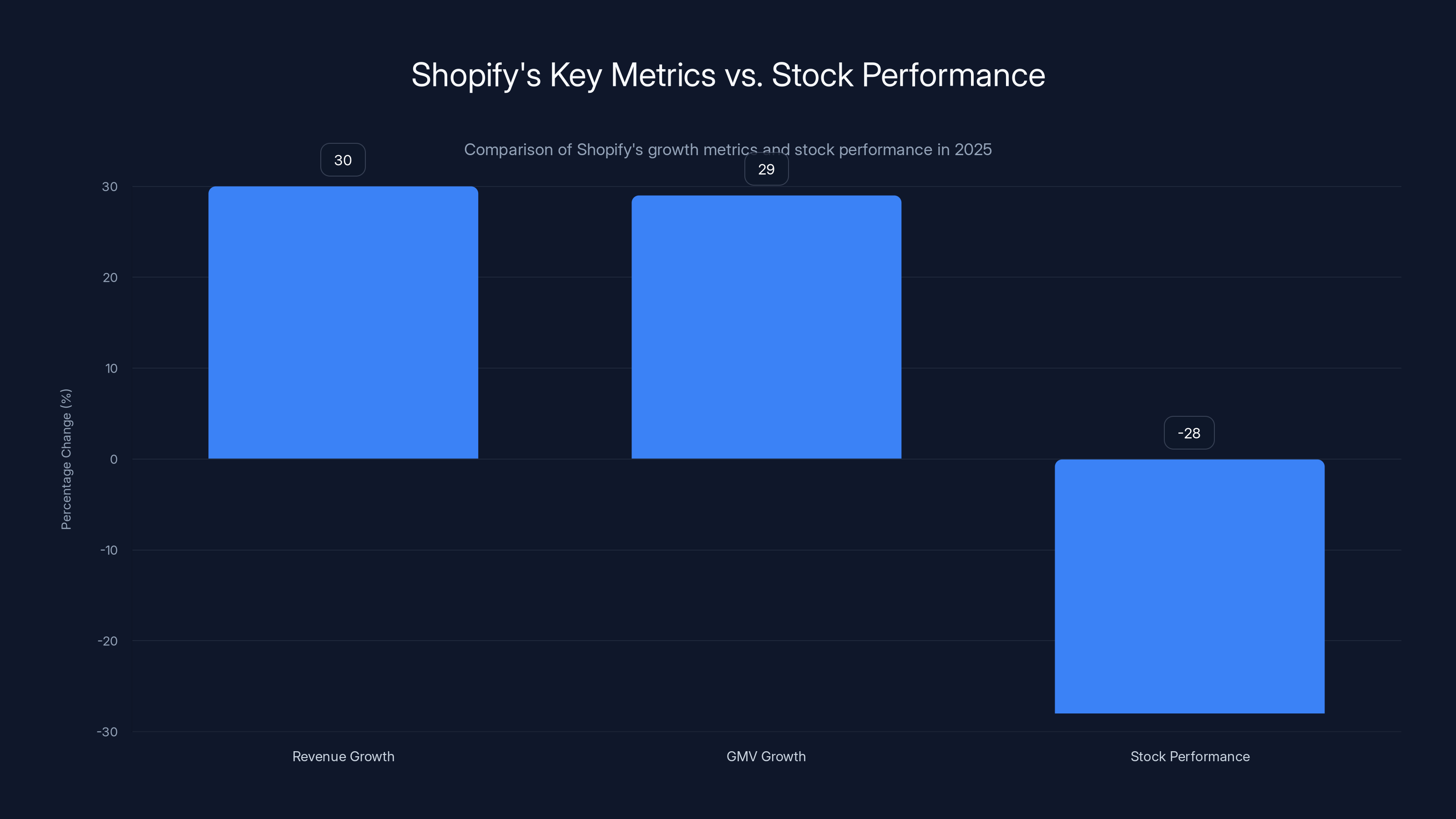

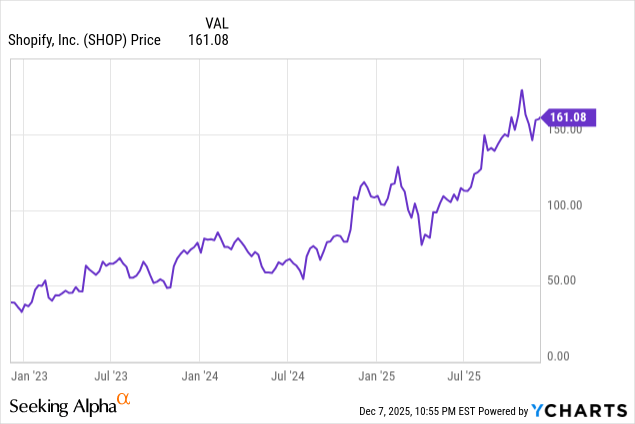

![Shopify's 30% Growth, $378B GMV, Yet Stock Down 28%: The Disconnect Explained [2025]](https://tryrunable.com/blog/shopify-s-30-growth-378b-gmv-yet-stock-down-28-the-disconnec/image-1-1771429160072.jpg)

Shopify's 30% Growth, $378B GMV, Yet Stock Down 28%: The Disconnect Explained

Picture this. A company posts 30% revenue growth at nearly

Welcome to Shopify in 2025. Welcome to a case study in the widest disconnect between what a business is actually doing and what the market values it at.

For SaaS founders, this moment matters more than you think. Shopify's situation reveals something fundamental about public markets right now: growth alone isn't enough. Valuation multiples, forward guidance, and the question of whether a company can ever grow into its stock price dominate the narrative more than actual operational excellence.

But here's what the numbers actually tell you. Shopify isn't struggling. The underlying business is one of the strongest in all of B2B and commerce. The company commands over 14% of US ecommerce. Its payments business has become a second growth engine. Its B2B expansion is accelerating despite the broader commerce slowdown. And its free cash flow generation proves it's not sacrificing profitability for growth theater.

So what's really happening? And what should founders take away from this?

