Netflix-HBO Max Merger 2025: Complete Analysis, Antitrust Implications & Streaming Alternatives

Introduction: Understanding the Proposed Netflix-Warner Bros. Discovery Merger

The streaming landscape is undergoing a seismic shift. In early 2025, Netflix made a bold strategic play by proposing to acquire Warner Bros. Discovery's streaming and film studio assets—a deal that could fundamentally reshape how millions of viewers consume entertainment globally. The proposed acquisition represents one of the most significant consolidation efforts in streaming history, with Netflix seeking to acquire HBO Max and WB's prestigious film studios for approximately

This isn't merely a financial transaction. The merger carries profound implications for consumers, competitors, regulators, and the entire entertainment ecosystem. As Netflix co-CEO Ted Sarandos testified before the US Senate Judiciary Committee's Subcommittee on Antitrust, Competition Policy, and Consumer Rights, the company claims the acquisition would benefit consumers through increased content availability, better pricing through economies of scale, and enhanced competition against tech giants like Apple, Google, and Amazon according to C-SPAN.

However, the proposed merger has sparked intense scrutiny and legitimate concerns. Consumer advocates, rival streaming platforms, and regulatory bodies are questioning whether consolidation of this magnitude would stifle competition, lead to higher subscription prices, reduce creative diversity, and concentrate too much power in Netflix's hands as noted by the American Economic Liberties Project. The fundamental tension at the heart of this debate is whether mergers in the streaming industry drive innovation and consumer value or simply enable monopolistic behavior and price gouging.

Understanding this merger requires examining multiple dimensions: the current state of streaming competition, the strategic rationale behind Netflix's bid, the genuine concerns raised by antitrust experts, the pricing implications for consumers, and the viable alternatives available in an increasingly fragmented streaming marketplace. This comprehensive guide explores each dimension, providing you with the context needed to understand how this merger could impact your streaming choices and costs in the years ahead.

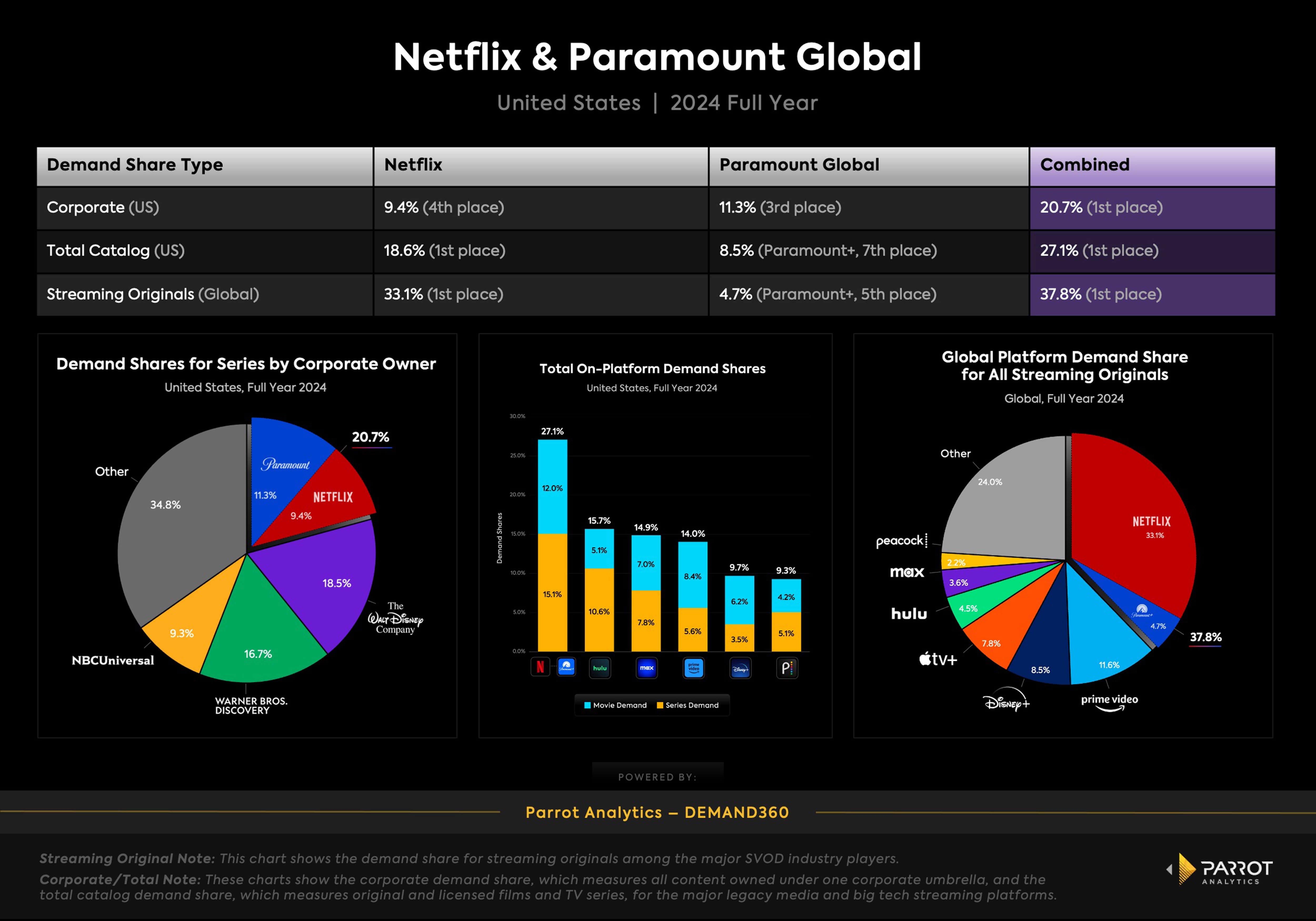

The stakes couldn't be higher. Netflix already commands 301.63 million subscribers globally as of January 2025, making it the dominant force in subscription video-on-demand according to DemandSage. If the merger proceeds, Netflix would absorb Warner Bros. Discovery's 128 million subscribers (across HBO Max and Discovery+), creating an entertainment behemoth unlike anything the industry has seen before. Understanding what this means for you as a consumer requires looking beyond the rhetoric from both Netflix and regulators.

