![IQM's $1.8B SPAC IPO: Quantum Computing's Next Unicorn [2025]](https://tryrunable.com/blog/iqm-s-1-8b-spac-ipo-quantum-computing-s-next-unicorn-2025/image-1-1771866573559.jpg)

Introduction: When Quantum Computing Goes Public

There's a moment in every emerging technology's lifecycle when the startups stop being scrappy R&D labs and start becoming household names on stock exchanges. For quantum computing, that moment is arriving faster than anyone expected.

In early 2025, IQM Quantum Computers, a Finnish company founded in 2018, announced plans to go public through a special purpose acquisition company (SPAC) merger. The deal values the company at approximately $1.8 billion, making it one of the largest quantum computing exits to date. What makes this announcement particularly significant isn't just the valuation—it's the timing and what it reveals about the entire quantum computing sector.

Just weeks before IQM's announcement, Infleqtion, a neutral-atom quantum company, had jumped on the New York Stock Exchange via SPAC. Meanwhile, Canadian firm Xanadu Quantum Technologies planned its own SPAC listing on Nasdaq. This isn't a coincidence. It's a wave.

But here's what nobody's talking about directly: every single one of these companies went public through SPACs, a route that peaked in 2021 and left many investors nursing six-figure losses. The irony is thick. We're riding another SPAC wave—but this time in quantum computing, a field where commercial applications are still, realistically, years away.

This article digs into what IQM's IPO means. Not the hype version. The real version. What's the company actually worth? Why are investors suddenly interested in quantum computing again? What could go wrong? And most importantly, what does this tell us about the quantum computing industry's actual progress versus its marketing claims?

IQM Quantum Computers: Who They Are and What They Actually Do

IQM isn't a household name, and for good reason. The company operates in one of the most specialized segments of the quantum computing space—and that's actually its strength.

Founded in 2018 as a spinout from Aalto University and VTT Technical Research Center in Finland, IQM built its business on a specific technical approach: superconducting qubits. The company commercializes two product categories: on-premises full-stack quantum computers and a cloud platform for remote access to its systems.

When we say "full-stack," that's important. IQM doesn't just build the qubits (the quantum bits that do the actual computing). The company handles the entire stack: the qubits themselves, the control electronics, the cryogenic cooling systems (which run at temperatures colder than outer space), the software layer that translates problems into quantum operations, and the error correction frameworks.

Why does this matter? Because most quantum computing companies are point solutions. IBM focuses on qubit design and cloud access. Rigetti combines hardware and hybrid classical-quantum algorithms. Ion Q uses trapped-ion technology instead of superconducting qubits.

IQM's bet is different: by controlling the entire stack, they can optimize across every layer. When error rates are too high, they can tweak the qubit design. When software performance lags, they can modify the control electronics. When customers need specific capabilities, they can build them from the ground up rather than jury-rigging solutions.

The company's clients include academic research labs and industrial partners across Europe, North America, and Asia. The specificity here is crucial—IQM isn't selling to startups trying to build quantum-powered AI. They're selling to serious computational organizations: pharmaceutical research labs doing molecular simulations, materials science researchers designing new compounds, and financial institutions exploring optimization problems.

This positioning is both a strength and a limitation. Strength because it means IQM has real customers with real problems willing to pay for hardware and access. Limitation because the addressable market is comparatively small—there are only so many organizations globally that need on-premises quantum computers today.

IQM's valuation multiple of 51 times revenue is significantly higher than the typical 6-10 times for mature software companies and 15-20 times for high-growth cloud companies. Estimated data.

The $1.8 Billion Valuation: Is It Reasonable?

Let's talk about the elephant in the room:

On its surface, the math is brutal. IQM's valuation is roughly 51 times its annual revenue. By comparison, mature software companies trade at 6-10 times revenue. Even high-growth cloud companies rarely exceed 15-20 times revenue at IPO. So what justifies this multiple?

The valuation is based on several factors, and understanding them is key to assessing whether this is exuberance or reasonable pricing:

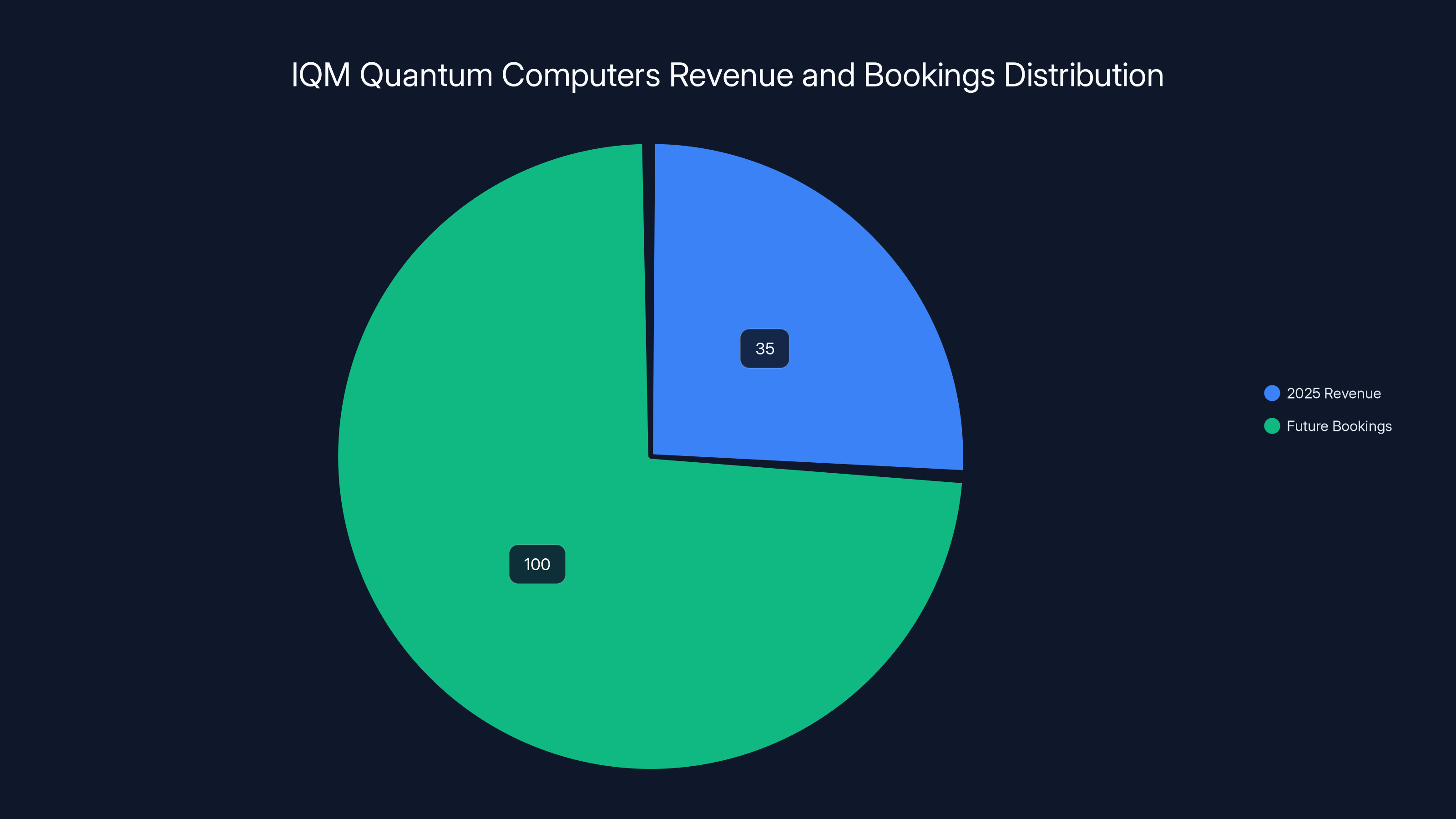

The Bookings Argument: IQM reported over

Growth Trajectory: The quantum computing field is growing exponentially, at least in venture capital interest. Compound annual growth rates (CAGR) for quantum computing hardware and software are projected between 25-35% through 2030. If IQM maintains a leadership position and captures market share in the full-stack hardware segment, the $1.8 billion valuation could look like a bargain in five years.

