![Uber's Autonomous Solutions: The Robotaxi Platform Redefining AV Mobility [2025]](https://tryrunable.com/blog/uber-s-autonomous-solutions-the-robotaxi-platform-redefining/image-1-1771889879749.jpg)

Introduction: The Pivot From Building to Enabling

There's a moment in every platform company's journey when they realize something crucial: they can make more money enabling others than building everything themselves. For Uber, that moment arrived with the announcement of Uber Autonomous Solutions, a strategic shift that marks one of the most interesting pivots in autonomous vehicle history.

Five years ago, Uber was building its own autonomous vehicles. The company poured billions into Uber ATG (Advanced Technologies Group), assembled teams of roboticists and engineers, and believed—like most of the industry—that controlling the entire stack was the path to dominance. Then a test vehicle killed a pedestrian in Tempe, Arizona in 2018. The cultural shock rippled through the organization. Two years later, in a complex restructuring deal, Uber sold ATG to Aurora.

That sale looked like a retreat. But it was actually a strategic reposition. Instead of competing directly with specialized AV makers, Uber is now building the infrastructure layer that makes those companies work. Think of it like this: during the California Gold Rush, fortunes were made not by miners striking gold, but by companies selling pickaxes and shovels.

Uber Autonomous Solutions is the pickaxe vendor for the autonomous mobility ecosystem.

The division officially launched in February 2025, formalizing years of quiet work behind the scenes. The company has been investing in AV startups, building partnerships with nearly two dozen autonomous vehicle technology companies, and quietly constructing the operational backbone that every robotaxi, delivery robot, and autonomous truck needs to function at scale.

What makes this moment significant isn't just that Uber is entering a new business line. It's that Uber is becoming the platform that stands between AV technology and commercial viability. That's an enormous shift in how autonomous mobility might actually reach mainstream adoption.

Understanding Uber Autonomous Solutions: More Than a Software Play

When Sarfraz Maredia, Uber's global head of autonomous mobility and delivery, talks about Uber Autonomous Solutions, he's careful not to call it a software company. It's not. It's an operating system wrapped around autonomous mobility operations.

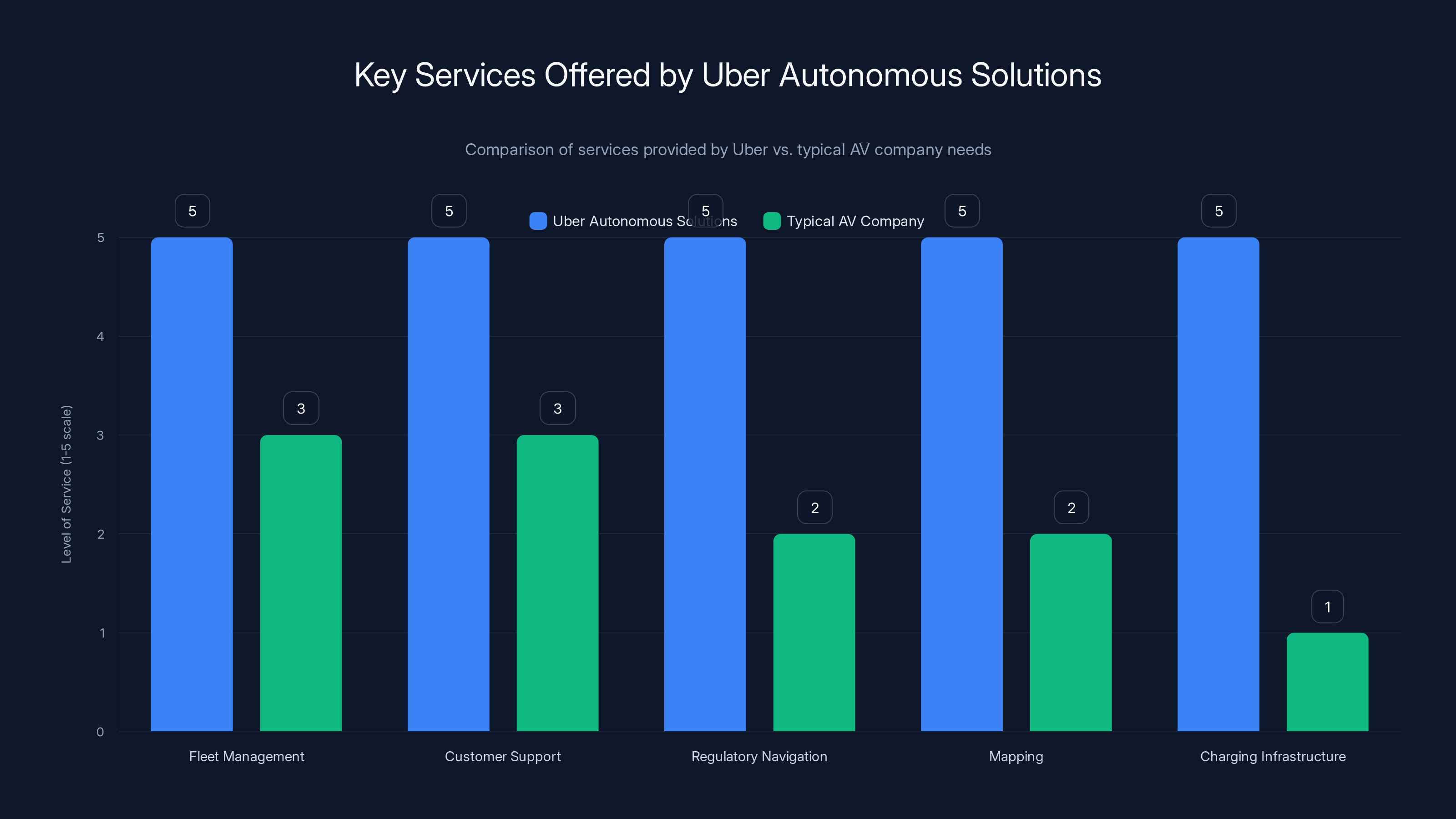

The core idea is deceptively simple: AV makers need to focus on their core competency—developing safe, reliable autonomous driving technology. Everything else? Insurance, fleet management, customer support, regulatory navigation, demand generation, data infrastructure, remote assistance networks—that's where complexity explodes. Uber is saying it will own that complexity.