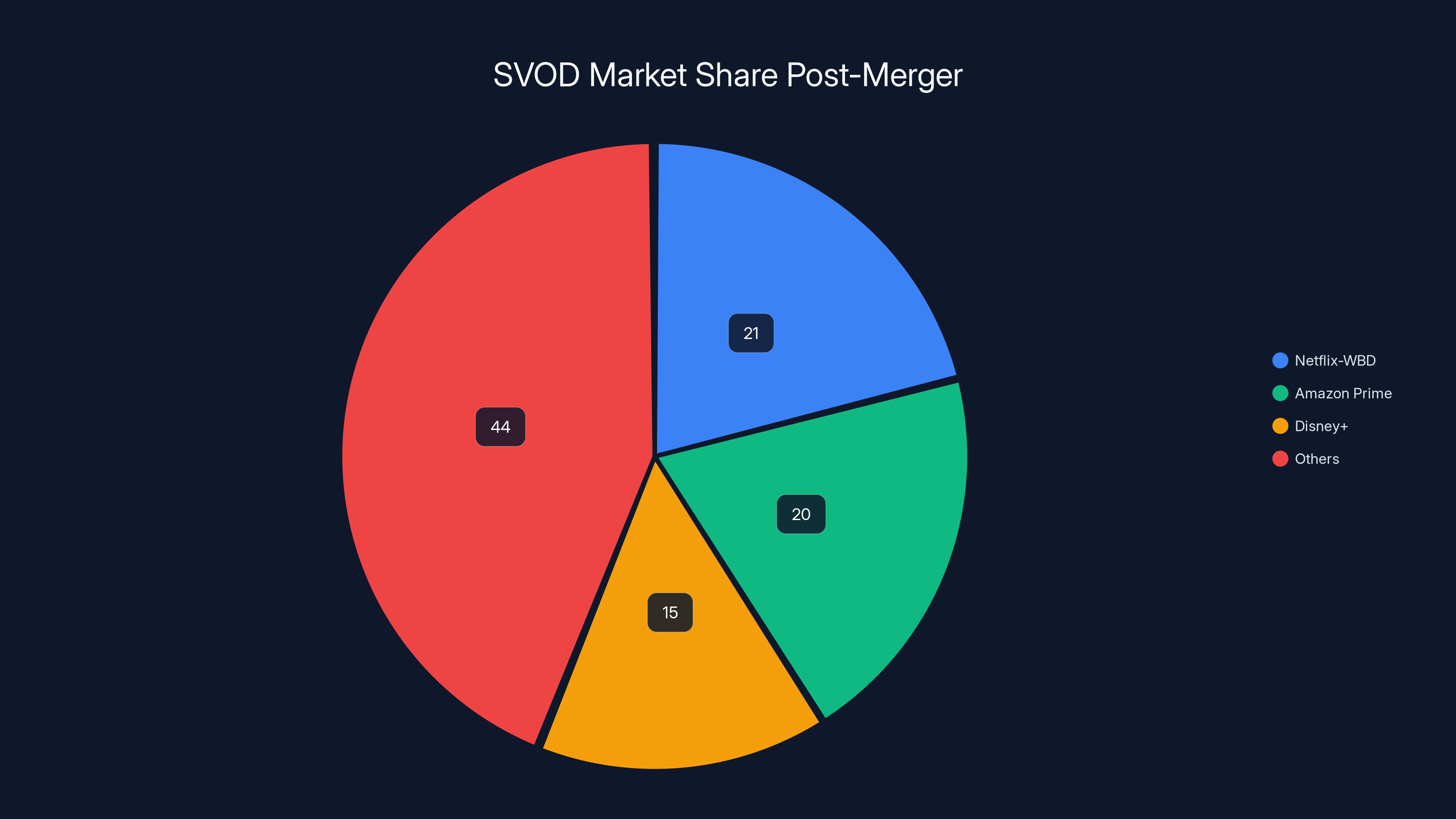

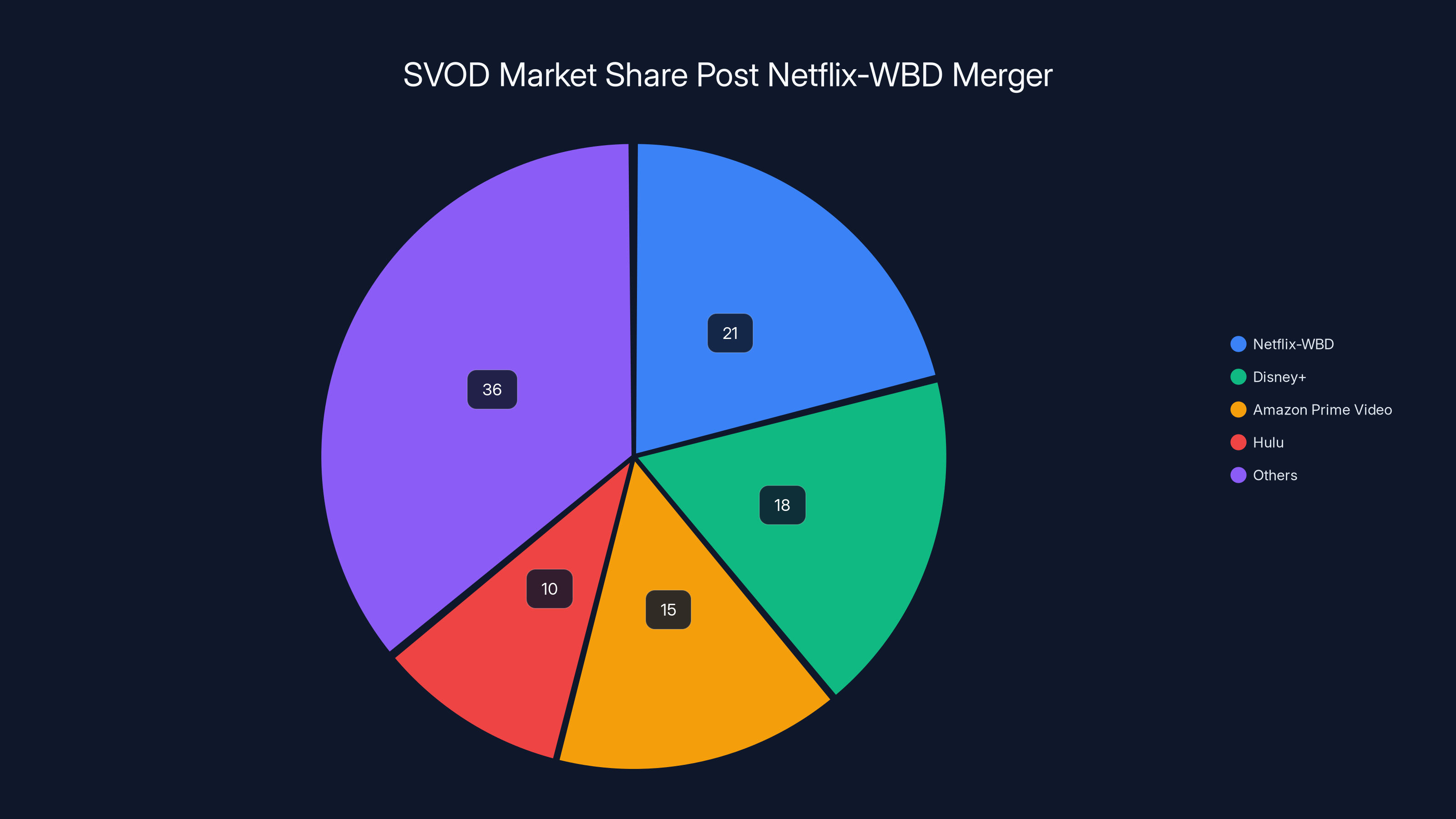

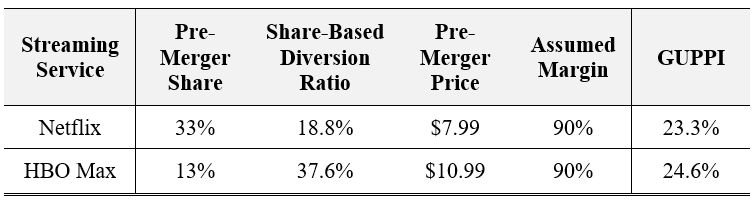

The proposed Netflix-WBD merger would control approximately 21% of the SVOD market, increasing their competitive edge against other major players like Amazon Prime and Disney+. Estimated data.

The Current Streaming Landscape: Market Consolidation in Motion

Market Share and Competitive Positioning

The streaming industry has evolved dramatically since Netflix's early dominance in the mid-2010s. What began as Netflix versus cable television has transformed into Netflix competing against five or six major players simultaneously, each backed by deep-pocketed corporate parents and tech giants. The current landscape reveals a market in flux, with consolidation pressures building from multiple directions.

As of early 2025, the subscription video-on-demand (SVOD) market is dominated by a handful of players: Netflix leads with over 301 million subscribers, making it larger than the next three competitors combined as reported by DemandSage. Disney+ has grown substantially since its launch in 2019, now commanding a significant subscriber base through Disney's aggressive bundling strategy. Warner Bros. Discovery controls HBO Max, the premium streaming service built on decades of HBO's prestige brand, along with Discovery+, which targets documentary and reality TV audiences according to Collider. Paramount+ (formerly CBS All Access) leverages Paramount's extensive content library and represents Viacom CBS's streaming ambitions. Amazon Prime Video, technically the largest video platform by content volume, bundles streaming with broader Prime membership benefits.

Outside these incumbents, newer challengers like Apple TV+, Peacock (NBC/Comcast), and niche services like The Criterion Collection, Shudder, and specialty platforms serve specific audience segments. However, the market dynamics increasingly favor consolidated players with massive content budgets and technological infrastructure.

Netflix's dominance stems from its first-mover advantage, superior technology infrastructure, sophisticated recommendation algorithms, and original content investment. As of January 2025, Netflix subscribers pay

Why Consolidation Pressures Exist

The push toward consolidation reflects fundamental economics of the streaming business. Content production costs have exploded as every major player invests billions in original programming to compete with Netflix's legendary shows. The average cost of producing prestige drama series has risen from

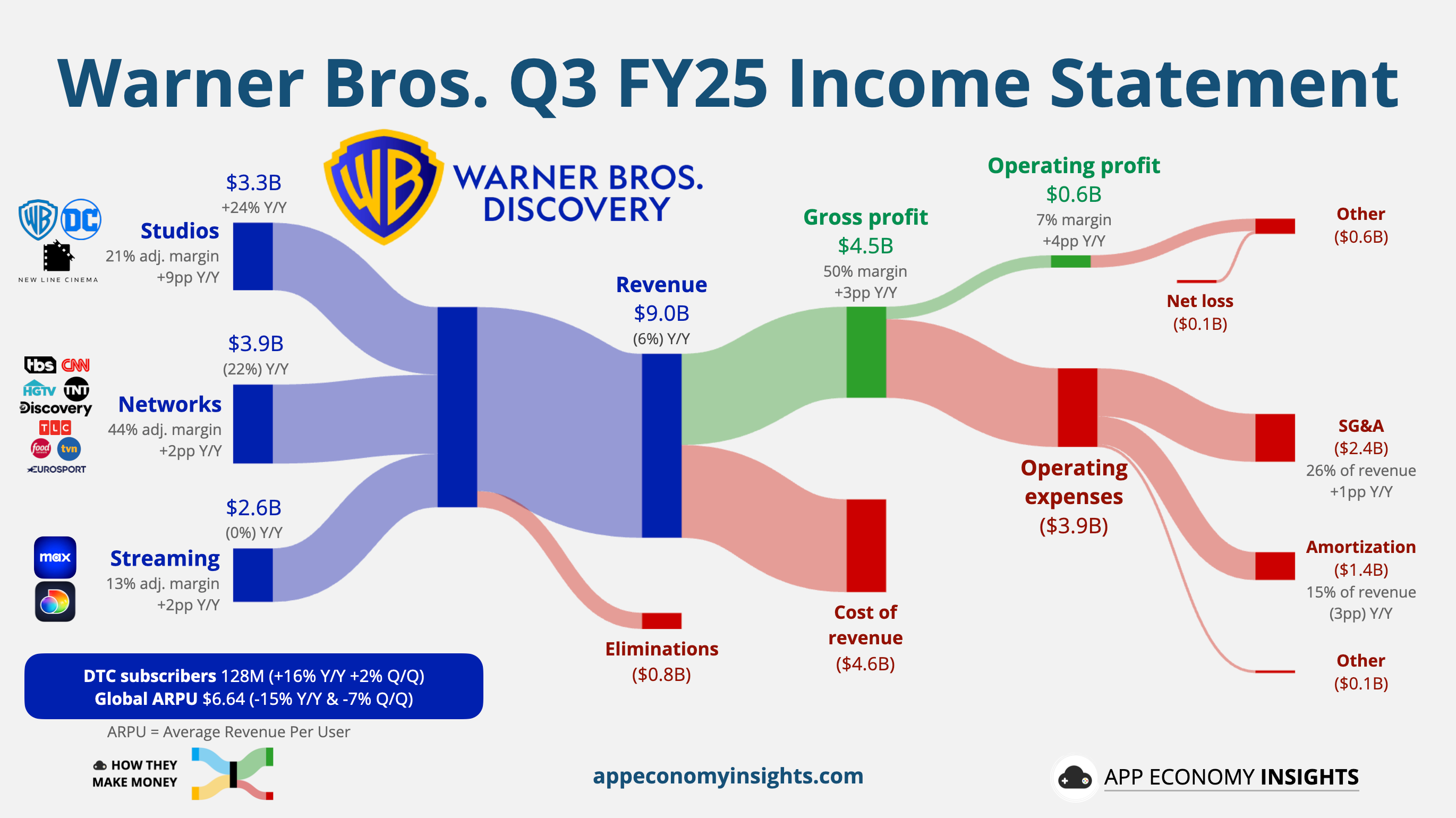

Netflix's content spend approaches $16-17 billion annually as of 2025. To maintain this spending, Netflix needs subscriber growth, pricing power, or both. However, as markets saturate in developed countries and as global expansion faces regulatory headwinds, pricing power becomes the lever. This is precisely why Netflix raised prices in January 2025 despite adding subscribers—the company is optimizing for revenue per user rather than pure subscriber growth as analyzed by Business.com.

