![The Great Myth of the Liquidation Preference: Why It Matters Less Than You Think [2025]](https://tryrunable.com/blog/the-great-myth-of-the-liquidation-preference-why-it-matters-/image-1-1772379266869.jpg)

Introduction

Last month at a startup pitch event, I overheard a conversation that many founders have had at one point or another. "I know liquidation preference is a big deal, but I'm not sure exactly how it impacts our fundraising." It's a common concern, especially for those new to venture capital. Liquidation preferences can seem intimidating, but the reality is more nuanced. Yes, they matter—just not in every scenario you might expect.

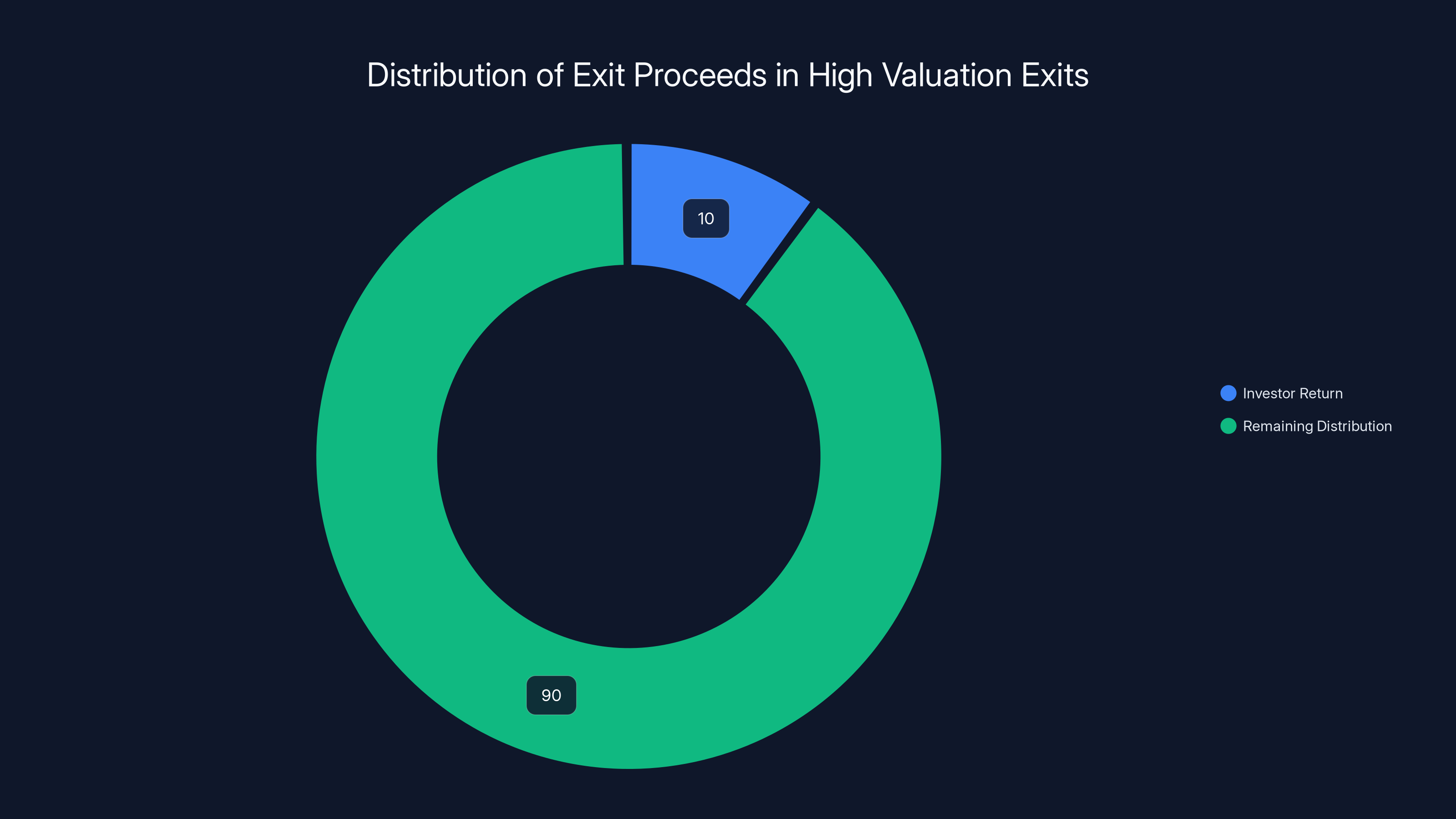

In successful exits, such as a

TL; DR

- Liquidation preferences protect investors by ensuring they recoup their investment before others in a liquidation event, as explained in Investopedia's guide on liquidation preferences.

- Scenarios like early exits or distressed sales are where these preferences most significantly impact outcomes.

- Common agreements include 1x non-participating preferences, but variations exist with complex implications, as noted in Kruze Consulting's analysis.

- For successful, growing companies, liquidation preferences often don't affect the founders or employees.

- Understanding your cap table and terms is crucial for founders when negotiating with VCs.

