![SpaceX's IPO and the Secondary Market Boom [2025]](https://tryrunable.com/blog/spacex-s-ipo-and-the-secondary-market-boom-2025/image-1-1769803748963.jpg)

Space X's IPO and the Secondary Market Boom: What It Means for Private Markets in 2025

Introduction: The IPO Drought and What Comes Next

Last month, Space X reportedly began talks with four major Wall Street banks about a potential 2025 IPO. For a company that's been private for over two decades, this single conversation sent shockwaves through the financial world. But here's the thing that nobody's talking about enough: the most interesting story isn't the IPO itself. It's what's been happening in the years leading up to it.

Since 2021, the IPO market effectively froze. The glamorous public debut, once the ultimate achievement for any tech company, became something founders actively avoided. Companies stayed private longer. They raised bigger rounds. They built empires in the shadows of public scrutiny. And while they waited for the right moment, something unexpected happened: a thriving secondary market exploded into existence.

Think of secondary markets as a hidden economy. While the general public has no access to private company shares, sophisticated investors have quietly spent the last few years buying and selling stakes in the most valuable private companies on Earth. Space X shares traded at valuations that swung between

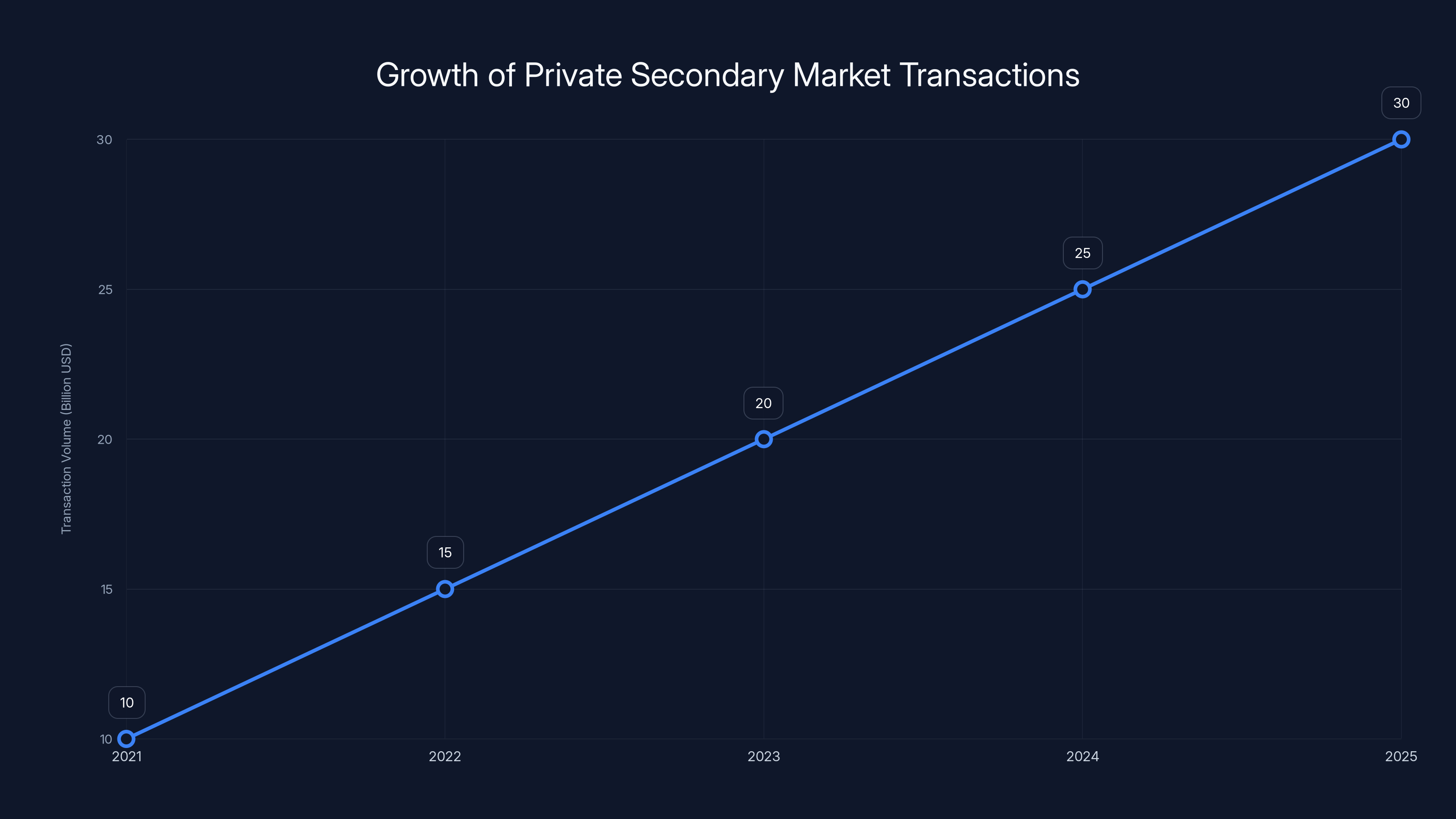

This isn't small-time activity. Venture capitalists, hedge funds, sovereign wealth funds, and private equity firms have collectively deployed tens of billions into secondary transactions for pre-IPO companies. The market moved $20+ billion in private secondary deals in 2023 alone, and that number keeps growing. Companies are staying private so long that the private markets are now housing more total market cap than the public stock exchanges could absorb in a single year.

What's driving this shift? Why would a legendary founder like Elon Musk, who spent years saying he'd never take Space X public until rockets launched to Mars regularly, suddenly change his mind? And what does this mean for employees, early investors, and the future of how we fund innovation?

The answer sits at the intersection of market constraints, regulatory shifts, and a fundamental reshaping of who gets access to high-growth companies before they go public. This is the story of how private markets are eating the IPO process from the inside.

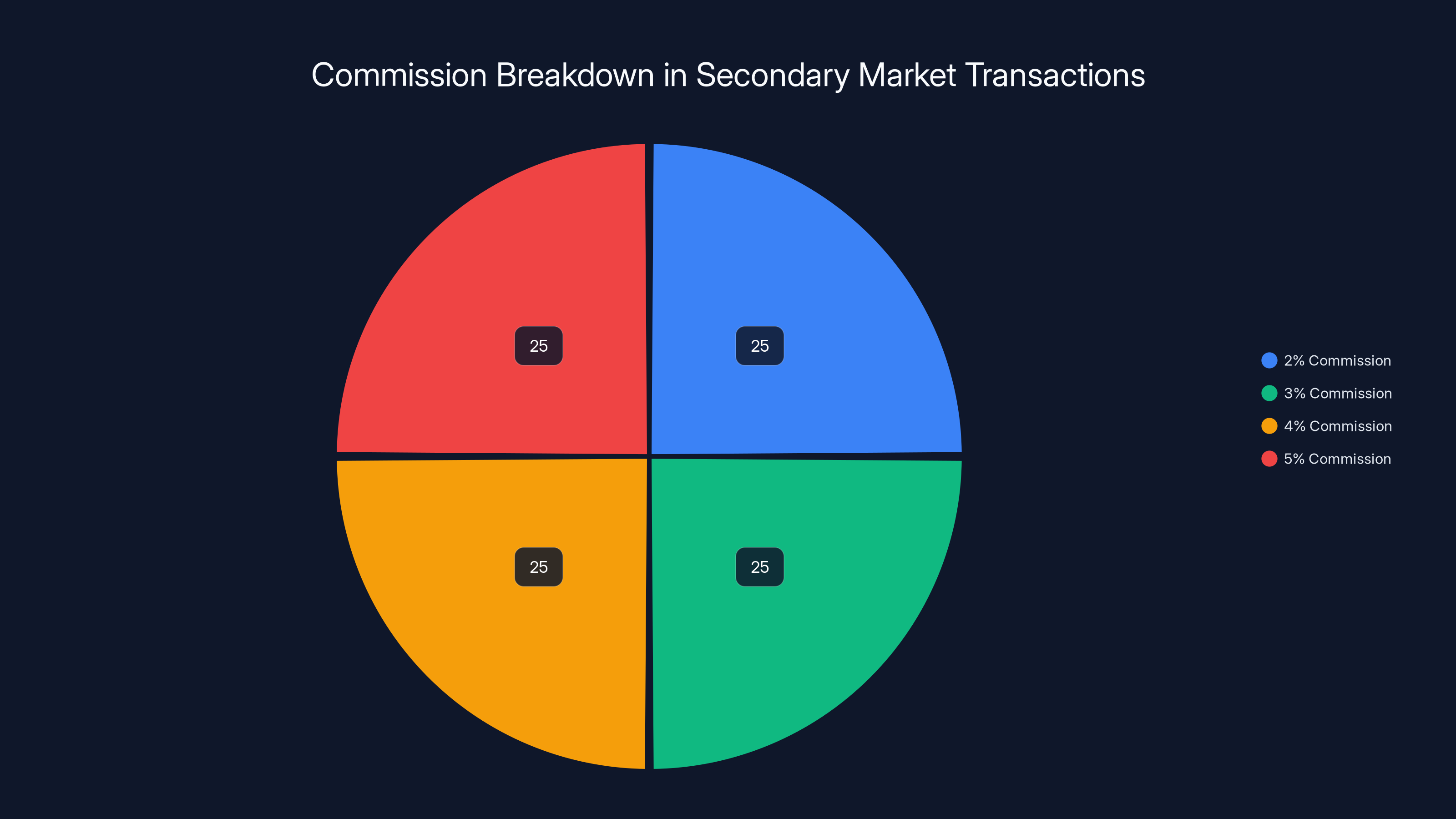

Broker-dealers in private share sales typically charge a commission between 2% and 5% of the transaction value, with each rate equally common. Estimated data.