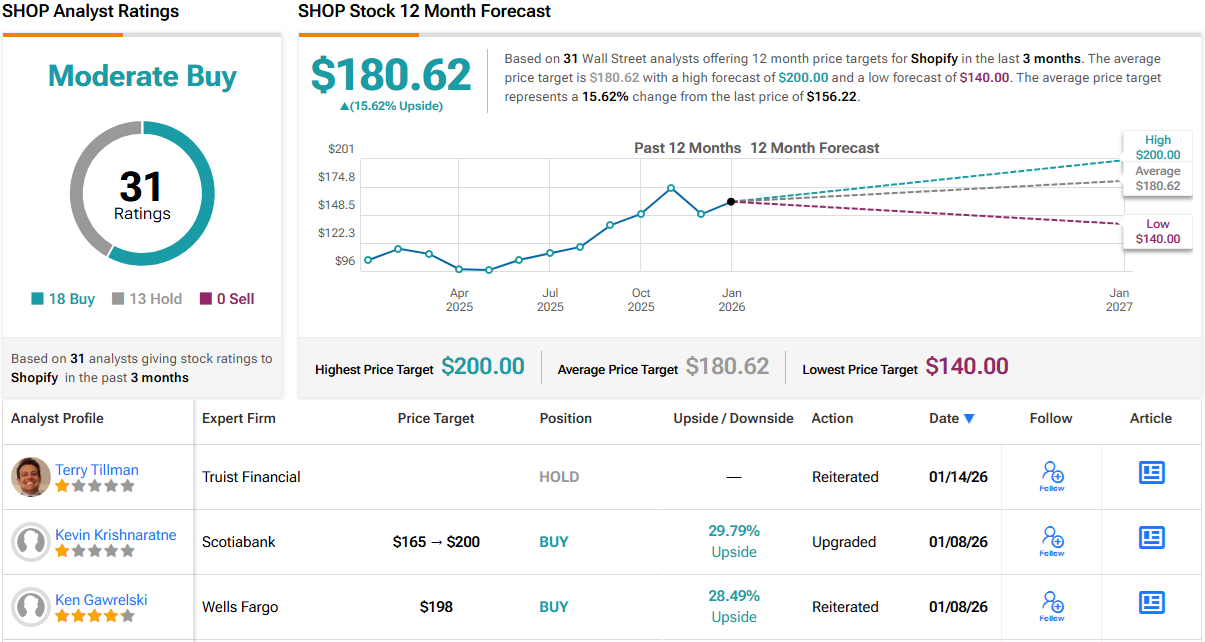

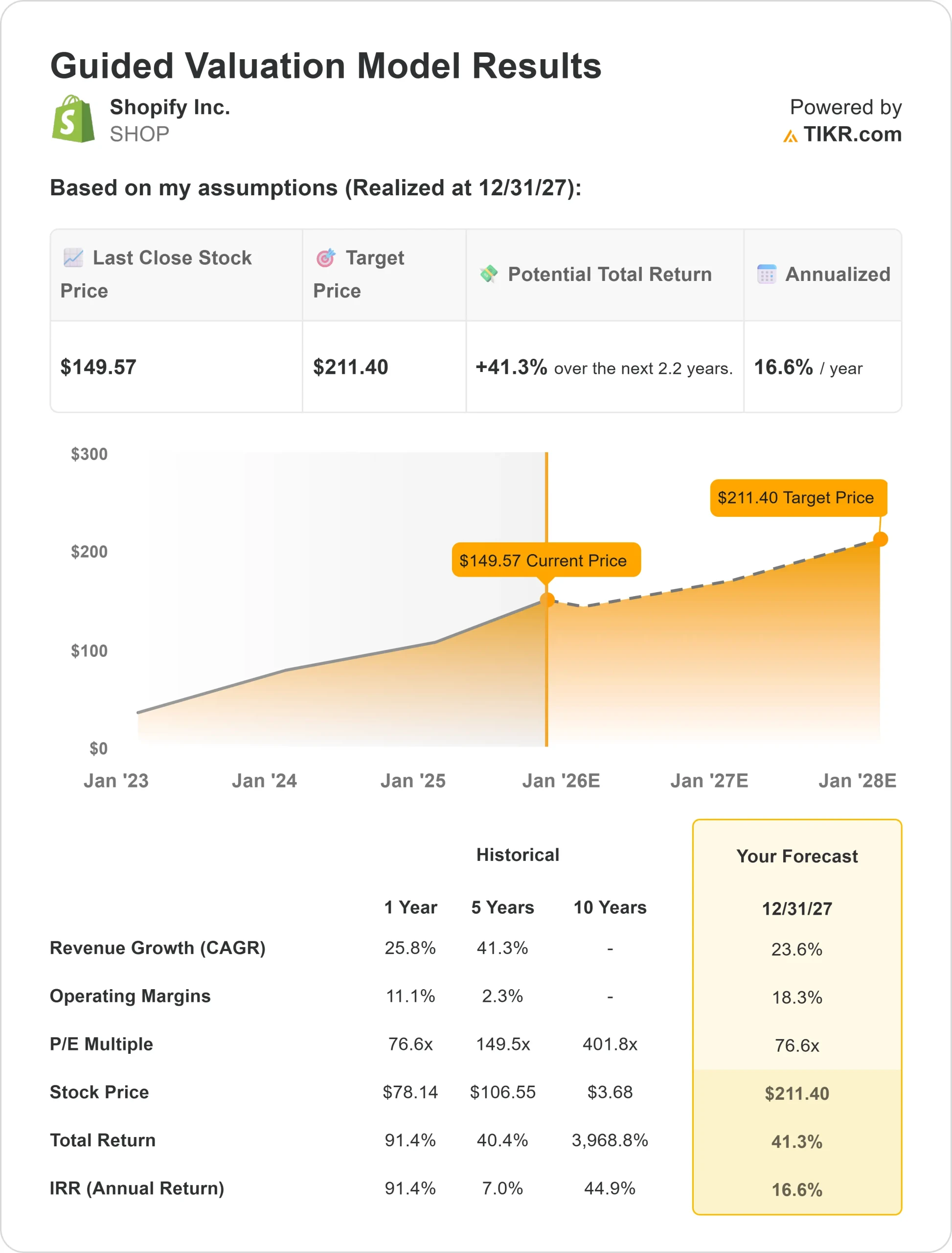

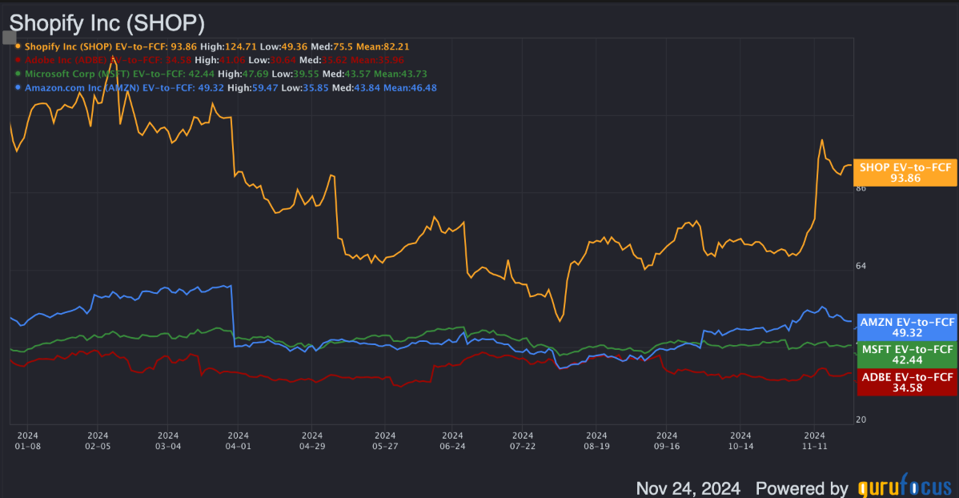

The honest answer involves a conversation about expectations, valuations, and the reality that even great businesses sometimes trade at prices that seem disconnected from their fundamentals. Shopify still trades at roughly 100x earnings and 73x forward earnings. At those multiples, even 30% growth isn't always enough to satisfy market appetite. The stock needs the company to either grow even faster or deliver multiple expansion that seems unlikely in this environment.

But the disconnect also tells another story. It tells you that the market is price-sensitive to expectations in ways many founders don't fully appreciate until they're public. It shows you that consistency, guidance accuracy, and meeting or beating forecasts matter as much as the absolute growth rate. And it demonstrates that once you hit a certain scale, the market starts pricing in perfection.

Let's pull apart the numbers that actually matter for founders building in this space, and what they reveal about how to think about growth, valuation, and the long game in SaaS.

