IPO Outcomes 2025: What Wealthfront's Decline Reveals About Tech Company Valuations

Introduction: The Diverging Paths of Two IPOs

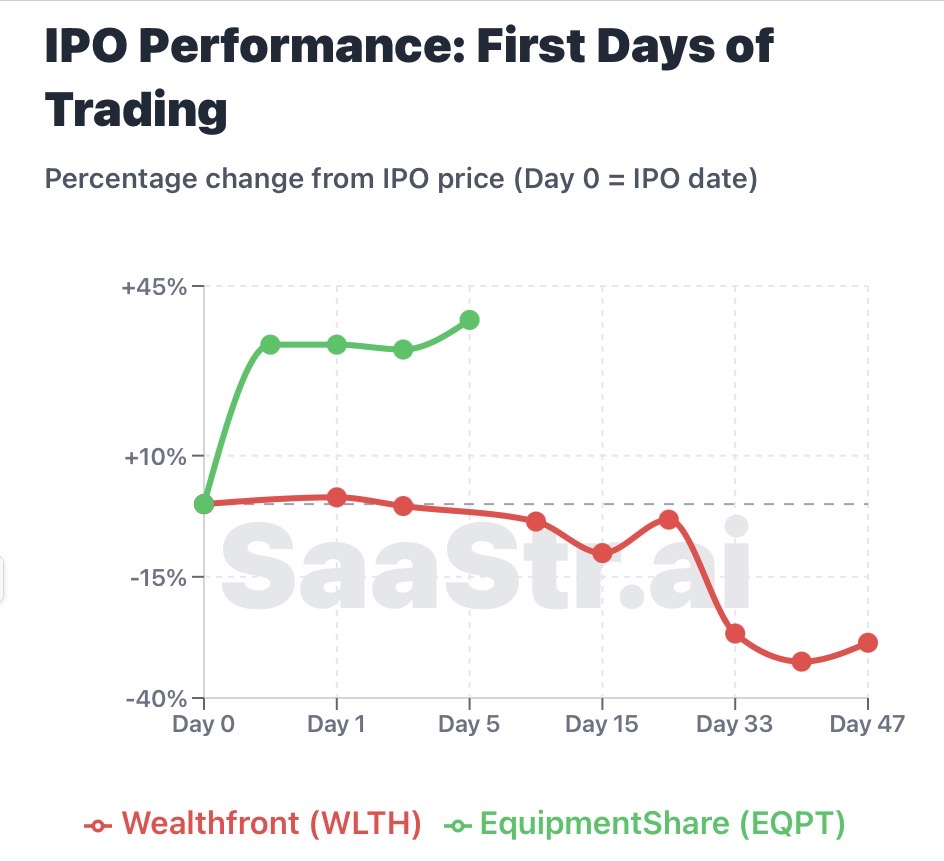

The IPO market reopened in late 2025, but it came with a stark reminder: not all successful companies experience successful public debuts. Two companies—Wealthfront and Equipment Share—went public just six weeks apart, yet their trajectories tell dramatically different stories about what modern investors actually value in a company going public.

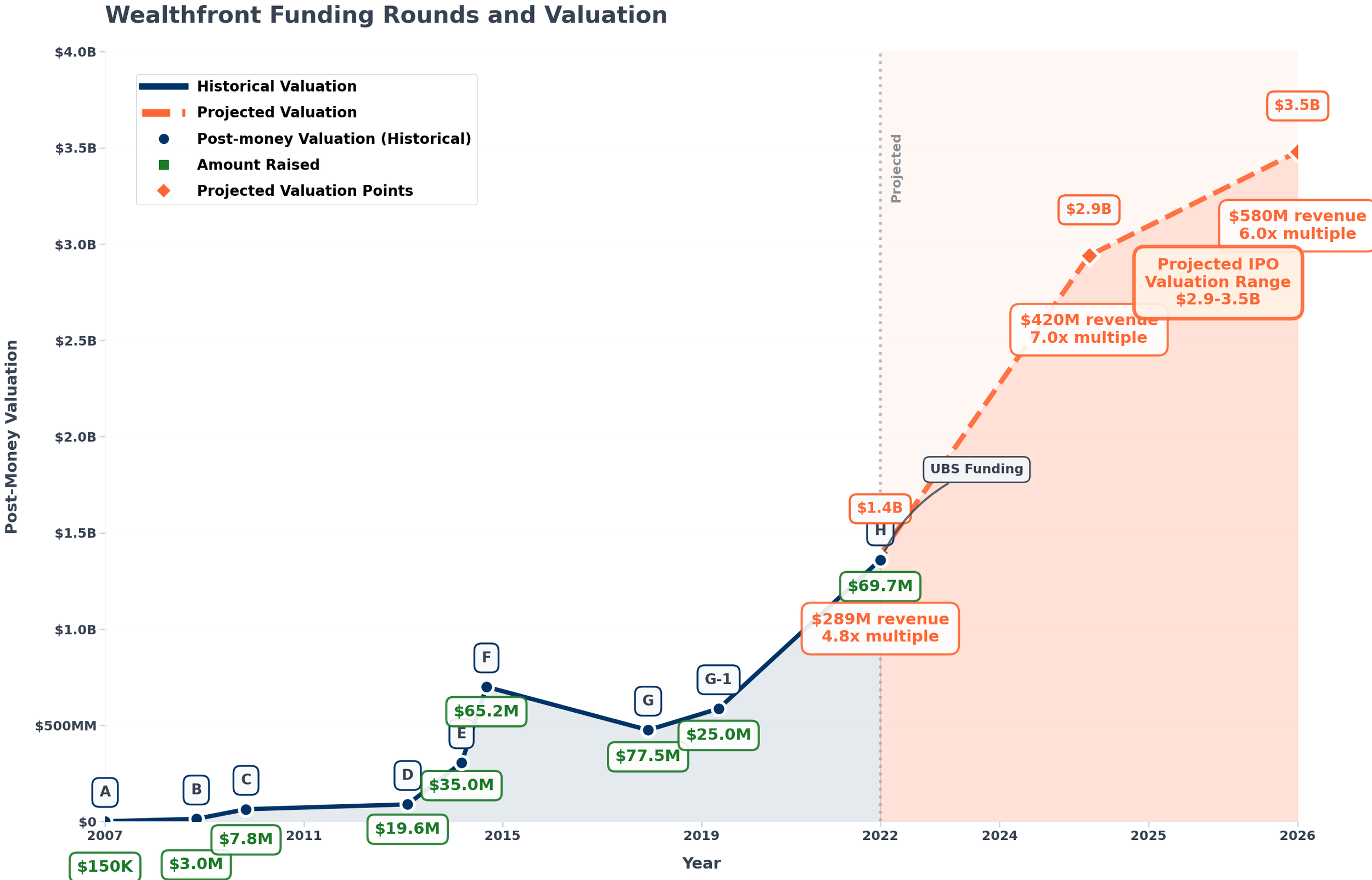

Wealthfront, a fintech automation platform that manages billions in assets, priced at the top of its range in December 2025 at

Meanwhile, Equipment Share—a less glamorous equipment rental platform providing technology solutions to construction contractors—priced at

On the surface, this divergence seems paradoxical. Both companies operated in functioning markets. Both benefited from macro tailwinds. Both had compelling growth stories. Yet the investment community voted with dramatically different conviction. Understanding why requires moving beyond superficial metrics and examining the fundamental questions that sophisticated institutional investors ask when evaluating public company opportunities.

This analysis explores five critical lessons emerging from these contrasting IPO outcomes. These insights extend beyond mere financial metrics—they reveal shifts in investor psychology, changing definitions of business quality, and emerging risks that founder-led companies must address before going public. For any startup approaching IPO readiness, the gap between Wealthfront's and Equipment Share's first-day performance offers invaluable guidance about what actually moves the needle with institutional capital.

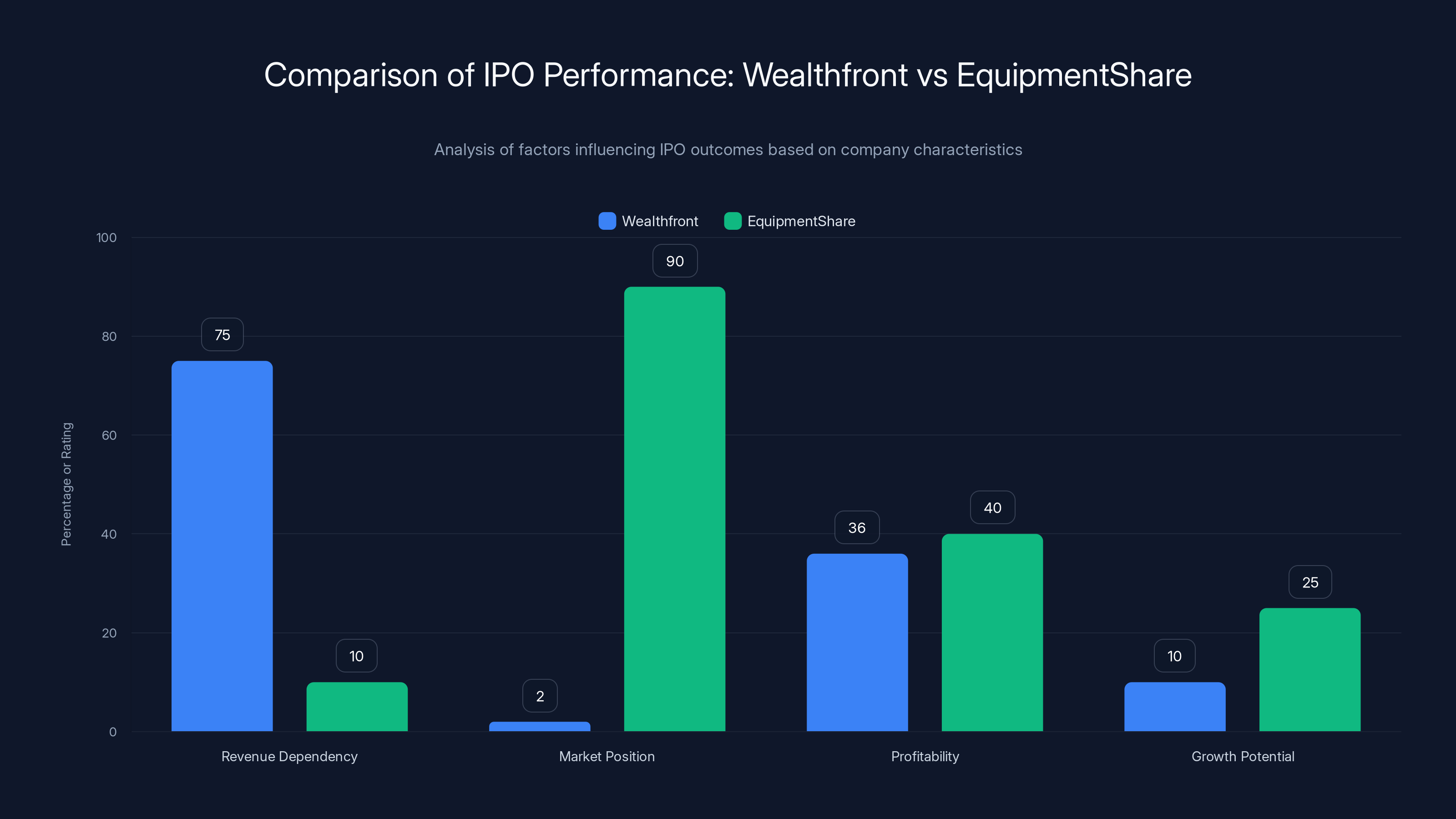

EquipmentShare's IPO success was driven by strong market position and diversified revenue, while Wealthfront's decline was influenced by high interest rate dependency and limited growth. (Estimated data)