TL; DR

- Secondary markets have become the new liquidity engine: Pre-IPO companies now trade billions in secondary shares annually, creating liquidity without going public

- Space X's $800B+ valuation signals IPO momentum: When mega-cap privates start trading up, it often precedes a broader market reopening for debuts

- Private market cap now exceeds public market absorption capacity: The shift to later-stage funding rounds means late-stage companies stay private 3-5 years longer than historical precedent

- Employees and early investors see secondary rounds as primary exits: Tender offers and secondary sales have become the new path to liquidity before any IPO

- A single Space X IPO could trigger a cascade effect: Once the bellwether company goes public, investor appetite for other pre-IPO companies typically intensifies rather than disappears

Part 1: Understanding the IPO Drought and Why It Happened

The 2021 IPO Boom and the Sudden Halt

To understand today's private market dynamics, you need to rewind to 2021. That year was absolutely insane for IPOs. Companies debuted at ridiculous valuations. Robinhood went public. Coinbase went public. Rivian went public at an $66 billion valuation before it had ever made a single car. The IPO window was wide open, and every founder wanted to run through it.

Then 2022 arrived, and the door slammed shut. The Federal Reserve started hiking interest rates to fight inflation. Growth stocks got decimated. The Nasdaq dropped 33%. Suddenly, companies trading at 40x revenue didn't make sense anymore. IPO underwriting became a nightmare. Deals that were supposed to close by September got delayed to October, then November, then "we'll call you next year."

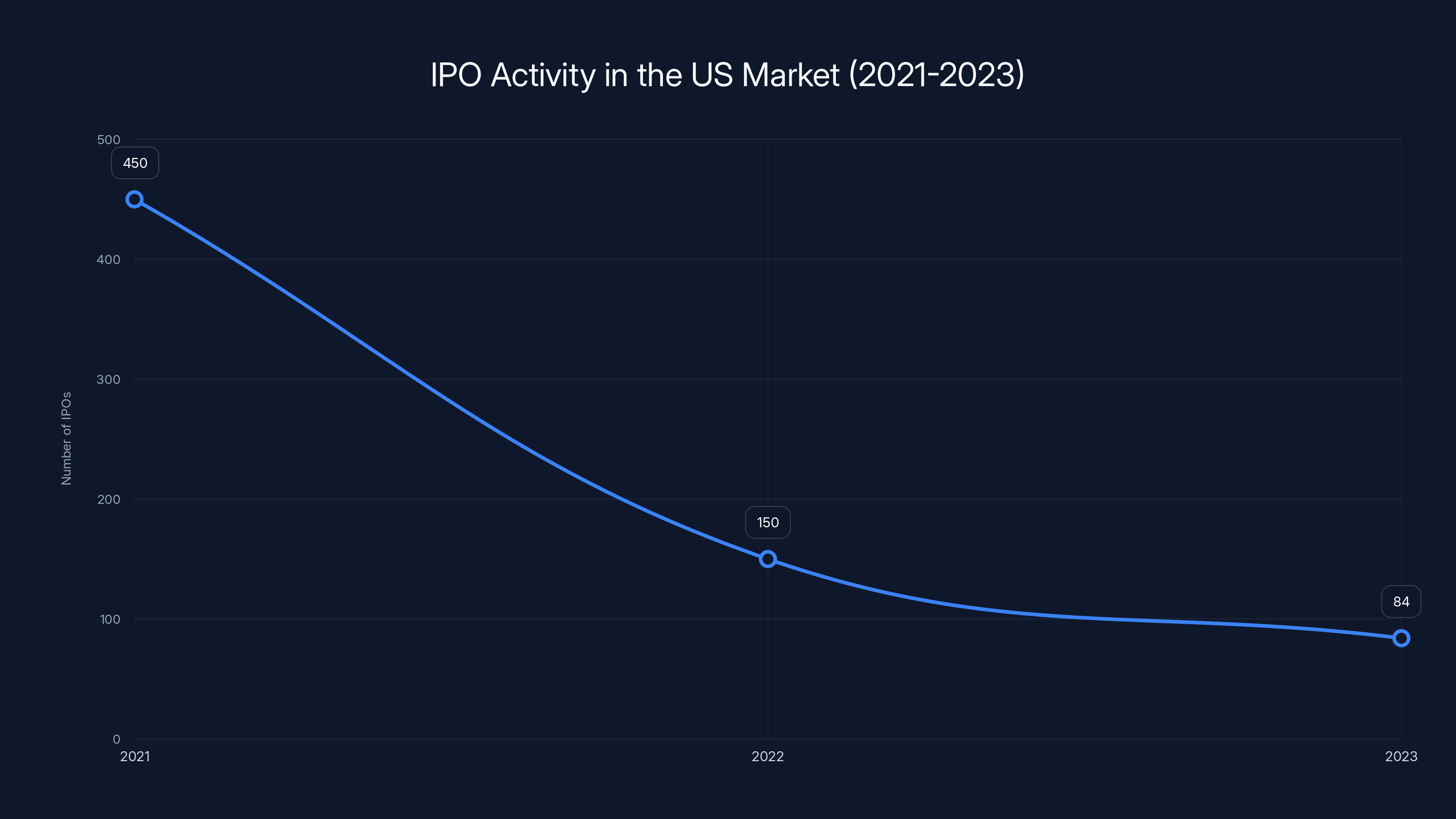

By 2023, the IPO market wasn't just slow. It was dead. Only 84 IPOs happened in the entire US market that year—the worst performance since 2009. Founders stopped even trying to go public. They raised larger Series D, E, and F rounds instead. Private companies learned they could stay private, avoid the quarterly earnings rat race, and still access capital.

Here's the critical part: while founders were opting out of IPOs, the companies themselves kept growing exponentially. They hit billion-dollar valuations, then

This created a mathematical problem. The stock market could absorb one

The Private Market Responds: Secondary Trading Emerges

Nature abhors a vacuum. When employees, founders, and early investors found themselves unable to sell shares through an IPO, they got creative. If the public markets weren't an option, could they create their own trading marketplace?

The answer was yes, and secondary markets emerged as the solution. These aren't informal side transactions. They're structured, broker-facilitated marketplaces where qualified investors can buy and sell stakes in private companies. The mechanics work like any other stock trade, just with much higher minimums and far fewer participants.

Companies themselves started facilitating these transactions through tender offers. Space X hosted tender rounds at $800 billion. When new investors wanted in, or old investors wanted out, these tenders became the mechanism for price discovery and liquidity. Unlike public stock trading where millions of shares exchange hands daily, private secondaries might involve a few hundred million dollars changing hands once or twice a year.

The participants changed too. Historically, private company shareholders were venture firms, angels, and employees. Secondary markets attracted hedge funds, private equity firms, mutual funds, and sovereign wealth funds. These institutions wanted exposure to high-growth companies but couldn't justify a whole new VC fund just for that. Secondary shares provided a simpler path to direct ownership.

What shocked everyone was the scale. Once you aggregated all these secondary transactions across all the mega-cap private companies, you got to billions of dollars annually. The market wasn't big enough to be called liquid by public market standards, but it was definitely real.

