The Collapse of Venture Capital Investor Loyalty in AI

The artificial intelligence investment landscape has undergone a seismic shift in 2025 and 2026. What was once a fundamental principle of venture capital—unwavering loyalty to portfolio companies—has begun to crack under the weight of unprecedented funding rounds and fierce competition between AI titans. The evidence is striking: as Open AI prepares to close a

This phenomenon represents a fundamental departure from the traditional venture capital playbook that governed the industry for decades. Historically, VC firms maintained clear boundaries around portfolio company conflicts. A fund manager who took a seat on Company A's board and received access to sensitive competitive intelligence would never simultaneously invest in Company A's primary rival. The unwritten rule was sacrosanct: loyalty, fiduciary duty, and ethical conflict-of-interest management formed the bedrock of venture capital relationships.

Yet today, prominent firms including Founders Fund, Iconiq Capital, Insight Partners, and Sequoia Capital have announced investments in both Open AI and Anthropic. Sequoia's dual commitment is particularly noteworthy—the legendary Sand Hill Road institution that essentially created the modern VC playbook now openly embraces simultaneous major investments in fierce competitors. This shift signals not just a change in investment strategy, but a fundamental recalibration of how venture capitalists perceive their responsibilities to the companies they fund.

The implications extend far beyond the boardrooms of Silicon Valley. Founders considering venture capital financing must now add conflict-of-interest policies to their due diligence checklist. Employees at competing AI companies worry about information asymmetries. And industry observers question whether the traditional VC model—built on exclusivity, loyalty, and concentrated focus—can survive in an era where capital requirements have become absurdly massive and opportunity costs from missing a deal have become equally enormous.

This comprehensive guide explores the collapse of investor loyalty in AI, examining why it happened, which firms have embraced dual investments, the ethical implications, and what founders and investors should understand about this new reality.

Understanding the Traditional VC Loyalty Model

The Historical Foundation of Investor Exclusivity

Venture capitalism emerged as a structured asset class in the 1960s and 1970s, but it wasn't until the 1980s and 1990s that the loyalty-based relationship model became institutionalized. Early venture capitalists like Arthur Rock, Don Valentine, and the partners at Kleiner Perkins Caufield & Byers established a clear ethical framework: when a VC firm invested in a startup, that investment came with an implicit contract. The VC would provide not just capital, but also strategic guidance, operational expertise, market connections, and—critically—protection from competitive threats posed by other portfolio companies.

This loyalty model served multiple purposes simultaneously. First, it reassured founders that their investor would actively work in their interest, not hedge bets across competing approaches. Second, it created information asymmetries that protected portfolio companies' strategic secrets. When a VC took a board seat, they received access to detailed financial models, customer lists, technology roadmaps, and competitive positioning—information that could prove invaluable (or catastrophic) if shared with rivals.

Third, the loyalty model aligned incentives across the entire ecosystem. A VC that backed Company A in a market segment wouldn't simultaneously back Company B in the same space, because doing so would create direct conflicts between the investors' fiduciary duties to each company. The VC's legal obligation was to maximize returns for Company A's shareholders, but if the VC also owned significant equity in Company B (a direct competitor), their loyalties would be fundamentally divided.

The model became self-reinforcing through practice and reputation. Firms that maintained clear ethical boundaries attracted founders who valued commitment and confidentiality. This selectivity actually enhanced returns—founders told VCs more, shared more honestly about challenges, and took more ownership of the relationship knowing they weren't competing against other portfolio companies for their investor's attention. By the late 1990s and 2000s, investor loyalty had become a defining feature of venture capital brand positioning. Firms marketed themselves as "founder-friendly," "hands-on," and "committed," with exclusivity as the implicit foundation of those claims.

Board Seats and Fiduciary Responsibilities

The complexity of VC loyalty extended beyond just avoiding investments in direct competitors—it fundamentally related to the board representation that typically accompanied significant venture investments. When a VC firm invested in a startup, they almost always negotiated a seat on the company's board of directors. This wasn't merely a position of prestige; it represented a formal fiduciary duty established by corporate law.

A board member legally must act in the best interest of the corporation and all its shareholders (or, in the case of startups, all equity holders). This duty encompasses an obligation to protect the company from harm, maximize shareholder value, and ensure management operates in the stockholders' collective interest. Board members have access to materials that aren't available to the public or even to other employees—financial projections, strategic plans, detailed competitive analyses, technology roadmaps, and sensitive customer information.

When a VC firm had a board member at Company A and simultaneously invested in Company A's competitor Company B, a legal and ethical minefield emerged. The VC's board representative at Company A couldn't simply share information with the Company B investment team—that would constitute breach of fiduciary duty. But the firms existed within the same organization, often with overlapping discussions, shared meeting spaces, and informal information transfer. The risk of inadvertent leakage was substantial, and the appearance of impropriety created trust issues regardless of actual information transfer.

Traditionally, the solution was simple: firms didn't make those investments. They declined to participate in Series rounds for competitor companies. They explicitly stated, when courted by rivaling founders, that they had existing loyalty to companies occupying similar market positions. This self-imposed constraint maintained both legal compliance and ethical reputation.

The Y Combinator Effect and Sam Altman's Understanding

Sam Altman, Open AI's CEO, comes from within the venture capital world itself—he served as president of Y Combinator, the most influential startup accelerator program in history. Altman's deep understanding of VC culture informed his approach to Open AI's funding strategy. In 2024, Altman reportedly provided his investors with an explicit list of rivals he preferred they wouldn't back, including Anthropic (founded by former Open AI VP Dario Amodei), Elon Musk's x AI, and Safe Superintelligence Inc. (founded by Ilya Sutskever, a former Open AI research scientist).

Initially, Altman's request wasn't presented as a hard mandate—he denied claims that he threatened to exclude investors from future rounds if they backed companies on his rival list. However, according to documents that emerged during Elon Musk's lawsuit against Open AI, Altman did establish a consequence for "non-passive" investments in rival companies: those investors would lose access to Open AI's confidential business information. This was a sophisticated application of traditional VC boundary-setting.

Altman's approach demonstrated that even in the AI era, someone deeply versed in venture capital culture understood that loyalty and information protection mattered. By offering a clear choice—full participation as a loyal investor with information access, or partial participation as a financial investor without strategic access—Altman attempted to maintain the traditional model. The strategy implicitly acknowledged that the loyalty-based VC framework still held value, even if maintaining it required explicit negotiation.

Yet even this nuanced approach ultimately failed. Despite Altman's preferences and the threatened information restrictions, major venture firms proceeded to back both Open AI and Anthropic. The gravitational pull of capital requirements and competitive dynamics proved stronger than traditional ethical frameworks.

The scale of AI funding rounds dwarfs traditional venture capital fund sizes, requiring participation from numerous investors, including non-traditional ones. Estimated data for traditional rounds.

The Scale Factor: How $100+ Billion Rounds Changed Everything

Record-Breaking Capital Requirements in AI

The traditional venture capital market operated within relatively predictable capital range brackets. In the 1990s and 2000s, a successful Series A typically ranged from

AI fundamentally altered this calculus. Training and running large language models requires extraordinary computational infrastructure. Open AI's infrastructure spending alone reportedly reaches hundreds of millions monthly. Anthropic's capital raise of

At a

This scale fundamentally changed the math. When a

The Opportunity Cost Calculus

Conventional VC wisdom suggests that funds should maintain focus within specific domains and invest thesis areas. A fund that backs healthcare software shouldn't also back consumer social networks; the expertise, market understanding, and syndication relationships differ substantially. This specialization created natural boundaries that prevented simultaneous investments in direct competitors—they simply fell outside the fund's stated investment thesis.

AI has eliminated this natural boundary. Because AI capabilities apply across every industry and sector, a fund that positions itself to "invest in AI" essentially means investing in AI companies that might potentially compete with each other. There's no vertical specialization that naturally prevents dual investments. An AI fund might reasonably argue it invests in "AI infrastructure," which could include investments in both model companies (Open AI, Anthropic) and supporting infrastructure (Databricks, Together AI, Lambda Labs).

Moreover, the returns potential from AI have created a FOMO (fear of missing out) dynamic more intense than any previous technology wave. Early internet investors who missed Amazon, Google, or Facebook lamented the opportunity cost for decades. Venture capitalists who participated in those companies' subsequent rounds reaped extraordinary returns. The AI moment offers a window that might never repeat—the foundational models that will power everything for the next decade are being built right now, in 2025-2026.

For a VC firm evaluating whether to participate in an Anthropic round after already backing Open AI, the calculus becomes stark: What if Anthropic's Claude models prove superior? What if Anthropic's approach to AI alignment and safety becomes the industry standard? What if this

Quantitatively, if a fund believes Anthropic has even a 20% chance of achieving

The "Hat Passing" Phenomenon

One prominent investor quoted in industry discussions described the phenomenon with striking clarity: when the hat is being passed around for capital collections of record-breaking magnitude, and the needs are so extraordinary, and the possibilities of returns so magnificent, "who can be expected to say no?"

This metaphor captures something essential about how VC norms erode. Investor loyalty wasn't abandoned through explicit policy changes or formal debates about ethics. Rather, it dissolved gradually through thousands of individual investment decisions, each one seemingly reasonable in isolation. Fund partner A attends a board meeting at Open AI, then encounters Anthropic's fundraising roadshow. Their check would help close Anthropic's round. Their FOMO increases. They think about the opportunity cost. They consult their fund's investment committee. The decision gets rationalized: "As long as we don't have board representation at both companies, information leakage risk is limited. As long as we maintain ethical walls, fiduciary duty concerns can be managed. As long as the space is large enough, both companies can succeed."

Repeat this decision across Sequoia, Founders Fund, Insight Partners, Iconiq Capital, and dozens of other firms, and you have a market transformation. No single firm formally rejected investor loyalty. Instead, all of them simultaneously decided that the opportunity was too large, the returns potential too attractive, and the risk manageable enough that they could participate in both camps.