Lesson 1: Profitability Is Necessary But Not Sufficient—Context Determines Everything

The Profitability Paradox

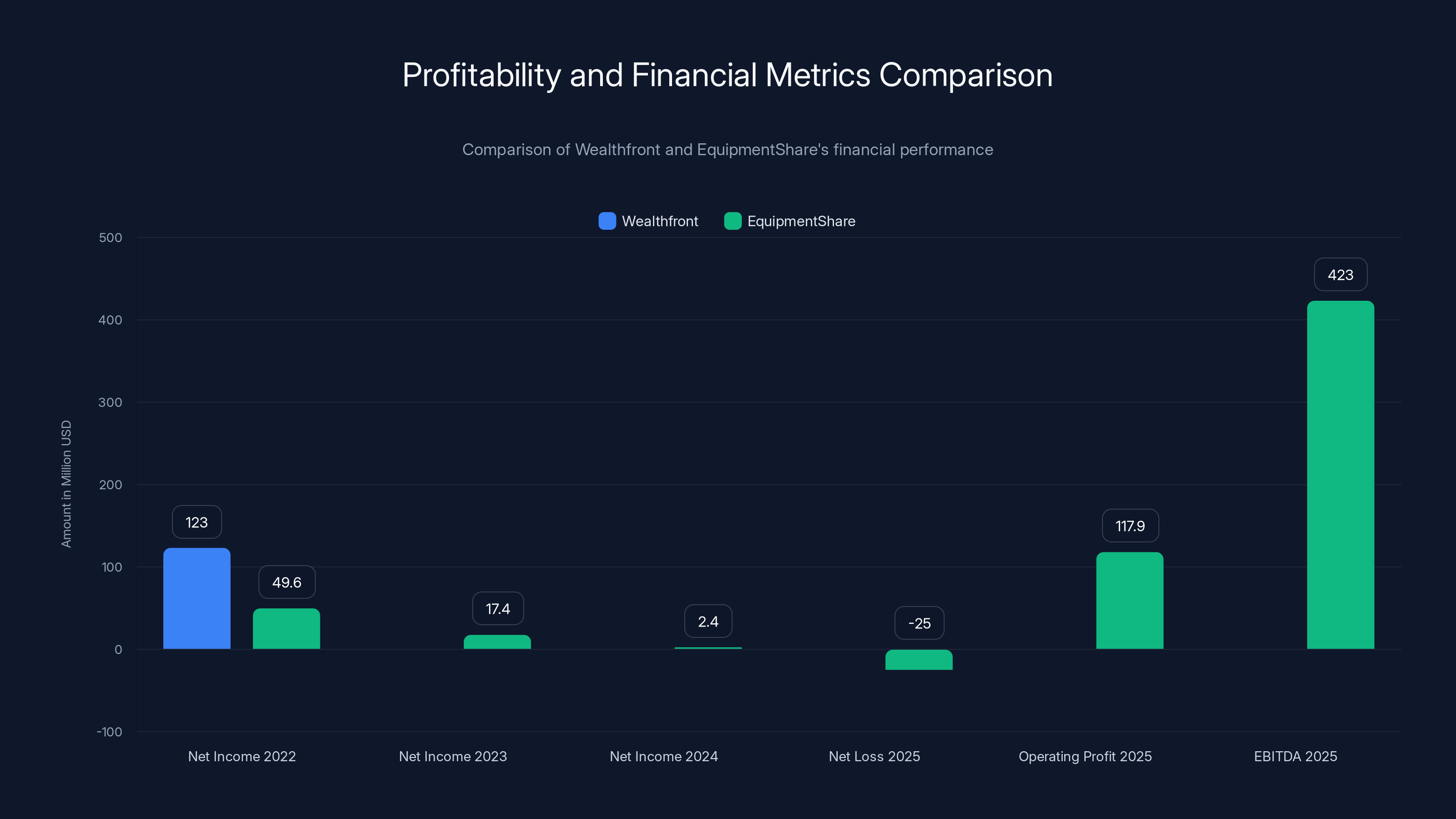

Wealthfront's profitability metrics appeared unimpeachable. The company generated

Yet this profitability became almost irrelevant to the stock's performance. Investors didn't celebrate the company's margin achievement; instead, they questioned whether the margins reflected genuine business durability or temporary conditions unlikely to persist. This distinction marks a crucial evolution in IPO-era investor thinking.

Equipment Share presented a more nuanced profitability story that paradoxically generated more investor confidence. The company demonstrated profitability in 2022 (

Intuition suggests this deterioration should have triggered investor skepticism. Instead, the market focused on different metrics:

The Quality-of-Profitability Framework

The divergent investor responses reveal an implicit framework investors now apply to IPO-stage companies. Profitability scores points, but the framework asks:

Can this company be profitable when it chooses to be? Equipment Share answered yes decisively. The company had demonstrated profitable operations across multiple years and multiple market conditions. Even during aggressive expansion, underlying operating economics remained strong. Investors essentially believed: if Equipment Share paused growth investments today, profitability would quickly return.

Wealthfront's profitability raised a different question: Is this profitability durable across changing market conditions? Wealthfront's exceptional margins derived substantially from interest income on customer cash management accounts—revenue that fluctuates with Federal Reserve policy decisions, not company execution. As Section 3 explores in detail, this revenue quality concern fundamentally undermined investor confidence despite impressive headline numbers.

Has this company achieved profitability while still investing in growth? Equipment Share answered affirmatively. The company maintained strong profitability while simultaneously expanding into new markets, upgrading technology infrastructure, and building market share. This suggested the business could scale without sacrificing returns. Wealthfront's profitability, by contrast, came partly from harvesting an existing customer base rather than from scaling new customer acquisition efficiently.

The lesson for pre-IPO companies proves counterintuitive: pursuing aggressive growth while sacrificing short-term profitability may signal more investor confidence than achieving high profitability while growth rates moderate. The market increasingly interprets steady-but-declining margins as a warning sign—suggesting the company has exhausted growth vectors or is managing to profitability rather than scaling toward profitability.

Practical Framework for IPO Preparation

Companies approaching IPO should model three profitability scenarios for investor presentations:

- Current-trajectory profitability: Where will we be in 18-24 months if we maintain current growth investments?

- Full-throttle-growth profitability: How much would we sacrifice in near-term profit if we invested aggressively in expansion?

- Harvest-mode profitability: What would our margins look like if we paused growth and optimized for cash generation?

Investors increasingly want to see companies demonstrating strength across all three scenarios, with clear trade-off explanations rather than optimistic projections that assume perpetual growth without margin pressure.

Lesson 2: Absolute Scale Creates Optionality—Market Position Trumps Growth Rate

The Scale Multiplier Effect

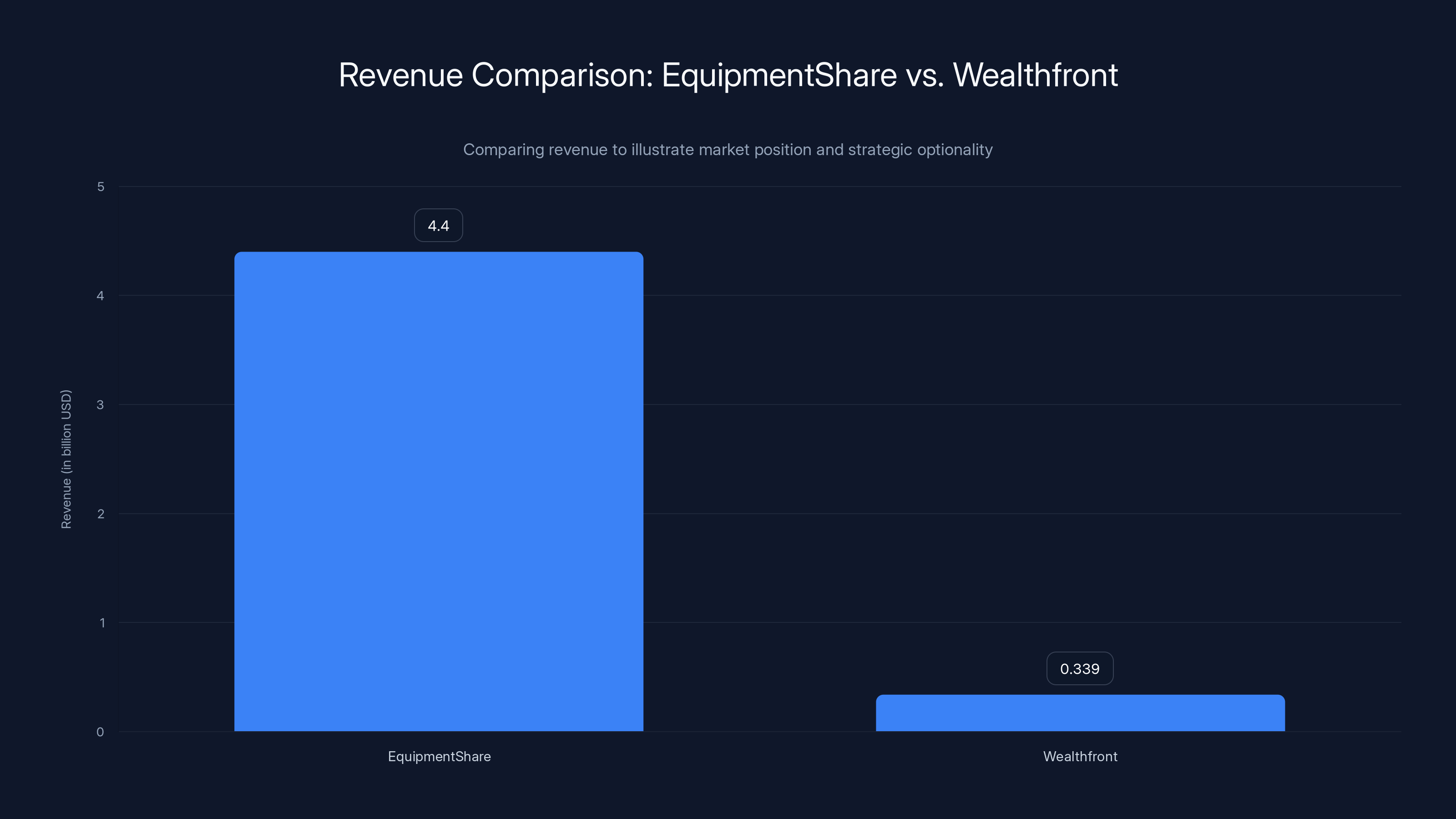

Equipment Share's revenue of

At $4.4 billion in revenue, Equipment Share has already established itself as one of the largest equipment rental providers in the United States. The company claims that over 90% of the Top 50 general contractors already rent from them. This market penetration creates a qualitatively different business dynamic than Wealthfront faces. Equipment Share isn't competing to become a market leader; the company is already a market leader. This status creates multiple sources of optionality unavailable to smaller competitors.

