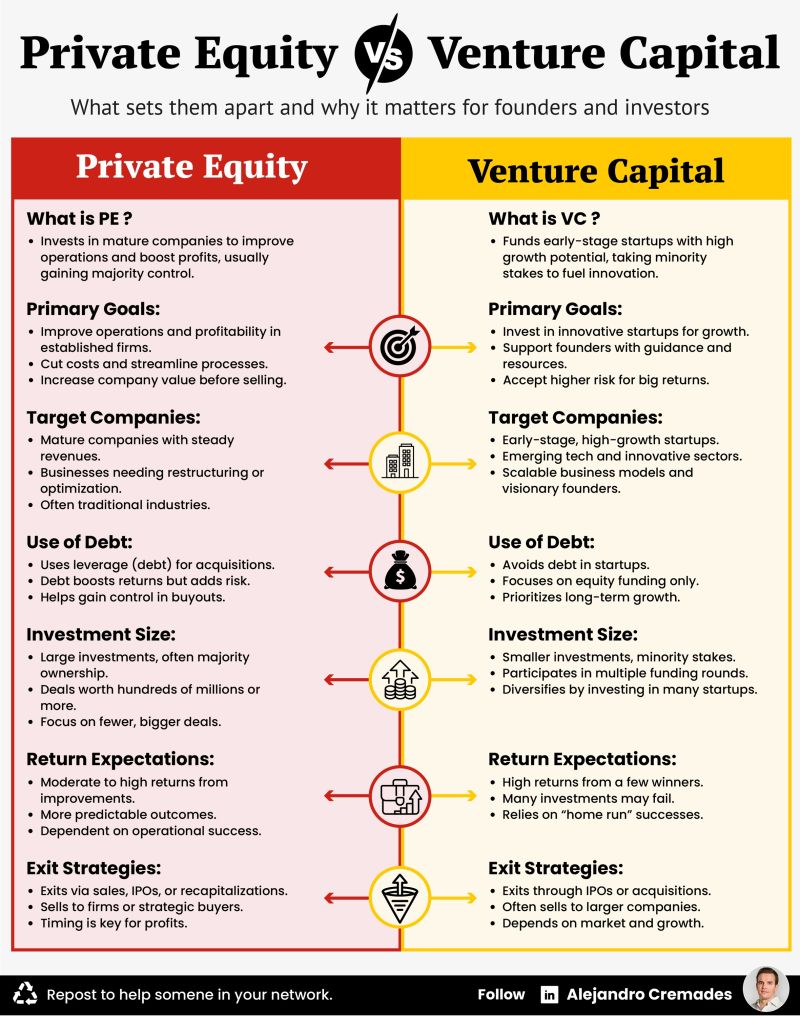

![Private Equity Is Abandoning Mid-Market SaaS. Here's What Founders Must Do [2025]](https://tryrunable.com/blog/private-equity-is-abandoning-mid-market-saas-here-s-what-fou/image-1-1770392238752.jpg)

Private Equity Is Abandoning Mid-Market SaaS. Here's What Founders Must Do [2025]

There's a moment that hits every bootstrapped SaaS founder around $15-20M ARR. You're talking to an investor at a conference, maybe you bumped into a partner at Thoma Bravo or Vista Equity Partners, and suddenly someone's asking about your numbers. Your retention is solid. Growth is predictable. The conversation shifts from "Can we build this?" to "At what multiple?"

For the last decade, that conversation ended one way: a term sheet.

PE had the playbook down. Find a B2B SaaS company with decent metrics, solid unit economics, and predictable cash flow. Slap 5-7x revenue multiple on it. Roll up your sleeves and either compound it quietly or merge it into a portfolio company for scale. Eventually, take it public or flip it to a strategic buyer at 9-10x. Rinse, repeat, get rich.

That script is done. And if you're building a solid-but-not-spectacular SaaS company in 2025, you need to know this before you waste a year chasing PE conversations that won't materialize.

The data is brutal. M&A in tech hit

Let's be honest about what's happening, why it happened, and what you actually need to do about it if you're in the middle of this storm.

TL; DR

- PE concentration is extreme: Megadeals drive 50%+ of 2025 transaction value; non-AI, steady-growth SaaS saw deal flow drop 17%

- The old playbook is dead: Hitting $20M ARR with 20% growth and solid retention no longer guarantees a PE exit

- Three forces converged to kill it: Higher rates destroyed the multiple math, growth expectations reset upward, and the exit environment got tighter

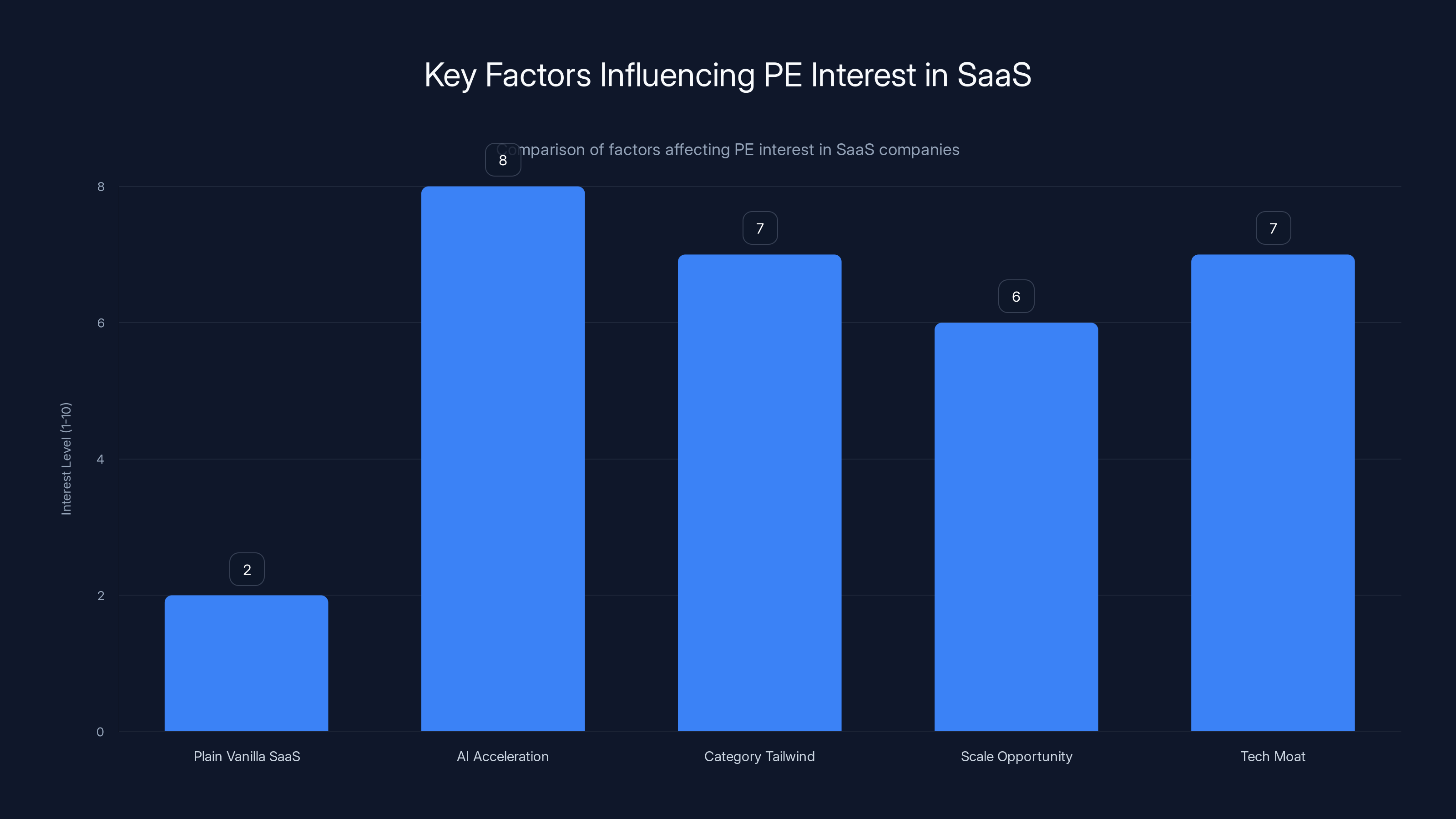

- Plain vanilla SaaS is radioactive: PE checks out on solid-but-uninspiring companies unless they have AI acceleration or category tailwinds

