![Snap's Q4 Earnings: Revenue Growth, User Decline, and the Specs Gamble [2025]](https://tryrunable.com/blog/snap-s-q4-earnings-revenue-growth-user-decline-and-the-specs/image-1-1770251870943.jpg)

Introduction: The Snap Paradox Playing Out in Real Time

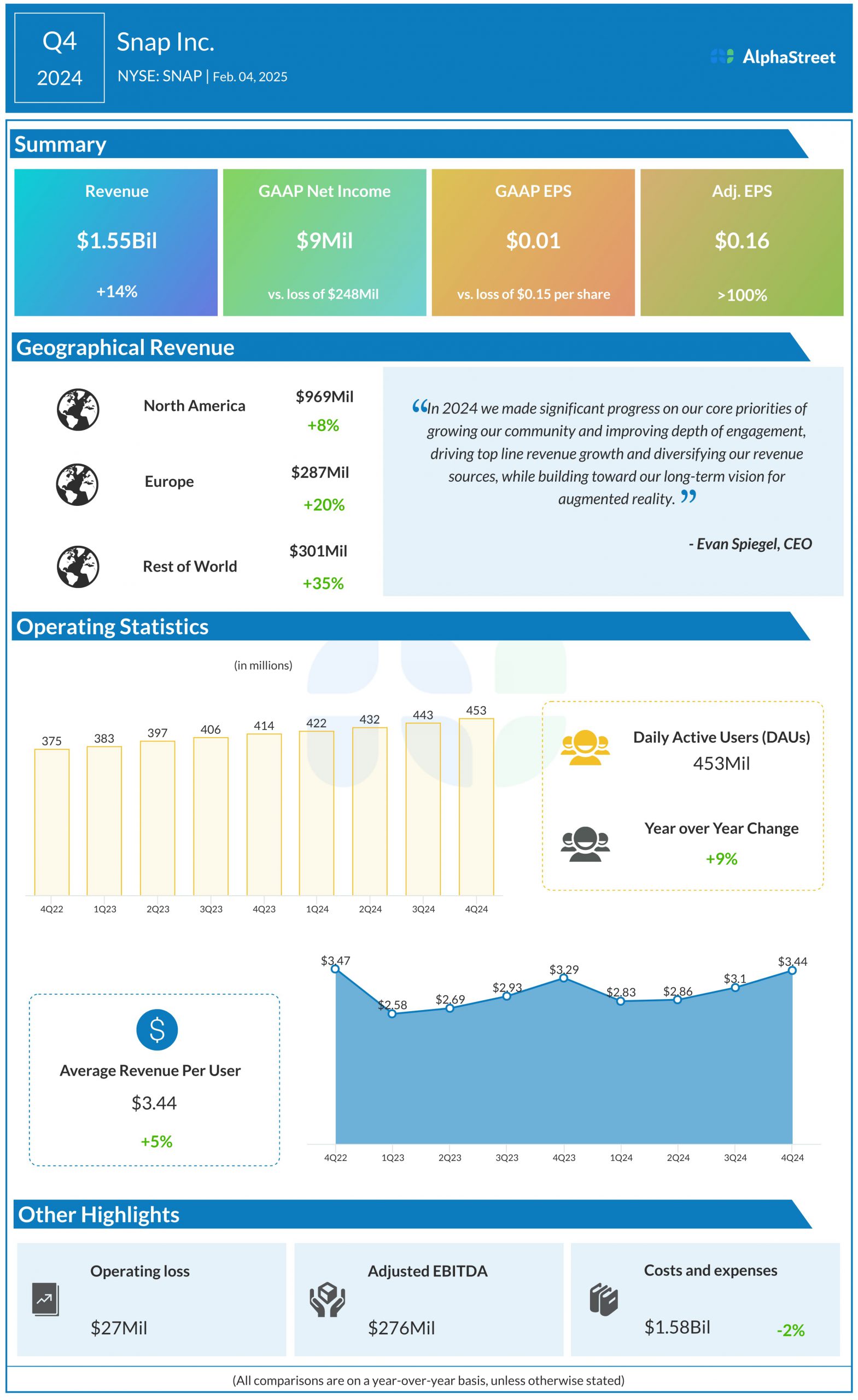

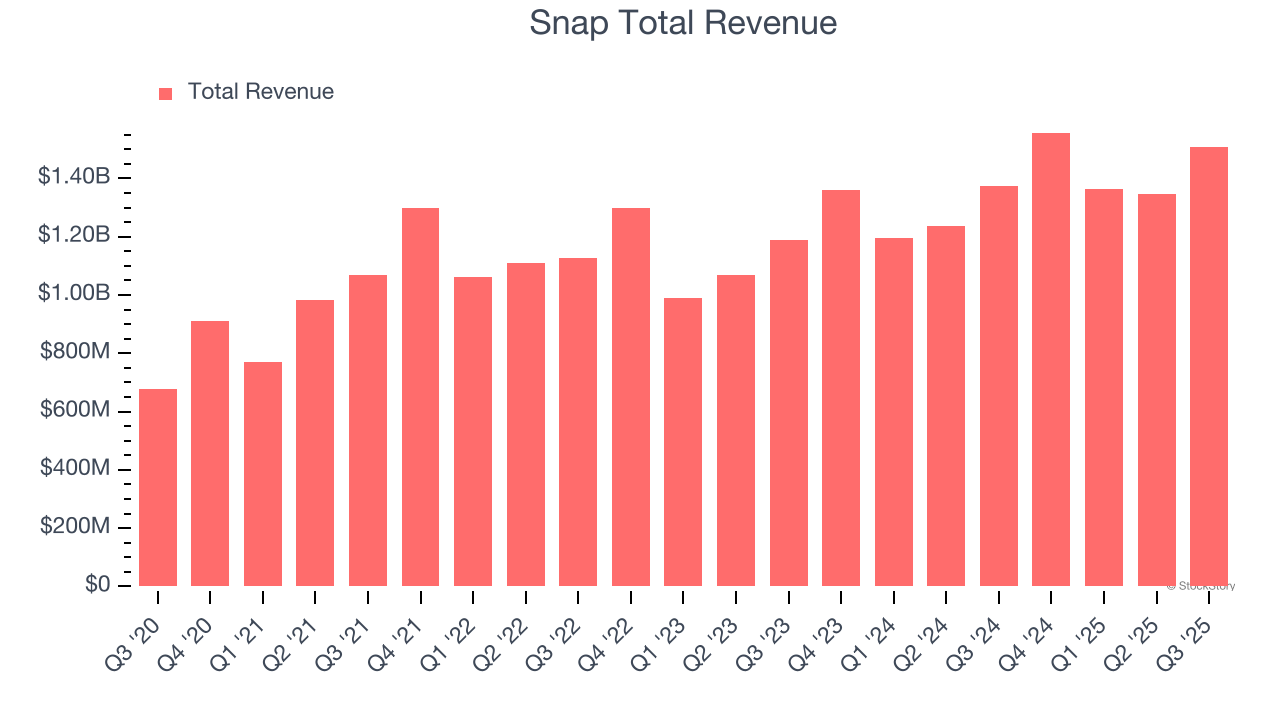

Here's the thing about Snap right now: the numbers tell two completely different stories depending on which ones you're looking at. On one hand, the company just reported