The AI Effect: Since late 2022, when Open AI launched Chat GPT, the entire tech sector has reassessed what's possible with advanced computing. Quantum computers theoretically excel at problems that classical computers struggle with: molecular simulation, optimization, and certain machine learning tasks. If quantum computing bridges the gap to practical applications faster than expected, the TAM explodes.

Capital Requirements: Building quantum computers is absurdly expensive. A single dilution refrigerator (the device that cools qubits to near absolute zero) costs

But Here's the Catch: None of this justifies the valuation if quantum computing remains 7-10 years away from genuine commercial advantage. And that's the real risk. Despite a decade of quantum computing research, the field still hasn't produced a single publicly documented instance of quantum computers solving a real-world problem faster than classical computers at scale. The famous "quantum advantage" demonstrations from Google and others in 2019-2022 were proof-of-concept wins, not business value demonstrations.

The valuation assumes that IQM's leadership position, customer relationships, and technical capabilities will position them to capture enormous value when that commercial breakthrough arrives. But it's a bet on the future, not based on current cash flows or even near-term revenue projections.

Estimated data shows that IQM's near-term focus is on revenue growth and customer acquisition, while medium to long-term goals shift towards profitability and market leadership.

The SPAC Route: Why Quantum Companies Are Choosing This Path

IQM didn't pursue a traditional initial public offering (IPO). The company is merging with Real Asset Acquisition Corp., a blank-check company already listed on Nasdaq. This SPAC merger is the route chosen by every major quantum computing company going public in 2024-2025.

SPACs experienced a spectacular boom and bust cycle. In 2020-2021, SPACs were everywhere. Celebrities and sports legends were launching blank-check companies to acquire companies in hot sectors like electric vehicles, space tech, and fintech. The narrative was simple: traditional IPOs are slow and expensive. SPACs get companies to public markets faster.

Then reality hit. Many SPAC mergers involved inflated projections, weak due diligence, and the involvement of promoters with questionable track records. Between 2022 and 2023, SPAC investors experienced brutal losses. The median SPAC that went public in 2021 was trading below its IPO price by 2024. The reputation damage was severe.

So why are quantum companies using SPACs in 2025? Several reasons converge:

Speed and Certainty: A traditional IPO involves a roadshow where company executives pitch institutional investors for weeks. The timing is uncertain. Underwriters might price the company lower than hoped. With a SPAC, the merger agreement specifies the valuation upfront. IQM knows it's getting $1.8 billion in enterprise value. No surprises.

Avoiding the IPO Process Cost: A traditional IPO costs 7-10% of capital raised in fees and commissions. A SPAC merger costs less in direct fees, though the founder's promote (the SPAC sponsor's reward) can be dilutive to shareholders. For IQM, which is raising $450 million+ in cash, the fee savings are substantial.

Market Timing: Quantum computing sentiment is hot right now. When IPO windows are narrow, SPACs offer a pathway to capital that doesn't require waiting for the traditional IPO calendar to align with market conditions. IQM is moving while quantum computing is a sector investors are actively seeking.

International Company, U. S. Market Access: IQM is a Finnish company but wants U. S. public market access. Traditional IPOs can be complex for foreign companies. SPACs are more accommodating to international targets. IQM will list American Depositary Shares (ADSs) on either Nasdaq or NYSE, with approval pending.

The Downside: History shows that investors in SPAC mergers often underperform compared to IPO investors. The SPAC structure incentivizes the sponsor to find a deal—any deal—to earn their promote. Less scrutiny sometimes means worse outcomes for public shareholders. Also, the blank-check company sponsor often retains a significant stake, misaligning incentives if they differ from public shareholders' interests.

For IQM specifically, the SPAC route makes sense. The company gets access to capital without the months of traditional IPO preparation. The quantum computing sector gets another credible public company, which itself lends legitimacy to the space. Investors get exposure to a genuine deep-tech company with real customers and significant technical talent.

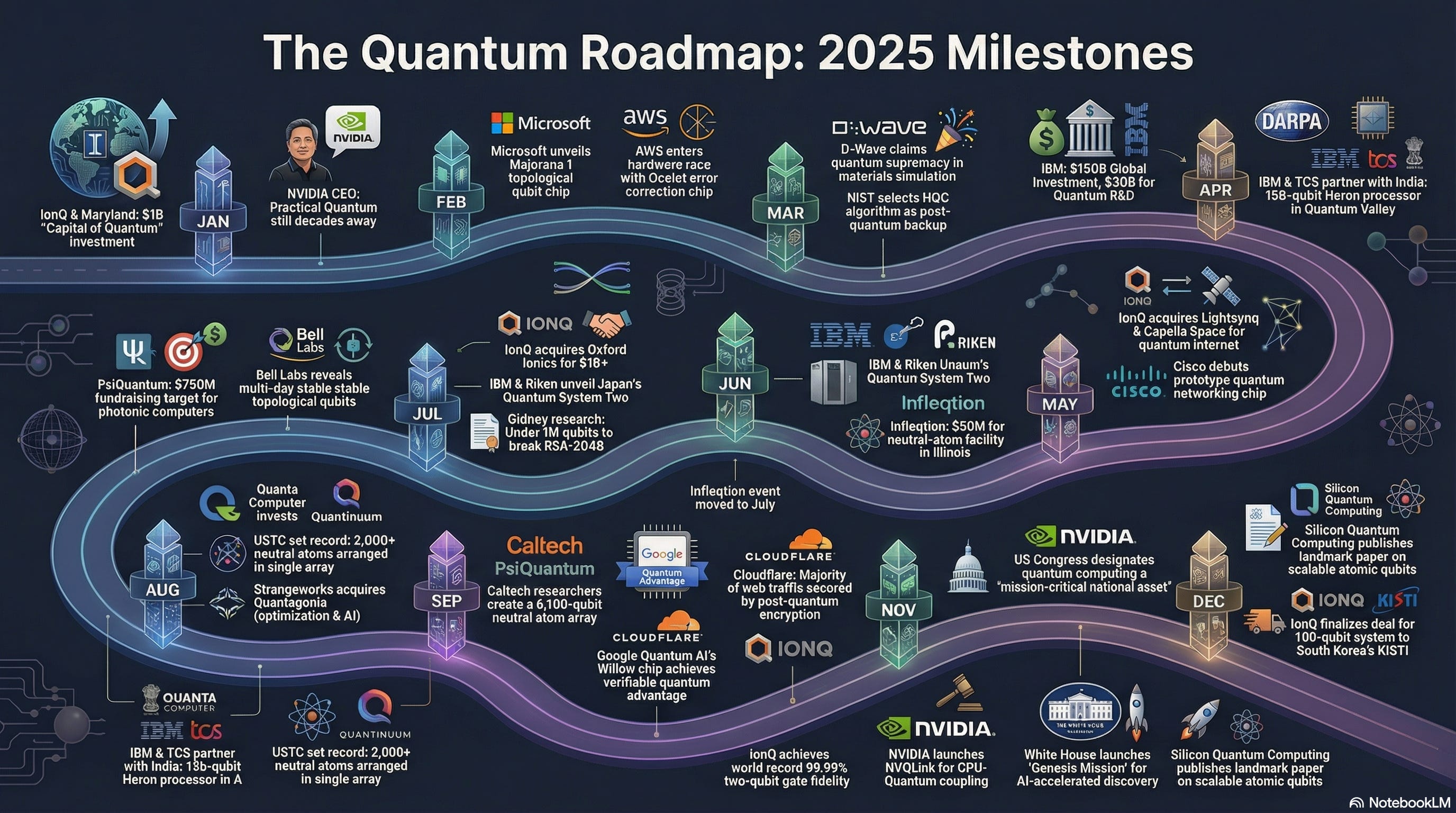

Quantum Computing Sector Momentum: The 2025 Wave

IQM's IPO isn't isolated. It's part of a wave that began in late 2024 and accelerated through early 2025.