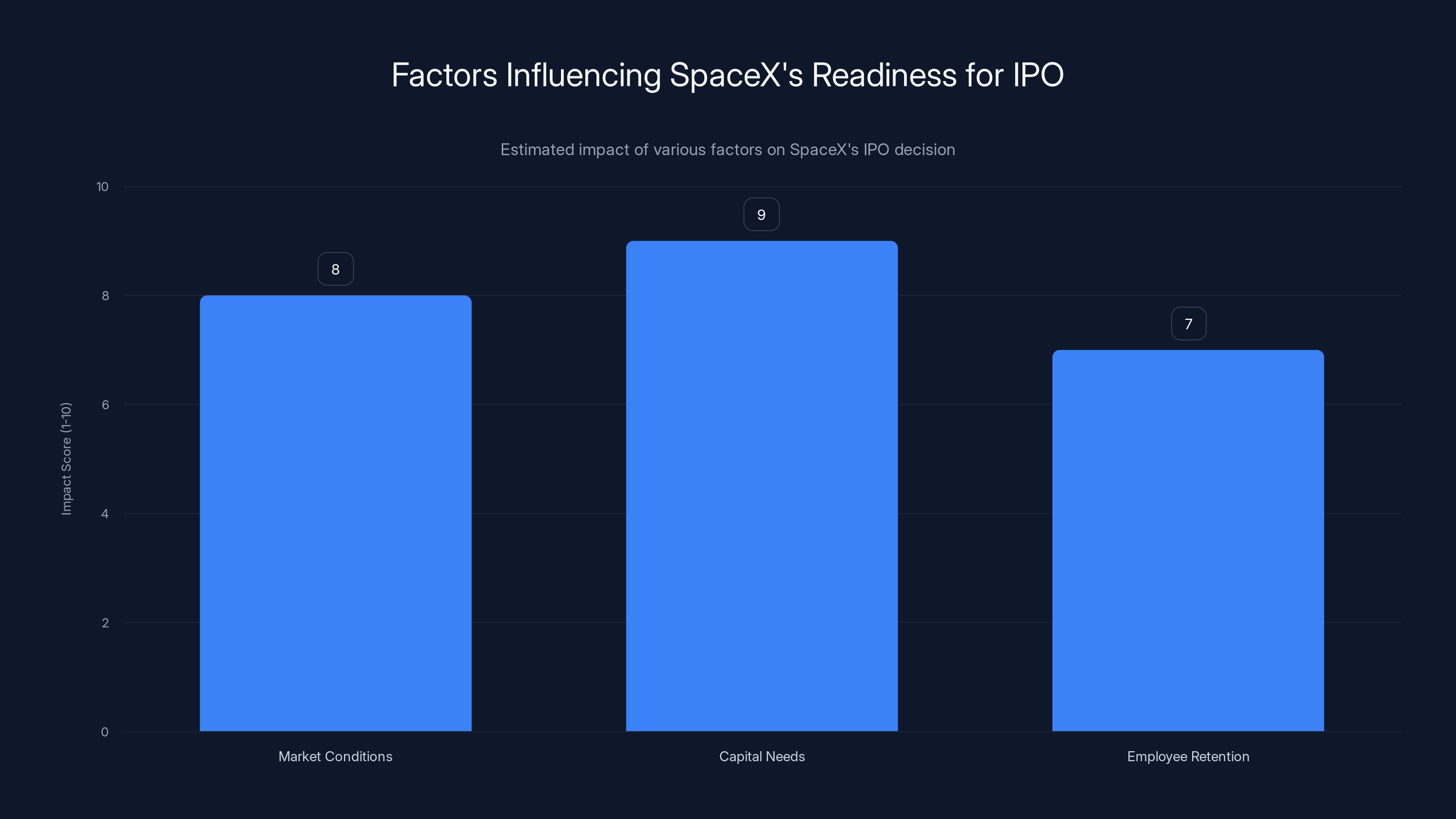

Estimated data: Market conditions, capital needs, and employee retention are key factors influencing SpaceX's decision to consider an IPO, with capital needs having the highest impact.

Part 2: The Mechanics of Secondary Markets and Private Liquidity

How Secondary Share Transactions Actually Work

Imagine you're a venture capitalist who invested

Enter secondary markets. A hedge fund approaches your VC firm. They want to buy some of your Space X shares at $800 billion valuation. You negotiate a price, agree on terms, and execute the sale. You get cash. The hedge fund gets shares. The company? It doesn't even issue new shares. Existing shares just change hands. It's a secondary transaction—secondary because the company isn't involved, unlike primary transactions where a company raises new capital.

But here's where it gets complex. These aren't casual transactions. They involve broker-dealers (like Rainmaker Securities, mentioned in the original article) who specialize in private company share sales. These brokers maintain networks of qualified investors, negotiate terms, handle legal documentation, and manage settlement. They take a commission, usually 2-5% of the transaction value.

The infrastructure matters because private share sales come with massive friction. The shares can't be freely traded like public stocks. There are employee non-compete clauses, board approval requirements, and legal restrictions on who can own them. Foreign investors face SEC compliance headaches. Accredited investor status matters. The brokers who know these rules become invaluable.

Pricing works differently too. In public markets, stocks ping between bid-ask spreads constantly. In secondary markets for private companies, pricing happens infrequently. Space X might execute one tender round per year or every two years. Between those events, prices are somewhat fictional. If you ask a secondary market broker what Space X shares are worth today, they'll quote you a range based on recent transactions and market sentiment. But unlike public stocks, you can't actually execute that trade in real-time.

Why Companies Facilitate These Transactions

You might think companies would hate secondary markets. More shares changing hands means more dispersed ownership, more complexity, and more people with partial stakes in your company. Why allow it?

The answer is employee retention. When your company is worth $100 billion but hasn't gone public yet, your employees' equity grants are worthless on paper. They can't buy a house with theoretical future wealth. They leave for startups where they can actually sell shares. Secondary markets solve this by letting employees convert at least some of their equity into cash.

Think about Space X's situation. The company employs tens of thousands of people. Many have been there for a decade or more. Their options are worth hundreds of thousands of dollars, maybe millions. But those options won't vest for years, and even then, they can't be sold. If Space X's competitors offer secondary liquidity and Space X doesn't, top talent starts getting poached.

So Space X hosts tenders. "Alright, here's a day where we'll let employees and early investors sell shares at a fair-market valuation." Employees can convert a portion of their holdings into cash. The company maintains an updated valuation that feels real. Morale stays high because people have actual proof that their equity isn't worthless.

From a company perspective, the downside is minimal. New shareholders come in, old shareholders cash out, but the cap table just shuffles. The company doesn't have to issue new shares or raise new capital. It's just a transaction between existing and incoming shareholders.

The Price Discovery Problem

Here's a weird dynamic nobody talks about enough: in secondary markets, the price of private company shares often reflects not the company's true value, but rather the negotiating power of specific buyers and sellers at specific moments.

Consider what happened with Space X. The company completed a tender at

Public markets solve this through continuous price discovery. Millions of shares trade daily. The price adjusts second-by-second based on supply and demand. Private markets don't have that luxury. Prices get stuck for months or years until the next tender or secondary sale. During that time, the actual value of the company might shift dramatically, but the share price doesn't reflect it.

This creates opportunities and disasters. Early investors who buy at a low secondary price before a tender round might see their shares jump 20% overnight. But later investors might watch that jump and think they overpaid, especially if the company's growth trajectory weakens.

Investors handle this by looking at peer companies, comparable metrics, and market sentiment. If you're buying Space X shares at $800 billion, you're asking: "Is Space X really 16x more valuable than it was five years ago, or did the market just get more excited about space?" The answer usually depends more on sentiment than fundamentals.

Part 3: The Mega-Cap Private Company Ecosystem

Who Are the Other Giants Stuck in Private Markets?

Space X isn't alone. There's a growing club of companies worth $50 billion+ that have chosen to stay private. Understanding these companies and their valuations shows why the secondary market boom matters so much.

Open AI represents the most spectacular ascent. Founded in 2015 with modest funding, the company was valued at

Anthropic, the AI safety company, moved from

Stripe remains one of the most valuable private companies, with a valuation around $95 billion. The company has been in that rarified air for several years, periodically raising funding rounds that adjusted the valuation upward.

Byte Dance, the Chinese company that owns Tik Tok, is valued somewhere between $60-150 billion depending on which analyst you ask. Regulatory uncertainty keeps it private despite its massive scale.

Databricks, a data analytics company, crossed $40 billion valuation with a recent funding round, making it one of the fastest private companies to reach that milestone.

Perplexity has emerged as a dark horse, recently raising funding at over $15 billion valuation. It's following the AI company playbook of rapid scaling without an IPO.

That's just the top tier. Below this are dozens of companies valued at

The scale matters because it shows why the secondary market had to exist. There's simply too much wealth trapped in private companies for normal VC exit mechanisms (IPO or acquisition) to absorb.

The Valuation Question: Are Private Companies Over or Under-Valued?

One of the most contentious debates in finance right now is whether private companies are priced correctly. Are their valuations realistic, or is the market just caught up in hype?

The bulls argue that private companies can move faster, iterate quicker, and achieve higher growth rates than public companies. They don't have quarterly earnings pressure. They can reinvest all profits into growth. They can afford to be patient. Open AI didn't have to worry about quarterly guidance when it was investing billions into AI infrastructure. That's a real advantage.

