![Why America's $12B Mineral Stockpile Proves the Future Is Electric [2025]](https://tryrunable.com/blog/why-america-s-12b-mineral-stockpile-proves-the-future-is-ele/image-1-1770307945357.jpg)

Introduction: The Quiet Admission Hidden in $12 Billion

When the Trump administration announced a $11.7 billion critical minerals stockpile initiative earlier this year, most people saw it as political posturing. A show of strength against China. A response to trade wars and supply chain vulnerabilities.

But here's the thing: it's actually much more interesting than that.

Project Vault, as it's branded, reveals something the administration hasn't explicitly said. Something that contradicts years of rhetoric favoring fossil fuels and skepticism toward clean energy. The message hidden in that $12 billion commitment is unavoidable once you look at the data: the future economy runs on electricity, not oil.

This isn't speculation or wishful thinking from climate advocates. It's now official policy acknowledgment, buried inside one of the largest commodity stockpile investments in modern U.S. history.

The comparison Trump himself made is telling. He tied this minerals reserve to the Strategic Petroleum Reserve, established in the 1970s after the OPEC oil embargo sent the U.S. economy into chaos. That reserve holds roughly 370 million barrels of oil worth about $20 billion at current prices. The new minerals initiative represents half that value for a market that's roughly 1% the size of global oil markets. On paper, the math looks absurd. Why allocate that much capital to such a small sector?

Unless, of course, that sector is about to become dramatically larger.

That's exactly what's happening. Demand for critical minerals—the cobalt, lithium, gallium, nickel, and rare earth elements that power batteries, semiconductors, and renewable energy infrastructure—is accelerating at rates that have caught even aggressive forecasters off guard. This stockpile isn't just about addressing today's supply constraints. It's a bet on the shape of tomorrow's economy.

And that matters more than any trade war or geopolitical posturing, because it means even administrations philosophically opposed to clean energy are being forced to invest in the infrastructure that enables it.

Let's dig into what's actually happening, why it matters, and what the mineral reserve tells us about where the global economy is really heading.

Understanding Critical Minerals: Why They Matter More Than Oil

What Are Critical Minerals and Why Do We Need Them?

Critical minerals aren't sexy. Nobody campaigns on them. They don't make headlines the way oil prices do. But they're far more essential to modern life than most people realize.

These are elements—cobalt, lithium, nickel, rare earth elements, gallium, aluminum, copper—that are essential for manufacturing everything from smartphone displays to wind turbine magnets. They're the backbone of clean energy infrastructure, semiconductor manufacturing, aerospace components, and medical devices.

Lithium is perhaps the most famous, especially after the battery boom. Cobalt is critical for battery chemistry and doesn't have easy substitutes. Rare earth elements are essential for permanent magnets used in wind turbines and electric vehicle motors. Gallium powers semiconductors and solar panels. There's no synthetic replacement for most of these. You either have access to them or you don't.

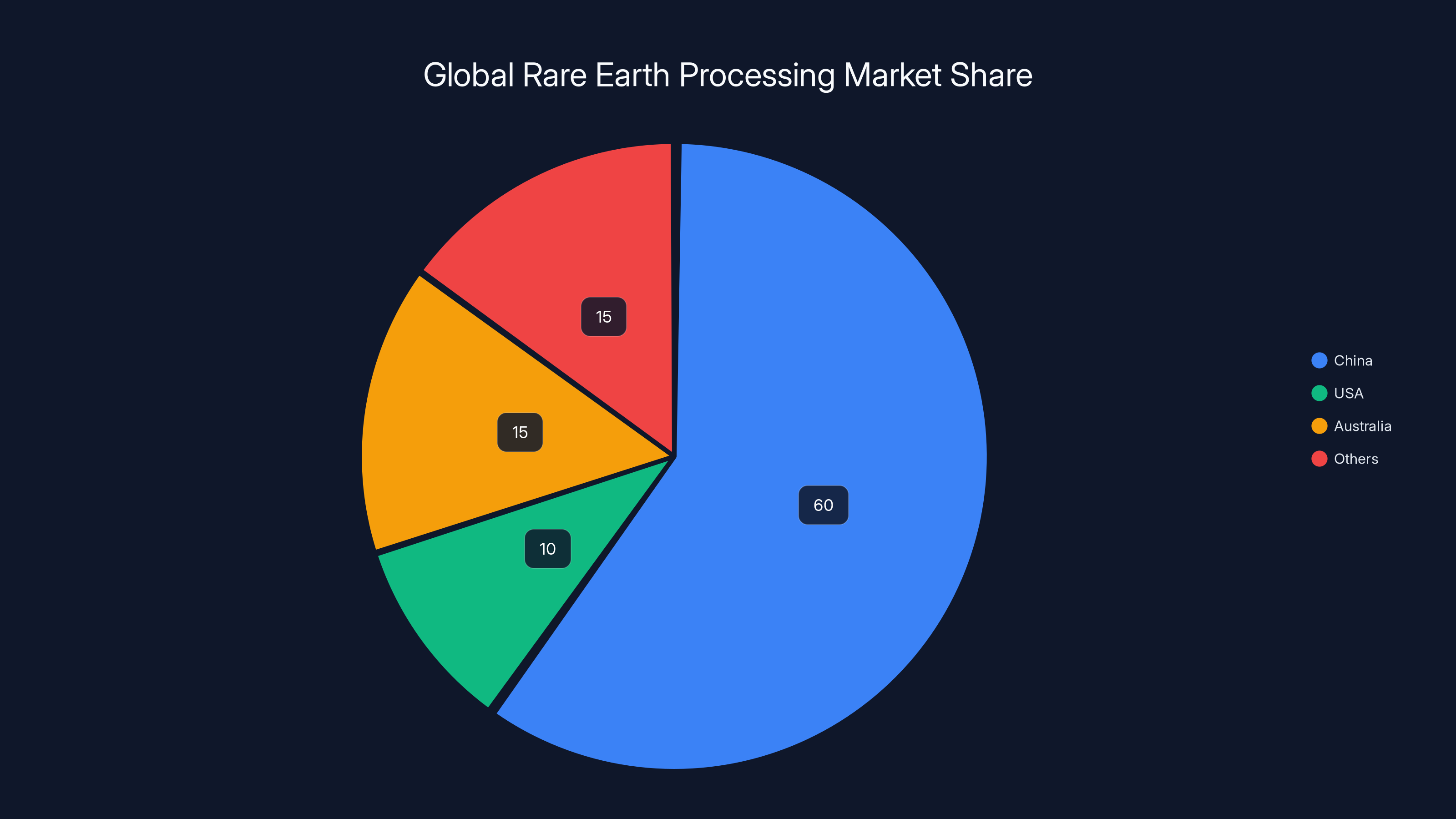

The difference between oil and critical minerals is fundamental. You can drill more oil. You can find new reserves. You can develop alternatives (electric vehicles, solar power, wind turbines). But critical minerals? You need actual geological deposits, mining infrastructure, and processing capability. They're concentrated in specific countries. China controls roughly 60% of global rare earth processing. Indonesia and the Democratic Republic of Congo dominate nickel and cobalt extraction, respectively.

This concentration creates vulnerability. It's not theoretical. In the past two years, we've seen it weaponized.

The China Factor: How One Country Controls Global Supply Chains

China doesn't just extract critical minerals. That would be impressive enough. China also refines and processes them, controlling the conversion from raw ore into usable material. That's where the real power lives.

In 2023 and 2024, as the Trump administration escalated trade tensions, China responded with what looked like economic judo. They didn't engage in direct confrontation. Instead, they restricted exports of rare earth elements and lithium-related materials. The message was subtle but unmistakable: we can make your economy stop working anytime we want.

America had options at that point. Limited options, but options. Ramp up domestic production. Negotiate. Develop substitutes. None of these move quickly. Mining projects take years to permit and build. Processing facilities require massive capital investment. Material science breakthroughs are uncertain.

The mineral stockpile approach is the fastest interim solution. You can't change geology overnight. You can't build a lithium mine in six months. But you can accumulate strategic reserves while longer-term production capacity is developed.

What makes this genuinely interesting is that the administration is doing it despite philosophical opposition to the technologies these minerals enable. That signals something important: market forces and geopolitical necessity trump ideology.

