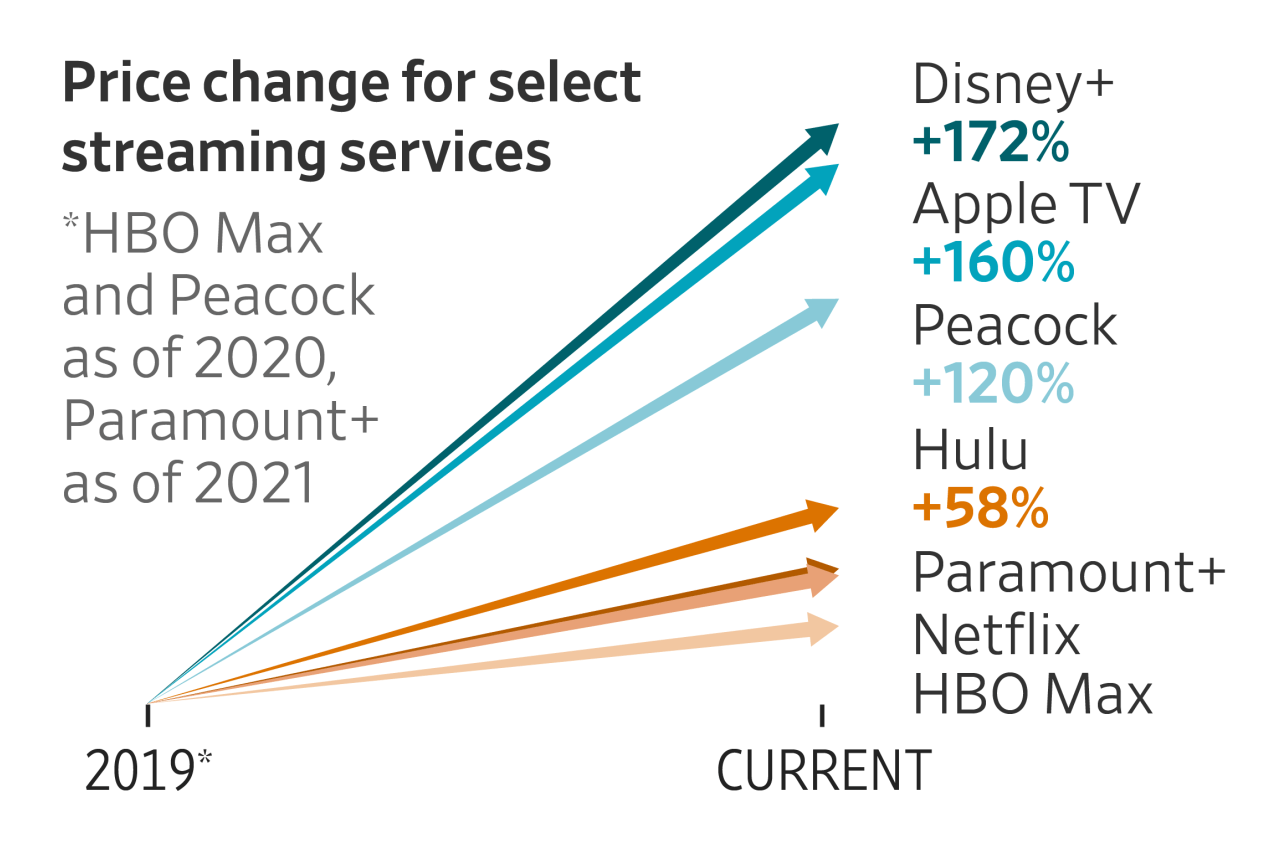

Streaming Services didn't start as premium offerings. They started as Netflix trying to destroy Blockbuster. They were cheap. Netflix was nine dollars a month when it launched its streaming service in 2007. It undercut cable. It offered a compelling value proposition: unlimited streaming of thousands of movies and shows for less than you'd spend on a single cable movie channel.

That pricing strategy worked because it served a purpose: get people to switch from cable. Build subscriber volume. Establish market share. Then profit would follow.

It worked. Streaming became the dominant way Americans watch television. Cable subscriptions plummeted. Streaming companies went from scrappy startups to the primary entertainment distribution platform. They'd won.

Once you've won, you don't keep competing on price. You compete on content, interface, and ecosystem lock-in. You raise prices to maximize profit from your existing customer base. You segment your customer base into tiers: ad-free premium for price-insensitive customers, ad-supported for price-sensitive customers, and basic for whoever will accept bandwidth limitations or other restrictions.

This is textbook monopolistic competition. When one firm has significant market power and few close substitutes, it doesn't need to keep prices low to attract customers. It raises prices to extract maximum value from its existing base. Streaming companies had become that firm. The 29 percent increase reflected that new reality.

But there's a limit to how far you can push. Customers have finite entertainment budgets. Streaming fatigue became real in 2025. The average household with multiple subscriptions was paying

When you're approaching cable prices without the sports, local news, and broader content diversity of cable, some customers start asking whether they should just go back to cable. That question marks the ceiling on pricing power.

Streaming prices saw a dramatic increase from 1.6% in 2024 to 29% in 2025, indicating a strategic shift in the industry. Estimated data.

