![India's Zero Tax AI Initiative Through 2047: A Game-Changer for Global Cloud [2025]](https://tryrunable.com/blog/india-s-zero-tax-ai-initiative-through-2047-a-game-changer-f/image-1-1769965624977.jpg)

India's Aggressive Play for the Global AI Infrastructure Game

India just made a move that's impossible to ignore. On Sunday in February 2026, Finance Minister Nirmala Sitharaman announced something that sounds almost too good to be true: zero taxes on cloud services sold outside India if those workloads run from Indian data centers through 2047. That's a 21-year tax holiday aimed squarely at Amazon, Google, Microsoft, and every other cloud giant racing to build AI infrastructure. According to The Economic Times, this move is part of India's broader strategy to attract foreign investment in its tech sector.

Here's the thing. The global cloud computing market is restructuring in real time. Data centers aren't just utility infrastructure anymore—they're strategic assets. Countries are bidding against each other like it's an Olympic competition, and India just entered the game with a proposal so aggressive it raised eyebrows across the tech industry. As noted by StateTech Magazine, data centers are increasingly seen as critical strategic assets in the digital economy.

For cloud providers drowning in capex for new data centers, this is massive. We're talking about eliminating one of the biggest operational expenses across two decades. But India isn't doing this out of generosity. The country is positioning itself as the alternative hub for AI compute, betting that lower taxes plus engineering talent plus growing domestic demand equals the next wave of trillion-dollar cloud infrastructure investment. According to PwC's analysis, the global cloud market is expected to continue its rapid growth, making India's tax incentives even more attractive.

The proposal reflects a larger strategic calculation. The U.S. dominates cloud infrastructure today, but the political and regulatory environment has become unpredictable. Europe imposes strict data sovereignty rules. Asia's fragmented between competing jurisdictions. India sees an opening. It's offering stability, scale, and financial incentives that are hard to walk away from. As reported by JD Supra, data localization and sovereignty are becoming increasingly important in the global tech landscape.

But there's a catch, and it's a significant one. India faces real infrastructure constraints: power shortages, water stress, and capacity limitations that could slow deployment. The policy is visionary, but execution in a complex regulatory environment with infrastructure gaps remains the real test. According to Broadcom's predictions, the success of such policies hinges on overcoming these infrastructure challenges.

The Strategic Context: Why India, Why Now

India's move doesn't exist in a vacuum. It's a direct response to a fundamental shift in how cloud giants are thinking about geographic diversification. For years, the U.S. and Europe dominated AI infrastructure spending. But geopolitical tensions, data residency regulations, and the sheer scale of AI workloads are forcing hyperscalers to rethink their global footprint. As highlighted by Carnegie Endowment, AI adoption is driving significant changes in infrastructure needs globally.

Last October, Google announced it would invest

Microsoft followed in December 2025 with a

The pattern is clear: global cloud providers see India as the next frontier for AI infrastructure investment. The country has advantages that are hard to replicate. The engineering talent pool is deep and growing. Salary costs are still lower than Western alternatives, though that gap is narrowing. The domestic market for cloud services is expanding rapidly as Indian enterprises digitize. And the regulatory environment, despite challenges, is more stable than many emerging economies. According to Deloitte's economic outlook, India's economic fundamentals are strong, making it an attractive destination for investment.

But the tax holiday accelerates an already-existing trend. It removes one of the final barriers to massive capital deployment. Instead of a cloud provider agonizing over a $5 billion data center investment with a 15-year payback period and uncertain taxation, they now have guaranteed clarity. Zero taxes on exports for 21 years changes the return calculation fundamentally.

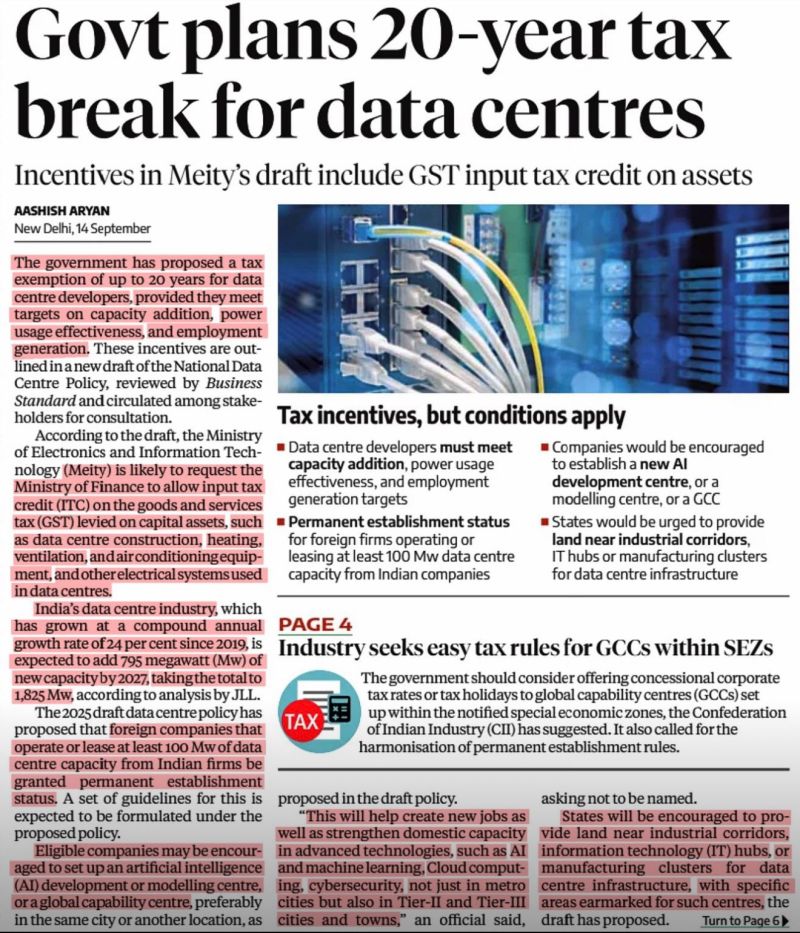

India's government isn't stupid either. They're not trying to win on tax policy alone. The broader budget allocation signals this is a strategic priority. The finance ministry proposed a second phase of the India Semiconductor Mission focused on manufacturing equipment, materials, and intellectual property. They increased funding for the Electronics Components Manufacturing Scheme to ₹400 billion (approximately $4.36 billion). These aren't random policy moves. They're part of a coordinated effort to build India into a comprehensive AI and semiconductor hub, not just a data center location. As noted by Forbes India, the government is making significant investments to support this vision.