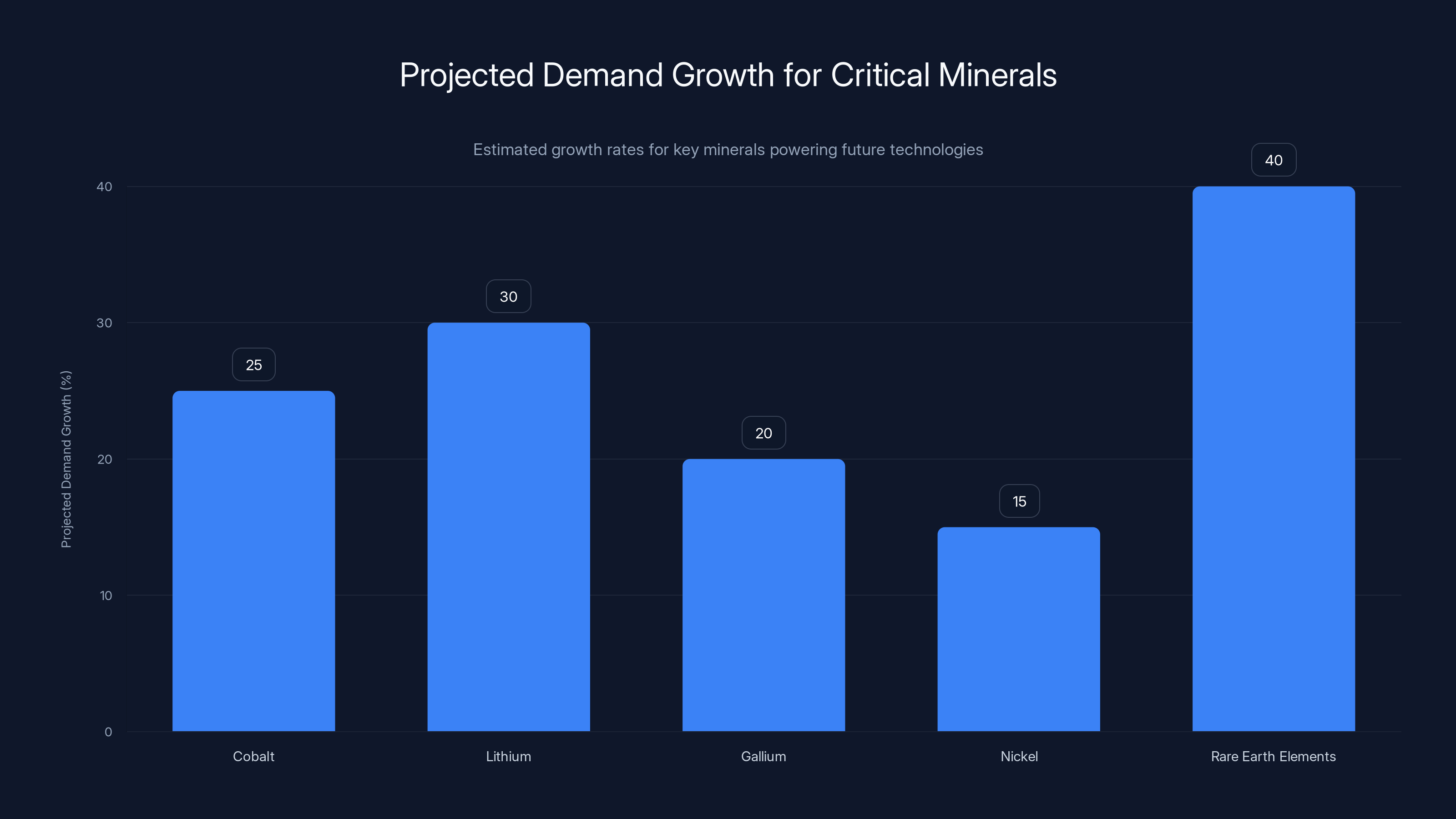

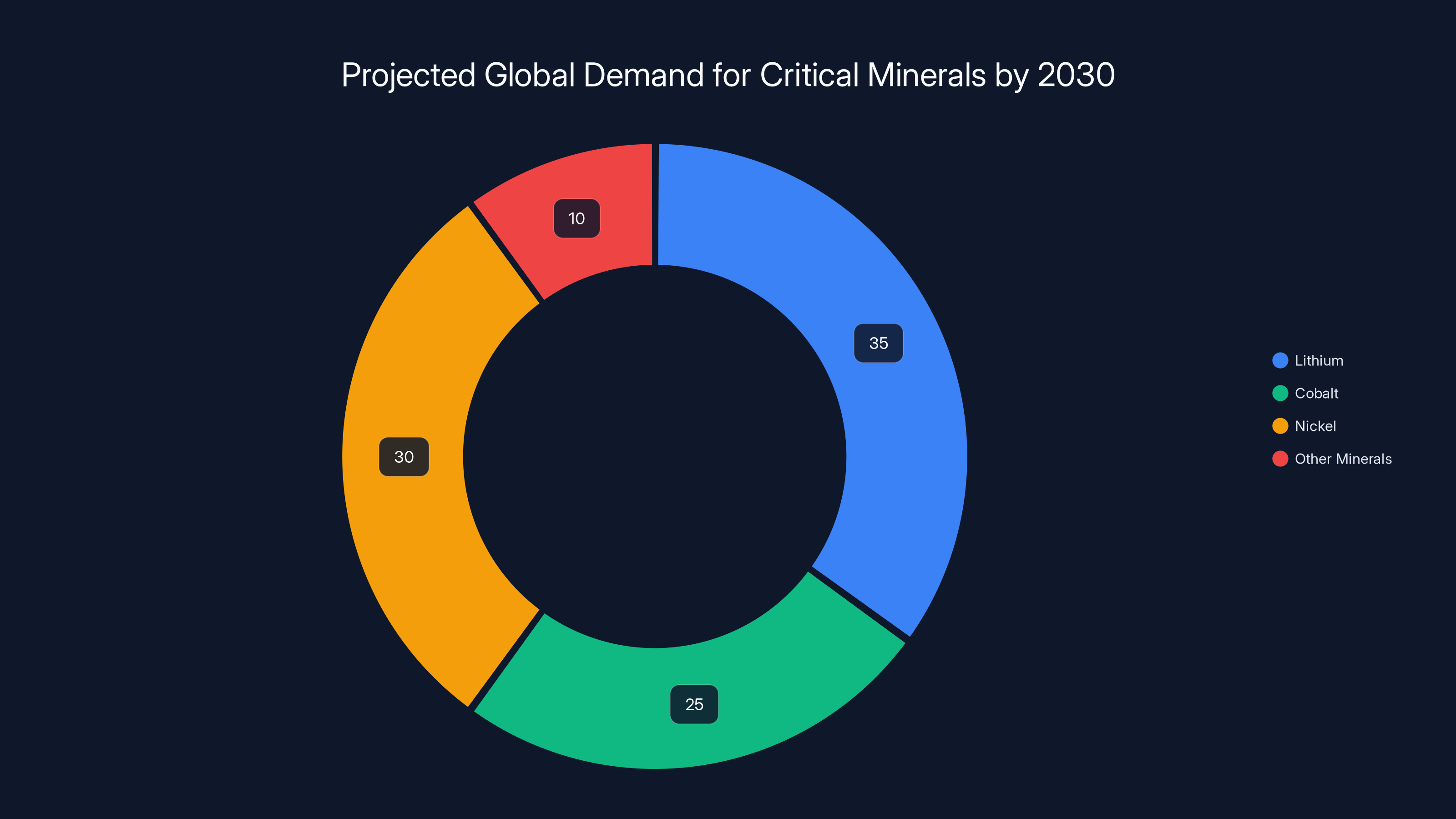

Estimated data shows significant projected demand growth for critical minerals, highlighting their increasing importance in future technologies.

The Electric Vehicle Acceleration: Driving Mineral Demand Through the Roof

EV Growth Is Outpacing Every Forecast

Electric vehicles are the primary driver of critical mineral demand growth. It's not close. Of the growth in rare earth element demand expected through 2050, more than half comes from electric vehicles and wind turbines. For cobalt and lithium specifically, electric vehicles represent the vast majority of growth.

The numbers are staggering. In 2020, global EV sales were around 3 million units. By 2024, that had more than doubled to over 8 million units. Plug-in hybrids add another 3-4 million to the total. In some markets, EV adoption is even more aggressive. In Norway, over 90% of new car sales are electric. In China, it's approaching 50%. Even the U.S., which lags in EV adoption compared to developed nations in Europe and Asia, saw over 10% of new car sales be electric in 2024.

This matters because a single electric vehicle requires roughly 8-10 kg of lithium, 15-20 kg of cobalt (though that's decreasing as battery chemistry improves), and significant quantities of nickel. An internal combustion engine car needs essentially none of these.