Password Sharing Crackdowns and Ads as Revenue Strategies

Streaming companies understood they couldn't raise prices infinitely without pushback. So they deployed other revenue extraction strategies. Netflix's password-sharing crackdown was the most aggressive. For years, people shared Netflix accounts with family members and friends. One household paid, five households watched. Netflix tolerated this because it built habits and brand loyalty.

Then Netflix realized: we could charge for these accounts. They started requiring paid adds or password restrictions. This forced account sharers to either buy their own subscription or downgrade to a lower tier. It wasn't a price increase in the traditional sense, but it was certainly more money out of customer pockets.

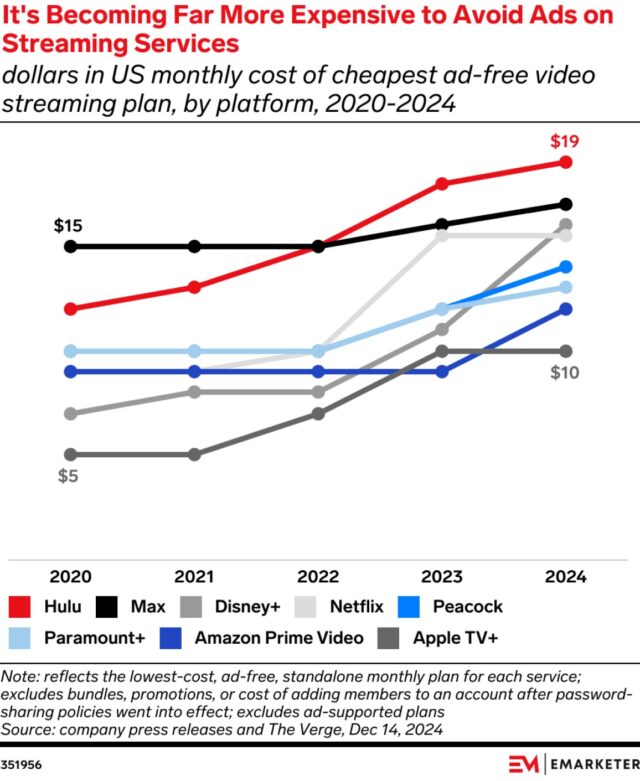

Ads were the other strategy. Disney+ introduced an ad-supported tier. Netflix expanded its ad tier. These services dangled "lower prices" but with the catch that you'd watch 4-5 minutes of ads per 30 minutes of content. That made them feel like the cable experience they were supposed to replace. But it captured price-sensitive customers without losing ad revenue from them.

These strategies worked. They sustained subscriber growth while raising prices and broadening monetization. They're exactly what you'd expect from a maturing industry. Cable did this too. Streaming companies just got to do it faster because the technology allowed it.

The Consolidation Problem Nobody Expected

When streaming launched, people celebrated the diversity. Instead of one cable company owning all the content, you had Netflix, Amazon Prime, Apple TV+, and others competing independently. More choice. More competition. Better prices.

Except the content side consolidated. Disney owns Disney+, Hulu, and ESPN+. It acquired Marvel, Pixar, and all of Twentieth Century Fox's entertainment assets. Warner Bros owns HBO Max and owns content from HBO, Warner Bros Studios, and DC Comics. Paramount owns Paramount+, CBS, and MTV. Amazon owns Prime Video and MGM. Netflix is independent but also the largest.

Three to five companies control most of the content Americans want to watch. When three companies control most of the supply, they don't need to compete aggressively on price. They can raise prices in coordination. They did exactly that in 2025.

Consumers felt this consolidation acutely. They couldn't just buy Netflix if they wanted the Marvel content, HBO's prestige shows, and Paramount's sports. They needed multiple subscriptions. The savings from cutting cable evaporated once you added up four or five streaming subscriptions and the associated price increases.

How Streaming Outpaced Food Inflation (and Why That Matters)

This is the stat that keeps economists up at night. Streaming price increases exceeded even food inflation—a category with real supply chain vulnerabilities, weather impacts, and commodity price swings.

Beef steak prices rose 17.8 percent. Coffee prices rose 18.7 percent to 28 percent depending on the type. These are agricultural products affected by drought, disease, labor availability, and feed costs. Food prices are supposed to be volatile. Consumer services like streaming are supposed to be more stable.

Instead, streaming outpaced them. This happened because streaming companies faced no real constraints. Their marginal costs are nearly zero. Adding another user to Netflix costs Netflix essentially nothing. The infrastructure exists. The content is already produced. The service already runs.

Food producers have real constraints. Raising cattle takes years. Growing coffee requires land and weather cooperation. Shipping costs real money. Disrupting any part of the chain increases costs. So food inflation reflects genuine economic pressures.

Streaming inflation reflects something different: market power and pricing strategy. Netflix can raise prices because Netflix faces no real competition for Netflix content. You can't get The Crown or Stranger Things anywhere else. They own the supply. In economics, ownership of unique supply is called monopolistic power.

When a company with monopolistic power raises prices, that's worth asking about. It's not responding to costs. It's extracting value from customers. The federal data suggests that's exactly what happened in streaming in 2025.

Streaming services account for 8% of monthly spending but have a disproportionate impact on inflation due to a 29% price increase. Estimated data.

Why 2024 Was Different: The Patience Phase

In 2024, streaming companies were patient. The 1.6 percent increase was modest. It reflected a different strategy: customer retention and market stabilization.

