![SEC Closes Fisker Investigation: What It Means for EV Startups [2025]](https://tryrunable.com/blog/sec-closes-fisker-investigation-what-it-means-for-ev-startup/image-1-1771006107106.jpg)

Introduction: The Quiet End of a Regulatory Spotlight

In September 2025, something happened that would have seemed unthinkable just two years earlier. The SEC quietly closed its investigation into Fisker, the bankrupt electric vehicle startup that had once promised to revolutionize the automotive industry with radical new technologies. The public didn't find out until January 2026, when TechCrunch filed a Freedom of Information Act request and discovered the probe had already wrapped up.

This isn't just a footnote in the collapse of another EV startup. It's a window into a much larger story about regulatory priorities, the fate of the electric vehicle industry, and what happens when government enforcement suddenly shifts direction.

For years, the SEC had been investigating high-profile EV startups with aggressive scrutiny. The agency pursued fraud cases against Nikola, Lordstown Motors, Canoo, and Hyzon Motors. It settled charges, extracted penalties, and sent a clear message: if you make claims you can't back up, we're coming for you. But something changed in 2025. Enforcement actions plummeted by 27%. Monetary settlements fell 45%. And one by one, investigations into EV startups started closing without resolution.

Fisker's investigation closure is the clearest example of this reversal. But the real question is why. What drove this dramatic shift in the regulatory environment? Who benefits from these decisions? And what does it mean for investors, consumers, and the future of electric vehicles?

This article digs into the facts, traces the timeline, and explains the implications of the SEC's changing approach to startup enforcement.

TL; DR

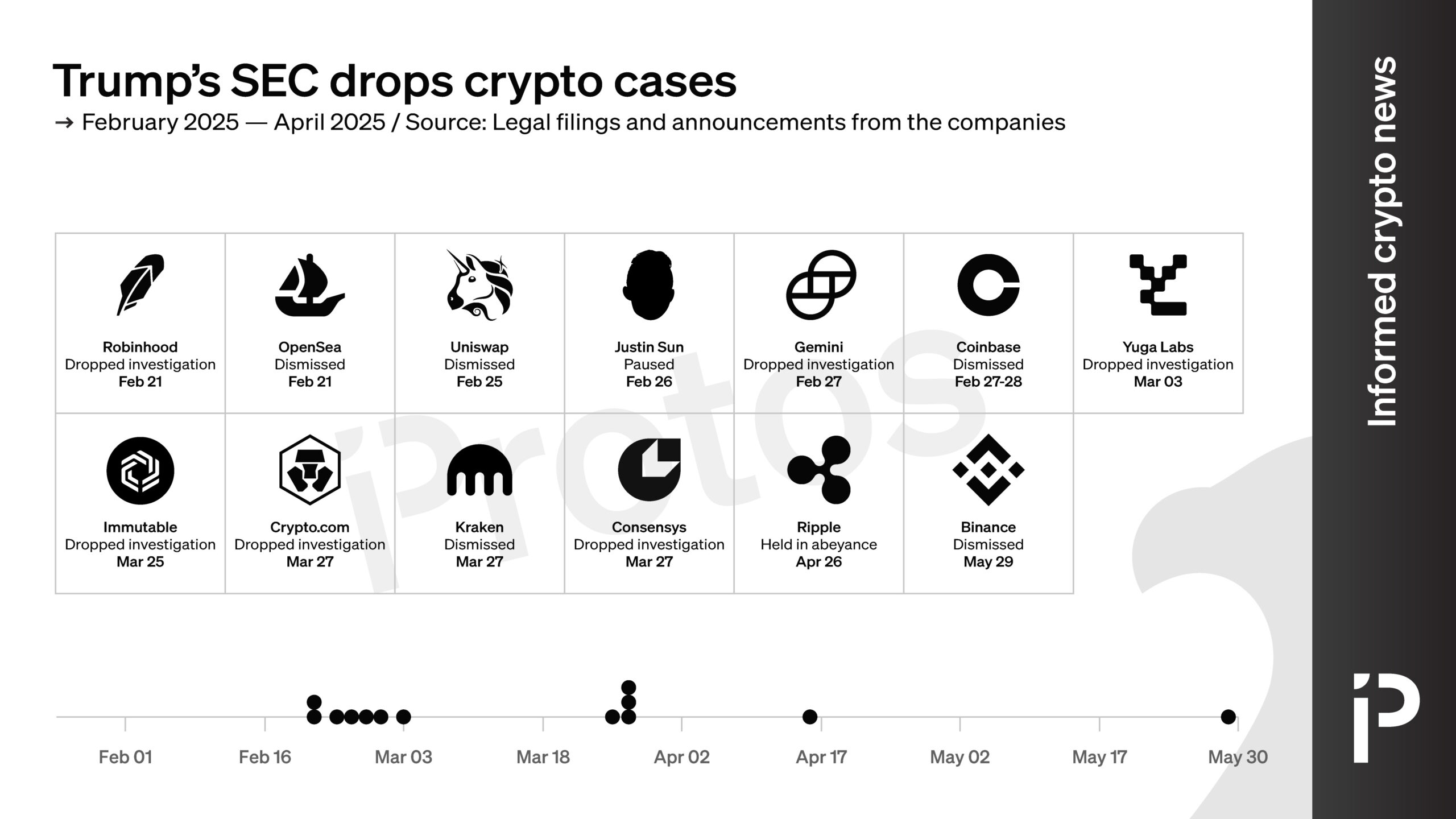

- SEC Closed Fisker Probe: The investigation that began in October 2024 wrapped up silently in September 2025 without any enforcement action or public announcement.

- Dramatic Enforcement Decline: The SEC initiated 313 enforcement actions in 2025, down 27% from 2024 and the lowest number in a decade, with monetary settlements falling 45%.

- EV Startup Pattern: Multiple electric vehicle startups that faced SEC investigations (Nikola, Lordstown, Canoo, Hyzon) settled charges, but Fisker avoided formal action entirely.

- Political Context: The shift coincides with President Trump's second term and a reported policy focus on reducing regulatory burdens on business.

- Active Investigation Remains: Only Faraday Future still faces an active SEC investigation, receiving Wells notices in July 2025 but no subsequent enforcement action.