Multiply 8 million vehicles by 10 kg of lithium per vehicle. That's 80 million kilograms of lithium demand just from one year of vehicle production. And that's growing. Conservative forecasts suggest we'll see 15-20 million EVs produced annually by 2030. Aggressive forecasts suggest over 30 million.

That trajectory isn't discretionary. Car manufacturers have committed to it publicly. Regulatory frameworks mandate it (Europe's ICE phase-out, California's rules, China's new energy vehicle policies). The infrastructure is being built. Charging networks are expanding. Battery factories are coming online. This isn't a trend that might reverse. It's locked in by capital investment and policy.

Lithium and Cobalt: The Constraining Minerals

If critical minerals were equally constrained, the problem would be simpler. But they're not. Some are abundant and just need processing capacity. Others are geographically concentrated with real supply limitations.

Lithium is the tightest constraint right now. Global lithium production happens primarily in a geographic triangle: Australia, Chile, and Argentina. China also produces lithium, primarily from hard rock mining in Tibet. That's essentially it for economically viable production at scale.

Australia produces about 50,000 tons annually. Chile produces similar quantities. Argentina is ramping up and could produce significant volumes by 2027-2028. But even if all three countries maximize production, we're looking at maybe 800,000-1,000,000 tons globally by 2030. Battery manufacturers and mineral processors are currently consuming about 350,000 tons annually, with growth rates of 15-25% year-over-year.

The math is concerning. At current growth rates, we'll hit supply constraints by 2027 or 2028. That's when prices spike, when projects start getting delayed, when supply chains fracture.

Cobalt is similarly constrained, though for different reasons. The Democratic Republic of Congo accounts for about 70% of global cobalt production. That's geopolitical risk in a single data point. Cobalt mining in the DRC has serious human rights concerns, child labor problems, and environmental issues. That creates pressure to develop cobalt-free batteries and to diversify sourcing. Both are happening, but neither moves fast enough to eliminate cobalt demand.

These constraints are why the mineral stockpile matters. It buys time for production capacity to scale up. It reduces price volatility in the interim. It ensures that a supply disruption doesn't cascade into economic chaos.

China dominates the global rare earth processing market with a 60% share, highlighting its significant leverage in the supply chain. Estimated data.

Renewable Energy Infrastructure: The Secondary Driver of Mineral Demand

Wind Turbines Need More Minerals Than You'd Think

Wind turbines are less famous than electric vehicles, but they're driving comparable mineral demand growth. A single large wind turbine (3-5 megawatts) requires roughly 200-300 kg of rare earth elements for the permanent magnets in the generator. That's more than the total rare earth content in 50 electric vehicles.

Global wind capacity additions have been growing steadily. In 2023, roughly 75 gigawatts of new wind capacity came online globally. In 2024, that increased to over 90 gigawatts. Solar installations are even larger, though solar uses different materials (silicon, aluminum, copper).

The International Energy Agency projects that renewable energy (wind, solar, hydroelectric, geothermal) will account for over 50% of global electricity generation by 2035. That requires massive capital investment in generation infrastructure and energy storage systems. Every megawatt of renewable capacity built requires critical minerals.

Battery storage is emerging as another major mineral consumer. Grid-scale battery systems are necessary to manage the intermittency of wind and solar. A 100-megawatt-hour battery installation might consume 500+ tons of lithium and significant cobalt. Battery storage deployment is ramping from roughly 20-30 gigawatt-hours in 2023 to projections of 100+ gigawatt-hours by 2030.

The renewable infrastructure trend is geographically distributed unlike EV adoption. Wind projects are happening in the U.S., Europe, China, India, and increasingly in developing nations. Solar installations span every continent. That geographic diversity reduces supply chain bottlenecks compared to EV-concentrated demand but doesn't eliminate them.

Data Centers and the AI Infrastructure Boom

This is the second-order effect that most mineral demand forecasts underestimate. Artificial intelligence infrastructure requires massive computational capacity. Data centers require cooling systems, power distribution equipment, and semiconductor fabrication. All of these need copper, aluminum, gallium, and indium.

Datacenter power consumption is growing exponentially. Microsoft, Google, Amazon, and other cloud providers are building new datacenters specifically for AI workloads. NVIDIA GPUs require gallium nitride semiconductors. Custom silicon chips need rare earth processing. The infrastructure behind Chat GPT, Claude, and other AI systems is mineral-intensive.

This demand wasn't anticipated in earlier mineral forecasts. It's a second-order effect that's becoming first-order as AI infrastructure scales. Some analysts now estimate that AI-related semiconductor demand could add 10-15% to critical mineral consumption by 2030.

That changes the minerals equation. Suddenly, you have three massive demand drivers: electric vehicles, renewable energy infrastructure, and AI computing infrastructure. All three are scaling simultaneously. All three are accelerating faster than anyone predicted five years ago.

China's Strategic Dominance: Why the U.S. Feels Vulnerable

Extraction vs. Processing: Where Real Power Lives

America and other Western nations have significant mineral deposits. The U.S. has rare earth resources in California, Montana, and other states. Lithium exists in Nevada and California. Copper mining is domestic. So why is there panic about supply chains?

Because having minerals and being able to use them are different things.

China controls roughly 60% of global rare earth processing. That means taking raw rare earth ore and converting it into usable material. It's a complex, capital-intensive process with significant environmental impact. It requires specialized knowledge and infrastructure that took decades to build.

A rare earth mine in the U.S. produces ore. That ore gets shipped to China for processing. It comes back as usable material for manufacturers. That's not the optimal supply chain design, but it's what exists.

Changing this requires building domestic processing capacity. A new rare earth processing facility costs $1-2 billion and takes 5-7 years to build and permit. The U.S. government has funded a few small processing plants, but meaningful scale-up would require years and massive capital investment.

Lithium processing is somewhat simpler, which is why there's more optimism about domestic capacity. But even lithium refining takes time and capital. Chile and Argentina have decades of mining and processing experience. Scaling U.S. lithium production requires not just mining but also building the infrastructure to convert ore into battery-grade lithium.

China's advantage isn't just processing. It's also downstream battery manufacturing. China produces roughly 70% of global battery cells. CATL, BYD, and other Chinese manufacturers dominate production. They control the design of battery chemistry, cell architecture, and manufacturing processes. That gives them influence over mineral sourcing.

The 2023-2024 Export Restrictions: A Warning Signal

In 2023 and early 2024, as trade tensions escalated, China began restricting exports of rare earth elements and gallium. The restrictions were surgical. Not total bans, but enough to create uncertainty and tighten supply.

The message was unmistakable. Mess with us on trade, and we'll make your supply chains hurt. You need our minerals. You can't replace them quickly. We can wait longer than you can.

This created the political pressure for the mineral stockpile. It's not abstract strategic planning. It's direct response to demonstrated vulnerability.

The restrictions eventually eased after negotiations, but the damage was done. Western manufacturers realized they were genuinely dependent on Chinese supply chains for materials they couldn't quickly replace or substitute. That realization cascaded through policy circles. If China could do it with rare earths, they could do it with lithium or cobalt processing next.

That's the implicit threat that Project Vault is designed to address.