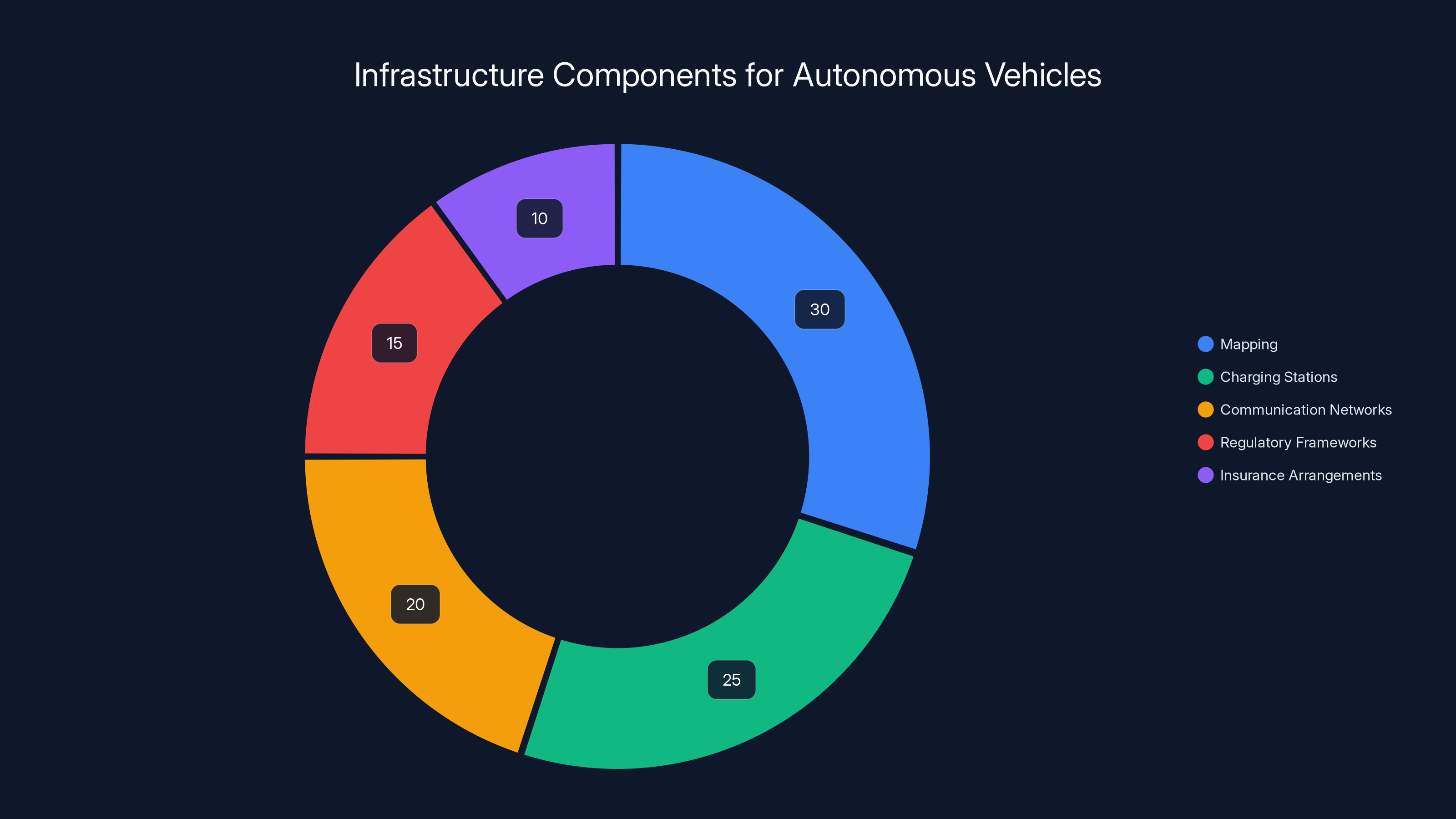

Consider what it takes to operate a robotaxi service. You need mapping infrastructure that covers every street in every city where you operate. You need real-time traffic data. You need to train machine learning models on millions of miles of driving data. You need regulatory relationships in every jurisdiction. You need customer support available 24/7. You need insurance arrangements. You need financing for vehicles. You need algorithms to optimize routes and match riders. You need backend systems to handle payment. You need incident response capabilities.

That's not operating a robotaxi business. That's operating a technology infrastructure that enables multiple competing AV makers to operate robotaxis.

Uber's angle is that it's already built much of this infrastructure for its human-driver ride-hailing business. When someone orders an Uber today, they're using routing algorithms, payment systems, customer support infrastructure, and incident management that cost billions to develop. Uber is essentially amortizing those costs across a new revenue stream.

The business model here is worth understanding. Uber isn't selling software licenses. It's selling operational depth. An AV startup spends engineering time on things like fleet management software, customer support systems, and regulatory compliance. Uber says: stop. Let us handle that. Let your engineers focus exclusively on the autonomous driving problem.

For that service, Uber takes a cut of the revenue. How large a cut? The company hasn't disclosed final terms, but the structure is clear: Uber benefits when AV partners succeed and scale. The incentives are aligned.