- Founders must adapt: The only viable paths forward are go-big (hunt for strategic growth), go-profitable (maximize cash flow), or go-different (find alternative buyers)

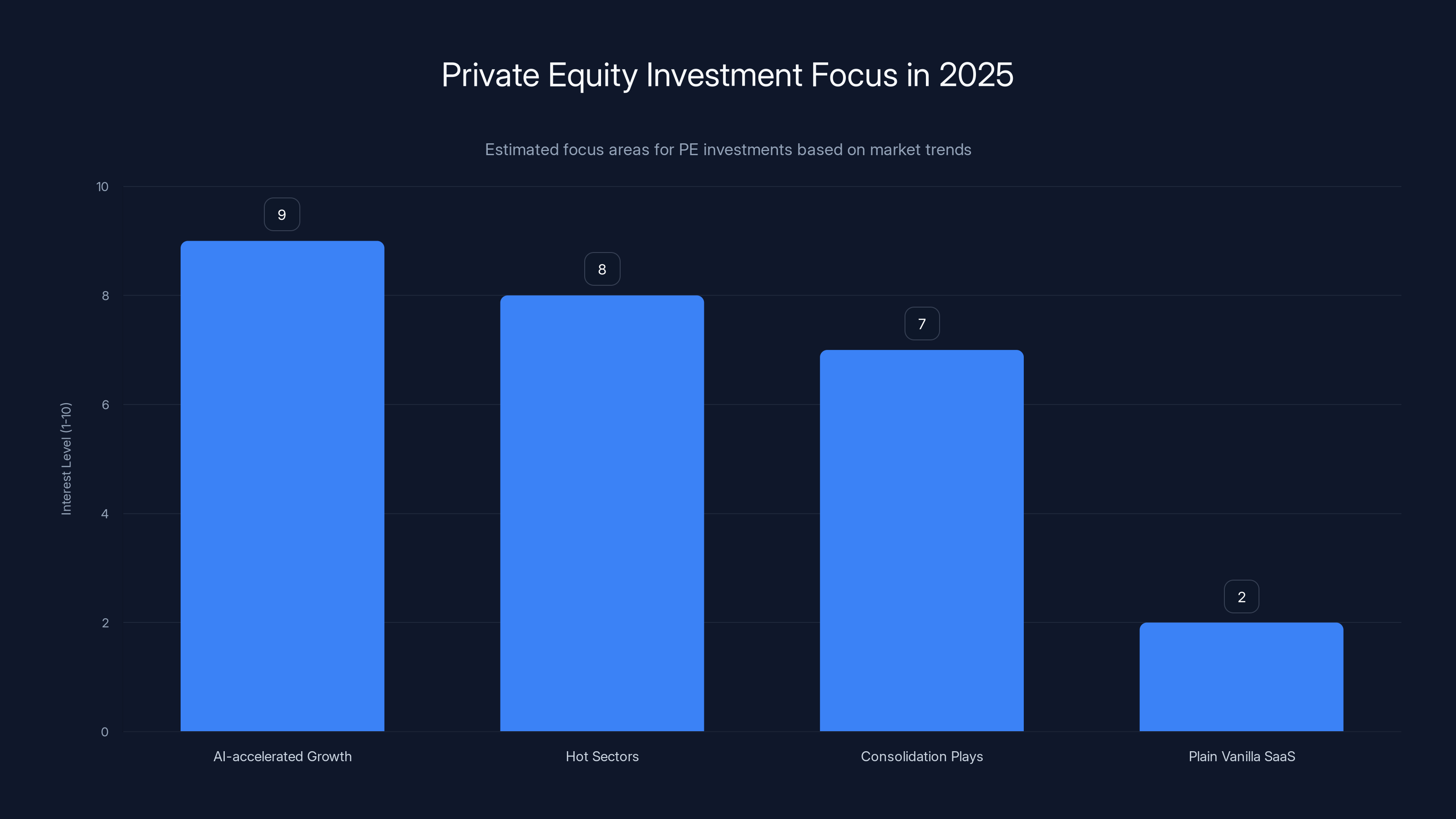

In 2025, PE firms are highly interested in AI-driven growth and hot sectors, while traditional SaaS without AI or market tailwinds sees minimal interest. (Estimated data)

The PE Playbook That Worked for a Decade—And Why It Suddenly Collapsed

Let me paint the picture of how this actually worked from 2012 to 2023.

You hit $20M ARR. You had maybe 110% net revenue retention—customers not churning, expanding a bit. You weren't burning insane cash. You grew at least 20% year over year. That was it. You didn't need to be hypergrowth. You didn't need to be winning your category. You just needed to exist on that specific grid.

When you did, PE firms materialized. Sometimes two, sometimes three. They'd look at your customer base, see that attrition was low and expansion was real, model out 15-year cash flows, and suddenly you had multiple 6x offers on the table. Sometimes 7x or 8x if you were in a decent sector.

Why was this so reliable? Because NRR was everything. If customers stuck around and spent more over time, the underlying economics worked. PE didn't need you to be a rocket ship. They needed you to be a compounding machine. They could borrow cheap money, buy your company, let it compound, and in five years the debt would be paid down and they'd have a 4-5x return even if they never accelerated growth at all.

This created a safety net that fundamentally shaped an entire generation of SaaS company-building. You could optimize for profitability instead of growth. You could focus on customer success instead of land-and-expand. You could be boring and boring was worth

Then everything changed.

Three forces hit the system simultaneously:

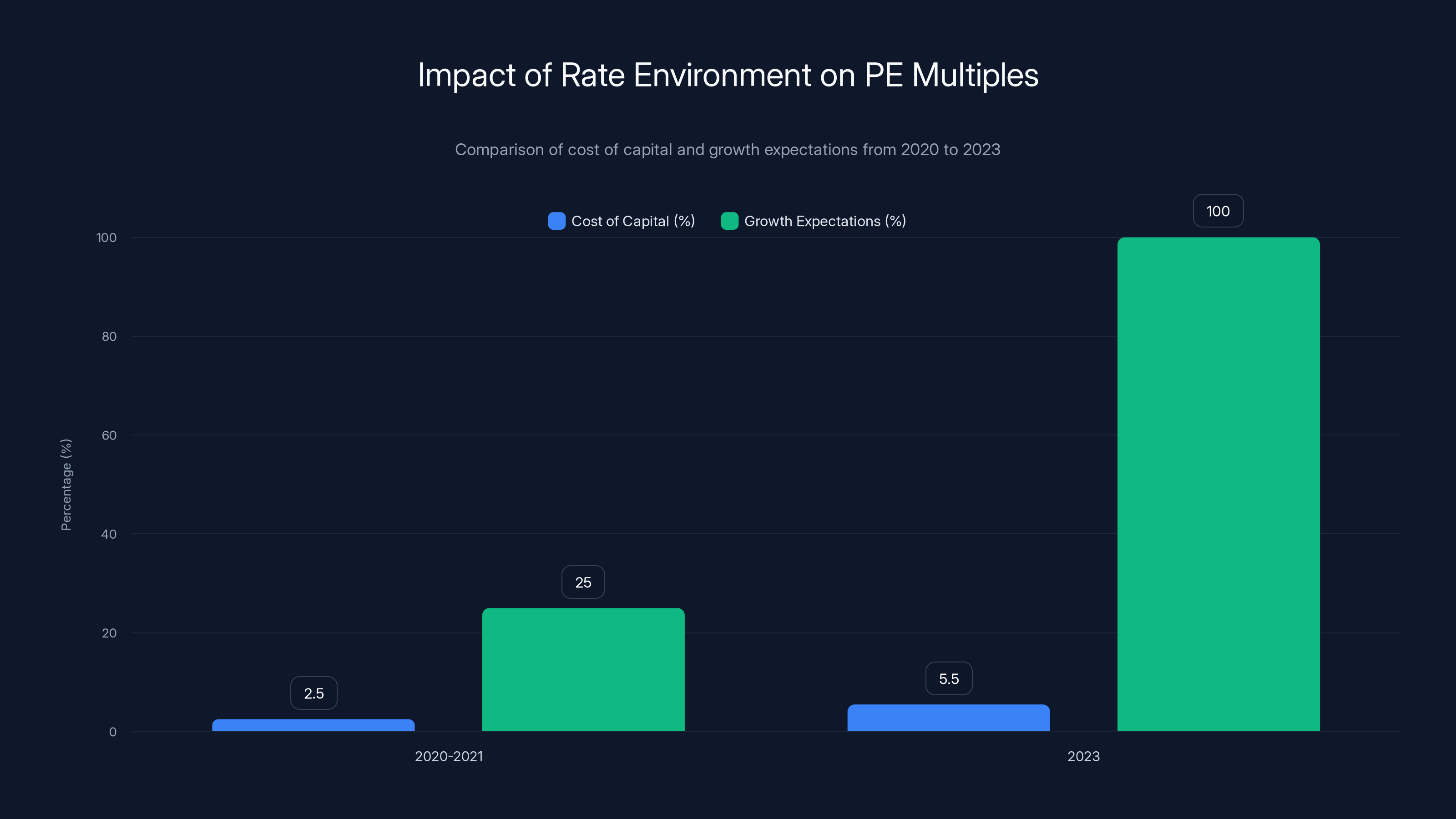

First, the rate environment: PE firms borrowed aggressively when money was free. Your 5% cost of capital suddenly became 5%+. For a 20% growth company, that math breaks immediately. When your hurdle rate jumps 500 basis points, you can't pay the same multiples. A company that generated solid returns at 3% cost becomes mediocre at 5%. PE's entire return model, which relied on cheap leverage, collapsed.

Second, the growth bar reset: AI happened. Suddenly PE firms were seeing companies with 100%+ growth rates. Not theoretical growth. Real growth in real companies. After seeing that, why would they get excited about a steady 20% grower? They started hunting for everything to potentially 3x or 4x with AI tailwinds. Slow-and-steady wasn't slow-and-steady anymore. It was slow-and-boring.

Third, the exit environment tightened: PE ultimately needs exits. IPOs or strategic sales. With only 6 pure-play software IPOs in all of 2025, that path narrowed considerably. And strategic acquirers stopped buying at whatever multiples. They got selective. If PE can't confidently exit at 10x+ ARR, they can't pay 8x on the way in.

Let me be blunt: all three of these forces are still in effect. They're not going away in 2026. The rate environment isn't returning to zero. The growth bar isn't resetting downward. The exit environment isn't loosening.

This is the new normal.

The 2025 Bifurcation: What Changed and What It Means

The data from 2025 tells a story of extreme concentration. It's not that PE disappeared. They're doing record numbers of deals. But they're hunting very different prey than they used to.

Here's what PE is buying right now:

AI-accelerated growth stories. If AI is genuinely reigniting your growth curve, not marketing fluff but real acceleration in the numbers, PE gets interested. They can model the upside. They can see a thesis beyond "steady compounder." A SaaS company that was growing 25% suddenly accelerates to 50% because of AI features? That pencils at different multiples.

Hot sectors with secular tailwinds. Security. Certain parts of fintech. Infrastructure plays benefiting from AI workloads. If you're in a category where the market itself is expanding, PE can justify higher multiples because the rising tide lifts their returns. The multiple you get is no longer just on your current business—it's betting on category growth.

Consolidation plays at real scale. PE is still happy to buy a

Here's what PE has completely checked out on:

Plain vanilla SaaS. Good retention. Okay growth. Solid but uninspiring unit economics. No clear AI angle. No hot category tailwind. Maybe a $200M exit opportunity five years ago. Today? Silence.

The messaging is usually polite. "We think you're a great business, but it's not the right stage for us." What they actually mean is: "The multiple math doesn't work. Your debt service would crush returns. And I have no idea how to exit this in five years."

Let me show you what this bifurcation actually looks like in numbers:

The megadeals (Wiz, Scale AI, Armis) are pulling in capital that used to be distributed across 50-100 mid-market deals. Those companies aren't just bigger—they're solving different problems. Wiz is AI for security. Scale AI is AI infrastructure. These aren't plain vanilla SaaS. They're category-defining, venture-backed hypergrowth companies that happen to be getting PE attention.

The tuck-ins are still happening, but they're happening at the high end. A

The also-rans, the solid B2B SaaS companies that would've been perfect PE candidates in 2020, are sitting in a weird gap. Too big to ignore, too small to be interesting. Too profitable to be venture-scale, too slow-growing to be AI-worthy.

That's where most founders are right now. And that's the problem.