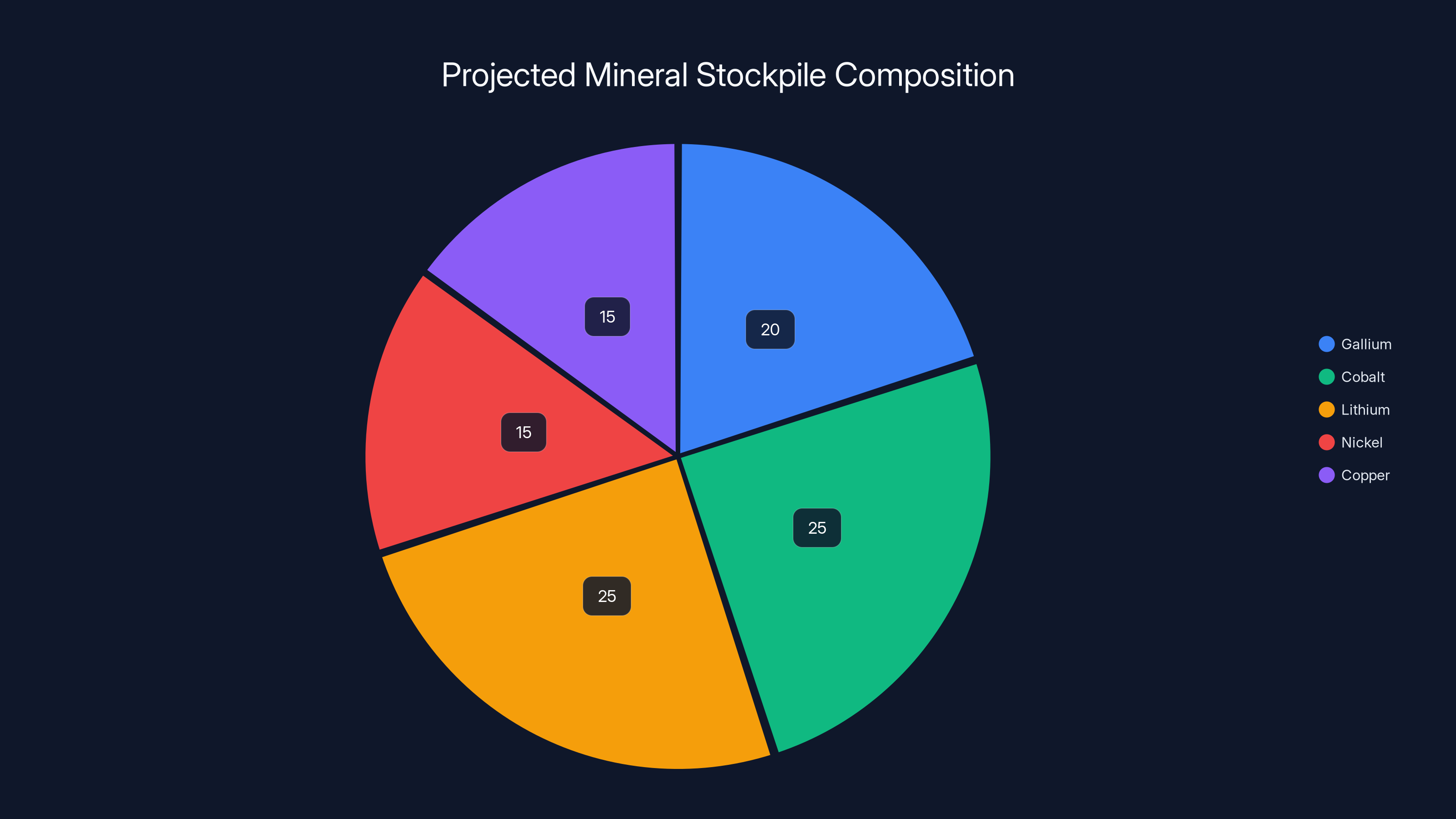

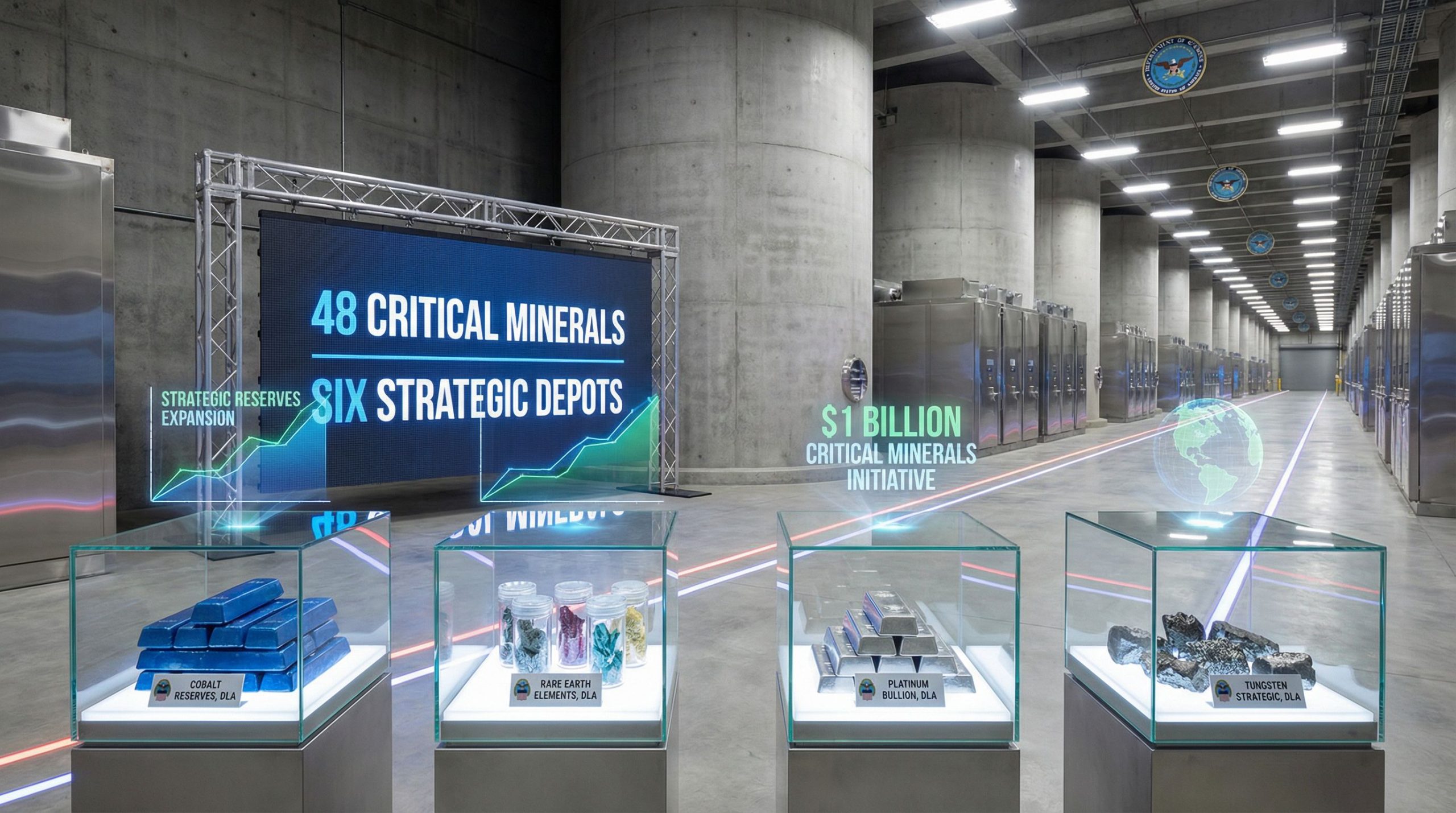

Estimated data suggests that gallium, cobalt, and lithium are key components of Project Vault's stockpile, each comprising around 20-25% of the total. Nickel and copper are likely included, making up the remaining 30%.

Project Vault: What the Stockpile Actually Includes

The Minerals Being Stockpiled

The Trump administration hasn't released a complete list of which minerals will be included in Project Vault, but reports indicate gallium, cobalt, and lithium are confirmed. Nickel and copper are likely candidates, though they weren't explicitly mentioned in initial announcements.

The choice of these minerals makes sense. Gallium is essential for semiconductor manufacturing and solar panels. Supply is concentrated, and substitutes are limited. Cobalt is essential for batteries and has significant supply constraints, particularly sourcing concerns in the DRC. Lithium is the binding constraint on battery production.

If nickel and copper are included, that would expand the scope beyond batteries and semiconductors into broader infrastructure. Copper is essential for electrical transmission and distributed renewable energy systems. Nickel is used in battery chemistry alongside cobalt and lithium.

The total value of minerals being stockpiled is significant but not unlimited. Reports suggest the initial stockpile might hold 1-2 years of U.S. domestic consumption of key minerals. That's not enough to eliminate supply concerns but enough to bridge critical supply gaps if disruptions occur.

The Financing Structure

Project Vault is funded through a combination of government loans and private capital. The Export-Import Bank is providing

This structure is interesting because it's not a pure government expenditure. It's designed to leverage private capital and create economic returns. If mineral prices increase (which the analysis suggests they will), those stockpiled minerals gain value. That's not the primary goal, but it's a useful secondary benefit.

The financing also includes equity stakes in domestic miners like MP Materials and USA Rare Earth. These aren't massive stakes, but they align government interests with industry success. The government becomes partially dependent on these companies succeeding, which creates political pressure to support domestic mining.

How This Compares to the Strategic Petroleum Reserve

Trump compared Project Vault to the Strategic Petroleum Reserve, which holds roughly 370 million barrels of oil. That reserve was established in the 1970s after the OPEC embargo threatened U.S. energy security.

