The CEO Who Emerged from the Shadows: Understanding Tether's Legitimacy Offensive

For nearly a decade, Paolo Ardoino managed Tether from the strategic vantage point of offshore jurisdictions, carefully maintaining distance from the regulatory scrutiny that has defined the cryptocurrency industry. The company he oversees—the issuer of USDT, the world's most widely circulated stablecoin—operated in what many critics called a gray zone: massive in scale ($187 billion in circulation), enormously influential across crypto markets, yet persistently controversial regarding its reserve composition and operational transparency.

But something fundamental shifted in early 2026. Ardoino, the 41-year-old executive who joined Tether just months after its founding in 2014, transformed from a relatively anonymous figure into a omnipresent voice in mainstream financial media. Within a single week, he appeared in features across Fortune, Bloomberg, Reuters, and major tech publications. This wasn't a spontaneous emergence—it represented a carefully orchestrated strategic pivot that signals Tether's ambitions to transition from its position as crypto's most dominant-yet-controversial player into a legitimate, regulated financial infrastructure company.

The timing of this media offensive was neither coincidental nor random. Tether simultaneously announced the launch of USAT, a new U.S.-regulated stablecoin issued through Anchorage Digital Bank. This product represents Tether's direct challenge to Circle's USDC, which has dominated the regulatory-compliant stablecoin market in the United States. Additionally, the broader stablecoin ecosystem has begun consolidating around regulated offerings: Fidelity Investments launched its own dollar-pegged token, while JPMorgan Chase and PayPal had already announced competing products. The competitive landscape that was once dominated by Tether's USDT now features heavyweight financial institutions entering a market that has matured significantly.

What makes this moment particularly significant is the political and regulatory context. Howard Lutnick, the former Cantor Fitzgerald CEO and longtime Tether associate, now serves as Commerce Secretary—a position that places him directly in conversation with banking, financial services, and cryptocurrency regulation discussions at the highest levels of government. Cantor Fitzgerald itself manages a substantial portion of Tether's reserves, creating an interconnected structure that would have been unthinkable during the offshore era. These institutional connections represent a form of political and financial legitimacy that no amount of media coverage alone could generate.

Tether's transformation raises fundamental questions about cryptocurrency legitimacy, regulatory capture, and the nature of financial infrastructure in the emerging digital economy. Does an organization with Tether's controversial history—including allegations of connections to money laundering and sanctions evasion—deserve a place at the table of mainstream financial institutions? Or does the sheer scale of USDT's adoption, its utility in emerging markets, and its demonstrable technological advantages for law enforcement justify its normalization within the financial system?

The Origins of Tether: From Controversial Beginnings to Market Dominance

The 2014 Launch and Early Skepticism

Tether's founding in 2014 occurred at a moment when cryptocurrency remained deeply experimental and philosophically fractured. Bitcoin had survived its early existential threats, but the broader ecosystem lacked infrastructure, trust mechanisms, and institutional adoption. The innovation that Tether introduced—a blockchain-based representation of the U.S. dollar that could move across crypto networks—addressed a critical practical problem: how to convert between volatile crypto assets and stable fiat currency without exiting the blockchain ecosystem.

However, from the beginning, Tether embodied the essential tension that continues to define it. The company promised that every USDT token in circulation was backed by equivalent U.S. dollars held in reserve. Yet the actual reserves—where they were held, how they were audited, who controlled them—remained opaque. When Ardoino joined the company just months after its launch, the organization was already attracting skeptics who questioned whether the promised reserves actually existed. This skepticism would prove prescient, as Tether's reserve composition became the subject of regulatory scrutiny, journalistic investigation, and academic analysis that continues to this day.

The Scale of Adoption That Defied the Critics

Despite persistent questions about its backing and governance, USDT achieved extraordinary market adoption. The reasons for this adoption reveal something important about how financial infrastructure actually develops in decentralized systems. USDT offered superior liquidity compared to alternatives. It worked across nearly every cryptocurrency exchange globally. It functioned on multiple blockchain networks simultaneously (Ethereum, Tron, Solana, Polygon, and others), providing genuine network effects that competitors couldn't match. And critically, it existed and functioned reliably at massive scale, while competitors remained relatively small or had failed entirely.

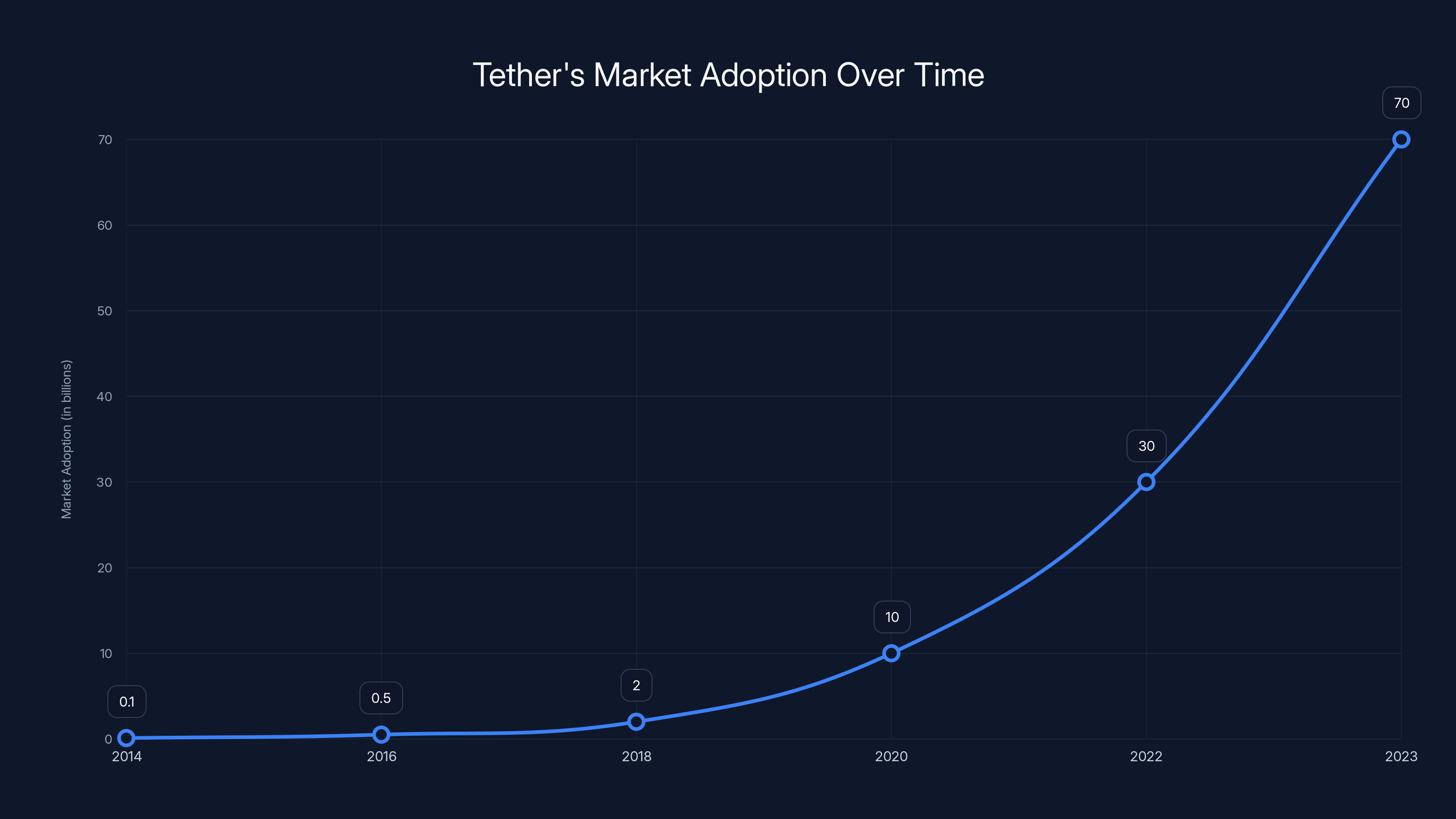

By 2026, USDT had achieved a market capitalization of $187 billion—larger than all competing stablecoins combined. The daily transaction volume measured in the tens of billions of dollars. Most remarkably, Tether reported approximately 536 million users of USDT, growing at a rate of 30 million new users per quarter. To contextualize this growth: no traditional fintech company has achieved comparable expansion. The growth trajectory resembled that of Facebook during its hypergrowth phase more closely than conventional banking technology adoption patterns.

This scale created a form of network effect moat that protected Tether from competition. Merchants and financial institutions needed to support the stablecoin with the broadest ecosystem. Traders preferred the token with the deepest liquidity and tightest spreads. Users wanted the stablecoin that worked everywhere, accepted by everyone. Tether had become too big to fail in the cryptocurrency ecosystem—or so the logic went—because removing it would cause systemic disruption affecting hundreds of millions of transactions and billions of dollars in value.