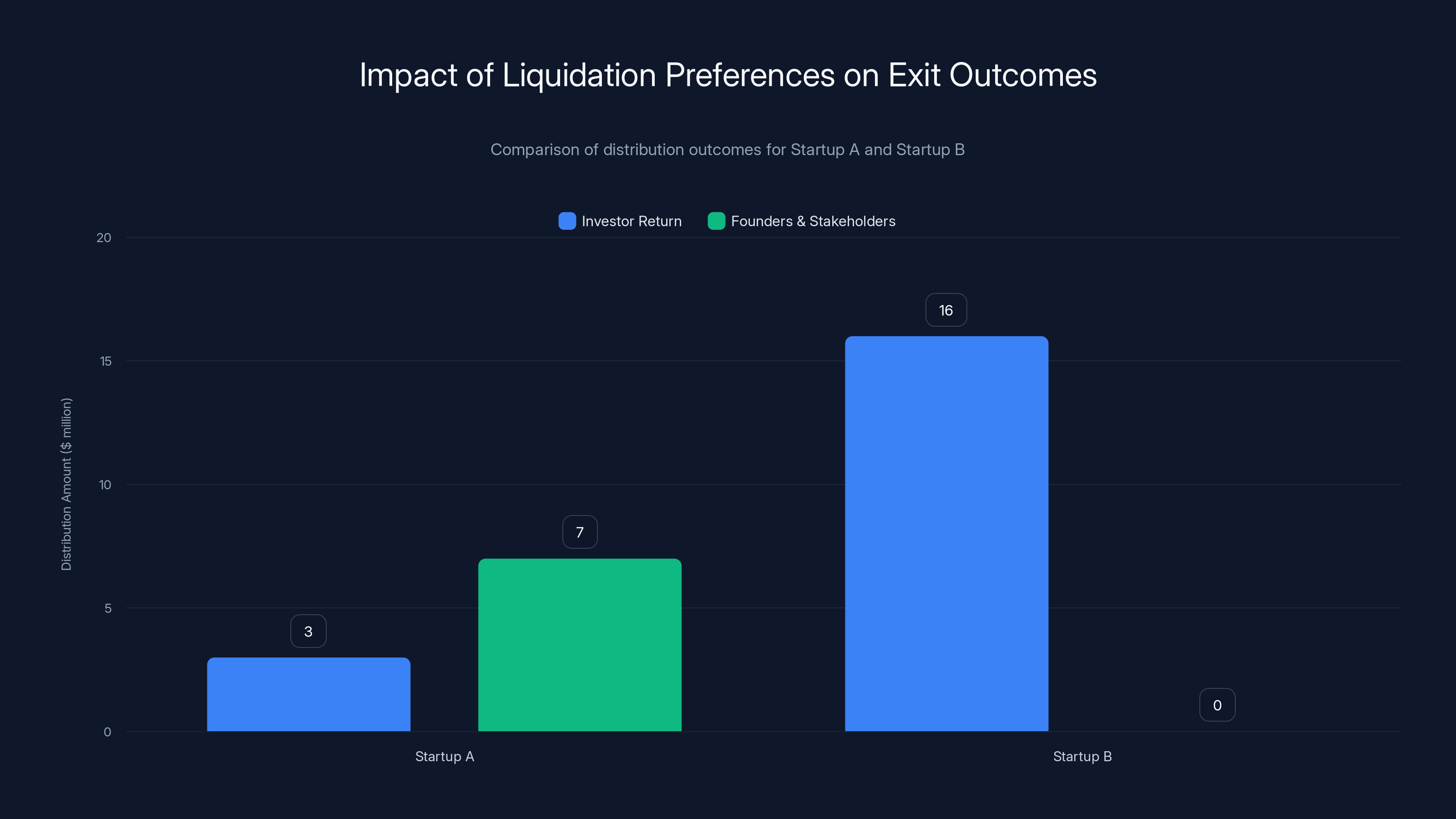

Startup A's investors received their initial