The comparison is useful but imperfect. The Strategic Petroleum Reserve was built to address a temporary supply disruption in a commodity (oil) where substitutes exist. Renewable energy and electric vehicles eliminate oil dependence long-term. The reserve helped bridge from one energy system to another.

The minerals reserve is different. It's not bridging to a different system. It's supporting the infrastructure for that different system. The minerals enable the transition to electricity-based transportation and renewable energy. They're not a substitute for something else. They're foundational inputs for the future economy.

That's a crucial distinction. The oil reserve addressed scarcity in a declining market. The minerals reserve addresses scarcity in a growing market. One buys time for alternatives to develop. The other creates the conditions for transformation.

The Unspoken Truth: Why Even Trump Admits the Future Is Electric

The Contradiction in Policy

Here's where things get genuinely interesting. The Trump administration has been philosophically opposed to clean energy and climate policy. They've rolled back environmental regulations, reduced funding for renewable energy research, and repeatedly expressed skepticism toward electric vehicles.

But they're spending $12 billion on critical minerals that are essential specifically for electric vehicles and renewable energy.

That's not a contradiction born of weakness or confusion. It's a rational response to economic reality. You can dislike electric vehicles as a policy matter and still recognize that global demand for them is accelerating. You can be skeptical of climate policy and still understand that mineral constraints will become binding.

It's also a recognition that American manufacturers need these minerals to stay competitive. Tesla produces more than a million electric vehicles annually. That requires massive quantities of lithium, cobalt, and nickel. Domestic suppliers need access to these materials at competitive prices.

There's no version of the future—whether you're an optimist about EVs or a skeptic—where critical mineral supply becomes less important. In the skeptical scenario, we stay dependent on China for essential materials. In the optimistic scenario, we need even more minerals as adoption accelerates.

Either way, securing supply makes sense. That's why the policy has bipartisan appeal despite philosophical differences. Democrats support it because it enables clean energy transition. Republicans support it because it strengthens American manufacturing and reduces dependence on China.

Market Forces Always Win

There's a broader lesson here about markets and policy. Individual administrations can express preferences about which technologies they favor. But market forces—price signals, technological advantage, consumer demand—eventually dominate.

Electric vehicles are becoming economically superior to internal combustion engines in more and more markets. Battery costs have fallen 90% in the past 15 years. Production volumes are scaling rapidly. Manufacturing infrastructure is being built. Consumer adoption is accelerating.

None of that depends on policy support. It's driven by fundamentals. Technology is improving. Manufacturing is scaling. Costs are falling. Consumers are responding.

Governments can accelerate or decelerate adoption with subsidies or regulations. But they can't reverse the underlying trend. Not without massive cost. And attempting to do so becomes politically unsustainable once the economic advantage is clear.

The mineral stockpile is tacit acknowledgment of that reality. We can't stop this transition. We can prepare for it and position ourselves to benefit from it. That's the actual policy message.

Estimated data suggests that lithium, cobalt, and nickel will dominate the demand for critical minerals by 2030, driven by electric vehicle and renewable energy needs.

Supply Chain Decoupling: Building Redundancy at Cost

The Long Game: Building Domestic Production Capacity

The $12 billion stockpile is the short-term fix. The long-term solution is building domestic production capacity that can meet U.S. demand without relying on China or other single sources.

This is expensive and slow. A new lithium mine requires 5-10 years of permitting and development before production starts. A processing facility adds another 2-3 years. Total investment for a new lithium project might be $1-2 billion.

For rare earth elements, the timeline is even longer. Rare earth mining and processing are complex. Environmental impacts are significant. Community opposition can delay projects. Building a fully integrated rare earth supply chain domestically would require $3-5 billion and 7-10 years.

That's why the stockpile is necessary. It bridges the gap between today's supply constraints and tomorrow's expanded capacity. It gives time for capital to flow, projects to be permitted, and infrastructure to be built.

But here's the catch: if pricing is too low, new projects don't get built. Mining companies won't invest billions to develop new mines if mineral prices stay depressed. Processors won't build new facilities if margins are thin.

So the stockpile has a dual function. It addresses scarcity now. But it also potentially supports pricing that makes future capacity viable. If the government is accumulating minerals during periods of supply abundance, that supports prices and makes new mining projects economically attractive.

Allies and Partnerships: The Missing Piece

Domestic U.S. production won't meet all future demand. Lithium reserves in the U.S. are significant but not unlimited. Rare earth deposits exist but aren't as rich as some international sources. Some minerals (cobalt, most nickel) aren't found domestically in economically viable quantities.

That's why partnerships matter. The U.S. is developing relationships with Australia, Canada, and other allied nations to ensure access to diverse mineral sources. These relationships create preferential trading agreements and joint ventures that provide supply security without requiring total domestic production.

Australia has significant lithium and rare earth reserves and is a natural strategic partner. Canada has cobalt, nickel, and critical minerals in areas with strong environmental standards. Developing integrated supply chains with allies provides diversification and reduces dependence on any single source.

This is longer-term relationship building that's not captured in a simple stockpile announcement. But it's arguably more important than the physical reserves. Relationships and partnerships create lasting supply chain resilience.

The Global Race for Supply: Every Nation Wants These Minerals

Europe's Competing Interests

Europe is pursuing parallel strategies to secure critical minerals. The EU has different geographic advantages and disadvantages than the U.S. Europe is closer to African mining regions and Russian resources (though Russia is problematic after the Ukraine invasion). Europe also has different minerals that are geographically available.

Europe is investing in domestic processing capacity for minerals. They're also developing relationships with African nations and other sources to ensure supply diversity. The EU Critical Raw Materials Act sets targets for domestic production and processing that are more ambitious than the U.S. approach.

But Europe faces a constraint the U.S. doesn't. They lack large-scale mining operations for most critical minerals. Building domestic mining capacity in Europe is complex due to environmental regulations and community opposition. Processing capacity is being developed, but it will take years and billions in investment.

That creates competition. Europe is bidding against the U.S. for long-term supply contracts from allied nations. They're both trying to secure relationships with Australia, Chile, and other suppliers. Both are trying to reduce dependence on China.

China's Response: Securing Long-term Supplies

China isn't sitting idle while the U.S. and Europe build redundant supply chains. They're moving in the opposite direction: securing long-term supply relationships with miners.

Chinese companies are investing in cobalt mining in the Democratic Republic of Congo, lithium projects in Chile and Argentina, and rare earth mining in various countries. These aren't just equity stakes. They're long-term supply contracts that guarantee Chinese processors access to raw materials.

This is brilliant strategy. They're not just processing. They're securing the inputs to processing. That creates a supply chain advantage that's durable even if other nations build processing capacity.

China is also developing domestic reserves. They're mining rare earth elements in Tibet and other regions. They're investing in lithium extraction in Xinjiang and other provinces. As domestic reserves become depleted globally, China's ability to access their own reserves creates additional leverage.

The global supply chain race is becoming more competitive and more strategic. Every major economy is trying to secure access to critical minerals. The competition is driving investment and causing prices to increase. In the long term, that makes new projects viable. It also makes supply chains more resilient because higher prices justify investment in diverse sources.