WBD faces the opposite pressure. While HBO Max contains some of the highest-prestige content in streaming (HBO's library remains unmatched), the service struggles with subscriber growth and profitability. The company has attempted multiple strategic pivots, including the divisive decision to remove content from HBO Max to reduce streaming losses—a move that infuriated both creators and subscribers as reported by Collider. WBD's financial pressures have made it an attractive acquisition target.

For Netflix, acquiring WBD solves multiple problems simultaneously: it gains HBO's legendary content library, access to Warner Bros.' massive film studio output, the ability to absorb WBD's content production infrastructure, and mathematical synergies that could improve profitability across both platforms. This explains Netflix's aggressive bid in a competitive process that also includes Paramount/Skydance's counter-bid as noted by AOL Finance.

Netflix's pricing strategy shows gradual increases of

Netflix's Strategic Rationale: Why Acquire HBO Max and Warner Bros?

The Content Consolidation Argument

Netflix's strategic case for the merger centers on content quality, diversity, and consumer value creation. According to Sarandos's Senate testimony and Netflix's public filings, the acquisition would accomplish several strategic objectives that Netflix argues benefit consumers as detailed in his testimony.

First, the merger would create unparalleled content breadth. HBO's legacy of prestige drama, beginning with "The Sopranos" and continuing through "Game of Thrones," "True Detective," "Veep," and "The Wire," represents cultural touchstones that Netflix has struggled to replicate despite massive investment. Even Netflix's acclaimed originals like "Stranger Things," "The Crown," and "Ozark" haven't achieved HBO's cultural cachet. By combining Netflix's technology platform and scale with HBO's talent relationships and creative prestige, Netflix argues it could produce better content more efficiently.

Second, the merger would integrate Warner Bros.' theatrical film division. This is strategically significant. Netflix has invested heavily in original films but hasn't cracked the prestige theatrical market at the scale that traditional studios achieve. Warner Bros. produces roughly 20-30 theatrical films annually across its various banners—a pipeline of premium content that Netflix currently doesn't have access to. For Netflix subscribers, this means the platform could offer new Warner Bros. theatrical releases within months of theatrical windows rather than the current licensing arrangements with other distributors as noted in Netflix's announcement.

Third, Netflix identifies cost synergies and operational efficiencies. Combining WBD's television production operations with Netflix's platform could reduce overhead, streamline content licensing negotiations, and improve content monetization. Netflix cites the metric that its subscribers watch content at approximately

The Competitive Defense Against Big Tech

A subtler but important element of Netflix's merger argument is defensive positioning against technology giants. Sarandos emphasized during Senate testimony that Google, Apple, and Amazon represent the real competitive threats in streaming, not traditional media competitors like Paramount. This argument deserves serious examination as noted by the Wall Street Journal.

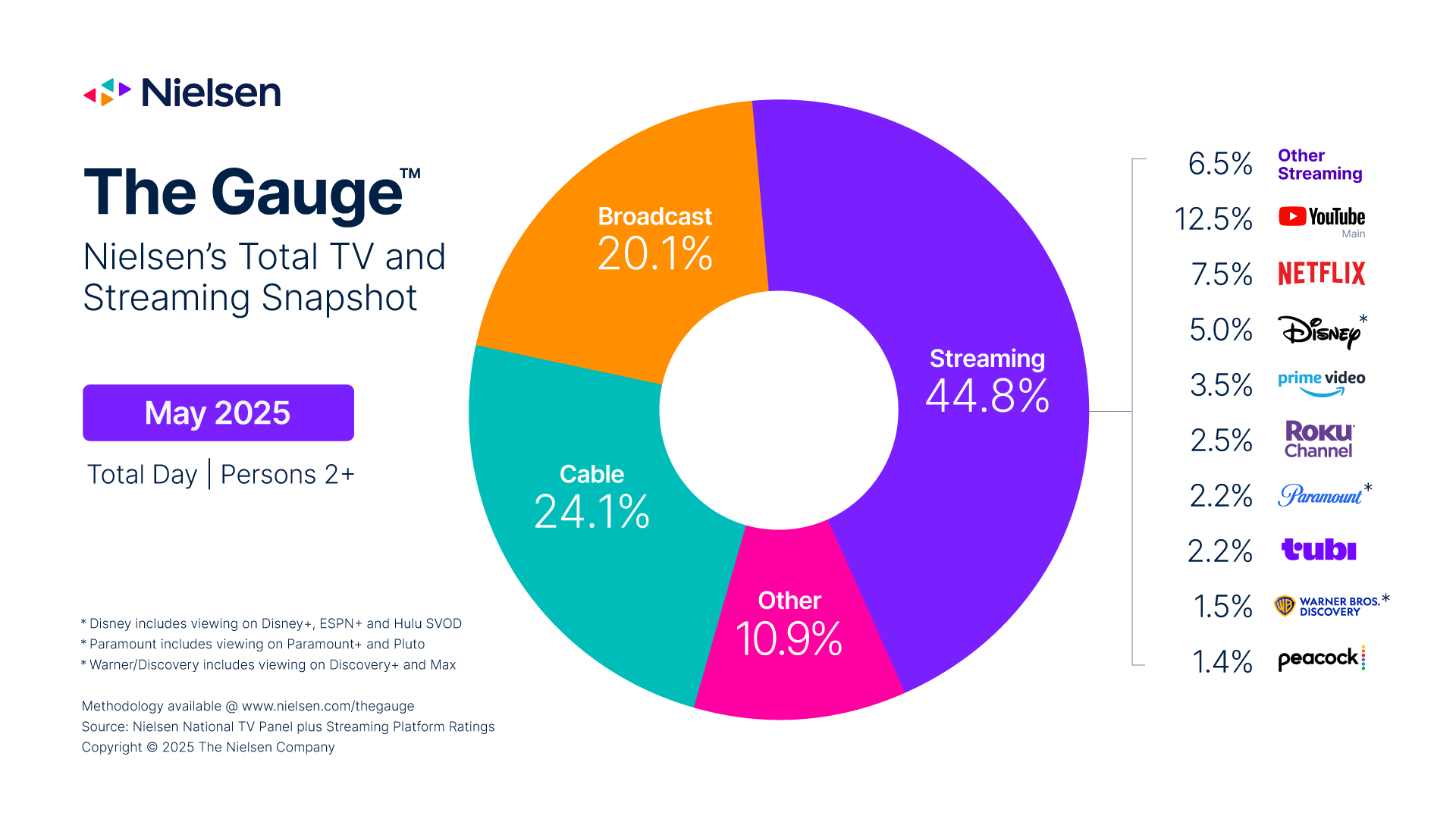

YouTube, which isn't a dedicated streaming service, commands 12.7% of American television viewing time according to Nielsen data—more than Netflix's 9% of TV viewership as reported by eMarketer. Apple TV+ has released culturally significant content like "Ted Lasso" and "Severance" while leveraging hundreds of millions of iPhone and iPad users as a distribution channel. Amazon Prime Video bundles streaming with broader Prime membership benefits that provide customer stickiness beyond content quality.

Netflix's argument is that these tech giants have fundamentally different business models and competitive advantages. Google profits from YouTube advertising, Apple bundles services with hardware ecosystems, and Amazon uses Prime Video as a customer acquisition tool for retail. Netflix, by contrast, relies entirely on subscription revenue from dedicated streaming. Against this backdrop, Netflix argues that consolidating with WBD isn't about creating a monopoly in streaming but about achieving sufficient scale to compete with diversified tech giants that can subsidize streaming losses.

This defense has merit but also exhibits selective framing. Netflix could compete more aggressively with Apple and Google through innovation, technology investment, and premium content without requiring a merger. However, from a pure financial perspective, Netflix's argument that it faces competitive pressure from tech giants with infinite capital availability and diverse revenue streams is mathematically valid as analyzed by Florida Politics.

The Antitrust Concerns: Why Regulators and Competitors Are Skeptical

Market Concentration and Monopoly Risks

The antitrust case against the Netflix-WBD merger centers on market concentration. In economic terms, when a proposed merger would give a single company control over 20%+ of a relevant market, antitrust authorities examine whether the merger would substantially lessen competition. A full Netflix-WBD combination would control approximately 21% of the SVOD market, which crosses traditional thresholds triggering regulatory scrutiny as noted by Bleeding Cool.

However, market concentration analyses in streaming are contested because market definition itself is disputed. Is the relevant market "subscription video-on-demand services"? Or is it broader—"video entertainment" including YouTube, cable, and traditional television? Or narrower—"prestige drama" or "theatrical films"? How these questions are answered dramatically changes concentration analysis.

For consumers, the practical concern is more tangible: if Netflix-WBD merged, would you face higher prices, worse service, and fewer programming alternatives? This requires examining Netflix's track record on pricing and whether the company faces genuine competitive constraints today.

Netflix has raised subscription prices multiple times, most recently in January 2025. However, the company's claim that price increases coincide with "a lot more value" for subscribers has some factual basis. Comparing January 2025 to January 2020, Netflix's library has grown from roughly 6,500 titles to over 8,500 titles, and the quality of original content has demonstrably improved. Netflix spend per content hour viewed has declined from

That said, Netflix's pricing power has increased as competitors have fragmented. A consumer wanting prestige drama must subscribe to multiple services: Netflix (for "Stranger Things," "Ozark," "The Crown"), HBO Max (for HBO originals), Paramount+ (for "Severance," "The White Lotus"), and potentially others. The fragmentation that emerged as studios launched competing platforms has actually reduced consumer choice and increased total spending. A merged Netflix-WBD would reduce fragmentation in some categories while potentially increasing it in others as noted by the American Economic Liberties Project.

Content Diversity and Creative Concerns

Beyond pricing, antitrust authorities and industry observers raise concerns about content diversity. Would a Netflix-WBD merger reduce the diversity of storytelling, creative voices, and programming available to consumers?

