![India's $1.1B State-Backed VC Fund: Deep-Tech Boom [2025]](https://tryrunable.com/blog/india-s-1-1b-state-backed-vc-fund-deep-tech-boom-2025/image-1-1771087135639.jpg)

India's $1.1 Billion State-Backed Venture Capital Fund: The Government's Bold Bet on Deep-Tech Innovation

India just made a major move in the venture capital playbook. In February 2025, the government cleared a $1.1 billion state-backed venture capital program—a massive push to inject public money into startups through private investors. This isn't just another funding round. It's a strategic bet that deep-tech and advanced manufacturing will define India's next decade of innovation.

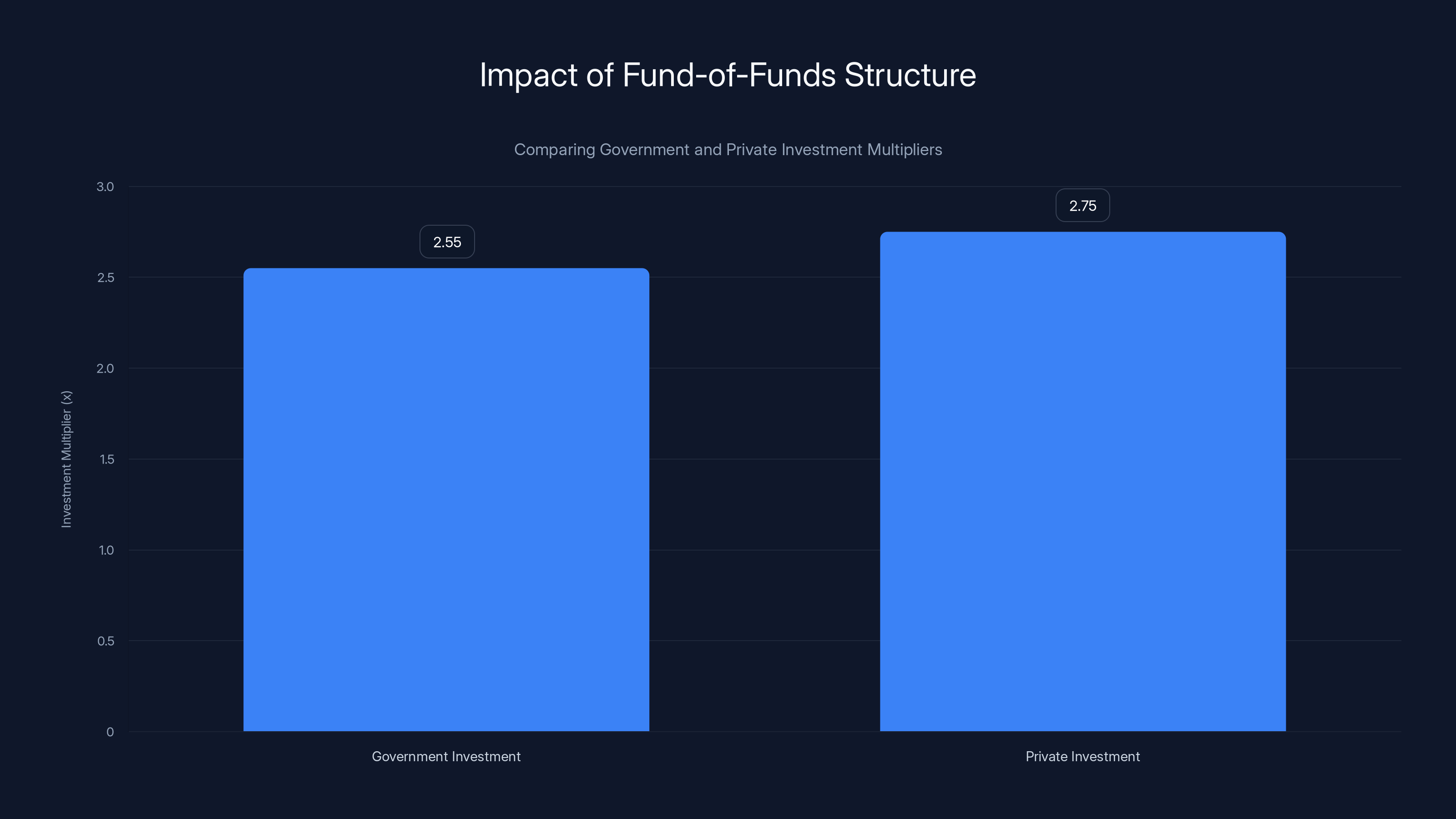

Here's what makes this different from typical government initiatives. The program operates as a fund-of-funds, meaning the government doesn't pick individual startups directly. Instead, it backs private venture capital firms that make the actual investment decisions. This indirect approach has proven effective before. India's previous iteration, launched in 2016, deployed ₹100 billion (roughly $1.2 billion at current rates) across 145 private funds, which then invested over ₹255 billion into more than 1,370 startups. That's real money hitting real companies.

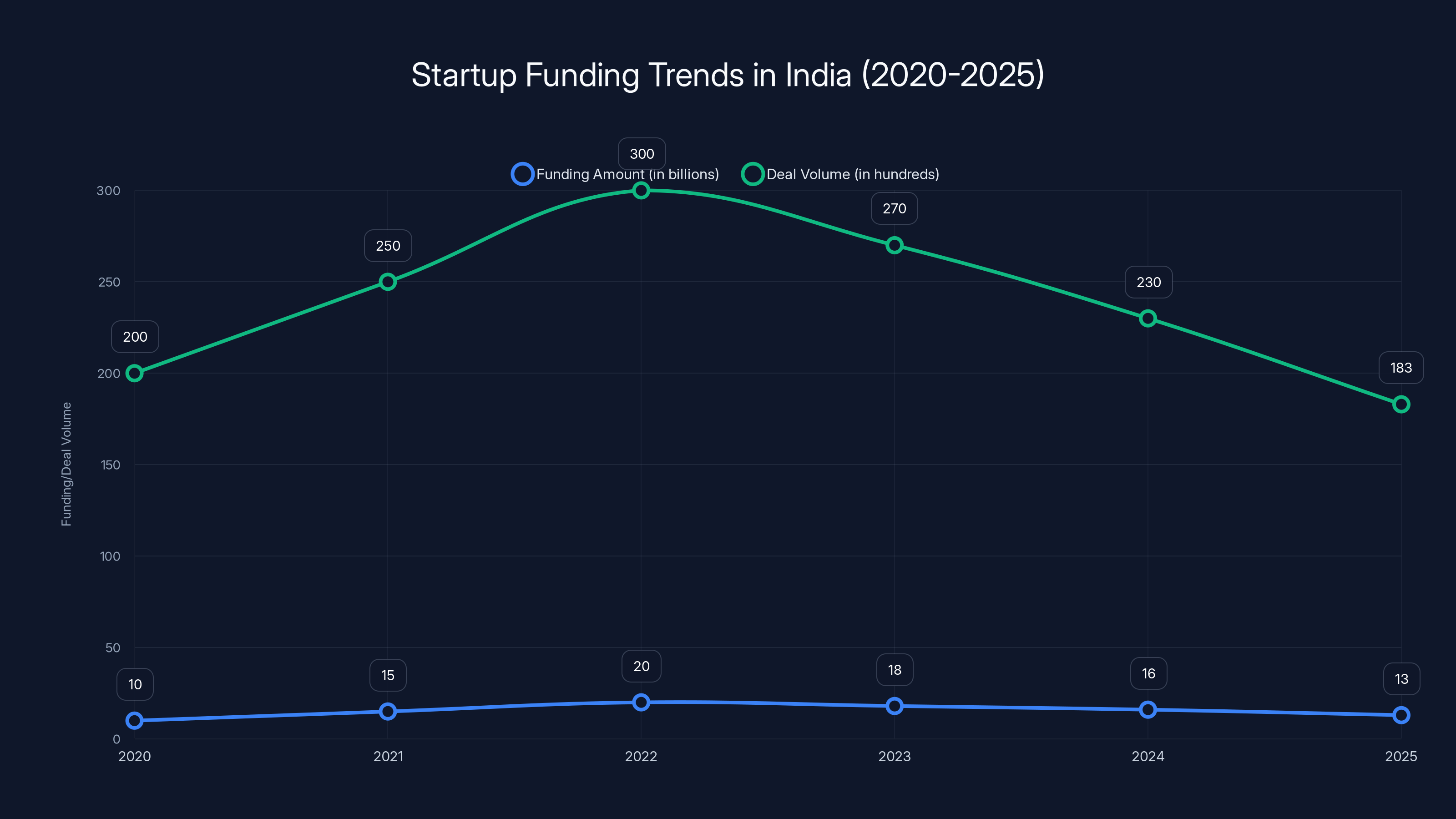

But here's the catch that nobody talks about. India's startup ecosystem faced serious headwinds in 2025. Funding dropped 17% year-over-year to