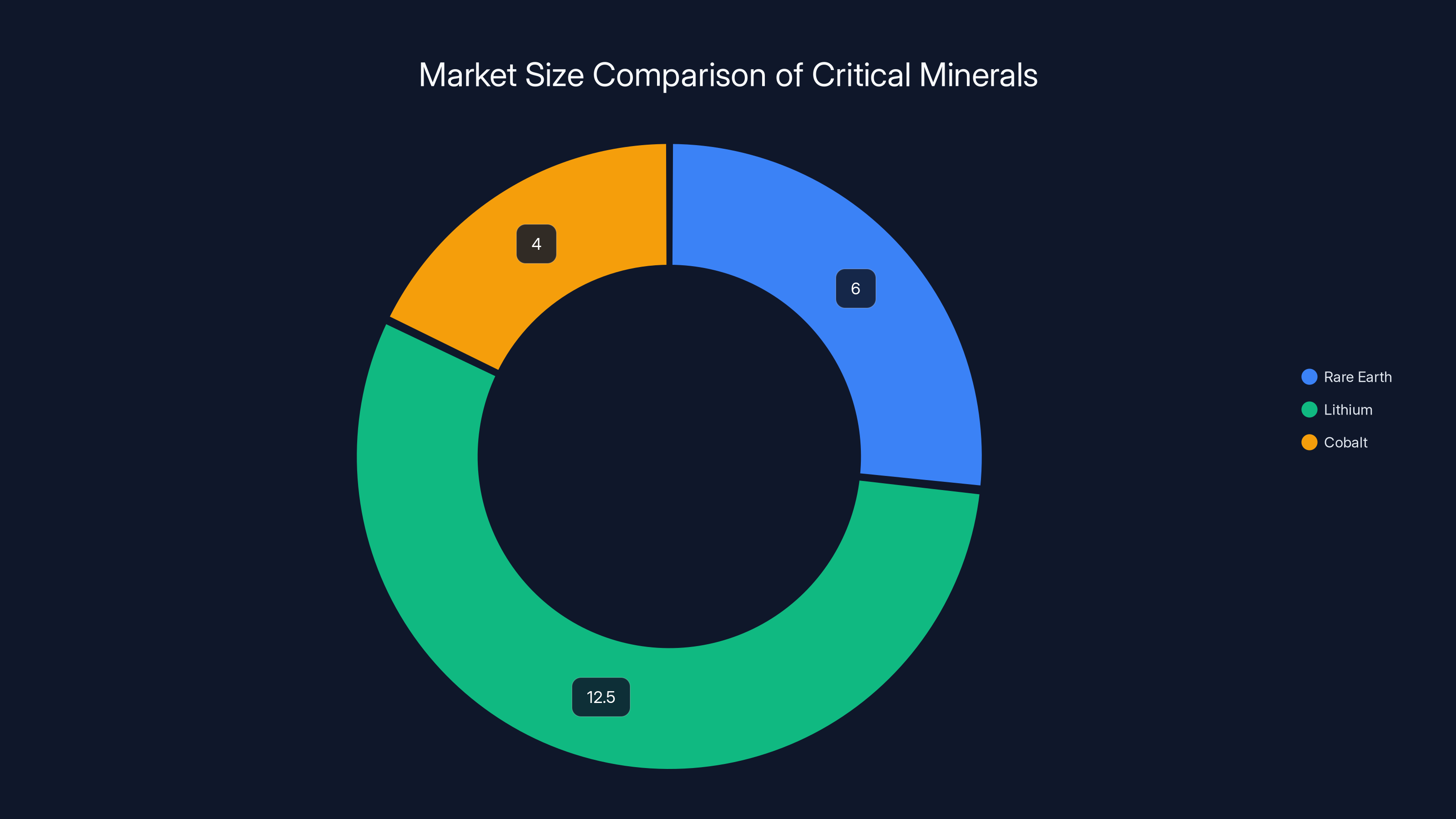

The $12 billion allocated to Project Vault is substantial, equating to nearly the entire annual market size of rare earth and lithium combined. Estimated data.

Minerals and Manufacturing: The Semiconductor Angle

Gallium and the Chip Industry

Gallium seems less famous than lithium or cobalt. That's because it's not consumer-facing. You don't know if your device has gallium. But it's essential for semiconductor manufacturing, and that matters enormously.

Gallium is used in high-speed integrated circuits and optoelectronic devices like LEDs and solar cells. It's also used in 5G and satellite communications infrastructure. As these technologies scale, gallium demand increases.

The geopolitics of gallium supply are interesting. China produces about 90% of global gallium. That's higher concentration than for any other critical mineral. The U.S. production is minimal. Europe has virtually none.

When China restricted gallium exports in 2023, it affected chip manufacturing worldwide. Supply tightened. Prices increased. Semiconductor fabs reduced production. The restriction eventually eased, but it demonstrated vulnerability.

Gallium inclusion in Project Vault is recognition of this vulnerability. It's also recognition that semiconductor manufacturing is essential infrastructure in the modern economy. You can't build 5G networks, advanced computing systems, or modern defense systems without semiconductors. And you can't build semiconductors without gallium.

The Broader Semiconductor Supply Chain

Beyond gallium, semiconductor manufacturing requires a complex supply chain of critical materials: rare earth elements for magnets in manufacturing equipment, aluminum for interconnects, copper for wiring, silicon dioxide for insulation.

The U.S. has significant silicon deposits and manufactures silicon wafers domestically. But advanced semiconductor manufacturing requires materials that aren't domestically available or require significant processing improvements.

This is why semiconductor self-sufficiency is a major policy goal. The CHIPS Act, passed in 2022, provided $52 billion in subsidies for semiconductor manufacturing in the U.S. The goal is to increase domestic capacity and reduce dependence on Taiwan for advanced chips.

That's a different policy lever than mineral stockpiling, but it's addressing the same underlying issue: supply chain vulnerability in essential technologies. Both are responses to recognition that distributed, resilient supply chains are more important than pure cost optimization.

Price Implications: What $12 Billion Actually Means for Markets

The Scale of Mineral Markets

The

So $12 billion is roughly one year of global rare earth production plus one year of lithium production. That's substantial but not enormous relative to the size of these markets.

However, the announcement itself has price implications. When governments signal they're going to accumulate critical minerals, that can increase prices. It signals expected scarcity. It signals demand that wasn't previously anticipated. Both of these push prices up.

Higher prices have multiple effects. They make new mining projects economically viable. They create incentives to develop substitutes. They slow demand growth in price-sensitive applications. But they also increase costs for manufacturers who use these materials.

Who Pays the Cost?

Ultimately, the costs of critical mineral scarcity are distributed. Governments absorb costs through increased defense spending (advanced systems require more rare materials). Manufacturers absorb costs through higher input prices. Consumers absorb costs through higher prices for electronic devices and vehicles.

The mineral stockpile concentrates cost in government hands rather than distributing it. That has political benefits (easier to manage in a crisis) and economic costs (government is paying market prices for materials that might appreciate).

But there's a broader economic point: mineral scarcity is real. Costs will be borne somehow. The question is how to distribute them most efficiently. A well-managed stockpile might be more efficient than allowing price spikes to cascade through supply chains.

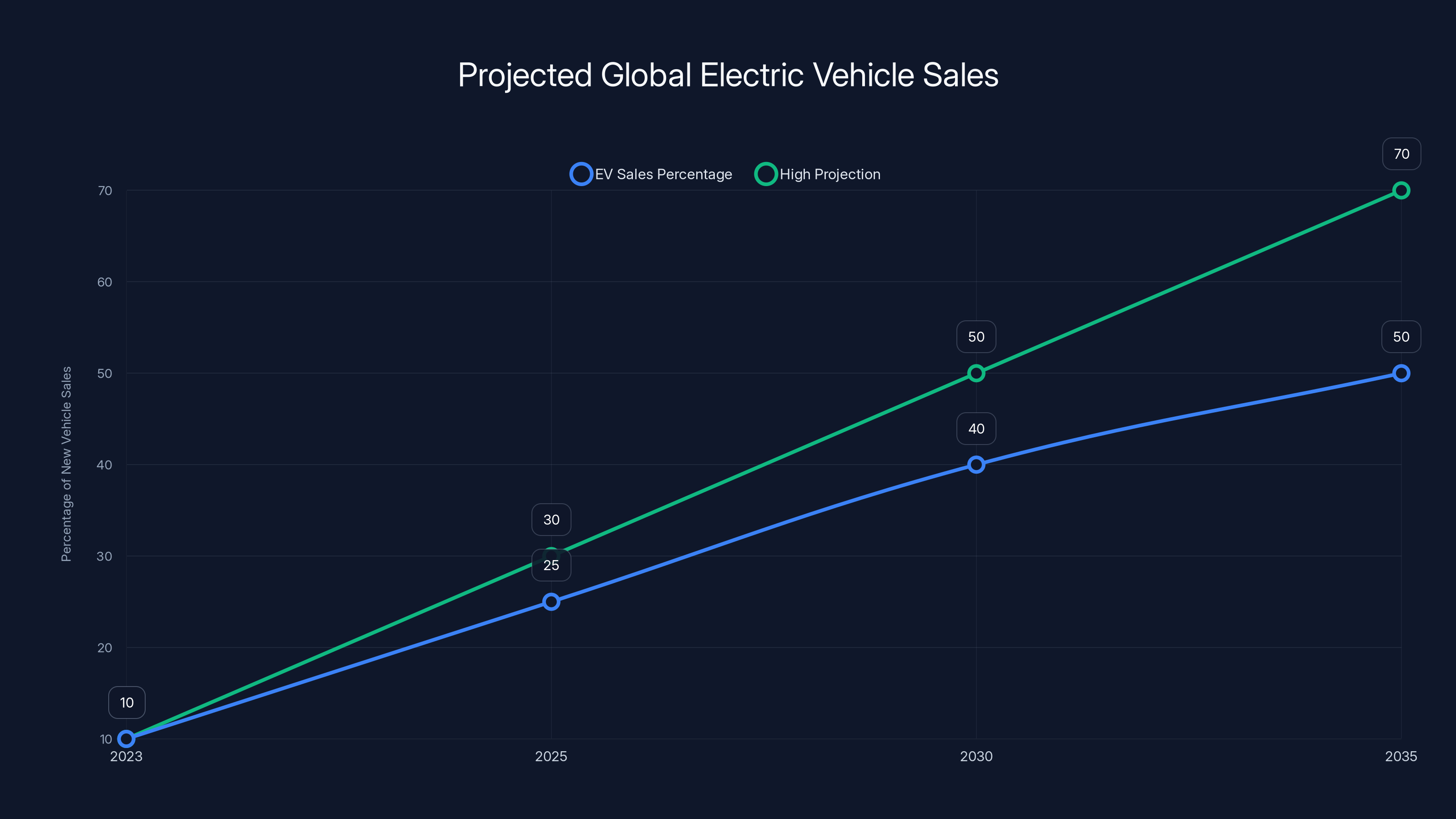

Electric vehicle sales are projected to reach 50% of new vehicle sales by 2035, with some forecasts suggesting up to 70%. Estimated data based on industry trends.