The bears counter that without public market discipline, private company valuations become detached from reality. There are no short-sellers to call out overvaluation. There's no adversarial press asking hard questions. There's no SEC scrutiny. Every analyst covering private companies is either an investor or a broker trying to facilitate transactions—both have incentives to talk valuations up, not down.

The data suggests the bears might have a point. When private companies finally go public, they often see significant post-IPO pops followed by subsequent corrections. This implies private valuations were actually below where public markets priced them initially (hence the pop), but above where the true value settled long-term.

For Space X specifically, the company's valuation has risen almost monotonically from

Investors betting on secondaries are essentially making a bet that the private valuation will persist when the company goes public. That bet has worked out most of the time, but not always. Some private darlings have gone public and immediately disappointed.

Part 4: Why Elon Musk and Space X Are Ready for an IPO Now

The Strategic Shift: From "Never" to "Maybe This Year"

For years, Elon Musk was adamant. Space X wouldn't go public until the company was flying regular missions to Mars and establishing a sustained presence. That sounded reasonable in 2015. It seemed increasingly unrealistic by 2025. At what point does "flying to Mars regularly" actually start? When people are there 50% of the time? 80%? When the colony is self-sustaining?

Elon's stance created a paradox. The more successful Space X became, the less sense it made to stay private. By 2024, Space X was the dominant commercial launch provider, supporting everything from government defense contracts to private satellite constellations. The company had demonstrated profitability and was cash-flow positive. It had a clear competitive moat. It had massive growth opportunities. The only thing preventing an IPO was a founder's philosophical preference.

But philosophical preferences change when circumstances shift. Several factors converged:

First, market conditions improved dramatically. After the rate-hiking cycle ended, growth stocks stopped getting hammered. The Nasdaq recovered. Investor appetite for mega-cap tech debuts returned. For the first time since 2021, an IPO didn't feel like walking into a buzzsaw.

Second, capital constraints emerged. Space X needs capital to build out Starship manufacturing, develop lunar landers, and execute the Mars program. The private funding window has limits. The company has raised capital from diverse investors (Saudi Arabia's PIF, Google Ventures, others), but the well isn't infinite. A public offering would raise tens of billions quickly.

Third, employee retention became acute. Space X employs roughly 10,000 people. Many have been there for a decade, watching their options become increasingly valuable on paper while becoming increasingly hard to exercise or sell. Secondary tender offers help, but they're not enough. Public stock options are way more liquid. Space X people want to see the IPO.

Fourth, Musk's own circumstances changed. His net worth plummeted after buying Twitter at

The $800 Billion Tender and What It Signals

In late 2024, Space X completed a tender offer at an $800 billion valuation. This matters because it's the current market price for Space X shares in secondary trading. It tells us what sophisticated investors think the company is worth right now, today, before any IPO.

An

But Space X's market position is potentially bigger than any of those. The company controls roughly 60% of the commercial launch market and has genuine monopolistic advantages through Starship. If Space X can achieve even a fraction of the addressable market in satellite internet (Starlink), space tourism, or in-space manufacturing, the valuation multiplier makes sense.

The

- Liquidity premium: Public shares are way more liquid than private shares. Investors will pay extra for that liquidity.

- Analyst coverage: Public companies get analyst reports and research. That visibility adds value.

- Broad market access: Private shares are only available to accredited investors. Public shares available to anyone with a brokerage account.

- Lock-up expiration pop: Founder and insider shares are locked up for 180 days post-IPO. When the lock-up expires and shares can be sold, it sometimes creates a temporary pop beforehand.

If Space X IPOs in 2025 and prices at $1.2 trillion (midpoint estimate), that's a 50% pop from the tender price. That's healthy but not crazy. Some IPOs have popped 100%+ on day one.

The Bellwether Effect: Why Space X Matters More Than Just One Company

Here's where Space X becomes strategically important for the entire market. The company isn't just a mega-cap going public. It's the bellwether. It's the test case. It's the pent-up demand released.

For years, investors have been saying "we can't wait for the IPO market to reopen." But they can't actually invest in the reopening until something kicks it off. Space X going public is the catalyst. It shows that mega-cap private companies can successfully transition to public markets. It shows there's demand. It shows the process works.

Once Space X IPOs successfully, the floodgates open. Suddenly Open AI, Stripe, Anthropic, Byte Dance, and others have cover. They can point to Space X and say "we're ready too." The regulatory environment becomes clear (if Space X navigated it, so can we). The investor appetite is proven. The logistics are worked out.

Historically, this is exactly how IPO cycles work. One mega-cap IPO succeeds. Momentum builds. Five more mega-caps IPO within the next year. Markets run hot for a while, then cool down. But that initial spike is essential for the whole ecosystem.

Investors know this. On secondary markets, as Space X's IPO prospects get stronger, other mega-cap private companies see secondary trading prices rise. Byte Dance shares might go up 10% not because Byte Dance did anything different, but because investors expect an overall IPO cycle to strengthen market sentiment for private mega-caps.

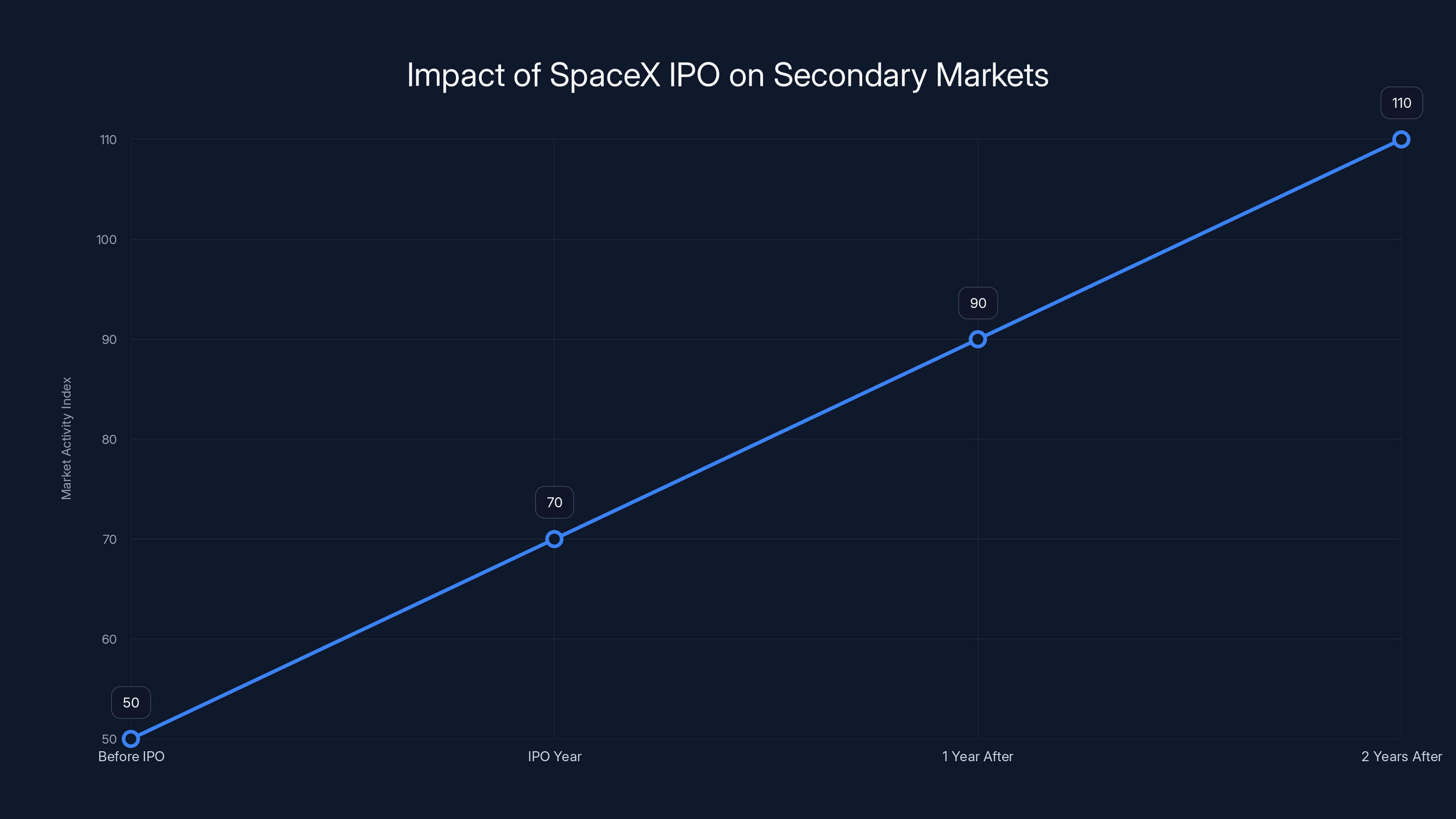

Estimated data suggests that secondary market activity may increase following a successful SpaceX IPO, as investor interest in private companies grows.