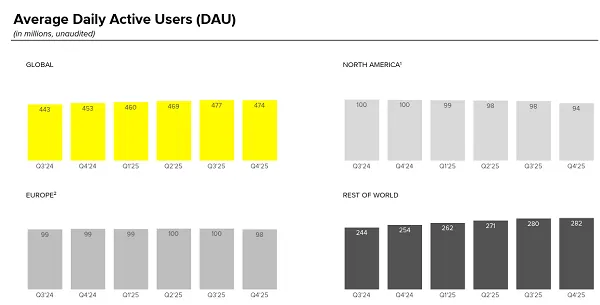

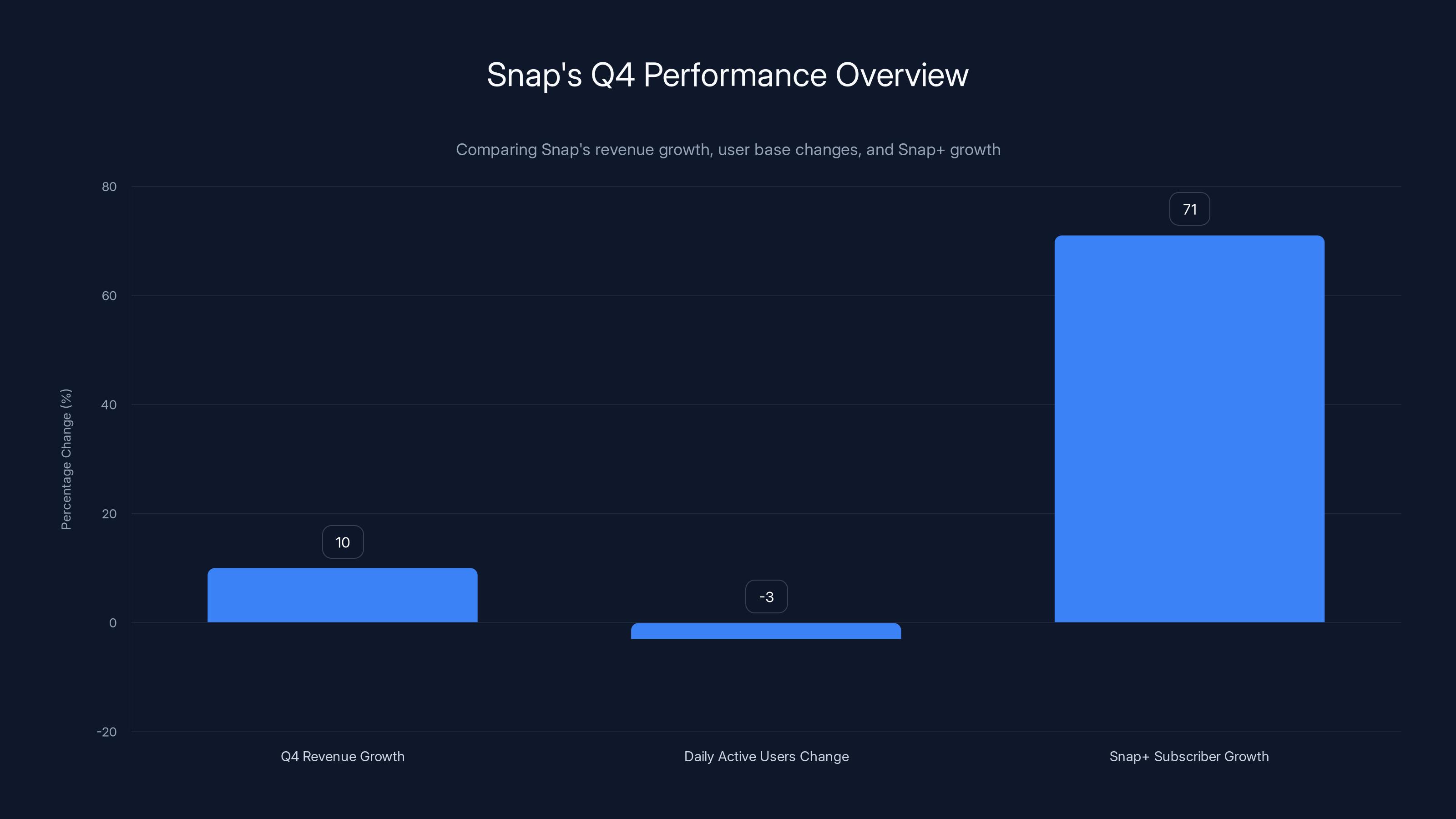

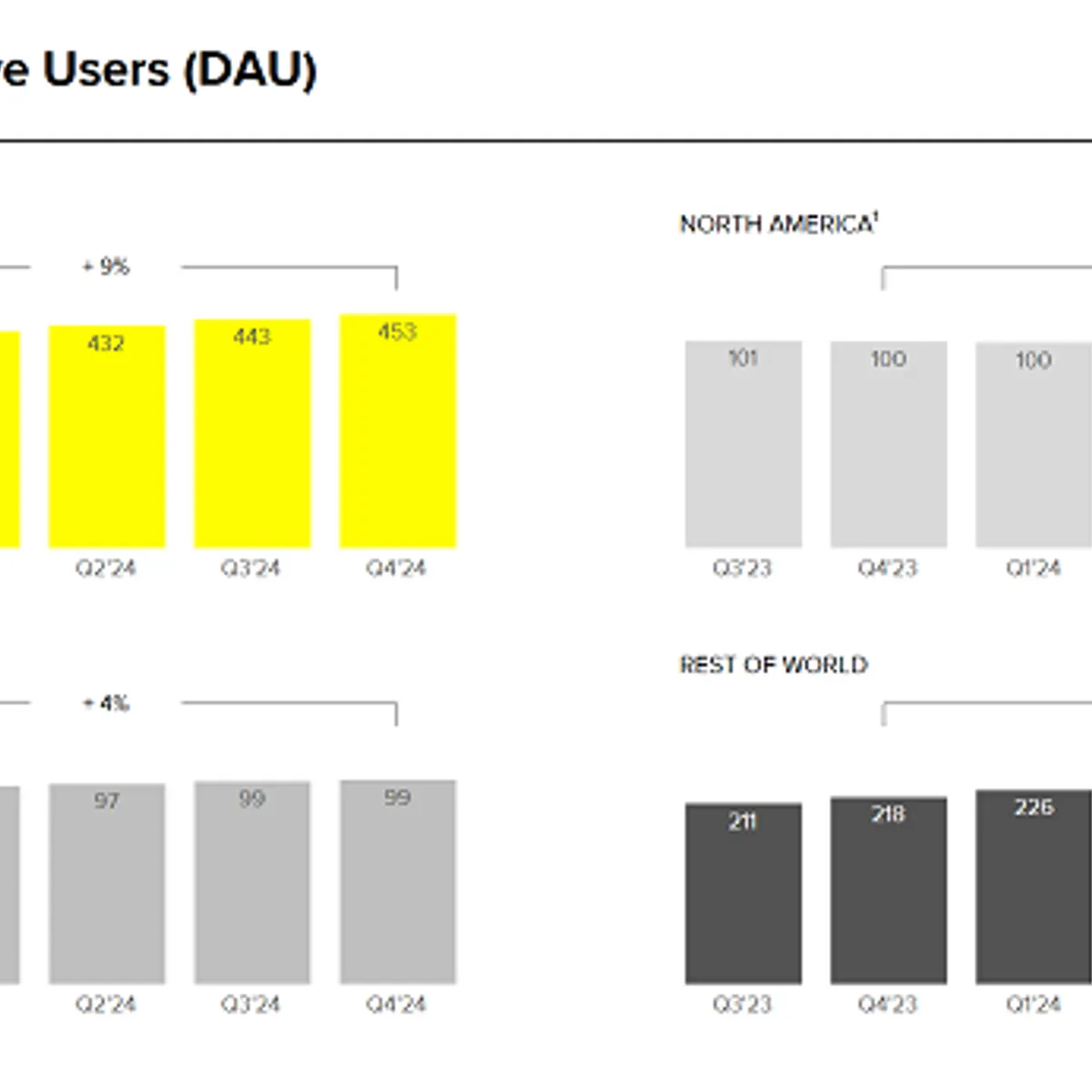

But here's the catch that's keeping investors up at night: daily active users actually declined last quarter. The platform dropped from 477 million to 474 million users. That's a 3-million-user loss, concentrated in North America and Europe—the company's most lucrative markets where advertisers pay the most per impression.

This tension sitting at the center of Snap's latest earnings report tells you everything you need to know about where the company stands heading into 2025. It's simultaneously succeeding and struggling. It's growing revenue while losing users. It's diversifying revenue streams while warning that Q1 growth will come in below analyst expectations due to competitive pressure from Facebook, Instagram, and TikTok.

What's actually happening behind the scenes is a company in the middle of a high-stakes strategic pivot. Snap is trying to break free from its addiction to advertising revenue—a smart move in a world where privacy regulations keep tightening and platform competition keeps intensifying. The company is betting heavily on three new revenue pillars: subscriptions through Snap+, hardware through its upcoming Specs augmented reality glasses, and alternative monetization through things like charging for Memories storage.

The question isn't whether Snap's strategy makes sense. It does. The real question is whether the company can execute this transition fast enough while holding its user base steady and keeping advertisers happy in the meantime. And based on the latest numbers, that execution is looking messier than the company probably hoped it would be.

Let's break down what Snap actually achieved in Q4, what it reveals about the social media landscape in 2025, and what the company's hardware bet means for the future of computing and communication.

TL; DR

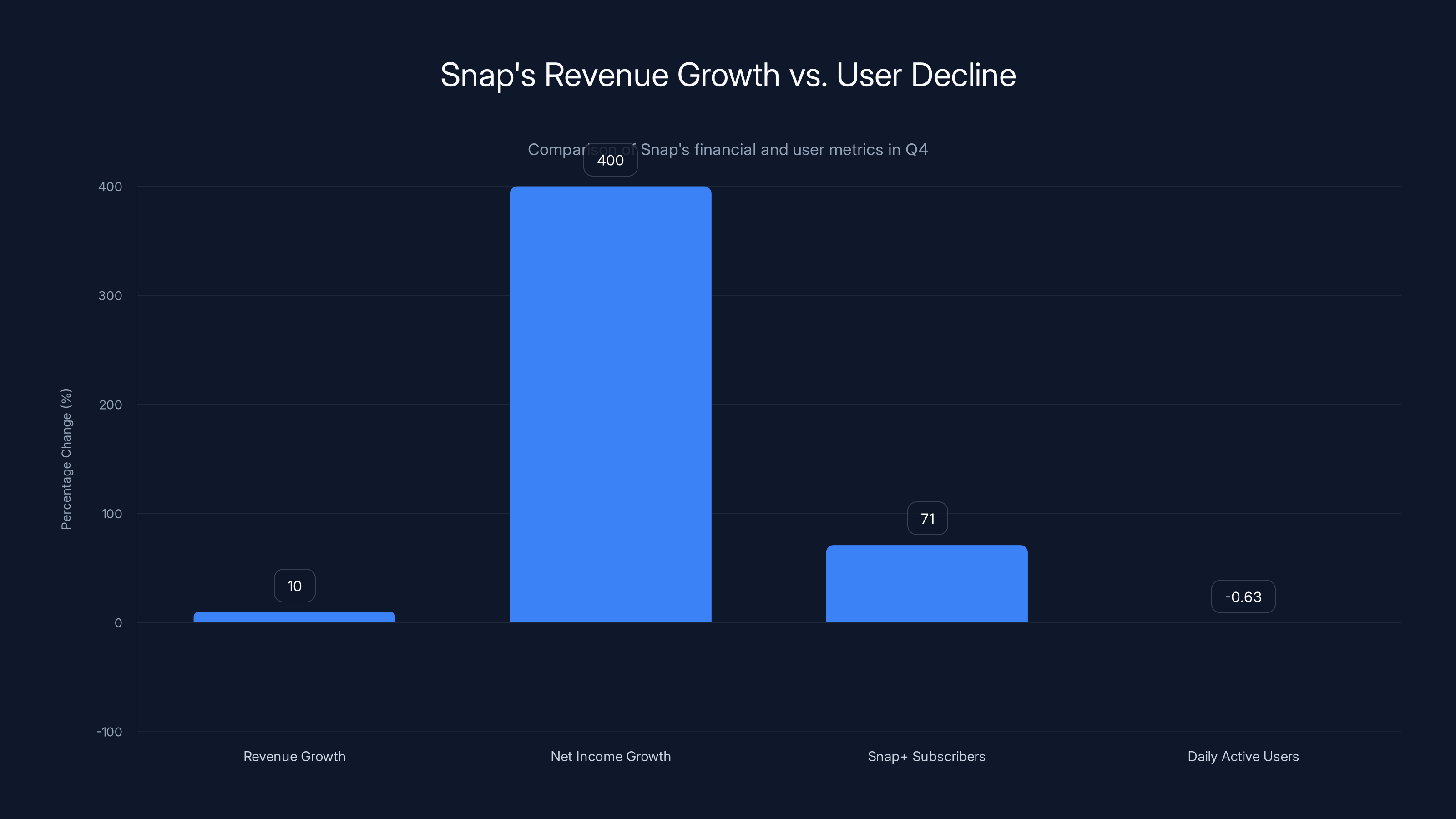

- Revenue Growth Masks User Losses: Snap hit $1.7B in Q4 revenue (+10% Yo Y), but daily active users dropped from 477M to 474M, with declines concentrated in North America and Europe.