Environmental and Ethical Considerations

Mining Impact: The Other Side of the Story

Critical minerals don't appear magically. They require mining. Mining has environmental and social costs that are often overlooked in discussions of supply chain security.

Lithium mining in South America's lithium triangle (Chile, Argentina, Bolivia) uses enormous quantities of water in arid regions. A single lithium mine can consume millions of gallons of water daily in areas where water is already scarce. The environmental impact includes salt accumulation, habitat disruption, and threats to indigenous communities.

Cobalt mining in the Democratic Republic of Congo has serious human rights concerns. Child labor, unsafe working conditions, and environmental pollution are documented problems. Artisanal mining (small-scale informal operations) is particularly problematic, with minimal environmental controls or worker protections.

Rare earth mining produces radioactive waste. The minerals themselves aren't particularly radioactive, but they're often found in association with thorium and uranium. Processing rare earth ore generates tailings that must be managed carefully.

These are genuine problems that don't have easy solutions. Securing supply while maintaining environmental and ethical standards requires higher costs and more complex supply chains. It's easier and cheaper to source from locations with minimal environmental and labor standards.

But it's also a strategic vulnerability. Environmental and ethical concerns create political pressure to restrict mining in responsible locations and supply chains. That was part of the lithium restriction issue in South America, where communities mobilized against mining expansion.

The long-term solution isn't ignoring these concerns. It's building supply chains that combine security with responsibility. That's more expensive and slower than rapid, unrestricted expansion. But it's more sustainable.

The Recycling Opportunity

One approach that could substantially reduce primary mining demand is improved recycling of critical minerals from electronic waste and end-of-life vehicles.

A used electric vehicle battery contains significant quantities of lithium, cobalt, and nickel. Rather than mining new ore, recycling those batteries could recover 90% of the materials. Similarly, old electronics contain copper, aluminum, and other valuable minerals.

Recycling isn't at commercial scale yet for most critical minerals. The infrastructure doesn't exist. The economics aren't quite there. But as primary minerals become more expensive and scarce, recycling becomes more economically attractive.

This is an area where technology improvements and capital investment could have substantial impact. Better recycling processes could reduce primary mining demand by 20-30% within 15 years. That would substantially reduce environmental pressure and supply constraints.

Government policy could accelerate this. Extended producer responsibility rules that require manufacturers to handle end-of-life recycling create incentives for design and infrastructure improvements. Tax incentives for recycling operations could accelerate commercial deployment. But this requires intentional policy focus.

What This Means for Investors and Businesses

Mining and Processing Opportunities

For investors, the critical minerals trend creates multiple opportunities. Mining companies exploring for lithium, cobalt, nickel, and rare earth elements have better long-term prospects than they did five years ago. As primary minerals become more valuable and more sought after, successful mining companies will capture significant value.

Processing and refining companies have even better prospects. The bottleneck in critical minerals is processing capacity, not extraction. Building processing capacity is capital-intensive but generates strong returns as prices increase and volumes scale.

Recycling companies represent an emerging opportunity. As EV batteries and electronic waste accumulate, recycling infrastructure will become economically viable. First-mover companies could establish competitive positions in valuable markets.

Battery manufacturers benefit from supply security because it reduces input cost volatility. Securing long-term mineral contracts at predictable prices is valuable. Companies that do this successfully will have cost advantages over competitors.

Manufacturing and Supply Chain Resilience

For manufacturers in dependent industries (automotive, electronics, renewable energy), critical mineral supply security becomes a strategic issue. Companies that secure long-term supply contracts gain competitive advantages. Those that don't face potential supply disruptions and cost volatility.

This is driving consolidation in battery manufacturing and semiconductor production. Larger companies can afford to invest in securing mineral supplies and building processing capacity. Smaller competitors face increasing difficulty. That's pushing consolidation and creating scale advantages.

Supply chain diversification also becomes valuable. Companies that source from multiple geographic regions rather than concentrating supply in single countries reduce vulnerability to geopolitical disruption. That's more expensive in the short term but reduces long-term risk.

Geographic and Geopolitical Implications

For countries with mineral deposits, the demand growth creates economic opportunities. But it also creates risks. Resource-rich nations face pressure to maximize extraction for short-term revenue while often underestimating long-term environmental costs.

Countries with mineral refining and processing capacity have significant strategic leverage. That's why building domestic processing capacity is such a priority for the U.S. and Europe. Whoever controls processing controls much of the value chain.

Geopolitically, mineral supply chains are becoming as important as energy supply chains. Nations are building relationships, securing long-term contracts, and making strategic investments to ensure access. This is creating new alliances and tensions in international relations.

The Future of Mineral Demand: Trends and Forecasts

Electrification Acceleration

Electric vehicles will continue accelerating in adoption. The technology is improving, costs are falling, and infrastructure is expanding. Most forecasts suggest 50% of new vehicle sales globally will be electric by 2035. Some projections push that to 70% or higher.

That requires exponential growth in mineral supply. A doubling of EV production from today's 8-10 million units annually to 16-20 million would roughly double lithium demand. If EV adoption continues accelerating beyond that, mineral demand becomes genuinely constrained.

Renewable energy deployment is accelerating even faster than EV adoption in some regions. Solar and wind continue to provide the majority of new generation capacity. That trend is likely to continue and accelerate as costs fall and climate policies tighten.

Substitution and Alternatives

There's ongoing research into battery chemistries that use less cobalt or no cobalt. Sodium-ion batteries and other chemistries are emerging as potential alternatives. These substitutes will reduce cobalt demand but not eliminate it. And they'll require other minerals (sodium, manganese) that have their own supply constraints.

Rare earth magnets might be replaceable in some applications. Direct-drive wind turbines don't require gearboxes and could use alternative materials. But these alternatives are often slightly less efficient or more expensive. They'll be deployed where supply constraints are most severe, not universally.

Substitution happens, but slowly. It requires R&D investment, manufacturing retooling, and supply chain restructuring. It's measured in decades, not years. So substitution won't eliminate mineral constraints in the next 10-15 years.

Demand from Emerging Markets

India, Southeast Asia, and Africa represent emerging demand sources. As these regions develop, vehicle ownership increases. Infrastructure is built. Electronics consumption grows. All of this requires critical minerals.

India's transportation sector is electrifying rapidly. India's solar capacity is expanding faster than any other country. As manufacturing relocates from China to India and Southeast Asia, mineral demand from these regions will accelerate.

Africa is both a supply source and an emerging demand market. Mineral extraction will accelerate. But so will local consumption as development continues. That creates competition for supplies between mining companies and local demand.

Policy and Geopolitical Implications

The Shifting Energy Paradigm

The critical mineral reserve announcement signals a fundamental shift in how governments think about strategic resources. For the past 50+ years, energy security meant oil security. Governments competed for oil reserves, maintained strategic reserves, and organized geopolitical strategy around petroleum access.

Now, energy security is becoming mineral security. Oil remains important, but its strategic importance is declining as transportation and power generation electrify. The minerals that enable that transition—lithium, cobalt, rare earths, gallium—are becoming the new strategic commodities.

This shift has enormous geopolitical implications. Energy-rich nations that built power and wealth on oil reserves face declining strategic importance. Mineral-rich nations gain relative influence. Geographic power dynamics shift.

It's one of the most significant geopolitical transitions of the 21st century, and it's happening with less public attention than energy transitions typically receive.