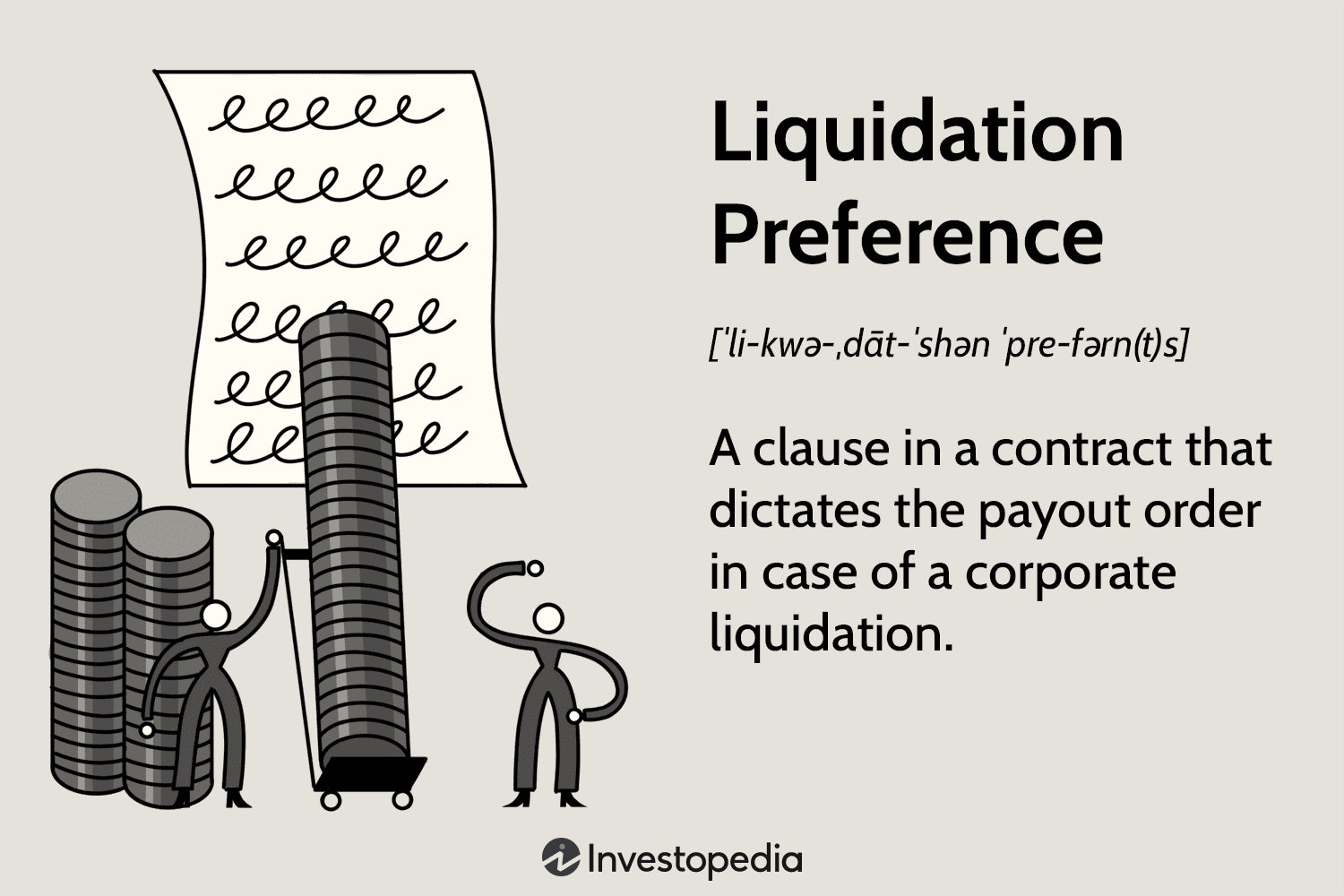

What Are Liquidation Preferences?