The philosophical shift from "we will invest in this winner and not that loser" (the traditional VC thesis) to "we will invest in multiple potential winners and hedge our bets" represents a fundamental departure from how venture capitalism positioned itself for decades. But it arrived not through programmatic change but through thousands of logical decisions, each reasonable in context, that collectively dismantled institutional norms.

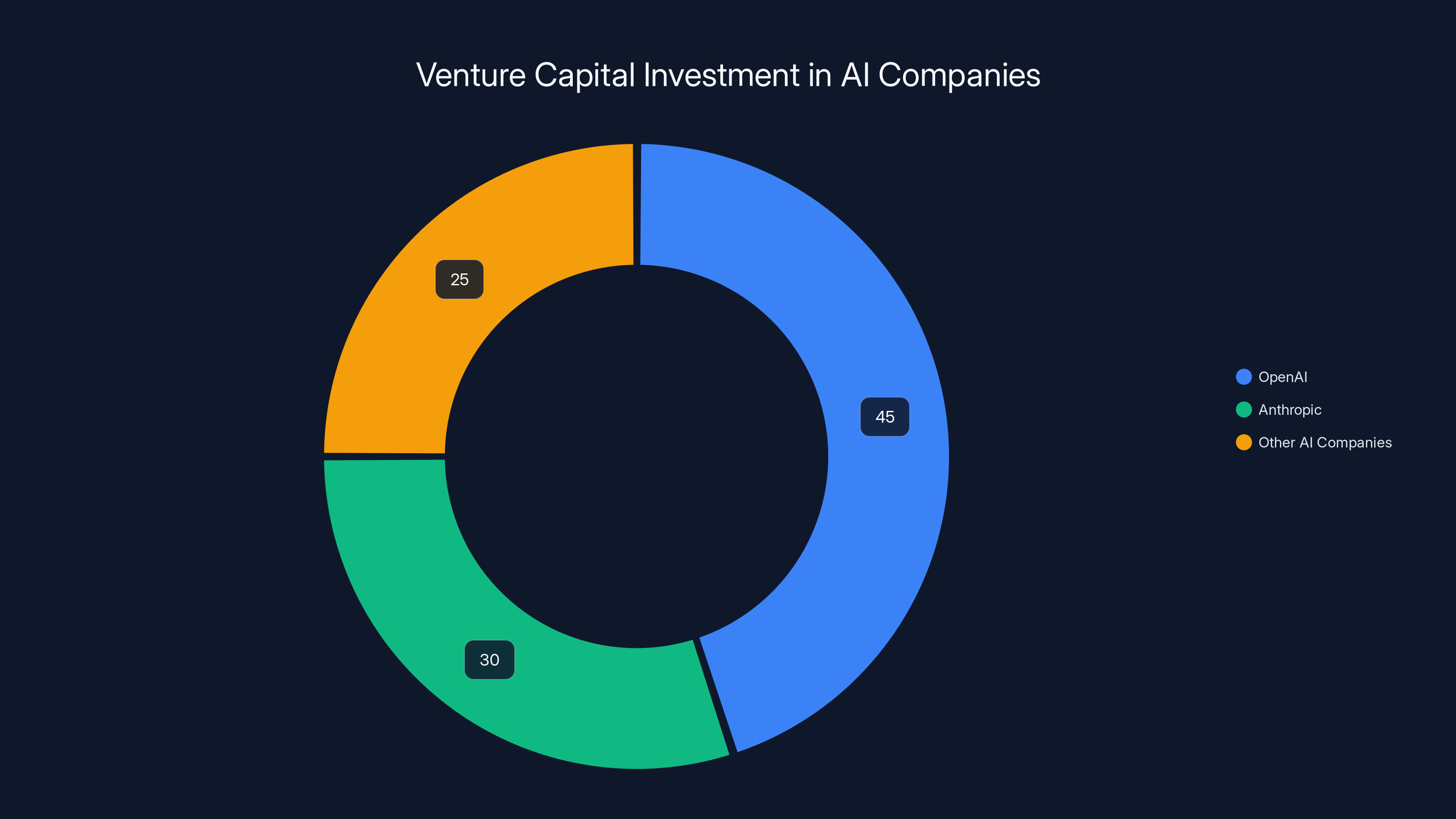

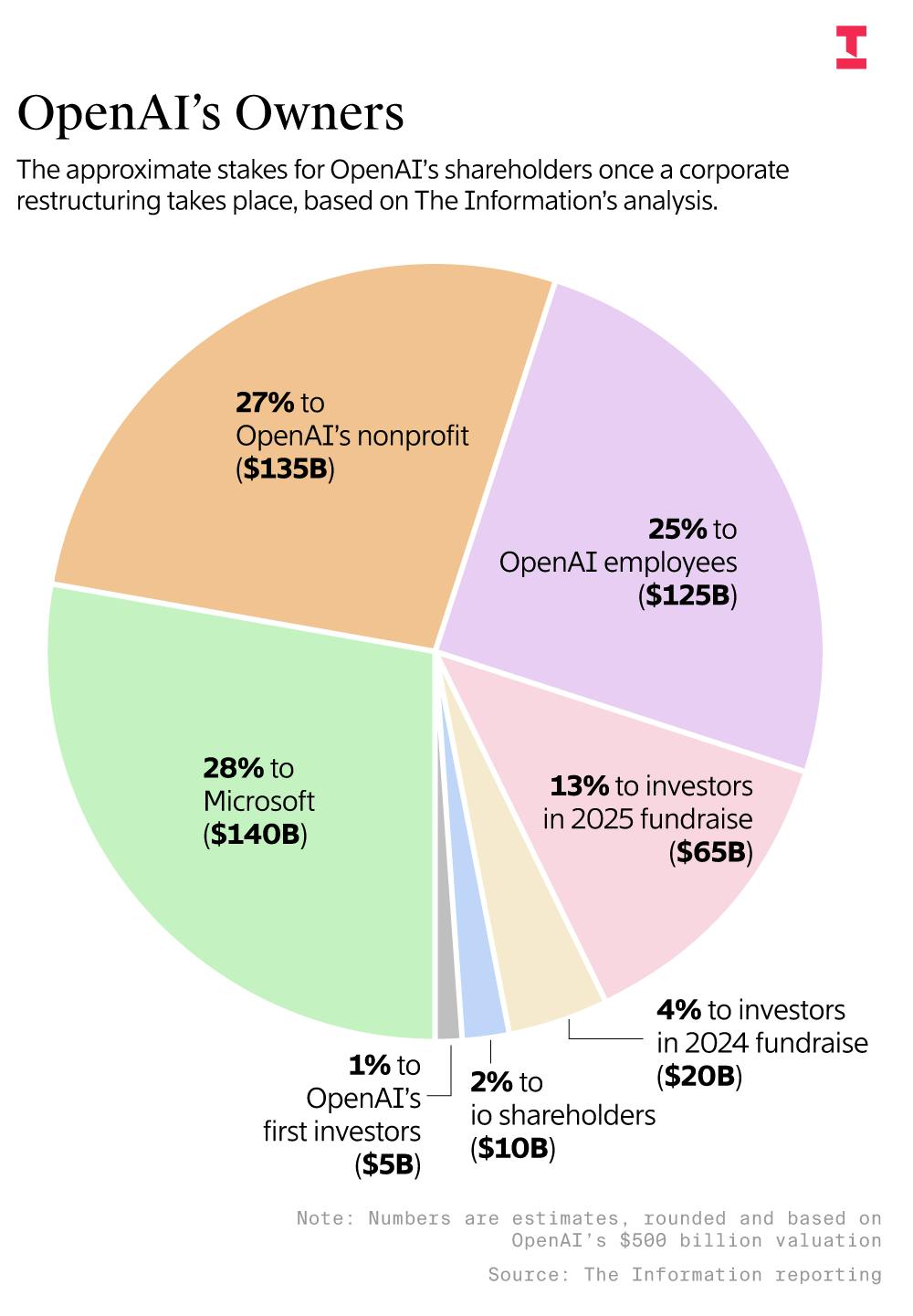

Estimated data shows that OpenAI and Anthropic are major focuses for VC investments, reflecting their large capital requirements and potential returns.

The Dual Investors: Which Firms Are Backing Both Open AI and Anthropic

The Major Players in Both Camps

The list of venture capital firms with announced investments in both Open AI and Anthropic reads like a who's who of Silicon Valley elite. Sequoia Capital tops many lists—the firm that backed Google, Apple, Airbnb, and countless other industry titans now has significant positions in both Open AI and Anthropic. This fact alone signaled to the market that investor loyalty concerns were no longer paramount.

Founders Fund, another legendary firm known for contrarian bets and deep domain expertise, similarly backs both companies. The fund, known for its partnership with Peter Thiel and its investments in companies like Facebook and Palantir, maintains substantial positions in the AI space across competing camps. Iconiq Capital, which focuses on ultra-wealthy individuals and families, participates in both rounds—a sign that even conservative wealth management embraced dual AI investments.

Insight Partners, which specializes in software and infrastructure, committed capital to both companies. D1 Capital, the multi-billion-dollar hedge fund founded by Dan Sundheim, invested in Anthropic's recent round. Greenoaks Capital, which targets post-seed growth companies, has maintained positions in competing AI firms. The list extends through perhaps a dozen or more recognized institutions, representing the complete absence of institutional coordination around conflict-of-interest principles.

What's particularly striking is that these aren't obscure or marginal VC firms. These are the firms with the strongest reputations for founder support, market expertise, and operational excellence. The firms themselves would argue that their board presence, expertise, and strategic guidance create differentiation. Yet that same board presence creates the exact fiduciary conflicts that traditional VC ethics were designed to prevent.

The Corporate Venture Exception: Microsoft, Nvidia, and Alphabet

Corporate venture arms deserve separate analysis because they operate under different strategic logics than traditional VC funds. Microsoft, which has a strategic partnership with Open AI and has invested billions in the company's infrastructure, also participates in broader AI ecosystem development. This includes potential investments in infrastructure or supporting technologies that might benefit Anthropic users or development platforms.