First, pricing power emerges naturally from category leadership. When 90% of major contractors already use your platform, those contractors face switching costs—operational disruption, integration costs, team retraining—that protect pricing. Equipment Share can potentially increase prices modestly, and customers will absorb the increases rather than undertake costly platform migrations.

Second, geographic and vertical expansion becomes self-reinforcing. When most major contractors in a region already use your platform, you own the network effects. A contractor considering a new regional office naturally requests the platform they already use. Equipment Share doesn't need to out-compete specialists in each new market; they leverage existing relationships to expand into adjacent regions.

Third, platform evolution compounds. A company managing $4.4 billion in equipment revenue can invest significantly in technology platforms—like Equipment Share's T3 platform providing real-time tracking, predictive maintenance, and remote access control across 235,000+ pieces of equipment. These investments become easier to justify with scale and create competitive moats that smaller competitors cannot match on spending.

Wealthfront's Different Challenge

Wealthfront's $339 million revenue places the company in a completely different competitive context. The company operates in wealth management and financial advice—markets where Schwab, Fidelity, and Vanguard have established dominant positions with substantially larger customer bases, brand recognition, and distribution networks. Even with strong profitability metrics, Wealthfront faces constant competitive pressure from rivals with superior scale.

The company's technology is sophisticated, its user experience is compelling, and its advisory algorithms represent genuine intellectual property. Yet these advantages exist in a market where competitors possess vastly greater scale, which translates to lower per-customer acquisition costs, broader distribution networks, and greater ability to cross-sell products. Wealthfront must continue winning market share in a zero-sum competitive environment. There is no comfortable "we've already won our category" position.

This distinction fundamentally influences how investors assess risk and opportunity. A market leader with

Revenue Scale as a Valuation Multiplier

Public market investors increasingly apply different valuation frameworks based on absolute scale rather than growth rate alone. A company generating

Wealthfront's impressive 40%+ annual growth rate means little to investors if the company must win customers from entrenched competitors who can match Wealthfront's product offering while leveraging superior distribution. Equipment Share's slower growth rate matters less because the company is expanding from a position of category leadership rather than fighting for relevance.

The valuation implications proved substantial. Equipment Share's first-week trading activity suggested investor positioning that valued the company at a higher revenue multiple than Wealthfront despite slower growth, because investors assessed Equipment Share's revenue as more durable and defensible.

EquipmentShare's revenue of

Lesson 3: Revenue Quality Eclipses Revenue Quantity—The Interest Rate Dependency Crisis

Wealthfront's Hidden Vulnerability

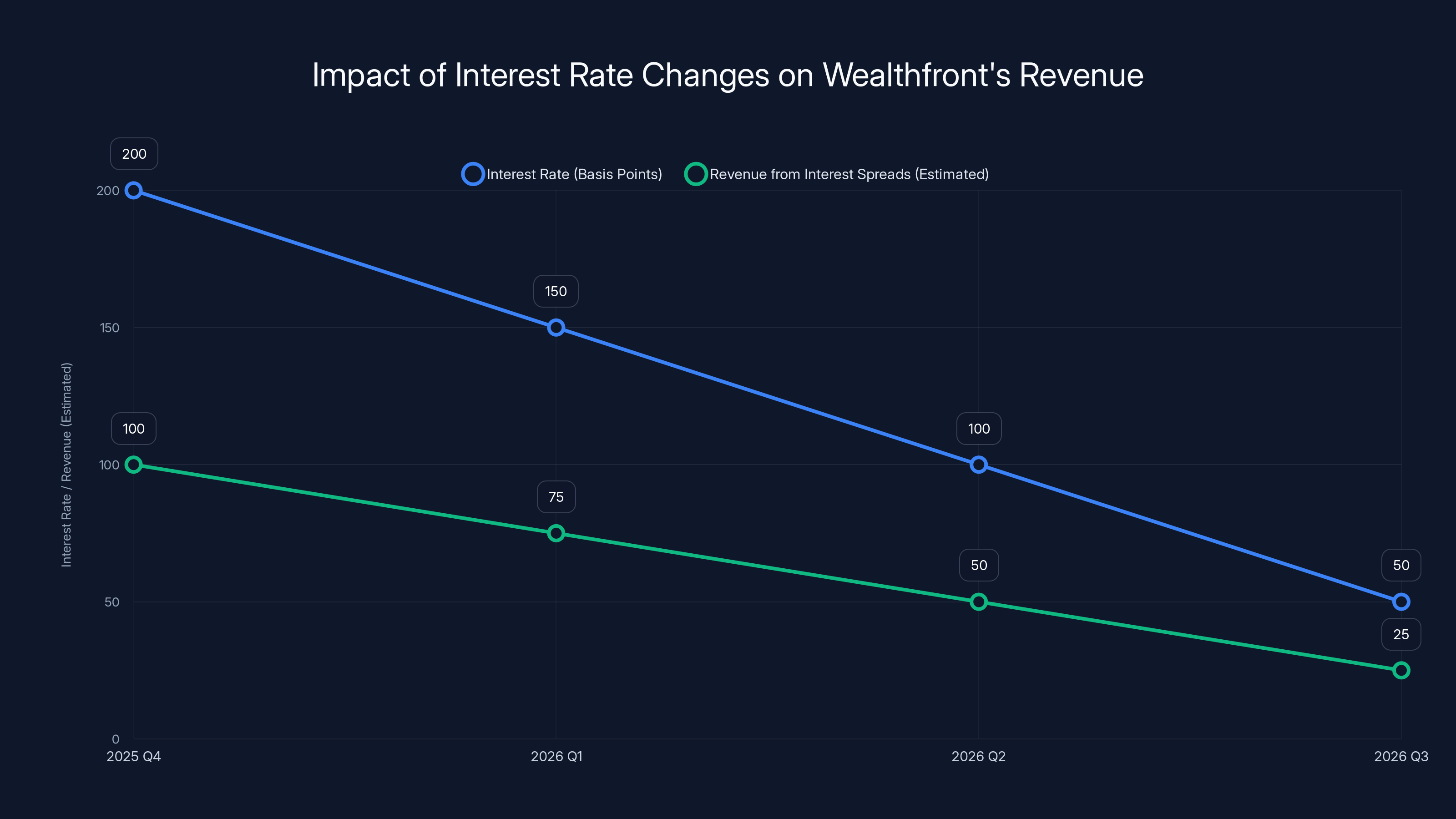

Understanding Wealthfront's stock decline requires examining a critical detail buried in operational metrics: approximately 75% of the company's revenue now derives from cash management—specifically, the interest rate spreads earned on customer deposit accounts. This revenue concentration creates profound vulnerability to a single macroeconomic variable: Federal Reserve interest rate policy.

When the Federal Reserve maintains elevated interest rates, banks holding customer deposits can earn substantial spreads on those deposits. Wealthfront's robo-advisor platform aggregates billions in customer assets, and the company earns spread income on the cash portion of those portfolios. In a high-rate environment (which characterized 2022-2024), this revenue component generated enormous cash flows with minimal operational cost.

However, Federal Reserve policy in late 2025 and early 2026 began rotating toward lower rates. Market consensus anticipated 100-200 basis points of rate reductions over 12-24 months. Mathematically, this creates a straightforward problem: if rates decline 150 basis points, the spread Wealthfront earns on customer deposits declines proportionally. A company deriving 75% of revenue from interest spreads faces a structural revenue headwind that has nothing to do with business execution or market share.

Further complicating matters, Wealthfront's traditional advisory fee revenue—the portion derived from assets under management and investment advisory services—grew only 10% year-over-year. This growth rate suggests the company is not rapidly expanding its customer base or increasing average customer lifetime value. The core advisory business appears to be maturing, while short-term growth came entirely from interest income harvesting.

The Revenue Quality Framework

Sophisticated institutional investors increasingly disaggregate revenue into quality tiers:

Tier 1 (Highest Quality): Subscription revenue from fixed customer contracts, with automatic renewal and transparent per-unit economics. SaaS companies exemplify this category. Revenue visibility is high, churn is predictable, and growth is repeatable.

Tier 2 (High Quality): Usage-based revenue with demonstrated unit economics and predictable scaling patterns. Platform companies where customer success drives increased usage tend to generate Tier 2 revenue.

Tier 3 (Moderate Quality): Revenue tied to customer outcomes or performance metrics. As customers succeed, they generate more revenue. Conversely, customer failure reduces revenue. This creates alignment but also cyclicality.

Tier 4 (Lower Quality): Revenue dependent on macroeconomic variables, interest rates, or market conditions outside company control. Float income, interest spreads, and currency-dependent revenue fall into this category.

Wealthfront's revenue composition shifted toward Tier 4 sources—exactly the direction that concerns sophisticated investors. Even though Tier 4 revenue is currently abundant and profitable, it's vulnerable to macro shifts. Investors assign lower valuation multiples to Tier 4-heavy companies because revenue durability depends on factors outside management control.

Equipment Share's Revenue Quality Advantage

Equipment Share generates revenue from equipment rentals—Tier 3 quality revenue. When construction activity increases, contractors rent more equipment and Equipment Share's revenue increases. When construction activity declines, revenue declines. This creates cyclicality, but the cyclicality depends on real economic activity and customer success, not monetary policy.

Furthermore, Equipment Share has introduced T3 platform services—fleet management, predictive maintenance, and optimization tools—that generate additional recurring revenue streams. These Tier 1 and Tier 2 revenue components (subscription-like platform fees) grow independently of construction cycles. The company is essentially layering higher-quality revenue on top of cyclical rental revenue, reducing dependence on any single economic variable.

Wealthfront, conversely, moved in the opposite direction—layering more interest-sensitive revenue on top of advisory fees. This created concentration risk that sophisticated investors immediately recognized.

Market Expectations and Reality Gaps

Wealthfront's IPO pitch likely emphasized the profitability and cash generation capacity of interest income. The company probably presented rosy scenarios about sustained interest rate environments and customer deposit growth. When market expectations shifted in late 2025 (as Fed policy clearly indicated rate reductions were coming), the gap between IPO-era optimism and emerging reality became impossible to ignore.

Equipment Share, by contrast, operated with more conservative assumptions. Construction cycles are notoriously unpredictable, and the company clearly communicated cyclicality risks to investors. When macro trends evolved, the surprise factor was minimal because investors already anticipated volatility.

The lesson: Revenue quality matters more than revenue quantity because it determines valuation multiple sustainability. A company earning

Lesson 4: Founder Control and Capital Allocation Signals Conviction

Dual-Class Share Structures and Founder Positioning

Both Wealthfront and Equipment Share utilized dual-class share structures enabling founders to maintain control despite public ownership. However, the founders took diametrically opposite approaches to personal capital allocation—with dramatically different implications for investor confidence.