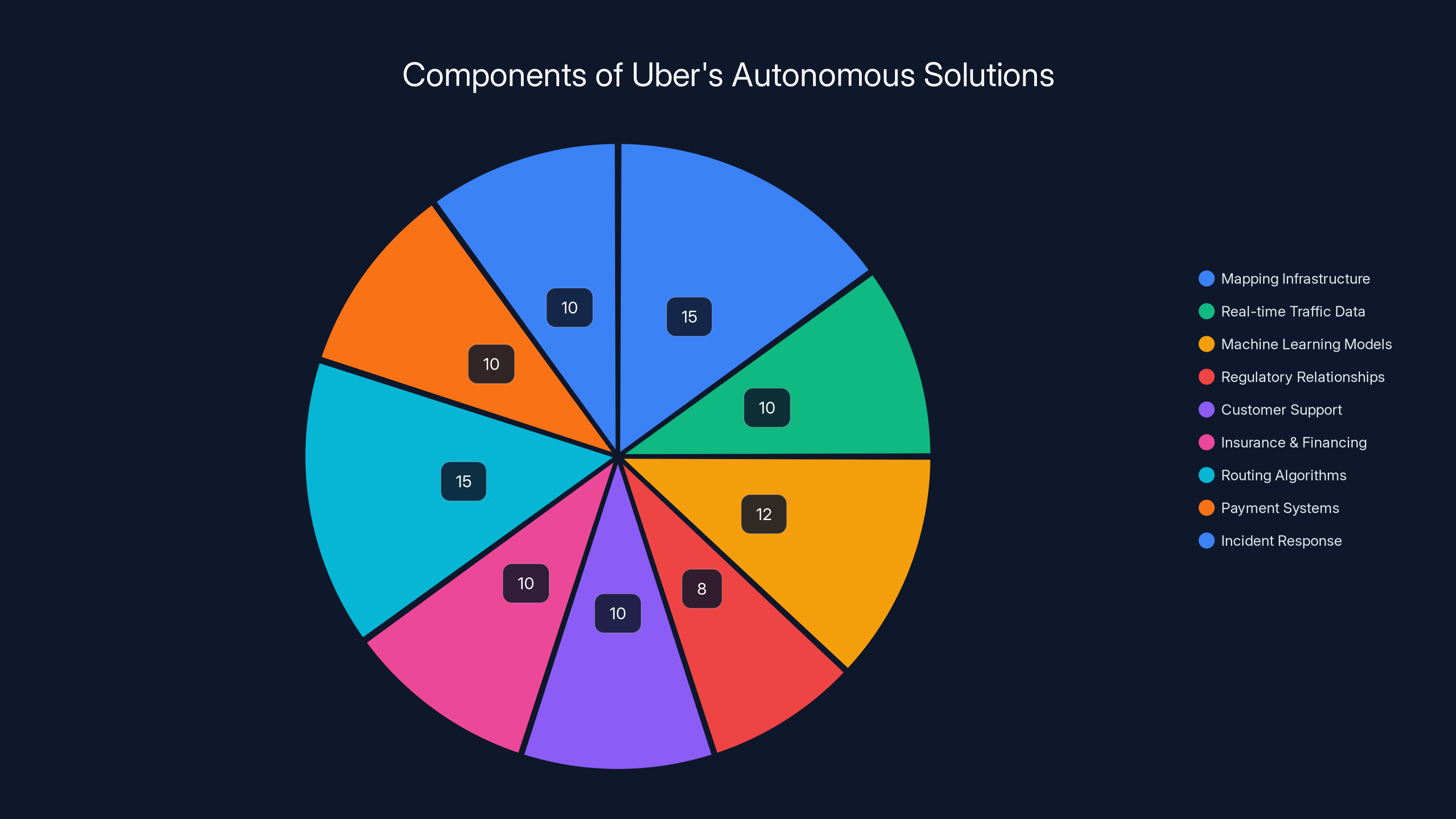

Uber Autonomous Solutions provides comprehensive services across multiple domains, allowing AV companies to focus on technology development. Estimated data based on service offerings.

The Partnership Ecosystem: Building an AV Alliance

You can't understand Uber Autonomous Solutions without understanding the network of partnerships Uber has assembled. This isn't a coincidence. It's a deliberate strategy to position Uber as the indispensable operating layer for autonomous mobility.