The corporate venture space has always operated with different conflict-of-interest frameworks than traditional VC. When a corporation invests through a dedicated venture arm, those investments serve multiple strategic purposes: financial returns, market intelligence, technology scouting, partnership development, and ecosystem influence. A corporate investor might reasonably argue that simultaneous investments in potentially competing companies serve their broader strategic interest in understanding multiple technical approaches and maintaining optionality.

Nvidia, the chip manufacturer powering both Open AI's and Anthropic's infrastructure, clearly benefits regardless of which company succeeds in the AI race. Nvidia's venture arm can reasonably argue that investments in multiple model companies further Nvidia's strategic interest in seeing widespread AI adoption and healthy competition in the space.

Hedge funds and asset managers like Fidelity, Black Rock, and TPG occupy a similar category. These are financial investors primarily focused on capital returns, not strategic control or partnership. When Black Rock's vast array of funds invest in both Open AI and Anthropic, the firm is essentially acting as a diversified portfolio manager, similar to how mutual funds might hold stocks in competing companies in the same industry.

These exceptions highlight that the collapse of loyalty primarily affects traditional venture capital firms—the funds that have historically positioned themselves as "founder-friendly," hands-on strategic partners who provide value beyond just capital.

Notable Holdouts: Firms That Haven't Gone Dual

Not all venture firms have embraced dual investments. Andreessen Horowitz, one of the largest and most influential VC firms globally, has committed to Open AI but—as of the most recent publicly available information—hasn't announced a major investment in Anthropic. This positioning suggests that some firms still recognize value in maintaining exclusivity and are willing to sacrifice certain opportunities to preserve their reputation for loyalty and focused portfolio management.

Menlo Ventures, a prominent Sand Hill Road firm with a strong track record in infrastructure and platforms, backs Anthropic but not Open AI (at least not in announced major rounds). Bessemer Venture Partners, known for operational excellence and long-term founder partnerships, similarly maintains more selective positioning without publicly announced dual investments in the top AI competitors.

General Catalyst and Greenberg Quintana Rossi (GQR), while influential in the space, haven't participated in both major Open AI and Anthropic rounds at announced levels. These firms' restraint might reflect strategic positioning, investment thesis clarity, or continued commitment to traditional conflict-of-interest principles. Their positioning, standing apart from the stampede toward dual investments, creates competitive differentiation—they can market themselves to founders concerned about investor loyalty and conflict-of-interest issues.

The existence of holdouts proves the choice isn't inevitable. Firms could maintain traditional VC loyalty models if they valued doing so. The fact that major institutions abandoned the principle suggests they made a deliberate strategic calculation that the benefits of dual positioning outweighed the costs of abandoning institutional norms.

Information Asymmetry and Confidential Business Intelligence

What Board Access Actually Means

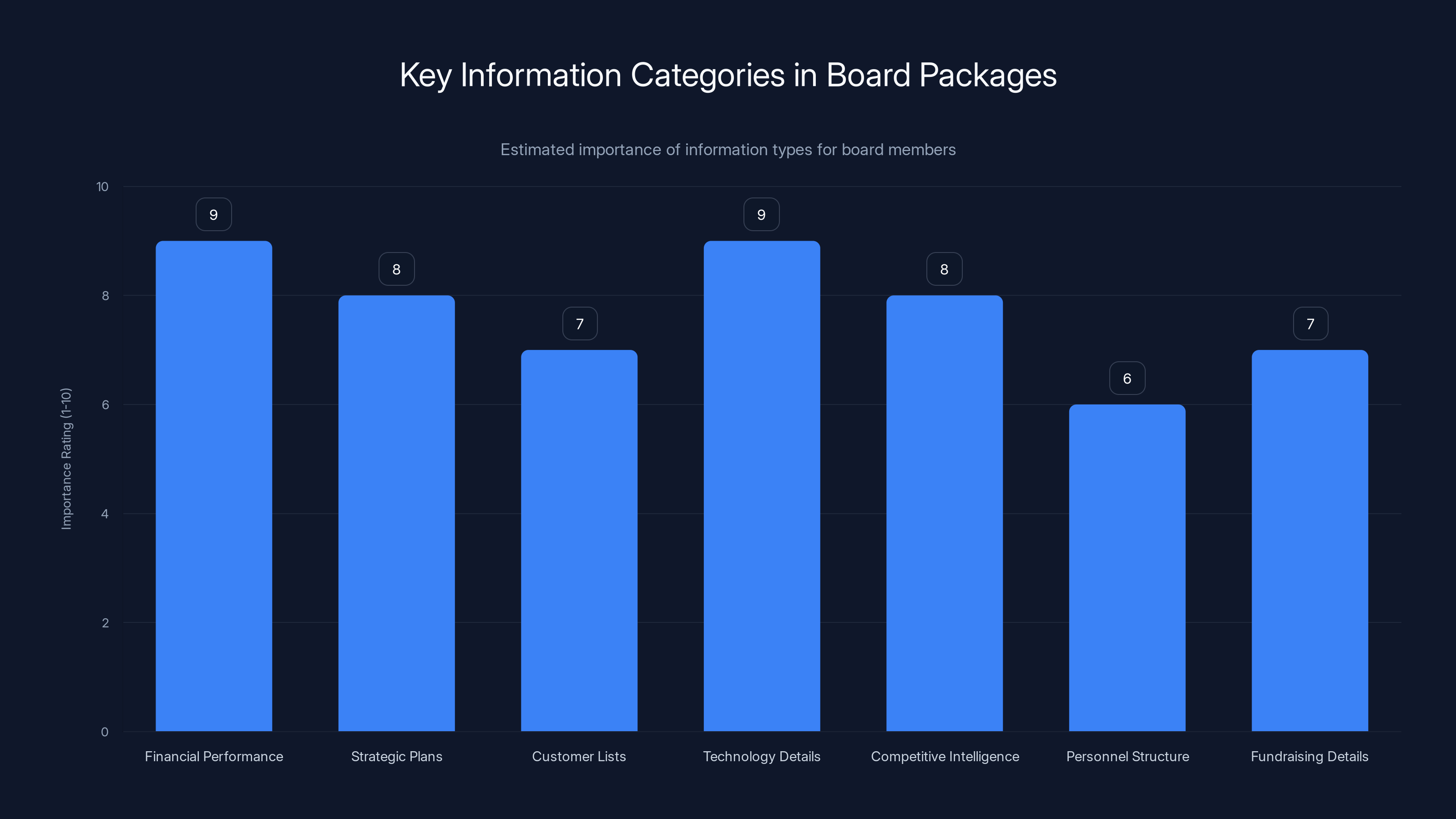

When a venture capitalist sits on a company's board of directors, they don't just attend meetings and vote on major decisions. They receive regular business updates far more detailed than what's available publicly or even to most employees. Board packages typically include:

- Financial performance data: Monthly and quarterly revenue figures, unit economics, customer acquisition costs, and profitability metrics

- Strategic plans: Detailed roadmaps for product development, market expansion, and competitive positioning

- Customer lists and relationships: Names of major customers, contract values, churn risk, and expansion opportunities

- Technology details: Information about proprietary algorithms, model architectures, training data sources, and technical differentiation

- Competitive intelligence: Formal assessments of competitor capabilities, market positioning, and strategic threats

- Personnel and organizational structure: Details about hiring plans, organizational changes, and key person risks

- Fundraising details: Information about future capital needs, valuation expectations, and strategic partnerships

This information is the crown jewel of any technology company. For AI companies particularly, details about training data, model architectures, safety approaches, and compute infrastructure represent tremendous competitive advantage. An investor at Open AI could learn precisely how the company thinks about alignment, safety, and long-term development paths—information that could directly inform how an Anthropic board representative thinks about the competitive landscape.

Traditional VC ethics existed precisely to prevent this information from flowing across portfolio companies. The assumption was that a board member would maintain absolute confidentiality about Company A's business details, even when that board member's firm had financial interest in Company A's competitors. This assumption rested on professional ethics, legal frameworks around confidentiality, and reputational incentives.

The Information Leakage Problem

In practice, preventing information leakage between company teams within the same VC firm is extraordinarily difficult. Even with explicit ethical walls and confidentiality agreements, the risk of inadvertent communication is substantial. A partner working with Anthropic might mention casually to a colleague that "the AI safety approach at Anthropic is quite different from typical industry practice," not realizing the colleague just joined from working on Open AI's board.

Furthermore, the relevant information often leaks through subtle channels that confidentiality agreements don't technically cover. A board member observes that a company is hiring aggressively in certain areas—that's public information from Linked In. But the timing and scale of hiring, combined with board-level knowledge about upcoming products, reveals strategic priorities that haven't been publicly disclosed.

Or a board member notes that a company made a certain strategic partnership decision—perhaps a choice to work with a particular infrastructure provider or data source. That decision, observable from public announcements, carries different significance when you know from board meetings why the company made that choice, what alternatives were considered, and what risks the company identified.

The problem intensifies in smaller information ecosystems. Open AI and Anthropic exist in the same geography (both have offices in San Francisco and Seattle), serve overlapping markets, and employ many people with connections across both companies. Employees dated, friends who worked at both companies, and the general information flow through drinks, dinners, and professional networks creates a baseline of cross-company knowledge.

When major VC firms have board representation at both companies, they add a formal channel for information exchange that makes complete information isolation virtually impossible to guarantee, even with the best intentions and strictest protocols.

Theoretical vs. Practical Risk Management

Many investors who embrace dual positioning argue that information leakage risks are manageable through practical governance. As one investor quoted in industry discussion acknowledged: "As long as the firm doesn't have a board seat, no one sees the harm in it anymore."

This argument holds that financial investment without board representation creates acceptable information barriers. A firm that invests $500 million in Anthropic but doesn't have a board seat has less direct access to confidential strategic information. The firm's partner attending board meetings at Open AI might have information about competitive threat assessments, but that information would come from open strategy discussions rather than confidential board materials.

However, this distinction between "financial investor without board seat" and "board member" may be overstated in practice. VC firms with major positions often have enormous influence despite not holding formal board seats. Their general partners might attend investor updates meetings, have regular calls with leadership, participate in fundraising discussions, and exercise strong voice in major company decisions.