The timing is strategic, not accidental. The Indian government announced this initiative in its January 2025 budget speech, but cabinet approval took over a year. Why the delay? Government bureaucracy, policy refinement, stakeholder consultations—the usual friction. Yet now that it's approved, the deployment can finally accelerate.

What's compelling about this initiative isn't just the size. It's the targeting. Previous programs cast wide nets. This one focuses laser-sharp on deep-tech and manufacturing sectors—areas where India wants to build global competitive advantage. AI, quantum computing, biotech, advanced materials, semiconductors, and industrial automation. These aren't sexy consumer apps that go viral. They're infrastructure plays. Foundation-layer technology that takes five to ten years to mature but creates trillion-dollar businesses if you get them right.

India's government clearly understands something that venture capital hasn't fully grasped yet. The best returns don't come from social media platforms or consumer SaaS. They come from solving hard technical problems at scale. And India, with its massive talent pool and growing engineering prowess, is positioned to be a serious competitor in these sectors.

TL; DR

- $1.1B fund approved: India's government cleared a state-backed venture capital program to invest through private VCs

- Deep-tech focus: The fund targets AI, advanced manufacturing, and long-horizon innovation sectors

- Previous success: The 2016 iteration deployed $1.2B across 145 funds and backed over 1,370 startups

- Ecosystem context: India's startup funding dropped 17% in 2025, making government capital more critical

- Strategic timing: Extended startup classification to 20 years and raised revenue thresholds to support long-term deep-tech companies

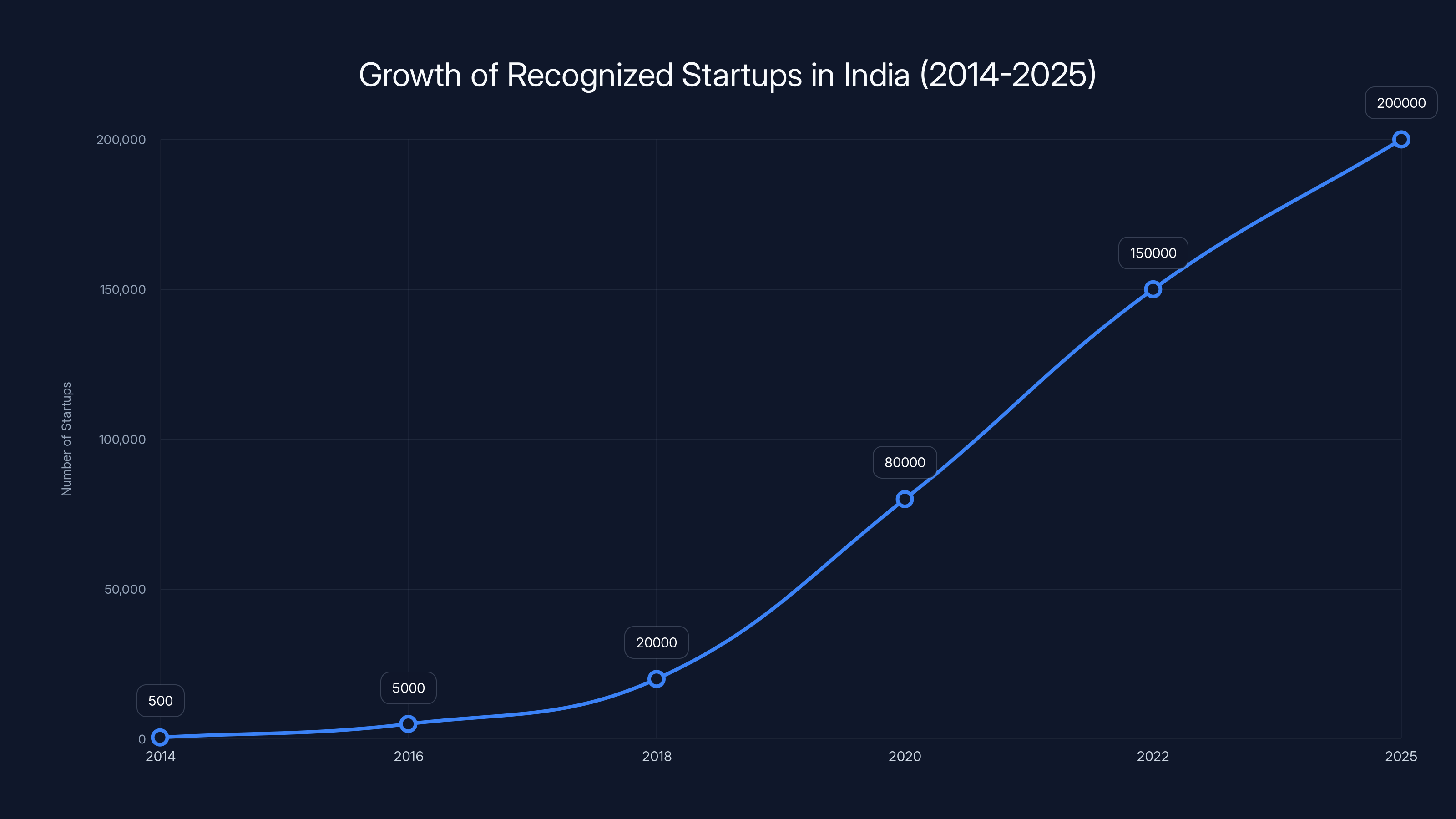

India's startup ecosystem has experienced exponential growth, from fewer than 500 startups in 2014 to over 200,000 projected by 2025. This growth is driven by increased internet penetration, affordable technology, and successful exits. (Estimated data)

Why Government Capital Matters Now More Than Ever

You need to understand the economics of deep-tech to grasp why government money is essential here. Consumer startups can bootstrap or raise seed rounds at $1-5 million. They hit profitability or hit a wall within 18-24 months. Either they grow or they die. The feedback loop is fast.

Deep-tech works differently. A quantum computing startup needs

Private venture capital has become increasingly short-term focused. Returns matter. Management fees are paid annually regardless of performance, but LPs demand exits within 10 years. Venture funds chase hype cycles. In 2021, everyone invested in crypto. In 2023, everyone invested in AI. Actual deep-tech work? That requires patience. That requires accepting that a company might spend $10 million annually for a decade with no revenue. That's not compatible with venture fund economics.

This is where government capital becomes invaluable. Governments think in decades, not quarters. They care about building national capabilities, not quarterly IRR targets. They can hold investments longer. They accept lower returns if the strategic payoff is building a domestic semiconductor industry or AI research capability.

India's approach is smarter than it might appear. By using a fund-of-funds structure, the government gets professional management—private VCs make investment decisions—while providing patient capital. Private funds handle selection, monitoring, and exit management. Government capital provides the dry powder that lets those funds take bigger bets on riskier technologies.