Part 5: The Impact of Space X Going Public on Private Markets

Will Secondary Markets Shrink or Explode?

Here's the most interesting question: what happens to secondary markets if Space X IPOs successfully? Conventional wisdom says secondary trading should shrink. Once Space X is public, investors don't need to buy secondary shares at a discount. They can buy public shares at the market price. Employees can diversify their holdings more easily. The rationale for secondary markets diminishes.

But that's probably wrong. History suggests something different: secondary markets will likely explode in parallel.

Why? Because a successful Space X IPO doesn't solve the fundamental problem that secondary markets exist to solve: there are way more valuable private companies than can reasonably go public in any given year. Space X going public removes one company from the private market. But it doesn't remove Open AI, Stripe, Anthropic, Byte Dance, Databricks, Perplexity, and dozens of others.

If anything, a Space X IPO strengthens the case for a thriving secondary market for other companies. Investors will have proven that mega-cap privates can succeed as public companies. That success will increase institutional appetite to own these mega-cap privates in any form—including secondary shares.

Moreover, the cash flowing into public equities from a Space X IPO doesn't disappear. Some of it will cycle back into private company secondaries. New wealth will want exposure to other mega-cap privates. The secondary market becomes not the alternative to public markets, but a complement to them.

The Cascade Effect: When One Bellwether IPOs, Others Follow

Historically, when a mega-cap company IPOs and doesn't disappoint, you see a cascade. Other companies follow quickly.

Look at 2012. Facebook went public and had a complicated IPO (pricing issues, lockup problems), but ultimately validated mega-cap tech IPOs. Suddenly, Alibaba prepared for its 2014 debut, Twitter went public in 2013, and others accelerated timelines.

In the current environment, a successful Space X IPO would likely trigger a cascade within 12-18 months:

- Year 1 (2025): Space X IPOs. Market absorbs it successfully. Stock performs decently.

- Year 2 (2026): Observing Space X's success, other mega-caps prepare accelerated timelines. Open AI might announce IPO plans. Stripe might file confidentially. Anthropic might gear up.

- Year 3 (2027): The floodgates open. Multiple mega-cap IPOs execute. The market gets crowded.

For secondary markets, this cascade is actually bullish. As more companies prepare for IPO, secondary trading often picks up. Founders take secondary sales as an opportunity to diversify. Early investors cash out before the lock-up period. Pre-IPO secondary volumes can spike in the 6-12 months before an IPO as insiders try to exit.

But longer term, more companies going public means less total private market cap, which means lower secondary trading volumes overall. The flow becomes cyclical: intense secondary activity pre-IPO, then a shift of shares into public markets, then secondary focus moves to the next cohort of pre-IPO companies.

Market Concentration and Investor Appetite Questions

One risk that nobody talks about: what if the IPO market reopens but doesn't have appetite for as many mega-cap debuts as expected?

The public markets have finite appetite. Mutual funds can own so much in any sector. Index funds have constraints on position sizes. Retail investors have attention spans. There's a real possibility that three or four mega-cap IPOs can proceed healthily, but the fifth one struggles.

That would impact secondary markets significantly. If Open AI goes public successfully, the secondary market for Open AI shares evaporates (or shrinks to tiny volume). But if the market shows signs of saturation, other mega-cap CEOs might delay their IPO plans. Those companies' secondary prices could decline if investors suddenly think the IPO is 2-3 years out instead of months away.

This dynamic creates volatility in secondary markets that public markets don't experience. In public markets, you can always sell at the market price (though it might be lower). In secondary markets, if investor sentiment shifts, trading might just stop. Bid-ask spreads widen. Liquidity evaporates.

Sophisticated secondary market participants know this and price it in. They're not just buying Space X shares at $800 billion hoping for a pop. They're analyzing the odds that Space X actually IPOs and at what price range. They're asking whether other mega-caps can coexist in a multi-IPO environment. They're calculating risk accordingly.

Part 6: The Employee Liquidity Story

Why Options and Equity Are Increasingly Worthless Until Secondary Sales Happen

If you joined Space X in 2008 and worked there for fifteen years, you deserve to see some money. That's the foundational principle of startup equity. Employees trade lower salaries for the promise of upside. That promise only makes sense if there's eventually a liquidity event.

But here's the modern problem: employees are waiting 15+ years for a liquidity event that never materializes. Meanwhile, they can't sell their options. They can't use them as collateral for loans (well, they couldn't until recently). Their entire net worth is tied up in a company that may or may not go public.

Secondary sales changed this. Suddenly, a Space X employee who accumulated options worth $10 million could sell 20-30% of those holdings at a secondary tender. They could pay taxes, take money out of the company, diversify their portfolio a bit. They're not cashing out entirely, but they're getting a meaningful liquidity event years before an IPO.

This matters for talent retention more than any stock option plan ever could. An employee at a startup might get 50,000 options at a $0.25/share strike price (4-year vest). Those options are worth nothing unless the company succeeds. But if the company does succeed and reaches private valuation milestones, secondary sales let the employee prove their options have real value.

The mechanics often involve specialized lenders. Companies like Liquid Stock (mentioned in the original article) essentially offer loans collateralized by private equity. An employee who can't sell their shares can borrow against them. The employee gets cash, the lender takes a claim on future proceeds. When an IPO eventually happens, the loan gets repaid out of the proceeds.

These arrangements are slightly predatory (lenders take a cut, loan terms aren't generous), but they're better than the alternative: employees leaving the company because they can't access any of their accumulated wealth.

The Wealth Concentration Problem

Here's something rarely discussed: secondary markets have massively concentrated wealth within early-stage companies. The early employees and investors made enormous returns. The later employees get scraps by comparison.

Consider a hypothetical Space X employee:

- Employee A: Joined in 2006, accumulated options that are now worth 30-40 million.

- Employee B: Joined in 2015, accumulated options worth 10-20 million if Space X IPOs and stocks pop, but that's not guaranteed.

- Employee C: Joined in 2022, accumulated options worth 1-2 million after taxes. That's life-changing money but in a completely different category than Employee A.

The early-employee advantage has always existed in startups. But secondary markets have amplified it. Early employees can start cashing out while the company is still private and valuations are rising. They're not forced to hold everything for an IPO. They de-risk and capture value as it accrues, not all at once years later.

This creates an equity incentive structure that actually works against later employees. Why join a 15-year-old private company with options when you could join a public company and buy shares? The options probably won't make you rich, but the wait is forever.

Part 7: The Institutional Investor Perspective

Why Hedge Funds and PE Firms Are Obsessed With Secondary Shares

From an institutional investor's perspective, secondary shares in mega-cap private companies are an incredibly attractive asset class. They're way less risky than early-stage venture, with much better downside protection. They're potentially more lucrative than public equities if the company IPOs successfully.

Consider a hedge fund buying Space X shares at $800 billion valuation. What are the scenarios?

Scenario 1 (Base case): Space X IPOs at $1.2-1.5 trillion valuation. The hedge fund's shares go public. They can hold for public market upside or sell during lockup expiration for a 50% gain. Expected return: 50-80%, realized over 12-18 months. That's fantastic.

Scenario 2 (Upside): Space X IPOs at $2 trillion valuation (if Starlink becomes massive, space economy accelerates). The hedge fund sees a 2.5x return. Expected return: 150-200%.

Scenario 3 (Downside): Space X doesn't IPO for another 5 years. The hedge fund's capital is tied up. But Space X's revenue and profitability keep growing. The company might become worth $1.5 trillion by 2030 even without an IPO. The hedge fund still gets returns, just delayed and less liquid. Expected return: 20-30% annually but over a longer timeframe.

Scenario 4 (Disaster): Space X faces a regulatory setback or technical failure. The company's valuation crashes to $300 billion. The hedge fund loses 60% of its investment. Expected return: -60%.

A sophisticated investor runs these scenarios and assigns probabilities. They might think there's an 80% chance of Scenario 1-2 (good IPO outcome), a 15% chance of Scenario 3 (continued private growth), and a 5% chance of Scenario 4 (disaster). The weighted expected return is very attractive relative to the risk.

Compare this to public market investing. Buying Tesla at $1.2 trillion valuation? You're betting on AI robotics, energy transitions, and autonomous driving. The company is already valued fairly. Your upside is 20-30% annually if everything works perfectly. Your downside is significant if sentiment shifts.

Buying Space X shares at

This is why institutional appetite for mega-cap private secondaries is so strong. These aren't speculative bets. They're rational capital allocation decisions.

