![Polestar's 4 New EV Models: Can This Strategy Save the Brand? [2025]](https://tryrunable.com/blog/polestar-s-4-new-ev-models-can-this-strategy-save-the-brand-/image-1-1771443498185.jpg)

Polestar's Ambitious EV Expansion: A Make-or-Break Moment for the Swedish-Chinese Automaker

Polestar is betting big on a risky strategy. In the span of just three years, the Chinese-owned Swedish electric vehicle maker plans to launch four entirely new models, redesign two existing ones, and somehow transform itself from a money-losing startup into a profitable, competitive EV brand. No pressure, right?

Here's the thing: Polestar is running out of runway. The company reported a staggering net loss of $1.558 billion for the first nine months of 2025, despite posting a 34% increase in sales to approximately 60,119 vehicles for the full year. That's a classic startup problem—growing fast but bleeding money faster. Parent company Geely has propped up Polestar with equity injections and loan guarantees, but that generosity won't last forever.

The automaker's new product roadmap isn't just ambitious. It's existential. If these four vehicles succeed, Polestar could finally achieve profitability and establish itself as a genuine alternative to Tesla, Lucid, and the rising Chinese EV makers. If they fail, Geely might pull the plug entirely.

Let's break down what Polestar is actually trying to do here, why the timing matters, and whether this strategy actually makes sense in an EV market that's getting meaner by the day.

The State of Polestar: From Volvo's Performance Division to Independent EV Maker

Polestar wasn't always independent. The brand started in 1996 as Volvo's in-house motorsports and performance division, tuning Volvo's sedans and wagons into slightly faster versions of themselves. It was a niche operation, the kind of thing that impressed car enthusiasts but didn't move the needle financially.

Then in 2017, Volvo decided to spin Polestar into its own thing. The company launched the Polestar 1, a performance-focused hybrid grand tourer that cost around $155,000. It was beautiful, rare, and absolutely not a volume play. Only 1,500 were built across the entire production run.

But that was the old world. Volvo wanted Polestar to become an electric vehicle brand. So in 2020, the company unveiled the Polestar 2, a sleek electric sedan that undercut Tesla's Model 3 on price while matching it on performance. The Polestar 2 actually became successful. It became Polestar's bread and butter, the model that proved the brand could sell EVs at scale.

Then came the problems. The Polestar 3, an electric SUV that launched in 2023, was supposed to capitalize on the booming EV SUV market. It has decent specs—up to 402 miles of range, clean Scandinavian design, 0-60 in 4.2 seconds for the Performance variant—but the problem was timing and price. The Polestar 3 arrived when the EV market was turning competitive. Prices were dropping. Buyers were getting pickier. And Polestar, saddled with manufacturing costs that haven't come down fast enough, couldn't compete on price or volume.

The Polestar 4 followed, and it's already controversial. The car sacrifices a rear windshield to boost cargo space in an unusual design move. Some people think it's brilliant innovation. Most people think it's weird. Either way, the Polestar 4 hasn't been the volume seller Polestar hoped for.

By 2024, it became clear something had to change. Polestar stopped taking new orders for the Polestar 2, triggering fears the company was killing its most successful model. Revenue was growing, but losses were deepening. The brand needed a new strategy, and fast.

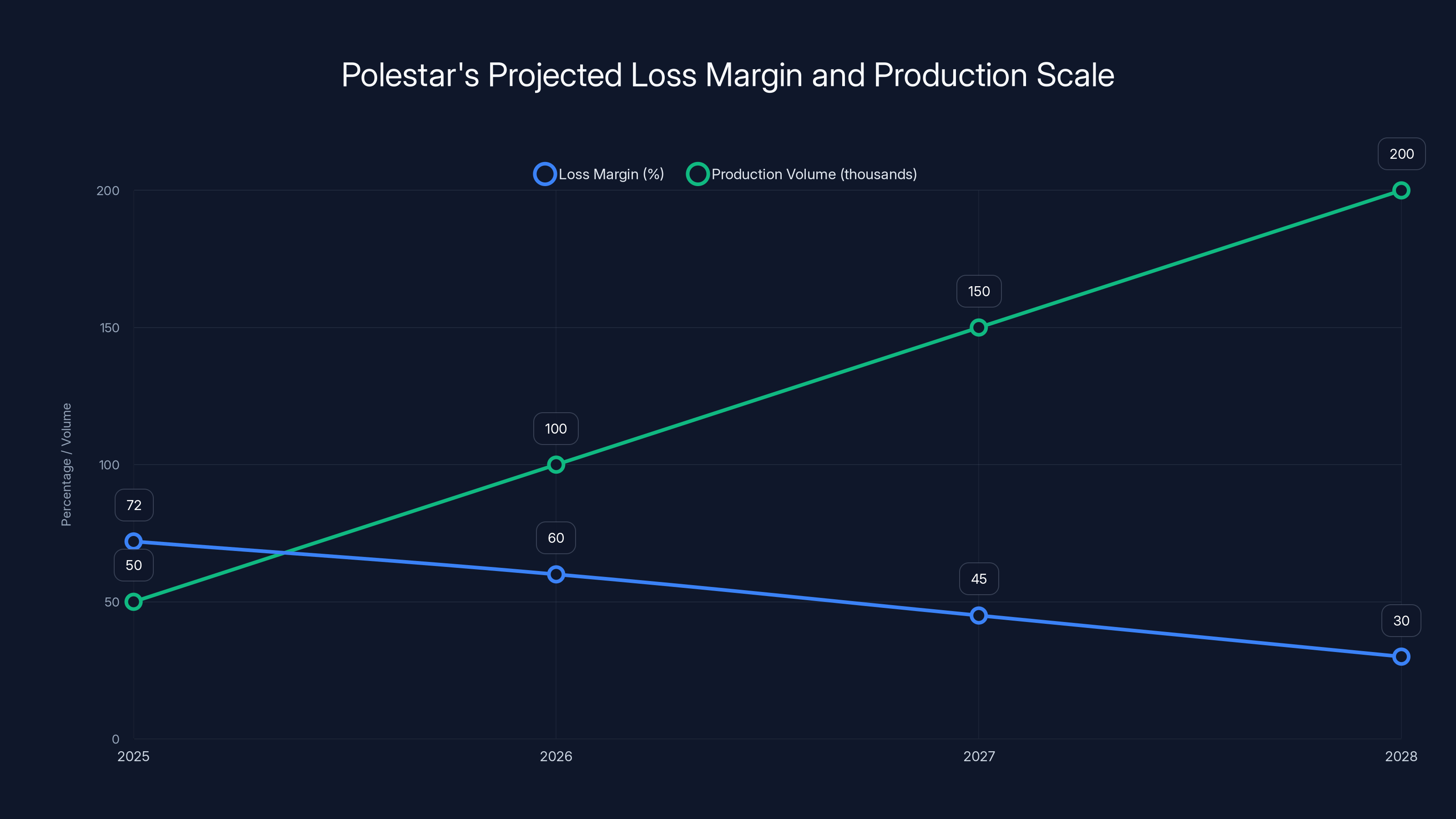

Polestar's loss margin is expected to decrease from 72% in 2025 to 30% by 2028 as production volumes increase, indicating improved economies of scale. (Estimated data)

Why 2025-2028 Is Now or Never for Polestar

The EV market has fundamentally shifted since Polestar's early days. In 2020, when the Polestar 2 launched, the EV market was booming. Buyers wanted electric cars, and there weren't enough to go around. Margins were fat. Competition was manageable.