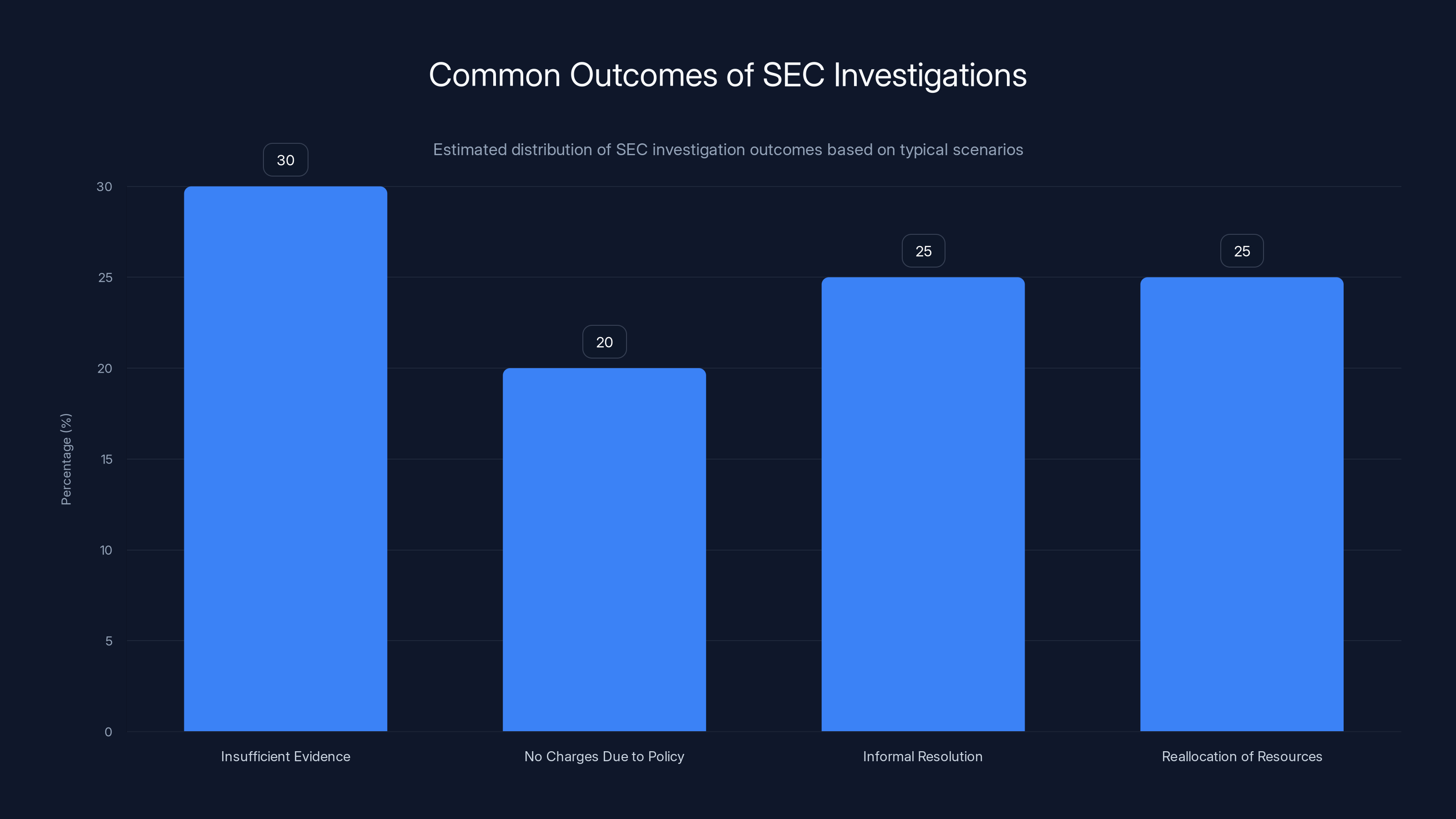

Estimated data suggests that SEC investigations often close without charges due to various reasons, with insufficient evidence being a common outcome.

What Happened to Fisker: Timeline of a Startup's Collapse

Fisker's story reads like a cautionary tale written in real time. The company didn't fail overnight. It collapsed under the weight of mounting problems, broken promises, and financial mismanagement that accumulated over years.

Henrik Fisker founded the company in 2016 with a bold vision. He wasn't a newcomer to the space—he'd previously designed cars at Tesla and Aston Martin. He had credentials. He had credibility. And he had plans to upend the industry with technologies that sounded revolutionary when announced but proved unrealistic or unnecessary when scrutinized.

The company spent years pivoting from one technological focus to another. It promised solid-state batteries. Then it shifted strategy. It promised ultra-fast charging. Then that changed too. Each pivot felt like a reset button on the company's previous commitments. Investors watched these shifts with growing concern. Media outlets started asking harder questions. And eventually, the SEC took notice.

By 2024, the problems had become impossible to ignore. Production issues plagued the Ocean SUV, Fisker's first vehicle. Quality control failed repeatedly. Consumers reported serious defects. Sales projections missed targets by massive margins. The company burned through cash at an unsustainable rate. Cash burn, when it accelerates beyond revenue generation, becomes the death knell of any startup. For Fisker, it became terminal.

In June 2024, Fisker filed for Chapter 11 bankruptcy. This isn't a gentle reorganization. It's a legal declaration that the company cannot pay its debts. The bankruptcy filing included an SEC investigation that had been quietly underway since at least October 2024. According to court documents, the SEC had sent subpoenas to Fisker and indicated it might request additional documents "relating to its ongoing investigation."

But no enforcement action came. The investigation closed in September 2025, roughly one year after it began. No lawsuits. No settlements. No penalties. No public explanation.

The October 2024 Disclosure

The SEC's investigation became public knowledge through a filing in Fisker's bankruptcy case. This is important because it shows the agency was concerned enough to formally document its work, but not concerned enough to pursue charges. The disclosure mentioned subpoenas had been issued and that the agency might request more documents, suggesting an active investigation with momentum.

Yet in the space of eleven months, that investigation went from active to closed.

The September 2025 Closure

When the SEC responded to TechCrunch's FOIA request in January 2026, it revealed the investigation had been closed in September 2025. The agency identified "approximately 21.7 gigabytes of electronically maintained records" related to the probe, suggesting the investigation had accumulated significant documentation.

But the SEC provided no statement about why it closed the case. No press release. No explanation. The agency's spokesperson declined to comment when asked directly about the decision.

Henrik Fisker, the company's founder and former CEO, also did not respond to requests for comment. This silence is telling. If he'd been cleared of wrongdoing, he might celebrate the news publicly. If he'd reached some kind of agreement with regulators, that might be disclosed. But nothing. Just quiet closure.

The Broader Pattern: Enforcement Actions Crater Under Trump Administration

The Fisker investigation closure didn't happen in a vacuum. It's part of a massive, documented shift in SEC enforcement priorities that began in early 2025.

The numbers tell the story clearly. The SEC initiated just 313 enforcement actions in 2025. That's the lowest number in a decade. It's also 27% lower than 2024, when the agency initiated 429 enforcement actions. Put another way, the SEC brought fewer cases in 2025 than in any other year in recent memory.

But enforcement actions are just part of the picture. Total monetary settlements fell even more dramatically, declining 45% year-over-year. In 2024, the SEC extracted substantial penalties from companies and executives. In 2025, it pulled back significantly. This isn't a matter of the same number of cases settling for smaller amounts—it's fewer cases settling for lower total penalties.

What makes this shift particularly striking is the focus area. Out of 313 enforcement actions in 2025, only four targeted public companies. Four. That means 309 actions targeted private companies, individuals, and other entities. The SEC had effectively stepped back from policing publicly traded firms.

According to analysis by the law firm Morgan Lewis, this decline is deliberate policy, not an accident of caseload. The Trump administration signaled from day one that it intended to reduce regulatory burden on business. The SEC, as a government agency under executive branch influence, appears to have taken that signal seriously.

Historical Context: What Normal Looks Like

To understand how dramatic this shift is, you need context. During the final year of President Biden's administration in 2024, the SEC was more active than it had been in years. The agency was pursuing cases aggressively, settling for substantial amounts, and making public examples of companies that violated securities laws.