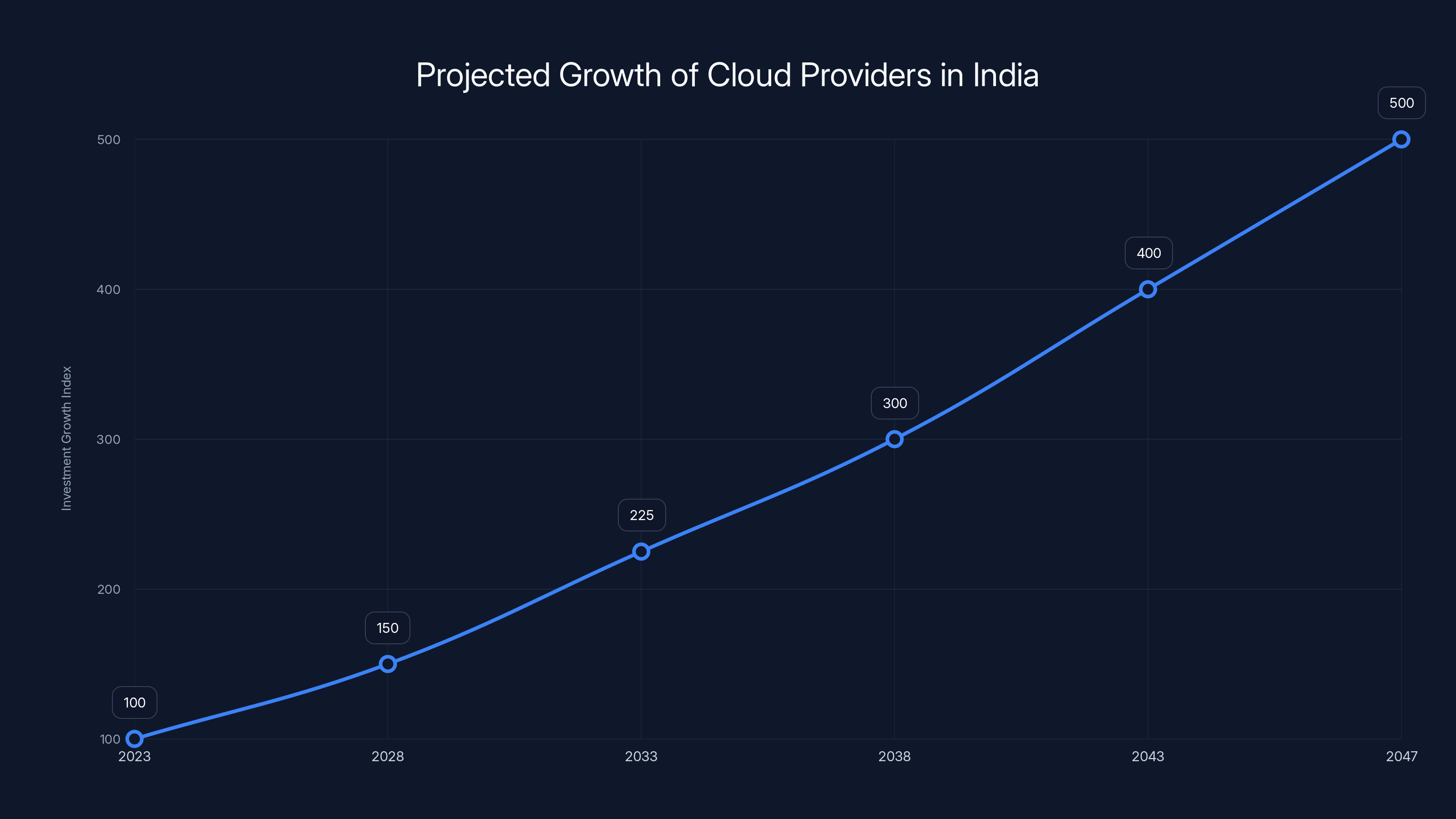

The zero-tax policy is expected to significantly boost cloud service investments in India, with projected growth reaching 500% by 2047. Estimated data.

The Mechanics: How the Tax Policy Actually Works

The tax holiday structure is more nuanced than the headline suggests, and understanding the mechanics matters if you're evaluating whether this policy actually achieves what India intends.

The core proposal: zero taxes on revenues from cloud services sold outside India if those services are executed from Indian data centers. This applies through 2047—that's 21 years of clarity. For cloud providers calculating long-term capex, this is significant. A data center investment that takes 5-7 years to build and 10-15 years to reach peak profitability looks completely different when you know your export revenues are tax-free. According to TechCrunch, this policy is designed to attract significant foreign investment.

But here's the important part: services sold to Indian customers don't get the same treatment. If a cloud provider runs workloads from an Indian data center and sells them to Indian enterprises, those revenues must be routed through locally incorporated resellers and taxed domestically. This isn't a blanket zero-tax play. It's specifically targeted at export services.

This structure matters for a few reasons. First, it incentivizes cloud providers to use India as an export hub without completely eliminating taxation on domestic revenue. India still captures tax revenue from services sold to Indian customers. Second, it creates a legal pathway for foreign cloud providers to participate in the domestic market while supporting the growth of Indian reseller companies. It's protectionist without being explicitly xenophobic.

The government also introduced a 15% cost-plus safe harbor for Indian data center operators providing services to related foreign entities. This is a significant carve-out. Instead of dealing with complex transfer pricing rules, Indian companies can charge affiliated foreign entities a cost-plus margin of 15%. That provides certainty and removes some of the regulatory arbitrage that makes international business operations complex.

The combination of these mechanisms is clever. It attracts foreign investment while protecting domestic players. It generates tax revenue from domestic services while offering incentives for export-oriented infrastructure. And it provides the regulatory clarity that global companies need to justify massive capex commitments to their boards.

However, there's a constraint that doesn't get enough attention. These policies require consistent implementation across budget cycles. Tax policy in democracies can change. A different government could theoretically modify these provisions. But committing to 21 years of zero taxes is India essentially locking itself into this policy framework. That kind of commitment is rare, and it signals serious intent.

The Response From Global Cloud Giants

The announcements from Amazon, Google, and Microsoft didn't happen by accident. These companies have detailed financial models and long-range planning processes. When all three increase India commitments within a four-month window, they're responding to something specific.

Let's look at what each company is actually doing with the money.

Google's $15 billion is explicitly focused on building an AI hub and expanding data center infrastructure. This isn't vague. Google is planning to build facilities capable of supporting large-scale AI training and inference workloads. They're not just spinning up a few servers in an existing facility. They're committing to comprehensive infrastructure expansion across computing, networking, and storage. As reported by TechBuzz, this investment is part of a broader strategy to make India a key player in the global AI landscape.

Microsoft's $17.5 billion through 2029 is earmarked for expanding AI and cloud services, funding new data centers, infrastructure, and training programs. The training component is interesting. Microsoft isn't just building capacity for their own services. They're committing to build local talent, which suggests they're thinking about India as a long-term operational hub, not just a cost-arbitrage play.

Amazon's $35 billion additional investment by 2030 is split between retail and cloud operations. For AWS specifically, Amazon is building out capacity in India that mirrors their global expansion strategy. They're not catching up; they're leading.

What's remarkable is the speed of these commitments. Typically, cloud providers announce investments, then spend months or years in planning, permitting, and site acquisition. These announcements came very quickly after each other, suggesting they were coordinated responses to seeing India as suddenly more attractive. Whether that's because of the tax policy announcement or because the policy formalized something already being discussed behind closed doors, the effect is the same: India just got a massive vote of confidence from the companies that matter most.

But implementation is a different story. All three companies announced expansions in India before. Google's $10 billion in 2020 didn't overnight transform India into a cloud superpower. Some of that capital went to building facilities, yes. But some of it also went to acquiring talent, building partnerships, and navigating regulatory complexity. Cloud infrastructure takes time.