Now, the market is oversupplied. Tesla cut prices aggressively, compressing margins across the industry. Chinese EV makers like BYD, NIO, and Li Auto are producing vehicles at costs Western automakers can't match. Traditional automakers—Volkswagen, BMW, Ford—are finally getting serious about EVs, and they have massive scale and manufacturing expertise advantages.

In this environment, a small, independent EV maker like Polestar faces an existential question: grow fast or die. There's no profitable middle ground. You either achieve sufficient scale to spread fixed costs, or you get crushed.

That's why Polestar is launching four new models in three years. It's not greed or overconfidence. It's survival. The company needs to capture market share across multiple segments before Tesla, Ford, or one of the Chinese makers dominates those segments completely.

Here's the math: right now, Polestar is tiny. 60,000 vehicles per year is respectable, but it's nothing compared to Tesla's 1.8 million annual deliveries or BYD's 3 million. To achieve profitability at automotive scale, Polestar probably needs to reach 400,000 to 500,000 vehicles per year. That requires not just new models but a completely different portfolio.

The current lineup—the Polestar 2, 3, and 4—doesn't span enough market segments. You've got a sedan, two SUVs, and that's it. There's no compact car, no sporty coupe, no small SUV for budget-conscious buyers. You're leaving money on the table.

By adding the Polestar 5 (grand tourer), Polestar 7 (compact premium SUV), a revamped Polestar 4 (estate wagon for Europe), and a new Polestar 2 (the core sedan), Polestar is trying to create a complete portfolio. It's a strategy that makes sense—if they can execute it.

The Polestar 5: The Halo Car That Needs to Prove Something

The Polestar 5 is, in many ways, the company's bet-the-farm vehicle. It's a four-door grand tourer, the kind of car that combines the comfort and space of a luxury sedan with the performance of a sports car. Think of it as Polestar's answer to the Porsche Taycan or the Mercedes-AMG EQS.

On paper, the specs are genuinely impressive. The Polestar 5 boasts:

- 460 miles of EPA range (this is the key differentiator, especially against traditional sports cars)

- 800-volt electrical architecture for ultra-fast charging (50 minutes to 80%, according to Polestar)

- 884 horsepower in Performance trim (the base model is less powerful)

- 0-60 mph in 3.1 seconds (Performance trim)

- Dual-motor all-wheel drive

- Advanced thermal management system to keep the battery efficient in extreme conditions

These aren't just marketing numbers. The 800-volt architecture is legitimately important technology. It's the same approach Hyundai uses in the Ioniq 6 and Kia EV9, and it delivers real benefits: faster charging, better efficiency, and less heat loss. The 460-mile range is also genuinely competitive with luxury EV sedans.

But here's the problem: the Polestar 5 is expensive. The company hasn't officially announced pricing, but industry estimates suggest it will start north of **

Here's where strategy becomes tricky: the Polestar 5 is designed as a "halo car," a vehicle that burnishes the brand's image and attracts enthusiasts, even if it doesn't generate massive profit. Porsche uses the 911 this way. Ferrari uses every model it makes. But halo cars only work if they influence buyers to also buy your less expensive, higher-volume vehicles.

For Polestar, that means the Polestar 5 needs to make people who love performance and luxury also consider the Polestar 2, 3, and 7. The problem? Those cars will start around

The Polestar 5 starts delivering this summer, which means the company will get real-world feedback within months. If it's poorly received or if production delays emerge, the entire roadmap could crumble. This is a high-pressure launch.

Polestar aims to capture 5-10% of the European premium EV market, translating to

The Polestar 4 Estate: A Weirdly Smart Play for Europe

When Polestar unveiled the Polestar 4 in 2023, the biggest question wasn't about performance or range. It was about that missing rear windshield. The design choice immediately became meme material. Why would Polestar intentionally remove a rear window to add cargo space? It seemed backward.

But now Polestar is doubling down. The company is developing a long-roof variant of the Polestar 4—essentially turning it into an estate car or station wagon—that will launch in Q4 2025 (this year, as we look back).

This is actually brilliant product strategy, and here's why: Europe loves station wagons. The estate car market in Europe represents something like 10 to 15% of all vehicle sales, compared to just 2 to 3% in the United States. BMW, Audi, Mercedes—all the premium brands offer wagon variants. Buyers in Germany, Sweden, and the UK actively prefer them.

The Polestar 4 estate addresses a real gap in the EV market. Right now, if you want an electric wagon with performance credentials and Scandinavian design, your options are extremely limited. Tesla doesn't make one. Most Chinese EV makers don't market wagons in Europe. It's wide open.

The challenge, of course, is that the regular Polestar 4 has already struggled to find its audience. Adding a wagon variant doesn't fix the underlying problems—high costs, uncertain demand, design choices that divide opinion. But for the European market specifically, it's a defensible move.

Polestar CEO Michael Longscheller explicitly positioned this as playing to European strengths. "Sweden is famous for its estate cars, and its SUVs are world-class," he said. "We are combining the space of an estate and the versatility of an SUV with the dynamic performance that is Polestar."

Translation: We know Scandinavian buyers, we know European design sensibilities, and we're going to dominate the premium electric estate market. That's a narrower target than global dominance, but it's more defensible.

The Polestar 2 Successor: Resurrecting the Brand's Most Important Model

One of the most unsettling moves Polestar made was stopping production of the Polestar 2. The second-generation sedan was the company's volume seller, the model that proved Polestar could build EVs people actually wanted. When new orders halted, it felt like a death knell.

Now Polestar is saying the new Polestar 2 is coming in early 2027, and it's supposedly being developed at "record speed." CEO Longscheller claims the company is rushing to bring the next-generation model to market.

This is essential, because the Polestar 2 is the financial backbone of the entire company. Without a competitive sedan offering, Polestar is a niche brand. With one, it can compete directly against the Tesla Model 3, BMW i 4, and Mercedes-Benz EQE.

The original Polestar 2 launched with a starting price around $59,900 (before incentives). It offered genuine competition to the Tesla Model 3, with comparable range, faster acceleration (depending on trim), and a vastly superior interior design. The problem was that by 2024, the price advantage had eroded as Tesla cut prices and the EV market became oversupplied.