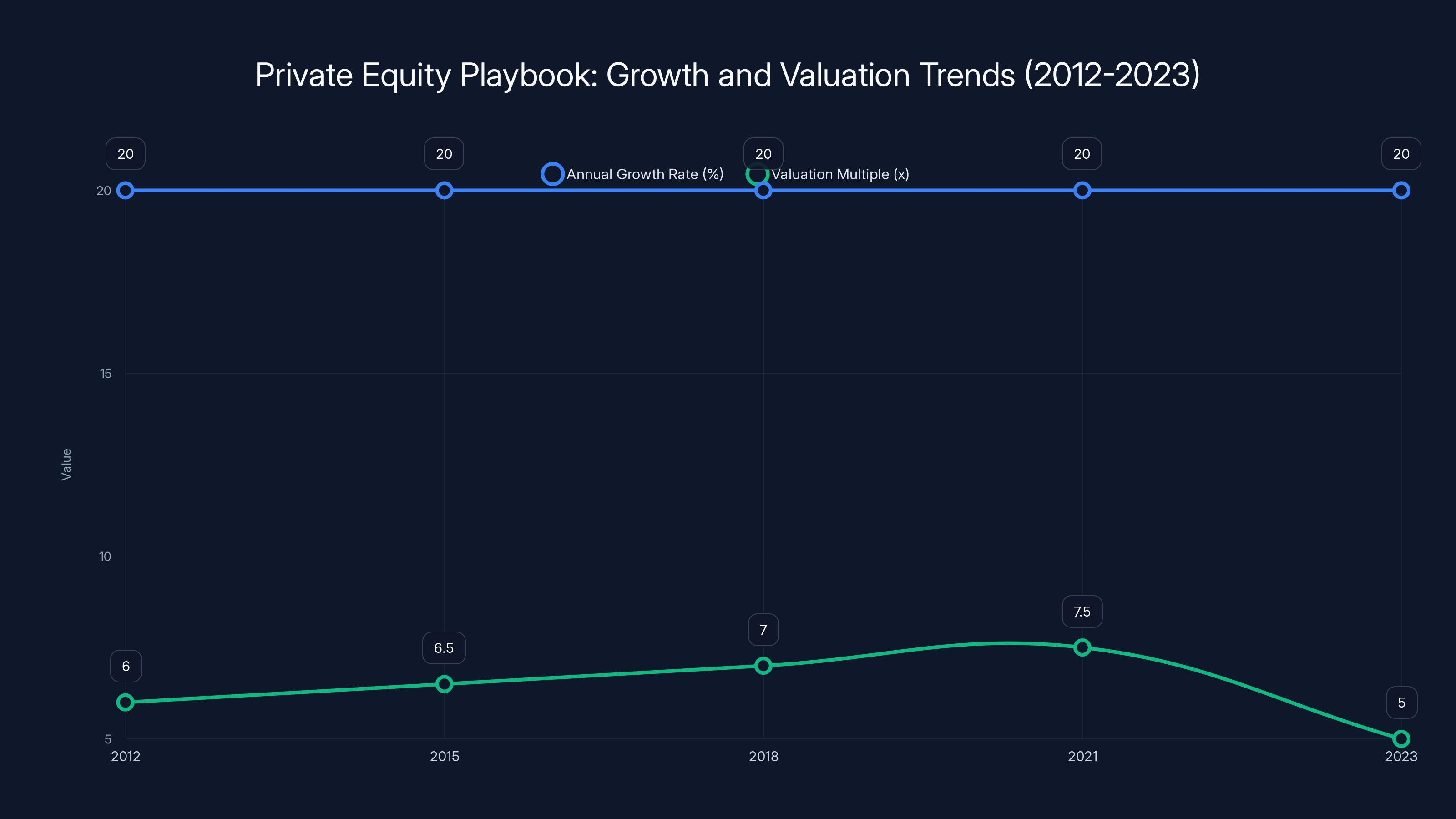

From 2012 to 2021, SaaS companies consistently grew at 20% annually with valuation multiples increasing from 6x to 7.5x. However, by 2023, multiples dropped to 5x due to changing economic conditions. Estimated data.

Why the Multiple Math Broke: The Rate Environment, Growth Expectations, and Exit Velocity

Let me walk through the math that actually changed, because understanding this is critical if you're trying to decide what to do with your company.

The rate environment is the easiest to understand. PE borrowed aggressively at near-zero rates. Let's say you're modeling a $30M ARR business. In 2020-2021, a PE firm might finance the acquisition at 2-3% cost of capital. That allowed them to pay 6-7x ARR because they could model returns even with modest growth acceleration.

Now that rates are 5%+, the cost of capital has doubled. That same business, at the same multiples, suddenly generates terrible returns when your debt is costing 5% and the company is only growing 20%. The math is simple: higher debt service = lower equity returns. So either PE has to pay lower multiples, or the company has to be growing faster. Most companies in the middle market can't grow faster on demand, so multiples had to fall.

How much did this matter? A lot. For a moderately leveraged deal, a 200-300 basis point increase in cost of capital can swing a deal from "attractive" to "pass" in minutes.

The growth expectation reset is more subtle but more important. PE's definition of "exciting" used to be 20-30% growth with great retention. That was above market, sustainable, and valuable. Now PE has seen companies growing 80-100%+ with AI tailwinds. That changed their mental anchors.

It's the anchoring bias at scale. When you're pitching to PE, they're not just thinking about your company. They're thinking about the AI company they looked at yesterday that's doing 120% growth. A 25% grower doesn't excite them the way it used to. It's not bad, it's just boring relative to what's possible.

This doesn't require AI to actually work at scale. It just requires PE to believe it might. And they do. So the growth bar got reset, and steady compounders fell out of favor.

The exit environment tightness is the most concerning because it's structural. PE needs to eventually exit the businesses they buy. They either go public (IPO), get acquired by a strategic buyer, or get recapitalized/sold to another PE firm. Those are the only three paths.

IPOs are effectively closed. In 2025, there were 6 pure-play software IPOs. Six. In a market of thousands of SaaS companies, six exits via IPO. That path is essentially off the table for most companies. A PE firm can't pay 7x ARR if they're not confident they can IPO you at some point.

Strategic acquisitions are still happening, but strategics have gotten selective. They're not buying 30-person companies with $30M ARR. They're buying companies that 1) solve a specific problem they can't solve internally, 2) have irreplaceable engineering talent or tech, or 3) give them access to customers they can cross-sell into. Plain vanilla SaaS doesn't check those boxes.

PE-to-PE exits (one firm selling to another) are still possible, but they're competitive and multiples are getting compressed. If you're exiting to another PE firm, you need some story that justifies why they should pay more than the last guy paid. If you're just a steady compounder, that story is hard to tell.

Here's what this means for your company: The exit path that seemed inevitable in 2020-2023 is no longer inevitable. It's not even likely for most sub-$100M ARR companies.

The Data Shows Extreme Concentration at the Top

Let me show you what the actual market looked like in 2025.