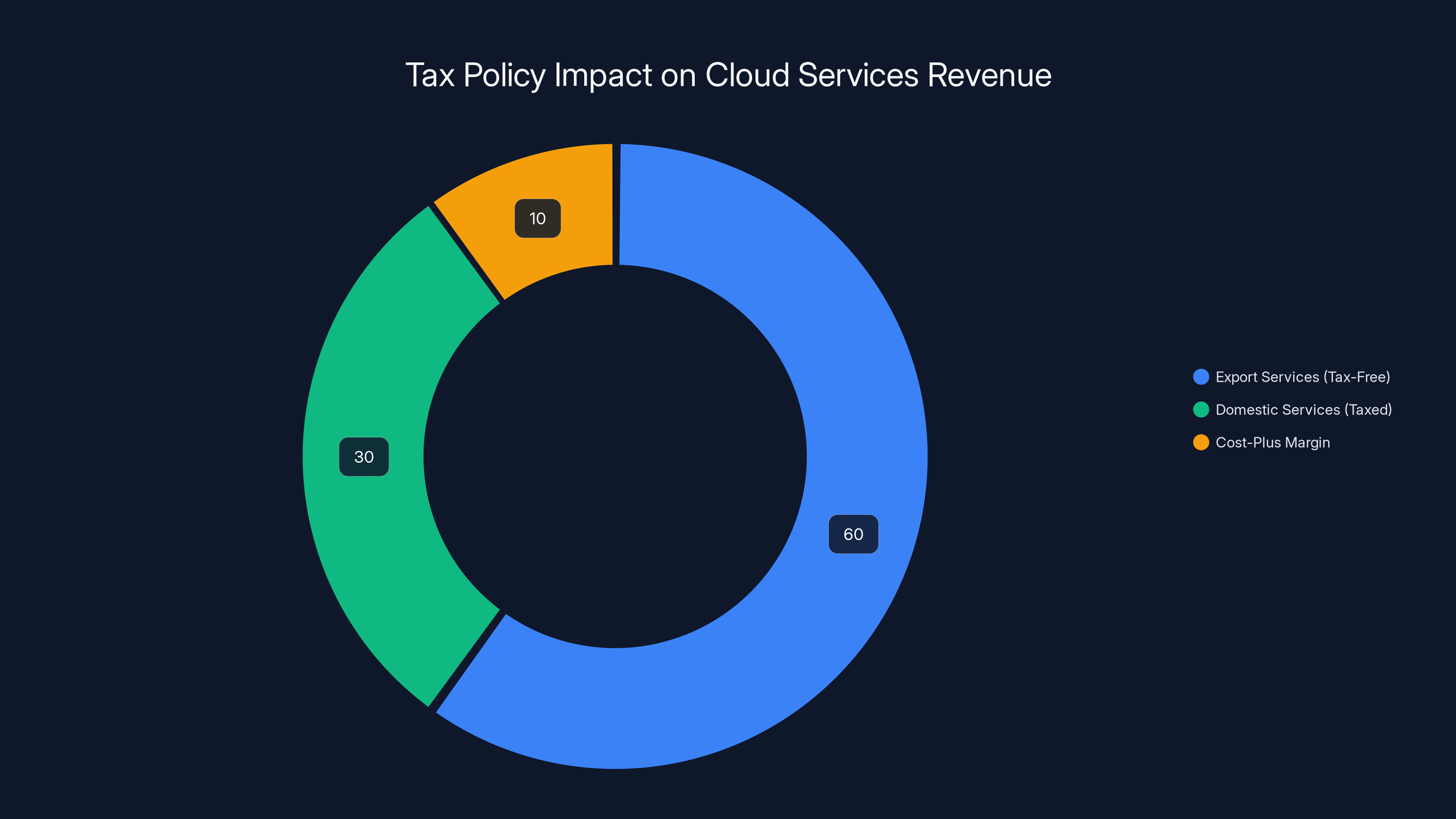

Estimated data: The tax policy incentivizes export services by offering tax-free status, while domestic services remain taxed, and a 15% cost-plus margin applies to related foreign entities.

The Domestic Player: Reliance, Adani, and India's Homegrown Data Center Ambitions

India's largest companies are stepping up too, and that's important context that often gets overlooked in coverage of foreign investment announcements.

In November 2025, Digital Connexion announced an $11 billion investment to develop a 1-gigawatt AI-focused data center campus in Andhra Pradesh by 2030. Digital Connexion is a joint venture backed by three significant entities: Reliance Industries (India's largest conglomerate), Brookfield Asset Management (a major global infrastructure investor), and Digital Realty Trust (the largest data center REIT in the world). This isn't a startup. This is serious capital paired with proven operational expertise.

The Visakhapatnam campus alone covers 400 acres. A gigawatt of data center capacity at a single campus is massive. For context, that's equivalent to a mid-sized cloud region in AWS or Azure. And it's being designed specifically for AI workloads, which require different thermal, power, and networking characteristics than traditional enterprise data centers.

Adani Group announced up to $5 billion alongside Google in its AI data center project. Adani is India's second-largest conglomerate, with deep experience in infrastructure, power, and logistics. Their involvement signals that India's traditional industrial players see AI infrastructure as a strategic business opportunity, not just foreign capital inflow.

What's happening is a convergence. Global cloud giants are bringing capital and technology. Indian companies are bringing operational experience, land access, and relationships with government. The tax policy is the accelerant that makes the partnership economics work.

This matters because it suggests India's ambitions aren't temporary. If this were just about foreign investment subsidies, you wouldn't see Reliance and Adani committing billions. But they are, which suggests they believe there's a sustainable business here. They wouldn't bet billions on a trend that disappears in five years.

The Infrastructure Challenge: India's Real Constraint

Now let's talk about the elephant in the server room: India's infrastructure isn't ready for what's being proposed.

Data centers are power-hungry. A 1-gigawatt facility needs consistent, reliable power. India generates sufficient electricity nationally, but distribution is uneven and reliability is variable. Power outages happen. Brownouts happen. For a data center operating at millions of dollars per hour, that's unacceptable.

Water stress is another constraint. Data centers need water for cooling, and India's water situation is increasingly constrained, especially in the southern regions where Digital Connexion and Google are planning facilities. Andhra Pradesh is facing water stress. The Visakhapatnam area has competing demands from agriculture, municipal supply, and industry. A 1-gigawatt data center campus could consume enormous quantities of water.

Land access is a third challenge, though it's often overlooked. Acquiring 400 acres for a data center requires navigating state and local regulations, acquiring permission from existing landholders, and managing environmental assessments. In India, this process is slow and unpredictable. A project that takes 6 months in the U.S. might take 18 months in India.

According to industry analysis, India's data center power capacity is currently just over 1 gigawatt, with projections to reach 2 gigawatts by 2026 and potentially exceed 8 gigawatts by 2030. That growth is substantial—an 8x increase in four years—but it requires everything to go right. The investments need to happen on schedule. The infrastructure upgrades need to happen on schedule. The regulatory approvals need to happen on schedule.

India's government is aware of these constraints. The budget includes increases in infrastructure funding and signals that data center buildout is a strategic priority. But policy signals aren't the same as solved problems. A gigawatt of power capacity doesn't appear overnight. Neither does reliable water supply or efficient land acquisition processes.

This is where India's policy is smart but not complete. Offering zero taxes is the easy part. Ensuring that cloud providers can actually execute on their data center plans is harder. It requires coordination across state governments, power utilities, water authorities, and local regulators. In a country as large and federal as India, that coordination is complex.

The Tax Impact: What Does Zero Tax Actually Cost India

Here's a question that deserves more attention: what's the revenue cost of this policy, and is it worth it?

If Google, Microsoft, and Amazon each run

But India's government is making an implicit calculation. The tax revenue forgone is less than the economic value created through infrastructure investment, job creation, and technology transfer. A data center employs hundreds of people directly and thousands indirectly. Infrastructure investment in power, fiber, and transport benefits the broader economy. Talent development and training programs create a more skilled workforce that benefits other sectors.

This is a bet on multiplier effects. India is saying: we'll forgo short-term tax revenue in exchange for long-term economic development. Whether that bet pays off depends on execution.

There's also a competitive dimension. If India doesn't offer attractive tax terms, companies build data centers elsewhere. Singapore, Indonesia, Japan, and other Asian nations are also competing for AI infrastructure investment. The zero-tax policy is partially about being the most attractive option in a competitive marketplace. It's a race to the bottom in terms of tax rates, but it's a race India believes it can win because of other advantages.

Policymakers also noted that the 15% cost-plus safe harbor for Indian data center operators protects domestic players. If foreign companies want to offer cloud services from India, they either do it themselves (and pay the zero-tax rate on exports) or they partner with Indian companies (who get the 15% cost-plus margin). This structure creates opportunities for companies like Digital Connexion.

Estimated data shows India's AI infrastructure investment could lead to

The Domestic Market Opportunity: Why Export Tax Breaks Matter Less Than They Seem

Here's a subtlety in India's policy that's often missed: the zero-tax incentive for exports matters less than it initially appears because the domestic cloud market is already huge and growing.