For the new Polestar 2 to succeed, it needs to offer something the current generation doesn't: lower cost, better efficiency, or both. That almost certainly means a significant redesign of the powertrain and structural components. You don't just speed up development by 30% and hope for the best. There's a technical reason for this urgency.

Likely, Polestar is targeting a starting price closer to

The timeline is aggressive. Developing a completely new sedan platform and getting it into production in under 18 months is ambitious even for established automakers. For a startup still losing money, it's nearly reckless. But it's also necessary. Without the Polestar 2, the entire strategy falls apart.

The Polestar 7: Betting Everything on the Compact SUV Segment

In 2028, Polestar is planning to launch the Polestar 7, a compact premium SUV designed specifically for the European market. This is, by Polestar's own admission, the largest market segment for EVs in Europe.

Let's look at the numbers: in Europe, the compact SUV segment (roughly the size of a Tesla Model Y) accounts for somewhere around 25 to 30% of all EV sales. It's the most competitive, fastest-growing, and most profitable segment. Everyone wants a piece of it.

Here's the problem: the compact premium SUV segment is absolutely brutal right now. Tesla dominates with the Model Y. Chinese makers like BYD (Song Plus DM-i), NIO (ES6), and Li Auto are shipping high-quality, well-designed compact SUVs at prices Western makers can't match. BMW has the X4, Audi has the Q4 e-tron, Mercedes has the GLC EV. Every major brand is already there.

So Polestar's pitch for the Polestar 7 is: "We can offer customers a progressive performance-driven car for a very attractive price point, built in Europe."

The key phrase here is "attractive price point." Polestar is explicitly trying to undercut the established players. That means the Polestar 7 probably targets a starting price around

Building a competitive, profitable compact SUV at that price is extremely challenging. It requires exceptional manufacturing efficiency, minimal features, and possibly battery compromises (smaller capacity, shorter range, less performance). Polestar would be competing on design and handling, not specs.

The upside? If Polestar can nail the design and actually deliver on the "progressive performance" claim, the Polestar 7 could attract a specific subset of European buyers who value Scandinavian aesthetics and responsive handling over maximum specs. It's a focused market, but it's real.

The downside? It's a crowded segment with powerful competitors. Launch timing in 2028 means Polestar won't have a volume compact SUV until the very end of this product roadmap. By then, the competitive landscape could shift dramatically.

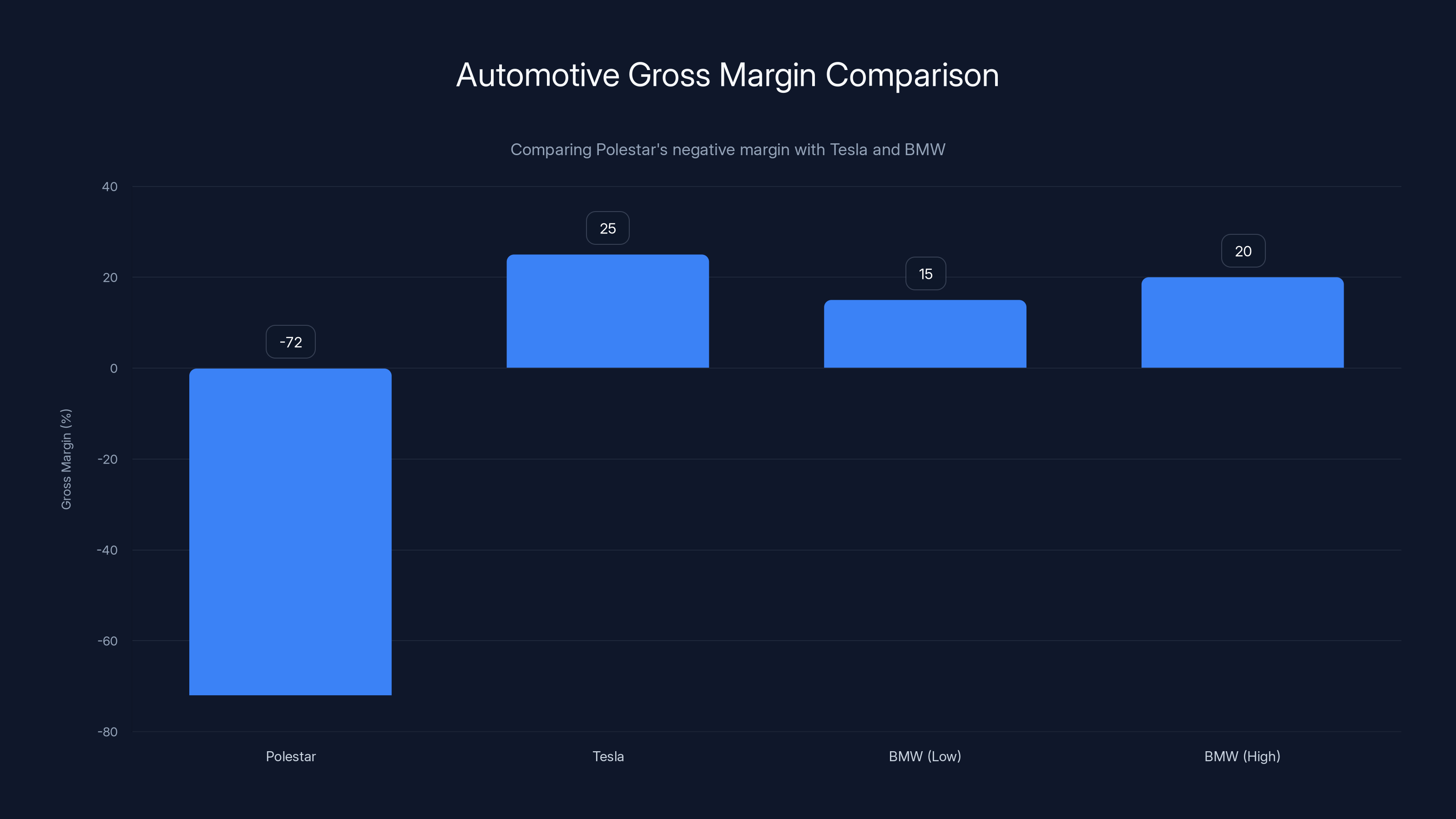

Polestar operates at a significant loss with a gross margin of -72%, compared to Tesla's 25% and BMW's 15-20%. Estimated data based on industry reports.

The Cost-Cutting Strategy: Revamped Models vs. All-New Platforms

Here's where the real business story lies: Polestar isn't just launching four new models. The company is also revamping the Polestar 4 and resurrecting the Polestar 2, which means it's actually refreshing or redesigning some existing platforms rather than building everything from scratch.

This is cost engineering, not product innovation. And it's absolutely critical to Polestar's survival.