The philosophy was straightforward: enforcement deters fraud and misconduct. If the SEC brings enough cases and extracts meaningful penalties, companies will think twice before misleading investors or breaking rules.

The 2025 approach is different. It suggests a belief that enforcement creates burden without corresponding benefit. If you reduce enforcement, companies spend less on compliance, legal fees, and settlements. They can allocate those resources to growth and hiring instead.

Whether that theory is correct remains an open question. History suggests that reduced enforcement does lead to increased misconduct, but that effect takes time to manifest.

SEC enforcement actions dropped by 27% from 2024 to 2025, with monetary settlements declining by 45%, reflecting a significant policy shift under the Trump administration. Estimated data for monetary settlements.

Electric Vehicle Startups Under Siege: A History of SEC Enforcement

Fisker wasn't the first EV startup to face SEC scrutiny. In fact, the agency had been investigating the sector for years, and it had developed a track record of bringing cases and winning settlements.

Nikola: The High-Profile Fraud Case

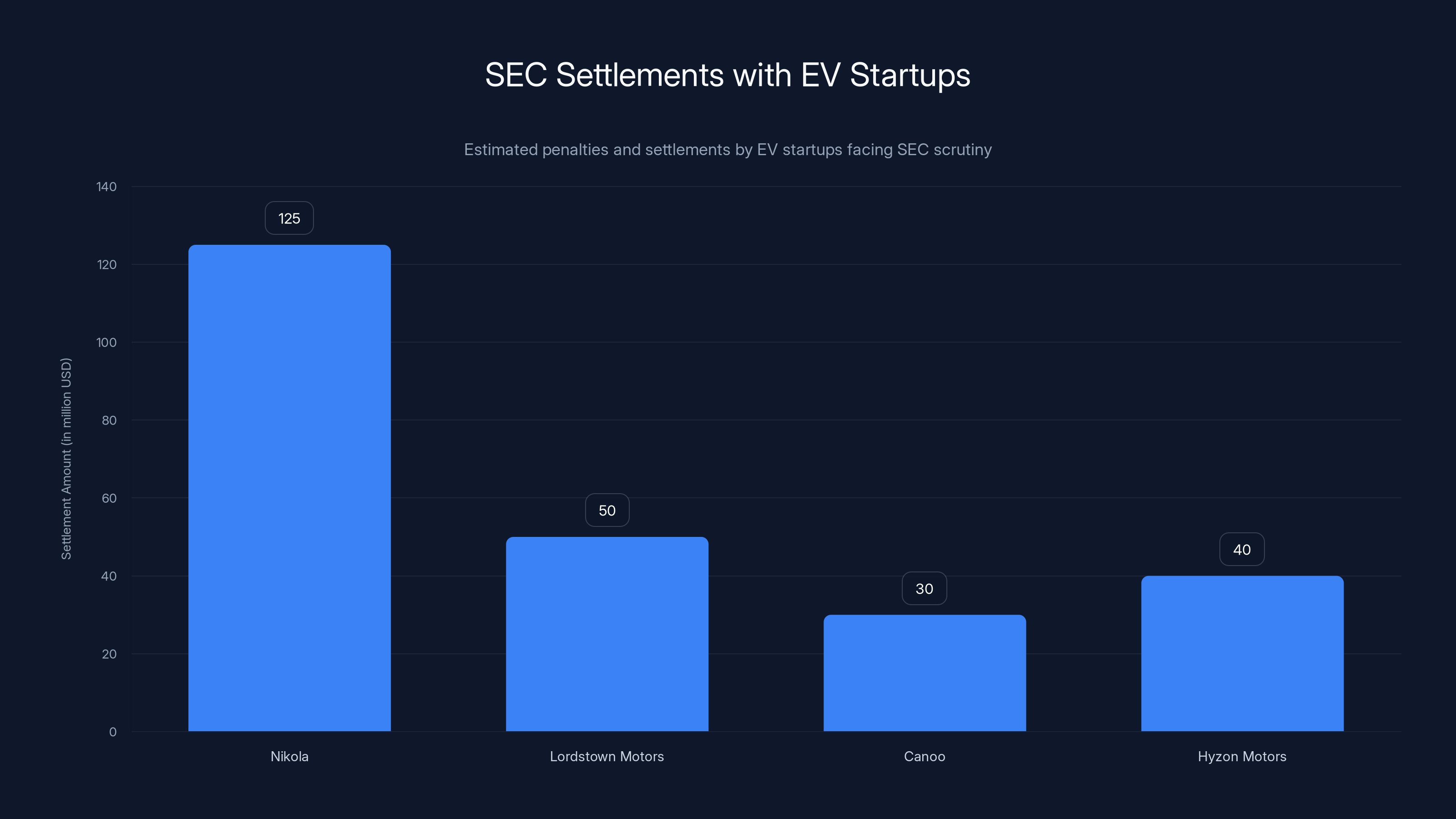

Nikola Motor Company faced perhaps the most serious allegations of any EV startup. The company's founder and executive chairman, Trevor Milton, made claims about Nikola's hydrogen truck technology that the SEC alleged were false and misleading. In 2022, the company settled fraud charges, paying a $125 million penalty. Milton himself faced criminal charges and was convicted in 2024 of wire fraud and securities fraud.

The Nikola case sent a shockwave through the EV industry. It demonstrated that the SEC was willing to pursue high-profile founder-led companies, extract substantial penalties, and coordinate with criminal prosecutors. For a time, it seemed like the agency had become a serious deterrent to startup misconduct.

Lordstown Motors: Another Settlement

Lordstown Motors, which had promised an all-electric pickup truck for commercial customers, also settled with the SEC. The company's founder, Steve Burns, settled charges of making false statements about the company's production timeline and vehicle demand. The settlement included cooperation with ongoing investigations.

These cases followed a pattern. Company makes aggressive claims. Investors pump money in based on those claims. Claims turn out to be false. SEC investigates. Company settles. Founder pays penalties. Case closed.

Canoo: The Quiet Settlement

Canoo, which designed electric vehicles for commercial fleets, reached an undisclosed settlement with the SEC. The case received less media attention than Nikola or Lordstown, but it fit the same pattern.

Hyzon Motors: Commercial Vehicle Focus

Hyzon Motors, focused on hydrogen fuel cell vehicles, also settled SEC charges related to misleading statements about its business partnerships and technology development.

Lucid Motors: The Investigation That Closed

Lucid Motors faced an SEC investigation that closed in 2023 without any enforcement action. This is interesting because it shows that not every investigation results in charges. But Lucid's investigation closure happened during the Biden administration, when enforcement activity was still relatively high. The closure suggested investigators found insufficient evidence, not that the agency had lost interest in the sector.

Why Did the Fisker Investigation Close?

This is the central mystery. The SEC spent roughly a year investigating Fisker. The agency issued subpoenas. It gathered 21.7 gigabytes of records. It had every indication of an active, ongoing investigation. Then, suddenly, it closed without explanation or enforcement action.

Several possible explanations exist, though the SEC's silence makes confirmation impossible.

Theory One: Insufficient Evidence

The most straightforward explanation is that investigators simply didn't find evidence of securities fraud or other violations that the agency could prove in court. This happens regularly. Investigations that start with strong suspicions sometimes peter out when the actual evidence doesn't support the allegations.