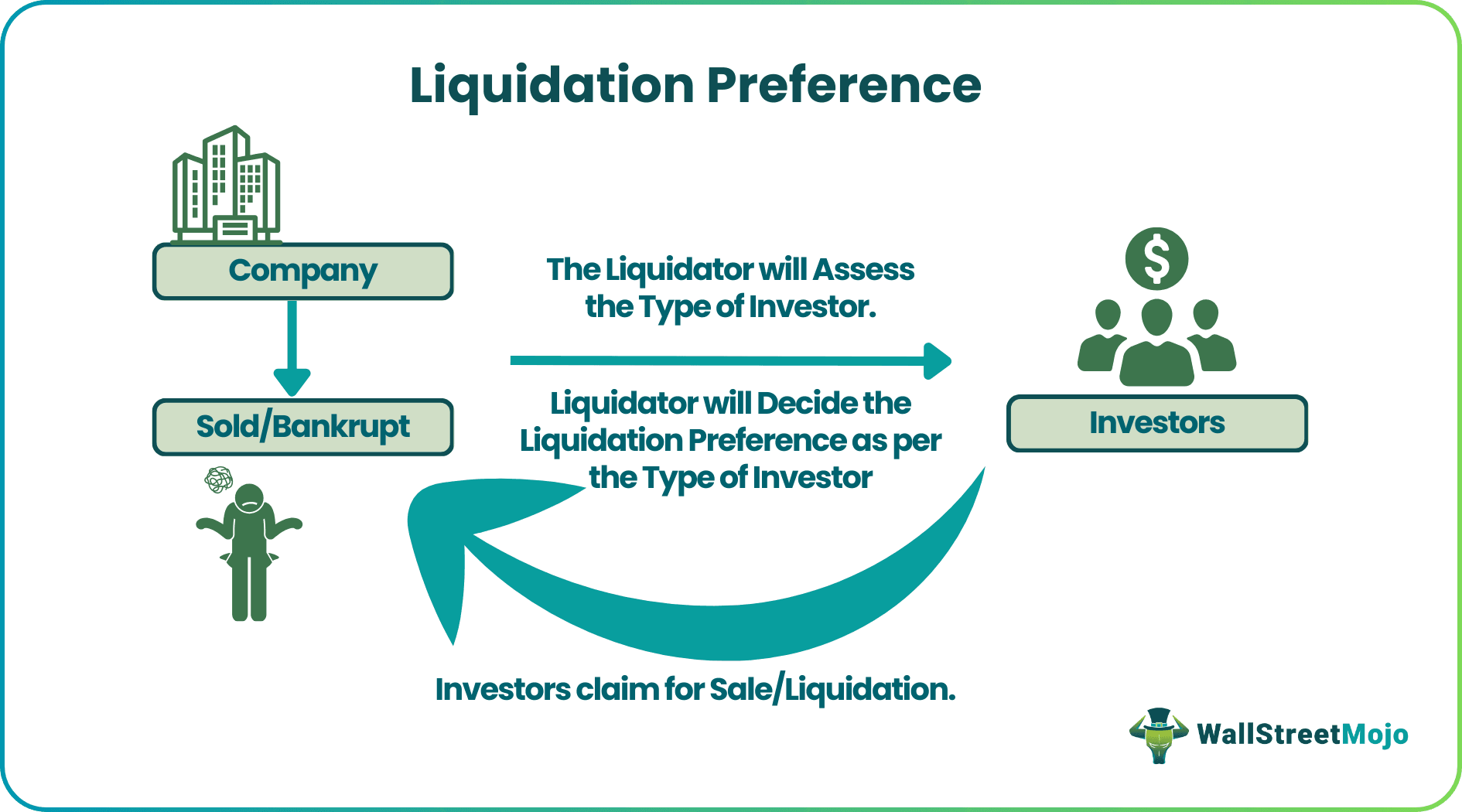

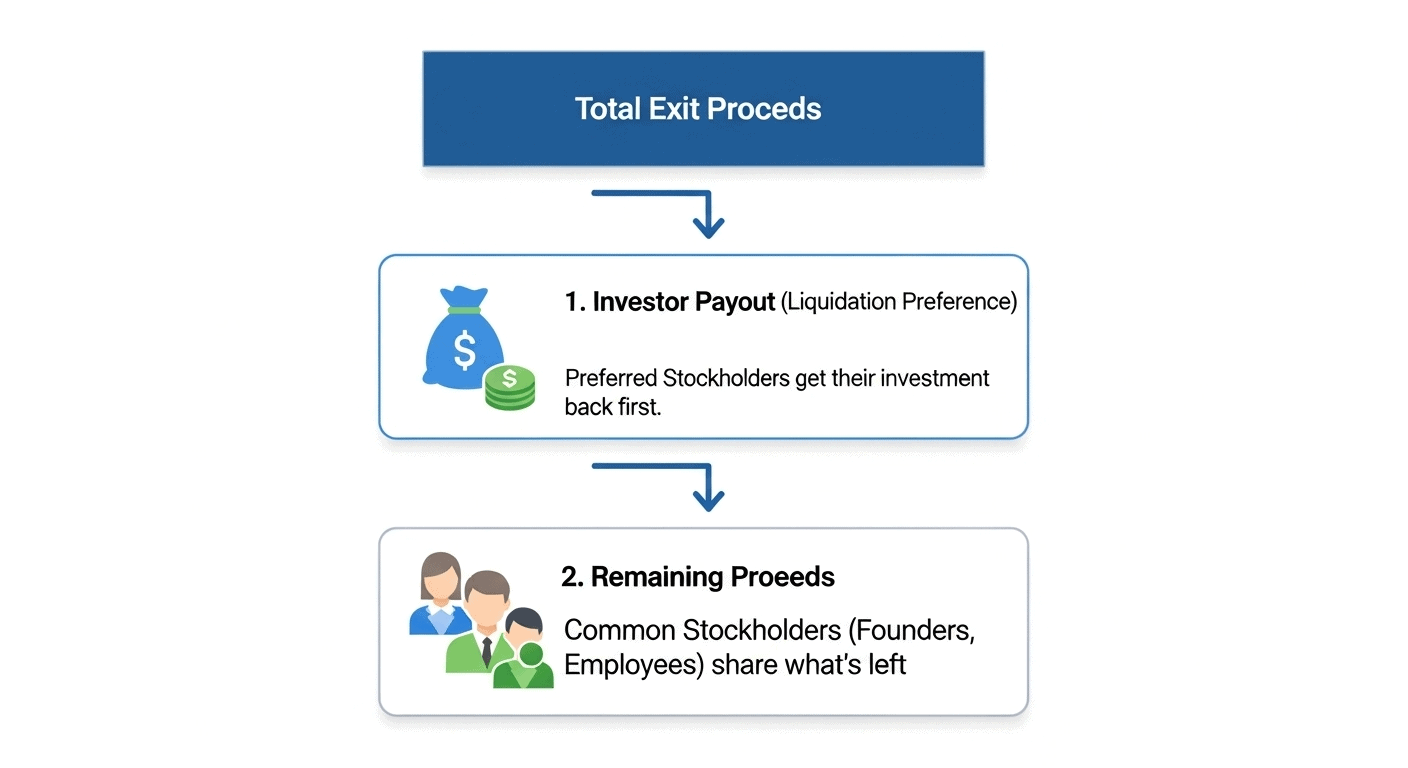

Before diving into when and why liquidation preferences matter, let's break down what they are. In venture capital, a liquidation preference is a term used to define the pecking order of payout in the event of a liquidation such as a sale, merger, or bankruptcy. It specifies that investors get their money back—often with interest—before anyone else sees a dime.