Moreover, the information asymmetry flows both directions. Even without board access, a firm investing significantly in Anthropic gains enormous amounts of intelligence about the company's approach, capabilities, and strategy through investor relations interactions, pitch materials, and financial performance discussions. A knowledgeable investor can infer tremendous amounts about competitive positioning from financial metrics and strategic priorities.

The theoretical risk management suggests that with appropriate ethical walls and confidentiality protocols, dual investment doesn't necessarily create insurmountable information problems. In practice, the guarantee of complete information isolation seems impossible to achieve, particularly within large VC firms where multiple teams and partners inevitably interact.

Financial performance and technology details are estimated to be the most critical information categories in board packages, reflecting their strategic importance for decision-making. Estimated data.

The Anthropic Perspective: Consequences of Accepting Conflicted Investors

Building Trust in an Investor Pool Containing Competitors

When Anthropic announced its $30 billion funding round with multiple firms also backing Open AI, the company faced a strategic decision: accept investors with clear conflicts of interest, or attempt to maintain investor loyalty exclusivity and potentially reduce available capital. Anthropic chose the former path, accepting investments from firms like Sequoia and others despite their positions in Open AI.

This decision reflects the reality that in 2025-2026, founders cannot afford to be selective about investor sources in ways previous generations could be. Anthropic needed $30 billion. The pool of capital sources capable of committing that magnitude of funding is limited to perhaps 15-20 firms globally (including corporate ventures, hedge funds, and sovereign wealth funds). Excluding the major VC firms would reduce available capital and increase risk that the round doesn't fully fund.

From Anthropic's perspective, accepting these investors creates both benefits and costs. The benefit is access to capital from the most experienced, connected, and operationally helpful firms in the industry. Sequoia's portfolio includes extraordinary companies and the firm brings relationships, strategic guidance, and operational expertise that can accelerate company growth. Turning away such investors based on conflict-of-interest principles that are increasingly accepted as exceptions rather than rules would be self-defeating.

The cost is the intelligence asymmetry and trust uncertainty. Anthropic's leadership team, including CEO Dario Amodei, must assume that investors with positions in Open AI potentially have influence over competitive positioning they observe at Open AI. This creates perpetual uncertainty about information flow and investor loyalty during critical moments.

Notably, Anthropic was founded by people who left Open AI specifically due to disagreement about the company's direction and safety approaches. This history makes the irony particularly acute—the company founded partly as an alternative to Open AI because of strategic disagreement now shares investors with Open AI, creating structural incentives for those investors to potentially pressure Anthropic toward Open AI-aligned positions.

Practical Governance Around Information and Decision-Making

In response to the information asymmetry challenges, companies now establish explicit governance frameworks around conflicted investors. These typically include:

- Restricted information access: Conflicted investors might receive financial updates and standard investor relations materials but be excluded from strategy discussions involving competitive positioning or technical details

- Executive session management: Board meetings might include sessions without the conflicted investor present when discussing competitive strategy

- Information compartmentalization: Different investor communication tracks, with conflicted investors receiving less sensitive information

- Explicit confidentiality agreements: Enhanced confidentiality commitments specifically addressing competitive information

However, these governance structures often feel like theater—they create the appearance of information protection without the substance. A skilled investor can infer tremendous amounts about competitive positioning from financial data, hiring patterns, partnership announcements, and product release timing, even without explicit access to strategic discussions.

Moreover, governance structures around information protection become unwieldy as the number of conflicted investors increases. With potentially a dozen major firms having stakes in both Open AI and Anthropic, creating individualized information protocols for each becomes practically impossible. Companies eventually adopt lowest-common-denominator approaches that provide little actual protection.

The Reputational and Trust Cost

Perhaps the most significant cost to Anthropic of accepting conflicted investors relates to perception and trust. How do employees at Anthropic think about investor loyalty when they know that major investors have significant positions in Open AI? How does this affect organizational culture and sense of mission? When a company's board includes people representing competing financial interests, the sense that everyone is aligned toward a shared goal diminishes.

Customers and partners also make inferences about alignment based on investor positioning. If you're a major enterprise customer evaluating whether to build your critical AI infrastructure on Anthropic's technology, knowing that Anthropic's board includes people representing Open AI investor interests creates hesitation. You worry about the company's independence and strategic direction.

The reputational cost isn't just internal—it's also a competitive disadvantage. Anthropic can't position itself as the "aligned alternative" to Open AI if Open AI's investors are also Anthropic's investors. The narrative becomes confused. Both companies benefit from being portrayed as competitors pursuing different AI development philosophies, but that narrative breaks down when they share major financial backers.

These costs aren't immaterial, but they were outweighed by the value of the capital itself and the operational expertise that came with the prestigious investors.

The Broader Implications for Startup Founders

Adding Conflict-of-Interest Due Diligence to Term Sheets

For founders navigating funding in 2025 and beyond, understanding investor conflict-of-interest profiles should become as standard as evaluating fund size, track record, and geographic focus. The traditional assumption—that a VC investor would provide unwavering loyalty and protect confidential information—can no longer be taken for granted.

Founders should now ask explicitly:

- Direct competitive investments: Does the fund have any existing investments in companies that might compete with our company? If so, what governance prevents information leakage?

- Related vertical investments: Does the fund invest across the supply chain in ways that might create conflicts? For example, investing in both an AI model company and a hardware infrastructure company serving that company's competitor?

- Board representation policies: If the fund invests in multiple potentially competing companies, which ones receive board representation and which don't?

- Information access protocols: What specific protocols does the fund have around information walls between investments with conflict potential?

- Historical precedent: Has the fund maintained conflicts in past situations? How did those situations resolve?

- Portfolio diversity: How many portfolio companies does the fund have? With more companies, conflict-of-interest management becomes harder, suggesting higher risk of information leakage.

These questions likely feel uncomfortable to raise with prospective investors—founders don't want to seem paranoid or difficult. But the AI industry's demonstration that major VC firms are comfortable accepting conflicted positions makes asking these questions reasonable and important.

Founders should also consider the long-term implications of accepting an investor with conflicted positions. If you raise from a fund that also backs your competitor, you're accepting that the fund's interests might not align fully with yours when the competitor needs additional capital or strategic support. This affects not just current dynamics but future funding relationships—if the competitor eventually needs bridge financing and your shared investor facilitates that, you're affected.

The Information Asymmetry Problem for Bootstrapped and Early-Stage Companies

The collapse of investor loyalty particularly disadvantages early-stage companies and startups that raise from conflicted investors without yet having significant capital. A Series A company that takes $5 million from a firm that also backs larger competitors faces information disadvantage relative to the competitor. The competitor might learn from investor discussions about market dynamics the early-stage company is discovering. The investor might provide strategic feedback to the larger, existing company informed by intelligence gathered from the early-stage company's pitch meetings.

This creates a "pecking order" dynamic where larger, more advanced companies benefit from information advantage over emerging competitors funded by the same firm. Traditional VC ethics specifically existed to prevent these dynamics—the assumption was that a firm would give equal information confidentiality protection to all portfolio companies regardless of size.

Without that protection, early-stage founders should think carefully about whether accepting an investor with conflicted positions makes strategic sense, even if the capital is available.

Building Alternatives to Conflicted VC

The collapse of VC loyalty might accelerate the emergence of alternative funding sources that don't require accepting information asymmetry risk. These include:

- Strategic corporate investment: Companies raising from industry players might accept conflict-of-interest risk in exchange for strategic benefit—access to customers, partnership opportunity, or acquisition option

- Government and quasi-government funding: DARPA, NSF, and other government sources don't operate under VC conflicts-of-interest concerns

- Sovereign wealth funds and endowments: Patient capital sources might be willing to maintain traditional loyalty approaches because they're not optimizing for maximum financial returns

- Founder-led syndicates: Founder networks and angel syndicates might maintain loyalty norms more rigidly than institutional VC

- Revenue-based financing: Lenders providing capital based on revenue rather than equity don't have conflicted investment positions

Founders with the flexibility to pursue non-traditional funding might find those alternatives worth the effort to avoid information asymmetry risks that come with conflicted VC capital.