Streamers had just spent years in a brutal competition for content and subscribers. They'd bid up licensing costs for movies and TV shows. They'd spent billions on original content to attract subscribers. Some services were losing money per subscriber because they paid so much for content.

2024 was when the pendulum started swinging back. Companies cut costs. They canceled shows and movies that weren't performing. They stopped spending like they were trying to overthrow cable overnight. Instead, they acted like they'd already won and needed to optimize profits.

This shift took time. First, you make sure you have a stable subscriber base. You take modest price increases to test customer elasticity. You see how many people will tolerate higher prices without leaving. Then, once you understand your market, you push harder.

That testing happened in 2024. The pushing happened in 2025. The federal data reflects exactly this progression: from tentative 1.6 percent increases to aggressive 29 percent increases once companies understood customers would pay.

The Feature-Tier Strategy That's Coming in 2026

Based on how 2025 played out, streaming companies will get subtler about price increases in 2026. Instead of raising base prices, they'll introduce "premium" tiers. They'll charge extra for 4K resolution. They'll charge extra for simultaneous streams on multiple devices. They'll charge extra for early access to new content or ad-free viewing.

This strategy works because it's less obvious than a base price hike. Someone paying

Except as technology improves and everyone wants 4K, the pressure to upgrade increases. What started as optional becomes expected. Streaming companies learned this from cable, which perfected tiered pricing. They're now applying the same strategy to streaming.

Expect the average streaming bill to increase another 15-20 percent in 2026, but delivered through premium features rather than base price hikes. It'll work because it's less obvious than a headline price increase.

Bundling as the Industry's Response to Fatigue

Streaming companies recognized in 2025 that they'd pushed single-service pricing as far as it would go. Customer fatigue was setting in. Households were cutting services. The economic incentive to subscribe to five separate services was eroding. So companies started bundling.

Disney bundled Disney+, Hulu, and ESPN+ into a package deal with a small discount. It's cheaper to buy all three together than separately. This is a smart move. It locks customers in. If you want Disney+ and ESPN+, bundling with Hulu is a marginally small extra cost. Many customers who wouldn't have paid separately for Hulu now have it.

Apple bundled Apple TV+ with Apple Music and Apple News+. Paramount+ is bundling with Showtime. Amazon is bundling Prime Video with broader Prime membership. These bundling strategies serve a purpose: they make subscriptions feel cheaper (you're getting multiple services in one package) while actually collecting more money (customers who buy the bundle pay more than they would for individual services).

This trend will accelerate. By 2027, most casual consumers won't be buying individual streaming services. They'll be buying bundles. The bundles will become the primary unit of pricing. Within bundles, companies will compete on content and features. But the bundle price will be the main thing marketing to consumers.

Streaming companies are basically re-creating cable packages. Instead of cable, ESPN, and premium movie channels as separate tiers, you'll have bundles from Disney, Warner Bros, Paramount, and others. The form has changed. The function is identical.

The inflation rate for streaming services surged from 1.6% in 2024 to 29% in 2025, significantly outpacing the overall inflation rate. Estimated data for overall inflation in 2025.

What Users Really Think About the Price Hikes

Here's where federal data leaves off and anecdotes take over. Streaming users were genuinely angry about 2025's price increases. The social media response was visible and vocal. Subreddits dedicated to streaming complained constantly.

But the federal data tells you the final story: people paid the higher prices. They complained and paid. They threatened to cancel and mostly didn't. Some households did cut services. Some people shared accounts or used password cracking tools to get free access. But the aggregate data shows that the price increases stuck.

This is the market working as economic theory predicts. When demand is inelastic—meaning consumers need the product and don't have good alternatives—companies can raise prices without losing significant volume. Netflix originals can't be watched on Disney+. Disney content can't be watched on HBO Max. Each service owns its exclusive content. That exclusivity makes demand inelastic.

So companies raised prices. Most customers paid. Some left. The math still worked. This will likely continue until something changes: either competition increases, services merge, or consumer budgets reach a breaking point.

The Investor Pressure That Drove the Increases

Why were streaming companies so aggressive with price increases in 2025? Because their investors demanded it.

For years, streaming companies chased growth. Subscriber numbers were the metric that mattered. You raised $5 billion, spent it on content, and booked those costs against revenues to show growth. Wall Street rewarded growth metrics, even at a loss.

This changed around 2023-2024. Investors realized that streaming companies would never show Netflix-like profitability if they kept spending like growth startups. They demanded profitability. They wanted earnings per share, free cash flow, and margin expansion. They wanted sustainable business models.

Streaming companies responded by cutting costs and raising prices. Cut content spending. Cut unnecessary staff. Raise prices on existing customers to boost margins. It worked. Streaming services reported much better profitability metrics in 2024 and 2025. Their stock prices rose. Investors were pleased.

This investor pressure explains why all services raised prices simultaneously. They weren't responding to different cost structures or market positions. They were all responding to the same investor demand for profitability. Raising prices is the fastest path to improved profit margins when you already have a large subscriber base.

This dynamic will likely continue. Investors won't relax their profitability demands. Streaming companies will keep looking for ways to increase margins. Price increases, premium tiers, and bundling strategies will continue.

Comparing to Cable's Rise and Fall

Cable companies spent decades raising prices. They'd raise subscriber fees, raise channel packages, raise equipment fees, and claim inflation required it. Customers grumbled but paid because they had no alternative. Sports lived on cable. News lived on cable. Shows that mattered were on cable.