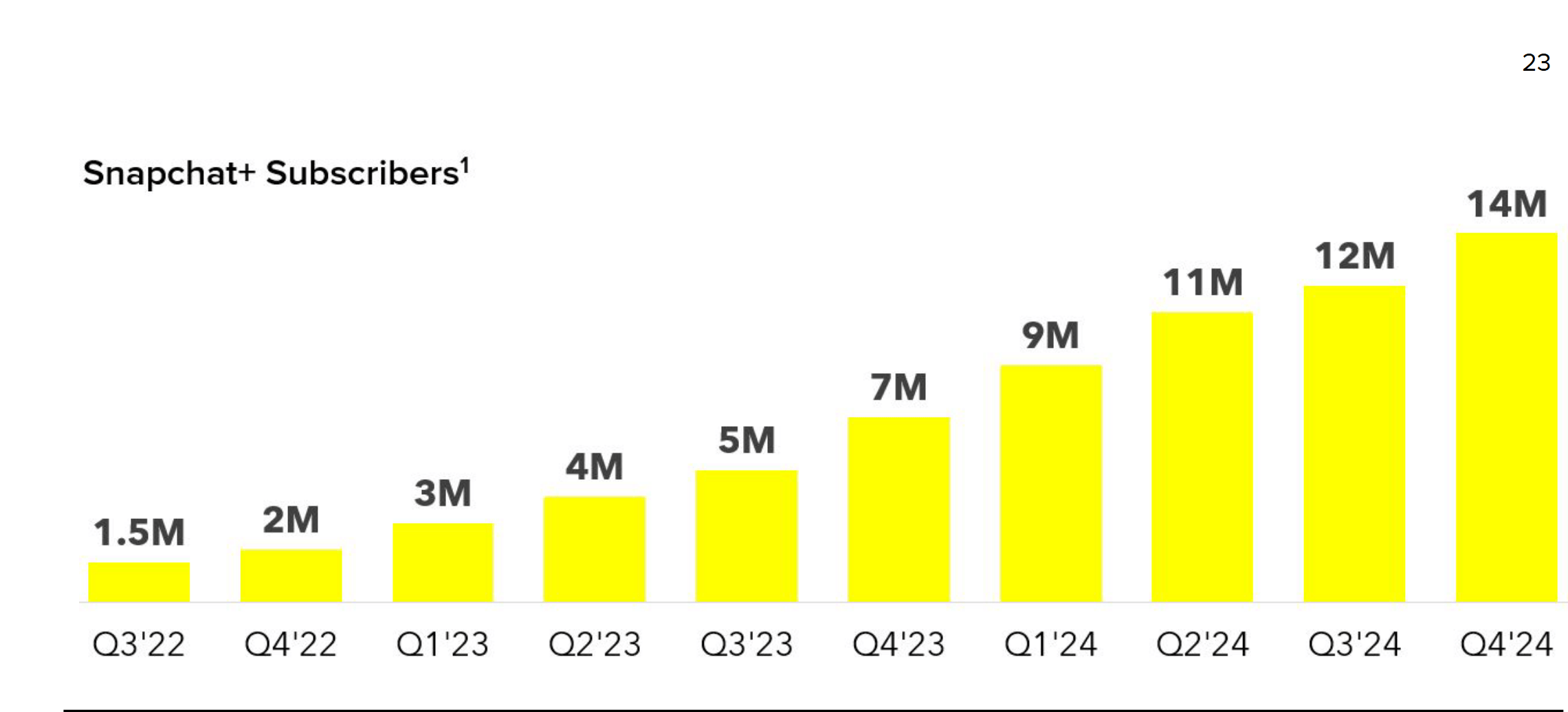

- Subscription Strategy Works: Snap+ grew 71% Yo Y to 24 million subscribers, proving the paid tier strategy works and delivering higher-margin revenue.

- Advertising Headwinds Ahead: The company warned that Q1 revenue will miss analyst expectations due to intensifying competition from Meta's platforms and TikTok.

- Hardware is the Big Bet: Snap created a new Specs Inc. subsidiary to develop augmented reality glasses, positioning hardware as a potential long-term revenue and user engagement driver.

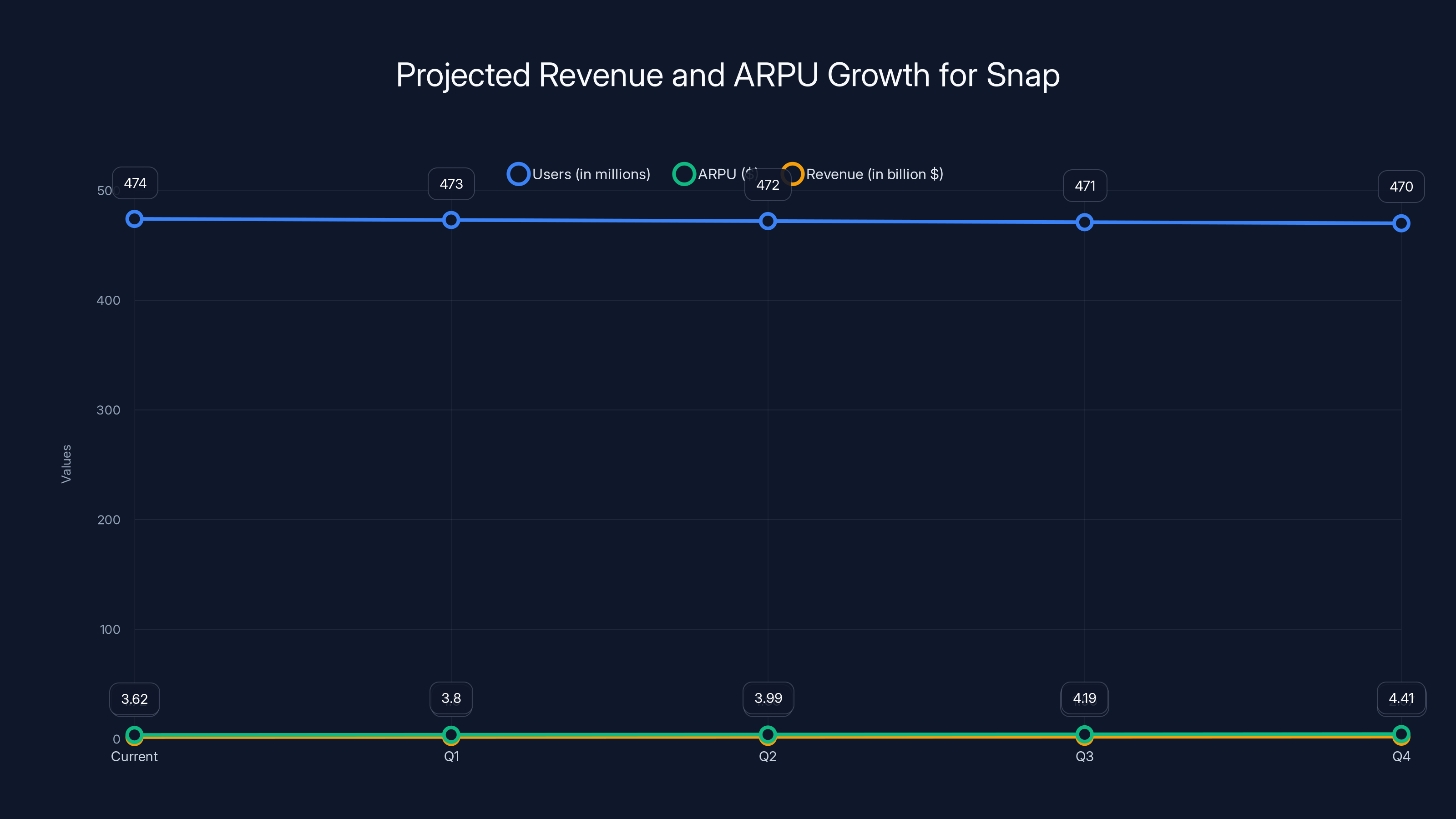

- ARPU Growth Can't Fix User Decline: Even though average revenue per user grew from 3.62, losing users in premium markets like North America signals deeper engagement problems.