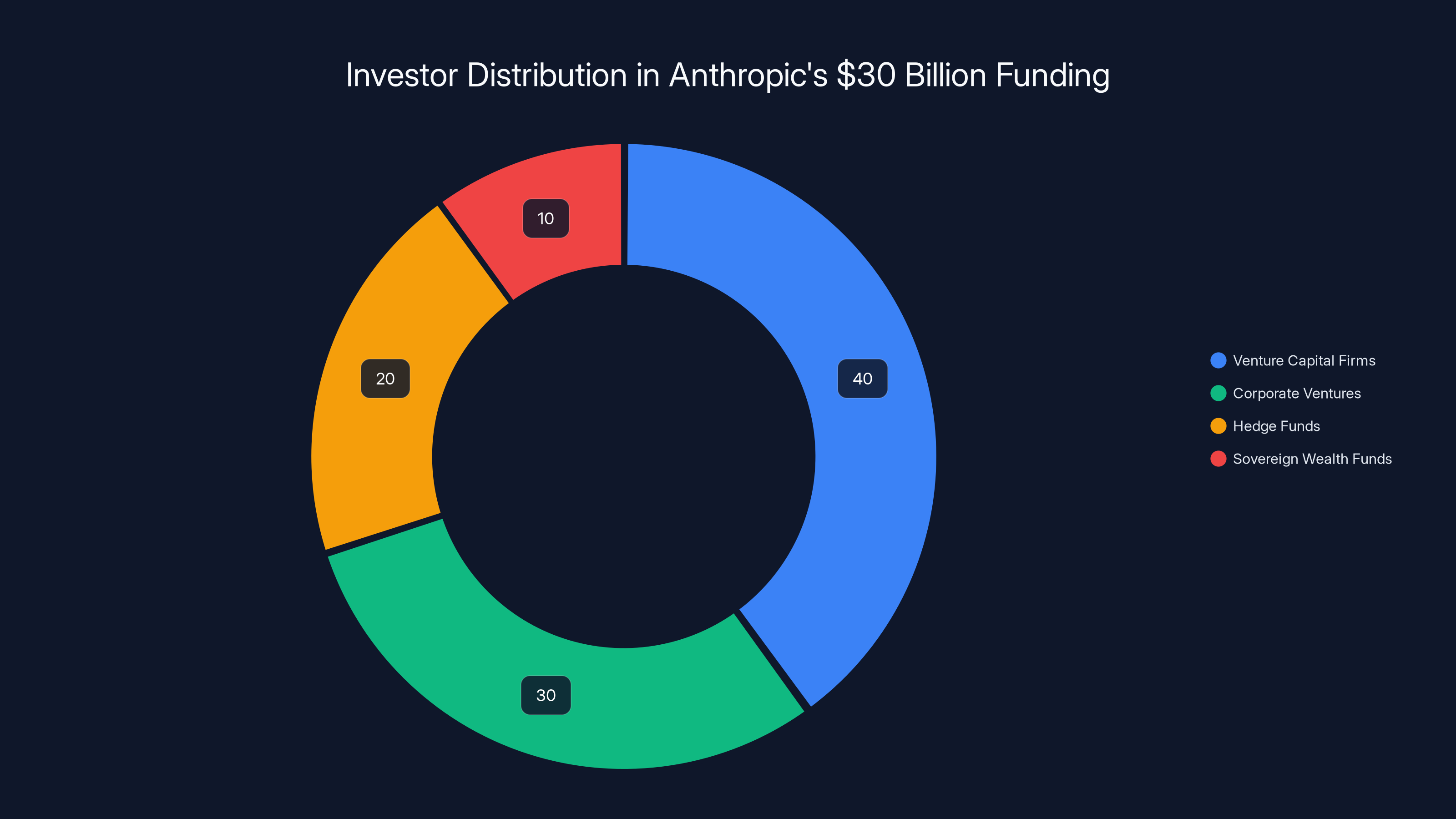

The majority of Anthropic's $30 billion funding round is estimated to come from venture capital firms, with significant contributions from corporate ventures and hedge funds. Estimated data.

The Ethical Collapse: How Professional Standards Eroded

The Role of Rationalization and Incremental Compromise

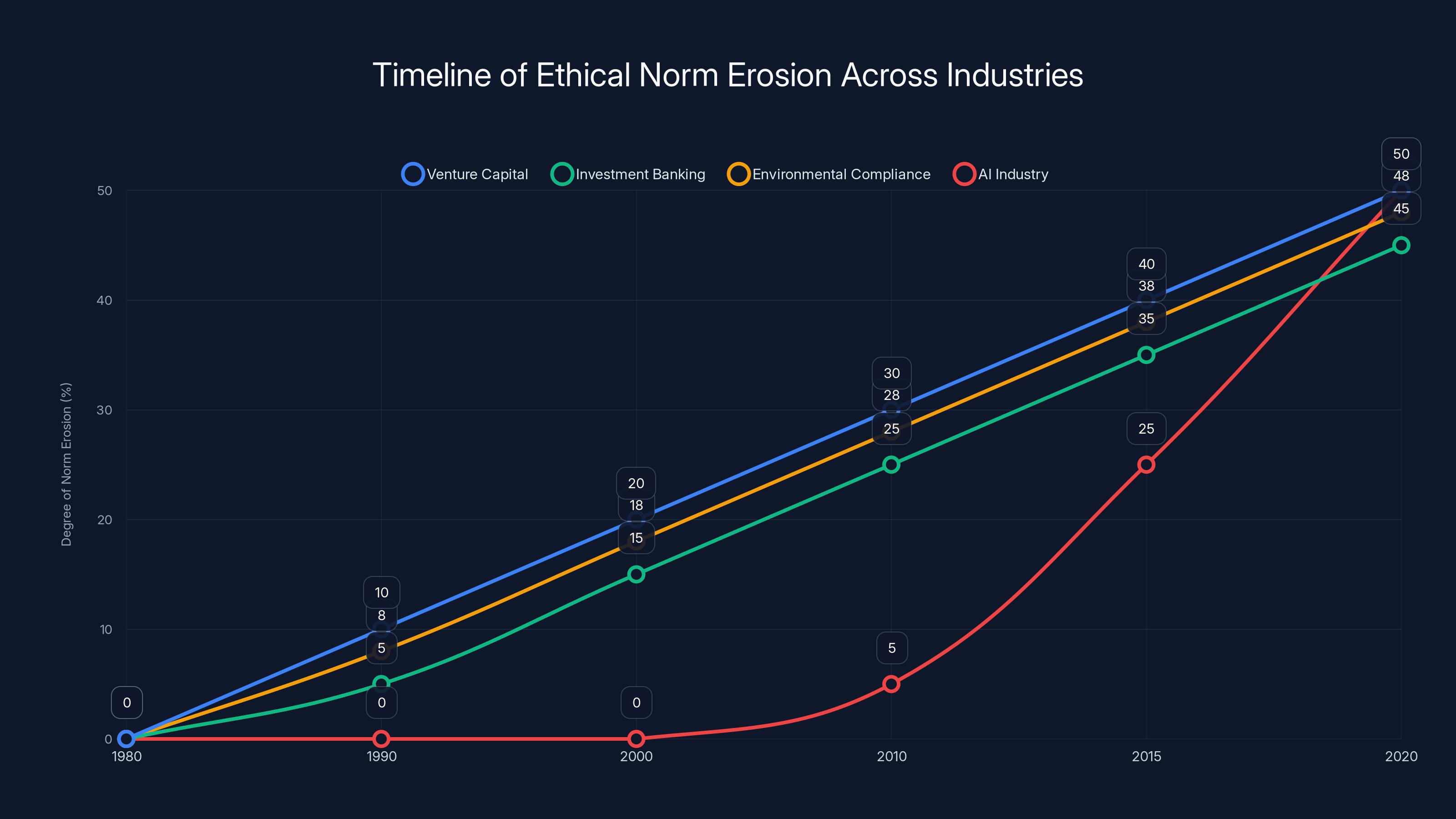

The collapse of investor loyalty norms didn't happen through explicit rejection of ethical principles. Instead, it occurred through thousands of individual rationalization decisions, each one seemingly reasonable in isolation. The process followed a pattern familiar from organizational behavior research—incremental norm erosion where small ethical compromises accumulate until the original principle becomes unrecognizable.

The initial boundary violation might have been something like: "We'll invest in both Company A and Company B but maintain strict board-seat segregation so information access is limited." This compromise seemed reasonable—it preserved some ethical protection while acknowledging business realities. The next iteration became: "We'll invest in both but without board seats everywhere, which further limits information leakage." Then: "Our hedge fund arm can invest alongside our VC arm; they have different information access standards." Each step seemed justified individually, but collectively they dismantled the original principle.

Research on organizational ethics shows that this pattern—where small compromises accumulate into complete norm reversal—happens across industries and time periods. It's not unique to venture capital or AI. Similar processes eroded restrictions on proprietary trading in investment banks before 2008, transformed environmental compliance from serious concern to box-checking in many industries, and degraded conflict-of-interest standards in pharmaceutical marketing to physicians.

What makes the AI case unique is how rapidly it happened. Previous industry norm erosion typically occurred over decades. The VC loyalty model lasted from the 1980s through the 2010s—a 30-year run before major cracks appeared. The collapse in AI happened in fewer than 5 years, suggesting the capital requirements and return potential were particularly effective at overriding traditional ethical frameworks.

The FOMO Multiplier and Competitive Dynamics

Fomo (fear of missing out) operated as a powerful accelerant for norm erosion. Once Sequoia—the most legendary and respected VC firm—announced dual investments in both Open AI and Anthropic, other firms faced acute competitive pressure. If Sequoia was willing to accept the conflict-of-interest risks, was there a reputational cost to doing so? If other major firms started backing both companies, would firms that maintained exclusivity miss out on the most important investment opportunity of the decade?

The dynamics mirror information cascade theory from behavioral economics. When a respected firm makes a choice, it updates market beliefs about whether that choice is reasonable. Sequoia's decision essentially said: "We believe the returns from dual investment in AI outweigh the costs of abandoned investor loyalty principles." Once that decision was public, other firms could look at Sequoia's choice as evidence that their own decision to do the same was justified.

This dynamic is self-reinforcing. Each major firm that announces dual investments makes it easier for the next firm to do the same. The reputational cost decreases with each additional firm embracing the practice. Eventually, maintaining the traditional standard becomes the contrarian position that requires explicit justification, rather than the default position of investor loyalty.

Competitive dynamics also affected willingness to accept these conflicts at the firm level. If you're Founders Fund or Iconiq, and you know that your competitors (other major firms) are getting allocations in both Open AI and Anthropic rounds, the competitive pressure to match those positions is enormous. VCs compete on access to the most valuable deals. Missing one of the two most important AI companies because of ethical concerns about conflict-of-interest is strategically difficult to defend to your own limited partners (the investors who funded your fund).

The Limited Partner Pressure Factor

Most VC funds aren't managed by single partners—they're organized as firms with partners answering to limited partners (LPs), which are the institutions and wealthy individuals who actually provided the capital to create the fund. These LPs evaluate fund performance based on returns. They're less interested in the fund's ethical frameworks around investor loyalty than in whether the fund generated superior returns.

When a VC partner proposes declining investment in Anthropic because their fund already backs Open AI, the partner must justify this decision to LPs who might lose billions in returns. The conversation might go: "We're declining a

LPs themselves increasingly include large institutional investors—pension funds, endowments, insurance companies—that invest across multiple competing companies in traditional industries. These LPs see nothing unusual about holding stock in both Pepsi and Coca-Cola, or both Apple and Microsoft. The idea that a venture fund should maintain exclusivity around investments seems provincial compared to how these institutions manage their broader portfolios.

LP pressure to maximize returns thus filtered down to VC fund decisions in ways that undermined loyalty-based frameworks. Partners who maintained traditional ethics faced pressure from their own investors to justify capital returns that lagged behind competitors willing to embrace dual investments.