Then streaming showed up. Younger people dropped cable. Cord-cutting became a verb. Cable's subscriber base shrank year after year. Eventually, cable's business model broke. Companies like Charter and Comcast are now trying to figure out how to make money when their subscriber base has declined by tens of millions.

Streaming companies might be repeating this pattern. They're raising prices aggressively, showing less restraint as they realize customers don't have alternatives. But unlike cable, streaming faces an open internet. Competition is theoretically infinite. A new company can launch a streaming service tomorrow. A foreign company can enter the US market. Technology can change how content is distributed.

Cable was protected by infrastructure. You couldn't build competing cable networks without massive capital. Streaming has no such barrier. The capital requirement is much lower. Yet the consolidation is real. Five companies control most American streaming content. That's less diverse than cable was at its peak, but feels more competitive because the interfaces are better and the content is on-demand.

Streaming companies might have overestimated their pricing power relative to cable's actual leverage. Cable was the only way to get content. Streaming is multiple ways to get different content. The comparison isn't exact. But the pricing aggressiveness of 2025 suggests streaming companies think they have cable-like leverage.

They might be wrong. Technology moves fast. A new entrant could disrupt streaming the way Netflix disrupted cable. Artificial intelligence could make content production cheaper, lowering licensing costs. Government regulation could break up content-distribution combinations. Lots could change.

But based on 2025's data, streaming companies are pricing like they believe they're permanent. The federal data tells you what they actually do when they believe that.

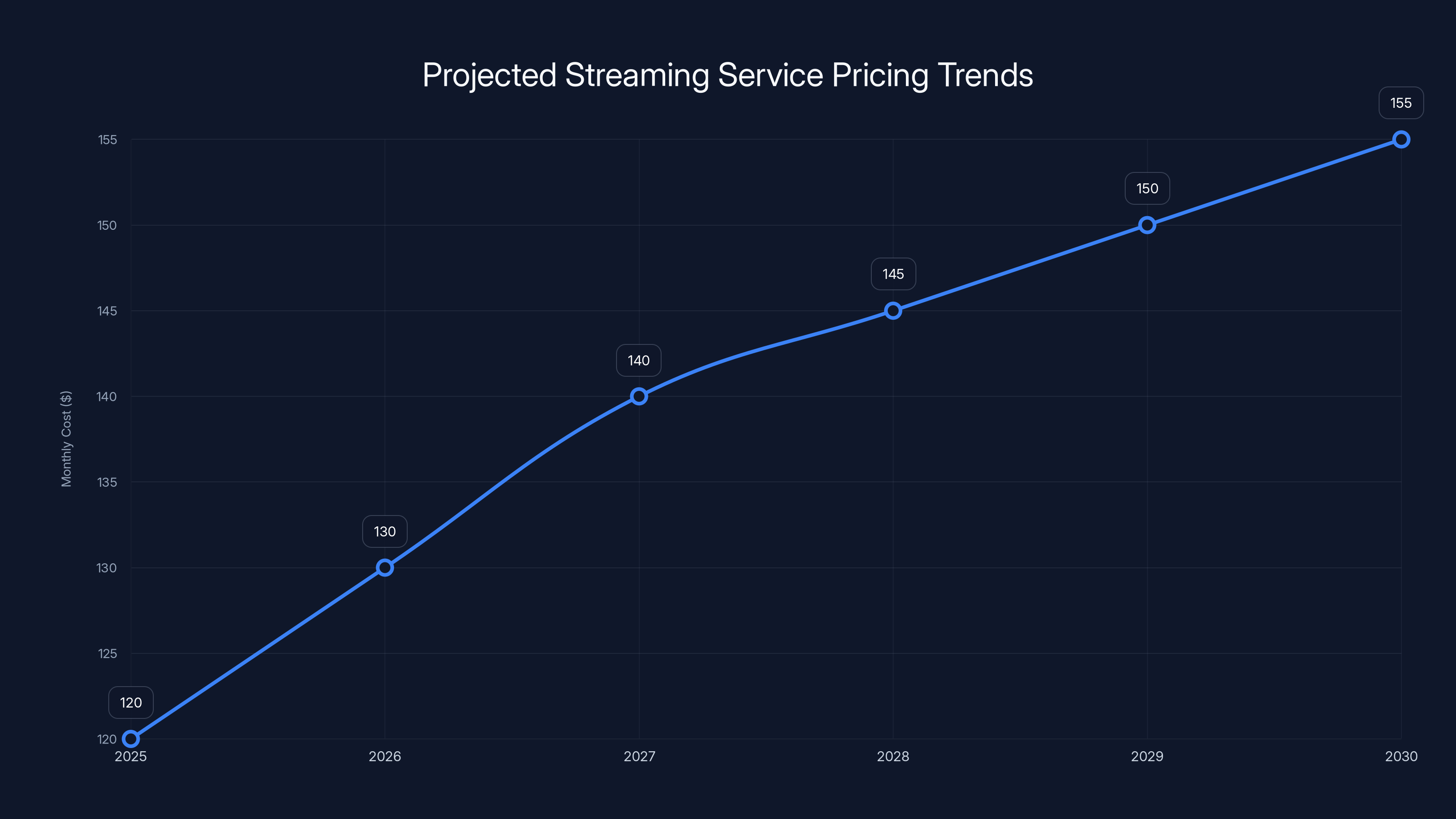

Estimated data suggests streaming service prices will gradually increase, stabilizing above 2025 levels by 2030. This reflects potential market consolidation and advanced pricing strategies.