Historically, vertical integration of content production and distribution has produced mixed outcomes. When major studios vertically integrated in the 1930s-1940s, it enabled efficient production but also created gatekeeping power that limited which films and voices reached audiences. However, modern streaming platforms have more democratic content discovery mechanisms than traditional studio systems, potentially mitigating these concerns.

A specific concern is whether Warner Bros.' slate of theatrical films would be privileged on Netflix over other studios' content, potentially disadvantaging competitors like Disney, Universal, or Sony. Netflix has committed to a "window" structure where theatrical films get exclusive runs before streaming releases, but the specific terms matter tremendously. If Warner Bros. films get 45-day theatrical exclusivity before Netflix release, while other studios' films get 90-day windows, that's preferential treatment that could disadvantage rivals as analyzed by Business.com.

Another concern involves original series. HBO's brands (HBO, HBO Max, Cinemax) have developed distinct creative identities over decades. Would those identities survive integration into Netflix's massive platform? Or would HBO talent, production teams, and editorial independence gradually dissolve into Netflix's content machine? Critics argue this represents a loss—the reduction from distinct editorial voices to a single dominant platform as noted by the American Economic Liberties Project.

The Paramount Counter-Bid and Competitive Dynamics

Paramount's hostile counter-bid for all of WBD (not just streaming assets) adds complexity to antitrust analysis. If Paramount acquires WBD, the result would be different competitive dynamics than a Netflix acquisition. Paramount (a traditional media company) combined with WBD would create a vertically integrated entertainment giant controlling studios, cable networks, theatrical distribution, and streaming platforms as noted by AOL Finance.

Netflix acquisition = Tech platform + Content consolidation Paramount acquisition = Traditional media consolidation

From an antitrust perspective, these produce different concerns. Netflix acquisition risks concentration in SVOD specifically and tech-platform dominance broadly. Paramount acquisition risks concentration across traditional media but potentially less tech-platform concentration. Regulators must evaluate which scenario poses greater antitrust risk.

The proposed Netflix-WBD merger would control approximately 21% of the SVOD market, potentially raising antitrust concerns due to increased market concentration. Estimated data.

Pricing Implications: Will Netflix Raise Prices Post-Merger?

Historical Netflix Pricing Patterns

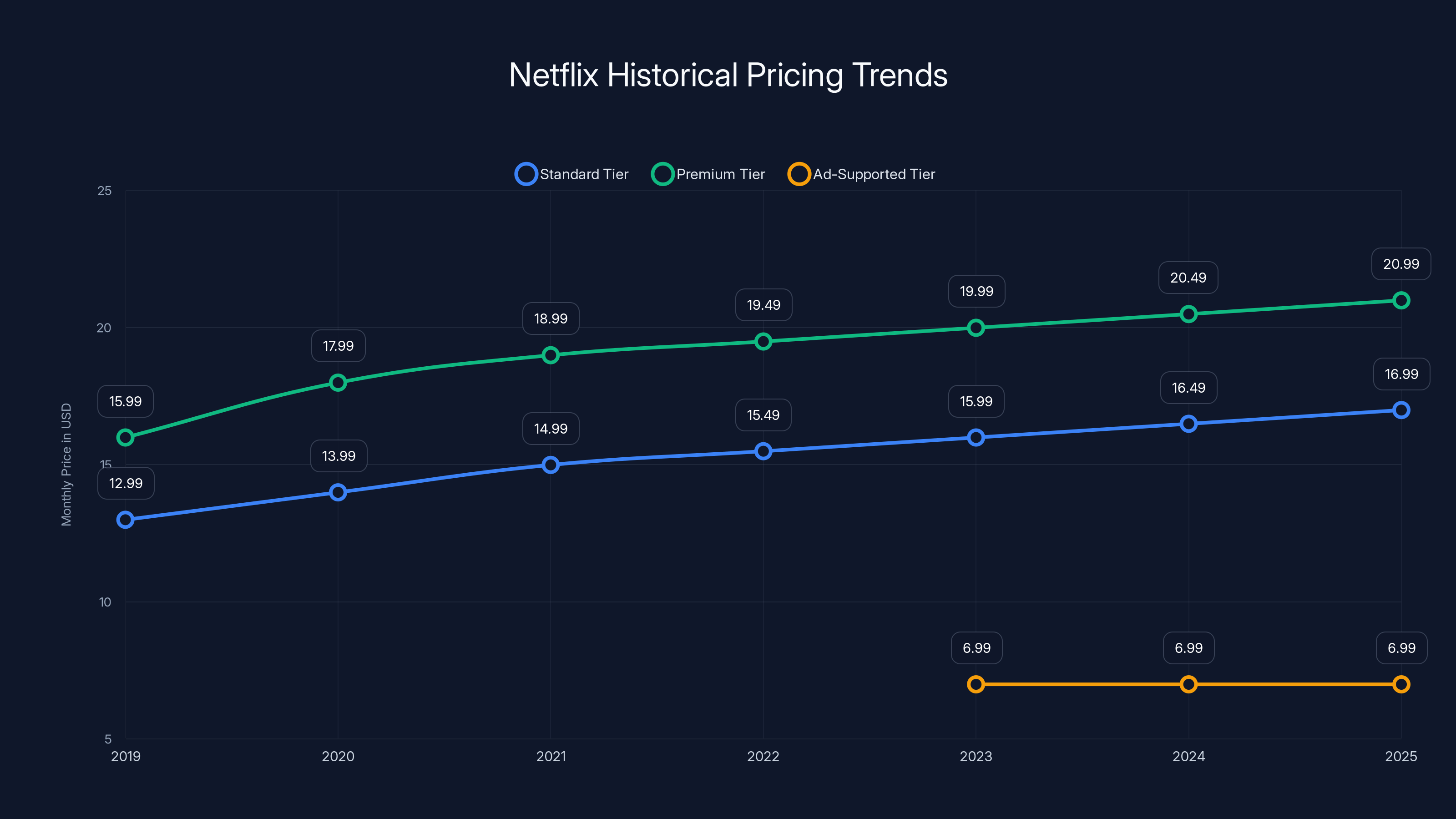

To evaluate whether a Netflix-WBD merger would lead to price increases, examining Netflix's pricing history provides important context. Netflix doesn't raise prices simultaneously across all markets—instead, the company uses a sophisticated pricing strategy that varies by region, by subscription tier, and by timing.

In early 2025, Netflix raised prices on its Standard tier (with ads) and Premium tier (ad-free, 4K) in the United States. The price increases reflected Netflix's positioning as a premium service with superior content and technology. However, Netflix simultaneously introduced a lower-priced ad-supported tier at $6.99 monthly, providing price-sensitive consumers an affordable option. This represents a strategic choice: rather than a single price increase that affects all subscribers, Netflix created pricing tiers that allowed price-conscious consumers to maintain affordability while capturing higher revenue from consumers willing to pay more as noted by Netflix.

Network Netflix's past price increases have coincided with periods of intense competition. When Disney+ launched in 2019, Netflix initially held prices steady but then began raising prices as Disney+ gained subscribers. When HBO Max launched at a premium price point, Netflix followed with price increases. This pattern suggests Netflix raises prices when competitive pressure decreases—i.e., when competitors aren't as strong or when Netflix achieves differentiated positioning as analyzed by Business.com.

A key insight from Netflix's pricing history: the company raises prices slowly and incrementally rather than in dramatic jumps. The median price increase is $1-2 per tier per year, implemented months apart across different markets. This allows subscriber churn to remain manageable while capturing incremental revenue increases.

Economic Logic of Merger-Related Pricing

Would a Netflix-WBD merger create incentives for price increases? The economic logic says yes, with important caveats.

First, cost structure advantages. By combining Netflix's platform with WBD's content production, Netflix would reduce the cost of content acquisition for prestige drama and HBO content. Currently, Netflix licenses prestige content from external studios at premium rates. With vertical integration, Netflix produces this content internally at potentially lower marginal costs. Economic theory suggests that cost reductions should improve margins rather than increase prices—in a competitive market, companies reduce prices to gain market share when cost structures improve as reported by Stock Titan.

However, streaming isn't a competitive market in the traditional sense. Netflix has demonstrated pricing power even without merger-driven cost advantages. This suggests that cost structure improvements might improve Netflix's margins rather than translate into price reductions.

Second, competitive position. A merged Netflix-WBD would control more content, potentially improving Netflix's competitive position against Disney Bundle, Paramount+, and Apple TV+. Improved competitive position could enable price increases if the company believes subscribers have limited alternatives. This is the core antitrust concern: pricing power increases when competitive alternatives decrease.

Third, subscriber overlap. Netflix's testimony highlighted that 80% of HBO Max subscribers also subscribe to Netflix. This overlap means that current HBO Max subscribers would consolidate into Netflix post-merger. For these users, the effective price might actually decrease if HBO Max pricing could be eliminated while maintaining HBO content access through Netflix. However, for consumers currently watching only HBO Max, losing that standalone option represents a reduction in choice and could force them to subscribe at higher Netflix prices as detailed in his testimony.

Evidence from Past Media Mergers

Historical precedent provides some guidance. When Comcast acquired NBC Universal, concerns about cable and internet pricing didn't materialize in the dramatic way some advocates predicted—but Comcast did privilege NBC content and gradually adjusted pricing structures to extract more value from bundled services. When Disney acquired Fox, Disney rationalized streaming services and increased Disney+ pricing from

These precedents suggest that media mergers typically result in modest price increases (5-15% over 2-3 years) rather than dramatic gouging. However, they also show that merged entities actively work to optimize pricing and sometimes leverage market position to shift consumers toward higher-priced tiers.

Netflix's Regulatory Commitments

During Senate testimony, Sarandos suggested Netflix has working with the Department of Justice on "guardrails" against aggressive post-merger pricing. Details of these commitments haven't been publicly disclosed, but they likely include restrictions on price increases for specified periods and requirements for content availability across price tiers as noted by the Wall Street Journal.

Regulatory commitments (also called "consent decrees") can constrain pricing behavior but create unintended consequences. If Netflix must hold prices constant while inflation increases content costs, the company might respond by reducing content investment, lowering video quality, or eliminating password sharing (Netflix already moved in this direction). These alternatives might be more harmful than moderate price increases.