The Liquidity Premium and Market Inefficiency

One of the strangest dynamics in secondary markets is that private shares sometimes trade at a discount to implied public valuations. This shouldn't happen, but it does.

Imagine Space X files for IPO and the underwriters tell the market that shares will be priced at

Why does this happen? Partly because private market investors can't perfectly predict public market outcomes. Partly because there's less information available. Partly because secondary markets are less efficient (fewer traders, less competition). Partly because private shares include illiquidity discounts that disappear when they go public.

But it also happens because of regulatory and structural constraints. Not every investor can buy private shares. Only accredited investors with sufficient capital can participate. That shrinks the buyer pool relative to public markets. With fewer buyers, prices stay lower.

Once a company IPOs, suddenly millions of investors can own shares. Supply and demand get rebalanced. Prices adjust upward. That "inefficiency" disappears.

Sophisticated investors exploit this. They buy heavily in secondary markets right before IPO announcements or shortly after private price discovery indicates momentum. They're banking on exactly this dynamic: private price to public price arbitrage.

Secondary market prices are typically 25-80% lower than IPO prices due to liquidity premiums and broader market access in IPOs. Estimated data based on typical market conditions.

Part 8: The Regulatory Landscape for Private Markets

Rule 506 and Accredited Investor Requirements

The entire secondary market for private company shares exists in a regulatory gray zone that's actually well-defined once you understand it. The key is the SEC's Rule 506, part of Regulation D.

Regulation D allows companies to raise capital without public registration if they follow certain rules. Rule 506 specifically allows unlimited fundraising from accredited investors plus up to 35 non-accredited investors. The accredited investor threshold is typically

When private company shares trade in secondary markets, they're usually structured as Rule 506 transactions too. The buyers must be accredited investors. That's why secondary markets are restricted to institutional investors, high-net-worth individuals, and qualified employees.

This creates an interesting dynamic. Secondary markets can be massive ($20+ billion annually), but completely invisible to retail investors. Most retail investors don't even know they exist. Most people own index funds that own publicly-traded companies. The private market is a different universe for wealthy and institutional participants only.

This regulatory restriction is probably a long-term vulnerability for secondary markets. There's political pressure to democratize investing, to let retail investors own private company shares. If regulators eventually relax Rule 506 and allow retail participation in private secondaries, the market could 10x. But it could also become chaotic and dangerous (retail investors getting crushed on bad private company bets).

For now, the restrictions keep secondary markets functioning efficiently. The limited participant pool makes it easier to execute large transactions. Information asymmetries are smaller than they'd be if retail investors were competing.

The IPO Process and Lockup Periods

Once a company actually files for IPO and goes public, secondary markets become less relevant for a simple reason: lockup periods. For typically 180 days (six months) after an IPO, founders and early shareholders are forbidden from selling. This creates a dry period where secondary share selling stops (you can't sell if you're locked up) and everyone waits to see if the stock appreciates.

The lockup is meant to protect the integrity of the IPO. Imagine if Elon Musk could immediately start dumping billions in Space X shares the day after the IPO. The stock would crater from supply shock. Lockups prevent that.

But lockups create their own dynamics. At the end of lockup periods, there's often massive selling pressure. Insiders finally get to diversify. The stock might drop 10-20% on lockup expiration alone. Sophisticated investors know this and either sell ahead of lockup expiration or short the stock in anticipation.

After lockup expires, secondary markets remain relevant but in a different way. Instead of pre-IPO insiders using secondary markets, post-IPO insiders use them to carefully distribute holdings. A large shareholder might not want to dump 1% of shares on the open market all at once (would crash the stock). They'd use block traders and sophisticated mechanisms to distribute holdings over time.

Part 9: The Tax Implications Nobody Discusses

How Secondary Sales Trigger Unexpected Tax Bills

Here's something that trips up employees constantly: secondary sales create immediate tax liability even though the money isn't cash yet (or is just becoming cash).

When an employee exercises their options and purchases shares, they realize a taxable gain equal to the difference between their strike price and fair market value. If an employee has a

For example:

- Strike price: $0.25 per share

- Fair market value at exercise: 800B valuation)

- Taxable gain per share: $399.75

- For 100,000 options: $39.975 million in taxable gain

- Marginal tax rate (employee is now wealthy): 37% federal plus state taxes

- Tax bill: ~$15 million

Wait, but the employee hasn't sold anything yet. They don't have cash. They just have shares. But the IRS says they owe $15 million in taxes this year, due next April.

This is why secondary sales are crucial. The employee exercises options during the secondary tender. They immediately sell shares at the fair market value used for the tax calculation. They pocket the cash, pay the taxes, and keep the remainder. Without this mechanism, employees would have phantom income with no way to pay the taxes.

The alternative used to be margin loans and other dangerous structures. Employees would borrow against their options to pay taxes, then hope the company IPOs so they can repay. That worked fine until companies didn't IPO and employees got crushed.

Modern secondary markets and loan products solved this problem. But it's still complex and highly dependent on tax counsel.

Long-Term Capital Gains vs. Short-Term Treatment

One more tax complexity: whether an employee gets long-term capital gains treatment (15-20% rates) versus short-term treatment (ordinary income rates, up to 37%) depends on how long they've held the shares.

This creates perverse incentives. An employee who wants to use a secondary sale to diversify might hold onto shares longer than they strategically should, just to get long-term capital gains treatment. They're not making the best financial decision for their portfolio. They're optimizing for tax treatment.

Conversely, some employees rush into secondary sales before they get long-term treatment because they fear the company might have issues later. It's a balancing act with real financial consequences.

Part 10: Comparing Private Markets Then and Now

How Secondary Markets Have Changed the VC Ecosystem

Twenty years ago, secondary markets barely existed. The mechanics for private company share trading were primitive. Most founders and early investors had three paths: hold until IPO, accept an acquisition offer, or maintain illiquid shares forever.

The secondary market boom has fundamentally changed venture capital dynamics. Here's how:

Then (2000-2010): Venture firms had a simple model. Invest early, help the company grow, achieve an exit (IPO or M&A) after 5-10 years. That exit is the return event. The fund collects distributions and returns capital to LPs.

Now (2015-2025): Venture firms deploy capital, the company grows, years pass, the company is worth billions but hasn't exited. The VC firm uses secondary sales to recycle capital. They sell some shares at an appreciated value, return some capital to LPs, and reinvest the capital into new opportunities. This is way more efficient than waiting 15 years for an IPO.

This acceleration of capital recycling has direct implications for startup funding. Money moves faster. Successful firms can fund more companies because they're getting return of capital quicker. The overall pace of venture activity increases.

It also changes VC incentives. A partner at a venture firm now has a mechanism to show LPs that the fund is working (secondary sales proving valuations are real) without waiting for an exit. That's psychologically powerful. LPs feel better about their investments when they see periodic secondary distributions proving the valuations weren't fantasy.

The Rise of Crossover Funds and Later-Stage Capital

Secondary markets enabled an entire category of funds that didn't exist before: crossover funds. These are funds that invest in both late-stage private companies (through secondaries and primary rounds) and early public company IPOs. They're positioned to catch companies on both sides of the public/private transition.

Crossover funds have become massive. They deploy tens of billions annually. They're not pure VC and not pure growth equity. They're hybrid. And they only make sense if secondary markets exist to give them liquidity and price discovery for private holdings.

The proliferation of these funds has changed cap table dynamics. A mega-cap private company like Space X now has ownership from traditional VCs, hedge funds, PE firms, crossover funds, sovereign wealth funds, and others. It's way more complex than it would have been 15 years ago.

This diversity of ownership actually creates friction. More investors means more voices. Decision-making slows. But it also means more capital access and more perspectives on strategy.

The private secondary market has seen significant growth, with transaction volumes increasing from

Part 11: The Downside Risks and Criticisms

When Secondary Markets Disconnect From Reality

Secondary markets aren't always efficient or fair. Sometimes they become vehicles for hype and speculation. A company shows promise, secondary share prices pop, and suddenly the valuation is disconnected from fundamentals.

This happened with some failed startups. Zenefits was valued at $4+ billion at one point based on rapid growth. Secondary shares traded hands enthusiastically. Then regulatory issues emerged, executives were replaced, and the company's actual value was revealed to be much lower. Secondary market investors who bought at peak valuation got crushed.

The We Work collapse is the ultimate cautionary tale. The company's valuation skyrocketed to $47 billion based on growth metrics and hype. Secondary shares flew. Then the IPO filing revealed the actual financials, unit economics were terrible, and the whole thing fell apart. Secondary investors who bought near the peak lost 80%+ of their investment.

These failures show that secondary markets are only as good as the information available. If a company is misrepresenting its business, secondary investors are just as vulnerable as public investors. The illiquidity and small participant pool might make secondary markets even more vulnerable to fraud or misrepresentation since there's less scrutiny than public markets get.