In January 2025, Infleqtion, which specializes in neutral-atom quantum computers, went public on the New York Stock Exchange after merging with a SPAC. Neutral-atom systems use individual atoms trapped and manipulated by lasers to function as qubits. Infleqtion's technology is fundamentally different from IQM's superconducting approach, yet the market welcomed the IPO enthusiastically.

Xanadu Quantum Technologies, based in Toronto, was planning its Nasdaq listing for late March 2025. Xanadu focuses on photonic quantum computing—using photons (particles of light) as qubits. Three different technical approaches, three different companies, all pursuing public markets simultaneously.

What's driving this?

Government Investment Signals: The U. S. government has signaled serious commitment to quantum computing. The National Quantum Initiative and various Department of Energy programs are funding quantum research at billions of dollars annually. When governments invest heavily in a technology sector, private capital follows because it reduces risk.

Big Tech Interest: Google's quantum research division, IBM's quantum computing efforts, and Microsoft's quantum research have all made public progress announcements. When trillion-dollar companies are actively investing in a field, it validates the technology's potential.

NVIDIA's AI Success as a Template: NVIDIA's stock price increased roughly 10x from 2020 to 2024 on the back of AI chip demand. Investors are asking: could quantum computing be the next frontier technology where early-mover hardware companies see explosive growth? The template exists. Quantum computing could follow a similar trajectory if breakthrough applications arrive.

Media Narrative Momentum: Press coverage of quantum computing has shifted from skeptical to optimistic. The consensus narrative is that quantum computing will "soon" solve problems that matter. The definition of "soon" is conveniently vague—anywhere from 18 months to 10 years, depending on the article—but the optimism is palpable.

FOMO Among Institutional Investors: Fear of missing out is real in tech investing. If quantum computing becomes the transformative technology everyone claims, institutional investors who didn't get exposure earlier want to participate now. Quantum IPOs provide that exposure without requiring venture capital connections.

The result is a self-reinforcing cycle. Positive sector sentiment makes capital cheap for quantum companies. Cheap capital allows quantum companies to hire talent, build better products, and pursue ambitious R&D. Better products generate more interest from customers and investors. The cycle continues—until it doesn't.

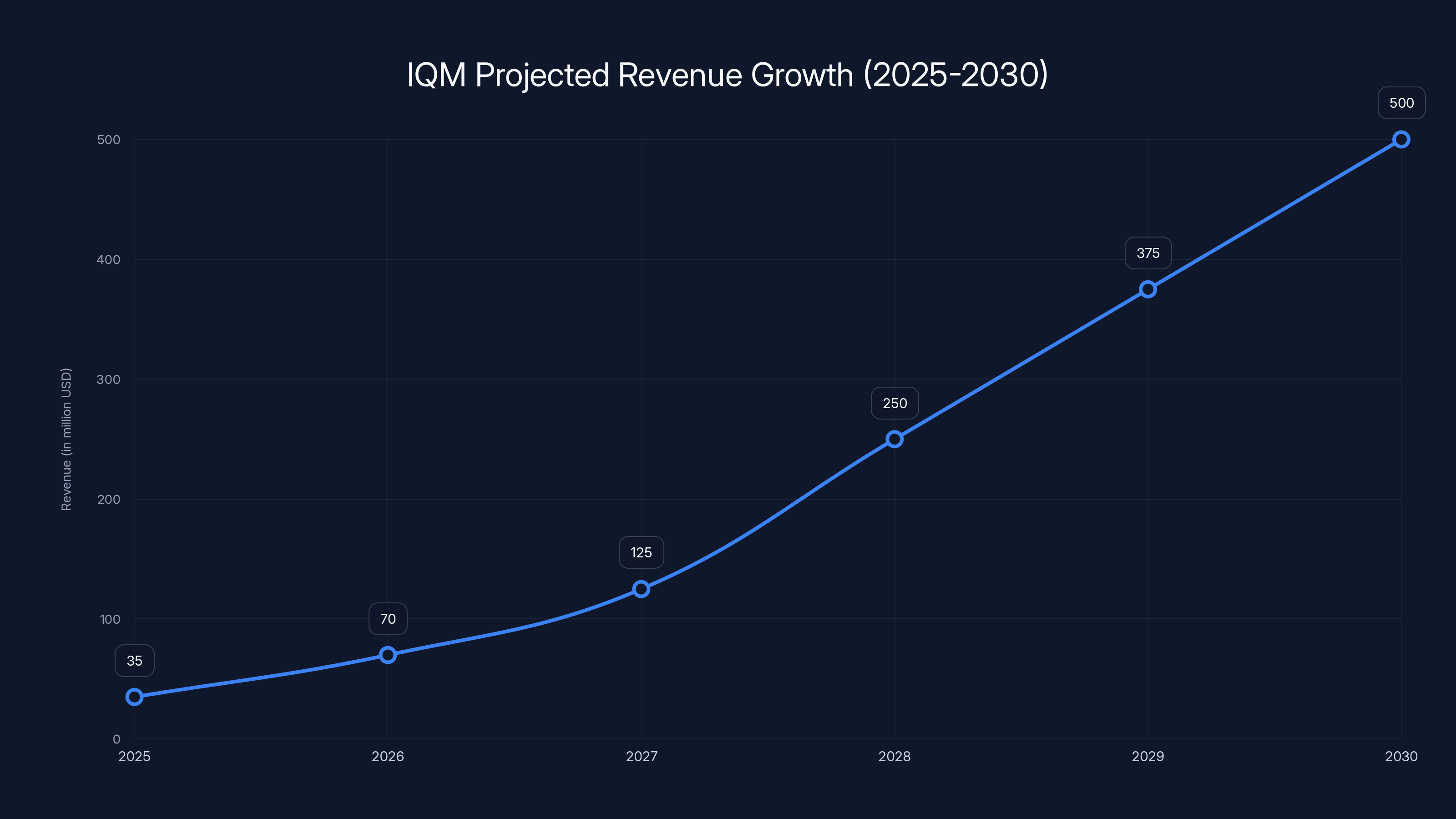

IQM's revenue is projected to grow significantly from

IQM's Technical Approach: Superconducting Qubits Explained

Understanding IQM requires understanding its core technology: superconducting qubits. This is where the physics gets real, and where IQM's technical bets become apparent.

A qubit (quantum bit) is the quantum equivalent of a classical bit. Where a classical bit is either 0 or 1, a quantum bit can exist in a "superposition" of both 0 and 1 simultaneously. This property is what gives quantum computers their theoretical power. In theory, if you have 300 qubits, you can represent

Of course, that theoretical power collapses the moment you measure the qubits, at which point they collapse into either 0 or 1. The art of quantum computing is designing algorithms that manipulate qubits so that the probability of measuring the right answer is high.

Superconducting qubits work by exploiting quantum properties in superconductors—materials that conduct electricity with zero resistance when cooled below a critical temperature. IQM's superconducting qubits operate at temperatures around 20 millikelvin (0.02 degrees above absolute zero). At these temperatures, quantum mechanical effects dominate classical physics, allowing qubits to maintain their quantum properties.