Building a completely new vehicle platform costs somewhere between

That's why Polestar is using a hybrid approach:

- New platform for the Polestar 5 (grand tourer requires unique proportions and architecture)

- Modified version of the Polestar 4 platform (estate wagon variant reuses much of the existing structure)

- Heavily redesigned Polestar 2 (likely uses a more efficient platform structure, possibly shared with the Polestar 7)

- New compact SUV platform for the Polestar 7 (but potentially shares underbody components with the Polestar 2)

If Polestar can engineer the Polestar 2 and Polestar 7 to share a platform—the same strategy Volkswagen uses with the MEB platform for the ID.4 and ID.5—the company dramatically reduces development costs. One platform, two vehicles, different body styles and proportions. It's standard automotive engineering.

Longscheller's mention of developing the Polestar 2 at "record speed" likely means they're not building something entirely new. They're probably taking proven components (battery packs, motors, electrical architecture) and optimizing the structure and software for lower cost and better efficiency.

This approach makes financial sense. But it also means Polestar isn't fundamentally innovating. The company is iterating. And in a market where Tesla, Lucid, and Chinese makers are pushing battery technology and autonomy capabilities forward, iteration might not be enough.

Manufacturing Reality: Can Polestar Actually Build These Cars?

Here's a question that doesn't get asked enough: can Polestar actually manufacture four new models in three years while maintaining quality and hitting profitability targets?

Right now, Polestar doesn't own any factories. The company uses manufacturing partners, primarily in China (Geely's Luqiao plant and Chongqing plant) and potentially in other regions. This outsourcing approach reduces fixed costs, but it also limits control over production and scaling.

For perspective, Tesla took nearly a decade to reach profitability, and Elon Musk owned the factories outright. Lucid has been burning cash since day one, despite controlling its Arizona facility. Building EVs at scale profitably is hard.

Polestar's expansion plan assumes the company can:

- Develop four vehicle platforms (or platform variants) simultaneously

- Maintain design consistency and brand identity across all of them

- Establish manufacturing capacity for each vehicle type

- Achieve unit economics that allow profitability even on lower-volume models

- Manage supply chain complexity across multiple production locations

This is genuinely ambitious. Most established automakers can do it because they have decades of institutional knowledge and existing supply chain relationships. Polestar doesn't.

The company's parent, Geely, helps substantially. Geely has manufacturing expertise, supply chain relationships, and financial resources. But there's a limit to how much a parent company can help before the startup loses independence and becomes just another division.

There's also the question of timing. The Polestar 5 launches summer 2025. The Polestar 4 estate launches Q4 2025. The Polestar 2 successor launches early 2027. The Polestar 7 launches in 2028. That's a launch every 6 to 9 months, which is extremely aggressive.

For context, most automakers space major launches 12 to 18 months apart to avoid cannibalizing sales, overwhelming manufacturing capacity, and spreading out development costs. Polestar is compressing that timeline significantly. It's a huge bet that manufacturing partners can scale up, software can be debugged quickly, and the brand can absorb all this new product all at once.

The Profitability Question: When Does Polestar Actually Make Money?

Let's address the elephant in the room: Polestar is losing money at a catastrophic rate.

For context, Tesla's gross margin on automotive sales is around 25%. BMW's is around 15% to 20%. Polestar's is clearly deeply negative, which means the company is losing money on every vehicle sold before you even account for R&D, marketing, and overhead.

How does this happen? The most likely explanation is that Polestar's manufacturing costs are too high relative to its selling prices. The company might be losing

This could be because:

- High-cost manufacturing partnerships with shared profits

- Small production volumes that don't allow for economies of scale

- Quality issues requiring warranty expense or recalls

- Aggressive pricing strategy to gain market share

- Inefficient supply chain and component sourcing

The new product roadmap is supposed to fix this through scale. If Polestar can eventually produce 200,000 vehicles per year instead of 60,000, unit costs drop significantly. A component that costs

But here's the math: to break even at the current loss rate, Polestar would need to reach roughly 250,000 to 300,000 vehicles per year if it only improves gross margins to 5 to 10% (still below industry average). To hit 40% gross margins and actually earn decent profits, the company needs to reach 500,000+ vehicles per year.

The product roadmap aims for maybe 150,000 to 200,000 vehicles per year by 2028 if each model hits reasonable production targets. That would cut losses substantially but might not deliver profitability. Polestar is basically betting that either:

- Manufacturing costs drop faster than expected (battery costs, labor, supply chain improvements)

- Selling prices remain stable (or consumers accept premium pricing for the brand)

- Follow-on products launch after 2028 to reach the ultimate scale targets

Geely's willingness to keep funding suggests the parent company believes in the long-term potential. But financial patience isn't infinite. If Polestar isn't on a clear path to profitability by 2026 or 2027, Geely might cut losses and sell the brand or shut it down.

Estimated pricing for Polestar models shows a strategic range from

Competitive Threats: Why Polestar's Timeline Is So Tight

Polestar isn't operating in a vacuum. The EV market is getting more competitive every quarter. Here's what's coming:

Tesla's Roadster is finally launching in 2025-2026, and it's supposed to have 622 miles of range and acceleration that makes the Polestar 5 look slow. The Cybertruck is ramping production. Model Y pricing continues to drop, making it nearly impossible for any competitor to underprice Tesla in the mass market.

BMW's i 7 and Mercedes-Benz EQS are fully developed and mature, with proven reliability and customer satisfaction. Porsche's Taycan refresh is coming, with better range and lower pricing. These established luxury brands will always have advantages in service networks, financing options, and brand prestige.

Chinese makers are flooding European and Asian markets with well-designed, affordable EVs. BYD just became the world's largest automaker by volume. NIO is expanding into Europe. Li Auto is making profit. These companies have economies of scale, lower labor costs, and battery manufacturing expertise that Polestar can't match.

Traditional automakers are finally getting serious. Volkswagen's ID.5 and ID.4 are becoming real competitors. Audi's e-tron lineup is expanding. Hyundai and Kia are shipping excellent products at competitive prices. Ford and GM are ramping EV production with established dealer networks.

In this environment, Polestar has maybe 24 to 36 months before it becomes irrelevant. That's when this product roadmap needs to pay off. If the Polestar 5 flops, if the Polestar 2 successor misses its timing, if manufacturing problems delay the Polestar 7, the company could lose its window entirely.

It's not just about beating Tesla or Porsche. It's about staying alive long enough to reach profitability before Geely gets impatient or before the competitive landscape shifts in ways Polestar can't adapt to.

Regional Strategy: Why Europe Matters More Than Global Ambitions

Notice that much of Polestar's messaging around these new models emphasizes Europe specifically. The Polestar 4 estate is explicitly designed for European preferences. The Polestar 7's "attractive price point" is benchmarked against European competitors. The Polestar 2 successor will need to compete in markets like Germany, Sweden, and the UK.