Consider the scale problem. India has 49,000 newly registered startups annually. Most are consumer software or B2B SaaS—important, but not particularly novel. Deep-tech companies? Maybe 5-10% of that total. These companies get starved for capital because they're harder to understand and slower to return money. A fund-of-funds approach solves this by creating institutional incentives to actually fund these companies systematically.

The Startup Ecosystem Context: From 500 to 200,000 in Nine Years

To understand why this funding matters, you need the context. Nine years ago, India had fewer than 500 recognized startups. Today, that number exceeds 200,000. The 2025 annual total hit 49,000 new registrations—a record. This isn't gradual growth. It's exponential scaling.

Where did this explosion come from? Several factors converged. Internet penetration crossed critical mass around 2014-2015. India's mobile-first population became accessible to digital products. Cheap smartphones and data plans meant founders could reach millions of users without expensive infrastructure. Venture capital discovered India as an arbitrage opportunity—you could build a company in India for 30% of the cost of doing it in Silicon Valley.

Successful exits changed the game. Companies like Flipkart (sold to Walmart for $16 billion), Paytm (IPO), and Ola (unicorn valuations) proved that billion-dollar businesses could be built in India. That success created a blueprint. It also created wealth. Founders from those early exits became angels and micro-VCs backing the next generation.

But here's where the narrative gets interesting. Most of that growth happened in B2B services, consumer apps, and fintech. Easy markets. Markets with immediate PMF signals. Founder-friendly sectors that attract capital quickly because they generate revenue fast.

Deep-tech never scaled the same way. Why? Risk. Long timelines. Difficulty. A typical deep-tech founder might spend two years building and get zero revenue. During those two years, she can't raise from traditional VCs because there's nothing to show. She can't bootstrap because deep-tech costs money. She either needs wealthy angels (rare in India) or she pivots to something easier.

The government is trying to solve this structural problem. By creating institutional capital explicitly for deep-tech, they're removing the constraint. Suddenly, brilliant engineers working on quantum algorithms don't have to work for Google. They can start companies. Researchers in advanced materials don't need to work for CSIR labs. They can commercialize their work.

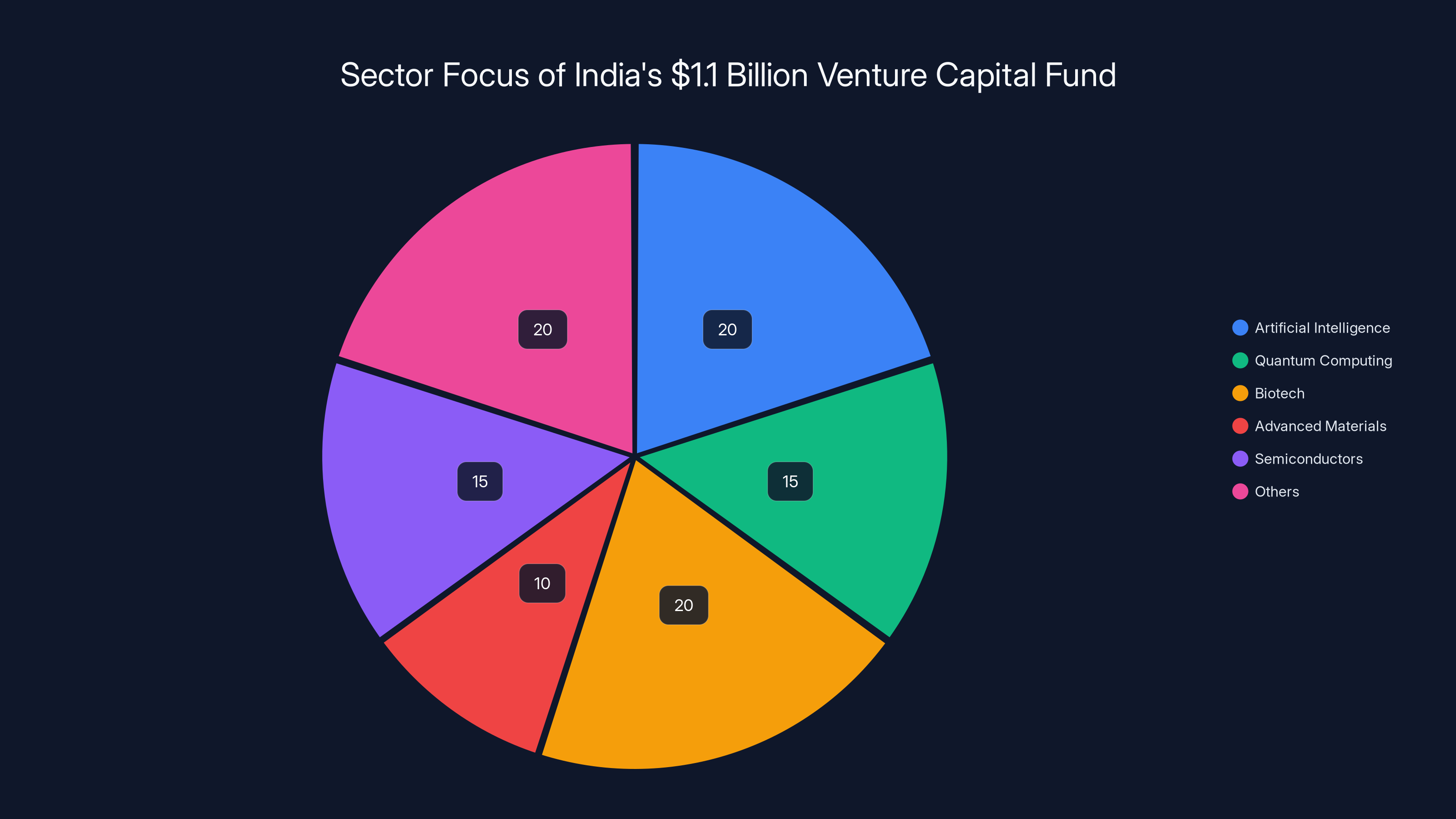

Estimated data suggests a balanced allocation across key sectors like AI, biotech, and semiconductors, each receiving significant attention to foster innovation.

Fund-of-Funds Structure: How It Actually Works

Understanding the mechanics matters here because it explains why this is cleverer than just dumping $1.1 billion into random startups.

A traditional venture capital fund works like this. Investors (LPs) commit money. A fund manager (GP) takes 20% carry on returns and 2% annual fees. The GP invests in 30-50 companies. Most fail. A few succeed spectacularly. If the fund returns 3x, it's considered successful.

A fund-of-funds is different. The government acts as LP. Instead of investing directly in startups, it commits capital to existing venture funds. Those funds then make the actual startup investments. From the government's perspective, they get professional management and diversification. From the VCs' perspective, they get patient capital from an LP with long time horizons.

Here's the clever part. The government's money doesn't crowded out private capital. Instead, it unlocks it. A private VC fund might raise

The 2016 version of this program deployed ₹100 billion across 145 funds. That's an average of ₹690 million per fund—roughly $8.3 million. Most of these were smaller VCs, regional funds, and emerging managers who couldn't raise that amount from traditional LPs. By backing these funds, the government effectively created a middle layer of the venture capital market that didn't exist before.

Data supports this worked. Those 145 funds deployed over ₹255 billion into 1,370 startups. That's a 2.55x multiple on the government's initial capital just in follow-on investments. Private investors matched or exceeded the government money. The multiplier effect is real.

The new $1.1 billion fund is likely to follow a similar model. It won't invest directly. It will commit to existing funds with mandates for deep-tech and manufacturing. Those funds will deploy the capital over five to seven years. The government's role is catalyst, not operator.

This matters because it answers the question everyone should ask: why can't the government just invest the money directly? Answer: they could, but it would be worse. Governments are bad at picking startups. They're political. They create corruption risks. They lack domain expertise. They move slowly. By delegating actual investment decisions to professional VCs, the government gets better capital deployment and avoids the political minefield.

Deep-Tech Focus: AI, Manufacturing, and Long-Horizon Innovation

The fund's explicit focus on deep-tech isn't random. It reflects strategic thinking about where India can compete globally.