Market Normalization and the Change in Dialogue

Once enough firms announced dual investments, market dialogue shifted. The question changed from "Is it ethical to invest in both Open AI and Anthropic?" to "How do we manage the information-protection protocols when investing in both?" This reframing—from ethical principle to operational management—essentially conceded that the investment would happen, and the only question was execution risk.

This linguistic and conceptual shift normalized the practice. Articles about the funding rounds stopped presenting dual investments as novel or ethically questionable. Instead, they became factual observations: "Sequoia is investing in both," presented without moral judgment. The absence of widespread criticism or outrage in major media reinforced the sense that market participants had accepted this as normal.

Industry dialogue also shifted to emphasize mitigating factors. Investors pointed out that board seats weren't universally provided, that hedge funds and asset managers are different from VC firms, that the companies might not ultimately compete if they both succeed in different market segments or serve different use cases. These points are arguably valid, but they operated primarily to rationalize decisions that had already been made on financial grounds.

The Technical Limitations of Information Walls

Why Ethical Walls Fail in Practice

Information walls—the legal and organizational structures designed to prevent confidential information from flowing between teams with conflicting interests—are notoriously difficult to maintain, particularly within large organizations. Firms from investment banking to law firms to consulting have long dealt with the challenge of maintaining information walls between teams that might have conflicts of interest.

The theoretical problem is straightforward: if Person A and Person B work for the same firm, they share the same physical spaces, use the same communication systems, attend the same firm meetings, and socialize with the same colleagues. Information naturally flows through these channels. While explicit transfer of confidential information violates ethical walls, implicit knowledge transfer through observation, inference, and casual conversation is much harder to prevent.

In the case of VC firms investing in both Open AI and Anthropic, the information wall would need to prevent the partner managing the Open AI investment from any discussions about competitive positioning with the partner managing the Anthropic investment. But these same people eat lunch together, attend firm meetings together, and work on investment committee decisions together. The wall exists only when it's explicitly invoked, not as a permanent structural feature.

The Practical Reality of Multi-Company Discussions

VC firms make investment decisions through committee processes that involve multiple partners. When discussing whether to increase the firm's position in Open AI or maintain the current allocation, partners discuss strategic rationale: market potential, competitive positioning, management quality, technical differentiation, and competitive threat assessment.

If one partner in that meeting also manages the Anthropic investment, the information walls become porous. A partner might mention in an investment committee meeting, "We're thinking Open AI has really important advantages in [specific area]," as justification for increasing allocation. That information—coming in a public firm meeting—isn't technically a breach of the information wall, yet it's precisely the kind of competitive intelligence that one would expect the information wall to prevent from being communicated to the Anthropic-side partners.

Moreover, investment committee decisions themselves reflect information from board meetings and investor updates. If the Open AI investment committee meeting discusses risk factors that came up in board meetings, and the Anthropic team observes which factors the Open AI team focuses on, they gain indirect insight into Open AI's strategic thinking.

Research on information walls in investment banks and financial services consistently shows that even with formal protocols, policies, and legal consequences for violation, information still leaks across supposedly impermeable boundaries. The leakage is usually more subtle than explicit communication—it's pattern recognition, inference from available data, and implicit knowledge that accumulates from proximity and shared firm culture.

Chinese Walls vs. Silicon Valley Informality

Information walls work somewhat better in formal, hierarchical organizations with explicit protocols and consequences for violation. Investment banks maintain walls around investment banking and trading operations because there's clear delineation of roles, explicit protocols, and significant legal and regulatory consequences for violation.

Silicon Valley VC culture is typically the opposite—informal, collaborative, and strongly discouraging of explicit rules and hierarchy. Partners pride themselves on being accessible, collaborative, and willing to share ideas across the firm. The very values that make Silicon Valley VC culture effective for supporting entrepreneurs make it poorly suited to maintaining information walls.

When Sequoia partners gather for a firm meeting, they don't organize into separate rooms for Open AI discussions and Anthropic discussions. They gather together, discuss recent activity at all major portfolio companies, and share strategic insights. This collaborative culture is a feature of VC firms—it's what partners value—but it's fundamentally incompatible with effective information walls.

This creates an impossible situation: maintain the collaborative culture that makes the firm valuable to entrepreneurs and limiting, or establish the formality and hierarchy necessary for genuine information walls, sacrificing culture for ethics. Most firms chose culture over ethics.

The Impossibility of Cognitive Firewalls

Even if a VC firm established the formal protocols necessary for information walls, there's a deeper cognitive problem: preventing a single human brain from integrating information it has separately received from two sources.

A partner at Sequoia might receive information in an Open AI board meeting about the company's strategic priorities and technical challenges. Later, in a different context, that same partner receives information in an Anthropic investor update about Anthropic's strategic priorities. Cognitively integrating these two information streams is automatic—the brain naturally tries to find patterns and comparisons.

Even if the partner explicitly tries to prevent this integration (maintains a mental information wall), the integration happens subconsciously. Studies in cognitive psychology show that people cannot reliably prevent their brains from processing information they've received, even when they're explicitly instructed to do so. The more relevant two pieces of information are to each other, the more automatically the brain integrates them.

This creates a situation where no amount of formal protocol can prevent the actual information leakage that matters most—the cognitive integration of competitive intelligence that gives one company insight into another's thinking.

The AI industry experienced rapid ethical norm erosion within 5 years, compared to decades in other industries. Estimated data.

Alternative Models: How Investors Could Maintain Loyalty

The Strict Segregation Approach

Some institutional investors, particularly endowments and pension funds with long time horizons, have maintained principles of investor loyalty by strictly segregating their investments. Yale's endowment, for example, maintains policy restrictions on holdings in companies that represent material conflicts of interest. The institution chooses to accept potential opportunity costs (not participating in certain deals) to maintain ethical principles.

A VC firm could theoretically adopt similar strict segregation: establish explicit policy that the firm will not maintain significant direct investments in companies that directly compete in the same market segment. This would require the firm to:

- Define what constitutes "direct competition" clearly

- Establish a formal process for reviewing potential investments against existing portfolio holdings

- Accept declining allocations in certain major funding rounds to avoid conflicts

- Communicate this policy publicly to founders and competitors

The strategic downside is significant—the firm would miss allocation in potentially the most valuable investments of the decade. The competitive firms that embraced dual investments would outperform on returns, creating LP pressure. Yet some firms might have found this trade-off acceptable if they valued reputation and founder loyalty sufficiently.

Andreessen Horowitz appears to have partially adopted this approach, backing Open AI while reportedly passing on major Anthropic allocations. Whether this reflects deliberate policy or circumstantial timing isn't clear, but the result is that the firm maintains clearer exclusivity around its AI investments than rivals did.

The Passive Investment Model

Another approach would be for active management VC firms to separate their active portfolio management from purely passive financial investment. Under this model:

- Active investments: Board seats, operational involvement, strategic guidance, and information access would come with explicit exclusivity—the firm wouldn't invest in direct competitors

- Passive financial investments: Financial investments without board access or strategic involvement could be made across competing companies, as the firm's role is purely as a capital provider

This model acknowledges that passive financial investment creates minimal conflict-of-interest risk (the investor is largely indifferent between competitors succeeding, as long as one of them does). Only active investments that include board representation and strategic involvement would be subject to loyalty constraints.

Some of the dual-investing firms arguably moved toward this model—firms like Fidelity, Black Rock, and TPG could argue that their investments in both Open AI and Anthropic are largely passive financial positions without the strategic involvement that characterizes their active board seats at other companies.

The problem with this model is that it still permits information leakage through the active investments. A firm with a board seat at Open AI learns competitive intelligence that could benefit it even as a passive investor in Anthropic. Moreover, even passive investors with large positions exercise influence through other channels—investor rights, follow-on funding discussions, strategic partnership conversations.

The Independent Subsidiary Model

Some large financial institutions maintain multiple investment firms that operate independently, with firewalls between them. Berkshire Hathaway maintains completely separate investment vehicles for different asset classes and strategies. JPMorgan maintains separate divisions for different aspects of investment management.

A VC firm could theoretically establish multiple independent entities with separate capital, separate limited partners, and minimal information sharing between them. One subsidiary could focus on Open AI and competitors, while another focuses on different areas of AI or different industries entirely.

The upside is complete elimination of information-leakage risk—separate entities are genuinely independent. The downside is operational complexity and fragmentation of the fund's collective expertise and relationships. Most VC firms chose not to adopt this model, viewing it as inefficient and destructive to firm culture.

The Explicit Ethical Commitment Model

Some investors could differentiate themselves through explicit public commitment to investor loyalty and conflict-of-interest management. A firm could announce: "We maintain traditional venture capital ethics around investor loyalty. Founders can trust that we will not simultaneously invest in your direct competitors without your explicit consent."

This public commitment would create reputational benefit—founders would preferentially work with firms known for loyalty. Over time, this could differentiate the firm positively, attracting the best founders who value alignment and commitment.

The risk is that this strategy only works if the market values it. If founders and entrepreneurs don't actually penalize conflicted investors, or if the return advantage from dual investing outweighs the founder loyalty advantage, then explicit commitment becomes a liability (the firm misses major deals while competitors participate).

The fact that few major firms adopted this strategy suggests the market didn't sufficiently value investor loyalty to make commitment economically rational.

The Future of Investor-Founder Relationships

The Permanent Shift in Assumptions

The normalization of dual investing in AI creates a permanent shift in how founders should think about VC relationships. The assumption that a VC investor will provide unwavering loyalty, information confidentiality, and preference for your company over competitors can no longer be taken as default.

This doesn't mean investors are acting unethically in a legal sense—most dual investments don't violate formal policies or legal standards. But the ethical framework that governed VC culture for decades has shifted. Founders must now operate under the assumption that their major investors might simultaneously back competitors.

This shift forces a recalibration of founder-investor relationships toward more transactional framing. Rather than expecting the VC to operate as a strategic partner committed to the startup's success, founders might view the VC relationship as capital provisioning with advisory services, where the investor's interest is financial return rather than the startup's specific success.