Key Components of Liquidation Preferences

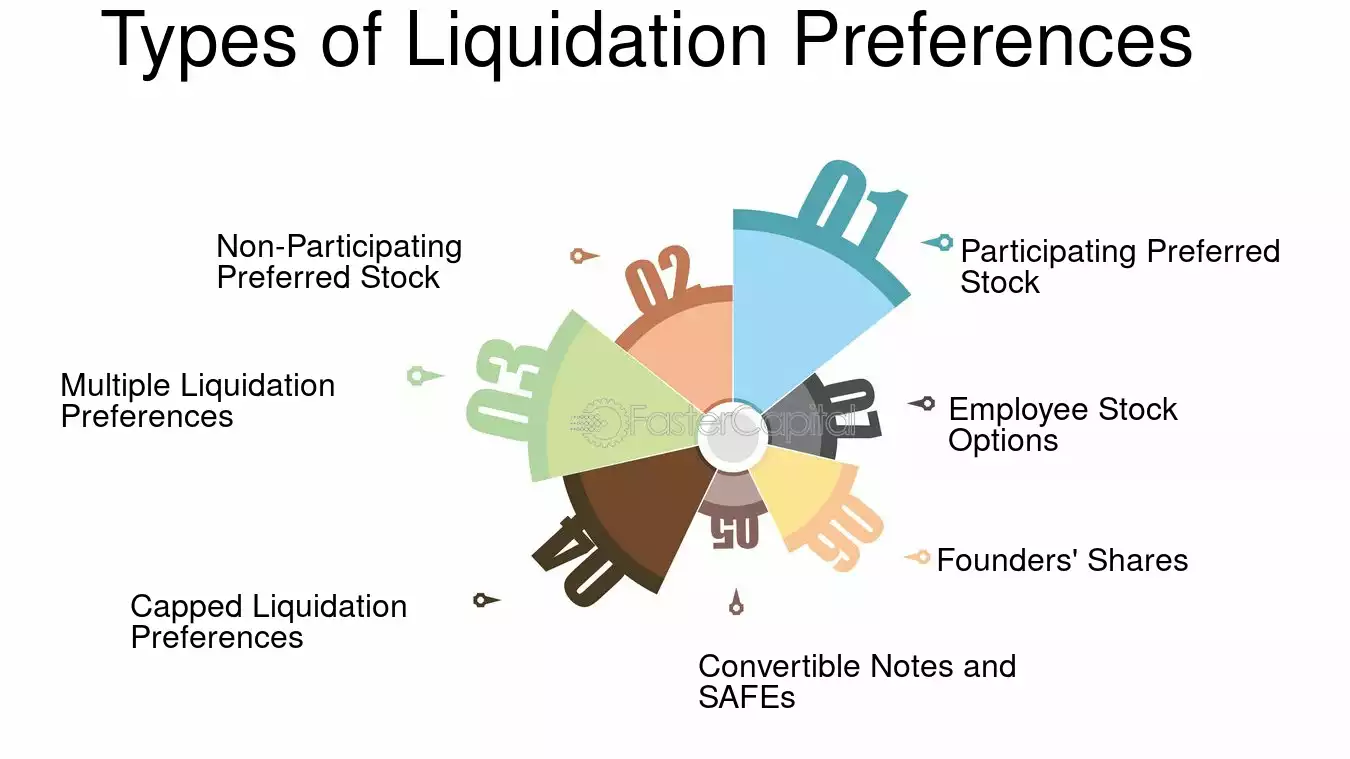

There are a few key terms to understand when it comes to liquidation preferences:

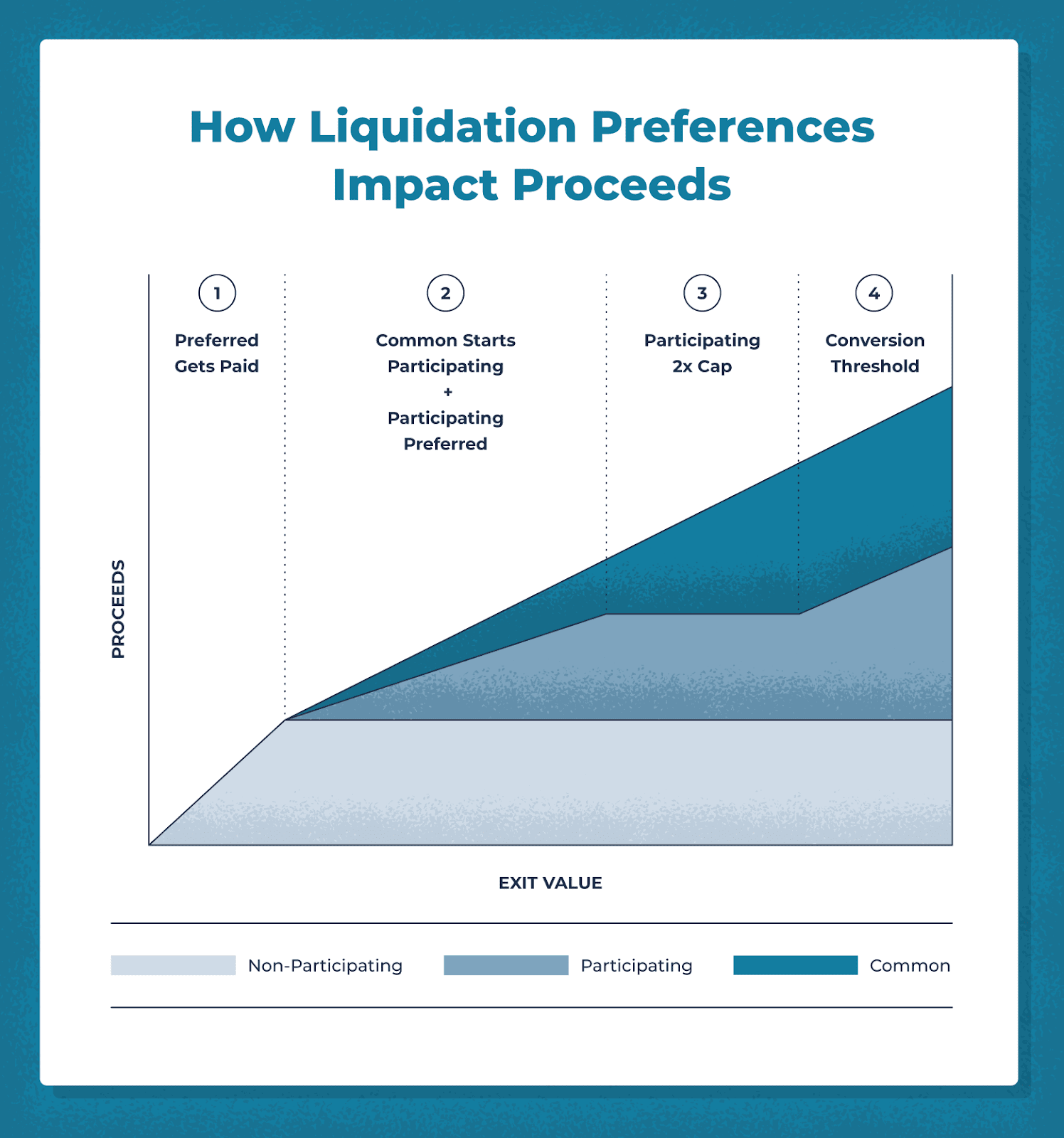

- Multiplier: This is typically expressed as "1x," "2x," etc., indicating how many times the initial investment needs to be returned before any other payouts.