Fisker certainly made bold claims about its technology and capabilities. But did anyone at the company knowingly make false statements? Or did they simply overestimate their own abilities, as founders often do? Proving the mental state—that executives knowingly made false statements—is far more difficult than proving the statements themselves were false.

If investigators concluded that Fisker's failures were born of incompetence and bad judgment rather than fraud, they might close the investigation without pursuing charges. Civil fraud liability requires proof of intent to deceive. Criminal fraud requires even higher standards of proof.

Theory Two: Priorities and Bandwidth

The SEC has limited resources. With enforcement actions declining by 27%, the agency might have been actively deprioritizing certain cases. An investigation into a startup that was already bankrupt and liquidating its assets might have seemed less urgent than other matters demanding attention.

Why pursue a case against a company that's already destroyed shareholder value and shut down operations? The company can't pay penalties. The founder might lack assets to seize. The practical benefit of enforcement might be minimal.

Yet this logic seems weak. The SEC pursued cases against Nikola, Lordstown, and others partly to deter future misconduct. Enforcement has deterrent value beyond just extracting money from the particular violators.

Theory Three: Political Priorities and Regulatory Philosophy

The timing is suspicious. The investigation closed in September 2025, during the Trump administration's first year back in power. The SEC had signaled it was reducing enforcement activity across the board. It's reasonable to wonder whether leadership simply decided that pursuing Fisker wasn't worth the effort.

This wouldn't require direct orders or explicit mandates. It could work through more subtle channels. Leaders set tone. Tone affects priorities. Priorities shape which cases get pursued and which get closed.

If the SEC's leadership decided the agency should focus enforcement on clear, provable cases that affect large numbers of investors, an investigation into a bankrupt startup might not meet that bar. Fisker shareholders are already decimated. Employees are already out of work. New investors are already protected by the company's bankruptcy status.

The question becomes whether that reasoning is sound or merely rationalization for reduced enforcement.

Faraday Future: The Last EV Startup Under Investigation

Faraday Future remains under SEC investigation, making it the last major electric vehicle startup still under formal federal scrutiny. The company's situation is instructive because it shows what active enforcement still looks like, even in the reduced environment of 2025.

In July 2025, the SEC sent Faraday Future and multiple of its executives "Wells notices." These letters inform recipients that SEC staff has recommended enforcement action. They represent a formal step in the enforcement process, essentially saying: "We believe you violated securities laws, and we're recommending charges."

Recipients of Wells notices typically have the opportunity to respond, presenting arguments for why enforcement shouldn't proceed. This back-and-forth can take months or years. It's also a chance for settlement negotiations, where companies can agree to penalties without admitting wrongdoing.

But as of early 2026, no enforcement action had followed the July 2025 Wells notices. Six months had passed. Nothing. Faraday's regulatory filings indicate the company has not yet formally responded to the notices.

This is significant for several reasons. First, it shows the SEC's enforcement process grinding in slow motion. Wells notices don't guarantee enforcement—they signal intention, but outcomes remain uncertain. Second, it demonstrates that the reduced enforcement environment hasn't completely halted the SEC's ability to take action. The agency is still willing to signal recommendations for enforcement when it deems appropriate.

But the timing is telling. Wells notices sent in July 2025, with no follow-up by January 2026, suggests the investigation isn't moving with urgency. Under previous administrations, enforcement cases progressed more quickly once Wells notices were issued.

Fisker's journey from its founding in 2016 to its bankruptcy in 2024 and the closure of the SEC investigation in 2025 highlights a series of strategic pivots and financial struggles. (Estimated data)

The EV Startup Reckoning: Success, Failure, and Regulatory Impact

The electric vehicle startup ecosystem has experienced dramatic consolidation since 2024. The wave of optimism that characterized 2021 and 2022, when dozens of new EV startups filed for IPOs and raised billions in venture funding, has given way to harsh reality.

Many of these companies promised production timelines they couldn't meet. They promised technologies that turned out to be either impossible or unnecessary. They promised profitability that never materialized. The market corrected these overstatements harshly.

Fisker is just one prominent example, but the pattern extends across the entire sector. Companies that raised $1 billion or more have filed for bankruptcy. Former CEOs have faced legal consequences. And the investment community has become much more skeptical of EV startup claims.

But here's what's interesting from a regulatory perspective: The SEC's reduced enforcement activity coincides with this consolidation. Just as the market was punishing over-optimistic startups through bankruptcy and stock price collapse, the regulatory environment became more lenient.

It's worth asking whether the SEC's enforcement activity in 2023 and 2024 actually had a positive effect. Did the Nikola case deter other founders from making false claims? Did the Lordstown settlement make other startups more careful about their public statements? Or did the market's own dynamics teach that lesson more effectively?

Securities Laws and What Constitutes Fraud

Understanding why the SEC might have closed the Fisker investigation without charges requires understanding what the agency must actually prove to bring an enforcement action.

Securities fraud under Section 10(b) of the Securities Exchange Act requires proof of several elements. First, the defendant made a misstatement or omission. Second, the misstatement was material, meaning it would matter to a reasonable investor's decision. Third, the defendant acted with scienter—that's legal terminology for intent to deceive, manipulate, or defraud.

That last element is crucial. It's not enough that a company made false statements. The SEC must prove that whoever made those statements knew they were false or was reckless about whether they were true.

This standard creates a gap between failed promises and provable fraud. A startup that optimistically projects future technology capabilities, then fails to deliver, might have made false statements. But if the company genuinely believed those capabilities were achievable, proving intent to defraud becomes extremely difficult.

For a company like Fisker, which consistently pivoted its strategy and revised its plans, investigators might have concluded that the executives were incompetent optimists rather than deliberate fraudsters. The company burned through billions trying to achieve its goals, not sitting on the sidelines laughing at defrauded investors.

That doesn't mean Fisker's conduct was ethical or that it didn't harm investors. It means the SEC's standard for enforcement, which requires proof of intentional deception, might not have been met.

Scienter: The Missing Link

Legal scholars and enforcement professionals often note that scienter is the hardest element to prove in securities fraud cases. It requires showing what someone believed or knew at a particular moment in time. That's inherently difficult. People rarely admit to intentional fraud. And circumstantial evidence can support multiple interpretations.

Did Henrik Fisker knowingly make false claims about his company's prospects? Or was he a visionary founder whose ambitions exceeded his execution? The difference between those two descriptions determines whether the SEC has a viable case.

With Fisker already bankrupt and the company's failures already public, the SEC might have concluded that prosecuting the case didn't meet its threshold for resource allocation. The company's story already serves as a cautionary tale. Investors already learned the lesson. What additional value would enforcement provide?

The Political Economy of Regulatory Enforcement

The SEC's dramatic shift in enforcement activity reflects broader political choices about the role of regulation in market economies. These aren't technical decisions about law interpretation. They're policy choices about whether enforcement deters fraud or merely burdens business.

During the Trump administration, the prevailing philosophy is that reducing regulation removes barriers to business growth. Less compliance burden means more resources available for hiring, investment, and innovation. From this perspective, aggressive enforcement by the SEC makes companies more cautious, and caution slows progress.