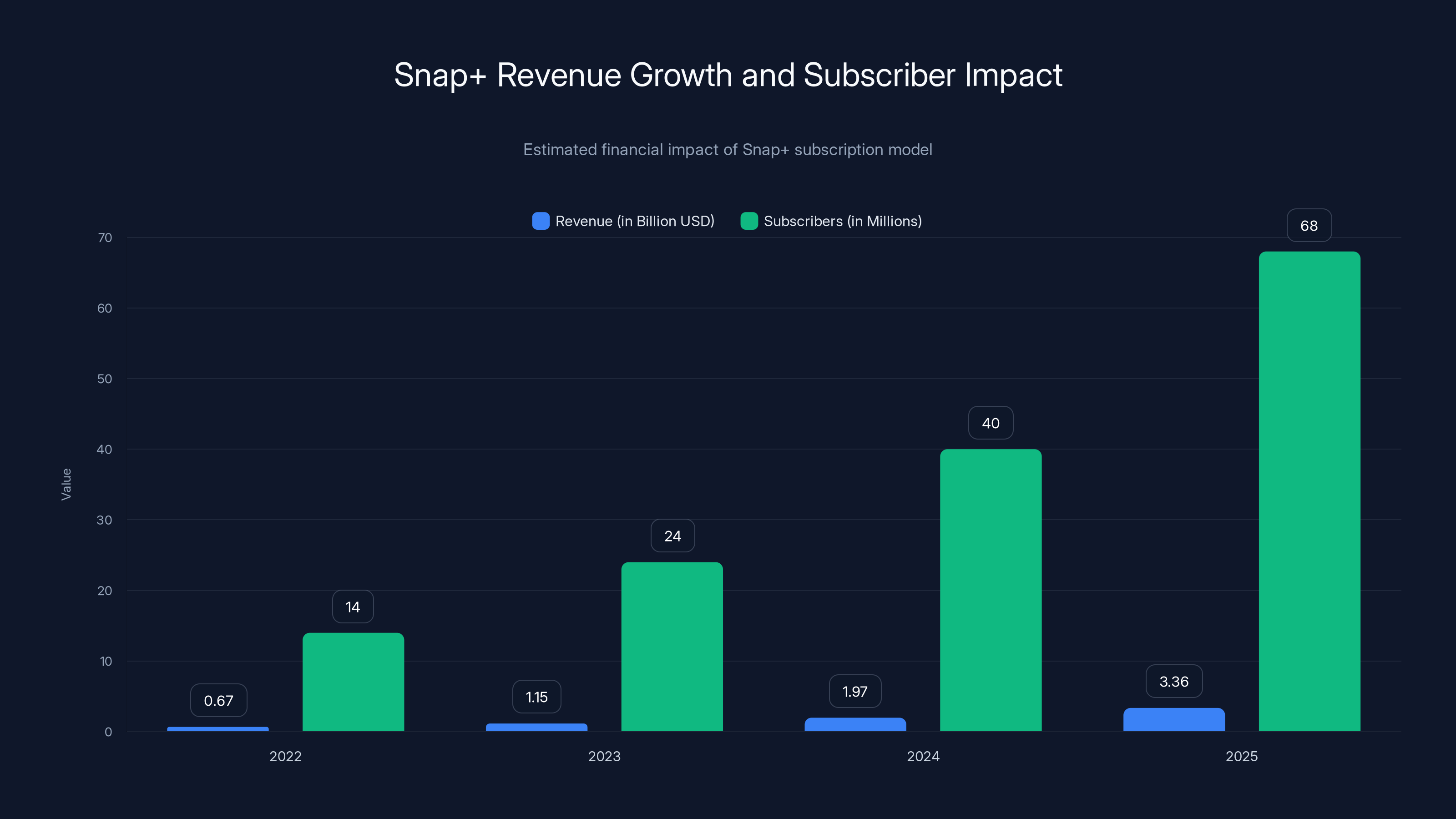

Snap+ is projected to grow significantly, with revenue reaching approximately $3.36 billion by 2025 and subscriber count increasing to 68 million. Estimated data based on current growth trends.

The Revenue Growth Story: How Snap Actually Made More Money With Fewer Users

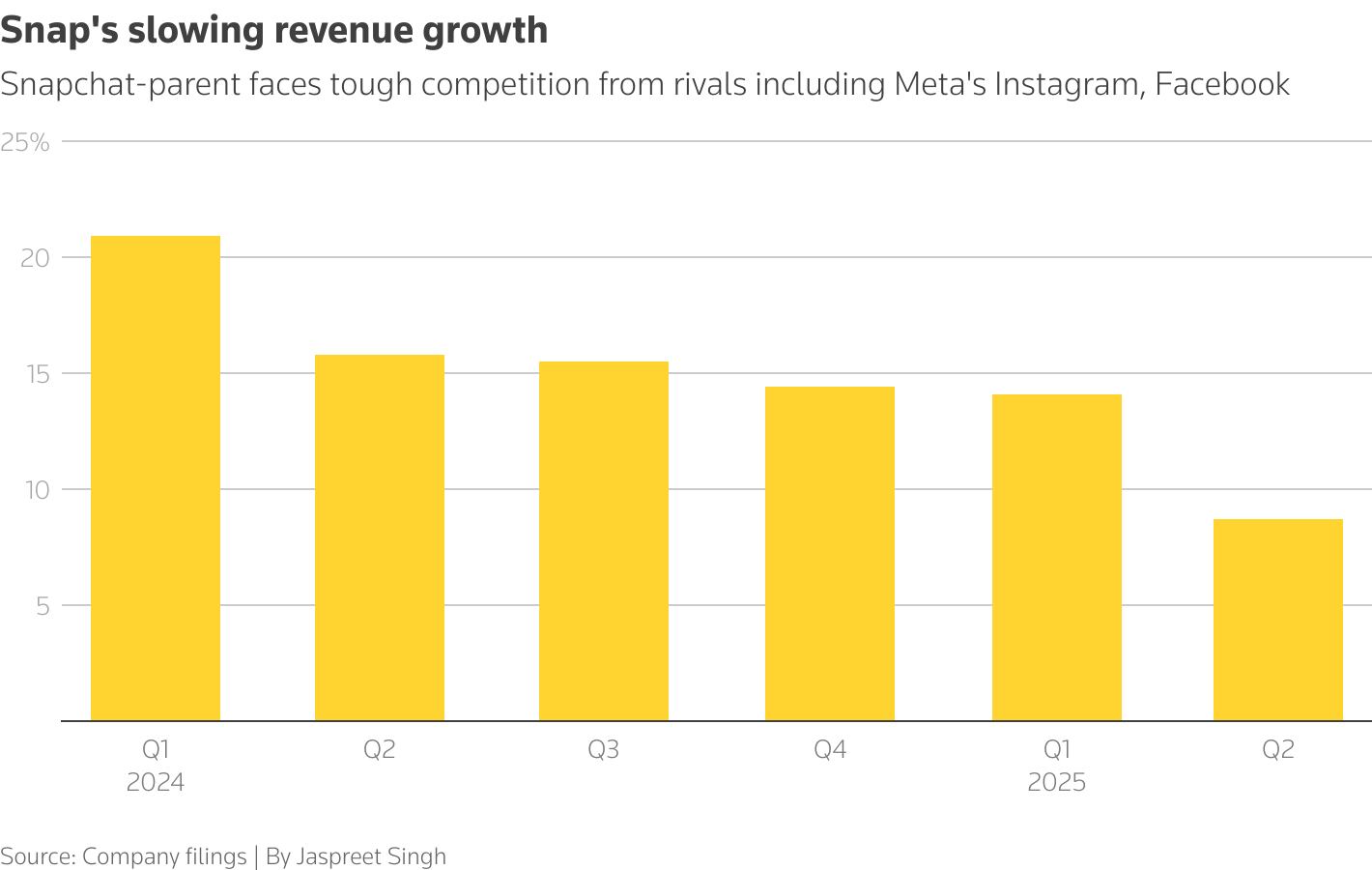

Let's start with the part of Snap's earnings report that would normally be celebrated at any other company: revenue up 10% year-over-year. That's solid growth for a platform operating at Snap's scale, especially when you consider it's happening in an advertising market that's increasingly dominated by giants with better targeting capabilities and more user data.

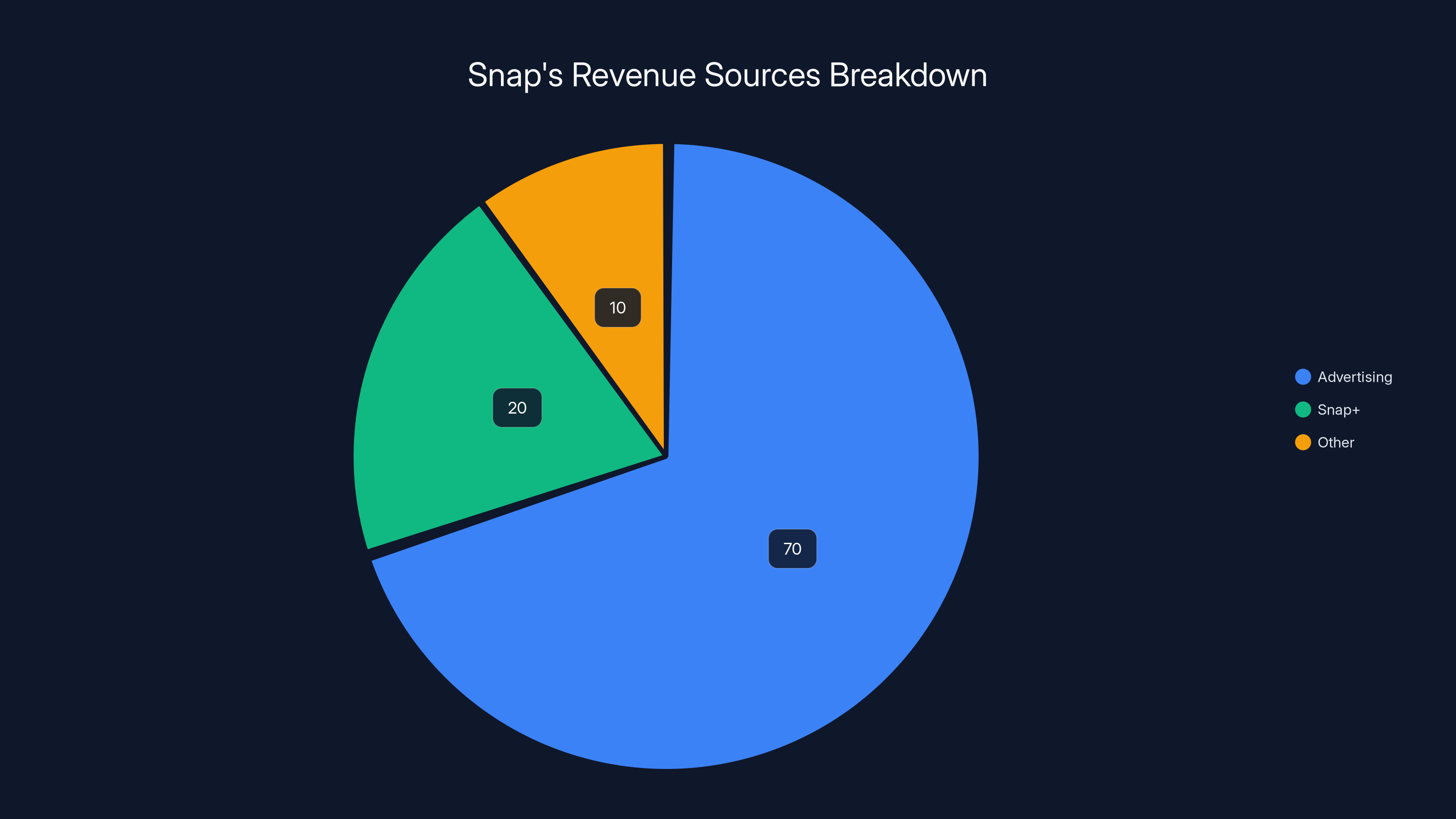

The $1.7 billion number breaks down across multiple sources now, and that's the real story here. Snap is no longer purely an advertising business, even if ads still represent the vast majority of revenue. The company's been aggressively developing non-advertising revenue streams, and Q4 shows those efforts are actually moving the needle.

Snap+ is the obvious flagship here. The subscription service, launched in 2022, lets users pay monthly for premium features like the ability to see who's viewed their Snap story, custom emojis next to their username in chats, and the ability to reorder their friend list. It sounds almost quaint compared to what other subscription services offer, but here's what matters: it works. Growing to 24 million subscribers at a 71% year-over-year growth rate means the feature is accelerating, not plateauing. That's the kind of velocity that makes investors lean forward in their chairs.