The Broader Economic Question: What Does This Mean for Inflation?

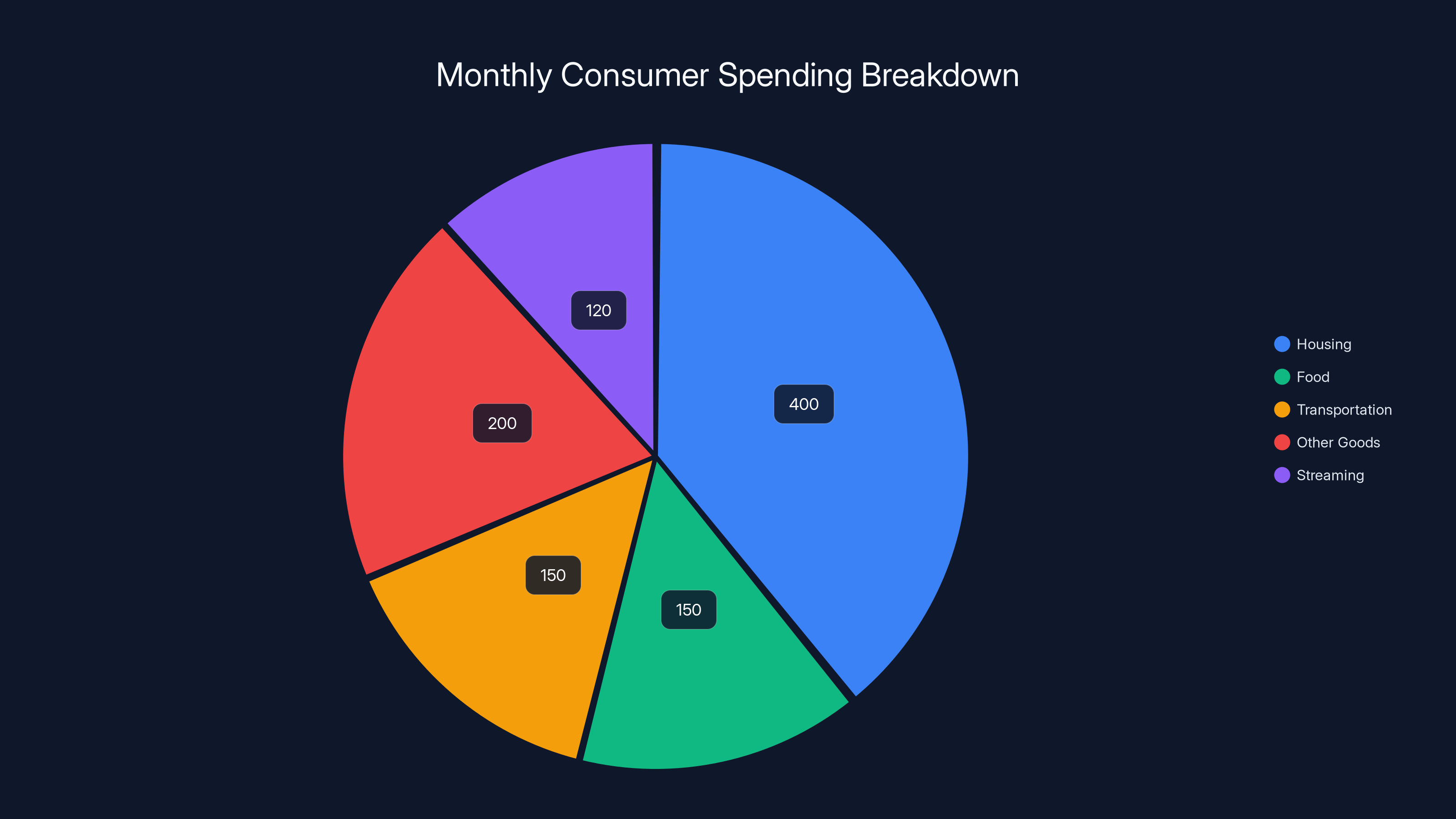

Streaming subscriptions are a small portion of overall consumer spending. If you spend

But streaming's 29 percent inflation drags the overall inflation index up. If you're calculating inflation across all categories, streaming's weight in the calculation means it contributes more to overall inflation than if streaming prices had risen 2.7 percent like everything else.

Federal Reserve economists and the Bureau of Labor Statistics track this. If a major category shows anomalous inflation, they examine whether it's driven by real economic forces (like food inflation driven by crop failures) or market power (like streaming inflation driven by pricing strategy).

Streaming inflation looks like market power. It's not driven by costs. The Federal Reserve cares about this distinction because market power inflation is different from demand-driven inflation. Demand-driven inflation—too many dollars chasing too few goods—requires interest rate hikes to cool down. Market power inflation requires either regulation, competition, or antitrust action to address.

The fact that streaming inflation is this high might influence Fed policy, regulation, or antitrust actions against streaming companies. It certainly influences how economists think about subscription-based services as a growth area in the American economy.