Artificial intelligence is the obvious one. India has massive AI talent. The country trains more engineers annually than any other nation. Indian engineers built significant portions of major AI systems at Google, Meta, OpenAI, and Anthropic. Brain drain is real, but reversing it is possible if you can offer interesting problems and capital to solve them.

Where can India win in AI? Not in foundation models. That's locked up by the US and China with their massive capital reserves and computational resources. But vertical AI solutions? Industry-specific applications? Building AI systems for Indian use cases? Absolutely. A company building AI for agricultural optimization in the subcontinent has an unfair advantage. It understands the problem deeply. It has access to relevant data. It can serve millions of farmers who speak regional languages. That's defensible competitive advantage.

Advanced manufacturing is even more strategic. India wants to reduce dependence on imports for semiconductors, electronics, and advanced materials. The government has launched the Production-Linked Incentive scheme (PLI) to attract manufacturing. But PLI programs just subsidize existing manufacturing. You also need innovation in manufacturing processes, automation, and materials science.

Deep-tech plays here are obvious. Robotics for factory automation. Advanced materials for electronics. Semiconductor design and fabrication tools. AI for supply chain optimization. These aren't cool consumer products, but they're the foundation for industrial leadership.

Biotech and healthcare innovation matter too. India is the world's largest producer of generic pharmaceuticals. But generics are low-margin. The future is in biologics, gene therapy, and personalized medicine. Building biotech capabilities requires patient capital and world-class talent. Both are available in India.

Quantum computing, renewable energy technology, climate tech—these are global megatrends. India can't ignore them. A quantum computer built by an Indian company would be a landmark achievement. Renewable energy technology developed in India would serve the world's most challenging deployment environments—the subcontinent's grid with its constraints and scale.

The common thread? These sectors require long timelines, serious capital, and top-tier talent. They're not spaces where traditional venture capital can operate profitably. But they're spaces where nations build enduring competitive advantages. That's why government capital is appropriate here.

Policy Changes: Extended Runway for Deep-Tech Startups

The government didn't just approve capital. They also changed the rules to help deep-tech companies survive longer.

Startups in India get special tax benefits, regulatory breaks, and grant eligibility. But these benefits have conditions. You can only call yourself a startup for five years. After that, you're classified as a regular company and lose the benefits. For deep-tech companies, five years is nothing. You're still in development phase. You haven't generated revenue. You shouldn't graduate to standard corporate taxation yet.

The new policy doubles this window. Startups can now maintain their classification for 20 years if they're working in deep-tech or specified manufacturing sectors. This is huge. A quantum computing company has two decades to develop its technology before facing the full tax and regulatory burden. A biotech startup can spend 15 years on R&D and clinical trials without losing benefits.

The government also raised the revenue threshold for startup classification. Previously, companies with over ₹1 billion in annual revenue (

Why does this matter? Tax breaks for startups typically include reduced corporate tax rates and exemptions from certain regulations. For a deep-tech company burning

Regulatory breaks are even more valuable. A biotech startup doesn't have to jump through all the hoops a pharma company must. An autonomous vehicle company gets exemptions from certain safety regulations during testing. These breaks accelerate development and reduce compliance costs.

The 20-year window signals something else: patience. The government is saying "we understand you won't hit the metrics of a normal company for a long time, and that's okay." This psychological signal matters. Founders can build without watching the clock.

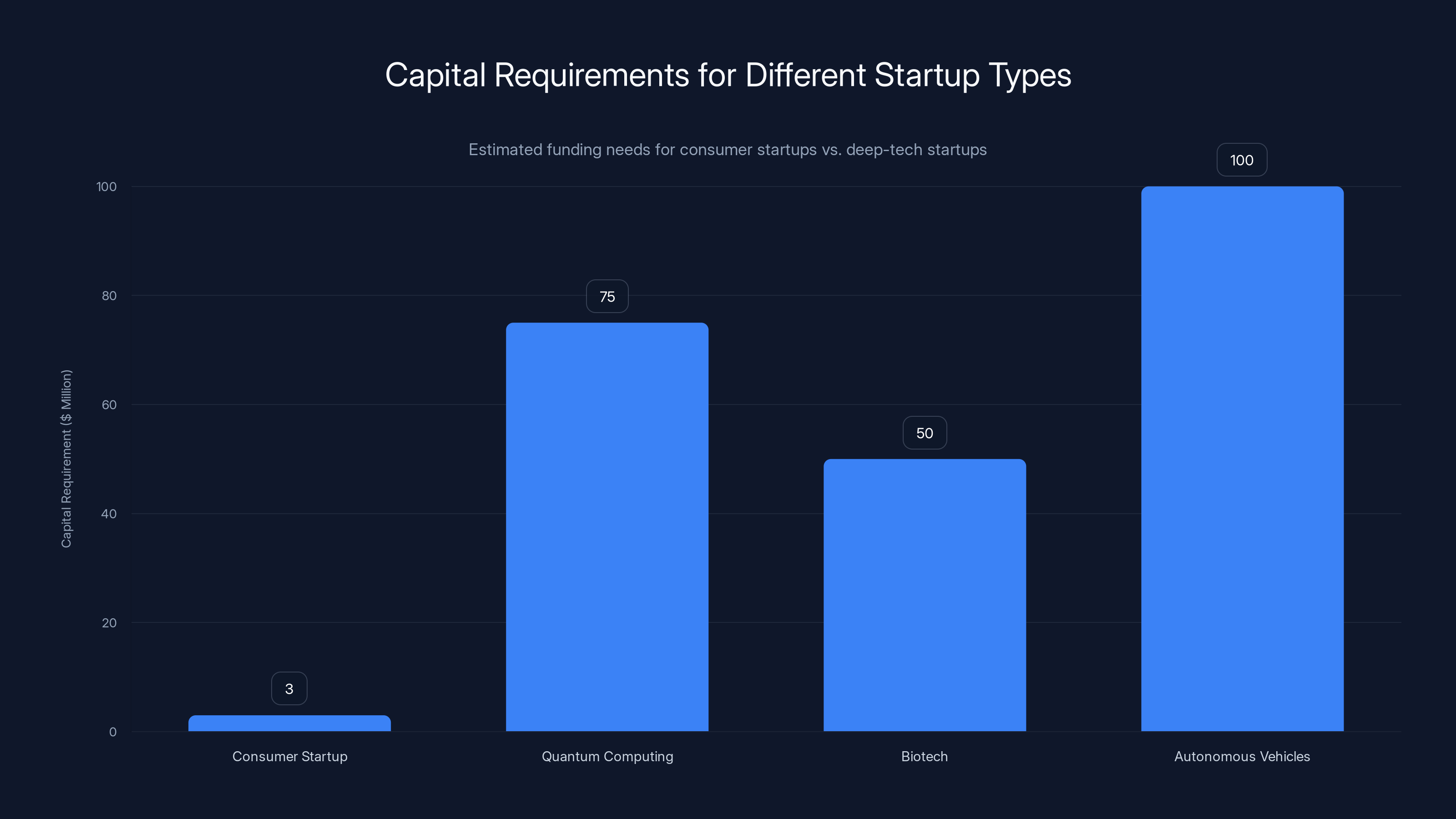

Deep-tech startups like quantum computing and autonomous vehicles require significantly higher capital compared to consumer startups, highlighting the importance of government funding. Estimated data.

The 2016 Precedent: What Worked and What Didn't

Analyzing the previous program reveals what worked and what needs improvement in the new fund.

The 2016 program deployed ₹100 billion across 145 funds and those funds invested over ₹255 billion in 1,370 startups. The headline numbers look good. But what about outcomes?

There's limited public data on how many of those companies survived, grew, or exited. This is a common problem with government-backed programs—transparency is lacking. But we can infer from ecosystem trends. India's startup ecosystem grew massively from 2016 to 2021, then contracted in 2022-2025. The program probably backed some winners and many duds, like all venture capital.