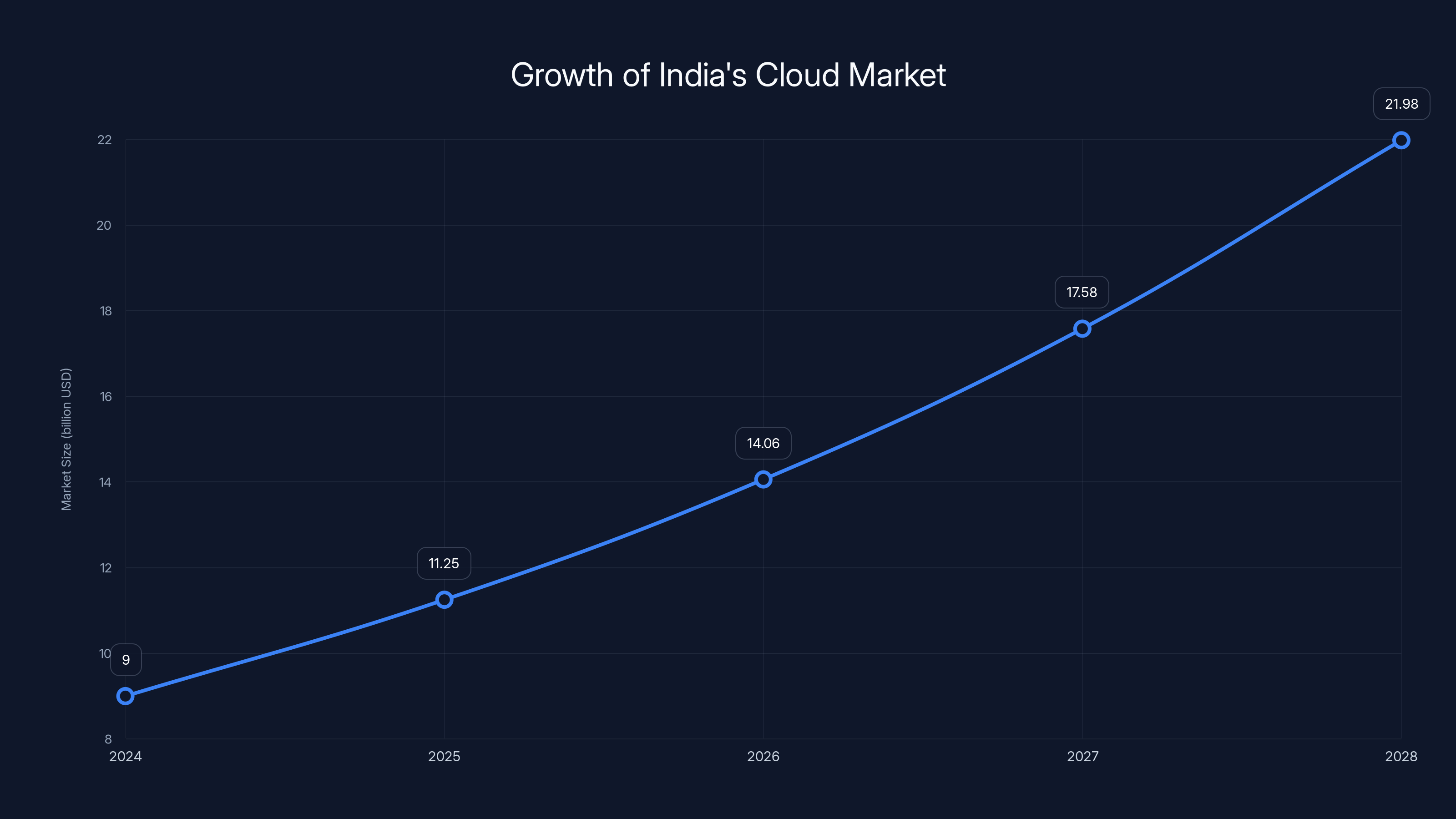

India's cloud market reached approximately $8-10 billion in 2024 and is growing at 25-30% annually. That's faster than global cloud market growth. Why? Because India has 1.4 billion people, and only 10-15% of them have internet access to cloud services today. The addressable market is enormous and largely untapped.

When Amazon, Google, or Microsoft build data centers in India, they're not just supporting export workloads. They're also supporting the domestic market. An enterprise in Bangalore using AWS for its application infrastructure generates revenue for AWS. That revenue is taxed domestically (routed through Indian resellers), but it drives utilization of the data center infrastructure.

So the zero-tax policy for exports is the headline, but the real business is domestic. Cloud providers are expanding in India because they want to serve Indian customers. The tax policy sweetens the deal for their boards, but the actual business case is already compelling.

This matters strategically. It means the data center investments aren't dependent entirely on the tax policy. Even if the tax incentive disappeared tomorrow, cloud providers would still maintain and operate their India facilities because of domestic demand. The tax policy accelerates investment, but it doesn't create it entirely.

Semiconductor Manufacturing: The Complementary Strategy

India's broader budget initiative includes significant pushes on semiconductor manufacturing, which is complementary to the data center ambitions but often discussed separately.

The government launched a second phase of the India Semiconductor Mission focused on producing semiconductor equipment and materials, developing full-stack domestic chip intellectual property, and strengthening supply chains. They increased funding for the Electronics Components Manufacturing Scheme to ₹400 billion (approximately $4.36 billion).

Why does this matter for data centers? Because modern AI infrastructure requires custom silicon. Google develops TPUs (Tensor Processing Units). Microsoft has invested in custom AI accelerators. Amazon designs AWS Trainium and Inferentia chips. Having semiconductor manufacturing capacity in-country reduces dependency on global chip supply chains and creates opportunities for Indian companies to participate in the value chain.

If India can develop the capability to manufacture chips locally, it makes the country even more attractive as a data center hub. Instead of importing GPUs and other accelerators, you can manufacture them locally (or manufacture components for them). That improves supply chain resilience and reduces costs.

This is a longer-term play than the immediate data center expansion. Semiconductor manufacturing takes years to scale. But it reflects India's thinking about building a comprehensive AI and infrastructure ecosystem, not just attracting data center investment for its own sake.

The Competitive Landscape: How India Stacks Up Against Other Regions

India isn't the only country offering incentives for data center and AI infrastructure investment. To understand why India's policy matters, it helps to see where it fits globally.

The United States remains the largest and most mature cloud infrastructure market, with the most total data center capacity. But U.S. policy is moving in the opposite direction of India. Data center tax incentives are inconsistent and vary by state. The political environment is becoming less predictable. Some policymakers want to tax tech companies more, not less. The U.S. retains advantages in technology and capital access, but it's not aggressively courting new investment through tax policy.

Europe imposed stringent data sovereignty requirements. Companies must keep European data within European borders, which limits cloud providers' ability to operate efficiently across regions. This is good for European data center operators but bad for cost optimization. Europe isn't using aggressive tax incentives; it's using regulation to mandate local presence.

Singapore offers tax incentives and business-friendly policies, but it has limited land and power capacity. It's becoming a regional hub, not a global player in data center infrastructure.

Japan and South Korea are investing in cloud infrastructure, but their costs are higher and their markets smaller than India's. They're important regional hubs, but they're not competing globally for the world's AI workloads.

Australia has announced infrastructure investments but hasn't offered equivalent tax incentives.

In this context, India's move is strategically positioned. By offering zero taxes on exports, a large and growing domestic market, significant engineering talent, and lower costs than most developed nations, India is positioned as the alternative to the U.S. for global AI infrastructure. That's the strategic positioning, and it's compelling for cloud providers looking to diversify geographically.

India's cloud market is projected to grow rapidly, reaching nearly $22 billion by 2028, driven by increasing domestic demand. Estimated data.

The Execution Risk: Can India Actually Deliver

Policy is easy. Execution is hard. And India has a mixed track record on execution for large infrastructure projects.

The power infrastructure challenge is real. India's power sector is undergoing transition from coal to renewables, and that transition has caused supply disruptions. Data centers need predictable, reliable power. If a facility loses power for even a few minutes, it can corrupt data and disrupt services. Indian power utilities have improved, but they're not yet at the reliability level of utilities in developed nations.

There's an opportunity here. Data centers could drive investment in renewable energy infrastructure. Solar and wind capacity near data centers could improve overall grid reliability while supporting the transition to clean energy. But this requires coordination between central government, state governments, utilities, and data center operators. That's complex.

Water availability is another execution risk. Andhra Pradesh and Karnataka, where major data center projects are planned, face water stress. Climate change is making water scarcity worse, not better. A 1-gigawatt data center might need 300,000-500,000 gallons of water per day for cooling. That's significant, and it requires securing reliable supply sources. Some companies are exploring waterless cooling technologies, but those are expensive and still in early deployment.

Land acquisition is a perennial challenge in India. Private land ownership is fragmented, and the regulatory process is opaque. Acquiring 400 acres for a single project requires navigating complex negotiations and regulatory approvals. Digital Connexion claimed they're working on this, but actual timelines are often longer than announced.

There's also the question of maintaining policy continuity. The zero-tax holiday runs through 2047. That's 21 years, which spans multiple election cycles. Will a different government honor the commitment? Politically, it's hard to break such a high-profile commitment, but it's not impossible. Cloud providers are betting on policy stability, but that's an assumption, not a certainty.

Lastly, there's operational execution. Building and operating world-class data centers requires specific expertise. Indian companies are learning, but they're not yet at the operational sophistication of companies like Digital Realty or Equinix. The fact that Digital Connexion includes Digital Realty as a partner addresses this to some extent, but it's a risk factor.

The Talent Advantage: Why India's Engineering Workforce Matters

One factor that's sometimes underestimated in discussions of India's infrastructure ambitions is the talent advantage. India produces more than 1 million engineering graduates annually. The quality varies, but the quantity is enormous. For a cloud provider needing to staff new data centers, hire engineers for customization and optimization, and build local sales and support teams, India offers talent at a scale and cost that few places match.