This shift creates several downstream effects on how companies operate:

- Information compartmentalization: Startups will increasingly restrict what information they share with investors, knowing that information might be accessible to people with competitive interests

- Board structure changes: Companies might demand observer-only roles for investors they view as conflicts rather than full board representation

- Investor diversification: Founders will seek funding from more diverse sources rather than relying on single VC firms, reducing dependency on any one firm with conflicted interests

- Alternative funding emphasis: Non-VC funding sources (corporate investment, strategic partners, revenue-based financing) might become more attractive for companies concerned about investor conflicts

The New Founder Due Diligence Checklist

Future founders evaluating VC funding should add several questions to their standard due diligence:

- What is your current portfolio in adjacent spaces? Request a clear list of investments that might represent competitive conflicts

- What is your explicit policy on competitive investments? Ask whether the firm has any formal rules restricting simultaneous investments in competitors

- How will you manage information protection if you have conflicted positions? Get specifics on what information you won't have access to and how walls work in practice

- Who specifically will represent us? Understand which partners will spend time on your company and whether they have divided attention across competitors

- What happens if we need capital and a competitor also needs capital? Get clarity on allocation frameworks and preferences

- What happens if a competitor later acquires talent or capability that becomes strategically important? Understand the investor's stance on supporting competitor initiatives

- What are your investor conflicts right now? Request an explicit list of companies backed by the fund that might compete with you in related spaces

These questions likely feel uncomfortable to ask—founders don't want to seem difficult or untrustworthy. But the AI industry's demonstration that investor loyalty can't be assumed makes asking these questions reasonable.

The Rise of Mission-Aligned and Values-Based Investing

One potential response to the collapse of traditional investor loyalty is the emergence of venture firms that explicitly organize around mission and values alignment rather than pure financial return optimization. These firms might market themselves to founders who care about investor alignment:

- Founders seeking firms with explicit founder-loyalty commitments

- Founders building solutions to societal problems who want investors aligned on mission, not just returns

- Founders from underrepresented backgrounds seeking investors committed to diversity and inclusion

- Founders in industries (climate, health, education) where values alignment matters

This segment likely won't be the largest segment of VC capital—investors optimizing purely for returns will always dominate. But it could provide meaningful alternative for founders who value alignment more than access to the absolute largest funds.

The Regulatory and Legal Evolution

Over time, regulatory bodies and legal frameworks might evolve to address the information asymmetry and conflict-of-interest risks created by dual investing. Potential regulatory responses could include:

- Disclosure requirements: Regulators might require VCs to disclose all conflicted positions to founders before term sheets are signed

- Mandatory information walls: Formalized legal frameworks around information walls with penalties for violation

- Restricted board representation: Limiting board seats for investors with conflicted positions

- Founder rights: Legal protections allowing founders to request removal of conflicted investors from certain decisions

- Transparency databases: Public registries of investor conflicts to help founders identify problematic patterns

These regulatory approaches would add friction to capital allocation and might reduce overall venture returns, creating political resistance. But if information asymmetry and conflict-of-interest problems become clearly demonstrated and harmful, regulatory response could eventually mandate more explicit protections.

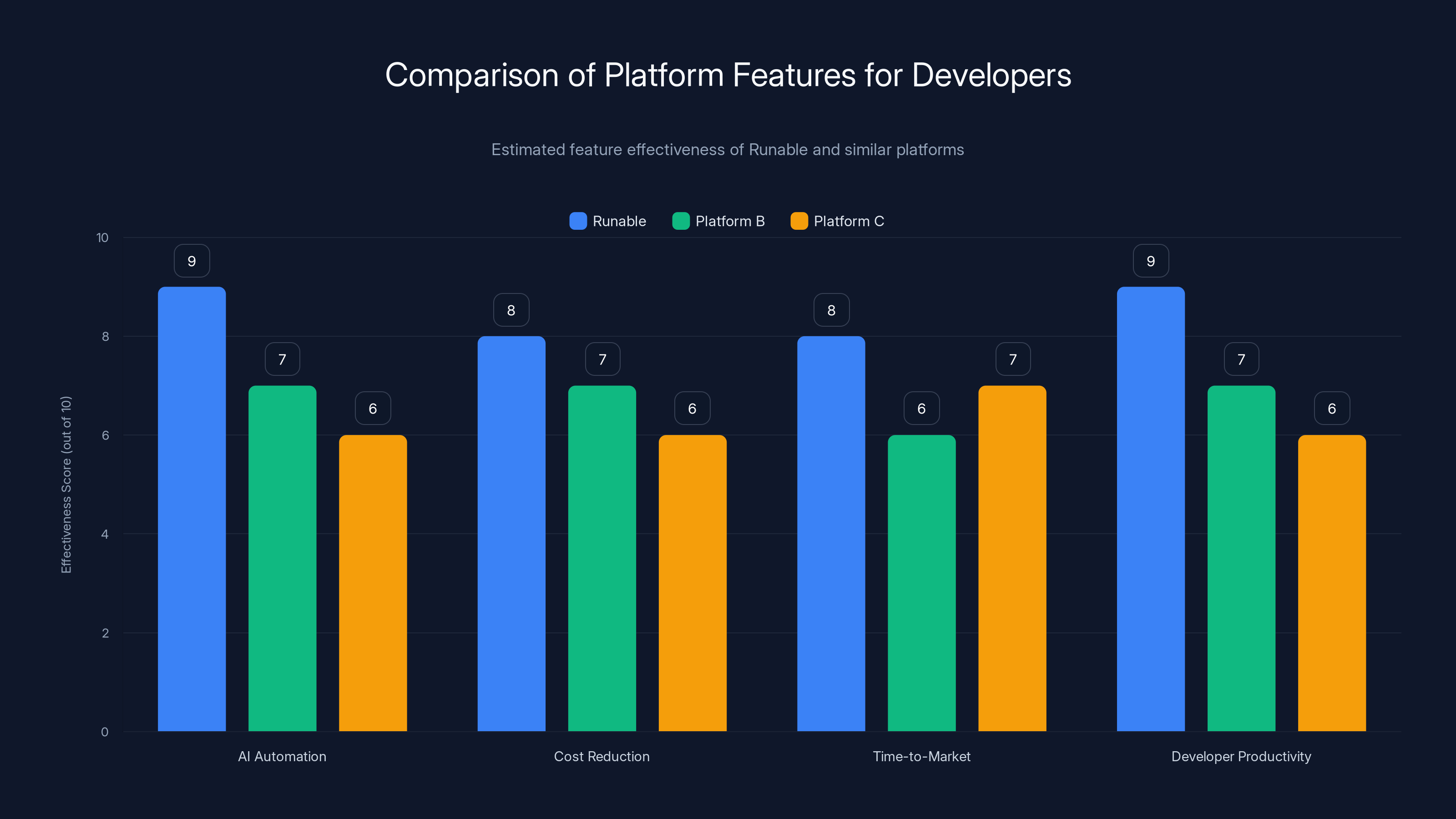

Runable scores highly in AI automation and developer productivity, making it a strong choice for reducing capital dependency. Estimated data.

Comparing AI Investment Dynamics to Traditional Industries

Venture Capital in Mature Industries

Traditional venture capital in mature industries (software, biotech, hardware) has long dealt with investor conflicts. When a VC firm invests in competing enterprise software companies, for example, the firm often maintains some exclusivity through practical realities—the fund only has so much capital, and meaningful participation in two major competitors exhausts resources.

However, even in traditional software venture capital, selective dual investing occurs. A software-focused fund might invest in competing companies if they target different market segments (one serving enterprises, another serving SMBs), different verticals (one in healthcare, another in financial services), or different technology approaches (one cloud-based, another on-premises).

The AI case is unique because the potential TAM (total addressable market) is so enormous that even competing companies might both become multi-hundred-billion-dollar businesses. Software competitors often collapse into winner-take-most dynamics where one company achieves dominance. AI currently shows signs of sustaining multiple winners, which makes dual investment more defensible (both companies can succeed financially).

Public Market Analogues and Differences

In public markets, institutional investors routinely hold positions in competing companies simultaneously. A mutual fund might hold both Apple and Microsoft shares, even though they compete in cloud services and office productivity software. The difference between public market investing and venture investing is that public investors:

- Don't have board seats or access to confidential information

- Can't exert strategic control over company decisions

- Have fully transparent information through SEC filings

- Are indifferent between which company succeeds (they own both)

- Face regulatory oversight on insider trading and other conflicts

Venture investors, by contrast, have much greater access to information, strategic control, and investor asymmetry. The public market analogy is somewhat misleading—venture investing creates fundamentally different conflict-of-interest dynamics.

Private Equity Distinctions

Private equity firms, which acquire majority or substantial minority positions in companies, maintain stricter exclusivity than venture firms. A PE firm that owns a significant stake in one company typically won't simultaneously own stakes in competitors, because doing so creates operational complexity and strategic conflicts.

The difference reflects the operational control that PE firms exercise. If a PE firm owns 60% of Company A and 40% of Company B, and they're competitors, the firm faces impossible governance questions: whose growth do we prioritize? Which company gets resources and reinvestment? How do we allocate synergies across the portfolio? The conflicts are so acute that PE firms avoid them through exclusivity.

Venture firms, which typically own minority stakes with less operational control, face less acute conflicts. But the conflicts still exist, particularly when venture firms take board seats and influence strategic direction.

Alternative Solutions: What Platforms Like Runable Offer

The Shift Toward Platform-Independent Development

As venture capital investor dynamics become more complex and potentially conflicted, some founders are exploring alternative approaches to company building that reduce dependency on single venture firms and institutional capital sources.

Platforms and tools that enable efficient, low-cost company building become increasingly attractive in this environment. For developers and entrepreneurs concerned about venture capital conflicts, platforms that reduce capital requirements and accelerate time-to-market become strategic assets.

Runable, for example, offers AI-powered automation tools for developers and teams that can significantly reduce the operational overhead typically requiring external capital. By providing tools for AI-generated content, automated workflows, and developer productivity, platforms like Runable help teams accomplish more with less external funding.