Why does Snap+ matter beyond just the pure revenue number? Because subscription revenue has fundamentally different economics than advertising revenue. Subscription customers pay predictable, recurring amounts each month. That money isn't subject to advertiser budget cuts or seasonal fluctuations. It's not influenced by Apple's privacy policy changes or changes in how Meta's algorithm distributes content. For a company that spent the last decade getting punched in the face by privacy regulations, this shift is existential.

The company also started charging users for Memories storage during Q4, a feature that lets users save and back up their Snaps indefinitely. This is still relatively new, so the revenue contribution is modest compared to Snap+, but it's telling about where Snap's head is at strategically. The company is experimenting with charging for functionality that used to be free. Some of those experiments will fail. Some will stick and turn into meaningful revenue streams.

Average revenue per user grew from

Net income surged to

But here's where the reality check comes in: none of this revenue growth changes the fundamental problem. Snap is losing users in the markets where it makes the most money. Advertising still represents the vast majority of Snap's revenue, and advertising depends on having engaged users. Revenue growth is real, but it's being accomplished despite headwinds, not because the core business is thriving.

Snap's revenue is primarily from advertising (70%), but Snap+ (20%) and other sources (10%) are growing. Estimated data.

The User Decline Problem: Why Losing 3 Million Users Actually Matters

Okay, so Snap lost 3 million daily active users last quarter. In the context of a platform with 474 million users, that's less than 1% of the user base. It's easy to dismiss. Snap's management basically did exactly that during the earnings call, downplaying the decline and focusing instead on revenue growth and the Snap+ subscription business.

But losses in North America and Europe are not the same as losses in other markets, and that's the crucial detail everybody needs to lock in.

North America and Europe are Snap's premium markets. Advertisers pay the most for eyeballs in these regions. The per-user economics are dramatically better than in emerging markets. When your user base is declining in your highest-value markets while growing slightly elsewhere, that's not a sign of health. That's a sign of competitive pressure where it matters most.

Why is Snap losing users in North America and Europe specifically? The obvious answer is competition. Instagram and Facebook have copy-pasted basically every feature Snap invented—Stories, ephemeral messaging, augmented reality filters. Meta (the parent company) has 3 billion monthly active users across its family of apps and vastly superior monetization per user. TikTok has become the destination app for younger demographics, and Snap's historically core audience (teens and early twenties users) is increasingly spending time there instead.

Snap's been losing the engagement war to TikTok for years now. The company tried its own version of TikTok-style content with Spotlight (a feed of short user-generated videos), but it never achieved TikTok's cultural velocity. When you're competing against TikTok—an app specifically engineered by a massive tech company to be maximally engaging and entertaining—it's hard to win as a messaging-first platform trying to be everything.

The user decline also raises questions about Snap's value proposition in 2025. When you strip away the novelty and the brand coolness that came with being the first major platform built around ephemeral messaging, what's actually unique about Snap anymore? Instagram Stories work the same way. Instagram Reels compete with TikTok content. Instagram has more users and better monetization. TikTok has more entertainment value. Meta has messenger apps with end-to-end encryption. Snap's differentiation has eroded significantly.

Here's another angle that's getting less attention: Snap's regulatory environment is getting worse, not better. The app faces pressure globally on data privacy, child safety, and content moderation. Every regulatory tightening makes it harder for Snap to compete, because regulatory compliance costs money and limits the data Snap can collect for advertising. Meta has more resources to handle regulatory costs. TikTok has geopolitical backing. Snap is stuck in the middle with fewer resources than Meta and less political capital than TikTok.

The company also faces a pure UX problem that's rarely discussed openly. Snap's app is complicated. It's powerful and feature-rich, but it's not intuitive. You have to learn Snap's grammar—the swipe gestures, the menu structures, the way Stories work, the way Memories work. Compare that to TikTok, which you can understand within 30 seconds of opening it. Compare it to Instagram, which is designed to be obvious to anyone who's used a smartphone. Snap's complexity is a feature for power users, but it's a bug for new user onboarding.

The combination of these factors—competitive pressure from better-resourced competitors, regulatory headwinds, UX complexity, and loss of cultural cache—creates a situation where user retention is genuinely difficult. Three million fewer daily active users isn't a number to dismiss. It's a symptom of a platform struggling to hold onto its most valuable market segments against better-capitalized competition.

The Advertising Business Under Pressure: Why Q1 Will Be Tougher

Snap's forward guidance was sobering. The company told analysts that Q1 revenue will come in below expectations because of intensifying advertising competition from Meta and TikTok. This is important context for understanding Snap's actual financial situation versus what the Q4 numbers might suggest on the surface.

Advertising revenue for social platforms is supposed to be a steady, predictable business. Users are on the platform, advertisers want to reach those users, the platform offers ad inventory, advertisers pay for placements. The model hasn't changed since Google and Facebook perfected it in the 2000s and 2010s. But in 2025, advertising is getting dramatically harder for anybody who's not Meta or Google (which commands search advertising). Here's why.

First, the iOS privacy changes that Apple rolled out in 2020-2021 are still causing headaches for platforms that depend on targeting precision. Apple limited third-party tracking, which made it harder for advertisers to understand which ads drive conversions. This hit Facebook hard in 2021, and the company has spent years rebuilding its ad targeting using first-party data and machine learning instead of individual-level tracking data. Snap took the same hit but had fewer resources to invest in rebuilding. The company's ad targeting capabilities are legitimately worse than they used to be relative to what advertisers expect.

Second, the global advertising market has shifted. Advertisers are increasingly consolidated around a small number of mega-platforms. Meta has the users and the data. Google has search. Amazon has commerce. TikTok has engagement and content velocity. Snap has... Snap. When a CMO is allocating a marketing budget, they're not thinking "let's split ad spend across Snap, Meta, and TikTok equally." They're thinking "TikTok and Meta are the essentials, Google is mandatory for search, and then we've got discretionary budget left over for other platforms." Snap has become the "other platforms" category.

Third, TikTok's growth in the US and Western markets has been the biggest disruption to the advertising business in years. TikTok's algorithm is uncanny at finding the right content for the right users. The platform is engaging. That engagement translates to attention. Advertisers follow attention. So ad budgets that might have gone to Snap or Instagram Stories a few years ago are going to TikTok instead. This is a zero-sum game, and Snap is losing.

Snap's advertising product has improved over the years. The company's built out tools for conversion tracking, audience targeting, and measurement that are respectable. But respectable isn't good enough when you're competing against Meta (which has Facebook, Instagram, WhatsApp, and Messenger all feeding data into a unified advertising network) and TikTok (which has the algorithm and the engagement).

The company's own data backs this up. Snapchatters (the company's term for the media kit) show that advertisers are still interested in Snap as a channel, particularly for reaching younger demographics. But interest isn't translating to budget growth. Advertising revenue is up 10% year-over-year, but when you control for inflation, that's basically flat. The company's advertising business is stagnant.

That's why Snap's forward guidance warning is actually the most important piece of information in the entire earnings report. The company is telling analysts and investors that the advertising headwinds are getting worse, not better. Q1 will be below expectations. This suggests that advertising revenue growth is decelerating further as we move into 2025. At some point, advertising revenue becomes flat or declines. When that happens, Snap's entire financial model breaks unless the diversification efforts (Snap+, hardware, other monetization) can pick up the slack.

This is why Snap's hardware bet is so aggressive. The company literally can't rely on advertising growth anymore. It's got to find other sources of revenue or face a shrinking business.

Snap's Q4 revenue grew by 10%, but daily active users decreased by 3 million. Snap+ showed strong growth with a 71% increase in subscribers.

Snap+ as a Revenue Engine: What 24 Million Subscribers Actually Tells Us

Let's zoom in on Snap+ because it's genuinely the brightest part of this earnings report and it reveals something important about how social platforms can evolve their business models.

Snap+ launched in 2022 as a simple paid tier. For roughly $3.99 per month (pricing varies by region), users get:

- The ability to see who viewed their Story

- The ability to see who screenshot their Snaps

- Custom app icons for their profile

- Custom emoji reactions in chat

- The ability to prioritize specific friends at the top of their chat list

- Early access to new features

- Replay on the Stories page (letting you watch Stories again)

- Ability to change your username multiple times

It's not revolutionary. These are quality-of-life features that power users want. They're not essential. They're not transformative. But they're valuable enough to premium users that 24 million of them are willing to pay for the privilege.

Now think about what 24 million subscribers means financially. At roughly

The math here is why Snap+ matters so much strategically. Advertising revenue is competitive and commodified. If you're not Meta or Google, you're always going to lose to bigger competitors with better data and more resources. But subscription revenue is different. Subscription revenue is based on perceived value to individual users, not on attention commodity pricing. Meta's 3 billion users aren't going to save Meta $1.15 billion in annual revenue by itself, but Snap's 24 million subscribers are generating that much revenue for Snap. The per-user value of a Snap+ subscriber is orders of magnitude higher than the per-user value of an advertising impression.

Snap's been watching how other platforms have struggled to monetize subscriptions. Twitter tried Twitter Blue and initially bungled it before recovering. Facebook has been experimenting with a subscription tier. Discord makes most of its money from Nitro subscriptions. Twitch has channel subscriptions. What Snap figured out is that you don't need to make the subscription tier feel like a paywall that restricts core functionality. You charge for convenience, for status signals, for exclusive features that are nice to have but not essential. That's worked in Snap's case.

The bigger question is whether Snap+ can keep growing at 71% year-over-year. That's growth on top of growth on top of growth. At some point, the addressable market for people willing to pay for Snap+ maxes out. There are only 474 million daily active users. If 5% of them are Snap+ subscribers, that's roughly 24 million. If 10% become Snap+ subscribers, that's 47 million. At 15%, you're at 71 million. Those are the kind of penetration rates that would suggest the subscription effort had reached saturation.

Snap probably doesn't need Snap+ to reach those penetration rates to succeed. If it can hold subscribers in the 30-50 million range (which would be 6-10% penetration) and keep growing at double-digit rates annually (even if not the massive 71% we're seeing right now), that's a $2-3 billion annual revenue stream that's relatively stable and predictable. That changes Snap's financial profile fundamentally.

The real question is whether the company can use Snap+ as a testing ground for other subscription offerings. What if Snap+ got redesigned as a tiered system? What if there was a $9.99 tier with even more premium features? What if Snap developed subscription offerings for content creators? These are the kind of experiments that could unlock multiples of the current subscription revenue.