What worked: The fund-of-funds structure got capital to smaller VCs who otherwise couldn't raise this amount. The program increased the number of institutional VCs in India. It democratized access to capital beyond just Bangalore, Mumbai, and Delhi. Companies in Tier 2 and Tier 3 cities started getting funded.

What didn't work: The program was too broad. It backed everything from consumer apps to logistics to fintech. There was no strategic focus. Money was deployed quickly to hit targets, possibly without sufficient quality filters. Some of the funds were inexperienced, leading to poor outcomes. The program didn't explicitly back deep-tech, so much of the capital went to easier, faster-return opportunities.

The new program appears to have learned these lessons. It's narrower in scope—deep-tech and manufacturing only. It includes a 20-year classification window, showing the government understands these companies need more time. It's backed by policy changes that support long-term development.

But risks remain. Will the government actually stick to deep-tech focus, or will political pressure to deploy capital quickly lead to mission creep? Will smaller VCs, now flush with capital, make smart investments or follow herd behavior? Will exits happen at reasonable valuations or will government capital distort pricing?

These are open questions. The proof will be in the results over the next 3-5 years.

India's Global Startup Ranking and Its Aspirations

Context matters. Where does India stand globally in startup ecosystems?

By number of startups, India is top three worldwide. By funding volume, it's top five. By unicorn count, it's top three. By talent availability, it's number one by sheer volume. By innovation, it lags Silicon Valley and China but punches above its weight in certain sectors.

Where India wants to punch up is in deep-tech and manufacturing innovation. The US and China dominate semiconductor design and fabrication. Both countries have invested decades and hundreds of billions in building these capabilities. India is trying to leapfrog through a combination of subsidies (PLI scheme), talent attraction, and now venture capital.

The political calculation is explicit. India's government wants to reduce dependence on China for electronics and advanced materials. It wants to build indigenous AI capabilities. It wants to stop exporting raw talent to Silicon Valley and instead create companies that keep talent in India.

This is why $1.1 billion matters as a signal more than as absolute capital. It says "deep-tech is a national priority." It tells founders "build hard things, we'll back you." It tells VCs "focus on deep-tech, here's capital." It tells the world "India is serious about innovation beyond apps."

Compare this to how China approached deep-tech. The Chinese government didn't just provide capital. It provided talent access, manufacturing partnerships, intellectual property protection, and preferential market access. India is starting to do something similar. The venture capital is one piece of a bigger strategy.

The AI Impact Summit and Global Tech Investment Signals

The timing of this fund approval with the India AI Impact Summit isn't coincidental. Both events signal that India is becoming central to global tech strategy.

The summit attracted major players—OpenAI, Anthropic, Google, Meta, Microsoft, Nvidia. These companies wouldn't show up if India wasn't strategically important. They're not interested in just selling products. They're interested in talent access, R&D partnerships, and positioning for the next generation of AI competition.

OpenAI is particularly revealing. They opened their first office in India and are explicitly recruiting. Why? Because India has AI talent and OpenAI needs scale. Microsoft sees India as critical for cloud computing and AI service deployment. Google sees India as the largest internet market and a crucial geography for Gemini deployment. Meta sees billions of potential users.

When global tech companies are making bets on India, government capital becomes more valuable. If Microsoft invests $2.4 billion in India (which they have), that creates ecosystem momentum. When founders see Nvidia setting up R&D here, it becomes real. Government capital at the right moments amplifies these signals.

The summit also serves another purpose. It brings international investors and entrepreneurs to India. They see what's being built. They get exposed to companies that might not be on their radar. This drives private capital inflows that complement government funding.

The fund-of-funds model resulted in a 2.55x multiplier on government capital, with private investors matching or exceeding this, demonstrating the model's effectiveness in leveraging additional capital.

The Funding Contraction Problem and Why It Matters

Here's the shadow context everyone should understand. India's startup funding contracted 17% in 2025. Deal volume crashed 39%. This isn't growth. This is a correction.

What happened? The 2020-2022 period was a funding frenzy. Investors had cheap money from central banks. Fear of missing out on the "next unicorn" drove valuations insane. Companies with zero revenue and uncertain paths to profitability raised at stratospheric valuations. Founders who couldn't execute got funded anyway because capital was abundant.

Then it ended. Interest rates rose. Central banks stopped printing money. Returns from previous rounds disappointed investors. The realization hit: most startups fail, and the ones funded with inflated valuations have no path to profitability.

By 2025, selectivity became brutal. VCs focused on companies with clear paths to profitability, reasonable metrics, and experienced teams. Founders struggled to raise. Many of the 2021-2022 startups ran out of money and shut down.

Into this environment, the government is deploying $1.1 billion specifically for long-duration, hard-tech companies. This capital isn't seeking exits within five years. It's not competing with traditional VCs for the same deal flow. It's creating a different investment class.

For founders, this is lifesaving. A deep-tech team that couldn't raise Series A from private VCs because there's no revenue can now get funded. A biotech startup in a smaller city, building something complex but valuable, gets a chance. This fund provides alternatives to the traditional venture market when traditional capital is scarce.

The 17% funding contraction actually makes this capital more valuable, not less. When capital is scarce, patient capital becomes strategic. When returns are hard to achieve quickly, long-duration investors can survive periods where traditional VCs pull back.

Deep-Tech Definition and What Qualifies

What exactly counts as deep-tech for this fund? The government has implied criteria, but clarity matters.

Deep-tech broadly refers to companies building foundational technology that's hardware-intensive, capital-intensive, science-based, and difficult to replicate. Quantum computing is deep-tech. A SaaS analytics tool is not. Biotech is deep-tech. A social media app is not.

Examples the government likely includes: robotics, semiconductors, battery technology, biotech, advanced materials, quantum computing, synthetic biology, climate tech, aerospace, autonomous vehicles (hardware-focused), and advanced manufacturing processes.

Examples excluded: mobile apps, e-commerce, consumer SaaS, social media, digital marketing tools, and fintech software (unless it's truly novel architecture).