Allied Supply Chain Integration

The U.S. and Europe are increasingly integrating supply chains with allied nations (Australia, Canada, and others) while attempting to reduce dependence on China and other adversaries. This is driving a bifurcation of global supply chains.

Western companies are paying premiums for "alliance-friendly" mineral sources. Chinese companies are securing long-term contracts with non-allied nations. The result is two partially separate supply chains: one oriented toward Western manufacturers and one oriented toward Chinese manufacturing.

This bifurcation increases costs for everyone. Duplication reduces efficiency. Redundancy is expensive. But reduced geopolitical vulnerability justifies that cost.

Over the next decade, this bifurcation will become more pronounced. Each bloc will develop supply chains optimized for internal use. Cross-bloc trade will decrease as supply security takes priority over pure cost optimization.

Conclusion: The Inadvertent Admission

When the Trump administration announced Project Vault and a $12 billion commitment to critical mineral stockpiling, they likely didn't intend to make a statement about the direction of the global economy. But that's exactly what happened.

You can dislike electric vehicles. You can be skeptical of climate policy. You can prefer fossil fuels. But if you're responsible for national economic security, you can't ignore the reality that the global economy is shifting toward electricity.

The minerals reserve exists for one reason: critical minerals are essential for the technologies that are rapidly becoming central to the global economy. Electric vehicles aren't a fringe technology being forced by activists. They're scaling because they're economically superior and operationally better. Renewable energy isn't a symbolic gesture. It's the cheapest source of new generation capacity in most markets.

Government policy can accelerate or decelerate these transitions. But it can't reverse them without massive cost. And once the trajectory is clear, even administrations philosophically opposed to these technologies recognize the need to plan for and invest in the infrastructure they require.

That's what the mineral reserve represents. Not a commitment to clean energy or climate action. Simply recognition that the future economy will run on electricity and that securing the materials that enable that transition is a legitimate government responsibility.

In that sense, the announcement is less about Trump and more about market forces. Markets always win eventually. Policies align with market realities or become politically unsustainable. The mineral stockpile is simply the moment when policy explicitly acknowledged what markets had already decided.

The deeper implication is this: if you want to understand where the global economy is heading, don't listen to what politicians say about energy and technology. Look at where they're actually spending money and building infrastructure. The mineral reserve tells you everything you need to know.

FAQ

What exactly are critical minerals and why are they so important?

Critical minerals are rare elements—including lithium, cobalt, gallium, nickel, and rare earth elements—that are essential for manufacturing modern technology but have limited geographic supply sources. They're crucial for batteries (electric vehicles and energy storage), semiconductors (computer chips and 5G infrastructure), wind turbine magnets, solar panels, and advanced manufacturing. Unlike oil, which you can find in many locations globally, critical minerals are concentrated in specific countries, making supply vulnerable to geopolitical disruption.

How much do electric vehicles actually depend on critical minerals?

A single electric vehicle battery requires approximately 8-10 kg of lithium, 15-20 kg of cobalt (though decreasing), and significant quantities of nickel and other minerals. Internal combustion vehicles need essentially none of these materials. With global EV production currently at 8-10 million vehicles annually and growing toward 15-20 million by 2030, that translates to hundreds of millions of kilograms of critical minerals required just for transportation electrification.

Why is China's position in mineral processing so dominant and hard to challenge?

China controls roughly 60% of global rare earth processing—not just mining, but the complex conversion of raw ore into usable material. This processing capacity took decades to build and requires specialized knowledge, infrastructure, and environmental management capability. Creating competitive processing capacity elsewhere requires $1-2 billion per facility and 5-7 years of development. That's why even countries with mineral deposits must rely on Chinese processing, giving China leverage over the entire supply chain.

What does the Strategic Petroleum Reserve comparison tell us about government strategy?

Trump compared Project Vault to the Strategic Petroleum Reserve, suggesting both are critical infrastructure. However, the comparison reveals important differences: the oil reserve bridges to an alternative energy system (renewables), while the minerals reserve enables that transition. The oil reserve's declining importance (oil consumption is static while renewables grow) contrasts sharply with minerals, which become essential as electrification accelerates. This suggests governments recognize minerals as central to the future economy.

How long will it take for the U.S. to develop independent critical mineral supplies?

Developing meaningful domestic supply capacity requires 5-10 years for new mining projects and 2-3 additional years for processing infrastructure. For fully integrated supply chains across multiple minerals, timelines could extend to 15+ years. That's why the stockpile is necessary—it bridges the gap between today's supply constraints and tomorrow's expanded capacity. Without the stockpile, supply disruptions could create economic chaos during the development period.

Could recycling solve the critical mineral shortage instead of mining new deposits?

Recycling could reduce primary mining demand by 20-30% within 15 years as EV batteries and electronics reach end-of-life. However, recycling can't meet total demand because historical products (pre-EV boom) contain fewer minerals than new products, and growth in demand exceeds what recycling can supply. Additionally, recycling infrastructure doesn't exist yet at commercial scale. The realistic scenario involves both expanded mining and improved recycling, with recycling becoming increasingly important over time.

What happens if China restricts critical mineral exports the way they did with rare earths in 2023?

A sustained restriction would create cascading supply disruptions across semiconductor, battery, and renewable energy industries. Without adequate stockpiles and diversified supply sources, manufacturing would slow or halt. Prices would spike dramatically, making new projects viable but also economically disruptive. This scenario is why the U.S. and Europe are building strategic reserves, developing domestic capacity, and securing supply partnerships with allied nations—to reduce vulnerability to Chinese leverage.

How does critical mineral demand from artificial intelligence fit into this picture?

AI infrastructure requires specialized semiconductors (gallium, indium), cooling systems, and power distribution equipment—all mineral-intensive. Datacenters for AI training and deployment are being built at unprecedented scale. Some analysts estimate AI-related mineral demand could add 10-15% to critical mineral consumption by 2030. This demand wasn't anticipated in earlier forecasts and represents a second major driver alongside electric vehicles and renewable energy.

TL; DR

-

Critical mineral scarcity is real: Lithium, cobalt, and rare earth elements are geographically concentrated, China dominates processing, and demand is accelerating due to electric vehicles, renewable energy, and AI infrastructure—all simultaneously.

-

The $12 billion reserve bridges the gap: Project Vault provides interim supply security while domestic mining and processing capacity scales. It roughly equals one year of global lithium and rare earth production, buying time during supply constraints.

-

Supply security trumps ideology: Even administrations skeptical of clean energy are investing in critical minerals because global markets are shifting toward electrification regardless of policy preferences. Government investment follows market reality.

-

Geopolitical leverage shifts dramatically: Control of minerals is becoming as strategically important as control of energy was in the 20th century. This reshapes alliances, creates new tensions, and redistributes global economic power.

-

Mineral demand will exceed conservative forecasts: Electric vehicle adoption is accelerating faster than predicted. Wind and solar deployment is outpacing expectations. AI infrastructure is adding unanticipated demand. Combined, these create genuine supply constraints through 2035+.

Bottom Line

The critical mineral reserve isn't primarily about trade wars or beating China. It's an implicit admission that the global economy is transforming from petroleum-based to electricity-based faster than anyone anticipated. Governments are now investing in the infrastructure that enables that transformation, regardless of philosophical positions on climate or energy policy. That shift represents one of the most significant economic transformations in decades, and it's being driven by technology improvement and cost reduction, not by policy mandates. The mineral stockpile is simply the moment when government policy caught up to market reality.

Key Takeaways

- Critical minerals are geographically concentrated and essential for batteries, semiconductors, and renewable infrastructure—China controls 60% of rare earth processing

- Electric vehicle adoption is accelerating faster than predicted (10M+ units in 2024), requiring exponential mineral supply growth unsustainable with current capacity

- Project Vault's $12 billion allocation equals roughly one year of global lithium and rare earth production, buying time for domestic capacity development

- Even administrations skeptical of clean energy must invest in minerals because global market forces favor electrification regardless of political preferences

- Mineral scarcity will reshape geopolitics more significantly than energy did in the 20th century, with supply security becoming central to national strategy

Related Articles

- How Lunar Energy's $232M Funding Round Is Reshaping Grid Storage [2025]

- Nord Security's 400 Patents: The Future of Cybersecurity [2025]

- Waymo's $16 Billion Funding Round: The Future of Robotaxis [2025]

- US Offshore Wind Court Orders: Construction Restart [2025]

- SpaceX's 1 Million Satellite Data Centers: The Future of AI Computing [2025]

- SpaceX's Million Satellite Data Centers: The Future of Cloud Computing [2025]