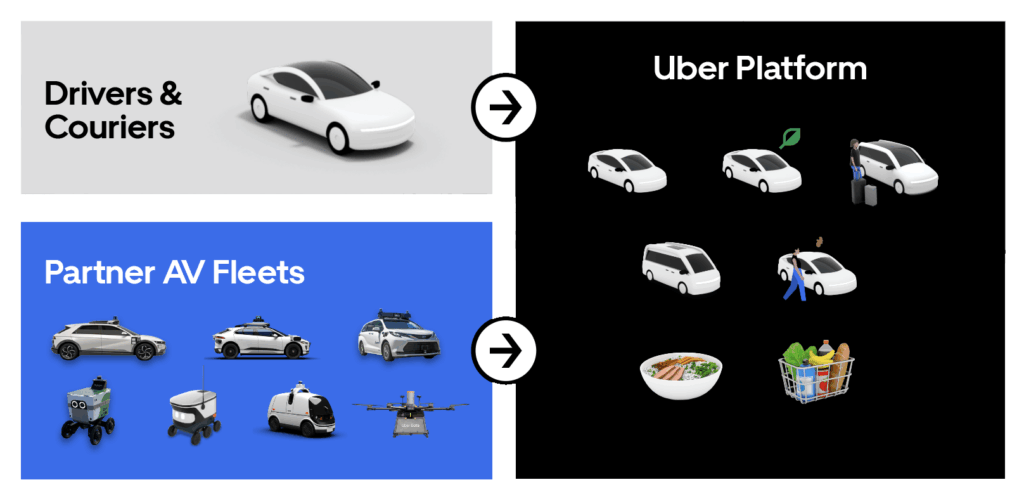

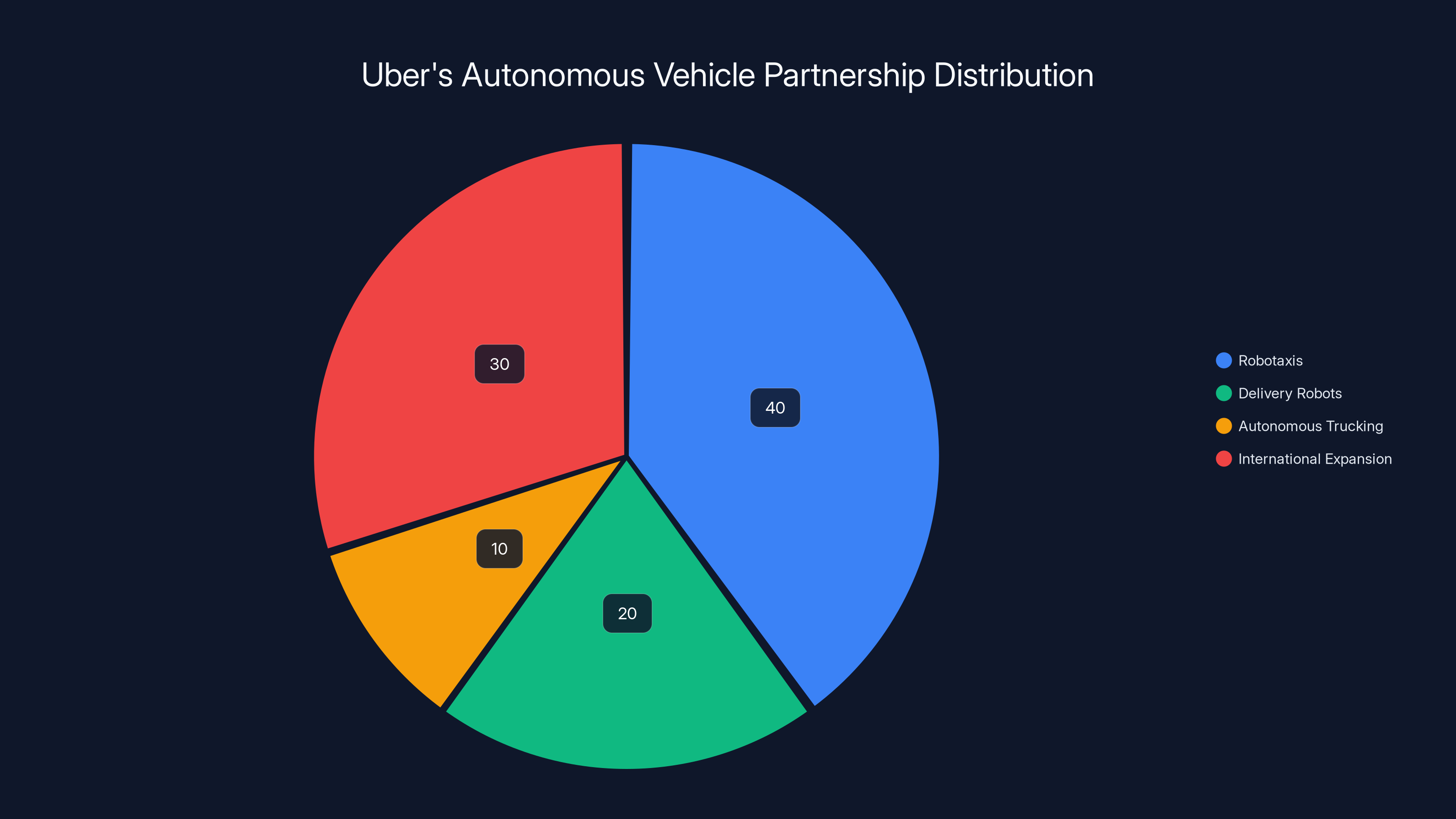

The partnerships span every relevant segment. Robotaxis: Waymo (joint Atlanta and Austin service), Volkswagen (Los Angeles launch planned for end of 2026), Motional, AVride. Delivery robots: Cartken, Starship, Serve. Autonomous trucking: Waabi. International expansion: China's We Ride, Baidu, Momenta, Pony.ai, UK-based Wayve.

That's not just partnerships. That's ecosystem dominance.

Each partnership gives Uber strategic optionality. If one AV maker stumbles, Uber has others. If one technology approach fails, alternatives exist. Most importantly, each partnership gives Uber data. Every vehicle operating through Uber's infrastructure generates information about how autonomous systems behave in real-world conditions. That data becomes proprietary. It becomes competitive advantage.

The financial commitments reinforce the partnership strategy. Uber invested $100 million specifically in fast-charging infrastructure for autonomous vehicles. That's not a casual investment. That's saying: we believe in this so much that we're building the electricity grid to power it.

Uber also established AV Labs, a specialized engineering team focused on gathering and analyzing data that helps robotaxi partners train their machine learning models better and faster. An AV startup can tap into that data pipeline. They get better training data than they could compile independently. Their models improve. Their safety metrics improve. Their path to deployment accelerates.

This creates lock-in without forcing it. Partners don't feel trapped. They feel enabled.