The Economist's Bombshell and Persistent Credibility Challenges

Yet despite this dominance, credibility remained elusive. In mid-2024, The Economist published a detailed investigation documenting how Tether had allegedly been used by Russian money launderer Ekaterina Zhdanova to connect British drug gangs, Moscow hackers, sanctioned oligarchs, and Russian intelligence operatives. The reporting provided specific transaction amounts, named sources, and documentary evidence suggesting that Tether's stablecoin played a functional role in facilitating international money laundering operations.

When Ardoino addressed these allegations in 2026 interviews, his response revealed the defensive posture that continued to characterize Tether's engagement with criticism. He dismissed the absolute amounts cited in The Economist investigation as a "drop in the ocean" relative to the overall $187 billion in circulation. He drew analogies to iPhones and Toyotas, arguing that any technology could be misused for illicit purposes. He pointed to Tether's collaboration with law enforcement agencies as evidence of legitimacy.

But this defense strategy itself illustrated the deeper credibility challenge Tether faces. The comparison to iPhones was rhetorically clever but analytically incomplete. The manufacturers of iPhones don't maintain absolute custody over all iPhones globally and retain the ability to freeze access to specific devices on demand. Tether, by contrast, operates a permissioned system where the company itself can and does prevent the movement of specific tokens—a power that no legitimate financial infrastructure company should retain without rigorous oversight and third-party governance.

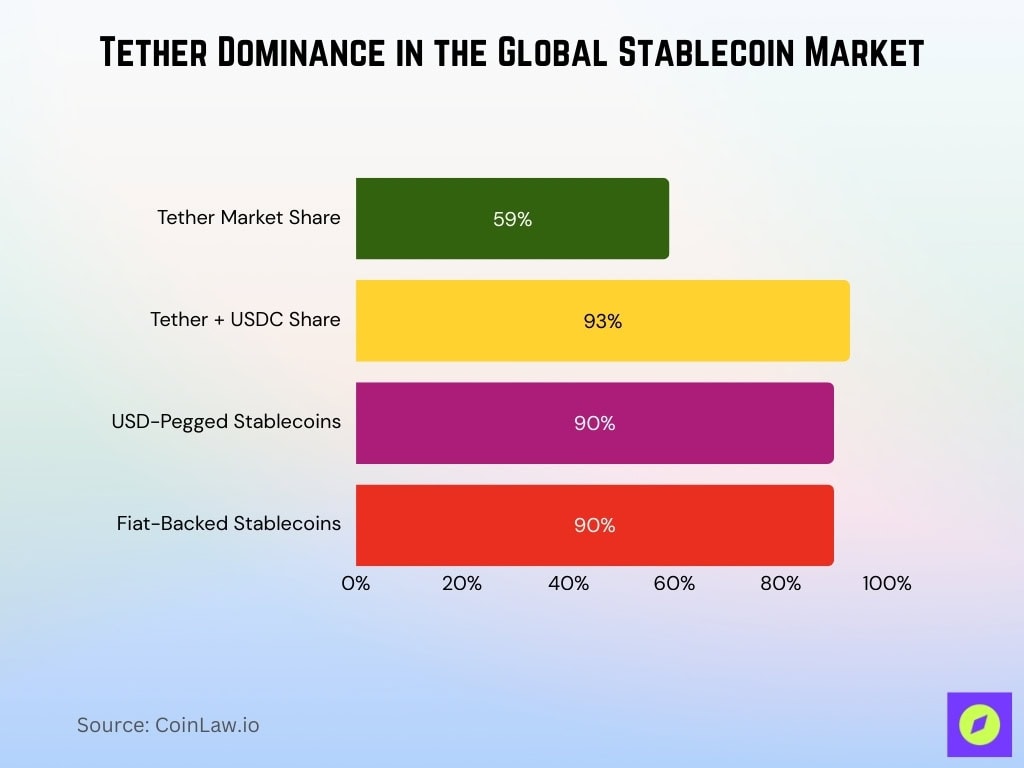

By 2026, USDT is projected to maintain a significant lead in the stablecoin market, particularly in unregulated segments, while USDC captures a substantial share due to its regulatory compliance. Estimated data.

Understanding USDT: The Stablecoin That Changed Global Finance

How USDT Functions as a Cross-Border Digital Dollar

At its core, USDT represents a technological solution to a specific problem that existed long before Tether designed it. Traditional international payments require involvement of multiple banks, clearing houses, and government regulatory frameworks. A dollar transfer from the United States to Argentina might take three to five business days, involve multiple intermediary institutions each taking a fee, and expose the sender to various compliance burdens.

Tether's innovation was conceptually simple: create a blockchain token that represents a dollar, make it transferable instantly across networks, and allow anyone with a wallet to hold it. From a technical perspective, USDT is not inherently different from other blockchain tokens—it's a digital representation of a unit of value. What distinguished USDT was Tether's promise that the company held actual dollar reserves in banks to back every token issued.

The economics of this model created powerful incentives for adoption. Individuals in countries with weak or unstable currencies discovered they could acquire USDT and preserve the value of their savings in dollar terms without actually leaving their country or converting their holdings into physical cash. Traders found they could move value between exchanges instantly without waiting for traditional banking transfers. International businesses could settle payments in USDT, eliminating currency conversion costs and settlement delays.

The Reserve Problem That Never Fully Resolved

Yet from inception, Tether's fundamental credibility challenge was straightforward: proving the reserves actually existed. In traditional banking, customers deposit dollars, the bank promises to maintain those deposits, and government-backed deposit insurance and banking regulations provide assurance. With Tether, users had to trust Ardoino's assertions that he was honestly maintaining dollar reserves.

Tether published periodic attestations from accounting firms confirming that reserves existed, but these attestations stopped short of full audits. The company disclosed that reserves were held across various banks globally but didn't specify exact amounts, precise locations, or the identity of all custodial institutions. Critics noted that Tether had moved reserves between banks multiple times, sometimes following public controversy or regulatory concern. The opacity created space for skeptics to hypothesize that Tether's reserves were insufficient, partially fictitious, or held in institutions of questionable financial soundness.

From an economic perspective, this reserve question mattered significantly. If USDT weren't fully backed by dollars, then holding USDT represented an implicit unsecured loan to Tether or whoever controlled the reserves. If a significant portion of Tether users attempted to exchange their tokens for actual dollars simultaneously, the company might not have sufficient reserves to honor all claims. This would trigger a bank run scenario—a scenario that Tether's massive scale made systemically important.

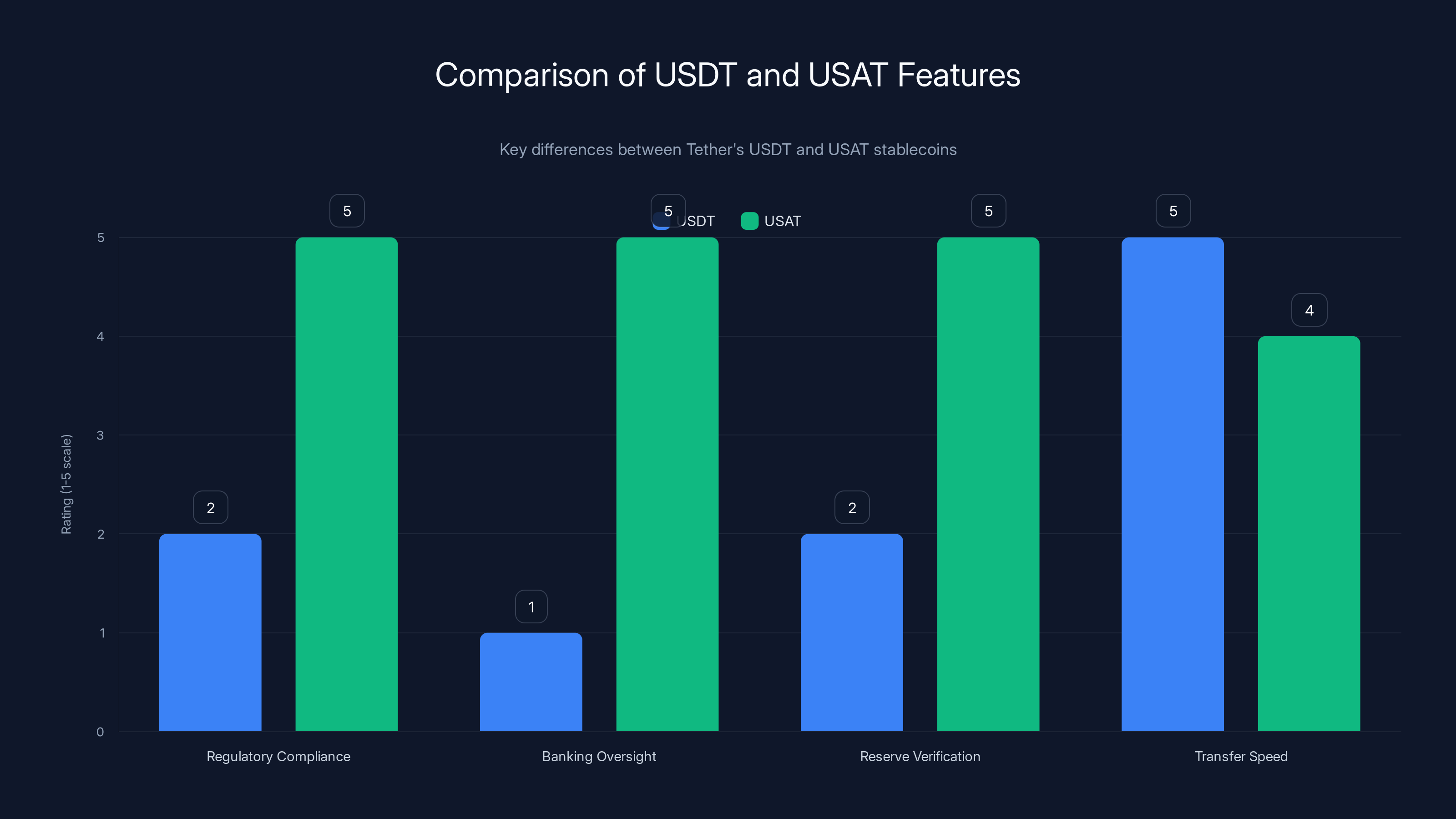

USAT offers higher regulatory compliance and banking oversight compared to USDT, while both maintain high transfer speeds. Estimated data based on described features.