Beyond raw numbers, India has a proven track record of producing world-class software engineers and infrastructure specialists. Many of Google, Microsoft, and Amazon's senior technical leaders were trained in India or have Indian heritage. The talent ecosystem is proven.

There's also the matter of training and education. Microsoft and others are committing to training programs in India as part of their investments. They're building local capacity not just for their operations but for the broader ecosystem. This creates a virtuous cycle where more companies move operations to India, creating demand for trained people, driving investment in education, producing more trained people.

For an emerging tech hub, talent is often the scarcest resource. India's abundance of talent is a significant advantage that the tax policy doesn't directly provide but depends on.

The Domestic Reseller Model: Protecting Local Companies While Attracting Foreign Investment

The requirement that cloud services sold to Indian customers be routed through locally incorporated resellers is often criticized as protectionist, but it's actually a clever policy mechanism.

Direct foreign competition is hard for domestic companies. If Microsoft or Google can sell directly to Indian enterprises, a local reseller can't compete on price or reach. But if foreign companies must partner with local resellers, it creates a business opportunity for Indian companies. They become the customer interface, the local support provider, the relationship manager.

This model has worked in other industries. In India's telecom sector, for example, foreign companies often operate through local partnerships. In pharmaceuticals, too. It's protectionism, but it's not isolation. Foreign companies get market access, but local companies get a piece of the value chain.

For cloud services, this matters economically. A local reseller employs sales engineers, support staff, and business development people. They generate local tax revenue and create high-skilled jobs. The policy preserves these opportunities for Indian companies while allowing foreign companies to serve the Indian market.

However, there's a concern worth noting. If the margin available to resellers is too thin, they can't sustain the business. If foreign cloud providers can make their margins on exports (zero tax) and minimal margins on domestic sales (to avoid reseller competition), then resellers might not have a viable business. The policy structure assumes reseller margins will be adequate, but that's not guaranteed.

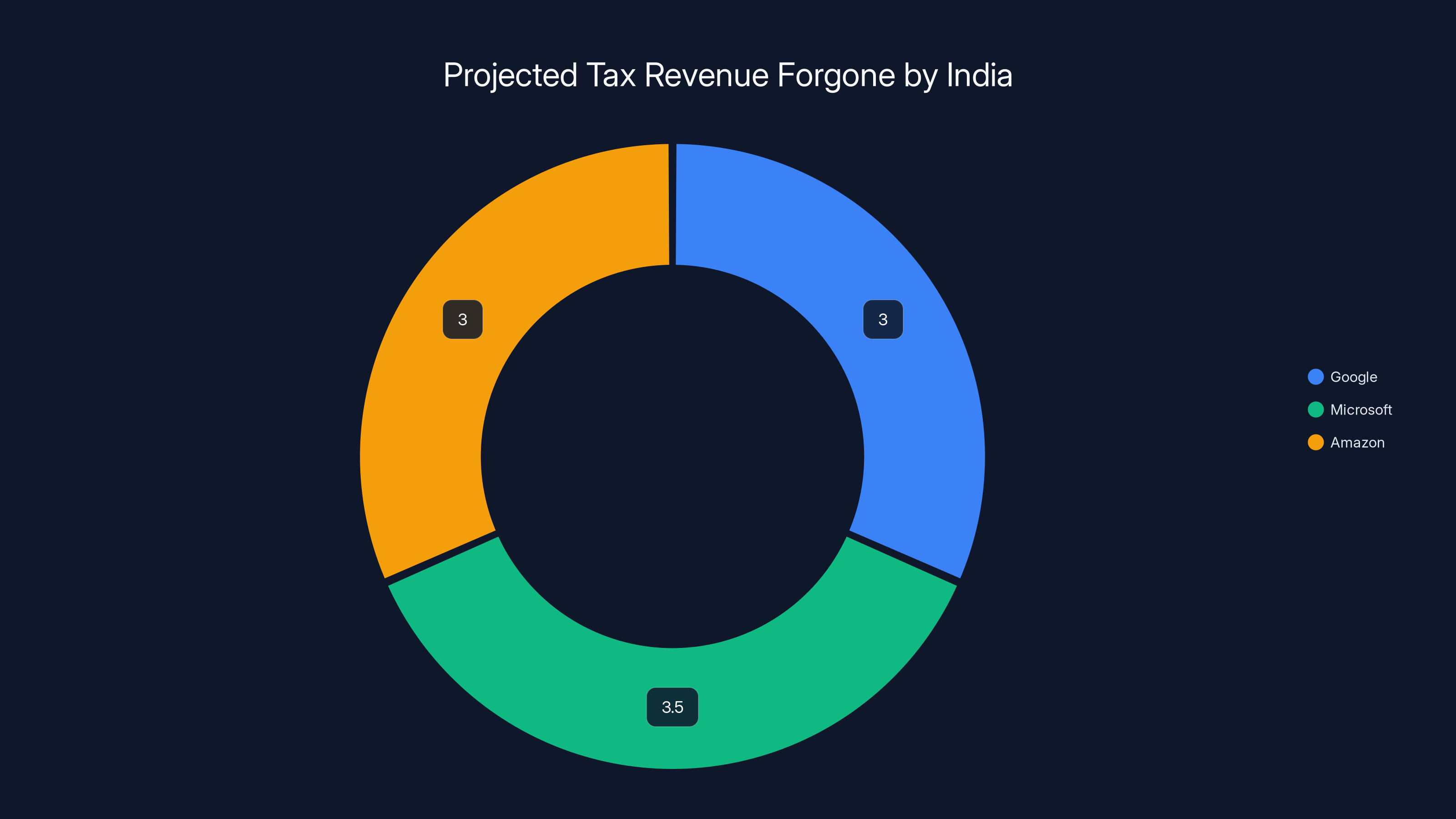

India potentially forgoes $9-13.5 billion in tax revenue from Google, Microsoft, and Amazon over 10 years due to zero-tax policy on cloud exports. Estimated data.

The Geopolitical Dimension: India as an Alternative to U.S. Dominance

Underlying all of this is a geopolitical reality that's not always explicitly stated but is definitely present.

The United States dominates global cloud infrastructure. AWS has about 32% global market share. Microsoft Azure has about 23%. Google Cloud has about 11%. Together, these three U.S. companies control two-thirds of the global cloud market. For many countries, this represents a dependency. Their digital infrastructure, their data, their workloads all run on U.S. platforms.

India's policy isn't just about attracting investment or tax revenue. It's about reducing dependency on U.S. infrastructure. If India becomes a hub for AI workloads, Indian companies can process data locally, train models locally, and reduce their dependency on U.S. cloud platforms.

For India's government, this is also a strategic play in global technology competition. China has built its own cloud infrastructure (Alibaba Cloud, Tencent Cloud) to avoid dependency on U.S. companies. India is not trying to build a completely separate infrastructure; rather, it's trying to be an attractive alternative where global companies choose to invest and where Indian companies can maintain greater control over their digital infrastructure.

This geopolitical angle isn't stated in the budget announcement, but it's understood. Reducing dependency on any single country's technology infrastructure is a strategic imperative for nations trying to maintain autonomy.

The Environmental Angle: Renewable Energy and Sustainability

Data centers are energy-intensive, and energy use has environmental implications. India is in the midst of a transition to renewable energy, with targets to reach 500 gigawatts of renewable capacity by 2030. Data center expansion is compatible with this goal if done right.

Several cloud providers have committed to operating on renewable energy. Google aims for carbon-free operations. Microsoft has set ambitious net-zero targets. If India's data centers operate on renewable power, it supports both cloud provider sustainability goals and India's climate targets.

There's also economic opportunity. Building renewable energy capacity to support data centers creates jobs in solar, wind, and grid infrastructure. It accelerates India's transition to clean energy. The cost curves for renewables have fallen dramatically, so powering data centers with solar and wind is increasingly cost-effective.

However, the challenge is matching power supply with data center demand. Data centers need continuous, reliable power, while renewable supply is variable. This requires battery storage, grid upgrades, and smart energy management. India is investing in these areas, but the infrastructure isn't complete.

A well-executed data center expansion, paired with renewable energy infrastructure investment, could accelerate India's clean energy transition. A poorly executed expansion, dependent on fossil fuels and unreliable power, would undermine climate goals. The stakes are high on both sides.