The alternative view, prominent during the Biden administration, is that enforcement is necessary to maintain investor confidence and market integrity. Without enforcement, companies feel free to mislead investors. That leads to fraud, bubbles, and market crashes. From this perspective, reduced enforcement enables bad actors and harms the broader economy.

These aren't questions that data can definitively answer. Both positions have reasonable arguments. But the SEC's behavior clearly reflects the prevailing political philosophy of the administration in power.

Enforcement as Signaling

One often-underappreciated aspect of enforcement is its signaling function. When the SEC pursues high-profile cases, it sends a message to the broader market: "This is what happens when you mislead investors." That message has deterrent value beyond the specific case.

When the SEC stops pursuing cases, it sends a different message: "Misleading investors is not a priority for us right now." That message might encourage more aggressive marketing by startups, more optimistic projections, and more aggressive investor claims. It's not that entrepreneurs suddenly decide to commit fraud. It's that the cost-benefit calculation shifts. When enforcement is active, the cost of being caught is high. When enforcement is quiet, the cost diminishes.

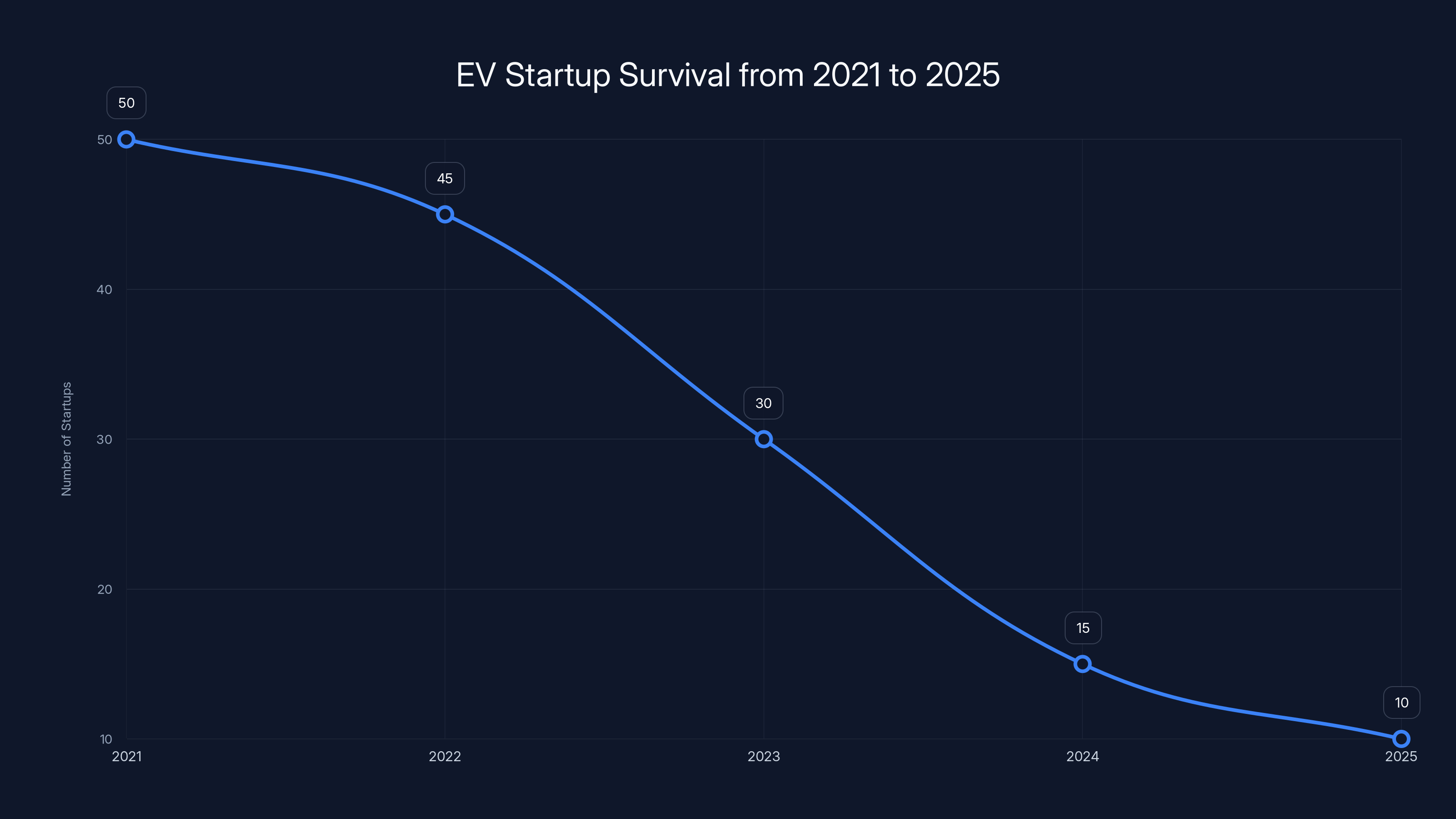

The number of operational EV startups dramatically decreased from over 50 in 2021 to fewer than 10 by 2025, primarily due to market forces rather than regulatory actions. (Estimated data)

What Happens to Investors and Creditors During EV Startup Bankruptcies?

Fisker's bankruptcy process shows what happens when an EV startup runs out of money and runs to bankruptcy court. The outcome isn't pretty for anyone except, potentially, secured creditors.

Fisker shareholders lost virtually everything. Early investors who bought stock at the IPO saw their investment become worthless. Later investors who bought on the down slopes of the stock price lost money faster. That's how the market works—equities are risky. But investors who were misled about the company's prospects have legitimate grievance claims.

Employees also suffered. Thousands of workers at Fisker lost their jobs when the company shut down. They had placed their careers on the company's promise of delivering profitable electric vehicles. That didn't happen.

In bankruptcy, Fisker's remaining assets were liquidated. The company sold its inventory of Ocean SUVs to a ride-hail leasing company. Equipment, IP, and other assets were auctioned off. The proceeds went through a defined order of priority: secured creditors first, then unsecured creditors, then shareholders. By the time you reach shareholders, there's usually nothing left.

For creditors who had contracts with Fisker, the bankruptcy process allowed them to file claims and hope for partial recovery. But that hope was dim. The company's liabilities far exceeded its assets.

The Supplier Perspective

Suppliers who had provided components or services to Fisker found themselves caught in the bankruptcy process. Those with existing contracts might have legitimate claims in bankruptcy. Those owed money for recent deliveries became unsecured creditors competing with others for a minuscule recovery percentage.

This is one reason why the EV startup landscape consolidation mattered. Suppliers learned to be skeptical of startup customers with uncertain financial futures. When credibility is damaged, it's hard to rebuild. Fisker's failure made every other EV startup's fundraising harder because investors became more skeptical.

Lessons for the Electric Vehicle Industry Going Forward

The Fisker case, combined with the SEC's reduced enforcement activity, carries several important lessons for the EV industry as it matures.

First, the market itself is becoming a more effective enforcer than regulators. Companies that make false promises face harsh punishment through bankruptcy and stock price collapse. Surviving EV companies have learned to make more conservative claims because their survival depends on execution, not just promises.