TL; DR

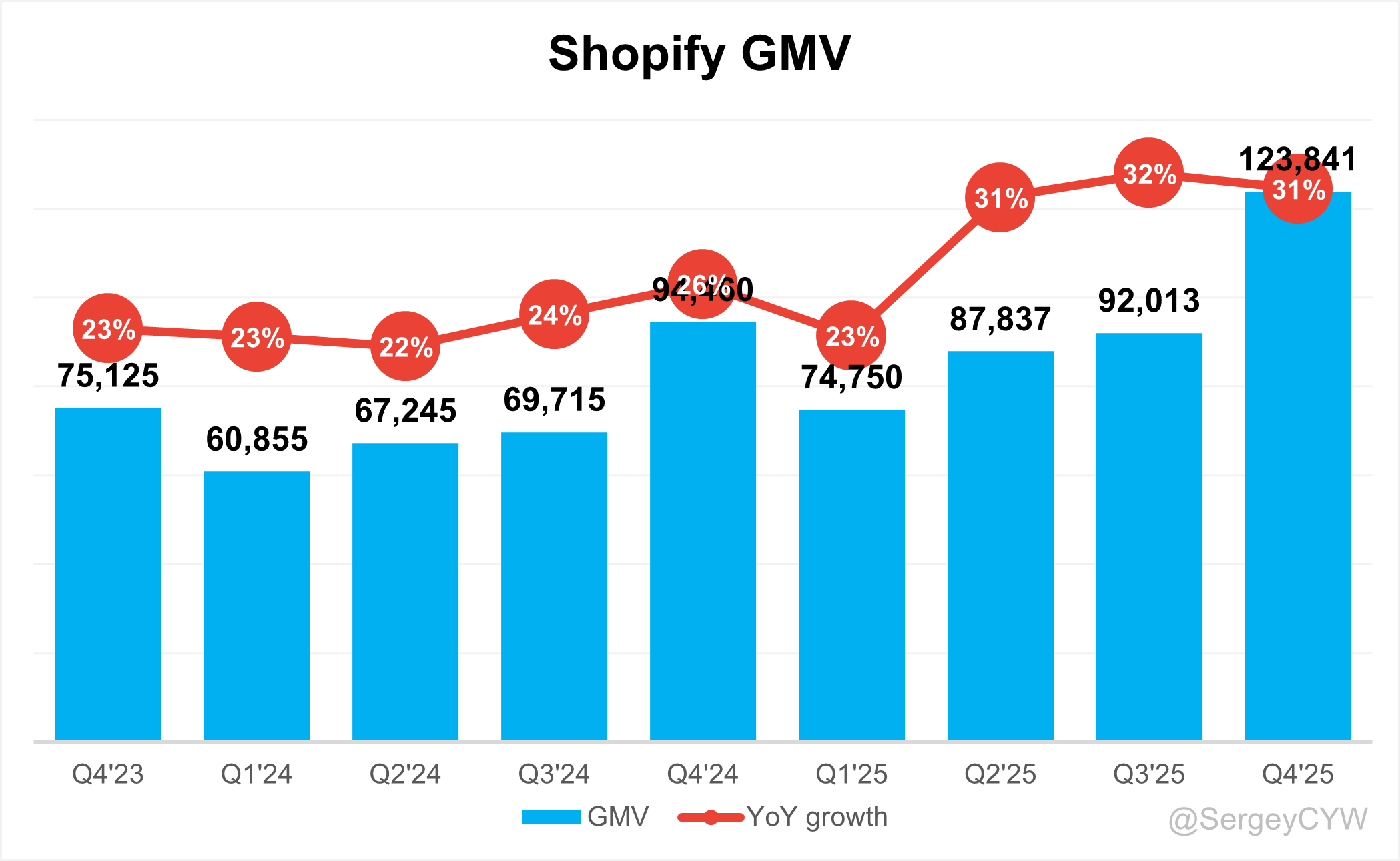

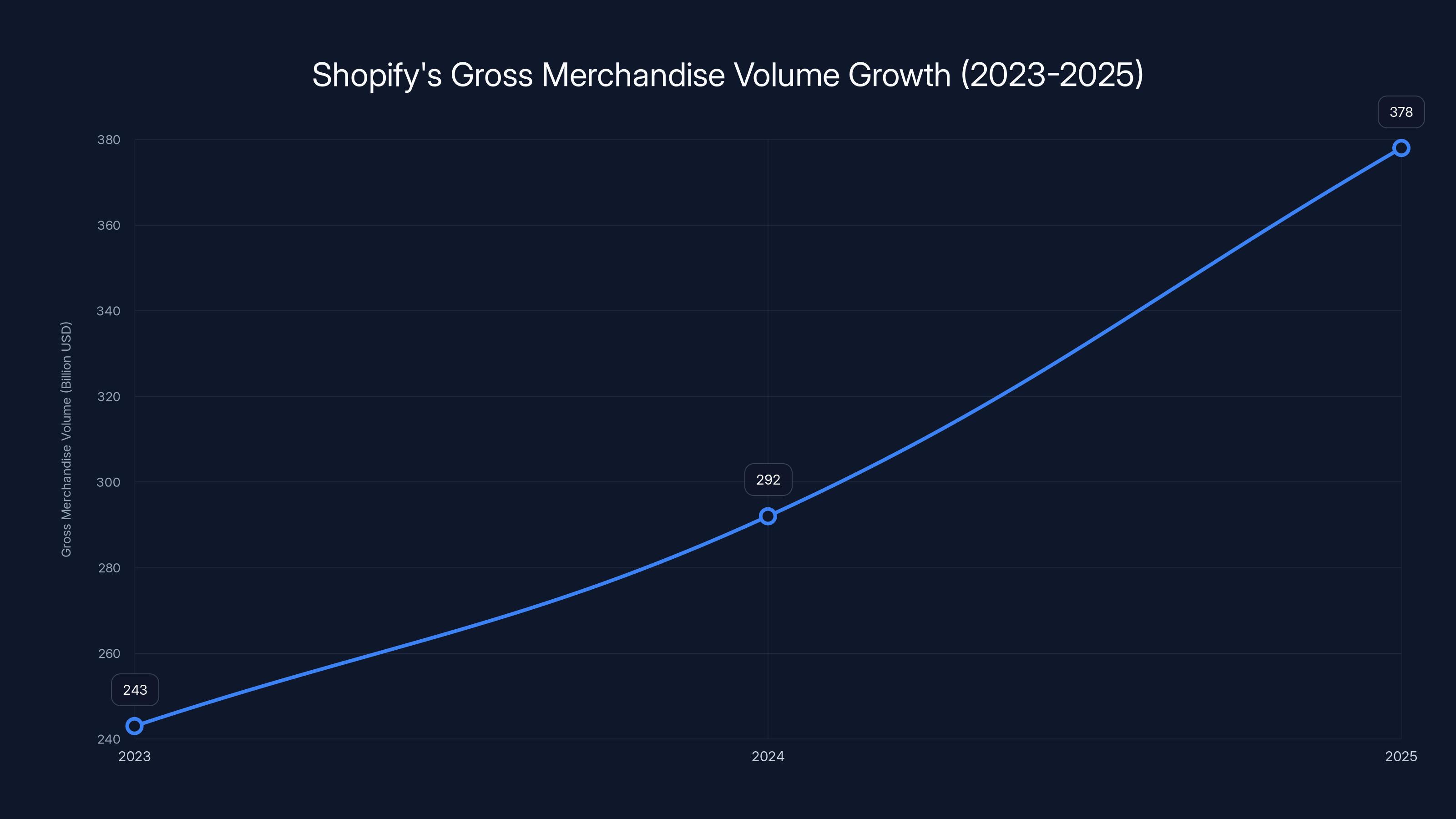

- Shopify's core business remains exceptionally strong: 30% revenue growth at 2B in free cash flow and accelerating GMV growth at $378B (+29%) as reported by Shopify's Q4 2025 financial results.