Why does IQM focus on superconductors instead of other approaches like trapped ions (Infleqtion's choice) or photonic qubits (Xanadu's choice)?

Superconducting qubits have several advantages:

Maturity: The superconducting qubit approach has been researched longer than other methods. More academic papers, more engineering solutions, more known techniques for improving performance. IBM, Google, and numerous academic labs use superconducting qubits.

Scaling Potential: In theory, superconducting qubits scale to very large numbers (100s or 1000s of qubits) because you can pack them densely on a chip. Trapped-ion systems face physical limits on how many ions you can trap and control simultaneously.

Manufacturing: Superconducting qubits are fabricated using semiconductor manufacturing techniques that are well-established. Companies like IQM can partner with existing chip manufacturers rather than building entirely custom manufacturing from scratch.

Disadvantages: The catch is that superconducting qubits are extremely noisy. They lose their quantum properties ("decohere") quickly—typically in microseconds. Building a 100-qubit superconducting system is possible; building one where the qubits maintain coherence long enough to solve useful problems is much harder.

This is where IQM's full-stack approach becomes critical. If the control electronics introduce too much noise, qubits decohere faster. If the cryogenic system isn't precise enough, temperature fluctuations cause problems. If the software layer doesn't efficiently pack quantum operations, you need longer coherence times than available. By controlling the whole stack, IQM optimizes all these interconnections.

IQM has published papers in peer-reviewed journals demonstrating steady improvements in qubit quality metrics. The company's latest systems feature error rates that are competitive with academic labs and rival companies. But competitive doesn't mean "solved the decoherence problem." It means the problem is still being worked on, with incremental progress.

Revenue Model and Customer Acquisition

Understanding how IQM makes money is crucial to assessing whether the $1.8 billion valuation has any grounding in business reality.

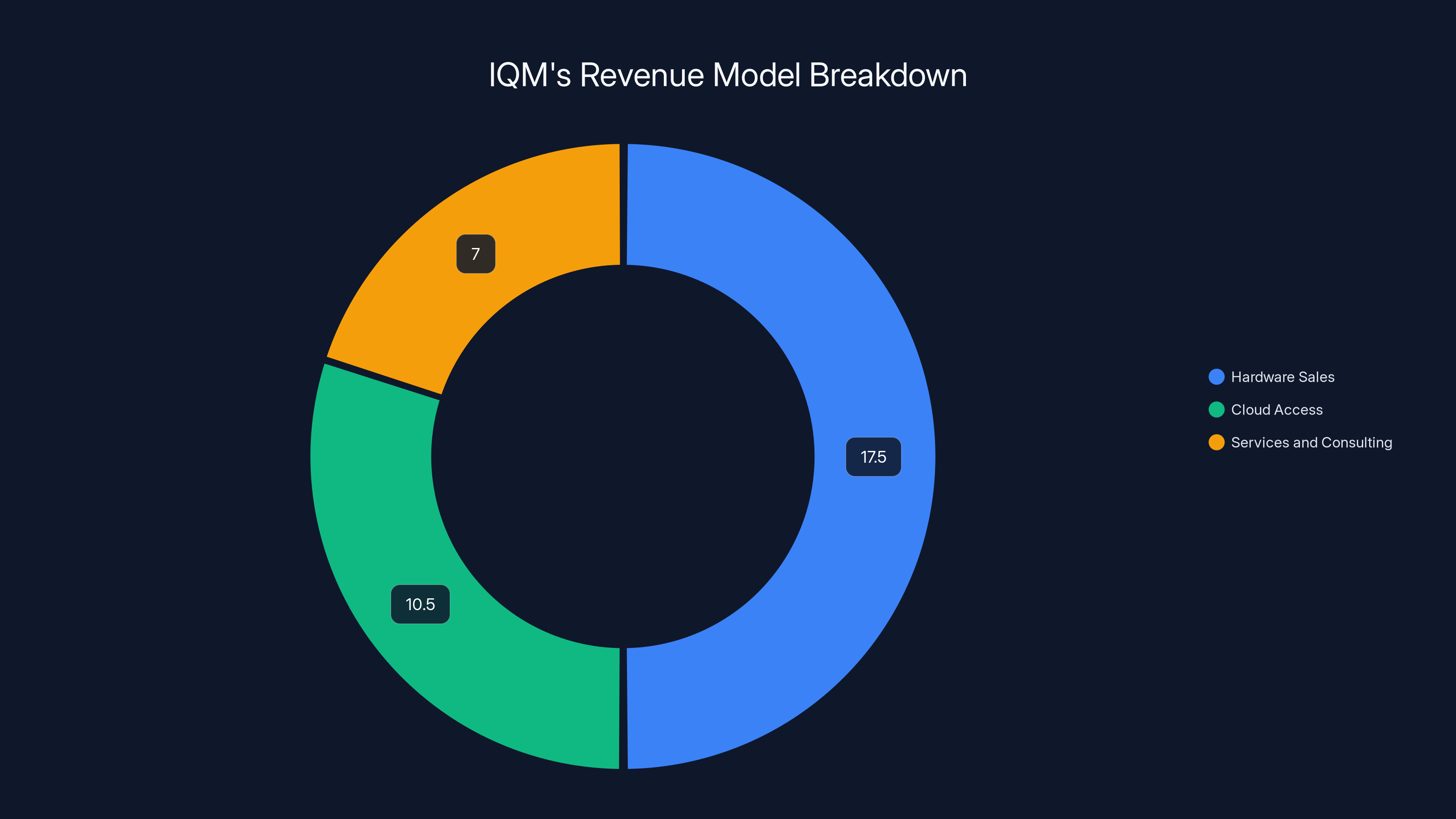

IQM's revenue comes from three primary sources:

Hardware Sales: Selling on-premises quantum computers to organizations that want dedicated systems. These are high-value transactions—a fully assembled quantum computer with control systems, cryogenics, and integration can cost $5-15 million depending on qubit count and specifications. IQM has installed systems at academic institutions, research centers, and some industrial partners. The margin on hardware sales is healthy (60%+), but the sales cycle is long (12-24 months from initial discussions to installed system) and the customer base is small.

Cloud Access and Subscription: IQM offers cloud-based access to its quantum computers hosted in company data centers. Customers can submit quantum programs, and IQM's systems execute them, returning results. This is a recurring revenue model with lower margins (30-40%) but more predictable cash flow. The addressable market is larger because companies can pay for access without the $10 million capital commitment of owning hardware.

Services and Consulting: Custom integration, algorithm development, and technical support. Margins are highest here (70%+), but volume is limited because it requires IQM engineers' time. This is essentially professional services revenue, which doesn't scale as well as pure software.

The reported

Customer acquisition for IQM happens through:

Direct Sales: IQM's team directly approaches quantum research labs, pharmaceutical companies, and financial institutions known to have quantum computing initiatives. The sales process emphasizes IQM's full-stack advantages and ability to customize systems.

Academic Partnerships: Offering systems to universities at favorable terms builds brand, creates trained next-generation engineers, and generates research partnerships. University-developed algorithms and use cases become IQM marketing materials.

Industry Consortiums: Participating in quantum computing industry groups and standards bodies. When companies in the automotive, pharma, or finance sectors discuss quantum applications, IQM's presence ensures the company is part of those conversations.

Customer Success Stories: Publishing case studies showing real results from IQM systems. Did a pharmaceutical company design a new drug candidate faster using IQM hardware? Did a financial institution solve an optimization problem more efficiently? These stories drive new customer interest.

The challenge is that quantum computing's customer base is extremely concentrated. Global headcount of people actively researching quantum applications in industry is probably under 5,000 today. Every quantum computing company is competing for attention from the same small pool of potential customers.