Expert Predictions for 2026 and Beyond

Industry analysts expect streaming prices to continue increasing in 2026, but with more subtlety than 2025. Instead of headline price hikes, expect premium features, ad-tier adjustments, and bundling strategies.

We'll likely see more consolidation. Smaller streaming services will merge, go out of business, or get acquired by larger companies. The capital requirements to produce original content at scale are enormous. Dropout can't compete with Netflix in content production budget. So Dropout gets acquired or finds a niche. The economics push toward consolidation.

We'll also likely see more international pricing strategies. Streaming companies will charge different prices in different markets. This is already happening with Netflix, which prices differently in the US, UK, India, and other markets. As companies optimize globally, some markets will see faster price increases than others.

We might see pressure on licensing costs. If streaming companies own content (like Netflix with its originals), they set their own costs. But if they license content from studios (like Apple TV+ or Netflix licensing theatrical films), they're subject to studio pricing. Studios might push for higher licensing fees, which would drive streaming price increases.

Finally, we'll see whether government regulators notice streaming price inflation. The Federal Trade Commission has been aggressive about competition issues. The Justice Department has blocked media mergers in the past. If streaming consolidation continues and prices keep rising, antitrust action becomes more possible. It would be slow—government antitrust cases take years—but it would create legal risk for streaming companies.

The Subscriber Fatigue Factor

Subscriber fatigue is real. It's not an economic theory. It's people feeling genuinely tired of managing multiple subscriptions, dealing with different interfaces, and paying cumulative bills that approach or exceed cable.

Surveys consistently show that Americans want fewer subscriptions but better content. They're willing to pay more per service if it means they can drop three other services. This preference is rational. Managing five subscriptions with different billing dates, interfaces, and password requirements is annoying. Paying $120 a month is expensive. Both together create fatigue.

Streaming companies recognize this. Bundling addresses it by reducing the number of subscriptions while increasing the per-subscription value. But bundling also locks customers in. Once you subscribe to a bundle, switching costs increase. You need to decide whether the bundle is worth keeping, even if you're only using two of the three services. That inertia benefits streaming companies.

In 2026 and beyond, expect subscriber fatigue to be the primary driver of strategy. Not content production (that will be scaled back), not interface design (that's mature), not global expansion (that's already happening). Instead: reducing the number of subscriptions consumers need to buy while increasing the value per subscription.

This pushes toward consolidation, bundling, and tiering. It might look like competition to newcomers, but it's the opposite. It's optimization toward a mature, consolidated market structure where a few major bundles serve most customers.

What Consumers Can Actually Do About Rising Prices

Your options are real but limited. You can cancel subscriptions you don't use. Most households have at least one service they pay for but barely watch. Cutting that saves money immediately. You can share accounts within your household (most services allow this; password sharing outside your household is against terms of service after 2024's crackdowns).

You can rotate subscriptions. Pay for Netflix for two months while binge-watching everything you want, then cancel and rotate to Disney+ for two months. This reduces monthly costs but increases friction and delays your access to new content. Some people do this; most don't.

You can negotiate with customer service. If you threaten to cancel, representatives have discretion to offer discounts or reduced pricing. It works sometimes. It works better if you've been a long-term customer and if you actually seem like you'll cancel.

You can buy gift cards or use promotional pricing. Companies offer reduced rates to new subscribers. If you rotate subscriptions, you're always a "new" customer to the service you're switching to, eligible for promotional rates.

You can use ad-supported tiers. Disney+ and Netflix both offer cheaper, ad-supported versions of their services. If you tolerate ads, the savings are substantial.

None of these options are great. They all involve friction or compromise. The reality is that if you want access to the full breadth of streaming content, you're going to pay more in 2026 than you paid in 2024. The federal data confirms this is happening. Individual consumer choices can't change industry-wide trends, only optimize personal spending against those trends.

The Long-Term Sustainability Question

Here's the question nobody can answer with certainty: is this pricing sustainable?

In the short term, yes. Streaming companies raised prices in 2025 and kept most of their customers. Investor expectations for profitability were met. The economics worked. For 2026, it'll probably work again unless something changes dramatically.

But long term? It's harder to predict. At some point, price increases collide with customer budgets. When households are paying $150 a month for streaming and the service quality hasn't improved, and they're seeing ads and not seeing shows they want, something has to give. People will cut services. Or they'll go back to piracy. Or they'll settle for less content. Or new competition will emerge.

Streaming companies are banking on one of a few scenarios: either prices stabilize at current levels and customer bases stop growing but remain stable, or content production becomes cheaper through technology and automation, or new revenue streams (like ad sales or premium features) offset subscriber sensitivity to pricing, or the market consolidates further and prices stabilize at higher levels but with fewer, more expensive services.

One thing that seems unlikely: prices go back down. Streaming companies have learned they can raise prices and keep customers. That lesson doesn't get unlearned. Even if growth slows or competition increases, pricing discipline is easier to maintain when you know the customer base will tolerate increases.

So expect pricing to stabilize somewhere above 2025 levels but with more sophistication about HOW prices increase. Bundling, tiering, premium features, and dynamic pricing based on viewing habits are all more likely than simple headline price hikes.

Government and Regulatory Implications

The Federal Trade Commission is watching. When a data set shows clear evidence of market power being exercised—29 percent price increases in a category while overall inflation is 2.7 percent—regulators notice. It's not illegal to raise prices. But it's evidence of market power. And market power that results in anti-competitive behavior can be actionable.