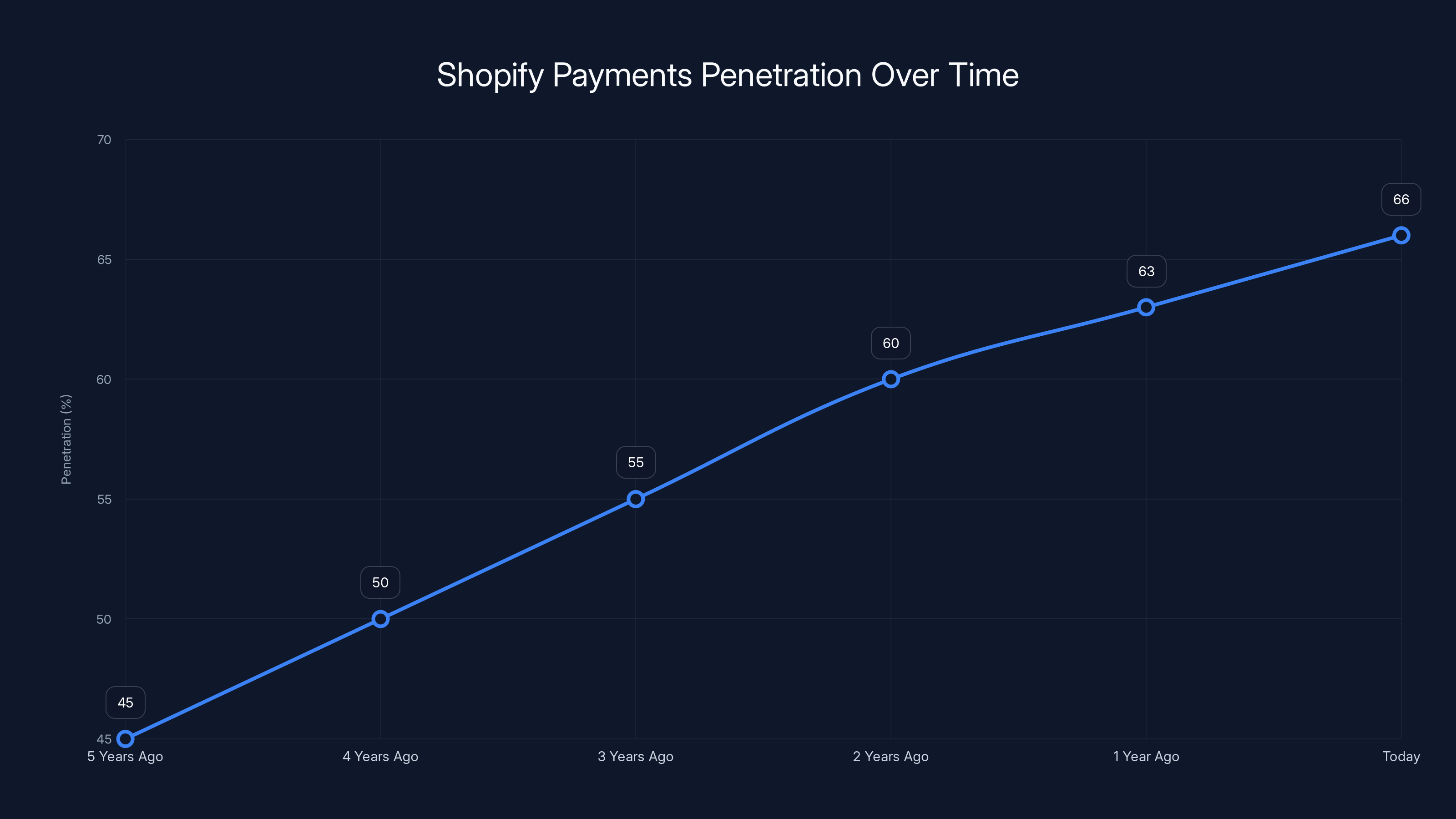

- Payments penetration is the hidden compounding engine: Shopify Payments grew from 248B in five years as penetration hit 66% of GMV, now driving 76% of revenue, according to PYMNTS.

- B2B nearly doubled with sustained momentum: B2B commerce grew 96% YoY despite market headwinds, with every quarter showing 84%+ growth rates, as highlighted by Digital Commerce 360.

- The stock-to-business disconnect reveals market expectations: Trading at 100x earnings despite strong cash flow shows investors expect either faster growth or multiple expansion that's unlikely to materialize, as noted by Barron's.

- The lesson for founders: Expectations management and guidance accuracy matter as much as raw growth rate; valuation multiples create a treadmill where hitting numbers isn't enough if the bar keeps rising.

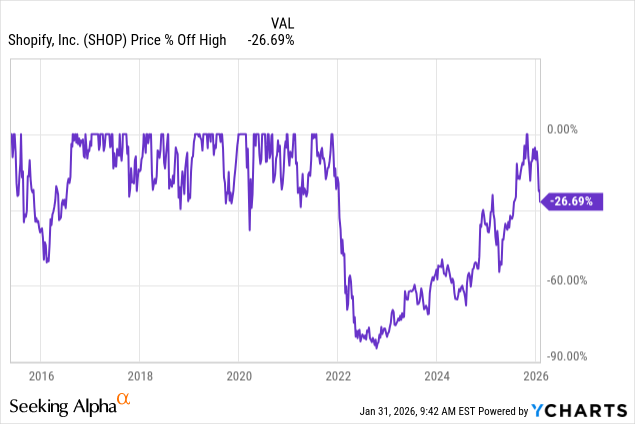

Despite Shopify's 30% revenue growth and 29% GMV increase, its stock fell by 28% in 2025, highlighting a disconnect between operational success and market valuation.

The $378 Billion Gross Merchandise Volume Milestone: Why This Number Matters More Than the Stock Price

Let's start with the number that should make every commerce founder sit up straight. Shopify processed

But here's what makes this number meaningful rather than just impressive. Shopify now captures over 14% of all US ecommerce, according to Digital Commerce 360. That's not market share in a traditional sense. That's becoming infrastructure. When you control 14% of a $1 trillion+ market, you're not a company competing for space anymore. You're the foundation that space is built on.

The growth trajectory tells an even more interesting story. GMV growth accelerated from +20% in 2023 to +24% in 2024 to +29% in 2025, as reported by Investing.com. Most companies at scale decelerate. They hit a ceiling. Growth flattens toward single digits. The market matures. Competition increases. Shopify is doing the opposite. At a scale most startups can't even imagine, it's accelerating.

This matters for founders because it answers a critical question about your total addressable market. If you're building on Shopify's ecosystem, or if you're competing in commerce, this tells you the TAM underneath your opportunity is expanding, not contracting. The pie isn't shrinking. It's growing faster than it did last year, despite macro uncertainty, recession chatter, and all the reasons people said ecommerce would slow down.

The mechanics of how Shopify achieved this acceleration reveal something most companies get wrong about scale. They didn't do it through a single lever. They grew GMV through:

- Organic expansion from existing merchants (mature cohorts doing more volume)

- New merchant acquisition (still adding customers at significant scale)

- International expansion (UK, Canada, Australia, and other markets still in early innings)

- Enterprise tier growth (larger merchants migrating to more advanced tiers)

- Vertical specialization (focusing on specific industries like beauty, fashion, food and beverage)

Most companies pick one of these and optimize it to death. Shopify is pulling multiple levers simultaneously, which creates compounding effects. When you add merchants and accelerate volume per merchant and expand internationally and move upmarket, the growth rates don't just add together. They multiply.

For comparison, this is what most SaaS companies do wrong. They optimize customer acquisition. They optimize retention. They optimize expansion revenue. But if they're lucky, they get two of these three truly working at scale. Shopify has all three firing. That's why the business accelerates despite being enormous.

Shopify Payments penetration has increased from 45% to 66% over the past five years, indicating a strong adoption of their proprietary payment system.

The Payments Penetration Machine: How Shopify Became a Fintech Company

If the $378 billion in GMV is the headline number, the payments penetration story is the plot twist that explains everything about Shopify's business model evolution.