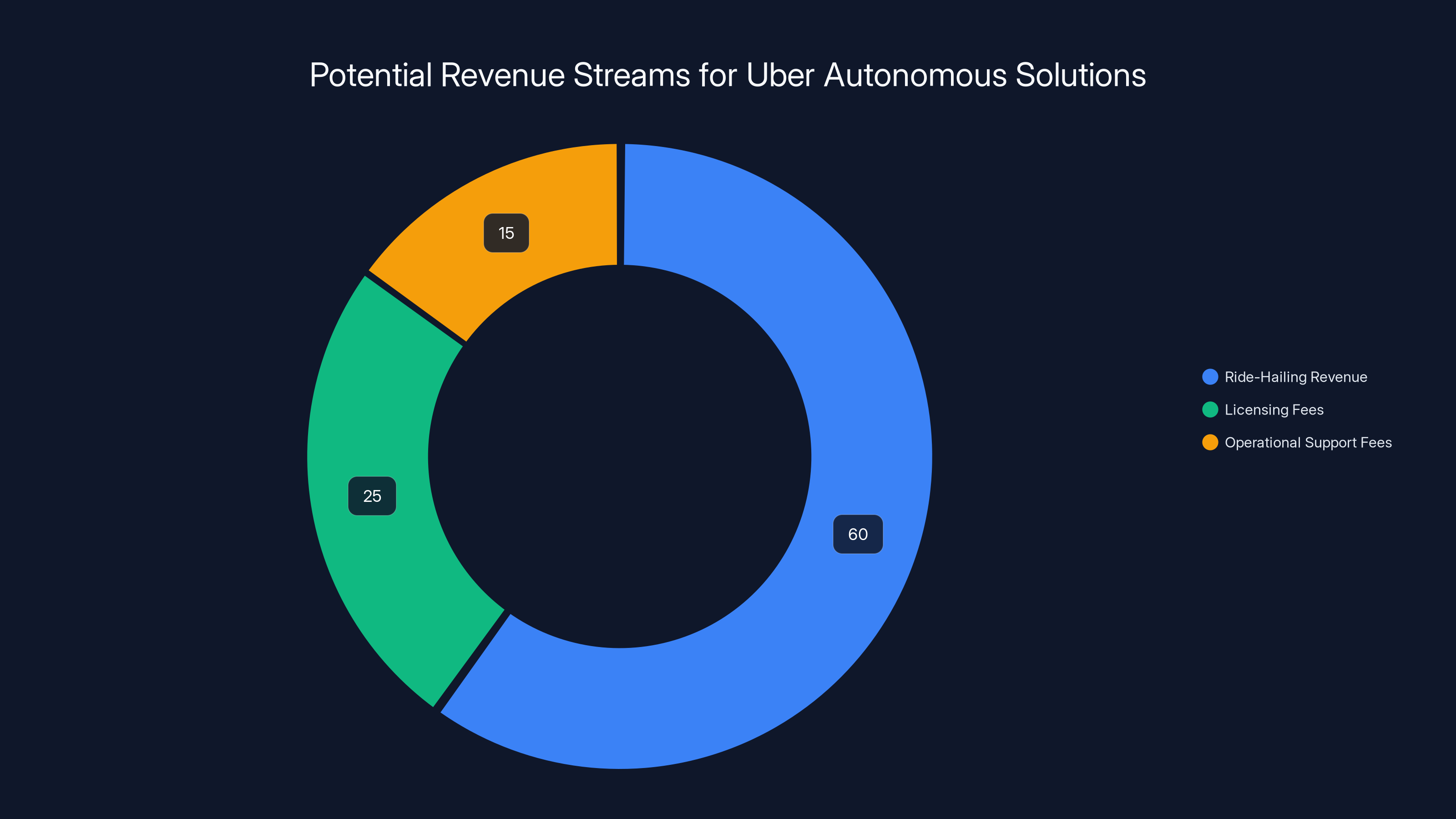

Estimated data suggests Uber's revenue from autonomous solutions could primarily come from ride-hailing (60%), with significant contributions from licensing (25%) and operational support fees (15%).

The Data Advantage: Training AI Models at Scale

There's a hidden layer to Uber Autonomous Solutions that separates it from typical software platforms: data. Specifically, the data required to train autonomous driving systems.

Building a self-driving system requires exposing machine learning models to millions of miles of driving footage, edge cases, failure modes, and unusual scenarios. A startup building AVs in isolation faces a brutal data collection problem. They need to deploy vehicles, drive them millions of miles (or simulate millions of miles), capture that data, label it, and use it to train models.

Uber is solving this for partners by operating a fleet of specially equipped Lucid vehicles that collect driving data across multiple cities and conditions. This isn't just helping partners. It's creating a data moat.

Here's why this matters: the company with the best, most diverse, highest-quality training data wins in autonomous driving. Not necessarily the company with the smartest engineers. The data. The company with 50 million miles of real-world driving data from 50 different cities has an advantage over the company with 50 million miles from 2 cities.

By controlling the data collection and curation process, Uber becomes critical to partner success. Partners get access to better training data than competitors. Their models train faster. Their safety metrics improve more quickly.

There's also a regulatory angle here. Federal regulators and safety organizations increasingly want to see evidence that autonomous systems have been exposed to edge cases and failure modes. The more diverse the training data, the stronger the safety case. Uber's data sharing becomes regulatory advantage for partners.

Infrastructure as Strategic Moat: Mapping, Charging, and Beyond

Autonomous vehicles don't exist in a vacuum. They require infrastructure: updated maps, charging stations, communication networks, regulatory frameworks, insurance arrangements.

Uber's $100 million commitment to fast-charging infrastructure for autonomous vehicles is strategic in ways that extend far beyond altruism. When Uber funds charging station development, it's not just enabling AV deployment. It's creating a dependency. Partners need charging. Uber controls charging. Partners depend on Uber.

Similarly with mapping. Modern autonomous vehicles rely on precise, constantly updated maps showing not just roads but detailed features: lane markings, traffic light positions, curb heights, historical traffic patterns, construction zones. Building and maintaining mapping infrastructure is expensive and ongoing. Lucid vehicles in the Uber data collection fleet are simultaneously updating and improving mapping coverage across regions where Uber operates.

Partners get access to this mapping data. They don't have to build it independently. They deploy faster. Their vehicles operate with better safety margins because they're navigating with more accurate maps.

There's also communication infrastructure. Remote assistance—the ability for human operators to take control or guide autonomous vehicles through complex situations—requires low-latency network connectivity. Uber is building that infrastructure. Partners can plug into it. They don't have to develop it separately.

This infrastructure approach reflects lessons learned from mobile platforms. Apple and Android didn't succeed because they were better operating systems. They succeeded because they abstracted away complexity. Developers didn't need to understand cellular networks, GPS, touch screen hardware, or device management. The platform handled that. Developers focused on apps.

Uber Autonomous Solutions is doing the same thing. AV developers focus on driving software. Uber handles everything else.

Mapping and charging stations are crucial components, comprising over half of the infrastructure needs for autonomous vehicles. Estimated data.

Fleet Management and Remote Assistance: The Human Layer

Here's what doesn't get discussed enough in autonomous vehicle coverage: the human layer. No matter how good autonomous driving technology becomes, situations will arise requiring human intervention or judgment. How that's handled matters enormously—both operationally and politically.

Uber's fleet management service includes remote assistance. This means human operators, somewhere in the world, can take control of vehicles or provide guidance when needed. This capability recently became a political issue when federal lawmakers raised concerns about Waymo's use of remote operators based overseas. The concern: labor practices, oversight, security.

Uber is positioning fleet management as an advantage over competitors. Instead of partners handling remote assistance independently, Uber manages it. That means trained operators, consistent oversight, and potentially better optics around labor practices.

Fleet management also includes insurance and employment. If a remote operator needs to take control of a vehicle, who's responsible? If something goes wrong, who pays? These are questions that Uber solves through fleet management. Partners don't have to figure it out.

There's also the pure operational aspect: tracking vehicle maintenance, scheduling repairs, managing vehicle lifecycle, handling accidents and incidents. Uber operates thousands of human-driver vehicles today. The fleet management infrastructure for that can be adapted for autonomous vehicles. It's another case of amortizing existing costs.

The human layer also matters for incidents. When an autonomous vehicle gets into an accident, who manages the response? Who talks to police? Who documents what happened? Who analyzes why it happened? Uber can provide that as a service, leveraging expertise from managing thousands of incidents daily with human drivers.

Demand Generation and Customer Experience: The Revenue Side

This is the side of Uber Autonomous Solutions that gets the least attention but might be most valuable: demand generation and customer experience.

Building a good autonomous vehicle is hard. Convincing people to ride in it is a different problem. Consumer adoption of robotaxis has been slower than many predicted, partly because of safety concerns, partly because of poor user experiences, partly because of limited availability.

Uber is a consumer brand with brand recognition. When Uber operates a robotaxi service (even with Waymo's driving software), that carries consumer confidence. Uber has infrastructure for rider support. Uber has reputation management. Uber has payment integration that customers already trust.