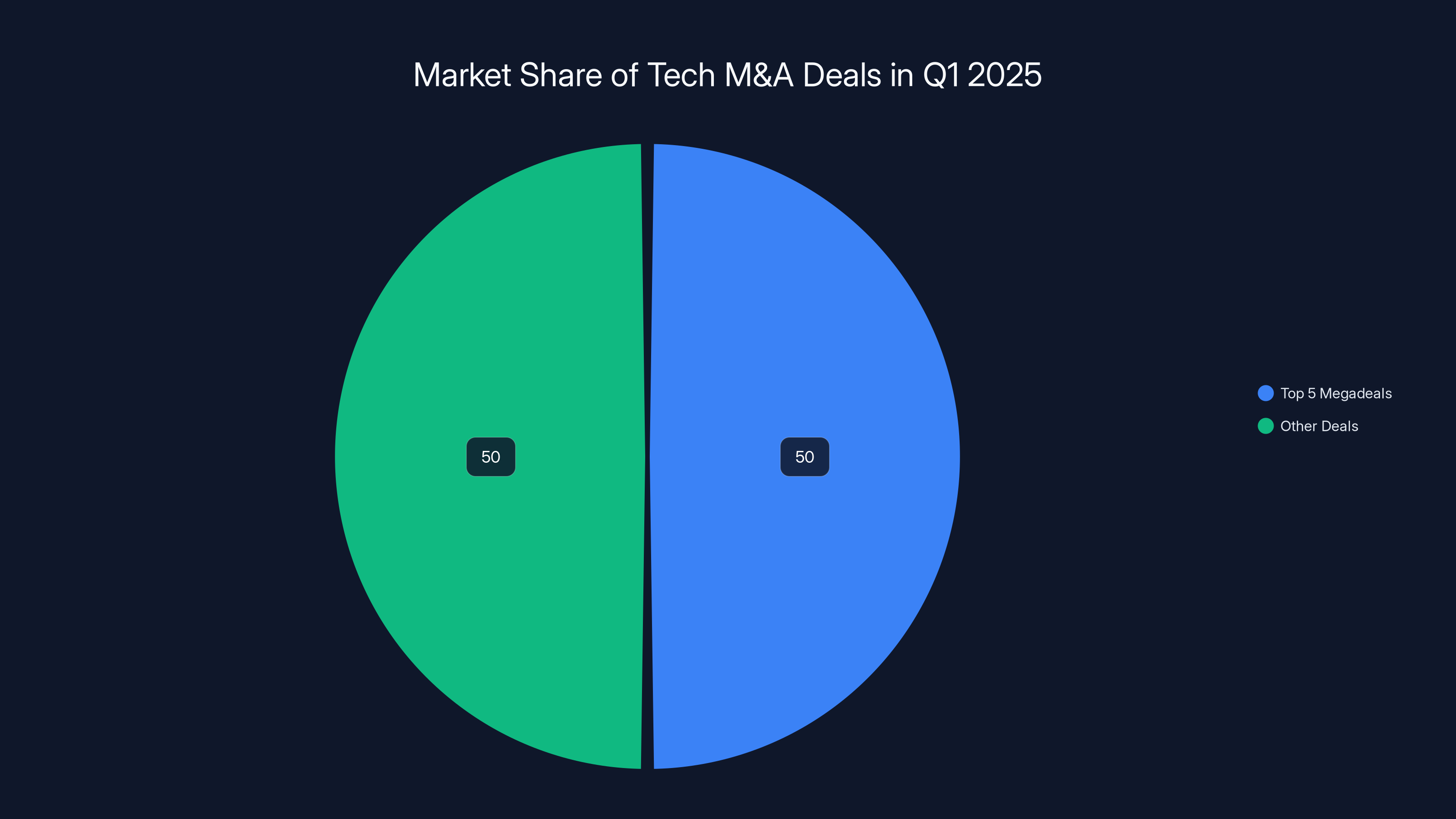

Total tech M&A: $587 billion. That sounds insane. And it is. But it's also incredibly concentrated.

The megadeals. In Q1 2025 alone, five deals accounted for nearly 50% of total transaction value. Five. Wiz, Scale AI, Armis, and a couple others pulled in hundreds of billions of capital. Those deals are real. They're happening. They're just not happening for you unless you're building something with AI acceleration or are already at $1B+ valuation.

The middle. Strip away the five megadeals, and deal sizes actually dropped 17%. The average M&A transaction got smaller even though the total pie got bigger. That's the bifurcation. Everything is either mega or meh.

The number of PE deals. PE firms did more deals in 2025 than in previous years. But the total capital deployed actually went to fewer companies, which means the average deal size went down across the board except at the very top.

So PE is busier, but busier on different stuff. They're doing smaller follow-on deals in their existing portfolios. Optimizing existing investments. But new company acquisitions? Those went from being a steady flow of mid-market deals to being concentrated on either consolidation plays or category-defining companies.

For most founders, this means the phone stops ringing around Q2 of any given year if PE is interested. If they're not interested by summer, they're not interested at all. You can spend a year chasing conversations that went nowhere.

Plain Vanilla SaaS Is Now Invisible to PE

Let me define what I mean by "plain vanilla SaaS" because this is important.

Plain vanilla SaaS is:

- B2B, usually mid-market

- Stable business model (SaaS revenue, mostly annual contracts)

- Good retention (80%+ net dollar retention)

- Decent margins (40%+ gross margin)

- 20-30% growth

- Mature sales org

- No AI angle

- Not in a hot sector

This used to be the PE sweet spot. This was what they were built to buy and improve. Add a CFO. Optimize the sales org. Maybe build international. Improve margins. Compound for 5-7 years, then exit.

Now? PE looks at that same company and sees dead weight.

Why? Because it doesn't pencil anymore. The debt math doesn't work. The growth is boring. There's no AI acceleration to show future investors. There's no category tailwind to justify a higher exit multiple.

A company that was worth 6-7x ARR in 2022 might be worth 4-5x in 2025, but PE isn't paying even that because they can't model how they get out.

What makes PE interested in something nowadays:

Genuine AI acceleration. Not "we have an AI feature in our product." Real, measurable acceleration. If you can show that AI is making your growth rate increase, and you have a coherent story about why that's sustainable, PE gets interested. But it has to be real. They'll dig into your metrics hard.

Category tailwind. If you're in security, or infrastructure, or DevOps, or anything that benefits from AI workloads, PE considers that. The category itself is growing. That creates multiple expansion optionality.

Scale and consolidation opportunity. If you're already at $50M+ ARR, PE can model tuck-in synergies. The acquisition thesis becomes about consolidation, not about growth. That changes what they're willing to pay.

Defensible tech moat. If you have something competitors can't easily copy—either proprietary data, a specific technical breakthrough, or irreplaceable engineering talent—PE can justify a higher price because the risk profile is lower.

Most plain vanilla SaaS companies don't have any of these. So PE passes. And they pass quietly, with polite emails and vague language. The result is founders spend a year waiting for conversations that never materialize.

PE interest in SaaS companies is now driven by factors like AI acceleration and category tailwinds, rather than traditional stable models. Estimated data based on industry trends.

The Debt Markets Are Actually Stressed Right Now

There's another factor that's not getting as much attention but matters enormously: the debt markets are under stress.

PE deals require debt. Lots of it. Even with equity from the fund, a typical deal might be 60% debt financed. If the debt markets seize up, PE can't deploy capital, and deals don't happen.

Right now, the tech credit market is showing stress signals. In early 2025, 14.5% of tech loans were distressed—the highest since the 2022 bear market. Tech bond distressed ratios hit 9.5%, the highest since Q4 2023. These are leading indicators that the debt markets are tightening.

When debt markets stress, PE has to pay more for capital. That raises their cost of capital even further. A already-unattractive deal becomes toxic.

This creates a cascading effect:

- Debt markets stress

- Cost of capital rises for PE

- Multiples have to fall to justify the cost of debt

- Deal flow slows because the math doesn't work

- Founders get fewer PE offers

We might be entering that phase right now. It's not visible in the headline M&A numbers because the megadeals are still happening (those firms have access to capital). But mid-market deal flow could be grinding to a halt.

If you're relying on a PE exit in the next 18 months, you should be worried. The debt markets are not cooperating.

What Changed in SaaS Founder Strategy and Thinking

The death of the PE exit path is forcing a fundamental rethink of how founders approach building.

For the last decade, the implicit strategy was: optimize for acquisition metrics, not profitability. Get to $20M ARR with good retention, and PE will take the company off your hands at a solid valuation. That freed up founders to invest aggressively in growth, hiring, and product. The exit was somewhat guaranteed.

Now that's not true. And founders are starting to realize this.