The Schlacks brothers, founders of Equipment Share, retained approximately 81% voting control through Class B shares, enabling them to direct company strategy and major decisions despite not owning 81% of economic value. This structure is common in founder-led companies, but the critical signal emerges from what the founders did after the IPO.

Public records indicate the Schlacks brothers maintained substantial personal holdings and did not execute massive secondary share sales. Founders who go public and immediately sell large equity stakes signal a different narrative than founders who maintain concentrated positions. The market interprets massive founder liquidation as a withdrawal of confidence—the message: "We've won, we're taking chips off the table, and we're less invested in what comes next."

The Schlacks' decision to maintain concentrated ownership (with voting supermajority intact) communicated the opposite narrative: "We believe in the next chapter of this company. We're not harvesting today's value; we're betting on future value creation."

Wealthfront's Different Capital Allocation Story

Wealthfront had a more distributed ownership structure coming into the IPO, with early venture capital backers including Tiger Global, Index Ventures, and Ribbit Capital taking significant liquidity at the IPO. This is entirely normal and legitimate—venture investors expect IPO-stage exits and recapitalization. However, the broader narrative was different.

Wealthfront didn't have a founder-led structure in the traditional sense (the company was founded by Adam Nash and Alyssa Auerbach, though leadership evolved over time). The absence of a concentrated founder position meant there was no dominant insider whose post-IPO share holdings would signal conviction about future value creation.

From an investor perspective, seeing primary insiders and early venture backers take simultaneous liquidity creates psychological unease. It suggests the company has reached a natural inflection point—growth is moderating, profitability is excellent, the investment has been realized—and now it's a question of executing a mature business rather than scaling toward dramatic upside.

The Behavioral Finance of Founder Signaling

This distinction touches on behavioral finance principles that sophisticated investors understand intuitively: founder actions speak louder than founder words. Management presentations can claim any strategy. However, personal capital allocation decisions reveal actual conviction.

When a founder maintains majority control and concentrated ownership post-IPO, investors observe that the founder is willing to bet personal wealth on future stock price appreciation. Conversely, when founders diversify holdings or take liquidity, investors observe that founders prefer diversification over concentrated upside. Neither decision is "wrong," but each communicates different information.

Equipment Share's founder positioning communicated: "We believe we can build substantial incremental value post-IPO. We're willing to maintain concentrated voting control and personal wealth concentration to ensure we can execute our vision." This resonated with investors seeking founder-led growth narratives.

Wealthfront's positioning communicated: "We've built something valuable. We've achieved profitability. Early investors have realized returns. Let's optimize this business for reliable cash generation." This narrative appeals to certain investors but disappoints those seeking founder-led growth momentum.

The Schlacks brothers' positioning made more sense for an IPO: founder control + founder conviction + founder concentration = narrative momentum for post-IPO growth. Wealthfront's more distributed structure made sense for an operational holding company narrative but didn't inspire IPO-era excitement.

Lesson 5: The "Tech Company Inside an Industry" Premium—Innovation Over Traditionalism

The Narrative Transformation Strategy

Equipment Share operates what, on surface inspection, seems like a decidedly unsexy business: equipment rental. Excavators, bulldozers, compressors, aerial lifts. The company manages inventory, handles logistics, coordinates maintenance, and executes typical rental operations that have defined construction equipment rental for decades.

Yet the way Equipment Share positions itself to investors—and the way investors receive the company—treats it as a software and technology company that operates equipment rental as its go-to-market channel. This reframing proves crucial to understanding the IPO outcome.

Equipment Share emphasizes its T3 platform: an integrated software system providing real-time equipment tracking, predictive maintenance analytics, remote access control, and fleet optimization across its 235,000+ pieces of equipment. The platform generates data about equipment utilization, maintenance patterns, and customer behavior. This data feeds machine learning models improving predictive maintenance accuracy and reducing downtime.

For contractors, the T3 platform becomes increasingly indispensable. Contractors get equipment insights that help them optimize job site operations, predict equipment failures before they disrupt projects, and manage fleet costs more effectively. The software moat deepens as Equipment Share accumulates proprietary data about equipment performance patterns, contractor usage patterns, and market trends.

From an investor perspective, this positioning matters enormously. A traditional equipment rental company competes on inventory, geographic coverage, and customer service. Profitability depends on utilization rates, pricing power, and operational efficiency. The business is fundamentally cyclical and commoditized.

A software-driven equipment platform company operates with fundamentally different economics. Technology creates competitive advantages, data creates network effects, and software can scale without proportional cost increases. The business appears less cyclical because software revenue streams exist independently of equipment utilization.

Wealthfront's Innovation Positioning Gap

Wealthfront operates in fintech—a sector explicitly defined as combining finance and technology. The company should theoretically benefit from strong "tech inside financial services" positioning. Yet the IPO outcome suggests Wealthfront struggled to maintain that positioning.

Wealthfront's core business involves robo-advisory algorithms—technology for asset allocation and automated rebalancing. This is genuine innovation that creates value for customers. However, the market positioning challenge emerges: technology-based robo-advisory already exists at Schwab, Fidelity, and Vanguard. Wealthfront didn't invent robo-advisory; the company implemented robo-advisory exceptionally well and brought it to market first at scale.

Furthermore, Wealthfront's public narrative increasingly centered on profitability and cash management spreads—financial services business model elements, not technology innovation. The company began sounding like a financial institution that happens to use software rather than a software company that operates in financial services.

Equipment Share, by contrast, emphasized T3 platform capabilities, data analytics, machine learning, and technology-enabled competitive advantages. Even though equipment rental is distinctly unsexy, the technology overlay transformed the narrative into an innovation story.

The Competitive Moat Perception

Sophisticated investors assign substantially higher valuations to companies with durable competitive moats. Technology-based moats—proprietary algorithms, network effects, data-driven advantages—command premium valuations. Cost-based moats and brand-based moats receive lower premiums.

Wealthfront's robo-advisory algorithms are good, but they're not uniquely defensible in the way machine learning models can become. Competitors can build equivalent algorithms. The company's competitive moat rests more on brand and customer acquisition advantage than on unsustainable technological superiority.

Equipment Share's T3 platform, conversely, becomes more defensible as it accumulates proprietary data about equipment performance and customer behavior. Competitors can build equivalent functionality, but they cannot access Equipment Share's accumulated data about 235,000+ pieces of equipment across multiple customer segments. The moat deepens with every additional data point.

Investors paying attention during IPO roadshows would have heard Equipment Share emphasize: "We are becoming a technology platform company that operates in equipment rental." They would have heard Wealthfront emphasize: "We are a profitable financial services company with strong margins." One narrative inspires technology investors and venture-oriented institutional funds. The other appeals to financial services-oriented investors and value funds.

For an IPO-stage company, attracting growth-oriented technology investors matters more than attracting value-oriented financial services investors. Technology investors drive momentum, generate media coverage, and establish higher valuation multiples. Wealthfront failed to maintain strong positioning as a technology-first story, and the market responded accordingly.

As interest rates decline from 200 to 50 basis points, Wealthfront's revenue from interest spreads is estimated to decrease significantly, highlighting its dependency on Federal Reserve policies. Estimated data.

The Interest Rate Environment: A Macroeconomic Case Study in Risk

Timing the Rate Cycle

Wealthfront's IPO timing proved spectacularly unfortunate relative to emerging macroeconomic trends. The company went public in December 2025, at the precise moment the Federal Reserve began signaling serious commitment to reducing interest rates through 2026. Market participants understood that rate declines of 100-200 basis points were likely over the following 12-24 months.

For a company generating 75% of revenue from interest rate spreads, this timing created an immediate valuation challenge. IPO investors project forward-looking cash flows and discount them to present value. When investors understand that a primary revenue stream will decline significantly in coming quarters, they naturally discount the company's valuation. The stock's 30% decline from IPO price reflected nothing more than forward-looking rate expectations crystallizing into the valuation.

Equipment Share's January 2026 IPO timing proved advantageous by comparison. While construction cycles are similarly cyclical and unpredictable, the company had better visibility into construction trends and provided more conservative guidance. Moreover, Equipment Share faced no equivalent macro headwind like rising rate sensitivity.

The Case Against Macro-Dependent Revenue

The investment lesson extends beyond Wealthfront's specific situation. Companies deriving significant revenue from macro-dependent sources face structurally lower valuation multiples than companies with comparable revenue from micro-based (customer-driven) sources. This principle applies across industries:

- Currency exposure: Companies earning revenue in foreign currencies face lower valuations than companies earning in domestic currency, all else equal, because forex volatility is uncontrollable.

- Commodity price exposure: Businesses dependent on commodity prices receive lower multiples because commodity prices are exogenous to business execution.

- Interest rate sensitivity: Financial services companies generating significant revenue from interest rate spreads receive lower multiples than companies with fee-based revenue streams.

- Energy or commodity market dependency: Businesses whose profitability depends on oil prices, metal prices, or agricultural commodity prices face valuation discounts relative to businesses with independent unit economics.

Investors can model macro-dependent businesses' likely performance ranges, but the valuation uncertainty justifies multiple compression. Wealthfront's investors faced this reality: the company's profitability could compress dramatically when rates decline, and no amount of operational excellence could offset macro headwinds.

Pre-IPO Due Diligence Failures

One wonders whether Wealthfront's bankers and advisors fully stress-tested the rate sensitivity scenario during pre-IPO preparation. A professional financial advisor would project interest rate scenarios and show investors how Wealthfront's profitability changes across rate environments. If bankers presented scenarios showing 30-40% profit margin compression under lower rate environments, sophisticated investors should have discounted the stock accordingly at IPO.

The stock's performance suggests either: (a) the due diligence process underestimated rate sensitivity, or (b) Wealthfront and its advisors misunderstood how sophisticated investors would weight macro risks. Either scenario represents a failure in IPO preparation.

Equipment Share, by contrast, probably emphasized construction cycle risks, capacity utilization risks, and pricing power risks. By front-loading risk communication, the company reset investor expectations. Subsequent performance surprises were less likely to shock the market.

Market Dynamics and Investor Psychology in IPO Windows

The IPO Window Phenomenon

The concept of an "IPO window" reflects a real psychological phenomenon in capital markets. Investors experience cycles of appetite for newly public companies, driven by a combination of rational factors (market valuations, interest rates, earnings forecasts) and psychological factors (recent IPO performance, media narratives, portfolio manager performance pressure).

In late 2025 through early 2026, an IPO window opened—meaning institutional investors showed renewed appetite for newly public companies. The window doesn't mean all newly public companies perform well; it means investors actively evaluate IPO opportunities rather than ignoring them. An open window means an IPO can potentially succeed; a closed window means nearly all IPOs struggle.

Wealthfront went public when the window was opening but before investor appetite fully recovered. The timing was awkward—the window was cracking open but not yet fully welcoming. Equipment Share benefited from the window being more fully open by late January 2026.