Five years ago, Shopify Payments processed 45% of the gross merchandise volume flowing through the platform. Today, it's 66%. In Q4 alone, it hit 68%, as noted in Shopify's financial results. That's a 23-percentage-point increase in penetration over five years. And the gross payment volume went from

Let's be precise about what this means. This isn't Shopify acquiring more customers. This is existing customers increasingly choosing Shopify's payments product over alternatives. It's default effect. When something becomes the path of least resistance, adoption compounding accelerates.

The lesson here is profound for any B2B founder thinking about product strategy. Shopify proved that if you can make an adjacent product the default, you don't just grow that product's revenue. You accelerate the entire company's growth. Here's why.

When Shopify's Payments penetration was 45%, the company was competing on equal footing with every other payments processor. Stripe, Square, traditional acquirers, all fighting for volume. But as penetration climbed toward 66%, something shifted. Shopify had data on every transaction. It could underwrite better than competitors. It could price dynamically. It could offer better terms to merchants who used it. The more merchants switched to Shopify Payments, the better Shopify got at the payments business, which made more merchants want to switch.

This is the compounding effect most SaaS companies never achieve. You don't just grow your product's revenue. You create a moat around your core business.

Merchant Solutions, the revenue segment that includes payments, now represents 76% of Shopify's total revenue. Subscriptions (pure software) are just 24%, as highlighted by Tikr. This is a profound shift. Shopify has become a fintech company that happens to sell commerce software, not the other way around.

The margins on payments are different from software. Typically thinner in percentage terms, but massive in absolute dollars. Shopify Payments gross margins are likely in the 30-35% range, versus 75-80% for pure software. But when you're processing $248 billion in volume, even 30% margins equals billions in gross profit.

Here's where it gets interesting for the valuation conversation. Wall Street doesn't typically pay software multiples for fintech business. Software companies trade at 8-15x revenue. Fintech companies trade at 2-5x revenue. So as Shopify's revenue mix shifts more toward Merchant Solutions, some investors value it as a lower-multiple business.

This is part of why the stock is down despite the business thriving. Investors look at the 76% of revenue coming from payments and think "that's fintech margins, not software margins." They're right. But they might be wrong about whether the business is actually less valuable for that reason.

B2B Commerce Growth of 96%: The Sleeper Hit Nobody Talked About

While everyone focused on Shopify's core ecommerce business, something quietly remarkable happened in B2B. Shopify's B2B commerce segment grew 96% in 2025, as reported by Digital Commerce 360. That's nearly doubling. At a company already doing $11.6 billion in revenue, that's a meaningful absolute growth rate, not just a percentile performance.

But the quarterly cadence is where this gets interesting. Q1 grew 109%. Q2 grew 101%. Q3 grew 98%. Q4 grew 84%, according to PYMNTS. If you're looking at this and thinking "deceleration," you're technically right but also missing the point. 84% growth in the slowest quarter is a number most B2B SaaS companies would trade their entire product roadmap for. Most B2B SaaS companies at scale are doing 10-15% growth. Shopify's B2B business, which started from a relatively smaller base, is doing 84%.

The reason this matters is that it shows Shopify's expansion into B2B isn't a one-time burst. It's sustained momentum. This is a company that solved a problem for D2C merchants (ecommerce) and is now solving it for B2B merchants (wholesale, distribution, large retailers with multiple sales channels).

Who are the early customers? Brands like Carrier (HVAC equipment), Dermalogica (professional skincare), Progress Lighting (commercial lighting). These are not small merchants. These are companies with complex B2B sales processes, multiple channels, and sophisticated buying flows.

Why does B2B matter for Shopify? Because B2B commerce deals are bigger, stickier, and have higher lifetime value. A D2C fashion brand might do

For founders, this is a masterclass in market expansion done right. Shopify didn't kill its core business to chase B2B. It layered B2B on top. It took the core commerce infrastructure and adapted it for complex B2B workflows. Then it powered the growth with sales, marketing, and product investment.

The B2B playbook is also worth studying for what it reveals about Shopify's product philosophy. B2B required different features: custom pricing, order management, wholesale channels, complex approval workflows, batch quoting. Shopify built a lot of this from scratch. But it did it without fragmenting the core platform. The same underlying infrastructure powers both D2C and B2B.

That architectural decision is why B2B could grow 96% while the core business grew 30%. It wasn't cannibalizing. It was additive.

Shopify's B2B commerce segment experienced significant growth in 2025, with Q1 seeing the highest increase at 109% and Q4 still achieving a robust 84% growth rate.

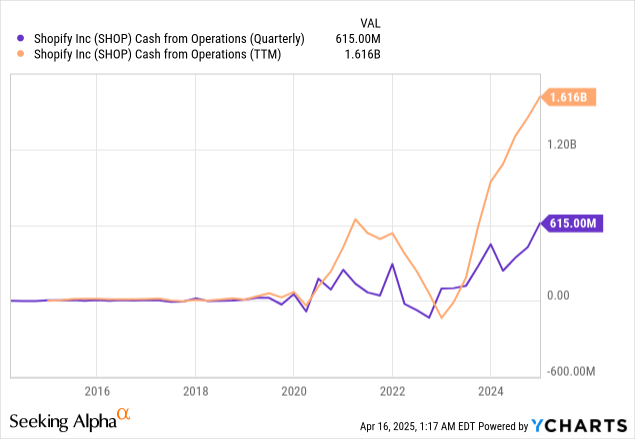

Free Cash Flow: $2 Billion and Why It Matters More Than Growth Rate

Here's what the stock market seemed to ignore. Shopify generated $2 billion in free cash flow in 2025, as detailed in Shopify's financial results. That's not profit. That's cash you can actually spend, invest, return to shareholders, or use for acquisitions.

For a company generating

Why does this matter more than revenue growth? Because FCF is hard to fake. You can manipulate revenue recognition. You can adjust cost accounting. But cash is either in the bank or it isn't. $2 billion in FCF means Shopify is converting its topline growth into actual profit while still reinvesting in the business.

The company announced a $2 billion buyback program alongside this earnings announcement, as reported by Investing.com. That's significant. A company doesn't buy back shares if leadership thinks the stock is overvalued. It suggests management believes the stock is trading below intrinsic value despite the 100x earnings multiple.

For founders thinking about venture fundraising and eventual exits, Shopify's FCF generation tells an important story. The market rewards not just growth, but proof that the growth is profitable. Shopify proved it could grow 30% while maintaining 17% FCF margins. That's a rare combination.

Most companies have to choose. Grow fast and burn cash. Or grow slowly and generate profit. Shopify did both. This is the operating excellence that separates tier-one companies from everything else.

How did Shopify achieve this? Several factors:

-

Operating leverage: At $11.6 billion in revenue, the cost to add incremental revenue is lower than at smaller scale. Servers, support teams, and engineering infrastructure already exist.

-

Pricing power: Shopify raised prices on many tiers without major churn. The value of the platform justifies higher costs.

-

Mix shift to higher-margin revenue: The Merchant Solutions segment (payments) is growing faster than pure software, which actually improves margins because the company is already absorbing fixed costs from the software business.

-

Efficient marketing: Shopify has moved from expensive CAC-heavy acquisition to more organic and self-serve models, reducing CAC and improving unit economics.

-

Vertical specialization: Rather than building generic features for everyone, Shopify is building vertical-specific solutions (beauty, food and beverage, fashion) that justify premium pricing and reduce feature bloat.

This combination of factors is worth studying if you're thinking about how to scale profitably.

The Valuation Paradox: Why 30% Growth at Scale Isn't Enough for Some Investors

Now we get to the uncomfortable part. The disconnect between the stock and the business fundamentals comes down to expectations and multiples.

Shopify trades at roughly 100x earnings and 73x forward earnings, as noted by Barron's. Those are extraordinary multiples. For context, the broader market trades at 15-20x earnings. Meta and Nvidia, the AI darlings, trade in the 30-50x range. Shopify is asking for 100x.