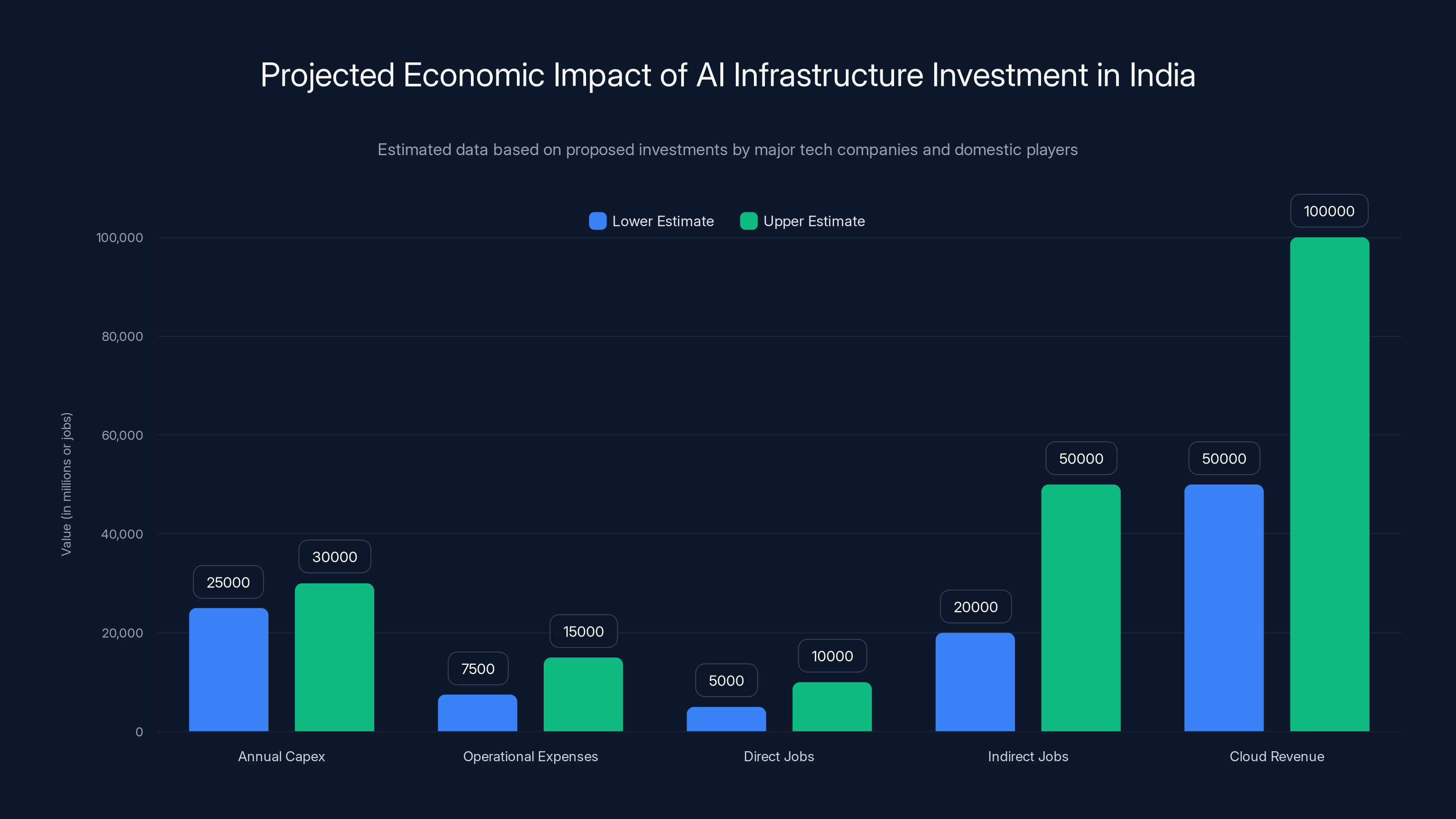

Revenue Projections and Economic Impact Modeling

What's the potential economic impact of India successfully attracting and maintaining AI infrastructure investment at the scale being proposed?

Let's model some scenarios. If Google, Microsoft, and Amazon combined are investing approximately

Each data center facility generates ongoing operational expenses: power, water, staffing, maintenance. Operational expenses typically run 30-50% of capex over a facility's lifetime. So

Staffing is significant. A large data center campus might employ 500-1,000 people directly. With 10+ facilities under development, that's 5,000-10,000 direct jobs. Indirect jobs (construction, utilities, suppliers, support services) could exceed direct jobs by 3-5x. That's potentially 20,000-50,000 jobs.

Tax revenue is more complex. For export services, it's zero by policy. For domestic services and operational expenses, tax revenue flows to the government. A facility with $500 million in annual operational expenses would generate significant tax revenue despite the export tax exemption.

If the facilities achieve projected capacity and utilization, they could support

These are rough projections, but they illustrate the scale. If executed successfully, India's data center expansion could generate hundreds of thousands of jobs, billions in tax revenue, and substantial economic growth. If execution fails, India invested heavily in infrastructure that sits partially utilized.

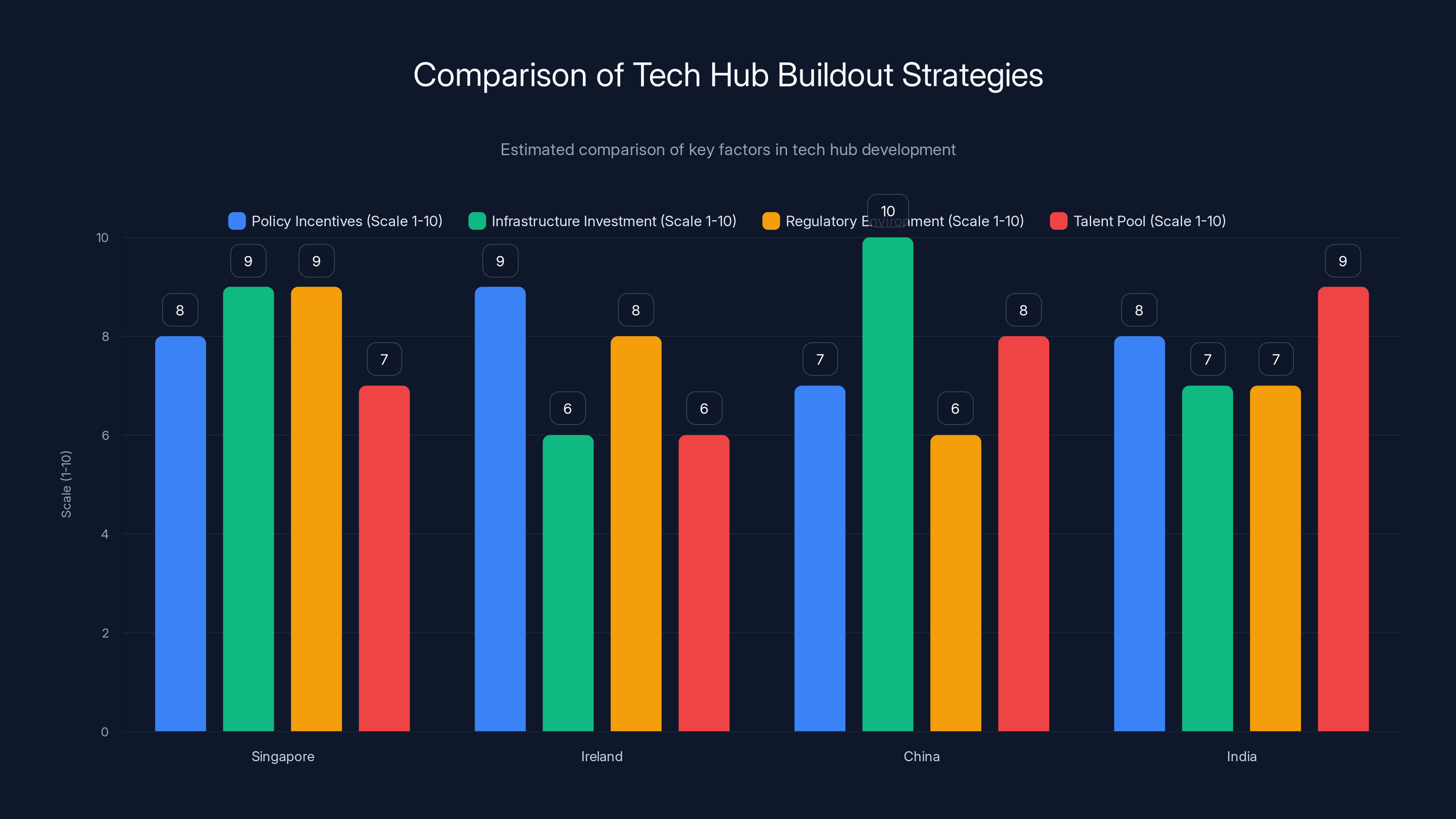

This chart compares key factors in tech hub development across different countries. India's approach is similar to Singapore's but on a larger scale, with significant challenges in execution. (Estimated data)

The Comparison with Previous Tech Hub Buildouts

India isn't the first country to try to build a tech hub through policy incentives. How does this compare historically?