Narrative Arc and Market Reception

Beyond macro timing, the companies' narrative positioning influenced investor psychology. Equipment Share offered a compelling narrative arc: a founder-led company, operating in an unsexy industry, that applied technology to drive competitive advantages. The narrative includes expansion opportunities, margin expansion opportunities, and scale dynamics. Investors can envision a 10-year trajectory where the company compounds value through technology and scale.

Wealthfront's narrative arc proved less compelling: a profitable fintech company with strong margins... that will face margin compression when rates decline. The narrative doesn't include obvious optionality or expansion vectors that drive additional value. Investors might envision a 10-year trajectory where the company generates stable cash flows but doesn't substantially compound value beyond starting point.

From an IPO psychology perspective, Equipment Share's narrative aligns with investor desires for growth optionality and expansion potential. Wealthfront's narrative aligns with investor desires for stability and profitability—but those desires carry lower valuation multiples.

The Fintech Headwinds: Category-Specific Challenges

Fintech's Valuation Crisis

Wealthfront's IPO slide should be contextualized within broader fintech valuation pressures that emerged in 2024-2025. Fintech as a category faced multiple headwinds:

- Incumbent competition intensification: Major banks and investment firms upgraded digital capabilities, making fintech startups' differentiation harder to maintain

- Regulatory pressure: Fintech regulations matured, increasing compliance costs and reducing competitive advantages

- Profitability expectations: Investors demanded profitability before scale, constraining growth investments

- Interest rate sensitivity: As discussed, fintech business models showed systematic vulnerability to rate cycles

- Narrative exhaustion: The "fintech disruption" narrative saturated investor consciousness; new fintech stories struggled to generate excitement

Wealthfront faced these category headwinds in addition to company-specific challenges. The IPO decline partly reflected fintech sector trends, not Wealthfront execution failures.

Robo-Advisory's Mature Category Problem

Robo-advisory specifically—Wealthfront's core offering—became a mature product category by 2025. Schwab, Fidelity, Vanguard, and numerous other competitors offered sophisticated robo-advisory services. The category's differentiation points narrowed. Customers chose between providers based on fee structures, user experience, and brand trust, not revolutionary innovation.

Wealthfront invented robo-advisory at scale and built a strong brand. However, by IPO time, the company operated in a mature category with numerous competitors. This positioning problem compounds over time: as categories mature, customer acquisition costs rise, churn risk increases, and innovation requirements increase. Equipment Share, conversely, operates in a less-saturated competitive environment for technology-enabled equipment rental platform solutions.

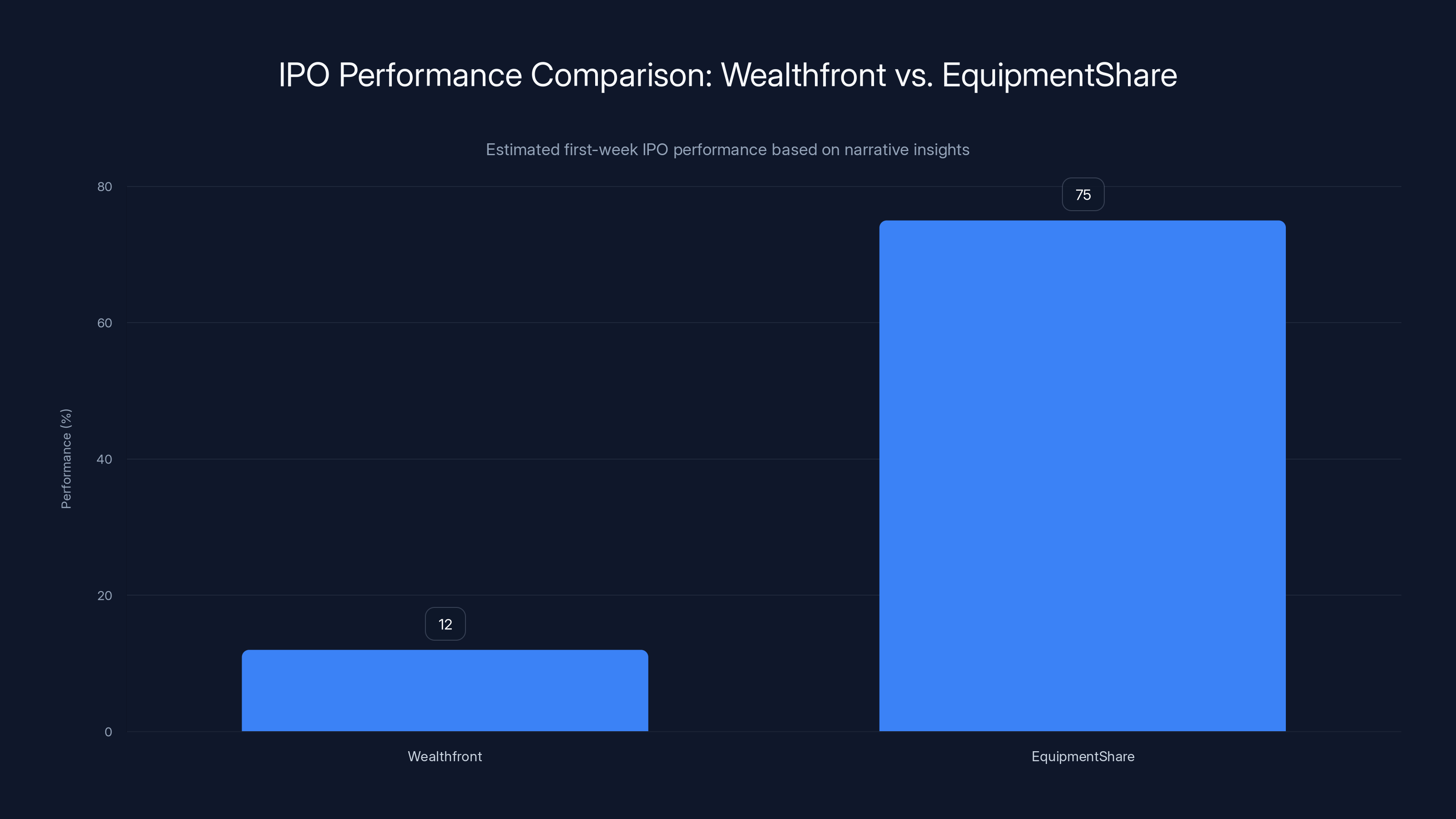

Estimated data shows EquipmentShare outperformed Wealthfront by 63 percentage points in first-week IPO performance, highlighting the importance of market positioning and revenue quality.

Organizational and Operational Factors Beyond Financials

Management Depth and Operational Clarity

Wealthfront's management team is experienced and capable, but the company's positioning reflects certain organizational realities. Wealthfront probably emphasized stability, profitability, and operational execution—metrics that appeal to operators and financial managers. Equipment Share's positioning emphasized growth optionality and technology innovation—narratives that inspire investors seeking founder-led growth companies.

These differences in tone and positioning reflect deeper organizational choices. A company emphasizing profitability and margin management is probably optimizing for steady-state cash generation. A company emphasizing growth optionality and technology innovation is positioning for continued scaling and value creation.

From an IPO perspective, demonstrating capability to scale creates more investor excitement than demonstrating capability to optimize. Both are valuable, but they appeal to different investor cohorts, and scaling narratives drive higher valuations.

Technology Differentiation Clarity

Equipment Share communicated clear technology differentiation: the T3 platform, predictive maintenance capabilities, real-time tracking, and data analytics. Investors could understand specifically how technology created competitive advantage.

Wealthfront's technology differentiation—robo-advisory algorithms and portfolio optimization—is real but familiar. Investors already understand robo-advisory exists at competitors. Articulating specific technology advantages above existing robo-advisory platforms from Schwab or Fidelity proved challenging in IPO communications.

This reflects a fundamental challenge in fintech IPOs: demonstrating innovation in a category where multiple credible competitors already deployed similar technology. Equipment Share faced no equivalent challenge—few existing equipment rental companies offer sophisticated T3-equivalent platforms.

What This Means for Future IPO Preparation

Pre-IPO Risk Assessment Framework

Companies approaching IPO should conduct thorough risk assessment specifically focused on factors that influence institutional investor psychology:

Macro Risk Assessment: Model your business across 3-5 macroeconomic scenarios. If profitability or growth varies significantly across scenarios, expect valuation multiple compression. Companies should specifically model interest rate scenarios, economic growth scenarios, and industry-specific cycle scenarios.

Revenue Quality Assessment: Categorize your revenue streams by durability. Recurring, customer-driven revenue generates premium multiples. Macro-dependent, cyclical, or trend-dependent revenue generates discount multiples. Companies with more than 50% revenue from Tier 4 sources should address this proactively in IPO communications.

Competitive Position Assessment: Clearly articulate your position in the competitive landscape. Are you operating in a mature, saturated category where differentiation is marginal? Or are you operating in a growth category where competitive positions remain unsettled? Position yourself accordingly in IPO communications.

Founder Positioning Assessment: Define whether you're positioning as a founder-led growth company or as an operational/financial services company. These require different capital structures and different founder involvement levels post-IPO. Equipment Share's founder control positioning made sense for a growth narrative. Wealthfront's distributed ownership made sense for a financial services narrative.

Technology Moat Assessment: Articulate specifically what technology differentiation exists and how that differentiation widens over time as you accumulate proprietary data or user networks. Generic statements about "advanced algorithms" or "sophisticated systems" won't convince experienced technology investors.

Timing Consideration Framework

Wealthfront's December 2025 timing proved suboptimal relative to emerging macro trends. Conversely, Equipment Share benefited from January 2026 timing when the IPO window was more fully open.

Companies should consider whether broader market conditions align with their specific business dynamics. Going public when: (1) your growth category is in favor, (2) macro trends support your revenue model, (3) investor appetite for your sector is high, and (4) your competitive position is clear creates dramatically different outcomes than going public when conditions are less favorable.

Wealthfront's bankers probably pushed for a December 2025 IPO to capture the year-end window. However, the timing proved unfortunate relative to early 2026 rate expectations. Companies should be willing to defer IPO timing if macro conditions are misaligned with business fundamentals.

Valuation Multiples and the Equity Narrative

Multiple Compression in Macro-Sensitive Businesses

The mathematics of valuation prove useful for understanding the IPO outcomes. Imagine two companies with identical

A financial services company with stable-to-declining growth and significant macro sensitivity might receive a 2-3x revenue multiple on IPO, valuing the company at

Wealthfront likely anticipated a higher revenue multiple—perhaps 6-8x—based on profitability and growth rates. When institutional investors applied a lower multiple (perhaps 3-4x) based on macro sensitivity, the gap between expected and realized valuations created disappointment and selling pressure.

Revenue Quality Impact on Multiples

Two companies with $400 million in revenue receive different valuation multiples based on revenue source:

- **SaaS company with 3.2-4.8 billion valuation

- Financial services company with 100M fees: Typical multiple 3-4x revenue = $1.2-1.6 billion valuation

- **Equipment rental company with 1.6-2.4 billion valuation

The revenue quality framework directly translates into valuation multiple frameworks. Companies deriving substantial revenue from Tier 4 (macro-dependent) sources should expect lower multiples. Understanding this framework helps companies optimize their business model and positioning for higher valuations.