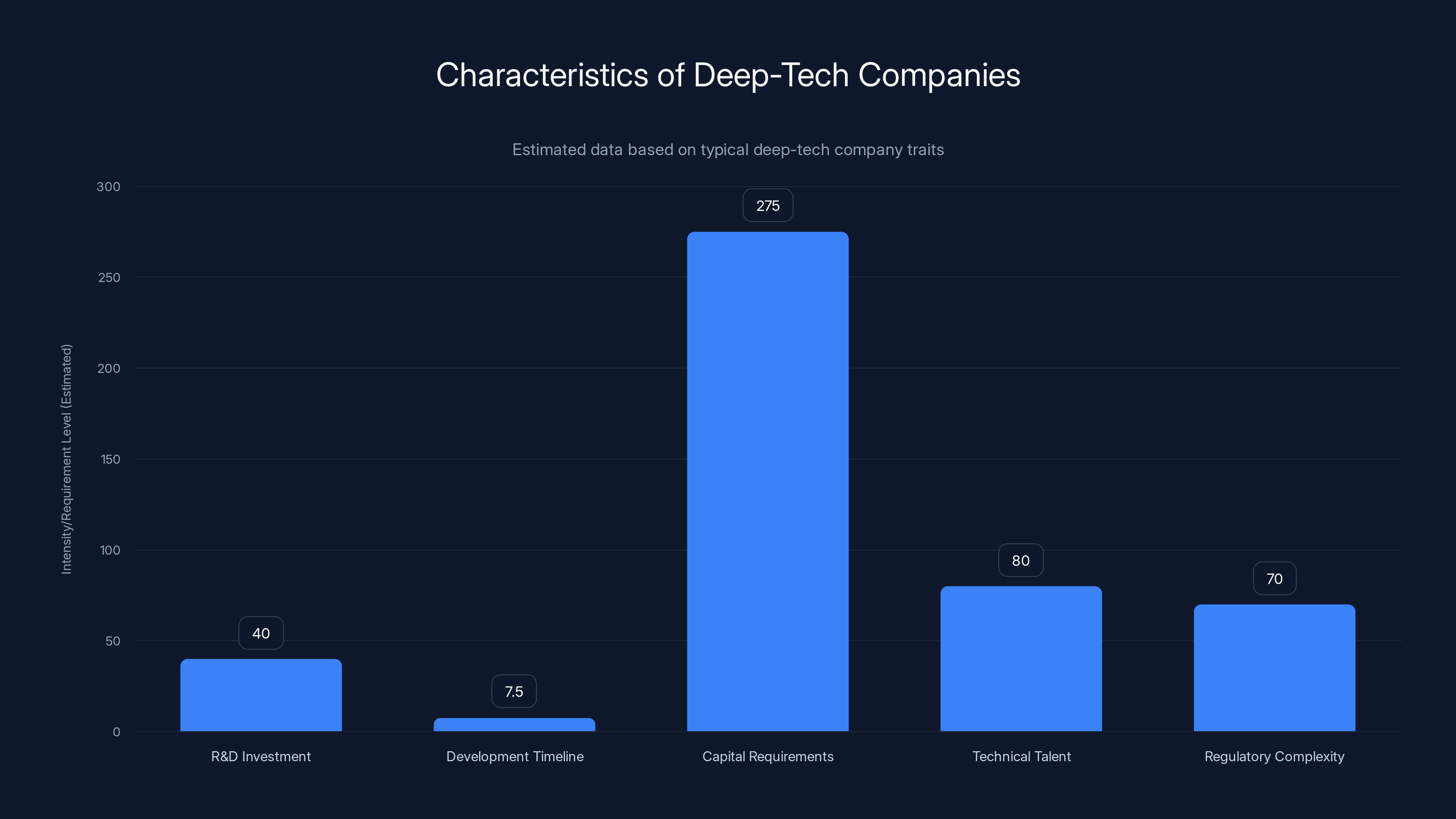

The distinction matters because deep-tech companies typically require:

- Significant R&D Investment: 30-50% of revenue going to research, sometimes before there's any revenue

- Long Development Timelines: 5-10 years to develop and commercialize technology

- Large Capital Requirements: 500 million before meaningful revenue

- Technical Talent Requirements: PhDs, researchers, and highly specialized engineers

- Regulatory Complexity: Approval processes, safety standards, compliance requirements

- Competitive Moats: Defensible IP, difficult-to-replicate technology, patents

These characteristics make deep-tech unsuitable for typical venture capital, which seeks 5-7 year exits and demands revenue traction early. This fund is designed for exactly these characteristics.

The question is whether the fund will stay disciplined about what counts as deep-tech or whether the definition will expand. Regulatory capture is a risk. Founders will claim they're doing deep-tech when they're not. VCs will rationalize soft definitions to deploy capital faster. The government will face pressure to "move the money" to hit deployment targets.

Maintaining rigor on definition will be critical to the program's success.

Global Comparisons: How Other Nations Fund Deep-Tech

India isn't alone in backing deep-tech with government capital. Understanding how other countries do it provides perspective.

The United States: The US government doesn't run explicit venture funds, but it provides deep-tech capital through DARPA (Defense Advanced Research Projects Agency), NSF (National Science Foundation), NIH (National Institutes of Health), and DOE (Department of Energy). These agencies fund research and early-stage companies. DARPA alone distributes roughly $3-4 billion annually to advanced technology development.

China: The Chinese government backs deep-tech aggressively through state-owned enterprises, sovereign wealth funds, and explicit venture programs. The National Integrated Circuit Industry Investment Fund controls tens of billions specifically for semiconductors. China also uses industrial policy—preferential access to state-owned enterprise procurement—to support domestic deep-tech winners.

Israel: The Israeli government runs OCS (Office of the Chief Scientist), which funds early-stage R&D and de-risks technology development. This capital then attracts venture funding. The model is government de-risking followed by private capital scaling. Israel has become a deep-tech powerhouse through this approach.

Singapore: The government runs Enterprise Singapore and Spring Singapore, which provide grants and equity investments for deep-tech startups. Capital is modest compared to China or the US, but focused and disciplined.

Europe: Various European nations run deep-tech funds. Germany has KfW (development bank) programs for innovation. France has BPI France backing deep-tech. The EU has the European Innovation Council. European governments explicitly recognize venture capital alone won't fund century-long research timelines.

What India is doing is squarely in this tradition. Government as de-risker and catalyst for deep-tech development. The $1.1 billion is modest compared to what China deploys, but proportional to India's development stage and budget constraints.

The comparison also reveals what works: discipline on focus, patience with timelines, and integration with broader industrial policy. India's PLI scheme for manufacturing, the 20-year startup classification, and this venture fund form a coherent strategy, not isolated programs.

The chart illustrates the contraction in startup funding and deal volume in India from 2020 to 2025, highlighting a 17% drop in funding and a 39% drop in deal volume by 2025. Estimated data.

Risk Factors: What Could Go Wrong

This fund is promising, but risks are real.

Risk 1: Mission Creep: Pressure to deploy capital quickly could lead to funding non-deep-tech companies. A founder claims their logistics software is deep-tech. A software company claims they're building advanced manufacturing algorithms. The line blurs. Capital flows to easier, faster-return opportunities. The fund becomes just another venture program.

Risk 2: Poor Fund Selection: The government picks which VCs get capital. This is a political process, not purely meritocratic. Well-connected mediocre VCs might get funded. Brilliant emerging managers might be overlooked. Fund quality matters enormously in venture capital. Bad managers with capital destroy returns.

Risk 3: Regulatory Burden: Deep-tech companies need regulatory approval. A biotech startup needs drug approvals. An autonomous vehicle needs safety certification. An AI system needs governance review. Government capital creates an incentive to also create more regulatory barriers, protecting funded companies from competition. This could inhibit innovation overall.

Risk 4: Valuation Distortion: Government capital, if undisciplined, inflates valuations. Founders expect easy money. That makes it harder for other companies to raise at reasonable valuations. It also sets founders' expectations unrealistically, leading to failures later.

Risk 5: Talent Concentration: Billions in capital directed to deep-tech will attract talent. But India's talent pool in deep-tech fields like quantum computing or advanced materials is small. Concentrating too much capital in too few companies could create bubbles in specific sectors.

Risk 6: Execution Risk: Government fund management requires competent people. India needs experienced VCs managing the deployments. If the management team is weak, outcomes will be weak. This isn't automated. It requires skill.

These risks aren't disqualifying. They're manageable with good governance. But they're real, and success isn't guaranteed. The fund could produce great outcomes or mediocre ones depending on execution.

Private Sector Response and Investor Sentiment

How are private VCs and entrepreneurs responding to this announcement?

Sentiment among private VCs appears cautiously optimistic. More capital in the ecosystem is good for everyone. A rising tide lifts all boats. If the government successfully de-risks deep-tech investing, private VCs benefit by getting better deal flow and clearer market signals about which sectors to focus on.

But there's also defensiveness. Private VCs worry the government might preferentially deploy capital to state-sponsored funds or companies aligned with government priorities. They worry about competing against subsidized capital. They worry the government might become a VC itself, directly picking winners, which would be disastrous because government VCs are terrible at picking startups.

Entrepreneur sentiment is probably more enthusiastic. For deep-tech founders, this is the capital source they've been waiting for. A quantum computing founder who couldn't raise Series A suddenly has hope. A biotech founder working on novel therapies can now think long-term.

For consumer and B2B SaaS founders, this changes nothing. The $1.1 billion isn't for them. Traditional venture capital already funds these sectors adequately. If anything, this fund removes some competition for generalist capital, making it easier for SaaS founders to raise in the private market.

The broader signal is that the Indian government is serious about technology leadership. That attracts global attention. If global investors believe India will become a deep-tech hub, they'll deploy capital there themselves. This $1.1 billion is seed capital for much larger private flows.