In 2025, IQM Quantum Computers reported

Competitive Landscape: IQM's Rivals and Relative Position

IQM operates in one of the most crowded deep-tech spaces imaginable. Dozens of companies are competing in quantum computing hardware and software. Understanding how IQM compares is essential for assessing investment risk.

Direct Hardware Competitors:

IBM Quantum is the 800-pound gorilla. IBM has quantum computers with 100+ qubits, offers free and paid cloud access, has built partnerships with industry players, and has invested billions in quantum research. IBM's advantage: brand, enterprise relationships, and resources. IBM's disadvantage: quantum is one of thousands of business units. The company won't go all-in on quantum if it becomes a difficult business.

Google Quantum AI has demonstrated quantum advantage (or "quantum supremacy") and has been publishing impressive technical results. But Google hasn't committed to a business model. The company offers limited cloud access but doesn't appear focused on commercialization.

Ion Q went public in late 2023 via a SPAC merger (cautionary tale here—Ion Q's stock traded significantly below its IPO price within a year). Ion Q uses trapped-ion technology rather than superconducting qubits. Ion Q claims advantages in error rates and has aggressive growth projections. However, the company has faced skepticism about real-world performance and revenue metrics. As of early 2025, Ion Q trades near

Rigetti Computing combines hybrid classical-quantum algorithms with its own hardware. Rigetti has customers and revenue but remains private with lower visibility.

Quantinuum is a UK-based company (formed by merging Honeywell's quantum division with Cambridge Quantum Computing) that focuses on trapped-ion systems. Well-funded and technically solid, but also facing the challenge of building a sustainable business around a technology still in the research phase.

Infleqtion, newly public, uses neutral-atom technology. The company has customers and funding but must now prove it can maintain investor faith while delivering on ambitious technical and commercial projections.

IQM's Positioning: IQM isn't the largest by qubit count. It's not as well-known as IBM or Google. But IQM has several differentiation points:

- Full-stack ownership: Most competitors rely on partners for certain components. IQM controls the end-to-end product.

- European pedigree: Drawing from Aalto and VTT's research, IQM brings academic credibility and engineering excellence.

- Customer focus: IQM seems more focused on actual customer success than on academic prestige.

- Financial discipline: The $100 million in bookings and steady revenue growth suggest IQM is building a business, not just running a research lab.

The risk is that none of these differentiators matter if quantum computing's commercial timeline extends beyond IQM's capital runway or if a larger player (IBM, Google, Microsoft, AWS) commits fully to commoditizing quantum computing.

The "Quantum Advantage" Problem: Why Timelines Matter

Everything about IQM's $1.8 billion valuation rests on a single assumption: quantum computers will, within the next 5-7 years, solve practically useful problems faster and cheaper than classical computers.

This is not guaranteed.

Let's be precise about what has actually happened in quantum computing:

What Quantum Companies Have Done:

- Built quantum computers with increasing qubit counts (from 5 qubits in 2015 to 1000+ qubit prototypes today)

- Demonstrated quantum advantage in carefully constructed academic problems where quantum systems outperform classical systems

- Published peer-reviewed papers showing steady improvements in qubit error rates and coherence times

- Attracted billions in investment and government funding

- Hired top physics talent

What Quantum Companies Have NOT Done:

- Solved a single practically useful real-world problem faster than classical computers at production scale

- Demonstrated quantum advantage in any commercially relevant scenario (drug discovery, materials science, optimization, machine learning)

- Built a quantum computer that can maintain computational fidelity for long enough to solve complex problems

- Achieved error rates low enough that quantum error correction doesn't require more physical qubits than useful logical qubits

The reason is fundamental: quantum computers are extraordinarily fragile. Every interaction with the environment introduces error. To solve useful problems, you need error rates below a certain threshold (typically estimated around

That sounds close. It's not. Improving error rates by one order of magnitude has taken the field roughly 8-10 years. If progress continues linearly, we might reach the threshold by 2035-2040. If progress accelerates (possible but not guaranteed), we might reach it by 2030-2032.

Even reaching the threshold doesn't mean useful quantum advantage. You still need to:

- Develop algorithms that leverage quantum properties

- Integrate quantum systems into classical computing workflows

- Train a workforce that understands quantum programming

- Build economics where quantum solutions are cheaper than classical alternatives

All of this is years away from happening at scale.

For IQM's valuation to be justified, the company needs quantum advantage to arrive soon enough that:

- Current investors haven't lost faith

- The market for quantum computing expands 10-20x from current levels

- IQM maintains a meaningful market share

- Profit margins remain healthy despite potential commoditization

None of these are guaranteed.

In 2025, IQM's revenue is projected to be $35 million, with 50% from hardware sales, 30% from cloud access, and 20% from services, highlighting a balanced revenue model. Estimated data.

Government and Big Tech Investment: Is This Real Support?

A significant part of quantum computing's current momentum comes from government and big tech support. These aren't small signals to ignore—but understanding what they mean requires reading between the lines.

U. S. Government Commitment:

The National Quantum Initiative Act authorized $1.2 billion in federal quantum computing research funding over five years (2018-2023). This was reauthorized with additional funding beyond 2023.

The Department of Energy established quantum information science centers to focus research on near-term applications.

The National Science Foundation has supported quantum computing research at universities and national labs.

What this means: Government is betting on quantum computing's importance for national security (quantum computers could theoretically break current encryption), scientific advancement (quantum simulations could solve problems classical computers can't), and economic competitiveness (whichever country commercializes quantum computing first gains enormous advantage).

What this doesn't mean: Government support guarantees that quantum computing will be useful or profitable. The government funds lots of research that doesn't lead to commercial products. Radio transmission research was government-funded, and it led to commercial applications. Much fundamental physics research is government-funded and has never led to products.

Big Tech Investment:

IBM, Google, Microsoft, and Amazon have invested billions in quantum research.

What this means: These companies take quantum computing seriously enough to spend significant capital on it. They're hedging against the possibility that quantum computing becomes important.

What this doesn't mean: Any of these companies has committed to making quantum computing a core business. For most, it's a strategic research bet, not a revenue driver. If quantum takes longer to commercialize than expected, these companies can deprioritize quantum work without materially impacting their financials.

Microsoft's approach is instructive. Rather than building its own quantum computers, Microsoft is investing in topological qubits (a different approach than superconducting qubits) and focusing on the software layer. The bet is that when quantum hardware improves enough to be useful, Microsoft will have the software framework ready. This is a long-term play, not an expectation of near-term revenue.

What This Means for IQM:

Government and big tech support validates that quantum computing is worth working on. It does not validate specific timelines or commercial viability. IQM benefits from the rising tide of sector interest and investment. But the company is also betting that its technical approach and customer focus will position it to capture value when (and if) quantum advantage arrives.

If that timeline extends beyond 2030-2035, IQM and other quantum companies could face investor pressure to show returns or merge/be acquired by larger players. The IPO gives IQM runway to reach that inflection point, but the clock is ticking.

Financial Projections and Risk Factors

IQM's SPAC merger documents (publicly available) likely contain financial projections, though the details differ from traditional IPO prospectuses. Understanding what IQM projects versus the risks those projections face is critical for investors considering IQM shares post-IPO.

Revenue Projections (estimated based on announced metrics):

If IQM is at

- 2026: $60-80 million (conservative conversion of some bookings to revenue)

- 2027: $100-150 million (continued hardware sales, growing cloud access)

- 2028-2030: $250-500 million+ (quantum advantage arrives, TAM expands)

These are speculative, but they illustrate the growth assumption embedded in the

Key Risk Factors:

Quantum Advantage Delays: If practical quantum advantage doesn't arrive until 2035 or later, demand stalls and IQM burns cash without corresponding revenue growth. This is the single biggest risk.