Second, the remaining EV startups that succeed will likely be those with strong fundamentals: real technology, clear paths to profitability, experienced management, and careful capital allocation. Fisker failed partly because it constantly pivoted strategy, burning billions on unproven concepts. More disciplined approaches are naturally selected for.

Third, the relationship between startups and regulators matters. During high-enforcement periods, startups become more cautious and transparent. During low-enforcement periods, they might become more aggressive. This creates a cycle where regulatory intensity fluctuates with political administrations.

Comparing Fisker's Fate to Successful EV Companies

Tesla survived its startup phase with skeptics calling it doomed at every stage. Elon Musk made optimistic claims that skeptics said were unrealistic. Yet Tesla delivered. The company achieved profitability, real production scale, and market dominance. Because Tesla actually executed on its promises, regulatory scrutiny never gravitated toward securities fraud investigations.

Lucid Motors, despite facing an SEC investigation, has continued operating. The company raised substantial capital from Saudi Arabia's PIF (Public Investment Fund). It started delivery of its Sapphire sedan, one of the fastest four-door cars ever produced. Despite execution challenges and slower-than-expected sales, Lucid has maintained a path forward.

Rivian, the electric truck startup, has also survived its startup phase, though its path hasn't been smooth. The company faced production delays, cost overruns, and skeptical investors. But it didn't collapse entirely. It secured additional funding and continued building vehicles.

Fisker, by contrast, faced a combination of execution failures, poor capital management, quality control problems, and strategic confusion. Each of those problems independently might have been survivable. Together, they were fatal.

The SEC's investigation into Fisker sought to determine whether this failure was partly due to securities fraud—misleading investors about the company's prospects. The investigation's closure suggests investigators either found no evidence of fraud or decided not to pursue it.

Nikola faced the largest SEC settlement at $125 million, highlighting the agency's focus on high-profile cases. Estimated data for other startups.

The Broader Question: Does Regulatory Enforcement Matter?

The Fisker investigation closure raises a meta-question about regulatory enforcement itself. If the SEC closes an investigation without charges, what does that mean? Did the investigation fail to find evidence of wrongdoing? Did it find evidence but decide not to pursue? Did priorities simply shift?

Without explanation, it's impossible to know. And that lack of transparency is itself a problem. Investors in public markets rely on credible regulatory oversight. When the SEC's reasoning for enforcement decisions isn't transparent, confidence in the system erodes.

One perspective is that enforcement matters mainly as a deterrent. If companies know the SEC might investigate and bring charges for misleading claims, they're more careful. If companies think the SEC has lost interest in enforcement, they become bolder in their claims. This suggests that enforcement activity, even against failed companies like Fisker, serves a broader function of maintaining market integrity.

Another perspective is that enforcement costs resources that could be spent on prevention, education, or market-making activities. Maybe the SEC should focus on helping companies understand securities law requirements, rather than prosecuting those who allegedly violate them. This perspective suggests that reduced enforcement might not be harmful if it's replaced by more effective regulatory approaches.

These perspectives aren't reconcilable without evidence about actual enforcement effectiveness. That evidence is sparse. We don't have clear data showing whether the SEC's aggressive enforcement during 2023-2024 actually deterred fraud, or whether reduced enforcement leads to increased misconduct.

What we do know is that the EV startup ecosystem faced natural market discipline regardless of SEC activity. Companies that couldn't execute failed. Companies that could execute survived. Regulatory enforcement was one factor among many, but probably not the decisive one.

Media Coverage and Public Understanding

Fisker's collapse received substantial media coverage. Outlets like TechCrunch, The Verge, and traditional business media followed the company's struggles closely. This public coverage itself serves an enforcement function. Investors learned what happened. The market adjusted. Startups learned lessons.

When the SEC closed its investigation without explanation, the media coverage was minimal. TechCrunch filed the FOIA request and reported the closure, but it didn't generate the kind of widespread attention that enforcement actions typically do.

This difference in media attention suggests that the deterrent effect of regulatory enforcement might partly work through media amplification. High-profile SEC cases get covered by major outlets. They become cautionary tales. They shape behavior through public narrative.

Quiet case closures, by contrast, disappear from public view. Few people know that the investigation closed. There's no opportunity for the case to serve as a cautionary tale.

This creates an asymmetry where enforcement actions are amplified but case closures without action are silent. From a deterrence perspective, that's problematic. The regulatory absence sends its own message, but it's a quieter one.

International Perspective: How Other Regulators Handle EV Startups

The SEC's reduced enforcement isn't unique to the United States. Regulatory agencies globally have had to grapple with electric vehicle startups making ambitious claims.

In the European Union, regulators have also faced EV startup fraud cases. The approach has been somewhat more stringent, partly because European regulators tend toward more active intervention in markets. But the basic tension remains the same: how much enforcement is appropriate, and when does enforcement become counterproductive?

China, despite its authoritarian system, has also seen EV startup failures and alleged fraud cases. The Chinese government supported several EV startups, then had to deal with the consequences when some failed or allegedly defrauded investors.

The pattern globally suggests that EV startup boom-bust cycles are natural to the industry, not unique to the United States. The regulatory question is how much government intervention should attempt to prevent these cycles, and how much should simply let market forces work.