For AV partners, this is valuable. Instead of building consumer trust from scratch, they leverage Uber's. Instead of building customer support infrastructure, they use Uber's. Instead of managing the complexity of consumer payments, they let Uber handle it.

Demand generation is perhaps the most underrated aspect of Uber Autonomous Solutions. A startup producing autonomous driving software can't easily generate demand for robotaxi rides. They don't have a consumer app. They don't have consumer relationships. Uber has millions of users. When Uber offers a robotaxi option, those users see it. Demand materializes.

That's why Uber's plan to scale partners to 15+ cities by end of 2025 is credible. It's not that the AV technology suddenly becomes universally available. It's that Uber's scale and demand-generation capability enables accelerated deployment.

Uber's partnerships are distributed across various segments with a focus on robotaxis and international expansion, highlighting their strategy for ecosystem dominance. (Estimated data)

The Competitive Threat: Why Established AV Makers Should Be Concerned

Waymo, Cruise, and other established autonomous vehicle companies built end-to-end businesses. They developed the driving technology. They built consumer experiences. They managed operations.

Uber's model disrupts that. By breaking apart the stack and allowing specialists to own different layers, Uber potentially fragments value capture.

Consider Waymo's model. Waymo invests heavily in autonomous driving technology. Waymo also invests in consumer branding and operations. Waymo captures value across both layers. But if Waymo can license their driving technology to work with Uber's operations infrastructure, do they need to invest in operations themselves? Could they focus purely on technology?

That's actually good for Waymo in some ways (focus, efficiency) and bad in others (lower margin capture, reduced control over customer relationship).

The real threat comes for mid-tier AV companies. Companies investing

This potentially accelerates innovation in the driving technology layer—more competition, faster improvement—while concentrating operational control with Uber. That's a platform dynamic: enable innovation in layers above and below, concentrate power at the platform level.

For Uber, that's strategically perfect. The company doesn't need to be the best at autonomous driving. It needs to be the essential operating layer that all autonomous vehicles depend on.

Regulatory Navigation: The Invisible Layer

One aspect of Uber Autonomous Solutions that rarely gets discussed: regulatory services. But it's enormous.

Autonomous vehicle deployment requires approval from multiple regulatory bodies. Federal level: NHTSA and FMCSA set rules for autonomous vehicles. State level: most states regulate AV testing and deployment differently. Local level: cities impose their own requirements.

An AV startup needs to navigate this patchwork. Different documentation for different jurisdictions. Different safety requirements. Different insurance arrangements. Different permitted operating areas.

Uber navigates this for human-driver services in all those jurisdictions. That infrastructure exists. Uber Autonomous Solutions can provide regulatory guidance and potentially leverage relationships with agencies across these jurisdictions.

This isn't a small advantage. It's the difference between a 6-month regulatory process and an 18-month process. It's the difference between operating in 3 cities and operating in 15 cities by year-end.

Regulatory relationships are often invisible to consumers and investors. But they're absolutely critical for deployment speed. Uber has accumulated 15+ years of regulatory relationship capital. Partners benefit from that directly.

Uber's autonomous solutions focus on multiple operational components, with significant emphasis on mapping infrastructure and routing algorithms. Estimated data.

The Financing Question: How Uber Makes Money

Uber hasn't publicly detailed the financial terms for Uber Autonomous Solutions. But the model is clear enough to understand.

Uber likely takes a percentage of ride-hailing or delivery revenue generated through its platform by partner vehicles. Maybe 20-30% of revenue, comparable to Uber's cut of human-driver rides (typically 25% in the US, varies by market).

Alternatively, Uber could charge licensing fees for infrastructure, data, and operational support. Flat monthly fees. Per-vehicle fees. Usage-based fees. Or a combination.

The economics work because Uber's marginal costs are low. The infrastructure is already built for human-driver services. Extending it to autonomous vehicles increments costs in mapping updates, data handling, and support infrastructure, but not dramatically.

At scale, this could be extremely profitable. If Uber takes 25% of

That's the size of the prize Uber is playing for. Not by being the best autonomous vehicle maker, but by being the platform that enables all autonomous vehicle makers.

Partnerships With Established Players: The Waymo-Uber Relationship

The Waymo-Uber partnership in Atlanta and Austin is a practical demonstration of how Uber Autonomous Solutions works in practice.

Waymo develops the autonomous driving technology. Waymo's vehicles operate on Waymo's software stack. But riders access Waymo robotaxis through the Uber app. Customer support is Uber. Payment is Uber. Logistics and routing optimization is Uber.

Riders don't really care that it's Waymo technology. They care that they opened Uber, requested a ride, got picked up by a robot, and paid through their trusted payment method.

That partnership benefits both parties. Waymo gets access to Uber's demand generation and scale. Uber gets access to what might be the best autonomous driving technology available. Riders get options and safety.

The Volkswagen partnership for Los Angeles represents a different model. Volkswagen is a legacy automaker entering the robotaxi space. Volkswagen doesn't want to become an operations company. Volkswagen wants to sell vehicles and provide driving technology. Uber Autonomous Solutions handles everything else. Volkswagen launches faster, with less capital expense, with lower operational risk.

That's the partnership value prop: focus on what you're good at. Let Uber handle operations.

Waymo and Cruise invest heavily in both technology and operations, while mid-tier companies face challenges. Uber's model potentially reduces operational investment needs, allowing more focus on technology. (Estimated data)

International Expansion: We Ride, Baidu, and the China Advantage

Uber's partnerships with Chinese AV companies (We Ride, Baidu, Momenta, Pony.ai) reveal an interesting strategic dimension.

China has different regulatory frameworks, different consumer expectations, and a different competitive landscape than the US. Chinese AV companies are well-funded and technically sophisticated. But they lack Uber's operational scale and brand presence internationally.

These partnerships allow Chinese AV companies to expand into global markets potentially using Uber's infrastructure. Meanwhile, Uber gains access to advanced Chinese autonomous driving technology without investing billions to develop it independently.

It's a mutual benefit arrangement that reflects broader platform strategy: we'll provide the operations layer, you provide the technology layer.

China's rapid autonomous vehicle progress over the past few years—particularly from companies like Baidu and Waymo's Chinese competitors—suggested that geography-specific development was crucial. By partnering with Chinese companies, Uber stays connected to that innovation while maintaining its position as the global operational platform.