At those multiples, the stock price is essentially pricing in perfection. It's pricing in consistent delivery of guidance. It's pricing in no macro slowdowns. It's pricing in no competitive threats. It's pricing in execution of all the company's most ambitious plans.

When a company trades at 100x earnings, it needs to grow roughly 30-40% annually just to maintain the multiple. If it grows slower than that, the multiple contracts and the stock falls even if earnings are up. If it grows faster, the multiple expands and the stock rises dramatically.

Shopify is growing 30%. That's right at the floor of what the valuation requires. Miss guidance by a point or two, and investors start asking whether the multiple is justified. Especially in an environment where interest rates are rising and Treasury bonds are paying 4-5%, the opportunity cost of owning a 100x earnings multiple stock looks different than it did when rates were 0%.

This is where the disconnect becomes clearer. Shopify isn't the problem. The valuation that the market assigned to it at its peak was the problem. The stock was up massively in 2020-2021 when growth was 50%+ and multiple expansion was running hot. Now growth has decelerated to 30% (which is still exceptional, but slower than before) and multiple compression is hitting hard.

For founders, this is a lesson in how valuations work. During bull markets, you get multiple expansion on top of earnings growth. A company growing 50% at 8x revenue might jump to 20x revenue in a bull market. Your stock price soars. But in bear markets, the multiple compresses. That same 50% growth might warrant 5x revenue instead of 8x. The stock falls despite accelerating business performance.

Shopify's situation is actually healthier than it looks on the surface. The business is genuinely getting better (more cash generation, accelerating GMV growth, new market expansion). The stock is falling because the starting valuation was too high and the multiple is normalizing.

Is a 100x earnings multiple justified? That depends on your view of interest rates, risk-free rate alternatives, and whether 30% growth is sustainable. If you think Shopify can grow 30%+ forever, then maybe 100x earnings is reasonable. If you think growth will slow to 20% within a few years (still exceptional), then 70x earnings might be more appropriate.

The honest answer from management seems to be: we don't know how fast it will grow, but we're guiding for low 30s in Q1 and maintaining our long-term guidance. That's what a company does when it's trying to under-promise and over-deliver.

Shopify's 17% free cash flow margin significantly outperforms the typical SaaS company, which ranges from 5% to 10%. This highlights Shopify's ability to convert revenue into cash effectively.

The International Opportunity: $378 Billion in GMV Understates Shopify's TAM

One number Shopify doesn't emphasize as much as it should: the addressable market for its payments and platform business internationally is absolutely enormous, and most of it is still untapped.

The company has meaningful presence in Canada, UK, and Australia, as noted by Shopify's financial results. But Europe, Asia, and Latin America represent markets where Shopify has only scratched the surface. Germany, France, Japan, Mexico. These are markets with billions in ecommerce transactions annually. Shopify's penetration in most of these markets is still in the single digits.

Why does this matter? Because when the US market matures and growth slows, Shopify has a massive geographic expansion lever. Every developed market has a version of what Shopify did in the US. Build the best commerce platform for SMB merchants. Expand upmarket over time. Become infrastructure.

International expansion is harder than it looks. It requires local payment methods, local tax compliance, local language support, local competition. Shopify's advantage is that it has cash, brand, and proven product-market fit that it can export. It's not building from scratch in each country.

Over the next 5-10 years, if the company executes internationally, the $378 billion in current GMV could look like a rounding error relative to total addressable market.

This is why the 28% stock decline might represent an opportunity for long-term believers. The market is pricing in near-term valuation compression and missing the long-term geographic expansion upside.

The Merchant Solutions Shift: From Software to Fintech Economic

We mentioned earlier that Merchant Solutions is now 76% of revenue. Let's dig deeper into why this shift changes how to think about Shopify's future.

Merchant Solutions includes Shopify Payments, but also Shopify Capital (short-term merchant loans), Shopify Balance (merchant banking), and other fintech services. These products have completely different unit economics than pure software.

Payments are transaction-based. You process

The advantage of fintech economics is that they compound faster than software once you hit scale.

The disadvantage is that fintech carries regulatory risk and competitive intensity that pure software doesn't. Stripe, Block, and traditional payment processors are all competing for the same merchant base. Shopify's advantage is being embedded in the merchant's daily software. But it's not an unbeatable moat.

Shopify's strategy seems to be to use the software platform as a distribution channel for fintech services. You're already in Shopify. You already see Shopify Payments as an option. Why switch to an external processor? The lower switching cost and higher convenience drive adoption.

This is a smart strategy. But it also means Shopify is increasingly competing as a fintech company, not just a software company. That's a different competitive battle.

For founders, the lesson is that distribution of financial services through a platform is one of the highest-leverage business models. Shopify took a 45% penetration in payments and is pushing it toward 70%+. At that penetration, the payments business is more valuable than the core software business.

Shopify's GMV grew from

Guidance and Expectations Management: The Real Reason for the Stock Decline

Shopify guided for Q1 to grow in the low 30s, as noted by Shopify's financial results. That's above analyst expectations. So why did the stock fall so hard?

Because guidance matters less than beating guidance. And beating guidance matters less than raising guidance. The market has trained itself to expect companies to grow into their valuations and then expand them through better-than-expected performance.

When Shopify was growing 50% and guiding for 50%, the market celebrated. When it's growing 30% and guiding for low 30s, the market sees deceleration. The absolute growth rate doesn't matter as much as the trajectory.

This is a brutal dynamic for large companies. You're always chasing the multiple you had last year. If you maintain the same growth rate, you're underperforming. If you decelerate even slightly, you're disappointing.

Shopify seems aware of this. The company is being conservative with guidance (low 30s could mean 31-35%). There's room to beat. If Q1 comes in at 32-33% growth, management can claim "beat," which might stabilize the stock.

But the deeper issue is that Shopify is in a valuation trap. At 100x earnings, the stock price is decoupled from business performance. Good news gets priced in immediately. Bad news gets punished severely. And in-line performance (like 30% growth) disappoints.

This is where investors need to decide if they're buying the business or the stock. The business is exceptional. The stock is facing multiple compression.

Enterprise Customers and Upmarket Migration: The Unseen Growth Driver

Shopify doesn't break out exact numbers for enterprise customers, but there's clear evidence the company is winning upmarket. Large retailers, brands with $100+ million in annual revenue, and enterprise merchants are increasingly moving to Shopify Plus (the enterprise tier).

Why does this matter? Because enterprise customers have 3-5x the lifetime value of SMB customers. They pay higher fees, they stay longer, they use more features, they require more support, and they drive expansion revenue.

When Shopify targets brands like Carrier and Dermalogica for B2B, those are enterprise-class customers. The ACV is likely in the hundreds of thousands to millions of dollars. Compare that to a typical SMB store where ACV might be $5,000-15,000 annually.

Shopify's upmarket strategy is less visible than its SMB strategy, but it's probably responsible for 20-30% of revenue growth at this point. Every large retailer that migrates from custom-built commerce or legacy Magento/SAP systems to Shopify Plus is a massive revenue win.

The advantage of upmarket migration is that it extends the company's TAM significantly. SMB ecommerce is maybe a

For founders, this is a playbook worth understanding. You don't have to choose between SMB and enterprise. You can start with SMB (easier to sell, faster to adopt, simpler product), then use that install base and reference base to move upmarket. That's exactly what Shopify has done.

Shopify trades at a significantly higher earnings multiple (100x) compared to Meta (40x), Nvidia (50x), and the broader market (18x), highlighting the high expectations set by investors.

The Buyback Announcement: What Management Believes About Valuation

Shopify announced a $2 billion buyback in the same earnings call where it announced 30% growth and a stock down 28%, as reported by Investing.com. That's a significant statement from management.