Competitive Displacement: Larger companies (IBM, Microsoft, Google) could capture quantum computing's TAM. IQM would become a niche vendor or acquisition target. Valuations would contract.

Technology Risk: Superconducting qubits face fundamental challenges. Other approaches (trapped ions, photonic, topological) could prove superior. If the industry shifts away from superconducting qubits, IQM's full-stack advantage becomes irrelevant.

Capital Efficiency Risk: With $450 million in cash, IQM has enough runway for several years of losses. But if the company doesn't achieve commercial traction before cash depletes, it faces pressure to merge or be acquired at unfavorable terms (from a minority shareholder perspective).

Customer Concentration Risk: With only ~50 quantum computers installed globally, losing even one major customer contract represents significant revenue loss. Customer concentration is extremely high.

SPAC Overhang: SPAC-merged companies often underperform because the merger narrative fades and investors focus on underlying business metrics. If IQM's revenue growth disappoints, stock performance could be poor.

Macro Conditions: A tech sector downturn could dry up capital for deep-tech companies. Investors might shift to profitable software companies instead of betting on unproven quantum computing.

Estimated data shows that early investors and founders will hold the largest share of IQM post-IPO, followed by public shareholders. Estimated data.

Market Capitalization and Stock Price Considerations

IQM will begin trading at a

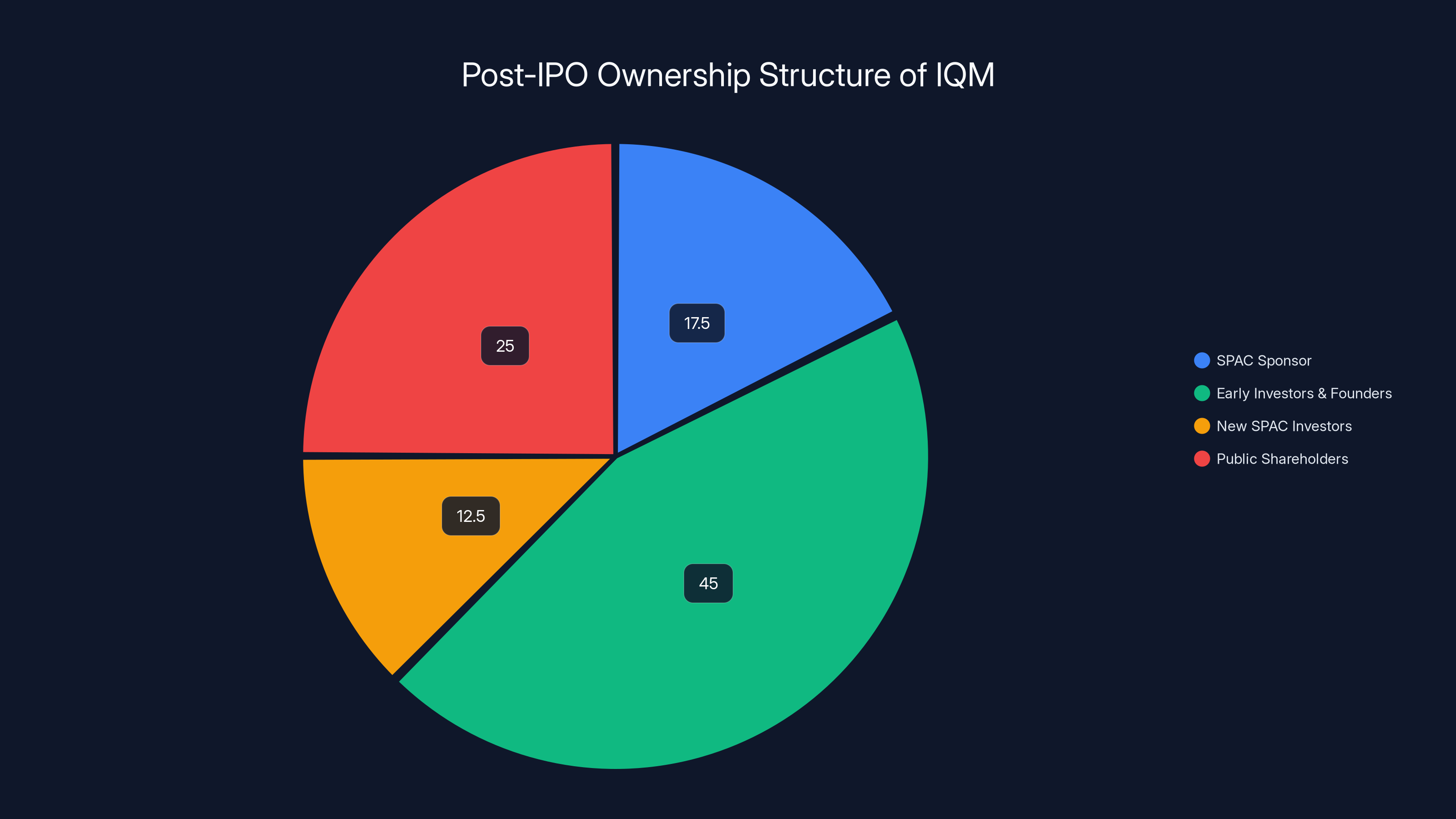

Post-IPO Ownership Structure (estimated):

- SPAC Sponsor (roughly 15-20%)

- Early IQM investors and founders (roughly 40-50%)

- New SPAC investors (roughly 10-15%)

- Remaining public shareholders (roughly 20-30%)

The SPAC sponsor holds shares that vest over time. Early investors and founders often have lock-up periods (typically 12-24 months) before they can sell. This staggered unlock schedule creates selling pressure opportunities as various shareholder groups become able to exit.

Stock Price Expectations:

IQM will IPO at a price determined by the SPAC merger agreement. That price is not yet public (this analysis is written in early 2025). However, recent quantum SPAC mergers have seen volatile trading:

- Infleqtion IPO'd in January 2025 and showed significant volatility in its first weeks of trading

- Ion Q merged with a SPAC in October 2023 at an IPO price around 5-7 range—down 30-50%

- D-Wave Systems went public via SPAC in 2024 and has traded below IPO levels

Historically, SPAC-merged companies see initial hype, then downward pressure as investor sentiment normalizes and the stock returns to fundamental valuation levels.

For IQM specifically:

- Bull case: Stock rises 20-50% in first year if quantum computing momentum continues, customer wins are announced, and revenue growth beats expectations

- Base case: Stock trades roughly flat to down 10-20% in first year as market focuses on revenue vs. hype and initial SPAC lockups expire

- Bear case: Stock declines 40-60% in first year if quantum advantage timeline extends, revenue disappoints, or sector sentiment shifts negative

Investors should understand that quantum computing stocks are extremely volatile and sentiment-driven. Fundamental valuation methodology is nearly impossible given the lack of near-term profit expectations.

The International Expansion Angle: Why Nordic Listing Matters

IQM has stated plans to consider listing on both U. S. and Nordic exchanges. This international approach is strategically smart and operationally complex.

Why Nordic Listing Makes Sense:

IQM is a Finnish company with European customers, European funding, and European regulatory relationships. Listing on Nasdaq Nordic or a local Finnish exchange gives home-country investors access to the stock.

European institutional investors might prefer European listings for tax and regulatory reasons. A dual listing increases the addressable investor base.

Nordic countries have strong quantum computing ecosystems. Finland specifically has academic strength in quantum research at Aalto and VTT. A Nordic listing reinforces IQM's position as a Nordic flagship quantum company.

Operational Complexity:

Dual listings create complexity. IQM must comply with both U. S. and European regulatory frameworks. Financial reporting must meet both GAAP and IFRS standards. Investor relations becomes more complex with two separate investor bases.