The Threat to Traditional Ride-Sharing: Autonomous Disruption of Uber's Core Business

There's an uncomfortable truth in Uber's strategy: autonomous vehicles fundamentally threaten Uber's core business model. If robotaxis fully replace human drivers, Uber's ride-hailing margins improve (no driver costs), but the business model shifts from taking a percentage of driver earnings to taking a percentage of vehicle costs.

The transition creates risk. During the period when both autonomous and human-driven services operate, Uber manages multiple networks. Consumers' choice between human and autonomous drivers impacts driver earnings and company economics.

Uber Autonomous Solutions could be interpreted as Uber trying to own the transition. Instead of being disrupted by autonomous vehicles, Uber is enabling and controlling their deployment. By becoming the platform for all autonomous vehicles, Uber benefits regardless of which AV company wins.

But there's another interpretation: Uber is protecting against the scenario where AV technology owners (Waymo, Tesla, others) start operating competing robotaxi services directly. If Waymo controls both the driving software and the operations platform, Uber becomes irrelevant. By positioning Uber as the essential operations layer, Uber reduces that risk.

That's existential strategy, not just opportunistic business development.

Comparing Uber's Approach to Competitors: Who's Executing at Scale?

Waymo, Cruise, and other standalone AV companies are building integrated businesses. They develop technology. They operate services. They manage consumers.

Tesla takes a different approach. Tesla integrates autonomy capability into vehicles it manufactures and sells. Tesla's strategy is vehicle distribution, not operations platform.

Uber's approach—becoming the operations platform—is distinct. It's closer to how AWS operates in cloud computing: provide infrastructure that others build on top of. Or how Stripe operates in payments: become the essential layer between commerce and payment processing.

The question is whether this model works for autonomous mobility. Does every AV maker need Uber's operations infrastructure? Or do large, well-capitalized companies like Waymo, Tesla, and established automakers like Volkswagen and Volvo just build their own?

Uber's bet is that specialization drives better outcomes. Companies focused exclusively on autonomous driving write better software. Companies focused exclusively on operations and customer experience do that better. Forcing one company to excel at both is suboptimal.

That might be right. Or it might underestimate the advantages of integration and control. Tesla's strategy of owning the entire value chain might prove superior to specialized approaches.

The 15-City Roadmap: Aggressive Scaling and What It Requires

Uber's stated goal is to scale robotaxi deployments to 15+ cities by end of 2025. That's aggressive. Maybe unrealistically so.

For context: Waymo operates in 4-5 cities. Cruise doesn't currently operate commercially (as of early 2025, following regulatory issues). Most AV projects are limited to specific geographic areas with favorable regulatory conditions.

Uber's 15-city goal assumes several things. First, that its operational infrastructure actually makes deployment faster. Second, that regulatory approval processes can be accelerated. Third, that partners have vehicles ready for rapid deployment.

It's an ambitious timeline. But it's grounded in something real: Uber's operational expertise can materially reduce deployment timelines. The company routinely launches new services in new cities. That operational capability transfers to autonomous vehicles.

If Uber executes on this roadmap, it would represent the fastest robotaxi scaling to date. That would validate the Uber Autonomous Solutions model. If the roadmap slips significantly, it would suggest that autonomous vehicle deployment challenges run deeper than just operations.

The Long-Term Vision: Platform Consolidation in Autonomous Mobility

Take a step back and look at where this goes.

Uber is positioning itself as the Android of autonomous mobility. Not the best Android phone, but the platform that powers the ecosystem. Other companies build on Android. They compete on features, design, and hardware. But they all depend on the Android platform.

That's Uber's vision for autonomous mobility. Waymo, Volkswagen, We Ride, Motional—they compete on driving technology and vehicle hardware. But they all potentially operate through Uber's operations platform.

If that vision wins, Uber becomes one of the most valuable companies in the world. Not because Uber is the best at autonomous driving. Because Uber controls the layer that all autonomous vehicles depend on.

But that's not guaranteed. It depends on whether the platform approach actually creates value versus integrated approaches. It depends on regulatory approval and scaling execution. It depends on consumer adoption of robotaxis being as rapid as optimists hope.

The strategy is sound in theory. Execution determines if theory translates to reality.

TL; DR

- Uber Autonomous Solutions pivots the company from owning AV technology to operating the infrastructure layer all AV makers depend on, including data, fleet management, demand generation, and regulatory navigation.

- The platform approach leverages Uber's existing operational scale and infrastructure while allowing partners to focus on autonomous driving technology, theoretically accelerating overall ecosystem deployment.

- Uber has assembled partnerships spanning every major autonomous vehicle category: robotaxis (Waymo, Volkswagen, Motional), delivery robots (Cartken, Starship), autonomous trucks (Waabi), and international companies (We Ride, Baidu, Pony.ai).

- Data infrastructure and charging investments create strategic dependencies, positioning Uber as essential to partner success and training autonomous systems more effectively.

- The financial model takes a percentage of ride/delivery revenue generated through Uber's platform, potentially worth hundreds of billions annually if autonomous mobility reaches projected scale.

- Success depends on execution: scaling to 15+ cities by end of 2025, maintaining regulatory advantage, and proving that specialized platforms outperform integrated approaches.

FAQ

What exactly is Uber Autonomous Solutions?

Uber Autonomous Solutions is a division launched in February 2025 designed to provide operational infrastructure and services for autonomous vehicle makers. Rather than building its own autonomous vehicles (as Uber attempted with ATG before selling to Aurora), the division offers software, fleet management, data infrastructure, regulatory navigation, customer support, and demand generation services that enable other AV companies to deploy robotaxis, delivery robots, and autonomous trucks more quickly and efficiently.

How does Uber Autonomous Solutions work differently from just being an AV company?

Instead of owning the entire value chain, Uber is separating layers: autonomous driving technology (owned by partners like Waymo, Volkswagen, We Ride) and operational infrastructure (owned by Uber). Partners focus on developing safe, efficient autonomous driving software. Uber handles everything else: mapping, charging infrastructure, fleet management, customer support, regulatory approval processes, and demand generation. This specialization allows partners to move faster and Uber to operate at scale across multiple competing AV technologies.

Why would AV companies partner with Uber instead of building everything themselves?