Buybacks send a signal: we think the stock is undervalued at the current price. We're willing to use cash to repurchase shares because we believe it's accretive to shareholder value over the long term.

Is management right? That depends on whether Shopify can actually sustain 30% growth and improve margins over the next few years. If it can, then shares at current prices might indeed be undervalued. If growth slows to 20% and margins compress, then the buyback might turn out to be value-destructive.

Management is clearly betting on the former scenario. And given what we know about the business (accelerating GMV, growing payments penetration, successful B2B expansion, strong free cash flow), their conviction makes some sense.

For investors, the buyback is worth noting not because it guarantees returns, but because it shows management's actual conviction about valuation. Talk is cheap. Using $2 billion of the company's balance sheet to buy back stock is putting real capital behind a thesis.

The Competitive Moat: Payment Penetration and Network Effects

As Shopify's Payments penetration has increased, the company's competitive moat has deepened. This is worth understanding because it explains why Shopify's valuation, even at a discount, might still be defensible.

Payment processors like Stripe have tried to compete with Shopify head-to-head. But Stripe doesn't have the ecommerce platform. It's a pure payments company trying to expand into commerce. Conversely, Shopify has the platform and is expanding into payments. The company with the broader surface area usually wins.

Why? Because of switching costs and network effects. Once a merchant is on Shopify, they use Shopify Payments, Shopify Markets, Shopify Analytics, Shopify Capital, Shopify Balance. Switching to a competitor means ripping out multiple integrations, not just switching a payment provider.

As penetration increases, this effect compounds. More merchants use Shopify Payments, which means Shopify accumulates more transaction data, which makes its underwriting and fraud detection better, which makes the product more valuable. Competitors can't match this data advantage because they don't have the platform relationship.

This is a legitimate moat. It's not unbeatable (companies can build good payment processing), but it's real. And as penetration climbs from 66% toward 75-80%, the moat gets deeper.

For investors, this suggests Shopify's competitive position is strengthening despite stock weakness.

Macro Concerns and How Shopify Is Insulated (and Exposed)

The broader macro environment is uncertain. Recession risks, interest rate volatility, consumer spending headwinds. How does this affect Shopify?

The good news: Shopify's GMV growth accelerated to 29% even during macro uncertainty, as reported by Shopify's financial results. This suggests merchants using the platform are doing well and increasing sales. If a major recession hits, GMV growth might slow, but the company has proven it can maintain growth even when conditions are tough.

The bad news: Shopify is economically sensitive. If consumers stop buying goods, merchants stop making sales, GMV falls, and Shopify's Payments volume and platform fees fall proportionally.

Unlike pure software (where one contract slowdown doesn't break the company), commerce is highly cyclical. Shopify's growth is dependent on overall economic health.

However, the B2B expansion is actually a hedge against this. B2B commerce is less cyclical than D2C. Businesses still buy equipment, supplies, and goods regardless of consumer spending. So Shopify's 96% B2B growth is simultaneously aggressive growth and defensive positioning.

For investors, the macro question is whether you believe the consumer and business spending environment will hold up over the next 2-3 years. If yes, Shopify is well-positioned. If you expect a major recession, the stock might have further downside because growth would slow materially.

Comparing Shopify to Other SaaS Unicorns: The Valuation Context

To contextualize Shopify's 100x earnings multiple, it's worth comparing to other large SaaS companies.

Salesforce trades at roughly 45x earnings. Workday trades at 60x. Datadog trades at 80x. Shopify at 100x is at the expensive end, but not completely out of line with other high-growth SaaS companies that have proven execution.

The difference is that Salesforce, Workday, and Datadog have all decelerated to lower growth rates (15-25%) while maintaining or expanding margins. Shopify is still at 30% growth with expanding margins. So the multiple is expensive relative to peers, but reasonable relative to growth.

This is the bull case: Shopify deserves a premium multiple because it's growing faster with better execution than most of its SaaS peers.

The bear case: Shopify's growth will eventually decelerate like every company, and when it does, the multiple will compress sharply. Investors are paying for growth that may not persist.

Both views have merit. The stock's 28% decline suggests the market is moving toward the bear case. But that might create an opportunity for longer-term investors with higher risk tolerance.

What This Means for Founders Building in the Commerce Ecosystem

If you're a founder building a company that depends on ecommerce growth or sits on top of Shopify, what should you take from all this?

First, the TAM is expanding. Shopify's 29% GMV growth is proof that the underlying ecommerce market is growing faster than expected, even despite macro concerns. If you're building in this space, the opportunity is real.

Second, the best companies in the ecosystem will be those that capture specific niches Shopify doesn't. Vertical-specific tools, fulfillment optimization, subscription tools, customer data platforms, email marketing. Shopify can't be everything. The best way to compete is to be better at a specific thing.

Third, the payments opportunity is real. As Shopify's Payments penetration climbs, payment processing becomes more important and more complex. Companies optimizing payments, reducing fraud, or improving conversion rates will find willing customers.

Fourth, the B2B expansion is opening a completely new TAM. B2B commerce is more complex than D2C. Merchants need features Shopify doesn't have (custom pricing, complex workflows, integration with ERP systems). Building vertical-specific B2B solutions on top of Shopify infrastructure could be huge.

Fifth, the margin story matters. As Shopify's mix shifts toward higher-transaction-volume customers, it's capturing more take rate on a per-transaction basis. This is great for Shopify, but it means more sophisticated merchants might look for alternatives that offer better margins. There's a competitive opening if you can offer better unit economics.

Forward Guidance and What Investors Should Monitor

Shopify guided for Q1 growth in the low 30s. For the full year, management is sticking with its "longer-term growth framework," which implies 25%+ growth sustainably, as reported by Shopify's financial results.

Here are the metrics investors and founders should watch:

Gross Merchandise Volume Growth: This is the leading indicator. If GMV growth slows below 25%, that's a warning sign that the underlying ecommerce market is decelerating. If it stays above 28-30%, that suggests the company maintains momentum.

Shopify Payments Penetration: Watch this climb from 66% toward 75%+. Every percentage point of penetration increase is roughly $6 billion in incremental Payments volume. This is the revenue growth driver that gets underestimated.

Free Cash Flow Margins: Monitor whether the company maintains 15%+ FCF margins. If margins compress below 12%, it suggests the company is having to invest more to maintain growth, which would be a warning sign.

B2B Revenue Growth: Track whether B2B maintains 80%+ growth rates. If it slows below 50%, that suggests the upmarket expansion is hitting saturation.

Customer Concentration: Shopify doesn't break out exact concentration, but enterprise customer concentration is worth monitoring. If a few large customers represent too much revenue, that's a concentration risk.

The Long-Term Thesis: Why the Disconnect Might Resolve

The bull case on Shopify is ultimately simple: the business is becoming better, not worse, despite stock weakness. Here's how this might resolve in the company's favor:

- Maintain 30%+ growth for 2-3 more years, proving the multiple is justified.

- Expand margins as operating leverage increases, showing the business can compound both top and bottom line.

- Increase investor base in Shopify if economic conditions hold, which could expand the multiple back up.

- Demonstrate international expansion is working, which would increase perceived TAM.

- Build strategic advantages in B2B, payments, and fintech that create defensible moats competitors can't replicate.

If Shopify can do these things, the stock could multiple from

The bear case is equally straightforward: growth slows below 25% within 2-3 years, multiple compresses further, and shareholders face a multi-year period of underperformance even as the absolute business thrives.

Both are plausible. The stock decline reflects uncertainty about which scenario plays out.

Key Lessons for SaaS Founders from Shopify's Disconnect

Beyond Shopify-specific analysis, there are lessons here that apply to any founder thinking about the arc of their company:

-

Growth alone doesn't protect you from valuation compression. Even 30% growth at $11.6B doesn't prevent stock declines if the multiple gets too high. This means managing expectations and being honest about growth rates matters as much as delivering growth.