Wealthfront probably didn't fully communicate to potential IPO investors that 75% of revenue came from interest-sensitive sources. Alternatively, the company communicated this fact, but investors underweighted it until macro trends made the risk suddenly tangible. Either scenario created a gap between expected and realized valuations.

Wealthfront's strong net income contrasts with EquipmentShare's strategic losses. EquipmentShare's focus on operating profit and EBITDA highlights its growth strategy.

Sector-Specific Lessons from the Equipment Rental Category

Construction Cycle Resilience

Equipment Share's business benefits from certain structural advantages within the construction equipment rental category. First, construction activity exhibits different cycle patterns than financial services. Construction cycles lag economic cycles by 6-12 months, giving companies like Equipment Share better visibility into coming trends.

Second, equipment rental creates stickiness through operational integration. When a contractor has integrated Equipment Share's T3 platform into job site operations, switching to a competitor creates operational disruption. This stickiness translates to more predictable cash flows and higher customer lifetime value.

Third, inflation in construction costs creates natural price increase opportunities. When construction material costs inflate, contractors accept corresponding increases in equipment rental costs because the rental cost remains small relative to total project cost. This pricing power protects margins during inflationary periods.

Wealthfront faces none of these advantages. Interest rate changes are outside management control, competitive differentiation is marginal in a mature category, and pricing power is limited by competition from larger, better-capitalized fintech and financial services providers.

Asset-Heavy Business Model Paradox

Equipment Share's asset-heavy business model (owning and maintaining 235,000+ pieces of equipment) might seem like a disadvantage compared to Wealthfront's asset-light model. However, the asset base created several advantages for IPO valuation:

- Tangible assets support debt financing, reducing dependence on equity for growth capital

- Physical assets create barriers to entry for competitors lacking manufacturing/procurement scale

- Maintenance and utilization data from owned assets feeds proprietary data advantages

- Asset fleet value anchors the company's balance sheet and justifies valuation through tangible asset backing

Wealthfront's asset-light model offers flexibility but provides less tangible backing for valuation narratives. The company's value rests entirely on customer relationships, brand, and algorithms—assets that are harder to value and more subject to competitive disruption.

Comparative Growth Strategy Implications

Expansion Vector Diversity

Equipment Share can pursue growth through multiple vectors: geographic expansion (new regions), vertical expansion (new equipment categories), customer size expansion (moving upmarket to larger contractors), and technology expansion (new platform capabilities). This diversity of expansion opportunities makes the company's growth narrative appear more sustainable.

Wealthfront's growth vectors prove more limited. The company can expand geographically and upmarket (managing larger customer asset bases), but the core business remains robo-advisory in wealth management—a mature, competitive category. Growth depends on winning share from entrenched competitors, not expanding addressable market through new verticals.

From an IPO perspective, demonstrating multiple growth vectors creates investor confidence that growth will continue regardless of specific market dynamics. A company dependent on a single growth vector faces higher execution risk and appears less attractive at IPO.

Market Share Dynamics

Equipment Share already possesses dominant market share (90% of Top 50 contractors) but operates in a fragmented overall market. The company can grow by expanding into smaller contractors, new geographies, or adjacent business categories. Market share gains come from market consolidation and category expansion, not pure category growth.

Wealthfront operates in a concentrated market with strong competitors. Market share growth requires winning share from Schwab, Fidelity, Vanguard, or other fintech competitors. Alternatively, growth comes from market expansion (growing the addressable market of people willing to use robo-advisory services), which slowed substantially by 2025.

Investors prefer growth from market expansion and consolidation (Equipment Share's position) over growth requiring share gains from entrenched competitors (Wealthfront's position). The strategic positions are reflected in valuation multiples.

Investor Psychology: What Moves the Needle on Day One

The First-Week Trading Volume Tell

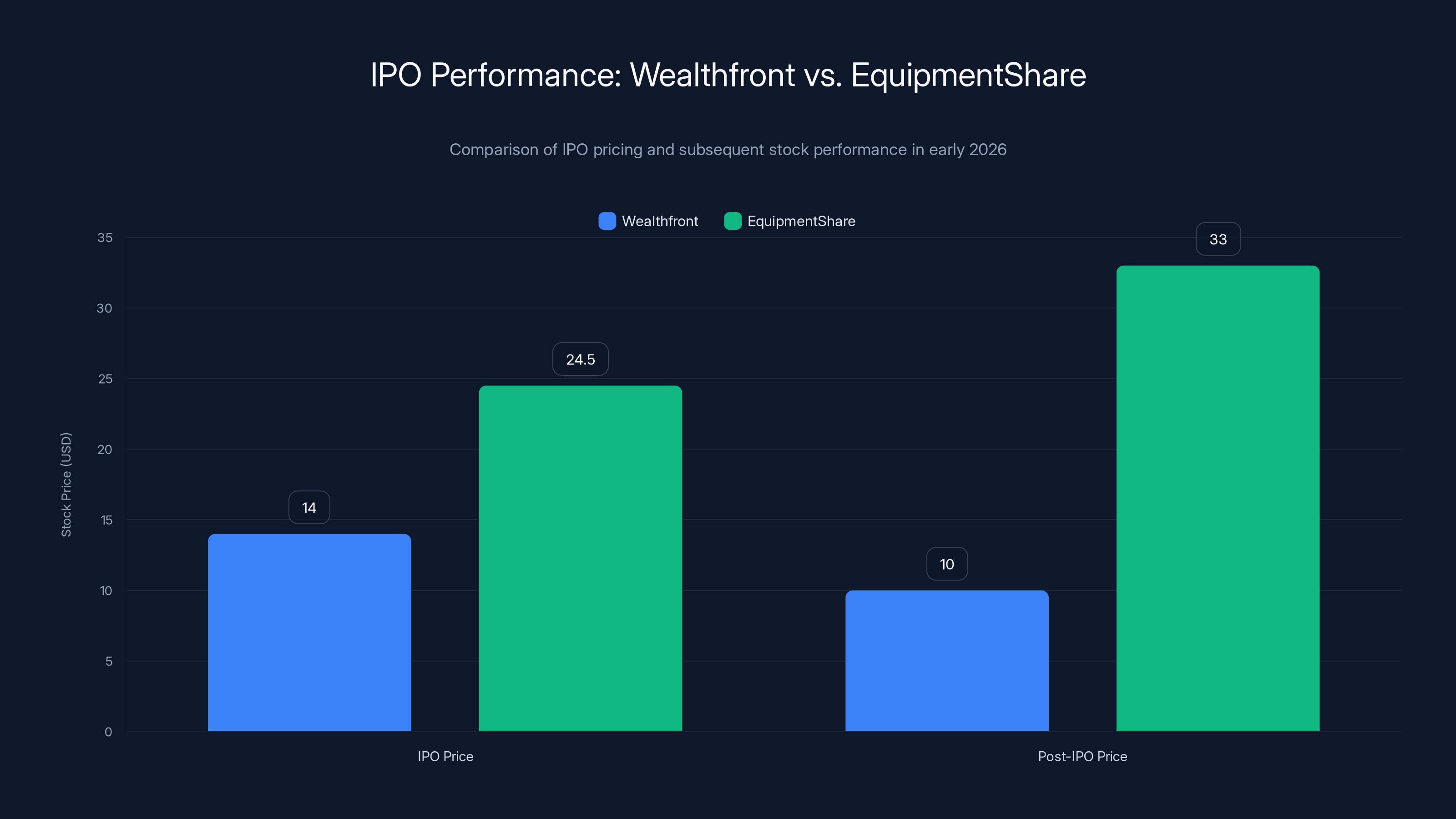

Equipment Share's 33% first-week pop wasn't driven by fundamental business surprises or unexpected profitability announcements. The stock moved higher because: (1) the IPO was underpriced relative to institutional investor demand, and (2) the market narrative aligned with investor appetite for founder-led growth companies operating in emerging technology categories.

Wealthfront's 30% decline from IPO price occurred despite profitability and strong financial metrics. The decline reflected: (1) the IPO was priced above institutional investor valuation frameworks, (2) the market narrative failed to inspire growth investor enthusiasm, and (3) macro risk factors (interest rate sensitivity) suddenly became salient.

These outcomes teach a crucial lesson: IPO pricing is less about fundamental valuation and more about matching investor appetite to company narrative. A perfectly priced IPO that misaligns with investor psychology will underperform. A slightly underpriced IPO that aligns with strong investor appetite will pop on day one.

Institutional Investor Cohort Preferences

Institutional investors segregate into different cohorts based on investment philosophy:

Growth Investors: Seek companies with high growth rates, founder-led positioning, and expansion optionality. They pay premium multiples for growth narratives. Equipment Share's positioning attracted growth investors.

Value Investors: Seek companies with strong profitability, mature business models, and stable cash generation. They pay lower multiples for stable cash flows. Wealthfront's positioning should have attracted value investors, but the macro risk factor undermined the appeal.

Technology Investors: Seek companies with sustainable technology moats, data advantages, and scaling software businesses. They pay premium multiples for technology leadership. Equipment Share's T3 platform attracted technology investors despite the equipment rental category seeming unsexy.

Sector-Specific Investors: Invest in specific sectors (fintech, construction, healthcare, etc.) based on sector theses. Wealthfront should have attracted fintech-focused investors, but fintech sector enthusiasm waned by late 2025.

The ideal IPO attracts multiple investor cohorts, creating diverse demand for shares. Wealthfront probably attracted primarily fintech investors and value investors. When fintech sentiment deteriorated and value investors recognized macro risks, demand dried up. Equipment Share attracted growth investors, technology investors, and infrastructure-oriented institutional investors, creating more diverse and resilient demand.

Despite Wealthfront's strong financials, its stock price fell by 30% post-IPO, whereas EquipmentShare saw a 33% increase, highlighting differing investor priorities.

Lessons for Developers and Technical Teams

The Build vs. Buy Decision in Platform Development

Wealthfront's reliance on third-party platforms (brokerages, custodians) for core infrastructure limited the company's technology differentiation. The company couldn't differentiate through superior brokerage or custodian capabilities; those functions are outsourced to regulated financial institutions.

Equipment Share, conversely, built proprietary technology (T3 platform) for core operations. This build decision created sustained competitive advantage and proprietary data collection. The infrastructure technology became a core business differentiator.

For technical teams approaching IPO, this distinction matters enormously. Companies that outsource technology critical to their value proposition face valuation challenges. Companies that build proprietary technology and accumulate proprietary data gain sustained competitive advantages that justify premium valuations.

Data and Analytics as IPO Narrative

Equipment Share's discussion of T3 platform capabilities, predictive maintenance analytics, and machine learning models impressed investors. These discussions signaled that the company was building sustainable technology advantages.

Wealthfront's robo-advisory algorithms, while sophisticated, are less exciting to investors because the category is mature and competitors deployed similar capabilities years prior. The company lacked obvious data advantages or machine learning innovations that would generate sustained competitive moats.