Singapore built a financial hub in the 1980s and 1990s through tax incentives, regulatory clarity, and infrastructure investment. It worked, but Singapore had advantages: a small, wealthy, well-educated population and an existing cosmopolitan business environment. India is trying to do something similar, but at a vastly larger scale and with more constraints.

Ireland attracted tech companies through low corporate tax rates (12.5% on most income). Over 20 years, it transformed from an agrarian economy to a tech hub. But Ireland is small and wealthy. India is large and middle-income. The economics and challenges are different.

China built tech hubs in Shenzhen, Beijing, and Hangzhou through industrial policy, massive infrastructure investment, and regulatory protection. It worked, but China could mandate industrial policy in ways democracies can't.

India's approach is closest to Singapore's: incentives plus infrastructure plus openness to foreign investment, plus talent advantages. But the scale is much larger, and the execution challenges are more complex.

Historically, tech hub buildouts take 10-15 years to achieve critical mass. The policy announcements in early 2026 are just the beginning. Real success would be evident in 2035-2040, when we can see whether India successfully built world-class AI infrastructure and whether the companies operating there remain profitable and expanding.

Future Outlook: What Happens After 2047

The tax holiday runs through 2047. That's specifically chosen because India celebrates 100 years of independence in 2047. It's symbolically significant. But it also raises questions about what happens after 2047.

Cloud providers won't commit to infrastructure investments if they know taxes will skyrocket after 2047. Once a data center is built, it has decades of useful life. If tax rates change dramatically after 2047, the business case deteriorates. This is a credibility problem for India's policy.

One possibility: India could extend the tax holiday further or make it permanent. Another possibility: India could transition to a tiered tax structure where zero rates decline over time. Or India could let the tax holiday expire and accept that facilities built during the holiday period continue operating but no new investment flows in.

The 2047 date is probably not the actual endpoint. But it's unclear how policy will evolve. This creates some uncertainty that tempers the enthusiasm for long-term commitments.

Alternatively, India could use the 2047 date as an opportunity to reassess. By 2047, India will know whether the policy worked. If it did, and India has a mature, profitable data center industry, the rationale for tax holidays diminishes. India could be in a position to charge normal tax rates and still attract investment because of competitive advantages that were built during the holiday period.

That would be the ideal scenario: use tax policy to bootstrap an industry, then rely on competitive advantages (talent, infrastructure, location) to maintain the industry. But reaching that point requires successful execution across 20+ years.

Policy Mechanics: How This Compares to Other Tax Incentives

Zero tax is aggressive, but it's not unprecedented. What makes this policy distinctive is the duration and scope.

Some U.S. states offer property tax abatements for data center development. These typically run 10-20 years and apply to property tax, not income tax. The scope is narrower but the incentive can be significant.

Ireland offers low corporate tax rates (12.5%) but not zero rates. That's applied broadly to all companies, not specifically to cloud providers.

India's policy is distinctive: it's zero income tax on export services, specific to cloud providers, for 21 years. It's more aggressive than most comparable incentives.

But there's a trade-off in the policy design. The zero rate only applies to export services. Domestic services are taxed at normal rates through resellers. This limits the scope compared to a blanket tax holiday. It also creates a separate regime for domestic versus export activities, which adds administrative complexity.

The 15% cost-plus safe harbor for Indian data center operators is also interesting. Transfer pricing is notoriously complex in international taxation. Offering a fixed 15% margin simplifies the calculation and removes uncertainty. This is beneficial for Indian companies operating data centers and contracting with related foreign entities.

The Role of State Governments: Execution at the Federal and State Level

Here's a detail that's easy to overlook but crucial for implementation. India's federal structure means state governments have significant power over infrastructure development.

The budget announcements are at the federal level. But actually building data centers requires acquiring land, providing power connections, managing water supply, and handling regulatory approvals at the state level. Andhra Pradesh, where major projects are planned, is a different political jurisdiction than the central government. If the state government isn't aligned with the federal policy, execution stalls.

India's track record on inter-government coordination is mixed. Sometimes states align with federal initiatives enthusiastically. Sometimes they prioritize local interests. For a $60+ billion infrastructure investment, state-level alignment is crucial.

Adani Group's involvement might help here. Adani has strong relationships with multiple state governments and a proven track record of executing large infrastructure projects. Their participation suggests they believe they can navigate the political complexity.

Another factor: state governments might see an opportunity. If a data center brings jobs and tax revenue, even if the operating company pays zero federal tax on exports, the state might benefit. Power generation, land fees, employment tax, and local economic activity all flow to state treasuries. This alignment of interests could facilitate execution.

The Broader Implications: What This Means for Global Tech Strategy

India's move is significant beyond India. It signals to global tech companies that geographic diversification is being actively courted and incentivized. It creates pressure on other countries and regions to reconsider their own approaches.

For the United States, it highlights a competitive vulnerability. The U.S. has technological advantages, access to capital, and a massive domestic market. But policy unpredictability and higher tax rates are becoming competitive disadvantages. If U.S. policymakers want to maintain infrastructure investment at home, they might need to revisit tax policy.

For Europe, it highlights the limits of regulatory approaches. Europe can mandate data sovereignty, but it can't mandate investment. If cloud providers find it easier and more profitable to operate in India and route European data through European endpoints, they might choose that architecture over building European infrastructure.

For other emerging markets, it's a template. Competitive policy frameworks, infrastructure investment, and long-term commitments can attract significant capital. It doesn't guarantee success, but it improves odds.

For existing cloud infrastructure hubs like Singapore, it's competitive pressure. Singapore has been the primary hub in Asia, but India's scale and growth potential make it a more attractive longer-term destination for some workloads.

Risks and Challenges: What Could Go Wrong

Even with strong policy and significant capital commitments, risks remain.

Power supply disruptions could undermine facility reliability. If a data center loses power and corrupts data or loses uptime, customer confidence erodes quickly. India's power infrastructure is improving, but it's not yet at U.S. or European reliability levels.

Water scarcity could force facilities to operate at reduced capacity or invest heavily in alternative cooling technologies. This increases costs and reduces economic viability.

Land acquisition disputes could delay projects. Disputes over land ownership, compensation, or environmental impacts could push timelines by years. This is a real risk in India given past infrastructure projects.

Technical execution challenges could emerge during construction. Building a 1-gigawatt data center campus is technically complex. Thermal management, power distribution, network architecture, and cooling systems all need to work flawlessly. If mistakes are made during construction, fixing them is expensive and time-consuming.

Policy changes could undermine the framework. While a 21-year commitment is strong, it's not immune to political change. A different government might modify the policy. International pressure could force changes. These risks are real even if the current government is committed.

Talent constraints could limit operational capacity. While India has many engineers, data center operations require specific expertise. If companies can't hire and retain experienced operational staff, facility performance suffers.

Geopolitical tensions could complicate operations. If U.S.-India relations deteriorate over trade or technology issues, it could affect cloud provider operations or investment. The policy assumes stable geopolitical relationships, which isn't guaranteed.

Success Metrics: How to Measure Whether This Works

How will we know if India's policy succeeds? What are the metrics that matter?

Capital deployment: Did cloud providers actually invest the committed billions? Are new data centers being built on schedule?

Capacity utilization: Are the facilities achieving targeted utilization rates? A beautiful empty data center is a failure.

Job creation: Did the projects create the projected jobs? Are those jobs retained and generating economic activity?

Tax revenue: Despite the zero-tax policy on exports, did India generate net positive tax revenue from operational expenses, domestic services, and induced economic activity?

Technology transfer: Did Indian companies and engineers gain capabilities and expertise that persist after the initial projects?

Domestic market growth: Did the infrastructure investments accelerate cloud adoption in India, enabling more domestic companies to digitize?