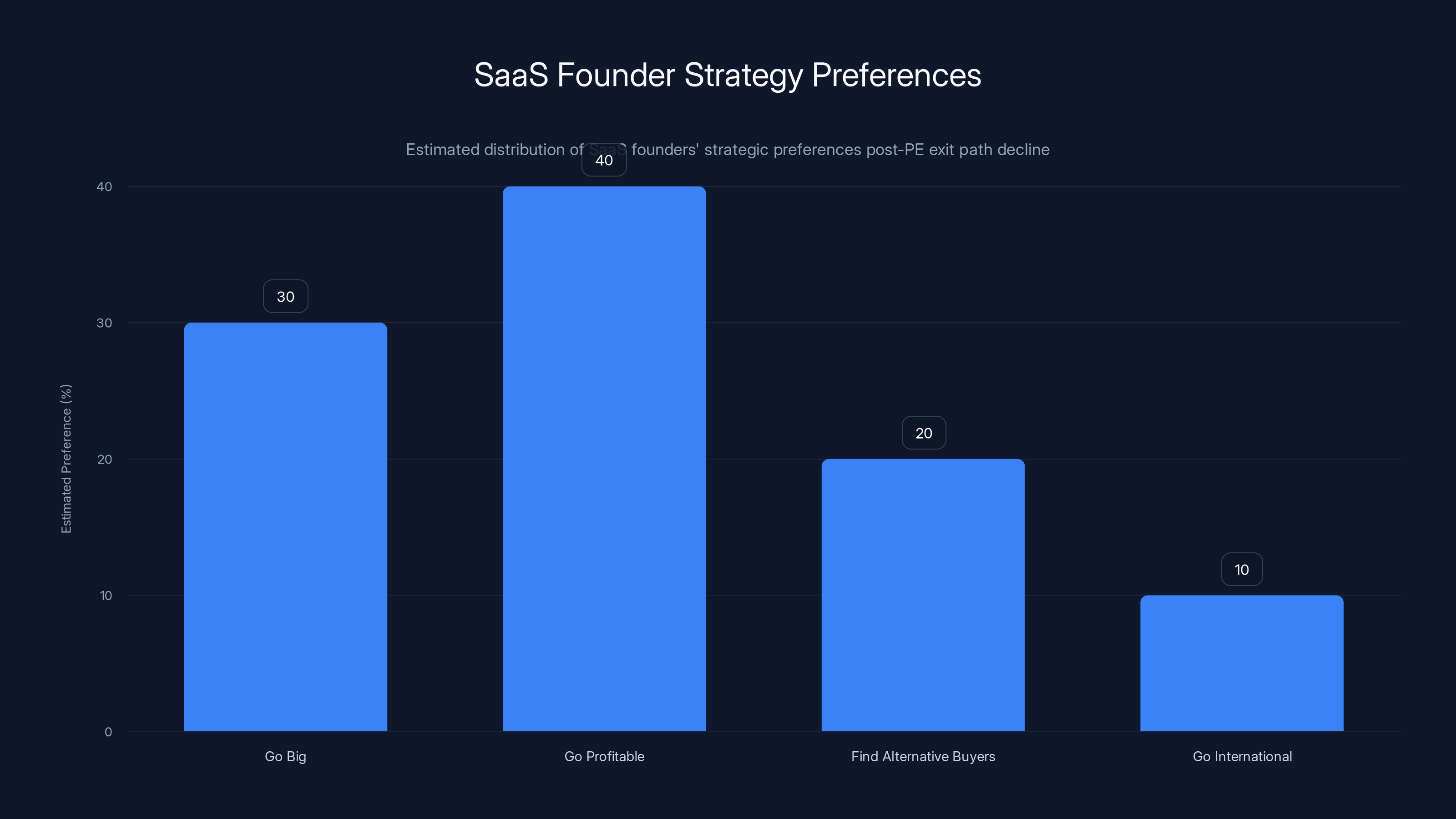

The new thinking is:

Option 1: Go big. If you want PE interest, you need to be in an AI-accelerated or high-growth category. That means aggressively pursuing that narrative. Repositioning your product to have an AI angle. Accelerating growth even if margins suffer. Building the story PE wants to tell.

This works if you can actually execute it. But it's a bet. You're spending aggressively to hit 50%+ growth, hoping that puts you in an acquisition conversation. It might not. You might spend $5M trying to accelerate growth and end up just being a slower-growing company with worse margins.

Option 2: Go profitable. If you're not going to get a PE exit, maximize cash flow. Optimize for profitability, not growth. Harvest the business. Use the cash to fund R&D, expansions, or product lines that might create new growth vectors.

This is less glamorous, but it's safer. Your company generates cash. You can invest in new initiatives. You can compound for decades if you want to.

Option 3: Find alternative buyers. Strategic acquirers, smaller PE firms, founder-led buyouts, private equity groups that specialize in lower growth rates. They exist. They're just not Thoma Bravo or Vista. They have different return requirements and different acquisition theses. A strategic buyer might acquire you at 5x because they can integrate your product into their platform and cross-sell. That math works even for plain vanilla SaaS.

Option 4: Go international or adjacent. If your home market is tapped out, expand internationally. If your product is mature, build adjacent products. Expand your addressable market. This doesn't guarantee a PE exit, but it increases your odds of being interesting to someone.

Most founders are realizing some combination of these is necessary. The one-path-to-success mentality is dead. You need multiple exits, multiple growth vectors, multiple strategic options.

The Strategic Acquirer Path: Who's Actually Buying Now

If PE is out, where is M&A actually happening?

Strategic acquirers. These are existing large software companies, tech giants, or private equity firms with different return models than the mega PE shops.

Large software companies. Salesforce, Adobe, ServiceNow, Workday—they're still doing M&A. But they're strategic about it. They buy companies that 1) fill a gap in their portfolio, 2) give them access to customers they want, or 3) provide technology they need.

Plain vanilla SaaS doesn't fit well here. Salesforce already has CRM. They're not buying another CRM competitor. But if you've built something that integrates into their ecosystem, or solves a problem adjacent to their core product, they might acquire you.

The valuations here are variable. Sometimes they're lower than PE would've paid (3-4x revenue). Sometimes higher (8-10x if they really want you). It depends entirely on strategic value.

Tech giants. Google, Microsoft, Amazon—they're acquiring capabilities, talent, and technology. They pay what they want because they have infinite capital. But they're very selective. You need something genuinely valuable to them.

Smaller PE firms. The mega PE shops have checked out of the mid-market. But smaller PE firms with different return thresholds are still active. They're okay with 20% growth companies if the margins are good and the exit opportunity is clear. These are the buyers that might actually care about your business if you're plain vanilla SaaS.

Financial buyers. Recapitalizations, management buyouts, founder buyouts funded by smaller investment groups. There's capital out there for solid businesses that generate cash. It's just not the mega PE names everyone knows.

For plain vanilla SaaS, the strategic buyer path is probably the most likely. But it requires thinking about your business from a buyer's perspective. What gap do you fill? What customers do you have access to? What technology did you build that someone else needs?

Estimated data suggests a shift towards profitability, with 40% of SaaS founders favoring this strategy over aggressive growth or alternative buyer searches.

The Real Culprit: Growth Expectations Have Permanently Shifted

Here's what I think is the deepest issue, and what's going to persist even if rates fall and debt markets loosen:

Growth expectations have permanently shifted upward.

PE used to be excited about 20-30% growth. That was above market, sustainable, and created good cash flow. Now PE has seen companies doing 80-100%+ growth. That changed their mental model.

Even if AI doesn't deliver on its promises at scale, the expectations are already baked in. PE is going to keep hunting for the next 100% growth company because they've seen it's theoretically possible.

This means the middle market—companies growing 20-40%—are permanently out of favor. Unless you can tell a story about AI acceleration or category tailwind, PE is just not interested.

This is important because it's not fixable by just cutting rates. Even if debt costs fall back to 2%, PE's growth expectations are not going back to 20%. They've seen the upside. They want it.

For founders, this means the safe harbor of "just build a solid 20-30% growth company and PE will eventually buy you" is permanently gone. You either need to 1) accelerate growth somehow, 2) find alternative buyers, or 3) give up on external exits and optimize for cash flow.

What Happens to the Portfolio: How Existing PE Investments Are Being Managed

PE firms aren't gone. They're just in optimization mode.

They've got billions locked up in existing portfolio companies. Those companies need exits. PE is focused on improving those, not necessarily buying a ton of new companies.

This manifests as:

Tuck-in acquisitions. PE firms are buying smaller companies to roll into existing portfolio companies. This creates scale, diversifies customer bases, or adds product lines. A $100M ARR software company getting acquired and merged into a portfolio company is a tuck-in. This is still happening, and it's actually one of the only things PE is actively deploying new capital on.

Add-on acquisitions. Smaller, adjacent acquisitions that expand a company's capabilities or geographic reach. These are happening because they improve the exit multiple of the portfolio company. Better metrics = higher multiple = better return.

International expansion. Many PE portfolio companies are being expanded internationally. Not through acquisition, but through organic investment. This is a growth vector that doesn't require finding new deal flow.

Operational improvements. Hiring better CFOs, sales leaders, product folks. Improving margins, reducing churn, increasing efficiency. This is invisible to the market but it's a huge focus right now.

From a founder perspective, this means PE isn't hibernating. They're just busy with their existing investments. New company acquisitions are lower priority.

If your company isn't already in a PE portfolio, your odds of getting acquired by PE just got much harder.