The FTC has been aggressive on competition issues. They've blocked Microsoft-Activision mergers. They've investigated Amazon's pricing practices. They've looked at Facebook and Google's market dominance. Streaming consolidation and aggressive pricing might eventually get regulatory attention.

Antitrust cases are slow. They take years to litigate. By the time regulatory action happens, streaming markets might have evolved into something different. But the FTC has long memories. If streaming companies keep raising prices and consolidating, enforcement action becomes more likely.

You'll also see increased scrutiny of exclusive content deals. If Disney+ has exclusive Disney content, Netflix has exclusive Netflix originals, and HBO Max has exclusive Warner content, that's vertical integration and potential anti-competitive behavior. Regulators have tools to address this. They might not use them soon. But the risk increases as price increases persist.

State-level regulation is another possibility. Some states are more aggressive on consumer protection than the federal government. A state attorney general could sue over unfair pricing or bundling practices. It would be a smaller action but could set precedents.

Long story short: streaming companies probably overestimate how much pricing power they have. The federal data revealing 29 percent price increases while overall inflation is 2.7 percent is exactly the kind of evidence that gets regulatory attention. Companies that show that kind of pricing power face more regulatory scrutiny. This dynamic will likely unfold over 2026-2027.

The Content Question: Is Streaming Worth the Price?

This is the personal calculation each household makes. Is the content on these services worth the price you're paying?

For many people, the answer is yes. Netflix has shows and movies nowhere else can touch. If you want quality prestige television, Netflix has it. Disney+ has Marvel and Star Wars content. HBO Max has HBO's decades of quality television. Apple TV+ has some originals worth watching. Prime Video has volume and also costs less because it's bundled with Prime membership.

But the average person probably doesn't want all of them. They want maybe two or three. And they're paying for five because they like having options and because they don't want to miss new releases. That's the market dynamic streaming companies count on.

What's changing is that the content production costs aren't matching the price increases. Netflix is cutting content production budgets while raising prices. Disney+ is doing the same. This won't be immediately visible, but over time, it means fewer new shows, older content becoming more prominent, and the quality/price ratio declining.

Consumers who realize this will cut services. Streaming companies' response will be bundling—make it cheaper to keep multiple services together. But the underlying reality is that streaming is maturing. The exceptional content that justified early subscriptions is becoming less exceptional. The prices are becoming less exceptional in the other direction.

By 2027 or 2028, expect a significant reckoning. Streaming price/value propositions will be clearer. Some services will fail or consolidate. Customer bases will stabilize. The exuberant expansion of 2015-2024 will be replaced by mature, profitable oligopoly.

The 29 percent price increase in 2025 is what that reckoning looks like in its early stages.

FAQ

What is the streaming price inflation data from 2025?

The US Bureau of Labor Statistics released data in January 2026 showing that subscription and rental access to video streaming services and video games increased 29 percent from December 2024 to December 2025. This unadjusted inflation represents what consumers actually paid, making it nearly 11 times higher than the overall inflation rate of 2.7 percent for that year. The data is drawn from the Consumer Price Index for All Urban Consumers (CPI-U), which represents over 90 percent of the US population.

How does the 29% streaming price increase compare to other inflation categories?

Streaming prices increased far more aggressively than almost any other category in the American economy in 2025. For context, cable television saw only 4.9 percent inflation. Even volatile food categories like instant coffee (28 percent), roasted coffee (18.7 percent), and uncooked beef steaks (17.8 percent) saw comparable or lower inflation. This positioning streaming as the most aggressively priced category tracked by federal statistics, suggesting market power rather than cost-driven inflation.

Why did streaming companies raise prices so aggressively in 2025?

Streaming companies raised prices for several interconnected reasons: achieving profitability demanded by investors, capitalizing on their market dominance as the primary way Americans watch television, responding to password-sharing crackdowns that reduced their revenue from existing subscribers, and implementing ads-supported tiers that monetize price-sensitive customers differently. Additionally, the consolidation of content ownership among five major companies reduced competition, allowing coordinated pricing behavior without explicit coordination being necessary.

Did customers actually stop using streaming services when prices increased?

Federal data suggests that most customers paid the higher prices. While some households did cancel services and others shared passwords or used other workarounds, the aggregate subscription numbers held relatively steady. This is textbook economic behavior when demand is inelastic—meaning customers need the product and don't have good alternatives. The exclusive content ownership (Netflix owns Netflix originals, Disney owns Disney+ content) creates this inelasticity, giving companies pricing power.

What pricing strategies are streaming companies likely to use in 2026?

Instead of direct price increases like those in 2025, streaming companies will likely employ subtler strategies: introducing premium tiers charging extra for 4K resolution, simultaneous device streams, or early content access; bundling multiple services together at a package price; launching ad-supported tiers at lower price points; and consolidating through acquisitions of smaller services. These strategies are less obviously aggressive than headline price increases while still extracting more revenue from existing customer bases.

What can consumers do about rising streaming prices?

Consumers have limited but real options: canceling subscriptions they barely use, rotating subscriptions monthly to always be a "new" customer eligible for promotional pricing, negotiating directly with customer service by threatening cancellation, using ad-supported tiers to reduce costs, sharing accounts within their household, and regularly reassessing whether their streaming bundle justifies the monthly cost. However, none of these options are as simple as the pricing transparency streaming customers enjoyed in the service's early years.