Timeline for Deployment and Expected Outcomes

When will this capital actually reach startups?

Based on the 2016 program's timeline, deployment takes 18-24 months. Cabinet approval happened in early February 2025. The government will likely announce which funds get capital by mid-2025. Those funds will deploy capital starting in late 2025 through 2026. Actual startup funding hits companies starting in mid-2026.

This timeline matters because founders waiting for capital need to know how long to hold out. If you're a deep-tech founder running out of runway in 2025, you need bridge funding or you need to adjust your burn rate. The government capital isn't immediate.

Expected outcomes over 3-5 years:

-

100-200 new startups funded: If the fund-of-funds model holds, $1.1 billion invested across 30-40 VCs could fund 150 startups on average.

-

30-50 companies raising Series B: Not all will succeed, but some will reach meaningful traction and attract private capital.

-

5-10 unicorn candidates: Out of 150 companies, 5-10 might grow to billion-dollar valuations. This is typical venture outcome distribution.

-

Increased deep-tech talent supply: Successful companies in quantum, biotech, robotics, etc., will create career opportunities that attract engineers from abroad back to India.

-

IP creation: Patents, published research, and defensible technology developed by these companies will become assets India can leverage.

-

Ecosystem strengthening: More institutional VCs, more entrepreneurs trying hard tech, more infrastructure to support deep-tech development.

These aren't guaranteed. They're scenarios if execution goes well. Poor execution produces weaker outcomes.

Deep-tech companies typically require high R&D investment, long development timelines, substantial capital, specialized talent, and face regulatory complexities. Estimated data based on typical industry insights.

Manufacturing Sector Focus and Industry 4.0

The fund's manufacturing focus deserves special attention because it's where India has real leverage.

India is the world's fifth-largest manufacturer. It's a major electronics and pharmaceutical manufacturer. But it lags in advanced manufacturing—robotics, automation, precision equipment, and process innovation. China dominates here. The US and Germany compete at the high end. India is cost-competitive but low-tech.

The opportunity is clear. A company that builds AI-powered factory optimization could serve millions of Indian manufacturers trying to compete. A startup that develops robotics for Indian assembly lines could scale across Asia. A company making advanced materials for electronics could displace imports.

Deep-tech applied to manufacturing is defensible. A foreign competitor can't easily build the same product for India's constraints and cost structure. A company that solves manufacturing challenges for Indian SMEs has an unfair advantage.

The fund is explicitly targeted here, which is smart. Manufacturing is not sexy, but it's foundational. Nations that lead in manufacturing innovation create wealth and employment. China figured this out. India is trying to catch up.

Expected impact: Within 5 years, several Indian companies should emerge as leaders in industrial robotics, factory automation, and advanced manufacturing processes. These companies will export globally because they've been optimized for India's constraints—which means they're hyper-efficient.

AI and Software Deep-Tech Convergence

One interesting dynamic is how traditional software deep-tech and AI intersect.

Traditional deep-tech has been hardware-heavy. Semiconductors, biotech, robotics, advanced materials. You need labs, fabrication plants, expensive equipment.

AI changes this. You can now do deep-tech work in software. A researcher can build novel neural architectures. A team can develop AI for scientific discovery. You can train large models on specialized domains—protein folding, materials science, drug discovery, circuit design—and use AI as a research tool.

This dramatically lowers the capital barrier for certain deep-tech startups. You don't need a fab to work on semiconductor design if you can use AI. You don't need to build prototypes if you can simulate them with AI. You don't need expensive experiments if AI can predict outcomes.

India's competitive advantage here is real. Indian engineers are good at software. The country has AI talent. Put them to work on applications in scientific domains and you get deep-tech without the extreme capital requirements.

The fund should attract these hybrid startups—companies using AI to solve hard technical problems. A startup applying AI to drug discovery is deep-tech, not just a software company. A startup using machine learning for semiconductor design is deep-tech. The fund's definition should explicitly include these hybrid AI-plus-domain-expertise companies.

Sectoral Deep-Dive: Where the $1.1B Likely Goes

If the fund deploys evenly across deep-tech sectors, here's a likely allocation:

Semiconductors and Chip Design: 20% ($220M). This is a government priority because import dependence is high. Companies building chip design tools, simulation software, and specialized semiconductors for Indian applications will get funded.

Quantum Computing and Computing Research: 10% ($110M). Prestigious, long-term, zero revenue probability for 10 years. Perfect government-funded project. India wants quantum computing capability for national security and competitive reasons.

Biotech and Life Sciences: 15% ($165M). Huge opportunity space. Manufacturing is expertise. Research is weak. Capital for biotech innovation is available but concentrated. Government funding expands access.

Robotics and Automation: 15% ($165M). Manufacturing use case is obvious. But also space exploration, defense, and infrastructure applications. India wants indigenous robotics capability.

Advanced Materials: 10% ($110M). Batteries, composites, electronic materials, manufacturing materials. Long-duration research, hard to commercialize, perfect for patient capital.

AI for Scientific Domains: 15% ($165M). Drug discovery, materials design, climate modeling, agricultural optimization. AI applied to hard problems, not just SaaS tools.

Climate Tech and Energy: 10% ($110M). Renewable energy technology, green manufacturing, carbon capture. Global megatrend. India has incentives to lead here.

Other: 5% ($55M). Space tech, defense tech, agriculture tech, other emerging deep-tech areas.

These allocations are estimates. Actual deployment will depend on what proposals VCs submit and what the government approves. But the distribution signals where India wants to build capability.

Competitive Dynamics and Private Capital Response

How will this government fund affect private venture capital's behavior?

Three scenarios:

Scenario 1: Complementary Investment: Private VCs view government capital as validation. If the government funds a deep-tech company, private VCs see it as de-risked and follow with Series B funding. The government fund becomes a signal that attracts private capital. This is healthy. Total capital flowing to deep-tech increases beyond the $1.1B.

Scenario 2: Crowding Out: Private VCs reduce deep-tech investing because the government is now their competition. Why take the risk when the government will handle it? Private VCs focus on safer bets in SaaS and consumer tech. This would be unfortunate because it concentrates risk—if government capital makes bad bets, nobody else is investing in alternatives.

Scenario 3: Hybrid Model: Private VCs adjust their strategy. Instead of making early-stage bets in deep-tech, they wait for government funding, then jump in at Series B with their own capital, minimizing their own risk exposure. This is somewhat problematic because it reduces appetite for truly early-stage, high-risk deep-tech work.

Healthy outcome would be Scenario 1—complementarity. The government fund creates a funding ladder that lets private VCs participate without bearing all the early-stage risk. This accelerates capital flows and reduces total capital needed to build the ecosystem.

Watching this dynamic over the next 2-3 years will tell you a lot about whether this program succeeds or fails. If private capital flows to deep-tech increase after government deployment, the program worked. If private capital redirects elsewhere, it failed.

Precedent from China and Lessons for India

China's approach to government-backed deep-tech funding offers instructive lessons, both positive and cautionary.

What China did right:

-

Strategic Focus: The government identified specific sectors (semiconductors, AI, quantum, 5G) and committed massive capital. No ambiguity about priorities.

-

Long-Term Commitment: Capital deployment stretched across decades. Companies understood they wouldn't be forced to exit quickly.

-

Ecosystem Integration: Government capital was paired with procurement advantages, IP protection, and talent incentives. It wasn't just money; it was a whole strategy.

-

Patience with Failure: Not every company funded succeeded. The government accepted losses because the strategic payoff of the winners was worth it.

What China did problematically:

-

State Champion Creation: The government picked winners and protected them from competition. This created inefficiency. Better companies couldn't compete against protected state favorites.

-

Opacity and Corruption: Fund management lacked transparency. Politically connected individuals got capital regardless of merit. This wasted a lot of money.

-

IP Restrictions: Government-backed companies faced pressure to keep technology within China, limiting global expansion opportunities.