The 2026 Regulatory Inflection: From Offshore to Compliant

The USAT Launch: Direct Competition in the Regulated Market

Tether's 2026 media offensive and USAT announcement represented a strategic acknowledgment that the offshore model had limitations. USAT is explicitly designed to comply with U.S. regulatory requirements that USDT cannot or will not satisfy. By issuing USAT through Anchorage Digital Bank—a chartered bank with explicit regulatory oversight—Tether accepted constraints that its USDT never did: it agreed to maintain specific reserve requirements, accept regular audits, and comply with banking regulations.

The competitive timing was significant. Fidelity Investments' stablecoin launch demonstrated that major financial institutions now viewed stablecoins as infrastructure, not speculative assets. JPMorgan's JPMCoin and PayPal's initiatives indicated that traditional finance saw stablecoins as inevitable evolution rather than temporary cryptocurrency phenomenon. In this environment, USDT's status as an unregulated digital currency represented a limitation rather than a feature. Institutions required regulatory compliance certifications and transparent reserve documentation.

UAST's positioning explicitly challenged Circle's USDC, which had successfully positioned itself as the regulatory-compliant alternative to USDT. By launching USAT, Tether signaled that it would compete for institutional adoption in the regulated segment while maintaining USDT's dominance in global cryptocurrency trading. This two-product strategy reflected sophisticated market segmentation: USDT for unrestricted global use, USAT for regulated institutional deployment.

White House Engagement and FBI Collaboration

What elevated this legitimacy offensive beyond mere product announcements was Tether's reported engagement with U.S. government institutions. Ardoino indicated during 2026 interviews that Tether maintained active dialogue with White House officials, collaborated with the FBI and Secret Service, and worked with law enforcement agencies across more than 60 countries. Cantor Fitzgerald's involvement in reserve management created additional institutional legitimacy through connections to established finance.

This government engagement served multiple strategic purposes. First, it created legitimacy by association—if federal law enforcement agencies chose to work with Tether rather than oppose it, that suggested some level of official acceptance. Second, it provided Tether with credible talking points about its law enforcement capabilities, which Ardoino emphasized extensively. Third, it created de facto allies within government who had institutional incentives to support Tether's expansion rather than constrain it.

From a strategic communications perspective, this was sophisticated positioning. Rather than making abstract arguments about Tether's legitimacy, the company embedded itself within government structures by providing value to law enforcement. When federal agencies needed to freeze stolen funds or track illicit transactions, they increasingly turned to Tether. This created positive associations—Tether as a law enforcement enabler—that countered narratives of Tether as a vehicle for money laundering.

The Emerging Stablecoin Competitive Landscape

Market Consolidation Around Regulated Alternatives

The period 2024-2026 witnessed fundamental restructuring in stablecoin competitive dynamics. Early stablecoins—including Terra's algorithmic UST, which catastrophically collapsed in 2022—were largely eliminated from consideration. The surviving competitors consolidated into two categories: legacy regulated alternatives seeking to compete with USDT (principally USDC), and newcomers backed by major institutional players entering the market for the first time.

Circle's USDC had emerged as the principal regulatory-compliant competitor to USDT. Operating under explicit banking oversight, USDC offered transparency and compliance that USDT didn't. However, USDC's liquidity and adoption lagged significantly behind USDT, particularly in Asia and emerging markets where Tether dominated. The USDC approach appealed primarily to institutions and users prioritizing regulatory safety over maximum optionality.

Meanwhile, JPMorgan's JPMCoin existed in a different category entirely—a wholesale payments tool designed for interbank transfers rather than broad retail use. Fidelity's entry signaled that major asset managers viewed stablecoins as infrastructure components necessary to provide financial technology services. PayPal's involvement indicated that payment processors expected stablecoins to become standard settlement mechanisms.

Tether's response was strategically sophisticated: rather than defending USDT as uniquely superior, the company launched USAT to compete in the regulated segment while accepting USDT's continued dominance in the unregulated, high-volume trading segment. This two-product strategy acknowledged market fragmentation while maintaining dominant position in the segment where Tether faced no realistic competition—global cryptocurrency trading and emerging market use cases.

The Emerging Markets Argument: Financial Inclusion Through Stablecoins

Ardoino's most compelling argument for Tether's legitimacy focused on financial inclusion in emerging economies. He cited specific statistics that revealed stablecoin utility in markets where traditional financial infrastructure was inadequate. In Argentina, where the peso had lost 94.5% of its value against the U.S. dollar over five years, USDT provided a store of value mechanism that conventional financial institutions couldn't offer. In Haiti, where the average salary was approximately $1.34 per day, USDT offered access to dollar-based financial systems to populations entirely excluded from traditional banking.

These use cases represented genuine value that Tether's technology provided. In inflation-ravaged economies, a blockchain-based stablecoin offered protection against currency devaluation that government-backed institutions couldn't provide. For individuals in countries with capital controls or banking sector collapse, USDT offered access to dollar-denominated value without requiring entry into the banking system. Critically, USDT's value proposition in these markets was not speculative—it addressed fundamental economic needs created by monetary instability and institutional failure.

From a development economics perspective, Tether's role in emerging markets was genuinely consequential. Traditional financial inclusion efforts focused on bringing unbanked populations into conventional banking systems. But in many emerging markets, conventional banking systems themselves were unstable or inaccessible. Stablecoins offered an alternative path to financial inclusion that bypassed traditional institutional barriers. The scale of USDT adoption in emerging markets—arguably the primary driver of the 30 million new quarterly users—validated this use case despite Tether's lack of explicit focus on financial inclusion strategy.