Rather than raising $30 million from potentially conflicted VC firms to build out operational and content infrastructure, teams can use AI automation platforms to achieve similar capability with lean teams. This doesn't eliminate the need for venture capital—product development and market expansion still require significant investment—but it reduces dependency on specific institutions.

For founders concerned about investor loyalty and conflict-of-interest issues, the ability to bootstrap certain functions and remain lean longer creates optionality. You can raise from fewer investors with clearer alignment rather than requiring the massive capital that forces acceptance of conflicted investors.

Cost Reduction and Capital Efficiency

The most direct way to avoid problematic venture relationships is to require less capital. AI automation tools like Runable's AI agents for document generation, workflow automation, and content creation enable teams to automate functions that previously required hiring or outsourcing.

A content-driven business—whether building documentation, generating reports, or creating presentations—traditionally required skilled writers and designers. Runable's AI tools can automate significant portions of this work, reducing the team size and associated capital requirements.

At $9/month per user, the cost is negligible compared to developer salaries or outsourced content services. The productivity acceleration means teams can achieve more with their existing personnel, stretching capital further and reducing the need for additional funding that brings investor conflicts.

This doesn't solve all problems—companies building infrastructure or pursuing aggressive market expansion still need substantial capital. But for companies in content, automation, and knowledge work spaces, tools that significantly reduce operational overhead create capital efficiency that translates to strategic flexibility.

Autonomous Teams and Reduced Hiring

Another angle where automation platforms address founder concerns relates to team composition and hiring. As companies grow, they typically hire specialists in various functions—content creators, operations, analytics, reporting. Each hire introduces complexity, dilutes cap table, and increases capital requirements.

Automation platforms that enable small teams to accomplish specialized functions reduce the hiring imperative. A three-person founding team might use Runable's AI automation capabilities to generate professional documentation, reports, and presentations that would traditionally require a content specialist. This keeps the team smaller, the cap table cleaner, and capital requirements lower.

Smaller teams also face less acute investor conflicts. A VC firm is less likely to behave unethically or acceptably conflicted toward a team of five people bootstrapping a company than toward a well-funded team already requiring ongoing investor relationships. Reducing the dependency on institutional capital reduces the power imbalance that enables conflicts.

Building Community and Alternative Capital Sources

Platforms and tools that reduce capital requirements enable alternative funding paths. Founders with lean operations can pursue:

- Revenue-based financing: Lenders willing to provide capital based on revenue without dilutive equity

- Strategic partnerships: Large companies providing capital in exchange for partnership terms

- Founder networks and angels: Crowdfunded capital from multiple smaller investors rather than concentrated VC positions

- International capital: Venture capital from geographies with different investment ethics and norms

- Corporate venture arms: Direct investment from industry players with strategic interests

Each of these alternatives has its own complications, but collectively they provide options beyond traditional VC. The ability to remain capital-efficient (through tools like Runable) creates the optionality to pursue these alternatives rather than requiring institutional VC with attendant conflicts.

Key Takeaways and Conclusions

The Permanent Transformation of Venture Capital Incentives

The acceptance of dual investments in competing AI companies by major VC firms like Sequoia, Founders Fund, and Iconiq represents a permanent transformation in how venture capital operates. This isn't a temporary response to the AI boom—it reflects fundamental shifts in capital requirements, return potential, and investor incentives that will persist beyond the current AI cycle.

Future venture capital will operate under different assumptions about investor loyalty and conflict-of-interest than the model that governed from the 1980s through the early 2010s. Founders and investors must adjust their expectations and due diligence accordingly.

Information Asymmetry as a Permanent Risk

While VC firms might establish protocols around information walls and board-seat segregation, the reality is that information leakage between companies with shared investors is a structural feature of this model, not a manageable edge case. Founders must operate with the assumption that investors with competitive interests will inevitably have access to information about competing companies.

This creates perpetual competitive disadvantage for any company that accepts investors with conflicted positions. The only solution is to either accept the risk as the cost of capital access or find alternative funding sources with clearer alignment.

Founder Agency and Due Diligence Standards

Founders must take more active roles in vetting investor conflicts before accepting capital. The traditional assumption—that major VC firms maintain ethical standards and investor loyalty automatically—can't be relied upon. Explicit conversation about conflict-of-interest policies, information walls, and competitive investment practices should become standard parts of term-sheet negotiation.

Founders also need to consider alternatives to traditional VC. Platforms and tools that reduce capital requirements (like Runable's AI automation capabilities) enable bootstrap strategies that reduce dependency on institutional capital. For founders concerned about conflicts, the ability to remain leaner longer creates negotiating power and alternative paths.

The Divergent Paths Forward

The venture capital industry likely faces divergent evolution. Some firms will continue optimizing purely for returns, accepting dual investments and managed information walls as acceptable practice. Other firms might differentiate themselves through explicit commitment to founder loyalty and exclusivity. Founders will increasingly self-select based on their priorities—those maximizing capital access will work with multi-investor firms, while those prioritizing alignment will seek firms with clear loyalty commitments.

This divergence already exists in the AI space, where Andreessen Horowitz has maintained some selectivity in AI investments while Sequoia embraced broader dual investing. Over time, this divergence will likely increase, creating a more heterogeneous venture capital market with clearer positioning around investor loyalty and conflict-of-interest standards.

The Role of Automation and Alternative Funding

As venture capital incentives shift toward accepting conflicts, alternative approaches to company building become more attractive. Teams using AI automation platforms to reduce operational overhead gain strategic flexibility. They can remain lean longer, require less capital, and therefore have more options in how they interact with institutional investors.

This doesn't eliminate the need for venture capital or the importance of investor relationships. But it creates a more balanced power dynamic. Rather than founders desperately needing capital and accepting whatever conditions come with it, founders with operational efficiency can make more choices about which investors to work with.

Platforms like Runable, which provide AI-powered automation for content generation, workflow management, and developer productivity, exemplify tools that enable this more efficient approach to company building. By reducing the headcount and specialized skill requirements for various functions, these tools help teams achieve more with less external capital.

Long-Term Industry Health Considerations

From an ecosystem perspective, the decline of investor loyalty creates both opportunities and risks. The opportunity is that capital flows more efficiently toward the most valuable opportunities regardless of existing portfolio incumbents. The risk is that information asymmetries and conflicted incentives create unfair competitive dynamics that reward larger, better-positioned companies over emerging challengers.

The AI industry specifically faces risks from investor conflicts because the competitive landscape is still forming. The companies that establish dominance in the next 3-5 years will likely shape the industry for decades. If investors with conflicts systematically advantage incumbents over challengers through information asymmetries and strategic biases, the resulting competitive dynamics might be suboptimal from an innovation perspective.

However, these concerns haven't generated regulatory response or institutional change yet. The market seems to have accepted investor conflicts as the new normal. Founders and entrepreneurs must operate accordingly.

Final Thoughts: A New Era of Startup-Investor Relations

We're at the end of an era where venture capitalists consistently positioned themselves as founder-friendly, loyal, and committed partners primarily interested in portfolio company success. The AI investment landscape revealed that these commitments are conditional on opportunity cost and return potential—when the cost of loyalty becomes enormous enough, the loyalty disappears.

This doesn't make venture capitalists uniquely unethical or opportunistic. It reflects the reality that institutions optimize according to the incentives they face. When capital requirements become large enough and return potential becomes compelling enough, even carefully constructed ethical frameworks will erode under the pressure of financial incentives.

Founders entering the venture capital landscape should understand this reality, adjust expectations accordingly, and seek structures that align incentives more fully or provide alternatives that reduce capital dependency. The age of assuming investor loyalty simply must end.

FAQ

What is investor loyalty in venture capital?

Investor loyalty refers to the traditional venture capital practice where firms would maintain exclusivity around their investments, avoiding simultaneous investments in direct competitors. This principle emerged as a cornerstone of VC culture from the 1980s onward, with the assumption that VCs would protect portfolio companies' confidential information, prioritize their strategic interests, and avoid conflicts that could harm their success. The practice was built on both ethical principles and legal frameworks around fiduciary duty and board-level obligations.

Why are venture capital firms now investing in competing AI companies?

Venture capital firms are participating in simultaneous investments in competing AI companies like Open AI and Anthropic primarily due to the unprecedented scale of capital requirements and return potential. With Open AI's Series C targeting

How does investor conflict of interest affect founders and startups?

Investor conflicts create information asymmetry risks where your venture capitalist's board access to Open AI (or your competitor) could theoretically benefit that competitor through implicit knowledge transfer, pattern observation, and inference from firm discussions. Even with formal information walls, cognitive integration of competitive intelligence happens naturally in shared firm environments. Founders also lose the traditional benefit of having an investor whose primary motivation is their company's success—a conflicted investor's attention and resources might be divided. Early-stage companies face particular disadvantage because larger competitors in the same investor's portfolio might receive preferential treatment or access to investor resources.

What information do board-seat investors actually have access to?

Venture capitalists with board seats receive detailed confidential information including monthly/quarterly financial performance data, strategic product roadmaps, detailed customer lists and contract values, proprietary technology details and architectures, formal competitive assessments, hiring and organizational plans, and detailed fundraising strategies. This information represents the crown jewels of competitive advantage, particularly for AI companies where training data sources, model architectures, and safety approaches constitute core differentiation. Even without explicit information sharing, having access to this intelligence about one company while simultaneously investing in a competitor creates structural risks of competitive disadvantage.

How should founders evaluate venture capitalist conflicts of interest?

Founders should add explicit conflict-of-interest due diligence to their investor evaluation process by requesting a clear list of existing portfolio companies in adjacent spaces, asking about formal policies restricting simultaneous investments in competitors, understanding specific protocols for information protection, requesting clarity about which partners will represent them and their other commitments, and requesting explicit information about whether conflicted investors maintain board seats versus financial-only positions. Founders might also consider alternative funding sources, use automation platforms like Runable to reduce capital requirements, or pursue non-traditional funding (revenue-based financing, strategic partnerships) to reduce dependency on potentially conflicted institutional investors.