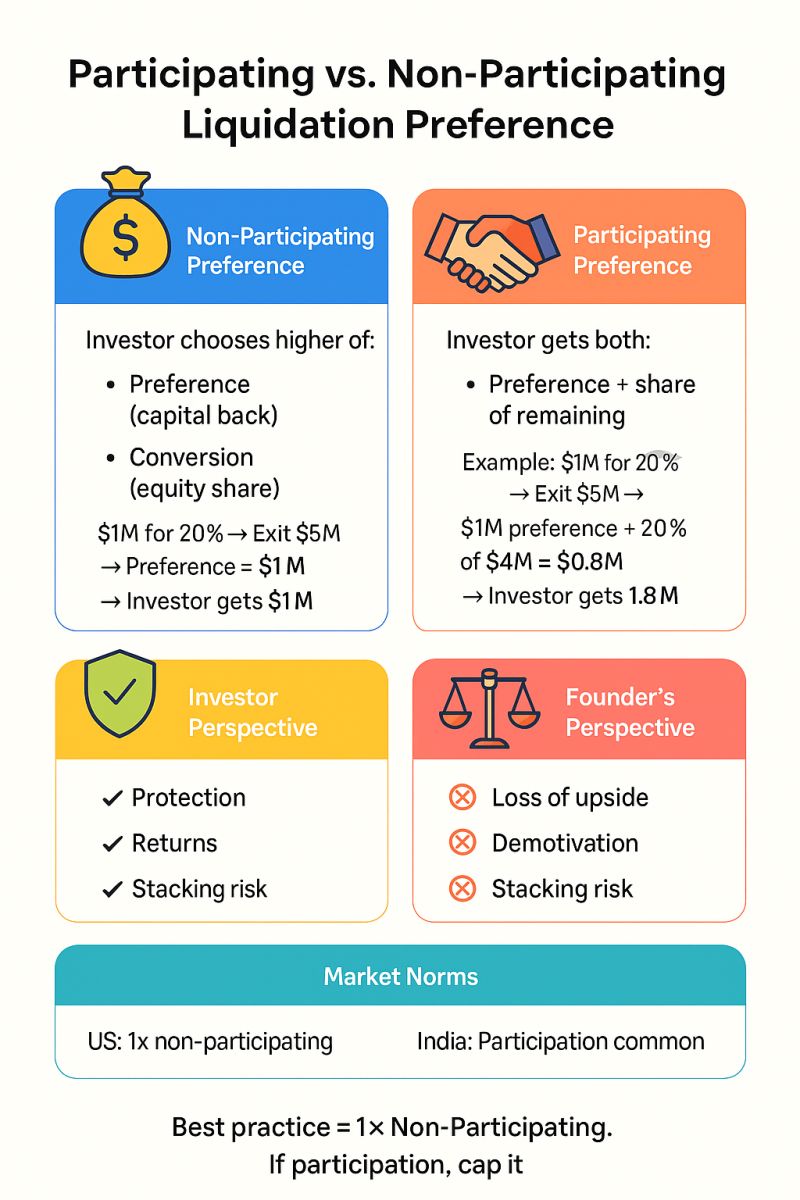

- Participating vs. Non-Participating: Non-participating preferences mean investors receive their preference and stop there. Participating preferences allow investors to receive their preference and then share in the remaining proceeds with common shareholders.

- Capped vs. Uncapped: A cap limits how much an investor can make in a liquidation event.

Common Scenarios Where Liquidation Preferences Matter

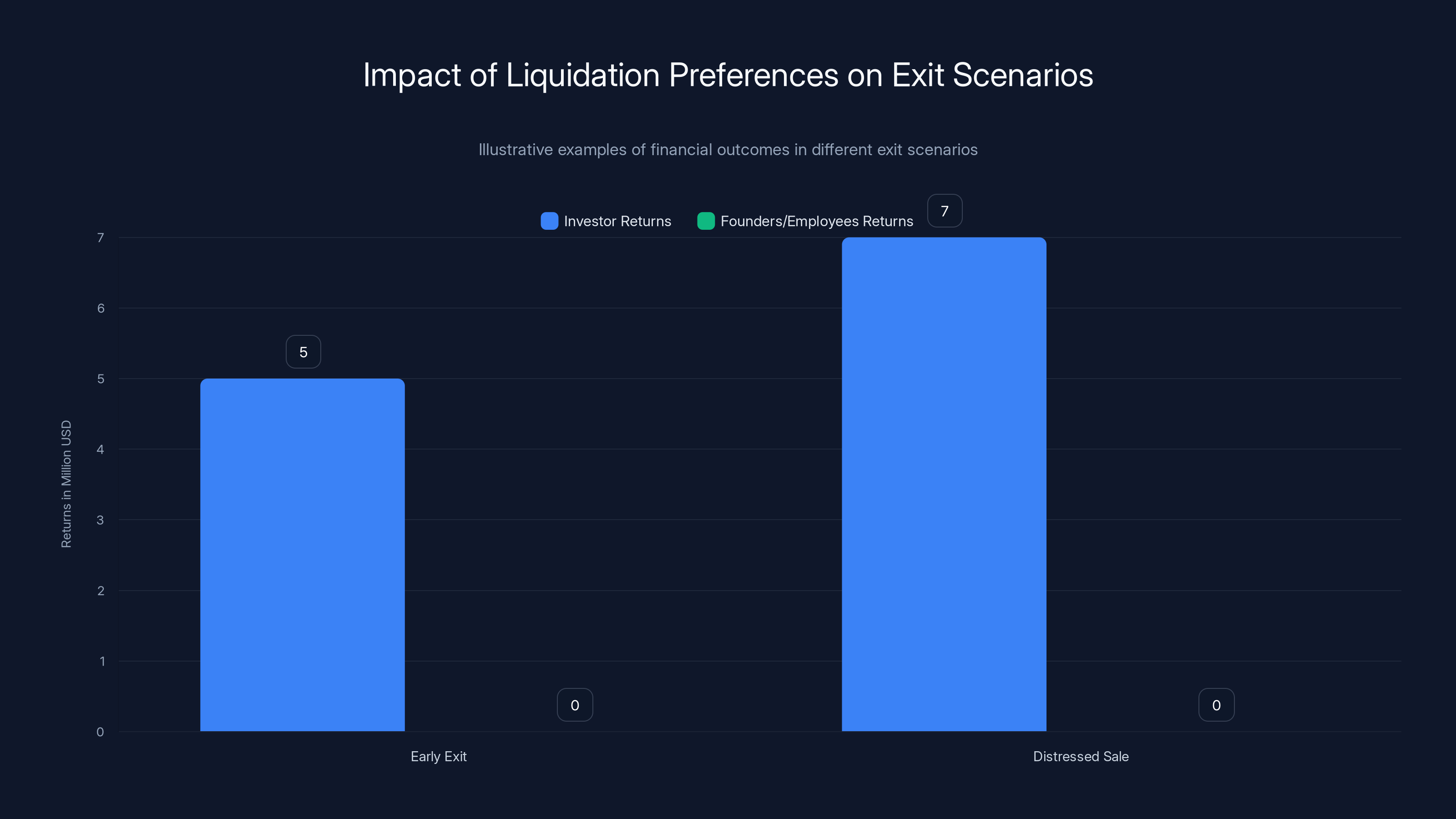

Early Exits

Imagine a startup that raised

Distressed Sales

In a situation where a company is sold for less than the amount raised, liquidation preferences ensure that investors receive at least some return. For instance, if a company raised

In early exits, investors can claim the entire sale value due to liquidation preferences, leaving nothing for founders. In distressed sales, investors recover funds up to the sale value, again leaving no proceeds for others.