The AI Angle: Why It Matters and Why It's Also Dangerous

AI is the one thing that gets PE interested right now. But there's a dangerous game being played.

If you can show real, measurable AI acceleration in your product or growth curve, PE gets excited. They can model higher returns. They can see a path to a bigger exit. The multiple math works because the growth story works.

But "real, measurable" is the key. PE is starting to get sophisticated about spotting AI theater. They're looking at:

- Actual usage data, not hype

- Measurable improvement in key metrics (churn, expansion, NRR)

- Coherent narrative about why AI creates durable competitive advantage

- Technical feasibility of scaling what you've built

If you just slapped an "AI-powered" label on your product and didn't actually change the underlying metrics, PE will figure it out. And when they do, you're worse off than if you'd just been honest about being plain vanilla SaaS.

The temptation right now is enormous: rebrand your company, add some AI features, tell a better story, hope PE bites. The risk is that you waste a year and a half on this play, realize it's not working, and now you've lost time and credibility.

My advice: If you're going to go all-in on AI, actually go all-in. Build real capabilities. Measure the impact. Show the numbers. Don't just talk about it.

If you can't actually deliver AI-driven acceleration, don't try to fake it for PE. It won't work, and when they find out (and they will), you'll have poisoned that relationship.

In Q1 2025, the top 5 megadeals accounted for 50% of the total $587 billion tech M&A value, highlighting extreme concentration at the top.

The Exit Funnel and What Founders Are Actually Doing Now

Let me trace what's actually happening with founders who were expecting PE exits:

Stage 1: The realization. Around mid-2025, founders started realizing PE interest was drying up. The phone stopped ringing. Conversations went nowhere. It became clear that the old playbook wasn't working anymore.

Stage 2: The pivot. Founders started looking at alternatives. Accelerate growth and chase AI narrative. Or optimize for profitability and cash flow. Or hunt for strategic buyers instead. Or explore founder-led buyouts or smaller PE firms.

Stage 3: The decision. Most of these decisions haven't been made yet. We're still in the middle market grappling with this reality. But the founders who've made decisions are picking one of three paths:

- Go big: Aggressively pursuing growth and AI acceleration, betting they can become interesting to PE again by having a better story

- Go deep: Optimizing for cash flow, profitable growth, and long-term sustainability. Accepting that the company might not get a big exit, but it can generate amazing cash

- Go different: Hunting for strategic buyers, smaller acquirers, or alternative capital structures

The distribution is probably 20% go big, 40% go deep, 40% still undecided.

Stage 4: Long-term outcomes. I think we'll see some interesting patterns emerge:

Companies that go big and successfully accelerate will attract PE or strategic buyers. Those exits will happen, and they'll be at decent multiples (5-7x).

Companies that go deep and optimize for cash will compound for decades. Some will eventually become acquisition targets (PE or strategic), some will stay independent, some will become acquirers themselves. These are stable, valuable businesses even if they never exit.

Companies that go different and find the right strategic buyer might actually get better outcomes than they would have with PE. A strategic buyer who can integrate your product and cross-sell might pay more than a PE firm would.

The graveyard will be companies that tried to fake an AI story, spent a ton of capital, and ended up in the middle of the road. Not big enough to be interesting, not profitable enough to be safe, no clear exit path.

What Founders Should Actually Do Right Now

If you're running a solid mid-market SaaS company and expecting a PE exit, here's what you need to do:

First, be honest about your story. Do you actually have AI acceleration, or are you using AI as a marketing angle? Can you show real, measurable metrics improvements? If yes, lean into it. If no, don't bother. PE will call you out.

Second, do the math yourself. Figure out what your company is actually worth to a buyer. Don't rely on what PE would have paid in 2022. Work backward from what strategic buyers are paying in your category. That's your realistic exit range.

Third, calculate your break-even economics. If you can't get a PE exit, can you stay independent? What does profitability look like? Can you fund growth organically? If yes, that's a real option. If no, you need an exit.

Fourth, map out strategic buyers. Who else in your space might want to acquire you? What gaps would you fill in their portfolio? Which ones have M&A appetite? Start conversations now, not when you're desperate.

Fifth, know your alternatives. Recaps, founder buyouts, secondary sales, smaller PE firms. There's capital out there. It's just not the mega PE shops. Know what's available to you.

Sixth, focus on unit economics. Whatever path you pick, solid unit economics make you attractive. CAC payback, LTV, gross margin, NDR—these are universally valued. Build these metrics ruthlessly.

Seventh, don't waste time on conversations that aren't real. If PE isn't calling, they're not interested. Don't spend a year chasing conversations that went nowhere. Pivot to your actual plan.

The Structural Shifts That Won't Reverse

Even if debt rates fall, even if M&A sentiment improves, three things are probably not going back to the way they were:

First, growth expectations have permanently reset. PE has seen 80-100% growth is possible. They're not going back to being excited about 20% growth companies. Even if you're a cash-flowing, profitable 20% grower, you're not interesting to mega PE shops anymore.

Second, exits are getting tougher. IPOs for boring software are effectively closed. Strategic buyers are selective. The exit funnel got narrower and it's not widening. This means PE has to be more careful about the companies they buy because they're less certain they can exit at the multiples they need.

Third, PE focus has shifted to optimization. They've got billions locked up in portfolio companies. The focus is on improving those, not necessarily deploying new capital. This is a structural shift that doesn't reverse quickly.

These factors are sticky. They're not interest-rate dependent or cycle dependent. They're structural. Plan accordingly.

The cost of capital for PE firms has more than doubled from 2020 to 2023, while growth expectations have shifted from 25% to 100% due to AI influences. Estimated data.

The Winners in This New Environment

Who actually wins in a PE pullback?

AI companies with real acceleration. If you can actually show that AI is driving growth and customers love it, you're going to attract attention. PE will pay up. Strategics will hunt you. You've got options.

Consolidators. Companies that can acquire competitors or adjacent players and roll them up. These become acquisition targets for PE firms doing portfolio consolidation. If you've built a platform that can integrate other companies, you're valuable.

Cash-generating machines. If you've optimized for profitability and cash generation, you're now valuable to smaller PE firms, financial buyers, and founder-led acquirers. These buyers exist. They're just quieter than mega PE shops.

Mission-critical infrastructure. If you're so embedded in your customers' operations that they can't afford to not use you, you're valuable. High switching costs = durable retention = attractive to any buyer.

Niche leaders. If you're the dominant player in a narrow vertical, that's valuable. Strategics will acquire narrow leaders because it gives them expertise and customer relationships in that vertical.

If your company doesn't fit one of these categories, you're in the middle of the road. Not exciting enough for mega PE, not clear enough to strategics, not profitable enough to be a standalone cash business.

That's the danger zone. Know whether you're in it.

How to Evaluate Offers and Conversations

If you do get acquisition interest—from PE, strategics, or anyone else—here's how to evaluate it:

Don't anchor on what you thought your company was worth. If you were expecting 6-7x ARR and someone offers 5x, that's not a lowball. That might be market rate now.

Look at multiple and terms. A 5x deal with good earnouts and minimal clawbacks might be better than a 6x deal with 50% held back and lots of risk.

Understand the buyer's thesis. Why do they want your company? If the answer is "consolidation" or "cross-sell," that's meaningful. If the answer is vague, be skeptical.

Assess execution risk. Integration risk is huge. Can they actually execute on what they're promising? Have they successfully integrated companies like yours before? If not, the acquisition upside is just hope.

Calculate your optionality. What happens if you turn down this offer? Can you stay independent? Can you attract more interest if you improve metrics? Is this truly your best option, or are you negotiating from desperation?