However, many European tech companies successfully manage dual listings. This isn't a deal-breaker, just a practical reality.

Timing Considerations:

IQM's SPAC merger with Real Asset Acquisition Corp. completes first, likely in late 2025. The Nordic listing could follow months or years later, once IQM is established as a public company.

The Hype Cycle Risk: Pattern Recognition from Past Tech Bubbles

Investing in quantum computing right now feels familiar if you've experienced previous tech bubbles. The pattern is recognizable:

- Genuinely promising technology (quantum computing is real, the physics works, potential is enormous)

- Government and big tech validation (signals that powerful institutions think this matters)

- Media narrative enthusiasm (every tech publication covers quantum computing optimistically)

- Venture capital money flow (billions flowing into quantum startups)

- Early exits and IPOs (companies go public to cash in on investor enthusiasm)

- Inflated projections (timelines compressed, revenue forecasts aggressive)

- Investor euphoria (anyone dismissing quantum computing is dismissed as not "getting it")

This exact pattern preceded the dot-com crash (where the internet was genuinely transformative, but valuations got absurd), the 2017-2018 blockchain bubble (where distributed ledgers were genuinely interesting, but most use cases didn't materialize), and the 2021-2022 SPAC wave (where some of the companies were good, but most were overvalued).

Lessons from Previous Cycles:

- Genuine technology + terrible timing = investor loss: Even if quantum computers become crucial to society, if you buy the IPO at peak hype, you'll likely lose money before profits arrive

- Execution matters more than potential: Companies that execute on realistic timelines and show customer success outperform those making aggressive promises

- Working backwards from revenue > working forwards from potential: Projecting from 500 million in 2030 requires multiple things to go right simultaneously

- Concentrated customer bases are risky: If IQM has 20 customers and loses 5, revenue drops significantly

- Sector sentiment drives individual stocks: A negative quantum computing news story could tank IQM stock even if the company is performing well

None of this proves quantum computing won't be transformative. It just means investors should be realistic about downside risk and the timeline for returns.

The Path Forward: What Success Looks Like for IQM

IQM's success over the next 5-7 years isn't guaranteed, but the company has advantages that increase its odds relative to other quantum startups.

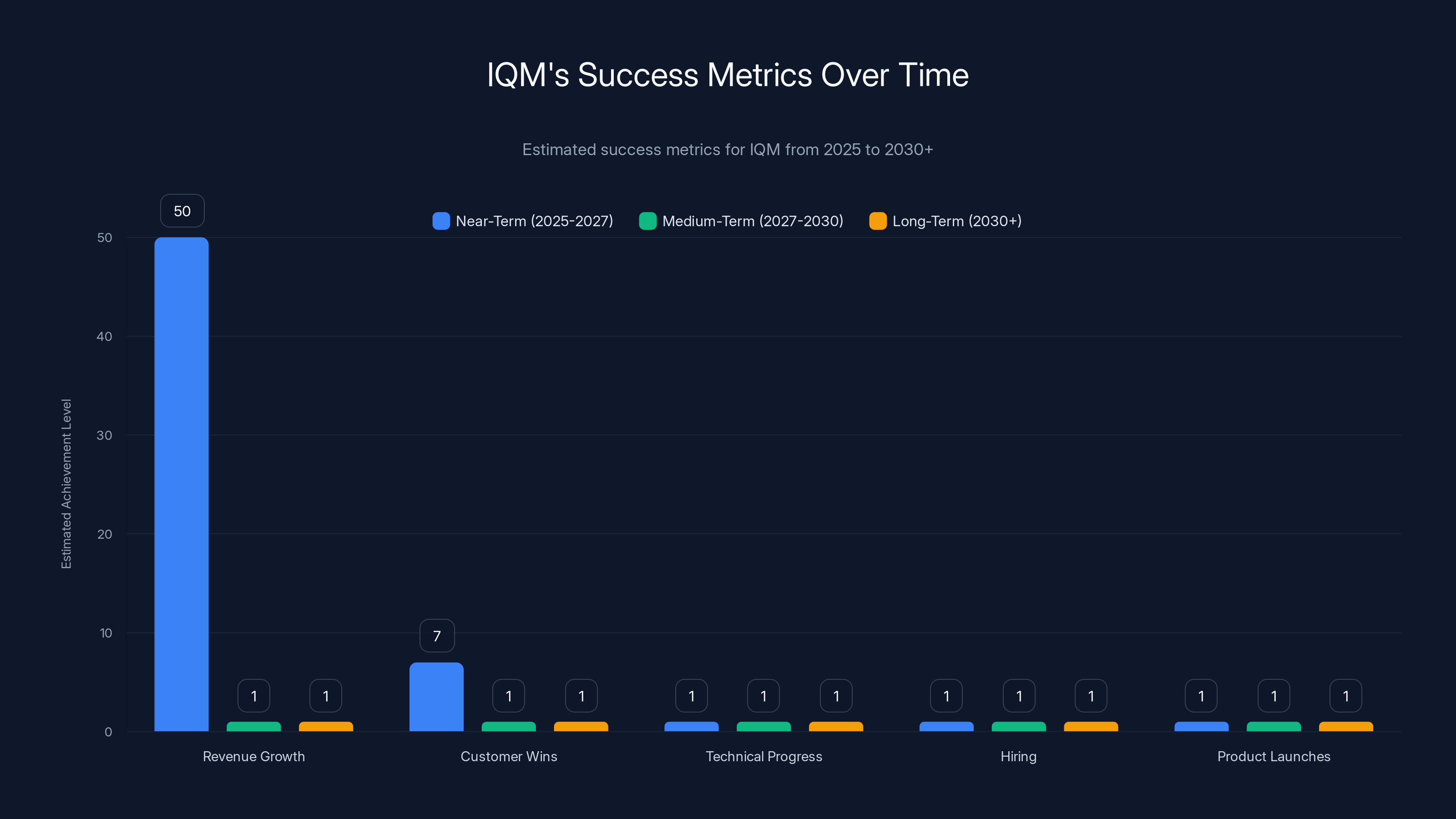

Near-Term Success Metrics (2025-2027):

- Revenue Growth: Converting bookings into revenue and growing top line 40-60% annually

- Customer Wins: Securing 5-10 new significant customers annually

- Technical Progress: Publishing research showing improved error rates and qubit performance

- Hiring: Building world-class engineering and business teams

- Product Launches: Releasing next-generation hardware with more qubits and better performance

Medium-Term Success Metrics (2027-2030):

- Path to Profitability: Revenue growth outpacing cash burn, with a visible path to EBITDA positivity

- Quantum Advantage Demonstration: Real-world use cases where IQM systems deliver measurable value

- Market Expansion: Moving beyond niche academic/research customers to industrial applications

- Partnerships: Forming strategic partnerships with enterprises that expand distribution or use cases

- Talent Retention: Keeping top physicists and engineers despite competitive poaching from big tech

Long-Term Success Metrics (2030+):

- Profitability: Actually making money, not just growing revenue

- Market Leadership: Either market leader in superconducting qubits or acquired/merged into larger player at favorable terms

- Technology Evolution: Moving from current systems to next-generation approaches (error-corrected logical qubits, larger systems)

- Customer Diversification: Revenue spread across many customers in different industries, reducing concentration risk

Why IQM Has a Better-Than-Average Chance:

- Full-stack control of product reduces dependency on partners

- Deep academic/technical roots provide credibility and access to talent

- European base provides access to government funding and customers

- Focus on actual customer success rather than just qubit counts

- $450 million in post-IPO cash provides runway for sustained R&D

Why IQM Could Fail:

- Quantum advantage timeline extends beyond capital runway

- Competitors develop superior technical approaches

- Customer churn if promised results don't materialize

- Larger tech companies commoditize quantum computing, competing on price

- Sector sentiment shifts negative, drying up capital

Broader Implications: What IQM's IPO Means for Quantum Computing

Beyond IQM specifically, the company's SPAC listing is significant for what it signals about the quantum computing sector.