The Concentration of Wealth Argument

Secondary markets have exacerbated wealth inequality. Early-stage investors and employees at mega-cap successes have made astronomical returns. But this wealth compounds: once you have

Meanwhile, employees who joined later are locked out. Their options probably won't make them rich. The secondary market doesn't benefit them the way it benefits early employees. Public markets will eventually reward them more than private markets ever could.

There's a moral hazard too. Early investors who make enormous returns from secondary sales have incentives to keep the company private longer (longer secondary trading period = more juice for them). But this might not be best for later employees or for the broader economy. The company should probably go public so employees can actually participate in long-term value creation.

Regulatory Uncertainty

Secondary markets exist in a somewhat gray regulatory zone. The SEC has largely left them alone, allowing them to flourish. But regulatory attitudes could change. If a major fraud involves secondary trading, regulators might crack down hard.

Also, there's the question of whether secondary market transactions should trigger reporting requirements or disclosure rules. Right now, when a hedge fund buys 5% of Space X shares, there's no public disclosure (unlike buying 5% of a public company). That could change if regulators decide private investors need more transparency.

The regulatory environment for private markets is likely to tighten as the markets grow. What's allowed today might be restricted tomorrow.

Part 12: What Happens to the Secondary Market During an IPO

The Pre-IPO Secondary Surge

In the months leading up to an IPO filing, secondary market activity often surges. Insiders who want to diversify accelerate selling. Employees exercise options and sell immediately. Early shareholders take the opportunity to cash out before the lockup period begins.

This creates a final window of opportunity in secondary markets. The implicit price is already factored in based on IPO rumors and regulatory signals. There's urgency because the window is closing (soon shares will be public and tradable).

Sophisticated players understand this dynamic. They sometimes load up on secondary shares in the final pre-IPO period, betting that the public market price pops compared to the secondary price.

The Lockup Period Aftermath

After an IPO and 180-day lockup expiration, secondary markets for the company become obsolete. The shares are public. They trade on NASDAQ or NYSE with millions of shares changing hands daily. Secondary market brokers have nothing to facilitate.

But the lockup expiration creates its own secondary market in a sense: the public market overflowing with shares from long-locked insiders finally able to sell. The stock often stumbles on lockup expiration as supply increases.

After that, attention moves to the next batch of mega-cap private companies waiting for their IPO turn.

Part 13: The Future of Private Markets and Secondary Trading

Can Private Markets Stay Private Forever?

One interesting question: do the mega-cap private companies ever have to go public? Technically, they could stay private indefinitely. If the secondary market is liquid enough and the company is profitable, there's no forcing function to IPO.

But staying private creates constraints. The company can't use public currency (stock) for acquisitions. It can't raise capital as cheaply at scale (debt markets prefer public companies). It can't access the talent premium that public stock options provide. And capital recycling becomes harder for earlier investors.

These constraints don't prevent a company from staying private. They just make it less optimal. Eventually, most mega-cap companies will IPO because it's the best path forward. But the timeline can be stretched dramatically through secondary markets.

The Consolidation Play

One scenario gaining traction: mega-cap private companies don't IPO at all. Instead, they get acquired by each other. Open AI gets acquired by Microsoft. Space X gets acquired by a larger aerospace/defense contractor. Stripe gets acquired by a financial services giant.

If this happens, secondary markets become the exit for insiders. You sell your shares to the acquirer or to acquirer-backed investment vehicles. The exit is still real; it's just not an IPO.

This would actually be bullish for secondary markets since it extends the period where private company shares are the dominant asset class.

Integration With Public Markets

Longer-term, there's a possibility that the boundary between private and public markets blurs. Maybe in 5-10 years, you can hold both public and private shares in the same brokerage account. Maybe fractional ownership of private companies becomes accessible to retail investors.

That would massively expand secondary markets. Volumes could 100x. But it would also require regulatory changes and potentially different market structures.

For now, secondary markets remain an institutional domain. That keeps them efficient but also limits their growth.

The number of IPOs in the US dramatically decreased from 450 in 2021 to just 84 in 2023, marking the slowest year since 2009. Estimated data based on market trends.

Part 14: Investor Strategy in Today's Environment

How to Think About Buying Private Shares at Today's Valuations

If you're a qualified investor with access to secondary markets, how should you think about deploying capital? What's the right thesis?

One approach: focus on the IPO catalyst. Buy shares in mega-cap companies that are likely to IPO within 24 months at valuations where you can see upside to IPO prices. Space X at

The risk is timing. If Space X delays its IPO, you're sitting on illiquid shares for years. Your capital is locked up. That's the real cost.

Alternative approach: focus on growth at any stage. Buy shares in companies you think will be worth 3-5x more in 5-10 years, regardless of whether they IPO. That's more traditional venture math. You're betting on business quality, not IPO timing.

Another approach: focus on cash flow and distributions. Some private mega-caps are already profitable and paying dividends. Buy those and collect quarterly distributions. You're basically treating private shares like bonds with equity upside. That's a lower-growth but lower-volatility strategy.

The Diversification Principle

One pattern successful secondary market participants follow: diversification. They don't put all capital into one mega-cap. They spread across 5-10 different companies and different stages. Some are pre-IPO. Some are stable cash-flow generators. Some are speculative high-growth bets.

This is just standard portfolio theory applied to private markets. Less concentration means less idiosyncratic risk.

The Tax Optimization Game

For high-net-worth individuals, secondary market participation is often wrapped up in tax strategy. When should I buy? When should I sell? Should I hold for long-term capital gains? Should I donate shares to charity?

These decisions need expert tax counsel. But the general principle is: get professional advice before you start trading. The tax efficiency of your trades can be bigger than the returns themselves.

Part 15: The Macro Context—Why This Moment Matters

The Shift of Capital to Private Markets

Over the past decade, more and more economic value has been created in private companies rather than public companies. The reasons are complex but include:

- Regulatory burden on public companies: SOX compliance, quarterly earnings pressure, disclosure requirements. Going public is expensive and restrictive.

- Longer time horizons: Founders don't want quarterly earnings pressure. Private markets let them focus on multi-year bets.

- Access to patient capital: PE, VC, and sovereign wealth funds provide capital that doesn't demand immediate returns.

- Network effects of scale: A startup at $100M valuation benefits from access to the secondary market. That makes staying private more feasible at larger scales.

The result: companies that would have gone public at

This creates an interesting economic situation. Enormous amounts of wealth are being created in private companies, but that wealth is concentrated among early investors and employees. Later employees and retail investors are excluded. That's politically and socially unstable long-term.

Eventually, these companies will go public (or be acquired by public companies), and the wealth will become visible. That's when debates about inequality, founder compensation, and economic fairness become acute.

The IPO Market as Pressure Release Valve

From a macro perspective, Space X's IPO is a pressure release valve. It's a signal that the economy is healthy enough for mega-cap debuts. It creates a path for capital recycling. It gives employees a tangible proof point that their equity isn't worthless.

Without IPOs, the pressure builds. Employees get frustrated and leave. Capital gets trapped. The private market becomes more dysfunctional, not more efficient.

A healthy capital market needs both private and public segments functioning well. Secondary markets are a bridge, but they're not a substitute for public markets.

Part 16: Expert Insights and Industry Perspectives

What Institutional Investors Are Actually Thinking

Based on the original source article's interview with Greg Martin at Rainmaker Securities, institutional investors see several clear narratives:

The bellwether thesis: Space X going public would reset the IPO market. Investors see it as the trigger. Once Space X proves mega-cap private-to-public transitions work, capital flows to other companies with similar profiles.

The valuation affirmation thesis: Secondary trading has already happened at

The supply and demand thesis: Private market cap has grown so large that secondary markets and IPOs must both exist. One can't absorb all the exits. The market needs both mechanisms.

The talent thesis: Mega-cap private companies compete for talent globally. Without secondary liquidity mechanisms (tenders, secondary sales), they can't retain people. This creates a forcing function for secondary market development.

What This Means for the Broader Ecosystem

If secondary markets continue to grow and IPOs eventually reopen, the combination creates a more sophisticated capital market. Companies have more options. Investors have more opportunities. Employees have more paths to liquidity.

The risk is fragmentation. If private and public markets become too separated, information asymmetries increase. Public market investors start wondering what the private market knows that they don't. Trust erodes.

Maintaining connection between the markets becomes important. That's what secondary market pricing and IPO pricing calibration provide. They're reference points that keep the system integrated.

Part 17: Practical Implications for Different Stakeholders

For Early-Stage Startup Founders

If you're starting a company in 2025, the existence of secondary markets changes your path. You know that if your company succeeds, staying private longer is now an option. You can recruit investors and employees by showing realistic secondary market evidence. You don't have to promise an IPO; you can promise liquidity through other mechanisms.