Because building everything is expensive and slow. An autonomous vehicle company needs to develop driving technology and also handle fleet management, customer support, insurance, charging infrastructure, mapping, regulatory relationships, payment processing, and consumer marketing. Each of these is a complex domain requiring specialized expertise and ongoing investment. By using Uber's platform, AV companies reduce capital requirements, accelerate time-to-market, and let engineers focus exclusively on autonomous driving technology rather than being stretched across operations and customer experience.

What's the financial model for Uber Autonomous Solutions?

Uber hasn't disclosed exact terms, but the model is revenue-sharing: Uber takes a percentage (likely 20-30%) of ride-hailing or delivery revenue generated through its platform by autonomous vehicles. Since Uber's operational infrastructure is already built for human-driver services, the incremental costs of serving autonomous vehicles are relatively low, making the margins potentially very attractive. At scale, this could represent tens of billions of dollars in annual revenue.

How does data collection fit into Uber Autonomous Solutions?

Uber operates a fleet of specially equipped Lucid vehicles that collect driving data across multiple cities and conditions. This data is curated and shared with AV partners to train their machine learning models. Better training data means safer, more reliable autonomous systems. The data pipeline also improves mapping coverage, which benefits all partners. This creates a competitive advantage for Uber's partners and lock-in effects that make Uber's infrastructure more valuable over time.

What's Uber's realistic timeline for scaling to 15+ cities?

Uber's goal of 15+ cities by end of 2025 is ambitious compared to Waymo's current 4-5 city footprint. It's achievable if Uber's operational infrastructure materially accelerates deployment and if regulatory processes move faster than they have historically. However, this timeline depends on multiple variables: partner vehicle production capacity, regulatory approval speed, and the complexity of integrating diverse autonomous driving systems into Uber's operations platform. Meaningful progress toward this goal would validate the platform model; significant delays would suggest deployment challenges run deeper than operations.

Is this strategy a threat to Waymo and other standalone AV companies?

It presents both opportunity and threat. Waymo could license its driving technology while using Uber's operations platform, allowing Waymo to scale faster with less operational overhead. But it also means Waymo captures less end-to-end value and loses direct customer relationships. For mid-tier AV companies, Uber's platform makes it easier to compete without being fully integrated. For companies like Tesla building integrated businesses, Uber's approach represents a different model that may or may not prove superior. The ultimate winner depends on whether specialization or integration drives better outcomes in autonomous mobility.

How does Uber's own ride-hailing business interact with Uber Autonomous Solutions?

Uber's core ride-hailing business is both complementary and potentially disrupted by autonomous vehicles. In the near term, offering robotaxi options alongside human-driver rides creates choice for consumers and lets Uber experiment with autonomous scaling. Long-term, robotaxis eliminate driver costs, improving Uber's margins significantly. But the transition period creates complexity managing two different networks. By controlling the operations platform for autonomous vehicles, Uber benefits regardless of which AV technology wins, protecting the company against disruption while transitioning its business model.

What gives Uber credibility with AV partners regarding infrastructure quality?

Uber operates thousands of human-driver vehicles today in over 70 countries. The demand generation, customer support, payment infrastructure, and fleet management systems serving human drivers can be adapted for autonomous vehicles. Uber has 15+ years of regulatory relationships with agencies worldwide. Uber understands operational challenges at extreme scale. Partners aren't betting on Uber's theoretical promise; they're leveraging proven infrastructure that already exists at global scale.

Conclusion: The Platform That Powers Autonomous Mobility

Uber Autonomous Solutions represents one of the most strategically interesting pivots in autonomous vehicle history. The company that once bet everything on building its own autonomous vehicles is now betting that controlling the operations layer is more valuable than owning the technology layer.

There's solid reasoning behind this approach. Specialization often drives better outcomes than forcing one organization to excel at radically different domains. A company focused exclusively on autonomous driving can iterate faster and invest more efficiently than a company split between driving software, vehicle operations, customer service, and fleet management. Uber's operational infrastructure is real, proven at massive scale, and expensive for competitors to replicate.

But the strategy faces real constraints. Not every AV company will want to depend on Uber for critical operations. Waymo, Tesla, and other large, well-capitalized companies may prefer integrated control. Regulatory approval processes might not accelerate as much as Uber hopes. Consumer adoption of robotaxis might progress slower than optimists project, limiting the overall market size.

The next 12-24 months will reveal whether Uber's platform approach works. If the company successfully scales AV operations to 15 cities, integrates multiple competing AV technologies, and demonstrates that partners can scale faster and cheaper using Uber's infrastructure, then the model is validated. If deployment stalls or partners discover they can move faster independently, then integration and control might prove superior to specialization.

What's not in question is that Uber is positioned to play a significant role in how autonomous mobility reaches the mainstream. By pivoting from building to enabling, from direct competition to platform operation, Uber has increased its optionality dramatically. The company wins if Waymo dominates robotaxis. Wins if Volkswagen wins. Wins if Chinese companies lead. Wins because Uber controls the operations layer across all scenarios.

That's sophisticated strategic positioning. Whether it translates into the tens of billions of dollars Uber is implicitly betting on remains to be seen. But the chess move itself is undeniably clever.

Key Takeaways

- Uber shifted from building autonomous vehicles to operating the infrastructure platform all AV makers depend on for deployment and scaling

- The platform model separates autonomous driving technology (owned by partners) from operations infrastructure (owned by Uber), allowing specialization and faster deployment

- Uber's partnerships span robotaxis, delivery robots, autonomous trucks, and international companies, positioning Uber as the central ecosystem hub

- Data infrastructure, charging networks, and regulatory relationships create strategic dependencies that make Uber essential to partner success

- If executed successfully, Uber Autonomous Solutions could generate hundreds of billions in annual revenue by taking a percentage of all autonomous vehicle ride-hailing and delivery revenue globally

Related Articles

- Uber's Autonomous Solutions Division: The Robotaxi Strategy [2025]

- Waymo's Nashville Robotaxis: The Future of Autonomous Mobility [2025]

- Tesla's Full Self-Driving: Why Elon Musk's Promises Keep Missing [2025]

- Aurora Triples Driverless Truck Network: The Future of Autonomous Logistics [2025]

- Uber's New CFO Strategy: Why Autonomous Vehicles Matter [2025]

- Waymo's $16B Funding Round: The Future of Autonomous Mobility [2025]