Beyond Snap+: The Broader Monetization Experiment

Snap+ isn't the only non-advertising revenue Snap's pursuing. The company's also been experimenting with charging for Memories storage, and CEO Evan Spiegel hinted at more monetization experiments coming.

Memories storage is particularly interesting as a case study. For years, Snap let users save their Snaps to Memories storage for free. This was a feature that encouraged people to take more Snaps (because they knew they could save them) and to stay engaged with the platform. It was a user retention feature that indirectly supported the advertising business by making users more invested in Snap.

Now Snap's charging for expanded Memories storage. The economics here are interesting. Snapchat stores billions of photos and videos. Storage infrastructure costs money—you need to pay for servers, for bandwidth, for data redundancy. As the user base takes more photos and videos, storage costs rise. At some point, it makes sense to pass some of those costs to users. Snap's done that.

This is a textbook example of finding monetization opportunities in existing infrastructure. The storage costs were always there. Snap was just eating the cost. Now it's asking users to pay for storage beyond a certain amount. Some users will, some won't. The ones who do represent additional revenue that wasn't there before.

The company also mentioned Creator Fund payments and other ways it's monetizing for creators. Snapchat has always had smaller creators on the platform, but it's never been a destination for creator-driven monetization the way YouTube or TikTok are. Snap's probably always going to lag YouTube and TikTok in creator monetization because the platform's smaller and less oriented around discovery. But even being third or fourth in the creator monetization space can generate meaningful revenue.

What all of this reveals is that Snap's leadership understands the fundamental problem: advertising revenue is under pressure, and it's not coming back at historical growth rates. So the company's attacking the diversification challenge aggressively. Some experiments will work (Snap+ is working). Some will fail (some future monetization experiment will probably generate minimal revenue and get shut down). But the overall strategy is sound: if you can't grow advertising revenue, grow other revenue streams.

Despite a decline in user base, Snap's projected revenue grows from

The Competitive Landscape: Snap Gets Squeezed From All Sides

Snap doesn't compete in a vacuum. It competes in an ecosystem dominated by Meta (3 billion users across Instagram, Facebook, WhatsApp, Messenger) and increasingly pressured by TikTok (1.5+ billion monthly active users). Understanding Snap's challenges means understanding the competitive environment it's operating in.

Meta is the 800-pound gorilla. The company has so much user data, so much capital, and so much engineering talent that it can basically feature-parity any successful competing product almost immediately. When Snapchat invented Stories, Instagram copied Stories in weeks. When Snapchat focused on ephemeral messaging, Facebook built disappearing message features into Messenger. When Snapchat invested heavily in AR filters, Instagram built better AR filters. Meta doesn't innovate faster than Snap, necessarily, but it has the resources to match Snap feature-for-feature and then leverage its larger user base to make the feature more successful.

Meta also has the advertising business locked up. Facebook and Instagram are the default advertising channels for most companies. They have the most comprehensive targeting options, the most user data, the best ROI tracking, the deepest integrations with commerce platforms. If you're a small business or a large advertiser, you're spending money on Meta. Snap is competing for budget that might otherwise go there, and it's almost always going to lose that competition because Meta's value proposition is stronger.

TikTok is different. TikTok competes on engagement and cultural relevance, not on database size or advertising sophistication. TikTok's algorithm is better at finding the right content for the right person. TikTok's platform is more entertaining. TikTok's where young people are increasingly spending their time. This is where Snap bleeds users. Teenagers and young adults are choosing TikTok over Snapchat because TikTok is more fun, more engaging, and more culturally relevant.

Snap's response has been to focus on what it does best: real-time messaging and camera-first communication. The company invested in Spotlight (its TikTok competitor) but never really committed to making it work. It focused on AR and filters, areas where Snap actually has some differentiation. It's investing in hardware. These are smart moves, but they're also essentially "dance in your lane and hope your competitors don't get better at what you do." That's a strategy for niche success, not market dominance.

The truth is Snap's in a squeeze. It's not Meta (doesn't have the advertising dominance or the user base). It's not TikTok (doesn't have the engagement or the algorithm). It's a specialized platform that does real-time social communication well, and those users are increasingly splitting their attention with other apps. Retention is hard. Growth is harder.

This is why the hardware bet is so aggressive. Snap's not going to out-Meta Meta at advertising. It's not going to out-TikTok TikTok at entertainment. But maybe it can differentiate in AR glasses, where nobody has a dominant position yet. Hardware is a way to break out of the competitive squeeze by creating a new category where the existing rules don't apply.

Specs: The $1 Billion Bet on Augmented Reality

This is the real story of Snap's Q4 earnings, even though it's not directly reflected in the Q4 numbers. Snap's betting aggressively on augmented reality hardware. The company just created a new subsidiary called Specs Inc. devoted solely to bringing its long-promised Specs AR glasses to market. This is important enough to discuss in serious detail.

Snap's been talking about AR glasses for years. CEO Evan Spiegel has mentioned AR as the company's "long-term vision" since at least 2018. The company released a prototype called "Spectacles" back in 2019 that was, frankly, a gimmick. It was camera glasses that shot video in Snapchat's native format. They were expensive, clunky, and not useful enough to generate meaningful adoption. Snap sold a few, admitted it was learning hardware was hard, and moved on.

Now, in 2025, Snap's trying again. Specs Inc. is a separate entity focused on developing AR glasses that actually work. The goal, presumably, is to build glasses that overlay digital information and experiences onto the real world through the wearer's vision. Imagine looking at a street and seeing navigation overlays. Imagine looking at a person and seeing contextual information. Imagine sharing experiences with friends through a camera that captures the world the way your eyes see it.

This is not a new idea. Google tried Google Glass in 2013 and failed because the technology wasn't good enough, the price was too high (

So why is Snap betting so aggressively? Partly because Snap needs growth vectors. Partly because AR is genuinely interesting and the tech is getting better. Partly because if AR ever does become mainstream, Snap wants to be in the game. Partly because creating a separate subsidiary gives the hardware effort focus and allows it to operate under different business model assumptions than the core Snapchat business (which is, right now, an advertising business competing in a brutal market).

But here's the thing: AR glasses are hard. The technical challenges are brutal. You need a display that's high-resolution and power-efficient. You need processing power that doesn't drain a battery in two hours. You need software that actually works and actually uses AR in ways people care about. You need to solve the social acceptance problem (are glasses with built-in cameras creepy? Most people think so). You need to figure out the business model (are AR glasses a subscription service? Do they have ads? Do they cost

Snap's probably investing

The upside, if it works, is potentially transformative. If Snap can build AR glasses that people actually want to wear, that actually offer a useful augmented reality experience, and that work as a platform for social communication, then the company has created a new computing interface. That's how you become a $100+ billion company. That's how you break out of the squeeze from Meta and TikTok. AR glasses connected to Snap's social network would be powerful in ways the iPhone never was.

But the downside is also brutal. If Snap ships AR glasses and they're clunky, or expensive, or don't work, or nobody wants them, then the company has burned $1 billion on a failed product. That's not survivable for a company with Snap's market cap and cash flow. It would force a strategic pivot, probably selling off parts of the company or getting acquired.

Snap's CEO Evan Spiegel acknowledged this in the earnings call. He said the company is "so close to launch" and that the "key here is really just nailing the launch and making sure that we deliver an extraordinary product." He also said the company has "a lot of flexibility to think about how we want to capitalize on it moving forward," which is CEO-speak for "we're still figuring out the business model."

The fact that Snap created a separate subsidiary for Specs is interesting. It suggests the company wants to give hardware a separate identity from Snapchat proper. This makes sense—Snapchat users might not be interested in AR glasses. Hardware might appeal to a "different audience segment" than the core Snapchat audience, as Spiegel put it. By creating a separate Specs Inc., the company can develop hardware without confusing the core social messaging app. It's a sensible organizational structure for a bifurcated business.

But organizationally separating the businesses doesn't reduce the fundamental risk. Snap is betting big on a hardware category that's never achieved mainstream adoption. The company's got maybe 2-3 years to ship a compelling product before investor patience runs out. That's aggressive, but it's also necessary. In the time it takes to ship a good AR glasses product, competitors (particularly Meta, which has infinite resources for this kind of thing) will be shipping their own versions.