This is genuinely different from 2005. Back then, the startup mythology was all IPO or nothing. Now, the mythology is more nuanced.

For Employees Joining Late-Stage Private Companies

If you're an employee negotiating an equity package at a mature private company, understand the cash-flow dynamics. Will the company facilitate secondary sales? Are your options actually convertible to cash, or are they purely speculative?

Inquire about this specifically. It affects whether the equity is real compensation or fantasy.

For Venture Capitalists

Secondary markets have shortened fund cycles. You can return capital to LPs faster through secondary sales. This changes portfolio strategy. You don't have to hold winners until IPO. You can partially exit and redeploy.

The flip side: secondary markets make it harder to justify holding underperformers. If the company is obviously struggling, secondary markets will price it down. You can't hide in the hope that an IPO will bail everyone out.

For Public Market Investors

Space X's IPO is a gift to public market researchers. You get to study how private valuations translate to public valuations. You get to spot inefficiencies. You get to understand which mega-cap private companies are actually good businesses and which are just expensive.

The key is not to assume private pricing = public pricing. They often diverge. Understand why and capitalize on the divergence.

Part 18: The Risks and Edge Cases

What If Space X IPO Fails?

The whole thesis depends on Space X going public successfully. What if the company files for IPO and then withdraws? What if markets crash before the IPO prices? What if Elon Musk changes his mind?

If that happens, secondary market confidence would evaporate. Other mega-cap companies would delay their IPO plans. Secondary valuations would correct downward significantly. The bullish thesis would reset.

That's the tail risk. It's probably 10-15% probability, but it's real.

What If The IPO Market Doesn't Reopen?

An alternative scenario: Space X IPOs, but the overall IPO market doesn't reopen. Only mega-cap companies with proven profitability and massive moats can go public. Everyone else stays private.

In that case, secondary markets become more important than ever. They become the exit for non-mega-cap companies. The size of secondary markets might actually grow as a percentage of total private market activity.

This would be a modest positive for secondary market brokers and intermediaries, but a negative for later-stage startups that don't have mega-cap status.

What If Regulation Changes?

Secondary markets exist in a deregulated space relative to public markets. If the SEC decides to regulate secondary market transactions more heavily (disclosure requirements, accredited investor verification, anti-fraud rules), the market could shrink significantly.

Most sophisticated market participants would adapt. But the friction would increase. The convenience advantage would decrease.

Conclusion: The Next Chapter in Private Market Evolution

Space X's potential IPO in 2025 is not just about Space X. It's a referendum on the entire private market ecosystem that's developed over the past few years. It's a test case for whether mega-cap companies can successfully transition to public markets after staying private for 15+ years.

If Space X IPOs successfully, we'll likely see a cascade. Other mega-cap private companies will feel emboldened to pursue their own public debuts. The IPO market will reopen. Capital will flow. Secondary markets might actually expand before they contract, because investors will want exposure to pre-IPO mega-caps across the entire cohort.

But even if the IPO happens, secondary markets won't disappear. They've solved a real problem: the need for liquidity in companies that choose to stay private. As long as mega-cap companies exist in private form, secondary markets will facilitate trading.

The macro implication is significant. We're witnessing a fundamental shift in how capital markets function. Public markets are no longer the only significant marketplace. Private markets are increasingly sophisticated, deep, and real. Secondary trading is proving that private shares have legitimate economic value outside of a binary IPO-or-bust framework.

For participants in this ecosystem—whether investors, employees, brokers, or founders—the 2025-2026 period will be defining. Space X's IPO will answer several key questions:

- Can mega-cap private companies actually go public in this regulatory environment?

- Will the public market price reflect the secondary market pricing?

- Does an IPO trigger a cascade of other mega-cap debuts?

- How do lock-up expirations play out when insiders have massive holdings?

The answers will shape private market dynamics for years. Secondary market participants are watching closely, pricing in probabilities, and positioning accordingly. The next chapter is being written in real-time, and Space X is the protagonist.

For now, the secondary market boom continues. Capital flows into mega-cap private companies. Employees cash out secondary shares at spectacular valuations. Early investors recycle capital into new opportunities. The system adapts and evolves.

When the IPO window finally opens—whether through Space X or another mega-cap—the private markets will be ready. They've already proven they can function at scale. The question is no longer whether they can work. It's whether they'll coexist with public markets or gradually replace them as the center of gravity for capital allocation.

That's the real story here. Secondary markets aren't temporary patches. They're the future of how capital markets actually work.

FAQ

What is a secondary market in private company shares?

A secondary market for private company shares is a marketplace where existing shareholders can buy and sell stakes in privately-held companies without the company issuing new shares or raising new capital. Unlike primary fundraising rounds where companies issue new shares, secondary transactions involve existing shareholders (founders, employees, early investors, venture firms) selling to new buyers (hedge funds, private equity, sovereign wealth funds) at negotiated prices. These transactions are typically facilitated by specialized broker-dealers and are restricted to accredited investors.

How does the secondary market pricing work compared to IPO pricing?

Secondary market pricing is determined by supply and demand between specific buyers and sellers, often with significant negotiation and broker involvement. The prices reflect current sentiment about the company's value but are less frequent and less liquid than public market pricing. When a company goes public, the IPO price is typically higher than the most recent secondary market price because public shares command a liquidity premium, broader investor access, analyst coverage, and the potential for price discovery through continuous trading. The difference between secondary price and IPO price is often 25-80%, depending on market conditions and investor appetite.

What are the benefits of secondary markets for employees?

Secondary markets provide employees at late-stage private companies with partial liquidity before any IPO event. Rather than waiting years for a company to go public while their equity remains worthless on paper, employees can sell a portion of their vested options during tender offers or secondary sales. This allows them to pay taxes on options exercises, diversify their personal wealth, and reduce their financial dependence on the company's eventual exit. Without secondary markets, employees at companies that stay private for 15+ years would face phantom income tax bills with no ability to liquidate shares.

Why would a company stay private if it's worth billions?

Companies choose to stay private to avoid regulatory burden, quarterly earnings pressure, mandatory disclosure requirements, and public market scrutiny. Founders can focus on long-term strategy rather than quarterly guidance. The company can maintain operational flexibility and make bold bets without stock market consequences. Additionally, secondary markets now provide liquidity alternatives so companies don't have to IPO to give employees and investors liquidity events. The tradeoff is that staying private limits the company's ability to use stock as acquisition currency and may restrict access to the deepest capital markets.

What triggers a company to finally go public after staying private for years?

Companies typically go public when they face capital constraints, want to execute large acquisitions using public currency, need to access the broadest possible investor base, or when market conditions become favorable (rising equity markets, strong IPO sentiment). Additionally, founder circumstances can change—wealth diversification needs, retirement planning, or changing business philosophies about public ownership. For Space X, factors include capital needs for Mars missions, favorable market conditions, employee retention requirements, and Elon Musk's willingness to pursue public markets after years of resistance.

Can secondary share prices predict IPO prices?

Secondary market prices provide directional guidance but aren't perfect predictors of IPO prices. Secondary prices are usually 25-80% below IPO prices due to the liquidity premium investors pay for public shares and broader market access. However, secondary prices do reflect the sentiment and valuation range that institutional investors believe is reasonable. If secondary prices are rising, it often indicates building confidence that an IPO will succeed. If secondary prices are stagnant or declining despite good company fundamentals, it may signal investor skepticism about near-term IPO prospects. Sophisticated investors use secondary prices as one data point among many when valuing private companies.

Summary: Key Takeaways

The secondary market for private company shares has become a critical component of modern capital markets. Space X's potential 2025 IPO represents a potential catalyst for both the IPO market and secondary market dynamics. If Space X successfully goes public, we'll likely see increased activity in both secondary markets (as investors gain confidence and seek exposure to other mega-cap privates) and the IPO market (as other mega-cap companies follow Space X's lead). Secondary markets will continue to matter because the private market cap is now so large that secondary transactions provide essential liquidity for employees, founders, and investors who can't wait for an eventual IPO. The ecosystem is evolving faster than regulators are responding, creating both opportunities and risks. For participants—whether as employees, investors, or founders—understanding secondary market mechanics, tax implications, and valuation dynamics is increasingly essential.

Key Takeaways

- Secondary markets for private company shares have grown from invisible to $25B+ annually, providing crucial liquidity before IPO events

- SpaceX trading at 1.2-1.5T as a public company

- A successful SpaceX IPO would trigger cascading IPO activity from other mega-cap private companies within 12-18 months

- Employees at late-stage private companies now depend on secondary sales and tender offers for partial liquidity instead of waiting 15+ years for IPO

- Private market cap now exceeds public market absorption capacity, making secondary markets essential rather than optional