This isn't accidental. It's smart strategy. Polestar is effectively choosing to be a European brand rather than a global brand. Here's why that makes sense:

-

European buyers accept higher EV prices than U. S. or Chinese buyers. EV adoption rates in Europe are significantly higher (around 25% of new car sales), which means consumers are more comfortable with electric vehicles and willing to pay premiums for design and performance.

-

European market advantages: Polestar has Volvo and Geely heritage in Europe. The brand is trusted, understood, and associated with Scandinavian quality. That's valuable in markets like Germany, Sweden, and the UK where such associations matter.

-

Regulatory tailwinds: Europe is implementing increasingly strict CO2 emissions regulations, which incentivize automakers to sell more EVs. ICE vehicles will become more expensive to own in Europe over the next decade. That creates a structural advantage for EV-only brands.

-

Smaller market to dominate: Europe's premium EV market is much smaller than China's or potentially the U. S. If Polestar can capture 5 to 10% of the European premium EV market, that's

3 billion in annual revenue. That's enough to be profitable. Trying to compete globally would require 2 to 3 times the scale. -

Supply chain proximity: Volvo's manufacturing facilities are in Europe. Polestar's design studios are in Gothenburg, Sweden. There's natural infrastructure and talent already in place. Trying to build a manufacturing presence in the U. S. or China would require enormous additional investment.

The downside of this strategy is obvious: Polestar is deliberately limiting its addressable market. By focusing on Europe, the company is saying "we don't think we can compete in the U. S. or China, so we're going to dominate in Europe instead." That's a legitimate strategy, but it also means Polestar's ceiling for growth is lower.

For a company losing $1.5 billion annually, a limited-market strategy might actually be more viable than chasing global dominance. Smaller, defensible markets are easier to serve profitably than massive, competitive ones.

The Technology Bet: 800-Volt Architecture and Thermal Management

One consistent theme in Polestar's new vehicles is the emphasis on 800-volt electrical architecture. The Polestar 5 will have it. It's very possible the other models will eventually adopt it too.

Why does this matter? Because 800-volt architecture is becoming the standard for premium EVs, and it delivers real benefits:

-

Faster charging: 800-volt systems can accept higher currents more safely. The Polestar 5 claims 50 minutes to 80% on a DC fast charger. Traditional 400-volt systems might take 45 minutes to 60 minutes for the same amount of charge.

-

Better efficiency: Higher voltages mean lower currents for the same power, which reduces resistive losses in the wiring and components. Over a full charge cycle, that might improve efficiency by 2 to 4%, which translates to 10 to 20 additional miles of range for a given battery size.

-

Better thermal management: 800-volt systems generate less heat, which means less energy is wasted cooling the battery. In hot climates or during fast charging, that's significant.

-

Future-proofing: As charging infrastructure upgrades to faster DC fast chargers (350 k W, 400 k W), 800-volt systems are ready. 400-volt systems will be bottlenecks.

BUT—and this is important—800-volt architecture is not proprietary Polestar technology. Hyundai uses it in the Ioniq 6. Kia uses it in the EV9. Porsche uses it in the new Taycan. It's becoming industry standard.

So while Polestar is right to emphasize this, it's not a differentiator anymore. By the time the Polestar 7 launches in 2028, most premium EVs will have 800-volt systems. It's table stakes, not a competitive advantage.

The real differentiator would be if Polestar develops some proprietary thermal management technology or achieves better efficiency than competitors. But there's no indication that's happening. Polestar is following the industry trend, not leading it.

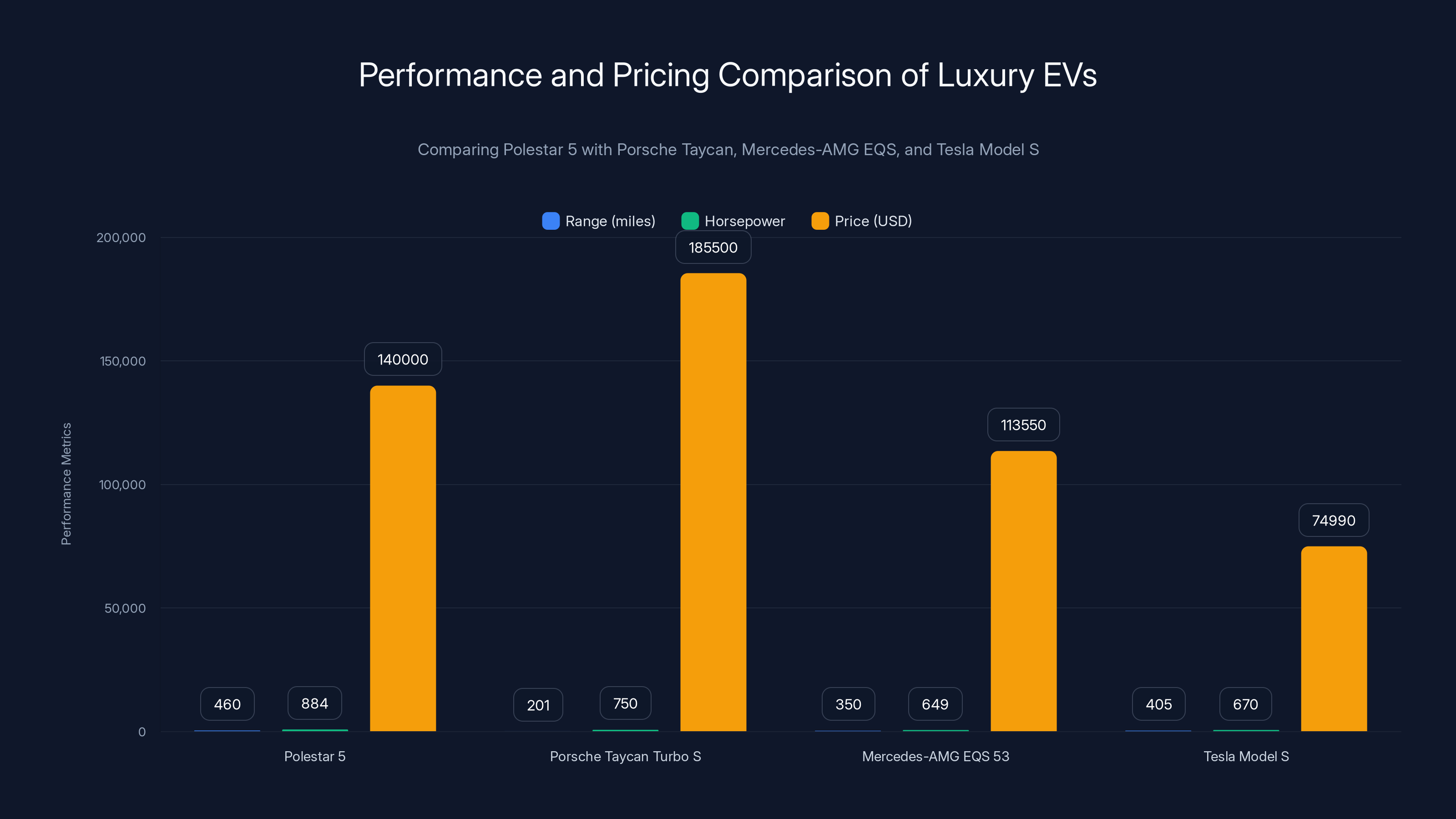

The Polestar 5 offers the highest range and horsepower among its competitors, but its estimated price places it in a competitive luxury market. Estimated data used for Polestar 5 pricing.