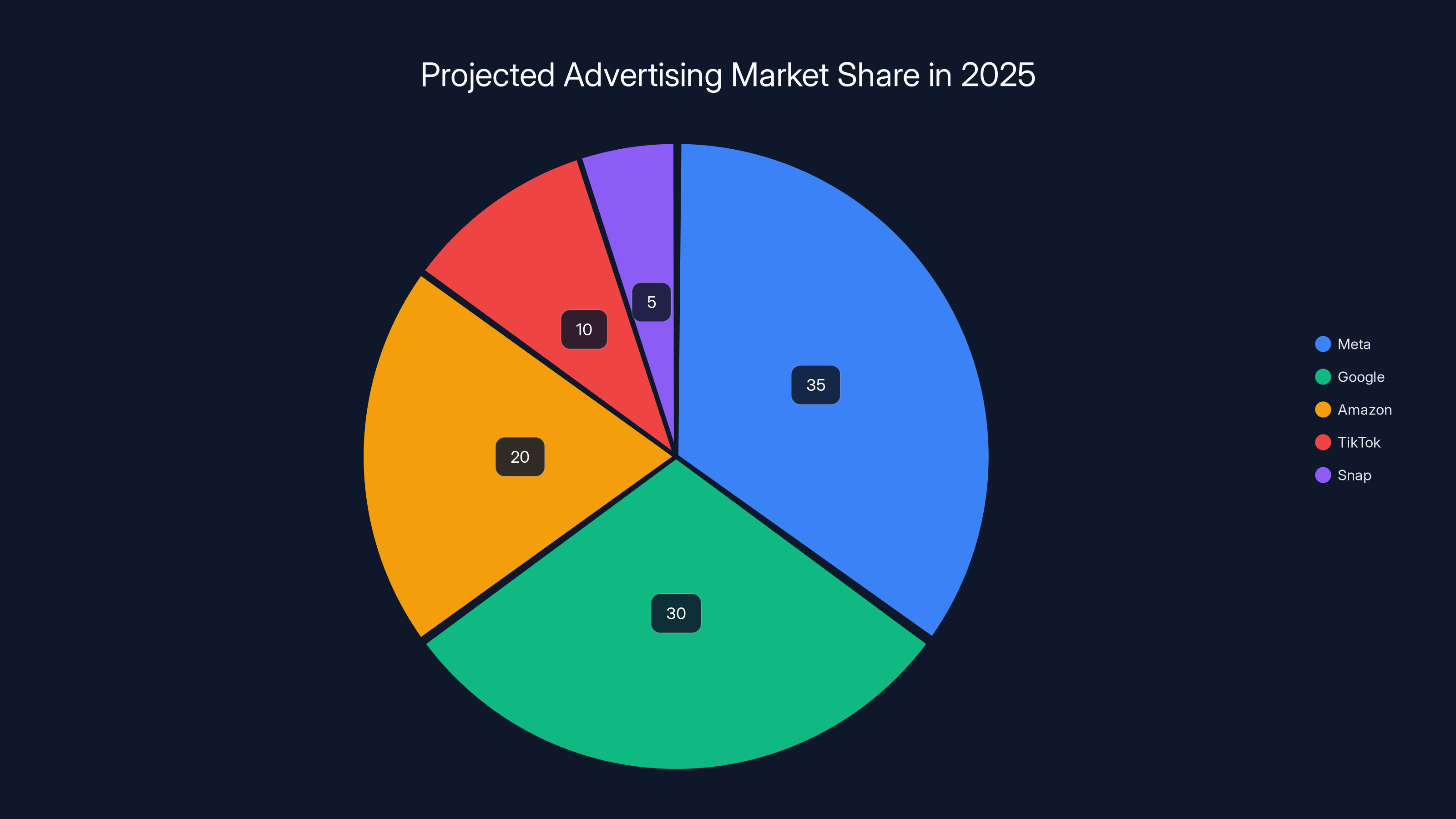

Estimated data suggests that by 2025, Meta and Google will dominate the advertising market, leaving Snap with a smaller share. Estimated data.

The Revenue Per User Play: Squeezing More Value From a Shrinking Base

Average revenue per user grew from

Here's how this works: Snap's got 474 million daily active users. It's monetizing those users through advertising, Snap+, Memories storage, and other channels. The company manages to extract an average of $3.62 per user per quarter. That's the definition of ARPU (average revenue per user).

When a platform's user base is declining but ARPU is growing, it usually means one of two things:

First, the company is extracting more value from its premium user base. If Snap's user base is declining overall but declining faster among low-value users (like teenagers in developing countries) and maintaining better in high-value users (like professionals in North America), then ARPU will naturally go up. That's what's probably happening with Snap—it's losing users in low-value markets while trying to hold onto high-value users. The problem is, it's losing users in high-value markets too, so the ARPU growth is masking deeper problems.

Second, the company is successfully monetizing at higher rates. More users adopting Snap+, more users paying for Memories storage, advertisers paying more per impression. This is actually happening for Snap too—Snap+ growth is accelerating, which means premium users are becoming a larger percentage of the total user base.

But here's the critical limitation: ARPU growth can only offset user losses for so long. Let's do the math.

If Snap has 474 million users and

- Users: 474M - (4 × 1M) = 470M

- ARPU: 4.41

- Revenue: 470M × 2.07B

That's nice growth. But the math breaks down if user losses accelerate. If Snap loses 2 million users per quarter:

- Users: 474M - (4 × 2M) = 466M

- ARPU: $4.41 (same as above)

- Revenue: 466M × 2.05B

At a certain point, losing users faster than ARPU is growing means revenue starts declining. And eventually, if ARPU keeps growing while users keep declining, you hit a point where you're maximizing revenue from a dying user base—you're extracting every dollar possible from a shrinking number of people. That's a slow-motion business decline.

Snap needs to actually stabilize or grow its user base. ARPU growth is helpful, but it's not a substitute for user growth. The company knows this, which is why it's investing in hardware, why it's experimenting with monetization, why it's trying to compete with TikTok and Instagram to hold onto its user base.

User Growth in International Markets: The Only Bright Spot

Snap's user losses were concentrated in North America and Europe. Everywhere else, the company actually grew users "slightly," according to the company's earnings report. This is important context because it reveals where the company actually has momentum.

International markets represent growth, but lower monetization per user. A user in India or Brazil or Southeast Asia is worth significantly less advertising revenue than a user in the United States or Western Europe. This is why tech companies obsess over user growth in developed markets—the economics are simply better.

But growth is growth. If Snap can stabilize North America and Europe (or better yet, grow there) while continuing to expand internationally, it could return to a positive growth trajectory. This is the path forward for a lot of mature social platforms. You can't grow in developed markets forever (penetration eventually maxes out), but you can grow in developing markets for years.

Snap's probably aware that it needs to make international markets more valuable. That might mean improving monetization (developing more sophisticated local advertising markets, for example), or it might mean building features that are specifically valuable to international users. The company's relatively small size compared to Meta might actually be an advantage here—it can be more nimble about building for local markets, rather than trying to apply a one-size-fits-all approach.

The fact that Snap is still growing users internationally while declining in the West suggests the platform has some appeal to users globally, even if it's losing engagement war in its core markets. That's worth paying attention to.

Snap's Q4 shows a paradox: while revenue and Snap+ subscriptions grew significantly, daily active users declined by 0.63%, highlighting a strategic challenge.

Forward Guidance and the Q1 Worry: Why Snap's Own Forecast Matters More Than Q4 Results

Maybe the most important information in Snap's entire earnings report isn't in the Q4 numbers—it's in what the company said about Q1. Snap told analysts that Q1 revenue will come in below expectations. This is significant because it's the company essentially saying "things are getting harder, not easier."

Why does forward guidance matter more than current quarter results? Because forward guidance is management's best estimate of whether business conditions are improving or deteriorating. If Snap was confident that growth would continue, it would guide to growth. Snap's guiding to below-expectations growth, which means management believes competitive pressure is intensifying or that advertising market conditions are softening.

Advertising revenue is the lifeblood of Snap's business. If advertising growth is decelerating or turning negative, then Snap's entire financial model is in trouble. Snap+ and other monetization efforts can help offset declining advertising revenue, but they can only go so far. The company needs to keep advertising growing or at least flat.

Snap's guide of "below expectations" growth suggests that advertising is decelerating. The company attributed this to "competition from Facebook, Instagram, and TikTok," which is basically admitting that Meta and TikTok are winning the advertising market share battle. That's not shocking given the competitive dynamics we discussed earlier, but it's a formal acknowledgment that the pressure is real and intensifying.

This forward guidance is the real story of the earnings report. Everything else—the Q4 revenue growth, the ARPU increase, the Snap+ subscriber growth—is positive. But the forward guidance is telling investors that the company sees deteriorating market conditions ahead. That's why Snap's stock would probably trade relatively flat or down after these earnings despite the positive Q4 numbers.

Investors have learned to trust forward guidance more than historical results. A company with great Q4 numbers but weak forward guidance is not a company you want to own. Snap's essentially signaling that it thinks Q1 will be difficult and that it's bracing for further challenges. Whether that turns out to be true will matter more than what happened in Q4.

The Strategic Picture: Diversification or Desperation?

Snap's earnings report reveals a company at a strategic inflection point. The company is successfully diversifying away from pure advertising revenue. Snap+ is growing fast. The company's profitable. Cash flow is positive. By normal standards, this would be considered a healthy, growing business.

But the context matters. Snap's diversification effort isn't happening because the company has solved the social media competitive puzzle. It's happening because Snap knows it can't out-advertise Meta and it can't out-entertain TikTok. Diversification is Snap's way of playing a different game.

Is this a good strategy? Probably yes, in the long run. Building subscription revenue, developing hardware, monetizing creator communities—these are all valuable revenue streams that have lower risk and higher margins than pure advertising. Over time, a more diversified Snap would be a more resilient Snap.

But "long run" is the operative phrase. In the near term, Snap's still depends on advertising revenue. And if advertising is decelerating (which the company's forward guidance suggests), then near-term financial performance could suffer even as the company's long-term strategy is sound. This is the uncomfortable position Snap's in.

The company needs to:

-

Stabilize advertising revenue - This means competing more effectively with Meta and TikTok, which is hard. But at minimum, Snap needs to stop the deceleration.

-

Maintain user growth - The company needs to stop losing users in premium markets like North America. This is critical because all the ARPU growth in the world doesn't matter if the user base is shrinking.

-

Execute the hardware bet - Specs needs to ship a compelling product. If it doesn't, the entire strategic pivot looks like it was built on wishful thinking.

-

Keep diversification moving - Snap+ needs to keep growing, new monetization experiments need to find traction, and the creator ecosystem needs to develop.

This is a lot to execute simultaneously. Most companies that try to fix everything at once end up fixing nothing. Snap's got resources and talent, but it's also operating in an incredibly competitive environment with limited margin for error.

What This Means for Snap's Competitors and the Broader Market

Snap's earnings report is a useful lens for understanding the state of social media competition in 2025. Here's what it tells us:

First, advertising-based social media is a consolidating market. Meta and TikTok are winning. Everyone else is struggling. This is the natural result of network effects and the winner-take-most dynamics of social platforms. Snap's one of the few remaining alternatives, but even Snap is struggling to compete.

Second, diversification is becoming essential. Platforms that depend on a single revenue stream are vulnerable. Snap's figuring this out. Twitter learned it the hard way. Pinterest has Ads and commerce and now it's experimenting with search. YouTube has ads and memberships and Super Chat. The era of the single-revenue-stream social platform is ending.

Third, hardware is a potential escape route from the social media competition squeeze. If AR glasses or other hardware form factors take off, they could reset the competitive landscape. Companies like Snap, Meta, Apple, and others are betting on this. The winner of the hardware game could reshape social media competition for the next decade. Snap's betting big on this possibility.

Fourth, user retention is the hardest competitive challenge. Growing your user base in a mature market with strong competitors is nearly impossible. Snap's learned this. So has everyone else. The way to win in mature markets is to keep your existing users engaged and to find ways to make money from them without driving them away. This is an incredibly hard game to play, which is why Meta spends so much money on R&D and why platforms keep adding features and experimenting with new monetization.

Snap's earnings report is essentially a case study in how social media companies compete in 2025: diversify revenue, keep users engaged, bet on new hardware and interfaces, accept that advertising growth is slowing, and hope that some of your big strategic bets hit. It's a reasonable strategy. Whether it works remains to be seen.