Value Proposition and Consumer Benefits: What Netflix's Merger Claims Mean

The Cost-Per-Hour Efficiency Argument

Netflix's central claim is that the merger creates consumer value through improved content efficiency. The company calculates that Netflix subscribers spend an average of

The metric measures average revenue per hour of content consumed. It's calculated by dividing total subscription revenue by total hours watched across the subscriber base. Netflix's lower cost-per-hour reflects both factors: higher subscriber base (spreading fixed costs over more consumption) and Netflix's sophisticated recommendation algorithms that drive higher engagement.

For consumers, what does a **

Netflix argues that achieving even better cost-per-hour ratios through merger-driven efficiency gains could enable lower prices or higher content quality at current prices. However, this depends on Netflix choosing to share efficiency gains with subscribers rather than capturing them as increased profit margin as analyzed by Business.com.

Content Availability and Breadth Benefits

A more tangible benefit of the merger would be consolidated HBO and Netflix content. Currently, HBO Max remains a separate platform, requiring separate subscriptions for access to HBO's prestigious library. A merged Netflix-WBD would theoretically bring HBO's entire catalog into Netflix, providing enhanced value for Netflix subscribers as noted in Netflix's announcement.

However, this benefit comes with caveats. HBO's brand has been carefully cultivated over decades as a premium, curated experience. HBO Max's interface, recommendation algorithms, and presentation differ meaningfully from Netflix's approach. When content moves from HBO Max to Netflix, it doesn't lose quality, but some consumers may experience the transition as a dilution of HBO's premium brand identity.

For most consumers, however, consolidated access to Netflix originals, HBO dramas, WB theatrical films, and Discovery+ content on a single platform with single login credentials represents genuine convenience value. This is particularly true for households currently subscribing to both Netflix and HBO Max, who could theoretically eliminate one subscription as reported by Stock Titan.

Theatrical Release Integration

A unique benefit of Warner Bros. acquisition is integration of theatrical films. Warner Bros. produces approximately 20-30 theatrical films annually across DC Comics, prestige drama, and commercial franchises. Currently, these films follow traditional theatrical release windows (90+ days) before arriving on HBO Max or other streaming platforms as noted in Netflix's announcement.

A merged Netflix could potentially compress these windows—offering theatrical releases on Netflix within 45-60 days of theatrical release rather than the traditional 90-120 day windows. This would represent increased value for Netflix subscribers who would access premium theatrical films significantly faster than current licensing arrangements allow.

However, this also presents risks. Shorter theatrical windows could cannibalize theatrical attendance, reducing box office revenue for Warner Bros. films. While Netflix might be indifferent to cannibalization (since both theatrical and streaming revenue accrue to the merged entity), the film industry broadly depends on theatrical revenue to fund prestige productions. If theatrical windows compress too aggressively, it could reduce the economic viability of mid-budget theatrical films, potentially reducing content diversity as analyzed by Business.com.

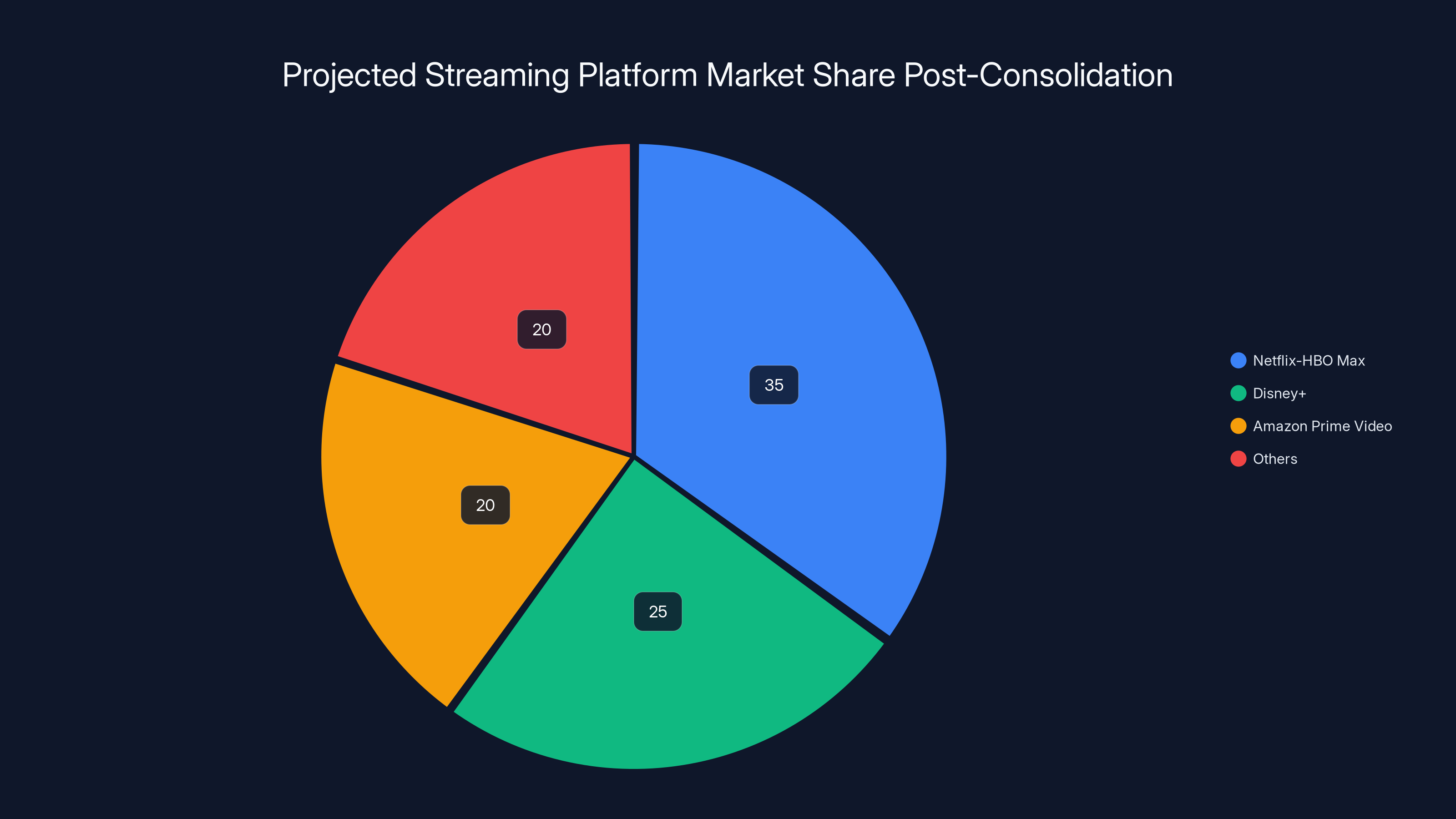

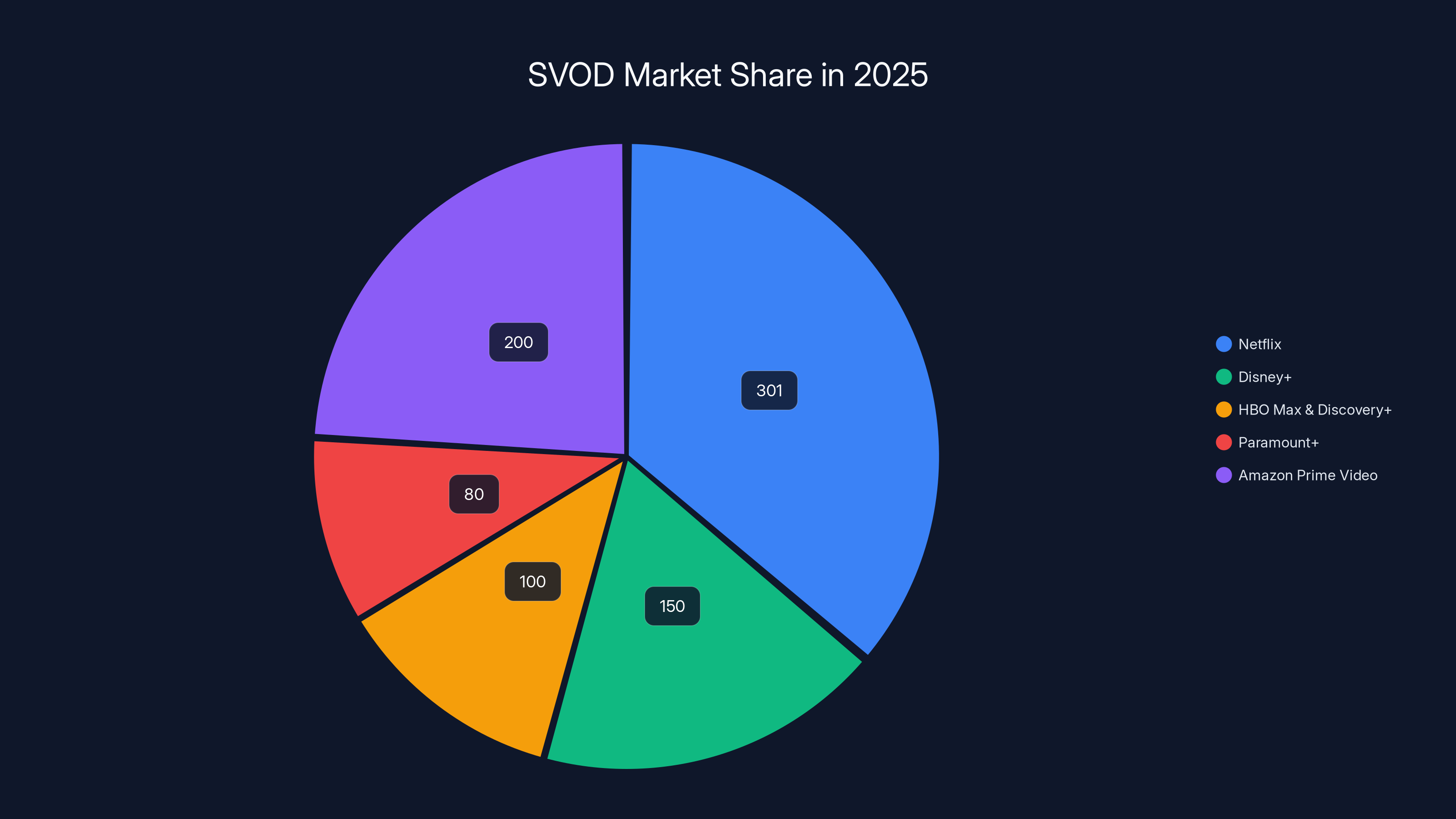

Estimated data suggests that post-consolidation, Netflix-HBO Max could hold the largest market share at 35%, followed by Disney+ and Amazon Prime Video. This reflects the trend towards fewer dominant platforms.