Competitiveness: Did India become a top-three global destination for AI infrastructure investment, competing with the U.S. and other major regions?

Sustainability: Did the facilities operate sustainably, with renewable energy and water conservation?

These metrics aren't all easily quantifiable, but they define success beyond just capital deployment.

Conclusion: A Bold Bet with Significant Stakes

India's decision to offer zero taxes on cloud services through 2047 is a bold strategic gamble. It's not the first country to use tax policy to attract tech investment, but it's doing so at a scale and with a commitment level that's rare.

The policy makes strategic sense. India has advantages—talent, scale, growth potential—that make it attractive for cloud infrastructure investment. Tax incentives remove barriers and accelerate deployment. The timing is right, with global cloud providers actively seeking geographic diversification.

But success depends on execution across multiple dimensions: power infrastructure, water management, land acquisition, regulatory coordination, and maintaining policy stability over 21 years. These challenges shouldn't be underestimated. They're significant, and India's track record on infrastructure execution is mixed.

If India succeeds, it could transform itself into a genuine global hub for AI infrastructure, creating hundreds of thousands of high-skilled jobs, generating billions in economic value, and establishing a foundation for technological leadership in emerging domains. The early indicators are encouraging: Google, Microsoft, and Amazon are committing billions, and domestic companies like Reliance and Adani are participating.

If India struggles with execution—if power constraints persist, water becomes unavailable, political complications emerge—the investment might be wasted, and the tax revenue forgone (in the billions) would be a permanent loss.

The next five years will be telling. Will new data centers be built on schedule? Will they achieve targeted capacity and utilization? Will the policy generate the expected economic multipliers? The answers will shape not just India's tech future but global cloud infrastructure architecture for decades to come.

For now, the policy is ambitious, the capital commitments are real, and the stakes are high. India has thrown down a significant challenge to the existing order of cloud infrastructure. Whether it can follow through is the defining question.

FAQ

What does the zero-tax policy mean for cloud providers operating in India?

Cloud service providers running workloads from Indian data centers can earn zero taxes on revenue generated from services sold to customers outside India through 2047. However, services sold to Indian customers must still be routed through locally incorporated resellers and are subject to normal domestic taxation. This structure allows foreign cloud providers to dramatically improve the return on investment for their India data center facilities while still generating tax revenue for India from domestic cloud services.

How long will the tax holiday remain in effect?

The zero-tax holiday runs through 2047, which coincides with India's 100-year independence celebration. This 21-year commitment signals strong policy continuity, though it does raise questions about what happens after 2047. India could extend the policy, implement a tiered structure where rates increase gradually, or allow the holiday to expire. The long duration is significant because it allows cloud providers to forecast returns across an entire facility lifecycle and justify massive capital investments to their boards.

Why does India need this policy when it already has advantages like talent and cost?

While India does have significant advantages—including abundant engineering talent, lower salary costs than developed nations, and a rapidly growing domestic cloud market—it still faces competition from other regions and countries. The zero-tax policy removes the last major financial barrier to deployment and signals that India is serious about becoming a global AI infrastructure hub. Without it, companies might choose to expand in the United States, Europe, or Southeast Asia instead. The policy accelerates a trend that was already happening but removes uncertainty from the investment decision.

What are the main challenges to executing this infrastructure expansion?

India faces several execution risks. Power supply reliability remains inconsistent in some regions, and data centers require continuous, predictable electricity to maintain service uptime. Water scarcity is increasingly acute, particularly in southern states where major projects are planned, and data center cooling is water-intensive. Land acquisition in India involves complex negotiations and regulatory approvals that can delay projects. Finally, India must maintain policy continuity across multiple government administrations and navigate coordination between federal and state authorities, all while managing competing demands on limited infrastructure resources.

How does this policy compare to incentives offered by other countries?

India's zero-tax rate on export cloud services is more aggressive than most comparable incentives globally. The United States offers state-level property tax abatements (typically 10-20 years), which are narrower in scope. Ireland uses low corporate tax rates broadly (12.5%), but not zero rates specifically for cloud providers. The key difference is that India is offering zero income tax specific to a strategic industry for 21 years—a more targeted and aggressive approach than most precedents. This signals India's determination to win in the global competition for AI infrastructure investment.

Will cloud providers actually build the data centers they've committed to?

The commitments are real—Google (

What happens to Indian companies under this policy?

The policy protects domestic opportunities for Indian companies through two mechanisms. First, cloud services sold to Indian customers must be routed through locally incorporated resellers, creating a business opportunity for Indian intermediaries. Second, Indian data center operators (like Digital Connexion) get a 15% cost-plus safe harbor for transfer pricing when providing services to related foreign entities, providing profit certainty. Additionally, the infrastructure investments will generate jobs and demand for Indian services. However, if reseller margins are too thin, some domestic companies might struggle to compete. The policy protects market access but doesn't guarantee profitability for all players.

How does the domestic market component of this policy work?

Services sold to Indian customers can't access the zero-tax benefit. Instead, foreign cloud providers must work through locally incorporated Indian reseller entities, which handle direct customer relationships and are subject to normal domestic tax rates. This creates a partnership model similar to what exists in India's telecom and pharmaceutical sectors. The reseller becomes responsible for sales, support, and customer relationship management, while the foreign cloud provider handles backend infrastructure. This approach allows foreign companies to participate in India's growing cloud market while creating business opportunities for domestic companies and ensuring India generates tax revenue from the domestic cloud market.

What's the role of companies like Reliance and Adani in these plans?

Reliance (through Digital Connexion joint venture) and Adani are committing billions to build data center infrastructure themselves, not just benefiting from foreign investment. Digital Connexion plans a 1-gigawatt facility in Andhra Pradesh; Adani is investing alongside Google. Their participation is significant because it demonstrates that India's largest conglomerates see AI infrastructure as a strategic business, not just foreign capital inflow. They bring operational expertise, relationships with state governments, and capital that complement and accelerate foreign investments. This domestic-foreign partnership suggests India's infrastructure ambitions are sustainable beyond just attracting foreign companies.

Could India's power and water constraints actually stop this expansion?

Power and water constraints are real risks, but not necessarily fatal ones. India is simultaneously investing in renewable energy (targeting 500 gigawatts by 2030) and grid infrastructure. Data centers could drive investment in solar and wind capacity, improving overall reliability. Water is tougher because competing demands are high, but technology like waterless cooling and on-site treatment can mitigate impacts. The bigger risk is cost. If constrained power or water requires expensive infrastructure solutions (renewable capacity investment, cooling technology), project economics worsen. Execution success depends on coordinating data center expansion with power and water infrastructure development across multiple government jurisdictions.

TL; DR

- Zero-Tax Strategy: India offers zero taxes on cloud services sold outside the country if services run from Indian data centers through 2047, a 21-year commitment designed to attract global cloud infrastructure investment.

- Major Commitments: Google (17.5 billion), and Amazon ($35 billion) announced massive India expansions, signaling the policy's effectiveness in attracting capital from the world's largest cloud providers.

- Domestic and Foreign Investment: Reliance and Adani are committing billions to build homegrown data center capacity, suggesting India's AI infrastructure ambitions are driven by both foreign and domestic investment.

- Infrastructure Challenges: Power supply reliability, water scarcity, and land acquisition complexity remain significant execution risks that could slow deployment or increase costs beyond projections.

- Competitive Positioning: India is positioning itself as the primary alternative to U.S.-dominated cloud infrastructure, offering scale, talent, cost advantages, and now financial incentives that competing regions (Europe, Singapore, Japan) don't match at this magnitude.

- Bottom Line: The policy is ambitious and capitals are flowing, but success depends entirely on India's ability to execute infrastructure projects reliably across 20+ years while maintaining policy consistency through political changes.

Key Takeaways

- India's 21-year zero-tax policy on cloud exports is more aggressive than comparable global incentives, designed to attract $60+ billion in data center investment

- Google (17.5B), and Amazon ($35B) rapidly increased India commitments after the policy announcement, signaling confidence in the market

- Domestic companies like Reliance and Adani committed $16+ billion to data center infrastructure, proving the expansion is driven by both foreign and Indian capital

- Power reliability, water scarcity, and complex land acquisition remain critical execution risks that could delay projects or increase costs significantly

- Success would position India as the primary alternative to U.S.-dominated cloud infrastructure, reshaping global technology geography for decades