For technical teams, the lesson is direct: build and communicate proprietary data collection capabilities that generate machine learning and analytics advantages. Companies that accumulate proprietary datasets and apply machine learning to solve customer problems inspire institutional investor confidence. Companies with good algorithms but no proprietary data advantage face valuation challenges.

Broader Context: The 2025-2026 IPO Market

IPO Market Conditions and Volume

The IPO market reopened in late 2025 after a challenging 2024 period when public market volatility and higher interest rates suppressed IPO activity. The Wealthfront and Equipment Share IPOs occurred within a window of renewed IPO activity, but conditions remained uncertain. Investors were testing waters cautiously, not rushing to underwrite every IPO opportunity.

This cautious environment meant IPO companies had to earn investor enthusiasm rather than simply benefiting from broad market appetite. Wealthfront and Equipment Share competed for institutional investor attention within a moderately receptive IPO window. Both companies had opportunities, but one positioned itself more effectively for the market's actual preferences.

Comparable Company Valuations

Context about other recent IPOs helps explain investor behavior toward Wealthfront. By late 2025, investors had observed that Figma—a high-growth, venture-backed software company—was trading below its IPO price despite strong growth metrics. This suggested that even glamorous tech companies faced valuation headwinds. In this environment, Wealthfront's fintech positioning didn't automatically generate premium valuations.

Conversely, companies with strong profitability, tangible assets, and construction/infrastructure exposure (like Equipment Share) benefited from institutional investor preferences for value and durability during uncertain times.

Strategic Implications for Pre-IPO Founders and Management

The Narrative Matters More Than You Think

Wealthfront probably believed its financial metrics would speak for themselves. $339 million in revenue, 36% net margins, 40%+ growth—these numbers appeared compelling. However, the numbers alone failed to overcome narrative concerns about macro sensitivity and mature market competition.

Equipment Share understood that narrative positioning would influence IPO success. The company positioned itself as a technology platform transforming an unsexy industry, with founder-led conviction and expansion optionality. The narrative attracted investors despite the category seeming less exciting than fintech.

For pre-IPO companies, the lesson: invest substantially in narrative development and messaging strategy, not just financial optimization. Your financial metrics matter, but they matter within the context of the story you tell about future value creation.

The Macro Risk Communication Problem

Wealthfront either underestimated macro risk sensitivity or failed to communicate it effectively. Sophisticated investors should have recognized the interest rate exposure, but perhaps the company's presentation downplayed the risk. Alternatively, Wealthfront's management believed rate declines were unlikely and positioned conservatively based on that belief.

The lesson: quantify and explicitly communicate macro risk factors to investors, rather than hoping they won't notice. Companies with macro-dependent revenue should model scenarios, show investor sensitivity analysis, and explain explicitly why the company can thrive across multiple scenarios. Failing to address obvious risks invites investor skepticism.

Equipment Share probably communicated construction cycle sensitivity explicitly, which reset investor expectations. When actual performance varies from expectations, the market's reaction is more muted.

Timing and Window Selection

Wealthfront likely faced pressure from bankers to complete the IPO before year-end 2025. Companies often prioritize closing an IPO before calendar year-end for tax and accounting reasons, regardless of actual market conditions. This decision proved costly when macroeconomic expectations shifted toward lower rates in early 2026.

The lesson: defer IPO timing if market conditions don't align with company fundamentals. Going public in a moderately receptive window with suboptimal conditions is riskier than waiting for conditions to improve. The cost of deferring an IPO six months is typically lower than the cost of going public at the wrong time and having your stock decline 30% immediately.

The Broader Significance: What This Tells Us About Public Market Maturation

Sophistication in Investor Analysis

The divergent IPO outcomes demonstrate that institutional investors have become sophisticated at disaggregating financial metrics and assessing business quality. Wealthfront's 36% net margin and strong profitability provided less protection than the company probably anticipated because investors looked beyond headline numbers to assess revenue quality, macro sensitivity, and competitive positioning.

This sophistication will continue increasing. IPO-stage companies can no longer assume that strong profitability will generate strong IPO reception. The market will assess:

- Revenue durability: Is this revenue sustainable across multiple scenarios?

- Competitive positioning: Have you won your category or are you fighting for relevance?

- Macro sensitivity: What external factors could threaten profitability?

- Growth sustainability: Can growth continue at current rates, or does the company face natural deceleration?

- Founder conviction: Are insiders betting on future value or harvesting current value?

Companies that can address these questions clearly will receive premium valuations. Companies that cannot address these questions will face valuation discounts.

The Fintech Category Reassessment

Wealthfront's IPO challenges reflect broader reassessment of fintech within institutional investor portfolios. The sector experienced tremendous hype and capital allocation in 2020-2023. By 2025, investors recognized that: (1) incumbent financial services companies upgraded digital capabilities, (2) profitability proved harder to achieve than anticipated, (3) regulatory compliance became more expensive, and (4) many fintech innovations weren't as revolutionary as initially believed.

This reassessment doesn't mean fintech companies can't go public successfully. However, fintech companies need to demonstrate clearer competitive advantages and more durable business models than simply offering digital alternatives to incumbent services.

The Non-Tech Tech Company Premium

Equipment Share's success illustrates that institutional investors will pay premium valuations for "non-traditional technology companies"—companies operating in unsexy industries but using sophisticated technology to create competitive advantages. This trend reflects investor recognition that sustainable technology moats aren't limited to software-first companies; they exist wherever proprietary data, algorithms, and systems create advantages.

This trend will accelerate as investors seek sustainable competitive advantages outside the increasingly saturated software category. Construction tech, manufacturing tech, transportation tech, and other "industry tech" will see increasing investor appetite, particularly when founders demonstrate how technology creates sustainable moats.

FAQ

What were the primary reasons for Wealthfront's IPO decline?

Wealthfront's stock declined approximately 30% from its $14 IPO price primarily due to three factors: (1) approximately 75% of the company's revenue derives from interest rate spreads on customer cash accounts, creating vulnerability to Federal Reserve rate reduction expectations; (2) the company operates in the mature robo-advisory category where differentiation is limited compared to larger competitors like Schwab and Fidelity; (3) advisory fee growth remained modest at only 10% year-over-year, suggesting limited core business expansion momentum. The company's profitability metrics were strong (36% net margins), but institutional investors focused on revenue quality and macro sensitivity rather than headline profitability numbers.

What made Equipment Share's IPO more successful than Wealthfront's?

Equipment Share's 33% first-week gain reflected several positioning advantages: (1) the company positioned itself as a technology platform company operating in equipment rental rather than as a traditional rental provider, emphasizing its T3 platform with predictive maintenance and data analytics capabilities; (2) founder control with 81% voting power signaled founder conviction about future value creation; (3) the company's $4.4 billion revenue base demonstrated market leadership position with over 90% penetration among Top 50 general contractors; (4) the company demonstrated profitability across multiple years while maintaining aggressive growth investments, suggesting business resilience across various scenarios; (5) equipment rental revenue exhibits different cycle patterns than interest-dependent fintech revenue, reducing exposure to single macroeconomic variables.

How does revenue quality differ between Wealthfront and Equipment Share?

Revenue quality categorizes based on durability and sustainability. Wealthfront's revenue split approximately 75% from interest rate spreads (Tier 4: macro-dependent) and 25% from advisory fees (Tier 2: customer-driven). Interest spread revenue is vulnerable to Federal Reserve policy decisions outside management control. Equipment Share's revenue derives from equipment rental (Tier 3: outcome-dependent on customer success) plus emerging platform subscription revenue (Tier 1-2: recurring). Equipment rental revenue depends on construction activity cycles but not on single macro variables. Tier 4 revenue typically receives 2-4x valuation multiple discounts compared to Tier 1 revenue for otherwise identical companies, which helps explain the IPO outcome divergence.

Why is founder control considered important in IPO valuation?

Founder control signals founder conviction about future value creation. When founders maintain voting supermajority (as Equipment Share's Schlacks brothers did with 81% voting control) and don't liquidate holdings at IPO, investors interpret this as evidence that founders believe substantial value will be created post-IPO. Conversely, when founders take substantial liquidity at IPO or don't maintain control, investors question founder conviction about future prospects. The signaling mechanism proves powerful because founders' personal incentives align with share performance, making founder actions more credible than founder words in investor communications.

What is the "Tech Company Inside an Industry" premium?

Institutional investors assign higher valuation multiples to companies that apply proprietary technology to create competitive advantages within traditional industries compared to traditional competitors lacking technology moats. Equipment Share benefited from positioning as a tech platform (T3 software system) operating in equipment rental rather than as a traditional rental company. This positioning justifies technology sector valuation multiples (higher) rather than equipment rental sector multiples (lower). The premium reflects investor recognition that technology creates sustainable competitive moats, proprietary data advantages, and scaling opportunities that traditional business models cannot match. Companies seeking IPO success should emphasize technology moats and data advantages even in non-traditional tech categories.

How should companies assess macro risk sensitivity before IPO?

Companies approaching IPO should model business performance across 3-5 macroeconomic scenarios including interest rate environments, economic growth rates, and industry-specific cycle scenarios. Specifically, companies should calculate how profitability, growth rates, and cash flows change if interest rates increase/decrease 100-200 basis points, if economic growth accelerates/decelerates, or if industry cycles shift. Companies deriving more than 50% of revenue from macro-dependent sources should explicitly communicate sensitivity analyses to investors. McKinsey's financial risk frameworks provide structured approaches for quantifying macro sensitivity. Failing to address obvious macro risks invites investor skepticism and valuation discounts.

What signals do investor institutions look for regarding business quality?

Sophisticated institutional investors assess business quality through multiple dimensions: (1) revenue durability - does the revenue persist across changing market conditions?; (2) competitive positioning - are you a category leader or fighting for relevance?; (3) growth sustainability - can current growth rates continue, or does the business face natural deceleration?; (4) founder conviction - are insiders maintaining wealth concentration post-IPO?; (5) technology moats - do you possess proprietary algorithms, data advantages, or systems competitors can't replicate?; (6) macro sensitivity - does business performance depend on factors outside management control?. Companies addressing these dimensions clearly in IPO communications tend to receive premium valuations.

How does interest rate sensitivity specifically affect fintech valuations?

Fintech companies generating revenue from interest rate spreads (the difference between rates paid to depositors and rates earned on invested capital) face structural valuation challenges. When Federal Reserve policy signals rate reductions, investors immediately discount expected cash flows because spread revenue will decline mathematically. Unlike profitability or growth metrics that management can influence through execution, interest rate sensitivity is exogenous to company control. Institutional investors typically apply 2-4x lower valuation multiples to fintech revenue 30%+ dependent on interest spreads compared to fintech revenue derived from management fees or subscription sources. Wealthfront's 75% interest-dependent revenue created significant valuation vulnerability once rate reduction expectations became clear.

What differentiates "founder-led growth narratives" from operational narratives in IPO positioning?