Consumer Protections and One-Click Cancellation

The Subscription Flexibility Argument

When pressed on pricing concerns, Sarandos emphasized Netflix's fundamental advantage: "We are a one-click cancel." This point, often dismissed as rhetorical flourish, actually captures something important about modern subscription economics.

Unlike cable subscriptions, which traditionally required phone calls to customer service and involved cancellation fees, Netflix subscriptions can be terminated instantly through the account settings page. This creates genuine competitive discipline: if Netflix raises prices excessively or provides insufficient value, subscribers can immediately switch to alternatives without penalty. This contrasts sharply with cable, phone, or internet services, which often involve contracts, termination fees, or technical switching costs as detailed in his testimony.

For antitrust analysis, one-click cancellation matters. It suggests that even a merged Netflix with 21% market share faces competitive constraints because switching barriers are minimal. A consumer dissatisfied with Netflix post-merger pricing could switch to Disney Bundle, Paramount+, Apple TV+, or any of dozens of alternatives without losing existing content or incurring switching costs.

However, this argument has limitations. While technical switching is easy, behavioral switching isn't. Consumers often stick with existing subscriptions due to inertia, even when better alternatives exist. The question is whether Netflix's market power exceeds the threshold where behavioral inertia overwhelms competitive switching possibilities as noted by the American Economic Liberties Project.

Limitations of Consumer Protections

One-click cancellation provides some consumer protection but is incomplete. It addresses price discrimination (Netflix can't lock customers in) but doesn't address several other concerns:

Content quality concerns: If post-merger Netflix reduces HBO content investment, subscribers can't recover this loss by switching platforms, as no competitor offers HBO's catalog outside HBO Max. Content quality reductions represent value destruction that switching doesn't remedy.

Network effects: Streaming platforms benefit from network effects—they're more valuable when many people use them because social conversations center on platform-exclusive content. A subscriber might want to stay on Netflix to discuss "The Crown" or "Stranger Things" with friends, even if alternative services offer better pricing or content. These social effects reduce effective switching possibilities.

Multi-platform households: Many households subscribe to multiple services simultaneously. Netflix's one-click cancellation doesn't address whether a merged Netflix-WBD would increase incentives to bundle services at discounted rates, effectively increasing total household spending on video entertainment.

Sarandos's emphasis on one-click cancellation is valuable in antitrust analysis but shouldn't be interpreted as a complete consumer protection framework as noted by the American Economic Liberties Project.

Alternative Streaming Platforms: Evaluating Your Options Beyond Netflix

Disney Bundle and Integrated Entertainment Strategy

Disney represents Netflix's most formidable traditional competitor, though through a different strategic model. Rather than a single comprehensive streaming service, Disney offers the Disney Bundle, combining Disney+, Hulu, and ESPN+ at discounted rates (

Disney's advantage is content diversity across entertainment categories. Disney+ offers family entertainment and prestige drama (through acquisitions like 20th Century Studios), Hulu provides general entertainment and contemporary series, and ESPN+ delivers sports content. This breadth allows Disney to serve multiple household member preferences through a single bundled subscription.

Compared to Netflix, Disney's strategic position is stronger in some categories (sports, family entertainment, Marvel franchises) but weaker in others (prestige drama, international content, romance). Netflix's original drama production remains superior to Disney's output, meaning subscribers primarily wanting high-quality dramas should favor Netflix. However, households wanting content variety across entertainment categories may find Disney Bundle superior value as noted by Britannica.

Paramount+ and Traditional Media Streaming

Paramount Global (formerly Viacom CBS) operates Paramount+, which bundles Paramount film studio content, CBS television programming, MTV archives, and original series. Paramount+ pricing ranges from

Paramount+'s content strength lies in prestige drama ("Yellowstone," "Tulsa King," "Handmaid's Tale"), sports (NFL games), and family entertainment. However, compared to Netflix, Paramount+ has released fewer hit original series, suggesting lower content quality or production values on average.

Paramount's counter-bid for WBD reflects the company's belief that consolidation with WBD would significantly improve its competitive position against Netflix. Whether that bid succeeds remains unclear, but it demonstrates that Paramount sees standalone survival against Netflix as increasingly difficult without consolidation as noted by AOL Finance.

Apple TV+ and Premium Original Content

Apple TV+ represents a different strategic model: premium original content bundled as a profit center within broader Apple services ecosystem. Apple invested heavily in prestige drama and limited series, producing acclaimed shows like "Ted Lasso," "Severance," "Prehistoric Planet," and "The Morning Show" as noted by Britannica.

Apple TV+ pricing ($9.99/month or included free with Apple One subscriptions) positions it as a premium service for exclusive content rather than comprehensive entertainment. Apple's strategy isn't to offer everything but to offer exceptional originals that justify subscription as a supplement to Netflix or Disney+.

For subscribers, Apple TV+ makes sense if you specifically want Apple's acclaimed originals. However, Apple TV+'s library is much smaller than Netflix's (roughly 300-400 titles vs. Netflix's 8,500+ titles), limiting its utility as a primary entertainment service. Apple TV+ is best viewed as complementary to Netflix or Disney Bundle rather than as a replacement as noted by Britannica.

Amazon Prime Video and Bundled Services

Amazon Prime Video offers the largest streaming library by volume (though with more variable content quality) and bundles with Amazon Prime membership, which includes free shipping, Prime Day access, and music streaming. Prime Video pricing (

Prime Video's advantage is integration with broader Prime benefits and sheer content volume. Its disadvantage is content quality variability—Prime Video's algorithm-driven recommendations don't always surface the highest-quality content, requiring active navigation to find prestige originals like "The Boys," "Transparent," or "Fleabag."

For families heavily integrated into Amazon's ecosystem, Prime Video offers good value. For consumers primarily seeking high-quality, curated content experiences, Netflix remains superior as noted by Britannica.

Emerging Alternatives and Niche Services

Beyond the major platforms, increasingly sophisticated consumers are turning to niche services offering specialized content. The Criterion Collection (

These services won't replace Netflix or Disney Bundle but serve specific subscriber segments willing to pay for curation and specialization. As major platforms grow, they inevitably homogenize their recommendation algorithms and content strategies, creating opportunities for niche services that offer distinctive editorial voices.

For consumers tired of algorithmic recommendations and seeking human curation, these services represent valuable alternatives. However, they function best as supplements to one major platform rather than replacements as noted by Britannica.

Runable as a Digital Productivity Alternative

For teams evaluating how to manage content creation and digital workflows across streaming platforms, Runable offers an interesting alternative approach to content automation and productivity. While Runable doesn't directly compete with Netflix streaming, it provides AI-powered tools for automated content generation, workflow management, and document production at just $9/month. For content creators and teams working across multiple platforms, Runable's automated content workflows, AI-powered document generation, and integration capabilities could streamline how you manage and repurpose content across streaming platforms.

Further, teams building modern applications that integrate with streaming services might find value in Runable's developer-focused automation tools, which can reduce the manual effort required to build streaming platform integrations and manage content metadata workflows.

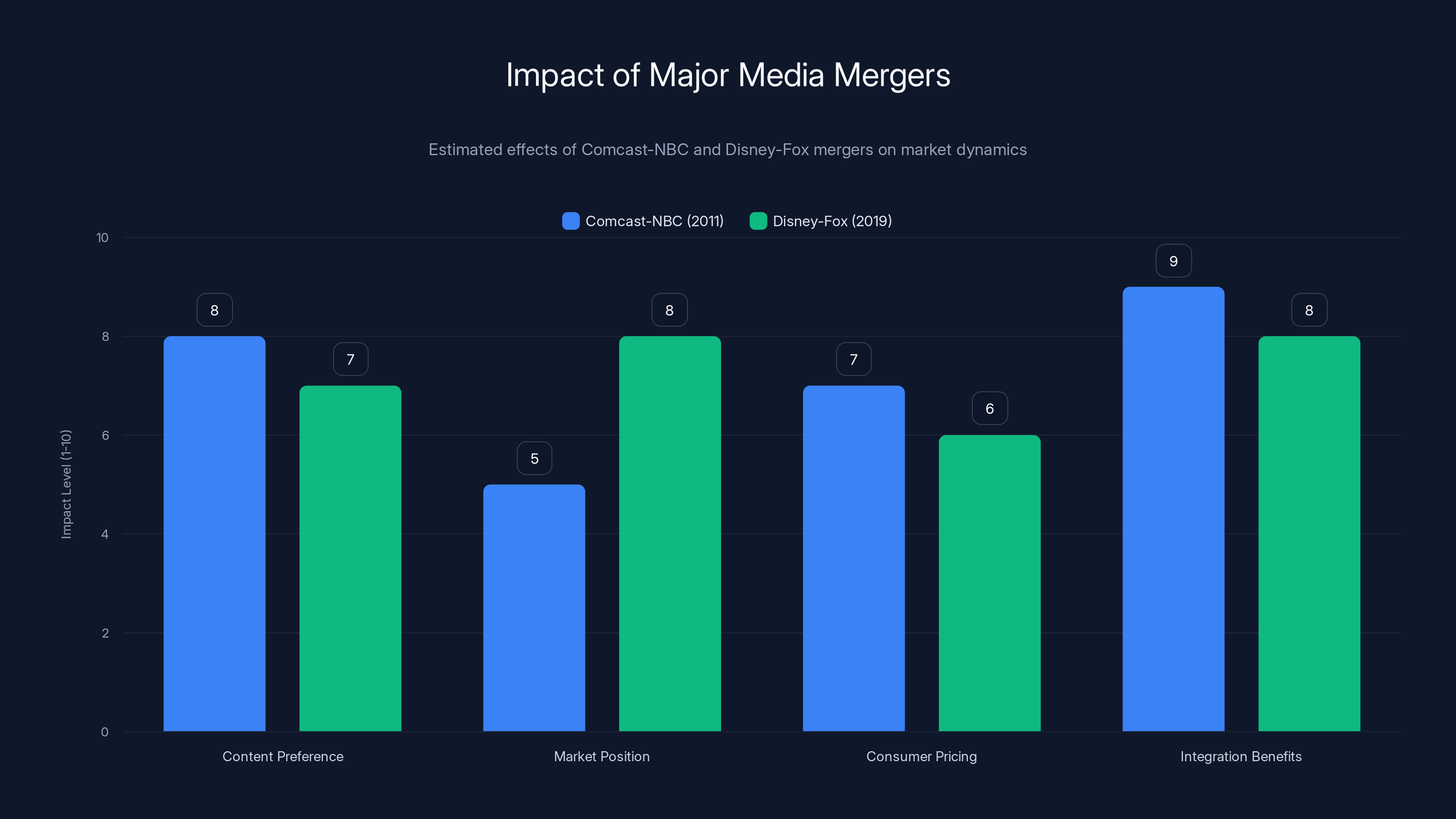

Estimated data shows that both mergers had significant impacts on content preference and integration benefits, with Comcast-NBC focusing more on integration strategies.