Sector Validation: When multiple quantum companies go public simultaneously (Infleqtion, Xanadu, IQM in early 2025), it signals investor confidence in the sector's long-term viability. This isn't a guarantee of near-term returns, but it does mean the sector has critical mass.

Capital Access: Public markets provide capital that enables quantum companies to move faster. R&D budgets expand, hiring accelerates, and customer acquisition becomes more aggressive. The sector moves from "promising research" to "competitive businesses."

Accountability Shift: Private companies can miss timelines without much accountability. Public companies face quarterly earnings pressure and analyst scrutiny. This creates pressure for transparency but also risk-taking—companies might push aggressive timelines to satisfy investors.

Talent Competition: As quantum companies go public, they can offer stock options with real liquidity events. This intensifies competition for quantum talent with academia and big tech.

Investment Cascades: When Infleqtion goes public successfully, it makes Xanadu's IPO easier (similar sector, established narrative). This creates a cascade effect where once the floodgates open, multiple companies go public in quick succession.

Consolidation Potential: Public companies have currency (stock) they can use for acquisitions. IQM could acquire smaller quantum software companies, hardware component suppliers, or customer service businesses to accelerate growth.

These dynamics accelerate the quantum computing industry's development cycle. Whether that's ultimately good or bad depends on execution.

Conclusion: The Quantum Computing IPO Wave and What It Means

IQM's $1.8 billion SPAC listing is a milestone, not an endpoint. It signals that quantum computing has graduated from pure research to commercial industry. The company gets capital to accelerate development. Investors get exposure to the sector. The field gets credibility and momentum.

But let's be clear about what this IPO is and isn't.

It's not a validation that quantum computers will be useful anytime soon. Most credible timelines put practical quantum advantage 5-10 years away. IQM's valuation assumes that happens, but assumes don't make it so.

It's not a safe investment for risk-averse investors. Quantum computing stocks are volatile, sentiment-driven, and dependent on technology breakthroughs. Short-term price movements could be dramatic in either direction.

It is a signal that institutions—government, big tech, venture capital, investment banks—are serious about quantum computing. When that many smart actors align on a technology's importance, even skeptics should pay attention.

It is a potential future opportunity for patient investors. If quantum advantage arrives and IQM captures meaningful market share, investing at today's valuations could look like a steal in 2035. But "could look like" and "will look like" are very different things.

It is a test case for whether SPAC mergers can work in deep tech. Most SPAC-merged companies have underperformed. IQM's execution over the next 3-5 years will demonstrate whether SPACs are a viable path to public markets for legitimate deep-tech companies or just a faster route to eventual losses.

For IQM specifically, the IPO is a beginning, not a destination. The company now has the capital, credibility, and scrutiny that comes with public markets. Success requires executing on technical progress, converting customer bookings to revenue, and navigating the quantum computing sector's competitive landscape.

The next chapter is genuinely interesting. In five years, we'll know whether IQM's $1.8 billion valuation was prescient or premature. Until then, the company joins the growing list of quantum startups with public markets access—and the pressure to prove quantum computing's potential.

FAQ

What is IQM Quantum Computers?

IQM Quantum Computers is a Finnish quantum computing company founded in 2018 as a spinout from Aalto University and VTT Technical Research Center. The company designs, manufactures, and operates superconducting quantum computers, offering both on-premises systems and cloud-based access to its quantum processors. IQM reported

How does IQM's superconducting qubit technology work?

IQM uses superconducting qubits that operate at temperatures near absolute zero (around 20 millikelvin). These qubits exploit quantum mechanical properties in superconductors—materials that conduct electricity with zero resistance when cooled below critical temperatures. By maintaining qubits in superposition states and manipulating them through precise control electronics, IQM's systems can represent multiple computational states simultaneously, the key advantage of quantum computing over classical systems.

Why is IQM going public via a SPAC instead of a traditional IPO?

IQM chose the SPAC (Special Purpose Acquisition Company) route because it's faster than a traditional IPO and provides certainty of valuation upfront. With a SPAC merger, the price and structure are negotiated directly with the blank-check company sponsor, eliminating the uncertainty of a public roadshow. For a company like IQM seeking capital while quantum computing sentiment is hot, SPAC mergers offer speed and access to capital without the months-long IPO process, though they come with additional risks related to SPAC sponsor incentives and historical SPAC underperformance.

What is the $1.8 billion valuation based on?

The

What are the main risks for IQM as a public company?

Key risks include timeline delays in achieving practical quantum advantage (pushing returns further into the future), competitive displacement by larger tech companies entering quantum commercialization, fundamental technology risks if superconducting qubits prove inferior to alternative approaches, customer concentration (currently limited to 50-100 organizations globally), capital efficiency under public market scrutiny, and macro conditions affecting investor appetite for deep-tech investments. Additionally, SPAC-merged companies historically underperform due to valuation hype and shareholder dilution from sponsor incentives.

When will quantum computers deliver practical value?

There's no consensus timeline. Most credible estimates place practical quantum advantage 5-10 years away (2030-2035), though optimists suggest 3-5 years and skeptics believe it could be 15+ years. Quantum computers must solve real-world problems faster than classical systems at scale, achieve error rates below critical thresholds, and demonstrate economic advantage. Current systems remain in research phases with limited commercial applications, despite progress in qubit technology and error correction approaches.

How does IQM compete against IBM, Google, and other quantum computing giants?

IQM differentiates through full-stack control (designing qubits, control electronics, cryogenics, and software in-house), focus on customer success over qubit count rankings, and specialization in superconducting systems. IBM and Google have more resources and broader businesses, but quantum is peripheral to their operations. IQM's smaller size enables faster iteration and customer-centric development. However, IQM faces risk if larger players commit fully to quantum commercialization or if alternative qubit technologies outperform superconducting approaches.

What should investors know about buying IQM stock post-IPO?

Investors should understand that IQM is a high-risk, long-duration bet on quantum computing's commercial timeline. Stock performance will be volatile and sentiment-driven. The company's success depends on quantum advantage arriving within its cash runway, converting customer bookings to revenue, and maintaining market share against competitors. SPAC-merged companies historically underperform; patience and realistic timeline expectations are essential. Dollar-cost averaging and treating IQM as a long-term speculative position (not core portfolio) are prudent approaches for interested investors.

Key Takeaways

- IQM's $1.8B SPAC valuation assumes quantum advantage arrives within 5-7 years—an unproven timeline that represents the company's greatest risk factor

- The company reported 100M in bookings, suggesting strong customer interest but revenue conversion risk remains high

- Full-stack quantum computer control (qubits, cooling, electronics, software) gives IQM competitive advantages over point-solution competitors like IBM and Google

- SPAC-merged quantum companies face headwind from sector precedent: IonQ stock declined 30-50% within one year of its 2023 IPO

- Quantum computing's addressable market remains tiny (~50 organizations globally operate dedicated quantum systems), limiting IQM's near-term revenue potential despite ambitious projections

Related Articles

- Quantum Computing Funding Boom: Why VCs Are Betting $260M on the Future [2025]

- [2025] Unlocking Quantum Potential: Google's Quest with UK Experts

- 7 Biggest Tech News Stories This Week [February 2026]

- Network Modernization for AI & Quantum Success [2025]

- Light-Controlled Magnetism at Room Temperature: The Breakthrough [2025]

- The 11 Biggest Tech Trends of 2026: What CES Revealed [2025]