Founder-led growth narratives emphasize expansion optionality, technology innovation, market expansion opportunities, and founder vision for future value creation. These narratives appeal to growth investors and venture-oriented institutional funds willing to pay premium multiples for growth potential. Examples: Equipment Share's positioning emphasized founder-led scaling and platform expansion. Operational narratives emphasize profitability, cash generation, operational efficiency, and stable business model optimization. These narratives appeal to value investors and financial services-oriented institutional funds but typically command lower valuation multiples. Wealthfront's positioning emphasized operational maturity and profitability, which appeals to different investor cohorts than growth narratives. IPO success requires intentionally selecting between these narratives and committing to the positioning consistently throughout IPO communications.

Conclusion: Key Takeaways for Navigating IPO Success

The contrasting IPO outcomes of Wealthfront and Equipment Share—two companies separated by just six weeks but diverging by 63 percentage points in first-week performance—encapsulates lessons that extend far beyond these specific companies. The findings reveal fundamental shifts in how institutional investors evaluate companies approaching public markets, and what founders must understand to navigate the IPO process successfully.

The first and perhaps most important lesson centers on revenue quality over revenue quantity. Wealthfront's impressive profitability metrics and revenue scale proved insufficient because approximately three-quarters of revenue derived from interest rate spreads—a source entirely dependent on Federal Reserve policy rather than company execution. Sophisticated investors immediately recognized this vulnerability and discounted the company's valuation accordingly. The lesson applies broadly: all revenue is not created equal. Companies should audit their revenue sources, categorize them by durability, and address concentration risks before going public. Macro-dependent revenue commands lower valuations regardless of how profitable that revenue currently appears.

The second lesson involves competitive positioning and market domination. Equipment Share operated from a position of category leadership, with 90% penetration among Top 50 general contractors. This leadership position creates pricing power, expansion optionality, and natural defensibility. Wealthfront, conversely, competed in a mature category where larger, better-capitalized competitors offer equivalent products. The company's technology and user experience were strong, but they weren't sufficient to overcome the disadvantage of fighting for share in an established market. Companies should honestly assess whether they've won their category or are fighting for relevance, then position accordingly to investors.

The third lesson emphasizes founder signaling and capital allocation decisions. Equipment Share's founders maintained 81% voting control and didn't liquidate holdings at IPO—signaling conviction about future value creation. Wealthfront's more distributed ownership structure (with early venture capital backers taking liquidity) signaled a different narrative: "we've achieved profitability, early investors have realized returns, let's optimize the business." This narrative is legitimate but generates lower investor enthusiasm than founder-led growth stories. Companies approaching IPO should intentionally consider founder positioning and what their capital structure communicates about conviction.

The fourth lesson involves narrative positioning within your industry. Equipment Share reframed equipment rental—traditionally an unsexy, commoditized business—as a technology platform story through emphasis on T3 platform capabilities, predictive maintenance analytics, and data-driven competitive advantages. This positioning attracted growth and technology investors willing to pay premium valuations. Wealthfront, despite being in fintech (a theoretically more exciting category), positioned itself as a profitable financial services company, which attracted different investor cohorts and justified lower multiples. The lesson: how you position your business in investor communications matters as much as what your business actually does.

The fifth lesson focuses on macroeconomic timing and window selection. Wealthfront went public in December 2025, just as Federal Reserve policy expectations shifted toward rate reductions in 2026. This timing created an immediate valuation disconnect—the market understood that Wealthfront's primary revenue source would face significant pressure from the exact macro trends taking hold at IPO. Companies should carefully assess whether broader market conditions align with their specific business dynamics before committing to IPO timing. Deferring an IPO six months to wait for better market conditions typically costs less than going public at suboptimal timing and watching your stock decline 30% immediately.

For developers and technical teams within companies approaching IPO, the lesson emphasizes building proprietary technology moats rather than relying on outsourced platforms. Wealthfront's core capabilities depend on third-party brokerages and custodians for infrastructure. Equipment Share's T3 platform represents proprietary technology the company built and maintains, creating sustained competitive advantage. Companies that build and accumulate proprietary datasets, apply machine learning, and create technology competitors can't replicate will justify premium valuations. Conversely, companies that outsource technology core to their value proposition face valuation challenges regardless of other metrics.

The broader significance of these IPO outcomes extends to what they reveal about market maturation and investor sophistication. Institutional investors no longer accept simple narratives about profitability and growth. Instead, they conduct sophisticated analysis of revenue quality, macro sensitivity, competitive positioning, and business durability. Companies that can articulate clear answers to these analysis dimensions will receive premium valuations. Companies that cannot address these questions—or that hope investors won't notice problematic dynamics—will face valuation discounts.

For the broader technology and business community, these IPO outcomes signal that the era of "growth at all costs" has clearly passed. However, the counterbalance isn't "profitability at all costs." Instead, the market increasingly rewards sustainable value creation through competitive advantage, founder-led scaling, and business models demonstrating durability across multiple scenarios. This framework applies regardless of your company's industry, stage, or growth trajectory.

Companies approaching IPO readiness should conduct thorough self-assessment across these dimensions: revenue quality, competitive positioning, macro sensitivity, founder conviction, and technology moats. Where gaps exist, address them proactively through business model adjustments, narrative refinement, or timing deferrals. The investment to achieve true IPO readiness—not just financial readiness, but investor readiness—returns dividends far exceeding the costs.

Ultimately, Wealthfront and Equipment Share's diverging outcomes teach that IPO success depends less on absolute financial metrics and more on alignment between business fundamentals, market conditions, investor psychology, and narrative positioning. Companies that achieve alignment across these dimensions create value for shareholders. Companies that miss alignment watch their valuations compress regardless of operational quality. The challenge, and the opportunity, lies in understanding which dimension requires attention and addressing it before public markets render their verdict.

Additional Considerations for Growing Companies

Building Institutional Investor Relationships Pre-IPO

Successful IPOs benefit from pre-IPO relationship building with institutional investors. Wealthfront could have addressed investor concerns about macro sensitivity through investor education and presentation refinement. Companies should consider pre-IPO "investor education" campaigns, analyst briefings, and stakeholder presentations that give sophisticated investors early familiarity with company positioning.

Equipment Share probably benefited from pre-IPO relationship building that emphasized T3 platform capabilities and founder conviction. Investors who understand the company narrative before IPO day prove more likely to bid aggressively for shares and support the stock post-IPO.

The Role of Investment Banking and IPO Advisory

Investment banks play crucial roles in IPO preparation, including pricing strategy, investor roadshow messaging, and timing decisions. Wealthfront's IPO pricing at the top of the range (

Companies should thoughtfully evaluate whether maximizing IPO-stage capital raise justifies the risk of overpricing and subsequent stock decline. Sometimes IPO pricing slightly below market clearing rate creates momentum and positive investor sentiment that drives long-term shareholder value more effectively than maximizing the IPO fundraise.

Long-Term Value Creation vs. Day One Performance

This analysis focuses on short-term IPO performance (first-week trading, day-one investor reception). However, long-term shareholder value depends on company execution far more than first-week trading performance. Wealthfront's 30% decline might prove temporary if the company successfully navigates macro challenges or repositions its business model. Equipment Share's 33% pop might evaporate if the company fails to execute on expansion plans or faces unexpected competitive pressure.

The lessons about IPO positioning and market expectations remain valid for long-term value creation. However, companies should balance short-term IPO success (important for investor confidence and capital raising) with long-term business fundamentals (critical for actual value creation).

Looking Ahead: IPO Market Evolution

The 2025-2026 IPO outcomes suggest continued evolution in how institutional investors evaluate companies approaching public markets. We should anticipate:

Increased macro risk assessment: Investors will more systematically analyze how companies perform across different macroeconomic scenarios. Companies with concentration risk (like Wealthfront's interest rate exposure) will face systematic valuation discounts until they diversify revenue sources.

Technology moat emphasis: Investors will increasingly value technology defensibility, proprietary data, and machine learning advantages. Companies that articulate clear technology moats will justify premium valuations even in traditional industries.

Founder positioning clarity: Investors will continue using founder actions and positioning as signals of conviction. Companies with clear founder-led narratives and founder wealth concentration will attract more enthusiastic institutional investor reception.

Narrative-driven valuations: The gap between fundamental valuation and narrative-driven valuations will continue widening. Companies that tell compelling stories about future value creation will receive premium multiples regardless of current profitability. Companies with weak narratives will struggle with valuation despite strong fundamentals.

Non-traditional tech premium: Institutional investors will increasingly allocate to non-traditional tech companies applying technology to traditional industries. Construction tech, transportation tech, manufacturing tech, and other industry-specific technology companies will see increasing investor appetite.

Companies preparing for IPO in coming years should position themselves within these evolving investor expectations and preferences. The specific details of Wealthfront and Equipment Share's situations will evolve, but the underlying principles—revenue quality, competitive positioning, macro sensitivity, and narrative alignment—will remain fundamental to IPO success.

Key Takeaways

- Revenue quality matters more than revenue quantity: Wealthfront's impressive profitability was undermined by 75% revenue concentration in interest rate spreads (macro-dependent source), while EquipmentShare's equipment rental and platform revenue demonstrated greater durability

- Absolute scale creates optionality: EquipmentShare's 339M revenue requires constant competitive share-winning

- Profitability context must address investor questions: Rather than simply being profitable, investors ask 'can you be profitable when you choose to be?' EquipmentShare demonstrated this across multiple years; Wealthfront's recent profitability lacked similar proof

- Founder control and conviction signal future value: EquipmentShare's founders maintained 81% voting control and personal wealth concentration, signaling conviction; Wealthfront's distributed ownership suggested value realization rather than future scaling

- Non-traditional tech companies receive innovation premium: EquipmentShare's T3 platform transformed equipment rental narrative from commodity business to technology platform, justifying higher valuation multiples despite unsexy category

- Macro risk sensitivity creates systematic valuation discounts: Institutional investors apply 2-4x lower valuation multiples to companies with substantial macro-dependent revenue regardless of current profitability metrics

- Narrative positioning eclipses financial metrics: How companies position themselves (growth platform vs. profitable financial services) influences which investor cohorts bid for shares, determining first-week trading momentum

- Revenue diversity reduces valuation risk: Companies deriving 75%+ of revenue from single sources face concentration discounts; companies with diversified revenue tiers receive premium multiples for the same absolute revenue

- IPO timing relative to macro trends matters significantly: Wealthfront's December 2025 timing coincided with Fed rate reduction expectations, creating immediate valuation gap; EquipmentShare benefited from January 2026 timing with clearer macro positioning

- Technology moats attract premium institutional capital: Companies building proprietary data, machine learning capabilities, and systems competitors can't replicate justify higher multiples than companies relying on outsourced platforms

Related Articles

- How Elon Musk Is Rewriting Founder Power in 2025 [Strategy]

- The ARR Myth: Why Founders Need to Stop Chasing Unrealistic Growth Numbers [2025]

- Linq's $20M Series A: How AI Assistants Are Moving Into Messaging Apps [2025]

- Once Upon a Farm IPO 2025: What Investors Need to Know [2025]

- AI Labs' Reputation War at Davos: The Real Competition Behind the Scenes [2025]

- General Fusion's $1B SPAC Merger: Fusion Power's Survival Strategy [2025]</a