Pricing Strategy: Can Polestar Make Money While Staying Competitive?

Pricing is the fundamental constraint on Polestar's profitability. The company needs to price high enough to cover manufacturing costs and fixed overhead, but low enough to compete with established brands and cheaper Chinese alternatives.

Let's estimate what Polestar might price these vehicles at, based on segment positioning:

Polestar 5 (grand tourer):

Polestar 4 estate (SUV wagon):

Polestar 2 successor (sedan):

Polestar 7 (compact SUV):

If we assume average selling prices of

Now, to be profitable at that scale, Polestar needs to achieve:

- Gross margin: 15% to 20% (This is low for premium brands but necessary given startup status)

- Operating expenses: 8% to 12% of revenue (R&D, marketing, overhead)

- Net margin: 3% to 5% (800 million annually)

That's achievable. But here's the catch: Polestar needs to hit 300,000 vehicles per year AND achieve a 15% gross margin simultaneously. That requires both scaling production and dramatically reducing manufacturing costs.

For a company currently losing 72% on revenue, that's an enormous jump. It probably requires:

- Massive battery cost reductions (through better supply chain or next-gen chemistry)

- Manufacturing cost reduction of 25% to 35%

- Operational efficiency improvements across all functions

- Potential asset sales or restructuring to reduce overhead

Geely has to be confident these improvements are achievable, or the company wouldn't be investing in this roadmap. But execution risk is extremely high.

Product Cannibalization: Will These Models Steal Sales From Each Other?

Here's a classic automotive industry problem that Polestar has to manage: when you launch multiple new models in quick succession, they cannibalize each other's sales.

Imagine a customer interested in a Polestar EV. In 2025, they might consider the Polestar 4 estate wagon. But if they wait six months, the Polestar 5 is available. If they wait another year, the Polestar 2 successor launches. If they can wait until 2028, the Polestar 7 is there.

Instead of selling four different products to four different customers, Polestar ends up with one customer who can't decide between four products, so they buy nothing or buy a competitor's product.

Traditional automakers manage this through:

-

Careful pricing separation: Make sure each model has a clearly defined price point. The Polestar 5 at

50,000. There's no overlap. -

Distinct brand positioning: Each model targets a different buyer psychographic. The Polestar 5 is for performance enthusiasts willing to pay premium prices. The Polestar 2 is for practical buyers who want clean design and solid performance at a reasonable price.

-

Timing strategy: Space launches far enough apart that the prior model has already established market share. Don't launch too many models in quick succession.

-

Inventory management: Don't build too much inventory of old models when new ones launch. Accept the loss rather than keep old stock around that cannibalizes the new product.

Polestar is doing some of this through clear price separation. But the launch cadence (every 6-9 months) is aggressive enough that cannibalization risk is real.

This is especially true for the Polestar 2 successor and Polestar 7. Both will be compact vehicles in the

Polestar's hope is that by offering both options, the company captures buyers who might otherwise choose a Tesla, BMW, or Audi. But there's definitely cannibalization happening internally.

Supply Chain Risks: Battery, Semiconductors, and Raw Materials

Every automaker launching new products in 2025 to 2028 is betting that supply chains stabilize and improve. Battery costs continue to drop. Semiconductor supply remains available. Raw materials (lithium, cobalt, nickel) stay affordable.

But these assumptions are not guaranteed. Here's what could go wrong:

Battery supply: If battery suppliers face capacity constraints or if demand outpaces supply, battery costs could stay elevated. This would directly impact Polestar's unit economics. A

Semiconductor supply: If there's another shortage of automotive-grade semiconductors, production could be delayed. Polestar doesn't have the scale leverage to secure supply like Tesla or VW does. Smaller companies get cut in line.

Raw material costs: Lithium prices have already dropped significantly from their 2022 highs, but they're volatile. If geopolitical tensions reduce supply from Australia or China, prices could spike. Cobalt prices are notoriously unpredictable.

Competition for components: As more automakers ramp EV production, competition for key components intensifies. Polestar's smaller scale means it might not get preferred pricing or terms from suppliers.

Vertical integration: Polestar doesn't own battery manufacturing, semiconductor design, or raw material mining. The company is entirely dependent on suppliers and manufacturing partners. If those relationships deteriorate, Polestar has limited options.

Geely's ownership helps here. Geely has relationships with battery suppliers and can potentially secure favorable terms. But Polestar is still more vulnerable to supply chain disruption than an integrated automaker like Tesla or a massive conglomerate like VW.

Estimated data shows that revamping existing models like the Polestar 4 and 2 is significantly cheaper than developing entirely new platforms, aiding Polestar's cost-cutting strategy.

The Marketing Challenge: Building a Desirable Brand While You're Losing Money

Polestar faces a brutal marketing problem: the brand needs to convince buyers it's a premium alternative to established brands, while it's actively losing money and still building reputation.

Tesla solved this through Elon Musk's personal brand and by offering genuinely superior performance specs. Porsche solved it through decades of motorsports heritage. Mercedes solved it through 140+ years of luxury brand history.

Polestar has what? A spin-out from Volvo that's only 8 years old as an independent brand, with a couple of successful models and a lot of failed promises.

That's not a good narrative to sell. Buyers don't want to buy from a startup that might fail. They want to buy from established brands with proven service networks and reliable resale values.

Polestar's marketing bet is that Scandinavian design and performance, combined with Swedish heritage (through Volvo), can resonate with European buyers who value minimalism and quality. That's a legitimate positioning. But it requires consistent execution and massive marketing spend.

The company is investing in design as a differentiator, which is smart. Polestar's cars look better than most competitors. The interiors are cleaner. The user experience is more thoughtful. These intangibles matter to premium buyers.

But intangibles don't overcome economic uncertainty. If Polestar is still losing money in 2027, and if Geely signals that profitability is further away than expected, brand perception will deteriorate rapidly. Buyers will see Polestar as a risky bet, not a premium choice.

Polestar's marketing roadmap needs to include big splashy moments—racing victories, celebrity endorsements, tech innovations that get media attention. The Polestar 5's launch this summer is exactly that kind of moment. A halo car with impressive specs gets auto journalists excited and generates free press.

But one good launch isn't enough. The company needs consistent wins over the next three years. Every product launch needs to exceed expectations, impress reviewers, and generate positive sentiment.

Geely's Strategic Patience: How Long Will Parent Company Support Continue?