Will streaming prices continue increasing in 2026 and beyond?

Industry analysis suggests prices will continue increasing, though perhaps more subtly than the direct 2025 increases. Investors demand profitability. Streaming companies have demonstrated customers will pay higher prices. The barriers to entry are low enough that new competitors could theoretically emerge, but consolidation has proceeded far enough that breaking incumbent market position is difficult. Barring regulatory intervention or dramatic technological change, pricing discipline will likely persist.

Is streaming consolidation driving these price increases?

Consolidation is a major factor. Five companies now control most streaming content Americans want to watch: Netflix, Disney (operating Disney+, Hulu, and ESPN+), Warner Bros (HBO Max), Amazon (Prime Video), and Paramount. When competition is limited to a few large players with differentiated content offerings, those companies can coordinate price increases without explicit coordination, each raising prices knowing competitors will follow. This oligopolistic price leadership explains why essentially every major service raised prices in 2025.

How does streaming price inflation compare to historical cable price inflation?

Streaming companies are repeating cable's pricing playbook from the 1990s and 2000s, when cable companies regularly raised prices while claiming inflation required it. The difference is that streaming faced no infrastructure barriers to competition, yet consolidation happened anyway. Cable was protected by network effects and infrastructure investment. Streaming has lower barriers to entry but higher consolidation. The pricing aggressiveness is similar, but streaming companies might have overestimated their structural pricing power relative to cable's actual leverage.

Could government regulation address streaming price increases?

Possible but not imminent. The Federal Trade Commission has demonstrated aggressive enforcement on competition issues and could investigate streaming consolidation or exclusive content practices for anti-competitive behavior. Antitrust cases move slowly (often taking years to litigate), but the 29 percent price increase versus 2.7 percent overall inflation is exactly the kind of evidence that attracts regulatory attention. State attorneys general could pursue consumer protection cases more quickly. However, regulation is more likely to reshape market structure than directly control pricing.

What does this data mean for broader economic inflation?

Streaming inflation is significant for inflation measurement because it shows an example of market power inflation rather than demand-driven inflation. Demand inflation means too many dollars chasing too few goods, typically addressed through higher interest rates. Market power inflation means dominant firms raising prices due to leverage over customers. These require different policy responses. The Federal Reserve and other economic policymakers care about this distinction when setting monetary policy. Streaming's 29 percent inflation while overall inflation is 2.7 percent is a notable anomaly suggesting market power rather than broad-based economic pressures.

Conclusion

The federal data from the Bureau of Labor Statistics tells a clear story about 2025's streaming economy. Prices didn't just go up. They skyrocketed. From 1.6 percent inflation in 2024 to 29 percent in 2025 represents a fundamental shift in how streaming companies view their market position.

Streaming started as a disruptor, undercutting cable through cheaper pricing and better convenience. Streaming became the dominant way Americans watch television. Once you've reached dominance, you stop competing on price. You start extracting value from existing customers.

The 29 percent increase is what value extraction looks like at scale. It's ten times faster than overall inflation. It exceeds food inflation driven by agricultural volatility. It's concentrated at the end of the year when customers are distracted. It's coordinated across multiple companies without needing explicit coordination because they all face the same investor pressure for profitability.

Consumers paid these prices. Some complained. Some left. Most paid. The economics worked. Streaming companies will repeat this playbook in 2026, but with more sophistication about HOW they raise prices. Premium tiers, bundling, and feature-based pricing will be less obvious than headline price increases but will achieve similar revenue extraction.

The long-term question is whether this pricing is sustainable. At some point, customers' entertainment budgets reach a limit. When a household is paying $150 monthly for streaming and considering canceling services or switching back to piracy, something breaks. We haven't reached that point yet. But the 29 percent increase in 2025 suggests we're heading toward it.

Streaming companies are pricing like they believe they're permanent, dominant utilities. Maybe they are. Or maybe they're repeating cable's mistake, which was assuming its market position was unshakeable until consumers decided it wasn't. The federal data tells us what happened in 2025. The next few years will determine whether this pricing strategy was smart or overconfident.

Key Takeaways

- Streaming subscription prices jumped 29% from December 2024 to December 2025, according to federal Bureau of Labor Statistics data

- This inflation rate was nearly 11 times faster than overall US inflation of 2.7%, and exceeded even volatile food categories

- All major streaming services including Netflix, Disney+, HBO Max, and Apple TV+ raised prices simultaneously, indicating market consolidation

- Households subscribing to five major streaming services now pay $95-150 monthly, approaching traditional cable pricing levels

- Federal data suggests streaming companies exercised market power through coordinated price increases rather than cost-driven inflation

Related Articles

- Grok AI Regulation: Elon Musk vs UK Government [2025]

- Best Smart Locks [2025]: Complete Testing Guide & Reviews

- AI Models Are Cracking High-Level Math Problems: Here's What's Happening [2025]

- Anthropic's Cowork: Claude's Agentic AI for Non-Coders [2025]

- WP Engine Acquires Big Bite: WordPress Consolidation Reshapes Enterprise Publishing [2025]

- Google Trends Explore Gets Gemini AI: What Changed [2025]