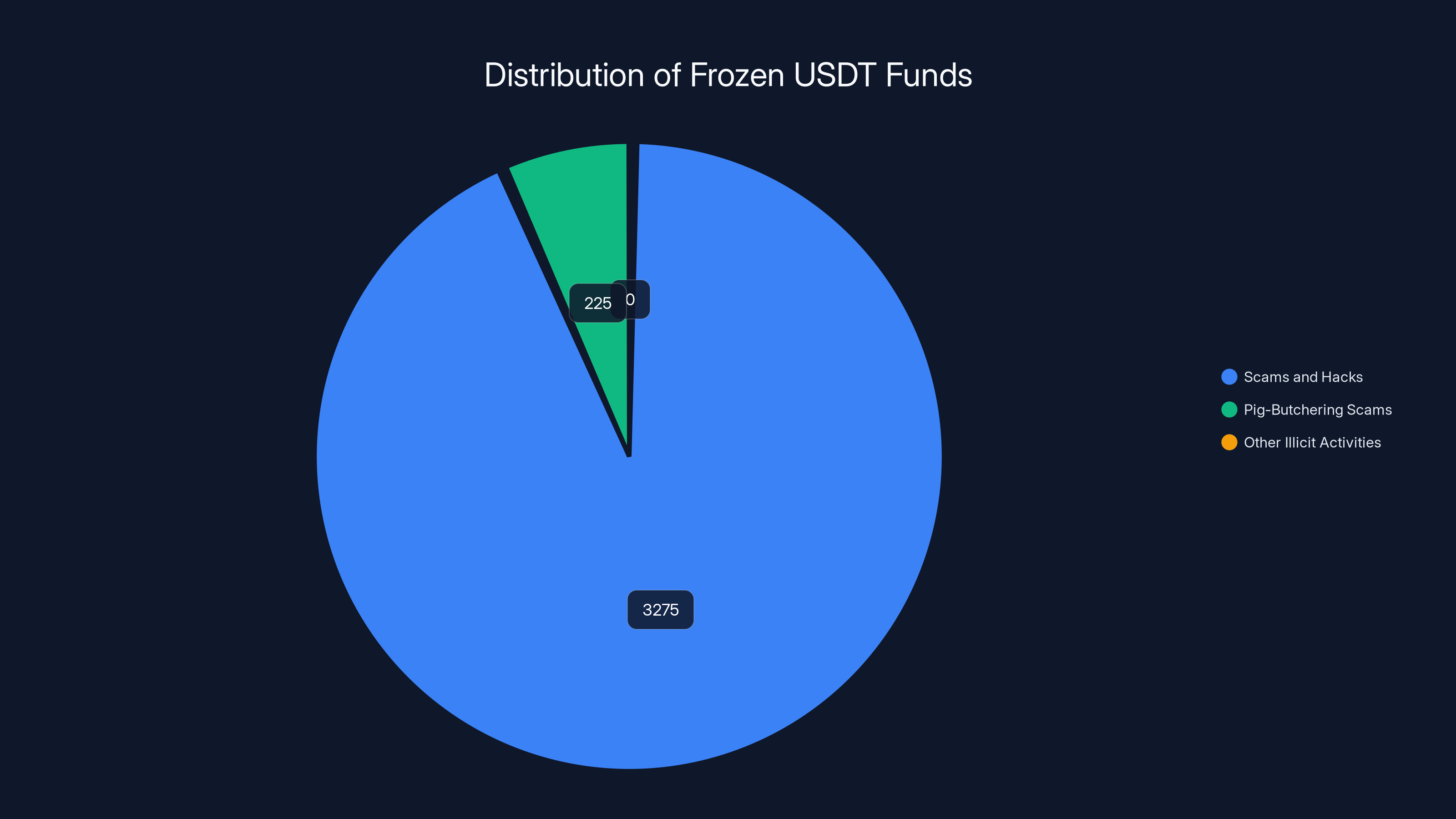

Tether has frozen approximately

Tether's Law Enforcement Narrative: Freezing Funds as Legitimacy Proof

The $3.5 Billion in Frozen Tokens

One of Ardoino's primary legitimacy arguments rested on Tether's capacity and willingness to freeze tokens associated with illicit activity. The company claimed to have frozen approximately $3.5 billion in USDT tokens, with the vast majority of frozen funds belonging to "people who have been scammed or hacked." This statistic was presented as evidence that Tether served law enforcement interests and protected victims of financial crime.

The pig-butchering scam example illustrated this argument. Pig-butchering scams represent a sophisticated form of financial fraud where scammers invest substantial time in relationship development before directing victims into fake investment schemes. Tether reported identifying $225 million in pig-butchering scam proceeds and coordinating with authorities to freeze the funds "in the blink of an eye." By comparison, Ardoino argued, traditional financial institutions failed to identify such fraud with comparable speed or effectiveness.

From a technical perspective, Tether's capacity to freeze tokens did represent a genuine advantage for law enforcement compared to cash-based systems. A traditional bank run—involving physical pallets of cash moving internationally—would be virtually undetectable and essentially impossible for law enforcement to interdict in real-time. USDT's blockchain basis made every transaction traceable and enabled rapid intervention once illicit activity was identified.

However, this capability also represented the fundamental tension in Tether's legitimacy narrative. The same power to freeze tokens that law enforcement found valuable represented a form of centralized control that contradicted the founding principles of cryptocurrency. Bitcoin's entire value proposition rested on irreversible, censorship-resistant transactions. Tether's capacity to override transaction finality suggested that USDT was fundamentally a permissioned system dependent on Tether's discretionary judgment, not a trustless protocol.

The OFAC Compliance Infrastructure

Tether's statements about OFAC compliance indicated that the company maintained sophisticated infrastructure for screening transactions against U.S. Treasury sanctions lists. OFAC (Office of Foreign Assets Control) requirements obligate financial institutions to prevent transactions involving sanctioned individuals and entities. For a company with Tether's global reach and $187 billion in annual transaction volume, maintaining OFAC compliance at scale represented a significant operational undertaking.

The company's engagement with law enforcement agencies and sanctions compliance pointed toward a specific strategic positioning: Tether as a financial infrastructure company operating under equivalent regulatory and compliance frameworks as traditional banks, even though no banking charter technically existed. By demonstrating OFAC compliance, FBI coordination, and Secret Service collaboration, Ardoino constructed a narrative suggesting that Tether operated with equivalent oversight and control mechanisms as regulated financial institutions.

This positioning was rhetorically powerful but analytically incomplete. True regulatory equivalence would require independent regulatory authority capable of examining Tether's reserves, approving its policies, and enforcing compliance. The cooperation with federal agencies was voluntary—Tether could theoretically refuse engagement or resist inquiries. Traditional banks lacked this discretion; regulators could compel actions, demand information, and impose sanctions. The distinction between voluntary cooperation and mandatory regulatory oversight represented a critical difference in governance structures.

The Howard Lutnick Factor: Political Capital Meets Financial Infrastructure

From Cantor Fitzgerald to Commerce Secretary

Perhaps the most significant element in Tether's legitimacy strategy involved Howard Lutnick's transition into formal government position. Lutnick had maintained longstanding business relationships with Tether and Cantor Fitzgerald maintained substantial involvement in Tether's reserve management. When Lutnick became Commerce Secretary—a position that places him directly in conversation with banking, financial services, and cryptocurrency regulation—this created an unprecedented form of political legitimacy.

From Tether's strategic perspective, Lutnick's government position created multiple valuable effects. It provided direct access to senior government decision-makers regarding cryptocurrency and financial services policy. It signaled to other financial institutions that Tether had legitimate government relationships and shouldn't be dismissed as purely crypto speculation. It created implicit assurance that Tether's interests would be represented in policy discussions at the highest levels.

For Lutnick, the Tether relationship created different benefits. As Commerce Secretary managing international trade and financial services relationships, Lutnick could position cryptocurrency and stablecoins as emerging financial infrastructure that the United States should lead in rather than constrain. His involvement with Cantor Fitzgerald's reserve management role provided him with deep knowledge of Tether's operations and, implicitly, credibility for defending the company's legitimacy.

From a government affairs perspective, this constellation of relationships represented sophisticated political infrastructure. Tether wasn't simply engaging with regulators as a company seeking approval; Tether had embedded itself within government decision-making structures through appointed officials with personal and professional reasons to support the company's expansion. This wasn't unique to Tether—major financial institutions routinely cultivate relationships with government officials—but it marked a significant shift for a company that had previously operated from offshore positions distanced from U.S. government engagement.

The Regulatory Capture Concern

Critical observers noted that this configuration raised legitimate concerns about regulatory capture—the process by which regulated industries gain disproportionate influence over the regulators assigned to oversee them. When Commerce Secretary Lutnick maintained active involvement in Tether through Cantor Fitzgerald relationships, it created potential conflicts between his government responsibilities and his commercial interests.

The formal ethics guidelines governing executive branch conflicts would presumably address these relationships. However, the optics of a government official overseeing cryptocurrency and financial services policy while connected to a controversial cryptocurrency company were inherently problematic. It suggested that Tether had moved from defensive positioning against regulatory oversight toward active integration within government decision-making processes.

Tether (USDT) has seen exponential growth in market adoption from its inception in 2014 to 2023, despite ongoing controversies and scrutiny. (Estimated data)

The Money Laundering Allegation Problem: Can Tether Escape Its Reputation?

The Persistence of the Illicit Finance Narrative

Despite Ardoino's media efforts and government engagement, one fundamental credibility challenge remained stubbornly difficult to resolve: the documented connection between USDT and money laundering activities. The Economist's detailed investigation of Ekaterina Zhdanova's use of Tether to facilitate international money laundering networks couldn't be dismissed as mere allegations. The reporting included transaction amounts, named sources, and documentary evidence.

The essential problem with Ardoino's defense strategy was that it didn't adequately address the structural question: if USDT's transparency for law enforcement was genuine, why hadn't Tether's own analysis caught the Russian money laundering network before The Economist's investigation exposed it? If the company truly operated sophisticated compliance infrastructure, why did external journalists identify illicit activity that Tether's internal systems apparently missed?

Tether's response—that illicit usage represented an infinitesimal percentage of overall USDT circulation—while statistically true, didn't resolve the fundamental concern. The relevant question wasn't whether the vast majority of USDT users were legitimate. Obviously they were. The relevant question was whether Tether could definitively claim to have eliminated, prevented, or even adequately detected illicit use. The evidence suggested that significant money laundering operations had successfully utilized USDT despite the company's claimed law enforcement collaboration and compliance infrastructure.

The Comparative Advantage Argument and Its Limitations

Ardoino's comparative argument—that cash-based money laundering was harder to detect than USDT-based laundering—contained some analytical merit but also significant limitations. Yes, physical cash movements were notoriously difficult for law enforcement to detect. But the existence of a worse alternative didn't make a bad alternative acceptable. The fact that cash-based money laundering networks operated successfully didn't justify building a stablecoin that also enabled money laundering networks, just at somewhat lower detection costs.

This argument also overlooked the fundamental difference between making something slightly harder versus structurally impossible. Tether's argument suggested that USDT represented marginal improvements in law enforcement capacity compared to cash. But actual banking infrastructure provides genuine protections against money laundering—including Know Your Customer (KYC) requirements, Suspicious Activity Reporting (SAR) obligations, and regular regulatory audits. Tether's decentralized stablecoin structure, by contrast, allowed anonymous holders to transact with minimal friction.