Ultimately, this entire roadmap depends on Geely's willingness to keep funding Polestar's losses.

Let's be clear:

Why hasn't Geely? A few theories:

-

Geely believes in the long-term potential. The parent company sees a path to profitability and thinks Polestar will eventually be worth

20 billion. That's a reasonable bet if you're willing to lose5 billion to get there. -

Geely uses Polestar for brand elevation. Volvo is a reliable, slightly boring brand. Polestar is performance-focused, premium, and edgy. By nurturing Polestar, Geely gains a luxury brand that can charge premium prices and attract younger, more enthusiastic buyers.

-

Strategic optionality. Geely is betting that EV technology evolves in ways that favor Polestar's platform choices, supply chain positions, or design philosophy. If battery costs drop faster than expected, Polestar suddenly becomes profitable.

-

Exit strategy. Geely might be building Polestar to eventually sell to a larger automaker or private equity firm. A successful IPO or strategic sale could generate billions in value. That's not crazy—Volvo itself was spun out from Ford and sold to Geely for $1.8 billion in 2010. Polestar could follow a similar path.

But here's the key question: how much longer will Geely wait?

If the Polestar 5 launches and gets poor reviews, if pre-orders disappoint, if manufacturing issues emerge, Geely's patience could evaporate quickly. Strategic patience has limits.

My estimate is that Geely has maybe

So Polestar's profitability timeline isn't just about business strategy. It's about survival. The company needs to demonstrate a clear path to breakeven by 2027, or the funding might stop.

The Upside Scenario: If Everything Goes Right

Let's imagine best-case execution. What does success look like for Polestar?

By 2028, Polestar could have:

- Polestar 5 (grand tourer): 15,000 to 20,000 units annually at 2.1 to300 to $400 million in gross profit**.

- Polestar 4 (estate wagon): 30,000 to 40,000 units annually at 2.0 to240 to $310 million in gross profit**.

- Polestar 2 (sedan): 80,000 to 100,000 units annually at 4.0 to400 to $500 million in gross profit**.

- Polestar 7 (compact SUV): 70,000 to 90,000 units annually at 3.4 to340 to $430 million in gross profit**.

Total: 195,000 to 250,000 vehicles annually,

With operating expenses managed to around

That's profitable. Not spectacularly profitable, but profitable enough to sustain operations, reward investors, and fund product development. It's realistic if execution is strong.

The Downside Scenario: Where This Falls Apart

Now let's imagine things go wrong. What does failure look like?

The Polestar 5 launch is mediocre. Reviews are mixed. Production ramps slower than expected. Customers complain about quality issues or long wait times. By 2026, the company has delivered only 5,000 to 8,000 units instead of projected 15,000.

The Polestar 4 estate wagon flops. European buyers don't love it. Design reviews criticize it. By 2027, annual sales are only 10,000 to 15,000 units instead of 35,000.

The Polestar 2 successor is delayed. Manufacturing problems, software bugs, or design changes push launch to mid-2027 instead of early 2027. By the time it arrives, it's outdated and underwhelming. Sales are sluggish.

The Polestar 7 faces intense competition. By 2028, the compact SUV market is flooded with excellent alternatives. Polestar's premium positioning doesn't resonate with price-conscious buyers. Annual sales reach only 30,000 to 40,000 units instead of 80,000.

In this downside scenario, Polestar's 2028 revenue is maybe

With operating expenses still around

What Analysts Are Saying: Market Skepticism

Polestar's announcement of four new models was received with cautious optimism by market analysts, but there's underlying skepticism.

The core concern is execution. Polestar has promised ambitious product roadmaps before. The original business plan was supposed to deliver profitability by 2023 or 2024. That didn't happen. Now the company is promising profitability by 2027 or 2028. Why should anyone believe it?

Second, there's doubt about whether the market actually wants four new Polestar models. The brand still has limited recognition compared to Tesla or traditional luxury brands. Can Polestar really sell 200,000+ vehicles per year when most people have never heard of the brand?

Third, there's the Geely question. How much longer will the parent company fund losses? If Geely decides to cut Polestar loose, the entire roadmap collapses. That risk premium is baked into how analysts value the business.

My reading is that most analysts see Polestar's roadmap as ambitious but achievable—if everything goes right. The probability of everything going right is maybe 40% to 50%. The probability of some combination of delays, competitive pressure, and execution issues derailing the plan is 50% to 60%.

Those aren't great odds.

Investment Thesis: Is Polestar Worth Betting On?

For potential investors or stakeholders, the question is whether Polestar represents a good long-term bet.

The bull case is straightforward: Polestar has premium positioning, Scandinavian design heritage, and a parent company with deep pockets. If the company can execute on this roadmap and reach 250,000+ vehicles per year at 12% to 15% gross margins, the business could be worth

That would represent a 10x to 15x return on Geely's investment, which is compelling. For Geely, that might mean returning Volvo and Polestar as a separate, IPO-ready company worth tens of billions.

The bear case is equally straightforward: Polestar is a startup losing $1.5 billion per year, trying to compete in a market being dominated by Tesla and Chinese makers. The company has no proven track record of profitability. The product roadmap is unproven. Geely's patience isn't infinite. The company is more likely to be acquired, sold for scrap, or shut down than to achieve independent profitability.

My assessment: Polestar is a high-risk, high-reward bet. The outcome depends almost entirely on execution over the next 18 to 24 months. If the Polestar 5 succeeds and if there are no major setbacks with the Polestar 4 estate wagon, Polestar's odds of survival improve dramatically. If either of those falters, the company's future becomes very uncertain.

For Geely, the bet makes strategic sense. For other investors or stakeholders, it's a speculative wager on a company with limited margin for error.

TL; DR

- Polestar is launching four new EV models by 2028: the Polestar 5 grand tourer (summer 2025), Polestar 4 estate wagon (Q4 2025), Polestar 2 sedan successor (early 2027), and Polestar 7 compact SUV (2028)

- **The company is losing 2.17 billion in revenue, making profitability a critical business challenge that new models must address

- Scale is the key lever: Polestar needs to reach 250,000 to 300,000 vehicles per year to achieve profitability, compared to current production of 60,000

- Europe is the strategic focus: Rather than pursuing global dominance, Polestar is targeting the European premium EV market where the brand has heritage and regulatory tailwinds

- Execution risk is extremely high: The 18-month launch cadence is aggressive, competition is intensifying from Tesla and Chinese makers, and supply chain risks remain

- Geely's funding is the survival factor: The parent company's continued investment is critical, but patience likely expires by 2027 if profitability isn't on the horizon

FAQ

What is Polestar's four-model strategy?

Polestar announced plans to launch four new electric vehicles between 2025 and 2028: the Polestar 5 (grand tourer), Polestar 4 estate wagon variant, a redesigned Polestar 2 sedan, and the Polestar 7 (compact SUV). The strategy aims to expand the brand's portfolio across multiple market segments and achieve profitability through increased scale. This aggressive roadmap represents Polestar's attempt to compete in a rapidly consolidating EV market.