Scenarios Where Liquidation Preferences Matter Less

Successful Exits

For companies that exit at high valuations, liquidation preferences may not impact the distribution significantly. If a company sells for

Growing Companies

For startups on a solid growth trajectory, liquidation preferences are often a minor concern. The focus is on scaling and increasing the valuation, which diminishes the relative impact of preferences.

Real-World Examples and Use Cases

Case Study: Startup A

Startup A raised

Case Study: Startup B

Conversely, Startup B raised

Practical Implementation Guides

Negotiating Terms

When negotiating with VCs, understanding your leverage is crucial. Founders should:

- Know Your Worth: If your startup is in demand, you might negotiate better terms.

- Understand the Terms: Get familiar with common terms and how they impact you.

- Consult Experts: Lawyers and experienced advisors can help you navigate complex negotiations, as advised by Entrepreneur's guide on negotiating with VCs.

Managing Your Cap Table

A clear cap table is essential. Regularly update it to reflect new investments and understand how liquidation preferences might affect different scenarios, as highlighted in Carta's explanation of cap tables.

Common Pitfalls and Solutions

Misunderstanding Terms

Many founders make the mistake of not fully grasping the implications of liquidation preferences. Ensure you understand the terms before signing any agreements, as advised by Startup Grind's guide on liquidation preferences.

Overvaluing Preferences

While important, liquidation preferences might not matter in high-value exits. Focus on building a strong company rather than getting bogged down in preferences.

Future Trends and Recommendations

Shift Towards Founder-Friendly Terms

There is a growing trend among VCs to offer more founder-friendly terms. These include lower preferences and non-participating clauses to attract high-potential startups, as noted in TechCrunch's report on venture capital trends.

Increasing Transparency

As startups and investors seek clearer terms, transparency in agreements is becoming more common. Tools and platforms that help visualize cap tables and terms are on the rise, as highlighted in Forbes' discussion on transparency in startup funding.

Conclusion

Liquidation preferences play a critical role in determining the financial outcomes of venture-backed startups—but only in specific scenarios. For many successful startups, these preferences are just a minor footnote. The key is understanding when they matter and how to manage them effectively. Remember, a good understanding of your terms and a clear cap table can save you from unexpected surprises down the road.

FAQ

What is a liquidation preference?

A liquidation preference determines the order in which investors are paid back in the event of a liquidation, ensuring they recoup their investment before others.

How does a liquidation preference work?

Liquidation preferences work by specifying a multiplier and participation terms, dictating how much investors receive before other stakeholders.

What are the benefits of liquidation preferences?

Benefits include protecting investors by ensuring they retrieve their investment first in liquidation events, as detailed in this venture capital guide.

When do liquidation preferences matter most?

They matter most in early or distressed exits where the company is sold for less than the total investment raised.

Can liquidation preferences impact successful exits?

In successful exits with high valuations, liquidation preferences often have little effect as the proceeds far exceed the investment amount.

What are common pitfalls with liquidation preferences?

Common pitfalls include misunderstanding terms and overvaluing their impact on high-value exits.

How can founders manage liquidation preferences?

Founders can manage preferences by negotiating favorable terms, maintaining a clear cap table, and consulting with advisors.

What trends are emerging in liquidation preferences?

Emerging trends include more founder-friendly terms and increased transparency in venture capital agreements.

How do participating preferences differ from non-participating?

Participating preferences allow investors to receive their initial preference and share in remaining proceeds, while non-participating preferences limit them to the initial preferred amount only.

Key Takeaways

- Understanding liquidation preferences is crucial for startup founders.

- Liquidation preferences are most impactful in early or distressed exits.

- Successful exits often diminish the impact of these preferences.

- Founder-friendly terms are becoming more common in venture agreements.

- Clear cap tables and well-negotiated terms can prevent surprises.

Related Articles

- Understanding Venture Debt: Is It the Right Choice for Your Startup? [2025]

- The Rapid Rise of Startups Reaching $10M ARR in 3 Months [2025]

- TechCrunch Disrupt 2026: The Ultimate Guide to Saving $680 on Tickets [2025]

- TechCrunch Disrupt 2026: Your Complete Guide to Early Bird Savings [2025]

- Neo's Low-Dilution Accelerator Model: Reshaping Founder Economics [2025]

- Solving Open Source's Funding Dilemma: A New Approach [2025]