Comparative Stablecoin Analysis: How USDT, USAT, and USDC Differ

Reserve Composition and Verification

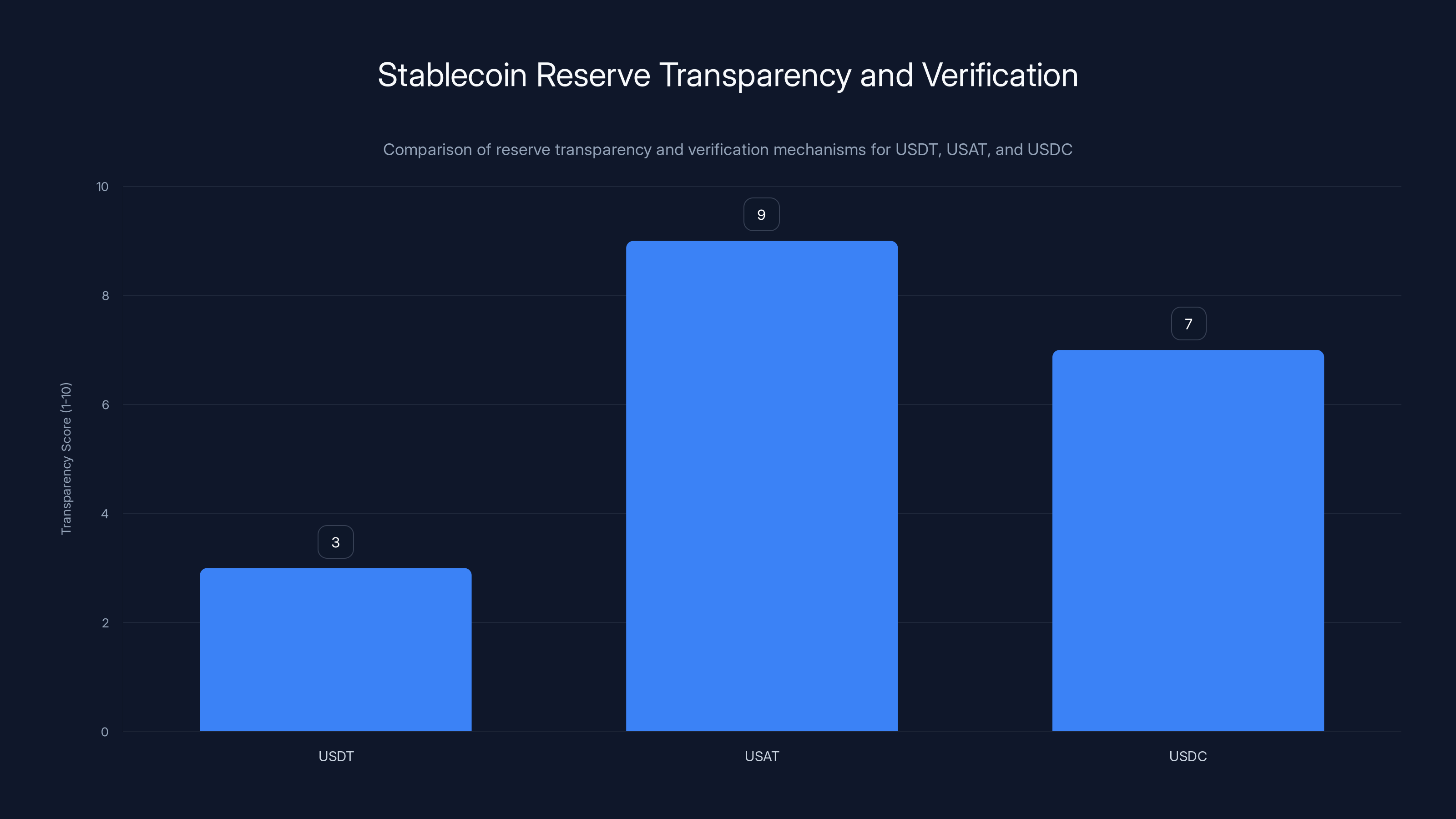

The critical difference between USDT, USAT, and USDC involved reserve composition and verification mechanisms. USDT promised full backing by dollar reserves but provided limited transparent verification—periodic attestations rather than full independent audits. USAT, being issued by Anchorage Digital Bank, operated under banking regulations requiring specific reserve maintenance ratios, regular audits, and regulatory oversight. USDC, while operating outside traditional banking, maintained transparent reserve reporting and allowed regular audits by third-party firms.

From a risk perspective, USAT's banking charter represented the highest assurance level. Regulators could examine Anchorage's books at any time, demand information, and enforce corrective action. USDC's approach, while less formally regulated, maintained transparency that enabled market participants to assess risk independently. USDT's approach retained maximum opacity while claiming the highest levels of backing—a stance that critics found least credible.

Blockchain Network Availability

Tether had deployed USDT across multiple blockchain networks: Ethereum, Tron, Solana, Polygon, Bitcoin Layer 2 solutions, and others. This multi-chain deployment created significant network effects and liquidity advantages. Every major exchange supported USDT because users expected it. Merchants accepted it because it was ubiquitous.

USAT's deployment strategy remained initially constrained—the company announced availability on specific networks but not the full breadth of Ethereum, Tron, and other deployments where USDT dominated. USDC similarly operated across multiple networks but with less extensive deployment than USDT. This fragmented availability gave USDT a genuine competitive advantage in liquidity and accessibility.

User Base and Geographic Distribution

The scale difference was staggering. USDT's 536 million users and 30 million quarterly growth rate vastly exceeded other stablecoins' adoption. USDC's user base, while substantial, was primarily concentrated in North America and Europe. USAT's initial rollout hadn't yet reached meaningful scale. From a network effects perspective, USDT's dominance was self-reinforcing—more users meant more merchants accepting it, more exchange support, deeper liquidity. USDT's massive user base in emerging markets was difficult for competitors to overcome.

USAT scores highest in reserve transparency due to banking regulations, followed by USDC with regular third-party audits. USDT scores lowest due to limited verification.

The Legitimacy Question: Is Regulatory Acceptance Credibility?

The Difference Between Legal Acceptance and Ethical Legitimacy

Tether's 2026 legitimacy offensive conflated regulatory acceptance with genuine credibility in ways that merit careful examination. The company's engagement with government agencies, its compliance infrastructure, and its USAT launch created legal legitimacy—the company was moving toward operational frameworks that U.S. regulators would accept. But legal legitimacy differed from ethical credibility about past conduct.

A company could become legally compliant while remaining ethically questionable about its origins. Tether's transformation from offshore opacity to regulated infrastructure addressed future conduct but didn't retroactively resolve questions about how Tether had operated during years when it maintained minimal transparency. The company was, in effect, negotiating regulatory amnesty—accepting compliance frameworks going forward in exchange for regulatory acceptance that overlooked past opacity.

The Precedent Problem: Does Financial Infrastructure Get Grandfathered?

What Tether's rise suggested was that sufficiently large and entrenched financial infrastructure, regardless of its origins, becomes politically difficult to dismantle or fundamentally restructure. With $187 billion in circulation, 536 million users, and transaction flows measured in the tens of billions of dollars daily, Tether had achieved a level of systemic importance that made radical regulation politically infeasible. The cost of constraining or shutting down Tether would be substantial—disrupting financial flows, destroying value, and disrupting commerce particularly in emerging markets dependent on USDT.

This dynamic suggested a troubling precedent: if a financial infrastructure company became large enough, its original sins and ongoing skepticism about its operations could be managed through integration into regulatory frameworks rather than resolved through enforcement action. The company maintained its original structure and benefited from the competitive advantages that scale provided, while accepting some regulatory oversight without losing the fundamental control mechanisms that had made it valuable.

Alternative Approaches: What Legitimate Stablecoin Infrastructure Looks Like

The Fidelity Model: Traditional Finance Enters Stablecoins

Fidelity Investments' stablecoin launch represented an alternative legitimacy pathway. Rather than trying to rehabilitate a cryptocurrency-native company with a questionable history, Fidelity leveraged its 75-year institutional reputation and regulatory track record to enter stablecoins. Fidelity's approach suggested that institutions could provide stablecoin functionality without requiring the equivalent of regulatory amnesty for historical conduct.

Fidelity's stablecoin benefited from the company's existing banking relationships, regulatory compliance infrastructure, and institutional governance frameworks. A major institutional player entering the market meant that users skeptical of Tether had a credible alternative backed by a name with demonstrated regulatory credibility.

The JPMorgan Model: Wholesale Infrastructure From a Global Bank

JPMorgan's JPMCoin occupied a different strategic position—wholesale payments infrastructure for interbank transfers rather than broad retail access. This positioning accepted regulatory limitations but also recognized that the primary value of stablecoins involved institutional settlement efficiency. Rather than trying to capture the consumer retail market, JPMorgan focused on its core competency—connecting major financial institutions with settlement infrastructure.