Why is Polestar losing so much money?

Polestar is operating at a gross loss, meaning manufacturing costs exceed selling prices. This is typical for startups scaling production, but the magnitude is extreme, with the company reporting a 72% loss margin in 2025. The primary culprits are high manufacturing costs (Polestar doesn't own factories and relies on partners), production volumes too small to achieve economies of scale, and aggressive pricing needed to gain market share. As the company scales to higher production volumes, unit costs are expected to drop significantly, improving margins.

What makes the Polestar 5 special?

The Polestar 5 grand tourer offers 460 miles of EPA range, 800-volt charging architecture, 884 horsepower, and 0-60 acceleration in 3.1 seconds. These specifications are competitive with the Porsche Taycan Turbo and Mercedes-AMG EQS, but at a different price point. The Polestar 5 is positioned as a luxury performance vehicle starting above $120,000, designed as a halo car to enhance brand perception and attract performance-focused customers.

How does the Polestar 4 estate wagon address market demand?

The estate wagon variant of the Polestar 4 targets European preferences, where station wagons represent 10 to 15% of vehicle sales. This variant combines the cargo space and practicality of a traditional wagon with the efficiency and performance of an electric vehicle. In Europe's premium EV segment, there are few high-performance electric wagons available, making the Polestar 4 estate a differentiated offering in a valuable niche.

When will the new Polestar 2 arrive, and why was it discontinued?

The original Polestar 2 stopped accepting new orders in 2024, and the next-generation model is launching in early 2027. Polestar halted production to focus development resources on the complete redesign, aiming for lower manufacturing costs and better efficiency. The new Polestar 2 is critical to profitability because it will be the highest-volume model, targeting a starting price around

What is the Polestar 7, and why does it matter?

The Polestar 7 is a compact premium SUV launching in 2028, targeting the largest EV market segment in Europe. Compact SUVs currently represent 25 to 30% of EV sales in Europe, and Polestar is positioning the Polestar 7 as a performance-focused alternative at an "attractive price point" (estimated

Can Polestar achieve profitability with this roadmap?

Profitability depends on Polestar reaching approximately 250,000 to 300,000 vehicles per year while achieving gross margins of 12% to 15%. If the four new models hit sales targets and manufacturing costs drop as expected, the company could reach operating profitability by 2028 or 2029. However, execution risk is high. Delays, competitive pressure, or lower-than-expected sales would keep the company unprofitable and dependent on Geely's continued funding.

What is the 800-volt electrical architecture, and why does it matter?

An 800-volt electrical system enables faster charging speeds, better efficiency, and improved thermal management compared to traditional 400-volt systems. The Polestar 5 will feature this technology, allowing 50-minute charging to 80% on compatible fast chargers. However, 800-volt architecture is becoming industry standard, with Hyundai, Kia, and Porsche already adopting it. It's a necessary feature, not a competitive advantage.

How is Polestar positioning itself regionally?

Rather than pursuing global dominance, Polestar is strategically focusing on Europe, where the brand has heritage through Volvo and Geely. This approach allows Polestar to compete in a defined market with favorable regulations, higher EV adoption rates, and buyer preferences aligned with Scandinavian design. European buyers are willing to pay premiums for design and prestige, and estate cars remain popular in a way they aren't in the U. S., making Europe Polestar's natural primary market.

What are the biggest risks to Polestar's roadmap?

Major risks include manufacturing delays (the 6 to 9-month launch cadence is aggressive), supply chain disruptions, competitive intensity in key segments, and Geely's funding decisions. The Polestar 5's launch performance will be crucial for demonstrating feasibility. Additionally, if the new Polestar 2 is delayed or if the Polestar 7 faces stronger competition than expected, the entire profitability timeline shifts. Most critically, if Geely determines that losses will continue beyond 2027, the company could pull funding entirely.

Conclusion

Polestar is at a critical inflection point. The company's announcement of four new models by 2028 represents either a carefully calculated survival strategy or an ambitious gamble that will end in failure. The truth probably lies somewhere in between.

The fundamentals are both compelling and terrifying. Yes, the EV market is growing. Yes, there's demand for premium, design-focused vehicles. Yes, Scandinavian heritage and Volvo's reputation provide some advantages. But Polestar is also bleeding cash at an unsustainable rate, competing against Tesla (which has proven it can win at scale and profitability), traditional luxury brands with deep pockets and established dealer networks, and increasingly capable Chinese EV makers.

The next 18 to 24 months will be decisive. If the Polestar 5 launches successfully, if customer demand is strong, and if manufacturing partners can reliably scale production, Polestar's odds of survival improve substantially. If any of those falters, the company's future becomes very uncertain.

For buyers considering a Polestar, that uncertainty matters. You're not just choosing a car. You're betting on a company. You're betting that service networks will exist in five years, that parts availability won't become a nightmare, that resale value won't collapse. For some buyers, that's worth the risk. The Polestar 5 is genuinely impressive. The design is exceptional. But risk is real.

For Geely, the bet is more speculative. The parent company is essentially saying "we're willing to lose

The EV market is consolidating rapidly. There will be winners and losers. Polestar has the positioning, the product, the parent company backing, and the strategic clarity to be a winner. But execution has to be nearly perfect. There's no margin for error. The company is running out of time to prove it can actually build profitable electric vehicles at scale.

Watch the Polestar 5's launch closely. That will tell you everything you need to know about whether this strategy actually works.

Use Case: Polestar's ambitious product roadmap requires sophisticated market analysis, competitive positioning, and financial forecasting—exactly what AI-powered automation platforms streamline.

Try Runable For FreeKey Takeaways

- Polestar is launching four new EV models between 2025-2028 (Polestar 5, 4 estate, 2 successor, 7) in a high-risk bid for profitability

- The company is currently losing 2.17 billion in revenue, requiring significant scale improvements for profitability

- Polestar needs to reach 250,000-300,000 vehicles per year at 12-15% gross margins to achieve sustainable profitability by 2028

- Strategic focus on Europe leverages Volvo/Geely heritage and favorable regulatory environment for EVs in premium market segments

- Execution risk is extremely high with aggressive 6-9 month launch cadence, intense competition from Tesla and Chinese makers, and Geely's patience as a critical limiting factor

Related Articles

- Tesla's 46% Profit Collapse in 2025: What Went Wrong [2026]

- Rivian's Software Partnership Saves the EV Maker: 2025 Analysis [2025]

- How Rivian's Software Strategy Saved the Company in 2025

- Tesla's Second Year of Revenue Decline: Market Analysis & Implications [2025]

- Volvo EX60 Software Revolution: How Volvo Solved EV Infotainment [2025]

- Chinese Battery Factories Are Reshaping Global Manufacturing [2025]