The Infrastructure Investment Required: Building for Hardware and Growth

What's not always obvious in earnings reports is the infrastructure investment required to support platform ambitions. Snap's betting on hardware, developing new monetization options, and trying to maintain and grow its user base. All of this requires infrastructure investment at scale.

Snap+ requires payment processing infrastructure that works globally, anti-fraud systems, customer support for billing issues, analytics to understand which users are converting to subscriptions. Memories storage requires more cloud infrastructure, more bandwidth, more redundancy. AR filters require more computing resources to process on-device or in the cloud. Hardware development requires physical manufacturing infrastructure, supply chain management, logistics, warranty support. Content moderation at Snap's scale requires AI systems, human moderators, legal expertise, and compliance infrastructure.

All of this costs money. Some of it shows up on the balance sheet as capital expenditures. Some of it shows up as opex. But it's all required to support the business.

Snap's Q4 profitability suggests the company has efficiently managed its infrastructure costs. But as the company invests in hardware and expands monetization, infrastructure costs are probably going to increase. The question is whether revenue grows faster than infrastructure costs. Based on forward guidance, Snap doesn't think advertising revenue will grow fast enough. This might be why the company's pushing so hard on Snap+ and other non-advertising revenue—these revenue streams might have better unit economics than advertising.

Looking Ahead: Q1 2025 and Beyond

Snap's Q1 outlook is sobering, but it's also an opportunity. If the company misses guidance, the stock probably sells off. If it beats guidance, the stock probably jumps. Either way, Q1 will be a test of whether the company's diversification strategy is actually working or whether it's just a distraction from a declining core business.

The real test for Snap in 2025 is execution on hardware. Specs needs to launch. It needs to work. It needs to be something people actually want to use. If that happens, Snap's probably fine long-term. If it doesn't, Snap's facing some hard strategic choices about whether to shut down the hardware effort and focus on defending its core messaging business, or whether to get acquired by someone with more resources (Meta or Microsoft probably).

The intermediate test is whether Snap can stabilize its user base. Losing users in North America and Europe is a warning sign. If that trend continues into Q1 and Q2, then the company's core competitive position is deteriorating. Snap can't afford to become a declining platform that's slowly losing relevance. It needs to either stabilize or grow users.

The optimistic case for Snap is that the company successfully executes the diversification strategy, Specs becomes a meaningful hardware product, Snap+ continues growing, and the platform remains relevant to hundreds of millions of users. In that scenario, Snap becomes a smaller but more resilient company with lower exposure to advertising competition.

The pessimistic case is that advertising decelerates faster than Snap's expecting, user losses accelerate, Specs launches and disappoints, and Snap becomes a slow-growth company fighting for survival in an industry dominated by much better-resourced competitors. In that scenario, Snap gets acquired or restructured within 2-3 years.

The realistic case is probably somewhere in the middle. Snap probably stabilizes user losses, Snap+ probably keeps growing at reasonable rates, Specs probably launches something decent but not transformative, and the company remains competitive but smaller and less culturally dominant than it was 3-4 years ago. That's not a disaster, but it's also not the moonshot Snap's probably hoping for.

The Broader Story: What Snap's Earnings Tell Us About Social Media in 2025

Zoom out from the specific numbers and Snap's earnings reveal a lot about the state of social media competition in 2025.

First, platforms that built their entire business on advertising are facing structural challenges. Advertising growth is slowing across the industry. Privacy regulations are limiting targeting capabilities. Competition from better-resourced competitors is intensifying. Platforms like Snap, Twitter, Pinterest, and others built in an era when advertising was the obvious monetization strategy. In 2025, that's proving increasingly insufficient.

Second, user growth in mature markets has essentially stopped. Everyone who wants a smartphone has one. Everyone who wants a social media account has multiple. The days of 30% year-over-year user growth for established platforms are over. Now it's about retention, reactivation, and finding pockets of growth in specific geographies or demographics.

Third, differentiation is everything. Platforms that offer something unique (TikTok's algorithm, Discord's communities, Twitch's streaming) have a path forward. Platforms that are just "an alternative to Facebook" (which is how most people think about Snapchat, honestly) are struggling. Snap's trying to create differentiation through hardware and through features that Meta hasn't copy-pasted yet. Whether that works remains to be seen.

Fourth, revenue diversification is essential. Advertising alone isn't enough. Subscriptions, hardware, creator monetization, commerce, payments—platforms need multiple revenue streams to reduce risk and to improve unit economics. Snap's doing this. So is everyone else. The question is how quickly each platform can move.

Fifth, capital intensity is increasing. Building hardware is expensive. Building effective AI systems for moderation and content recommendation is expensive. Competing in a world of machine learning and sophisticated algorithms requires talented engineers and substantial R&D budgets. Snap's probably spending more on R&D than ever before. The winners will be the companies that can afford to spend more than their competitors.

Snap's earnings report is a window into all of these dynamics. It's a case study in a platform that's trying to adapt to a fundamentally changed competitive landscape. Whether the adaptation succeeds is an open question. But the attempt is the real story.

FAQ

What was Snap's Q4 revenue growth, and how does it compare to expectations?

Snap reported $1.7 billion in Q4 revenue, representing 10% year-over-year growth. While this might seem solid on the surface, it's actually slower than historical growth rates for the company and came in line with or slightly below analyst expectations. More concerning is the company's forward guidance for Q1, which suggested growth would decelerate further due to advertising competition from Meta and TikTok.

Why did Snap lose daily active users despite growing revenue?

Snap lost 3 million daily active users in Q4, dropping from 477 million to 474 million. This happened primarily in North America and Europe—the company's most valuable markets where advertisers pay the most per impression. The user losses reflect competitive pressure from TikTok (which offers superior entertainment and engagement) and Instagram (which replicates Snapchat's core features at scale). However, Snap grew users slightly in international markets where monetization is lower.

How important is Snap+ to the company's financial future?

Snap+ is critically important and represents a successful proof of concept for diversifying away from pure advertising revenue. The subscription service reached 24 million subscribers with 71% year-over-year growth, generating approximately $1.15 billion in annual gross revenue. More importantly, subscription revenue has better unit economics and predictability than advertising revenue. If Snap+ can reach 50-60 million subscribers while maintaining double-digit growth rates, it would fundamentally transform the company's financial profile and reduce dependence on advertising.

What is Specs, and why is Snap investing so heavily in AR glasses?

Specs is Snap's upcoming augmented reality glasses product, which the company is developing through a new subsidiary called Specs Inc. Snap is investing heavily (likely

What does Snap's forward guidance mean for investors?

Snap's guidance that Q1 revenue would come in below analyst expectations is a critical signal that business conditions are deteriorating, not improving. This suggests that advertising revenue growth is decelerating faster than the company previously expected, likely due to competition from Meta and TikTok. Forward guidance is typically more important than historical results because it reflects management's current assessment of market conditions. Investors who rely on positive Q4 numbers while ignoring weak forward guidance risk being surprised by weaker Q1 results.

How does Snap's monetization per user compare to Meta and TikTok?

Snap's average revenue per user is approximately

Why are international markets important for Snap's future?

While Snap's losing users in its premium markets (North America and Europe), the platform is actually growing users in international markets. International markets represent long-term growth opportunities, even if monetization is currently lower. As Snap improves monetization in emerging markets (through localized advertising products, creator programs, and other features), the company could unlock significant revenue growth. This is how companies like Meta maintain growth despite saturation in developed markets—by expanding monetization in developing countries.

What's the risk that Specs fails or doesn't achieve mainstream adoption?

The risk is substantial. The AR glasses market has a track record of failed products. Google Glass failed. Meta's Ray-Bans have achieved limited adoption. Apple's Vision Pro, despite being a technically impressive product, failed to achieve mainstream adoption despite

How does Snap's strategy compare to Twitter, Pinterest, and other struggling social platforms?

Snap's diversification strategy is actually more advanced than most of its struggling competitors. Twitter tried to diversify through subscriptions (Twitter Blue) but hasn't achieved meaningful traction. Pinterest has subscription features but remains advertising-dependent. Snap's actually executing on multiple diversification vectors simultaneously: subscriptions through Snap+, hardware through Specs, alternative monetization through Memories storage and creator programs. This multi-pronged approach is more likely to succeed than single-vector strategies. However, Snap still faces the fundamental challenge that its core business is advertising, and advertising is the hardest revenue stream to grow in 2025.

Conclusion: Snap at a Crossroads

Snap's Q4 earnings report paints a picture of a company that's executing reasonably well tactically but struggling strategically. Revenue is growing, profit is positive, Snap+ is thriving, and the company has cash to invest in the future. By many measures, this is a healthy business.

But the context tells a different story. User growth is negative in the markets that matter. Advertising revenue is decelerating. The company's warning that Q1 will be tougher than expected. The only way for Snap to achieve its ambitions is to execute flawlessly on three major initiatives: stabilize the user base, keep Snap+ growing, and ship a compelling hardware product with Specs.

That's a lot of execution risk for a company competing against Meta (infinite resources) and TikTok (cultural momentum and engagement superiority). Snap's probably aware of this. That's why the company's making big bets instead of trying to incrementally improve the status quo.

The next 12-18 months will determine whether Snap's strategy works. If Specs ships and resonates, if Snap+ reaches 50+ million subscribers, if user losses stabilize, then Snap probably survives as an independent company and possibly even thrives. If any of those things don't happen, Snap's probably facing acquisition or restructuring.

For now, Snap's Q4 earnings show a company that's moving in the right direction on some metrics while losing ground on others. It's profitable. It's growing revenue. It's investing in the future. But the future of social media is being written by companies with more resources, more users, and stronger competitive positions. Snap's trying to write its own future through diversification and hardware. Whether that works is the most interesting question in social media in 2025.

Key Takeaways

- Snap achieved 45M net income, but daily active users declined to 474M from 477M, with losses concentrated in premium markets like North America and Europe.

- Snap+ subscriptions reached 24 million with 71% year-over-year growth, generating approximately $1.15 billion annually and proving the diversification strategy is gaining traction.

- Average revenue per user grew 5% to $3.62, but this ARPU growth is masking deeper engagement problems as the company loses users in its most valuable markets.

- Forward guidance warning that Q1 revenue will miss expectations reveals that advertising growth is decelerating due to competition from Meta and TikTok.

- Snap's 1B hardware bet on Specs AR glasses represents a high-risk strategic pivot away from advertising dependence, with success dependent on product execution and market adoption.