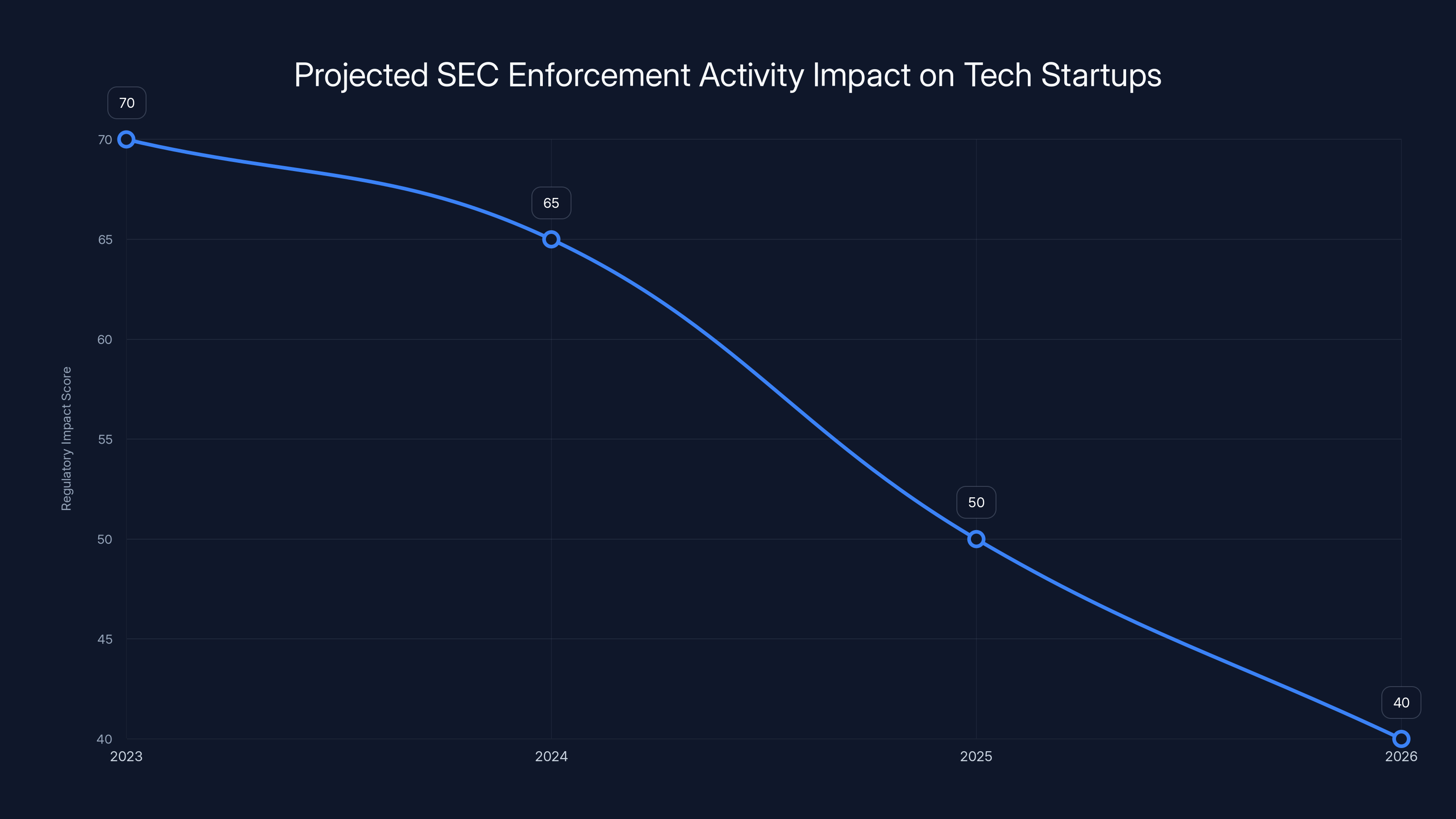

The regulatory environment is projected to become more permissive from 2023 to 2026, leading to increased optimism among tech startups. (Estimated data)

The Faraday Future Investigation: Active Enforcement in a Dormant Environment

Faraday Future represents what active enforcement looks like, even in the reduced environment of 2025. The company continues to operate despite ongoing SEC investigation. The Wells notices issued in July 2025 represent formal notice of recommended enforcement.

Faraday's situation is precarious. The company has survived longer than many EV startups, but it faces continuous struggles with production, capital raising, and market acceptance. The SEC investigation adds another layer of uncertainty.

If the SEC eventually brings charges against Faraday Future and its executives, the case would serve as the capstone to a broader story about EV startup enforcement. If the investigation continues indefinitely without resolution, it represents a different message: enforcement is slow and uncertain, and companies can operate under investigation for years without resolution.

Faraday's resilience despite these challenges suggests that strong management and customer demand can overcome regulatory headwinds. The company's continued operation, despite not achieving profitability, shows that some stakeholders remain confident in its eventual success.

What About Shareholders and Investment Losses?

Fisker shareholders lost substantial amounts when the company collapsed. Early investors who bought at the IPO saw shares go from public market prices to worthless. Later investors who bought on the downside hoping for a recovery lost too.

These losses are material. People invested retirement savings, student loans, and trading account money into Fisker shares based on public statements about the company's prospects. When those prospects didn't materialize, they suffered real financial harm.

The question of whether that harm was caused by fraud—provable SEC violations—is distinct from the question of whether the harm occurred. Even without fraud, investors lost money when they backed a failed company. The absence of SEC charges doesn't restore those losses.

This is one reason why some argue for broader investor protection mechanisms beyond just fraud prosecution. If a company makes claims it can't verify, perhaps investors deserve protection regardless of whether fraud can be proven. But that's a broader policy question beyond the scope of this article.

What's clear is that Fisker shareholders have no realistic avenue for recovery through SEC enforcement or shareholder lawsuits. The company is bankrupt. Its assets have been liquidated. Any damages would come from a fraction of the assets remaining, which is essentially nothing.

Timeline of Key Events: The SEC's Involvement with Fisker

Understanding the chronology helps clarify what happened.

October 2024: The SEC's investigation into Fisker is publicly disclosed in a bankruptcy court filing. The agency indicates it has sent subpoenas and may request additional documents.

November 2024 - August 2025: Investigation continues with minimal public awareness. The agency gathers the approximately 21.7 gigabytes of records related to Fisker's operations.

September 2025: The SEC closes the investigation. No announcement is made publicly. No explanation is provided. The agency's actions occur quietly.

January 2026: In response to a FOIA request from TechCrunch, the SEC reveals that the investigation was closed in September 2025.

February 2026: TechCrunch reports the investigation closure, providing the first public account of the decision.

This timeline shows how regulatory decisions that might affect investors can occur entirely without public transparency. The investigation closed in September, but investors and the general public didn't learn about it until January, five months later.

The Role of Bankruptcy Courts in Regulatory Cases

Fisker's bankruptcy process intersected with the SEC's investigation in interesting ways. When a company files for bankruptcy, a bankruptcy court takes control of the assets and the process. The SEC's investigation didn't prevent the bankruptcy proceedings or stay the liquidation process.

Bankruptcy courts and regulatory agencies have different focuses. The bankruptcy court's job is to maximize recovery for creditors and follow the priority rules of bankruptcy law. The SEC's job, theoretically, is to protect investors and maintain market integrity.

In Fisker's case, these goals didn't conflict enough to create drama. The company's assets were worthless. There was nothing to recover. The SEC's investigation, regardless of its outcome, wouldn't affect the liquidation process or the distribution of assets.

But the bankruptcy filing itself became a source of information for the SEC. As Fisker's accounting records, business plans, and communications were disclosed in the bankruptcy process, the SEC had access to that information. Some of this material might have gone into the investigation.

Future Implications: What This Means for Tech Startups More Broadly

The Fisker case and the broader decline in SEC enforcement activity carries implications beyond just EV startups. It affects all tech startups that raise capital from public investors or plan to go public.

When enforcement is active, startups become more careful about claims. Founders consult with securities lawyers before making public statements. Board members push back on optimistic projections. The culture shifts toward conservatism.

When enforcement is dormant, the opposite occurs. Founders feel freer to make ambitious claims. Board members worry less about securities law compliance. The culture shifts toward optimism.

Neither extreme is ideal. Over-caution might prevent companies from communicating legitimately impressive plans. Over-optimism might mislead investors and set companies up for failure when reality doesn't match promises.

But the pendulum is swinging now toward the optimistic side. Startups operating in 2025 and 2026 face a different regulatory environment than those operating in 2023-2024. That environment is more permissive, more forgiving, more focused on growth and less on compliance.

For investors, this means increased responsibility to conduct due diligence. If the SEC isn't actively policing startups, investors need to be more skeptical of claims. They need to verify assertions independently rather than relying on regulatory oversight as a backstop.

FAQ

What is the SEC's role in investigating startups?

The Securities and Exchange Commission is the federal agency responsible for enforcing securities laws. When companies make false or misleading statements to investors, the SEC can investigate and bring enforcement actions including civil penalties, disgorgement of profits, and injunctions against future misconduct. The agency investigates both publicly traded companies and private companies planning to go public or raising capital through securities offerings.

Why did the SEC investigate Fisker?