This approach suggested that stablecoin utility could be provided through traditional financial institution participation without requiring revolutionary transformation of banking infrastructure. JPMorgan's stablecoin represented evolution of existing banking systems rather than disruption of them.

The Circle/USDC Approach: Regulatory Compliance Without Traditional Banking

Circle's USDC represented a middle path—operating outside traditional banking while maintaining regulatory compliance and transparent operations. USDC didn't require a banking charter but accepted oversight and transparent reserve verification. This approach was less capitally efficient than Tether's model but more credible than Tether's historical opacity.

USDAC's slower growth compared to USDT suggested that regulatory compliance came with competitive costs. Users seemed willing to accept slightly less liquidity and network availability in exchange for greater regulatory certainty. But USDC demonstrated that legitimate stablecoin infrastructure was possible without Tether's scale advantages.

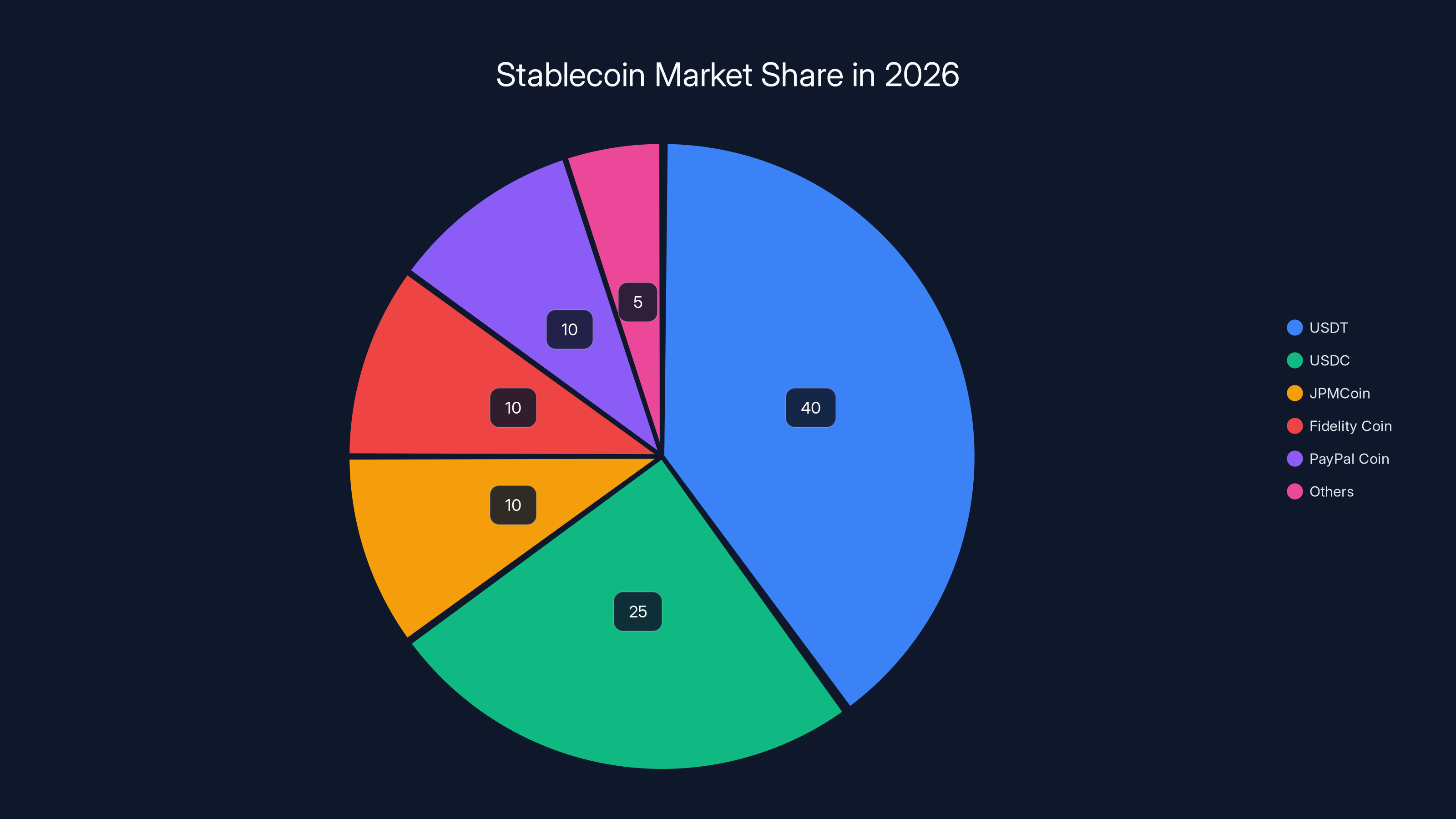

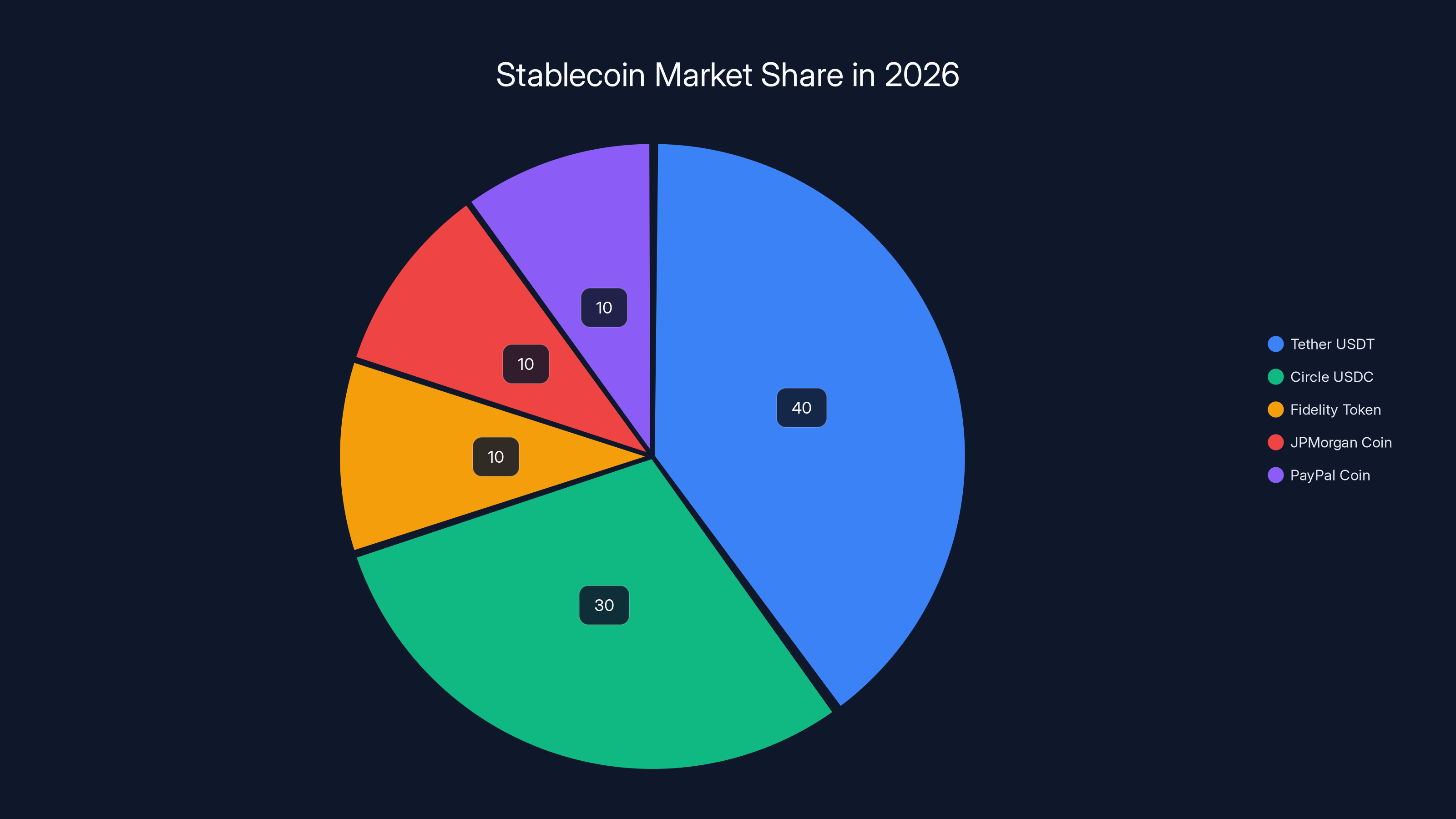

Estimated data shows Tether USDT holding a 40% market share in 2026, with increased competition from regulated stablecoins like Circle USDC and new entrants from major financial institutions.

The Systemic Importance Question: Too Big to Fail?

Concentration Risk in Global Financial Systems

Tether's dominance in global stablecoin markets created concerning concentration in financial infrastructure. A single private company—still ultimately controlled by a small group of individuals—maintained custody of $187 billion in assets representing the settlement mechanism for trillions in annual transaction volume. No traditional financial institution would be permitted to concentrate that much critical infrastructure without extensive government oversight, capital requirements, and governance restrictions.