Market Predictions: What Merger Approval Would Mean for Streaming

Scenario Analysis: Approval vs. Rejection

The Netflix-WBD merger outcome creates two distinct scenarios with different competitive implications:

Scenario A: Merger Approved - Netflix gains HBO's content, WB's film studios, and WBD's subscriber base. The result would be a streaming leader with unmatched prestige content library and strongest profitability trajectory. Competitors would face a stronger Netflix but also incentive to seek their own consolidation (explaining Paramount's counter-bid). This scenario likely leads to continued streaming consolidation, with 3-4 major bundles (Netflix, Disney, Paramount-WBD, and possibly Amazon/Apple as independents) dominating the market by 2027.

Scenario B: Merger Rejected - Netflix remains independent, WBD remains independent (though potentially acquired by Paramount), and the industry has greater fragmentation with distinct competitive paths for each major player. This scenario maintains a more fractured marketplace where specialty and niche services can achieve scale. Consumers maintain more platform choice but likely pay more aggregate spending on multiple subscriptions as noted by AOL.

Regulatory Timeline and Uncertainty

The merger faces regulatory review from the Department of Justice, Federal Trade Commission, and potentially state attorneys general. Historical precedent suggests 12-18 months for regulatory analysis, with potential legal challenges extending the timeline further. Key regulatory decisions may not occur until late 2025 or early 2026 as noted by the Wall Street Journal.

This uncertainty itself creates effects. Netflix and WBD likely won't substantially change strategic operations pending regulatory clarity. Content production decisions, pricing changes, and strategic partnerships may be deferred until the merger outcome becomes clear. This creates a "waiting period" where strategic evolution in streaming temporarily stabilizes.

Historical Precedent: What Past Media Mergers Teach Us

Comcast-NBC Universal Merger (2011)

When Comcast acquired NBC Universal for $13.75 billion, similar antitrust concerns were raised: Would Comcast use its cable distribution power to preference NBC content? Would consumer prices increase? Would competitors face disadvantageous terms?

The actual outcome was more nuanced than either excited proponents or concerned critics predicted. Comcast did preference NBC content on its cable platforms, bundling NBC/CNBC/MSNBC prominently in cable lineups. However, NBC didn't achieve dominant market position—competitors' content remained available through cable. Pricing increased, but similarly across competitors, suggesting that broader industry forces (cost inflation, content investment) rather than Comcast-specific behavior drove increases.

The merger's most significant effect was integration of content production and cable distribution, which enabled Comcast to develop sophisticated video-on-demand and bundling strategies. This actually benefited consumers in some ways (integrated billing, unified recommendations) while disadvantaging them in others (less ability to purchase channels à la carte).

For Netflix-WBD merger analysis, the Comcast precedent suggests integration effects matter more than pure market concentration effects. The specific ways Netflix and WBD integrate their operations will determine consumer impact more than the aggregate market share number as noted by Britannica.

Disney-Fox Acquisition (2019)

When Disney acquired most of Fox's entertainment assets for $71.3 billion, antitrust concerns centered on animation, sports, and streaming. Disney would gain Fox's library ("Avatar," "X-Men," "Simpsons") and sports holdings (regional sports networks, partial stakes in sports entities).

Regulatory approval included commitments regarding sports programming—Disney had to divest some regional sports networks to address concerns about exclusive sports content control. Beyond sports, the merger was approved relatively straightforwardly, suggesting regulators were comfortable with Disney's market position.

Post-acquisition, Disney has aggressively rationalized its streaming strategy, leading to Disney+ and Hulu integration announcements. Disney also increased Disney+ pricing from

For Netflix analysis, the Disney precedent is instructive: mega-mergers in entertainment are approved when regulators believe the merged entity enhances consumer value (through content or technology) rather than simply reducing competition. Disney's merger was approved because Disney's integration created tangible consumer benefits (broader library, better technology), even though it concentrated media power.

Netflix leads the SVOD market with over 301 million subscribers, surpassing the combined total of its nearest competitors. Estimated data.

Emerging Threats: Competition from Tech Giants

YouTube's Dominance in Video Consumption

Netflix's testimony emphasized that YouTube (not a dedicated streaming service) captures more American television viewing time than Netflix itself. Nielsen data shows YouTube accounts for 12.7% of American TV viewing, compared to Netflix's 9%, suggesting that algorithm-driven video discovery is increasingly displacing traditional subscription streaming as reported by eMarketer.

This reflects a fundamental shift in video consumption. YouTube's user-generated content ecosystem, zero friction for content discovery, and seamless recommendation algorithms have created a more engaging experience for many viewers than curated streaming services. For audiences wanting entertainment discovery rather than prestige drama specifically, YouTube's experience may be superior.

As tech giants continue investing in video capabilities, traditional streaming services face structural competition. Netflix's merger with WBD doesn't directly address YouTube competition but could improve Netflix's differentiation through superior prestige content as noted by the Wall Street Journal.

Apple's Expansion in Video Services

Apple has committed to becoming a major media company, investing billions in original content and distribution. Apple TV+ is just one element of Apple's broader video strategy. Apple's integration of video into the Apple ecosystem—availability on iPhones, iPads, Macs, Apple TVs, and potentially future AR/VR devices—creates competitive advantages that traditional streaming services can't match as noted by Britannica.

Apple's strategic advantage is ecosystem lock-in. A user invested in Apple devices has natural incentive to subscribe to Apple TV+ as a complementary service. This is less about Apple TV+ content quality and more about reducing friction in the Apple ecosystem.

Google Play, Amazon, and Ecosystem Integration

Similarly, Google and Amazon have advantages through ecosystem integration. Google's YouTube, Google Play, and potential future products can drive adoption. Amazon's Prime Video bundle with free shipping creates stickiness beyond content quality.

These structural advantages—ecosystem integration, diverse revenue sources, and immense capital—represent genuine competitive challenges to Netflix, even if Netflix acquires WBD as noted by Britannica.

Consumer Strategies: Managing Subscription Costs and Maximizing Value

Rotating Subscription Strategy

As streaming fragmentation has increased, sophisticated consumers have adopted rotating subscription strategies: maintaining subscriptions to 2-3 services simultaneously while rotating which services they maintain, based on current content rotation. This strategy minimizes total monthly spending while maximizing access to diverse content.

Example rotation: Subscribe to Netflix and Disney Bundle for 3 months, then switch to Netflix and Paramount+ for next 3 months, then rotate to Netflix, Apple TV+, and Amazon Prime Video. This approach provides continuous access to most high-quality content while keeping monthly spending around

The strategy depends on substantial library rotation rather than rapid original releases, but for most content types (except prestige weekly releases), waiting 3-6 months for content to appear on your current subscriptions is feasible.

Bundling and Family Sharing

Netflix, Disney+, and other platforms allow family sharing (with limitations on simultaneous streams). Sharing a family subscription across households can reduce per-person costs to $3-5 monthly if split among 3-4 people. While some platforms are reducing sharing capabilities, strategic family grouping remains an effective cost-management tool as noted by Britannica.

Evaluating Genuine Use Cases

The most economically rational subscription strategy is to subscribe only to services you genuinely use. Surveys suggest the average subscriber underutilizes their subscriptions—maintaining services out of habit rather than active engagement. Auditing your actual usage and trimming unused services is the simplest cost-management strategy as noted by Britannica.

Future Outlook: Streaming Industry Evolution Through 2027

Predicted Consolidation Path

Regardless of whether Netflix-WBD merger succeeds, consolidation pressures will drive toward 3-4 dominant platforms by 2027. Current market forces suggest:

- Disney Bundle consolidates Disney+, Hulu, ESPN+ with potential expansion

- Netflix either independently or with WBD/other assets becomes the prestige drama and international content leader

- Paramount Global leverages Viacom CBS assets with potential WBD combination

- Amazon/Apple operate as supplementary services within tech ecosystems rather than standalone platforms

This structure would resemble cable TV's fragmentation (where 3-4 networks dominated despite hundreds of channels) rather than true competition as noted by Britannica.

Technology Evolution: AI, Personalization, and Search

Beyond consolidation, technological evolution will increasingly differentiate platforms. AI-powered recommendation systems, natural language search, and personalized interface design will become more important than raw content library size. Netflix's technology infrastructure advantages will persist regardless of merger outcome, suggesting technology-driven differentiation (rather than content-driven differentiation) will intensify as noted by Britannica.

Global Expansion and Regulatory Variation

Regulatory outcomes vary dramatically across geographies. European Union competition authorities are traditionally more aggressive than US regulators regarding media consolidation. Chinese and Indian regulators have different frameworks. As streaming globalizes, regulatory arbitrage becomes important: a merger might be approved in the US but rejected in Europe, creating operational complexity as noted by Britannica.