Don't get attached to a narrative. Just because someone tells you they're going to take your company public doesn't mean they will. Judge them on what they've actually done with previous acquisitions.

Building Your Company for a Post-PE World

If you're just starting out, how do you build a company that has optionality in a post-PE world?

Build real defensibility. Not growth, not hype. Real competitive advantage. This makes you valuable to any buyer—PE or strategic—and also gives you optionality to stay independent.

Focus on unit economics from day one. Customers who pay, stick around, and expand are always valuable. Every buyer cares about this. Build this ruthlessly.

Pick a category with tailwinds. If you're in security, or infrastructure, or DevOps, or anything riding AI, you're starting with more optionality. If you're in a flat category, your optionality is lower.

Build for strategic buyers, not just PE. Think about who might want to acquire you as a platform. Who's got customer relationships that value you? Who's got distribution you could plug into? Design your product with those integrations in mind.

Stay profitable, or get to profitability. Profitability is freedom. It means you can fund growth yourself, stay independent if you want to, and negotiate from strength.

Don't optimize for one path. Build your company such that multiple outcomes are possible. PE, strategic, stand-alone, rollup platform. Each of these should be realistic for you.

This is harder than the old playbook. You can't just optimize for metrics that look good to PE. You have to optimize for actual business fundamentals. But it's also more resilient. You've got more optionality.

The Likely Outcomes for Different Founder Profiles

Let me paint pictures of how this plays out for different founder archetypes:

The growth hacker. You built a 30% growth SaaS company with okay margins. You were expecting PE. Most likely outcome: PE doesn't bite unless you can accelerate growth or find a strategic buyer. You either 1) pivot aggressively to chase AI angle and accept the risk of failure, or 2) optimize for cash and plan to stay independent, or 3) hunt for smaller acquirers or strategics. Most likely: option 3.

The profitability play. You built a profitable, slow-growth (15%) SaaS company. Nobody expected this to get a mega PE exit, but you were hoping for a strategic buyout. Most likely outcome: You get interest from smaller PE firms, financial buyers, and maybe strategics if there's strategic value. Multiples are lower (3-5x) but the deal happens. You're probably fine.

The AI accelerator. You built a company and genuinely integrated AI in a way that's moving the growth needle. Most likely outcome: You get real PE interest, strategics are hunting you, you've got multiple options. Multiples are strong (6-8x+). You're probably fine.

The niche leader. You dominated a narrow vertical. Most likely outcome: Strategics who want that vertical will acquire you. Multiple is dependent on strategic value, but you've got a clear buyer. Probably fine.

The plain vanilla builder. You built a solid, boring 20% growth SaaS company. Nice retention, okay margins. Most likely outcome: PE passes. Strategic buyers only if there's some strategic angle. Your real optionality is probably staying independent and compounding, or finding a smaller acquirer who's okay with your metrics. Harder situation.

The key insight: Where you end up depends on how defensible your business is, not just on growth rate. Growth matters, but defensibility matters more now.

FAQ

Why did private equity stop buying mid-market SaaS companies?

Three forces converged: First, higher interest rates (5%+) made the debt math unworkable for companies growing only 20-30%. Second, PE saw companies growing 80-100%+ with AI, so their growth expectations permanently reset upward. Third, exit paths got narrower (IPOs closed, strategics selective), making it harder for PE to model returns. Plain vanilla SaaS stopped penciling at any multiple PE was willing to pay.

What's the difference between a strategic buyer and private equity?

Private equity firms buy companies primarily for financial returns, planning to improve them and resell them at a higher multiple. Strategic buyers are existing companies (like Salesforce or Microsoft) who buy other companies to fill product gaps, access customer relationships, or acquire technology. Strategics often value things differently than PE does, and sometimes they'll pay more for integration potential.

Is it possible to get a PE acquisition if I'm not growing fast enough?

Unless you have a clear AI angle or are in a hot sector with tailwinds, getting mega PE interest is extremely difficult now. Smaller PE firms or financial buyers might still be interested if you have great margins, solid retention, and good unit economics. But you should probably plan for alternatives like strategics, recaps, or staying independent. Don't spend a year chasing a PE exit that isn't coming.

What should I do if I can't get acquired?

You have several options: First, optimize for profitability and cash generation—stay independent and compound long-term. Second, pursue strategic buyers in your ecosystem—they often value you differently than PE does. Third, explore recapitalizations, founder buyouts, or smaller investment groups. Fourth, aggressively chase growth and AI acceleration to attract better buyers. Pick one and commit to it; don't half-execute multiple strategies.

Will PE come back to the mid-market when interest rates fall?

Not quickly, and maybe not at all in the way it did before. Even if rates drop, PE's growth expectations have permanently reset. They've seen 100% growth is possible, so they're not going back to being excited about 20% growers. The structural shift (higher growth expectations, narrower exits, portfolio optimization focus) is more important than rates. Plan for PE to stay focused on high-growth, AI-accelerated, or consolidation plays.

How do I know if my company is attractive to strategics?

Ask yourself: What gap does my product fill in a larger company's portfolio? What customers or distribution do I give them access to? What technology did I build that they can't easily build themselves? What reduces their risk or increases their revenue? If you can answer these questions clearly, you're strategically interesting. If you're just a smaller version of what they already have, you're not.

Should I try to accelerate growth just to attract buyers?

It depends on whether you can actually sustain the acceleration. Burning cash to hit 50% growth for a year, then dropping back to 25% looks bad to buyers and burns capital. If you can genuinely build an AI-driven feature that moves the growth needle sustainably, do it. If you're just doing aggressive marketing to look better, don't bother. Buyers will find out and it kills your credibility.

What's the realistic valuation I should expect for my company?

Work backward from what strategics are paying in your category, not from what PE would have paid in 2022. Look at actual recent acquisitions of similar companies. Factor in your defensibility (moat, retention, unit economics), not just your growth rate. And be honest about whether you actually have something a buyer wants, or if you're just a smaller version of what they already have. That's your realistic range.

The Final Reality Check

Here's the hard truth: If you built a plain vanilla SaaS company expecting a PE exit, you've got a problem. The exit path you planned for is closing.

But this isn't entirely bad. It's a reset. The companies that win in this environment are the ones that are actually defensible, not the ones that just have good metrics. It's the ones that generate cash, not the ones that just grow fast. It's the ones that matter to customers, not the ones that are just another tool in a crowded category.

For some founders, this will be painful. You were counting on that exit to make all the work worth it. You're not getting it at the multiple you expected.

For others, this is actually liberating. You can stop optimizing for PE metrics and start optimizing for what actually makes a great company. You can focus on profitability, customer success, defensibility. You can stay independent. You can actually enjoy the business you've built instead of constantly chasing the exit.

The game changed. The old playbook is dead. But the game isn't over. You've just got to play it differently now.

Figure out your path. Commit to it. Build accordingly. And don't waste a year chasing conversations that aren't real.

That's the only way forward.

Key Takeaways

- PE firms have effectively checked out of plain vanilla SaaS: $587B in 2025 M&A was concentrated in megadeals while mid-market deal sizes dropped 17%

- Three structural forces killed the old PE playbook: higher rates (5%+) destroyed leverage math, growth expectations permanently reset upward (PE now hunts 100%+ growers), and exit paths narrowed (only 6 software IPOs in 2025)

- Mega PE firms now only buy companies with AI acceleration, hot sector tailwinds, or $50M+ ARR consolidation opportunities—plain vanilla SaaS is invisible

- Founders have three viable paths: go big (aggressively accelerate growth/AI angle), go profitable (optimize cash flow for long-term independence), or go different (hunt strategic buyers or smaller acquirers)

- The safety net is gone permanently: even if rates fall, PE's growth expectations won't return to 20% as baseline—the structural shift is permanent