-

Market Distortion: Subsidized companies at scale distorted entire industries. Competitors couldn't compete against state-backed pricing.

India should learn from both. It should be strategic and patient like China but transparent and competitive. India should avoid picking specific winners and instead let VCs make those decisions. India should remain open to global competition and partnership.

So far, the India program's structure suggests more transparency and less state championship than China's approach. The fund-of-funds model means professional VCs make investment decisions, not government bureaucrats. This is better governance.

Long-Term Vision: Where This Leads in 10 Years

If this fund succeeds, what does India's deep-tech ecosystem look like in 10 years?

Optimistic scenario: India becomes a global deep-tech hub. Quantum computing startups headquartered in Bangalore compete globally. Indian biotech startups develop novel therapies. Indian robotics companies power factories worldwide. Indian semiconductor companies design chips for global markets. The country transitions from a service and software economy to a technology innovation economy. Talent that left for Silicon Valley starts returning because interesting problems and capital are available at home.

This scenario requires: continued government support, disciplined venture fund management, regulatory coherence, and maintained political commitment across electoral cycles. If any of these falter, the vision fails.

Realistic scenario: The fund produces 30-50 successful companies across various deep-tech sectors. Some become significant businesses. Some become important infrastructure players in India. The ecosystem strengthens but remains smaller than Silicon Valley or China. India becomes a regional deep-tech hub rather than a global leader. This is still valuable—it creates prosperity and reduces dependence on imports.

Pessimistic scenario: The fund deploys capital but with poor discipline. Politically connected mediocre VCs get capital and make bad investments. Mission creep occurs and capital flows to non-deep-tech companies. Returns are weak. The program becomes seen as government waste. Subsequent governments reduce funding or eliminate the program entirely. Deep-tech companies struggle to get capital again.

Which scenario happens depends on execution. The structure is sound. The intent is clear. The timing is right. But execution is where most government initiatives fail.

FAQ

What is India's new $1.1 billion venture capital fund?

India's government approved a $1.1 billion state-backed venture capital program in February 2025 designed to invest in deep-tech and manufacturing startups through private venture capital firms. The program operates as a fund-of-funds, meaning the government commits capital to private VCs who make actual investment decisions in startups. This approach combines government patient capital with private sector expertise and discipline.

How does the fund-of-funds structure work?

The government acts as a Limited Partner (LP) and commits capital to existing venture capital funds. Those funds then invest in startups while making all investment decisions. This indirect approach provides several benefits: government avoids the risk of directly picking startups, professional VCs handle due diligence and monitoring, and the government's patient capital enables longer investment timelines. The 2016 version deployed ₹100 billion across 145 funds, which then deployed over ₹255 billion into 1,370 startups—a 2.55x multiplier effect.

What sectors does this fund target?

The fund explicitly focuses on deep-tech and manufacturing sectors including artificial intelligence, quantum computing, biotech, advanced materials, semiconductors, robotics, autonomous vehicles, renewable energy technology, and climate tech. These are long-horizon, capital-intensive sectors where companies typically need 5-10+ years before generating significant revenue, making them unsuitable for traditional venture capital focused on quicker exits.

Why is government capital necessary for deep-tech?

Private venture capital typically seeks exits within 7-10 years and demands early revenue traction. Deep-tech companies often spend 5-10 years on R&D with zero revenue before commercialization. A quantum computing startup might never generate revenue from hardware sales alone. Biotech companies spend years in regulatory approval. These timelines don't match venture capital fund economics. Government capital, by contrast, can accept 10-20 year timelines and focus on strategic impact rather than quarterly returns, making it ideal for funding deep-tech innovation.

What policy changes support this fund?

The Indian government doubled the period deep-tech startups can maintain startup classification from 5 to 20 years and raised the revenue threshold from ₹1 billion to ₹3 billion annually. These changes allow companies to benefit from startup tax breaks and regulatory flexibility for significantly longer, providing extended runway during long development phases. A biotech startup can now remain classified as a startup for 20 years while conducting clinical trials and seeking regulatory approval.

How much money will actually reach startups?

The $1.1 billion will be deployed by private venture capital funds over approximately 3-5 years starting in 2026. Based on the 2016 program structure, the capital will likely reach 100-200+ startups across 30-40 different funds. However, the deployment timeline means actual startup funding begins in mid-2026 at the earliest, not immediately after cabinet approval in February 2025.

What happened to India's startup ecosystem in 2025?

India's startup funding declined 17% in 2025 to $10.5 billion, and the number of completed funding deals crashed 39% to just 1,518 transactions. This contraction followed the hyperinflated 2021-2022 period when abundant capital funded companies with weak fundamentals. The 2025 decline represents investor discipline returning to the market. In this capital-scarce environment, government backing for deep-tech becomes more strategically valuable.

How does this compare to other countries' deep-tech funding approaches?

The US funds deep-tech through DARPA, NSF, and NIH, distributing billions annually for research and technology development. China backs deep-tech aggressively through state-owned enterprises and sovereign wealth funds with explicit strategic focus on semiconductors and AI. Israel's government funds early-stage R&D through OCS, then lets private capital scale successful companies. Europe has various national programs through development banks and the EU's Innovation Council. India's approach is similar to Israel's—government de-risking followed by private capital scaling, which is more market-friendly than China's state championship model.

Will this fund distort India's venture capital market?

Risk exists. Government capital could inflate valuations if deployed without discipline, could crowd out private investment if it becomes too large, or could distort competition if politically connected but less-qualified VCs receive capital. However, the fund-of-funds structure limiting decision-making to professional VCs and the focused sectoral mandate for deep-tech help mitigate these risks. Success depends on disciplined governance and resistance to mission creep toward non-deep-tech companies.

What are the success metrics for this program?

Key success metrics include: actual deployment of capital by end of 2026, number of startups funded by 2027, follow-on funding from private VCs showing complementarity rather than crowding out, 3-5 year survival rates of funded companies, companies reaching Series B or beyond, and ultimately 5-10 unicorn-class companies within the portfolio. Equally important are indirect metrics like increased deep-tech talent concentration in India and IP creation (patents, published research) from funded companies.

Key Takeaways and Future Implications

India's $1.1 billion state-backed venture capital program represents a calculated bet that deep-tech innovation will define the next phase of India's economic growth. The strategy is sound, the structure is disciplined, and the timing addresses a real gap in the venture capital market.

But success isn't guaranteed. The fund will succeed if it maintains focus on genuinely deep-tech sectors, resists political pressure to deploy capital quickly to non-qualifying companies, backs experienced and emerging VCs with real domain expertise, and integrates with broader government initiatives around manufacturing and AI development.

Three years from now, in 2028, we'll know if this worked. If 100+ companies got funded, if private capital is flowing alongside government capital, if some of these companies are achieving meaningful technical milestones, and if the broader startup ecosystem shows signs of strengthening in deep-tech, then the program succeeds. If, instead, capital was deployed slowly or to mediocre VCs, if few startups actually received funding, and if deep-tech remains starved for capital, then the program failed.

The broader question is whether governments can effectively catalyze innovation. History is mixed. Some government initiatives create lasting competitive advantages. Others waste money. This one has ingredients for success. Now comes execution.

For deep-tech founders in India, this changes everything. The capital source you've been waiting for might finally exist. That quantum computing idea you've been sitting on. That biotech innovation you couldn't finance. That manufacturing automation startup you shelved due to capital constraints. These now have pathways to funding. The question is whether you execute fast enough and well enough to reach that capital before it deploys elsewhere.

For the broader startup ecosystem, this signals that the Indian government takes innovation seriously beyond consumer apps. That's a powerful signal for attracting global talent and capital. When foreign investors see that India's government backs deep-tech, they take India more seriously. This $1.1 billion becomes the spark for a much larger capital flow.

India's aspiration to become a technology innovation leader, not just a technology services provider, has just gotten more credible. Whether that aspiration becomes reality depends on what happens next.