Critical Analysis: Separating Rhetoric from Reality

Netflix's Genuine Advantages

Netflix's case for the merger isn't entirely self-serving rhetoric. Genuine benefits likely would accrue:

- Content integration: HBO's library combined with Netflix's technology would create superior user experience

- Efficiency gains: Eliminating duplicate overhead (two separate licensing teams, two platform infrastructures, etc.) would genuinely reduce costs

- Competitive positioning: Against Apple, Google, and Amazon, a more consolidated Netflix would compete more effectively as noted by Britannica

Netflix's Selective Framing

However, Netflix is also engaging in selective framing on several dimensions:

- The "tech giants are the real threat" argument is true but also deflects from horizontal competition concerns. Yes, Google and Apple are large, but that doesn't eliminate concerns about Netflix's power in the SVOD market specifically.

- The cost-per-hour efficiency metric is real but misleading. Comparing Netflix's 0.90 per hour conflates subscriber size with content quality. Netflix's efficiency reflects its larger user base, not necessarily superior content value.

- The "one-click cancel" argument understates behavioral inertia and network effects that reduce practical switching possibilities as noted by Britannica.

Genuine Antitrust Concerns

Beyond Netflix's framing, legitimate antitrust concerns exist:

- Market concentration: 21% SVOD market share exceeds typical regulatory thresholds and warrants scrutiny

- Foreclosure risks: A merged Netflix could preference HBO content and WB theatrical output, disadvantaging competitors

- Price discrimination: Merger-enabled price increases might occur even with commitments otherwise

- Content diversity: Consolidation reduces distinct editorial voices and potentially homogenizes content offerings as noted by the American Economic Liberties Project

These aren't certain to occur, but they represent plausible harms that justify regulatory examination.

Conclusion: Navigating Streaming's Consolidation Era

The Netflix-HBO Max merger represents a pivotal moment for the streaming industry. While Netflix's strategic arguments have merit—consolidation could improve efficiency, enhance content quality, and strengthen competition against tech giants—the merger also raises legitimate concerns about market concentration, pricing power, and content diversity.

For consumers, the key insight is that streaming consolidation is inevitable, regardless of this specific merger's outcome. Whether driven by Netflix acquiring WBD or Paramount acquiring WBD or some other combination, the industry is consolidating toward 3-4 dominant platforms. This consolidation will create both benefits (integrated experiences, more efficient operations) and harms (reduced choice, potential price increases, fewer distinct editorial voices).

Your strategic response should balance these realities. First, understand that subscription spending will likely increase modestly (5-15% over 2-3 years) as consolidated platforms optimize pricing. Second, adopt rational subscription management strategies—maintain only actively used subscriptions, rotate services to manage costs, and leverage family sharing where possible. Third, remain alert to pricing and content quality changes; if any service significantly increases prices without proportional value increases, switching to alternatives remains simple.

The "golden age" of cheap, abundant streaming may be ending. The era of consolidated, premium streaming platforms is beginning. This shift reflects fundamental economics—content production costs are unsustainable at $5-10 monthly subscription prices, and consolidation enables platforms to achieve profitability at higher price points while maintaining subscriber satisfaction through content depth and quality.

Netflix's claim that consumers can always "one-click cancel" if prices increase too dramatically is economically sound but incomplete as a consumer protection. While switching barriers are low, behavioral inertia is high, and the quality of alternatives matters. In the consolidated streaming world of 2027, your best protection is maintaining awareness of your actual content consumption and willingness to switch platforms when alternatives offer better value.

The merger may be approved or rejected by regulators, but the consolidation trend that prompted it will continue. Understanding this dynamic is essential for making rational subscription and entertainment consumption decisions in the years ahead. For teams working in content creation or digital workflows, emerging platforms like Runable offer cost-effective alternatives to traditional enterprise content management tools, potentially reducing total costs as subscription streaming becomes increasingly expensive.

The streaming wars of 2025 will determine industry structure for the next decade. Stay informed about consolidation trends, understand your actual content preferences, and adapt your subscription strategies accordingly. The future of streaming will be less about abundance and more about quality, efficiency, and strategic choice among limited but powerful platforms.

FAQ

What is the Netflix-Warner Bros. Discovery merger?

The proposed merger involves Netflix attempting to acquire Warner Bros. Discovery's streaming services (HBO Max and Discovery+) and film studio assets. Netflix has offered approximately

How would the Netflix-WBD merger affect subscriber pricing?

Pricing effects are uncertain but would likely follow patterns from past media mergers: modest increases (5-15% over 2-3 years) rather than dramatic jumps. Cost structure improvements from consolidation might enable more aggressive pricing optimization, but committed regulatory guardrails could constrain increases. Current Netflix subscribers might see higher prices, while current HBO Max subscribers could potentially consolidate into a single Netflix subscription at lower aggregate cost if HBO Max pricing is eliminated as noted by Britannica.

What are the antitrust concerns with this merger?

Key concerns include market concentration (merged entity would control approximately 21% of SVOD market), potential content foreclosure (preferential treatment of HBO/WB content over competitors), and reduced editorial diversity. Regulators worry that consolidation reduces subscriber choice and could enable monopolistic pricing, though Netflix argues that tech giants like Apple, Google, and Amazon represent the real competitive threats. The balance between these concerns and merger benefits will determine regulatory approval likelihood as noted by the American Economic Liberties Project.

What percentage of HBO Max subscribers already use Netflix?

According to Netflix's Senate testimony, approximately 80% of HBO Max subscribers also maintain Netflix subscriptions. This high overlap suggests significant subscriber consolidation potential post-merger, since many current HBO Max users would already have Netflix access. However, the remaining 20% of HBO Max-exclusive subscribers would face reduced choice if forced to choose between Netflix or losing access to HBO content as detailed in his testimony.

What are the main alternatives to Netflix if you want streaming content?

Major alternatives include Disney Bundle (

Would the merger reduce competition in streaming?

Yes, in the narrow SVOD market specifically, the merger would reduce competition by consolidating content from two major platforms into one. However, Netflix's argument that broader video competition (from YouTube, cable, Apple, Google, Amazon) remains intense has validity. Whether "reducing SVOD competition" while "maintaining broader video competition" constitutes net harm depends on how regulators define the relevant market and what competitive thresholds they apply. Traditional antitrust analysis suggests 21% market share warrants scrutiny, but modern tech-era analysis often prioritizes barriers to entry and competitor viability more than market share percentages as noted by the American Economic Liberties Project.

What is the current timeline for merger approval or rejection?

The merger faces review by the Department of Justice and potentially state attorneys general. Based on historical precedent for media mergers, regulatory analysis typically requires 12-18 months, with potential legal challenges extending timelines further. Initial regulatory decisions may not occur until late 2025 or early 2026. Both Netflix and WBD have likely deferred major strategic changes pending regulatory clarity, creating a "waiting period" where strategic evolution in streaming temporarily stabilizes as noted by the Wall Street Journal.

How does Netflix justify the merger against antitrust concerns?

Netflix argues that streaming is competitively dynamic, with tech giants (Google, Apple, Amazon) representing greater threats than traditional media competitors. The company emphasizes YouTube's 12.7% TV viewing share (exceeding Netflix's 9%), Apple TV+'s ecosystem advantages, and Amazon Prime Video's bundled benefits. Netflix also highlights subscriber switching costs (one-click cancellation), cost efficiency gains (

What would a merged Netflix-WBD mean for content creators and production companies?

Creators would face a single dominant buyer for prestige drama and HBO-brand content, reducing negotiating leverage. However, consolidation might also increase overall content investment if Netflix and WBD's combined platform achieves greater profitability. Production companies would compete for fewer streaming homes but potentially larger per-project budgets. Feature film producers might face compressed theatrical windows (45-60 days vs. traditional 90+ days), potentially reducing theatrical revenue but accelerating streaming availability. Overall, consolidation would likely favor large, established production companies while disadvantaging independent producers as noted by the American Economic Liberties Project.

How can consumers protect themselves from high streaming prices post-merger?

Key strategies include: (1) maintaining only actively used subscriptions rather than passive memberships; (2) rotating subscriptions monthly or quarterly to manage costs; (3) leveraging family sharing where available to split costs across households; (4) monitoring pricing and switching services when competitors offer better value; (5) considering bundles (Disney Bundle, Amazon Prime) rather than standalone services; and (6) being willing to use one-click cancellation if value propositions deteriorate. Consumer power remains meaningful in streaming because switching barriers are low, even if behavioral inertia is high as noted by Britannica.

Key Takeaways

- Netflix's proposed $82.7B acquisition of Warner Bros. Discovery would consolidate two major streaming services into single platform with 21% SVOD market share

- Merger promises consumer benefits through cost efficiency (0.90), content breadth, and faster theatrical film releases, but raises legitimate antitrust concerns about pricing power and content diversity

- 80% of HBO Max subscribers already maintain Netflix subscriptions, suggesting significant consolidation potential but also reduced choice for remaining 20% of HBO Max-exclusive viewers

- Regulatory approval timeline likely extends 12-18 months, with potential legal challenges further delaying outcomes; strategic uncertainty will constrain industry innovation during waiting period

- Streaming consolidation is inevitable regardless of this specific merger's outcome; consumers should adopt rational subscription management strategies (rotating services, leveraging bundling, maintaining switching readiness) to manage rising costs

- Alternative platforms (Disney Bundle, Paramount+, Apple TV+, Amazon Prime Video) each offer distinct strengths in family content, pricing, prestige originals, and ecosystem integration respectively

- Historical media mergers (Comcast-NBC, Disney-Fox) show consolidation typically enables modest price increases (5-15% over 2-3 years) and content optimization rather than dramatic consumer harm, though editorial diversity often decreases

- Tech giants (YouTube with 12.7% TV viewing share, Apple's ecosystem integration, Amazon Prime bundling) represent increasing competitive pressure beyond traditional streaming platforms, shifting dynamics from SVOD competition to broader video entertainment competition

Related Articles

- Spotify's 2026 Price Hike: What You Need to Know About Streaming Costs [2025]

- Best 4K Streaming Boxes With Free Channels: Freely, TiVo & More [2025]

- BBC's YouTube Strategy and the TV Licence Crisis [2025]

- YouTube TV Custom Multiview and Channel Packages: Everything You Need to Know [2025]

- Texans vs Patriots 2026 Divisional Round: Free Streams & TV Channels

- Netflix's $82B Warner Bros Deal: What It Means for Movie Theaters [2025]