Fisker faced investigation because the company made ambitious claims about its technology, production capabilities, and financial prospects that later proved inaccurate or unrealistic. The SEC investigates such situations to determine whether executives knowingly or recklessly misled investors about material facts. The agency issued subpoenas to the company to gather documents and testimony relevant to its inquiry into whether securities fraud occurred.

What does it mean when the SEC closes an investigation without charges?

When an SEC investigation closes without enforcement action, it typically means one of several things: the investigators found insufficient evidence of violations, they determined the violations occurred but decided not to pursue charges based on policy priorities, the company cooperated and reached an informal resolution, or the agency reallocated resources to higher-priority cases. The SEC rarely discloses which explanation applies, leaving public speculation about the actual reasoning.

How does SEC enforcement activity affect startup behavior?

When the SEC actively investigates and brings cases against startups, it creates a deterrent effect that causes founders and boards to be more cautious about public claims and projections. High-profile enforcement actions send signals to the broader startup community about what the agency considers serious violations. Conversely, when enforcement activity declines, startups face lower perceived costs to making aggressive claims, potentially leading to more optimistic communications and higher fraud risk.

What happened to Fisker's shareholders after the bankruptcy?

Fisker shareholders lost virtually everything when the company filed for Chapter 11 bankruptcy in June 2024. In bankruptcy, equity shareholders are last in the priority order for asset distribution, coming after secured creditors and unsecured creditors like suppliers and employees. Since Fisker's liabilities far exceeded its assets, there was essentially nothing left for shareholders after other creditors were paid. This is a common outcome in startup bankruptcies.

Why is Faraday Future still under investigation while Fisker's is closed?

Faraday Future received Wells notices from the SEC in July 2025, indicating that the agency's staff recommended enforcement action. The investigation continues despite no public enforcement action being taken. The reasons for the different treatment between Faraday and Fisker are unclear, but may relate to the strength of evidence, the severity of alleged violations, the company's current status (Faraday continues operating while Fisker is liquidating), or simply the SEC's assessment of enforcement priorities. Both companies face significant operational challenges and investor skepticism regardless of regulatory status.

What is a Wells notice and what does it mean?

A Wells notice is a formal letter from the SEC informing a person or company that the agency's staff has recommended bringing an enforcement action. Recipients typically have the opportunity to submit a response, often called a Wells submission, presenting arguments for why the recommended action shouldn't proceed. Wells notices don't guarantee enforcement action but represent a significant step in the SEC's enforcement process. Receiving a Wells notice signals that the agency believes violations occurred and is serious about pursuing the matter.

How did Trump's second term affect SEC enforcement?

The SEC initiated 313 enforcement actions in 2025, representing a 27% decline from 2024 and the lowest number in a decade. Total monetary settlements fell 45%. This dramatic shift reflects the Trump administration's stated policy of reducing regulatory burdens on business. The SEC, as an executive branch agency, appears to have taken direction to reduce enforcement activity, focusing resources on fewer, higher-priority cases rather than pursuing investigations across the broader landscape of potential violations.

Can Fisker shareholders sue for their losses?

Fisker shareholders might pursue class action lawsuits against the company or its executives for securities fraud if they can prove that false statements were made with intent to deceive and that they relied on those statements. However, such lawsuits face significant obstacles: the company is bankrupt with no assets for recovery, the executives likely lack personal assets to pursue, and proving fraud rather than mere business failure is difficult. Most investor losses from failed startups go uncompensated through the legal system.

What makes securities fraud different from regular business failure?

Security fraud involves making false or misleading statements to investors with intent to deceive (or reckless disregard for truth) about material facts. Regular business failure means a company didn't execute on its plans, even if those plans were communicated honestly. The distinction matters legally because fraud is punishable while honest failure isn't. A startup founder who genuinely believed his company could succeed but failed due to execution problems isn't committing fraud. One who knew the company couldn't succeed but claimed it could is.

Conclusion: The Changing Landscape of Startup Accountability

Fisker's story is ultimately about the tension between ambition and accountability, between innovation and fraud prevention, between allowing startup founders freedom to pursue bold visions and protecting investors from deliberate deception.

The company's collapse was real. Thousands of people lost jobs. Billions of dollars in investor capital evaporated. Suppliers went unpaid. The pain was concrete and distributed across many people. Yet the SEC investigation closed without charges, suggesting the agency found no provable fraud.

This doesn't mean Fisker's executives acted ethically. It means their actions, from the SEC's perspective, didn't cross the legal line into securities fraud. That's a meaningful distinction but a cold comfort to those who lost money.

The broader pattern revealed by the Fisker case is significant. The SEC's enforcement activity has declined dramatically in the early months of Trump's second term. This shift reflects broader philosophical differences about regulation's role in markets and startups' rights to make optimistic claims.

For investors, the lesson is clear: don't assume regulatory oversight protects you from startup fraud. The SEC investigates some cases but not others. Some investigations result in charges while others close quietly. The agency's priorities shift with political administrations. You need to conduct your own due diligence.

For startups, the message is similarly complex. The regulatory environment has become more permissive, which means lower compliance burdens but also higher investor skepticism. The days of startups making wild claims without scrutiny have returned, but investors have learned the hard lessons of the 2021-2025 cycle. They're less credulous now.

For the electric vehicle industry specifically, Fisker represents one chapter in a longer story. The startup boom has given way to consolidation. Companies that can execute on their promises survive and thrive. Companies that can't fail. The SEC's investigation, its closure, and its decision not to bring charges will barely register in that bigger narrative.

What matters more is whether EV technology improves, whether costs decline, whether companies find real paths to profitability. On those metrics, Fisker failed. The SEC's investigation was peripheral to that core failure.

As we move forward, startup ecosystems will continue to produce ambitious visions and tragic failures. Regulators will continue to decide which cases deserve enforcement attention. Investors will continue to take risks and sometimes lose money. That cycle isn't broken by reduced SEC enforcement. It's just made more risky for those who can't independently verify startup claims.

The Fisker case is closed. The company is liquidated. The founder is quiet. The investors are gone. And the SEC has moved on to other priorities. That's the new normal.

Key Takeaways

- SEC closed its Fisker investigation in September 2025 without charges, revealed through FOIA request in January 2026

- SEC enforcement actions dropped 27% to 313 total in 2025, the lowest in a decade, with monetary settlements falling 45%

- Multiple EV startups faced enforcement (Nikola, Lordstown, Canoo, Hyzon) but Fisker escaped charges despite investigation

- Faraday Future remains under investigation with July 2025 Wells notices, the only active EV startup enforcement case

- SEC's reduced enforcement reflects political shift toward reducing regulatory burden, not conclusive evidence of no fraud

- Investors cannot rely on SEC oversight and must conduct independent due diligence on startup claims and capabilities

Related Articles

- Elon Musk's $150M SEC Lawsuit: Why Trump Won't Back Him [2025]

- How Rivian's Software Strategy Saved the Company in 2025

- DOJ Antitrust Chief's Surprise Exit Weeks Before Live Nation Trial [2025]

- Epstein's Secret Role in Musk's Tesla Private Deal [2025]

- xAI Co-Founder Exodus: What Tony Wu's Departure Reveals About AI Leadership [2025]

- State Department Deletes X Posts Before Trump's Term: What It Means [2025]