The concentration became particularly concerning in emerging markets where USDT served as primary dollar-denominated value storage for populations excluded from traditional banking. If Tether failed, faced severe operational disruption, or made governance decisions contrary to users' interests, the consequences would be substantial for millions of individuals in countries already facing monetary instability.

The Systemic Disruption Scenario

The Federal Reserve and other central banks expressed concern about stablecoin systemic importance. If a stablecoin collapse triggered financial disruption affecting major markets, the consequences would ripple across financial systems. Central banks worried that stablecoins could become vehicles for bank runs in traditional banking systems—if institutional customers believed traditional banks faced problems, they might flee into stablecoins, undermining banking system stability.

Tether's dominance meant it occupied a critical node in this potential disruption scenario. Regulatory accommodation of Tether reflected partly policymakers' recognition that shutting down the company would be disruptive, but also the hope that regulatory integration might prevent catastrophic scenarios.

The 2026 Strategic Positioning: Tether's Path Forward

From Crypto Native to Financial Institution

Tether's 2026 positioning represented aspiration to transform from cryptocurrency-native company into legitimate financial infrastructure company. The USAT launch, government engagement, FBI collaboration, and Lutnick relationship all pointed toward institutional legitimacy rather than crypto market dominance. Ardoino's media offensive was designed to present Tether as already transformed rather than still transforming.

But the narrative faced an inherent credibility problem: Tether couldn't escape its history through strategic communication. The company's opacity, the historical questions about reserves, the documented use in money laundering networks—these facts remained regardless of how effectively Ardoino managed media relations. The legitimacy offensive was partially addressing perception problems that could be managed through better communication, but also underlying structural problems that required more fundamental changes.

The Competitive Threat from Institutional Entrants

Tether's dominance might face genuine threat from institutional entrants in ways that cryptocurrency competitors never achieved. Fidelity, JPMorgan, and PayPal brought customer relationships, regulatory relationships, and institutional credibility that Tether couldn't match. If institutions systematized their stablecoin offerings, users might gradually migrate from USDT to institutional alternatives simply because institutional stablecoins became integrated into mainstream financial technology.

This migration would likely occur gradually and unevenly. Sophisticated institutional users might preference regulated alternatives. Retail and emerging market users would likely remain with USDT due to network effects and existing adoption. But if the trend accelerated, USDT's dominance could gradually erode from the institutional segment while maintaining retail dominance.

The Reserve Question That Never Fully Resolves

No matter how effectively Tether executed its legitimacy strategy, the fundamental question about reserve composition remained partially unresolved. The company had accepted some level of transparency through USAT and banking relationships, but USDT itself remained less transparent than comparable institutional alternatives. As long as that opacity persisted, sophisticated observers would maintain skepticism about Tether's true reserve position and the company's financial health.

This suggested that Tether's legitimacy offensive was about managing rather than resolving credibility questions. The company would become more integrated into regulatory and institutional frameworks, but never achieve the complete transparency that true financial institutions provided. The strategy was to make that partial transparency sufficient for broad market acceptance while maintaining operational advantages that full transparency would eliminate.

Future Developments: What's Next for Stablecoins and Financial Infrastructure

Central Bank Digital Currencies as Ultimate Threat

One often-overlooked element of the stablecoin landscape was the potential for central bank digital currencies (CBDCs) to ultimately supplant private stablecoins. The Federal Reserve, European Central Bank, People's Bank of China, and other central banks were actively developing digital versions of their currencies. If CBDCs achieved broad deployment with institutional and retail support, they could gradually displace stablecoins like USDT, USDC, and USAT.

From a policy perspective, CBDCs represented regulators' preferred solution to stablecoin problems. Rather than trying to regulate private companies maintaining reserve-backed digital tokens, central banks would directly issue digital currency. This would eliminate the private intermediary and provide government-backed assurance of value and stability.

For Tether, this represented the ultimate competitive threat—not from other private stablecoins, but from government-issued alternatives that could eventually provide equivalent functionality with superior credibility. The company's 2026 legitimacy offensive was partly an effort to establish permanent presence before CBDCs potentially disrupted the market.

Blockchain Interoperability and Cross-Chain Settlement

The technical landscape was also evolving in ways that could affect stablecoin dominance. As blockchain networks became increasingly interoperable—allowing tokens and value to move freely between different blockchain layers and distinct chains—the advantage of deploying on a single dominant chain would diminish. Stablecoins that couldn't maintain sufficient liquidity across fragmented blockchain ecosystems might face pressure regardless of their initial dominance.

Tether's multi-chain deployment was a strength in this environment, but competitors could catch up. If institutional players prioritized specific blockchain environments where they concentrated liquidity, they might capture institutional trading even if retail users continued relying on USDT.

Regulatory Fragmentation and Jurisdictional Arbitrage

Another likely development was increasing regulatory fragmentation, with different jurisdictions taking divergent approaches to stablecoin regulation. Some countries might accept unregulated stablecoins like USDT while others mandated licensed issuers. Some might restrict stablecoin functionality while others promoted it. This fragmented landscape would create opportunities for regulatory arbitrage but also challenges for global stablecoin operators trying to serve multiple jurisdictions simultaneously.

Tether's strategy of developing both USDT (for less-regulated markets) and USAT (for regulated markets) anticipated this fragmentation. The company was essentially building separate products for different regulatory environments rather than trying to develop a single solution for all jurisdictions.

Implications for Developers and Technical Teams: Alternative Solutions and Platforms

For development teams considering how to integrate stablecoins into applications or how to build on stablecoin infrastructure, the landscape presented distinct options with different risk profiles and capabilities. Teams needed to evaluate not just technical functionality but the governance and regulatory underpinnings of their chosen stablecoin.

Tether's technical advantages—liquidity, multi-chain deployment, adoption breadth—remained meaningful for developers requiring maximum optionality and user accessibility. But teams prioritizing regulatory certainty and operational stability might select USDC or institutional alternatives. The choice involved trade-offs between maximum market reach and reduced regulatory risk.

For teams building automation or workflow tools designed for financial applications, the stablecoin choice could also impact operational architecture. Runable, for instance, offers AI-powered workflow automation and content generation tools that could streamline processes for fintech applications managing multiple stablecoin standards or helping organizations evaluate stablecoin strategies. The platform's ability to automate report generation and analysis could assist financial teams in comparative stablecoin assessment or risk analysis.

FAQ

What is USDT and how does it differ from traditional currency?

USDT (Tether) is a cryptocurrency token designed to maintain a stable value equivalent to the U.S. dollar through blockchain technology, allowing for instant cross-border transfers without traditional banking intermediaries. Unlike traditional currency held in banks, USDT exists as a digital token on multiple blockchain networks and can be transferred directly between users without requiring banking institutions or government oversight. The key theoretical difference is that USDT achieves stability through Tether's promise to maintain equivalent dollar reserves, whereas traditional currency is backed by government and central banking authority.

Why did Tether's CEO launch a media campaign in 2026?

Paolo Ardoino's media offensive in early 2026 was strategically timed to coincide with the launch of USAT, Tether's newly regulated stablecoin product, and to capitalize on the broadening institutional stablecoin market where major competitors like Fidelity and JPMorgan had entered. The campaign served to reposition Tether from its historically opaque offshore operations toward mainstream financial legitimacy through government collaboration, FBI coordination, and regulatory compliance frameworks. The timing also aligned with Howard Lutnick's position as Commerce Secretary, which provided unprecedented political access and institutional credibility for Tether's expansion narrative.

What is USAT and how does it differ from USDT?

USAT is Tether's new U.S.-regulated stablecoin issued through Anchorage Digital Bank, designed to comply with federal banking regulations and compete directly with Circle's USDC in the institutional market. Unlike USDT, which operates without explicit banking oversight or regulatory approval, USAT maintains traditional banking regulatory requirements including reserve verification, regular audits, and government supervision. USDT remains positioned for global cryptocurrency trading and emerging market use, while USAT targets institutional and regulated market adoption where regulatory compliance is required.

What are the advantages of stablecoins for emerging market users?

Stablecoins provide fundamental financial inclusion benefits for populations in countries experiencing monetary instability, currency devaluation, or limited access to banking infrastructure. In Argentina, where the peso lost 94.5% of its value against the dollar in five years, stablecoins offer value preservation without requiring access to traditional banks or international currency conversion. In Haiti and similar economies with collapsed or inadequate banking systems, stablecoins provide access to dollar-denominated financial systems for populations entirely excluded from institutional banking, protecting savings and enabling cross-border transactions without geographic or institutional constraints.

How can Tether freeze USDT tokens and is this a security feature or a control mechanism?

Tether maintains technical capability to prevent the movement of specific USDT tokens by using centralized controls available on blockchain networks where USDT is deployed. The company characterizes this capability as a security feature enabling law enforcement collaboration, pointing to examples like freezing

What are the credibility concerns about Tether's reserve backing?