-

Adjacent products that become default can create exponential growth. Shopify Payments went from 45% to 66% penetration by becoming the default option. If you can make an adjacent product essential, you can grow faster than the core business.

-

Profitability matters more than you think. $2 billion in free cash flow is why Shopify can weather the stock decline. If the company were burning cash, the stock decline would be catastrophic. Aim to hit profitability earlier than people expect.

-

Market expansion is as important as market penetration. Shopify's B2B growth at 96% shows expanding into adjacent customer types can drive superlinear growth. Don't assume your original customer cohort is your TAM ceiling.

-

International expansion is a long-term lever. Shopify has barely penetrated most non-English-speaking markets. As the US market matures, geography becomes the next growth frontier. Build with global scalability in mind from the start.

-

Specificity beats generality at scale. Shopify's move toward vertical specialization (beauty, fashion, food and beverage) shows that trying to be everything limits growth. Vertical-specific solutions command premium pricing and reduce churn.

-

Expectations management is as important as beating expectations. A company that guides conservatively and beats by 5% often outperforms a company that guides aggressively and matches. Wall Street rewards guidance accuracy as much as absolute performance.

FAQ

Why is Shopify's stock down 28% if the business is growing 30%?

The stock decline is primarily due to multiple compression, not business deterioration. Shopify was valued at exceptionally high multiples (150x+ at its peak) based on expectations of sustained 50%+ growth. Now that growth has moderated to 30% (still exceptional) and market conditions are different, investors are applying lower multiples. A company trading at 100x earnings instead of 150x earnings will see stock declines even with strong business growth.

What is Shopify Payments penetration and why does it matter?

Shopify Payments penetration is the percentage of gross merchandise volume processed through Shopify's proprietary payments system. It's grown from 45% five years ago to 66% today, as noted by Shopify's financial results. This matters because as more volume flows through Shopify Payments, the company earns more revenue from transaction fees, gains more data to improve underwriting and fraud detection, and creates switching costs that lock in merchants. Each percentage point of penetration increase represents billions in incremental revenue.

Can Shopify maintain 30% growth indefinitely?

Maintaining exactly 30% growth indefinitely is unlikely for a company at $11.6 billion in revenue. However, 25-30% growth for the next 3-5 years is plausible if the company successfully expands internationally, continues B2B growth, and increases Merchant Solutions penetration. Eventually, growth will decelerate toward 15-20% as the company matures, which is still exceptional for a company of this size.

Is Shopify's 100x earnings multiple justified?

It depends on your assumptions about growth sustainability and risk-free rate alternatives. If Shopify can grow 30%+ for 5+ years while maintaining 15%+ free cash flow margins, then 100x earnings might be justified. If growth slows to 20% within 2 years, then 70x earnings is more appropriate. The market's view seems to be that the starting valuation was too optimistic, which is why the multiple is compressing.

What opportunities exist for companies building on Shopify?

The biggest opportunities are in areas Shopify doesn't focus on: vertical-specific tools for niche industries, payment optimization and fraud prevention, fulfillment and logistics, customer data platforms and analytics, subscription management, and B2B commerce solutions. Companies that solve specific problems within the Shopify ecosystem can find willing customers at the intersection of the $378B GMV market and their specialized domain.

How does B2B commerce growth of 96% compare to the rest of Shopify?

B2B commerce growth of 96% is extraordinary and significantly outpaces core ecommerce growth of approximately 20-25%, as reported by Digital Commerce 360. This shows that Shopify's expansion into B2B wholesale and complex merchant relationships is succeeding. B2B customers typically have higher lifetime value, larger transaction sizes, and greater stickiness, making this segment strategically important despite representing a smaller portion of total revenue currently.

What would cause Shopify's stock to recover?

The stock would likely recover if one or more of the following occur: (1) Sustained 30%+ growth for 2-3+ consecutive quarters, beating or maintaining guidance consistently; (2) Margin expansion showing the business can improve profitability while growing; (3) Successful international expansion demonstrating meaningful growth in non-US markets; (4) Material improvements in B2B customer acquisition and retention showing this segment can sustain 80%+ growth; (5) Multiple expansion if macro conditions improve and investors return to valuing growth more aggressively.

Is now a good time to invest in Shopify?

The answer depends on your time horizon and risk tolerance. For long-term investors (5+ years) who believe in the business fundamentals, current prices might represent an opportunity after multiple compression from peak levels. For shorter-term traders, the stock remains volatile and subject to earnings surprises. The business itself remains strong, but the valuation remains uncertain.

Conclusion: The Disconnect Is Real, But the Business Is Real Too

Shopify's situation represents one of the most interesting disconnects in public markets right now. On paper, the business is exceptional. 30% growth at

By almost any operational metric, Shopify is succeeding beyond the expectations set for most companies. The core metrics that matter for sustainable business growth are all improving. GMV acceleration. Payment penetration. Free cash flow generation. Margin stability.

Yet the stock is down 28% in a single year from previously elevated levels. The disconnect is real. But it's not because the business is broken. It's because the market applied too high a valuation at the peak, and now it's repricing based on new expectations about growth sustainability and risk-free alternatives.

For founders, this is a masterclass in how valuations work in practice. Growth matters. Execution matters. Profitability matters. But valuation multiples matter most of all. A company that grows slower than expected but at the right multiple will outperform. A company that grows faster than expected but at an unsustainable multiple will underperform.

Shopify is in the second scenario right now. The business is genuinely getting better, but the stock is falling because the multiple was too high. That's not a contradiction. That's how markets work.

The real question for investors isn't whether Shopify is a good company. It clearly is. The question is whether Shopify's current stock price reflects a good opportunity given the company's ability to grow into its remaining valuation multiple over the next 3-5 years.

For founders building in the commerce ecosystem, the lesson is different. The TAM is expanding. The platforms you build on top of are becoming more powerful. The opportunity to specialize and win in vertical niches is real. Shopify's situation—a great business with a stock price that doesn't reflect it—creates opportunities for specialized solutions that address gaps Shopify doesn't fill.

The disconnect between Shopify's stock and its business might resolve in the company's favor over the long term. Or it might persist as investors remain skeptical of the valuation. Either way, the underlying business tells an important story about how to build, scale, and dominate in commerce. That story is worth paying attention to, regardless of which way the stock moves on any given Tuesday.

Key Takeaways

- Shopify grew revenue 30% to 2B free cash flow, yet stock declined 28% due to valuation multiple compression from 150x to 100x earnings, as reported by Shopify's financial results.

- Shopify Payments penetration grew from 45% to 66% over five years, increasing volume from 248B and proving how making adjacent products default drives exponential growth, as noted by PYMNTS.

- B2B commerce grew 96% year-over-year with every quarter showing 84%+ growth, demonstrating successful expansion into high-value market segment with better unit economics, as highlighted by Digital Commerce 360.

- Merchant Solutions now represents 76% of revenue (up from 24% software subscriptions), showing Shopify's transformation from pure SaaS to fintech-dominant platform, as reported by Tikr.

- The stock-business disconnect reveals that for high-valuation companies, maintaining expected growth rates isn't enough—exceeding them or raising guidance is required to sustain stock price.

Related Articles

- The ARR Myth: Why Founders Need to Stop Chasing Unrealistic Growth Numbers [2025]

- MrBeast's Step Acquisition: Why Creator Economics Met Fintech [2025]

- How Shopify Works: Complete Setup to First Sale Guide [2025]

- IPO Outcomes 2025: What Wealthfront's Decline Reveals About Tech Company Valuations

- ElevenLabs 11B Valuation [2025]

- How to Launch an Online Store in 2026: Founder's Complete Guide [2025]