Tether has historically maintained opacity about its reserve composition, locations, and custody arrangements, promising full backing by dollar reserves while providing only periodic attestations from accounting firms rather than full independent audits. Critics note that competitors like Circle offer more transparent reserve verification, and that regulatory-compliant alternatives like USAT provide formal banking oversight requiring regular audits and regulatory examination. The fundamental concern is whether Tether maintains truly sufficient reserves to honor all USDT claims in a stress scenario—a question that limited transparency makes impossible to definitively resolve, leaving users implicitly trusting Ardoino and Tether management without independent verification.

How do USDT, USDC, and USAT compare on regulatory compliance?

USTC operates without explicit banking charter or regulatory approval, relying on voluntary cooperation with law enforcement agencies and maintaining unilateral control over reserve composition. USDC operates outside traditional banking but maintains transparent reserve reporting and accepts regular third-party audits providing independent verification. USAT operates under banking regulation through Anchorage Digital Bank, requiring mandatory regulatory oversight, regular government examinations, specific reserve maintenance ratios, and compliance with banking laws. The regulatory framework increases assurance but also increases operational constraints and reduces Tether's unilateral control compared to USDT's permissioned architecture.

What is the relationship between Howard Lutnick's Commerce Secretary position and Tether's legitimacy strategy?

Howard Lutnick's role as Commerce Secretary creates unprecedented political access for Tether and institutional legitimacy through government association, while Cantor Fitzgerald's involvement in managing Tether's reserves provides additional financial infrastructure credibility. From Tether's perspective, this arrangement provides direct influence over cryptocurrency and financial services policy at the highest government levels. From a critical perspective, this configuration raises regulatory capture concerns—the possibility that a government official overseeing financial services policy maintains commercial interests in a cryptocurrency company that he partially oversees. While ethics guidelines presumably address these relationships, the appearance of conflicts between government responsibilities and commercial interests remains potentially problematic.

What are the systemic importance concerns about Tether's market dominance?

Tether's $187 billion in circulation with 536 million users and trillions in annual transaction volume means that a collapse or severe operational disruption would affect global financial flows, particularly in emerging markets where USDT serves as primary dollar-denomination storage. No traditional financial institution would be permitted to concentrate this much critical infrastructure without extensive government oversight, capital requirements, and governance restrictions. Central banks and financial regulators worry that stablecoin dominance by private companies could create systemic risk—potentially triggering bank runs if users lose confidence in traditional institutions and flee into stablecoins, or conversely if stablecoin operators face problems that disrupt financial settlement. This concentration explains why regulatory accommodation of Tether reflects policymakers' recognition that shutting down the company would be disruptive, combined with hope that regulatory integration might prevent catastrophic scenarios.

How might central bank digital currencies affect Tether's long-term viability?

Central bank digital currencies (CBDCs) represent the ultimate competitive threat to private stablecoins because they would provide government-issued digital currency with superior credibility and central bank backing, potentially displacing private stablecoins like USDT, USDC, and USAT as central banks deploy digital versions of their currencies at institutional and retail scale. From a policy perspective, CBDCs are regulators' preferred solution to stablecoin problems—eliminating the private intermediary and providing government assurance of value and stability. Tether's 2026 legitimacy offensive is partly an effort to establish permanent institutional presence and regulatory integration before CBDCs potentially disrupt the market, but long-term, government-issued digital currencies could gradually erode private stablecoin market dominance, particularly in regulated institutional segments where governments have direct authority to promote CBDC adoption.

Conclusion: The Legitimacy Question in Practice

Paolo Ardoino's transformation from offshore executive avoiding the United States to ubiquitous voice in mainstream financial media represents a pivotal moment in cryptocurrency's evolution toward mainstream acceptance. The media blitz, government engagement, and USAT launch signal Tether's ambition to transition from controversial crypto-native company to integrated financial infrastructure provider. Yet this transformation raises fundamental questions about whether regulatory acceptance and institutional integration constitute genuine legitimacy or merely sophisticated management of persistent credibility problems.

Tether's dominance is undeniable. With $187 billion in circulation, 536 million users growing at 30 million per quarter, and unmatched liquidity across cryptocurrency exchanges, USDT has achieved a form of market entrenchment that competitors struggle to overcome. The network effects protecting USDT—deep liquidity, universal exchange support, broad merchant acceptance—represent genuine competitive advantages that regulatory approval alone cannot displace. For institutions and users requiring maximum optionality and market access, USDT remains the default stablecoin choice despite historical questions about the company's operations.

Yet Tether's benefits for financial inclusion, particularly in emerging markets devastated by monetary instability, are equally undeniable. In countries where traditional financial systems have failed or remain inaccessible, USDT provided real value to millions of people otherwise excluded from dollar-denominated financial systems. The humanitarian justification for Tether's continued existence isn't merely promotional rhetoric—it reflects genuine use cases where the stablecoin serves populations with limited alternatives.

The challenge is that both narratives can be simultaneously true. USDT can provide legitimate financial inclusion benefits while also being utilized by money launderers, sanctions violators, and other illicit actors. The company can maintain some law enforcement collaboration while remaining less transparent than regulatory-compliant alternatives. Tether can be integrating into government structures while also raising legitimate governance concerns about regulatory capture. These tensions can't be resolved through better communication or strategic positioning—they require wrestling with uncomfortable complexity.

For policymakers, the question is whether Tether's systemic importance justifies regulatory accommodation despite historical opacity and ongoing concerns. The company has become too large and too integrated into global financial flows to be easily unwound or fundamentally restructured. Regulatory engagement appears more feasible than enforcement action that would disrupt billions in daily transactions. Yet accommodation without fundamental reform simply validates the principle that sufficiently large financial institutions can escape accountability by making themselves too big to fail.

For users evaluating stablecoin choices, the landscape now offers genuine alternatives. Circle's USDC provides comparable functionality with greater regulatory certainty. Fidelity, JPMorgan, and other institutional entrants offer alternatives backed by established financial institutions with demonstrated regulatory credibility. USAT itself provides Tether's ecosystem with a regulated alternative for users prioritizing compliance. The competitive environment has matured beyond Tether's historical dominance—users can now select among options based on their specific risk profiles and regulatory preferences.

For developers and teams considering stablecoin integration, this environment presents both risks and opportunities. The concentration risk in USDT dominance justifies evaluation of institutional alternatives. The competitive landscape suggests that users increasingly distinguish between regulatory compliance levels and will support alternatives offering greater certainty. The rise of institutional stablecoin offerings indicates that development teams should anticipate a fragmented landscape where different applications require different stablecoin choices based on their regulatory, technical, and operational requirements.

Tether's 2026 legitimacy offensive ultimately reveals less about the company's transformation and more about cryptocurrency's maturation. As the technology moves from speculative fringe toward mainstream financial infrastructure, the questions that once seemed academic become practically consequential. Can financial systems operate at scale without traditional regulatory authority? Can cryptocurrency achieve institutional adoption while retaining decentralized principles? Can private companies maintain trust when they control financial infrastructure affecting millions of users?

These questions won't be definitively answered by Ardoino's media appearances or government engagement. They will be answered through years of operational history, competitive pressure from institutional alternatives, potential regulatory intervention or accommodation, and the ultimate competitive outcomes in stablecoin markets. Tether may successfully integrate into regulatory frameworks while maintaining its market dominance. It may gradually lose institutional and emerging market share to alternatives offering greater certainty. It may eventually face constraints or restrictions from government action. All scenarios remain possible.

What seems clear is that Tether's evolution from controversial crypto experiment to mainstream financial player marks an inflection point for cryptocurrency broadly. The technology that was conceived as trustless, decentralized alternative to financial institutions is now seeking legitimacy through integration with those same institutions. The outcome will determine whether cryptocurrency becomes genuinely transformative financial infrastructure or remains a niche domain appealing to specific use cases and user preferences. For billions of potential users in emerging markets and for the infrastructure providers trying to serve them, the stakes of Tether's legitimacy question are genuinely consequential.

Key Takeaways

- Tether's 2026 media offensive marked strategic shift from offshore operations toward regulatory integration and mainstream legitimacy

- USAT launch represents direct competition with Circle's USDC in regulated institutional market while USDT maintains dominance in unregulated global trading

- Howard Lutnick's Commerce Secretary position created unprecedented political access and raised regulatory capture concerns despite strengthening Tether's institutional credibility

- $187 billion in circulation with 536 million users gives USDT systemic importance making complete regulatory constraint politically infeasible

- Emerging markets represent genuine financial inclusion success story where USDT provided value to populations excluded from traditional banking

- Documented use in money laundering networks despite law enforcement collaboration raised credibility questions that regulatory acceptance doesn't fully resolve

- Institutional alternatives including Fidelity, JPMorgan, and Circle now provide users genuine choices based on regulatory compliance and transparency preferences

- Central bank digital currencies represent ultimate competitive threat to private stablecoins by offering government-backed alternatives with superior credibility

- Tether's evolution from crypto-native company to financial infrastructure illustrates broader cryptocurrency maturation toward institutional adoption

- Regulatory accommodation reflects acknowledgment that USDT became too systemically important to fundamentally disrupt while hoping integration prevents catastrophic scenarios